Embed Size (px)

Citation preview

www.MarshBerry.com

SITTING ON THE INSURTECH SIDELINES

Why are agents and brokers refraining from InsurTech investments while venture capitalists and carriers pile on? Page 2

N O V E M B E R 2 0 1 7

ADDING VALUE for Clients

Page 4

The Beat GOES ON

Page 8

The Role of Technology for the SPECIALTY

DISTRIBUTORPage 10

Will Your Agency BE DISRUPTED?

Page 12

MARSHBERRYlearn. improve. realize.

800.426.2774 MarshBerry.com

Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 (440.354.3230).

Marsh, Berry & Company, Inc. is honored to be the investment banking firm that brokered the transactions that brought these 24 agencies and one networking organization together to form Alera Group1, as funded by Genstar Capital.

HAS ACQUIRED A&B Insurance and

Financial, Inc., AB Capital Group, LLC, Insurance

Exchange, LLC, & Smart Choice Health Plans, LLC

dba Florida Health Team, LLC

HAS ACQUIRED C.M. Smith

Agency, Inc.

HAS ACQUIRED Coury Health Services, Inc.

HAS ACQUIRED Hampson

Mowrer Agency, Inc. dba Hampson

Mowrer Kreitz Agency

HAS ACQUIRED K.B. Group

Services, Inc. dba Group

Services, Inc.

HAS ACQUIRED Shirazi Benefits,

LLC

HAS ACQUIRED American Insurance

Administrators, Inc. dba AIA

Benefits Resource Group

HAS ACQUIRED Centennial Group

Benefits and Insurance

Services, Inc.

HAS ACQUIRED Forum

Benefits, Inc.

HAS ACQUIRED HP Planning, LLC (dba CBP and/or Creative Benefit

Planning)

HAS ACQUIRED

Pentra, Inc.

HAS ACQUIRED Shirazi-Miller Benefits, LLC

HAS ACQUIRED Benefit Advisors

Network, LLCdba BAN

HAS ACQUIRED Beacon Retiree Benefits Group,

LLC

HAS ACQUIRED

MFG Retirement Systems, Inc. dba

PWA Insurance Services

HAS ACQUIRED TRUEBenefits,

LLC

HAS ACQUIRED

Benico, Ltd.

HAS ACQUIRED INGROUP

Associates, Inc.

HAS ACQUIRED Robert G. Relph Agency, Inc. (dba

Relph Benefit Advisors) & Flexible

Benefits System, Inc.

HAS ACQUIRED Virtus Benefits,

LLC

HAS ACQUIRED

Brown & Noyes, LLC dba Ardent Solutions

HAS ACQUIRED Corporate Plans, Inc. dba CPI-HR

HAS ACQUIRED GCG Financial,

Inc.

HAS ACQUIRED J.A. Counter &

Associates, Inc.

HAS ACQUIRED Silberstein

Insurance Group, LLC

1 Marsh, Berry & Company, Inc. was financial adviser to the participating selling organizations. These organizations were acquired by Alera Group effective December 30, 2016.

1CounterPoint November 2017

CONTRIBUTING AUTHORSGEORGE BUCUR, Vice President

JAMES GRAHAM, Senior Consultant

JONATHAN HULL, Financial Analyst

JACK MCDERMOTT, Data Analyst

CHAD MORGAN, Vice President

GERARD VECCHIO, Senior Vice President

COUNTERPOINT EDITORIAL BOARDMEGAN BOSMA, Senior Vice President

LAUREN BYERS, Vice President, Marketing

ALISON WOLF, Director, Research

ABOUT COUNTERPOINTCounterPoint is the proprietary publication of MarshBerry. The magazine offers eleven editions annually and is published for independent insurance agents and brokers, national brokers, private equity firms, banks, credit unions, insurance carriers and specialty distributors.

NO

VEM

BER

SPO

TL

IGH

T Disruption is making its way to the Insurance IndustryAcross industries, disruptions are shifting existing business models from product-focused to consumer-focused and we’re starting to see the impact on the insurance industry.

Fueled by societal and demographic changes accompanied by technological developments, the accessibility and leveraging of “big data” is becoming more prominent from existing competitors and creating opportunities for new and more innovative participants to enter the industry. The Internet of Things, blockchain infrastructure, and mobile applications are generating additional streams of data accessible to external parties that were once exclusive to insurance companies.

Everyday activities are now becoming streamlined and are not only shifting the way individuals interact with peers, but also how consumers evaluate purchases and conduct business.

COMPARED TO PRIOR PERIODS, DATA HAS NEVER BEEN MORE ACCESSIBLE THAN IT IS RIGHT NOW. Moreover, these capabilities are expanding. With an increase of user-friendly services, consumer expectations are continuing to rise as well as their demand for personalized products. The one-size fits all model is becoming a thing of the past. For the most part, the insurance industry over the years has experienced little change to its fundamental operations; however, it is unlikely that it will be able to continue with this “same old” mentality that historically has stifled innovation.

With change comes opportunity. As the consumer changes its habits, new risks will emerge. As InsurTech companies are either used as third parties or acquisition targets to enhance insurance companies’ operational capabilities and shift product offerings to more customer-focused, it is a logical progression that innovation makes its way to distribution.

