Embed Size (px)

Citation preview

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL

FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31, 2014 AND 2013

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL TABLE OF CONTENTS

YEARS ENDED DECEMBER 31, 2014 AND 2013

INDEPENDENT AUDITORS’ REPORT 1

MANAGEMENT’S DISCUSSION AND ANALYSIS 3

FINANCIAL STATEMENTS

STATEMENTS OF NET POSITION 11

STATEMENTS OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION 13

STATEMENTS OF CASH FLOWS 14

NOTES TO FINANCIAL STATEMENTS 16

CliftonLarsonAllen LLP CLAconnect.com

(1)

An independent member of Nexia International

INDEPENDENT AUDITORS’ REPORT

Board of Commissioners Skagit County Public Hospital District No. 2 dba Island Hospital Anacortes, Washington Report on the Financial Statements

We have audited the accompanying financial statements of Skagit County Public Hospital District No. 2 dba Island Hospital (the Hospital), which comprise the statements of net position as of December 31, 2014 and 2013, and the related statements of revenues, expenses, and changes in net position and cash flows for the years then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Board of Commissioners Skagit County Public Hospital District No. 2 dba Island Hospital

(2)

Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Skagit County Public Hospital District No. 2 dba Island Hospital as of December 31, 2014 and 2013, and the changes in its financial position and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America. Other Matters

Required Supplementary Information

Our audits were conducted for the purpose of forming an opinion on the financial statements as a whole. Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis information on pages 3 through 10 be presented to supplement the basic financial statements. Such information, although not a part of the financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the financial statements, and other knowledge we obtained during our audit of the financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

CliftonLarsonAllen LLP Bellevue, Washington April 23, 2015

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL MANAGEMENT’S DISCUSSION AND ANALYSIS

DECEMBER 31, 2014 AND 2013

(3)

Using this Annual Report

The Hospital’s consolidated financial statements consist of three statements – statements of net position; statements of revenues, expenses, and changes in net position; and statements of cash flows. These financial statements and related notes provide information about the activities of the Skagit County Public Hospital District No. 2 doing business as Island Hospital (the Hospital) including resources held by the Hospital but restricted for specific purposes by contributors, grantors, or enabling legislation. Statements of Net Position and Statements of Revenues, Expenses, and Changes in Net

Position

Our analysis of the Hospital’s finances begins on page 4. One of the most important questions asked about the Hospital’s finances is, “Is the Hospital as a whole better or worse off as a result of the year’s activities?” The statements of net position and the statements of revenues, expenses, and changes in net position report information about the Hospital’s resources and its activities in a way that helps answer this question. These statements include all restricted and unrestricted assets and all liabilities using the accrual basis of accounting. All of the current year’s revenues and expenses are taken into account regardless of when cash is received or paid. Those two statements report the Hospital’s net position and changes in net position. You can think of the Hospital’s net position – the difference between assets and liabilities – as one way to measure the Hospital’s financial health or financial position. Over time the increases or decreases in the Hospital’s net position are one indicator of whether the financial health is improving or deteriorating. You will need to consider other nonfinancial factors, however, such as changes in the Hospital’s patient base and measures of the quality of service it provides to the community, as well as local economic factors to assess the overall health of the Hospital. Statements of Cash Flows

The final required statement is the statement of cash flows. The statement reports cash receipts, cash payments, and net changes in cash resulting from operations, investing, and financing activities. It also describes the sources and uses of cash during the reporting period. Introduction

The discussion and analysis of the Hospital financial performance provides an overview of the financial activities for the years ended December 31, 2014 and 2013. The financial statements and notes are to be read in conjunction with this section. The following narrative utilizes approximate amounts unless otherwise specified.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL MANAGEMENT’S DISCUSSION AND ANALYSIS

DECEMBER 31, 2014 AND 2013

(4)

Financial Highlights

For the fiscal year ended December 31, 2014, the Hospital reported net operating gain of $1,472,371 and excess of revenues over expenses before capital contributions of $2,784,617, a margin of 3.3 percent. This compares to respective amounts in 2013 of a net operating loss of $521,660, excess of revenues over expenses of $926,898 and a margin of 1.1 percent. The following significant events had an impact on the operating results for the Hospital:

The Hospital entered into an agreement with Challenge Developments II, LLC in March 2006 to

form the Island Medical Center Condominium Association for the purpose of purchasing the Island Medical Center medical office building which is located adjacent to the Hospital. The condominium is structured such that Challenge Developments II, LLC owns the first floor which houses four physician office practices. The Hospital owns the lower level which houses several hospital departments. The costs associated with operating and maintaining the building are shared on the basis of square footage owned by each party. The Hospital purchased its share of the condominium using Hospital reserves. The Hospital’s share of operating costs in 2014 were $41,504 offset by $29,162 of rental income and in 2013 were $39,692 offset by $28,754 of rental income respectively.

In November 2008, the Hospital entered into an agreement with Skagit Valley Hospital and United General Hospital to form Medical Information Network-North Sound to develop, implement, and maintain an electronic health record system for health care providers in Skagit County. Initial funding for this corporation came from a $50,000 grant received from the Health Care Authority and subsequent funding will be shared by the three hospitals equally. United General Hospital withdrew from the agreement in 2012. In 2010 the Hospital received an additional grant of $85,000 for this project. In 2014 the Hospital received another grant in the amount of $900,000 of which will be paid over 3 years. In 2014, $190,742 was requested to reimburse MIN-NS. In addition the Hospital contributed $383,298 in 2014, $379,655 in 2013, $281,557 in 2012, $133,088 in 2011, and $230,333 in 2010 for its share of the operating costs.

In 2008 the Hospital acquired the Zap Tune property and in January 2009 acquired the old KLKI radio station property. In December 2010 the Hospital entered into a construction contract with Lydig Construction to build the Medical Arts Pavilion on these parcels as well as other land already owned by the Hospital. Construction commenced in January 2011 with a scheduled completion date of December 2011. In June 2011 a new entity, Island Hospital Medical Properties, was created by the Hospital to hold and own the building. In August 2011, Island Hospital Medical Properties completed financing arrangements for the Medical Arts Pavilion utilizing the federal New Market Tax Credit program. The Hospital has entered into an agreement to lease the land to Island Hospital Medical Properties. The Hospital has also entered into a lease agreement with Island Hospital Medical Properties to lease the building for an annual lease amount of $545,000. Services housed in this new building include an expanded Cancer Care Center, Physical Therapy, and Wound Care. Construction was completed in December 2011 and the building opened for business January 2012.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL MANAGEMENT’S DISCUSSION AND ANALYSIS

DECEMBER 31, 2014 AND 2013

(5)

Financial Highlights (Continued)

In June 2011, the Hospital entered into an agreement with Restorix Medical Group, PLLC and Restorix Health LLP to provide advanced wound care services and hyperbaric medicine services in the new Medical Arts Pavilion. The Hospital provides the building space and bills the technical side while Restorix provides the staff, equipment and expertise and bills for the professional services. The service opened to see patients in January 2012. In December 2012, the Hospital received notice from Restorix that they were in receivership. The Center for Wound Healing purchased the name and assets of Restorix LLP and the Restorix Foundation and continues to provide the staff, equipment and expertise. The Restorix Medical Group was not included in the purchase and the physician that was providing his services via the Medical Group gave his notice to the medical group and was subsequently hired by the Hospital, which began billing for the professional services in 2013. In 2014, the employed physician relocated out of the area and Cloud Healthcare was hired to provide the professional services for Wound Care and will bill for these directly.

In June 2011, the Hospital entered into an agreement with Dr. David Slepyan, M.D. to provide plastic surgery services to patients at the Hospital and clinics. The Center for Aesthetic, Reconstructive and Hand Surgery opened in September 2011. In 2014, Dr. Slepyan retired and the clinic no longer provides plastic surgery services.

