Embed Size (px)

Citation preview

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

11 April 2013

Asia Pacific/Singapore

Equity Research

Utilities

Singapore Utilities Sector SECTOR REVIEW

Significant capacity growth ahead

Figure 1: Credit Suisse’s power generation model suggests reserve margin

could increase to 2007 levels

0%

10%

20%

30%

40%

50%

60%

70%

0

2000

4000

6000

8000

10000

12000

14000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Total Generation Capacity - LHS Peak demand - LHS Reserve Margin - RHS

(MW)

Source: Energy Market Authority, Company data, Credit Suisse estimates

■ Power generation capacity to grow by 30% in 2013–14E: Following the

completion of Singapore’s LNG terminal in 2Q13 which will increase gas supply into the country, power generation capacity is expected to increase by 3.0GW or 30% in 2013–14E. Based on the Credit Suisse demand-supply model, we expect reserve margin to increase to 47% in 2013E from 37% in 2011, and will return to the 2012 level only in 2020E.

■ Uniform Singapore Electricity Price (USEP) declined 23% in 1Q13: The increase in capacity has led to a 23% fall in the pool price in 1Q13, relative to a 13% fall in fuel costs. Vesting prices for contracts which commit gencos to sell a specified amount of electricity were also revised down in January 2013. However, we expect downside support to be provided by rational pricing behaviour given high acquisition price of generation assets, retail contracts locked in, and contribution from non-electricity sale.

■ Downgrade Sembcorp Industries to NEUTRAL: We downgrade

Sembcorp Industries to NEUTRAL (from Outperform; lower TP to S$5.10 from S$5.90) as we believe market earnings expectations for 2013 do not factor in any potential decline in profit from industry capacity additions. Within China Utilities, we switch our top sector pick from HNP (raise TP to HK$9.00 from HK$7.00) to CRP, given the risks of a fall in Singapore tariffs and higher capacity adds in CRP versus HNP. We maintain our UNDERPERFORM rating on YTL Power (lower TP to RM1.40 from RM1.82).

Research Analysts

Gerald Wong, CFA

65 6212 3037

Edwin Pang

852 2101 6406

Annuar Aziz

60 3 2723 2084

Louis Chua

65 6212 3024

11 April 2013

Singapore Utilities Sector 2

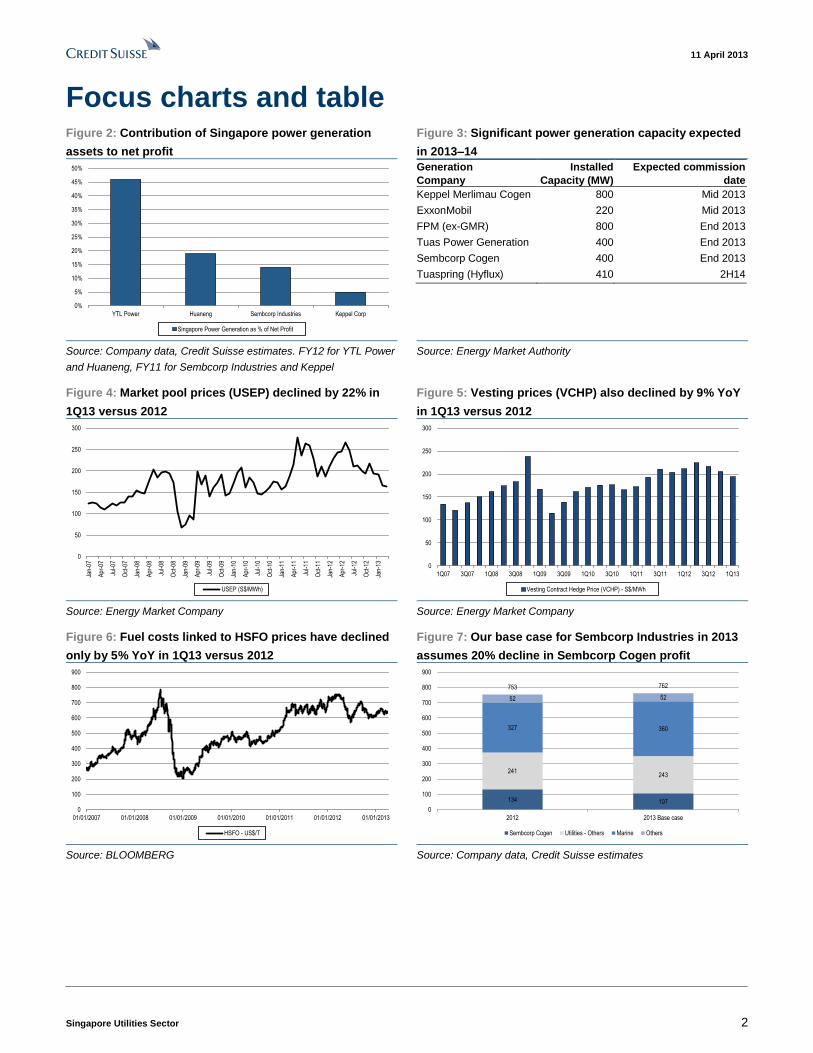

Focus charts and table Figure 2: Contribution of Singapore power generation

assets to net profit

Figure 3: Significant power generation capacity expected

in 2013–14

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

YTL Power Huaneng Sembcorp Industries Keppel Corp

Singapore Power Generation as % of Net Profit

Generation

Company

Installed

Capacity (MW)

Expected commission

date

Keppel Merlimau Cogen 800 Mid 2013

ExxonMobil 220 Mid 2013

FPM (ex-GMR) 800 End 2013

Tuas Power Generation 400 End 2013

Sembcorp Cogen 400 End 2013

Tuaspring (Hyflux) 410 2H14

Source: Company data, Credit Suisse estimates. FY12 for YTL Power

and Huaneng, FY11 for Sembcorp Industries and Keppel

Source: Energy Market Authority

Figure 4: Market pool prices (USEP) declined by 22% in

1Q13 versus 2012

Figure 5: Vesting prices (VCHP) also declined by 9% YoY

in 1Q13 versus 2012

0

50

100

150

200

250

300

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

USEP (S$/MWh)

0

50

100

150

200

250

300

1Q07 3Q07 1Q08 3Q08 1Q09 3Q09 1Q10 3Q10 1Q11 3Q11 1Q12 3Q12 1Q13

Vesting Contract Hedge Price (VCHP) - S$/MWh

Source: Energy Market Company Source: Energy Market Company

Figure 6: Fuel costs linked to HSFO prices have declined

only by 5% YoY in 1Q13 versus 2012

Figure 7: Our base case for Sembcorp Industries in 2013

assumes 20% decline in Sembcorp Cogen profit

0

100

200

300

400

500

600

700

800

900

01/01/2007 01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013

HSFO - US$/T

134 107

241243

327 360

52 52

753 762

0

100

200

300

400

500

600

700

800

900

2012 2013 Base case

Sembcorp Cogen Utilities - Others Marine Others

Source: BLOOMBERG Source: Company data, Credit Suisse estimates

11 April 2013

Singapore Utilities Sector 3

Significant capacity growth ahead Strong profitability could reverse with capacity

growth

While power generation companies in Singapore have enjoyed improving profitability since

2007, driven by the lack of new capacity addition, we expect this to reverse in 2013.

According to Energy Market Authority, total installed capacity is expected to grow by

3.0GW or 30% in 2013–14 following the completion of Singapore’s LNG terminal in 2Q13,

which will increase gas supply into the country. Planned capacity addition includes Keppel

Merlimau Cogen expansion (800MW) in mid-2013, as well as plants by First Pacific-

Meralco (800MW), Tuas Power (400MW) and Sembcorp Cogen (400MW) in end 2013.

Reserve margin could increase to 2007 levels

Based on the Credit Suisse power generation demand-supply model, we expect reserve

margin to increase to 47% in 2013E, close to the 2007 level. Assuming steady demand

growth of 3.5% per annum, the reserve margin recovers to the 2012 level only in 2020.

This expected rise in reserve margin has led to a decrease in the Uniform Singapore

Electricity Price (USEP) by 23% in 1Q13, relative to a 13% decline in fuel costs. At the

same time, vesting prices for contracts which commit generation companies to sell a

specified amount of electricity were also revised downwards in January 2013, following a

review of the long-run marginal cost parameters.

Mitigating factors could provide downside support

While reserve margin and power spreads could revert to 2007 levels with the significant

capacity increase, our base case assumptions are less negative. We believe a number of

factors could provide downside support. (1) Dominant gencos and new players are likely to

exercise rational pricing behaviour given the high acquisition price of assets. We note that

the sale of the dominant generation companies by Temasek in 2008 was at a EV/Licensed

capacity valuation range of S$1.2–1.6mn/MW, while the recent sale of assets by GMR to

First Pacific and Meralco was at S$2mn/MW. (2) Generation companies have contracts

locked in with retail customers, which typically make up about 30–40% of electricity sales.

(3) There can be revenue contribution from sale of steam to industrial customers, which

tends to be less volatile.

Downgrade Sembcorp Industries to NEUTRAL

Amongst listed companies that own power generation assets in Singapore, Keppel has the

smallest contribution from power generation in Singapore (5%), while YTL Power through

its holding in PowerSeraya, has the largest (46%). 19% of Huaneng’s profit was from

Singapore through its holding in Tuas Power, and 14% of Sembcorp Industries’ profit

came from Sembcorp Cogen.

We downgrade Sembcorp Industries to NEUTRAL (from Outperform) and lower our target

price to S$5.10 (from S$5.90). In our view, market earnings expectations for 2013 are

optimistic and do not factor in any decline in tariffs and profit. Our preference is for Keppel

(OUTPERFORM, TP S$13.70), given smaller contribution from Singapore power

generation market, as well as low expectations for its Infrastructure division.

Within the China Utilities sector, we switch our top sector pick from Huaneng Power (HNP)

to China Resources Power (CRP) given the downside risks of a fall in Singapore tariffs

and higher capacity adds in CRP versus HNP.

We maintain our UNDERPERFORM rating on YTL Power as we expect potential profit

decline in Singapore to add to its woes in Malaysia and the UK. For exposure to the YTL

group, we prefer YTL Corp.

Total installed capacity is

expected to grow by 3.0GW

or 30% in 2013–14

Downside support could

come from: (1) rational

pricing behaviour by

gencos, (2) contracts

already locked-in and (3)

industrial sales

11 April 2013

Singapore Utilities Sector 4

Strong profitability could reverse with capacity growth While power generation companies in Singapore have enjoyed improving profitability since

2007 driven by the lack of new capacity planting, we expect this to reverse in 2013.

According to Energy Market Authority, total installed capacity is expected to grow by

3.0GW or 30% in 2013–14 following the completion of Singapore’s LNG terminal in 2Q13,

which will increase gas supply into the country.

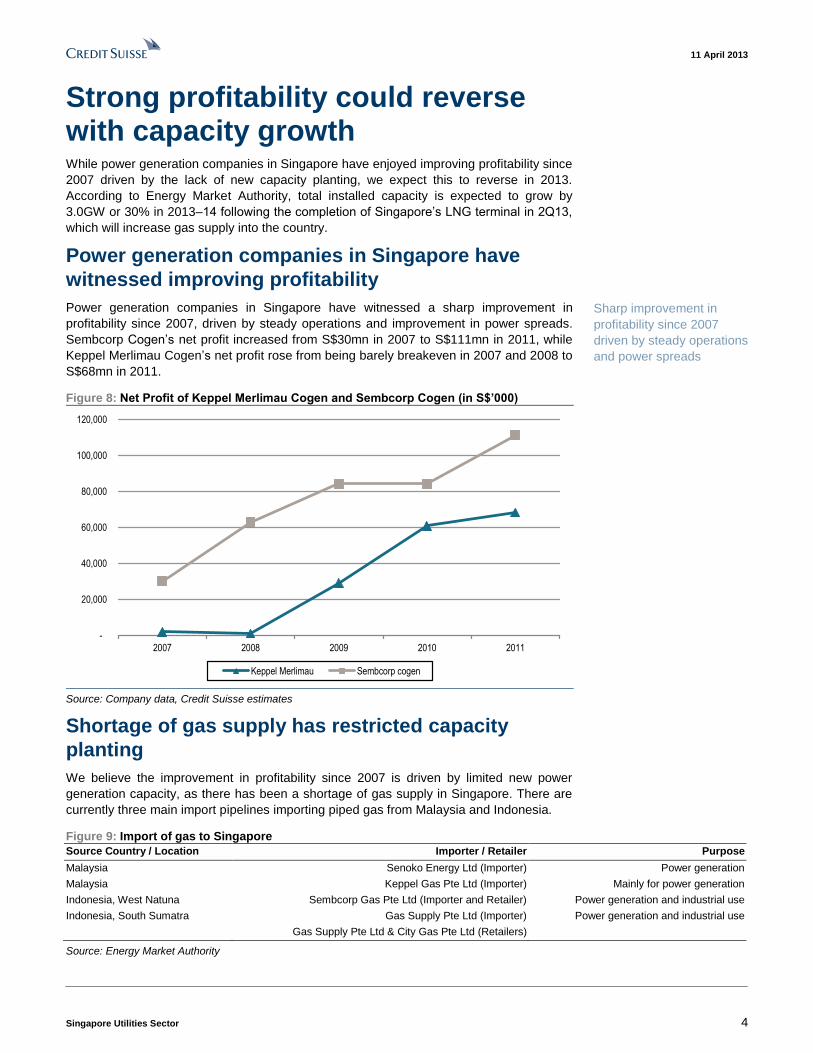

Power generation companies in Singapore have

witnessed improving profitability

Power generation companies in Singapore have witnessed a sharp improvement in

profitability since 2007, driven by steady operations and improvement in power spreads.

Sembcorp Cogen’s net profit increased from S$30mn in 2007 to S$111mn in 2011, while

Keppel Merlimau Cogen’s net profit rose from being barely breakeven in 2007 and 2008 to

S$68mn in 2011.

Figure 8: Net Profit of Keppel Merlimau Cogen and Sembcorp Cogen (in S$’000)

-

20,000

40,000

60,000

80,000

100,000

120,000

2007 2008 2009 2010 2011

Keppel Merlimau Sembcorp cogen

Source: Company data, Credit Suisse estimates

Shortage of gas supply has restricted capacity

planting

We believe the improvement in profitability since 2007 is driven by limited new power

generation capacity, as there has been a shortage of gas supply in Singapore. There are

currently three main import pipelines importing piped gas from Malaysia and Indonesia.

