Embed Size (px)

Citation preview

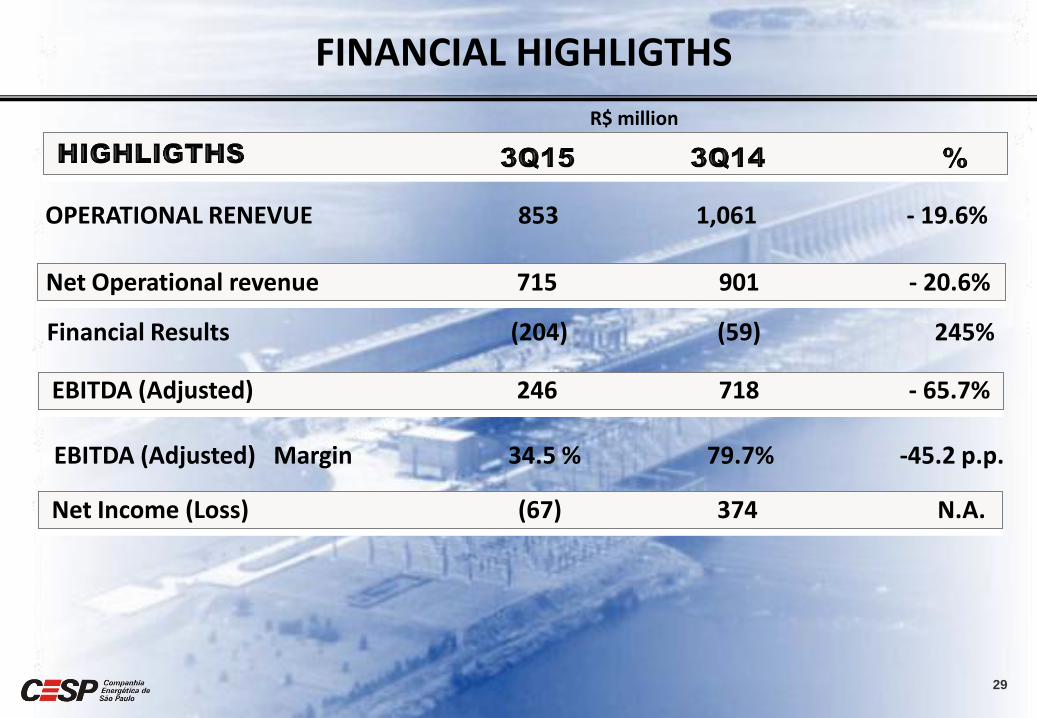

3Q15

Coreia do Sul

França

Brasil

Alemanha

Canadá

Japão

Rússia

Índia

EUA

China

Total

540

562

584

616

640

996

1.064

1.296

4.330

5.583

23.636

2014

8th

POSITION

Fonte: Global Energy Statistical Yearbook 2015

ELECTRICITY GENERATION

2

(2,3%)

(2,4%)

(2,5%)

(2,6%)

(2,7%)

(5,5%)

(4,2%)

(4,5%)

(18,3%)

(23,6%)

(100%)

World’s Largest Producers (TWh)

Hidráulica Carvão Nuclear Gás Óleo Outras

16,3%

41,3%

10,6%

21,7%

4,4% 5,7%

64,9%

2,4% 1,3%

8,5% 6,7%

16,2%

World Brazil

Fonte: EPE - Balanço Energético 2015 e IEA - Key World Energy Statistics 2015

3

Electricity Generation(%) – World(2013) x Brazil (2015)