In August 2011, the Hospital entered into a Lease and Services Agreement with Orcas Medical Foundation. The Hospital agreed to lease the 6,000 square foot facility and Orcas Medical Foundation contracted with Island Hospital to operate and manage the primary care medical facility with federal rural health clinic status. The Orcas Medical Foundation has committed to provide grant funding to support the operation of the clinic up to annual maximum amounts of $200,000 for 2012 and 2011, with decreasing annual caps starting in 2013. In 2014 and 2013, Orcas Medical Foundation provided support in the amount of $120,000 and $109,272, respectively. In June 2012, the medical center received federal rural health clinic status and in December received notification of the encounter rate based upon the 2011 cost report.

In October 2011, the Hospital entered into a refundable grant agreement in support of professional urology services in Skagit County with Skagit Valley Hospital. The grant calls for an initial grant of $107,000 which was paid in 2011, and an additional $227,000 for the first year of the agreement defined as November 1, 2011 to October 31, 2012. Additional grant funding is determined by a set formula in the agreement based upon the financial performance of the clinic. Additional grant funding was requested in 2014 and 2013 of $280,721.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL MANAGEMENT’S DISCUSSION AND ANALYSIS

DECEMBER 31, 2014 AND 2013

(6)

Financial Highlights (Continued)

The Hospital submitted an application to the Office of Management and Budget (OMB) of the United States of America requesting a reclassification from the Mount Vernon-Anacortes MSA to the Seattle-Tacoma-Olympia CSA for purposes of increasing reimbursement from the Medicare program. The application was approved by OMB in December 2006 and approved by the Medicare Geographic Review Board in February 2007. The Hospital received extensions in subsequent periods that are effective through September 30, 2016.

The Hospital received $500,000 in 2010 and $100,000 from 2011 through 2014 from the Island

Hospital Foundation for the purpose of funding the Medical Arts Pavilion with a commitment to receive $100,000 per year through 2020. The Hospital also received $115,000 in 2014, $113,472 in 2013, $148,910 in 2012, $144,200 in 2011, and $135,655 in 2010 from the Foundation for other capital equipment, as well as $202,028 in 2014, $175,853 in 2013, $241,851 in 2012, $86,700 in 2011, and $90,900 in 2010 for other programs in the Hospital.

In November 2014 $9,190,000 refunding bonds were issued for the advance refunding of the

District’s outstanding Limited Tax General Obligation Bonds, 2005 plus $2,900,000 in additional bonds. Moody’s gave the 2014 Refunding bonds a rating of “A2”. Over the term of the refunded bonds, the District will save taxpayers an estimated $800,000.

In 2014, 2013, and 2012, the Hospital applied for and received federal Medicare Meaningful

Use under the Health Information Technology for Economic and Clinical Health Act in the amount of $639,648, $1,052,007, and $1,176,766, respectively. The Hospital also applied for and received in 2014 and 2012 state Medicaid Meaningful use funds in the amount of $380,216 and $336,345, respectively.

In September 2013, the Hospital purchased the property at 2520 Commercial Avenue for future expansion plans. The Hospital leased the property back to the former owner under a 3-year lease term.

In December 2013, the Hospital was notified by Sound Sleep Center that they no longer would provide physician services for the Sleep Center. The Hospital negotiated the employment of the current provider effective January 1, 2014.

In April 2014, the Hospital entered into an Accountable Care Network (ACN) with UW Medicine.

The ACN is currently an option for Boeing beneficiaries and UW is hoping to offer their product on a broader scale.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL MANAGEMENT’S DISCUSSION AND ANALYSIS

DECEMBER 31, 2014 AND 2013

(7)

Statements of Revenues, Expenses, and Changes in Net Position

The following table summarizes the operating results of the Hospital for the years ended December 31, 2014, 2013, and 2012:

Restated2014 2013 2012

Net Patient Service Revenue 82,360$ 79,279$ 77,614$ Other Operating Revenue 1,878 1,838 2,179 Total Operating Revenues 84,238 81,117 79,793

Salaries, Wages, and Benefits 46,396 45,747 43,982 Professional Fees 6,319 6,485 5,758 Supplies 15,206 14,505 15,003 Purchased Services 7,927 7,697 7,158 Depreciation 4,105 4,203 4,729 Other Expenses 2,812 3,002 2,890

Operating Expenses 82,765 81,639 79,520

Operating Gain (Loss) 1,472 (522) 273

Nonoperating Revenue and Expenses 1,312 1,449 1,050

Excess of Revenues over Expenses 2,785 927 1,322

Contributions for Capital 322 213 249

Change in Net Position 3,107 1,140 1,571

Total Net Position, Beginning of Year 46,064 44,923 43,352

Total Net Position, End of Year 49,171$ 46,064$ 44,923$

(Dollars in Thousands)

Sources of Revenue

Net patient service revenue for 2014 increased $3.0 million or 3.9 percent from 2013. This was a result of increases in outpatient volumes and a decrease in bad debt. Net patient service revenue for 2013 increased $1.7 million or 2.1 percent from 2012. Patient service revenues are reported net of contractual adjustments with Medicare, Medicaid, and other third-party payers. The collection percentage for the Hospital decreased during the year due to a decrease in commercial insurance payments, increase in Medicaid, lower inpatient volumes and higher outpatient volumes.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL MANAGEMENT’S DISCUSSION AND ANALYSIS

DECEMBER 31, 2014 AND 2013

(8)

Sources of Revenue (Continued)

The following table shows the percentage of revenue by payer class based upon total patient revenue for the years ended December 31, 2014 and 2013. Description 2014 2013 Change 2012

Medicare (Including MGH) 50.3 % 50.5 % (0.2)% 51.6 %Medicaid 13.7 9.8 3.9 8.8Other Government 7.2 6.4 0.8 7.0Commercial Insurances 27.0 29.5 (2.5) 29.0Self-Pay 1.8 3.8 (2.0) 3.6

100.0 % 100.0 % 100.0 %

In 2014, Medicare, including Medicare managed care dollars, decreased 0.2 percent; Medicaid, including Healthy Options, increased 3.9 percent; Government payers increased 0.8 percent, commercial payers decreased 2.5 percent and self-pay decreased 2 percent. In 2013, Medicare, including Medicare managed care dollars, decreased 1.1 percent; Medicaid, including Healthy Options, increased 1 percent; Government payers decreased 0.6 percent, Commercial payers were unchanged and self-pay decreased 0.2 percent compared to 2012. In 2014, bad debt expense decreased 36 percent and charity write-offs decreased 50 percent over the 2013 amounts. In 2013, bad debt expense increased 24 percent and charity write-offs decreased 19 percent over the 2012 amounts. Operating Expenses

Total operating expenses in 2014 increased $1.1 million (1.4 percent) over 2013 compared to an increase in 2013 of $2.1 million (3 percent) over 2012. The increase for 2014 was in all categories except professional fees and depreciation.

Salaries, Wages, and Benefits increased by 1.4 percent compared to 2013 as a result of collective bargaining agreements, annual wage adjustments and increases in benefit costs. Total FTE’s decreased by 5 to a total of 518 in 2014.

Professional fees expense decreased 2.6 percent in 2014 compared to 2013 due to fewer consulting fees. Professional fees expense increased 12.6 percent in 2013 due to consulting fees for the affiliation project, 2035 Strategic Plan, Medical Use Overlay and Surgery as well as legal fees for extended union negotiations to renew the SEIU contract.

Purchased Services increased 3.0 percent compared to 2013 due to increased volumes at the

wound center, increased computer maintenance service costs and increased use of contract labor.

Supplies increased 4.8 percent due to increased drug costs, increased oncology volume and increased blood product costs. Supplies decreased 3.3 percent in 2013 from new contracts with vendors for spine supplies as well as decreases in drug costs with oncology volumes being down as well as tighter management of drug ordering.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL MANAGEMENT’S DISCUSSION AND ANALYSIS

DECEMBER 31, 2014 AND 2013

(9)

Operating Expenses (Continued)

Depreciation decreased 2.3 percent in 2014 and increased 11 percent in 2013 compared to 2012.

Other expenses decreased 6.3 percent in 2014 compared to 2013.