Figure 9: Import of gas to Singapore

Source Country / Location Importer / Retailer Purpose

Malaysia Senoko Energy Ltd (Importer) Power generation

Malaysia Keppel Gas Pte Ltd (Importer) Mainly for power generation

Indonesia, West Natuna Sembcorp Gas Pte Ltd (Importer and Retailer) Power generation and industrial use

Indonesia, South Sumatra Gas Supply Pte Ltd (Importer) Power generation and industrial use

Gas Supply Pte Ltd & City Gas Pte Ltd (Retailers)

Source: Energy Market Authority

Sharp improvement in

profitability since 2007

driven by steady operations

and power spreads

11 April 2013

Singapore Utilities Sector 5

Capacity expected to grow by 30% in 2013–14

Based on data from the Energy Market Authority (EMA), total installed capacity in

Singapore is expected to grow by 3.0GW during 2013–14, with the bulk of the capacity

growth coming through in end 2013.

Figure 10: Planned installed capacity growth in 2013–14

Generation Company Installed Capacity (MW) Plant Type Expected commission date

Keppel Merlimau Cogen 800 CCGT Mid 2013

ExxonMobil 220 CCGT Mid 2013

FPM (ex GMR) 800 CCGT End 2013

Tuas Power Generation 400 CCGT End 2013

Sembcorp Cogen 400 CCGT End 2013

Tuaspring (Hyflux) 410 CCGT 2H14

Source: Energy Market Authority, Company data, Credit Suisse estimates

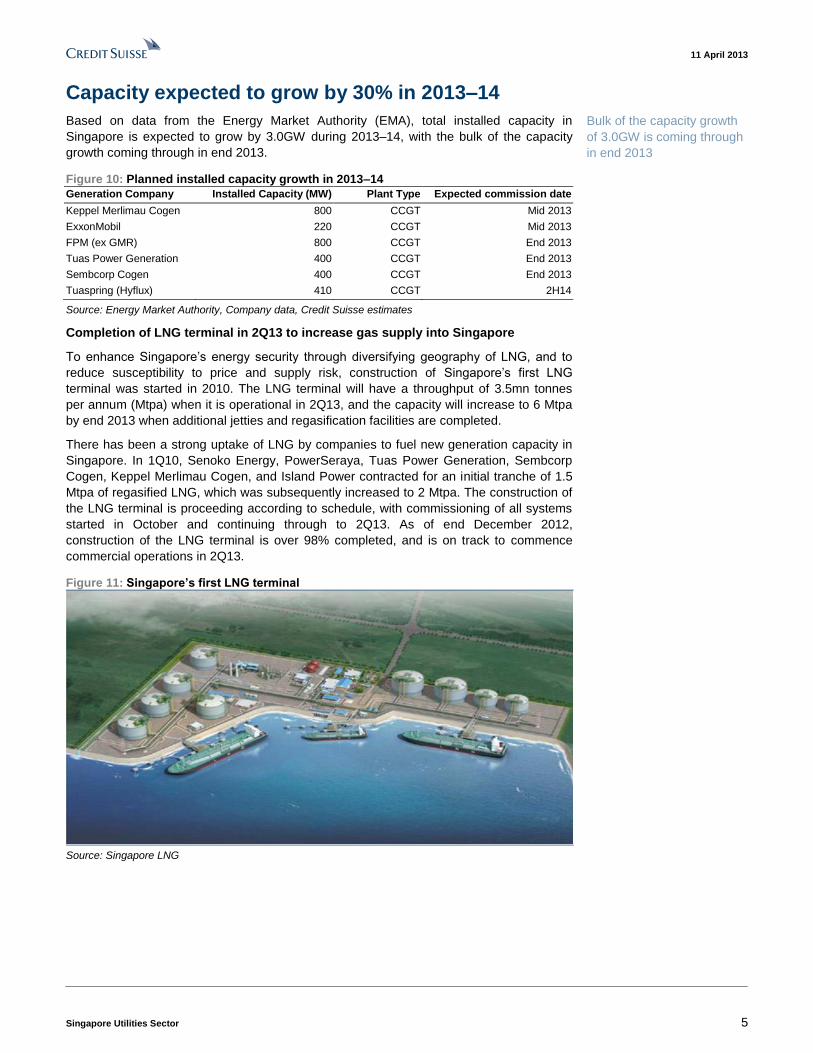

Completion of LNG terminal in 2Q13 to increase gas supply into Singapore

To enhance Singapore’s energy security through diversifying geography of LNG, and to

reduce susceptibility to price and supply risk, construction of Singapore’s first LNG

terminal was started in 2010. The LNG terminal will have a throughput of 3.5mn tonnes

per annum (Mtpa) when it is operational in 2Q13, and the capacity will increase to 6 Mtpa

by end 2013 when additional jetties and regasification facilities are completed.

There has been a strong uptake of LNG by companies to fuel new generation capacity in

Singapore. In 1Q10, Senoko Energy, PowerSeraya, Tuas Power Generation, Sembcorp

Cogen, Keppel Merlimau Cogen, and Island Power contracted for an initial tranche of 1.5

Mtpa of regasified LNG, which was subsequently increased to 2 Mtpa. The construction of

the LNG terminal is proceeding according to schedule, with commissioning of all systems

started in October and continuing through to 2Q13. As of end December 2012,

construction of the LNG terminal is over 98% completed, and is on track to commence

commercial operations in 2Q13.

Figure 11: Singapore’s first LNG terminal

Source: Singapore LNG

Bulk of the capacity growth

of 3.0GW is coming through

in end 2013

11 April 2013

Singapore Utilities Sector 6

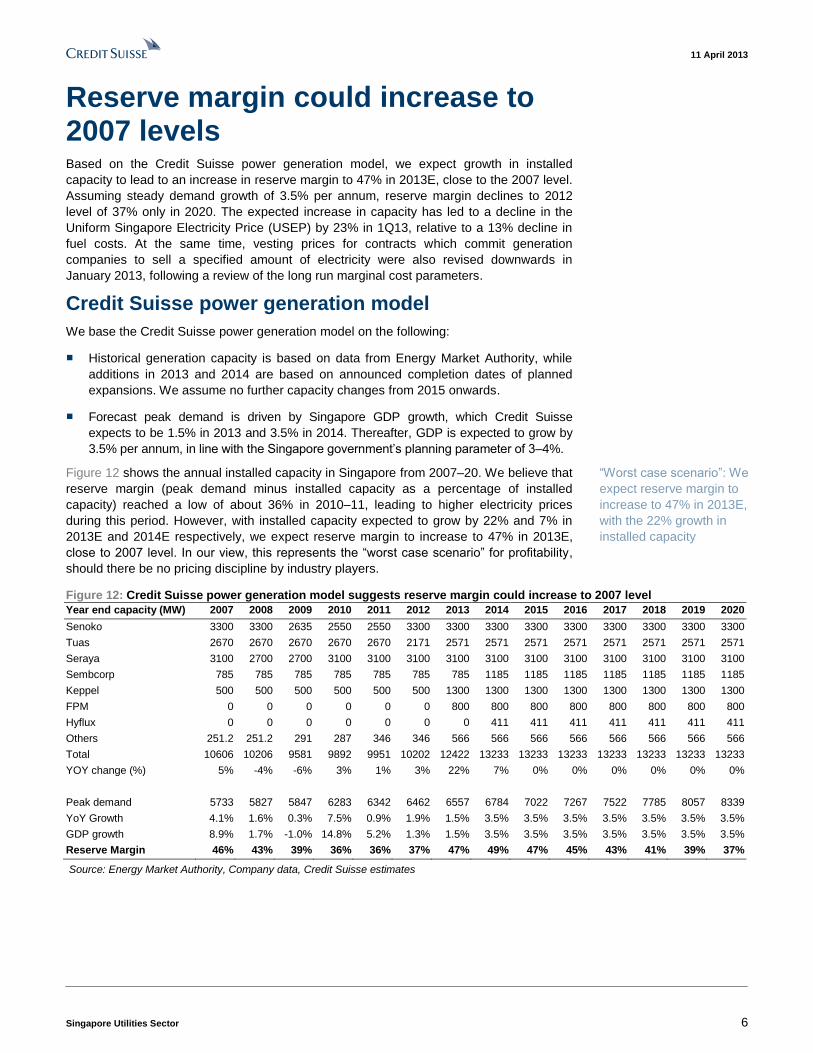

Reserve margin could increase to 2007 levels Based on the Credit Suisse power generation model, we expect growth in installed

capacity to lead to an increase in reserve margin to 47% in 2013E, close to the 2007 level.

Assuming steady demand growth of 3.5% per annum, reserve margin declines to 2012

level of 37% only in 2020. The expected increase in capacity has led to a decline in the

Uniform Singapore Electricity Price (USEP) by 23% in 1Q13, relative to a 13% decline in

fuel costs. At the same time, vesting prices for contracts which commit generation

companies to sell a specified amount of electricity were also revised downwards in

January 2013, following a review of the long run marginal cost parameters.

Credit Suisse power generation model

We base the Credit Suisse power generation model on the following:

■ Historical generation capacity is based on data from Energy Market Authority, while

additions in 2013 and 2014 are based on announced completion dates of planned

expansions. We assume no further capacity changes from 2015 onwards.

■ Forecast peak demand is driven by Singapore GDP growth, which Credit Suisse

expects to be 1.5% in 2013 and 3.5% in 2014. Thereafter, GDP is expected to grow by

3.5% per annum, in line with the Singapore government’s planning parameter of 3–4%.

Figure 12 shows the annual installed capacity in Singapore from 2007–20. We believe that

reserve margin (peak demand minus installed capacity as a percentage of installed

capacity) reached a low of about 36% in 2010–11, leading to higher electricity prices

during this period. However, with installed capacity expected to grow by 22% and 7% in

2013E and 2014E respectively, we expect reserve margin to increase to 47% in 2013E,

close to 2007 level. In our view, this represents the “worst case scenario” for profitability,

should there be no pricing discipline by industry players.

Figure 12: Credit Suisse power generation model suggests reserve margin could increase to 2007 level

Year end capacity (MW) 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Senoko 3300 3300 2635 2550 2550 3300 3300 3300 3300 3300 3300 3300 3300 3300

Tuas 2670 2670 2670 2670 2670 2171 2571 2571 2571 2571 2571 2571 2571 2571

Seraya 3100 2700 2700 3100 3100 3100 3100 3100 3100 3100 3100 3100 3100 3100

Sembcorp 785 785 785 785 785 785 785 1185 1185 1185 1185 1185 1185 1185

Keppel 500 500 500 500 500 500 1300 1300 1300 1300 1300 1300 1300 1300

FPM 0 0 0 0 0 0 800 800 800 800 800 800 800 800

Hyflux 0 0 0 0 0 0 0 411 411 411 411 411 411 411

Others 251.2 251.2 291 287 346 346 566 566 566 566 566 566 566 566

Total 10606 10206 9581 9892 9951 10202 12422 13233 13233 13233 13233 13233 13233 13233

YOY change (%) 5% -4% -6% 3% 1% 3% 22% 7% 0% 0% 0% 0% 0% 0%

Peak demand 5733 5827 5847 6283 6342 6462 6557 6784 7022 7267 7522 7785 8057 8339

YoY Growth 4.1% 1.6% 0.3% 7.5% 0.9% 1.9% 1.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5%

GDP growth 8.9% 1.7% -1.0% 14.8% 5.2% 1.3% 1.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5%

Reserve Margin 46% 43% 39% 36% 36% 37% 47% 49% 47% 45% 43% 41% 39% 37%

Source: Energy Market Authority, Company data, Credit Suisse estimates

“Worst case scenario”: We

expect reserve margin to

increase to 47% in 2013E,

with the 22% growth in

installed capacity

11 April 2013

Singapore Utilities Sector 7

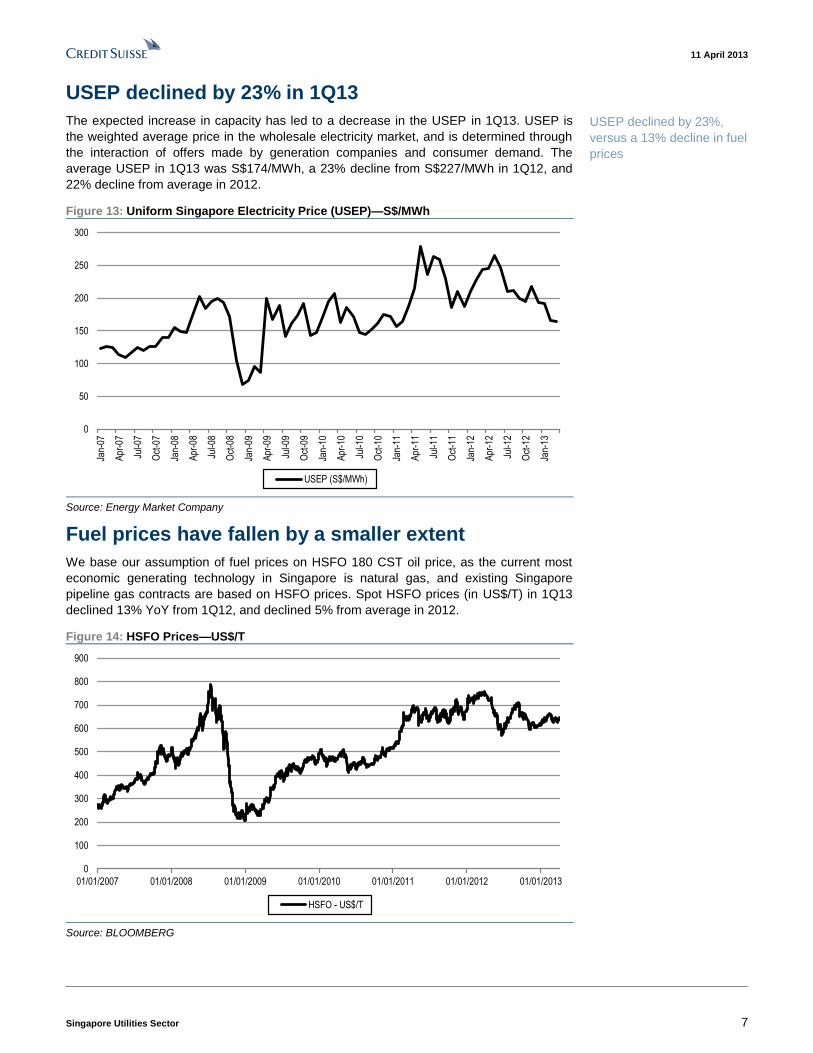

USEP declined by 23% in 1Q13

The expected increase in capacity has led to a decrease in the USEP in 1Q13. USEP is

the weighted average price in the wholesale electricity market, and is determined through

the interaction of offers made by generation companies and consumer demand. The

average USEP in 1Q13 was S$174/MWh, a 23% decline from S$227/MWh in 1Q12, and

22% decline from average in 2012.