Ease of use, transparency, and a positive experience could potentially become standard terms used by consumers purchasing insurance; leaving the unanswered question, what are firms doing to remain relevant in the evolving marketplace? n

NO

VEM

BER

FE

AT

UR

E

2 November 2017 CounterPoint

by Gerard Vecchio, Senior Vice President212.972.4886 | [email protected]

SITTING ON THE INSURTECH SIDELINES

Until recently, the insurance industry ran predominantly product-centric businesses. Carriers developed insurance

products that could be sold to large swaths of consumers and businesses. Insurance brokers took those same products and

educated their clients on which policies might best fit their needs. If a consumer or business suffered an insurable

loss, then a generic one-size-fits-most claims process was instituted to partly or fully remunerate the client.

Securities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

3CounterPoint November 2017

A CUSTOMER-CENTRIC MODEL EMERGES… ENTER THE INSURTECH INDUSTRY.InsurTech does insurance differently — changing the game with ultra-tailored policies, social consciousness components, and predictive analytics tools that segments insurance buyers by risk profile.

Taking a consumer-centric approach, InsurTech companies are putting customer preferences for researching insurance coverages, binding a policy, and filing an insurance claim ahead of the industry’s traditional product-centric model.

As one of the oldest industries, insurance firms tend to act like the grandfather, looking at new competitors with a discerning eye. Some believe that InsurTech is proving that change can not only be good, but it is highly attractive to consumers and essential for future sustainability. Others are taking a wait and see approach, convinced that an InsurTech industry shake-out is on the horizon.

Yet, billions of dollars of investments have been flowing into InsurTech in recent years. According to MarshBerry’s 2017 InsurTech study1 (“2017 Study”), approximately $1 billion has been invested in digital insurance brokers, coverage providers for the sharing economy, and artificial intelligence. More investment has also been made in claims systems, policy issuance technology, and digital property inspection, to name a few.

Can this large influx of investment dollars fundamentally change the way the next generation of businesses and consumers buy insurance products and services? The next few pages will explore this question.

What Is InsurTech? InsurTech is the confluence of insurance and technology — relying upon technology to solve problems, to address client demands — and to do things different, better and cheaper.

Some within the industry are skeptical that using technology as a hybrid vehicle, without traditional insurance underwriting, claims and distribution, can materially change consumer behavior. However, with significant venture capital dollars backing InsurTech companies, can distributors afford to ignore their mantra of market disruption? After all, why

would prominent venture capitalists bother investing in a concept that is likely to fail?

InsurTech companies are highly specialized, data-driven, progressive, mobile and focused on the unique needs of customers in today’s culture. They’re using artificial intelligence (AI) and predictive analytics to determine risk. These companies are also using aggregators and comparison shopping tools. They are employing digital brokers and using telematics to collect data from vehicles and more. InsurTech companies are digitizing claims processing and improving the customer experience. They are taking the “old way” of providing insurance and looking at the new ways in which people live, work and connect. Just as FinTech firms recognize that people want to bank when, where and how they want, InsurTech companies are utilizing technology to meet customers where they are — wherever that is. This is why the industry is seeing InsurTech receiving significant capital from strategic investors.

Who are these investors? Highly respected insurers and reinsurers that comprise some of the insurance industry intelligencia — firms like ACE Limited, American Family Insurance, Allianz Life, AXA Insurance, CUNA Mutual Group, Liberty Mutual Insurance, Markel Corporation (“Markel”), MassMutual Life Insurance Company, Nationwide Mutual Insurance Company (“Nationwide”), Transamerica Life Insurance Company, United States Automobile Association (USAA), and XL Catlin.

But the question is, where are the insurance distributors? With InsurTech winning the confidence and capital of such key players, why is there not a single significant strategic partner from the insurance distribution space?

InsurTech Focus Areas —Specialized, Smart, and Socially Conscious Before we go into the big “why,” let us take a closer look at some of the larger InsurTech deals and the companies focused on distribution.

MarshBerry’s 2017 Study identified 47 predominantly distribution-related InsurTech companies that combined received approximately $1 billion over the past few years. That includes participation from strategic insurance investors

Securities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

ME

TR

IC

ADDING VALUE FOR CLIENTS With the relatively recent introduction of InsurTech, many agency’s within the industry are rethinking how they can provide their clients with the best products and services.

In the past, many consumers have had to settle for the one-size-fits-all product, however, InsurTech is changing that mindset and leaving consumers wanting options.

To provide a holistic view of agency spend on Equipment & Technology (E&T), MarshBerry includes the following expenses within E&T: T-Com, computers & maintenance, office machine leases, both internal and value-add software expenses, and IT consulting.

For the last twelve months (LTM) ended June of 2013, the average agency was investing 2.7% of their Net Revenue into E&T. As major insurance companies continue to invest in innovative tech companies, agencies began to invest in technology as well. Through LTM June of 2017, the average agency is now investing 3.65% of their Net Revenue into Technology. In dollars, the average agency has gone from investing $343k a year in 2014 to investing $580k in 2017.

This represents an increase of 14% per year, on average. To put that in perspective, total compensation as a percentage of net revenue has increased by an average of 7% during that same time period. n

OF THE MONTH

4 November 2017 CounterPoint

(totaling $350 million) and venture capitalist infusions that did not include insurance company investors (totaling $680 million).1 Those strategic investors identified believe in technology as an innovative disrupter in the insurance industry — one that can deliver value and a return on investment.

SMALL BUSINESS Some key InsurTech companies are focused on the small business space. For example, Next Insurance, Inc. uses data analytics to tailor products to the small business client — a consumer-centric model that speaks to those entrepreneurial customers that are value-driven. These customers are seeking new ways to access insurance products that are specifically tailored for their small businesses. This venture has received $48 million in funding placed with high-quality carriers including Nationwide, Markel and Munich Re1.

