Embed Size (px)

Citation preview

CustomerInformationSEPA

Single Euro Payments Area – The standard European bank transfers system 9th EditionStatus as of: January 2014

Updated information aboUt the migration to Sepa

SepaCHECK

run t

he hVb Sepa Check now!

• www.hvb-sepa.de •

For this reason, switch to SEPA now with the help of HVB’s specialists – and continue to be able to make payments.The HVB SEPA Check supports youfind more at hvb.de/sepa

Your money transfers may no longer function unless you have switched to the new SEPA system .

Advertisment

3

Table of contents

4 Contents and aims of SEPA

5 Creation of SEPA

6 Timeline and SEPA parties

7 EU regulation

8 Single Euro Payments Area –

an overview

10 New standards

14 New payment instruments

16 The mandate

18 The SEPA Direct Debit mandate

22 Pre-notification

24 Creditor identifier

25 “Direct debit” returns process

25 Cycle of a SEPA Direct Debit

28 UniCredit product range and

SEPA services

37 SEPA – opportunities and benefits

38 Recommended actions for our

customers

39 SEPA Direct Debit mandate FAQs

49 SEPA cards

51 Key abbreviations

54 Contacts

55 Imprint

Identifiers are placed in the margin to quickly show you where the amendments have occurred.

4

Contents and aims of SEPAThe future of European payments

•With a single format •With transparent prices throughout Europe •With set time limits/durations •With a single harmonised legal framework •With cross-border direct debits in Europe •With UniCredit Group

SEPA will impact not only cross-border payments within Europe, but almost all (approx. 98%) pay-ment procedures currently handled as national procedures.

We are here to help you!

One of the aims of economic and monetary union is the creation of the internal market in the European Union. The third stage of the economic and monetary union – the introduction of a common currency, the euro – is linked with the political goal of creating the Single Euro Payments Area, or SEPA, as part of this internal market. At the core of this area are the current euro-zone countries. The other EU member states, along with Norway, Iceland, Liechtenstein, Monaco, San Marino and Switzerland, will also be included with their euro-denominated payments.

The European banking industry will thus combine the goal and the challenge of making future-proof payment instruments for bulk payments available to consumers and corporate customers throughout Europe on comparable terms. Realisation of SEPA is thus a strategic project for the entire European banking industry.

5

Creation of SEPA“The timeline is set in stone,” were the words used by Charlie McCreevy, former European Commissioner for the Internal Market and Services. Excerpt from the Deutsche Kreditwirtschaft (DK – former Zentraler Kreditausschuss) and German Central Bank (Bundes-bank) press release of 28 August 2006:

“The German banking industry unreservedly endorses the aims of SEPA and will be implementing the new payment instruments on schedule […] SEPA is a major political project, being part of the completion of the EU internal market.” SEPA has thus been a reality since 28 January 2008.

Initiative by European bodies

The European ministers of finance and economic affairs reached agreement on the Payment Services Directive (PSD) in March 2007. This directive regulates all payments in European currencies in Europe (thus also including existing systems and processes). The PSD therefore forms the framework for SEPA and is, at the same time, a key requirement for legal certainty, particularly for the new European direct debit proce-dure.

The PSD was passed by the European Parliament and entered into force on 1 November 2009. Switzerland endorses SEPA to the extent that it will adapt its legal system to the SEPA conditions.

Input by the European Payments Council (EPC)

The European banks have organised themselves through the European Payments Council (EPC) as re-gards the design of SEPA process and pledged its im-plementation through the pathway of self-regulation. UniCredit is actively involved in the work of the EPC via the Deutsche Kreditwirtschaft (DK). In addition, UniCredit is a member of the EPC committee.

The EPC has already defined several key instru-ments in the so called ‘Rulebook’. These form the cornerstones for the operational implementation and realisation of SEPA by the banks: the SEPA Rulebooks for credit transfers and direct debits, the SEPA Card Framework, and the SEPA Implementation Guidelines.

With the adoption of the Implementation Guidelines, the basic framework for availability of the new UNIFI (ISO 20022) XML data formats is also in place. These are mandatory for interbank payments (extended acceptance period for legacy electronic formats by banks until 1 August).

Summary

The EPC represents a clear political commitment on the part of the EU and the European banks. This includes further integration of the EU internal market and the necessary preparations for its realisation.

In Germany, realisation of SEPA is supported by the German Bundestag, the German Bundesbank and the representative service providers and service users.

6

Timeline and SEPA parties January 2008

SEPA Credit Transfers have been available since 28 January 2008.

1 November 2009

Almost 100% reachability became available for SEPA Credit Transfers. SEPA Direct Debit was introduced and SEPA CORE Direct Debit became mandatory for euro countries. SEPA Business to Business (B2B) Direct Debit was introduced on a voluntary basis.

9 July 2012

Entry into force of the new direct debit agreement of the German banks concerning pre-authorisation of the direct debit mandate and extension of the returns period in the event of objections from 6 to 8 weeks for direct debit mandates. From this point, it became possible to reinterpret the direct debit authorisation as a SEPA mandate (CORE Direct Debit) without obtaining a new SEPA mandate.

9 April 2013

The German SEPA Accompanying Act came into force.

1 February 2014

Replacement of national payment procedures for bank transfers and direct debits.

1 February 2014

Replacement of national payment procedures with exceptions

Until 1 August 2014*

Extension of acceptance period for electronic presen-tation of national collection authorisations and credit transfers in the old format.

April to October 2015

Conversion of card clearing for POS to the SEPA format.

1 February 2016

•Exception option to utilise account numbers and bank codes discontinued for consumers. Obligation for all customer groups to utilise IBAN.• Exception option for ELV to be discontinued. Paying

at retailers by signature must be converted to SEPA. •BIC obligation also to be discontinued for cross-bor-

der payments.

31 October 2016

SEPA obligation also for EU countries that do not use the euro as their currency.

* Subject to the amendment of the EU Regulation 260/2012 as planned by the EU .

7

EU regulationThe applicable EU regulation entered into force on 31 March 2012. The main contents are:

•The regulation applies to payments within the Euro-pean Union for credit transfers and direct debits in the euro currency. The regulation does not cover ur-gent payments, cheques, foreign exchange, Girocard payments or payments in other currencies.•Payment service providers in the EU participating in

the domestic credit transfer and CORE Direct Debit procedures must offer the relevant SEPA procedures.•Stipulated requirements concerning credit transfer

and direct debit payments must be adhered to from 1 February 2014 in euro-countries (e. g. customer identification is the IBAN, ISO 20022 format). •Member States can allow banks to convert account

numbers and bank numbers into IBAN for consumers until 1 February 2016. •EU payment service providers in non-euro countries

must adhere to the stipulated technical and special-ist requirements from 31 October 2016. If the euro is introduced within this period, the requirements must be met within a year.

•As Member States may allow exceptions, Germany allows the electronic direct debit pro-cedure for busi-ness to continue unchanged until 1 February 2016. •From 1 February 2014, banks may no longer request

the BIC (Business Identifier Code) of their customers for domestic payments. This provision will also apply to cross-border payments from 2016. •With the SEPA CORE Direct Debit, paying parties are

granted the right to block certain payment recipients, only to permit certain payment recipients and to restrict payments based on amount or frequency of submission.•Standard rules on the continued validity of direct

debit mandates in national procedures after the SEPA migration according to which existing direct debit mandates can continue to be used. •EU Regulation 924/2009 (“EU price regulation”)

eliminates the EUR 50,000 limit.•Since the migration rate in 2013 was not yet satis-

factory, the EU Regulation will be once again amend-ed in February 2014 by means of an accelerated procedure, with retroactive effect from 31 January 2014. According to the present stage of negotiations, the transition period for the acceptance of electronic presentations in the old format will be extended until 1 August 2014. In Germany, the Federal Finan-cial Supervisory Authority (BaFin) will suspend the sanctions for the acceptance of legacy formats until 1 August 2014. Direct debits under the direct debit order procedure do not benefit from the transition period; this product was cancelled by the banks on schedule on 31 January 2014.

