Embed Size (px)

Citation preview

Slave to Your Employer or to Your Financier?

Wage Structures When Employees Have Entrepreneurship Options

Veikko Thiele∗ and Mihkel Tombak†

June 20, 2010

Abstract

We examine a principal-agent model where the outside option for the risk-averse employee is to be-

come a capital-constrained entrepreneur. As the entrepreneurial enterprise is a spin out, we assume

that the outcomes of entrepreneurship are (imperfectly) related to the possible payoffs under employ-

ment. We show that firms exploit inefficiencies associated with entrepreneurship, such as a higher

cost of capital or lack of complementary assets, by offering lower wages. If starting new ventures is

highly lucrative, employment provides lower expected income levels for employees as compared to

entrepreneurship but, at the same time, imposes less risk on these employees. Finally, we show that

more risk averse employees would favor equity over debt to finance a potential venture, which in turn

allows firms to offer lower wages in equilibrium. In this way, when accounting for entrepreneurial

outside options, the risk aversion of employees can be beneficial for firms.

Keywords: Entrepreneurship, employment contracts, wages, spin outs, intrapreneurship, incentives,

moral hazard.

JEL classification: D86, J31, L26, M13.

∗Queen’s University, Queen’s School of Business, Goodes Hall, 143 Union Street, Kingston, Ontario, Canada K7L 3N6,e-mail: [email protected].†University of Toronto, e-mail: [email protected]

1 Introduction

By June 2008 as a severe recession hit the U.S., the number of private-sector wage employments went

down to 99% of its December 2007 level, while the number of self-employed increased to 102% (Shane,

2009a). Throughout 2009, both those numbers have declined in part because raising the required capital

to finance new businesses has become dramatically more difficult (Shane, 2009b). These facts illus-

trate two phenomena we explore in this paper. First, an alternative to private-sector wage employment

is entrepreneurship (and vice versa). Indeed, Franco and Filson (2005) find that startup firms are of-

ten “spin-outs” of larger corporations, suggesting that entrepreneurial activities resemble those within

firms.3 Second, pursuing entrepreneurship opportunities is often challenging as founding a new venture

requires capital, which is rarely possessed by the founders themselves. Many studies have empirically

demonstrated that financial constraints are indeed of great concern for entrepreneurs and small firms.4

As potential entrepreneurs are typically wealth-constrained, they rely on external sources to finance their

endeavors.5 While empirical contributions abound in the area of entrepreneurship, little is known about

how entrepreneurial opportunities for employees affect their wage schemes within firms. This paper

therefore examines how the value of entrepreneurial outside options for employees – which clearly de-

pends on the characteristics of the capital market – determines wage structures within firms.

To shed more light on the optimal design of employment contracts, we embed entrepreneurial outside

options into a classic principal-agent (PA) formulation. The employer designs a compensation contract

subject to the individual rationality (IR) constraint and the incentive (IC) constrained of the agent. As is

typical in such models, we assume that employers are risk-neutral, while agents are strictly risk-averse.

We know from the traditional PA literature that the optimal employment contract will then exhibit a trade-

off between incentive provision (making the agent’s compensation contingent on observable outcome)

and insurance for the agent as an optimal risk-sharing mechanism.3For example, Steve Jobs left Atari and Steve Wozniak left Hewlett-Packard to establish Apple Computer in 1977. Or

consider the case of Jorma Nieminen who left Nokia in 1988 to establish a new firm, Benefon, which also produces mobilephones. In 1997, Benefon generated a profit of US$3.9 million from revenues of US$55.4 million.

4See, e.g., Bitler, Moskowitz, and Vissing-Jorgensen (2005), Evans and Jovanovic (1989), Evans and Leighton (1989),Holtz-Eakin, Joulfaian, and Rosen (1994a, 1994b), as well as Blanchflower and Oswald (1998).

5In contrast, financial constraints for pursuing business opportunities are less prevalent for large corporations. For instance,Kaplan and Zingales (1997) found that financial constraints caused only 14.7% of the large corporations in their sample torestrict investments in promising projects.

1

The key departure of our framework from the classical PA model is that the agent’s outside option

is no longer considered to be an exogenous and constant feature. Instead, it is related to the payoffs

that the agent would obtain as a self-employed and capital-constrained entrepreneur. In order to focus

exclusively on the issue of employment versus entrepreneurship, we assume that the available production

technology is invariant to the organizational mode of the firm where it is utilized. However, the specific

investment problems differ across various organizational forms in that – consistent with the empirical

evidence presented by Kaplan and Zingales (1998) – the entrepreneur is capital constrained, while the

firm is not. Thus, the entrepreneur relies on an outside financier in order to fully exploit his business

idea. We consider two alternative sources for the entrepreneur to raise the required capital to start his

venture: equity and debt.

One of the key insights from our analysis is that the presence of more lucrative entrepreneurial op-

portunities forces firms to transfer more surplus to employees by offering higher equilibrium wages.

On the other hand, market imperfections, such as a higher cost of capital for entrepreneurs, make self-

employment less attractive, which in turn allows firms to retain employees despite offering lower wages

in equilibrium. We further show that not only total wage levels, but also the specific wage structures

within firms are closely tied to the prospects of entrepreneurship. If self-employment is anticipated to

be highly lucrative, firms can attract and retain employees by offering them incentive contracts, which

involve less uncertainty than the potential income levels under entrepreneurship.6 In this sense, em-

ployment provides insurance to risk-averse employees who – as self-employed entrepreneurs – would

otherwise be fully exposed to the risk associated with running their own businesses. Finally, in contrast

to many other studies, we find that risk-aversion or limited liability on the side of employees can actu-

ally benefit firms under certain conditions as this weakens employees’ entrepreneurial outside options,

allowing firms to ensure their participation even while offering lower wages.

One key property of our framework is that agents are wealth-constrained, and are thus reliant on

external capital when pursuing their entrepreneurship options. Market characteristics (such as the cost of

capital faced by entrepreneurs) then determine the attractiveness of self-employment and, hence, equilib-

rium wages within firms. Hubbard (1998) surveys a wide spectrum of empirical studies indicating that6Taylor (1996) provides empirical support for this implication. Using the British Household Panel Study data for 1991, he

found that the lack of job security is a deterrent to self-employment. That entrepreneurs face a greater degree of risk is indicatedby their survival rates compared to the probability of a wage earner becoming unemployed in any particular year.

2

financial constraints indeed play an important role in determining the cost of capital for firms. Specifi-

cally, imperfections of financial markets lead to higher costs of raising capital from sources outside the

corporation. Using Thai data, Paulson, Townsend, and Karaivanov (2006) provide empirical evidence

that the predominant reason for the existence of credit market imperfections is moral hazard rather than

the limited wealth of entrepreneurs. Such market imperfections can dramatically hamper entrepreneurial

activities, thereby making dependent employment relatively more attractive. Indeed, several surveys

indicate that – besides the riskiness of self-employment – raising the required capital was one of the

greatest concerns of potential and actual entrepreneurs when making their decisions about whether to

become self-employed (see e.g., Taylor (1996), and Blanchflower and Oswald (1998)).

Theoretical investigations of the optimal choice of agents between employment and entrepreneur-

ship include Kihlstrom and Laffont (1979), Kanbur (1979, 1982), Bannerjee and Newman (1993), and

Ghatak, Morelli, and Sjöström (2001). These models examine various aspects of entrepreneurship in a

general equilibrium framework, primarily focusing on risk aversion (with the exception of Ghatak, et.al.

(2001) who examine the financial constraint problem in a framework with overlapping generations).

Risk-aversion is also a feature of our framework, but one key aspect of our consideration is distinct from

that of the above studies. The main objective of these studies is to examine the distribution of risk-

aversion and its impact on the formation of new firms for a given wage structure. In contrast, our model

focuses on endogenous wage structures that arise in equilibrium, while retaining the feature of the above

models that integrates the labor market for entrepreneurs and for wage earners. We do this by modifying

the “often-overlooked participation constraint” in principal-agent relationships (Oyer, 2004). Specifi-

cally, we endogenize the outside option for employees by allowing them to become capital-constrained

entrepreneurs.

Our study proceeds as follows: We describe our modified principal-agent model in the next section.

We then derive in Section 3 the optimal employment contract for a given outside option. In Section 4, we

examine the entrepreneurial outside option under two scenarios: (i) when the entrepreneur finances his

venture through equity; and (ii), when he uses debt. In Section 5, we discuss some of the implications

that can be derived from our analysis. Section 6 summarizes our main results and provides conclusions.

All proofs for our Lemmas and Propositions can be found in the Appendix.

3

2 The Model

Consider a risk-averse agent facing two occupational choices: (i) working for a risk-neutral firm (hence-

forth referred to as employment); and (ii), starting his own venture (henceforth refereed to as en-

trepreneurship). In order to focus on the issue of employment versus entrepreneurship, we assume

that the agent’s skills and expertise are invariant to the organizational mode of the firm where they are

utilized. Moreover, the agent would pursue the same business idea when becoming an entrepreneur as

he would as an employee. The agent, however, has limited wealth, which implies that he is reliant on

external financing when pursuing his own business opportunity.

