Embed Size (px)

Citation preview

![Page 1: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/1.jpg)

1

UPSTREAMUPSTREAMUPSTREAM

September 15, 2003September 15, 2003

![Page 2: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/2.jpg)

2

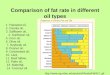

Dubai (P)

Trinidad y Tobago (E,P)

Cuba (E)

Venezuela (E,P)

Guyana (E)Colombia(E,P)

Ecuador (E,P)

Perú (E)

Bolivia (E,P) Brazil (E,P)

Argentina (E,P)

Libya (E,P)

Algeria (E,P)

Spain(E,P)

Kazakhstan (E)

Indonesia (E,P)

Malaysia (E)

Operator

Non-operator

Operator

Non-operator

Repsol YPF is present in 22 countries, being operator in 17

Repsol YPFRepsol YPF is presentis present in 22 in 22 countriescountries,, being being operatoroperator in 17in 17

Year 2002

USA (E,P) Irán (E)

Azerbaidján (E)

Solid Assets & Worldwide PresenceSolid AssetsSolid Assets && Worldwide PresenceWorldwide Presence

Gross Production: 2,129 kBOED

Gross Operated Production: 1,147 kBOED

Net Production : 1, 000 kBOED

Equatorial

Guinea (E)

Sierra Leone (E)

![Page 3: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/3.jpg)

3

STRATEGYSTRATEGYSTRATEGY

![Page 4: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/4.jpg)

4

Oper ating Excellence

Deconcentrati on

GrowthFinanci al Strength

Oper ating ExcellenceOper ating

Excellence

Deconcentrati onDeconcentrati on

GrowthFinanci al StrengthFinanci al Strength

VALUE CREATIO N

ORGANIC GROWTHORGANIC GROWTHORGANIC GROWTH

UPSTREAM

Trinidad & Tobago

Bolivia

Venezuela

Libya

Brazil

Gulf of Mexico,

Guinea & Others

New Areas

STRATEGY / GROWTHSTRATEGY / GROWTHSTRATEGY / GROWTHOrganic Growth ( 1 of 2 )

Projects to increase LIQUIDS production and

reserves

• Current developments in Libya (NC-186 :Fields A and

D) (NC-115 : Discoveries 0-1 and N-2 ).

• Current developments in Bolivia, Brazil (Albacora

Leste), Ecuador (OCP, block 16 )

• Gas production increases and associated liquids in

Trinidad & Tobago and Argentina.

• Improvement of recovery factors in mature oil fields

• Current appraisal and further development in Gulf Of

Mexico (Neptune discovery)

• Libya: Package 1 awarded and Package 2 & further

blocks under negotiations. Algeria: Block 401d

• Deep waters acreage in GoM, West Africa (Ecuatorial

Guinea, Sierra Leone), Canary Islands and Cuba.

![Page 5: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/5.jpg)

5

Oper ating Excellence

Deconcentrati on

GrowthFinanci al Strength

Oper ating ExcellenceOper ating

Excellence

Deconcentrati onDeconcentrati on

GrowthFinanci al StrengthFinanci al Strength

VALUE CREATIO N

ORGANIC GROWTHORGANIC GROWTHORGANIC GROWTH

UPSTREAM

Trinidad & Tobago

Bolivia

Venezuela

Argentina

Algeria

LNG Projects

STRATEGY / GROWTHSTRATEGY / GROWTHSTRATEGY / GROWTHOrganic Growth ( 2 of 2 )

Projects to increase GAS production and

reserves

- Trinidad & Tobago ( Trains 3 , 4 .... ) ( Plants of

Ammonia, Aluminum...)

- Bolivia ( GSA to Brazil , Pacific LNG )

- Venezuela ( Yucal Placer, QLC, QQ, Barrancas)

- Argentina ( Gas domestic market and exports )

- Algeria (Reggane blocks 351c-352c )

- LNG projects in Middle East and Libya

![Page 6: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/6.jpg)

6

Oper ating Excellence

Growth

Financi al Strength

DeconcentrationOper ating

ExcellenceOper ating

Excellence

GrowthGrowth

Financi al StrengthFinanci al Strength

Deconcentration

VALUE CREATIO N

Reduce Concentration In ArgentinaSTRATEGY / DECONCENTRATIONSTRATEGY / DECONCENTRATIONSTRATEGY / DECONCENTRATION

DECONCENTRATIONDECONCENTRATIONDECONCENTRATION

FUTURE GROWTH IN OTHER COUNTRIES

Trinidad & Tobago

Bolivia / Brazil

Venezuela

North Africa

Middle East

Increase of production out of Argentina due

to ongoing developments

Increasing activities in Exploration and New

Areas/Business out of Argentina mainly

focused on Liquids

LNG projects : T&T, Pacific LNG, Middle East

& Libya

Deep Water Projects : Gulf of México, Brazil,

Cuba, Spain (Canary Islands), West Africa.

Swaps of assets w/o a significant impact on

Cash Flow

![Page 7: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/7.jpg)

7

Deconcentrati on

Growth

Financi al Strength

Operating Excellence

Deconcentrati onDeconcentrati on

VALUE CREATIO N

GrowthGrowth

Financi al StrengthFinanci al Strength

Operating Excellence

STRATEGY / OPERATING EXCELLENCESTRATEGY / OPERATING EXCELLENCESTRATEGY / OPERATING EXCELLENCE

Additional improvements in operational efficiency in

order to :

continue being a low cost producer (Lifting Cost)

maintain low reserves replacement ratios

(Finding Cost, F&D Cost, Total Replacement Cost)

To give priority to environmental protection, security

in operations and good relationship with local

communities.