8

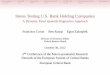

Single Euro Payments Area – an overview

geographical Sepa region biC-iSo code

iban-iSo code

Currency code

eU price regulation

pSd Sepa

Åland Islands FI FI EUR ◆ ◆ ◆

Albania1 AL AL ALL – – –Andorra AD AD EUR – – –Austria AT AT EUR ◆ ◆ ◆

Belgium BE BE EUR ◆ ◆ ◆

Bosnia and Herzegovina1 BA BA BAM – – –Bouvet Island BV – NOK – – –Bulgaria BG BG BGN ◆ ◆ ◆

Croatia HR HR HRK ◆ ◆ ◆

Cyprus CY CY EUR ◆ ◆ ◆

Czech Republic CZ CZ CZK ◆ ◆ ◆

Denmark DK DK DKK ◆ ◆ ◆

Estonia EE EE EUR ◆ ◆ ◆

Faroe Islands FO FO DKK – – –Finland FI FI EUR ◆ ◆ ◆

France FR FR EUR ◆ ◆ ◆

French Guiana* GF/FR GF/FR EUR ◆ ◆ ◆

French Polynesia* PF/FR PF/FR XPF – – –French Southern and Antarctic Lands* TF/FR TF/FR EUR – – –Germany DE DE EUR ◆ ◆ ◆

Gibraltar GI GI GIP ◆ ◆ ◆

Greece GR GR EUR ◆ ◆ ◆

Greenland GL GL DKK – – –Guadeloupe* GP/FR GP/FR EUR ◆ ◆ ◆

Guernsey GG GB/FR GBP – – –Hungary HU HU HUF ◆ ◆ ◆

Iceland2 IS IS ISK ◆ ◆3 ◆

Ireland IE IE EUR ◆ ◆ ◆

Isle of Man IM GB GBP – – –Italy IT IT EUR ◆ ◆ ◆

Jersey JE GB/FR GBP – – –

9

geographical Sepa region biC-iSo code

iban-iSo code

Currency code

eU price regulation

pSd Sepa

Kosovo according to UNSCR 124411 – – (EUR) – – EURLatvia LV LV EUR ◆ ◆ ◆8

Liechtenstein LI LI CHF ◆ ◆3 ◆

Lithuania4 LT LT LTL4 ◆ ◆ ◆

Luxembourg LU LU EUR ◆ ◆ ◆

Macedonia (former Yugoslavian Republic of)2 MK MK MKD – – –Malta MT MT EUR ◆ ◆ ◆

Martinique* MQ/FR MQ/FR EUR ◆ ◆ ◆

Mauritius MU MU MUR – – –Mayotte* YT/FR YT/FR EUR ◆ ◆5 ◆6

Monaco MC MC EUR – – ◆7

Montenegro2 ME ME EUR – – –Netherlands NL NL EUR ◆ ◆ ◆

New Caledonia* NC/FR NC/FR XPF – – –Norway NO NO NOK ◆ ◆3 ◆

Poland PL PL PLN ◆ ◆ ◆

Portugal (including the Azores, Madeira) PT PT EUR ◆ ◆ ◆

Réunion* RE/FR RE/FR EUR ◆ ◆ ◆

Romania RO RO RON ◆ ◆ ◆

San Marino SM SM EUR – – ◆8

Serbia RS RS RSD – – –Slovakia SK SK EUR ◆ ◆ ◆

Slovenia SI SI EUR ◆ ◆ ◆

Spain (including Ceuta and Melilla, Canaries) ES ES EUR ◆ ◆ ◆

Spitzbergen (Svalbard and Jan Mayen) SJ – NOK – – –St. Barthélemy* BL/FR BL/FR EUR ◆ ◆ ◆

St. Martin* (French part) MF/FR MF/FR EUR ◆ ◆ ◆

St. Pierre and Miquelon* PM/FR PM/FR EUR – – ◆6

Sweden SE SE SEK ◆ ◆ ◆

Switzerland CH CH CHF – – ◆

Turkey2 TR TR TRY – – –United Kingdom of Great Britain and Northern Ireland GB GB/IE GBP ◆ ◆ ◆

Vatican City VA – EUR – – –Wallis and Futuna* WF/FR WF/FR XPF – – –

* The IBAN and BIC country codes do not have to match but can each use “FR”.1 Is a potential candidate for accession to the European Union.2 Is candidate for accession to the European Union.3 Has declared the adoption of the act of law as a state of the European Economic Area (or will declare this).4 Will become member of the Eurozone – presumably on 1 January 2015. 5 Part of the European Union since 31 March 2011.6 According to the decision of the European Payments Council of June 2009.7 According to the decision of the European Payments Council of March 2009.8 Member of the SEPA as from February 2014 according to the decision of the European Payment Council of December 2013Source: BdB – Association of German Banks, 2 January 2014.

The EPC publishes a list of banks participating in SEPA on a monthly basis. This list contains the name of the bank, the address and the BIC of the head office. A complete directory of all available BICs is provided by EBA. EBA link www.ebaclearing.eu under STEP2, SEPA

Credit Transfer or SEPA Direct Debit and then under Participants. However, this sometimes only lists the BICs of the head office (8-digit BIC and check the last 3 digits of the place holder XXX).

10

New standardsHarmonised, simplified rules already exist for the most frequently used payment products – credit transfers and direct debits – for cross-border pay-ments between SEPA countries. It makes no difference whether the transaction takes place inside Germany or between Germany and France, for example.

The same technical standards will be used for SEPA Credit Transfers and the SEPA Direct Debits. As with current basic cross-border EU standard credit trans-fers, the IBAN (International Bank Account Number) and the BIC (Bank Identifier Code) will be used to identify the payee automatically. Name-matching is no longer a legal requirement.

Balance of payments reporting obligation

The party that is ordering the payment reports the balance of payments for SEPA payments directly at the Bundesbank (Z4) rather than using the payment file in XML format.

please note:The modified Balance of Payments Directive (AWV) came into force on 1 September 2013. This requires that reporting data are separated from bank transfers, so that parties that are required to make reports an-nounce their transactions directly to the Bundesbank.

•Since the AWV modifications came into force on 1 September 2013, companies, banks, public-sector entities and private individuals are now generally required to submit all balance of payments reports directly and electronically to the Deutsche Bundes-bank. As a consequence, paper reports will generally no longer be accepted.•The regulations for the electronic submission of pay-

ment orders (“DTAZV”) were adjusted accordingly with effect as of 4 November 2013, so that from this date the ordering party can no longer transmit statis-tical reporting information to the mandated bank.

Further current information can be found at:www.bundesbank.de/navigation/de/Service/ meldewesen/aussenwirtschaft/ aWV_aenderung_2013/awv_aenderung_2013.html

SEPA Credit Transfer require-ments for Switzerland

Switzerland is also a SEPA participant. One precondi-tion for SEPA payments to Switzerland is that the complete details of the paying party must be included in the data record.

As a service to its customers, UniCredit automatically adds the paying party’s details to the order/record. Note: Since Switzerland is not part of the EU, the EU price regulation does not apply. This also applies for all other countries participating in SEPA but which do not belong to the EU/EFTA, such as Monaco and San Marino.

11

IBAN composition using the example of Germany

Each IBAN in Germany consists of 22 alphanumeri-cal numbers beginning with the 2-digit country code DE followed by a 2-digit check number and your bank number and account number.

D E 4 0 7 0 0 2 0 2 7 0 0 0 1 2 3 4 5 6 7 8

de: Germany

Check digits: 2 digits

bank routing code: 8 digits

account number: 10 digits

Country code: DECheck number: 40Bank number: 70020270Account number: 12345678The IBAN is: DE40 70020270 0012345678

Further details on the structure of the various IBAN formats in other countries can be found in our IBAN information flyer.

please note:The IBAN must always be delivered correctly within the file; otherwise the entire file can be rejected. It is important to note in this context that country identifi-ers must only comprise capital letters, and that check digit must only comprise numbers. Letters are also possible from digit 5 on in the case of non-German IBANs. When entering the IBAN digits, take special care to differentiate between a zero (0) and the capital letter O. Spaces and other special symbols are not permitted.

The BIC is the business identifier code and is the recipient bank’s identifier. It is required to ensure your payment arrives. It is structured as shown below:

h Y V e d e m m X X X

bank code: 4 digits (e. g. HYVE for HypoVereinsbank)

Country: 2 digit, ISO code of the country

(e. g. DE for Germany

place/region code: 2 digit (e. g. MM for Munich)

branch code:3 digit

This enables you to provide the necessary details at any time to the paying party for a SEPA Credit Transfer to be made.

please note:The BIC must also be delivered correctly within the file; otherwise the entire file can be rejected. In this context, it is important that only capital letters be used in the first 6 positions, and that the BIC must consist of only 8 or 11 positions. In particular, confu-sion between O and zeros occurs frequently during manual entries.