To ease the differentiation between both potential occupations, we call the agent employee when

explicitly referring to the employment relationship and entrepreneur whenever he starts his own business.

In both cases, the agent (i.e., the employee as well as the entrepreneur) can either apply high effort e > 0,

or shirk, in which case his effort is zero. His specific effort choice is the agent’s private information, thus

leading to a typical moral hazard problem as in the classic principal-agent framework under employment.

While shirking does not impose any disutility of effort on the agent, implementing the high effort level e

leads to effort cost ψ > 0.

Let us first elaborate on a potential employment relationship between the firm and the agent (em-

ployment). The agent is employed to implement a project, which requires the firm to make an initial

investment X > 0. The firm’s opportunity cost of capital is denoted by r0 > 0, which reflects both

the characteristics of the capital market and also the firm’s degree of diversification. We will henceforth

refer to r0 as the firm’s risk-adjusted interest rate. Once initiated, the project generates a return π for the

firm. We assume that the return can be either high (π = πH ) or low (π = πL ≥ 0), with πH > πL. The

probability of the project generating a high return πH is conditional on the employee’s effort choice. For

parsimony, we define

Prob[π = πH |e] = ρe

Prob[π = πH |0] = ρ0,

4

where 1 > ρe > ρ0 > 0. The employee’s effort will generate the high payoff πH with probability ρe,

while his shirking results in the lower probability ρ0 for πH being realized.

As a result of the employee’s binary contribution to firm value π ∈ {πH , πL}, the firm can offer him

a wagewH paid whenever the outcome is good (i.e., π = πH ) andwL otherwise. The employee’s limited

wealth, however, requires that wH , wL ≥ 0. The wage wL can be interpreted as the base wage for the

employee and the wage differential, ∆w ≡ wH −wL, as his performance bonus. Letting u(·) denote the

agent’s concave utility function with u(0) = 0, it follows that the wage payment wi, i = L,H , provides

him with the utility level u(wi−ψ) when he implements a high effort level e, and u(wi) when he shirks.7

As an alternative to accepting an employment contract from the firm, the agent could start his own

venture (entrepreneurship). In this case, because of his limited wealth, the required investmentX > 0 for

pursing his business opportunity cannot originate from the entrepreneur’s own funds. He is thus reliant

on financiers who will provide him with the required capital. Due to their relevance for facilitating

entrepreneurial activities, we consider the following two alternatives: (i) equity-financed ventures (e.g.,

through venture capital); and (ii) debt-financed ventures. For both alternatives, we assume a perfectly

competitive capital market so that economic rents of financiers are competed down to zero. The modes

of financing differ, however, in that debt implies limited liability.

While the agent’s attributes – his skills and expertise – are invariant to the considered organizational

forms, firm-specific characteristics could nonetheless lead to a disparity between the productiveness of

employees and entrepreneurs. To account for this possibility, we assume that the (gross) profit of the

venture takes the from πE ∈ {ηπL, ηπH}, where the parameter η > 0 captures the relative productivity

of an entrepreneur compared to an employee. Clearly, employees in large firms can benefit from access

to various complementary assets (such as access to marketing networks and production expertise), which

in turn augments an agent’s productivity in these firms. On the other hand, large organizations can also

be adversely affected by diseconomies of scale (such as bureaucratic policies), which could impair the

performance of employees. In our framework η < 1 reflects a situation where complementarity effects

within the firm clearly dominate potential diseconomies of scale. This formulation will allow us to

capture productivity differences between employees and entrepreneurs with our model and to investigate7The disutility associated with effort provision ψ is measured in monetary terms, and the monetary unit is normalized so

that it enters the utility function of the risk-averse agent.

5

their effects on the efficient employment incentives as well as financing contracts. Finally, the conditional

probabilities for a high profit under employment also apply to entrepreneurship (with the adjusted payoffs

ηπH and ηπL).

3 Employment and the Optimal Incentive Contract

In this section we begin by briefly defining the optimal contract under employment. As is well known

from the PA literature, the optimal employment contract needs to satisfy two requirements: (i) ensuring

the agent’s participation in the employment relationship; and (ii) providing the employee with sufficient

incentive to provide effort. As stated in the Introduction, endogenizing the agent’s outside option is a key

element of our model. Before explicitly taking the agent’s entrepreneurial outside option into account,

however, we first treat his valuation of being a self-employed entrepreneur, denoted Γ, as exogenous.

Moreover, we adopt the following tie-breaking rule: Whenever the agent is indifferent between accept-

ing the employment contract offered by the firm and starting his own business, he decides in favor of

employment.8

We can now turn to the firm’s maximization problem. For the purposes of parsimony, suppose that

the spread πH − πL of the employee’s potential contribution is sufficiently large so that it is optimal for

the firm to induce a high effort level e and, at the same time, to make the investment X . The firm’s

objective is to find a compensation scheme {wL, wH} which maximizes the expected difference between

the employee’s contribution to firm value and his expected compensation, while ensuring the employee’s

participation in this employment relationship. The optimal wage scheme {wL, wH} thus solves

maxwH ,wL

Π = ρe (πH − wH) + (1− ρe) (πL − wL)− (1 + r0)X (1)

s.t.ρeu(wH − ψ) + (1− ρe)u(wL − ψ) ≥ Γ (2)

ρeu(wH − ψ) + (1− ρe)u(wL − ψ) ≥ ρ0u(wH) + (1− ρ0)u(wL) (3)

wL, wH ≥ 0. (4)8Alternatively, one could assume that the agent opts for entrepreneurship whenever he is indifferent between both occupa-

tional choices. In such a situation, the firm must offer the agent an additional (infinitesimally small) amount ε > 0 in order toensure his participation in the employment relationship.

6

Condition (2) is the employee’s participation and (3) his incentive constraint. Furthermore, (4) is a

liability limit constraint guaranteeing that payments to the employee are non-negative (wL, wH ≥ 0).

Cost minimization requires the firm to set the base wage wL and the performance bonus ∆w so that

the employee’s participation constraint (2) as well as his incentive constraint (3) are binding.9 Other-

wise, if either the participation constraint (2) or the incentive constraint (3) is not binding, the firm could

reduce the employee’s compensation without jeopardizing his participation and effort incentives, respec-

tively. Moreover, upon closer inspection of the firm’s maximization problem it becomes clear that the

performance bonus ∆w required to induce high effort e is solely defined by the employee’s incentive

constraint (3). Given the required bonus ∆w, the base wage wL is then set to just satisfy the employee’s

participation constraint (2). As a logical consequence, the optimal base wage w∗L also reflects the agent’s

valuation of starting his own venture as captured by Γ.

Before we turn to the agent’s choices as a self-employed entrepreneur, it is helpful to briefly analyze

his effort incentives ∆w when employed by the firm. In particular, we are interested in how the optimal

performance bonus responds to the sensitivity of the agent’s potential contribution to firm value (π) with

respect to his individual effort choice, as captured by the probabilities ρe and ρ0. Standard PA theory

implies that the optimal performance bonus ∆w used to induce high effort decreases in the probability

ρe and increases in the probability ρ0. Moreover, ∆w decreases in the probability difference ρe − ρ0.

That is, if a hard-working employee (with effort e) becomes more likely to make a high contribution

πH (i.e., ρe increases), the firm can reduce his performance bonus ∆w without compromising his effort

incentives. If, on the other hand, a shirking employee becomes more likely to produce πH (i.e., ρ0

increases), then motivating high effort necessitates a higher performance bonus ∆w in order to raise the

employee’s expected reward for effort. Also, this result shows that the optimal performance bonus ∆w

decreases in the probability difference ρe − ρ0. The difference ρe − ρ0 captures the sensitivity of the

employee’s effort on the expected firm value. To briefly elaborate on its economic interpretation, suppose

for a moment that the probability difference ρe− ρ0 is relatively large so that the employee’s effort leads

to a substantially higher expected firm value compared to his shirking. This could be rooted in synergies

between the firm’s capital provision X and the employee’s effort e. In other words, the presence of9As we will demonstrate in Sections 4.1 and 4.2, the optimal wage scheme {w∗L, w∗H} – which takes the agent’s en-

trepreneurial options into account – is such that the limited liability constraint (wL, wH ≥ 0) is not binding.

7

more such synergies within the firm augments – for a given capital provision – the productivity of the

employee and, hence, his expected contribution to firm value. This in turn implies that the employee is

more likely to succeed and, as a result, obtain his performance bonus ∆w. The firm can then scale back

the incentive bonus ∆w for the employee without compromising his incentives to implement high effort

e.

Now that we have derived the agent’s optimal incentive contract under employment for a given value

of his outside option Γ, we can focus on his alternative to being employed by the firm: pursuing the

business idea as a self-employed entrepreneur. This in turn allows us to investigate how entrepreneurial

opportunities of employees in firms influence their incentive contracts. To do so, we proceed in two

steps: First, we consider the case of an equity-financed entrepreneur in the next section. Subsequently,

we turn to the case where the entrepreneur is financed through debt.