Research and Development focused on improving of

recovery factors, technical capabilities and expertise.

![Page 8: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/8.jpg)

8

Oper ational Excellence

Deconcentrati on

GrowthFinancialStrength

Oper ational ExcellenceOper ational Excellence

Deconcentrati onDeconcentrati on

GrowthGrowthFinancialStrength

VALUE CREATIO N

STRATEGY / FINANCIAL STRENGTHSTRATEGY / FINANCIAL STRENGTHSTRATEGY / FINANCIAL STRENGTH

To give priority to speed up projects to generate

positive cash-flows in the short / medium term

Balance between capital investment discipline

policy and futher investments in new growth

projects opportunities

![Page 9: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/9.jpg)

9

UPSTREAMUPSTREAMUPSTREAM

• Crude oil production in Latin America and North Africa

• Natural gas production in Latin America and Caribe

• LNG projects in the Atlantic basin, American Pacific and Mediterranean

• Gas Production linked to own gas markets :

• Southern Cone: Argentina (Metrogas), Bolivia to Brazil (Rio de Janeiro and Sao Paulo South )

• Trinidad & Tobago to USA, Puerto Rico, Mexico (Monterrey, Mexico DF, …)

• North of Africa and Middle East to Europe (Spain )

CORE BUSINESSCORE BUSINESSCORE BUSINESS

![Page 10: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/10.jpg)

10

Deconcentrati on

Growth

Financi al Strength

Operating Excellence

Deconcentrati onDeconcentrati on

VALUE CREATIO N

GrowthGrowth

Financi al StrengthFinanci al Strength

Operating Excellence

STRATEGY :

OPERATING EXCELLENCE

STRATEGY :STRATEGY :

OPERATING EXCELLENCEOPERATING EXCELLENCE

![Page 11: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/11.jpg)

11

Exploration & ProductionExploration & Exploration & ProductionProductionCost Efficiency

0

2

4

6

8

10

Finding Cost F&D Cost Reserves Replacement Cost

($/Boe)

0%

100%

200%

1.00

3.65

151% (a)

Repsol YPF 2000-2001-2002 Average

2.29

Source: PFC

Industry range 2000-2001-2002 Average

300%

Repsol YPF’s Total Production 2000-2001-2002 Average

Replacement Index

(a) 97% Without acquisitions or

divestments

0

2

4

6

8

10

Finding Cost F&D Cost Reserves Replacement Cost

($/Boe)

0%

100%

200%

1.00

3.65

151% (a)

Repsol YPF 2000-2001-2002 Average

2.29

Source: PFC

Industry range 2000-2001-2002 Average

300%

Repsol YPF’s Total Production 2000-2001-2002 Average

Replacement Index

(a) 97% Without acquisitions or

divestments

![Page 12: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/12.jpg)

12

FindingFinding CostsCosts (3(3--years moving years moving average) average)

So urce : PFC

0

1

2

3

4

5

6

7

8

1997-1999 1998-2000 1999-2001 2000-2002Conoco Phillips ENI Statoil Bp Amoco

Chevron Texaco RD Shell Exxon Mobil Repsol YPF

OXY TFE

$/Boe

Repsol YPFDecrease : 73%

0

1

2

3

4

5

6

7

8

1997-1999 1998-2000 1999-2001 2000-2002Conoco Phillips ENI Statoil Bp Amoco

Chevron Texaco RD Shell Exxon Mobil Repsol YPF

OXY TFE

$/Boe

Repsol YPFDecrease : 73%

![Page 13: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/13.jpg)

13

FindingFinding && Development Costs Development Costs (3(3--years moving years moving average) average)

So urce : PFC

0123456789

10111213

1997-1999 1998-2000 1999-2001 2000-2002Conoco Phillips ENI Statoil Bp Amoco

Chevron Texaco RD Shell Exxon Mobil Repsol YPF

OXY TFE

$/Boe

0123456789

10111213

1997-1999 1998-2000 1999-2001 2000-2002Conoco Phillips ENI Statoil Bp Amoco

Chevron Texaco RD Shell Exxon Mobil Repsol YPF

OXY TFE

$/Boe

![Page 14: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/14.jpg)

14

Reserves Reserves Replacement Cost Replacement Cost (3(3--years movingyears moving average) average)

So urce : PFC

0

1

2

3

4

5

6

7

8

1997-1999 1998-2000 1999-2001 2000-2002Conoco Phillips ENI Statoil Bp Amoco

Chevron Texaco RD Shell Exxon Mobil Repsol YPF

OXY TFE

$/Boe Repsol YPFDecrease: 34%

0

1

2

3

4

5

6

7

8

1997-1999 1998-2000 1999-2001 2000-2002Conoco Phillips ENI Statoil Bp Amoco

Chevron Texaco RD Shell Exxon Mobil Repsol YPF

OXY TFE

$/Boe Repsol YPFDecrease: 34%

![Page 15: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/15.jpg)

