Embed Size (px)

Citation preview

ed: TH / sa: JC, PY

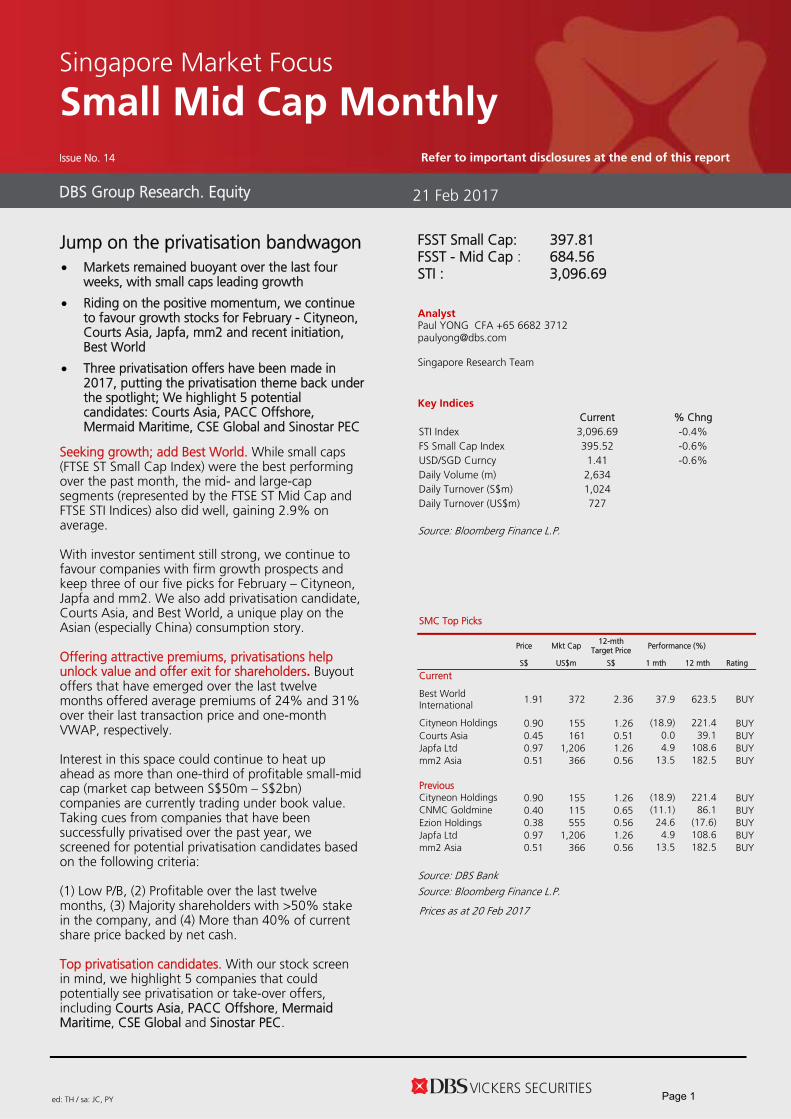

FSST Small Cap: 397.81 FSST - Mid Cap : 684.56 STI : 3,096.69

Analyst Paul YONG CFA +65 6682 3712 [email protected]

Singapore Research Team

Key Indices

Current % ChngSTI Index 3,096.69 -0.4% FS Small Cap Index 395.52 -0.6% USD/SGD Curncy 1.41 -0.6% Daily Volume (m) 2,634 Daily Turnover (S$m) 1,024 Daily Turnover (US$m) 727

Source: Bloomberg Finance L.P.

Prices as at 20 Feb 2017

Source: DBS Bank Source: Bloomberg Finance L.P.

DBS Group Research. Equity 21 Feb 2017

Singapore Market Focus

Small Mid Cap MonthlyIssue No. 14 Refer to important disclosures at the end of this report

Jump on the privatisation bandwagon Markets remained buoyant over the last four

weeks, with small caps leading growth

Riding on the positive momentum, we continueto favour growth stocks for February - Cityneon,Courts Asia, Japfa, mm2 and recent initiation,Best World

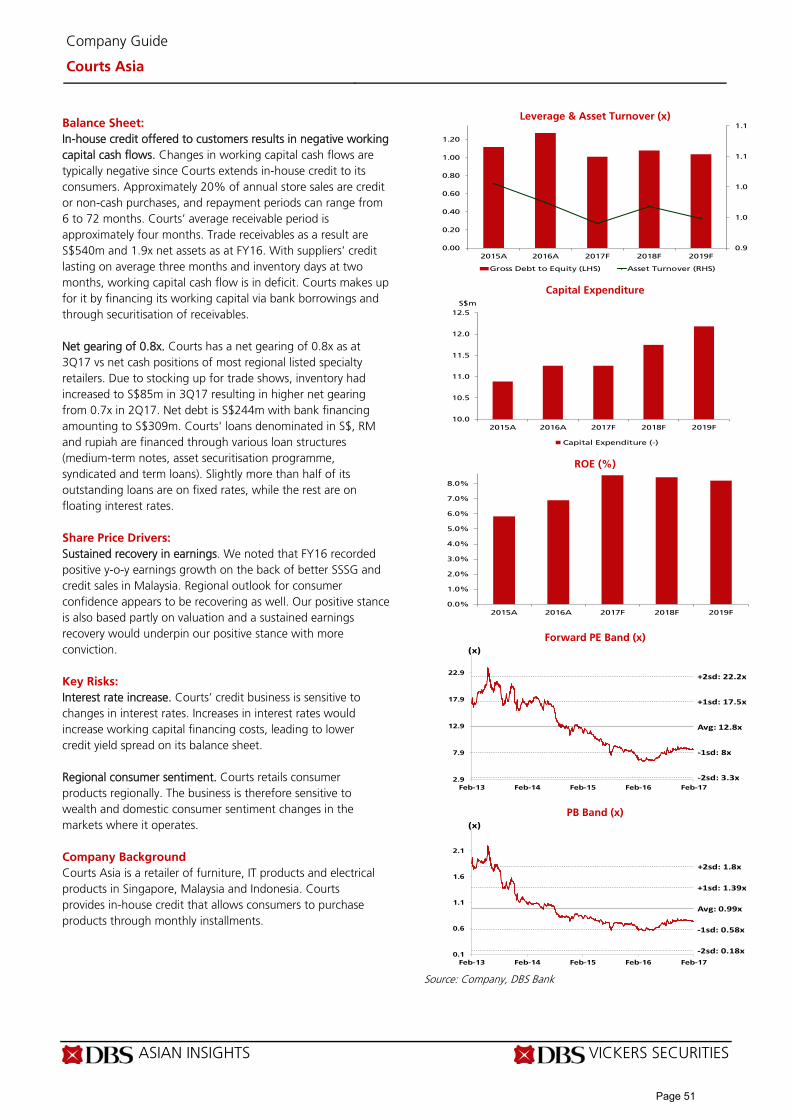

Three privatisation offers have been made in2017, putting the privatisation theme back underthe spotlight; We highlight 5 potentialcandidates: Courts Asia, PACC Offshore,Mermaid Maritime, CSE Global and Sinostar PEC

Seeking growth; add Best World. While small caps (FTSE ST Small Cap Index) were the best performing over the past month, the mid- and large-cap segments (represented by the FTSE ST Mid Cap and FTSE STI Indices) also did well, gaining 2.9% on average.

With investor sentiment still strong, we continue to favour companies with firm growth prospects and keep three of our five picks for February – Cityneon, Japfa and mm2. We also add privatisation candidate, Courts Asia, and Best World, a unique play on the Asian (especially China) consumption story.

Offering attractive premiums, privatisations help unlock value and offer exit for shareholders. Buyout offers that have emerged over the last twelve months offered average premiums of 24% and 31% over their last transaction price and one-month VWAP, respectively.

Interest in this space could continue to heat up ahead as more than one-third of profitable small-mid cap (market cap between S$50m – S$2bn) companies are currently trading under book value. Taking cues from companies that have been successfully privatised over the past year, we screened for potential privatisation candidates based on the following criteria:

(1) Low P/B, (2) Profitable over the last twelve months, (3) Majority shareholders with >50% stake in the company, and (4) More than 40% of current share price backed by net cash.

Top privatisation candidates. With our stock screen in mind, we highlight 5 companies that could potentially see privatisation or take-over offers, including Courts Asia, PACC Offshore, Mermaid Maritime, CSE Global and Sinostar PEC.

SMC Top Picks

Price Mkt Cap 12-mth Target Price Performance (%)

S$ US$m S$ 1 mth 12 mth Rating

Current

Best World International

1.91 372 2.36 37.9 623.5 BUY

Cityneon Holdings 0.90 155 1.26 (18.9) 221.4 BUY Courts Asia 0.45 161 0.51 0.0 39.1 BUY Japfa Ltd 0.97 1,206 1.26 4.9 108.6 BUY mm2 Asia 0.51 366 0.56 13.5 182.5 BUY

Previous Cityneon Holdings 0.90 155 1.26 (18.9) 221.4 BUY CNMC Goldmine 0.40 115 0.65 (11.1) 86.1 BUY Ezion Holdings 0.38 555 0.56 24.6 (17.6) BUY Japfa Ltd 0.97 1,206 1.26 4.9 108.6 BUY mm2 Asia 0.51 366 0.56 13.5 182.5 BUY

Page 1

Market Focus

Small Mid Cap Monthly

Conviction picks for January & February

Our January picks declined 0.5% on average. Performances among our conviction picks for January were fairly mixed, with mm2 Asia and Japfa further extending their gains by 8.6% and 7.4% over the last four weeks, respectively and outperforming the three indices (FTSE STI +2.8%, FTSE ST Small Cap +3.6% and FTSE Mid Cap +2.3%). Meanwhile, a pullback in Ezion following its four-month rally resulted in a 7.3% m-o-m decline. In anticipation of a weak set of results (mainly due to unrealised forex losses) for 4Q16, CNMC Goldmine also fell 7.0% m-o-m. Beyond the temporary blip, higher gold production and gold prices could catalyse earnings for the group, with further upside potential from M&A.

Desc. 1M Price Performance* Dec Conviction Picks +0.5% Cityneon Holdings -2.2% CNMC Goldmine -7.0% Ezion -7.3% Japfa +5.4% mm2 Asia +8.6% Indices (STI, FSTS and FSTM) +2.9% FTSE STI +2.8% FSTS Index +3.6% FSTM Index +2.3%

*Refers to change in last price between 17th Jan and 16th Feb Source: DBS Bank, Bloomberg Finance L.P

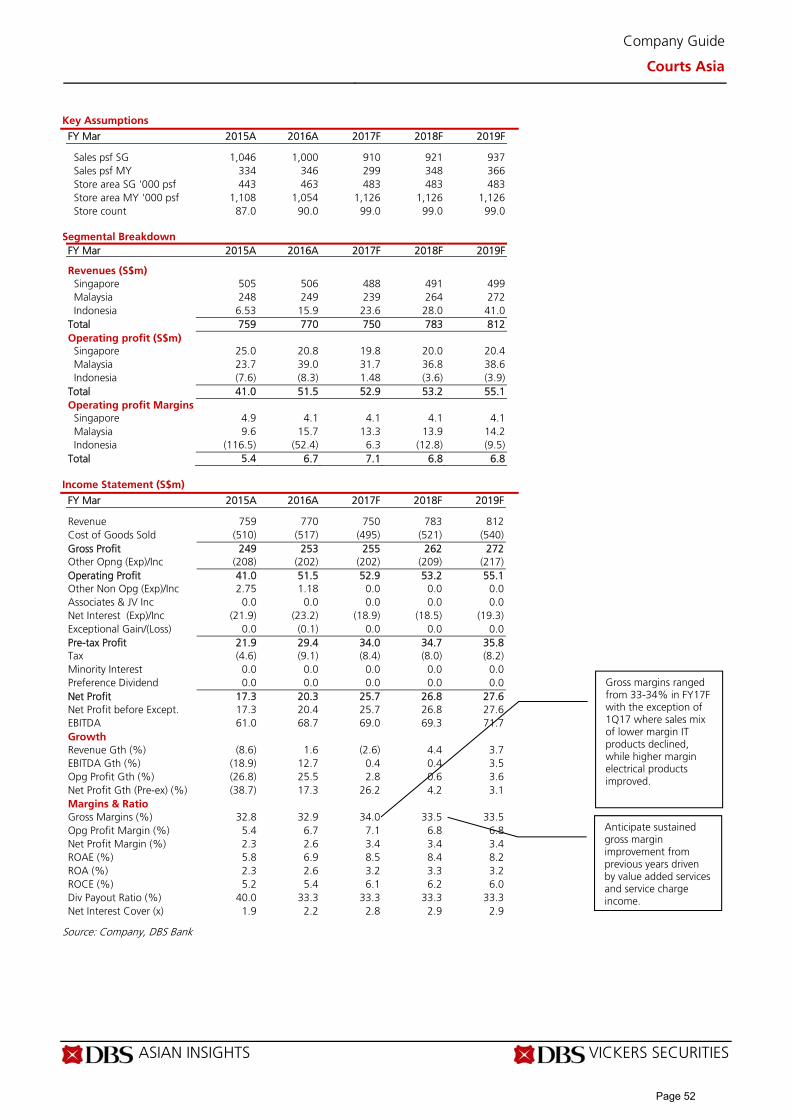

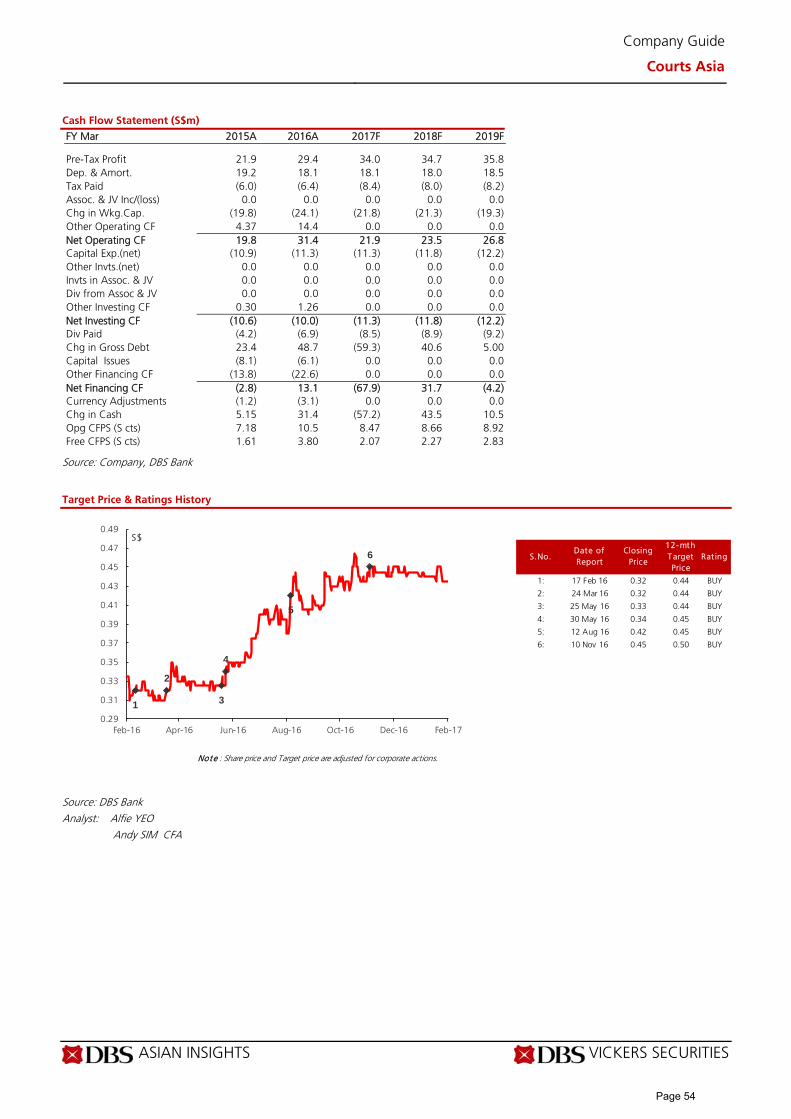

Include new initiation, Best World International (BUY, TP S$2.36) and Courts Asia (BUY, TP S$0.51) among conviction picks for February. With earnings momentum in Taiwan likely to be sustained by targeted efforts to cultivate existing networks and leapfrog into Northern Taiwan and MOFCOM’s indirect endorsement through the recent award of its direct selling license in the PRC providing the company with the credibility and platform needed to gain scale in China, we like Best World as a unique play on the Asian (especially China) consumption story. Riding on the steady growth outlook of its key markets of Taiwan and China, we project PATMI to rise quickly at 68% CAGR from S$10.1m in FY15 to S$48m by FY18F, and opine that it should trade at a smaller discount to global peers’ 19x forward PE. On track to to post core earnings growth of 30% y-o-y on the back of better cost controls, stronger gross margins and lower interest costs, earnings recovery for Courts Asia will be led by store network expansion plans in Indonesia and Malaysia, which in turn should benefit from the expected acceleration in GDP growth and consumer sentiment recovery regionally in 2017. Apart from compelling valuations of 8x FY18F PE (near -0.5SD of its historical forward PE valuation) and 0.7x P/B, we also like Courts , which is more than 70% owned by Singapore Retail Group, as a potential privatisation play.