Statements of Net Position

The following table shows the statements of net position as of December 31, 2014, 2013, and 2012:

Restated2014 2013 2012

(Dollars in Thousands)

Current Assets:Cash and Cash Equivalents 22,470$ 16,139$ 13,757$ Patient Accounts Receivable, Net 8,039 10,168 9,432 Other Current Assets 3,447 3,203 3,262

Total Current Assets 33,956 29,510 26,451 Capital Assets, Net 65,277 67,022 68,773 Other Assets 9,341 6,716 8,315 Deferred Outflows of Resources 1,903 1,614 1,722

Total Assets and Deferred Outflows of Resources 110,477$ 104,862$ 105,261$

Current Liabilities 10,603$ 9,446$ 8,671$ Long-Term Debt, Net 49,930 48,542 50,831 Other Liabilities 774 810 836

Total Liabilities 61,306 58,798 60,338

Net Position 49,171 46,064 44,923

Total Liabilities and Net Position 110,477$ 104,862$ 105,261$

Total assets and deferred outflows of resources increased $5,615,000 from 2013 and decreased $399,000 from 2012. Current liabilities increased $1,157,000 from 2013 and increased $776,000 from 2012. Long-term debt increased as a result of the Limited Tax General Obligation bond refunding in 2014 and decreased as a result of debt payments in 2013.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL MANAGEMENT’S DISCUSSION AND ANALYSIS

DECEMBER 31, 2014 AND 2013

(10)

Currently Known Facts, Decisions, or Conditions

The State of Washington Auditor’s Office performed a financial and compliance audit for the year ended December 31, 2013. The Hospital was issued a report with no findings. In 2010, the Hospital contracted with DNV Healthcare, Inc. to conduct the accreditation survey and was issued an accreditation certificate on March 19, 2013, which is good through March 2016. In March 2014 the Hospital also received ISO Certification through DNV which is good through March 2016. The DNV accreditation process requires annual surveys and DNV was on site January 19 through 21, 2015 conducting the annual unannounced survey. Unofficially they are closing all findings from last year’s survey and will be issuing a new report within 10 days with the findings from this year’s survey. The Medicare cost reports for 2012 through 2013 have been filed and are awaiting final review. The cost report for 2014 will be filed in May 2015. Contacting the Hospital’s Financial Management

This financial report is designed to provide our patients, suppliers, taxpayers, and creditors with a general overview of the Hospital’s finances and to show the Hospital’s accountability for the money it receives. If you have questions about this report or need additional financial information, contact Administration, Skagit County Public Hospital District No. 2, 1211 24th Street, Anacortes, Washington 98221.

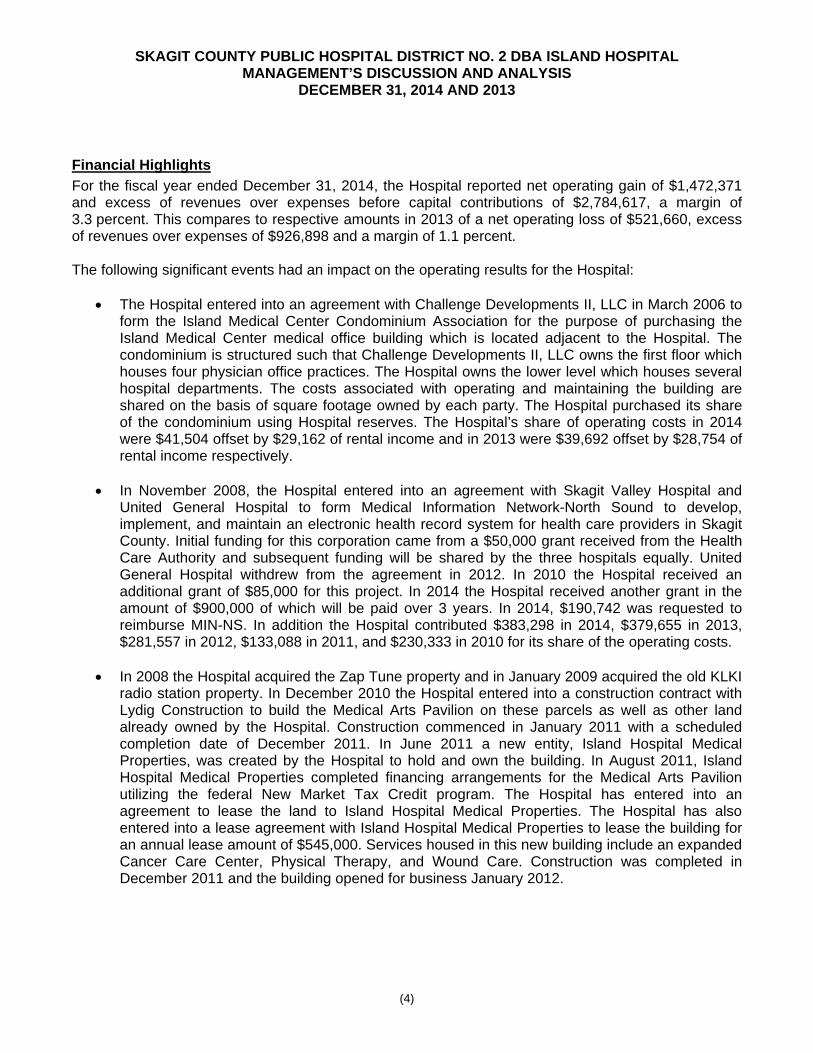

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL STATEMENTS OF NET POSITION DECEMBER 31, 2014 AND 2013

See accompanying Notes to Financial Statements. (11)

2014 2013

ASSETS AND DEFERRED OUTFLOWS OF RESOURCES

CURRENT ASSETSCash and Cash Equivalents 22,469,578$ 16,139,907$ Patient Accounts Receivable, Net 8,038,849 10,168,171 Other Receivables 729,091 572,610 Inventories 1,475,354 1,487,793 Prepaid Expenses 1,090,233 886,585 Current Portion of Assets Limited as to Use 152,243 256,056

Total Current Assets 33,955,348 29,511,122

NONCURRENT CASH AND INVESTMENTS, Less Current Portion 8,283,934 5,676,379

CAPITAL ASSETSArt 300,715 293,781 Land 4,708,577 4,708,577 Depreciable Capital Assets, Net 59,706,488 61,690,290 Construction in Progress 560,914 329,170

Total Capital Assets, Net 65,276,694 67,021,818

OTHER ASSETSIntangible Assets, Net 598,703 598,703 Purchase Option 458,449 440,449

Total Other Assets 1,057,152 1,039,152

Total Assets 108,573,128 103,248,471

DEFERRED OUTFLOWS OF RESOURCESLoss on Refunding of Long-Term Debt 1,903,416 1,613,912

Total Assets and Deferred Outflows of Resources 110,476,544$ 104,862,383$

(12)

2014 2013

LIABILITIES AND NET POSITION

CURRENT LIABILITIESCurrent Portion of Long-Term Debt 1,841,443$ 1,874,018$ Accounts Payable 4,661,965 3,872,190 Accrued Payroll and Related Liabilities 3,421,569 3,109,850 Accrued Interest 96,594 135,651 Estimated Third-Party Payer Settlements 454,855 440,000 Other Current Liabilities 126,142 14,402

Total Current Liabilities 10,602,568 9,446,111

LONG-TERM LIABILITIES Long-Term Debt, Less Current Portion 49,929,572 48,542,218 Deferred Compensation Payable 295,475 267,480 Professional Liability Claims Payable 478,202 542,857

Total Long-Term Liabilities 50,703,249 49,352,555

Total Liabilities 61,305,817 58,798,666

NET POSITIONNet Investment in Capital Assets 13,505,679 16,605,582 Unrestricted 35,665,048 29,458,135

Total Net Position 49,170,727 46,063,717

Total Liabilities and Net Position 110,476,544$ 104,862,383$

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL STATEMENTS OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION

YEARS ENDED DECEMBER 31, 2014 AND 2013

See accompanying Notes to Financial Statements. (13)

2014 2013

OPERATING REVENUESNet Patient Service Revenue 82,359,648$ 79,279,411$ Other Operating Revenue 1,877,795 1,838,290