15

“Lifting Cost ““Lifting Cost “

1,731,48

2,572,53

0,0

0,5

1,0

1,5

2,0

2,5

3,0

2000 2001 2002 1st SEM 03

$ / Boe

DECREASE = 33%

1,731,48

2,572,53

0,0

0,5

1,0

1,5

2,0

2,5

3,0

2000 2001 2002 1st SEM 03

$ / Boe

DECREASE = 33%

![Page 16: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/16.jpg)

16

Oper ational Excellence

Deconcentrati on

GrowthFinancialStrength

Oper ational ExcellenceOper ational Excellence

Deconcentrati onDeconcentrati on

GrowthGrowthFinancialStrength

VALUE CREATIO N

STRATEGY / FINANCIAL STRENGTHSTRATEGY / FINANCIAL STRENGTHSTRATEGY / FINANCIAL STRENGTH

STRATEGY :

FINANCIAL STRENGTH

STRATEGY :STRATEGY :

FINANCIAL STRENGTHFINANCIAL STRENGTH

![Page 17: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/17.jpg)

17

REPSOL YPF : NET DEBT RATIOREPSOL YPF : NET DEBT REPSOL YPF : NET DEBT RATIORATIO

7472 6424

16555 25,9

29,2

43,3

0

6000

12000

18000

DEC 01 DEC 02 JUN 03

15

25

35

45

Net Debt Net debt ratio

Million euro Net debt/Capitalization

Net Debt ratioJun 2003

25.9%

7472 6424

16555 25,9

29,2

43,3

0

6000

12000

18000

DEC 01 DEC 02 JUN 03

15

25

35

45

Net Debt Net debt ratio

Million euro Net debt/Capitalization

Net Debt ratioJun 2003

25.9%

![Page 18: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/18.jpg)

18

(*) Div estments 2000 : UK,Crescendo Pinacle, Vietnam, Gabón & Km-20

(**) Div estments 2001 : East Bahariy a, Western Desert, Gulf of Suez E/W, SEGOS, North Alexandria+East Delta+West Mediterranean ,Bloque El-71 GOM/USA,

& BITECH

(***) Div estments 2002 : Indonesia

Are not included Swap Operation w /o cash payment ( 2001 : 20,25% Andina PECOM)

( 2000 : 25% Quiamare La Ceiba Sipetrol-ENAP)

E&P : Investments & DivestmentsE&P : Investments & DivestmentsCapital discipline

0

5 0 0

1 0 0 0

1 5 0 0

2 0 0 0

2 5 0 0

2 0 0 0 2 0 0 1 2 0 0 2 1 s t S E M 0 3

In v es tm en t s w /o A cq u is i tio n sD ive st m e n ts

A c q u is it io n s

( *) ( ** ) (* ** )

Milli

on

eu

ros

Includes 20% T&T

and 25% QLC

Payment in Cash Andina(Pluspetrol)

10% T&T, 45% QQ, Ext LLL

0

5 0 0

1 0 0 0

1 5 0 0

2 0 0 0

2 5 0 0

2 0 0 0 2 0 0 1 2 0 0 2 1 s t S E M 0 3

In v es tm en t s w /o A cq u is i tio n sD ive st m e n ts

A c q u is it io n s

( *) ( ** ) (* ** )

Milli

on

eu

ros

Includes 20% T&T

and 25% QLC

Payment in Cash Andina(Pluspetrol)

10% T&T, 45% QQ, Ext LLL

![Page 19: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/19.jpg)

19

Oper ating Excellence

Deconcentrati on

GrowthFinanci al Strength

Oper ating ExcellenceOper ating

Excellence

Deconcentrati onDeconcentrati on

GrowthFinanci al StrengthFinanci al Strength

VALUE CREATIO N

Oper ating Excellence

Growth

Financi al Strength

DeconcentrationOper ating

ExcellenceOper ating

Excellence

GrowthGrowth

Financi al StrengthFinanci al Strength

Deconcentration

VALUE CREATIO N

STRATEGY :

GROWTH

&

DECONCENTRATION

STRATEGY :STRATEGY :

GROWTHGROWTH

&&

DECONCENTRATIONDECONCENTRATION

![Page 20: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/20.jpg)

20

Further oil Development

in Block 16(Ecuador) Development

Albacora Leste(Brazil)

Further OilDevelopmentsLibya (Murzuq)

Ongoing Oil Developments &Further Secondary recovery

projects in Argentina

GROWTH BEYOND 2003GROWTH BEYOND 2003GROWTH BEYOND 2003Crude oil plays

Deepwater Oil Exploration:

USA, Canary Islands, Brazil,Cuba and West Africa New Oil Opportunities

In Middle East

Ongoing oilDevelopment in Surubi-Mamore

(Bolivia)

Further development

In GoM (Neptune)

![Page 21: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/21.jpg)

21

Pacific LNG

Atlantic LNG(4th train)

North Africa LNG integrated

Projects

GROWTH BEYOND 2003GROWTH BEYOND 2003GROWTH BEYOND 2003

LNG Projects

Venezuela: Plat. Deltana, Block 1

![Page 22: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/22.jpg)

22

Increase of Argentinean gasexports to Chile & Brazil

GROWTH BEYOND 2003GROWTH BEYOND 2003GROWTH BEYOND 2003Natural Gas Growth Potential

Increase of Bolivian

Gas exports to Brazil,Pacific LNG. Increase of Argentinean

domestic gas demand

Venezuela: Additional gassales (Yucal Placer, QLC,Barrancas, etc)