No. Security Desc. Sector Rating Last Price

(17-Jan)

12-mth

Target Price

Upside/

(Downside)

Catalyst

1 Best World

International

Consumer

Services

BUY 0.910 2.36 24% 1) Earnings delivery

2) Successful expansion into new

markets

3) M&A

2 Cityneon Holdings

Consumer

Services

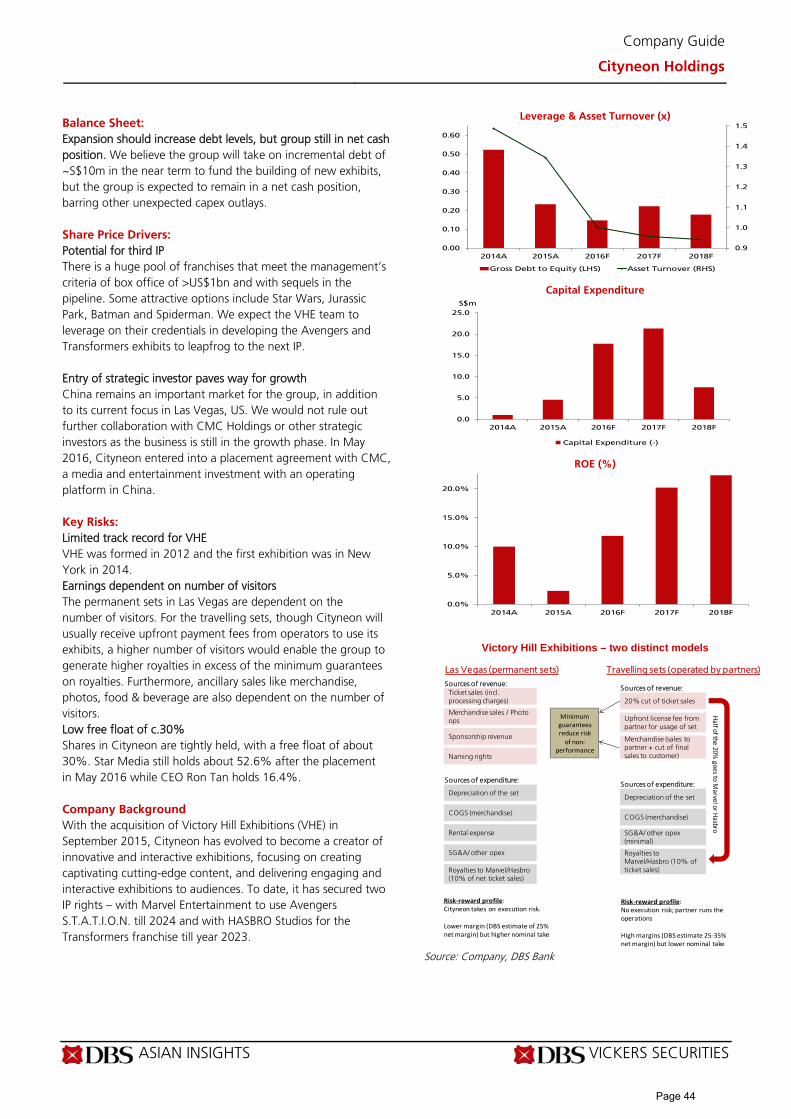

BUY 0.900 1.26 40% 1) Securing of third IP

2) Entry of strategic investor

3 Courts Asia

Consumer

Services

BUY 0.440 0.51 16% 1) Earnings recovery

2) M&A

4 Japfa Ltd Consumer

Goods

BUY 1.000 1.26 26% 1) Resilence despite typically weaker

4Q earnings

2) Continued growth in all segments

5 mm2 Asia Consumer

Services

BUY 0.505 0.56 11% 1) Earnings-accretive acquisitions

2) UnUsual listing

Source: DBS Bank, Bloomberg Finance L.P

Page 2

Market Focus

Small Mid Cap Monthly

Revisting potential privatisation plays Recent buyout offers put privatisation theme back under the spotlight. Barely two months into the new year, we have already seen buyout offers for three companies, including Healthway Medical and Auric Pacific, offering premiums between 5% to 21% over their last transaction price and 14% to 21% over one-month VWAP. Privatisation premium offered. We estimate that the 20 small-mid companies (of which 14 have been delisted and privatised) that have announced potential privatisations over the last 12 months offered average premiums of 24% and 31% over their last transaction price and one-month VWAP, respectively. At least two-thirds of privatisation candidates were trading below book, while a further two companies were trading at low P/BV of under 1.1x just before their respective offer announcements. A quarter of the privatisation candidates were S-Chips. Of the 20 offers, 75% were made by majority shareholders (nearly half of which were by founding families). At least 15% were led by management or the executive team, while third-party offers only represented 10%. Privatisations help unlock value and offer exit for shareholders. For majority-owned companies trading at persistently low valuations and with less incentive to maintain their listing - especially cash-rich companies with low capex

needs, privatisations can often serve as a means of unlocking value for shareholders, while freeing up company resources towards longer-term objectives and growth. What have been the premiums offered? Premiums can vary pretty widely across deals, looking at small mid-cap privatisations (deal size under S$2 bn and excludes third-party offers) that have gone through successfully over the last 12 months, we found that:- a) Low P/BV companies were more likely to receive privatisation offers (70% were trading below book value) and saw higher premiums on average, b) Higher premiums (>38% over 1mth VWAP) were often required to entice shareholders of companies trading at prices that were much lower compared to their historical peak, c) Conversely, premiums for companies trading close to the upper end of their historical range (i.e. Sim Lian) were more modest, at about 15-20%. Unsurprisingly, prior to the offer, these companies were at least 50% majority owned. While offerors in our sample year did not appear to show bias for net cash companies, we opine that in a rising rate environment, companies with net cash could potentially be more attractive targets, particularly for third-party buyers.

Target Company

Announcement

Deal Size (S$ m)

Final Offer Price

Premium/(Discount) of the Offer Price over Relevant Prices prior to Announcement

Book Value per Share*

(Last Reported)

% Majority owned

Net Cash (Debt)?

Last Transacted Price

1-month VWAP

3-month VWAP

China Yongsheng 24-Feb-16

34.94 $0.03 52% 68% 62% $0.05 68% Net Debt

Xinren Aluminum 25-Feb-16

469.28 $0.60 67% 64% 63% $0.34 75% Net Debt

Select Group 23-Mar-16

60.51 $0.53 24% 38% 43% $0.13 54% Net Debt

OSIM Int'l 7-Mar-16

823.17 $1.39 27% 41% 42% $0.51 69% Net Cash

Pteris Global 21-Apr-16

237.08 $0.85 34% 38% 44% $0.76 54% Net Cash

CMH Pacific 9-May-16

1,091.06 $1.02 23% 22% 25% $0.95 76% Net Debt Sim Lian Group 8-Aug-16

945.54 $1.08 15% 17% 19% $1.14 80% Net Cash

China Auto Electronics 24-Oct-16

88.61 $0.16 23% 57% 65% $0.29 74% Net Debt

Otto Marine 8-Jun-16

48.84 $0.32 39% 45% 43% $1.18 61% Net Debt

XYEC Hldgs 29-Mar-16

21.20 $0.30 50% 44% 47% $0.23 60% Net Cash

* converted to SGD at prevailing exchanges rates as at quarter Source: ThomsonReuters, DBS Bank

Page 3

Market Focus

Small Mid Cap

Page 4

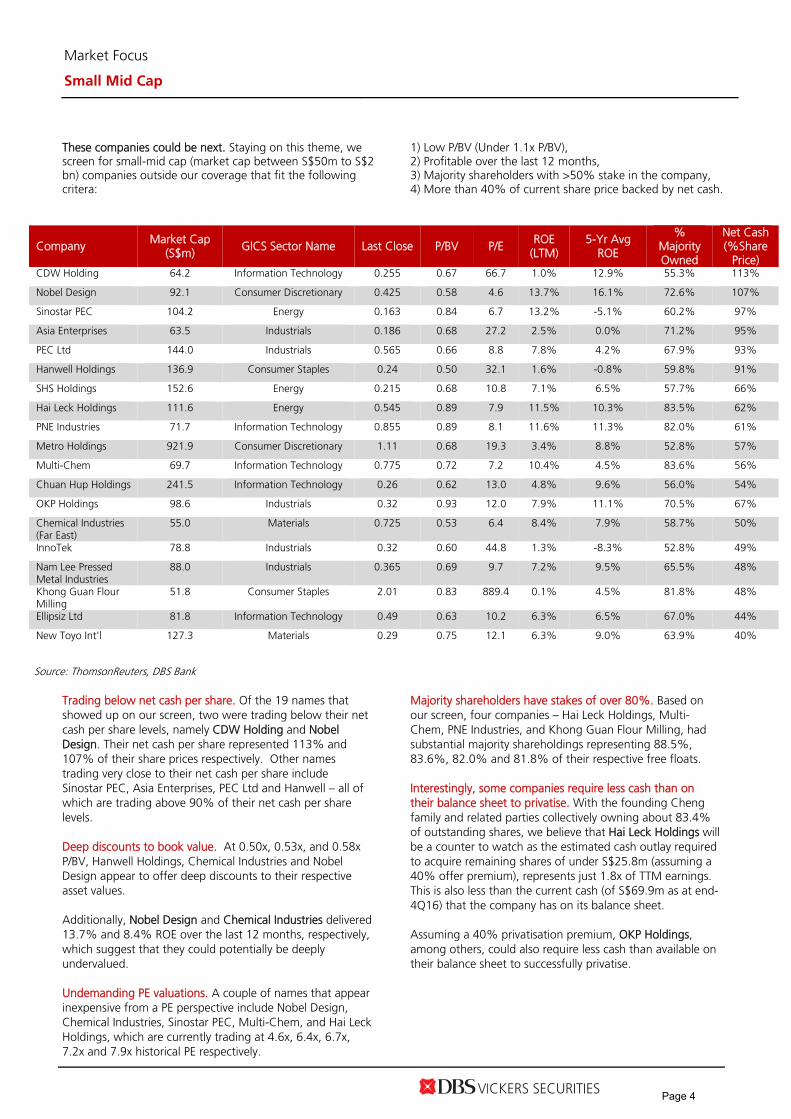

These companies could be next. Staying on this theme, we screen for small-mid cap (market cap between S$50m to S$2 bn) companies outside our coverage that fit the following critera:

1) Low P/BV (Under 1.1x P/BV), 2) Profitable over the last 12 months, 3) Majority shareholders with >50% stake in the company, 4) More than 40% of current share price backed by net cash.

Company Market Cap (S$m)

GICS Sector Name Last Close P/BV P/E ROE (LTM)

5-Yr Avg ROE

% Majority Owned

Net Cash (%Share

Price) CDW Holding 64.2 Information Technology 0.255 0.67 66.7 1.0% 12.9% 55.3% 113%

Nobel Design 92.1 Consumer Discretionary 0.425 0.58 4.6 13.7% 16.1% 72.6% 107%

Sinostar PEC 104.2 Energy 0.163 0.84 6.7 13.2% -5.1% 60.2% 97%

Asia Enterprises 63.5 Industrials 0.186 0.68 27.2 2.5% 0.0% 71.2% 95%

PEC Ltd 144.0 Industrials 0.565 0.66 8.8 7.8% 4.2% 67.9% 93%

Hanwell Holdings 136.9 Consumer Staples 0.24 0.50 32.1 1.6% -0.8% 59.8% 91%

SHS Holdings 152.6 Energy 0.215 0.68 10.8 7.1% 6.5% 57.7% 66%

Hai Leck Holdings 111.6 Energy 0.545 0.89 7.9 11.5% 10.3% 83.5% 62%

PNE Industries 71.7 Information Technology 0.855 0.89 8.1 11.6% 11.3% 82.0% 61%

Metro Holdings 921.9 Consumer Discretionary 1.11 0.68 19.3 3.4% 8.8% 52.8% 57%

Multi-Chem 69.7 Information Technology 0.775 0.72 7.2 10.4% 4.5% 83.6% 56%

Chuan Hup Holdings 241.5 Information Technology 0.26 0.62 13.0 4.8% 9.6% 56.0% 54%

OKP Holdings 98.6 Industrials 0.32 0.93 12.0 7.9% 11.1% 70.5% 67%

Chemical Industries (Far East)

55.0 Materials 0.725 0.53 6.4 8.4% 7.9% 58.7% 50%

InnoTek 78.8 Industrials 0.32 0.60 44.8 1.3% -8.3% 52.8% 49%

Nam Lee Pressed Metal Industries

88.0 Industrials 0.365 0.69 9.7 7.2% 9.5% 65.5% 48%

Khong Guan Flour Milling

51.8 Consumer Staples 2.01 0.83 889.4 0.1% 4.5% 81.8% 48%

Ellipsiz Ltd 81.8 Information Technology 0.49 0.63 10.2 6.3% 6.5% 67.0% 44%

New Toyo Int'l 127.3 Materials 0.29 0.75 12.1 6.3% 9.0% 63.9% 40%

Source: ThomsonReuters, DBS Bank

Trading below net cash per share. Of the 19 names that showed up on our screen, two were trading below their net cash per share levels, namely CDW Holding and Nobel Design. Their net cash per share represented 113% and 107% of their share prices respectively. Other names trading very close to their net cash per share include Sinostar PEC, Asia Enterprises, PEC Ltd and Hanwell – all of which are trading above 90% of their net cash per share levels. Deep discounts to book value. At 0.50x, 0.53x, and 0.58x P/BV, Hanwell Holdings, Chemical Industries and Nobel Design appear to offer deep discounts to their respective asset values. Additionally, Nobel Design and Chemical Industries delivered 13.7% and 8.4% ROE over the last 12 months, respectively, which suggest that they could potentially be deeply undervalued. Undemanding PE valuations. A couple of names that appear inexpensive from a PE perspective include Nobel Design, Chemical Industries, Sinostar PEC, Multi-Chem, and Hai Leck Holdings, which are currently trading at 4.6x, 6.4x, 6.7x, 7.2x and 7.9x historical PE respectively.