CoverWallet is a concierge service for small-to-mid-sized businesses that provides access to insurance quotes, advice and policy management tools. It is device agnostic — an omnichannel experience that is accessible via email, mobile, video and online chat. With approximately $8 million in funding, this InsurTech company is feeding customers’ desire for information when, where and how they want it1.

PolicyGenius analyzes existing insurance policies and points out coverage gaps for its clients. Again, there is a customer-

centric theme — problem-solving via technology. With $30 million in investments backing the company, investors are betting that their analytic tools can bring value and a better service model to customers.1

CoverHound, Inc. lets customers comparison shop for property and casualty coverage (including ride-sharing) and claims processing. Its business insurance products are available in 50 states, with Massachusetts the only exception.1

PERSONAL LINESInsurTech companies are putting a tech spin on auto, home and renters’ insurance. There are comparison shopping tools like The Zebra, which has about 200 carriers on the site including Allstate Corporation, MetLife, Inc. and Nationwide. Goji uses traditional agents yet is a digital agency. After consumers input data, they are called by an agent. Insurify, Inc. uses AI and advanced analytics to provide auto insurance quotes based on minimal information (zip code, type of car, driving record). Because employees are not agents, those interested in products are redirected to a partner licensed insurance representative.1

Quilt, Inc. is targeted to millennials, and offers mostly personal lines insurance while Jetty National, Inc. provides renters’ insurance and co-op insurance in urban areas. For new drivers, Cuvva offers pay-as-you-go coverages — as long as drivers clock fewer than 4,000 miles annually.1

Securities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

EQUIPMENT AND TECHNOLOGY GROWTH VS. TOTAL COMPENSATION GROWTH

5CounterPoint November 2017

Source: MarshBerry proprietary financial management system, Perspectives for High Performance (PHP); E&T: Equipment & Technology Past performance is not necessarily indicative of future results.

SHARING ECONOMYThe sharing economy allows people to borrow or rent assets from others (e.g. Uber Technologies Inc. [“Uber’], Lyft, Inc. [“Lyft’], or Airbnb models) that prompts a pooling, “we’re in it together,” culture that is appealing to millennials. In this space, Slice Insurance Technologies Inc. offers insurance for ridesharing and “homesharing.” For example, insurance could be for a single room within a house, or the entire house. There is also a pay-as-you-use ridesharing coverage for Lyft and Uber drivers.1

Sure Inc. provides limited use insurance like wedding coverage that is “one-and-done.” There is no human interaction — it is all robo-adviser/mobile chat. Carriers like Nationwide, Chubb Group of Insurance Co., Markel and MetLife are on board.1

You can use a smartphone to buy Trōv, Inc.’s individual product insurance for specified amounts of time — like insuring a camera during a two-week safari. Similarly, Square Trade Inc. is a warranty-type insurance for products like laptops,

INSURANCE IS NOT TYPICALLY CONSIDERED A FEEL-GOOD INDUSTRY, BUT SOME INSURTECH COMPANIES WANT TO CHANGE THAT.

tablets, appliances and electronic devices. Amazon.com, Inc., Staples and eBay Inc. are on board. Trov’s competitor, Upsie Technology Inc., offers the same type of insurance.1

SOCIALLY CONSCIOUSInsurance is not typically considered a feel-good industry, but some InsurTech companies want to change that. One is Lemonade Insurance Agency, LLC, which uses AI and behavioral economics to provide renters’ and homeowners’ insurance. The beauty of this model: excess premiums — after reinsurance and claims costs — are donated to charities chosen by policyholders. The idea is to improve customer experience and give policyholders a warm and fuzzy feeling that makes them think, “Insurance…is so nice!”1

Givesurance Insurance Services, Inc. will donate up to 5% from commissions that it receives from insurance carriers. This social conscious campaign is attractive to the 35-and-under crowd. Meanwhile, Givesurance acquires its customers through charitable organizations as an alternative distribution channel.1