New gas projects:

Reggane & TFT (Algeria)gas exploration in Sirte(Libya)

T&T: Increase of domestic & LNG Trains gas demand

![Page 23: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/23.jpg)

23

STRATEGY : GROWTH &

DECONCENTRATION

STRATEGY : GROWTH & STRATEGY : GROWTH &

DECONCENTRATIONDECONCENTRATION

• UPSTREAM PRODUCTION & RESERVES OVERVIEW UP TO 2003

• MAIN PROJECTS AND ASSETS

LIBYA & ALGERIA

MIDDLE EAST AND FSU

SPAIN, PORTUGAL & MOROCCO

LATIN AMERICA ( ex Argentina & Bolivia )

GULF OF MEXICO (USA) , MEXICO, WEST AFRICA

![Page 24: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/24.jpg)

24

UPSTREAM PRODUCTION &

RESERVES OVERVIEW

UP TO 2003

UPSTREAM PRODUCTION & UPSTREAM PRODUCTION &

RESERVES OVERVIEWRESERVES OVERVIEW

UPUP TO 2003TO 2003

![Page 25: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/25.jpg)

25

559 589 584

373 355 416

98

71

0

200

400

600

800

1.000

1.200

2000 2001 2002 2003 (E)

KB

OE

PD

Same Assets as 2002 - Liquids Same Assets as 2002 - Gas Divestment Assets

Liquids and Gas Net ProductionLiquids and Gas Net Production

C.A.G.R 5.6 %

10% T&T Incorporation

Andina Swap

20% T&T Incorporation

Indonesia DivestmentEgypt Divestment(WD)

UK,Egypt & USA(Midgar) Divestments

![Page 26: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/26.jpg)

26

Total E&PTotal E&P

Total Net Daily Production ( KBOEPD )Total Net Daily Production ( KBOEPD )

![Page 27: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/27.jpg)

27

Total E&PTotal E&P

Net Gas Daily Production ( MmNet Gas Daily Production ( Mm33/d )/d )

![Page 28: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/28.jpg)

28

Total E&PTotal E&P

Net Liquids Daily Production ( KBOPD )Net Liquids Daily Production ( KBOPD )

![Page 29: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/29.jpg)

29

Liquids and Gas Net Proved ReservesLiquids and Gas Net Proved Reserves

0

1000

2000

3000

4000

5000

6000

dic-99 dic-00 dic-01 dic-02 dic-03(E)

Mil

lio

n b

oe

Liquids Reserves Gas Reserves Divestment Assets

C.A.G.R 7.5 %

10% T&T Incorporation

Andina Swap

20% T&T Incorporation

Indonesia DivestmentEgypt Divestment(WD)

UK,Egypt & USA(Midgar) Divestments

Crescendo Divestment

0

1000

2000

3000

4000

5000

6000

dic-99 dic-00 dic-01 dic-02 dic-03(E)

Mil

lio

n b

oe

Liquids Reserves Gas Reserves Divestment Assets

C.A.G.R 7.5 %

10% T&T Incorporation

Andina Swap

20% T&T Incorporation

Indonesia DivestmentEgypt Divestment(WD)

UK,Egypt & USA(Midgar) Divestments

Crescendo Divestment

![Page 30: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/30.jpg)

30

Production

1112 Extensions

+Discoveries

655

Revisions +

Improved 426

Sales &

Acquisitions

594

0

200

400

600

800

1000

1200

1400

1600

1800

Production 2000-2002 Reserves Addition

Mil

lio

n b

oe

Liquids and Gas Net Proved ReservesLiquids and Gas Net Proved Reserves

Replacement Replacement ( 2000 ( 2000 –– 2002 )2002 )

151 %

97 %

Excluding S/A

![Page 31: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/31.jpg)

31

Liquids Net Proved ReservesLiquids Net Proved Reserves

Replacement Replacement ( 2000 ( 2000 –– 2002 )2002 )

Production

681

Extensions

+Discoveries

231

Revisions +

Improved 450

S & Acqu -131

-200

-100

0

100

200

300

400

500

600

700

800

Production 2000-2002 Reserves Addition

Mil

lio

n b

oe

81 %

100 % Excluding S/A

Production

681

Extensions

+Discoveries

231

Revisions +

Improved 450

S & Acqu -131

-200

-100

0

100

200

300

400

500

600

700

800

Production 2000-2002 Reserves Addition

Mil

lio

n b

oe

81 %

100 % Excluding S/A

![Page 32: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/32.jpg)

32

Production

431

Extensions

+Discoveries

424

Rev + Impr -24

Sales &

Acquisitions

724

-200

0

200

400

600

800

1000

1200

1400

Production 2000-2002 Reserves Addition

Mil

lio

n b

oe

Gas Net Proved ReservesGas Net Proved Reserves Replacement Replacement ( 2000 ( 2000 –– 2002 )2002 )

261 %

93 %

Excluding S/A

![Page 33: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/33.jpg)

33

Libya and AlgeriaLibya and AlgeriaLibya and Algeria

![Page 34: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/34.jpg)

34

LIBYA. Current AcreageLIBYA. LIBYA. Current AcreageCurrent Acreage

Package 1

PreviousBlocks

![Page 35: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/35.jpg)

35

LIBYA LIBYA

![Page 36: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/36.jpg)

36

LIBYA. NC-115 ( El-Sharara )