Majority shareholders have stakes of over 80%. Based on our screen, four companies – Hai Leck Holdings, Multi-Chem, PNE Industries, and Khong Guan Flour Milling, had substantial majority shareholdings representing 88.5%, 83.6%, 82.0% and 81.8% of their respective free floats. Interestingly, some companies require less cash than on their balance sheet to privatise. With the founding Cheng family and related parties collectively owning about 83.4% of outstanding shares, we believe that Hai Leck Holdings will be a counter to watch as the estimated cash outlay required to acquire remaining shares of under S$25.8m (assuming a 40% offer premium), represents just 1.8x of TTM earnings. This is also less than the current cash (of S$69.9m as at end-4Q16) that the company has on its balance sheet. Assuming a 40% privatisation premium, OKP Holdings, among others, could also require less cash than available on their balance sheet to successfully privatise.

Page 4

Market Focus

Small Mid Cap

Page 5

With our stock screen in mind, we highlight 5 companies that could potentially see privatisation or take-over offers:

Our Top 5 Privatisation Candidates 1

Courts Asia (BUY, TP S$0.51) 1) Compelling valuations of 8x FY18F PE and 0.8x P/BV. 2) 74.3% owned by Singapore Retail Group, the outlay required to acquire remaining shares does not seem excessive in our view (c.S$58m, and approximately 2.3x FY18F net profit level based on current share price).

2 PACC Offshore (BUY, TP S$0.41) 1) Share price has recovered off 2016 lows but at current prices, trades at >50% discount to book value 2) Approximately 81.9% owned by Kuok group 3) POSH is a more stable long-term bet versus peers with no immediate debt concerns, and has also demonstrated ability to secure work for its vessels amid an anaemic market

3

Mermaid Maritime (BUY, TP S$0.24) 1) Mermaid is c.87.3% held by the Thoresen group and its related management. With c. S$270m in cash on hand, the Thoresen group has the necessary ammunition to take Mermaid private. 2) Very low debt levels versus peers, and net gearing of only 0.11x as of 3Q16, which adds to Mermaid’s attractiveness as a privatisation candidate.

4 CSE Global (HOLD, TP S$0.41) 1) Net cash 20% of market cap, 0.9x P/B and 6.5% dividend yield. Reasonable PE of 11x. 2) Free float of over 50% and with no single shareholder holding more than 15%, CSE is a potential take-over target.

5 Sinostar PEC (NON-RATED) 1) Based in Shandong, China, Sinostar produces petrochemical products in two locations. 2) Company is trading below book at 0.8x, and under 7x PE, while trading nearly at net cash per share. 3) Single largest shareholder, the chairmain, owns over 50% of the company.

Source: ThomsonReuters, DBS Bank

Page 5

Market Focus

Small Mid Cap

Appendices

Page 6

Market Focus

Small Mid Cap

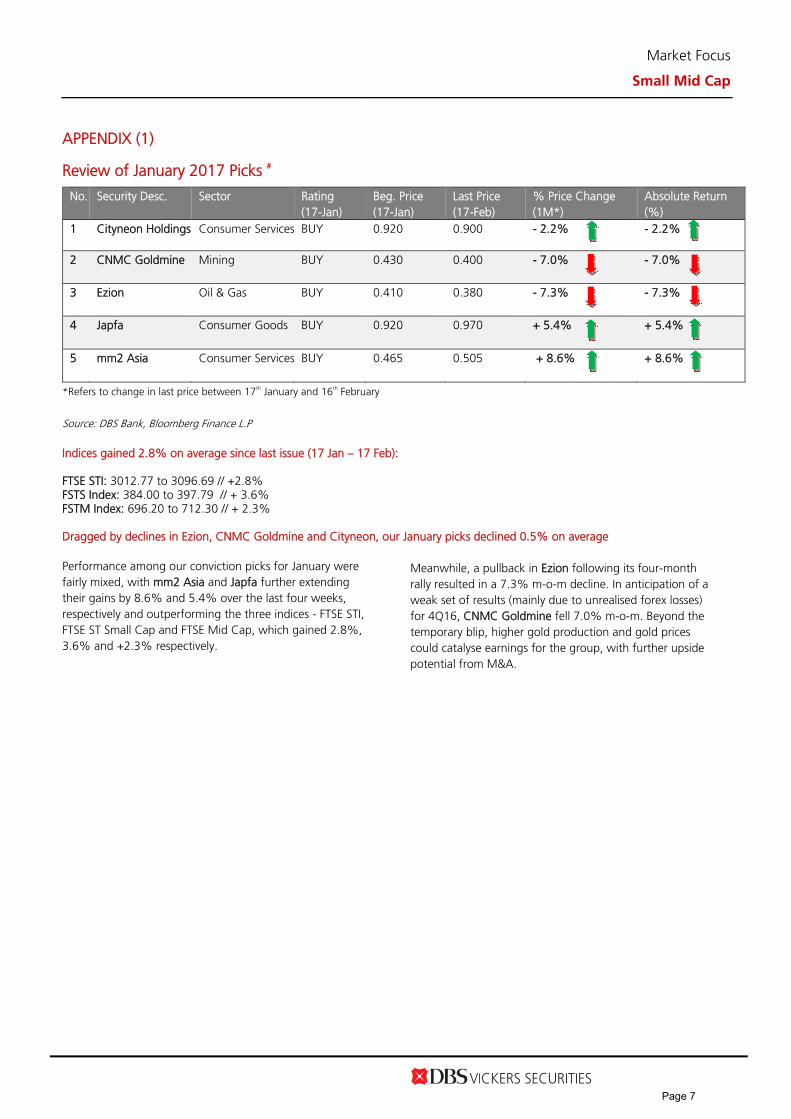

APPENDIX (1) Review of January 2017 Picks #

No. Security Desc. Sector Rating (17-Jan)

Beg. Price (17-Jan)

Last Price (17-Feb)

% Price Change (1M*)

Absolute Return (%)

1 Cityneon Holdings Consumer Services BUY 0.920 0.900 - 2.2% - 2.2%

2 CNMC Goldmine Mining BUY 0.430 0.400 - 7.0% - 7.0%

3 Ezion Oil & Gas BUY 0.410 0.380 - 7.3% - 7.3%

4 Japfa Consumer Goods BUY 0.920 0.970 + 5.4% + 5.4%

5 mm2 Asia Consumer Services BUY 0.465 0.505 + 8.6% + 8.6%

*Refers to change in last price between 17th January and 16th February

Source: DBS Bank, Bloomberg Finance L.P Indices gained 2.8% on average since last issue (17 Jan – 17 Feb): FTSE STI: 3012.77 to 3096.69 // +2.8% FSTS Index: 384.00 to 397.79 // + 3.6% FSTM Index: 696.20 to 712.30 // + 2.3% Dragged by declines in Ezion, CNMC Goldmine and Cityneon, our January picks declined 0.5% on average

Performance among our conviction picks for January were fairly mixed, with mm2 Asia and Japfa further extending their gains by 8.6% and 5.4% over the last four weeks, respectively and outperforming the three indices - FTSE STI, FTSE ST Small Cap and FTSE Mid Cap, which gained 2.8%, 3.6% and +2.3% respectively.

Meanwhile, a pullback in Ezion following its four-month rally resulted in a 7.3% m-o-m decline. In anticipation of a weak set of results (mainly due to unrealised forex losses) for 4Q16, CNMC Goldmine fell 7.0% m-o-m. Beyond the temporary blip, higher gold production and gold prices could catalyse earnings for the group, with further upside potential from M&A.

Page 7

Market Focus

Small Mid Cap

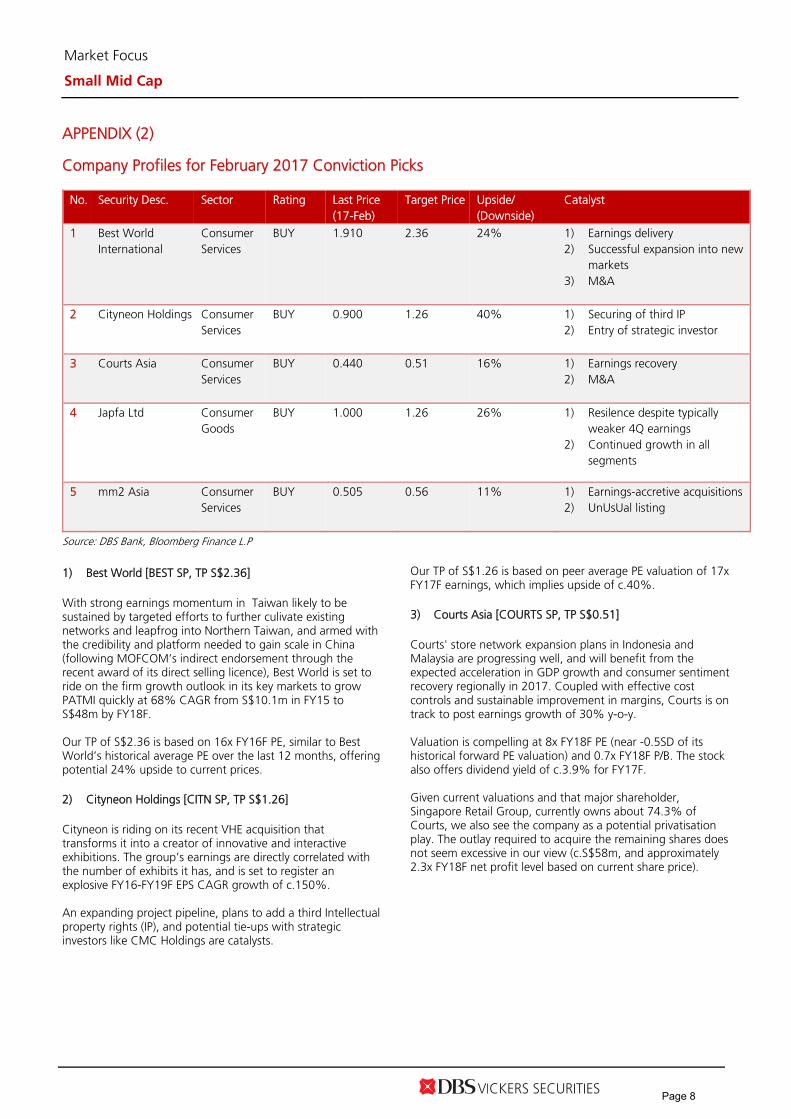

APPENDIX (2) Company Profiles for February 2017 Conviction Picks

No. Security Desc. Sector Rating Last Price (17-Feb)

Target Price Upside/ (Downside)

Catalyst

1 Best World International

Consumer Services

BUY 1.910 2.36 24% 1) Earnings delivery 2) Successful expansion into new

markets 3) M&A

2 Cityneon Holdings Consumer

Services BUY 0.900 1.26 40% 1) Securing of third IP

2) Entry of strategic investor

3 Courts Asia

Consumer Services

BUY 0.440 0.51 16% 1) Earnings recovery 2) M&A

4 Japfa Ltd Consumer

Goods BUY 1.000 1.26 26% 1) Resilence despite typically

weaker 4Q earnings 2) Continued growth in all

segments

5 mm2 Asia Consumer Services

BUY 0.505 0.56 11% 1) Earnings-accretive acquisitions 2) UnUsUal listing

Source: DBS Bank, Bloomberg Finance L.P 1) Best World [BEST SP, TP S$2.36] With strong earnings momentum in Taiwan likely to be sustained by targeted efforts to further culivate existing networks and leapfrog into Northern Taiwan, and armed with the credibility and platform needed to gain scale in China (following MOFCOM’s indirect endorsement through the recent award of its direct selling licence), Best World is set to ride on the firm growth outlook in its key markets to grow PATMI quickly at 68% CAGR from S$10.1m in FY15 to S$48m by FY18F. Our TP of S$2.36 is based on 16x FY16F PE, similar to Best World’s historical average PE over the last 12 months, offering potential 24% upside to current prices. 2) Cityneon Holdings [CITN SP, TP S$1.26]

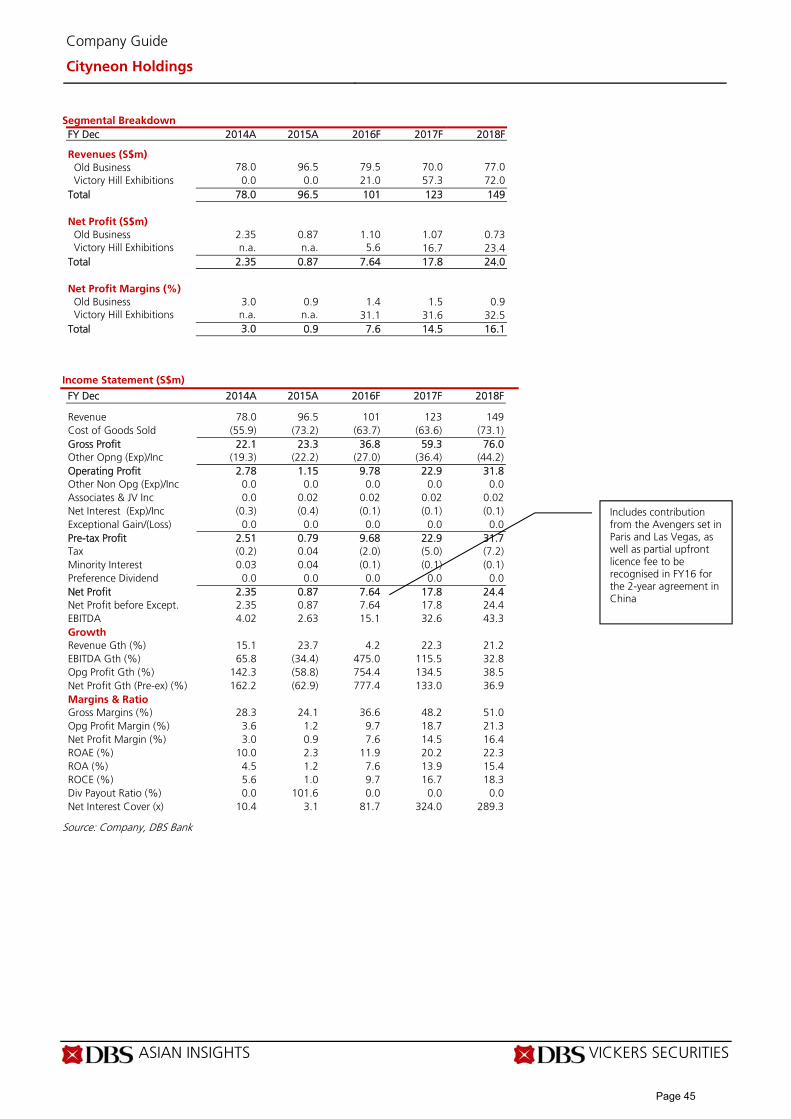

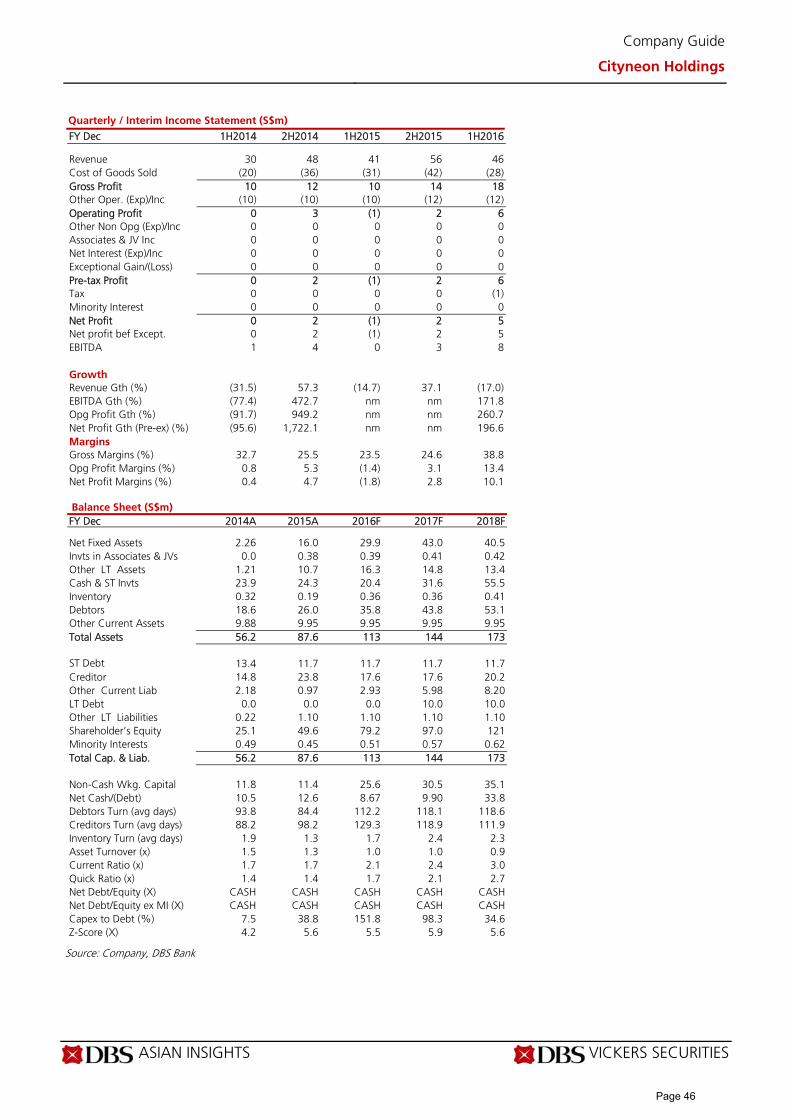

Cityneon is riding on its recent VHE acquisition that transforms it into a creator of innovative and interactive exhibitions. The group’s earnings are directly correlated with the number of exhibits it has, and is set to register an explosive FY16-FY19F EPS CAGR growth of c.150%. An expanding project pipeline, plans to add a third Intellectual property rights (IP), and potential tie-ups with strategic investors like CMC Holdings are catalysts.