Figure 13: Uniform Singapore Electricity Price (USEP)—S$/MWh

0

50

100

150

200

250

300

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

USEP (S$/MWh)

Source: Energy Market Company

Fuel prices have fallen by a smaller extent

We base our assumption of fuel prices on HSFO 180 CST oil price, as the current most

economic generating technology in Singapore is natural gas, and existing Singapore

pipeline gas contracts are based on HSFO prices. Spot HSFO prices (in US$/T) in 1Q13

declined 13% YoY from 1Q12, and declined 5% from average in 2012.

Figure 14: HSFO Prices—US$/T

0

100

200

300

400

500

600

700

800

900

01/01/2007 01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013

HSFO - US$/T

Source: BLOOMBERG

USEP declined by 23%,

versus a 13% decline in fuel

prices

11 April 2013

Singapore Utilities Sector 8

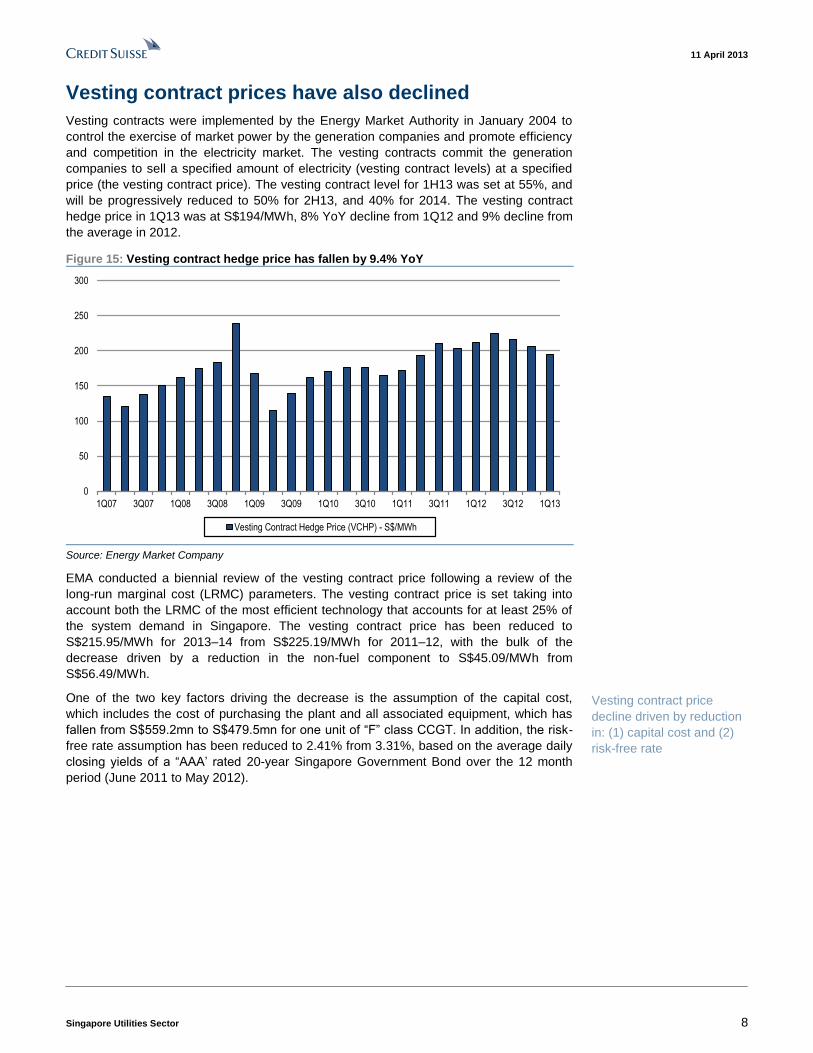

Vesting contract prices have also declined

Vesting contracts were implemented by the Energy Market Authority in January 2004 to

control the exercise of market power by the generation companies and promote efficiency

and competition in the electricity market. The vesting contracts commit the generation

companies to sell a specified amount of electricity (vesting contract levels) at a specified

price (the vesting contract price). The vesting contract level for 1H13 was set at 55%, and

will be progressively reduced to 50% for 2H13, and 40% for 2014. The vesting contract

hedge price in 1Q13 was at S$194/MWh, 8% YoY decline from 1Q12 and 9% decline from

the average in 2012.

Figure 15: Vesting contract hedge price has fallen by 9.4% YoY

0

50

100

150

200

250

300

1Q07 3Q07 1Q08 3Q08 1Q09 3Q09 1Q10 3Q10 1Q11 3Q11 1Q12 3Q12 1Q13

Vesting Contract Hedge Price (VCHP) - S$/MWh

Source: Energy Market Company

EMA conducted a biennial review of the vesting contract price following a review of the

long-run marginal cost (LRMC) parameters. The vesting contract price is set taking into

account both the LRMC of the most efficient technology that accounts for at least 25% of

the system demand in Singapore. The vesting contract price has been reduced to

S$215.95/MWh for 2013–14 from S$225.19/MWh for 2011–12, with the bulk of the

decrease driven by a reduction in the non-fuel component to S$45.09/MWh from

S$56.49/MWh.

One of the two key factors driving the decrease is the assumption of the capital cost,

which includes the cost of purchasing the plant and all associated equipment, which has

fallen from S$559.2mn to S$479.5mn for one unit of “F” class CCGT. In addition, the risk-

free rate assumption has been reduced to 2.41% from 3.31%, based on the average daily

closing yields of a “AAA’ rated 20-year Singapore Government Bond over the 12 month

period (June 2011 to May 2012).

Vesting contract price

decline driven by reduction

in: (1) capital cost and (2)

risk-free rate

11 April 2013

Singapore Utilities Sector 9

Figure 16: Summary of long-run margin cost (LRMC) parameters for setting vesting

contract price for the period 1 Jan 2013 to 31 December 2014

2011–12 2013–14

Technical parameters

Base month May-10 May-12

Capacity per generating unit (MW) 381 382.1

HHV Heat rate (Btu/kWh) 7010 7103.4

Build duration (months) 30 30

Economic lifetime (years) 24 22

Plant factor (%) 74.9 67.3

Capital cost (S$ mn) 559.2 479.5

Land, infrastructure and development cost (S$ mn) 152 150.2

Fixed annual running cost (S$ mn/yr) 22.49 23.51

Variable non-fuel cost (S$/MWh) 6.55 6.42

WACC parameters

Risk-free rate (%) 3.31 2.41

Debt premium 2.50 2.59

Gearing 0.342 0.497

Equity beta 1.00 1.00

Market risk premium 7.0 6.0

Corporate tax rate 17.0 17.0

Post-tax Nominal WACC (%) 8.43 6.29

Vesting contract price

Vesting contract price (S$/MWh) 225.19 215.95

Non-Fuel component (S$/MWh) 56.49 45.09

Fuel component (S$/MWh) 168.7 170.86

Source: Energy Market Authority

11 April 2013

Singapore Utilities Sector 10

Mitigating factors could provide downside support While reserve margin and power spreads could revert to 2007 levels with the significant

capacity increase, our base case assumptions are less negative. We believe a number of

factors could provide downside support, including: (1) likely rational pricing behaviour of

dominant gencos and new players given their high acquisition price; (2) retail contracts

locked in with industrial customers which could make up 60% of electricity sales, as well

as (3) contribution from non-electricity sales such as bundled utilities to customers on the

Jurong Island.

High acquisition cost could provide support to the

market pool prices

We believe downside support to market pool prices could be provided by the required

return of dominant generation companies, which purchased assets from Temasek

Holdings in 2008. The sale of Tuas Power (to China Huaneng), Senoko Power (to

Japanese consortium Lion Power) and PowerSeraya (to YTL Power) was made at a

EV/Licensed capacity valuation range of S$1.2–S$1.6mn/MW. More recently, First Pacific

and Meralco purchased a 70% stake in two 400MW plants from GMR at S$2 mn/MW.

Sale of major gencos at S$1.2–S$1.6mn/MW

In 2008, Temasek Holdings divested three of its wholly owned Singapore power

generation companies—PowerSeraya Ltd, Senoko Power Ltd and Tuas Power Ltd. In

March 2008, China Huaneng acquired Tuas Power for a cash consideration of S$4.235

bn. Tuas Power has generation assets with a licensed capacity totalling 2,670 MW

comprising 1,200 MW of oil-fired steam plants and 1,470 MW of gas-fired combined cycle

plants. In September 2008, Lion Power Holdings, a consortium comprising Marubeni,

GDF SUEZ, Kansai Electric Power, Kyushu Electric Power and Japan Bank for

International Cooperation, acquired Senoko Power for a cash consideration of S$3.65 bn.

Senoko has a combined installed capacity of 3,300 MW, comprising 1,945 MW of

combined cycle plants, 1,250 MW of thermal plants, and 105 MW of fast-start gas

turbines. In December 2008, YTL Power acquired PowerSeraya for a cash consideration

of S$3.6 bn. PowerSeraya has a registered capacity of 2,940 MW, comprising 732 MW of

combined cycle plants, 1,990MW of steam turbine plants and 218 MW of open cycle gas

turbine plants. The acquisition multiple of for these transactions were in the range of

S$1.2-S$1.6 mn/MW.

Figure 17: Acquisition of major gencos

Equity Net Enterprise Installed Licensed EV/ EV/

Value Debt Value Capacity Capacity Share of Installed Licensed

GenCo Date Sold Acquiror (S$ mn) (S$ mn) (S$ mn) (MW) (MW) SG needs MW MW

Tuas Power 14-Mar-08 China Huaneng 4,235 71 4,306 2,670 2,670 25% 1.61 1.61

Senoko Power 05-Sep-08 Lion Power 3,650 323 3,973 3,405 3,300 30% 1.17 1.20

PowerSeraya 02-Dec-08 YTL Power 3,600 201 3,801 3,240 3,100 27% 1.17 1.23

Source: Company data, Credit Suisse estimates

First Pac and Meralco acquire 800 MW facility from GMR at S$2mn/MW

In March 2013, GMR entered into a share purchase agreement to sell its 70% stake in

GMR Energy (GMRE) to FPM Power Holdings, a 60:40 joint venture between First Pacific

and MERALCO. GMRE owns 2x 400 MW natural gas fuelled power plant on Jurong Island,

Singapore. The plant is 96% complete, and is expected to commence operations in

December 2013.

Pool prices likely to be

supported by high required

return of dominant gencos

11 April 2013

Singapore Utilities Sector 11

The consideration will be a total of US$537 mn (S$660 mn) for a 70% stake in GMRE. The

sale translates to an Enterprise Value (100% basis) for GMRE of US$1,293 mn (S$1,612

mn) on project completion. The power plant was financed on a limited recourse basis by a

consortium of banks providing a US$545 mn 17-year debt facility and a further US$270 mn

credit facility. The remaining 30% stake in GMRE is held by PETRONAS that will continue to

stay invested in the project.

The acquisition multiple of S$2 mn per MW is at a premium to the valuation of assets

divested by Temasek in 2008. We believe this could be due to higher efficiency of a newly

completed plant, as well as improvement in power spreads since 2008.

We believe that there might be downside support to market pool prices based on the

required return of generation companies. For example, we estimate that a long-term

EBITDA of US$100 mn is required to generate an 11% IRR for the investments by First

Pacific and Meralco, which is almost in-line with the effective EBITDA for a 70% stake in

Sembcorp Cogen (800MW) in 2011.

Figure 18: NPV analysis of GMR acquisition

In US$ mn 0 1 2 3 4 5 6 7 … 29 30

Investment Cost -537

EBITDA 100.2 100.2 100.2 100.2 100.2 100.2 100.2 … 100.2 100.2

Debt Principal repayment -22.4 -22.4 -22.4 -22.4 -22.4 -22.4 -22.4

Interest expense -14.4 -9.4 -8.8 -8.2 -7.5 -6.9 -6.3

Tax -10.8 -11.6 -11.7 -11.8 -11.9 -12.0 -12.1 … -17.0 -17.0

Cash inflow -537 52.6 56.7 57.2 57.8 58.3 58.8 59.3 … 83.2 83.2

Source: Company data, Credit Suisse estimates

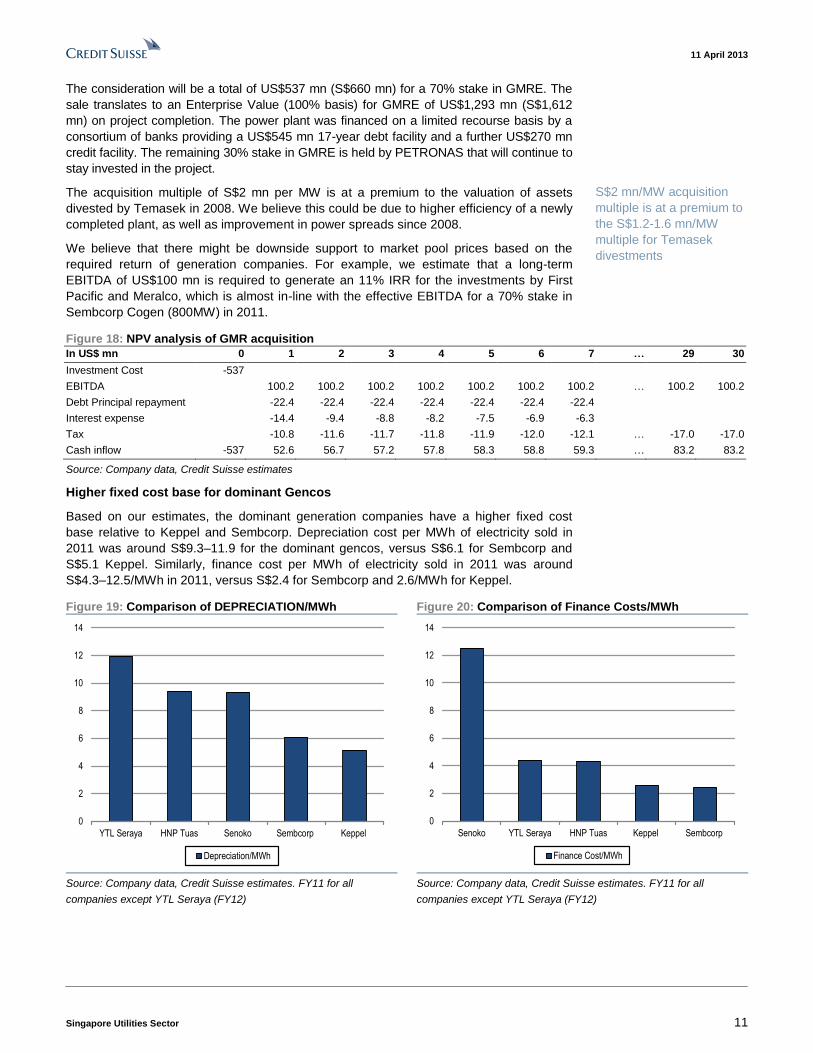

Higher fixed cost base for dominant Gencos

Based on our estimates, the dominant generation companies have a higher fixed cost

base relative to Keppel and Sembcorp. Depreciation cost per MWh of electricity sold in

2011 was around S$9.3–11.9 for the dominant gencos, versus S$6.1 for Sembcorp and

S$5.1 Keppel. Similarly, finance cost per MWh of electricity sold in 2011 was around

S$4.3–12.5/MWh in 2011, versus S$2.4 for Sembcorp and 2.6/MWh for Keppel.