Securities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

6 November 2017 CounterPoint

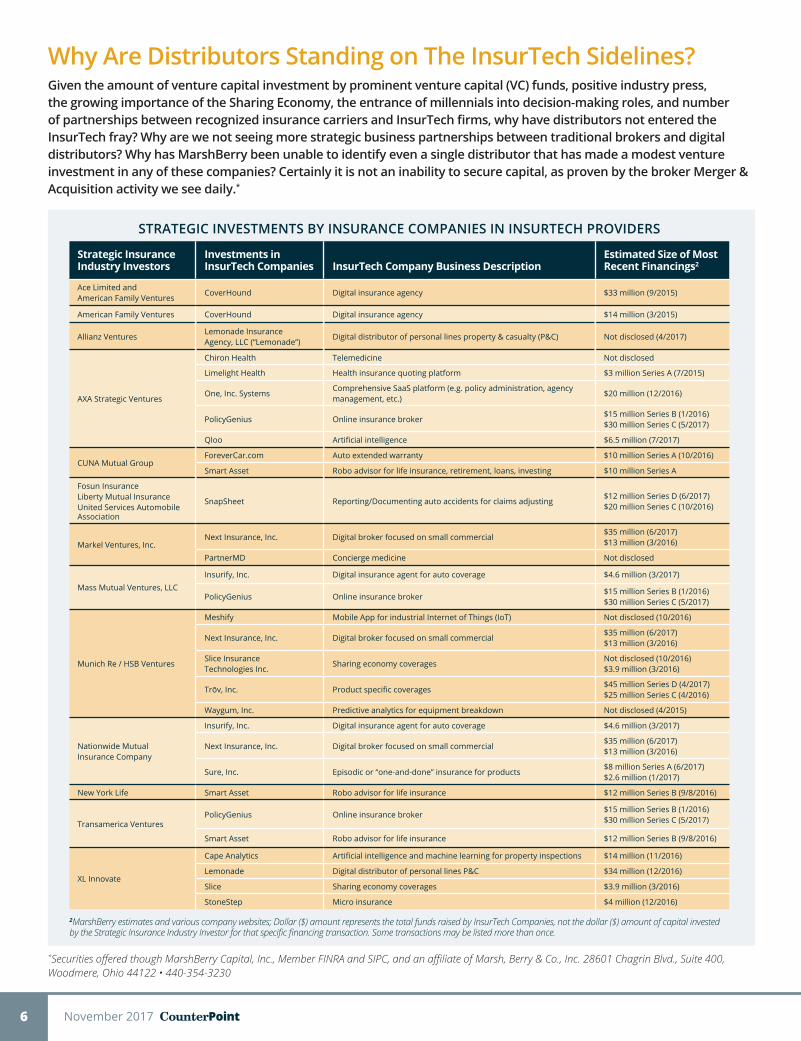

Why Are Distributors Standing on The InsurTech Sidelines? Given the amount of venture capital investment by prominent venture capital (VC) funds, positive industry press, the growing importance of the Sharing Economy, the entrance of millennials into decision-making roles, and number of partnerships between recognized insurance carriers and InsurTech firms, why have distributors not entered the InsurTech fray? Why are we not seeing more strategic business partnerships between traditional brokers and digital distributors? Why has MarshBerry been unable to identify even a single distributor that has made a modest venture investment in any of these companies? Certainly it is not an inability to secure capital, as proven by the broker Merger & Acquisition activity we see daily.*

STRATEGIC INVESTMENTS BY INSURANCE COMPANIES IN INSURTECH PROVIDERS

Strategic Insurance Industry Investors

Investments in InsurTech Companies

InsurTech Company Business Description

Estimated Size of Most Recent Financings2

Ace Limited and American Family Ventures

CoverHound Digital insurance agency $33 million (9/2015)

American Family Ventures CoverHound Digital insurance agency $14 million (3/2015)

Allianz VenturesLemonade Insurance Agency, LLC (“Lemonade”)

Digital distributor of personal lines property & casualty (P&C) Not disclosed (4/2017)

AXA Strategic Ventures

Chiron Health Telemedicine Not disclosed

Limelight Health Health insurance quoting platform $3 million Series A (7/2015)

One, Inc. SystemsComprehensive SaaS platform (e.g. policy administration, agency management, etc.)

$20 million (12/2016)

PolicyGenius Online insurance broker$15 million Series B (1/2016) $30 million Series C (5/2017)

Qloo Artificial intelligence $6.5 million (7/2017)

CUNA Mutual GroupForeverCar.com Auto extended warranty $10 million Series A (10/2016)

Smart Asset Robo advisor for life insurance, retirement, loans, investing $10 million Series A

Fosun Insurance Liberty Mutual Insurance United Services Automobile Association

SnapSheet Reporting/Documenting auto accidents for claims adjusting$12 million Series D (6/2017) $20 million Series C (10/2016)

Markel Ventures, Inc.Next Insurance, Inc. Digital broker focused on small commercial

$35 million (6/2017) $13 million (3/2016)

PartnerMD Concierge medicine Not disclosed

Mass Mutual Ventures, LLCInsurify, Inc. Digital insurance agent for auto coverage $4.6 million (3/2017)

PolicyGenius Online insurance broker$15 million Series B (1/2016) $30 million Series C (5/2017)

Munich Re / HSB Ventures

Meshify Mobile App for industrial Internet of Things (IoT) Not disclosed (10/2016)

Next Insurance, Inc. Digital broker focused on small commercial$35 million (6/2017) $13 million (3/2016)

Slice Insurance Technologies Inc.

Sharing economy coveragesNot disclosed (10/2016) $3.9 million (3/2016)

Trōv, Inc. Product specific coverages$45 million Series D (4/2017) $25 million Series C (4/2016)

Waygum, Inc. Predictive analytics for equipment breakdown Not disclosed (4/2015)

Nationwide Mutual Insurance Company

Insurify, Inc. Digital insurance agent for auto coverage $4.6 million (3/2017)

Next Insurance, Inc. Digital broker focused on small commercial$35 million (6/2017) $13 million (3/2016)

Sure, Inc. Episodic or “one-and-done” insurance for products$8 million Series A (6/2017) $2.6 million (1/2017)

New York Life Smart Asset Robo advisor for life insurance $12 million Series B (9/8/2016)

Transamerica VenturesPolicyGenius Online insurance broker

$15 million Series B (1/2016) $30 million Series C (5/2017)

Smart Asset Robo advisor for life insurance $12 million Series B (9/8/2016)

XL Innovate

Cape Analytics Artificial intelligence and machine learning for property inspections $14 million (11/2016)

Lemonade Digital distributor of personal lines P&C $34 million (12/2016)

Slice Sharing economy coverages $3.9 million (3/2016)

StoneStep Micro insurance $4 million (12/2016)

2MarshBerry estimates and various company websites; Dollar ($) amount represents the total funds raised by InsurTech Companies, not the dollar ($) amount of capital invested by the Strategic Insurance Industry Investor for that specific financing transaction. Some transactions may be listed more than once.