Total Operating Revenues 84,237,443 81,117,701

OPERATING EXPENSESSalaries and Wages 37,318,884 36,663,342 Employee Benefits 9,077,004 9,083,167 Professional and Physician Fees 6,318,836 6,484,665 Supplies 15,205,949 14,505,052 Purchased Services 7,926,714 7,696,907 Rents and Leases 777,998 844,020 Depreciation and Amortization 4,105,015 4,202,999 Other Expenses 2,034,672 2,159,209

Total Operating Expenses 82,765,072 81,639,361

OPERATING GAIN (LOSS) 1,472,371 (521,660)

NONOPERATING REVENUE AND EXPENSESInvestment Income 60,517 62,391 Interest Expense (2,048,021) (1,901,720) Revenue from Tax Levy 3,141,464 3,091,983 Loss from Investment in Joint Venture (626,145) (450,845) Other Nonoperating Revenues 784,431 646,749

Total Nonoperating Revenue and Expenses 1,312,246 1,448,558

EXCESS OF REVENUES OVER EXPENSES 2,784,617 926,898

Contributions for Capital 322,393 213,472

Net Position - Beginning of Year 46,063,717 44,923,347

NET POSITION - END OF YEAR 49,170,727$ 46,063,717$

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL STATEMENTS OF CASH FLOWS

YEARS ENDED DECEMBER 31, 2014 AND 2013

See accompanying Notes to Financial Statements. (14)

2014 2013

CASH FLOWS FROM OPERATING ACTIVITIESReceipts from and on Behalf of Patients 84,242,470$ 78,849,230$ Payments to Suppliers and Contractors (40,750,532) (40,678,349) Payments to Employees (36,867,429) (36,454,356) Other Receipts and Payments, Net 1,871,795 1,838,290

Net Cash Provided by Operating Activities 8,496,304 3,554,815

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIESOther Nonoperating Receipts - Including Contributions 845,428 603,326 Receipts from Tax Levy - Operations 151,666 91,213

Net Cash Provided by Noncapital Financing Activities 997,094 694,539

CASH FLOWS FROM CAPITAL AND RELATED FINANCINGACTIVITIES

Capital Expenditures (2,363,878) (2,457,622) Receipts from Issuance of Debt 12,842,738 - Cash Paid for Financing Costs (327,146) - Advanced Refunding of 2005 LTGO Bonds (9,583,417) - Principal Payments on Long-Term Debt (1,802,906) (1,741,397) Interest Paid (2,176,420) (2,223,209) Receipts from Tax Levy 3,012,279 3,029,171 Contributions for Capital 322,393 213,472

Net Cash Used by Capital and Related Financing Activities (76,357) (3,179,585)

CASH FLOWS FROM INVESTING ACTIVITIESInterest and Dividends on Investments 42,517 44,391 Capital Contributions for Investment in Joint Venture (626,145) (450,845) Changes in Noncurrent Cash and Investments (2,503,742) 1,719,200

Net Cash Provided (Used) by Investing Activities (3,087,370) 1,312,746

INCREASE IN CASH AND CASH EQUIVALENTS 6,329,671 2,382,515 Cash and Cash Equivalents - Beginning of Year 16,139,907 13,757,392

CASH AND CASH EQUIVALENTS - END OF YEAR 22,469,578$ 16,139,907$

(15)

2014 2013

RECONCILIATION OF OPERATING GAIN (LOSS) TO NET CASH PROVIDED BY OPERATING ACTIVITIES

Operating Gain (Loss) 1,472,371$ (521,660)$ Adjustments to Reconcile Operating Gain (Loss) to

Net Cash Provided by Operating Activities:Amortization 59,038 21,400 Depreciation 4,096,169 4,207,856 Provision for Bad Debts 2,503,807 3,934,574 (Increase) Decrease in Assets:

Patient Accounts Receivable (374,485) (4,670,968) Other Receivables (261,355) 55,152 Inventories 12,439 (204,592) Prepaid Expenses (203,648) 100,544

Increase (Decrease) in Liabilities:Accounts Payable 790,314 126,694 Accrued Payroll and Payroll Related Expenses 311,719 288,555 Estimated Third-Party Payer Settlements 14,855 251,061 Deferred Compensation Payable 139,735 (80,884) Professional Liability Claims Payable (64,655) 47,083

Net Cash Provided by Operating Activities 8,496,304$ 3,554,815$

NONCASH INVESTING AND FINANCING ACTIVITIES

Equipment Purchases Remaining in Accounts Payable 55,649$ 58,218$

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(16)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Reporting Entity

The financial statements include the accounts of Skagit County Public Hospital District No. 2 dba Island Hospital (the Hospital), located in Anacortes, Washington, and Island Hospital Medical Properties. The Hospital is organized as a municipal corporation pursuant to the laws of the state of Washington. As organized, the Hospital is exempt from federal income tax. The Hospital Board of Commissioners is comprised of five community members elected by local voters to six-year terms. The Hospital is not considered to be a component unit of the County. The Hospital is an acute-care community hospital with 43 licensed beds that provides services for Anacortes and surrounding communities. Island Hospital Medical Properties is a Washington nonprofit corporation organized and operated for the exclusive purpose within the meaning of Internal Revenue Code 501(c)(2) to hold title to property in support of its sole member, Skagit County Public Hospital District No. 2. The application for acquiring the 501(c)(2) status was accepted by the Internal Revenue Service (IRS) in June 2012. Island Hospital Medical Properties is a blended component unit of the Hospital, and activity related to Island Hospital Medical Properties is reflected in the financial statements. The Hospital operates four primary care clinics: Anacortes Family Medicine, Lopez Island Medical Center, Fidalgo Medical Associates at Island Hospital, and Orcas Medical Clinic. The Hospital leases the clinic facilities for Lopez Island Medical Center through a management contract with the Catherine Washburn Memorial Association, the facilities for Fidalgo Medical Associates from Challenge Developments, and the facilities for Orcas Medical Clinic from the Orcas Medical Foundation. Total clinic revenue represented approximately 14 percent of the Hospital’s net patient service revenues in 2014 and 2013. Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements. Estimates also affect the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Basis of Presentation

The accompanying financial statements have been presented in conformity with accounting principles generally accepted in the United States of America (“generally accepted accounting principles”) in accordance with the American Institute of Certified Public Accountants’ audit and accounting guide, Health Care Entities, and other pronouncements applicable to health care organizations and guidance from the Governmental Accounting Standards Board (GASB), where applicable. The basic financial statements include all of the accounts of Skagit County Public Hospital District No. 2 and Island Hospital Medical Properties. Intercompany accounts and transactions have been eliminated in consolidation.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(17)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Basis of Presentation (Continued)

The Hospital’s statements are reported using the economic resources measurement focus and the accrual basis of accounting. Revenue is recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Property taxes are recognized as revenue in the year for which they are levied. Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by the provider have been met. Cash and Cash Equivalents

For purposes of the statements of cash flows, cash and cash equivalents include investments in highly liquid debt instruments with an original maturity of three months or less. Patient Accounts Receivable, Net

The Hospital provides an allowance for uncollectible self-pay and miscellaneous commercial insurance accounts. Patients are not required to provide collateral for services rendered. Payment for services is required upon receipt of an invoice, after payment by insurance, if any. Self-pay accounts are analyzed for collectibility based on the months past due and payment history. An allowance is estimated for these accounts based on the historical experience of the Hospital. Accounts that are determined to be uncollectible are sent to a collection agency and written off at that time. Inventories

Inventories consist of medical, surgical, and pharmaceutical supplies, and are stated at the lower of cost (last-in, first-out) or market. Investments

Investments in debt and equity securities are reported at fair value except for short-term highly liquid investments that have a remaining maturity at the time they are purchased of one year or less. These investments are carried at amortized cost. Interest, dividends, and gains and losses, both realized and unrealized, on investments in debt and equity securities are included in nonoperating revenues when earned. Noncurrent Cash and Investments

Noncurrent cash and investments include assets set aside for future capital improvements or other designated uses over which the Board of Commissioners retains control, and assets restricted by donors or by bond agreements for capital improvements or debt service.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(18)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Capital Assets

