Embed Size (px)

Citation preview

Slide 1

Hodson Bay Hotel, Athlone, County Westmeath, Ireland

Tuesday & Wednesday, September 4th & 5th 2012

Peter Goth M.A., Ph.D, [email protected]

Credit Union Managers Credit Union Managers Conference Conference

“Time of Great Change…… Challenges and Opportunities”

The Commission’s ReportThe Commission’s Report1. Engaging With Credit Unions

‘Each credit union will have the opportunity to engage

with the ReBo. For the most part, this engagement will

involve a preliminary discussion on restructuring

options open to the credit union, based on available

information provided by the Central Bank.’

Slide 2

The Commission’s ReportThe Commission’s Report

2. Making it Happen

The ReBo’s roll will be to:

•Consider the information provided to it by the Central Bank with

a view to planning for and encouraging restructuring where it

considers that to be both necessary and appropriate. (Perhaps some

variant of DEA for credit unions)

•Engage with credit unions on the ground with a view to

formulating restructuring proposals for submission to the Central

Bank for funding approval.

Slide 3

The Commission’s ReportThe Commission’s Report

2. Making it HappenThe ReBo’s roll will be to (Cont.):

•Provide technical support and expertise for restructuring

proposals; project management the restructuring process;

and provide post-restructuring support.

•Provide the primary interface with the Central Bank on

restructuring proposals.

Slide 4

The Commission’s ReportThe Commission’s Report

Who takes the initiative within the movement….?

What is the plan?

How do you proceed?

Slide 5

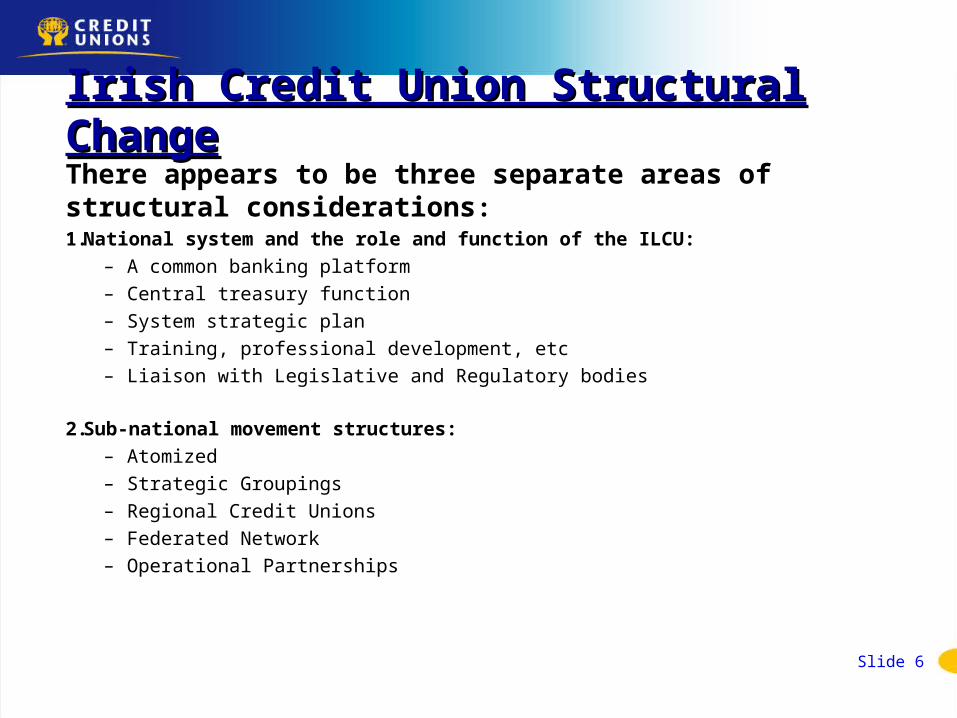

Irish Credit Union Structural Irish Credit Union Structural ChangeChangeThere appears to be three separate areas of structural considerations:1.National system and the role and function of the ILCU:

– A common banking platform– Central treasury function– System strategic plan – Training, professional development, etc– Liaison with Legislative and Regulatory bodies

2.Sub-national movement structures:– Atomized– Strategic Groupings– Regional Credit Unions– Federated Network– Operational Partnerships

Slide 6

Irish Credit Union Structural Irish Credit Union Structural ChangeChangeThere appears to be three separate areas od structural considerations (cont.):

3.Individual units:– Merge with another credit union– Form a federated network with other credit unions– Transfer of engagement to another credit union– Form informal or formal partnership for certain

operations, products and services, delivery of services, etc

– Go it alone

Slide 7

Mergers, Transfers of Mergers, Transfers of Engagements, Federated Engagements, Federated

Networks and Partnerships Networks and Partnerships • Mergers Combination of two credit unions into one, with the ‘acquirer’

assuming the assets and liabilities of the ‘target’ credit union…. Possibly into a new entity with a new name.

• Transfers of engagementAbsorption of one credit union into another…. ‘Any registered society may

by special resolution transfer its engagements to any other registered society which may undertake to fulfil those engagements; and if that resolution approves the transfer of the whole or any part of the society’s property to that other society, the whole or, as the case may be, that part of the society’s property shall vest in that other society without any conveyance or assignment.’

The decision to merge or to undertake a transfer of engagement needs to support the long term strategy and

growth objectives of the credit unions involved.

Slide 8

Mergers, Transfers of Engagements, Mergers, Transfers of Engagements, Federated Networks and Partnerships Federated Networks and Partnerships • Potential Opportunities for Partnerships (informal or

formal):

(CUSO is specifically a US phenomena and are defined by legislation and regulation … they are corporate entities separate from the participating credit unions.)– Clerical (back office)– professional and management services (purchasing, personnel,

marketing, etc)– financial counselling services,– electronic transaction service (banking platforms),– fixed asset services,– insurance brokerage or agency, – loan support services, – record retention,– security and disaster recovery services,– payroll processes, – call centre,– etc

Slide 9

Slide 10

Mergers, Transfers of Engagements, Mergers, Transfers of Engagements, Federated Networks and Federated Networks and

PartnershipsPartnerships

Year # of CUs Assets Average Asset

Members

Average Membersh

ip

2005 568 $86,060 $151 5,360,457

9,437

2006 549 $92,176 $168 5,382,049

9,803

2007 536 $97,661 $182 5,720,304

10,672

2008 513 $105,227 $205 5,719,362

11,149

2009 480 $111,809 $233 5,339,293

11,123

2010** 450*** $121,575 $270 5,292,697

11,762 Slide 11

Desjardins Credit Unions Desjardins Credit Unions 2005 – 2010 (CDN$ millions)