12

Examples of SEPA IBAN

Country digits example (fictitious!)Austria 20 AT61 1904 3002 3457 3201Belgium 16 BE68 5390 0754 7034Bulgaria 22 BG80 BNBG 9661 1020 3456 78Croatia 21 HR12 1001 0051 8630 0016 0Cyprus 28 CY17 0020 0128 0000 0012 0052 7600Czech Republic

24 CZ65 0800 0000 1920 0014 5399

Denmark 18 DK50 0040 0440 1162 43Estonia 20 EE38 2200 2210 2014 5685Finland 18 FI21 1234 5600 0007 85France 27 FR14 2004 1010 0505 0001 3M02 606Germany 22 DE89 3704 0044 0532 0130 00Greece 27 GR16 0110 1250 0000 0001 2300 695Hungary 28 HU42 1177 3016 1111 1018 0000 0000Iceland 26 IS14 0159 2600 7654 5510 7303 39Ireland 22 IE29 AIBK 9311 5212 3456 78Italy 27 IT60 X054 2811 1010 0000 0123 456Latvia 21 LV80 BANK 0000 4351 9500 1Liechtenstein 21 LI21 0881 0000 2324 013A ALithuania 20 LT12 1000 0111 0100 1000Luxembourg 20 LU28 0019 4006 4475 0000

Malta 31MT84 MALT 0110 0001 2345 MTLC AST0 01S

Netherlands 18 NL91 ABNA 0417 1643 00Norway 15 NO93 8601 1117 947Poland 28 PL61 1090 1014 0000 0712 1981 2874Portugal 25 PT50 0002 0123 1234 5678 9015 4Romania 24 RO49 AAAA 1B31 0075 9384 0000San Marino 27 SM86 U032 2509 8000 0000 0270 100Slovakia 19 SI56 1910 0000 0123 438Slovenia 24 SK31 1200 00 1987 4263 7541Spain 24 ES91 2100 0418 4502 0005 1332Sweden 24 SE12 1231 2345 6789 0123 4561Switzerland 21 CH93 0076 2011 6238 5295 7United Kingdom

22 GB29 NWBK 6016 1331 9268 19

Note: Only the bank managing the relevant account is in a position to check the accuracy of an IBAN!

IBAN conversion portal (cross-bank solution)

The “Deutsche Bundesbank”, the “Bundesverband deutscher Banken – BDB”, the “Bundesverband der Deutschen Volksbanken und Raiffeisenbanken”, the “Deutsche Sparkassen- und Giroverband” and the “Bundesverband Öffentlicher Banken Deutschlands” provide a cross-bank solution for the determination/verification of BIC and IBAN with the Bank-Verlag GmbH.

•Online service via the Bank-Verlag GmbH•UniCredit offers a European solution with its coop-

eration partner Experian

You are strongly discouraged from determining the IBAN yourself using the current existing data (reason: bank-specific converting rules exist). A further sum-mary on these two solutions can be found on pages 32 and 33.

Details about how IBANs are structured in various countries can be found at:www.swift.com/dsp/resources/documents/ iban_registry.pdf

13

IBAN-Only

Banks may no longer request the BIC from their cus-tomers for domestic payments from 1 February 2014. This provision will also apply to cross-border pay-ments within the EU from 2016. We nevertheless rec-ommend that the BIC is entered as this is still required for international non-SEPA payments. You benefit from stringent data storage. A further need to store the BIC is the identification of the bank in case of any bank mergers (future IBAN forward and return proce-dures) and for querying in directories as to whether the respective bank supports SEPA products such as Direct Debit B2B and Direct Debit CORE with shorter presentation period (COR1). At HVB, you can electroni-cally submit domestic payments without BIC.

Formats

The electronic delivery of payments has to be carried out with new XML formats. These replace the DTAUS formats. Please pay attention to our technical bro-chure (Attachment to the SEPA customer information – German Technical Specifications and Formats) for the technical configuration rules for SEPA Credit Trans-fers (pain.001) and SEPA Direct Debits (pain.008).

14

New payment instrumentsSEPA Credit Transfer

Harmonised standards will replace current dif-ferent national and cross-border procedures and formats.

SEPA CORE Direct Debit

This constitutes a genuine innovation in cross-border payments, as no standardised direct-debit procedure has been used to date.

SEPA Business to Business (B2B) Direct Debit

SEPA Business to Business (B2B) Direct Debit is being introduced in addition to SEPA CORE Direct Debit. This is only used for the collection of outstanding payments between non-consum-ers/corporates.

SEPA cards (Cards Framework)

Card-based payments are also part of SEPA (“any card at any terminal”).

SEPA Credit Transfer (SCT)

The standards apply to all credit transfers in euros within SEPA, regardless of the amount.

the key features of Sepa Credit transfers are: •The original amount is forwarded without any

deductions.•The ordering party and the beneficiary bear their own

costs.•Guaranteed maximum one bank working day until

the transaction reaches at the beneficiary’s bank.•Pan-European harmonised standards and data

formats simplify order placing and automation •The EU price regulation only applies for payments

within the EU/EFTA.•Harmonised standards, also for returned payments.

SEPA CORE Direct Debit

SEPA CORE Direct Debit requires a mandate. The debtor authorises the creditor to collect a payment. The bank maintaining the account is directed to carry out the debit instructions and debit the account concerned. The creditor’s bank is not obliged to check the mandate.

the key features of Sepa Core direct debits are: •This is a new procedure for the collection of

receivables.•Each creditor needs a single unique, standardised

identification number (Creditor Identifier). In Germa-ny, this number is issued by the Bundesbank (www.bundesbank.de/zahlungsverkehr/ zahlungsverkehr_sepa_identifikation.php).•A direct debit cannot be collected without a man-

date. Mandate data are forwarded along with the transaction.

15

•Only payments in euros will be executed. Credits to and debits from foreign-currency accounts will be the responsibility of the banks concerned.•The payment due date of SEPA Direct Debits

(specified by the creditor in the collection) is also the date on which the amount is debited from the debtor’s account.•The debtor must be informed of the debit amount

and due date in advance by pre-notification; a docu-ment, such as an invoice with information regarding the due date, is sufficient (see page 22).•The creditor and its bank must forward the debit

instruction for collection ahead of time, such that the file is available to the debtor bank at least 5 days (TARGET days) before the due date in the case of a first or one-off debit, and at least 2 days before the due date for recurrent debits.•With respect to returns/refunds, only the original

amount in euros is relevant.•The debtor can refund a direct debit payment up to 8

weeks after the debit date (time of debit/due date).•If there is no valid mandate, a refund is possible for

up to 13 months.•Harmonised procedures and standards for returns. •When a debit payment is returned to the creditor,

the customer’s reference is displayed in a predefined field.

SEPA CORE Direct Debit with shorter presentation period (COR1)

With the SEPA Rulebook November 2012, the option is made available that it is sufficient if the SEPA CORE Direct Debit is at the bank of the debtor one day be-fore the due date. A corresponding agreement for the nationwide use of this direct debit across Germany is planned for November 2013. This shorter presentation

period can be used for one-off, recurrent, first and last time debits. No additional agreement is required with the paying party for this direct debit. In the mandate and pre-notification, no differentiation has to be made between SEPA CORE Direct Debit (CORE) and SEPA CORE Direct Debit (COR1). The submission of a COR1 Direct Debit has to be made in a separate file and cannot be mixed up with CORE and B2B Direct Debits. COR1, CORE and B2B Direct Debits all have their own respective order types.

SEPA Business to Business (B2B) Direct Debit

the following features should be borne in mind in this instance as they differ from the Sepa Core direct debit: •Collections are only made between non-consumers/

corporates •The debtor is not entitled to obtain a refund (excep-

tion for unauthorised direct debits) •Return must be made within 2 days after the due

date by the debtor bank •The mandate must be a separate B2B mandate

which need to be stored with debtor bank•The debtor bank is obliged to check the B2B Direct

Debit against the mandate (this must be lodged with the bank) •Presentation of direct debits no later than 1 day

before the due date

16

The mandateThe mandate

SEPA CORE Direct Debit and SEPA B2B Direct Debit cannot be collected without a valid mandate from the debtor containing predefined elements.

Existing direct debit agreements you have already made with your bank remain unaffected by the new SEPA Direct Debit process and retain their validity.

•The mandate can be issued on paper or electroni-cally, an electronic mandate authorisation is still in the planning stages.•The creditor is obliged to keep the mandate and

present it on request. •The mandate can be revoked at any time by the

debtor with respect to the creditor.

note: FAQs regarding the SEPA Direct Debit mandate can be found from page 37 of this brochure onwards.

Mandate migration

In the terms and conditions for direct debit payments at banks, it is agreed that the previous Collection Authorisation Procedure has the quality of an authori-sation of payment for the bank of the payer/debtor → “pre-authorised” direct debit.

As a consequence, the payer/debtor thereby enjoys a right pursuant to Section 675x of the German Civil Code (BGB) to reimbursement for a period of 8 weeks after the booking/due date (as is the case with the SEPA Direct Debit Core).

Migration of legacy business mandates

The following migration requirements have to be taken into account with mandate migration:

•Written direct debit authorisation must exist •The paying party must be informed of the mandate

details before the first collection via SEPA CORE Direct Debit (e. g. via pre-notification) •The first collection of a SEPA CORE Direct Debit is

carried out with the “FIRST” sequence •The date of migration pre-notification is used as the

date for signing the mandate •This reclassification does not apply for collections

issued today via debit order under the debit order procedure (Abbuchungsauftragsverfahren). Here, new mandates (only between companies) are to be obtained.