![Page 37: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/37.jpg)

37

SEISMIC LINE WITH THE WELL LOCATION

NCNC ––115 : DISCOVERY O1 115 : DISCOVERY O1

![Page 38: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/38.jpg)

38

OWC

Top Hawaz

5151ft

5520ft

Well O1-NC115

H5

H4

H3

H2

H1

H6

H7

H8

NCNC ––115 : DISCOVERY O1115 : DISCOVERY O1

![Page 39: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/39.jpg)

39

LIBYA. NC-186: Fields “A” & “D”

![Page 40: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/40.jpg)

40

LIBYA. NC-190

![Page 41: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/41.jpg)

41

• Six new exploration blocks (“Package 1”)

awarded to Repsol YPF 60% (operator) and

OMV 40% with a total surface of 76,696 km2:

• M-1 block (Murzuq Basin),

• blocks O9 and O10 (Sirte Offshore Basin),

• block S36 (Sirte Basin) and

• blocks K1 and K3(Kufra Basin) .

LIBYA. Package 1

![Page 42: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/42.jpg)

42

PACKAGE 1. Block M-1 (Murzuq basin )

![Page 43: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/43.jpg)

43

PACKAGE 1. Blocks O-9 & O-10 ( Sirte basin )

O-10

O-9

LNG PlantMarsa El Brega

B1-88 Arco, 1963TD 3439 m

DST 35 mcfg/d & oil

D1-88 Arco, 1968

TD 3318 m

DST 13 mcfg/d & oil

![Page 44: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/44.jpg)

44

LIBYALIBYA

Net Liquids Daily Production ( BOPD )Net Liquids Daily Production ( BOPD )

![Page 45: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/45.jpg)

45

• Production reach 200,000 BOPD in NC-115 (20,000 bopd

Net Repsol YPF). High margin production

• Net Proven reserves @ June 2003: 95 M Bbl

• Start up of Field A (NC 186) early 2004

• Field D under development (NC 186)

• New Discoveries in NC 115 (O & N)

• Six new exploration blocks (“Package 1”)

• New explorations blocks under negotiations (“Package

2” and others)

• Libyan LNG Project under study

LIBYA . Large potential for growth

![Page 46: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/46.jpg)

46

ALGERIA. ALGERIA. Current acreageCurrent acreage

![Page 47: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/47.jpg)

47

ALGERIAALGERIA

Net Gas Daily Production ( MmNet Gas Daily Production ( Mm33/d )/d )

PSC effect of higher prices

MaintenanceOf Gas Plant

![Page 48: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/48.jpg)

48

ALGERIAALGERIA

Net Liquids Daily Production ( BOPD )Net Liquids Daily Production ( BOPD )

PSC effect of higher prices

MaintenanceOf Gas Plant

![Page 49: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/49.jpg)

49

DEVELOPMENT OF WESTERN AREAGas Field Model

ALGERIA. Field TFT

![Page 50: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/50.jpg)

50

ARGELIA : ARGELIA : Reggane Reggane

3D Seismic Acquisition (950 km3D Seismic Acquisition (950 km22))

Partnership: Sonatrach (25%) + Repsol YPF (33.75% Operator) + RWE Dea (22.50%) +

Edison International (18.75%).

Contract signed on July 2002 / Effective date: January 2003

Total surface: 12,217 km2

![Page 51: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/51.jpg)

51

TIO-1 RG-4

GivetianGivetian

SiegenianSiegenian

NW SE77 TAS 77 TAS 46S46S

HercynianHercynian

T ournaisianT ournaisian

FamennianFamennian

OrdovicianOrdovician

COMPRESSED LINE0 6Km3

77-TAS-46S

TIO-1

RG-4

Seismic Section NW-SE (REGGANE)

ALGERIA. ALGERIA. BlocksBlocks 351c351c--352c (352c (RegganeReggane))

![Page 52: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/52.jpg)

52

ALGERIA. ALGERIA. BlockBlock 401401--dd

OOIP- 391 MMBOBBR-ROD

OOIP- 155 MMBOSFNE

OOIP- 138 MMBOBSF

OOIP- 93 MMBO

RDB

25 KM

OOIP-2000 MMBO650 BCF

H ASSI BERKINE SUD

OOIP->2000 MMBO

667 BCFOURHOUD

STRUCTUREBERKINE

-

BORMA

OOIP-1350 MMBO

1.3 TCF

401 d

OOIP- 70 MMBOK A

H ASSI KESKESSA

Already acquired and processed 742 Km2 of 3D Seismic.

Drilling First well at end 2003.

![Page 53: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/53.jpg)

53

• 2002 Net production: 30.000 boepd (34% Liquids and

66 % gas)

• Proven Reserves @ June 2003: 83 M boes

• Development of Western Area of TFT Field

• Appraisal and further Development of Reggane

• Good exploration potential in Block 401d

• Looking for new business opportunities: Integrated

gas project in Gassi Touil and 4th Exploration Round.