*Securities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

7CounterPoint November 2017

Part of the answer could lie in the very early stage of most InsurTech companies. While the investment dollars are large in several of these entities, actual revenue generation has been tiny to date. Moreover, InsurTech business models continue to evolve. Witness Zenefits’ recent announcement that they will no longer accept Broker of Record commissions, instead converting to a more traditional software commission/SaaS economic model.

Part of the answer could lie in distributors historically owning the customer relationship. As a trusted adviser to their clients, insurance agents and brokers may not want to damage that customer relationship by making a bet on the wrong InsurTech company. Rather, they believe it is better to take a wait and see approach to better gauge the InsurTech winners from the also-rans.

Part of the answer could lie in pragmatism. A carrier may be able to partner with an InsurTech company because it only has one processing system to integrate. Agents and brokers, however, would need to integrate their service platforms with several different carriers and the InsurTech platform at the same time. This technological conundrum has plagued the insurance distribution system for a long time. With the amount of capital outlay required for this type of multi-participant, multi-processing system, knowing

Do you have an exciting success story, witnessing exceptional growth or wanting to highlight your culture to the insurance industry?

We want to hear from you! Every month MarshBerry will choose an agency to feature across our social media channels and, in some instances, CounterPoint.

Please help us by logging on to www.MarshBerry.com/Focus and filling out the brief form for consideration to be featured.Agency In Focus will be a great way to highlight your agency’s achievements!

which InsurTech companies will ultimately survive and thrive is probably a better approach.

Finally, part of the answer could lie in investment dollar allocation. With the Merger & Acquisition (M&A) markets for insurance distributors hot and remaining so, it may be in certain agent’s best interest to use their finite capital to buy companies, integrate them, and only then deploy a technology solution that is proven and reliable.

However, there will be InsurTech companies that develop successful business models, capturing both consumer and business market share. Waiting too long to invest in, partner, or compete with InsurTech firms may result in some distributors being left behind. And as InsurTech evolves, those who delay change too long run the risk of becoming irrelevant.

Therefore, the message is simple. InsurTech is capturing the interest and capital of investors who believe it will change the way insurance is delivered and serviced. Be prepared to move quickly as InsurTech winners emerge, and as consumers demand more customized approaches to risk mitigation. n

MarshBerry Launches New Initiative:

AGENCY IN FOCUS

1MarshBerry’s 2017 InsurTech Study collected information from a wide variety of sources including but not limited to individual company websites and press releases, VentureBeat, PitchBook, Insurance Journal, PropertyCasualty360, TechCrunch, Forbes, CrunchBase, LinkedIn, The New York Times, Bloomberg News, Reuters, and Business Wire.

Securities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

8 November 2017 CounterPoint

The Beat Goes Onby George Bucur, Vice President – Insurance Services Division 440.392.6543 | [email protected]

The beat goes on when it comes to merger and acquisition activity in the specialty insurance distribution sector.

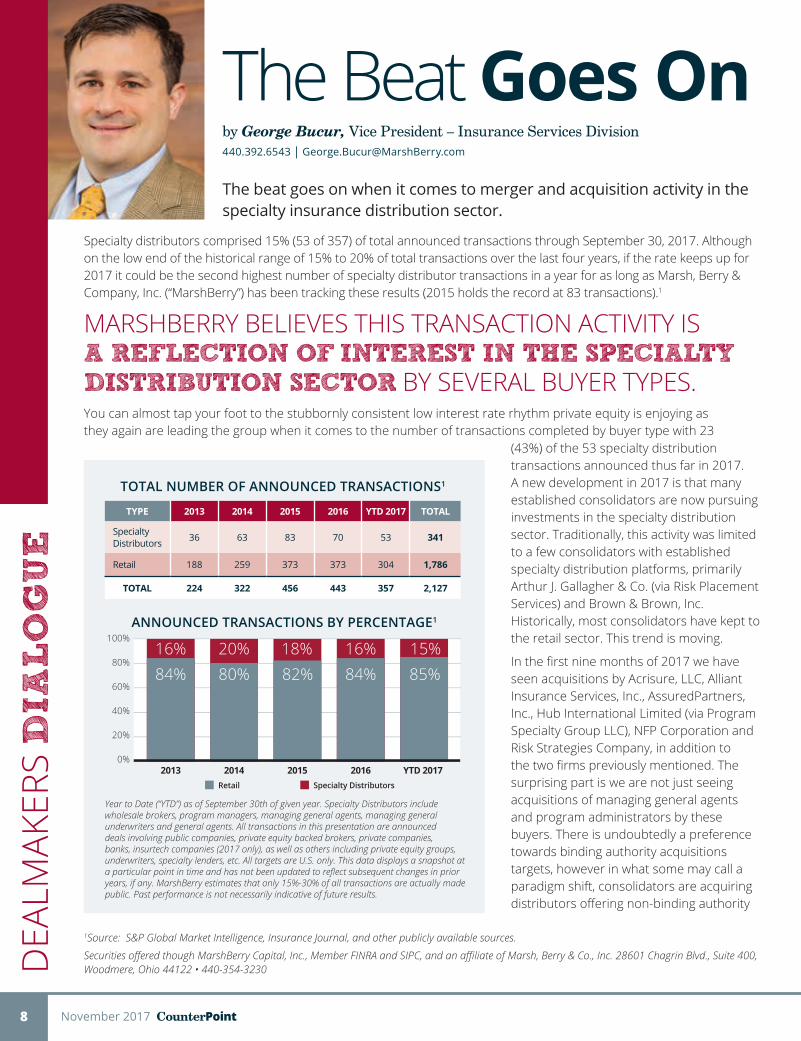

Specialty distributors comprised 15% (53 of 357) of total announced transactions through September 30, 2017. Although on the low end of the historical range of 15% to 20% of total transactions over the last four years, if the rate keeps up for 2017 it could be the second highest number of specialty distributor transactions in a year for as long as Marsh, Berry & Company, Inc. (“MarshBerry”) has been tracking these results (2015 holds the record at 83 transactions).1