17

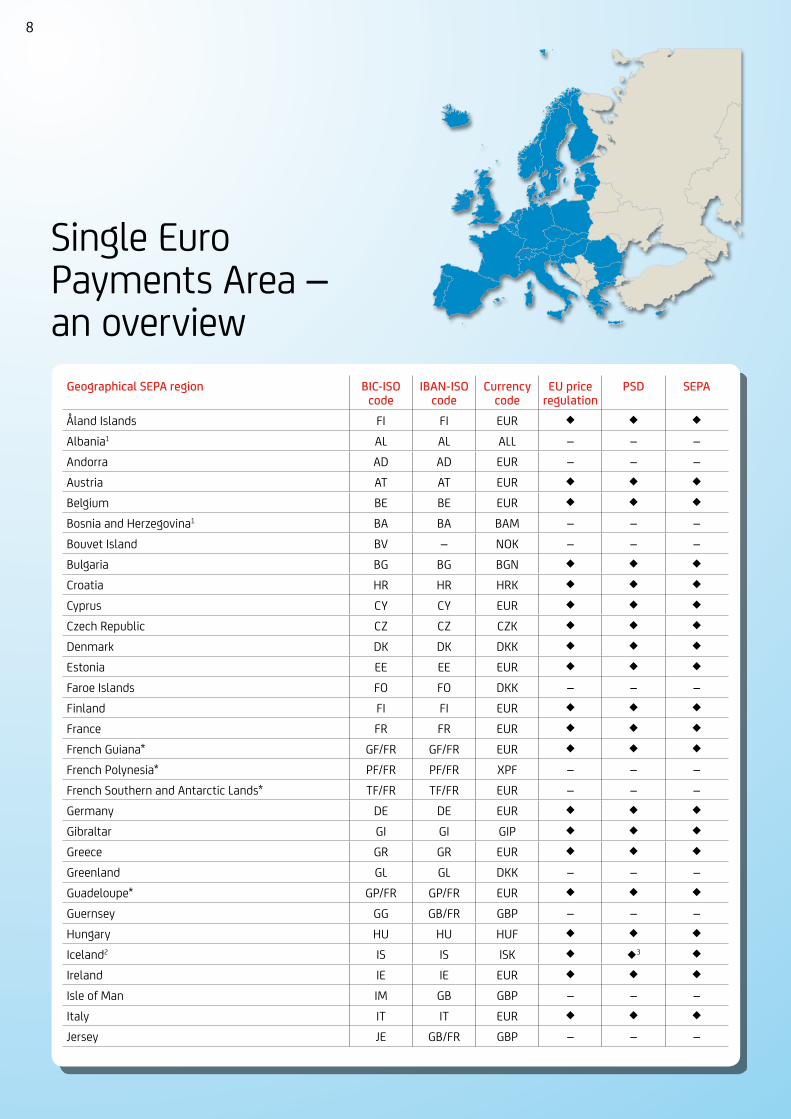

Example of a mandate migration

Example of a separate information notice to reinter-pret a written collection authorisation procedure with simultaneous pre-notification.

“Due to the migration to the SEPA payments system, we are converting our direct debit col-lections to the standard European SEPA CORE Direct Debit Scheme from 1 January 2014. The direct debit authorisation that you have already issued will continue to be used as a SEPA Direct Debit mandate in this context. This direct debit mandate is identified by the 0815 mandate reference and our creditor identifier DE02ZZZ01234567890, which we will state in all future direct debits. You do not need to under-take any action as we will implement this conver-sion. All such direct debits will be collected from 1 January 2014 monthly as of the 15th day of the month from your following account: IBAN: DE4012345678000123456, BIC: MUBADEFFXXX.”

reinterpretation of existing direct debit authorisa-tion by using the remittance information field: The form for communicating the reinterpretation is generally free. For this reason, a note relating to the option to reinterpret existing authorisation by informa-tion within the remittance information field of a DTA direct debit transaction can be found in publications. In other words, mandatory information for a reinter-pretation in the remittance information of the last DTA direct debit transaction will be transferred to the debtor.

example of a reinterpretation in the remittance informationASSOCIATION CONTRIBUTION OCTOBER 2013.

FUTURE DIRECT DEBITS WILL

BE COLLECTED BY SEPA

DIRECT DEBIT WITH OUR

CREDITOR ID DE99ZZZ01234567891

AND YOUR MANDATE REFERENCE

M123415. THE

COLLECTION OF THE CONTRIBUTION OF

EUR 55 WILL OCCUR AS OF THE FIRST DAY

OF EACH MONTH FROM 1 DECEMBER 2013

FROM THIS ACCOUNT.

YOUR ASSOCIATION TREASURER

This procedure to reinterprete existing authorisa-tions by using the remittance information field is cost efficient. It can help reduce the expense of the SEPA conversion, and is consequently interesting for the creditor. This communication form nevertheless carries risks to which we would like to draw your at-tention to. In particular, it does not ensure that the recipient reads the information. Remittance informa-tion generally conveys detailed information about the transaction. It is not a usual channel of information for information that is not directly connected with the payment. In addition, there is no indication as to whether the account holder receives his or her ac-count information. Under certain circumstances, this is not the case until the end of the respective quarter. The risk also exists that the remittance information is displayed in abbreviated fashion on the debtor’s ac-count statement because not all lines are transmitted. For these reasons, we cannot recommend this type of communication, and at this juncture make reference for only informational purposes to a procedure that exists on the market.

18

The SEPA Direct Debit mandateSEPA CORE Direct Debit mandate

The SEPA Direct Debit mandate is based on the “SEPA CORE Direct Debit Scheme Rulebook” issued by the European Payments Council (www.europeanpay-mentscouncil.eu). The design of the mandate is not rigidly determined – only the content. Abridged man-date texts in various languages can be found here:

www.europeanpaymentscouncil.eu/content.cfm? page=core_sdd_mandate_transalations

the mandate must also bear the following information:•Name, address and creditor identifier. The latter is

issued by the German Central Bank www.bundesbank.de/zahlungsverkehr/ zahlungsverkehr_sepa_identifikation.php•The specification whether the mandate is for recur-

rent payments or for a one-off payment •Name, account details and signature of the account

holder/debtor•Place and date need to be provided

the mandate reference assigned individually by the creditor •in conjunction with the creditor identification number

uniquely identifies the mandate •is up to 35 alphanumeric digits long and •can be included in the mandate or be notified to the

payer later.

Harmonised mandate

A harmonised mandate offers the option of obtaining a SEPA CORE Direct Debit mandate and a legacy direct debit authorisation at the same time. Through the legal reinterpretation of the direct debit authorisation, the use of harmonised mandates is no longer neces-sary. Now standard SEPA CORE Direct Debit mandates can already be obtained and also used up to the time of migration for an authorised direct debit mandate.

SEPA Business to Business (B2B) Direct Debit mandate

The SEPA Business to Business (B2B) Direct Debit mandate is based on the “SEPA Business to Business Direct Debit Scheme Rulebook” issued by the Euro-pean Payments Council (www.europeanpayments-council.eu). The design of the mandate is not rigidly determined – only the content.

Abridged mandate texts and a harmonised mandate are available. Text modules and samples for the SEPA Busi-ness to Business (B2B) Direct Debit can be found here: www.europeanpaymentscouncil.eu/content.cfm?page=sepa_b2b_dd_mandate_translations

19

the mandate must also bear the following information:•Name, address, account details, signature of the ac-

count holder / debtor and creditor identifier number. The latter is issued by the German Central •The specification whether the mandate is for recur-

rent payments or for a one-off payment•Name, address, account details and signature of ac-

count holder / debtor•Place and date need to be provided

We recommend that a mandate reference be provided at the same time, as the debtor requires to store the mandate at their bank.

20

Sepa Core direct debit mandateMandate reference – to be completed by the creditorCREDITOR’S NAME & LOGO

authorisation statement:By signing this mandate form, you authorise (A) {NAME OF CREDITOR} to send instructions to your bank to debit your account and (B) your bank to debit your account in accordance with the instructions from {NAME OF CREDITOR}.As part of your rights, you are entitled to a refund from your bank under the terms and conditions of your agreement with your bank. A refund must be claimed within 8 weeks starting from the date on which your account was debited.

Upper field texts:1 Your name / Name of the debtor(s)2 Your address / Street name and number3 Postal code / City4 Country5 Your account number / Account number – IBAN6 SWIFT BIC 7 Creditor name8 Creditor identifier9 Street name and number

10 Postal code / City 11 Country 12 Type of payment: Recurrent payment or one-off payment 13 City or town in which you are signing / Location / Date

Signature textsSignature(s)Please sign hereNote: Your rights regarding the above mandate are explained in a statement that you can obtain from your bank.