ALGERIA: Potential for growth

![Page 54: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/54.jpg)

54

Middle East and FSU Middle East and Middle East and FSUFSU

![Page 55: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/55.jpg)

55

IRAN. Block Mehr

![Page 56: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/56.jpg)

56

DubaiDubai

Net Liquids Daily Production ( BOPD )Net Liquids Daily Production ( BOPD )

![Page 57: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/57.jpg)

57

Spain, Portugal and MoroccoSpainSpain, Portugal , Portugal and Moroccoand Morocco

![Page 58: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/58.jpg)

58

SPAIN. SPAIN. CurrrentCurrrent AssetsAssets

![Page 59: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/59.jpg)

59

SPAIN : ALGA SPAIN : ALGA

Gas Gas StorageStorage EnlargementEnlargement

The project will allow :

•To double Working Gas from

779 Mm3 to 1600 Mm3 with

same Cushion Gas volume

• To increase Average

Production from 5,2 Mm3/d to

10,7 Mm3/d

• To increase Average Injection

from 3,7 Mm3/d to 7,6 Mm3/d

![Page 60: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/60.jpg)

60

CANARY & MOROCCO BLOCKSCANARY & MOROCCO BLOCKS

![Page 61: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/61.jpg)

61

SPAIN : CANARY ISLANDSSPAIN : CANARY ISLANDS

BLOCKS 1 BLOCKS 1 -- 99

![Page 62: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/62.jpg)

62

SPAINSPAIN

Net Liquids Daily Production ( BOPD )Net Liquids Daily Production ( BOPD )

![Page 63: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/63.jpg)

63

Latin America ( ex Argentina and

Bolivia)

Latin America Latin America ( ex Argentina ( ex Argentina andand

Bolivia)Bolivia)

![Page 64: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/64.jpg)

64

TRINIDAD & TOBAGO. TRINIDAD & TOBAGO. Current acreageCurrent acreage

TRINIDA D

VENEZUELA

TOBAGO

ATLAN TICO

OCEANO

5b

Samaan

Mahogany

Casia

Teak

Poui

ImmortelleTrinidad

Venezuela

Gas

Petróleo

Gas

Condensado

BPTT (30% Repsol YPF)

BP & Repsol YPF

3 (a)

23 (b)

24

2223 (a)

S11

![Page 65: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/65.jpg)

65

TRINIDAD & TOBAGOTRINIDAD & TOBAGO

Equipment & Offshore Capacity Equipment & Offshore Capacity (feb 2002)(feb 2002)

![Page 66: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/66.jpg)

66

TRINIDAD & TOBAGOTRINIDAD & TOBAGO

Equipment & Offshore Capacity Equipment & Offshore Capacity ((midmid 2002)2002)

![Page 67: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/67.jpg)

67

TRINIDAD & TOBAGOTRINIDAD & TOBAGO

Equipment & Offshore Capacity Equipment & Offshore Capacity ((endend 2005 )2005 )

![Page 68: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/68.jpg)

68

UPSTREAM MIDSTREAM

Reserves Stake in trains

Supplytrains

Marketingand Trading

30 % 23.4 % 22.3 % 43.5 %(*)

TRINIDAD & TOBAGO

Integrated LNG chain

TRINIDAD & TOBAGOTRINIDAD & TOBAGO

Integrated Integrated LNG LNG chainchain

(*) Assuming 100% Gas Natural cargoes

![Page 69: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/69.jpg)

69

TRINIDAD & TOBAGOTRINIDAD & TOBAGO

Net Gas Daily Production ( MmNet Gas Daily Production ( Mm33/d )/d )

![Page 70: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/70.jpg)

70

TRINIDAD & TOBAGOTRINIDAD & TOBAGO

Net Liquids Daily Production ( BOPD )Net Liquids Daily Production ( BOPD )

![Page 71: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/71.jpg)

71

TRINIDAD & TOBAGO

Evolution of Repsol YPF Production

TRINIDAD & TOBAGOTRINIDAD & TOBAGO

Evolution of Evolution of RepsolRepsol YPF Production YPF Production

boepd

0

20.000

40.000

60.000

80.000

100.000

120.000

1999 2000 2001 2002 2003 Est.

0

20,10022,800

28,000

105,000

13.4%

22.8%

275%

boepd

0

20.000

40.000

60.000

80.000

100.000

120.000

1999 2000 2001 2002 2003 Est.

0

20,10022,800

28,000

105,000

13.4%

22.8%

275%

0

20.000

40.000

60.000

80.000

100.000

120.000

1999 2000 2001 2002 2003 Est.

0

20,10022,800

28,000

105,000

13.4%

22.8%

275%

0

20,10022,800

28,000

105,000

13.4%

22.8%

275%

![Page 72: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/72.jpg)

72

TRINIDAD & TOBAGO

Evolution of Repsol YPF Proven Reserves

TRINIDAD & TOBAGOTRINIDAD & TOBAGO

Evolution of Evolution of RepsolRepsol YPF Proven Reserves YPF Proven Reserves

Million boe

Acquisition 20%

Extensions &Discoveries

-100

0

100

200

300

400

500

600

700

800

900

1.000

01.01.00 01.01.01 01.01.02 30.06.03Production

1st Sem 03

Revisions

230.6245.7

879.2

633,5

15.1

205.4

25.2

Reserves31-12-02

236.3

472.6

158.0

30.1

Million boe

Acquisition 20%

Extensions &Discoveries

-100

0

100

200

300

400

500

600

700

800

900

1.000

01.01.00 01.01.01 01.01.02 30.06.03Production

1st Sem 03

Revisions

230.6245.7

879.2

633,5

15.1

205.4

25.2

Reserves31-12-02

236.3

472.6

158.0

30.1

-100

0

100

200

300

400

500

600

700

800

900

1.000

01.01.00 01.01.01 01.01.02 30.06.03Production

1st Sem 03

Revisions

230.6245.7

879.2

633,5

15.1

205.4

25.2

Reserves31-12-02

236.3

472.6

158.0

30.1

230.6245.7

879.2

633,5

15.1

205.4

25.2

Reserves31-12-02

236.3

472.6

158.0

30.1

![Page 73: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/73.jpg)