MARSHBERRY BELIEVES THIS TRANSACTION ACTIVITY IS A REFLECTION OF INTEREST IN THE SPECIALTY DISTRIBUTION SECTOR BY SEVERAL BUYER TYPES. You can almost tap your foot to the stubbornly consistent low interest rate rhythm private equity is enjoying as they again are leading the group when it comes to the number of transactions completed by buyer type with 23

DEA

LMAK

ERS

DIA

LO

GU

E

TYPE 2013 2014 2015 2016 YTD 2017 TOTAL

Specialty Distributors 36 63 83 70 53 341

Retail 188 259 373 373 304 1,786

TOTAL 224 322 456 443 357 2,127

TOTAL NUMBER OF ANNOUNCED TRANSACTIONS1

ANNOUNCED TRANSACTIONS BY PERCENTAGE1

Year to Date (“YTD”) as of September 30th of given year. Specialty Distributors include wholesale brokers, program managers, managing general agents, managing general underwriters and general agents. All transactions in this presentation are announced deals involving public companies, private equity backed brokers, private companies, banks, insurtech companies (2017 only), as well as others including private equity groups, underwriters, specialty lenders, etc. All targets are U.S. only. This data displays a snapshot at a particular point in time and has not been updated to reflect subsequent changes in prior years, if any. MarshBerry estimates that only 15%-30% of all transactions are actually made public. Past performance is not necessarily indicative of future results.

(43%) of the 53 specialty distribution transactions announced thus far in 2017. A new development in 2017 is that many established consolidators are now pursuing investments in the specialty distribution sector. Traditionally, this activity was limited to a few consolidators with established specialty distribution platforms, primarily Arthur J. Gallagher & Co. (via Risk Placement Services) and Brown & Brown, Inc. Historically, most consolidators have kept to the retail sector. This trend is moving.

In the first nine months of 2017 we have seen acquisitions by Acrisure, LLC, Alliant Insurance Services, Inc., AssuredPartners, Inc., Hub International Limited (via Program Specialty Group LLC), NFP Corporation and Risk Strategies Company, in addition to the two firms previously mentioned. The surprising part is we are not just seeing acquisitions of managing general agents and program administrators by these buyers. There is undoubtedly a preference towards binding authority acquisitions targets, however in what some may call a paradigm shift, consolidators are acquiring distributors offering non-binding authority

1Source: S&P Global Market Intelligence, Insurance Journal, and other publicly available sources.

Securities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

in Partnership with Insurance JournalMarshBerry and Insurance Journal have joined forces to bring a series of online technical training courses designed specifically to provide new producers in the Property & Casualty insurance industry the knowledge they need to develop a foundation for success.This 15-hour, 8-week program is authored and instructed by Christopher J. Boggs, CPCU, ARM, ALCM, one of the top insurance educators in the country. In addition to the 8-week program, subscribers also have access to the entire catalog of courses and live webinars.

For more information, and to view a current training curriculum, visit: www.MarshBerry.com/training-portal

Property & Casualty Insurance Training for New Producers

9CounterPoint November 2017

products (i.e. wholesale brokerage). As a case in point, Specialty Program Group, LLC acquired Monarch E&S Insurance Services (Monarch E&S) in September of this year. As the name implies, Monarch E&S caters at least in part to the wholesale brokerage sector.

We believe there are several reasons consolidators may seek to acquire specialty distributors with binding authority. However, the risks associated with consolidators acquiring non-binding authority distributors should not be overlooked. One reason this paradox is occurring resides in that consolidators are hungry for growth and bigger is better (typically) when it comes to revenue. As consolidators seek out larger specialty distributors they are finding that these firms tend to offer both binding and non-binding authority products.

Resulting from consolidators’ acquisitions of specialty distributors is a potential (or perceived) conflict of interest. For example, a wholesale broker is likely to distribute through retail agents that compete with core retail operations of consolidators. Until recently, this alone may have discouraged many consolidators from entering the specialty distribution world.

As recent transaction activity implies, this is one tune that is changing. The new song may test the harmony between specialty distributors acquired by consolidators and their distribution chain. nSecurities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

CONGRATULATIONS to the following organization

that was recently represented by MarshBerry in their transaction:

J U N E 2 0 1 7

Alera Group, Inc. HAS ACQUIRED Group Benefits, LLC1

A U G U S T 2 0 1 7

Fred C. Church, Inc. HAS ACQUIRED Duble & O’Hearn, Inc.1

S E P T E M B E R 2 0 1 7

Hub International Limited HAS ACQUIRED Stellarus Benefits, Inc.1

Hub International Limited HAS ACQUIRED Benefit Advisory Group LLC1

O C T O B E R 2 0 1 7

GCG Financial, LLC an Alera Group, Inc. Company HAS ACQUIRED

Axis Benefits Consultants, Inc.1

Hub International Limited HAS ACQUIRED Banyan Consulting Group, Inc.1

Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, OH 44122 • 440.354.3230.

