Embed Size (px)

Citation preview

SIMS 2009The 2nd Seoul International Maritime and Shipbuilding

Conference

17 September 2009

Peter M. SwiftManaging Director, INTERTANKO

Key Issues for Shipowners Today

Key Issues for Shipowners Today ?• Establishing an international framework of

consistent regulations and standards

• Delivering best environmental performance

• Ensuring availability of good people (and quality ships)

• Ensuring welfare and well-being of ships’ crews

• Meeting the challenges of Piracy

• Surviving the financial crisis

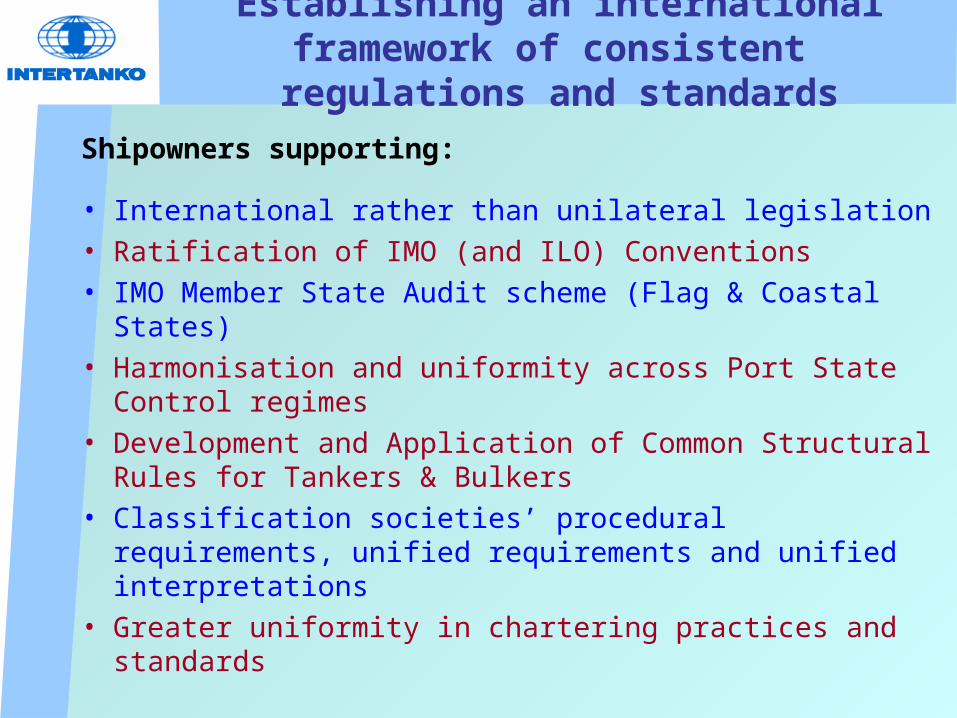

Establishing an international framework of consistent regulations and standards

Shipowners supporting:

• International rather than unilateral legislation• Ratification of IMO (and ILO) Conventions• IMO Member State Audit scheme (Flag & Coastal States) • Harmonisation and uniformity across Port State Control

regimes• Development and Application of Common Structural Rules

for Tankers & Bulkers• Classification societies’ procedural requirements, unified

requirements and unified interpretations• Greater uniformity in chartering practices and standards

Delivering best environmental performance

• Air emissions - Green House Gases - Exhaust Gas emissions (Annex VI & its revisions) - VOC emissions

• Spill Prevention and Response Planning• Ballast Water management • Biofouling• Antifouling systems• Ship Recycling• Port Reception Facilities (adequacy & affordability) • Waste management (onboard and ashore)• Radiated Noise pollution• Cetacean strikes

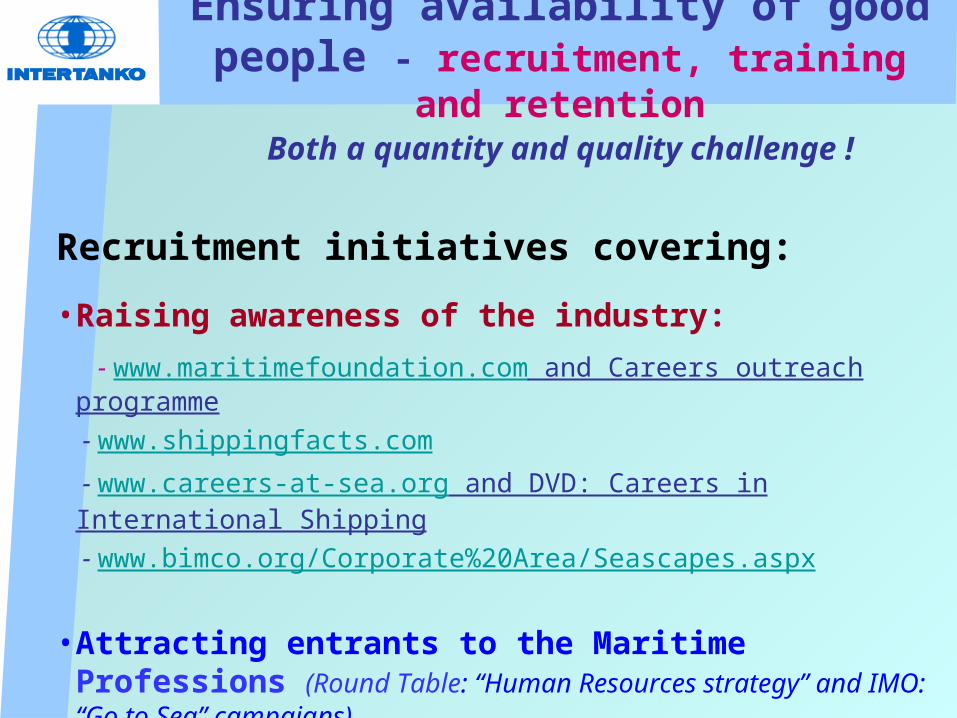

Ensuring availability of good people - recruitment, training and retention

Both a quantity and quality challenge !

Recruitment initiatives covering: • Raising awareness of the industry: - www.maritimefoundation.com and Careers outreach programme - www.shippingfacts.com - www.careers-at-sea.org and DVD: Careers in International Shipping - www.bimco.org/Corporate%20Area/Seascapes.aspx

• Attracting entrants to the Maritime Professions (Round Table: “Human Resources strategy” and IMO: “Go to Sea” campaigns)

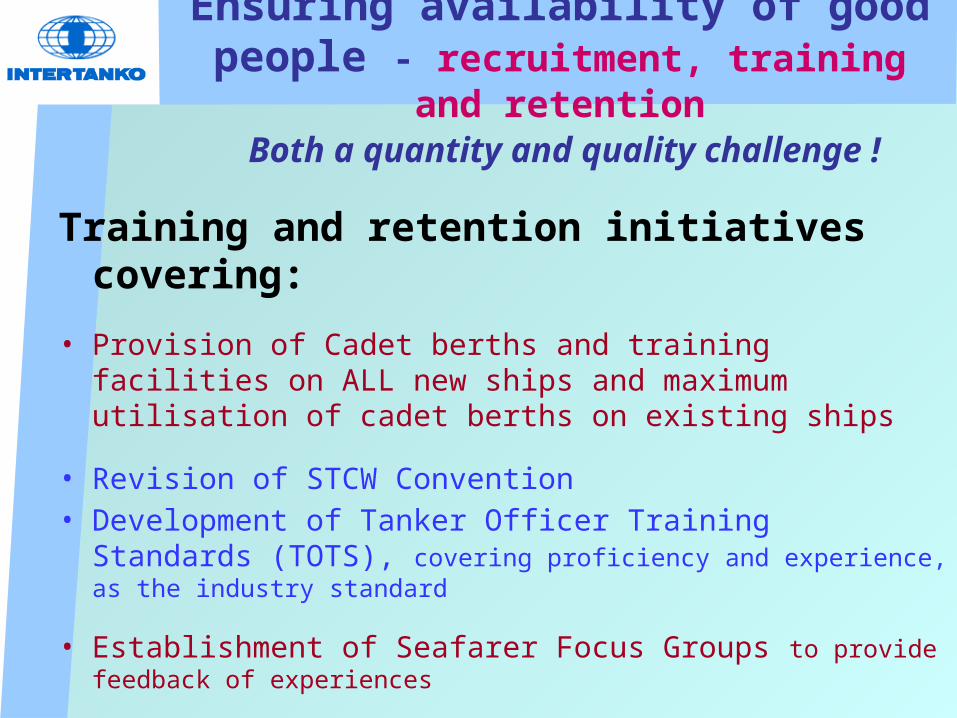

Ensuring availability of good people - recruitment, training and retention

Both a quantity and quality challenge !