4 Entrepreneurial Outside Options

4.1 Equity-Financed Entrepreneurs

In this section, we consider the agent’s alternative of starting his own venture using equity provided by

a financier. We are interested in how the characteristics of the equity contracts affect incentive contracts

under employment. We start by deriving the optimal financing contract offered to an equity-financed en-

trepreneur. Specifically, the financier provides the entrepreneur with the required capital X in exchange

for the share 1 − θ on the venture’s gross profit ηπ. The remaining share θ accrues to the entrepreneur.

The financier’s opportunity cost of providing the entrepreneur with capital X is denoted rE , where the

subscript E indicates equity financing. The financier, however, does not necessarily face the same cost

of capital as the firm. More specifically, the financier’s cost of capital might, in fact, exceed that of the

firm, potentially because of the venture capitalist’s limited ability to monitor the investment or the cor-

poration’s ability to capture synergies across investments in other divisions. Technically, we then have

rE > r0.10

10This assumption is based on empirical evidence that venture capital firms as suppliers of equity tend to take more risk thantraditional firms. While this assumption is not crucial for our subsequent analysis, it provides some interesting insights withrespect to the optimal design of employment contracts.

8

We assumed in Section 3, for the purposes of benchmarking, that inducing high effort e is optimal for

the firm under employment. Exerting high effort, however, is not necessarily optimal for the entrepreneur.

As discussed in Section 2, the agent can exploit potential complementarity effects under employment,

which might not be present in his own venture (i.e., η < 1). Depending on his individual disutility ψ of

implementing high effort e, the agent might be better off shirking as an equity-financed entrepreneur. To

account for these possibilities, we let θi denote the entrepreneur’s share on the venture’s gross profit ηπ

in case the financier anticipates that the entrepreneur will implement effort i = 0, e.11

Anticipating the effort level i ∈ {0, e}, and the corresponding probability of success ρi, the optimal

equity share θi satisfies the zero-profit condition for the financier:12

ρi(1− θi)ηπH + (1− ρi)(1− θi)ηπL − (1 + rE)X = 0. (5)

Solving (5) for the entrepreneur’s equity share θi yields

θi(η) =ρiπH + (1− ρi)πL − η−1(1 + rE)X

ρiπH + (1− ρi)πL(6)

The remaining equity share (1 − θi(η)) accrues to the financier and it balances the financier’s cost of

providing the entrepreneur with capital X with his expected return on investment. Observe from (6)

that the entrepreneur’s equity share θi(η) is increasing in the parameter η, which captures the relative

productivity of an entrepreneur compared to an employee. A higher relative productivity η augments the

expected profit of the new venture, which in turn allows the financier to cover his cost of investment,

rEX , with a lower equity share θi(η). The opposite applies for a lower relative productivity η. Finally,

whenever the entrepreneur is expected to exert high effort instead of shirking, he receives a higher equity

share (i.e., θe(η) > θ0(η)).13 This can be observed because a high effort level augments the expected

11After deriving the optimal equity share θi for a given effort level, we will characterize the incentive constraint for theequity-financed entrepreneur which specifies his optimal effort choice. This in turn allows us to identify the equity share andeffort levels that prevail in equilibrium.

12One could also assume a strictly positive premium for the financier due to his specific expertise (economic rent). However,as will become clear from our subsequent analysis, this would not affect the qualitative explanatory power of our results.

13To see this, we can rewrite (6) as

θi(η) = 1− η−1(1 + rE)X

ρiπH + (1− ρi)πL, (7)

which is clearly increasing in ρi as πH > πL.

9

profitability of the new venture, which in turn allows the financier to recover the investment X with a

smaller share on the venture’s profit.

We now turn to the effort choice of the equity-financed entrepreneur. Suppose for a moment that

the financier offers the equity share θe(η) in anticipation of high effort e. Then, the entrepreneur will

choose to exert high effort e if this provides him with a higher expected utility than shirking. Formally,

he implements the high effort level e if

ρeu(θe(η)ηπH − ψ) + (1− ρe)u(θe(η)ηπL − ψ) ≥ ρ0u(θe(η)ηπH) + (1− ρe)u(θe(η)ηπL), (8)

which constitutes the entrepreneur’s incentive constraint under equity financing. The financier anticipates

the entrepreneur’s specific effort choice and adjusts the equity share θi(η) accordingly. The following

lemma emphasizes a condition which ensures that exerting the high effort level e is optimal for the

entrepreneur.

Lemma 1 There exists a threshold complementarity parameter η̂E such that the equity-financed en-

trepreneur implements high effort e if η ≥ η̂E and shirks otherwise.

The condition in Lemma 1 has the following intuition: Only if the expected payoff of the venture is

sufficiently sensitive to the entrepreneur’s effort choice, is he willing to incur the disutility ψ of exerting

high effort e. This can be observed because the incremental gross profit of the venture, η(πH − πL)

increases in the complementarity parameter ψ. Moreover, implementing the high effort level emakes the

realization of η(πH − πL) more likely. Thus, choosing the high effort level e can only be worthwhile for

the entrepreneur if η is sufficiently high (i.e., η ≥ η̂E).

As pointed out in Section 2, equity-financed entrepreneurship constitutes one of two potential alter-

natives for the agent when accepting the employment contract {wL, wH} from the firm. Anticipating his

specific effort choice i, i ∈ {0, e}, the reservation utility of the employee, denoted ΓEi , is equal to the

entrepreneur’s expected utility:

ΓEi = ρiu(θi(η)ηπH − ci) + (1− ρi)u(θi(η)ηπL − ci), (9)

10

where the superscript ‘E’ indicates equity financing and ci ∈ {0, ψ} represents the agent’s disutility

of effort. One can infer from the firm’s maximization problem as stated in Section 3 that not only the

extent of ΓEi , but also its specific structure will eventually determine the optimal contract {wL, wH}

under employment. Moreover, one can expect that the entrepreneur’s individual effort choice will have a

substantial effect on the optimal design of employment contracts.

We are now equipped to characterize the optimal employment contract when becoming an equity-

financed entrepreneur is the employee’s best outside option. In particular, we are interested in the optimal

base wagewL and performance bonus ∆w under employment and how these payments differ to that of an

equity-financed entrepreneur. To ease the exposition, let πEH(η, i) ≡ θi(η)ηπH and πEL (η, i) ≡ θi(η)ηπL,

i = 0, e, denote the potential payoffs for the equity-financed entrepreneur, with ∆πE(η, i) ≡ πEH(η, i)−

πEL (η, i).

Proposition 1 Suppose the best outside option for the employee is to become an equity-financed en-

trepreneur. Then, the optimal base wage wEL (η) is characterized as follows:

πEL (η, 0) ≤ (≥)wEL (η) ≤ (≥)πEL (η̂E , e) if η ≤ (≥)η̂E ,

with strict equality holding when η = η̂E . Moreover, the optimal performance bonus is ∆wE(η̂E) =

∆πE(η̂E , e).

Proposition 1 shows that the optimal design of the employment contract hinges on the complemen-

tarity parameter η and, hence, on the specific profitability of equity-financed entrepreneurship. Consider

the case from Proposition 1 when η < η̂E . According to Lemma 1, the equity-financed entrepreneur

does not find it optimal to exert a high effort level. The complementarity parameter η is so low that

the entrepreneur’s incentive constraint (8) is violated. Motivating high effort e under employment there-

fore requires an incentive bonus ∆wE(η̂E), which exceeds the incremental payoff for the entrepreneur

∆πE(η, 0). This, however, imposes more uncertainty on the risk-averse employee, which in turn forces

the employer to offer a higher base wage wEL (η) (i.e., wEL (η) > πEL (η, 0)). The case in Proposi-

tion 1, where η > η̂E , has the opposite implication. The incremental payoff for the equity-financed

entrepreneur, ∆πE(η, e), is higher than necessary to motive effort e; see Lemma 1. The employer,

11

on the other hand, can therefore still induce the high effort level e by providing a lower incentive

bonus ∆wE(η̂E) (i.e., ∆wE(η̂E) < ∆πE(η, e)). Since this mitigates the uncertainty faced by the risk-

averse employee, his participation can still be ensured by offering him a lower base wage wEL (η) (i.e.,

wEL (η) > πEL (η, e)).

Next, consider the case in Proposition 1, where η = η̂E . Here, the optimal contracts under em-

ployment and equity-financed entrepreneurship are identical in equilibrium. Put differently, the firm

simply replicates the employee’s entrepreneurial outside option, thus making his wage equally uncertain.

In a broader sense, Proposition 1 shows that employees – facing the opportunities offered by a market

for equity – essentially become ‘intrapreneurs’, who are exposed to performance-related compensation

schemes which (imperfectly) replicate the conditions of this equity market.

To gain additional insight, we can derive the firm’s expected profit in case investment levels under

employment and equity-financed entrepreneurship are symmetric. To obtain a closed-form solution for

the firm’s expected profit, we henceforth focus on the case in Proposition 1, where η = η̂E . This in turn

facilities an illustrative discussion of how the characteristics of equity-financed entrepreneurship affect

the efficiency of employment contracts. However, our results are qualitatively the same for the other

cases in Proposition 1.