1MarshBerry represented the Seller in this transaction.

10 November 2017 CounterPoint

The Role of Technology for the Specialty Distributorby Chad Morgan, Vice President 949.234.9653 | [email protected]

Specialty distributors1 come from a legacy of innovation — they have a long track record of creating solutions that address unique and complex risks. How they do this is partly a function of the data they collect, analyze, and turn into information.

OVER TIME, THE PROCESS OF DISTILLING LARGE DATA SETS INTO USEFUL INFORMATION ASSISTS THEM WITH RISK SELECTION AND UNDERWRITING, AND THEY CAN BECOME THE DE FACTO EXPERTS IN THEIR RESPECTIVE LINES OF COVERAGE. Actionable information that is derived from the data that specialty distributors collect contributes to real economic value. However, this value can be difficult to tap into and it doesn’t necessarily translate into a higher enterprise valuation. As a matter of fact, early stage companies may consider the untapped-economic value (derived from data) to be an ‘intangible’ asset that takes the form of intellectual property, or know-how (as in, they know-how to turn data into information that leads to better underwriting decisions). As firms grow and predictable, profitable earnings streams are produced through positive underwriting results and proven business models, specialty distributors may unlock this intangible value and begin to realize what the Harvard Business Review has termed, the enterprise value of data2.

The concept of the enterprise value of data is beyond the scope of this article; however, in our experience, there is a positive correlation between (i) companies that financially outperform and (ii) companies that prudently and consistently invest in their technological platform (and systems in general). After all, a company is required to spend money to make money, right? Today, management teams are faced with many challenging decisions including that of buying versus building technology. The answer is not easy, and one size does not fit all. Moreover, many times the optimal solution is a combination of both purchasing off-the-shelf applications and modifying them to meet the organization’s need, and could include using external as well as internal data.

As management teams evaluate opportunities using technology to add and realize corporate value, we believe they should evaluate not only the external value proposition of the (potential) technological solution, but also the following four pertinent ideas:

1 STAFF CAPABILITIES Many companies have a mix of solutions that are vendor-bought and internally-developed. For those core insurance solutions such as underwriting and, possibly, policy administration, you will want to assess your personnel — both IT and business professionals. If your IT department does not have experience and skill sets necessary to build applications, (or a solid insurance background), it may be hard to attract that talent in a short

FOR

THE

RE

CO

RD

1For the purposes of this article specialty distributors are generally meant to include managing general agents / underwriters and program administrators that have carrier relationships with underwriting and binding authorities2https://hbr.org/2016/09/do-you-know-what-your-companys-data-is-worth

Securities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

Access our exclusive network partner library…

RESOURCEHUBResourceHub provides articles, tools, and resources to help you solve workplace challenges. It is a members-only online portal that anyone in your firm can access as part of your network partner membership. Archived MarshBerry University webinars, semiannual summit presentations, articles, and more are available for your on-demand review.

See what’s new today! ResourceHub.MarshBerry.com

PEER EXCHANGE NETWORK NEWS

INTERESTED IN LEARNING MORE ABOUT OUR PEER EXCHANGE NETWORKS? Please contact Tommy McDonald today at [email protected]

11CounterPoint November 2017

timeframe. Having dedicated and committed business resources who are willing to challenge the status quo are a must, regardless of whether you build or buy.

2 EXISTING TECHNOLOGY Unless you are a brand-new company, you will also have to clear the hurdle of how the new systems will fit into an already existing architecture (whether legacy or modernized). The ease of integration with your new solutions may not offer the ultimate end user experience you want to provide for your customers.

3 FUTURE OF YOUR BUSINESS In our opinion, one of the most important aspects to consider is what does your business look like today and how it will evolve? Will you be able to achieve the agility, flexibility and control over the products you want to offer? Can multiple products be offered together in a desirable distribution method? Can your organization adhere to a vendor-based offering without extensive customization?

4 COST Systems costs should be factored into one’s considerations for creating the most optimal technology solutions for the organization. Again, there is no one-size-fits-all solution. The good news is that data storage costs are trending lower. The bad news is that custom development is still significant. To balance these competing considerations, knowing the type of data that produces the best actionable information is one way to better evaluate cost vs. functionality.

In today’s world, how companies use technology is a differentiating factor — it can separate the winners from the losers. Technology not only unlocks intangible value via high-efficacy data-to-information transformation, but also assists specialty distributors with agent and broker demands for process speed and flexibility. And speaking of speed and flexibility, we all know today’s technology can be high on the soon-to-be obsolete or irrelevant scales.

For these reasons and more, we believe it is important that management teams comprehensively evaluate their buy-versus-build (or hybrid) options with not only their current capabilities in mind, but also the future. nSecurities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

12 November 2017 CounterPoint

Will Your Agency

Be Disrupted?by James Graham, Senior Consultant 949.234.0351 | [email protected]

The insurance agency system is being disrupted by the acceleration of technological advancement, but not in the way you might think.

Every so often supposed experts with little to no experience in the insurance distribution space will make grand predictions on how the insurance agency system will be disrupted and go the way of the horse and buggy. While these claims have consistently been proven wrong, we are seeing that disruption is happening.

THE INSURANCE AGENCY SYSTEM IS HERE TO STAY, BUT FIRMS THAT LEVERAGE NEW TECHNOLOGY AND BUSINESS MODELS TO ENHANCE THEIR SALES AND SERVICE PROCESSES WILL LIKELY OUTPACE TRADITIONAL MODELS.