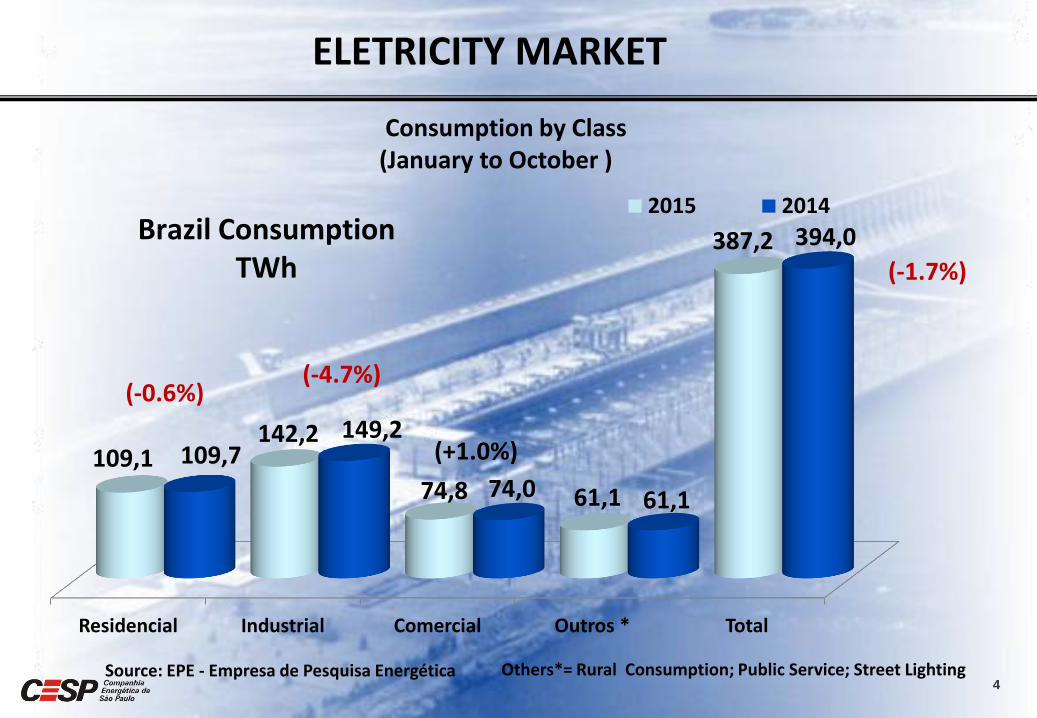

4 Source: EPE - Empresa de Pesquisa Energética

ELETRICITY MARKET

Residencial Industrial Comercial Outros * Total

109,1 142,2

74,8 61,1

387,2

109,7 149,2

74,0 61,1

394,0 2015 2014

Brazil Consumption TWh (-1.7%)

Others*= Rural Consumption; Public Service; Street Lighting

(-0.6%)

(+1.0%)

Consumption by Class (January to October )

(-4.7%)

29.8%

10

20

30

40

50

60

70

80

90

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2011 2012

2013 2014

2015

19.4%

5

Subsystem South East / Middle West (70% of the country's storage)

Source: ONS

Reservoir Levels

6

Energy Generation 2001 X 2014 - Brazil

Source: ONS

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

J F M A M J J A S O N D GH_2001 GH_2014 GT_2001 GT_2014 Carga_2001 Carga_2014

MWmed GH – Hydraulic Generation GT – Thermal Generation

65,114 MW average

37,750 MW average

7

Source: ONS

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

J F M A M J J A S O N D

MWavg

GH – Hydraulic Generation GT – Thermal Generation

GH_2001 GH_2015 GT_2001 GT_2015 Carga_2001 Carga_2015

37,835 MW Average

61,347 MW Average

Power Generation 2001 x 2015

PHYSICAL GUARANTEE X HYDRAULIC GENERATION - 2014

8 Source: CCEE GSF – Generation Scaling Factor

44,7

53,8 51,6 49,8 45,8

44,5 45,4 46,9 47,9 48,4 48,3 48,0 47,5

48,2 51,8

50,7 46,7 45,2 41,6

40,3 40,4 39,2

41,9 42,3 42,2 41,7

1,080 0,963

0,983 0,938 0,987 0,936 0,889 0,861

0,819 0,864 0,877

0,877 0,879

-

0,200

0,400

0,600

0,800

1,000

1,200

-

10

20

30

40

50

60

Dez-13 Jan-14 Fev-14 Mar-14 Abr-14 Mai-14 Jun-14 Jul-14 Ago-14 Set-14 Out-14 Nov-14 Dez-14

Physical Guarantee Hydraulic Generation GSF GW average GSF

9 Source: CCEE

Seasonalization of Physical Guarantee as provided by CCEE.