The Hospital’s capital assets are stated at cost. Donated capital assets are recorded as capital contributions at fair value at the date of donation. Expenditures for maintenance and repairs are charged to operations as incurred; betterments and major renewals are capitalized. When assets are disposed, the related costs and accumulated depreciation or amortization are removed from the accounts and the resulting gain or loss is classified in nonoperating revenues or expenses. All capital assets, other than land and art, are being depreciated or amortized (in the case of capital leases), by the straight-line method of depreciation using these asset lives:

Land Improvements 15 to 20 Years Buildings and Leasehold Improvements 13 to 60 Years Equipment 3 to 20 Years

Intangible Assets

Intangible assets include goodwill and restrictive covenants related to the purchase of the Island Radiology practice in January 2004, the purchase of Fidalgo Medical Associates in 2008, and the purchase of Island Surgeons in 2009. Goodwill is reviewed annually for impairment. Goodwill is $598,703 as of December 31, 2014 and 2013. The value of the restrictive covenants had been fully amortized in prior fiscal years. Investment in Joint Venture

The Hospital has an investment in Medical Information Network-North Sound (MIN-NS) to develop, implement, and maintain an electronic health record system for health care providers in Skagit County. The Hospital has a one-half interest in this joint venture. The interest is accounted for using the equity method of accounting. Payments to MIN-NS for future services are recorded as prepaid assets and as of December 31, 2014 and 2013, there were no such balances. The operations of MIN-NS have resulted in a loss in joint venture of $626,145 and $450,845 for the years ended December 31, 2014 and 2013, respectively, and an investment of $-0-. Deferred Outflows of Resources

In addition to assets, the statement of net position will sometimes report a separate section for deferred outflows of resources. This separate financial statement element, deferred outflows of resources, represents a consumption of net position that applies to future periods and so will not be recognized as an outflow of resources (expense) until then. The Hospital only has one item that qualifies for reporting in this category. It is the loss on refunding of long-term debt in the statement of net position. A loss on refunding of long-term debt results from the difference in the carrying value of refunded debt and its reacquisition price. This amount is deferred and amortized over the shorter of the life of the refunded or refunding debt. Compensated Absences

The Hospital’s employees earn paid time off for vacation, holidays, and short-term illnesses, at varying rates depending on years of service. The related liability is accrued during the period in which it is earned.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(19)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Tax Levy

The Hospital received approximately 3.7 and 3.8 percent of its financial support from property taxes in 2014 and 2013, respectively. These funds were available for the following:

2014 2013Operations 151,666$ 91,213$ Debt Service 2,989,798 3,000,770

Total 3,141,464$ 3,091,983$

Property taxes are levied by the County on the Hospital’s behalf on January 1 and are intended to finance the Hospital’s activities of the same calendar year. Amounts levied are based on assessed property values as of the preceding May 31. The state assessed value base of the taxing district of approximately $4.7 billion with a maximum levy rate of 0.1876 and 0.1820 per $1,000 assessed value for the years ended December 31, 2014 and 2013, respectively. The property tax calendar includes these dates:

Levy Date January 1 Lien Date January 1 Tax Bill Mailed February 14 First Installment Payment Due April 30 Second Installment Payment Due October 31

Property taxes are considered delinquent on the day following each payment due date and interest must be paid on delinquent taxes. No allowance for uncollectible taxes receivable was considered necessary at the statement of net position dates. Property Taxes

The Hospital is permitted to levy an annual expense fund levy upon the taxable property within the district without a vote of the taxpayers. In addition, taxes are levied annually upon the taxable property within the district to service bond principal and interest payments on the 2012, 2004 and 1996 Unlimited Tax General Obligation (UTGO) Bonds. Taxes to finance debt service on these bonds may be levied without limit as to rate and amount. The Hospital records property taxes on the accrual method. Grants and Contributions

From time to time, the Hospital receives grants from Skagit County and the state of Washington, as well as contributions from individuals and private organizations. Revenues from grants and contributions may be restricted for either specific operating purposes or for capital purposes. Amounts that are unrestricted or that are restricted for a specific operating purpose are reported as nonoperating revenues. Amounts restricted for capital acquisitions are reported after nonoperating revenues and expenses.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(20)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Net Position

The net position of the Hospital is classified in three components. Net position invested in capital assets net of related debt consists of capital assets net of accumulated depreciation and amortization and reduced by the current balances of any outstanding borrowings used to finance the purchase or construction of those assets. Restricted net position (expendable and nonexpendable) consists of noncapital assets that must be used for a particular purpose as specified by creditors, grantors, or contributors external to the Hospital. Unrestricted net position is the remaining net position that does not meet the definition of invested in capital assets net of related debt or restricted. When both restricted and unrestricted resources are available for use, it is the Hospital’s policy to use restricted resources first, and then unrestricted resources as they are needed. Operating Revenues and Expenses

The Hospital’s statements of revenues, expenses, and changes in net position distinguish between operating and nonoperating revenues and expenses. Operating revenues result from exchange transactions associated with providing health care services – the Hospital’s principal activity. Exchange transactions are those in which each party to the transaction receives and gives essentially equal values. Nonexchange revenues, including taxes, grants, and contributions received for purposes other than capital asset acquisition, are reported as nonoperating revenues. Operating expenses are all expenses incurred to provide health care services, other than financing costs. Net Patient Service Revenue

Such revenue is reported at the estimated net realizable amounts from patients, third-party payers, and others for services rendered, including estimated retroactive adjustments under reimbursement agreements with third-party payers. Retroactive adjustments are accrued on an estimated basis in the period the related services are rendered and adjusted in future periods as final settlements are determined. Charity Care

The Hospital provides care to patients who meet certain criteria under its charity care policies without charge or at amounts less than its established rates. Because the Hospital does not pursue collection of amounts determined to qualify as charity care, they are not reported as net patient service revenue. Foregone revenue for charity care provided during fiscal years 2014 and 2013, measured by the Hospital’s standard charges, was $802,119 and $1,597,245, respectively.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(21)

NOTE 2 DEPOSITS AND INVESTMENTS

The Revised Code of Washington (RCW), Chapter 39, authorizes municipal governments to invest their funds in a variety of investments including federal, state, and local government certificates, notes, or bonds; the State of Washington Local Government Investment Pool; savings accounts in qualified public depositories; and certain other investments. State law requires collateralization of all deposits with federal depository insurance or other acceptable collateral. The Hospital’s cash on deposit with banks is insured through the Federal Deposit Insurance Corporation up to $250,000 per financial institution. Cash on deposit with the Washington State Local Government Investment Pool and with qualified public depositaries is protected against loss by the state of Washington Public Deposit Protection Commission, as provided for by RCW 39.58, subject to certain limitations. The Skagit County Treasurer acts as the treasurer for certain deposits and investments of the Hospital. Deposits that are not covered by depository insurance are collateralized in the name of the County, and uninsured investments are registered in the name of the County. Cash and cash equivalents consisted of the following at December 31:

2014 2013Cash on Hand 3,800$ 3,210$ Bank of America, Payroll Account 3,157 16,247 Washington Federal Bank, Depository Accounts 529,632 1,688,856 Skagit County Treasurer's Office 1,375,221 242,801 Washington State Local Government Investment Pool 20,538,342 14,191,037

Bank Balances 22,450,152 16,142,151 Reconciling Items 19,426 (2,244)

Total Cash and Cash Equivalents per Statements of Net Position 22,469,578$ 16,139,907$

Noncurrent cash and investments consisted of the following at December 31:

2014 2013Internally Designated by the Board for Future

Capital Improvements:Cash and Cash Equivalents 168,646$ 118,805$ Accrued Interest 2,404 2,047 Washington State Local Government Investment Pool 2,708,860 3,397,598

Total 2,879,910 3,518,450

Restricted, Proceeds of 2004 Unlimited Tax GeneralObligation and 2005 Limited Tax General ObligationIssues to be Used for Capital Improvements:

Cash and Cash Equivalents 36,178 22,093 Washington State Local Government Investment Pool 245,379 226,030

Total 281,557 248,123

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(22)