Figure 19: Comparison of DEPRECIATION/MWh Figure 20: Comparison of Finance Costs/MWh

0

2

4

6

8

10

12

14

YTL Seraya HNP Tuas Senoko Sembcorp Keppel

Depreciation/MWh

0

2

4

6

8

10

12

14

Senoko YTL Seraya HNP Tuas Keppel Sembcorp

Finance Cost/MWh

Source: Company data, Credit Suisse estimates. FY11 for all

companies except YTL Seraya (FY12)

Source: Company data, Credit Suisse estimates. FY11 for all

companies except YTL Seraya (FY12)

S$2 mn/MW acquisition

multiple is at a premium to

the S$1.2-1.6 mn/MW

multiple for Temasek

divestments

11 April 2013

Singapore Utilities Sector 12

Profit decline could be moderated by contracts

locked in with retail customers

While public data is available on spot prices and vesting prices, there is limited disclosure

on the retail contracts of generation companies. Before 2001, all consumers in Singapore

were subjected to the Singapore Power Electricity Tariff. Following the liberalisation of

Singapore’s electricity retail market in 2001, a contestable customer with minimum

electricity consumption of 10,000 kWh and above has the option of choosing the retailer

that provides the best service. Such contracts, which typically range from a month to a

year, limit the impact of volatility from spot prices. We estimate that such retail customers

make up about 30–40% of electricity sales for Tuas Power and Sembcorp Cogen in FY11.

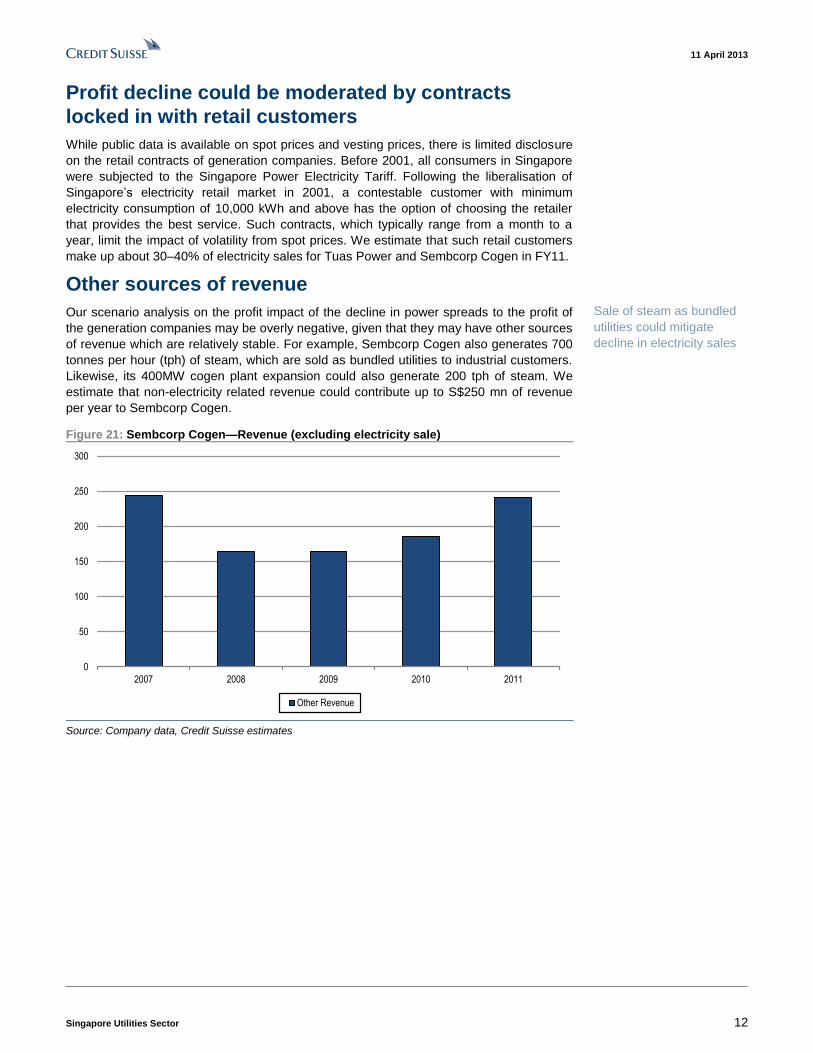

Other sources of revenue

Our scenario analysis on the profit impact of the decline in power spreads to the profit of

the generation companies may be overly negative, given that they may have other sources

of revenue which are relatively stable. For example, Sembcorp Cogen also generates 700

tonnes per hour (tph) of steam, which are sold as bundled utilities to industrial customers.

Likewise, its 400MW cogen plant expansion could also generate 200 tph of steam. We

estimate that non-electricity related revenue could contribute up to S$250 mn of revenue

per year to Sembcorp Cogen.

Figure 21: Sembcorp Cogen—Revenue (excluding electricity sale)

0

50

100

150

200

250

300

2007 2008 2009 2010 2011

Other Revenue

Source: Company data, Credit Suisse estimates

Sale of steam as bundled

utilities could mitigate

decline in electricity sales

11 April 2013

Singapore Utilities Sector 13

Downgrade Sembcorp Industries to NEUTRAL Amongst listed companies that own power generation assets in Singapore, Keppel has the

smallest contribution from power generation in Singapore (5%), while YTL Power—

through its holding in PowerSeraya—has the largest (46%). 19% of Huaneng’s FY12 profit

was from Singapore through its holding in Tuas Power, while 14% of Sembcorp Industries’

profit came from Sembcorp Cogen.

Figure 22: Singapore Power Generation as % of group net profit

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

YTL Power Huaneng Sembcorp Industries Keppel Corp

Singapore Power Generation as % of Net Profit

Source: Company data, Credit Suisse estimates. FY12 for YTL Power & Huaneng, FY11 for SCI & KEP

We downgrade Sembcorp Industries (NEUTRAL from Outperform, TP S$5.10), since we

believe the market’s earnings expectations do not factor in any potential decline in

profitability because of industry capacity additions. Within the Singapore conglomerate

sector, our preference is for Keppel Corp (OUTPERFORM, TP S$13.70), since market

expectations for its Infrastructure division are low as provisions were taken following the

cost overruns in Qatar.

Within the China Utilities sector, we switch our top sector pick from Huaneng Power to

China Resources Power given the downside risks of a fall in Singapore tariffs and higher

capacity additions in CRP versus HNP.

We maintain our UNDERPERFORM rating on YTL Power as we expect potential profit

decline in Singapore to add to its woes in Malaysia and the UK. However, for exposure to

the YTL group, we prefer YTL Corp.

Figure 23: Sector valuation table

Current Target Up/ down Mkt Cap Div yld P/E (x) P/B (x) ROE (%)

Rating FX price price side (%) US$ mn (%) 12A 13E 14E 12A 13E 14E 12A 13E 14E

Sembcorp Industries N SGD 5.08 5.10 0.4 7,320 3.0 12.0 11.9 10.1 2.0 1.8 1.6 16.7 15.2 15.9

Keppel Corporation O SGD 11.16 13.70 22.8 16,244 4.6 10.5 10.4 10.4 2.2 2.0 1.8 20.7 19.3 17.6

Hyflux Ltd O SGD 1.41 1.60 13.5 981 2.3 35.6 27.2 22.7 2.3 2.0 1.9 6.4 7.5 8.2

Huaneng Power O HKD 8.29 9.00 8.6 15,713 4.6 16.8 11.1 10.7 1.6 1.5 1.4 10.3 14.2 13.6

YTL Power U MYR 1.48 1.40 -5.4 3578 4.4 9.3 9.8 10.2 1.3 1.2 1.1 13.6 12.0 10.5

First Pacific O HKD 10.54 13.03 23.6 5,248 2.1 14.9 13.6 9.9 1.6 1.4 1.3 10.8 10.6 12.8

Manila Electric N PHP 325.00 262.00 -19.4 8,896 3.0 22.2 20.2 19.4 5.3 4.8 4.5 23.8 24.0 23.0

Average 3.8 17.2 14.6 13.9 2.3 2.1 2.1 14.6 14.8 15.2

Source: Company data, Credit Suisse estimates, Thomson Reuters

11 April 2013

Singapore Utilities Sector 14

Asia Pacific / Singapore

Conglomerates (Capital goods - Engineering (Asia)) / UNDERWEIGHT

Sembcorp Industries Limited

(SCIL.SI / SCI SP)

Expectations for Singapore utilities high

■ Downgrade to NEUTRAL. While Sembcorp Cogen has generated superior

returns relative to its peers, we believe market earnings expectations for

2013 are optimistic and do not factor in any potential decline in tariffs and

profit on the back of industry capacity additions. As such, we downgrade

Sembcorp Industries to NEUTRAL (from Outperform), as we expect positive

earnings momentum to be reversed.

■ Market expectations for Utilities optimistic. Our base case assumes a

20% fall in Sembcorp Cogen’s net profit in 2013 on lower power spreads. As

a result, we lower our 2013 Utilities net profit forecast to S$350 mn from

S$375 mn. Based on consensus earnings estimates, we believe the market

is expecting power spreads in Singapore to remain constant. In the worst

case scenario where profitability declines to 2007 levels, there could be 10%

downside to our net profit forecasts for Sembcorp Industries. However, we

expect downside support from retail contracts locked in, as well as sale of

steam to industrial customers.

■ Marine margins moderating. Marine operating margins declined to 12.5%

in 2012 from 18.6% in 2011. We expect 2013 operating margin to decline

further to 12.0%, in-line with management guidance of 10–13% but below

consensus of 12.5%, driven by profit recognition for the drill-ship and other

new products in its orderbook.

■ Valuation. We lower our target price to S$5.10 from S$5.90, based on

SOTP method, valuing the Utilities business at 2013 P/E of 10x, and the

Marine business using our target price of S$4.00.

Share price performance

60

80

100

120

2

4

6

8

Apr-11 Aug-11 Dec-11 Apr-12 Aug-12 Dec-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

FTSE STRAITS TIMES IDX which closed at 3285.81 on

08/04/13

On 08/04/13 the spot exchange rate was S$1.24/US$1

Performance Over 1M 3M 12M Absolute (%) -2.7 -5.0 -4.0 Relative (%) -2.5 -7.5 -14.0

Financial and valuation metrics

Year 12/12A 12/13E 12/14E 12/15E Revenue (S$ mn) 10,189.1 11,624.5 14,050.9 14,174.5 EBITDA (S$ mn) 1,385.0 1,393.7 1,609.9 1,639.5 EBIT (S$ mn) 1,103.4 1,111.1 1,326.3 1,355.9 Net profit (S$ mn) 753.7 762.4 895.4 923.2 EPS (CS adj.) (S$) 0.42 0.43 0.50 0.52 Change from previous EPS (%) n.a. -3.1 -0.1 -1.0 Consensus EPS (S$) n.a. 0.44 0.50 0.54 EPS growth (%) -6.9 1.1 17.3 3.0 P/E (x) 12.0 11.9 10.1 9.9 Dividend yield (%) 3.0 3.0 3.0 3.0 EV/EBITDA (x) 6.7 7.1 5.9 5.4 P/B (x) 2.0 1.8 1.6 1.4 ROE (%) 17.5 16.0 16.8 15.5 Net debt/equity (%) 3.3 13.2 4.8 net cash

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating (from Outperform) NEUTRAL* Price (08 Apr 13, S$) 5.08 Target price (S$) (from 5.90) 5.10¹ Upside/downside (%) 0.39 Mkt cap (S$ mn) 9,081 (US$ 7,311) Enterprise value (S$ mn) 9,912 Number of shares (mn) 1,787.55 Free float (%) 23.8 52-week price range 5.76 - 4.67 ADTO - 6M (US$ mn) 14.2

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Gerald Wong, CFA

65 6212 3037

11 April 2013

Singapore Utilities Sector 15

Sembcorp Cogen contributed 14% of SCI’s net profit

in FY11

Sembcorp Cogen operates a 815MW combined cycle gas turbine plant in the Sakra

district of Jurong Island in Singapore. Commissioned in 2001, the plant remains

Singapore’s largest cogeneration facility. Sembcorp Cogen generated S$111 mn of net

profit in 2011, representing 37% of Sembcorp Industries’ Utilities net profit, and 14% of

Sembcorp Industries’ net profit. While the breakdown in 2012 was not disclosed, we

estimate that the bulk of the increase in Singapore Utilities in 2012 to be driven by

Sembcorp Gas with the additional 90 bbtu of gas supply into Singapore.

Figure 24: Sembcorp Cogen’s contribution to Singapore net profit

Others 2007 2008 2009 2010 2011 2012E 2013E 2014E

Sembcorp Cogen 30 63 84 84 111 134 107 135

Sembcorp Gas 48 75 27 43 55 109 82 82

Others 49 -7 20 20 17 20 20 20

Singapore Total 127 131 131 147 183 263 209 237

Sembcorp Cogen as % of Singapore 24% 48% 64% 57% 61% 51% 51% 57%

Sembcorp Utilities 244 202 227 231 304 375 350 400

Sembcorp Cogen as % of Utilities 12% 31% 37% 36% 37% 36% 31% 34%

Sembcorp Industries 557 534 683 761 809 753 762 881

Sembcorp Cogen as % of SCI 5% 12% 12% 11% 14% 18% 14% 15%

Source: Company data, Credit Suisse estimates

Lower 2013 Utilities net profit forecast to S$350 mn

Our base case assumes a 20% fall in Sembcorp Cogen’s net profit in 2013 on lower power

spreads. As a result, we lower our 2013 Utilities net profit forecast to S$350 mn. In the

worst case scenario assuming that profitability declines to 2007 levels, Utilities net profit

could decline to about S$273 mn. This would imply 10% downside to our net profit

forecasts for Sembcorp Industries.