GSF – Generation Scaling Factor

46,7 58,6 58,4 57,6 51,2 49,1 47,5 45,4 45,7 46,4 46,4 46,4 45,7

41.1 47.2 45.8 45.1 42.3 39.9 37.7 38.9 38.8 40.5 42.7 42.4 43.8

0,879 0,806 0,786 0,783 0,825 0,812 0,794

0,857 0,849 0,872 0,921 0,913

0,957

-

0,200

0,400

0,600

0,800

1,000

1,200

-

10

20

30

40

50

60

70

Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15

GSF GW Average GSF Physical Guarantee Hydraulic Generation

PHYSICAL GUARANTEE X HYDRAULIC GENERATION - 2015

10

97.36

135.4

38.73

70.28

29.42

166.69

263.07

688.88

388.48 387.24

369.39

240.08

145.09

227.04 212.32 202.87

116.08

Average Price PLD - R$/MWh

Southeast/ Midwest Subsystem

Annual Average Monthly Average

Source: CCEE

11

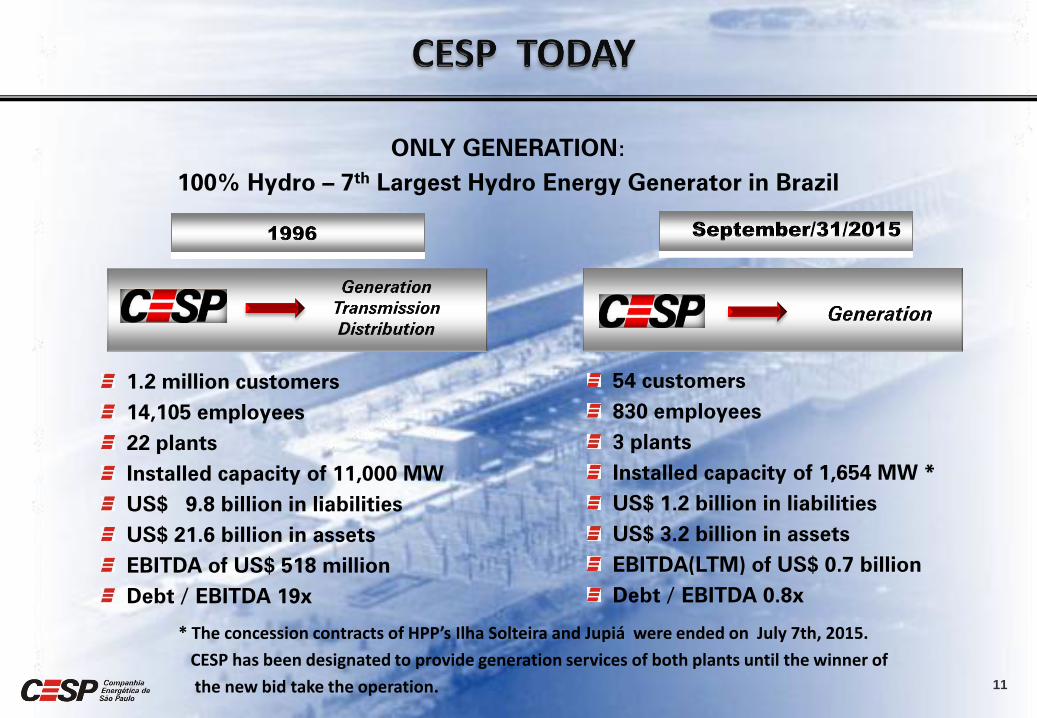

1.2 million customers

14,105 employees

22 plants

Installed capacity of 11,000 MW

US$ 9.8 billion in liabilities

US$ 21.6 billion in assets

EBITDA of US$ 518 million

Debt / EBITDA 19x

54 customers

830 employees

3 plants

Installed capacity of 1,654 MW *

US$ 1.2 billion in liabilities

US$ 3.2 billion in assets

EBITDA(LTM) of US$ 0.7 billion

Debt / EBITDA 0.8x

ONLY GENERATION:

100% Hydro – 7th

Largest Hydro Energy Generator in Brazil

* The concession contracts of HPP’s Ilha Solteira and Jupiá were ended on July 7th, 2015.

CESP has been designated to provide generation services of both plants until the winner of

the new bid take the operation.

13

CESP has three hydroelectric power plants located in the State of São Paulo with total installed capacity of 1,654 MW and total guaranteed power output of 1,081 average megawatts (MW).

14

INSTALLED

CAPACITY

14 1,540.0 1,017.0 23/Jan/99 21/May/28

2 87.0 50.0 20/Apr/78 09/Mar/21

2 27.6 14.0 05/May/72 20/May/20

52 6,649.8 3,698.5 - -

20 3,444.0 1,731.5 18/Jul/73 07/Jul/15

14 1,551.2 886.0 14/Apr/69 07/Jul/15

34 4,995.2 2,617.5 - -

GENERATING

UNITS

PHYSICAL GUARANTEE

(AVERAGE MW)

START

OF

OPERATIONS

CONCESSION

MATURITY

DATE

JUPIÁ

PORTO PRIMAVERA

ILHA + JUPIÁ

PARAIBUNA

JAGUARI

T O T A L

ILHA SOLTEIRA

18 1,654.6 1,081.0 - - PP+PAR+JAG

POWER PLANTS

15

Expiration of Concession

Nov 2011

MP 579

Edition

Including Três Irmãos

Sep 2012

CESP refuses

to renew the

concession

pursuant to

MP 579

Dec 2012

Auction of the Plant

CESP does

not take part

Mar 2014

CESP takes a lawsuit in

the amount of R$ 6.7

billion aiming to

receive the

undisputed

value of R$ 1.7 billion.

Justice denies. CESP appeals and

pleads to receive it in

7 years

Jul 2014

Favorable decision to

CESP

Union appeals

Nov 27 2014 Oct 19 2015

Union obtains a favorable

decision

CESP appeals

Payments have not started

16

MP 579 Edition

Including Ilha Solteira

and Jupiá

Indemnificati

on of R$ 20 million

Sep 2012

CESP refuses

to renew the

concession

pursuant to

MP 579

Dec 2012

Maturation of ACR

contracts

CESP sells 500 MW for

2014 and 100 MW for 1st half of

2015

Dec 2013

Accounting Effects

Provision of IFRS values

Dec 31 2014 Jul 7 2015

Expiration of Concession

Oct 2015

CTG (single applicant)

won the bid for Ilha

Solteira and Jupiá power

plants. Bonus for the grant

of R$ 13.8 billion

Nov 2015

Ministry defined R$ 2

million as compensation for Ilha Solteira

CESP filed a lawsuit

demanding compensation

of R$ 1.5 billion

Ilha Solteira and Jupiá HPP

17

September / 30 / 2015

(R$ million)