NOTE 2 DEPOSITS AND INVESTMENTS (CONTINUED)

2014 2013Restricted, for the Repayment of 1996 Unlimited Tax

General Obligation Refunding Bonds:Cash and Cash Equivalents -$ 4,530$ Washington State Local Government Investment Pool - 62,188

Total - 66,718

Restricted, for the Repayment of 2005 Limited TaxGeneral Obligation Refunding Bonds:

Cash and Cash Equivalents 14,260 10,597 Washington State Local Government Investment Pool 641,411 440,780

Total 655,671 451,377

Restricted, Proceeds of 2014 Limited Tax GeneralObligation Issues to be Used for Capital Improvements:

Washington State Local Government Investment Pool 2,623,140 -

Restricted for the Repayment of New Market Tax Credit Loans:

Cash and Cash Equivalents 1,708,934 1,421,290

Restricted, under Deferred Compensation Arrangements:Investments in Mutual Funds 286,966 226,477

Total Asset Limited as to Use 8,436,178 5,932,435 Less: Current Portion 152,244 256,056

Assets Limited as to Use, Less Current Portion 8,283,934$ 5,676,379$

Cash and cash equivalents included in noncurrent cash and investments are not considered cash and cash equivalents for purposes of presenting cash flows.

NOTE 3 ACCOUNTS RECEIVABLE

The Hospital has a concentration of credit risk with respect to unsecured patient accounts receivable. The majority of the Hospital’s patients are local residents and are insured under third-party payer agreements. Patient accounts receivable at December 31 consisted of the following:

2014 2013Receivable from Patients and Their Insurance Carriers 4,767,196$ 5,577,872$ Receivable from Medicare 2,834,506 4,085,220 Receivable from Medicaid 1,020,597 1,001,175

Total Patient Accounts Receivable 8,622,299 10,664,267Less: Allowance for Doubtful Accounts 583,450 496,096

Patient Accounts Receivable, Net 8,038,849$ 10,168,171$

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(23)

NOTE 4 CAPITAL ASSETS

Capital asset additions, retirements, and balances for the years ended December 31, 2014 and 2013 were as follows:

Balance BalanceDecember 31, December 31,

2013 Additions Transfers Retirements 2014Land 4,708,577$ -$ -$ -$ 4,708,577$ Art 293,781 6,934 - - 300,715 Land Improvements 2,121,761 - - - 2,121,761 Buildings and Leasehold

Improvements 68,769,108 500 658,693 - 69,428,301 Fixed Equipment 8,234,832 - - (18,782) 8,216,050 Major Moveable Equipment 25,922,904 1,267,721 192,286 (577,702) 26,805,209 Construction in Progress 329,170 1,082,723 (850,979) - 560,914

Total Historical Cost 110,380,133 2,357,878 - (596,484) 112,141,527

Less: Accumulated Depreciation:Land Improvements (1,204,551) (98,168) - - (1,302,719) Buildings and Leasehold

Improvements (17,414,996) (1,516,567) - - (18,931,563) Fixed Equipment (5,148,923) (414,246) - 18,782 (5,544,387) Major Moveable Equipment (19,589,845) (2,052,437) - 556,118 (21,086,164)

Total Accumulated Depreciation (43,358,315) (4,081,418) - 574,900 (46,864,833)

Total Capital Assets, Net 67,021,818$ (1,723,540)$ -$ (21,584)$ 65,276,694$

Balance BalanceDecember 31, December 31,

2012 Additions Transfers Retirements 2013Land 4,208,953$ 499,624$ -$ -$ 4,708,577$ Art 278,939 14,842 - - 293,781 Land Improvements 2,116,330 5,431 - - 2,121,761 Buildings and Leasehold

Improvements 68,351,476 266,623 151,009 - 68,769,108 Fixed Equipment 8,224,258 - 27,470 (16,896) 8,234,832 Major Moveable Equipment 24,879,616 1,225,320 2,318 (184,350) 25,922,904 Construction in Progress 64,185 445,782 (180,797) - 329,170

Total Historical Cost 108,123,757 2,457,622 - (201,246) 110,380,133

Less: Accumulated Depreciation:Land Improvements (1,103,232) (101,319) - - (1,204,551) Buildings and Leasehold

Improvements (15,872,135) (1,542,861) - - (17,414,996) Fixed Equipment (4,727,411) (438,408) - 16,896 (5,148,923) Major Moveable Equipment (17,648,388) (2,100,761) - 159,304 (19,589,845)

Total Accumulated Depreciation (39,351,166) (4,183,349) - 176,200 (43,358,315)

Total Capital Assets, Net 68,772,591$ (1,725,727)$ -$ (25,046)$ 67,021,818$

Construction in progress consists of various small improvement projects within the Hospital.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(24)

NOTE 5 LONG-TERM DEBT AND OTHER NONCURRENT LIABILITIES

Changes in the Hospital’s noncurrent liabilities for the years ended December 31, 2014 and 2013 are as follows:

Balance BalanceDecember 31, December 31, Amounts Due

2013 Additions Reductions 2014 Within 1 YearLong-Term Debt:

2004 UTGO Bonds $ 975,000 $ - $ (975,000) $ - $ - 2005 LTGO Bonds 9,190,000 - (9,190,000) - - 2011 Revenue Bond 436,728 - (258,732) 177,996 177,996 2012 Refunding UTGO Bonds 26,045,000 - (65,000) 25,980,000 1,130,000 2014 Refunding LTGO Bonds - 12,090,000 (320,000) 11,770,000 380,000 NDC CDE Loan A 5,373,200 - - 5,373,200 - NDC CDE Loan B 1,770,800 - - 1,770,800 - Kitsap CDE Loan C 2,121,000 - - 2,121,000 - Kitsap CDE Loan D 729,000 - - 729,000 - Capital Leases 434,297 - (255,286) 179,011 153,447

Subtotal 47,075,025 12,090,000 (11,064,018) 48,101,007 1,841,443

Unamortized Premiums 3,341,211 752,738 (423,941) 3,670,008 - Total Long-Term Debt 50,416,236 12,842,738 (11,487,959) 51,771,015 1,841,443

Other Noncurrent Payables:Deferred Compensation 267,480 54,885 (26,890) 295,475 - Professional Liability Claims 542,857 - (64,655) 478,202 -

Total Other Noncurrent Payables 810,337 54,885 (91,545) 773,677 -

Total Noncurrent Liabilities 51,226,573$ 12,897,623$ (11,579,504)$ 52,544,692$ 1,841,443$

Balance BalanceDecember 31, December 31, Amounts Due

2012 Additions Reductions 2013 Within 1 YearLong-Term Debt:

2004 UTGO Bonds $ 1,865,000 $ - $ (890,000) $ 975,000 $ 975,000 2005 LTGO Bonds 9,485,000 - (295,000) 9,190,000 320,000 2011 Revenue Bond 684,713 - (247,985) 436,728 258,732 2012 Refunding UTGO Bonds 26,110,000 - (65,000) 26,045,000 65,000 NDC CDE Loan A 5,373,200 - - 5,373,200 - NDC CDE Loan B 1,770,800 - - 1,770,800 - Kitsap CDE Loan C 2,121,000 - - 2,121,000 - Kitsap CDE Loan D 729,000 - - 729,000 - Capital Leases 677,709 - (243,412) 434,297 255,286

Subtotal 48,816,422 - (1,741,397) 47,075,025 1,874,018

Unamortized Premiums 3,749,602 - (408,391) 3,341,211 - Total Long-Term Debt 52,566,024 - (2,149,788) 50,416,236 1,874,018

Other Noncurrent Payables:Deferred Compensation 340,104 118,696 (191,320) 267,480 - Professional Liability Claims 495,774 96,936 - 542,857 -

Total Other Noncurrent Payables 835,878 215,632 (191,320) 810,337 -

Total Noncurrent Liabilities 53,401,902$ 215,632$ (2,341,108)$ 51,226,573$ 1,874,018$

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(25)

NOTE 5 LONG-TERM DEBT AND OTHER NONCURRENT LIABILITIES (CONTINUED)

Long-Term Debt

The terms and due dates of the Hospital’s long-term debt at December 31, 2014 and 2013 follows:

Unlimited tax general obligation bonds of $30,500,000, dated October 15, 2004, were issued to pay for a portion of the costs of a $40,000,000 project to remodel and expand the Hospital’s emergency room; construct, furnish, and equip new flexible-use inpatient rooms; relocate and expand the Hospital’s ancillary services such as radiology and laboratory; and make other related capital improvements. The unlimited tax general obligation bonds dated September 26, 2012 were issued to advance refund $26,730,000 of the 2004 unlimited tax general obligation bonds. As of September 26, 2012, $2,680,000 of the 2004 unlimited tax general obligation bonds remained. The remaining bonds were paid off in 2014. As part of the advance refunding issued on September 26, 2012, a loss on refunding was incurred, considering the refunding of the 2004 bonds, actual cash received as part of the issuance, and unamortized premiums and issuance costs related to the 2004 and 2012 bonds. The loss on refunding of $2,070,898 is amortized using the effective interest rate method through 2028. The recorded balance of the 2004 bonds at December 31, 2014 and 2013 also includes an unamortized bond premium of $-0- and $64,338, respectively.