Figure 25: Base case assumes 20% decrease in

Sembcorp Cogen profit in 2013E

Figure 26: Worst case assumes Sembcorp cogen profit in

2013E declines to 2007 levels

134 107

241243

327 360

52 52

753 762

0

100

200

300

400

500

600

700

800

900

2012 2013 Base case

Sembcorp Cogen Utilities - Others Marine Others

13430

241

243

327

360

52

52

753

685

0

100

200

300

400

500

600

700

800

900

2012 2013 Worst case

Sembcorp Cogen Utilities - Others Marine Others

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Base case: S$350 mn

Worst case: S$273 mn

11 April 2013

Singapore Utilities Sector 16

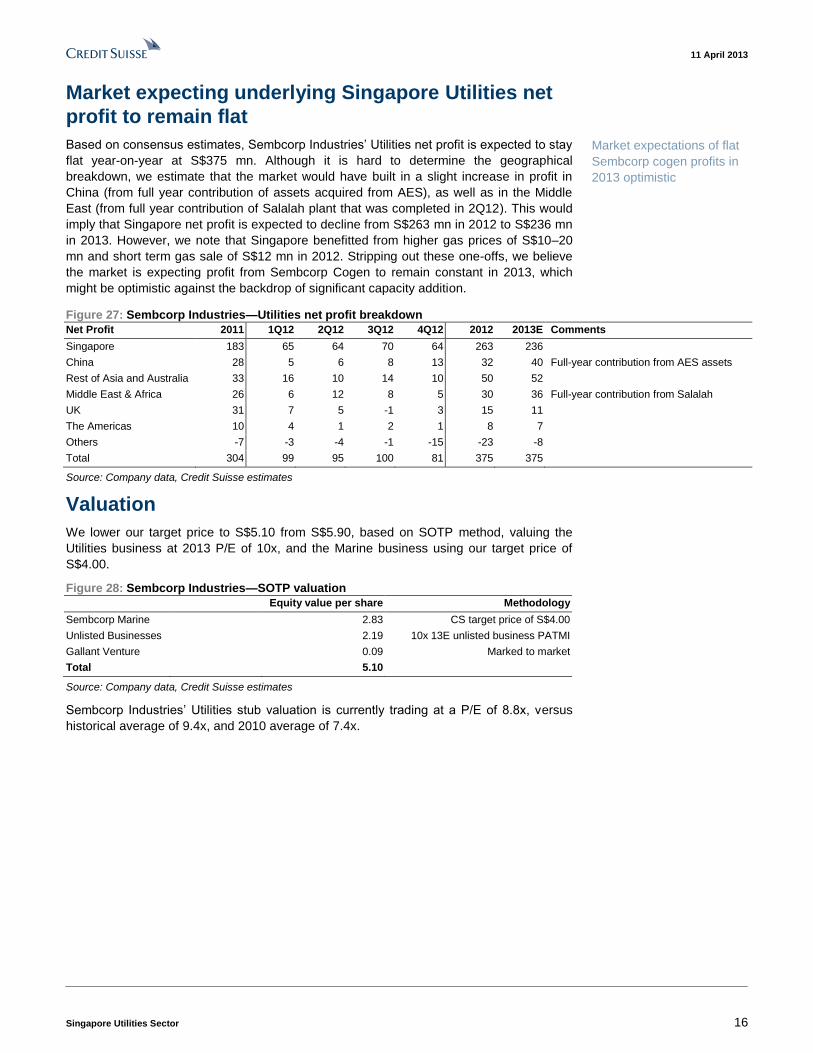

Market expecting underlying Singapore Utilities net

profit to remain flat

Based on consensus estimates, Sembcorp Industries’ Utilities net profit is expected to stay

flat year-on-year at S$375 mn. Although it is hard to determine the geographical

breakdown, we estimate that the market would have built in a slight increase in profit in

China (from full year contribution of assets acquired from AES), as well as in the Middle

East (from full year contribution of Salalah plant that was completed in 2Q12). This would

imply that Singapore net profit is expected to decline from S$263 mn in 2012 to S$236 mn

in 2013. However, we note that Singapore benefitted from higher gas prices of S$10–20

mn and short term gas sale of S$12 mn in 2012. Stripping out these one-offs, we believe

the market is expecting profit from Sembcorp Cogen to remain constant in 2013, which

might be optimistic against the backdrop of significant capacity addition.

Figure 27: Sembcorp Industries—Utilities net profit breakdown

Net Profit 2011 1Q12 2Q12 3Q12 4Q12 2012 2013E Comments

Singapore 183 65 64 70 64 263 236

China 28 5 6 8 13 32 40 Full-year contribution from AES assets

Rest of Asia and Australia 33 16 10 14 10 50 52

Middle East & Africa 26 6 12 8 5 30 36 Full-year contribution from Salalah

UK 31 7 5 -1 3 15 11

The Americas 10 4 1 2 1 8 7

Others -7 -3 -4 -1 -15 -23 -8

Total 304 99 95 100 81 375 375

Source: Company data, Credit Suisse estimates

Valuation

We lower our target price to S$5.10 from S$5.90, based on SOTP method, valuing the

Utilities business at 2013 P/E of 10x, and the Marine business using our target price of

S$4.00.

Figure 28: Sembcorp Industries—SOTP valuation

Equity value per share Methodology

Sembcorp Marine 2.83 CS target price of S$4.00

Unlisted Businesses 2.19 10x 13E unlisted business PATMI

Gallant Venture 0.09 Marked to market

Total 5.10

Source: Company data, Credit Suisse estimates

Sembcorp Industries’ Utilities stub valuation is currently trading at a P/E of 8.8x, versus

historical average of 9.4x, and 2010 average of 7.4x.

Market expectations of flat

Sembcorp cogen profits in

2013 optimistic

11 April 2013

Singapore Utilities Sector 17

Figure 29: Sembcorp Industries—Utilities Stub valuation

0

5

10

15

20

25

Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

P/E Average +1 std dev -1 std dev

Source: Company data, Credit Suisse estimates, BLOOMBERG

11 April 2013

Singapore Utilities Sector 18

Asia Pacific / Singapore

Conglomerates (Capital goods - Engineering (Asia)) / UNDERWEIGHT

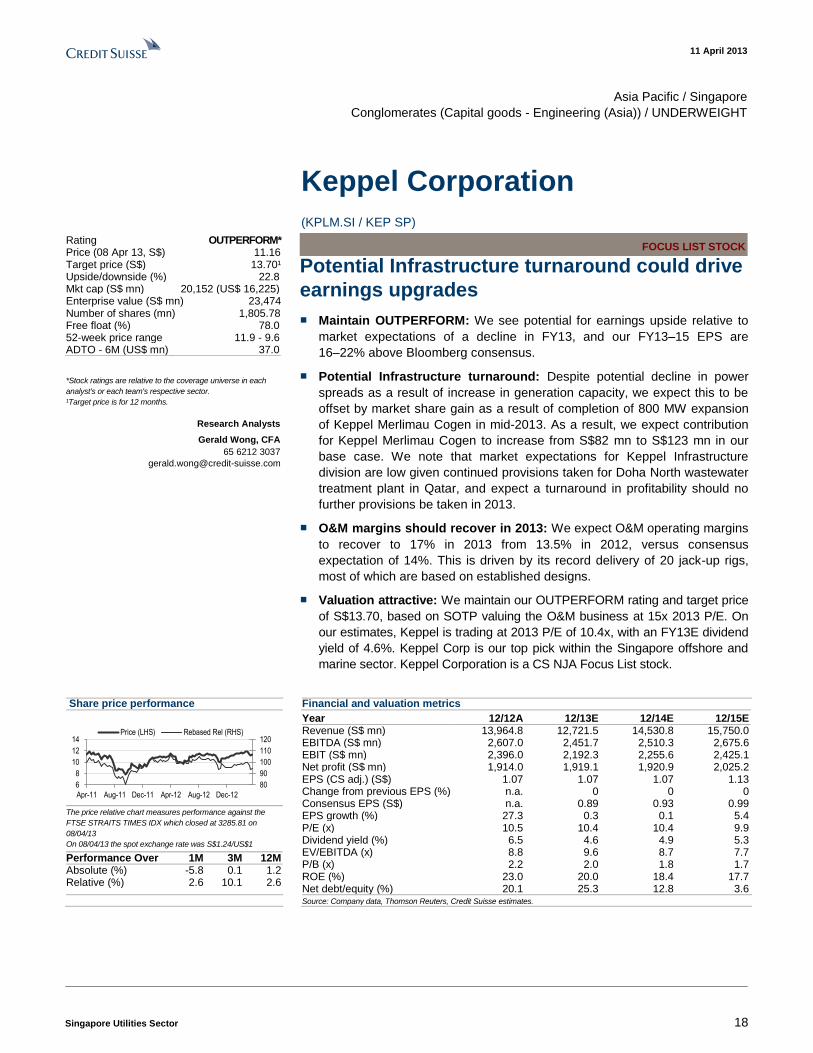

Keppel Corporation

(KPLM.SI / KEP SP) FOCUS LIST STOCK

Potential Infrastructure turnaround could drive

earnings upgrades

■ Maintain OUTPERFORM: We see potential for earnings upside relative to

market expectations of a decline in FY13, and our FY13–15 EPS are

16–22% above Bloomberg consensus.

■ Potential Infrastructure turnaround: Despite potential decline in power

spreads as a result of increase in generation capacity, we expect this to be

offset by market share gain as a result of completion of 800 MW expansion

of Keppel Merlimau Cogen in mid-2013. As a result, we expect contribution

for Keppel Merlimau Cogen to increase from S$82 mn to S$123 mn in our

base case. We note that market expectations for Keppel Infrastructure

division are low given continued provisions taken for Doha North wastewater

treatment plant in Qatar, and expect a turnaround in profitability should no

further provisions be taken in 2013.

■ O&M margins should recover in 2013: We expect O&M operating margins

to recover to 17% in 2013 from 13.5% in 2012, versus consensus

expectation of 14%. This is driven by its record delivery of 20 jack-up rigs,

most of which are based on established designs.

■ Valuation attractive: We maintain our OUTPERFORM rating and target price

of S$13.70, based on SOTP valuing the O&M business at 15x 2013 P/E. On

our estimates, Keppel is trading at 2013 P/E of 10.4x, with an FY13E dividend

yield of 4.6%. Keppel Corp is our top pick within the Singapore offshore and

marine sector. Keppel Corporation is a CS NJA Focus List stock.

Share price performance

80

90

100

110

120

6

8

10

12

14

Apr-11 Aug-11 Dec-11 Apr-12 Aug-12 Dec-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

FTSE STRAITS TIMES IDX which closed at 3285.81 on

08/04/13

On 08/04/13 the spot exchange rate was S$1.24/US$1

Performance Over 1M 3M 12M Absolute (%) -5.8 0.1 1.2 Relative (%) 2.6 10.1 2.6

Financial and valuation metrics

Year 12/12A 12/13E 12/14E 12/15E Revenue (S$ mn) 13,964.8 12,721.5 14,530.8 15,750.0 EBITDA (S$ mn) 2,607.0 2,451.7 2,510.3 2,675.6 EBIT (S$ mn) 2,396.0 2,192.3 2,255.6 2,425.1 Net profit (S$ mn) 1,914.0 1,919.1 1,920.9 2,025.2 EPS (CS adj.) (S$) 1.07 1.07 1.07 1.13 Change from previous EPS (%) n.a. 0 0 0 Consensus EPS (S$) n.a. 0.89 0.93 0.99 EPS growth (%) 27.3 0.3 0.1 5.4 P/E (x) 10.5 10.4 10.4 9.9 Dividend yield (%) 6.5 4.6 4.9 5.3 EV/EBITDA (x) 8.8 9.6 8.7 7.7 P/B (x) 2.2 2.0 1.8 1.7 ROE (%) 23.0 20.0 18.4 17.7 Net debt/equity (%) 20.1 25.3 12.8 3.6

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating OUTPERFORM* Price (08 Apr 13, S$) 11.16 Target price (S$) 13.70¹ Upside/downside (%) 22.8 Mkt cap (S$ mn) 20,152 (US$ 16,225) Enterprise value (S$ mn) 23,474 Number of shares (mn) 1,805.78 Free float (%) 78.0 52-week price range 11.9 - 9.6 ADTO - 6M (US$ mn) 37.0

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Gerald Wong, CFA

65 6212 3037

11 April 2013

Singapore Utilities Sector 19

Keppel Merlimau Cogen contributed 5% of Keppel’s

net profit in FY11

Keppel Merlimau Cogen operates a 500 MW gas-fired cogen plant at the Tembusu sector

of Jurong Island, Singapore. Keppel Merlimau Cogen generated S$68 mn of net profit in

2011, representing 5% of Keppel’s net profit. While the breakdown in 2012 was not

disclosed, we estimate that Keppel Merlimau Cogen’s profit increased by about 20%, in

line with the increase in power spreads.

Figure 30: Keppel Merlimau Cogen’s contribution to Keppel Corp’s Net Profit

2007 2008 2009 2010 2011 2012E 2013E 2014E

Keppel Merlimau Cogen 2 1 29 61 68 82 123 148

Keppel Infrastructure - Others 25 62 97 -4 14 -83 125 149

Keppel Infrastructure 27 63 126 57 82 -1 248 297

Keppel Corp 1026 1079 1190 1307 1491 1914 1919 1921

Keppel Merlimau Cogen as % of Keppel 0% 0% 2% 5% 5% 4% 6% 8%

Source: Company data, Credit Suisse estimates

Keppel Merlimau Cogen’s net profit could still

increase with 800 MW capacity expansion

Despite potential decline in power spreads as a result of increase in generation capacity,

we expect this to be offset by market share gain as a result of completion of 800 MW

expansion of Keppel Merlimau Cogen in mid-2013. As a result, we expect contribution for

Keppel Merlimau Cogen to increase from S$82 mn in 2012 to S$123 mn in 2013 in our

base case. In the worst case scenario assuming that profitability declines to 2007 levels,

Utilities net profit could decline to about S$33 mn. This would imply 4% downside to our

2013 net profit forecast for Keppel.