Três

Irmãos

Ilha

Solteira Jupiá Total

Assets Available for Reversion 3,529.1 2,126.3 589.6 6,244.9

Provision - Contingent Asset (1,811.7) - - (1,811.7)

Provision - Impairment - (1,656.9) (335.5) (1,992.5)

Accounting Balance 1,717.4 469.4 254.0 2,440.7

18

OPERATIONAL PERFORMANCE

2009 2010 2011 2012 2013 2014 2015

0.928 0.934 0.930 0.925 0.925 0.931 0.940

0.897

0.897

Source: ONS

0.0249

Data compiled by November 2015

19

OPERATIONAL PERFORMANCE

0,0059

0,0063

0,0069 0,0095

0,0101

0,0088

0,0050

2009 2010 2011 2012 2013 2014 2015

0.0249

2007 2008 2009 2010 2011 2012 2013 9M14 9M15

41.203 41.139 39.831 40.947 41.056 42.353

35.946

22.052

14.766 *

20

Energy Production (GWh)

34.304

Physical Guarantee: 3,698 MW avarage and 1.081 *

*without considering HPP’s Ilha Solteira and Jupiá

21

57.51

67.33

75.46

83.13

93.40

62.10

68.37

77.70 83.50

94.91

50,0

60,0

70,0

80,0

90,0

100,0

110,0

120,0

130,0

140,0

150,0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

109,40

270.81 (A-0)

104.74

5º Leilão – 2007 Energia Existente

132.39

116.00

(Botox)

121.81

134.99

120.86

128.42

137.44

78.87

(UHE - Sto.

Antonio) 71.37

(UHE

Jirau)

98.98

(UHE - Bxo.

Iguaçu)

145.23

(UTE’s

Outras

Fontes

77.97

Belo Monte

58.35 Teles Pires

124.97

(Botox)

126.77

134.67

138.85

191.41

128.37

99,48

Vários

67,31

11º LEN

91,20

UHE São

Roque

New Energy Auctions – Average (Hydro)

New Energy Auctions – Average (Thermal)

Alternative Energy Source Auctions – (Hydro)

Alternative Energy Sources Auctions – (Thermal)

105,12

13º LEN

Renewable Sources Auctions – (Wind Power)

UHE SINOP

165.20

129.97

Existing Energy Auctions – Average Existing Energy Auctions – CESP

New Energy Auctions – CESP

(Botox Energy 100%)

22

23

Capital Increase R$ 3.2 billions

Term: 10 years Grace Period: 5

years (for principal)

To match its cash flow generation with its debt service, CESP has launched a comprehensive capital restructuring plan with the following main components:

Privatization of CTEEP – R$ 1.2 billion Jul/2006

Public Offering of Preferred Class B Shares (PNB) – R$ 2.0 billion

Jul/2006

Bonds Operations US$220 millions = R$ 488 million - Aug/2006 US$350 millions = R$750 million - Jan/2007