Training and retention initiatives covering: • Provision of Cadet berths and training facilities on ALL new

ships and maximum utilisation of cadet berths on existing ships

• Revision of STCW Convention• Development of Tanker Officer Training Standards (TOTS),

covering proficiency and experience, as the industry standard

• Establishment of Seafarer Focus Groups to provide feedback of experiences

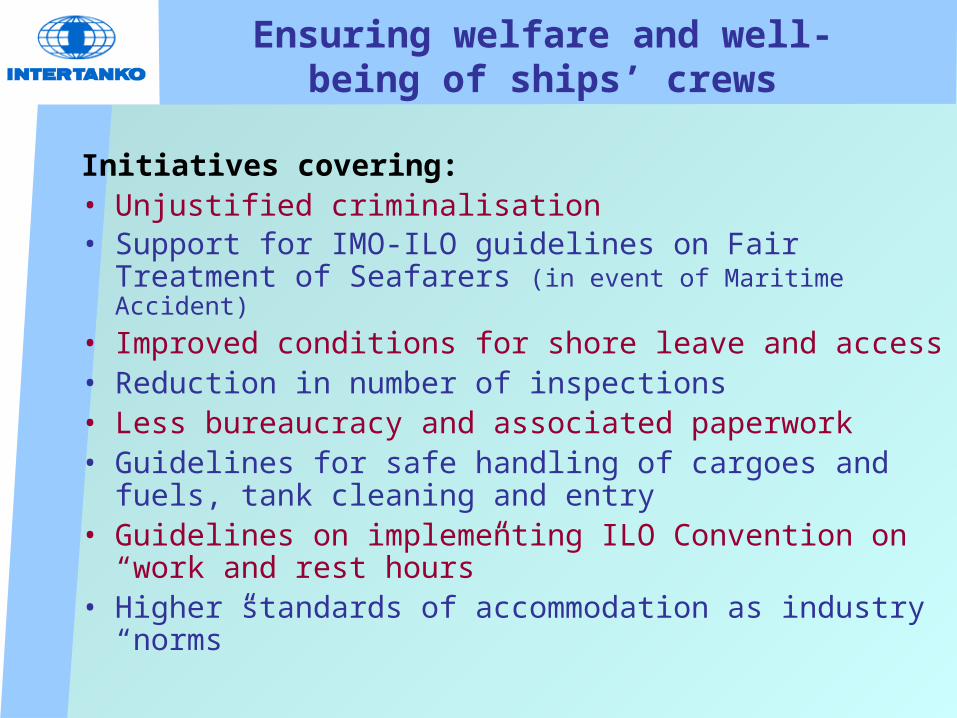

Ensuring welfare and well-being of ships’ crews

Initiatives covering: • Unjustified criminalisation• Support for IMO-ILO guidelines on Fair Treatment of

Seafarers (in event of Maritime Accident)• Improved conditions for shore leave and access • Reduction in number of inspections• Less bureaucracy and associated paperwork• Guidelines for safe handling of cargoes and fuels, tank

cleaning and entry• Guidelines on implementing ILO Convention on “work and

rest hours” • Higher standards of accommodation as industry “norms”

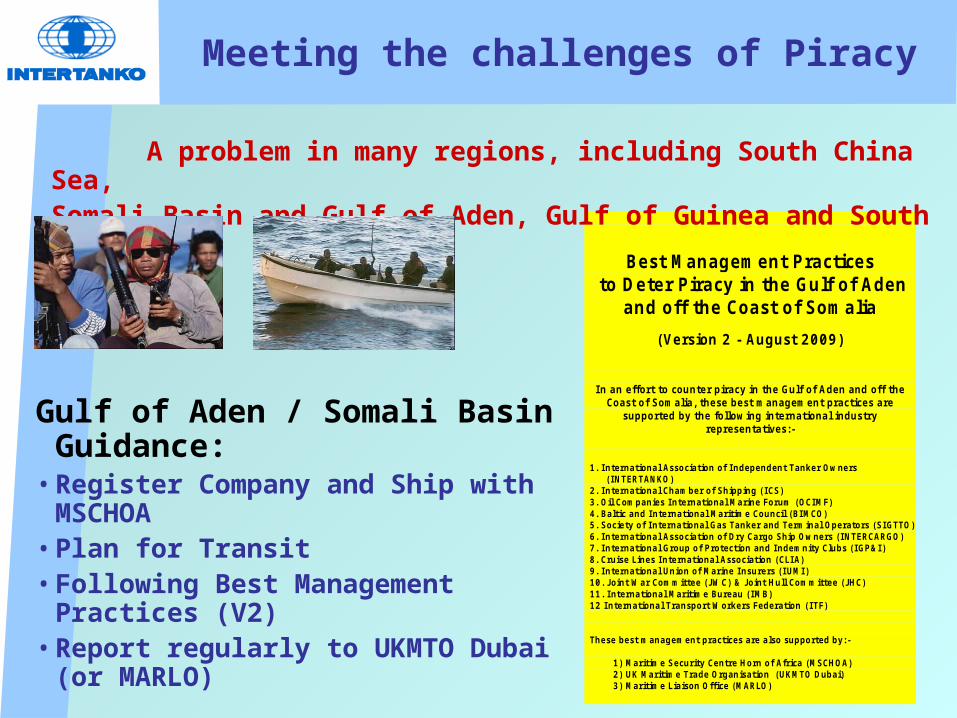

Meeting the challenges of Piracy

Gulf of Aden / Somali Basin Guidance:

• Register Company and Ship with MSCHOA

• Plan for Transit• Following Best Management Practices

(V2) • Report regularly to UKMTO Dubai (or

MARLO)

Best Management Practices to Deter Piracy in the Gulf of Aden

and off the Coast of Somalia

(Version 2 - August 2009)

I n an effort to counter piracy in the Gulf of Aden and off the Coast of Somalia, these best management practices are

supported by the following international industry representatives:-

1. I nternational Association of I ndependent Tanker Owners (I NTERTANKO)

2. I nternational Chamber of Shipping (I CS) 3. Oil Companies I nternational Marine Forum (OCIMF) 4. Baltic and International Maritime Council (BIMCO) 5. Society of I nternational Gas Tanker and Terminal Operators (SIGTTO) 6. I nternational Association of Dry Cargo Ship Owners (I NTERCARGO) 7. I nternational Group of Protection and I ndemnity Clubs (I GP&I ) 8. Cruise Lines I nternational Association (CLI A) 9. I nternational Union of Marine I nsurers (I UMI ) 10. J oint War Committee (J WC) & J oint Hull Committee (J HC) 11. I nternational Maritime Bureau (IMB) 12 I nternational Transport Workers Federation (ITF) These best management practices are also supported by:- 1) Maritime Security Centre Horn of Africa (MSCHOA) 2) UK Maritime Trade Organisation (UKMTO Dubai) 3) Maritime Liaison Office (MARLO)

A problem in many regions, including South China Sea, Somali Basin and Gulf of Aden, Gulf of Guinea and South America !

Surviving the financial crisis !