Figure 31: Base case assumes decline in spread offset by

increase in 800 MW expansion in 2013E

Figure 32: Worst case implies 5% downside to Keppel

Corp’s net profit in 2013E

82 123-83

125

937

1083

784394

194194

19141919

-200

200

600

1000

1400

1800

2200

2012 2013 Base case

Keppel Merlimau Cogen Infrastructure - Others O&M

Property Investments

82 33-83125

937

1083

784 394

194

194

1914

1829

-200

200

600

1000

1400

1800

2200

2012 2013 Worst case

Keppel Merlimau Cogen Infrastructure - Others O&M

Property Investments

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

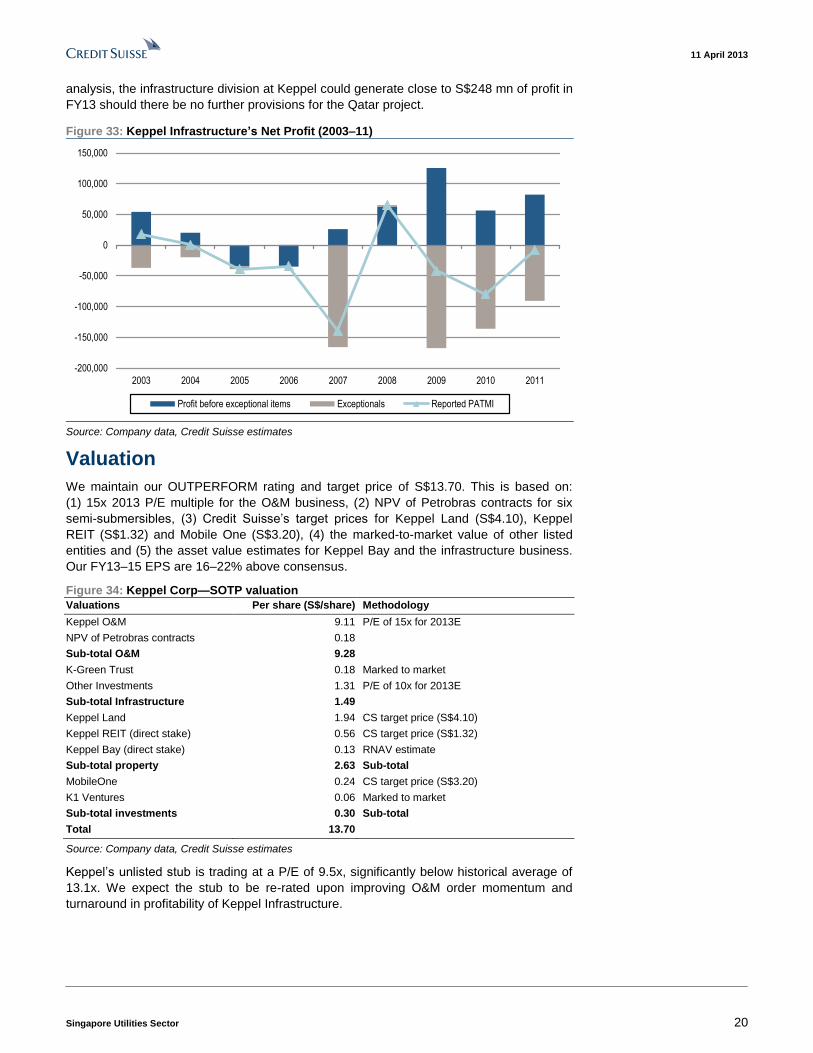

The Infrastructure unit at Keppel has been a drag on the group’s profitability in recent

years, mainly due to provisions made for cost overruns at the Qatar solid waste

management centre and Doha North wastewater treatment plant. We estimated that a

further S$200 mn of provision was taken in 2012, in addition to S$330 mn of provisions

taken between 2010–2011. As such, market expectations for Infrastructure remains low

due to limited visibility on whether there will be further provisions taken. Based on our

Base case: S$123 mn

Worst case: S$33 mn

11 April 2013

Singapore Utilities Sector 20

analysis, the infrastructure division at Keppel could generate close to S$248 mn of profit in

FY13 should there be no further provisions for the Qatar project.

Figure 33: Keppel Infrastructure’s Net Profit (2003–11)

-200,000

-150,000

-100,000

-50,000

0

50,000

100,000

150,000

2003 2004 2005 2006 2007 2008 2009 2010 2011

Profit before exceptional items Exceptionals Reported PATMI

Source: Company data, Credit Suisse estimates

Valuation

We maintain our OUTPERFORM rating and target price of S$13.70. This is based on:

(1) 15x 2013 P/E multiple for the O&M business, (2) NPV of Petrobras contracts for six

semi-submersibles, (3) Credit Suisse’s target prices for Keppel Land (S$4.10), Keppel

REIT (S$1.32) and Mobile One (S$3.20), (4) the marked-to-market value of other listed

entities and (5) the asset value estimates for Keppel Bay and the infrastructure business.

Our FY13–15 EPS are 16–22% above consensus.

Figure 34: Keppel Corp—SOTP valuation

Valuations Per share (S$/share) Methodology

Keppel O&M 9.11 P/E of 15x for 2013E

NPV of Petrobras contracts 0.18

Sub-total O&M 9.28

K-Green Trust 0.18 Marked to market

Other Investments 1.31 P/E of 10x for 2013E

Sub-total Infrastructure 1.49

Keppel Land 1.94 CS target price (S$4.10)

Keppel REIT (direct stake) 0.56 CS target price (S$1.32)

Keppel Bay (direct stake) 0.13 RNAV estimate

Sub-total property 2.63 Sub-total

MobileOne 0.24 CS target price (S$3.20)

K1 Ventures 0.06 Marked to market

Sub-total investments 0.30 Sub-total

Total 13.70

Source: Company data, Credit Suisse estimates

Keppel’s unlisted stub is trading at a P/E of 9.5x, significantly below historical average of

13.1x. We expect the stub to be re-rated upon improving O&M order momentum and

turnaround in profitability of Keppel Infrastructure.

11 April 2013

Singapore Utilities Sector 21

Figure 35: Keppel O&M’s stub valuation

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Dec-0

2

Jun

-03

Dec-0

3

Jun

-04

Dec-0

4

Jun

-05

Dec-0

5

Jun

-06

Dec-0

6

Jun

-07

Dec-0

7

Jun

-08

Dec-0

8

Jun

-09

Dec-0

9

Jun

-10

Dec-1

0

Jun

-11

Dec-1

1

Jun

-12

Dec-1

2

P/E Average +1 std dev -1 std dev

Source: Company data, Credit Suisse estimates, BLOOMBERG

11 April 2013

Singapore Utilities Sector 22

Asia Pacific / China

Electric Utilities

Huaneng Power International Inc (0902.HK / 902 HK)

Quantifying the risks of Tuas

■ We account for the negative impact of the rising competition in the

Singapore power market (i.e., lower tariffs for both vesting & spot) on HNP’s

recurring profit from 2013 onwards (Fig 2).

■ Tuas (one of three key Singapore gencos) constituted 19% of HNP’s 2012

profit. Our base case HNP recurring profit in 2013 implies a 38% decline in

SG profit on lower tariffs and generation (Fig 2). There is 14% downside

under the worst case (Fig 3). However, this is unlikely, in our view, given

Tuas’ exposure to less volatile vesting & direct contracts, rational pricing

behaviour given competitors’ high acquisition costs (i.e., GMR deal) and its

new captive multi-utility Tembusu-Jurong plant from 2014.

■ Our revised EPS forecast (+13%/18% in 2013/14E) takes into account its

-5% UFC and generation guidance (321 bn kwh, Fig 2) in China. Our new

DCF based target price is revised upwards to HK$9.00 (from HK$7.10).

■ While our EPS is 5–9% below consensus, we keep our rating given HNP’s

growing FCF, de-gearing and yield support (~4.6%). We switch our sector

pick to CRP given the risks of irrational price behaviour in SG and higher

capacity growth for CRP versus HNP.

Share price performance

0

100

200

300

400

2

4

6

8

10

Apr-11 Aug-11 Dec-11 Apr-12 Aug-12 Dec-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

MSCI CHINA F IDX which closed at 6033.06 on 08/04/13

On 08/04/13 the spot exchange rate was HK$7.76/US$1

Performance Over 1M 3M 12M Absolute (%) 5.9 17.4 85.5 Relative (%) 6.0 15.0 75.5

Financial and valuation metrics

Year 12/12A 12/13E 12/14E 12/15E Revenue (Rmb mn) 133,294.6 139,485.9 148,118.7 153,608.7 EBITDA (Rmb mn) 28,612.0 33,696.9 35,036.9 37,045.9 EBIT (Rmb mn) 17,579.3 20,804.6 21,320.2 22,467.5 Net profit (Rmb mn) 5,512.5 8,377.3 8,688.3 9,631.2 EPS (CS adj.) (Rmb) 0.39 0.60 0.62 0.69 Change from previous EPS (%) n.a. 13.2 17.6 8.1 Consensus EPS (Rmb) n.a. 0.64 0.69 0.82 EPS growth (%) 367.0 52.0 3.7 10.9 P/E (x) 16.9 11.1 10.7 9.7 Dividend yield (%) 3.2 4.5 4.7 5.2 EV/EBITDA (x) 8.9 7.6 7.2 6.6 P/B (x) 1.7 1.5 1.4 1.3 ROE (%) 10.3 14.2 13.6 14.0 Net debt/equity (%) 237.9 219.7 201.5 175.3

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating OUTPERFORM* Price (08 Apr 13, HK$) 8.29 Target price (HK$) (from 7.10) 9.00¹ Upside/downside (%) 8.6 Mkt cap (HK$ mn) 122,017 (US$ 15,717) Enterprise value (Rmb mn) 256,098 Number of shares (mn) 14,575.38 Free float (%) 51.9 52-week price range 8.54 - 4.27 ADTO - 6M (US$ mn) 16.9

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Edwin Pang

852 2101 6406

11 April 2013

Singapore Utilities Sector 23

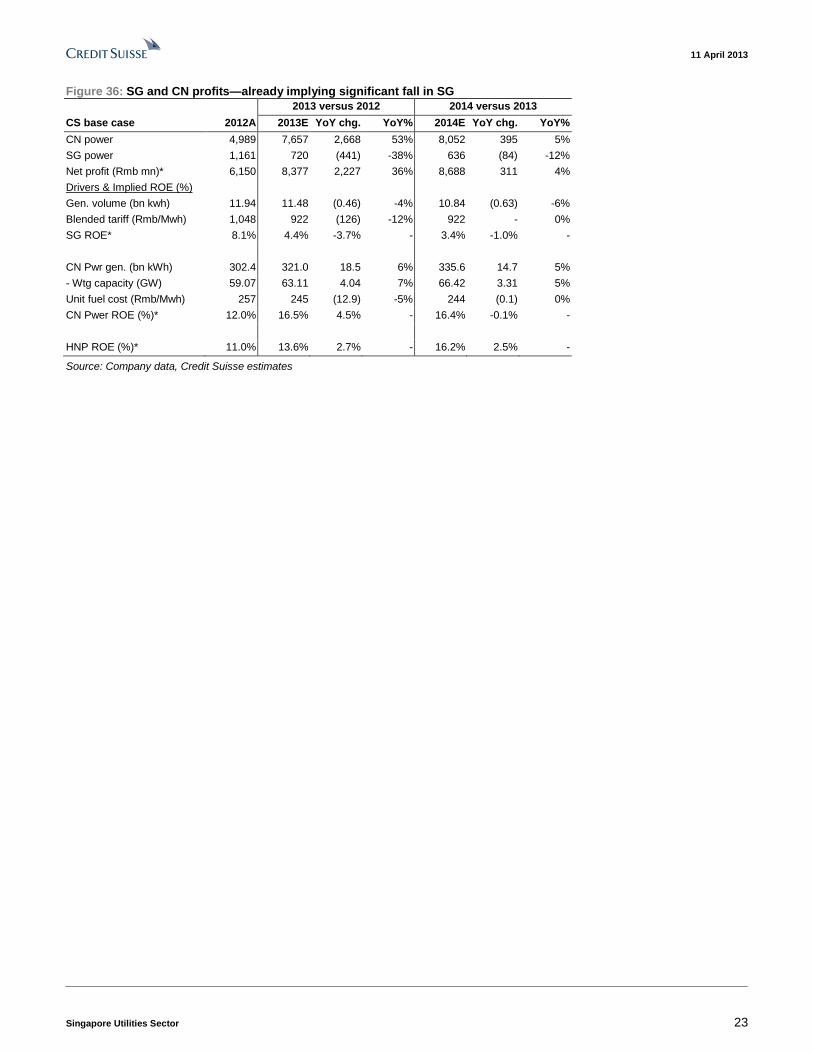

Figure 36: SG and CN profits—already implying significant fall in SG

2013 versus 2012 2014 versus 2013

CS base case 2012A 2013E YoY chg. YoY% 2014E YoY chg. YoY%

CN power 4,989 7,657 2,668 53% 8,052 395 5%

SG power 1,161 720 (441) -38% 636 (84) -12%

Net profit (Rmb mn)* 6,150 8,377 2,227 36% 8,688 311 4%

Drivers & Implied ROE (%)

Gen. volume (bn kwh) 11.94 11.48 (0.46) -4% 10.84 (0.63) -6%

Blended tariff (Rmb/Mwh) 1,048 922 (126) -12% 922 - 0%

SG ROE* 8.1% 4.4% -3.7% - 3.4% -1.0% -

CN Pwr gen. (bn kWh) 302.4 321.0 18.5 6% 335.6 14.7 5%

- Wtg capacity (GW) 59.07 63.11 4.04 7% 66.42 3.31 5%

Unit fuel cost (Rmb/Mwh) 257 245 (12.9) -5% 244 (0.1) 0%

CN Pwer ROE (%)* 12.0% 16.5% 4.5% - 16.4% -0.1% -

HNP ROE (%)* 11.0% 13.6% 2.7% - 16.2% 2.5% -

Source: Company data, Credit Suisse estimates

11 April 2013

Singapore Utilities Sector 24

Asia Pacific / Malaysia

Electric Utilities

YTL Power

(YTLP.KL / YTLP MK)

More bad news

■ Singapore sting: YTL Power’s (YTLP) wholly owned merchant power plant

in Singapore, Power Seraya, will be adversely affected by the 30% capacity

increase in the island state over 2013–14. The expected 15% fall in the

Uniform Singapore Electricity Price (USEP) will result in an estimated 19%

decline in YTL Power’s FY14 EPS.