Substituting the optimal employment contract {wEL (η),∆wE(η̂E)} for η = η̂E , as derived in Propo-

sition 1, into the firm’s objective function (1) (see Section 3) yields

ΠE = (1− η̂E) [ρeπH + (1− ρe)πL] +X [rE − r0] . (10)

Observe that the firm’s expected profit ΠE consists of two components: First, a return stemming from

potential complementarity effects within the firm as reflected by the parameter η, which in this case takes

on the value η̂E .14 The second component is rooted in the firm’s lower cost of capital as compared to

that of the external financier (i.e., rE − r0). The firm’s expected profit ΠE , as defined by (10), however,

provides another interesting implication: Whenever the firm does not enjoy any complementarity effects

(i.e., η̂E = 1) and faces the same cost of capital as the external financier (i.e., r0 = rE), the entire14Note that η̂E ≤ 1. Suppose the employer finds it optimal to induce high effort e, then the incentive constraint (8) is

satisfied for η = 1 since the high payoffs under employment and entrepreneurship occur with the same probability ρe. This inturn implies that η̂E ≤ 1.

12

surplus from the employment relationship accrues to the employee. This is obtained because the firm’s

contract offer {wL, wH} must at least match the value of the agent’s entrepreneurship option; so any

potential benefits from an employment relationship must stem from associated efficiency gains. In an

extreme case, where the firm suffers from substantial diseconomies of scale (i.e., η is sufficiently high)

employing the agent can be detrimental for the firm. In such a situation, pursuing his entrepreneurship

opportunity constitutes the only option for the agent.

In essence, we find that wage structures under employment (imperfectly) mimic the payoffs of an

equity-financed entrepreneur. When there is some comparative advantage for the activities to be within

a corporation (either due to synergies which increase productivity or because of a lower cost of capital),

the firm can then extract some surplus by exploiting a less attractive outside option for the employees

through lower compensation.

4.2 Debt-Financed Entrepreneurs

As an alternative to utilizing equity to finance his start-up, the entrepreneur can choose to borrow the

required amount X at the interest rate rD, referred to as debt-financed entrepreneurship. Although

the investment X may be the same for both alternatives, they nonetheless differ in one important aspect:

Under equity-financed entrepreneurship, the financier’s return is directly linked to the venture’s particular

payoff π, with π ∈ {πL, πH}. Under debt financing, the entrepreneur will need to repay the entire loan

plus interest irrespective of the specific profitability of his venture. In same cases, however, the venture’s

payoff might not suffice to repay the entire debt; the entrepreneur’s limited liability then becomes a

binding constraint. As we will show in this section, limited wealth on the side of the entrepreneur has

important implications for the design and efficiency of firm-internal employment contracts.

To unravel how firm-internal employment contracts respond to the alternative of employees to start

their own debt-financed ventures, we first characterize and briefly discuss the optimal employment con-

tract {wL, wH} under the presumption that the agent, as entrepreneur, can always completely repay the

financier. Technically, we assume for a moment that πL > (1 + rD)X holds.

13

We first characterize the entrepreneur’s effort choice when his new venture is financed through debt.

For a given cost of capital rD, the entrepreneur will exert high effort e if this leads to a higher expected

utility than shirking. Thus, he is better off implementing the high effort level e if

ρeu(ηπH − (1 + rD)X − ψ) + (1− ρe)u(ηπL − (1 + rD)X − ψ)

≥ ρ0u(ηπH − (1 + rD)X) + (1− ρ0)u(ηπL − (1 + rD)X). (11)

We can infer from condition (11), which constitutes the entrepreneur’s incentive constraint under equity

financing, that his specific effort choice is determined by the presence of complementarities, as indicated

by η, and his disutility of effort ψ. Based on these two parameters, the next lemma establishes a condition

that ensures that implementing effort e is optimal for the debt-financed entrepreneur.

Lemma 2 There exists a threshold complementarity parameter η̂D such that the debt-financed entrepreneur

implements effort e if η ≥ η̂D and shirks otherwise.

According to Lemma 2, exerting high effort e, and thus incurring the associated cost ψ, is only

worthwhile for the entrepreneur in the presence of sufficient complementarities. This can be observed

because the incremental gross profit of the new venture, η(πH−πL), is increasing in the complementarity

parameter. Only an adequately high expected payoff of the venture (which requires η being sufficiently

high) compensates the entrepreneur for incurring the disutility ψ and, hence, motivates him to implement

the high effort level e.

Anticipating his effort choice i ∈ {0, e} as a debt-financed entrepreneur, the reservation utility of the

employee, denoted ΓDi , must be equal to the entrepreneur’s expected utility in equilibrium:

ΓDi = ρiu(ηπH − (1 + rD)X − ci) + (1− ρi)u(ηπL − (1 + rD)X − ci), (12)

where the superscript ‘D’ indicates debt financing and, as before, ci ∈ {0, ψ} stands for the agent’s

disutility of effort. We can infer from (12) that the entrepreneur’s specific effort choice – as defined by

his incentive constraint (11) – can be expected to have a significant influence on the optimal design of

employment contracts.

14

We can now characterize the optimal employment contract when the employee’s best outside option

is to become a debt-financed entrepreneur. For parsimony, let πDH(η) ≡ ηπH − (1 + rD)X and πDL (η) ≡

ηπL − (1 + rD)X denote the potential net payoffs for the debt-financed entrepreneur, with ∆πD(η) ≡

πDH(η)− πDL (η).

Proposition 2 Suppose the best outside option for the employee is to become a debt-financed entrepreneur.

Then, the optimal base wage wDL (η) is characterized as follows:

πDL (η) ≤ (≥)wDL (η) ≤ (≥)πDL (η̂D) if η ≤ (≥)η̂D,

with equality holding when η = η̂D. Moreover, the optimal performance bonus is ∆wD(η̂D) =

∆πD(η̂D).

The implications of Proposition 2 are very similar to those of Proposition 1. The optimal design

of the employment contract accounts for the complementarity parameter η and, therefore, for the prof-

itability of debt-financed entrepreneurship. The key insight, however, is that the optimal adjustment of

the employment contract hinges on the incentive constraint of the debt-financed entrepreneur, which is

captured by the threshold η̂D. Whenever the debt-financed entrepreneur does not find it optimal to exert

high effort e (i.e., η < η̂D), the firm needs to provide a relatively higher spread of potential payoffs,

∆wD(η̂D), in order to motivate effort within the firm. However, since higher-powered incentives impose

more uncertainty on the risk-averse agent, the firm is concurrently forced to offer a higher base income

level wDL (η) to ensure the employee accepts the employment contract. In contrast, whenever the spread

of potential payoffs under entrepreneurship is sufficiently large to motivate effort e (i.e., η > η̂D), the

firm can still induce effort by providing the employee with a relatively lower income spread ∆wD(η̂D).

Since this concurrently mitigates the uncertainty in the employee’s compensation, the firm can provide a

lower guaranteed income wDL (η) without jeopardizing the employee’s participation.

To gain additional insight, we now focus on the optimal employment contract when the incentive

constraint of the entrepreneur is just binding, i.e., η = η̂D. In this case, we can infer from Proposi-

tion 2 that the firm adjusts the contract {wDL (η),∆wD(η̂D)} aimed at replicating the agent’s potential

payoffs as a debt-financed entrepreneur. As a result, the employee’s compensation exhibits the same

15

uncertainty as his income as a self-employed and debt-financed entrepreneur. However, due to the em-

ployee’s attractive outside option, we can predict that he captures most of the surplus stemming from the

employment relationship. Only the surplus originating from firm-specific efficiency gains is captured by

the employer. To see this, one can substitute the optimal contract {wDL (η),∆wD(η̂D)} for η = η̂D, as

shown in Proposition 2, into the firm’s objective function (1), which leads to

ΠD = (1− η̂D) [ρeπH + (1− ρe)πL] + [rD − r0]X. (13)

As for equity-financed entrepreneurship constituting the employee’s best outside option, the firm’s ex-

pected profit ΠD clearly comprises a return from potential complementarity effects (reflected by the

parameter η, which in this case takes on the value η̂D) and a revenue stemming from the firm’s possibly

lower cost of capital (i.e., rD − r0). Thus, the firm can exploit efficiency gains associated with an inter-

nal production by offering its employees lower compensation, which reflects their less attractive outside

options.

More interesting, however, is the case where the venture’s low payoff ηπL does not suffice to entirely

repay the entrepreneur’s debt (1+rD)X . Technically, this occurs whenever ηπL < (1+rD)X , implying

that the entrepreneur’s limited liability becomes a binding constraint. There are essentially two reasons

as to why this might occur. First, the venture’s production technology could be relatively inefficient –

which is reflected by a sufficiently low parameter η – so that in the worst case scenario (i.e., π = πL),

the generated payoff does not cover the entrepreneur’s financial liabilities. Second, the cost of capital

rD faced by the equity-financed entrepreneur could simply be too high to allow him to clear his debt in

any possible scenario. In any case, the entrepreneur must then declare bankruptcy, and the (insufficient)

payoff is seized by the financier. Note, however, that this does not necessarily imply that providing capital

X is unprofitable for the financier. This specifically depends on the high payoff πH in combination with

its probability of occurrence ρi, i = 0, e. Anticipating the potential loss (1 + rD)X− ηπL, which occurs

with probability (1 − ρi), the financier will raise the interest rate for the entrepreneur to account for the

default risk.