Our TP of S$1.26 is based on peer average PE valuation of 17x FY17F earnings, which implies upside of c.40%. 3) Courts Asia [COURTS SP, TP S$0.51]

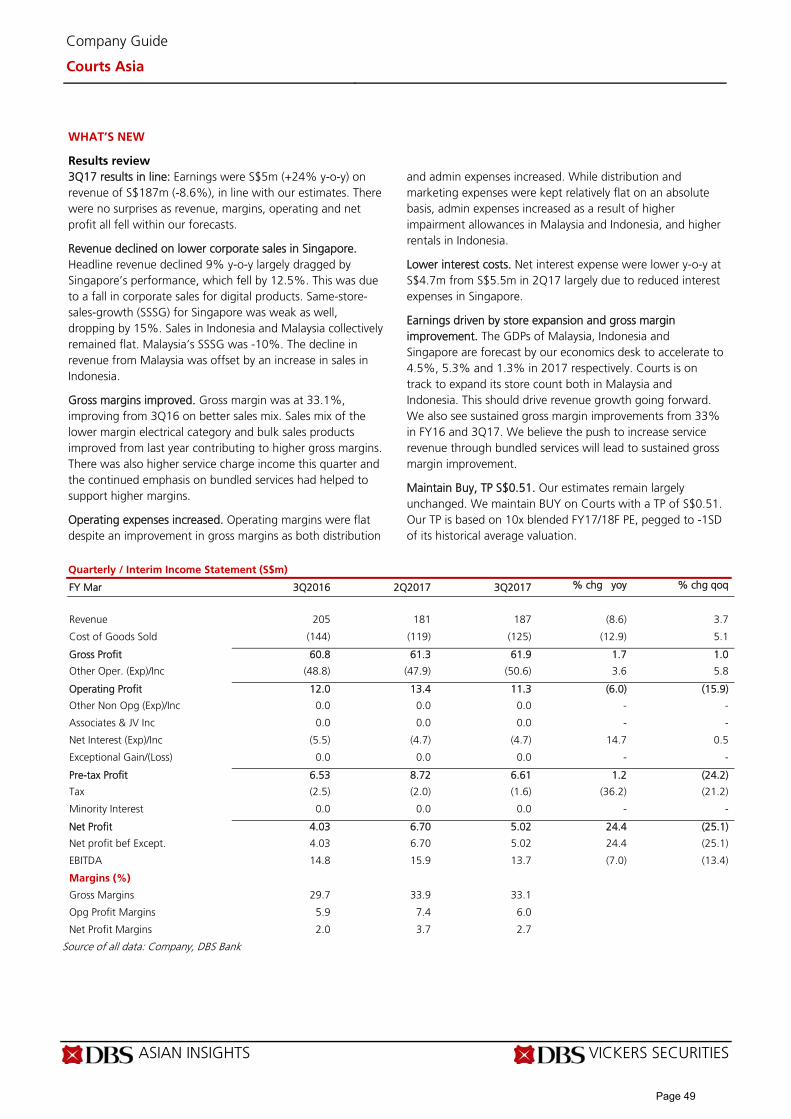

Courts' store network expansion plans in Indonesia and Malaysia are progressing well, and will benefit from the expected acceleration in GDP growth and consumer sentiment recovery regionally in 2017. Coupled with effective cost controls and sustainable improvement in margins, Courts is on track to post earnings growth of 30% y-o-y. Valuation is compelling at 8x FY18F PE (near -0.5SD of its historical forward PE valuation) and 0.7x FY18F P/B. The stock also offers dividend yield of c.3.9% for FY17F. Given current valuations and that major shareholder, Singapore Retail Group, currently owns about 74.3% of Courts, we also see the company as a potential privatisation play. The outlay required to acquire the remaining shares does not seem excessive in our view (c.S$58m, and approximately 2.3x FY18F net profit level based on current share price).

Page 8

Market Focus

Small Mid Cap

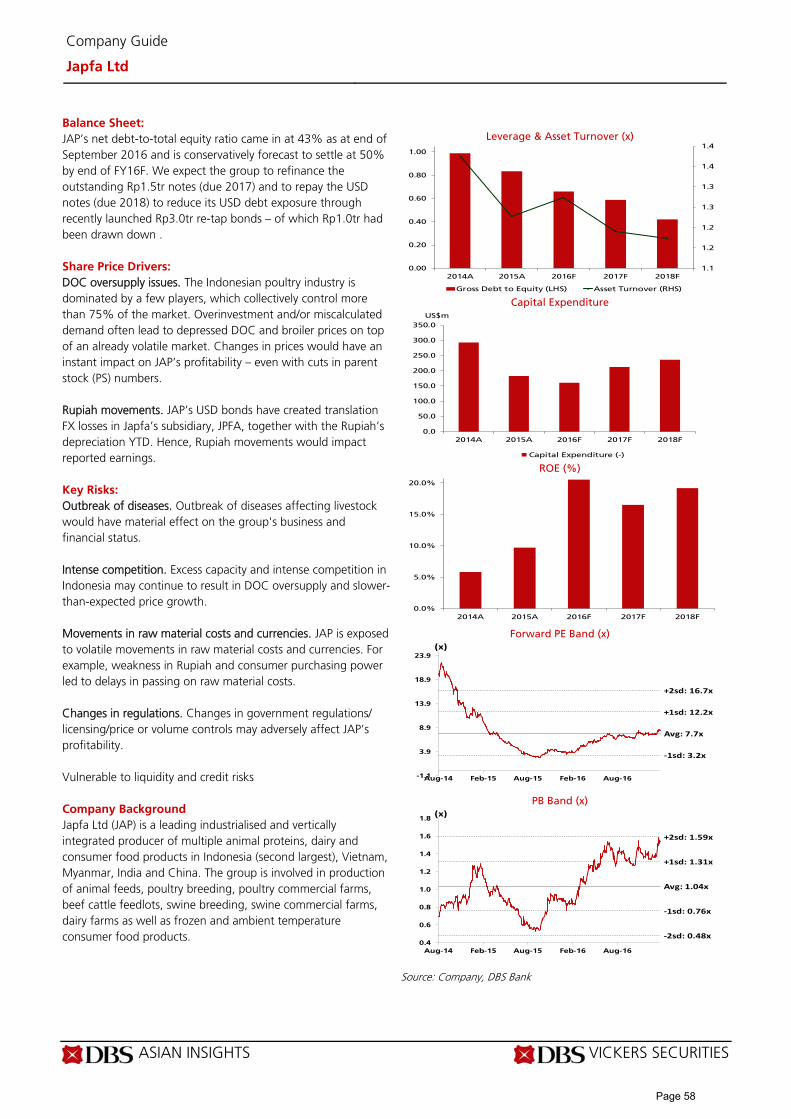

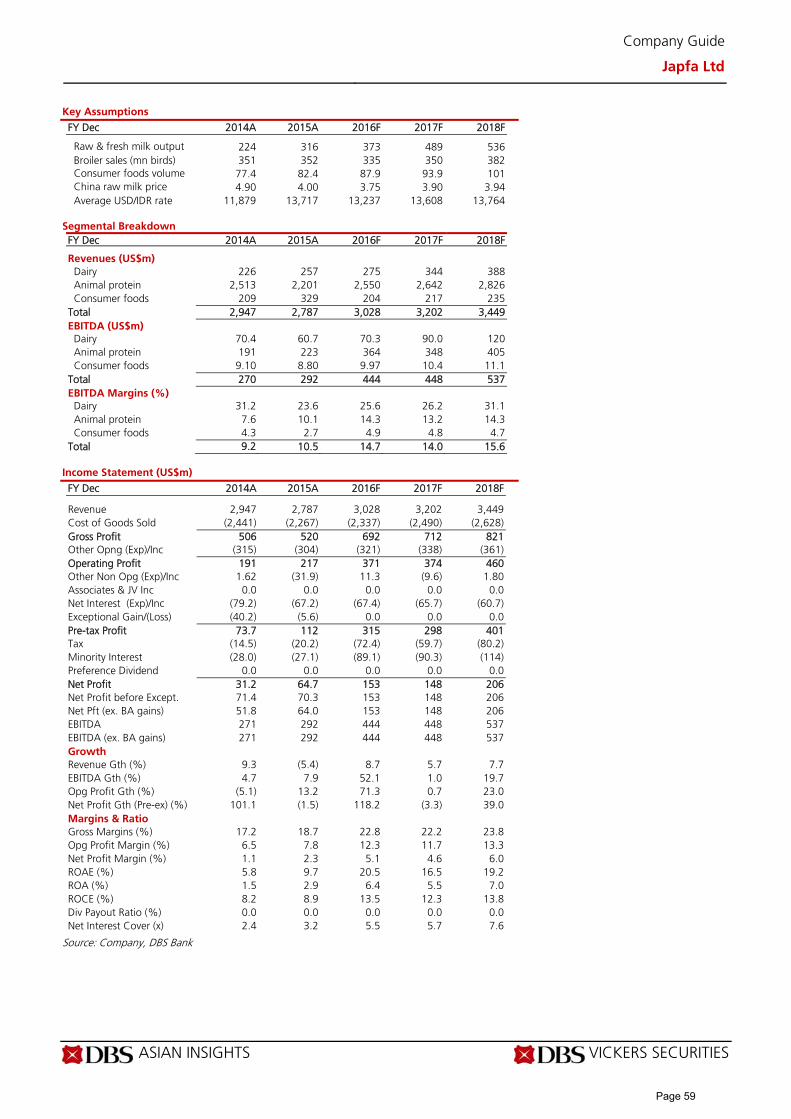

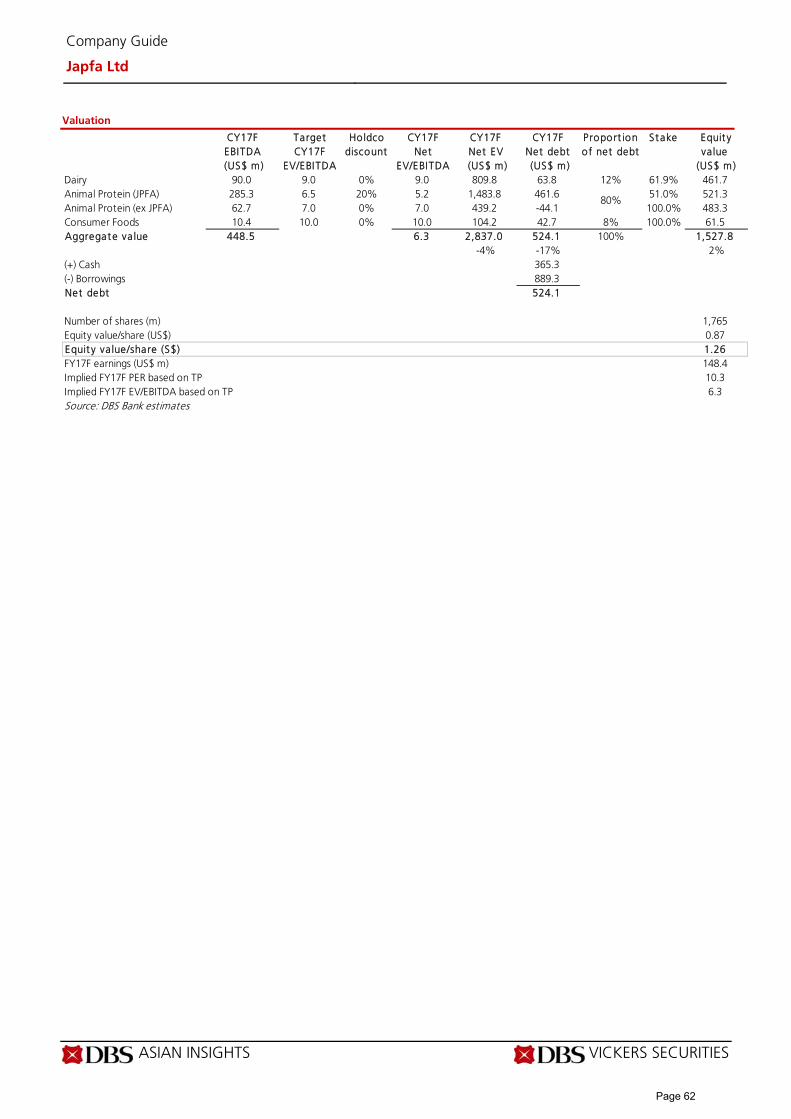

4) Japfa Ltd [JAP SP, TP S$1.26]

Japfa’s EBITDA is projected to expanded by 16% to c.US$465m, driven by lower borrowing costs and continued growth in all segments: 1) Expect resilient demand in Indonesian live broiler and DOCs over the next 12 months, 2) new product launches for the consumer food products segment, and 3) better productivity/raw milk in the dairy segment. At current prices, we believe that the stock is undervalued relative to its presence in Asia’s largest population, relative to peers, and for its secular growth prospects. Our SOP-based TP (pegged to forward EV/EBITDA) of S$1.26 implies upside of nearly 26%.