• Demand : World trade & by sector

• Supply : Ships on Order & Fleet development

• Shipbuilding capacity

• Tanker market

SIMS 2008

Issues and Challenges for Tanker Shipping

Global Financial Crisis

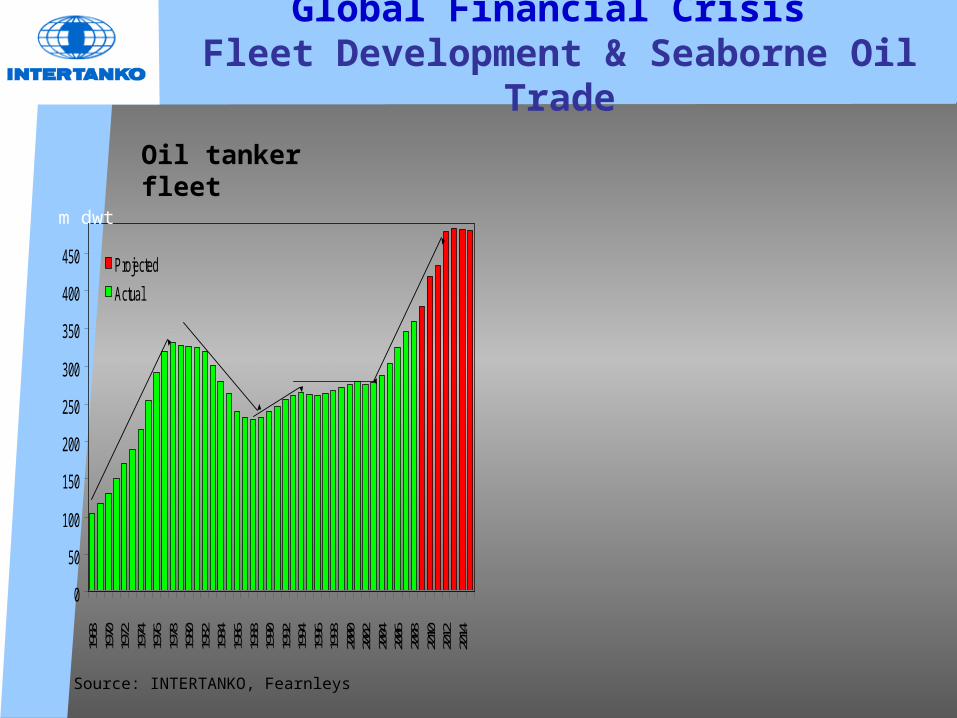

Global Financial Crisis Fleet Development & Seaborne Oil Trade

0

50

100

150

200

250

300

350

400

450

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

ProjectedActual

Oil tanker fleet

m dwt

Source: INTERTANKO, Fearnleys

0

2,500

5,000

7,500

10,000

12,500

72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06P08

P10

Oil productsCrude oil

???

Source: INTERTANKO, Fearnleys

Seaborne oil trade

bn tonne milesbn tonne miles

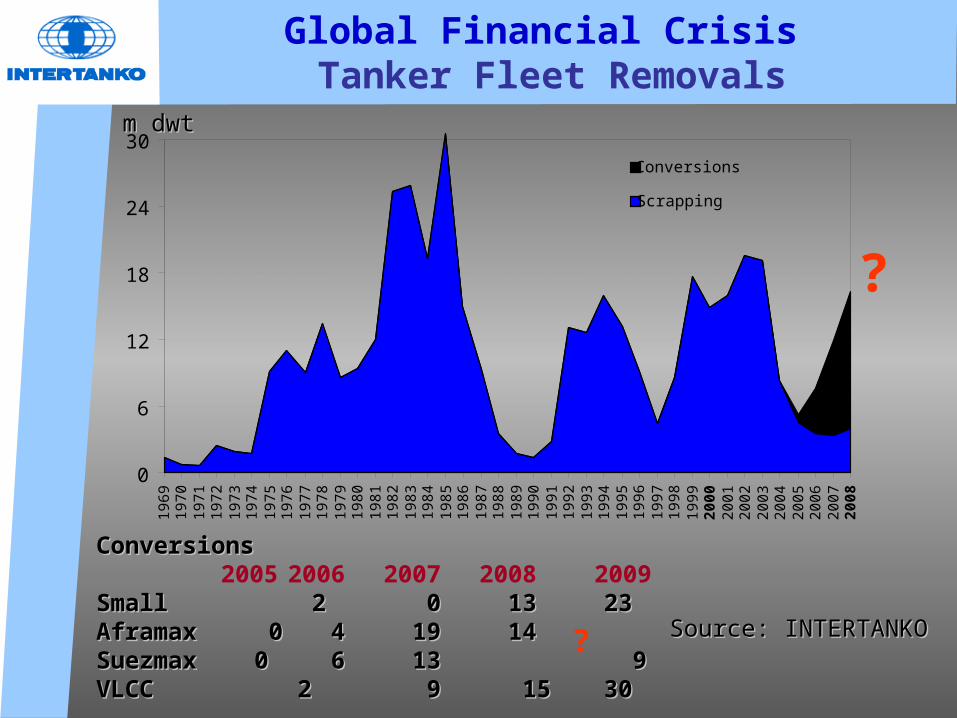

Global Financial Crisis Tanker Fleet Removals

Source: INTERTANKOSource: INTERTANKO

m dwtm dwt

ConversionsConversions 2005 2006 2007 2008 2009

Small 2Small 2 0 0 13 13 23 23Aframax 0Aframax 0 4 4 19 19 14 14Suezmax 0Suezmax 0 6 6 13 13 9 9VLCC 2VLCC 2 9 9 15 15 30 30

0

6

12

18

24

3019

6919

7019

7119

7219

7319

7419

7519

7619

7719

7819

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

08

Conversions

Scrapping

?

?

Credit crunch – liquidity; financing; exposures; covenants & more….

• Oil prices ?• Steel prices ?• Newbuild / scrap prices ?• Economic slowdown (or meltdown !) ?• Green agenda slowdown ?• Markets ?• Other ?

Global Financial Crisis

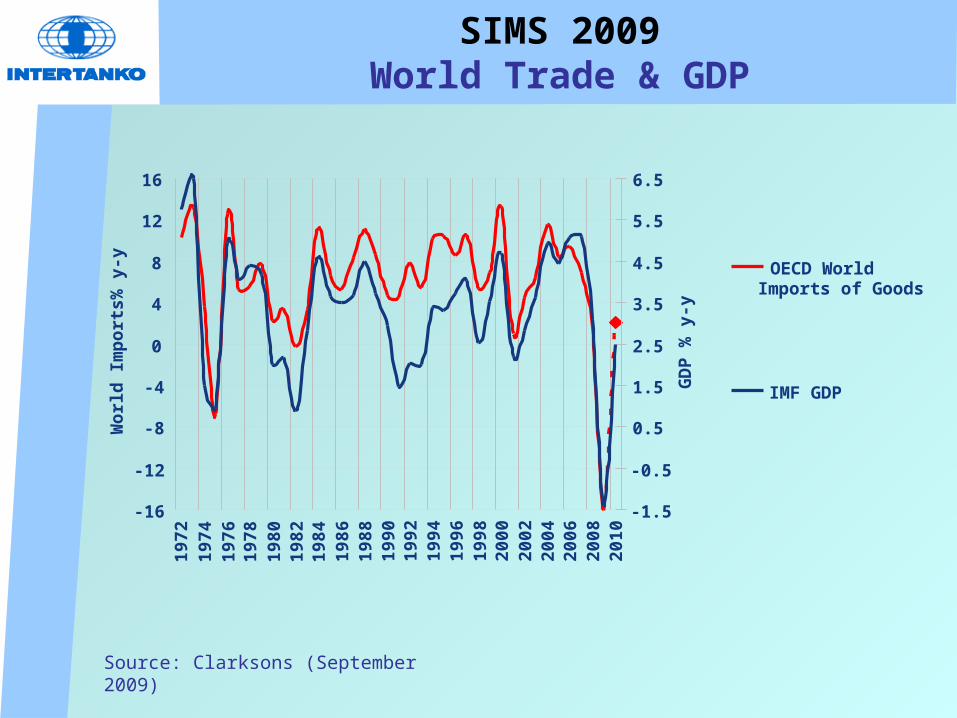

SIMS 2009World Trade & GDP

-16

-12

-8

-4

0

4

8

12

1619

7219

7419

7619

7819

8019

8219

8419

8619

8819

9019

9219

9419

9619

9820

0020

0220

0420

0620

0820

10

Wor

ld Im

port

s% y

-y

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

6.5

GD

P %

y-y

OECD WorldImports of Goods

IMF GDP

Source: Clarksons (September 2009)