FIDC III – R$ 650 million Aug/2006

FIDC IV – R$ 1.25 billion Jun/2007

Funds Involved in the Restructuring - R$ 6.3 billion

1.2

2.0

1.2

0.65

1.25

C

T

E

E

P

P

U

B

L

I

C

O

F

F

E

R

B

O

N

D

S

FIDC III

F

I

D

C

IV

24

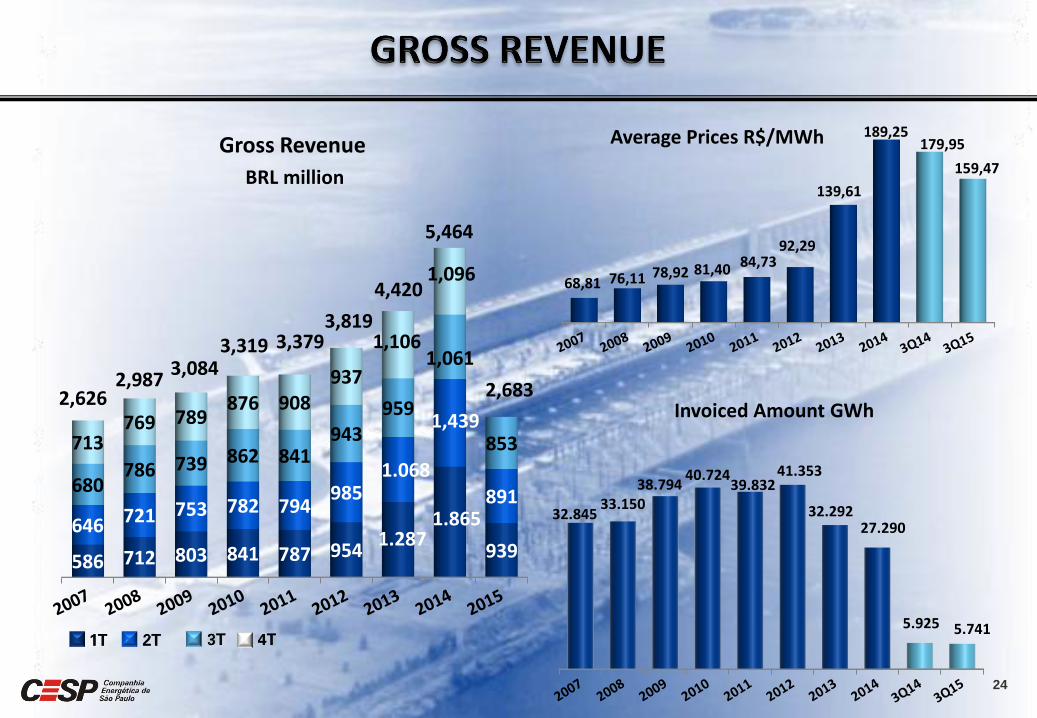

Gross Revenue

BRL million

32.845 33.150

38.794 40.724

39.832 41.353

32.292 27.290

5.925 5.741

586 712 803 841 787 954 1.287

1.865

939 646 721 753 782 794

985 1.068

1,439

891 680

786 739 862 841 943

959

1,061

853 713 769 789

876 908 937

1,106

1,096 68,81 76,11 78,92 81,40 84,73 92,29

139,61

189,25 179,95

159,47

2,626

3,819 3,319

3,084 2,987

4,420

5,464

3,379

Average Prices R$/MWh

Invoiced Amount GWh 2,683

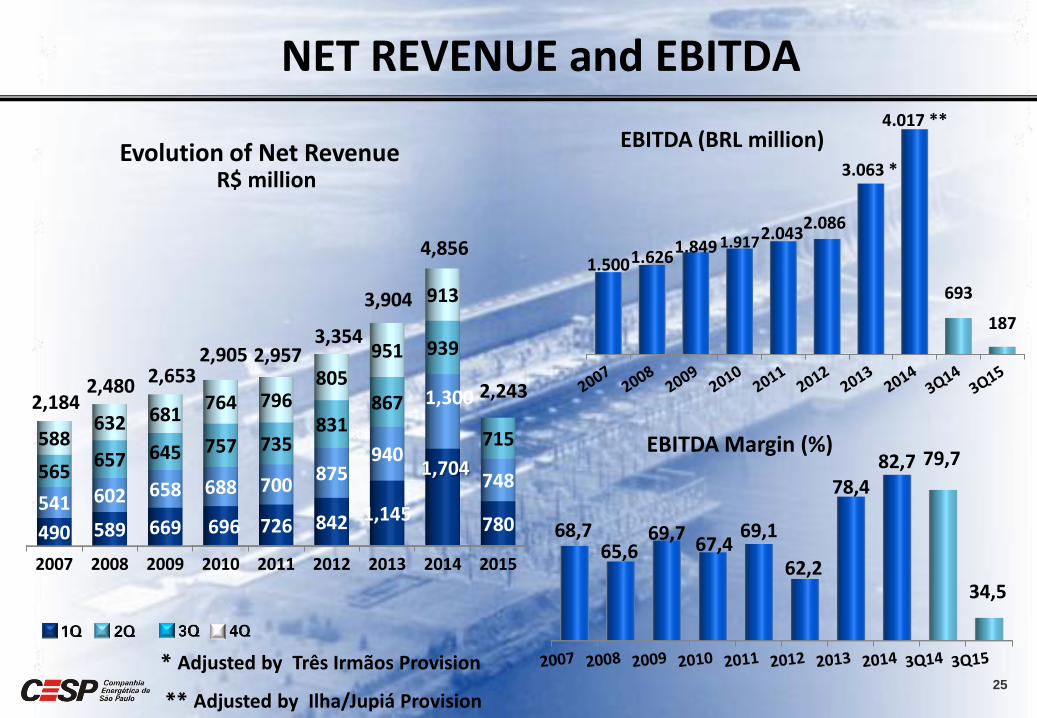

68,7 65,6

69,7 67,4

69,1

62,2

78,4 82,7 79,7

34,5

EBITDA Margin (%)

25

2007 2008 2009 2010 2011 2012 2013 2014 2015

490 589 669 696 726 842 1,145

1,704

780 541 602 658 688 700

875 940

1,300

748 565 657 645 757 735

831 867

939

715 588 632 681

764 796 805

951

913

2,184 2,480 2,653

2,905 2,957

1.500 1.626 1.849 1.917 2.043

2.086

3.063 *

4.017 **

693

187 3,354

Evolution of Net Revenue R$ million

3,904

* Adjusted by Três Irmãos Provision

NET REVENUE and EBITDA

4,856

** Adjusted by Ilha/Jupiá Provision

EBITDA (BRL million)