■ Malaysia maelstrom: The outlook for YTLP power in its home market

remains poor. The company was unsuccessful in extending the Power

Purchase Agreement (PPA) for its Pasir Gudang plant that is set to expire in

2016. The future of the power plant, which sits on TNB land leased until

2016, is also unclear at this stage. Meanwhile, we expect YTLP’s WiMax

based telco, YES, to continue to report losses as it struggles to achieve its

1 mn target subscriber base to break even (0.5 mn subs at end-2012).

■ UK water woes: YTLP’s Wessex Water is perceived to be in a low-risk

sector, with fixed regulatory framework and inflation-linked cash flows.

However, impending regulatory changes under the 2014 price control review

(PR14) could see a reduction in ‘allowed returns’ for the sector. Moreover,

regulator OFWAT is considering removing the RPI-linkage of prices. At the

same time, the UK’s ‘Office for National Statistics’ is considering adjusting

the way RPI is calculated, which could lower both RPI and returns to the

water companies.

■ Maintain UNDERPERFORM: On the back of these developments, we have

downgraded our FY13–14 forecast by 11–30%, and reduced our SOTP

based target price to RM1.40 (from RM1.82). We remain negative on YTLP

and reiterate our UNDERPERFORM rating on the stock. However, for

exposure to the YTL group, we prefer YTL Corp.

Share price performance

40

60

80

100

120

0

1

2

3

4

Apr-11 Aug-11 Dec-11 Apr-12 Aug-12 Dec-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

FTSE BURSA MALAYSIA KLCI IDX which closed at 1693.31

on 08/04/13

On 08/04/13 the spot exchange rate was RM3.06/US$1

Performance Over 1M 3M 12M Absolute (%) -4.5 -10.2 -17.6 Relative (%) -4.3 -12.6 -27.6

Financial and valuation metrics

Year 6/12A 6/13E 6/14E 6/15E Revenue (RM mn) 15,876.2 15,448.2 14,130.6 14,380.2 EBITDA (RM mn) 2,824.8 3,158.0 2,934.3 3,058.2 EBIT (RM mn) 1,664.3 2,052.8 1,807.3 1,909.1 Net profit (RM mn) 1,229.9 1,317.4 1,115.5 1,184.8 EPS (CS adj.) (RM) 0.15 0.16 0.14 0.15 Change from previous EPS (%) n.a. -10.6 -30.0 Consensus EPS (RM) n.a. 0.16 0.17 0.17 EPS growth (%) -7.7 6.8 -14.8 5.9 P/E (x) 9.7 9.1 10.7 10.1 Dividend yield (%) 4.4 4.4 4.4 4.4 EV/EBITDA (x) 12.0 10.8 11.6 11.1 P/B (x) 1.3 1.2 1.1 1.1 ROE (%) 13.7 13.4 10.5 10.5 Net debt/equity (%) 235.2 218.5 207.2 195.3

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating UNDERPERFORM* Price (08 Apr 13, RM) 1.50 Target price (RM) (from 1.82) 1.40¹ Upside/downside (%) -6.7 Mkt cap (RM mn) 11,007 (US$ 3,598) Enterprise value (RM mn) 33,993 Number of shares (mn) 7,337.94 Free float (%) 38.6 52-week price range 1.85 - 1.41 ADTO - 6M (US$ mn) 1.8

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Annuar Aziz

60 3 2723 2084

11 April 2013

Singapore Utilities Sector 25

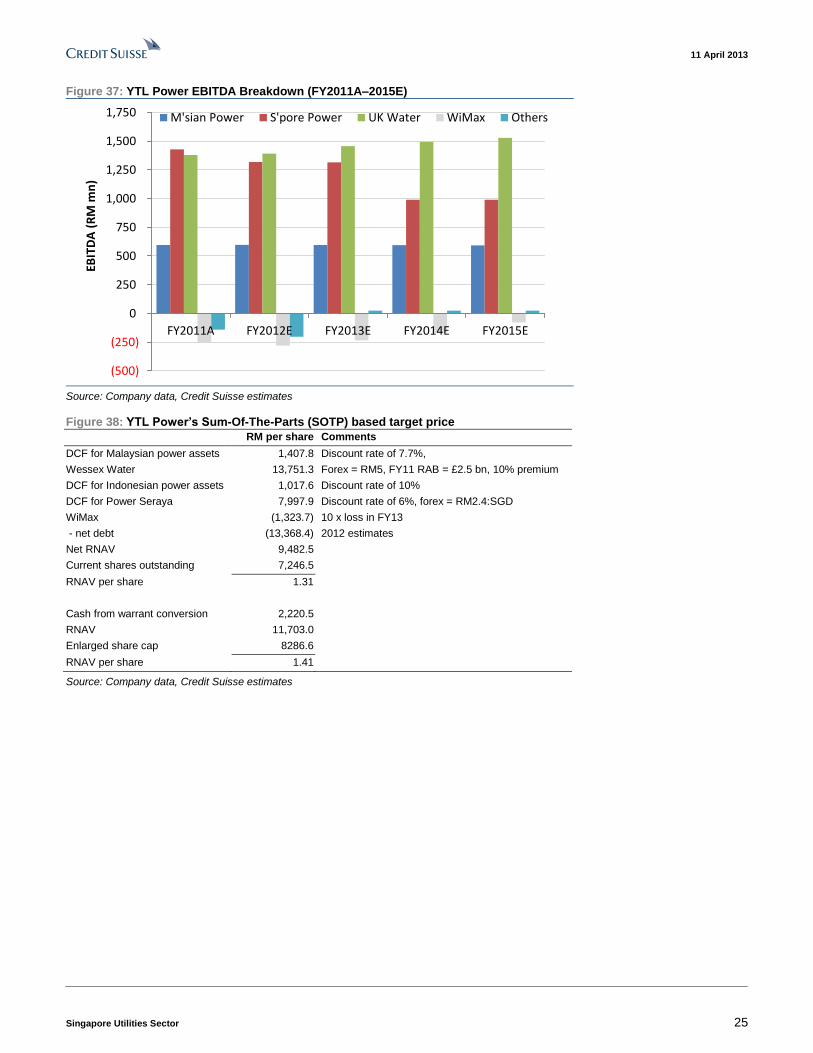

Figure 37: YTL Power EBITDA Breakdown (FY2011A–2015E)

(500)

(250)

0

250

500

750

1,000

1,250

1,500

1,750

FY2011A FY2012E FY2013E FY2014E FY2015E

EBIT

DA

(R

M m

n)

M'sian Power S'pore Power UK Water WiMax Others

Source: Company data, Credit Suisse estimates

Figure 38: YTL Power’s Sum-Of-The-Parts (SOTP) based target price

RM per share Comments

DCF for Malaysian power assets 1,407.8 Discount rate of 7.7%,

Wessex Water 13,751.3 Forex = RM5, FY11 RAB = £2.5 bn, 10% premium

DCF for Indonesian power assets 1,017.6 Discount rate of 10%

DCF for Power Seraya 7,997.9 Discount rate of 6%, forex = RM2.4:SGD

WiMax (1,323.7) 10 x loss in FY13

- net debt (13,368.4) 2012 estimates

Net RNAV 9,482.5

Current shares outstanding 7,246.5

RNAV per share 1.31

Cash from warrant conversion 2,220.5

RNAV 11,703.0

Enlarged share cap 8286.6

RNAV per share 1.41

Source: Company data, Credit Suisse estimates

11 April 2013

Singapore Utilities Sector 26

Appendix—Singapore power market Overview of the industry

The Energy Market Authority, a statutory board under the Ministry of Trade and Industry, is

responsible for the overall regulation of the electricity and gas industries in Singapore.

Governed by the Electricity Act, The National Electricity Market of Singapore (NEMS)

seeks to ensure an efficient supply of competitively priced electricity, amongst other

objectives.

The decision to liberalise the power and gas industries in Singapore was undertaken in

1995, when Singapore Power was first corporatised from a government statutory board to

a commercial company. Following the acquisition of Singapore Power by Temasek

Holdings, various power system assets were subsequently restructured to facilitate

privatisation, with the divestment of all three power generation companies in 2008: Tuas

Power was sold to China Huaneng Group, Senoko Power was sold to the Lion Power

consortium while PowerSeraya was sold to YTL Power.

Of the total electricity generated, a significant 78% is fuelled by Natural Gas, with

petroleum products such as fuel oil contributing 18% of the fuel mix and other fuel such as

waste incineration making up the remaining 4%. This is in line with the increasing role of

Combined Cycle Gas Turbines (CCGT) plants by generation companies due to its better

efficiency and cleaner environmental footprint. At present, 70% of the licensed generating

capacity in operation comprise CCGT plants.

Figure 39: Licensed generating capacity by type (2012) Figure 40: Fuel mix for electricity generation (2011)

Combined Cycle Gas

Turbine (CCGT)

70%

Steam Plant25%

Incineration & Others

3%

Open Cycle Gas Turbine

(OCGT)2%

Natural Gas78%

Petroleum Products

18%

Others4%

Source: Energy Market Authority Source: Energy Market Authority

Of the total licensed generating capacity of about 10,202 MW, PowerSeraya, Tuas Power

and Senoko Power command a dominant 84% of capacity, with Senoko Power having the

highest capacity of 3,300 MW comprising CCGT and steam plants. Historically, the market

share of generating capacity has remained largely unchanged due to the lack of new

plants coming on-stream. The market share of electricity sales in the power generation

market exhibit a similar proportion, with the three dominant generation companies

occupying a significant share of the entire market.

11 April 2013

Singapore Utilities Sector 27

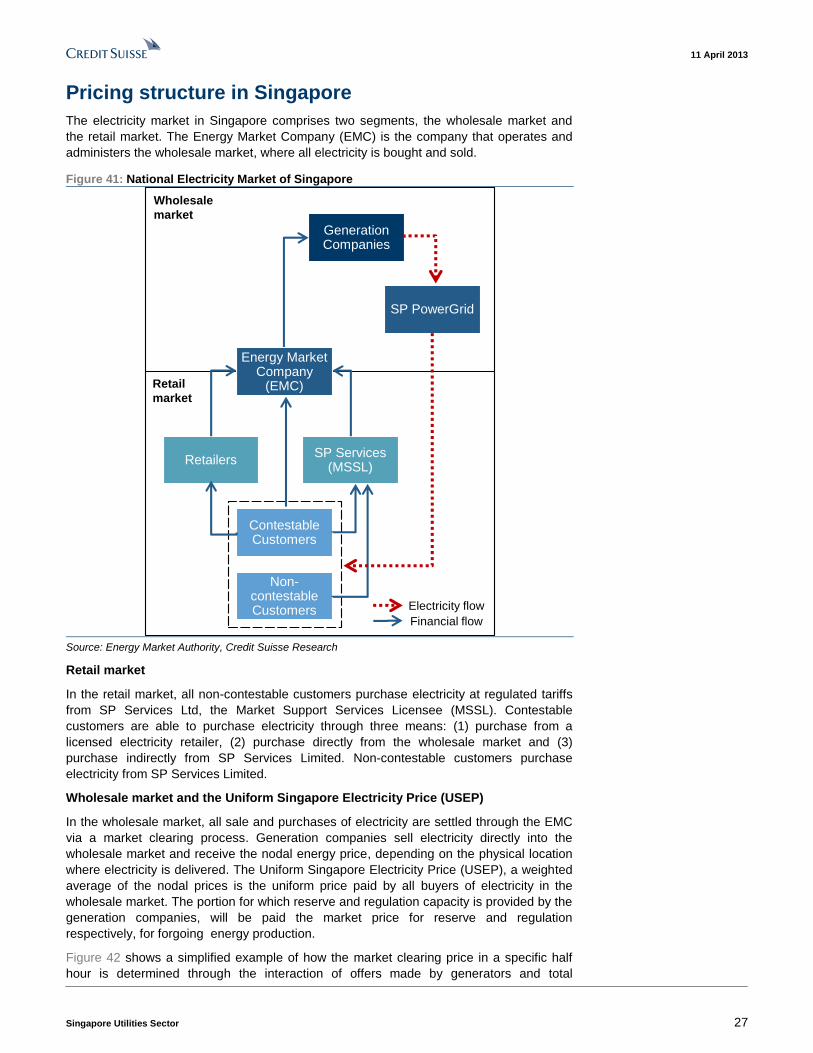

Pricing structure in Singapore

The electricity market in Singapore comprises two segments, the wholesale market and

the retail market. The Energy Market Company (EMC) is the company that operates and

administers the wholesale market, where all electricity is bought and sold.

Figure 41: National Electricity Market of Singapore

Generation Companies

Contestable Customers

Wholesale

market

Electricity flow

Non-contestable Customers

RetailersSP Services

(MSSL)

SP PowerGrid

Financial flow

Energy Market Company

(EMC)Retail

market

Source: Energy Market Authority, Credit Suisse Research

Retail market

In the retail market, all non-contestable customers purchase electricity at regulated tariffs

from SP Services Ltd, the Market Support Services Licensee (MSSL). Contestable

customers are able to purchase electricity through three means: (1) purchase from a

licensed electricity retailer, (2) purchase directly from the wholesale market and (3)

purchase indirectly from SP Services Limited. Non-contestable customers purchase

electricity from SP Services Limited.

Wholesale market and the Uniform Singapore Electricity Price (USEP)

In the wholesale market, all sale and purchases of electricity are settled through the EMC

via a market clearing process. Generation companies sell electricity directly into the

wholesale market and receive the nodal energy price, depending on the physical location

where electricity is delivered. The Uniform Singapore Electricity Price (USEP), a weighted

average of the nodal prices is the uniform price paid by all buyers of electricity in the

wholesale market. The portion for which reserve and regulation capacity is provided by the

generation companies, will be paid the market price for reserve and regulation

respectively, for forgoing energy production.