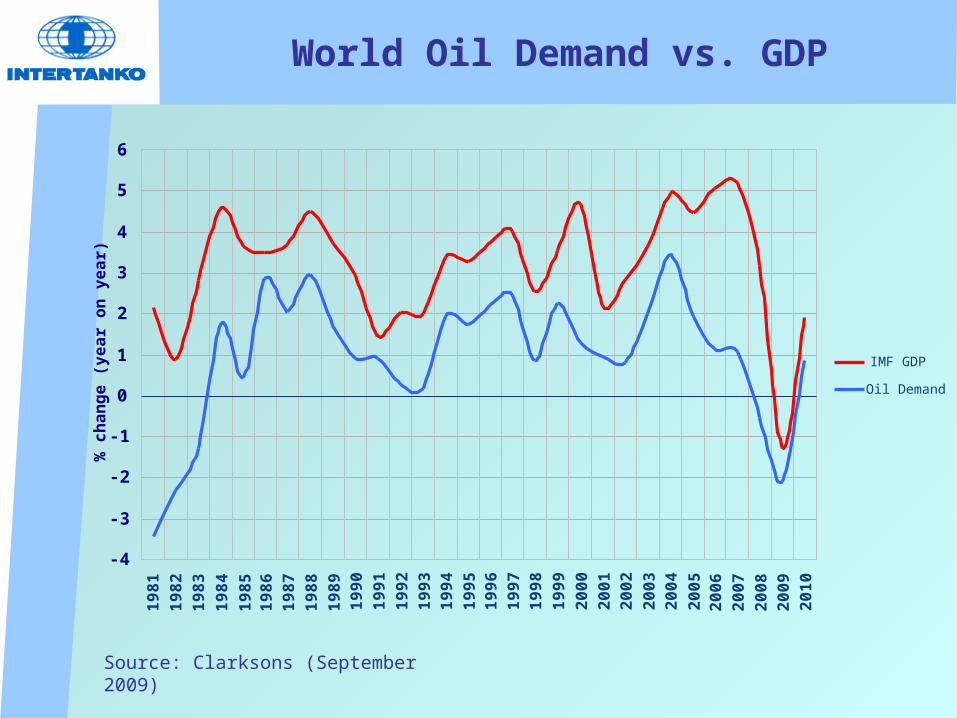

World Oil Demand vs. GDP

-4

-3

-2

-1

0

1

2

3

4

5

619

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

10

% c

hang

e (y

ear o

n ye

ar)

IMF GDP

Oil Demand

Source: Clarksons (September 2009)

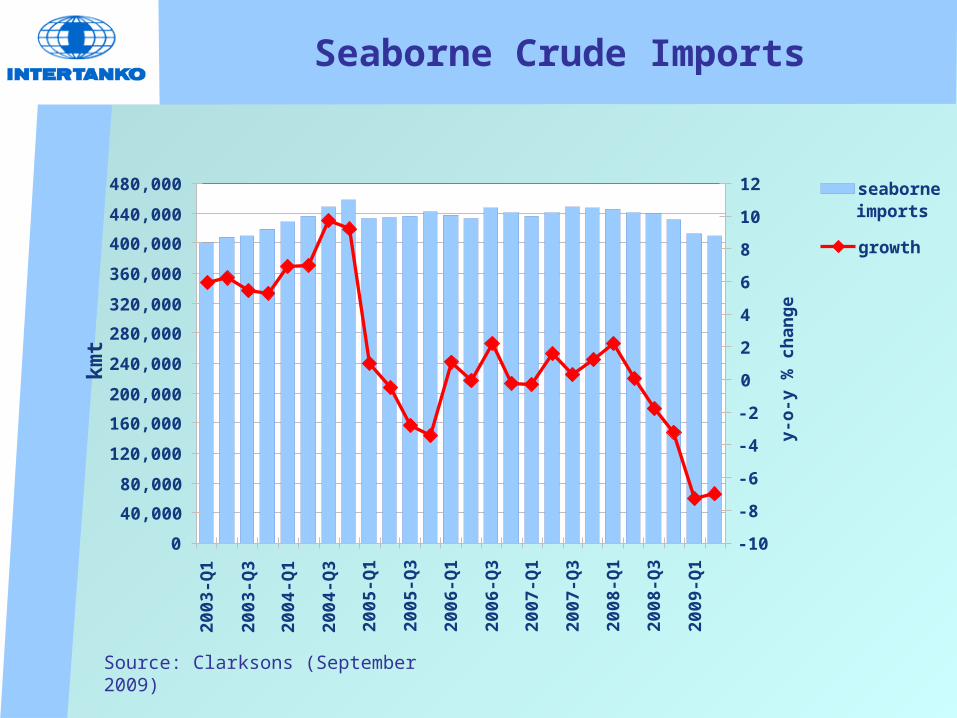

Seaborne Crude Imports

040,00080,000

120,000160,000200,000240,000280,000320,000360,000400,000440,000480,000

2003

-Q1

2003

-Q3

2004

-Q1

2004

-Q3

2005

-Q1

2005

-Q3

2006

-Q1

2006

-Q3

2007

-Q1

2007

-Q3

2008

-Q1

2008

-Q3

2009

-Q1

kmt

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

y-o-

y %

cha

nge

seaborneimports

growth

Source: Clarksons (September 2009)

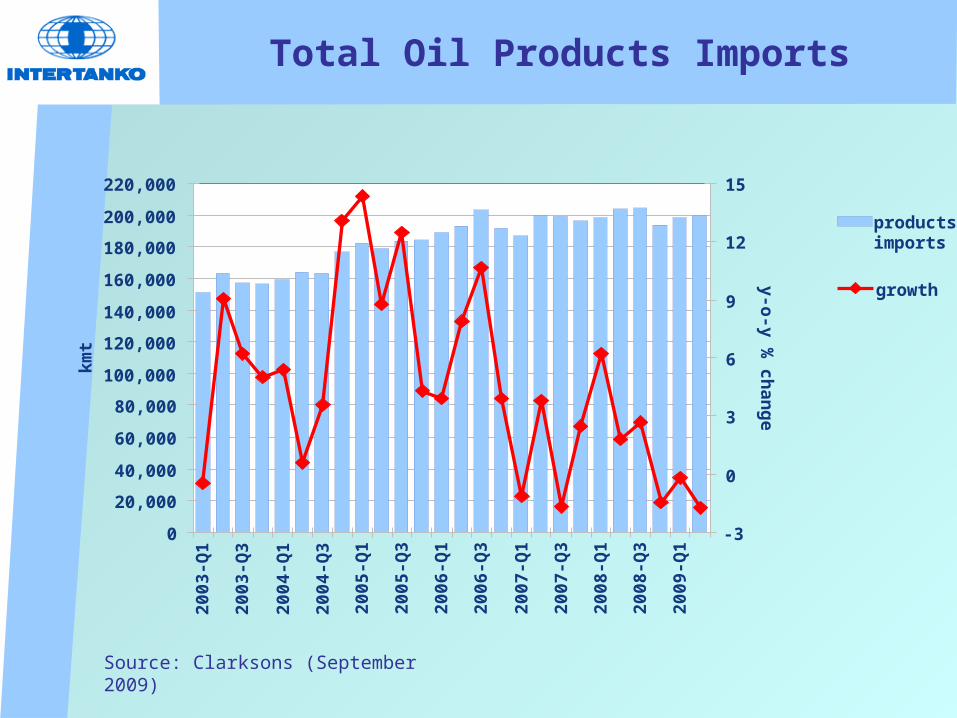

Total Oil Products Imports

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

220,00020

03-Q

1

2003

-Q3

2004

-Q1

2004

-Q3

2005

-Q1

2005

-Q3

2006

-Q1

2006

-Q3

2007

-Q1

2007

-Q3

2008

-Q1

2008

-Q3

2009

-Q1

kmt

-3

0

3

6

9

12

15y-o-y %

change

productsimports

growth

Source: Clarksons (September 2009)