2,243

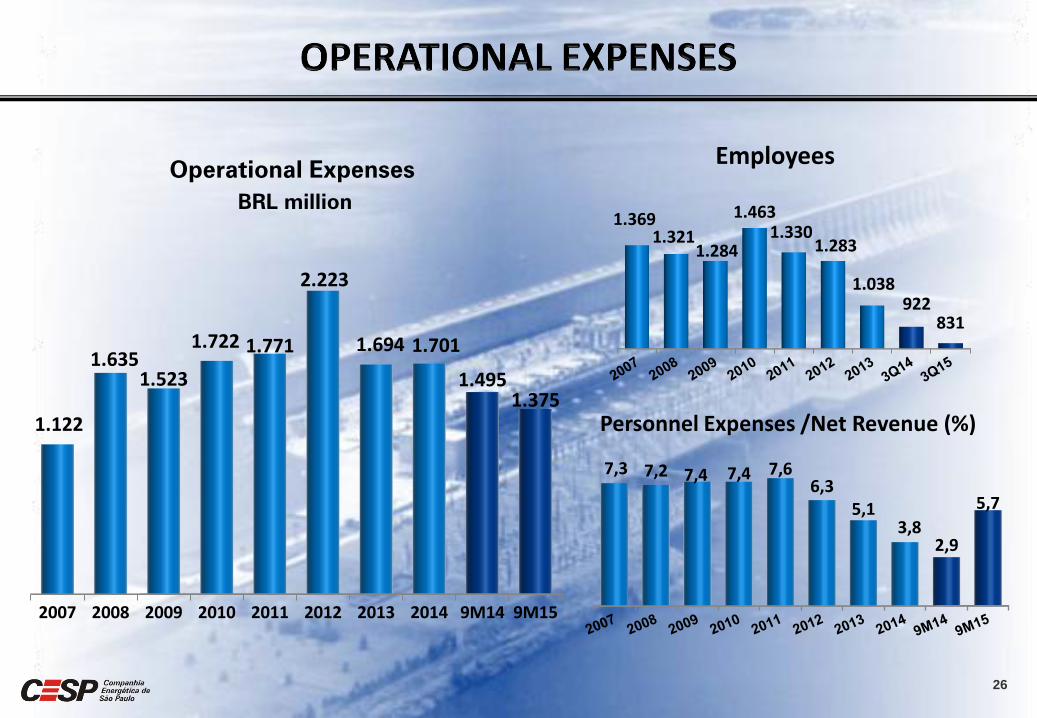

26

2007 2008 2009 2010 2011 2012 2013 2014 9M14 9M15

1.122

1.635 1.523

1.722 1.771

2.223

1.694 1.701

1.495 1.375

1.369 1.321

1.284

1.463 1.330

1.283

1.038 922

831

7,3 7,2 7,4 7,4 7,6 6,3

5,1 3,8

2,9

5,7

Operational Expenses

BRL million

Personnel Expenses /Net Revenue (%)

Employees

27

2007 2008 2009 2010 2011 2012 2013 2014 9M14 9M15

814

721

592

466 443

380 331

278

209 101

Debt Charges + Monetary Variation

(Excluding Exchange Variation)

R$ million

28

Capital Investments

R$ million

2007 2008 2009 2010 2011 2012 2013 2014 9M15

186

210

101 116 123 129

86

32 15

29

EBITDA (Adjusted) Margin 34.5 % 79.7% -45.2 p.p.

OPERATIONAL RENEVUE 853 1,061 - 19.6%

Net Operational revenue 715 901 - 20.6%

EBITDA (Adjusted) 246 718 - 65.7%

Net Income (Loss) (67) 374 N.A.

FINANCIAL HIGHLIGTHS

Financial Results (204) (59) 245%

R$ million

30

EBITDA (Adjusted) Margin 62.1 % 86.4% -24.3 p.p.