5) mm2 Asia [mm2 SP, TP S$0.56]

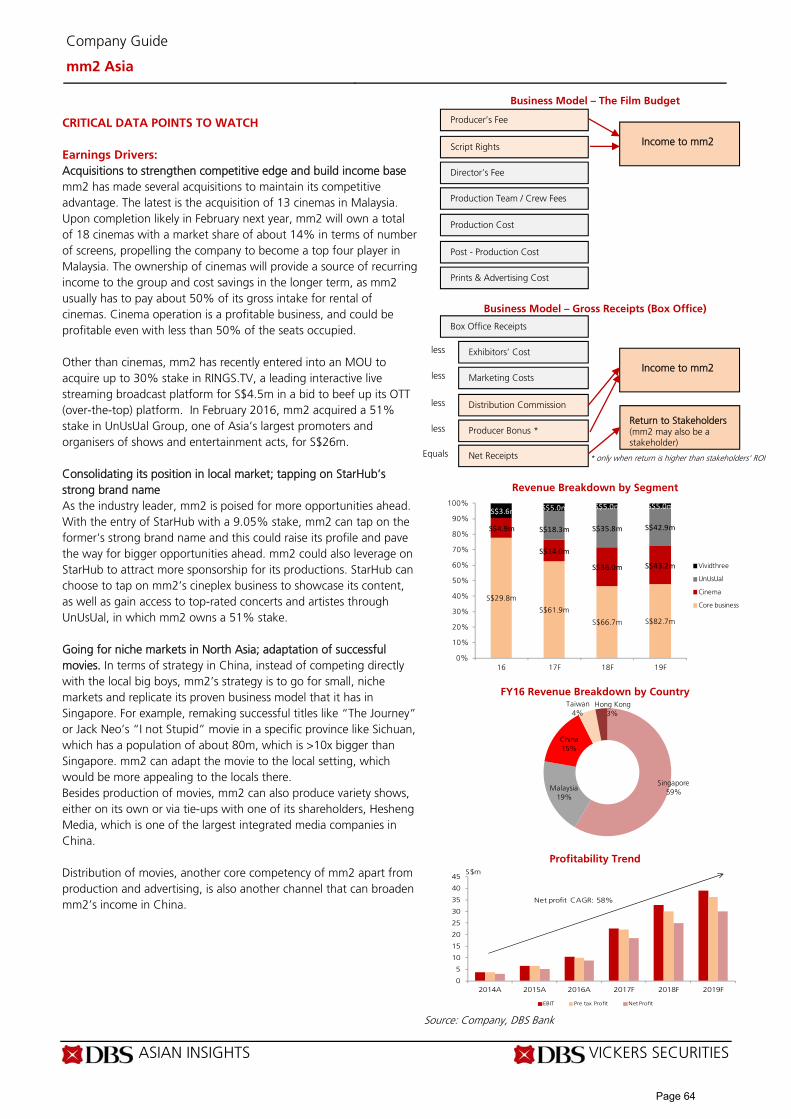

Underpinned by growth in productions, expansion into the China market and contributions from cinema operations and entertainment company, UnUsUal Group, mm2 Asia is projected to deliver an EPS CAGR of 50% from FY16-FY19F. Upside to earnings could come from earnings-accretive acquisitions and from more projects (especially in China where budgets are much higher). Separately, the successful listing of UnUsUal, which mm2 acquired at 10.2x PE back in February 2016, would enable mm2 to crystallise gains and unlock value. Our TP of S$0.56 is pegged to FYEMar18F earnings and peers’ average of 24x, which offers 11% upside to current prices.

Page 9

Market Focus

Small Mid Cap

APPENDIX (3) Historical Performance of Previous Conviction Picks

Conviction Picks - Jan 2016 No. Sec. Desc. Rcmd Absolute

Performance

Date Removed

Comments

1 China Merchants Holdings (Pacific) BUY -3.0% 2 Japfa Ltd BUY -3.1% 3 mm2 Asia BUY -12.2% 4 Riverstone Holdings BUY -11.7% 5 Sheng Siong Group BUY 0.6% 4-Feb-16 Replaced with new conviction idea

Simple Average: -5.9% vs STI: -6.3%

Conviction Picks - Feb 2016 No. Sec. Desc. Rcmd Absolute

Performance

Date Removed

Comments

1 China Merchants Holdings (Pacific) BUY 3.8% 2 Japfa Ltd BUY 10.5% 3 mm2 Asia BUY 42.9% 8-Mar-16 Re-rated near TP 4 OSIM International BUY 23.7% 8-Mar-16 Re-rated near TP and downgraded to

HOLD on 8-Mar-16 5 Riverstone Holdings BUY -10.8%

Simple Average: 14.0% vs STI: +9.5%

Conviction Picks - Mar 2016# No. Sec. Desc. Rcmd Absolute

Performance

Date Removed

Comments

1 China Merchants Holdings (Pacific) BUY -1.2% 2 Japfa Ltd BUY 11.4% 3 Innovalues Ltd BUY 19.3% 4 Riverstone Holdings BUY 2.6%

Simple Average: 3.6% vs STI: -0.4%

#Shown are 4 out of our 5 top picks. For full list, please refer to March issue: Sifting Out M&A Plays

Conviction Picks - Apr 2016 No. Sec. Desc. Rcmd Absolute

Performance

Date Removed

Comments

1 China Merchants Holdings (Pacific) BUY 0.6% 2 Courts Asia BUY -1.5% 5-May-16 Replaced with new conviction idea 3 Innovalues Ltd BUY 4.1% 5-May-16 Downgraded to HOLD on 4-May-16 4 Japfa Ltd BUY 20.5% 5 mm2 Asia BUY 8.9% 6 Riverstone Holdings BUY 0.5% 5-May-16 Replaced with new conviction idea

Simple Average: 5.5% vs STI: -0.0%

Source: DBS Bank

Page 10

Market Focus

Small Mid Cap

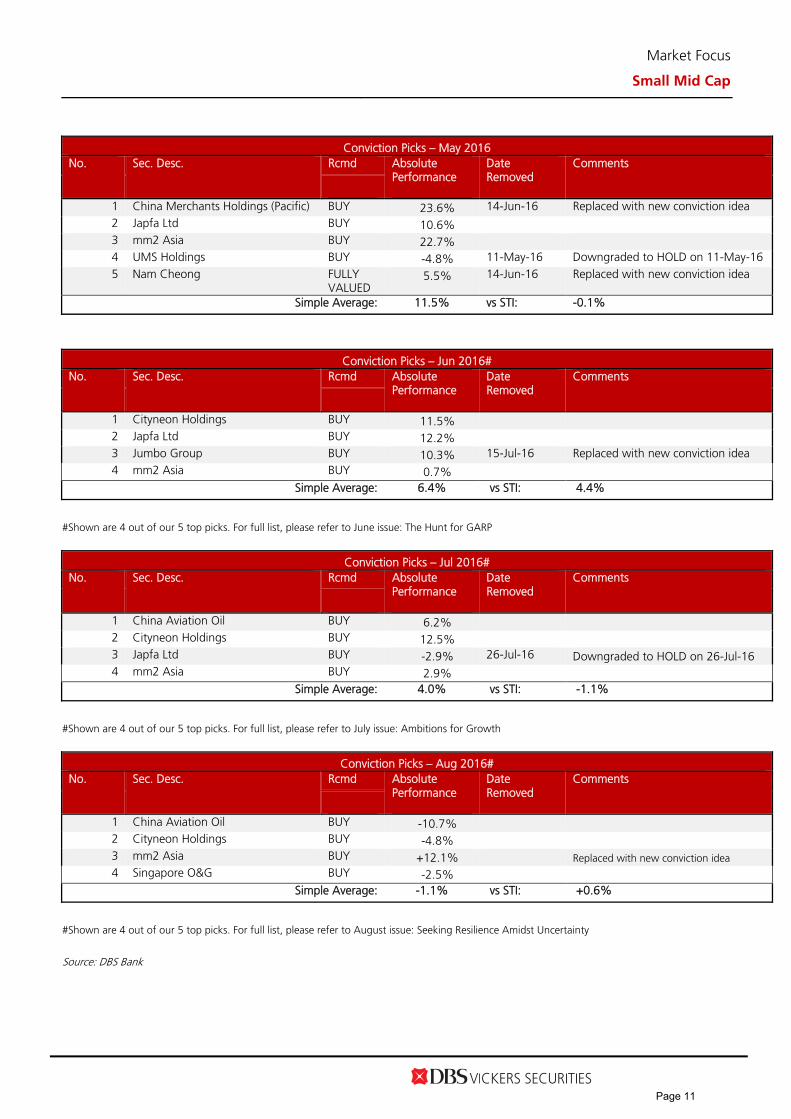

Conviction Picks – May 2016

No. Sec. Desc. Rcmd Absolute Performance

Date Removed

Comments

1 China Merchants Holdings (Pacific) BUY 23.6% 14-Jun-16 Replaced with new conviction idea 2 Japfa Ltd BUY 10.6% 3 mm2 Asia BUY 22.7% 4 UMS Holdings BUY -4.8% 11-May-16 Downgraded to HOLD on 11-May-16 5 Nam Cheong FULLY

VALUED 5.5% 14-Jun-16 Replaced with new conviction idea

Simple Average: 11.5% vs STI: -0.1%

Conviction Picks – Jun 2016#

No. Sec. Desc. Rcmd Absolute Performance

Date Removed

Comments

1 Cityneon Holdings BUY 11.5% 2 Japfa Ltd BUY 12.2% 3 Jumbo Group BUY 10.3% 15-Jul-16 Replaced with new conviction idea 4 mm2 Asia BUY 0.7%

Simple Average: 6.4% vs STI: 4.4%

#Shown are 4 out of our 5 top picks. For full list, please refer to June issue: The Hunt for GARP

Conviction Picks – Jul 2016#

No. Sec. Desc. Rcmd Absolute Performance

Date Removed

Comments

1 China Aviation Oil BUY 6.2% 2 Cityneon Holdings BUY 12.5% 3 Japfa Ltd BUY -2.9% 26-Jul-16 Downgraded to HOLD on 26-Jul-16 4 mm2 Asia BUY 2.9%

Simple Average: 4.0% vs STI: -1.1%

#Shown are 4 out of our 5 top picks. For full list, please refer to July issue: Ambitions for Growth

Conviction Picks – Aug 2016#

No. Sec. Desc. Rcmd Absolute Performance

Date Removed

Comments

1 China Aviation Oil BUY -10.7% 2 Cityneon Holdings BUY -4.8% 3 mm2 Asia BUY +12.1% Replaced with new conviction idea 4 Singapore O&G BUY -2.5%

Simple Average: -1.1% vs STI: +0.6%

#Shown are 4 out of our 5 top picks. For full list, please refer to August issue: Seeking Resilience Amidst Uncertainty

Source: DBS Bank

Page 11

Market Focus

Small Mid Cap

Conviction Picks – Sep 2016# No. Sec. Desc. Rcmd Absolute

Performance

Date Removed

Comments

1 China Aviation Oil BUY +0.0% 2 Cityneon Holdings BUY - 3.0% 3 Katrina Group BUY +0.0% 4 Singapore O&G BUY +2.2%

Simple Average: -0.5% vs STI: -0.4%

#Shown are 4 out of our 5 top picks. For full list, please refer to September issue: Safety First as Dark Clouds Gather

Conviction Picks – Oct 2016#

No. Sec. Desc. Rcmd Absolute Performance

Date Removed

Comments

1 China Aviation Oil BUY -3.3% 2 Cityneon Holdings BUY +15.7% 3 Katrina Group BUY -25.4% 4 Singapore O&G BUY -1.3%

Simple Average: -4.9% vs STI: -2.4%

#Shown are 4 out of our 5 top picks. For full list, please refer to October issue: Eye$ on the money

Conviction Picks – Nov 2016

No. Sec. Desc. Rcmd Absolute Performance

Date Removed

Comments

1 China Aviation Oil BUY +4.9% 2 Cityneon Holdings BUY -5.0% 3 CNMC Goldmine BUY -9.5% 4 Katrina Group BUY -6.4% 5 Singapore O&G BUY -0.0%

Simple Average: -3.2% vs STI: +5.2%

Conviction Picks – Dec 2016 No. Sec. Desc. Rcmd Absolute

Performance

Date Removed

Comments

1 China Aviation Oil BUY +10.4% 18-Jan-17 Replaced with new conviction idea 2 Cityneon Holdings BUY -11.0% TP lowered from S$1.37 to S$1.26 on 29

Dec 2016 3 CNMC Goldmine BUY - 4 mm2 Asia BUY +13.4% 5 Singapore O&G BUY +3.0% 18-Jan-17 Replaced with new conviction idea

Simple Average: +3.2% vs STI: +1.8%

Source: DBS Bank

Page 12

Market Focus

Small Mid Cap

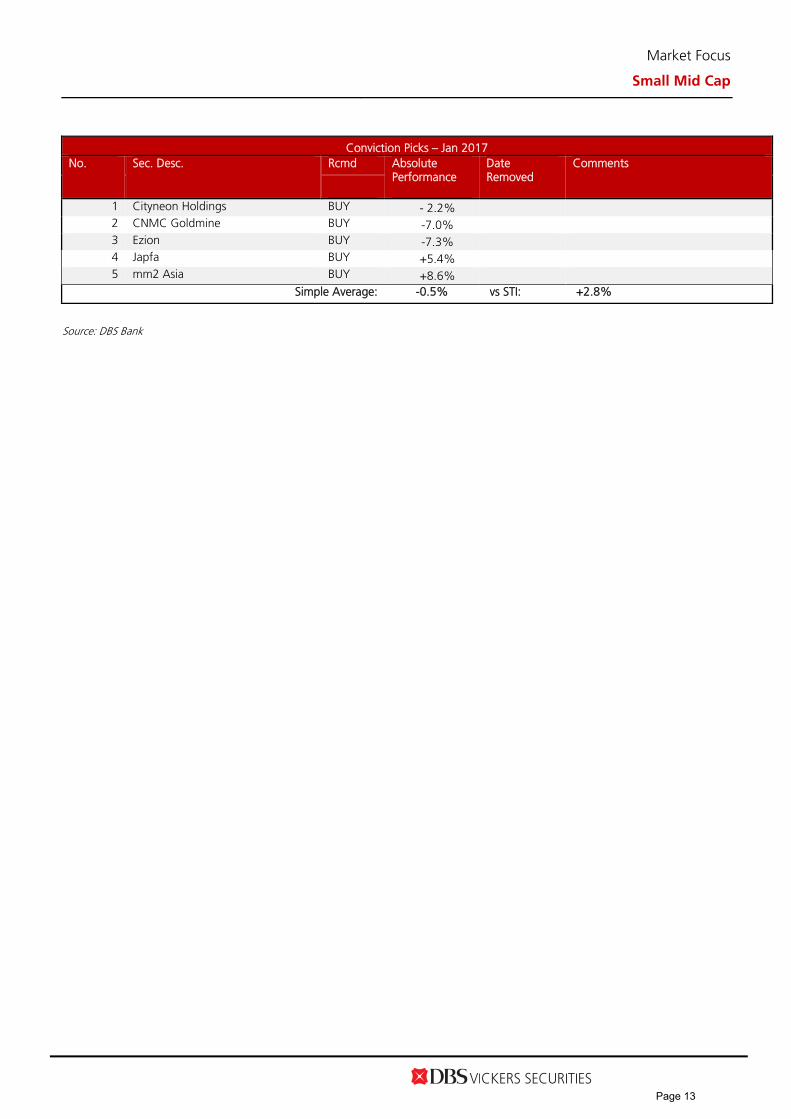

Conviction Picks – Jan 2017

No. Sec. Desc. Rcmd Absolute Performance

Date Removed

Comments

1 Cityneon Holdings BUY - 2.2% 2 CNMC Goldmine BUY -7.0% 3 Ezion BUY -7.3% 4 Japfa BUY +5.4% 5 mm2 Asia BUY +8.6%

Simple Average: -0.5% vs STI: +2.8%

Source: DBS Bank

Page 13

Market Focus

Small Mid Cap

APPENDIX (4) FSTS & FSTM Indices in January 2017

Top 5 Performing Sectors - FSTM Top 5 Performing Sectors - FSTS

ICB Sector No. of

Constituents

Net Market

Cap % Chg

ICB Sector No. of

Constituents

Net Market

Cap % Chg

(S$ m) (1m) (S$ m) (1m)