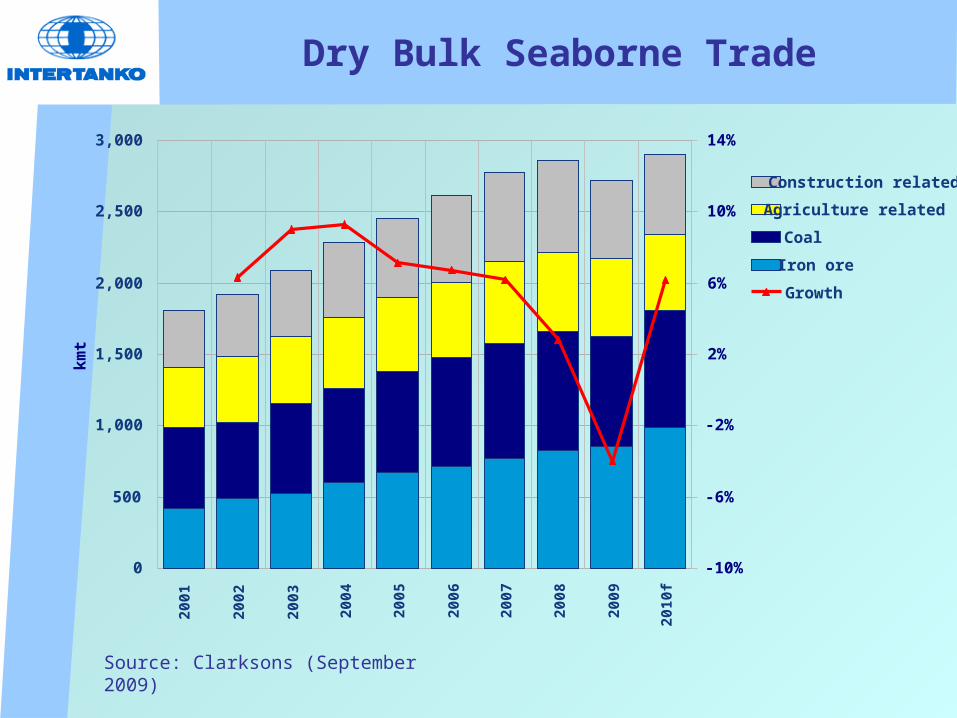

Dry Bulk Seaborne Trade

0

500

1,000

1,500

2,000

2,500

3,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

f

kmt

-10%

-6%

-2%

2%

6%

10%

14%

Construction relatedAgriculture related CoalIron oreGrowth

Source: Clarksons (September 2009)

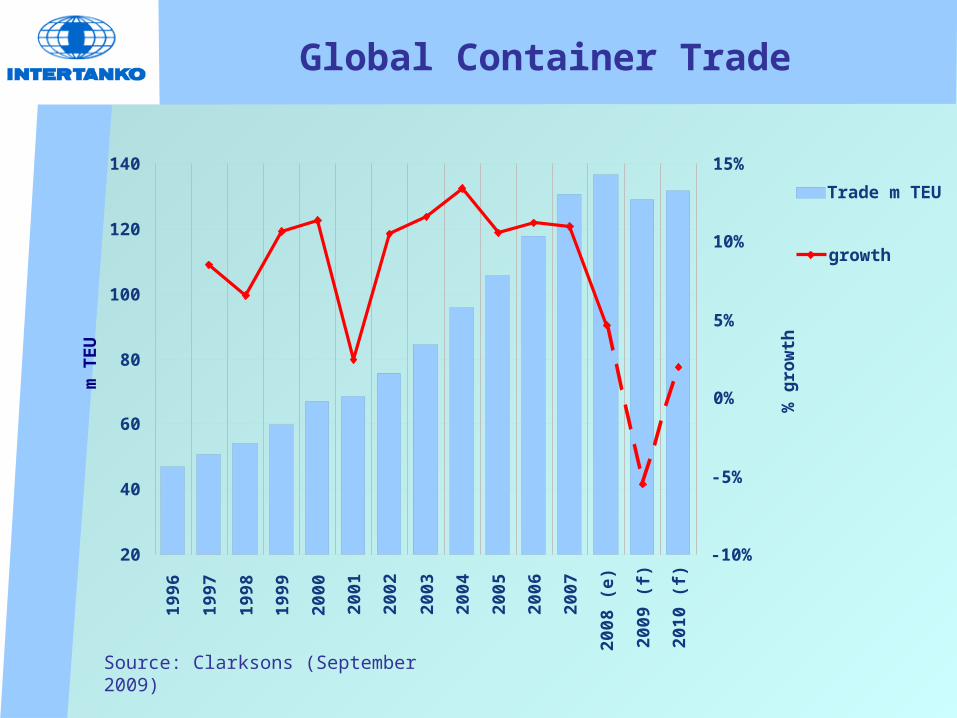

Global Container Trade

20

40

60

80

100

120

14019

96

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

(e)

2009

(f)

2010

(f)

m T

EU

-10%

-5%

0%

5%

10%

15%

% g

row

th

Trade m TEU

growth

Source: Clarksons (September 2009)

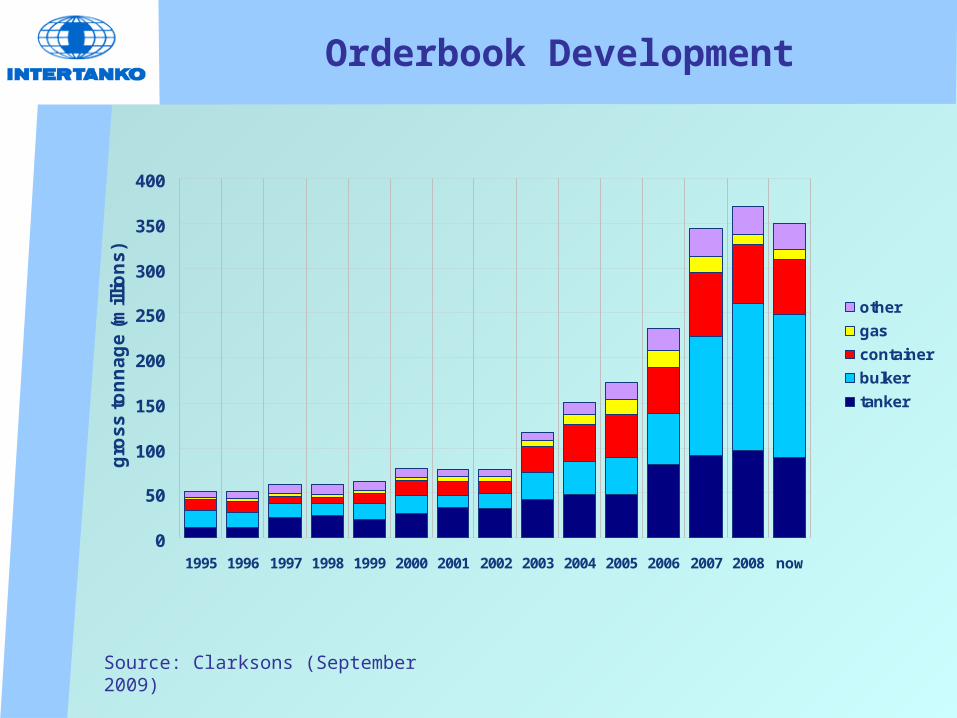

Orderbook Development

0

50

100

150

200

250

300

350

400

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 now

gros

s to

nnag

e (m

illio

ns)

othergascontainerbulkertanker

Source: Clarksons (September 2009)