We let r′D denote the risk-adjusted cost of capital for the debt-financed entrepreneur when the fi-

nancier is confronted with a default risk (i.e., ηπL < (1 + rD)X). In equilibrium, the risk-adjusted cost

16

of capital r′D guarantees the risk-neutral financier the same expected return as in the absence of a default

risk (i.e., when (1 + rD)X ≥ ηπL). Technically, r′D solves

(1 + rD)X = ρi(1 + r′D)X + (1− ρi)ηπL. (14)

From a closer inspection of (14) it becomes clear that r′D > rD as ηπL < (1 + rD)X in case of a

potential default. Rearranging (14) yields the risk-adjusted cost of capital r′D:

r′D =(1 + rD)X − (1− ρi)ηπL

ρiX− 1. (15)

Moreover, let η̂′D denote the adjusted threshold complementarity parameter which accounts for the en-

trepreneur’s new potential payoffs when facing the risk of insolvency. Formally, the adjusted threshold

η̂′D satisfies the new incentive constraint for the debt-financed entrepreneur when his liability limit is

binding (i.e., ηπL < (1 + rD)X):

ρeu(ηπH − (1 + r′D)X − ψ) + (1− ρe)u(−ψ) ≥ ρ0u(ηπH − (1 + r′D)X). (16)

Given the optimal effort choice under entrepreneurship as defined by (16), we can now characterize

the employee’s reservation utility ΓD′

i , i = 0, e, in case he faces the risk of insolvency as a debt-financed

entrepreneur (i.e., ηπL < (1 + rD)X):

ΓD′

i = ρiu(ηπH − (1 + r′D)X − ci) + (1− ρi)u(−ci), (17)

where ci ∈ {0, ψ}. Observe that in case of insolvency (i.e., π = πL, with ηπL < (1 + r′D)X), the

entrepreneur’s return from his endeavor is inevitably zero, which constitutes a unique characteristic of

debt-financed entrepreneurship: the risk of bankruptcy.

We are now well equipped to identify the optimal adjustment of employment contracts when em-

ployees, in pursuing their entrepreneurial outside option based on debt, need to accept the possibility –

and its consequences – of declaring bankruptcy.

17

Proposition 3 Suppose the best outside option of the employee is to become a debt-financed entrepreneur

facing the risk of insolvency (i.e., ηπL < (1 + rD)X). Then, the optimal base wage wD′

L (η) is charac-

terized as follows:

wD′

L (η) > (=)πDL (η) = 0 if η < (≥)η̂′D.

Moreover, the optimal performance bonus is ∆wD′(η̂D′) = ∆πD(η) = πDH(η).

A comparison of the optimal employment contract {wD′L (η),∆wD′(η̂D′)}, which accounts for in-

solvency risks (see Proposition 3), and the optimal contract {wDL (η),∆wD(η̂D)} in the absence of any

default risks (see Proposition 2) leads to the following conclusion for the case where a succeeding ven-

ture is sufficiently profitable (i.e., η ≥ max{η̂D, η̂′D}): Potential bankruptcy of debt-financed ventures,

and the associated higher costs for the entrepreneurs in raising the required capital, allows firms to re-

duce the base compensation for their employees down to zero without jeopardizing their participation.

Interestingly, their compensation then consists exclusively of a performance pay, which imposes more

risk on the risk-averse employees. In a sense, the firm emulates the potential payoffs of employees when

they become debt-financed entrepreneurs. Such intrapreneurship eliminates the necessity for the firm to

provide insurance by means of positive base wages, even though employees are strictly risk-averse.

It is clear that firms benefit from diminished compensations for their employees, which are rooted

in deteriorated outside options. Nonetheless, it still yields insight to quantify the surplus from the

employment relationship, which is captured by the firm solely as a result of potential bankruptcy of

debt-financed entrepreneurs. To obtain closed-form solutions, we focus on the case where the debt-

financed entrepreneur finds it optimal to exert effort e (i.e., η ≥ η̂′D). Substituting the optimal contract

{wD′L (η),∆wD′(η̂D′)} for η ≥ η̂′D – as exposed by Proposition 3 – into the firm’s objective function (1)

yields

ΠD′ = (1− η) [ρeπH + (1− ρe)πL] +[r′D − r0

]X. (18)

To characterize the surplus which is additionally seized by the firm, we can compare the firm’s expected

profits ΠD and ΠD′ as defined by (13) and (18), respectively. Keep in mind, however, that this compari-

son relies on the assumption that η = η̂D ≥ η̂′D. Nonetheless, it will become clear from our subsequent

18

discussion that we would obtain, qualitatively, the same implications for different values of η. One can

easily verify that ΠD′ > ΠD is equivalent to

ηπL − (1 + rD)X︸ ︷︷ ︸≡A

+ρe[(1 + r′D)X − ηπL

]︸ ︷︷ ︸≡B

. (19)

Notice that A equals the base wage wL, with wL > 0, for the case without bankruptcy risk and η =

η̂D; see Proposition 2. Moreover, as indicated by r′D, the term B in (19) refers to the case where the

entrepreneur’s liability limit is a binding constraint, which implies that B > 0. Accordingly, we have

ΠD′e > ΠD

e , i.e., the firm – as expected – strictly benefits from a potential bankruptcy of debt-financed

entrepreneurs. A closer inspection of (19) further reveals that the firm’s corresponding gain stems from

the now needless base wage wL, and the entrepreneur’s higher cost of capital r′D. The next Proposition

finally summarizes our previous observations.

Proposition 4 Limited liability of debt-financed entrepreneurs, and the associated higher cost of capital

for their ventures, results in a reduction of wages under employment and an increase in the profits of the

employer.

To conclude, Proposition 4 emphasizes that limited liability of entrepreneurs introduces another form

of imperfection into financial markets that the employer is able to exploit. Limited liability enhances

the costs of debt financing, and thereby reduces the value of entrepreneurship as an outside option for

employees. The employer, in turn, is able to take advantage of the deteriorated outside option of its

employees by reducing their compensation, eventually allowing the employer to capture more of the

surplus stemming from its employment relationships.

4.3 To be Spoiled for Choice: Equity versus Debt

We have shown in the previous sections that both types of financing – through equity and debt – have

various implications for optimal employment contracts within firms. To complete our analysis, we now

identify the optimal choice of an employee with respect to financing his potential endeavor and elaborate

on the implications for the design of employment contracts.

19

For parsimony, we do not explicitly distinguish in this section between a binding and a non-binding

liability limit for the entrepreneur under debt financing. Note, however, that the entrepreneur’s expected

income and expected utility under debt financing with a default risk (binding liability limit) can be

expressed in terms of the cost of capital rD by using the definition of the risk-adjusted cost of capital

r′D (see eq. (15) in Section 4.2). It is therefore important to keep in mind that our subsequent analysis

accounts for both cases under debt financing, even though we henceforth refer only to the cost of capital

rD.

We start our comparison by first focusing on the expected income for the entrepreneur under both

alternatives, i.e., equity and debt-financed entrepreneurship.

Lemma 3 Debt financing provides the entrepreneur with a higher expected income than equity financing

if rE ≥ rD.

Lemma 3 illustrates an intuitive result: the option with the lower cost of capital provides the en-

trepreneur with a higher expected income. Consequently, if the entrepreneur was risk-neutral, he would

prefer debt financing whenever the associated costs are below those of equity financing and vice versa.

The entrepreneur in our framework, however, is assumed to be risk-averse. Thus, in addition to the

expected income, the variation of potential payoffs under both alternatives (i.e., the associated risk) also

plays a key role for the entrepreneur’s choice. The next proposition sheds light on the entrepreneur’s

specific preferences with respect to the form of financing his venture.

Proposition 5 Suppose the entrepreneur is risk-averse. Then, there exists a threshold equity cost r̂E ,

with r̂E > rD such that the entrepreneur strictly prefers equity financing if rE < r̂E , and debt financing

otherwise.

It is inherent that the entrepreneur prefers debt financing whenever the cost of capital associated

with equity financing is sufficiently high (i.e., if rE ≥ r̂E). However, at first glance it seems somewhat

surprising that for rD ≤ rE < r̂E the entrepreneur strictly prefers equity financing even though it is

associated with a higher cost of capital and, hence a lower expected income (see Lemma 3). The reason

for this observation can be found in the concavity of the entrepreneur’s utility function.