Construction & Materials 1 1,306 10.6

Personal Goods 1 253 36.6

Software & Compurer Services

1 464 9.4

Chemicals 1 262 14.8

Oil Equipment, Services & Distribution

1 1,239 8.0

Mining 1 155 13.3

Real Estate Investment Trusts

3 4,607 6.5

Industrial Metals & Mining

1 294 7.0

Industrial Transportation

3 6,216 5.0

Travel & Leisure

1 530 6.4

Bottom 5 Performing Sectors – FSTM Bottom 5 Performing Sectors - FSTS

ICB Sector No. of

Constituents

Net Market

Cap % Chg

ICB Sector No. of

Constituents

Net Market

Cap % Chg

(S$ m) (1m) (S$ m) (1m)

Industrial Engineering

1 1,668 (1.2) Media 1 79 (9.4)

Food Producers

3 3,898 (0.7) Software & Computer Services

1 24 (7.5)

Gas,Water & Multiutilities

3 1,715 0.3 Food & Drug Retailers

1 294 (2.0)

General Industrials

1 1,520 0.6 Technology Hardware & Equipment

1 185 (1.9)

Travel & Leisure

3 1,757 0.8 Travel & Leisure

1 676 (1.6)

Source: DBS Bank, FTSE

Page 14

Market Focus

Small Mid Cap

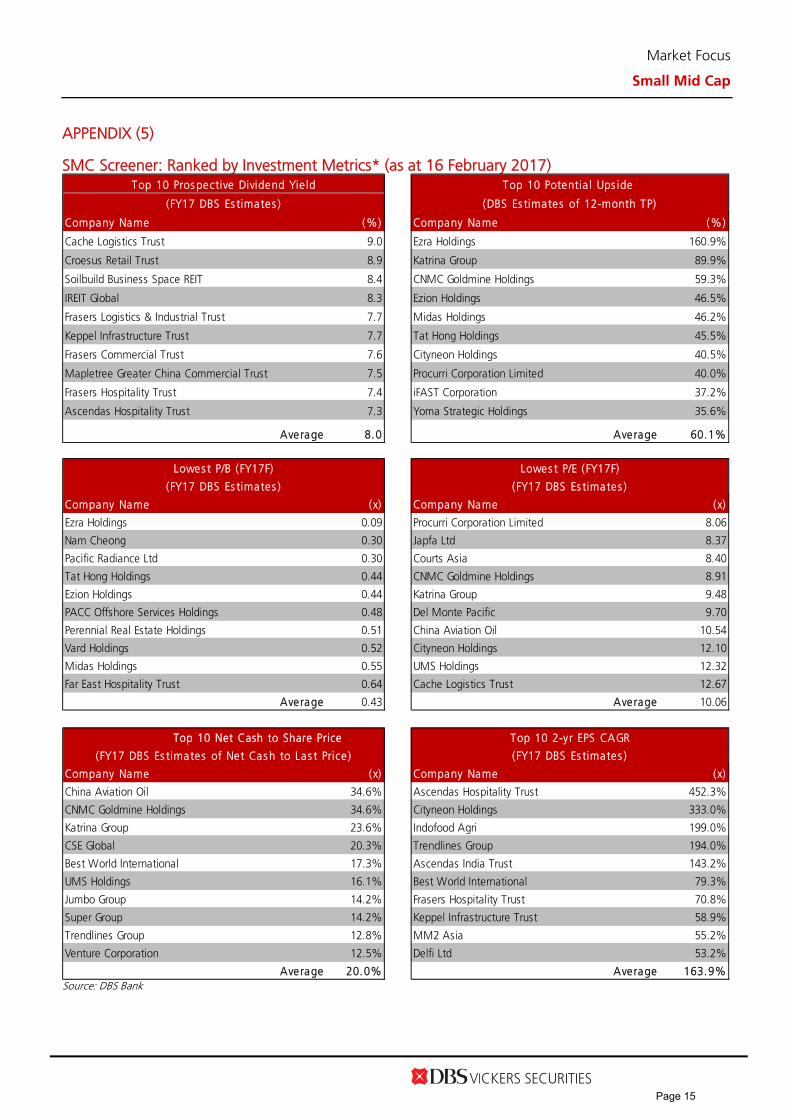

APPENDIX (5)

SMC Screener: Ranked by Investment Metrics* (as at 16 February 2017)

Company Name (%) Company Name (%)

Cache Logistics Trust 9.0 Ezra Holdings 160.9%

Croesus Retail Trust 8.9 Katrina Group 89.9%

Soilbuild Business Space REIT 8.4 CNMC Goldmine Holdings 59.3%

IREIT Global 8.3 Ezion Holdings 46.5%

Frasers Logistics & Industrial Trust 7.7 Midas Holdings 46.2%

Keppel Infrastructure Trust 7.7 Tat Hong Holdings 45.5%

Frasers Commercial Trust 7.6 Cityneon Holdings 40.5%

Mapletree Greater China Commercial Trust 7.5 Procurri Corporation Limited 40.0%

Frasers Hospitality Trust 7.4 iFAST Corporation 37.2%

Ascendas Hospitality Trust 7.3 Yoma Strategic Holdings 35.6%

Average 8.0 Average 60.1%

Company Name (x) Company Name (x)

Ezra Holdings 0.09 Procurri Corporation Limited 8.06

Nam Cheong 0.30 Japfa Ltd 8.37

Pacific Radiance Ltd 0.30 Courts Asia 8.40

Tat Hong Holdings 0.44 CNMC Goldmine Holdings 8.91

Ezion Holdings 0.44 Katrina Group 9.48

PACC Offshore Services Holdings 0.48 Del Monte Pacific 9.70

Perennial Real Estate Holdings 0.51 China Aviation Oil 10.54

Vard Holdings 0.52 Cityneon Holdings 12.10

Midas Holdings 0.55 UMS Holdings 12.32

Far East Hospitality Trust 0.64 Cache Logistics Trust 12.67

Average 0.43 Average 10.06

Company Name (x) Company Name (x)

China Aviation Oil 34.6% Ascendas Hospitality Trust 452.3%

CNMC Goldmine Holdings 34.6% Cityneon Holdings 333.0%

Katrina Group 23.6% Indofood Agri 199.0%

CSE Global 20.3% Trendlines Group 194.0%

Best World International 17.3% Ascendas India Trust 143.2%

UMS Holdings 16.1% Best World International 79.3%

Jumbo Group 14.2% Frasers Hospitality Trust 70.8%

Super Group 14.2% Keppel Infrastructure Trust 58.9%

Trendlines Group 12.8% MM2 Asia 55.2%

Venture Corporation 12.5% Delfi Ltd 53.2%

Average 20.0% Average 163.9%

(FY17 DBS Es timates )

Top 10 Net Cash to Share Price Top 10 2-yr EPS CAGR

(FY17 DBS Es timates ) (DBS Es timates of 12-month TP)

(FY17 DBS Es timates ) (FY17 DBS Es timates )

(FY17 DBS Es timates of Net Cas h to Las t Price )

Top 10 Pros pective Dividend Yie ld Top 10 Potentia l Ups ide

Lowes t P/B (FY17F) Lowes t P/E (FY17F)

Source: DBS Bank

Page 15

Market Focus

Small Mid Cap

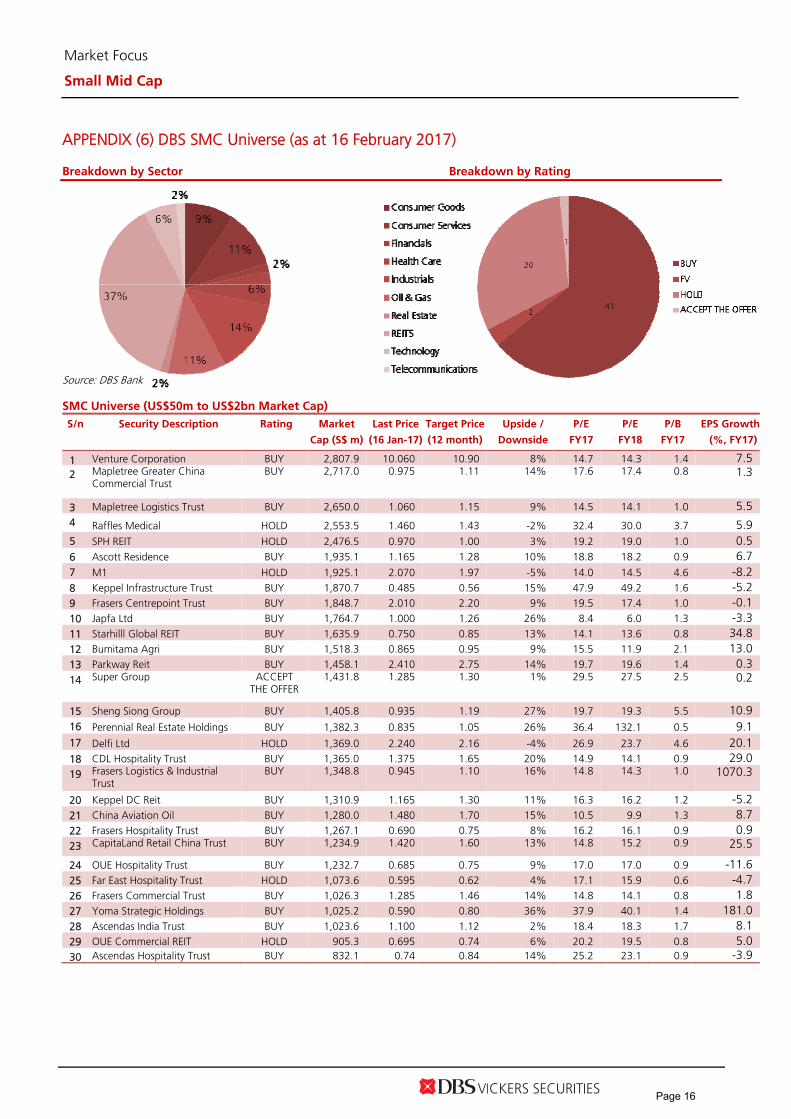

APPENDIX (6) DBS SMC Universe (as at 16 February 2017) Breakdown by Sector Breakdown by Rating

Source: DBS Bank

SMC Universe (US$50m to US$2bn Market Cap)

S/n Security Description Rating Market

Cap (S$ m)

Last Price

(16 Jan-17)

Target Price

(12 month)

Upside /

Downside

P/E

FY17

P/E

FY18

P/B

FY17

EPS Growth

(%, FY17)

1 Venture Corporation BUY 2,807.9 10.060 10.90 8% 14.7 14.3 1.4 7.5 2 Mapletree Greater China

Commercial Trust BUY 2,717.0 0.975 1.11 14% 17.6 17.4 0.8 1.3

3 Mapletree Logistics Trust BUY 2,650.0 1.060 1.15 9% 14.5 14.1 1.0 5.5 4 Raffles Medical HOLD 2,553.5 1.460 1.43 -2% 32.4 30.0 3.7 5.9 5 SPH REIT HOLD 2,476.5 0.970 1.00 3% 19.2 19.0 1.0 0.5 6 Ascott Residence BUY 1,935.1 1.165 1.28 10% 18.8 18.2 0.9 6.7 7 M1 HOLD 1,925.1 2.070 1.97 -5% 14.0 14.5 4.6 -8.2 8 Keppel Infrastructure Trust BUY 1,870.7 0.485 0.56 15% 47.9 49.2 1.6 -5.2 9 Frasers Centrepoint Trust BUY 1,848.7 2.010 2.20 9% 19.5 17.4 1.0 -0.1 10 Japfa Ltd BUY 1,764.7 1.000 1.26 26% 8.4 6.0 1.3 -3.3 11 Starhilll Global REIT BUY 1,635.9 0.750 0.85 13% 14.1 13.6 0.8 34.8 12 Bumitama Agri BUY 1,518.3 0.865 0.95 9% 15.5 11.9 2.1 13.0 13 Parkway Reit BUY 1,458.1 2.410 2.75 14% 19.7 19.6 1.4 0.3 14 Super Group ACCEPT

THE OFFER 1,431.8 1.285 1.30 1% 29.5 27.5 2.5 0.2

15 Sheng Siong Group BUY 1,405.8 0.935 1.19 27% 19.7 19.3 5.5 10.9 16 Perennial Real Estate Holdings BUY 1,382.3 0.835 1.05 26% 36.4 132.1 0.5 9.1 17 Delfi Ltd HOLD 1,369.0 2.240 2.16 -4% 26.9 23.7 4.6 20.1 18 CDL Hospitality Trust BUY 1,365.0 1.375 1.65 20% 14.9 14.1 0.9 29.0 19 Frasers Logistics & Industrial

Trust BUY 1,348.8 0.945 1.10 16% 14.8 14.3 1.0 1070.3

20 Keppel DC Reit BUY 1,310.9 1.165 1.30 11% 16.3 16.2 1.2 -5.2 21 China Aviation Oil BUY 1,280.0 1.480 1.70 15% 10.5 9.9 1.3 8.7 22 Frasers Hospitality Trust BUY 1,267.1 0.690 0.75 8% 16.2 16.1 0.9 0.9 23 CapitaLand Retail China Trust BUY 1,234.9 1.420 1.60 13% 14.8 15.2 0.9 25.5

24 OUE Hospitality Trust BUY 1,232.7 0.685 0.75 9% 17.0 17.0 0.9 -11.6 25 Far East Hospitality Trust HOLD 1,073.6 0.595 0.62 4% 17.1 15.9 0.6 -4.7 26 Frasers Commercial Trust BUY 1,026.3 1.285 1.46 14% 14.8 14.1 0.8 1.8 27 Yoma Strategic Holdings BUY 1,025.2 0.590 0.80 36% 37.9 40.1 1.4 181.0 28 Ascendas India Trust BUY 1,023.6 1.100 1.12 2% 18.4 18.3 1.7 8.1 29 OUE Commercial REIT HOLD 905.3 0.695 0.74 6% 20.2 19.5 0.8 5.0 30 Ascendas Hospitality Trust BUY 832.1 0.74 0.84 14% 25.2 23.1 0.9 -3.9

Page 16

Market Focus

Small Mid Cap

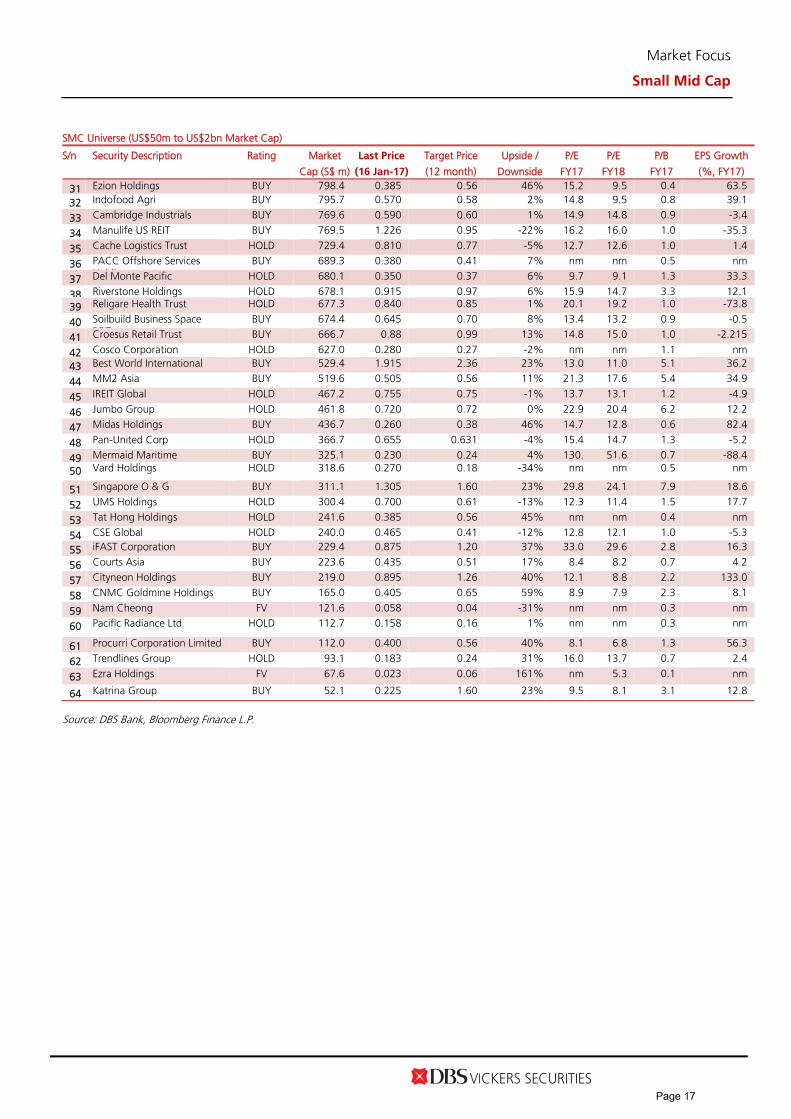

SMC Universe (US$50m to US$2bn Market Cap)