Limited tax general obligation bonds of $10,995,000, dated November 15, 2005, were issued to pay for a portion of the costs of expanding the Hospital’s facilities and to advance refund the 1996 limited tax general obligation bonds. A portion of the bond proceeds ($3,322,736) was transferred to Bank of New York to be held in escrow to pay the remaining principal balance and accrued interest related to the 1996 limited tax general obligation bonds on January 2, 2006. The recorded balance at December 31, 2014 and 2013, includes an unamortized bond premium of $-0- and $32,425, respectively. The limited tax general obligation bonds dated November 11, 2014 were issued to advance refund all of the 2005 limited tax general obligation bonds. As part of the advance refunding issued on November 11, 2014, a loss on refunding was incurred, considering the refunding of the 2005 bonds, actual cash received as part of the issuance, and unamortized premiums and issuance costs related to the 2005 and 2014 bonds. The loss on refunding of $393,417 is amortized using the effective interest rate method through 2033.

The Hospital issued a revenue bond dated August 22, 2011, for the purpose of financing the payoff of the Whidbey Island revenue bond. The bond is payable over a four-year period, in monthly payments of $22,691 commencing September 1, 2011, including interest at 4.2 percent, to Washington Federal bank, the bondholder.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(26)

NOTE 5 LONG-TERM DEBT AND OTHER NONCURRENT LIABILITIES (CONTINUED)

Long-Term Debt (Continued)

Unlimited tax general obligation bonds of $26,550,000, dated September 26, 2012, were issued to advance refund and in substance defease the principal amounts totaling $26,730,000 of the 2004 unlimited tax general obligation bonds. Interest is payable semiannually on June 1 and December 1, beginning December 1, 2012, at rates that range from 2 percent to 5 percent. The bonds mature in principal installments ranging from $440,000 in 2012 to $2,850,000 in 2028. Scheduled maturities on and after December 1, 2023, will be subject to redemption at the option of the Hospital on and after December 1, 2023, in whole or in part, at par plus accrued interest to the date of redemption. The recorded balance at December 31, 2012, includes an unamortized bond premium of $3,585,459. The Hospital irrevocably pledged to levy and collect taxes annually in sufficient amounts to pay the bond principal and interest payments when due. Such collections are reported as noncurrent cash and investments. The recorded balances at December 31, 2014 and 2013 include a bond premium of $2,920,407 and $3,247,553, respectively, which is being amortized using the effective interest method over the term of the bonds.

Limited tax general obligation bonds of $12,090,000, dated November 11, 2014, were issued to advance refund and in substance defease the principal amounts totaling, $9,190,000 of the 2005 limited tax general obligation bonds plus additional funds. Interest is payable semiannually on June 1 and December 1, beginning December 1, 2014, at rates that range from 2 percent to 5 percent. The bonds mature in principal installments ranging from $320,000 in 2014 to $2,695,000 in 2033. Scheduled maturities on and after December 1, 2023, will be subject to redemption at the option of the Hospital on and after December 1, 2023, in whole or in part, at par plus accrued interest to the date of redemption. The recorded balance at December 31, 2014, includes an unamortized bond premium of $749,601. The Hospital irrevocably pledged to levy and collect taxes annually in sufficient amounts to pay the bond principal and interest payments when due. Such collections are reported as noncurrent cash and investments. The recorded balance at December 31, 2014 includes a bond premium of $749,901 which will be amortized over the term of the bonds.

In August 2011, Island Hospital Medical Properties, a Washington nonprofit corporation of which the Hospital is the sole member, secured financing utilizing the New Market Tax Credit program. Washington Federal bank is the tax credit investor with NDC New Markets Investment LXIII, LLC and Kitsap County NMTC Subsidiary Allocatee Three, LLC. Interest only payments commenced September 1, 2011, at an interest rate of 4.829 percent and will continue for seven years.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(27)

NOTE 5 LONG-TERM DEBT AND OTHER NONCURRENT LIABILITIES (CONTINUED)

Long-Term Debt (Continued)

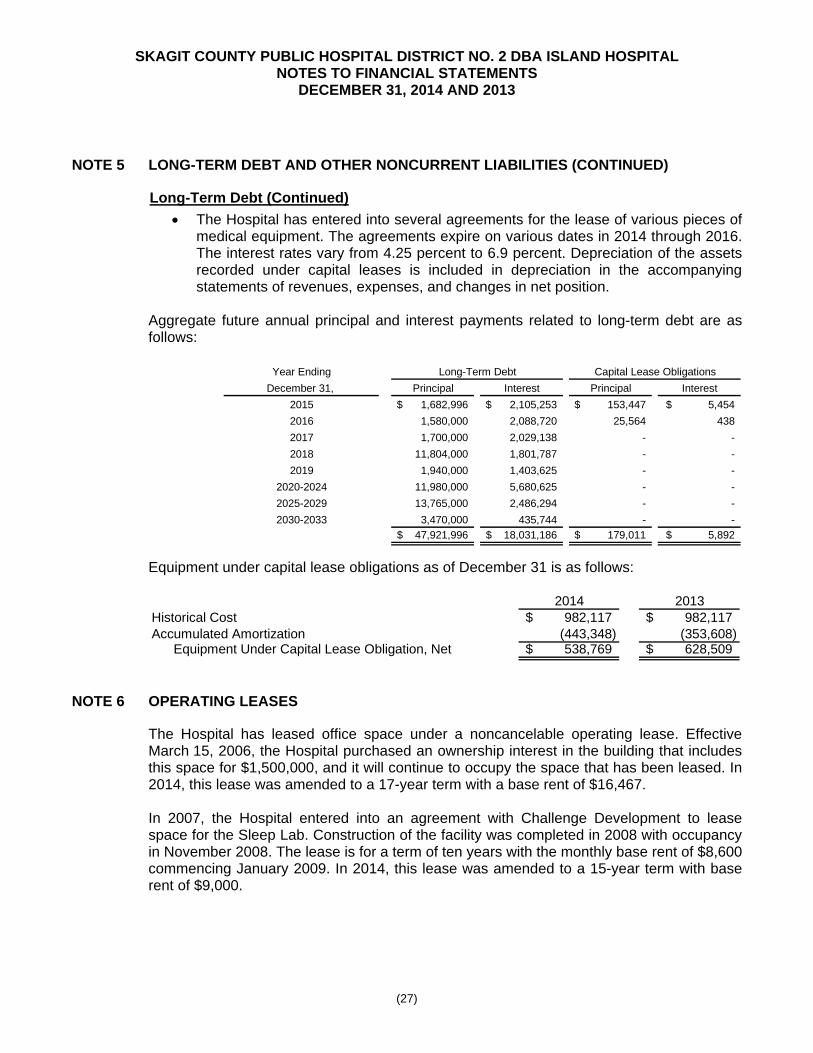

The Hospital has entered into several agreements for the lease of various pieces of medical equipment. The agreements expire on various dates in 2014 through 2016. The interest rates vary from 4.25 percent to 6.9 percent. Depreciation of the assets recorded under capital leases is included in depreciation in the accompanying statements of revenues, expenses, and changes in net position.