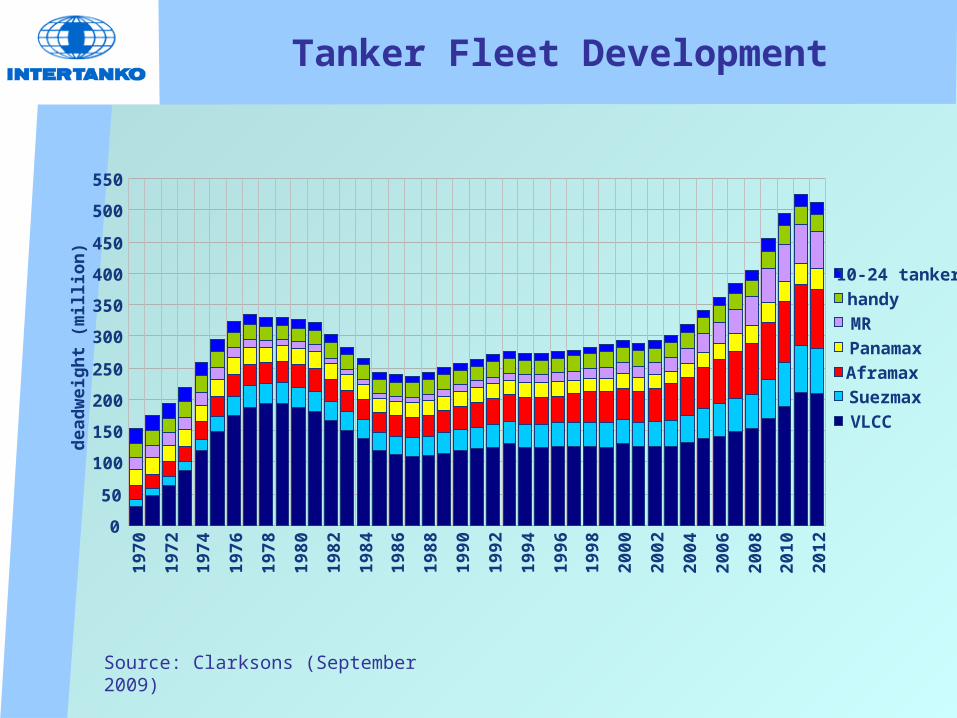

Tanker Fleet Development

0

50

100

150

200

250

300

350

400

450

500

550

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

dead

wei

ght (

mill

ion) 10-24 tanker

handyMRPanamaxAframaxSuezmaxVLCC

Source: Clarksons (September 2009)

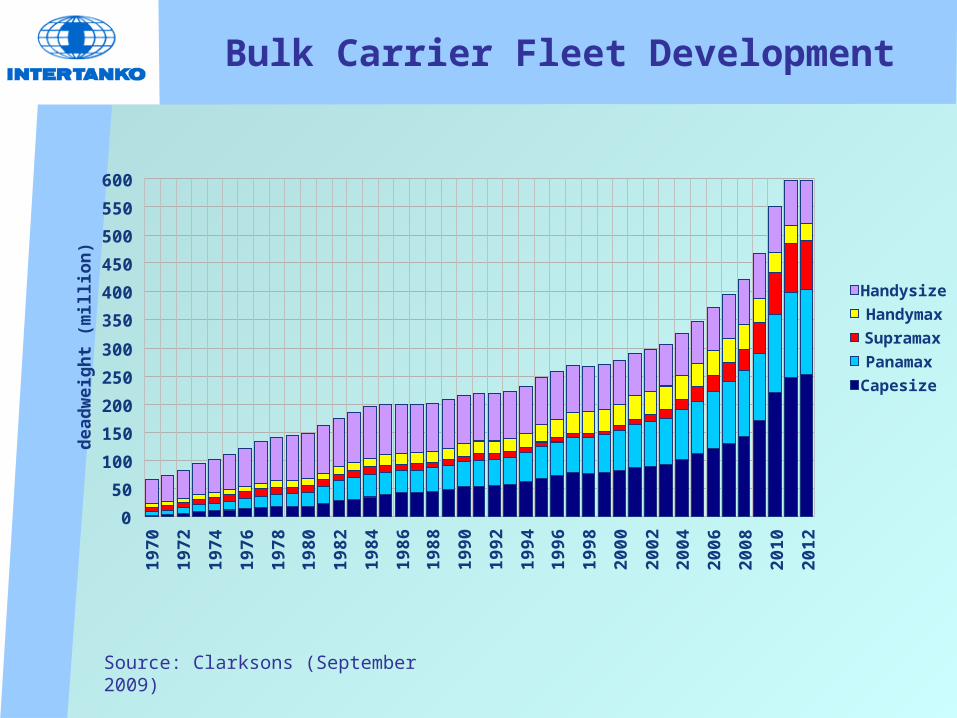

Bulk Carrier Fleet Development

050

100150200250300350400450500550600

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

dead

wei

ght (

mill

ion)

HandysizeHandymaxSupramaxPanamaxCapesize

Source: Clarksons (September 2009)

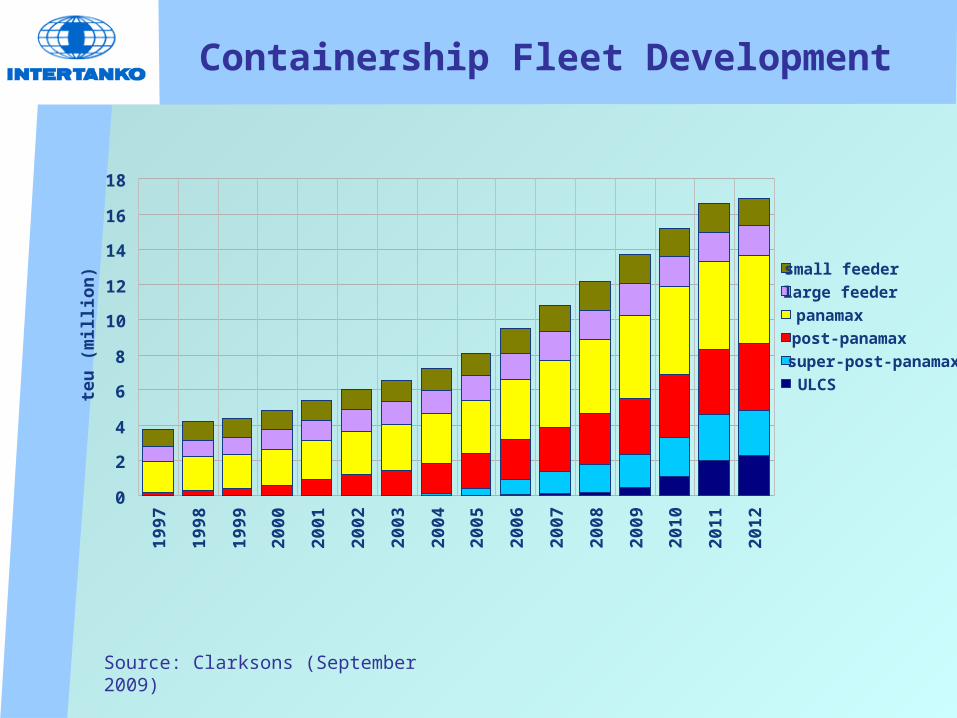

Containership Fleet Development

0

2

4

6

8

10

12

14

16

1819

97

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

teu

(mill

ion)

small feederlarge feederpanamaxpost-panamaxsuper-post-panamaxULCS

Source: Clarksons (September 2009)