20

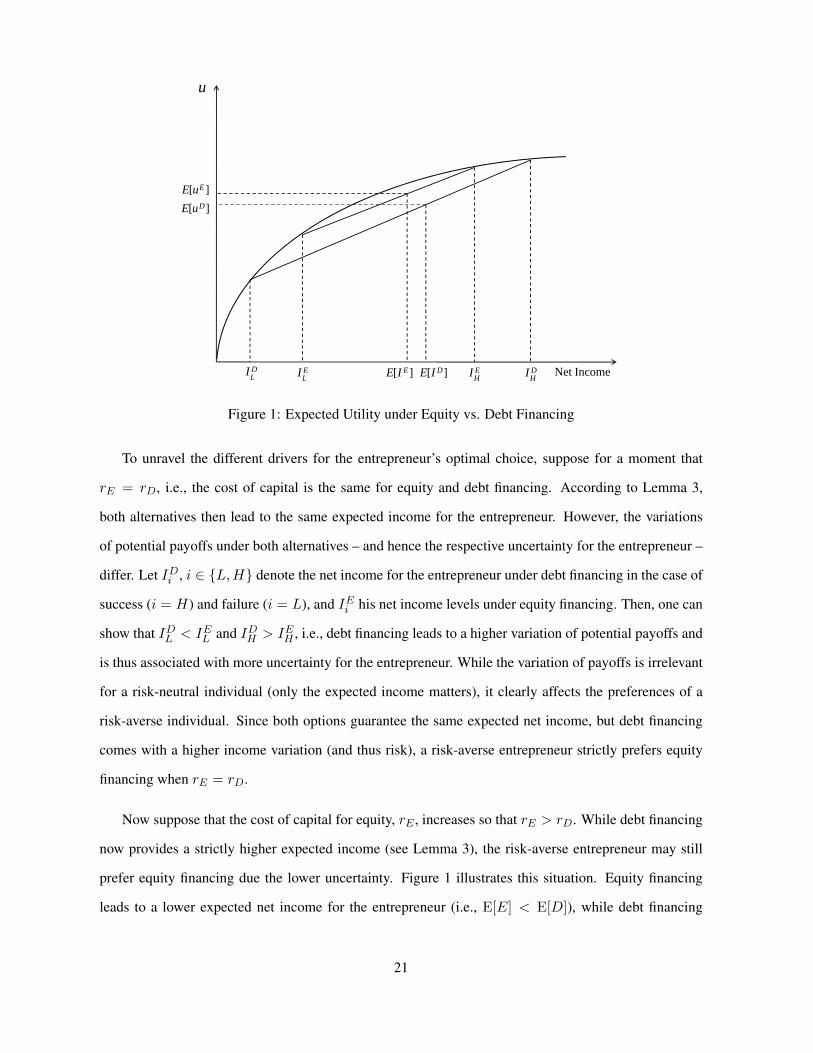

u

][ DE][ EuE][ DuE

][ DIE][ EIEDLI E

LI EHI D

HI IncomeNet

Figure 1: Expected Utility under Equity vs. Debt Financing

To unravel the different drivers for the entrepreneur’s optimal choice, suppose for a moment that

rE = rD, i.e., the cost of capital is the same for equity and debt financing. According to Lemma 3,

both alternatives then lead to the same expected income for the entrepreneur. However, the variations

of potential payoffs under both alternatives – and hence the respective uncertainty for the entrepreneur –

differ. Let IDi , i ∈ {L,H} denote the net income for the entrepreneur under debt financing in the case of

success (i = H) and failure (i = L), and IEi his net income levels under equity financing. Then, one can

show that IDL < IEL and IDH > IEH , i.e., debt financing leads to a higher variation of potential payoffs and

is thus associated with more uncertainty for the entrepreneur. While the variation of payoffs is irrelevant

for a risk-neutral individual (only the expected income matters), it clearly affects the preferences of a

risk-averse individual. Since both options guarantee the same expected net income, but debt financing

comes with a higher income variation (and thus risk), a risk-averse entrepreneur strictly prefers equity

financing when rE = rD.

Now suppose that the cost of capital for equity, rE , increases so that rE > rD. While debt financing

now provides a strictly higher expected income (see Lemma 3), the risk-averse entrepreneur may still

prefer equity financing due the lower uncertainty. Figure 1 illustrates this situation. Equity financing

leads to a lower expected net income for the entrepreneur (i.e., E[E] < E[D]), while debt financing

21

results in a higher variation of potential payoffs (i.e., IDH − IDL > IEH − IEL ). Due to the concavity of

the entrepreneur’s utility function u(·), financing the venture through equity leads to a higher expected

utility despite the lower expected net income. In this sense, financing with equity has an insurance

effect as it comes with more compressed income levels for the entrepreneur than financing the venture

with debt. This observation is clearly rooted in the division of equity – and hence in the division of the

venture’s profit – which implicates a more efficient risk sharing between the risk-averse entrepreneur and

risk-neutral financier. Finally, for sufficiently high rE (i.e., rE > r̂E), the expected income under equity

financing is so low that the entrepreneur now prefers debt financing despite the higher risk.

We can now elaborate on the implications for the optimal design of employment contracts within

firms. Suppose for a moment that the cost of capital under equity financing, rE , is sufficiently high so

that debt financing is preferred by an entrepreneur (i.e., rE ≥ r̂E). As shown, however, financing a

venture through debt results in a higher variation of potential payoffs for the entrepreneur as compared

to equity financing (i.e., IDH − IDL > IEH − IEL ). Since the optimal employment contract reflects the

employee’s potential payoffs as an entrepreneur, it comprises a relatively higher base wagewL to account

for the higher variation under debt financing and, thus, to provide the employee with more insurance. In

contrast, if rE is sufficiently low (rE < r̂E) financing a venture with equity is preferred. The employer

can then take advantage of the lower variation of the employee’s potential payoffs under entrepreneurship

by offering him a lower base wage.

Proposition 5 provides another interesting insight: For rD < rE < r̂E , the employee – as an en-

trepreneur – prefers equity financing even though debt financing would yield a higher expected income,

which, as discussed, is rooted in the employee’s risk-aversion. This in turn allows the employer to offer

a lower expected wage payment than would be required if the employee (as an entrepreneur) decided

in favor of debt financing. To illustrate the significance of this observation, consider a risk-neutral em-

ployee,A, and a risk-averse employee,B. For rD < rE , employeeAwould clearly prefer debt financing

(see our previous discussion), while, as long as rE < r̂E , employee B would favor equity financing (see

Proposition 5). According to Lemma 3, employee A would then enjoy a higher expected income as an

entrepreneur than employee B. This in turn would prompt the employer to offer the risk-averse em-

ployee B a contract with a lower expected compensation, implying that more of the surplus from the

22

employment relationship accrues to the employer. In a sense, when accounting for entrepreneurial out-

side options, risk-aversion on the side of employees can be beneficial for firms. This observation stands

in sharp contrast to the implications of the traditional principal-agent literature, where, unlike in our

framework, the value of the agent’s outside option is typically exogenous and constant.15

5 Discussion

5.1 Non-compete Clauses

Our analysis suggests that entrepreneurial outside options for employees can be both a blessing and a

curse for employers. A blessing because firms can replicate employee’s entrepreneurial outside options

(the intrapreneurship effect), thus exploiting any market imperfections (such as limited liability on the

side of the debt-financed entrepreneur or higher cost of capital of equity-financed entrepreneurs). A

curse, on the other hand, because improved outside options force employers to transfer more of the

surplus from the employment relationship to employees (the participation effect).

One alternative for firms to mitigate the participation effect is to include non-compete clauses in

employment contracts. In general, non-compete clauses prohibit former employees to directly compete

with their previous employers for a specified period of time, either by joining a firm operating in the same

market or by starting their own ventures to pursue similar business ideas. Thus, if skills and expertise

of employees are closely tied to the specific products and operations of their current employer, adopting

non-compete clauses can severely deteriorate the value of employees’ entrepreneurial outside options.

In our model, the inclusion of a non-compete clause in the employment contract is captured by a lower

complementarity parameter η. Suppose the optimal effort levels under employment and entrepreneurship

are symmetric. Then, irrespective of whether the best alternative for the employee is to become an equity-

or debt-financed entrepreneur, a lower value of his outside option – reflected by a lower η – will prompt

the employer to reduce the base wage wL, which in turn results in a lower total expected compensation

for the employee.15There are some exceptions where the outside option of an agent is endogenous; see, for instance, the literature on endoge-

nous matching (e.g., Besley and Ghatak (2005) and Serfes (2008)). In these models with endogenous matching, however, theoutside option of an agent is to contract with a different employer and, unlike in our framework, to become a capital-constrainedentrepreneur.

23

Our framework thus provides two interesting predictions with respect to the effects of non-compete

agreements. First, allowing firms to include non-compete clauses in employment contracts results in

lower base salaries offered to their employees as well as lower total compensation (which includes per-

formance pay). Second, as a consequence of these contract adjustments, applying non-compete clauses

ultimately transfers more of the surplus from the employment relationship to the firm, thus making em-

ployees clearly worse off.

5.2 Empirical Implications

The key insight from our analysis is that characteristics of the capital market indirectly affect the design

of employment contracts within firms and, hence the division of surplus stemming from employment

relationships. The particular effects on employment contracts, however, are closely tied to industry-

specific characteristics. In industries where spin offs are easy to establish for employees, our model

predicts that firms – in order to retain these employees – need to transfer more surplus in the form of

higher wages. This can be predicted for industries with low barriers to entry, little or no patent protection,

and generic production technologies. Notably, the developments in the market for venture capital over

the last two decades – accompanied by improved opportunities for employees to start their own ventures

– can be predicted to have substantially raised the compensations in these industries, in particular for the

middle and upper management.