73

• June 2003 Net production: 116,400 boepd

• Proven Reserves @ June 2003: 879 M boes

• End April 2003: Start up of 3rd LNG Train

• June 2003: Approval of 4th LNG Train

• Future increase in Domestic Demand (NGC, Ammonia

& Aluminium Smelter Plants)

• Good exploration potential for further LNG Trains

• Looking for new business opportunities

TRINIDAD TOBAGO.

Large Potential for growth

![Page 74: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/74.jpg)

74

VENEZUELA. VENEZUELA. Current acreageCurrent acreage

Seven Blocks (Six Production Blocks, One Exploration Block)

![Page 75: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/75.jpg)

75

Growth history in VENEZUELAGrowth history in VENEZUELA

0

10

20

30

40

50

60

70

80

90

100

Compra Astra

QLC

Adjudicación

MG

Compra

Maxus YPF

Compra 45%

Compra 25%

QLC

Licencias Gas

Barrancas

100%, Yucal

Placer 15%

Proyecto Gas

Compra 25%

QLC

Total

Venezuela

1996 1998 1999 2000 2001 2001 2003 2003

MBPED

Oil

Current

Assets

Quiamare

Quiriquire

Mene Grande

Guár ico

Gas

Quiriquire

Yucal Placer

Barrancas

![Page 76: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/76.jpg)

76

VenezuelaVenezuela

Net Gas Daily Production ( MmNet Gas Daily Production ( Mm33/d )/d )

![Page 77: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/77.jpg)

77

VenezuelaVenezuela

Net Liquids Daily Production ( BOPD )Net Liquids Daily Production ( BOPD )

![Page 78: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/78.jpg)

78

VENEZUELA : VENEZUELA :

QUIAMARE LA CEIBA ExplorationQUIAMARE LA CEIBA Exploration

![Page 79: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/79.jpg)

79

VENEZUELA. QUIRIQUIRE VENEZUELA. QUIRIQUIRE Exploration Exploration

![Page 80: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/80.jpg)

80

• 1st Half 2003 Net production: 98,200 boepd

• Proven Reserves @ June 2003: 247 M boes

• Growth potential based on:

• On-going gas development projects (Yucal Placer,

QQ )

• New gas development projects (QLC, Barrancas)

• On-going Exploration in current assets

• New opportunities (Deltana, Barúa-Motatan, Ceuta-

Tomoporo)

VENEZUELA.

Potential for additional growth

![Page 81: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/81.jpg)

81

BRAZIL. Current acreageBRAZIL. Current acreage

![Page 82: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/82.jpg)

82

BRAZIL : ALBACORA LESTE BRAZIL : ALBACORA LESTE

DEVELOPMENT (DEVELOPMENT (PetrobrasPetrobras 90% 90% RepsolRepsol YPF 10%)YPF 10%)

Año 2000 2001 2002 2003 2004 2005 2006

Diseño del

proyecto

Modulos Comp,

Gen, Proc, Ut.

Conversion

FPSO

Pozos y

Completacion

Flow Lines,

Risers,

Primera

producción

CRONOGRAMA DEL PROYECTO

ESTIMATED PLATEAU

PRODUCTION 100%150 / 160 KBOED

•Total reserves: 720 M boes

•Proven Reserves @ June

2003: 535 M boes

![Page 83: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/83.jpg)

83

• Proven Reserves @ June 2003: 53 M boes

• Development of Albacora Leste Oil Field with start-up

production by end of 2004

• Good exploration potential on seven Exploration

Blocks

BRAZIL.

Potential for growth

![Page 84: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/84.jpg)

84

ECUADOR. Current acreageECUADOR. Current acreage

![Page 85: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/85.jpg)

85

EcuadorEcuador

Net Liquids Daily Production ( BOPD )Net Liquids Daily Production ( BOPD )

![Page 86: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/86.jpg)

86

ECUADOR. Future Projects

• Net Proven Reserves @ June 2003: 68 M Bbl

• September 2003: Start up of OCP

• Ongoing Development of Block 16: Production

Plateau 75,000 bopd (September-October 2003) with a

further development Plan to increase plateau to

100,000 bopd

• Good exploration potential in current blocks

• New business opportunities:

• Ishpingo-Tambococha-Tiputini: 788 MBO

• Future Exploration Rounds

![Page 87: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/87.jpg)

87

REPSOL YPF 100%

890,3 km2

CATLEYA

OXY 75%REPSOL 25%

2522,7 km2

COSECHA

REPSOL YPF 100%

434,8 km2

SAN MIGUEL

REPSOL YPF 100%

402,43 km2

CAPACHOS

CAÑO LIMONRepsol Net 6,7MMBO

ECOPETROL 50% OXYANDINA 25%OXYCOL * 25%

*6,25% Repsol YPF

266,7 Km2

CRAV O NORTE

EXPLORATION PRODUCTION

COLOMBIA. COLOMBIA. Current acreageCurrent acreage

![Page 88: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/88.jpg)