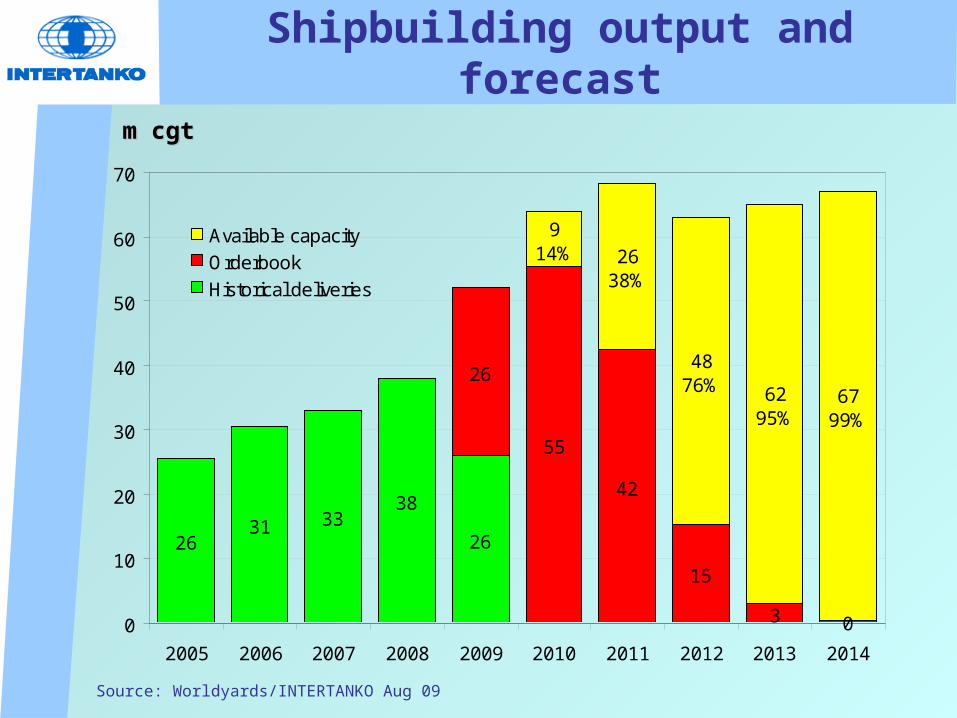

Shipbuilding output and forecast

Source: Worldyards/INTERTANKO Aug 09

m cgtm cgt

2631 33

38

26

26

55

42

15

3 0

914% 26

38%

4876% 62

95%67

99%

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Available capacityOrderbookHistorical deliveries

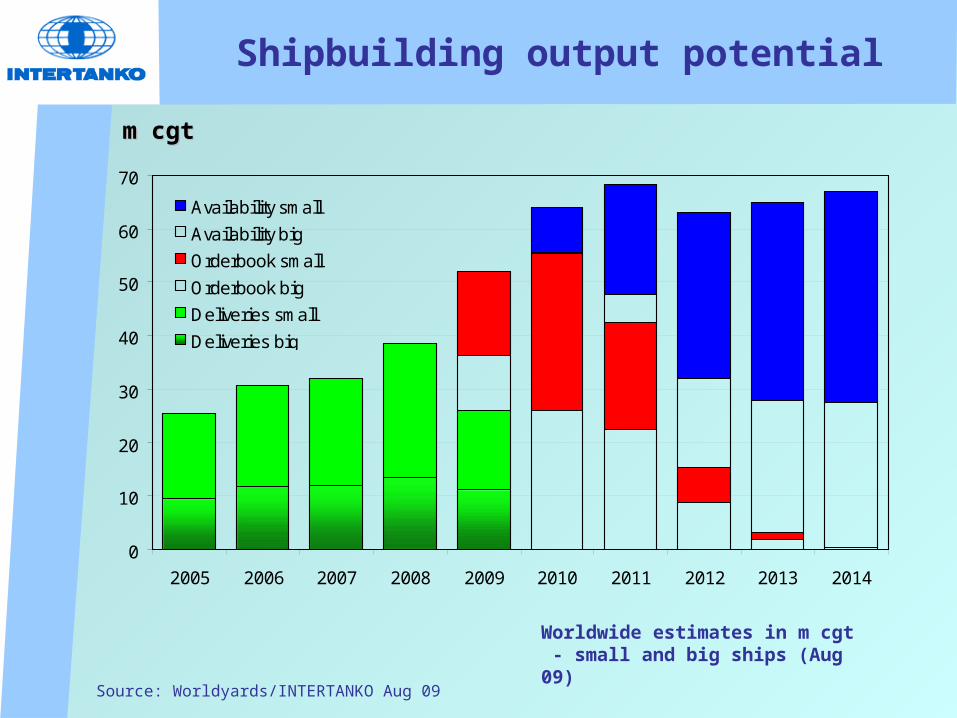

Shipbuilding output potential

Source: Worldyards/INTERTANKO Aug 09

m cgtm cgt

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Availability smallAvailability bigOrderbook smallOrderbook bigDeliveries smallDeliveries big

Worldwide estimates in m cgt - small and big ships (Aug 09)

Shipyard output potential - surplus

Implications ?

• Distressed sales / lower prices

• Quality and standards maintained or weakened

• Pressure on suppliers and sub-contractors

• Greater customer focus & customisation

• and government interventions ?

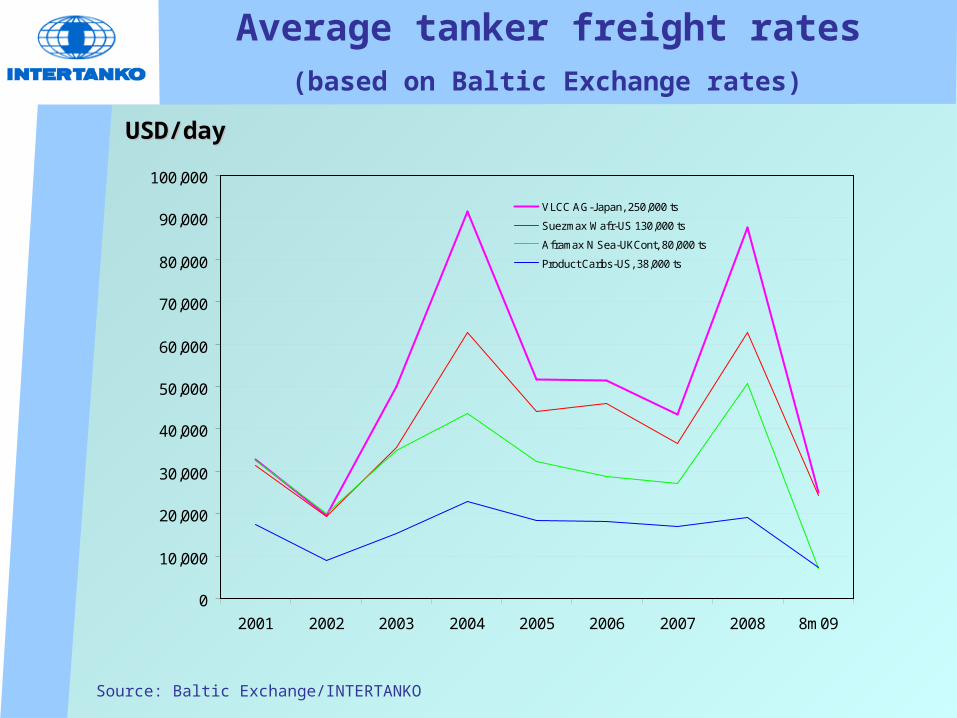

Source: Baltic Exchange/INTERTANKO

USD/dayUSD/day

Average tanker freight rates (based on Baltic Exchange rates)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2001 2002 2003 2004 2005 2006 2007 2008 8m09