OPERATIONAL RENEVUE 2,684 4,367 - 38%

Net Operational revenue 1,528 2,905 - 41%

EBITDA (Adjusted) 1,392 3,288 - 57%

Net Income 302 1,708 - 72.3%

FINANCIAL HIGHLIGTHS

Financial Results (359) (96) +275%

R$ million

Interest on Equity 193

31

32

Evolution by Currency

FINANCIAL DEBT

September/ 30/2015 R$ 1,719 million

7.5 6.9 7.0

5.3 4.5

4.2 3.7

3.0

-82%

9.8

8.1 6.2 4.6 4.3 2.8 2.2 2.1 1.7 1.1 0.7 0.8

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q15

45%

55%

1.7

36%

45%

64% 61% 65% 63% 69% 66%

75% 74%

55% 39%

35%

37% 31%

34%

25% 26%

55%

45%

2.8

Local Currency

Debt /

EBITDA

FIDC R$374 21,8%

ELETROBRAS R$ 21 1,2%

Fundação CESP R$ 375

21,8%

BIB'S R$ 2 0,1%

BNDES BRADY R$ 947 55,1%

33

September/30/2015 R$ 1,719 million

Debt in Foreign Currency

US$ 244 million

FINANCIAL DEBT

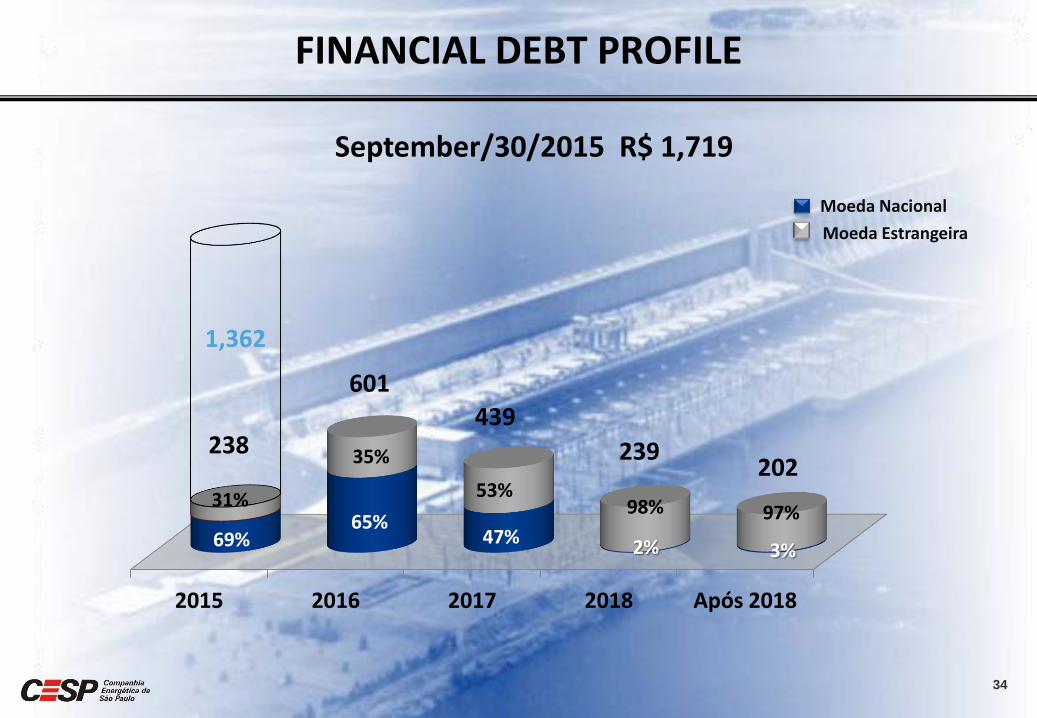

2015 2016 2017 2018 Após 2018

1,362

31%

34

439

239 202

Moeda Nacional

601

69% 65%

35%

53%

47% 2%

98% 97%

3%

Moeda Estrangeira

238

FINANCIAL DEBT PROFILE

September/30/2015 R$ 1,719

35

1 -

2 -

3 -

4 -

Low Operational Costs

Low CAPEX Requirements

Low Working Capital Requirements (less than 5% of net revenues)

Tax Credits Reducing Future Tax Payments

(R$2.3 billion)

Several factors enable CESP to generate strong operational cash flow.