Lower field texts:Details regarding the underlying relationship between the creditor and the debtor – for information purposes only.14 Debtor identification code / Write any code number here which you wish to have quoted by your bank15 Person on whose behalf payment is made / Name of the Debtor Reference Party: If you are making a payment in respect

of an arrangement between {NAME OF CREDITOR} and another person (e. g. where you are paying the other person’s bill) please write the other person’s name here. If you are paying on your own behalf, leave blank

16 Identification code of the Debtor Reference Party17 Name of the Creditor Reference Party:

Creditor must complete this section if collecting payment on behalf of another party18 Identification code of the Creditor Reference Party19 In respect of the contract: Identification number of the underlying contract20 Description of contract

information texts:Please return to creditor’s use only

21

Sepa business to business direct debit mandateMandate reference – to be completed by the creditorCREDITOR’S NAME & LOGO

authorisation statement:By signing this mandate form, you authorise (A) {NAME OF CREDITOR} to send instructions to your bank to debit your account and (B) your bank to debit your account in accordance with the instructions from {NAME OF CREDITOR}. This mandate is only intended for business-to-business transactions. You are not entitled to a refund from your bank after your account has been debited, but you are entitled to request your bank not to debit your account up until the day on which the payment is due.

Upper field texts:1 Your name / Name of the debtor(s)2 Your address / Street name and number3 Postal code / City4 Country5 Your account number / Account number – IBAN6 SWIFT BIC 7 Creditor name8 Creditor identifier9 Street name and number

10 Postal code / City 11 Country 12 Type of payment: Recurrent payment or one-off payment 13 City or town in which you are signing / Location / Date

Signature textsSignature(s)Please sign hereNote: Your rights regarding the above mandate are explained in a statement that you can obtain from your bank.

Lower field texts:Details regarding the underlying relationship between the creditor and the debtor – for information purposes only.14 Debtor identification code / For business users: write any code number here which you wish to have quoted by your bank15 Person on whose behalf payment is made / Name of the Debtor Reference Party: If you are making a payment in respect

of an arrangement between {NAME OF CREDITOR} and another person (e. g. where you are paying the other person’s bill) please write the other person’s name here. If you are paying on your own behalf, leave blank

16 Identification code of the Debtor Reference Party17 Party on whose behalf the creditor collects the payment Name of the Creditor Reference Party: Creditor must complete

this section if collecting payment on behalf of another party18 Identification code of the Creditor Reference Party19 In respect of the contract: Identification number of the underlying contract20 Description of contract

information texts:Please return to creditor’s use only

22

Pre-notificationPre-notification is a compo-nent of the SEPA Direct Debit scheme for CORE and B2B Direct Debits.

Original rulebook text: “The pre-notification must be sent by the creditor at least 14 calendar days before the due date unless another timeframe is agreed be-tween the debtor and the creditor.”

•The amount and the due date must be communicat-ed to the debtor. Furthermore, the creditor identifier and the mandate reference shall be provided.•The timeframe of 14 calendar days (two weeks)

before payment can be altered or shortened in the contract terms (e. g. on the day of submission).•A contractual waiver of the pre-notification regula-

tions is not allowed according to the rulebook, i. e. a correct SEPA Direct Debit payment must be an-nounced using a pre-notification. It is not the bank’s responsibility to ensure that a pre-notification has been issued; this responsibility solely concerns the relationship between the creditor and debtor.•The 14 day period for the pre-notification is calcu-

lated from the due date.•There are no rules stipulating the medium in which

a pre-notification should be transmitted. Possible methods include by letter, contract, invoice, text message, e-mail, fax, via the internet, General Terms and Conditions …

•The pre-notification and the reinterpretation infor-mation must be conveyed to the account holder. If you have no direct address information (e. g. grand-mother pays her grandson’s mobile phone charges), you should notify your counterparty to forward the pre-notification to the payer/account holder, or you should obtain the divergent address information. When sending the pre-notification to the divergent payer, please also comply with data protection law requirements pursuant to Section 203 of the German Penal Code (StGB).•What happens if the debtor is incorrectly informed

about the collection date or the collection amount? In such instances, the debtor cannot be forced to default (reminder fees, return fees …). The efficacy of the mandate, and consequently the authorisation of submitted direct debits, is nevertheless unaffected by an erroneous or missing notification

23

Pre-notification – one-off/recurrent

For recurrent direct debits where the amount to be debited remains the same, a single notification detail-ing the date of the first debiting and the timetable for subsequent payment due dates can be issued to the debtor.

•Example for an individual pre-notification per collec-tion: Telephone bill dated 5.12:

“The payment amount of EUR 68.11 will be collected by using the SEPA Direct Debit with mandate 4711 for creditor identifier DE321 from your account IBAN DE123 with HypoVereinsbank HYVEDEMM with due date 15 December 2013. Please ensure that there are sufficient funds on your account to cover the payment.”

•Example for a unique pre-notification:

Tenancy agreement: “The rent of EUR 500 will be collected by using a SEPA Direct Debit with mandate 4712, for creditor identifier DE321 from your account IBAN DE123 with HypoVereinsbank HYVEDEMM every first of the month, starting on 1 February 2013. If the due date falls on a week-end or holiday, the due date will be moved to the next working day.”

Creditor identifierCreditor identifier for SEPA Direct Debit presenters in Germany

Creditors are registered with a standardised, unique and harmonised identification number (creditor identifier).

•Digits 1–2 contain the ISO country code for Germany (DE) as the country issuing the creditor ID •Digits 3–4 contain the check digits, which are calcu-

lated in the same way as the IBAN check digits (ISO 13616) •Digits 5–7 contain the creditor business code for

which the direct debit creditor can assign any num-ber of alphanumeric digits. These three digits are “ZZZ” by default. •The following digits 8–18 contain the national

identification feature for the direct debit creditor in consecutively ascending numbering. The eighth digit of the creditor identification number is always oc-cupied by “0” until further notice •Foreign creditor identifiers may contain a total of

35 digits

DE

ISO country code

Check digits

Creditor business code

National identification feature

02 ZZZ 01234567890

24

The individual who is the economic beneficiary of the creditor account that submits the direct debit requires the creditor identifier.

notes for particular submitter groups:registered associations:Registered associations submit applications using their association name, and not in the name of the first chairperson or treasurer

german homeowner associations (Wegs):Application made by the administrator, potentially through a resolution passed by a homeowners’ meet-ing. Since the administrator of the joint property in WEGs represents the semiautonomous community with respect to third parties (utilities), as well as in the case of the collection of monthly advances, and the account must now be managed in the name of, and for the account of, the homeowner association, the homeowner association’s legal representative, in other words, the administrator, must apply to the Bundes-bank for a creditor identifier for each homeowner association. The creditor identifier is unchanged if the administrator changes.If the management account into which the rental payments are made is held in the owner’s name and the administrator has statutory authority only over the account, the owner’s creditor identifier is to be used. Creditor identifiers for WEGs are generally applied for as “Other Associations of Individuals” at the Bundesbank.

married couples:have to select the item “Other Associations of Indi-viduals” and then “Other Associations” at the Bundes-bank if they wish to share one creditor identifier.

how do i get a creditor identifier?It is issued by the German Central Bank. One creditor identifier is required for each legal entity (direct debit creditior).www.glaubiger-id.bundesbank.de

25

“Direct debit” returns processCountry digits example (fictitious!)Reject Return prior to settlement by the creditor bank within the

scope of the clearing and settlement mechanism or by the debtor bank

Debit cannot be processed, e. g. late submission, wrong format, wrong data, account closed, cus-tomer deceased

Refusal Return prior to due date initiated by creditor Debit account frozen by the debtor for individual or all direct debits

Return Return after interbank settlement by the debtor bank up to 5 TARGET days after due date

Debit not possible, e. g. account closed, insuffi-cient funds, customer deceased

Refund Return by the debtor bank up to 8 weeks after due date (later only due to absence of mandate) by debtor, not possible for SEPA B2B Direct Debits

Objection by the debtor without reason stated

Revocation Call back of the direct debit by the creditor/creditor bankReversal Cancellation of the direct debit by the creditor after settle-

ment via order for a credit transfer

Cycle of a SEPA Direct DebitMandate management – issuing

Creditor

mandate manage-ment

mandate form

debtoroptional:

•Create a unique mandate reference•Specify the date of the direct

debit booking or different agreement (pre-notification)

26

Mandate management – approval

Creditor

mandate manage-ment

mandate signed

b2b onlyAuthorisation order for direct debit (storing the mandate)

debtor bank

debtor•Data capture/scanning•Add mandate reference

if necessary•Archive

Mandate management – pre-notification

Creditor

mandate manage-ment

•Ensure cover for debit•Possibly:

Issue an order to block the mandate (refusal)

debtor bank

debtorinformation regarding:

•Execution days / frequency•Amount

@Not later than 14 days before due date(a different agreement is possible)