VLCC AG-Japan, 250,000 ts

Suezmax Wafr-US 130,000 ts

Aframax N Sea-UKCont, 80,000 ts

Product Caribs-US, 38,000 ts

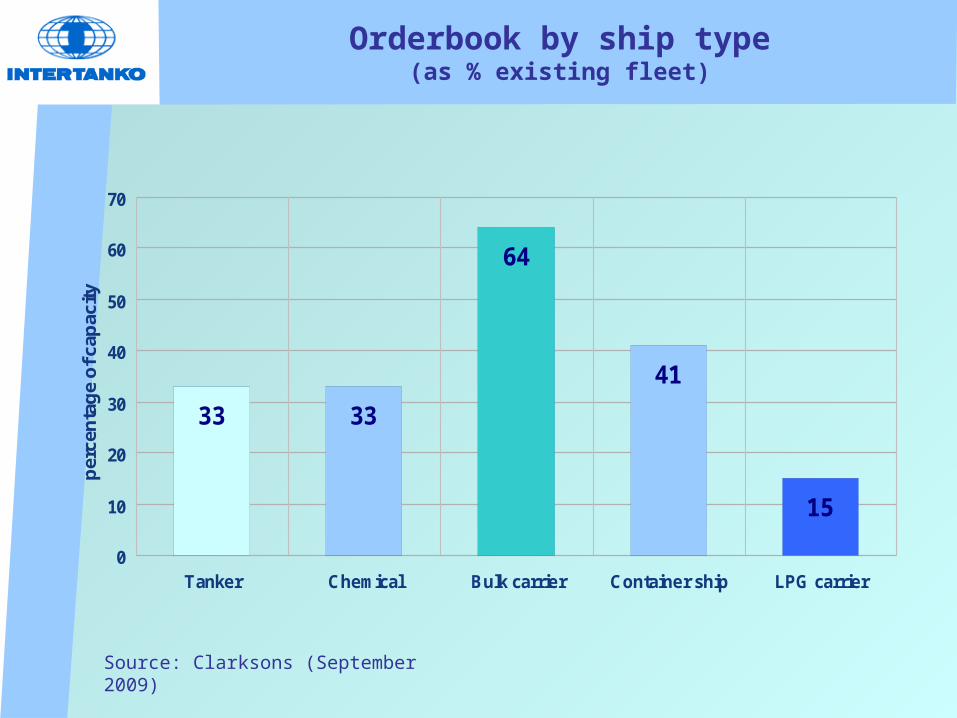

Orderbook by ship type(as % existing fleet)

Source: Clarksons (September 2009)

33

64

41

15

33

0

10

20

30

40

50

60

70

Tanker Chemical Bulk carrier Container ship LPG carrier

perc

enta

ge o

f cap

acity

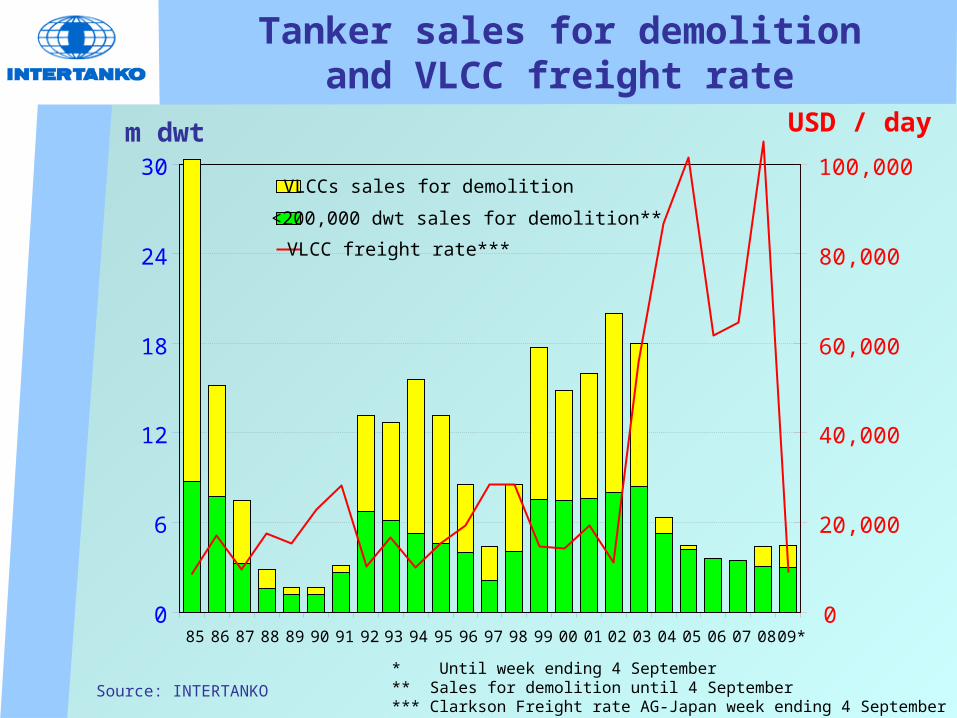

Tanker sales for demolitionand VLCC freight rate

Source: INTERTANKO

m dwt USD / day

* Until week ending 4 September** Sales for demolition until 4 September*** Clarkson Freight rate AG-Japan week ending 4 September

0

6

12

18

24

30

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09*0

20,000

40,000

60,000

80,000

100,000VLCCs sales for demolition

<200,000 dwt sales for demolition**

VLCC freight rate***

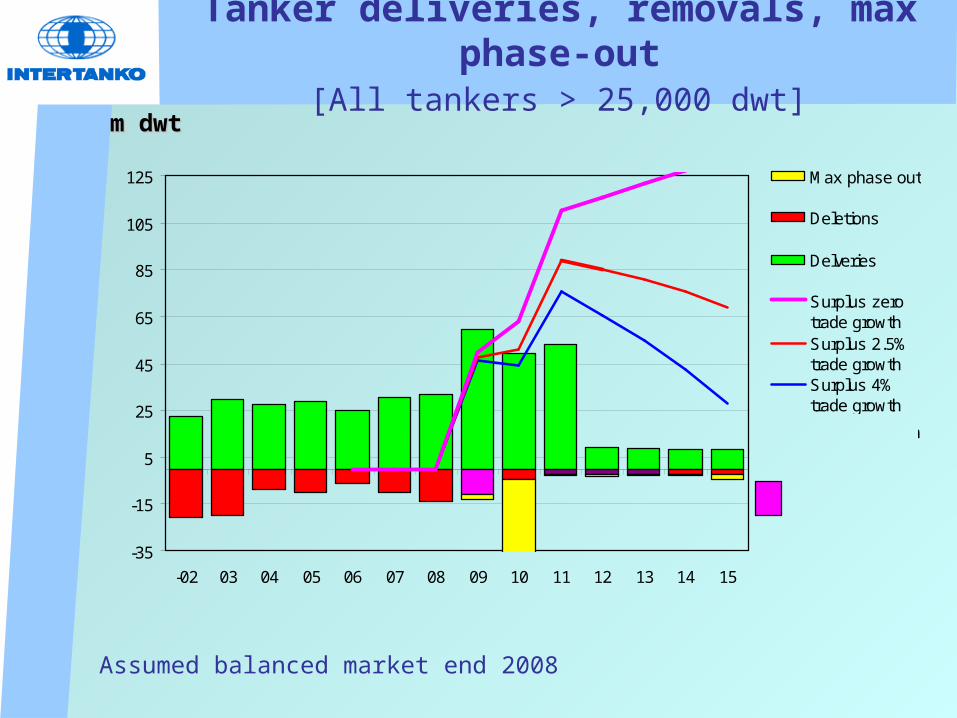

Tanker deliveries, removals, max phase-out [All tankers > 25,000 dwt]

m dwtm dwt

Assumed balanced market end 2008

-35

-15

5

25

45

65

85

105

125

-02 03 04 05 06 07 08 09 10 11 12 13 14 15

Max phase out

Deletions

Delveries

Surplus zerotrade growthSurplus 2.5%trade growthSurplus 4%trade growth

year

Removals in addition to phase out (conversions)

Minus 2% growth in 2009 and the above scenarios later

Lower Freight Rates & Fleet surpluses in ALL sectors – not just tankers

Implications ?

• Challenge to maintain quality and standards

• Challenge to meet the issues of the day

• and government interventions ?

Panel Discussion to follow on:- Financial Crisis, its prospect- Role and Responsibilities of Regulators, Class,

Shipbuilders, Repairers to Promote Maritime Safety and Quality Shipbuilding

Thank you 감사합니다For more information, please visit:

www.intertanko.com www.maritimefoundation.com

www.poseidonchallenge.comwww.shippingfacts.com