88

ColombiaColombia

Net Liquids Daily Production ( BOPD )Net Liquids Daily Production ( BOPD )

![Page 89: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/89.jpg)

89

PERU. PERU. Current acreageCurrent acreage

REPSOL YPF 100%

4,208Km2

REPSOL YPF 41%BURLINGTON 23.85% PECOM 35.15%

8,801 Km2

REPSOL YPF 76.15%BURLINGTON 23.85%

20,280 Km2

REPSOL YPF 41%BURLINGTON 23.85%PEREZ COMPANC 35.15%

7,585 Km2

Current Assets

35M

39

80 (TEA)

57

Under negotiation

![Page 90: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/90.jpg)

90

BLOCKS IN CUBA BLOCKS IN CUBA

![Page 91: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/91.jpg)

91

CUBA : Prospects & Leads Map

![Page 92: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/92.jpg)

92

CUBA :Yamagua XLINE 2672

![Page 93: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/93.jpg)

93

CUBA :Yamagua XLINE 4075

![Page 94: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/94.jpg)

94

Gulf of Mexico (USA), Mexico, West Africa...

Gulf of MexicoGulf of Mexico (USA), (USA), MexicoMexico,,West AfricaWest Africa......

![Page 95: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/95.jpg)

95

USA : Gulf of Mexico AcreageUSA : Gulf of Mexico Acreage

![Page 96: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/96.jpg)

96

USA : Gulf of MexicoUSA : Gulf of Mexico

![Page 97: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/97.jpg)

97

USA : Gulf of Mexico NeptuneUSA : Gulf of Mexico Neptune

![Page 98: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/98.jpg)

98

West Africa : Equatorial Guinea & Sierra West Africa : Equatorial Guinea & Sierra

LeoneLeone

![Page 99: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/99.jpg)

99

Equatorial Guinea : Block K & Others Equatorial Guinea : Block K & Others

OpportunitiesOpportunities

![Page 100: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/100.jpg)

100

Equatorial Guinea : Block KEquatorial Guinea : Block K

![Page 101: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/101.jpg)

101

West Africa : Sierra LeoneWest Africa : Sierra Leone

![Page 102: UPSTREAM.ppt [S.lo lectura] - Repsol Canary Islands, Brazil, Cuba and West Africa New Oil Opportunities In Middle East Ongoing oil Development in Surubi-Mamore (Bolivia) Further development](https://reader034.pdfslide.us/reader034/viewer/2022051802/5af3b2417f8b9a190c8bfb4e/html5/thumbnails/102.jpg)

102

West Africa : Sierra Leone West Africa : Sierra Leone Play ConceptPlay Concept --

Seismic LineSeismic Line 20442044

![Congreso M.Interna-Bilbao [S.lo lectura]somivran.es/fileadmin/reuniones/VIIICongreso/resumenes/Vitaminico… · achylia gastrica to pernicious anemia. I The effect of the administration](https://img.pdfslide.us/doc/110x75/5e96a52350044d5cf409c04c/congreso-minterna-bilbao-slo-lectura-achylia-gastrica-to-pernicious-anemia.jpg)

![New DR VITERI.ppt [S.lo lectura] - SAP · 2015. 7. 9. · and 9 mo of age, based on iron-replete, breast-fed infantsl 1-1b, g/L MCV, fL2 ZPP, gmol/mol heme Ferritin, pg/L TfR, mg/L](https://img.pdfslide.us/doc/110x75/600a8663da4a5e28c451c73c/new-dr-slo-lectura-sap-2015-7-9-and-9-mo-of-age-based-on-iron-replete.jpg)

![AMORTIGUADORES GABRIEL [S.lo lectura] - CDR.ES ... · Marketing. LVA Europe Historia ... (2-3 turnos de trabajo) ... Amortiguador de dirección 14000](https://img.pdfslide.us/doc/110x75/5bb68b6209d3f23d358b7605/amortiguadores-gabriel-slo-lectura-cdres-marketing-lva-europe-historia.jpg)

![Macroevoluc.n Hot (selecci.n sexual).ppt [S.lo lectura] · Esto se correlaciona con la hipertrofia de los testículos en los primates con sistemas de apareamiento promiscuo, ... un](https://img.pdfslide.us/doc/110x75/5bbeb61409d3f2d7718c843b/macroevolucn-hot-seleccin-sexualppt-slo-lectura-esto-se-correlaciona.jpg)

![Los Pactos de Integridad [S.lo lectura] - Cultura de la ... · - Islas de Integridad . • Programa de Fortalecimiento al Buen Gobierno en Entidades Territoriales. • Contrataciones](https://img.pdfslide.us/doc/110x75/5b561b8b7f8b9ac31e8bf994/los-pactos-de-integridad-slo-lectura-cultura-de-la-islas-de-integridad.jpg)

![REBOLEDO.pptx [S.lo lectura] - sap.org.ar · Integrante de la Comisión Directiva de SASIA-POSMODERNIDAD, ADOLESCENCIA Y ... ADOLESCENTE EN UN HOSPITAL PÚBLICO. Lic. Alicia Cytrynblum](https://img.pdfslide.us/doc/110x75/5baa6f4a09d3f209118c55f5/slo-lectura-saporgar-integrante-de-la-comision-directiva-de-sasia-posmodernidad.jpg)