Securities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

IND

UST

RY I

NSIG

HT

S

THE DISRUPTIVE INNOVATION MODEL

The diagram contrasts product performance trajectories (the red lines showing how products or services improve over time) with customer demand trajectories (the blue lines showing customers’ willingness to pay for performance). As incumbent companies introduce higher-quality products or services (upper red line) to satisfy the high end of the market (where profitability is highest), they overshoot the needs of the low-end customers and many mainstream customers. This leaves an opening for entrants to find footholds in the less-profitable segments that incumbents are neglecting. Entrants on a disruptive trajectory (red yellow line) improve the performance of their offerings and move upmarket (where profitability is highest for them, too) and challenge the dominance of the incumbents.

Source: Clayton M. Christensen, Michael Rynor, and Rory McDonald, from “What is Disruptive Innovation?” December 2015.

We are seeing an emergence of an increasing number of technologically savvy agencies such as CoverHound,Inc., The Zebra, and Insureon. An important characteristic they all share is they are focusing their innovations on the simplest insurance products. Disruptive Innovation is “an innovation that creates a new market by providing a different set of values, which ultimately (and unexpectedly) overtakes an existing market,” it was first defined by Clayton Christensen a Professor at the Harvard School of Business. As shown in the graph, disruptive companies target the bottom of a market and work their way up at an accelerating pace by leveraging new technology or business models and building an initial customer base of previously underserved consumers.

One of the key reasons companies with a disruptive strategy are successful is they provide value to clients that are currently either not served or not valued by incumbent firms. This allows them to create and grow new business models without

13CounterPoint November 2017

much competition from firms with deeper pockets and entrenched business models.

One of the best examples of disruptive innovation is when Netflix recently upended the video rental industry. Netflix began disrupting the video rental industry by creating a web platform to facilitate a mailing service catering to a segment of the market who were previously under served by retail stores when it came to movie selection. When Netflix began, their service was less convenient and less profitable than that of incumbent firms, but because Netflix could build on their initial web platform they were able to move upstream unexpectedly with the successful launch of their online streaming service. Today, the video rental industry has been redefined by the standards Netflix has set.

So how do you prevent your agency from being disrupted? For our clients, disruption can come from a number of directions and, in our opinion, creating a defensive strategy is imperative. Below are a few simple defensive tactics we believe agencies should consider deploying.

1 KEEP ABREAST OF WHAT IS HAPPENING IN INSURTECH. Don’t believe the hype and go beyond headlines. Look to understand new business models and technologies and how they could help your firm.

2 GET SERIOUS ABOUT YOUR STRATEGIC PLANNING AND UNDERSTAND YOUR AGENCY’S POSITION IN THE MARKETPLACE. Technology enables strategy. Spending on technology without guiding strategy can be a waste.

3 TAKE RISKS AND CREATE A CULTURE WHERE INNOVATION AND OUT OF THE BOX THINKING IS CELEBRATED. One reason many of our clients fail to stay independent is they aren’t doing anything beyond what is industry standard or average. Average will be disrupted.

Disruptive innovation is not easy and many of the new firms attempting to disrupt the industry may fail to become the dominate players they dream of becoming, but those that succeed will create new business models and technology capabilities that will likely define the next generation of insurance agencies. Now is the time to be innovative and be part of the change. nSecurities offered though MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440-354-3230

Join us for the preeminent event for specialty distributors in the insurance space — Peak Performance creates an intimate networking opportunity for executives to learn and help improve their business.

JANUARY 28 - JANUARY 30, 2018HYATT CENTRIC PARK CITYAGENDA HIGHLIGHTS:• State of the Industry for Specialty Distribution

• Keynote Address by Jack Uldrich, Global Futurist, Scholar & Author: The Big AHA — How to Future- Proof the Insurance Industry Against Tomorrow’s Transformational Trends

• Industry Panel Discussion: What’s Next in InsurTech?

• Current Perspectives on Specialty Distributors

REGISTER TODAYWWW.MARSHBERRY.COM/PEAK OR 800.426.2774

Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 (440.354.3230). Marsh, Berry & Co., Inc. and its affiliates are non-affiliated entities with BankDirect Capital Finance, Oak Street Funding, NetRate Systems, RSG Underwriting Managers and StateNational

Think Differently

THANK YOU TO OUR 2018 SPONSORS:

28601 Chagrin Blvd., Ste. 400 Woodmere, OH 44122

www.MarshBerry.com

@marshberryinc

facebook.com/MarshBerry

linkedin.com/company/ MarshBerry

Mark your calendars!

NOVEMBER 201711.8-9 • 11th Annual Insurance Brokerage Summit,

Washington D.C.

JANUARY 20181.28-1.30 • Peak Performance Summit,

Park City, UT

MAY 201805.03 • MarshBerry 360,

New York, NY

05.08 • MarshBerry 360, Chicago, IL

05.10 • MarshBerry 360, Las Vegas, NV

06.26 • MarshBerry 360, London, England

28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122

ENGAGE WITH MARSHBERRY

HORIZON

ON

TH

E

Log on to www.MarshBerry.com to register for events, view latest news and read back issues of CounterPoint.

WE WANT TO HEAR FROM YOU!

We want to make sure we’re providing the content you

want to read and want feedback on the articles we’re publishing.

Please send an email to us at [email protected]

to share your thoughts!