S/n Security Description Rating Market

Cap (S$ m)

Last Price

(16 Jan-17)

Target Price

(12 month)

Upside /

Downside

P/E

FY17

P/E

FY18

P/B

FY17

EPS Growth

(%, FY17)

31 Ezion Holdings BUY 798.4 0.385 0.56 46% 15.2 9.5 0.4 63.5

32 Indofood Agri BUY 795.7 0.570 0.58 2% 14.8 9.5 0.8 39.1

33 Cambridge Industrials BUY 769.6 0.590 0.60 1% 14.9 14.8 0.9 -3.4

34 Manulife US REIT BUY 769.5 1.226 0.95 -22% 16.2 16.0 1.0 -35.3

35 Cache Logistics Trust HOLD 729.4 0.810 0.77 -5% 12.7 12.6 1.0 1.4

36 PACC Offshore Services H ldi

BUY 689.3 0.380 0.41 7% nm nm 0.5 nm

37 Del Monte Pacific HOLD 680.1 0.350 0.37 6% 9.7 9.1 1.3 33.3

38 Riverstone Holdings HOLD 678.1 0.915 0.97 6% 15.9 14.7 3.3 12.1

39 Religare Health Trust HOLD 677.3 0.840 0.85 1% 20.1 19.2 1.0 -73.8

40 Soilbuild Business Space REIT

BUY 674.4 0.645 0.70 8% 13.4 13.2 0.9 -0.5

41 Croesus Retail Trust BUY 666.7 0.88 0.99 13% 14.8 15.0 1.0 -2.215

42 Cosco Corporation HOLD 627.0 0.280 0.27 -2% nm nm 1.1 nm

43 Best World International BUY 529.4 1.915 2.36 23% 13.0 11.0 5.1 36.2

44 MM2 Asia BUY 519.6 0.505 0.56 11% 21.3 17.6 5.4 34.9

45 IREIT Global HOLD 467.2 0.755 0.75 -1% 13.7 13.1 1.2 -4.9

46 Jumbo Group HOLD 461.8 0.720 0.72 0% 22.9 20.4 6.2 12.2

47 Midas Holdings BUY 436.7 0.260 0.38 46% 14.7 12.8 0.6 82.4

48 Pan-United Corp HOLD 366.7 0.655 0.631 -4% 15.4 14.7 1.3 -5.2

49 Mermaid Maritime BUY 325.1 0.230 0.24 4% 130. 51.6 0.7 -88.4

50 Vard Holdings HOLD 318.6 0.270 0.18 -34% nm nm 0.5 nm

51 Singapore O & G BUY 311.1 1.305 1.60 23% 29.8 24.1 7.9 18.6

52 UMS Holdings HOLD 300.4 0.700 0.61 -13% 12.3 11.4 1.5 17.7

53 Tat Hong Holdings HOLD 241.6 0.385 0.56 45% nm nm 0.4 nm

54 CSE Global HOLD 240.0 0.465 0.41 -12% 12.8 12.1 1.0 -5.3

55 iFAST Corporation BUY 229.4 0.875 1.20 37% 33.0 29.6 2.8 16.3

56 Courts Asia BUY 223.6 0.435 0.51 17% 8.4 8.2 0.7 4.2

57 Cityneon Holdings BUY 219.0 0.895 1.26 40% 12.1 8.8 2.2 133.0

58 CNMC Goldmine Holdings BUY 165.0 0.405 0.65 59% 8.9 7.9 2.3 8.1

59 Nam Cheong FV 121.6 0.058 0.04 -31% nm nm 0.3 nm

60 Pacific Radiance Ltd HOLD 112.7 0.158 0.16 1% nm nm 0.3 nm

61 Procurri Corporation Limited BUY 112.0 0.400 0.56 40% 8.1 6.8 1.3 56.3

62 Trendlines Group HOLD 93.1 0.183 0.24 31% 16.0 13.7 0.7 2.4

63 Ezra Holdings FV 67.6 0.023 0.06 161% nm 5.3 0.1 nm

64 Katrina Group BUY 52.1 0.225 1.60 23% 9.5 8.1 3.1 12.8

Source: DBS Bank, Bloomberg Finance L.P.

Page 17

Market Focus

Small Mid Cap

COMPANY GUIDES

Page 18

ASIAN INSIGHTS VICKERS SECURITIES ed: TH / JC, PY

BUY (Initiating Coverage) Last Traded Price ( 31 Jan 2017): S$1.83 (STI : 3,046.80) Price Target 12-mth: S$2.36 (29% upside) Potential Catalyst: Earnings delivery, successful expansion into new markets, and M&A Analyst

Paul YONG CFA +65 6682 3712 [email protected] Singapore Research Team [email protected]

Price Relative

Forecasts and Valuation FY Dec (S$m) 2015A 2016F 2017F 2018F Revenue 102 207 269 311 EBITDA 19.5 46.1 62.1 73.1 Pre-tax Profit 17.0 43.5 59.3 70.3 Net Profit 10.1 29.8 40.6 48.0 Net Pft (Pre Ex.) 10.1 29.8 40.6 48.0 EPS (S cts) 4.59 10.8 14.7 17.4 EPS Pre Ex. (S cts) 4.59 10.8 14.7 17.4 EPS Gth (%) 146 136 36 18 EPS Gth Pre Ex (%) 146 136 36 18 Diluted EPS (S cts) 4.59 10.8 14.7 17.4 Net DPS (S cts) 2.00 4.72 6.43 7.61 BV Per Share (S cts) 28.9 29.3 37.6 47.4 PE (X) 39.9 16.9 12.4 10.5 PE Pre Ex. (X) 39.9 16.9 12.4 10.5 P/Cash Flow (X) 23.6 14.7 8.7 9.2 EV/EBITDA (X) 18.1 9.6 6.6 5.2 Net Div Yield (%) 1.1 2.6 3.5 4.2 P/Book Value (X) 6.3 6.3 4.9 3.9 Net Debt/Equity (X) CASH CASH CASH CASH ROAE (%) 16.8 41.3 44.1 41.1 Consensus EPS (S cts): 11.3 14.3 17.3 Other Broker Recs: B: 3 S: 0 H: 0 ICB Industry : Consumer Services ICB Sector: General Retailers Principal Business: Best World International (BEST SP) is the only direct selling company to be listed on the SGX. A regional player with a presence in 12 markets, Best World is primarily engaged in the development, manufacture and distribution of personal care and wellness products (including premium skincare, health supplements and other nutritional products). Source of all data on this page: Company, DBS Bank, Bloomberg Finance L.P.

At A Glance Issued Capital (m shrs) 276 Mkt. Cap (S$m/US$m) 506 / 359 Major Shareholders (%) D2 Investment Pte Ltd 34.9 Beng Mui Hoan 5.6 Moi Tan Nee 5.6

Free Float (%) 45.2 3m Avg. Daily Val (US$m) 1.9

DBS Group Research . Equity 1 Feb 2017

Singapore Company Focus

Best World International Bloomberg: BEST SP | Reuters: BEST.SI Refer to important disclosures at the end of this report

Buckling down China Direct seller of premium skincare has made a breakthrough in

Taiwan, where it has strong earnings momentum China, a market over 50x larger than Taiwan, is ripe for Best World

to harvest Attainment of a rare direct selling licence in China should underpin

years of firm growth Initiate with BUY, TP of $2.36 based on 16x FY17F PE

Singapore-based direct seller enjoying great success in Taiwan. Best World’s flagship Dr’s Secret range of premium skincare, which represents nearly 70% of the group’s sales, has been immensely successful in Taiwan. Currently Best World’s largest market by revenue, operations in Taiwan have already achieved a decent scale but still hold more potential. Looking ahead, strong earnings momentum will likely be sustained by further cultivation of existing networks in its stronghold in Central and Southern Taiwan, and plans to leapfrog into the Northern region.

Attainment of a direct selling licence in China, a market over 50x larger than Taiwan, should underpin years of firm growth. Best World hopes to emulate its success in China, where the cosmetics sector is forecasted to grow at 12.9% CAGR into 2019. With much of the groundwork already laid in the PRC, MOFCOM’s indirect endorsement through the recent award of its rare direct selling licence provides Best World with the credibility and platform needed to gain scale in the world’s most populous nation and second-largest direct selling market. Stronger participation rates at Best World’s post-licence recruitment events also confirm this.

Riding on highly scalable model to deliver 68% PATMI CAGR over FY15-18F. Compared to traditional retailers, Best World’s advantage lies in its highly scalable model (with lower fixed costs). Supported by greater scale economies, we project PATMI to rise quickly from S$10.1m in FY15 to S$48m by FY18F as the group further extends its reach in its key markets of Taiwan and China.

Valuation: Initiate with BUY; TP of S$2.36 is based on 16x FY17F PE. As Best World enters into a period of firm growth, we opine that it should trade at 16x FY17F earnings (at a smaller discount to global peers’ 19x). In addition, Best World’s PEG ratio of 0.4 is among the lowest in its peer group, which provides further upside.

Key Risks to Our View: Key risks include lack of control over individual distributor’s selling process and impact of unanticipated changes in local regulations and restrictions.

72

272

472

672

872

1072

0.1

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Relative IndexS$

Best World International (LHS) Relative STI (RHS)

Page 19

ASIAN INSIGHTS VICKERS SECURITIES Page 2

Company Focus

Best World International

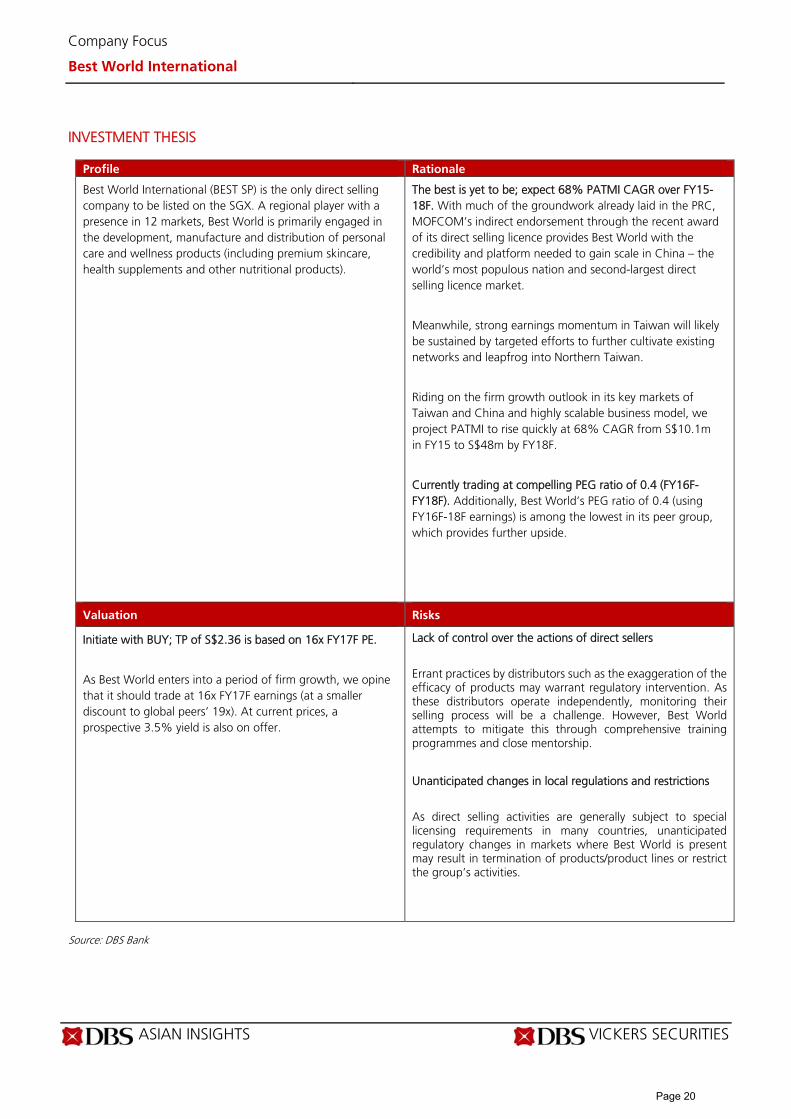

INVESTMENT THESIS

Profile Rationale

Best World International (BEST SP) is the only direct selling company to be listed on the SGX. A regional player with a presence in 12 markets, Best World is primarily engaged in the development, manufacture and distribution of personal care and wellness products (including premium skincare, health supplements and other nutritional products).

The best is yet to be; expect 68% PATMI CAGR over FY15-18F. With much of the groundwork already laid in the PRC, MOFCOM’s indirect endorsement through the recent award of its direct selling licence provides Best World with the credibility and platform needed to gain scale in China – the world’s most populous nation and second-largest direct selling licence market.

Meanwhile, strong earnings momentum in Taiwan will likely be sustained by targeted efforts to further cultivate existing networks and leapfrog into Northern Taiwan.

Riding on the firm growth outlook in its key markets of Taiwan and China and highly scalable business model, we project PATMI to rise quickly at 68% CAGR from S$10.1m in FY15 to S$48m by FY18F.

Currently trading at compelling PEG ratio of 0.4 (FY16F-FY18F). Additionally, Best World’s PEG ratio of 0.4 (using FY16F-18F earnings) is among the lowest in its peer group, which provides further upside.

Valuation Risks

Initiate with BUY; TP of S$2.36 is based on 16x FY17F PE.

As Best World enters into a period of firm growth, we opine that it should trade at 16x FY17F earnings (at a smaller discount to global peers’ 19x). At current prices, a prospective 3.5% yield is also on offer.

Lack of control over the actions of direct sellers

Errant practices by distributors such as the exaggeration of the efficacy of products may warrant regulatory intervention. As these distributors operate independently, monitoring their selling process will be a challenge. However, Best World attempts to mitigate this through comprehensive training programmes and close mentorship.

Unanticipated changes in local regulations and restrictions

As direct selling activities are generally subject to special licensing requirements in many countries, unanticipated regulatory changes in markets where Best World is present may result in termination of products/product lines or restrict the group’s activities.

Source: DBS Bank

Page 20

ASIAN INSIGHTS VICKERS SECURITIES Page 3

Company Focus

Best World International

SWOT Analysis

Strengths Weakness Strong brand equity and credibility SGX Mainboard listing and award of a rare direct selling licence in China helps to differentiate Best World from other fly-by-night schemes. Product appeal As a majority of its members (which we estimate to be 95%) are consumers rather than distributors, we think that the growing membership base is a good indication of the quality and demand for Best World products – particularly the Dr’s Secret range, which represents c.70% of the group’s sales. Scalable business model Compared to traditional retailers, Best World’s advantage lies in its highly scalable direct selling model, which has a lower proportion of fixed costs. Strong management team

Lack of control over the actions of direct sellers Errant practices by distributors such as the exaggeration of the efficacy of products may warrant regulatory intervention. As these distributors operate independently, monitoring their selling process will be a challenge. However, Best World attempts to mitigate this through comprehensive training programmes and close mentorship.