On the other hand, employee spin offs in industries with high barriers to entry, strong patent pro-

tection, or firm-specific production technologies are less likely to be feasible. For these industries, our

model predicts lower compensations for employees, which results in more surplus being captured by

firms. The same can be expected for firms enjoying strong complementarity effects in production (re-

flected by a low parameter η in our model), which cannot be replicated by employees when starting their

own venture. Here, again, firms can take advantage of less attractive entrepreneurial outside options by

offering their employees lower compensations.

24

6 Conclusion

In this paper, we develop and analyze a principal-agent model where the outside option for the risk-

averse agent is to become a capital-constrained entrepreneur. Central to our study is the question of how

entrepreneurial outside options affect employment contracts within firms. An important and intuitive

insight is that the presence of more lucrative entrepreneurship options forces firms to cede some surplus

by offering higher equilibrium wages to their employees. In an extreme case, where potential spin

outs are anticipated to be highly profitable, employees can even capture the entire surplus from their

productive effort. On the other hand, firms can take advantage of any potential inefficiency associated

with entrepreneurship, such as a higher cost of capital or lack of complementary assets, by offering their

employees lower wages.

Another key insight from our study is that employment results in lower expected income levels

for employees as compared to entrepreneurship whenever the respective production technologies are

very similar. In this case, firms can make employment contracts sufficiently attractive by imposing less

income risk on risk-averse employees. On the other hand, if production inside of firms is substantially

more efficient, employment contracts can impose even more income risk on employees – stemming from

high-powered performance pay – than pursuing entrepreneurial activities. This observation provides

a theoretical explanation for the recent increase in the adoption of high-powered performance pay, in

particular offered to corporate executives, in the form of high bonuses and lucrative stock option plans.

Traditional principal-agent literature suggest that optimal incentive contracts need to compensate

risk-averse agents for the uncertainty associated with their performance pay, typically by offering a fixed

wage component. We show, however, that this implication might not always hold when one accounts for

entrepreneurial outside options. When the best outside option is to become a debt-financed entrepreneur

facing the risk of insolvency, the optimal contract may only specify an uncertain performance pay (and no

fixed-wage component) even if agents are strictly risk-averse. Furthermore, we find that more risk-averse

agents, when considering starting their own venture, tend to prefer equity over debt financing as the latter

results in higher income variations. This in turn allows firms to attract these agents to employment even

by offering them lower expected (but less risky) incomes than they would receive as equity-financed

25

entrepreneurs. This leads to an important conclusion: When accounting for entrepreneurial outside

options, firms can actually benefit from the risk-aversion of their employees.

26

Appendix

Proof of Lemma 1.

First, using the entrepreneur’s incentive constraint (8), we define

ρeu(θe(η)ηπH − ψ) + (1− ρe)u(θe(η)ηπL − ψ)︸ ︷︷ ︸≡ICL

≥ ρeu(θe(η)ηπH) + (1− ρ0)u(θe(η)ηπL)︸ ︷︷ ︸≡ICR

. (20)

Observe that η = 0 implies ICL(η = 0) = u(−ψ) and ICR(η = 0) = u(0) = 0. Clearly, ICL(η =

0) < ICR(η = 0), which implies that the incentive constraint (20) is violated. Next, differentiating ICL

and ICR with respect to η yields

∂ICL∂η

= ρeu′(θe(η)ηπH − ψ)θe(η)πH + (1− ρe)u′(θe(η)ηπL − ψ)θe(η)πL > 0

∂ICR∂η

= ρ0u′(θe(η)ηπH)θe(η)πH + (1− ρ0)u′(θe(η)ηπL)θe(η)πL > 0.

Since ICL and ICR are both monotonically increasing in η, it remains to show that limη→∞ ICL ≥

limη→∞ ICR in order to prove that there exists a unique threshold η̂E which satisfies ICL(η̂E) =

ICR(η̂E). To do so, observe from (6) that limη→∞ θi(η) = 1. This observation, together with the

assumption that ρe > ρ0, implies that limη→∞ ICL ≥ limη→∞ ICR. Thus, there exists a unique thresh-

old η̂E such that the incentive constraint (8) is satisfied for η ≥ η̂E and violated for η < η̂E . 2

Proof of Proposition 1.

First, to minimize the risk-premium for the risk-averse agent, the firm chooses the lowest feasible per-

formance bonus ∆w which ensures that the employee’s incentive constraint (3) just binds:

ρeu(wH − ψ) + (1− ρe)u(wL − ψ) = ρ0u(wH) + (1− ρ0)u(wL). (21)

27

Moreover, recall from Lemma 1 that the entrepreneur’s incentive constraint (8) is binding for η = η̂E ,

i.e.,

ρeu(θe(η̂E)η̂EπH − ψ) + (1− ρe)u(θe(η̂E)η̂EπL − ψ)

= ρ0u(θe(η̂E)η̂EπH) + (1− ρ0)u(θe(η̂E)η̂EπL). (22)

Observe that (21) and (22) can only be satisfied at the same time when wL = θe(η̂E)η̂EπH and wL =

θe(η̂E)η̂EπL, implying that ∆wE(η̂E) = θe(η̂E)η̂E [πH − πL]. To demonstrate that ∆wE(η̂E) =

θe(η̂E)η̂E [πH − πL] is indeed the optimal performance pay, let ∆w denote an arbitrary wage spread

with ∆w 6= ∆wE(η̂E). First, suppose that ∆w < ∆wE(η̂E). Then, for ∆w the employee’s incentive

constraint (3) is violated, which implies that he will exert zero effort. Consequently, providing a perfor-

mance bonus ∆w with ∆w < ∆wE(η̂E) is not optimal for the firm. Now suppose that ∆w > ∆wE(η̂E).

Clearly, providing ∆w with ∆w > ∆wE(η̂E) would then induce the employee to exert high effort e.

However, the principal could reduce the performance bonus ∆w down to ∆wE(η̂E) without affecting

the employee’s effort choice. Because the agent is risk-averse, choosing the lowest feasible performance

bonus ∆w is optimal for the firm in order to minimize the required risk-premium for the agent. There-

fore, providing the performance bonus ∆w with ∆w > ∆wE(η̂E) cannot be optimal for the firm. To

summarize, the optimal performance bonus is defined by ∆wE(η̂E) = θe(η̂E)η̂E [πH − πL].

The optimal base wage wEL (η) is determined by the binding participation constraint (2). We need

to consider three cases: (i) η = η̂E , (ii) η < η̂E , and (iii) η > η̂E . Consider the first case (i) where

η = η̂E . As shown, the optimal performance bonus ∆wE(η̂E) then equals the spread of potential pay-

offs under entrepreneurship, thereby imposing the same risk on the risk-averse employee. Thus, (2)

can only bind if wEL (η̂E) = θe(η̂E)η̂EπL. Next, consider case (ii) where η < η̂E . According to our

previous results, the optimal performance bonus ∆wE(η̂E) then exceeds the spread of potential payoffs

under entrepreneurship, which in turn imposes more risk on the risk-averse agent. Concavity of u(·)

thus requires to set wEL (η) > θ0(η)ηπL for η < η̂E . Moreover, one can easily show that dΓEi /dη > 0.

Consequently, wEL (η) satisfies θ0(η)ηπL < wL(η) < θe(η̂E)η̂EπL for η < η̂E . Finally, consider case

(iii) where η > η̂E . In this case, as shown, the optimal performance bonus ∆wE(η̂E) is strictly smaller

28

than the spread of potential payoffs under entrepreneurship. Since this imposes less risk on the risk-

averse agent, the optimal base wage wEL (η), which satisfies the binding participation constraint (2), is

then characterized by wEL (η) < θe(η)ηπL for η > η̂E . Furthermore, because dΓEi /dη > 0, it must hold

that θe(η̂E)η̂EπL < wEL (η) < θe(η)ηπL for η > η̂E . 2

Proof of Lemma 2.

For convenience, we use (11) and define

ρeu(ηπH − (1 + rD)X − ψ) + (1− ρe)u(ηπL − (1 + rD)X − ψ)︸ ︷︷ ︸ICL

≥ ρ0u(ηπH − (1 + rD)X) + (1− ρ0)u(ηπL − (1 + rD)X)︸ ︷︷ ︸ICR

. (23)

Suppose for a moment that η = 0. Then, ICL(η = 0) = u(−(1 + rD)X − ψ) and ICR(η = 0) =

u(−(1 + rD)X) = 0, which implies that ICL(η = 0) < ICR(η = 0). Consequently, the incentive

constraint (11) is violated for η = 0. Differentiating ICL and ICR with respect to η gives

∂ICL∂η

= ρeu′(ηπH − (1 + rD)X − ψ)πH + (1− ρe)u′(ηπL − (1 + rD)X − ψ)πL > 0

∂ICR∂η

= ρ0u′(ηπH − (1 + rD)X)πH + (1− ρ0)u′(ηπL − (1 + rD)X)πL > 0.

Clearly, ICL and ICR are both monotonically increasing in η. Next, observe that limη→∞ ICL ≥

limη→∞ ICR since ρe > ρ0. Hence, there exists a unique threshold η̂D such that the incentive constraint

(11) is satisfied for η ≥ η̂D and violated for η < η̂D. 2

Proof of Proposition 2.