Aggregate future annual principal and interest payments related to long-term debt are as follows:

Year Ending

December 31, Principal Interest Principal Interest

2015 1,682,996$ 2,105,253$ 153,447$ 5,454$

2016 1,580,000 2,088,720 25,564 438

2017 1,700,000 2,029,138 - -

2018 11,804,000 1,801,787 - -

2019 1,940,000 1,403,625 - -

2020-2024 11,980,000 5,680,625 - -

2025-2029 13,765,000 2,486,294 - -

2030-2033 3,470,000 435,744 - -

47,921,996$ 18,031,186$ 179,011$ 5,892$

Capital Lease ObligationsLong-Term Debt

Equipment under capital lease obligations as of December 31 is as follows:

2014 2013Historical Cost 982,117$ 982,117$ Accumulated Amortization (443,348) (353,608)

Equipment Under Capital Lease Obligation, Net 538,769$ 628,509$

NOTE 6 OPERATING LEASES

The Hospital has leased office space under a noncancelable operating lease. Effective March 15, 2006, the Hospital purchased an ownership interest in the building that includes this space for $1,500,000, and it will continue to occupy the space that has been leased. In 2014, this lease was amended to a 17-year term with a base rent of $16,467. In 2007, the Hospital entered into an agreement with Challenge Development to lease space for the Sleep Lab. Construction of the facility was completed in 2008 with occupancy in November 2008. The lease is for a term of ten years with the monthly base rent of $8,600 commencing January 2009. In 2014, this lease was amended to a 15-year term with base rent of $9,000.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(28)

NOTE 6 OPERATING LEASES (CONTINUED)

The following is a schedule of future minimum operating lease payments as of December 31, 2014:

Year Ending December 31, Amount2015 557,997$ 2016 557,997 2017 557,997 2018 557,997 2019 557,997 Total 2,789,987$

NOTE 7 NET PATIENT SERVICE REVENUE

The Hospital has agreements with third-party payers that provide for payments at amounts different from its established rates. A summary of the payment arrangements with major third-party payers follows: Medicare

Inpatient and outpatient acute care services provided to Medicare program beneficiaries are paid at prospectively determined rates. These rates vary according to a patient classification system that is based on clinical, diagnostic, and other factors. The Hospital’s classification of patients under the Medicare program and the appropriateness of their admission are subject to an independent review by a peer review organization under contract with the Hospital. Medicaid

Medicaid reimbursement for most outpatient hospital and clinic services is prospectively set based on the ratio of estimated aggregate costs to aggregate charges. Certain outpatient services and physician services are reimbursed based on predetermined fee schedules. Other

The Hospital has entered into payment agreements with certain commercial insurance carriers and preferred provider organizations. The basis for payment to the Hospital under these agreements includes prospectively determined rates per discharge, discounts from established charges, and prospectively determined daily rates. The Hospital has settled its Medicare cost reports through December 31, 2011. Third-party settlements are accrued on an estimated basis in the period the services are rendered and adjusted in future periods, as final settlements are received. At December 31, 2014, net patient service revenue increased by approximately $100,000, due to removal of allowances previously estimated that are no longer considered necessary as a result of change in estimates or final settlements and years that are no longer subject to audits, reviews, and investigations.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(29)

NOTE 7 NET PATIENT SERVICE REVENUE (CONTINUED)

Other (Continued)

Net patient service revenue for the years ending December 31 consisted of the following:

2014 2013Gross Patient Service Revenue 199,444,414$ 191,011,133$ Less: Charity Care 802,119 1,597,245

Total 198,642,295 189,413,888 Contractual Adjustments:

Medicare 63,920,280 58,118,798 Medicaid 16,009,295 10,987,619 Other 33,849,265 37,093,486

Total Adjustments 113,778,840 106,199,903 Provision for Bad Debts 2,503,807 3,934,574

Net Patient Service Revenue 82,359,648$ 79,279,411$

NOTE 8 ELECTRONIC HEALTH RECORD INCENTIVE PROGRAM

The Electronic Health Record (EHR) incentive program was enacted as part of the American Recovery and Reinvestment Act of 2009 (ARRA) and the Health Information Technology for Economic and Clinical Health (HITECH) Act. These acts provided for incentive payments under both the Medicare and Medicaid programs to eligible health care organizations that demonstrate meaningful use of certified EHR technology. The incentive payments are made based on a statutory formula and are contingent on the Hospital continuing to meet the escalating meaningful use criteria. Under the program, the District received incentive payments of approximately $639,000 for Medicare and $378,000 for Medicaid for the year ended December 31, 2014. The District received incentive payments of approximately $1,052,000 for Medicare and $210,000 for Medicaid for the year ended December 31, 2013. The revenue has been recognized for incentive payments received as other operating revenue in the statements of revenues, expenses, and changes in net position.

NOTE 9 RETIREMENT PLAN AND DEFERRED COMPENSATION

The Hospital sponsors a qualified retirement plan under IRS Code Section 403(b)(7) which is available to employees who have attained the age of 21 and have completed 18 months of service. For eligible employees who defer at least 5 percent of their compensation, the Hospital makes contributions at rates ranging from 6.1 percent to 6.5 percent. Related Hospital contributions for the years ended December 31, 2014 and 2013 were $1,485,692 and $1,531,503, respectively.

SKAGIT COUNTY PUBLIC HOSPITAL DISTRICT NO. 2 DBA ISLAND HOSPITAL NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2014 AND 2013

(30)

NOTE 9 RETIREMENT PLAN AND DEFERRED COMPENSATION (CONTINUED)

The Hospital sponsors a Supplemental Executive Retirement Plan (SERP), which is a nonqualified defined contribution plan under IRS Code Section 403(f). Payments of accrued benefits are made based upon a vesting schedule for eligible employees. The accrued liabilities related to the SERP were $295,475 and $267,480 at December 31, 2014 and 2013, respectively.

NOTE 10 RISK MANAGEMENT

The Hospital is involved in litigation and regulatory investigations arising in the course of business. After consultation with legal counsel, management estimates that these matters will be resolved without material adverse effect on the Hospital’s future financial position or results of operations. The Hospital is exposed to various risks of loss related to torts; theft of, damage to, and destruction of assets; business interruption, errors, and omissions; injuries to employees; and natural disasters. The Hospital carries commercial insurance for these risks of loss. The Hospital has professional liability insurance coverage with Hudson Specialty Insurance Company and Physicians Insurance. The policies provide protection on a “claims-made” basis whereby only claims reported to the insurance carrier during the policy year are covered by the current policy. If there are unreported incidents that result in a claim, they will only be covered in the year the claim is reported to the insurance carrier if the Hospital purchases claims-made insurance in that year or if the Hospital purchases insurance coverage for “prior acts.” The Hospital’s present coverage is $1,000,000 per claim with an annual aggregate limit of $3,000,000, and is subject to an excess liability policy with the same carrier that has limits, per claim and annual aggregate, of $10,000,000. The Hospital records a liability for potential claims that may have been incurred but not reported in the current or prior years. As of December 31, 2014 and 2013, the Hospital recorded professional liabilities claims payable of $478,202 and $542,857, respectively. It is possible that claims may exceed coverage available in any given year.

![Safe Surgery 2015: South Carolina Presentation - Surgeons [ Insert Implementation Team Member Names] [ Insert Hospital Name] Insert Your Hospital’s Logo](https://img.pdfslide.us/doc/110x75/56649ec05503460f94bcbeea/safe-surgery-2015-south-carolina-presentation-surgeons-insert-implementation.jpg)

![Safe Surgery 2015: South Carolina Presentation [ Insert Implementation Team Member Names] [ Insert Hospital Name] Insert Your Hospital’s Logo Here](https://img.pdfslide.us/doc/110x75/56649dc45503460f94ab7476/safe-surgery-2015-south-carolina-presentation-insert-implementation-team.jpg)