- A Federated Network of Credit Unions -

**Desjardins Corporate Group December 31st 2010 Assets $175 billion

*** March 31st 2012 # of CPs 379

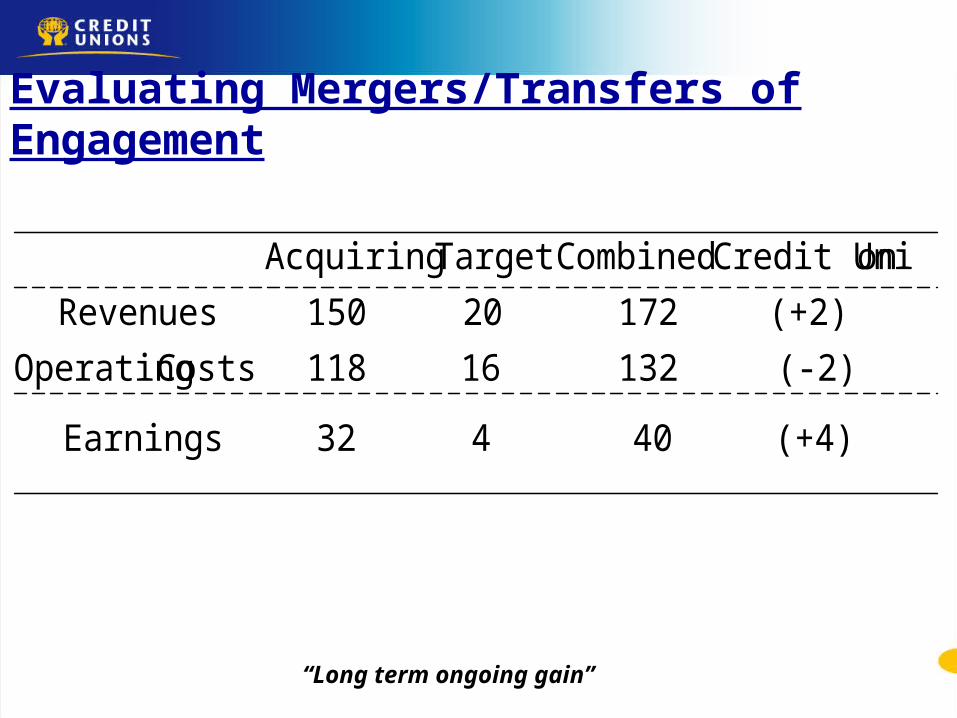

Evaluating Mergers/Transfers of Evaluating Mergers/Transfers of EngagementEngagement

• Questions:– Is there an overall economic and/or non-economic

gain to the Merger/Transfer of Engagement?– Do the terms of the merger make the resultant

credit union and its member/owners better off?

PV(B)+PV(A)>PV(AB)

Both financial and/or non-financial present-value (PV)

Long-term potential rather than immediate

Evaluating Mergers/Transfers of Engagement

(+4) 40 432Earnings

(-2) 13216118Costs Operating

(+2) 17220150Revenues

onCredit Uni CombinedTargetAcquiring

“Long term ongoing gain”

Four Reasons to Merge or Accept Four Reasons to Merge or Accept Transfer of Engagement Transfer of Engagement

1. Increase Member Value

a. Not necessarily only increased economic value (private sector) …. Economic and non-economic value

b. Offer members a larger product suite, better rates, more branches, greater online capacity, etc

c. Economies of scale… the opportunity to spread fixed costs across a larger volume of output, thus increasing residual income. (seldom in evidence.. “personnel costs”)

“As a small standalone credit union, I simply could not provide such a breadth of services to my members.”

Slide 14

Four Reasons to Merge or Accept Four Reasons to Merge or Accept Transfer of EngagementTransfer of Engagement

2. Growth….. Long term.

a. Long term potential growth rather than simple instant increase in assets and members ***.

b. Growth potential presented by the smaller credit union’s underpenetrated field of membership and/or poor-management

*** “We did not merge with ABC credit union for its assets… the headaches associated with all the ‘people’ issues and the IT conversion simply wouldn’t have been worth it”.

Slide 15

Four Reasons to Merge or Accept Four Reasons to Merge or Accept Transfer of EngagementTransfer of Engagement

3. Diversificationa. The credit union with an industrial bond (Select

Employee Group) is dependent upon the financial health of the corporate sponsor and if events detrimentally impact the sponsor then credit union performance will suffer.

b. Geographic diversification … a merger with a credit union in another geographic area can reduce exposure to any single area.