36

37

TOTAL CAPITAL COMMON x PREFERRED

ON 33.3%

PNA 2.3%

PNB 64.4%

ON 1/3

PNA + PNB

2/3

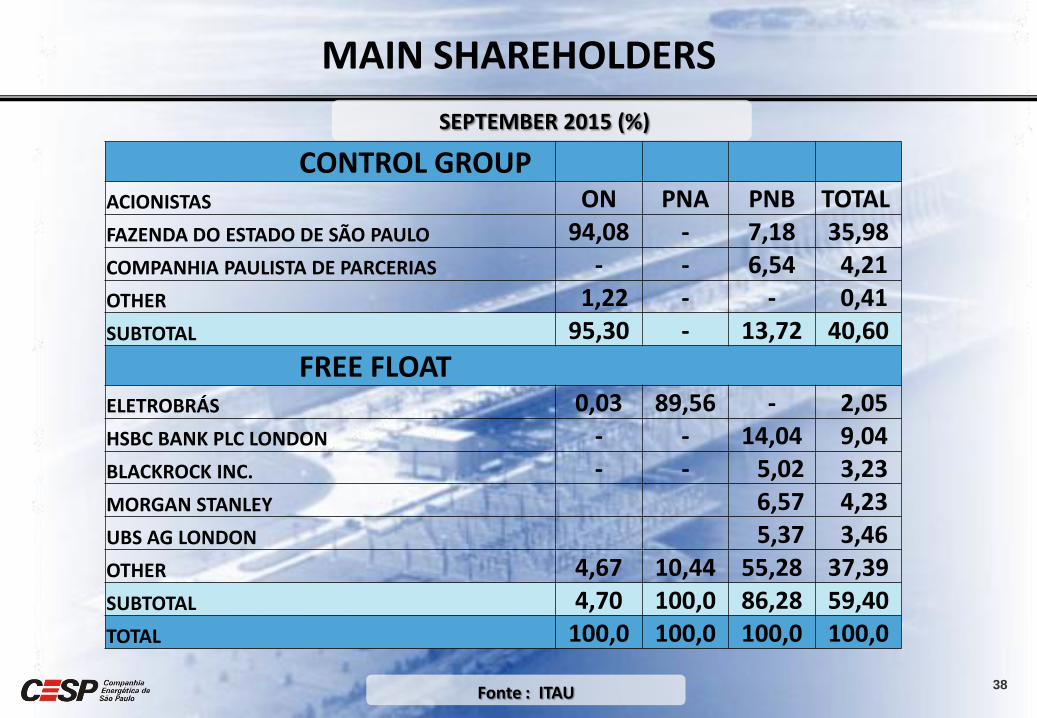

38 Fonte : ITAU

SEPTEMBER 2015 (%)

CONTROL GROUP ACIONISTAS ON PNA PNB TOTAL

FAZENDA DO ESTADO DE SÃO PAULO 94,08 - 7,18 35,98

COMPANHIA PAULISTA DE PARCERIAS - - 6,54 4,21

OTHER 1,22 - - 0,41

SUBTOTAL 95,30 - 13,72 40,60

FREE FLOAT ELETROBRÁS 0,03 89,56 - 2,05

HSBC BANK PLC LONDON - - 14,04 9,04

BLACKROCK INC. - - 5,02 3,23

MORGAN STANLEY 6,57 4,23

UBS AG LONDON 5,37 3,46

OTHER 4,67 10,44 55,28 37,39

SUBTOTAL 4,70 100,0 86,28 59,40

TOTAL 100,0 100,0 100,0 100,0

MAIN SHAREHOLDERS

39

Market 5%

SP Estate 95%

Market 87%

State SP 13%

Common and Preferred (PNA + PNB)

Common Shares Preferred (PNA + PNB)

40

2.6

3.8

93.6

5.1

7.4

181.9

80.1

133.9

3,480.9

33.3

2.3

64.4

109.2

7.4

210.9

1,710.7

133.9

4,034.4

100.0 194.5 3,694.9 100.0 327.5 5,879.0

R$ million

September 2015

41

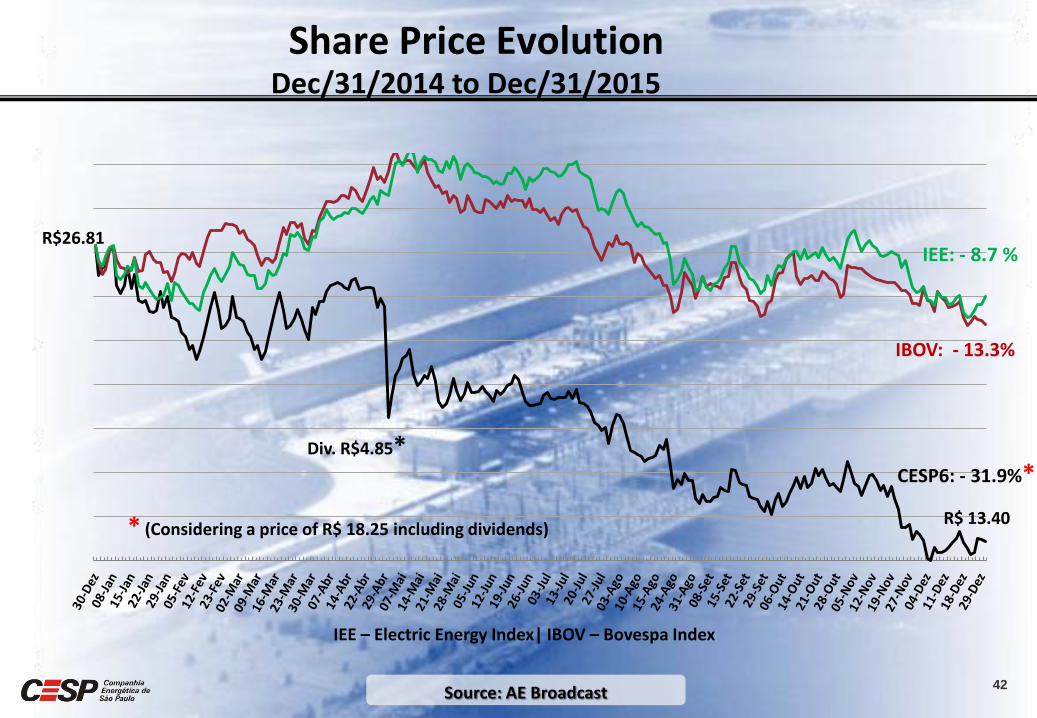

Share Price Evolution

Source: AE Broadcast

IEE – Electric Energy Index| IBOV – Bovespa Index

Dec/31/2014 to Dec/31/2015

Div. R$4.85*

R$26.81

R$ 13.40

CESP6: - 31.9%*

IEE: - 8.7 %

IBOV: - 13.3%

42

* (Considering a price of R$ 18.25 including dividends)

43

Evolution from 2003 to 2015

44