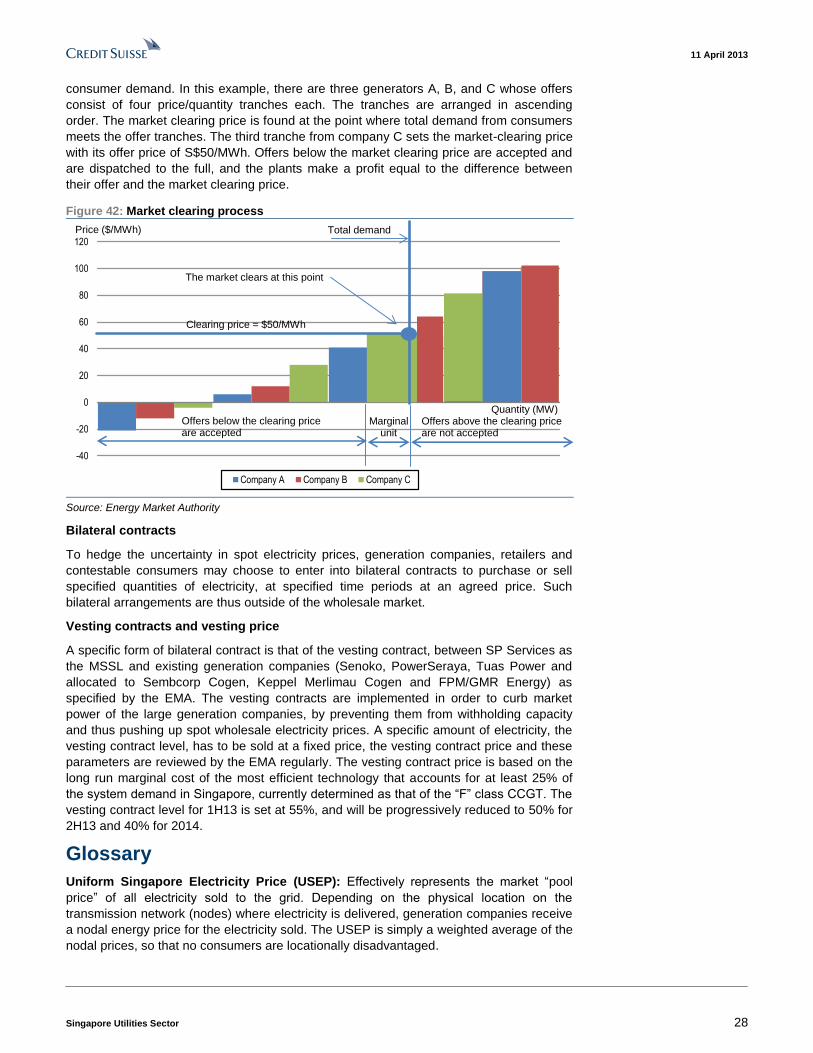

Figure 42 shows a simplified example of how the market clearing price in a specific half

hour is determined through the interaction of offers made by generators and total

11 April 2013

Singapore Utilities Sector 28

consumer demand. In this example, there are three generators A, B, and C whose offers

consist of four price/quantity tranches each. The tranches are arranged in ascending

order. The market clearing price is found at the point where total demand from consumers

meets the offer tranches. The third tranche from company C sets the market-clearing price

with its offer price of S$50/MWh. Offers below the market clearing price are accepted and

are dispatched to the full, and the plants make a profit equal to the difference between

their offer and the market clearing price.

Figure 42: Market clearing process

-40

-20

0

20

40

60

80

100

120

Company A Company B Company C

Price ($/MWh)

Offers below the clearing price are accepted

Offers above the clearing price are not accepted

Marginal unit

Clearing price = $50/MWh

Total demand

The market clears at this point

Quantity (MW)

Source: Energy Market Authority

Bilateral contracts

To hedge the uncertainty in spot electricity prices, generation companies, retailers and

contestable consumers may choose to enter into bilateral contracts to purchase or sell

specified quantities of electricity, at specified time periods at an agreed price. Such

bilateral arrangements are thus outside of the wholesale market.

Vesting contracts and vesting price

A specific form of bilateral contract is that of the vesting contract, between SP Services as

the MSSL and existing generation companies (Senoko, PowerSeraya, Tuas Power and

allocated to Sembcorp Cogen, Keppel Merlimau Cogen and FPM/GMR Energy) as

specified by the EMA. The vesting contracts are implemented in order to curb market

power of the large generation companies, by preventing them from withholding capacity

and thus pushing up spot wholesale electricity prices. A specific amount of electricity, the

vesting contract level, has to be sold at a fixed price, the vesting contract price and these

parameters are reviewed by the EMA regularly. The vesting contract price is based on the

long run marginal cost of the most efficient technology that accounts for at least 25% of

the system demand in Singapore, currently determined as that of the “F” class CCGT. The

vesting contract level for 1H13 is set at 55%, and will be progressively reduced to 50% for

2H13 and 40% for 2014.

Glossary

Uniform Singapore Electricity Price (USEP): Effectively represents the market “pool

price” of all electricity sold to the grid. Depending on the physical location on the

transmission network (nodes) where electricity is delivered, generation companies receive

a nodal energy price for the electricity sold. The USEP is simply a weighted average of the

nodal prices, so that no consumers are locationally disadvantaged.

11 April 2013

Singapore Utilities Sector 29

SP PowerGrid: Manages and operates the electricity network. SP PowerGrid is owned by

SP PowerAssets, which owns the network assets in Singapore.

High Sulphur Fuel Oil (HSFO): A form of residual (heavy) fuel oil with a high sulphur

content, used as a proxy to fuel costs. HSFO 180 CST is used as a benchmark as it is

widely used due to its emission standards. As Singapore’s electricity is mainly generated

from natural gas, the prices of natural gas as set out in commercial gas contracts signed

by generation companies are indexed to fuel oil prices.

Liquefied Natural Gas (LNG): Formed through the process of cooling natural gas (mainly

methane) to its liquid form. Transported through LNG tankers to regasification terminals

where they are heated and delivered in a gaseous state to power plants, as opposed to

natural gas from the gas fields delivered through pipelines.

Combined Cycle Gas Turbine (CCGT) plants: A more efficient plant with lower

emissions, primarily using natural gas to generate electricity. Excess heat produced

through a gas turbine is made use of to power a steam turbine, resulting in a greater

thermal efficiency.

Open Cycle Gas Turbine (OCGT) plants: Produces electricity through the combustion of

natural gas.

Wholesale market: Started on 1 January 2003. Represents the electricity market where

generation companies bid to sell electricity to the market at half hourly intervals daily. The

Energy Market Company (EMC) operates and administers the wholesale market.

Retail market: Represents the electricity market where end consumers purchase

electricity from retailers or from SP Services Ltd.

SP Services: Currently the only Market Support Services Licensee (MSSL), responsible

for providing services such as meter reading and meter data management. Also

responsible for supply electricity to all non-contestable consumers and maintains a central

register of all consumers in Singapore.

Contestable Consumers: Consumers who occupy a non-residential location and either

require high voltage supplies or has an average monthly electricity consumption of 10,000

kilowatt-hour and above. These customers are able to purchase electricity through three

means: 1) purchase from a licensed electricity retailer, 2) purchase directly from the

wholesale market and 3) purchase indirectly from SP Services Limited.

Non-contestable Consumers: Domestic consumers and all other consumers of electricity

in Singapore.

Reserve price: Consists of prices for three classes of reserves, namely primary,

secondary and contingency reserves. Represents the price paid to generation companies

for maintaining reserve generation capacity in the event of unexpected demand.

Reserve price: Represents the price paid for regulation capacity, used to cover second-

to-second variations in demand away from the estimated demand.

Vesting contracts: A unique form of bilateral contracts between SP Services and

generation companies. Implemented in order to curb market power of the large generation

companies, by preventing them from withholding capacity and thus pushing up spot

wholesale electricity prices. Determined by the authority every two years, a specific

amount of electricity, the vesting contract level, has to be sold at a fixed price, the vesting

contract price.

Vesting Contract Hedge Price (VCHP): Calculated quarterly. Set by the authority taking

into account both the long run marginal cost (LRMC) of the most efficient technology that

accounts for at least 25% of the system demand in Singapore.

Vesting Contract Hedge Quantity (VCHQ): Represents the hedge quantity allocated to

the generation companies, and settled quarterly based on the VCHP.

11 April 2013

Singapore Utilities Sector 30

Companies Mentioned (Price as of 08-Apr-2013)

China Resources Power Holdings (0836.HK, HK$22.9, OUTPERFORM, TP HK$23.0) First Pacific Company Limited (0142.HK, HK$10.54) GDF Suez (GSZ.PA, €15.25) GIL (GMRI.NS, Rs22.0) Huaneng Power International Inc (0902.HK, HK$8.29, OUTPERFORM, TP HK$9.0) Hyflux Ltd (HYFL.SI, S$1.41) Kansai Electric Power (9503.T, ¥912) Keppel Corporation (KPLM.SI, S$11.16, OUTPERFORM, TP S$13.7) Keppel Land (KLAN.SI, S$3.89) Keppel REIT (KASA.SI, S$1.36) Kyushu Electric Power (9508.T, ¥1,005) M1 Limited (MONE.SI, S$2.99) Manila Electric (Meralco) (MER.PS, P325.0) Marubeni Corp (8002.T, ¥666) Sembcorp Industries Limited (SCIL.SI, S$5.08, NEUTRAL, TP S$5.1) Sembcorp Marine Ltd. (SCMN.SI, S$4.33) YTL Power (YTLP.KL, RM1.5, UNDERPERFORM, TP RM1.4)

Disclosure Appendix

Important Global Disclosures

Gerald Wong, CFA, Edwin Pang and Annuar Aziz each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

Price and Rating History for China Resources Power Holdings (0836.HK)

0836.HK Closing Price Target Price

Date (HK$) (HK$) Rating

25-Aug-10 16.78 21.30 O *

27-Jan-11 13.62 18.36

23-Aug-11 13.16 18.05

13-Feb-12 15.20 18.25

21-Aug-12 17.06 19.00

03-Oct-12 16.78 19.70

19-Mar-13 22.65 23.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

Price and Rating History for Huaneng Power International Inc (0902.HK)

0902.HK Closing Price Target Price

Date (HK$) (HK$) Rating

25-Aug-10 4.55 5.86 O *

27-Jan-11 4.36 5.08

11-Aug-11 3.32 4.65

26-Oct-11 3.46 4.50

13-Feb-12 4.95 5.96

22-Mar-12 4.51 5.70

02-Aug-12 5.62 5.85

03-Oct-12 5.88 7.10

* Asterisk signifies initiation or assumption of coverage. O U T PERFO RM

11 April 2013

Singapore Utilities Sector 31

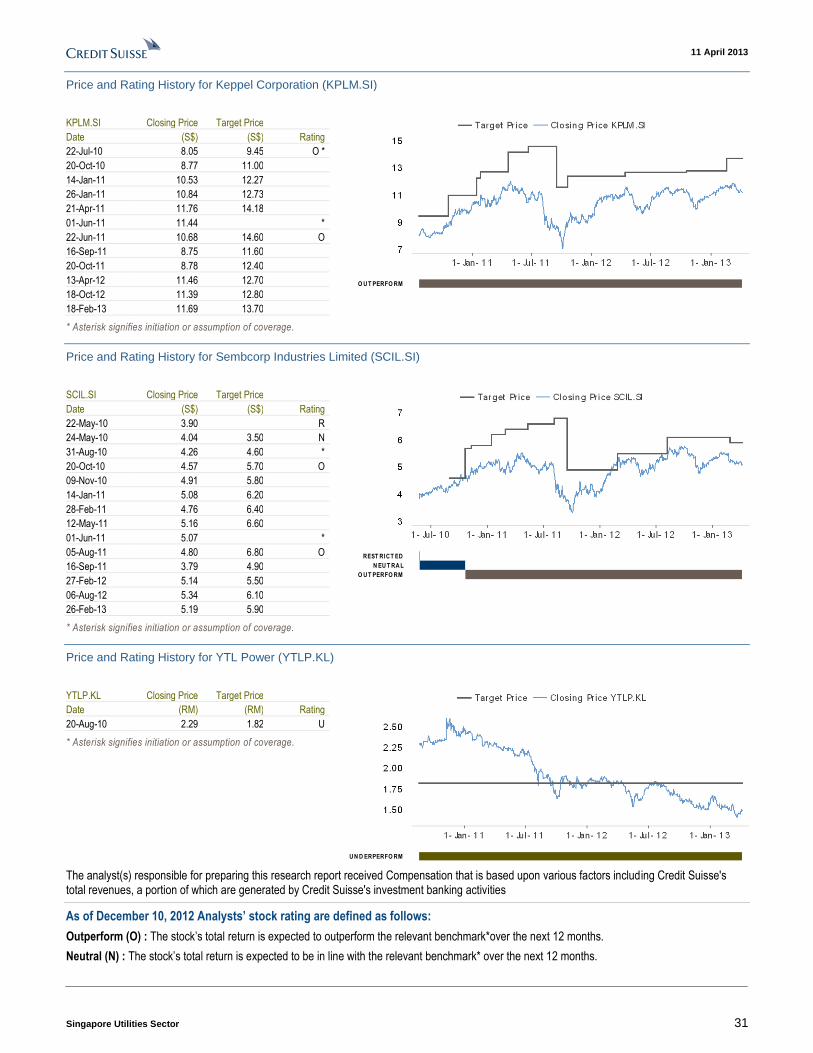

Price and Rating History for Keppel Corporation (KPLM.SI)

KPLM.SI Closing Price Target Price

Date (S$) (S$) Rating

22-Jul-10 8.05 9.45 O *

20-Oct-10 8.77 11.00

14-Jan-11 10.53 12.27

26-Jan-11 10.84 12.73

21-Apr-11 11.76 14.18

01-Jun-11 11.44 *

22-Jun-11 10.68 14.60 O

16-Sep-11 8.75 11.60

20-Oct-11 8.78 12.40

13-Apr-12 11.46 12.70

18-Oct-12 11.39 12.80

18-Feb-13 11.69 13.70

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

Price and Rating History for Sembcorp Industries Limited (SCIL.SI)

SCIL.SI Closing Price Target Price

Date (S$) (S$) Rating

22-May-10 3.90 R

24-May-10 4.04 3.50 N

31-Aug-10 4.26 4.60 *

20-Oct-10 4.57 5.70 O

09-Nov-10 4.91 5.80

14-Jan-11 5.08 6.20

28-Feb-11 4.76 6.40

12-May-11 5.16 6.60

01-Jun-11 5.07 *

05-Aug-11 4.80 6.80 O

16-Sep-11 3.79 4.90

27-Feb-12 5.14 5.50

06-Aug-12 5.34 6.10

26-Feb-13 5.19 5.90

* Asterisk signifies initiation or assumption of coverage.

REST RICT ED

N EU T RA L

O U T PERFO RM

Price and Rating History for YTL Power (YTLP.KL)

YTLP.KL Closing Price Target Price

Date (RM) (RM) Rating

20-Aug-10 2.29 1.82 U

* Asterisk signifies initiation or assumption of coverage.

UN D ERPERFO RM

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

11 April 2013

Singapore Utilities Sector 32

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.