27

Direct debit collection

Creditor

mandate manage-ment

Possibly•Pre-information from

the bank•Cover for debit•Mandate changes

Possible errors•Return before booking (reject)•Return before booking (refusal)

Creditor bank

debtor bank

debtorSepa Core direct debit: First execution (due date - 5)•Recurrent execution (due date - 2)•Final execution (due date - 2)•One-off execution (due date - 5)Sepa b2b/Cor1 direct debit•Due date - 1info•Mandate reference•Possible mandate changes

@Clearing

XML.pain

Checks•Formal•Blockings

Booking of the direct debit

Creditor

mandate manage-ment

Possible return after booking (return) (lack of funds, incorrect account, no B2B mandate)•CORE/COR1: due date + 5•B2B: due date + 2

Creditor bank

debtor bank

debit

debtorCredit

Settle-ment

Checks•Cover•Contents

28

Return due to objection up to 8 weeks

Creditor

mandate manage-ment

Creditor bank

debtor bank

CORE only: refund to debit

Return after booking due to objection (refund)Debit day +8 weeks

debtorReturn after book-ing due to objection (Refund) Due date +8 weeks

Refund due to objection within 13 months

Creditor

mandate manage-ment

Creditor bank

debtor bank

Check man-date within 10 days

CORE only: refund to debit up to 13 months

Check mandate receipt time within 30 day

Return after book-ing due to lack of mandate (refund not authorised)

debtorPresent mandate

mandate Present within the next 7 days

14

2

3

6

5

29

UniCredit Bank AG product range and SEPA servicesWe offer you SEPA payment services as part of our product range with various options such as SEPA Credit Transfer (credit transfer) SEPA CORE/COR1 Di-rect Debit and SEPA B2B Direct Debit as well as other SEPA services.

SEPA Direct Debit COR1

Since November 4th, 2013 direct debits with a shorter presentation period (COR1) are accepted by all banks in Germany.

DTAZV conversion into SEPA data format

Payments made via DTAZV and are subject to the EU price regulation, will be processed as SEPA payments (possible until February 2014). To do this, the orders must satisfy the following conditions or include the following information:

•Name of the beneficiary •The beneficiary’s international bank account number

(IBAN)•The bank identification code (known as the BIC or

SWIFT code) of the beneficiary’s bank•The amount in euros•The price option SHARE (shared fees)

Should it be not possible to convert the order (e. g. the beneficiary’s bank is not SEPA-ready, or it is an urgent order) or if the order includes additional instructions, the payment will be executed as a conventional cross-border payment.

Special UniCredit service – SEPA Credit Transfer (SCT)

Since some banks are not ready for SEPA yet, execu-tion of SEPA payment orders may prove impossible. As a special service for our customers, we automatically process payments that cannot be executed in a SEPA-compliant manner in the execution type most benefi-cial for the customer.

Same-day salary paymentsMany companies want to ensure their employees re-ceive their salary payments on time. We offer a special solution so that you do not have to split the salary data files yourself and divide them by recipient at UniCredit or third-party banks in the SEPA area. The special service for SEPA salary payments enables the salaries of all your employees to be booked on the same day (irrespective of whether payment recipients have their account with UniCredit or another bank within the SEPA area).

UniCredit offers this special service as part of its “SEPA Credit Transfer Preferred” product. This can now be individually managed for any data file submitted. In this way, SEPA Credit Transfers, where the payment recipients are with UniCredit, are booked on the same day on the debit and credit sides as standard. If the payment recipient is with a third-party bank, the set-tlement is also made on the same day by EBA clearing.

30

SEPA ultimate creditor – Different account used for returns

When submitting SEPA Credit Transfers (SCT) and SEPA Direct Debits (SDD), and entering the beneficiary or debtor for direct debits in the data file submitted, you can also indicate an account to which any return payments should be made in addition to the account of the submitting party. This is a particularly attractive option for companies which have standardised return processing systems for all their sites. This product will also appeal to public coffers which collect direct deb-its and transfers centrally on behalf of various local public bodies, such as tax offices, municipalities and public authorities.

Urgent XML euro payments – same-day

Urgent XML euro payments are same-day payments that can be mandated in XML format analogously to SEPA payments.

Target countries:•national payments within Germany•payments in EU/EMS countries

Send us your urgent euro payment mandates electron-ically e. g. through our UC eBanking prime software in pain.001 XML format by the 16:00 hours cut-off time. Execution to the beneficiary’s bank then occurs with the same-day value date. We execute payment orders that you send us after this cut-off time on a “best ef-forts” basis.

Data conversion is required since the TARGET2 large-value payment system is still based on MT format.

Urgent XML euro payments relate to individual payments that can only be processed on a single payment basis, and are not included among SEPA products.

Depending on the order type submitted, you also have the option of mandating a payment confirmation to be sent to the beneficiary by email or fax. You can find further information in the SEPA customer information appendix – technical specifications and formats.

XML-AZV

From now on, you can also mandate your foreign pay-ments (e. g. currency payments and euro payments to non-SEPA countries) electronically in the ISO-20022-XML format. We support this based on CGI (Common Global Implementation) standards. You can find more detailed information about the CGI standard here: www.swift.com/corporates/cgi/index. You can trans-mit your XML orders through the following electronic supply channels: EBICS, SWIFTnet or Host-to-Host.

Since the XML-ISO-20022 order format allows a greater data spectrum than the SWIFT MT103 format used in the interbank format, in individual cases it can mean that not all data fields can be transferred to the final beneficiary’s bank.

Payment Status Report/pain.002

The Payment Status Report is an electronic error log. It contains rejected payments submitted by SEPA Credit Transfer (pain.001) or SEPA Direct Debit (pain.008). The customer is sent incorrect files and transactions with an error code by e-mail before booking.

31

The XML “pain.002” data format contains the origi-nal fields of the submission and serves to check the submitted data file and make corrections quickly for resubmission. The pain.002 has become important because of the SEPA Direct Debit, which is sometimes cleared five days before the due date for other banks and is checked there before the booking date. If the paying bank rejects the direct debit before the booking date, these bank-initiated rejections (reject) e. g.

•Paying party’s account does not exist •Paying party’s account cannot be booked or

customer-initiated rejection (refusal) e. g.•Mandate block by debtor •General direct debit block•Objection of the collection before booking

will immediately be sent to submitter before booking using pain.002.

Presentation error reports were previously restricted to just the rejection of payments and files by the remit-ting bank (reject) e. g.

•Transfer to IBAN with incorrect check digits •Direct debit to non-SEPA-ready bank•Reject transfer file due to lack of cover

These rejections before booking – irrespective of whether by the remitting bank or the debtor’s bank – can now be immediately reported back to the cus-tomer without media conversion in XML format for automated processing.

The pain.002 message is comparable with the current presentation error report which immediately sends a file to the presenting party via fax/post or cancellation report. Optionally, a Payment Status Report/ pain.002 can also be sent to the customer for returns after they are booked. Please pay attention to our technical bro-chure (Attachment to the SEPA Customer Information Brochure – German Technical Specifications and For-mats) for further information on the technical configu-ration rules for the payment status report (pain.002).

SWIFTNet FileAct

With SWIFTNet, corporate customers have the option of sending and receiving messages directly via the SWIFT network. Participating firms receive their “own SWIFT access and SWIFT code”. Communication via SWIFT replaces the former classic eBanking access.

The advantages of this are clear: one standard for communication worldwide, extremely secure and rapid communication with maximum availability. The SWIFT connection has been possible for corporate customers of UniCredit since 2005 and the scope of services is constantly being expanded. SWIFTNet File-Act offers the opportunity to exchange finance-related messages of various formats in files via the SWIFT network. UniCredit has extended its existing SWIFTNet FileAct services to include the following formats:

•SEPA Credit Transfer and SEPA Direct Debit via SWIFTNet FileAct. Our customers can therefore sup-ply SEPA payments via SWIFTNet FileAct.•SEPA status report (pain.002) via SWIFTNet FileAct.

This means our customers can receive the SEPA sta-tus report via SWIFTNet FileAct

32

IBAN service from UniCredit

•IBAN conversion service•IBAN to-and-from method for determining and up-

dating IBAN and BIC (for accounts held at UniCredit). Data structure of the file to be checked:

field Length

Country (ISO code) 2

Customer 5

Customer name 30

BIC old 11

IBAN old or sorting code/account old 22

BIC new 11

IBAN new or sorting code/account new 22

Sorting code new 8

Return code 2

iban service portalDo you want to make maintaining and updating your master customer data significantly easier? Use the IBAN service portal from Bank-Verlag GmbH to con-vert German account numbers and sorting codes to IBAN and BIC! As part of the introduction of SEPA, this new service has been set up and is supported by all banking associations and UniCredit.

A registration fee of 45.00 euros (plus VAT) and a use-fee of 27.50 euros (plus VAT) are incurred for each file to customers of all banks. An 8-digit initial pass-word is required to register with the online portal. You will receive your entry password for UniCredit and a brief guide from your Cash Management & eBanking specialist.