The proof is equivalent to the proof of Proposition 1. The only difference is that the employee’s potential

payoffs, as a debt-financed entrepreneur, are now ηπH − (1 + rD)X and ηπL − (1 + rD)X , and the

threshold complementarity parameter, η̂D, is now defined by the binding incentive constraint (11). Thus,

the optimal performance pay is ∆wD(η̂D) = η̂D [πH − πL], and the optimal base wage wDL (η) is char-

29

acterized as follows: (i) wDL (η̂D) = η̂DπL − (1 + rD)X if η = η̂D, (ii) ηπL − (1 + rD)X < wDL (η) <

η̂DπL − (1 + rD)X if η < η̂D, and (iii) η̂DπL − (1 + rD)X < wDL (η) < ηπL − (1 + rD)X if η > η̂D.

2

Proof of Proposition 3.

First, the adjusted threshold complementarity parameter η̂D′ for ηπL < (1 + rD)X is characterized by

ρeu(η̂D′πH − (1 + rD)X − ψ) + (1− ρe)u(−ψ) = ρ0u(η̂D′πH − (1 + rD)X). (24)

Next, note that the only difference to the case where ηπL > (1 + rD)X (i.e., where the entrepreneur’s

liability limit is not binding) is that the lowest possible payoff under entrepreneurship is now zero. By

drawing on the results of Proposition 2, we can infer that the optimal performance bonus is ∆wD′(η̂D′) =

η̂D′πH−(1+rD)X . Furthermore, since wL must be non-negative by assumption, the optimal base wage

wD′

L (η) is characterized as follows: (i) wD′

L (η) > 0 if η < η̂D′ ; and (ii), wD′

L (η) = 0 if η ≥ η̂D′ . 2

Proof of Lemma 3.

First, we let ID ∈ {IDL , IDH} denote the net income for the entrepreneur under debt financing and IE ∈

{IEL , IEH} his net income under equity financing. Suppose for a moment that the entrepreneur’s liability

limit under debt financing is non-binding, i.e., ηπL ≥ (1 + rD)X . Then, his expected income E[ID]

under debt financing is

E[ID] = ρi(ηπH − (1 + rD)X) + (1− ρi)(ηπL − (1 + rD)X) (25)

= ρiηπH + (1− ρi)ηπL − (1 + rD)X. (26)

Likewise, the entrepreneur’s expected income E[IE ] under equity financing is

E[IE ] = ρiθi(η)ηπH + (1− ρi)θi(η)ηπL (27)

= θi(η) [ρiηπH + (1− ρi)ηπL] , (28)

30

with i = 0, e. Since

θi(η) =ρiπH + (1− ρi)πL − η−1(1 + rE)X

ρiπH + (1− ρi)πL, (29)

we have

E[IE ] = ρiηπH + (1− ρi)ηπL − (1 + rE)X.

Thus, E[ID] ≥ E[IE ] if

ρiηπH + (1− ρi)ηπL − (1 + rD)X ≥ ρiηπH + (1− ρi)ηπL − (1 + rE)X (30)

⇔ (1 + rE)X ≥ (1 + rD)X (31)

⇔ rE ≥ rD. (32)

Finally, we need to consider the case where the entrepreneur’s liability limit under debt financing is

binding, i.e., ηπL < (1 + rD)X . Then, his expected income E[ID] under debt financing is

E[ID] = ρi(ηπH − (1 + r′D)X). (33)

Accounting for the risk-adjusted cost of capital r′D as defined by (15), we can rewrite (33) as

E[ID] = ρi

(ηπH −

((1 + rD)X − (1− ρi)ηπL

ρi

))(34)

= ρiηπH + (1− ρi)ηπL − (1 + rD)X, (35)

which is equivalent to (26). Thus, even if ηπL < (1 + rD)X , we have E[ID] ≥ E[IE ] if rE ≥ rD. 2

31

Proof of Proposition 5.

Again, we let ID ∈ {IDL , IDH} denote the entrepreneur’s net income under debt financing and IE ∈

{IEL , IEH} his net income under equity financing. Using the entrepreneur’s share θi(η) under equity

financing as defined by 6, we get

IEL = θi(η)ηπL − ci =[η − (1 + rE)X

ρiπH + (1− ρi)πL

]πL − ci (36)

IEH = θi(η)ηπH − ci =[η − (1 + rE)X

ρiπH + (1− ρi)πL

]πH − ci (37)

IDL = ηπH − (1 + rD)X − ci (38)

IDH = ηπL − (1 + rD)X − ci. (39)

Suppose for a moment that rE = rD. Then, one can easily verify that IDL < IEL and IEH < IDH because

πL < ρiπH + (1− ρi)πL < πH ∀ ρi ∈ (0, 1).

Thus, var(ID) > var(IE). Moreover, recall from Lemma 3 that E[ID] = E[IE ] for rE = rD. Due to

the concavity of u(·), it follows that ΓEi > ΓDi if rE = rD.

Next, we fix rD and differentiate ΓEi with respect to rE :

∂ΓEi∂rE

= ρiu′EH )

∂IEH∂rE

+ (1− ρi)u′EL )∂IEL∂rE

. (40)

Note that u′(·) > 0. Moreover, observe from (36) and (37) that ∂IEi /∂rE < 0, i = L,H . Hence,

∂ΓEi /∂rE < 0. Furthermore, since θi(η) ≥ 0 due to the agent’s limited wealth, we can infer from (6)

that limrE→∞ θi(η) = 0. Thus, limrE→∞ ΓEi = u(ci) with u(ci) < ΓDi . Consequently, there exists a

threshold r̂E , with r̂E > rD, such that ΓEi > ΓDi if rE < r̂E , and ΓEi ≤ ΓDi if rE ≥ r̂E . 2

32

References

[1] Banerjee, A. and A. Newman, 1993, “Occupational Choice and the Process of Development” ,

Journal of Political Economy, 101(2), 274-293.

[2] Besley, T., and M. Ghatak, 2005, “Competition and incentives with motivated agents” American

Economic Review 95, 616-636.

[3] Bitler, M., T. Moskowitz, and A. Vissing-Jorgensen, 2005, “Testing Agency Theory with En-

trepreneur Effort and Wealth” Journal of Finance, 60(2), 539-576.

[4] Blanchflower, D., and A. Oswald, 1998, ”What Makes an Entrepreneur?” Journal of Labor Eco-

nomics, 16(1), 26-60.

[5] Evans, D., and B. Jovanovic, 1989, An estimated Model of Entrepreneurial Choice under Liquidity

Constraints” Journal of Political Economy, 97(4), 808-827.

[6] Evans, D., and L. Leighton, 1989, ”Some Empirical Aspects of Entrepreneurship” American Eco-

nomic Review, 79(3), 519-535.

[7] Franco, A., and D. Filson, 2005, “Spin-outs: knowledge diffusion through employee mobility”,

Department of Economics, Claremont Graduate University working paper.

[8] Ghatak, M., M. Morelli, and T. Sjöström, T, 2001, “Occupational Choice and Dynamic Incentives“

The Review of Economic Studies, 68(4), 781-810.

[9] Holtz-Eakin, D., D. Joulifaian, and H. Rosen, 1994a, ”Entrepreneurial decisions and liquidity con-

straints” RAND Journal of Economics, 25, 334-347.

[10] Holtz-Eakin, D., D. Joulifaian, and H. Rosen, 1994b, ”Sticking it out:Entrepreneurial survival and

liquidity constraints” Journal of Political Economy, 102(1), 53-75.

[11] Kanbur, R., 1979, “Of Risk-Taking and the Personal Distribution of Income” Journal of Political

Economy, 87(4), 769-797.

33

[12] Kanbur, R., 1982, “Entrepreneurial Risk-Taking, Inequality, and Public Policy: An Application of

Inequality Decomposition Analysis to the General Equilibrium Effects of Progressive Taxation”

Journal of Political Economy, 90(1), 1-21.

[13] Kaplan, S., and L. Zingales, 1997, ”Do Investment-Cash Flow Sensitivities Provide Useful Mea-

sures of Financing Constriants” The Quarterly Journal of Economics, 112, 169-215.

[14] Kihlstrom, R., and J.-J. Laffont, 1979, “A General Equilibrium Entrepreneurial Theory of Firm

Formation based on Risk Aversion” Journal of Political Economy, 87(4), 719-748.

[15] Oyer, P., 2004, “Why do firms use incentives that have no incentive effects?” The Journal of Fi-

nance, 59(4), 1619-1649.

[16] Paulson, A., R. Townsend, and A. Karaivanov, 2006, “Distinguishing limited liability from moral

hazard in a model of entrepreneurship” The Journal of Political Economy, 114(1), 100-144.

[17] Serfes, K., 2008, “Endogenous matching in a market with heterogeneous principals and agents”

International Journal of Game Theory 36, 587-619.

[18] Shane, S. 2009a, "Job loss in the Recession: If you work for yourself, are you worse off?", U.S.

News & World Report, January 26.

[19] Shane, S., 2009b, "From Start-up to Stop: The Recession and Entrepreneurship", The American,

The Journal of the American Enterpreise Institute, October 30.

[20] Taylor, M., 1996, ”Earnings, Independence or Unemployment: Why Become Self-Employed?”

Oxford Bulletin of Economics and Statistics, 58, 253-265.

34