Slide 16

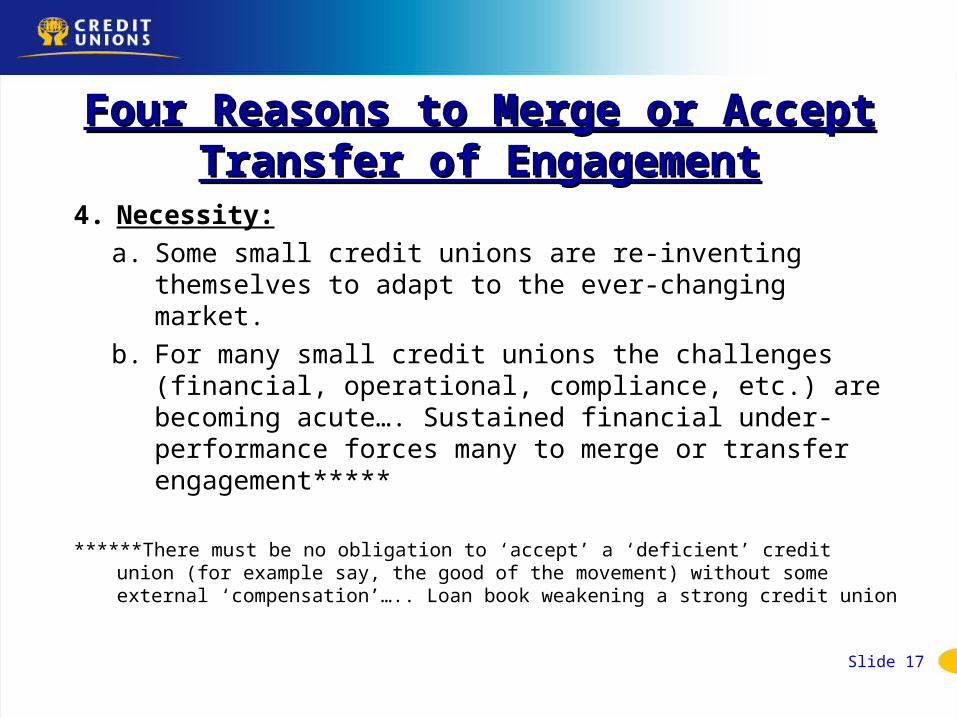

Four Reasons to Merge or Accept Four Reasons to Merge or Accept Transfer of EngagementTransfer of Engagement

4. Necessity:a. Some small credit unions are re-inventing

themselves to adapt to the ever-changing market.b. For many small credit unions the challenges

(financial, operational, compliance, etc.) are becoming acute…. Sustained financial under-performance forces many to merge or transfer engagement*****

******There must be no obligation to ‘accept’ a ‘deficient’ credit union (for example say, the good of the movement) without some external ‘compensation’….. Loan book weakening a strong credit union

Slide 17

Analysis of Potential MergersAnalysis of Potential Mergers1. Market Considerations

a. Market area - How well do the demographic and geographic characteristics of the target credit union’s market complement the acquirer’s market?

b. Branches and facilities – Are the target credit union’s branches in high-visibility, high-traffic corridors?

c. Business Strategies and operations – What services, delivery channels and branch hours does the target credit union off members and how is it performing?

d. Marketing - How extensive are the target credit union’s marketing efforts, and what marketing channels does it employ?

Slide 18

Analysis of Potential MergersAnalysis of Potential Mergers

2. Financial considerations - A thorough financial analysis is critical.a. Fixed assets – Evaluate the target CU’s fixed

assets, remaining depreciable life, existing leases and other contractual obligations, ongoing relevance and potential for liquidation. Compare the market values to book values.

b. Earnings assets – the loan book quality (Hidden Delinquency and potential risk)

c. Income statement efficiencies – Revenues and expenses – potential improvements for productivity and efficiency gains.

Slide 19

Analysis of Potential MergersAnalysis of Potential Mergers3. Other considerationsa. Cultural and political aspects - are often at the heart

of the most difficult merger discussions. Key issues for the target credit union include:

• Board representation in new organization• Management roles in the new organization• Accommodation of staff

b. Governance – How will the target credit union board and committee structure be incorporated into that of the continuing credit union

Slide 20

Analysis of Potential MergersAnalysis of Potential Mergers

3. Other considerations (cont.)c. Management – Does the target credit union have key

management that would benefit the continuing credit union?

d. Staff – a. Rehiringb. Cultural adjustmentsc. Redundanciesd. Pensions

Some very tough decisions

Slide 21