IBAN service portal https://www.iban-service-portal.de

Further solutions for master data conversion within companies (software solutions) are being implement-ed at Bank-Verlag GmbH.

example of an iban-forward CSV dataset:DE;;Ref;;;37060590;1234567893DE;;Customer;;;87095934;345679DE;;Number;;;87050000;9999999996example of an iban-return CSV dataset:DE;;Ref;;;37060590;1234567893;;GENODED1SPK;DE79370605901234567893;;00DE;;Customer;;;87095934;0000345679;;GENODEF1Z01;DE37870959340000345679;;00DE;;Number;;;87050000;9999999996;;CHEKDE81XXX;DE64870500009999999996;;00return codes (examples)00 → Conversion was successful10 → Invalid bank code11 → Erroneous account number structure13 → Bank code/account number combination not permitted

33

IBAN referencing through Bundesbank registry

Since June 2013, field 14 of the Bank Routing Code Directory also states whether special IBAN calcula-tion is required for this bank code. The Bundesbank’s extranet then includes detailed rules allowing to do a proprietary IBAN calculation. The bank codes file in-cludes an identifier for each bank code that describes the calculation of the IBAN (status as of December 2013):•Standard calculation for almost 60 per cent of bank

codes

•DE country identifier•Check digit based on Modulo 97-10 (ISO 7064)•Bank code•10-digit account number, with preceding zeros on

the left-hand side

•57 divergent rules for around 1/3 of bank codes, e. g.:•Donations accounts and dummy accounts are

converted into genuine account numbers for the purpose of IBAN calculation.•The accounts are not entered in the IBAN using

preceding zeros on the left-hand side. Instead, the zeros are placed at the end in the case of certain banks.•Certain banks utilise a divergent bank code for cal-

culating the IBAN.•Mergers at some banks have created extensive

divergences.•No IBAN calculation is possible for 173, not deleated,

bank codes because the respective banks do not participate in the payments system.

IBAN conversion service in Europe with the cooperation partner Experian

More and more internationally-active companies are looking for a solution to convert account numbers/sorting codes into IBAN/BIC. This data conversion is of particular interest to companies that wish to convert their payments across the entire SEPA zone to SEPA format.

The Bank Wizard software from our cooperation partner Experian enables companies to convert the existing account data of their business partners into IBAN and BIC. This rapid electronic data conversion is the complete opposite of the laborious, time-con-suming and costly procurement of data from business partners. Experian is the leader in data conversion and bank account validation. If you are interested in learn-ing more, please contact your Cash Management & eBanking specialist.

34

IBAN BIC calculator and UC SEPA format check

You can convert specific HVB accounts online us-ing the account number/ bank code in IBAN/ BIC at www.hvb.de/sepa. At this Internet address, you can also validate XML files (pain.001 and pain.008) in DK format to check whether they are correctly structured and filled, and whether they contain permissible BICs. Here, you will receive free-of-charge an extensive test report, an XML file with commentaries and a pain.002.

Electronic account information at UniCredit

As of 2008, an end-of-day customer statement or intraday statement may include SEPA transactions. SEPA-specific information – e. g. end-to-end reference – is organised so that it can be automatically pro-cessed by customers. Because a harmonised standard will be used, multi-bank capability will also be avail-able in the future.

•MT940 end-of-day statements in previous SWIFT structure converted to SEPA data•New/additional transaction codes (BTC) for electronic

search of bank statements for SEPA Direct Debits, SEPA Business to Business (B2B) Direct Debits, SEPA Credit Transfers and return transactions•MT942 intraday statements in previous SWIFT struc-

ture converted to SEPA data•DTI preparation of account booking adapted to SEPA

data. In the case of DTI, unlike MT940, separate files will be created for legacy payment transactions and SEPA transactions

provision of all account statements in iSo 20022 XmL format:•camt.052 (advice, in ref. to MT942)•camt.053 (statement of account, in ref. to MT940)•camt.054 (collector information, in ref. to DTI).

The XML formats can be provided in parallel to the well-known SWIFT/DTI format in order to enable a gradual and secure transition into the XML world.

UC eMandateManager

We provide you with a web-based mandate manage-ment system to support your migration to SEPA Direct Debits. In future, you can manage your man-dates in this application:

•New structure of mandates •Migration of direct debit authorisation •Management of mandate changes •Management of the use of mandates (sequence)•Deletion of mandates

As well as search and evaluation options, it is also possible to generate direct debits from the mandate database.

For the migration of collection authorisations, we ad-ditionally offer the following functions:

•Transfer of your debit authorisation by importing CSV or DTAUS files •Conversion of your DTAUS files into •SEPA Direct Debits: calculation of correct due date,

sequence check, etc.•SEPA Credit Transfers: incl. text-key mapping for

SEPA purpose code•Automatic processing of direct debit returns by pro-

cessing pain.002 files •Tracking of amendments using the history function

35

A further option offers the possibility to integrate UniCredit mandate management into your existing system environment (ERP systems) using online web services.

HVB eFIN

HVB eFIN is our multi-bank-enabled electronic banking software for business and corporate customers. You can execute your payments simply and cost efficient based on FinTS standards (formerly HBCI). Clear design and uncomplicated use ensure that you can keep a clear overview when managing your payment orders.

HVB eFIN is fully SEPA-enabled and supports all cur-rent SEPA formats in the SEPA payments system:

•SEPA Credit Transfer, SEPA Scheduled transfers and SEPA Multiple transfers•SEPA standing order•SEPA CORE Direct Debit, SEPA COR1 Direct Debit and

SEPA B2B Direct Debit as summary orders or poten-tially in the case of third-party banking connections also as individual orders•SEPA Direct Debit return

In addition to further extensive functions to process and organise your domestic and foreign payments, the current version of HVB eFIN supports you when converting to SEPA:

•automatic supplementation of saved domestic pay-ment master data to include IBAN and BIC (with automatic IBAN/BIC calculation)•simplified entry of SEPA orders using Excel

export/import•SEPA information area with IBAN calculator, link to

interactive checklist and more in-depth information especially for HVB eFIN customers•converting your existing domestic payment orders

(individual transfers, DTA) according to SEPA•entry and processing of SEPA Direct Debit mandates

You can download more information and the current SEPA-enabled version at www.hvb.de/efin.

36

UC eBanking prime

With UC eBanking prime, we are making available to you a multi-bank and multi-location enables software for payment transactions and cash management.

In the case of UC eBanking prime, your entire data remain where you have direct access to them – at home. Based on this “domestic environment”, we structure your individual solution to include optimal security and comfortable handling.

amendment/improvements in Version 4.3.0

Sepa conversion tools•Migration of domestic payment system master data

to SEPA master data using automatic IBAN/BIC calcu-lation•Notes relating to the migration in the local payment

system entry fields•Conversion option for periodic domestic payments•Conversion option for domestic payments templates•Conversion of DTAUS files in the case of uploads•IBAN/BIC calculator

Sepa mandate management•Fully integrated loading and administration of SEPA

mandate•Allocated, digital filing of scanned (signed) mandate

letters•Mandate import of payment file from payment sys-

tem file (optionally via DTAUS or SEPA)•CSV mandate import via the Master Data Tool (MDT)•Mandate export to mass mailing letters for form

printing•Status administration for SEPA mandate•Transfer of mandate data in direct debits•Mandate history for modification-relevant data•Mandate modifications with transfer of correspond-

ing data in direct debits

payments•Manual entry of COR1 Direct Debits•Balance of payments reporting management for Z4,

Z8 and Z10 reports•Automatic generation of IBAN/BIC in SEPA master

data if only bank code/account available•Coverage of DFÜ Agreement Annex 3 Version 2.7

Other services from UniCredit

•Individual parameter in input file to request single or batch booking on account•Regular customer newsletter regarding current SEPA

developments.•Customer events and presentations on the topic of

SEPA.•SEPA cross-border credit transfer with automatic

address completion by UniCredit (required for pay-ments to Switzerland).•Administration of standing orders for credit transfer

and direct debits (CORE and B2B)

37

SEPA – opportunities and benefitsSEPA will deliver benefits and improvements in pay-ment transactions for all market participants by sim-plifying the pan-European infrastructure and eliminat-ing trading barriers.

Besides the simplification of the European payment product offering, the shorter settlement times will constitute a key benefit for the parties involved in pay-ment transactions.

Consumers Corporate customers

public sector customers

Pan-European SEPA standards x x xNew payment processing products x x xOne account for outgoing payments for a single Europe x x xCost and price transparency x x xStandardised processes with reduced cost/complexity x x xFixed settlement times x x xNew European direct debit (CORE Direct Debit) x x xHarmonised legal framework x x xTransaction pooling – improved liquidity management x xEnd-to-end automated processes x xDebit cards accepted throughout the EU x x xMore card transactions/fewer cash transactions x x xLower terminal costs x xWider range of clearing services x xLower costs for standard software and services x x

More consumer rights, especially with the SEPA Direct Debit

The SEPA Direct Debit offers better consumer protec-tion compared with the legacy direct debit scheme. Consumers have the right to issue the following orders to their banks:

To limit direct debit bookings to a certain amount, a certain duration, or to both, to block an account en-tirely for direct debits, as well as to permit or exclude direct debits from certain creditors.

The SEPA CORE Direct Debit can also be returned within eight weeks after booking without stating rea-sons. These eight weeks have already been valid for the legacy German collection authorisation procedure since mid-2012. If the account holder has not issued any mandate previously, he or she can still revoke a direct debit charge up to 13 months later.

38

Recommended actions for our customersSEPA: A check from A to SEPA – your payments today and in the future

Sepa – Single euro payments areaThe extended migration period for previous national payment systems within the euro mass payments sys-tem in euro countries in Europe ends on 31 July 2014 (February 2016 in non-euro countries, too).

For us in Germany, especially for companies, this means that you:

•can no longer submit files in the DTA data format for credit transfer and direct debits to your banks, but instead from then on only in XML format;•require IBAN and BIC (IBAN-Only option: nationally

from 1 February 2014, cross-border from 1 February 2016) for payments in euro;•can only utilise direct debits with the new SEPA

schemes;•... and much more.

We would like to guide you through the conversion of your payment transactions with the interactive guide-lines available on the Internet. Simply select the topics that are relevant to you and then explore the detailed topics and information.

We recommend that you download the entire check-list with the “Start SEPA Check”. This will allow us to guide you through all relevant aspects. If needed, you can also just select and work through an individual step.

After you have selected your topics, you can print out and use your result as a checklist.

Sepa Check

Step 1Determining the related EUR payment transactions

Step 2Determining the related areas and interfaces

Step 3Implementation of product-independent modifications (organisational)

Step 4Implementation of cross-product modifications (technical)

Step 5Implementation of credit transfer (SEPA Credit Transfer)

Step 6Implementation of direct debit (SEPA Direct Debit)

Step 7Conversion to new account information

Step 8Help and service from HVB in your SEPA conversion

Source: www.hvb.de/Sepa

Perform the interactive SEPA check online at www.hvb-sepa.de

39

SEPA Direct Debit mandate FAQs1) The difference between a

collection authorisation for a legacy direct debit mandate and the SEPA mandate

Question: What is the difference between a collection authorisation for a direct debit and the mandate for a SEPA CORE Direct Debit?

answer:•The SEPA mandate contains a clear reference of the

direct debit (creditor identifier and mandate number).•In a dispute of the mandate issued by the debtor,

the creditor must deliver the SEPA mandate to the debtor via its bank. In collection authorisations for direct debits, the dispute has to be resolved bilater-ally between the creditor and the debtor without any intervention by the banks.•A collection authorisation for a legacy direct debit

does not expire after a period of 36 months if no col-lection had been processed.•The SEPA schemes also define the possibility of an

electronic mandate authorisation.

2) Process of a mandate submission

Question: Who takes responsibility for the first step of the mandate submission?

answer:•As with the collection authorisation for a direct debit,

the creditor generates a preprinted mandate form with their details and subsequently allows the debtor to sign it.•The signed mandate will then be collected/•scanned by the creditor who then commences the

collection process.•In the case of a SEPA B2B Direct Debit, the debtor

needs to present the mandate to its bank without delay.

40

3) Number of mandates per creditor/debtor relationship

Question: Is it possible in a single creditor/debtor re-lationship to have many different mandates and does attention possibly have to be paid to ensure that every direct debit is collected using the correct mandate reference?

For example, if a utility company provides the elec-tricity, gas and water for the same customer. In this case, is one single mandate for the individual creditor/debtor relationship sufficient (i. e. one mandate for all three utilities), or is it necessary for a separate man-date to be issued for every contract (one mandate for each separate utility)?

answer:There are two options. In this situation, the mandate system should be constructed around the specific requirements of the creditor. A later automatic change in the system without having to reissue a new man-date is only possible going from option “2” to option “1”, not from option “1” to option “2”. option 1: A harmonised mandate for all contractual relations between the same creditor and debtor. Here only one mandate is issued.option 2: Multiple mandates issued to coincide with the number of contractual relations between the same creditor and debtor. Each of these mandates must then be separately issued with their own man-date reference. The sequence of payments (first/final/recurrent/one-off) must be individually tailored to each mandate.

3.1) Number of mandates per creditor/debtor relationship;

about option 1: A harmonised mandate for all con-tractual relations between the same creditor and debtor. Here only one mandate is issued.advantage:•Easy to administer.disadvantages:•If the customer blocks its mandate, then all of the

direct debits from all of the contract relations are rejected. •Aside from that, should any separation between the

creditor and debtor take place, then new mandates have to be issued, as a mandate is only applicable to one creditor identifier. It may be changed, but you cannot divide it amongst two different companies if there are pending dispositions or outsourcing of a business field.

about option 2: Multiple mandates issued to coincide with the number of contractual relations between the same creditor and debtor. Each of these mandates must then be separately issued with their own man-date reference. The sequence of payments (first/final/recurrent/one-off) must be individually tailored to each mandate.advantages: •The debtor can block individual mandates.•The debtor has a clear overview which current pay-

ment responsibilities exist.•If the business field of the creditor is changed (for ex-

ample, electricity is sourced from a different provid-er), then a mandate can be passed onto the provider.

disadvantage: •Multiple contract obligations cannot be collected

with a single direct debit, as each transaction re-quires one individual mandate reference.

41

4) Mandate language

Question: In which language should the mandate text be produced?

answer:For a mandate within Germany, a mandate text in the German language along the lines of the Deutsche Kreditwirtschaft (DK – former Zentraler Kreditaus-schuss) recommendations is sufficient:•SEPA CORE Direct Debit (CORE/COR1)

www.die-deutsche-kreditwirtschaft.de/dk/ zahlungsverkehr/sepa/inhalte-der-sepa/ lastschrift.html•SEPA Business to Business (B2B) Direct Debit

www.die-deutsche-kreditwirtschaft.de/dk/ zahlungsverkehr/sepa/inhalte-der-sepa/ lastschrift.html

For a direct debit collected from abroad, the mandate text must be drafted in two languages•in the respective domestic language:•SEPA CORE Direct Debit (CORE/COR1)

www.europeanpaymentscouncil.eu/content.cfm? page=core_sdd_mandate_transalations•SEPA Business to Business (B2B) Direct Debit

www.europeanpaymentscouncil.eu/content.cfm? page=sepa_b2b_dd_mandate_translations

•as well as in English if possible

general rules:•www.europeanpaymentscouncil.eu/

knowledge_bank_detail.cfm?documents_id=175

5) Mandates for which countries

Question: In which countries can a mandate be is-sued?

answer:•Mandates can generally be obtained for all SEPA

member states*. However, not all banks currently support the SEPA Direct Debit. •All banks within SEPA member states which have the

euro as their currency have to support the SEPA CORE Direct Debit.•All banks within SEPA member states which do not

have the euro as their currency must support the SEPA CORE Direct Debit) from 31 October 2016.•There is no enforced implementation for the Busi-

ness to Business (B2B) Direct Debit or for the CORE Direct Debit with shorter presentation period (COR1).

The banks currently taking part can be found here: www.ebaclearing.eu under STEP2, SEPA Direct Debit and then under Participants.

* Please refer to pages 8 and 9 for SEPA countries

42

6) Changing a mandate

Question: How are changes to mandates implemented?

answer:Altered mandate data is conveyed with the direct debit (initially by the first debit after the change).The following mandate changes are permitted:•Creditor initiated•Mandate reference (provide old & new mandate

reference) •Creditor name (provide old & new creditor name)•Creditor ID (provide old & new creditor identifiers)•Debtor initiated•Account (provide old & new IBAN of the debtor pro-

vided that the accounts are within the same bank)•Banking institution (when bank institution changes

direct debit must be initiated again as a “first-time direct debit”)

Reasoning behind the forwarding of change notifications:•It provides information to debtor and enables the

debtor to give possible instructions to its bank (blockings, for example).

As a basic principle and especially in the case of Business to Business (B2B) Direct Debits, the credi-tor should advise the customer of any changes to the mandate that may have been made (in the pre-notification, for example), so that the debtor is able to transmit this information to his bank.

If the address changes (e. g. as a result of moving), the debtor name changes (e. g. through marriage), or the creditor’s bank in connection changes, no new man-date needs to be obtained. A special designation in the direct debit is not required in this case. If the identity of the debtor changes (e. g. change of tenant), how-ever, a new mandate must be obtained.

7) Mandate validity 36 months