Opportunities Threats Strong earnings momentum in Taiwan While Best World has already achieved a decent scale in Taiwan, earnings momentum ahead will likely be sustained by further cultivation of existing networks in its stronghold in Central and Southern Taiwan, and plans to leapfrog into the Northern region. Emulating its success in China The cosmetics sector is forecasted to grow at 12.9% CAGR into 2019. MOFCOM’s indirect endorsement of Best World through the recent award of its direct selling licence is set to spur local interest and demand. M&A opportunities Ahead, the group may utilise some of its net cash to accelerate growth via M&A.

Weakening currencies As revenues are denominated in Best World’s respective local currencies, a weakening of these currencies against its reporting currency, the SGD, may negatively impact the group’s performance. Competition from other sales channels Faced with keen competition in the cosmetics sector – from direct selling companies as well as other sales channels, Best World must continue to innovate to maintain its edge. Unexpected changes in local regulations and restrictions As direct selling activities are generally subject to special licensing requirements in many countries, unanticipated regulatory changes in markets where Best World is present may result in termination of products/product lines or restrict the group’s activities.

Source: DBS Bank

Page 21

ASIAN INSIGHTS VICKERS SECURITIES Page 4

Company Focus

Best World International

Company background

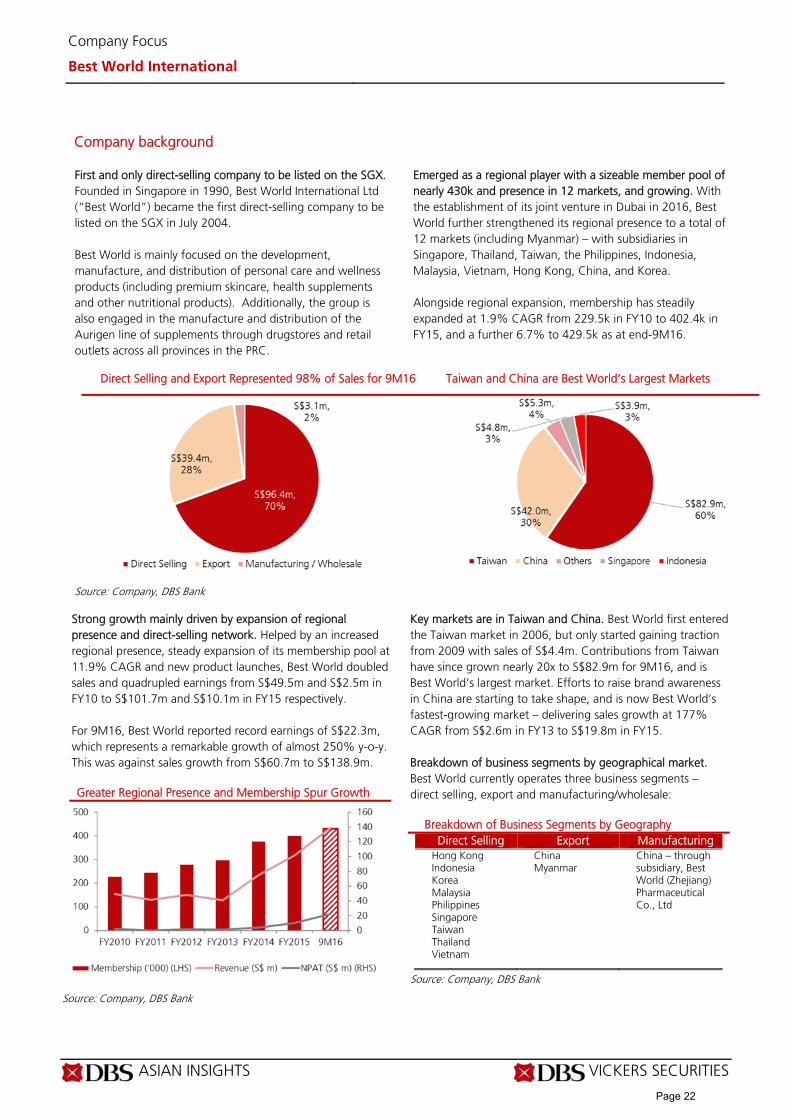

First and only direct-selling company to be listed on the SGX. Founded in Singapore in 1990, Best World International Ltd (“Best World”) became the first direct-selling company to be listed on the SGX in July 2004. Best World is mainly focused on the development, manufacture, and distribution of personal care and wellness products (including premium skincare, health supplements and other nutritional products). Additionally, the group is also engaged in the manufacture and distribution of the Aurigen line of supplements through drugstores and retail outlets across all provinces in the PRC.

Emerged as a regional player with a sizeable member pool of nearly 430k and presence in 12 markets, and growing. With the establishment of its joint venture in Dubai in 2016, Best World further strengthened its regional presence to a total of 12 markets (including Myanmar) – with subsidiaries in Singapore, Thailand, Taiwan, the Philippines, Indonesia, Malaysia, Vietnam, Hong Kong, China, and Korea. Alongside regional expansion, membership has steadily expanded at 1.9% CAGR from 229.5k in FY10 to 402.4k in FY15, and a further 6.7% to 429.5k as at end-9M16.

Direct Selling and Export Represented 98% of Sales for 9M16 Taiwan and China are Best World’s Largest Markets

Source: Company, DBS Bank Strong growth mainly driven by expansion of regional presence and direct-selling network. Helped by an increased regional presence, steady expansion of its membership pool at 11.9% CAGR and new product launches, Best World doubled sales and quadrupled earnings from S$49.5m and S$2.5m in FY10 to S$101.7m and S$10.1m in FY15 respectively. For 9M16, Best World reported record earnings of S$22.3m, which represents a remarkable growth of almost 250% y-o-y. This was against sales growth from S$60.7m to S$138.9m.

Greater Regional Presence and Membership Spur Growth

Source: Company, DBS Bank

Key markets are in Taiwan and China. Best World first entered the Taiwan market in 2006, but only started gaining traction from 2009 with sales of S$4.4m. Contributions from Taiwan have since grown nearly 20x to S$82.9m for 9M16, and is Best World’s largest market. Efforts to raise brand awareness in China are starting to take shape, and is now Best World’s fastest-growing market – delivering sales growth at 177% CAGR from S$2.6m in FY13 to S$19.8m in FY15. Breakdown of business segments by geographical market. Best World currently operates three business segments – direct selling, export and manufacturing/wholesale:

Breakdown of Business Segments by Geography Direct Selling Export Manufacturing

Hong Kong Indonesia Korea Malaysia Philippines Singapore Taiwan Thailand Vietnam

China Myanmar

China – through subsidiary, Best World (Zhejiang) Pharmaceutical Co., Ltd

Source: Company, DBS Bank

Page 22

ASIAN INSIGHTS VICKERS SECURITIES Page 5

Company Focus

Best World International

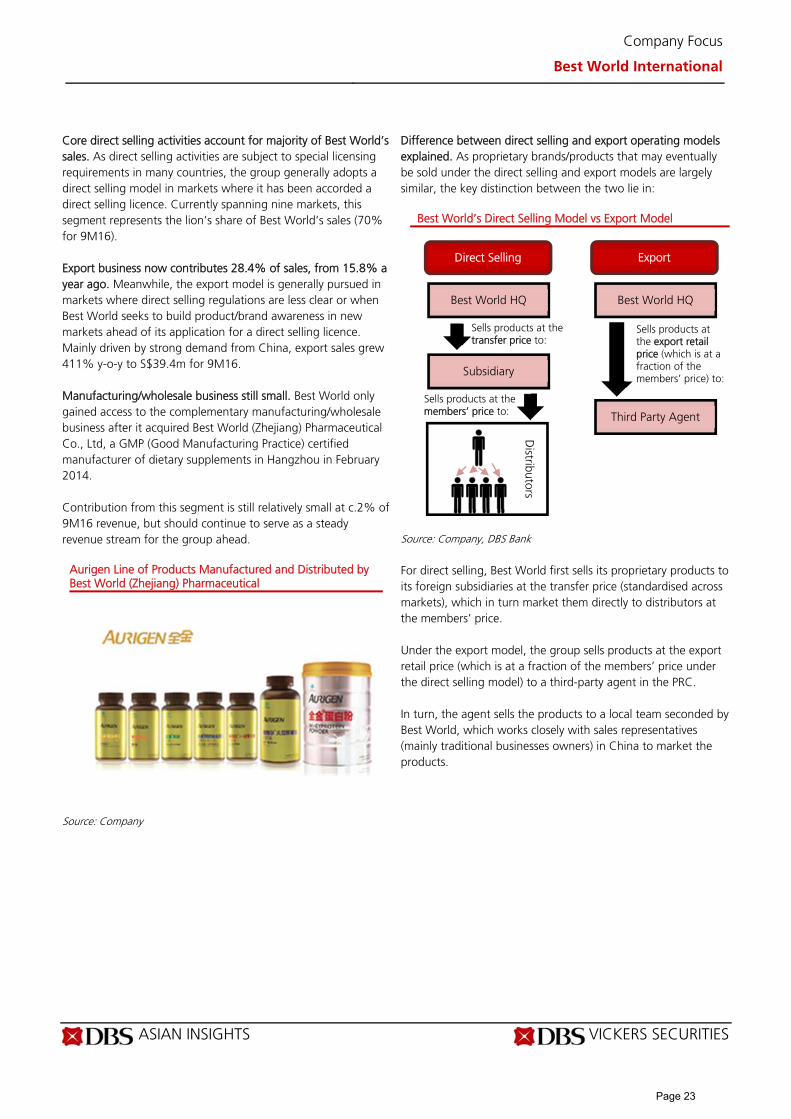

Core direct selling activities account for majority of Best World’s sales. As direct selling activities are subject to special licensing requirements in many countries, the group generally adopts a direct selling model in markets where it has been accorded a direct selling licence. Currently spanning nine markets, this segment represents the lion’s share of Best World’s sales (70% for 9M16). Export business now contributes 28.4% of sales, from 15.8% a year ago. Meanwhile, the export model is generally pursued in markets where direct selling regulations are less clear or when Best World seeks to build product/brand awareness in new markets ahead of its application for a direct selling licence. Mainly driven by strong demand from China, export sales grew 411% y-o-y to S$39.4m for 9M16. Manufacturing/wholesale business still small. Best World only gained access to the complementary manufacturing/wholesale business after it acquired Best World (Zhejiang) Pharmaceutical Co., Ltd, a GMP (Good Manufacturing Practice) certified manufacturer of dietary supplements in Hangzhou in February 2014. Contribution from this segment is still relatively small at c.2% of 9M16 revenue, but should continue to serve as a steady revenue stream for the group ahead.

Aurigen Line of Products Manufactured and Distributed by Best World (Zhejiang) Pharmaceutical

Source: Company

Difference between direct selling and export operating models explained. As proprietary brands/products that may eventually be sold under the direct selling and export models are largely similar, the key distinction between the two lie in:

Best World’s Direct Selling Model vs Export Model

Source: Company, DBS Bank For direct selling, Best World first sells its proprietary products to its foreign subsidiaries at the transfer price (standardised across markets), which in turn market them directly to distributors at the members’ price. Under the export model, the group sells products at the export retail price (which is at a fraction of the members’ price under the direct selling model) to a third-party agent in the PRC. In turn, the agent sells the products to a local team seconded by Best World, which works closely with sales representatives (mainly traditional businesses owners) in China to market the products.

Direct Selling Export

Best World HQ Best World HQ

Subsidiary

Third Party Agent

Sells products at the transfer price to:

Sells products at the members’ price to:

Sells products at the export retail price (which is at a fraction of the members’ price) to:

Distributors

Page 23

ASIAN INSIGHTS VICKERS SECURITIES Page 6

Company Focus

Best World International

Presence in 12 Markets through Subsidiaries and Joint Ventures in 11 Countries (as at end-2016) Markets Subsidiaries and JVs % Held Business Description Singapore Avance Living Pte. Ltd 100% Distribution of cosmetics, skincare, nutritional

supplements, personal care products and healthcare equipment

Best World Lifestyle Pte. Ltd 100% Distribution of nutritional supplements, personal care products and healthcare equipment

Celcott Investments Pte. Ltd 100% On 16 January 2017, Best World announced that Celcott has terminated its joint venture agreement with Prolife Biobank Private Limited, a stem cell banking service provider

Taiwan Best World Lifestyle (Taiwan) Co., Ltd

100% Distribution of health food, network services, sanitary products, skin care and cosmetic products

Hong Kong Best World Lifestyle (HK) Company Limited

100% Distribution of cosmetics, skin care, nutritional supplements, personal care products and healthcare equipment

Vietnam Best World Vietnam Company Limited 100% Trading and distribution of skincare and health-related products

Philippines BWL Health & Sciences, Inc. 100% Selling and distribution, on wholesale basis of skincare, nutritional supplements and personal care products and healthcare supplements

China Best World Lifestyle (Shanghai) Co., Ltd.

100% Import and distribution of cosmetics, skincare, nutritional supplements, personal care products and healthcare equipment

Best World (Zhejiang) Pharmaceutical Co., Ltd.

100% GMP-certified and focused on the development, manufacture and wholesale of the Aurigen brand of dietary supplements

Korea BWL Korea Co., Ltd 100% Distribution of skincare, health food and equipment

Malaysia Best World Lifestyle Sdn Bhd 77.5% Import and distribution of cosmetics, skincare, nutritional supplements, personal care products and healthcare equipment

Indonesia PT BWL Indonesia 80% Distribution of cosmetics, skincare, nutritional supplements, personal care products and healthcare equipment

Thailand PT Best World Indonesia 80% -

BWL (Thailand) Company Limited 49% Import and distribution of cosmetics, skincare, nutritional supplements, personal care products and healthcare equipment

Dubai BWL General Trading L.L.C 49% JV with local Dubai partner

Source: Company

Page 24

ASIAN INSIGHTS VICKERS SECURITIES Page 7

Company Focus

Best World International

Best World’s key success factors lie in…

Apart from product appeal, distributors are often the driving force of successful direct selling companies. As new competitors emerge, and given the primary role played by independent distributors in generating product awareness and ultimately, driving sales, a direct selling company’s ability to grow, motivate and retain its pool of distributors are key. We evaluate Best World based on several critical factors considered by direct sellers (both new and existing) when choosing a direct sales company and found that Best World’s key success factors lie in its strong product appeal, branding, reasonable start-up cost requirements, effective compensation plan and holistic support structure. This is evidenced by the company's growing member pool and higher earnings generated per member:

FY10 FY15 CAGR

Members 229,498 402,422 11.9%

Per member contribution to NPAT (S$)

S$10.7 S$25.1 18.7%

Source: Company, DBS Bank (1) Product appeal

Offers extensive range of premium skincare, personal care, nutritional and wellness products. Through its seven proprietary brands, Best World offers an extensive range of products (over 60 SKUs), that are mostly concentrated in the premium skincare, personal care, nutritional and wellness space. Products under the Aurigen line are distributed to drugstores and retail outlets in China via the manufacturing/wholesale channel, while those marketed under the six remaining proprietary brands (as shown below) are distributed through Best World’s direct selling and export channels. Brands Distributed Through Direct Selling and Exports

Source: Company, DBS Bank

Best World’s products are generally well received. According to the company, “members” refer to individuals who have made purchases within the last 12 months, and have opted to be members for a nominal fee, which would entitle them to benefits under the direct selling programme. Consumers also have the option to buy directly from the company without becoming a member. As a majority of its members (which we estimate to be 95%) are consumers rather than distributors, we think that the growing membership base is a good indication of the quality and demand for Best World products. Best kept secret? According to the company, its skincare products (Dr’s Secret) are the primary sales driver, and typically make up about 70% of the group’s total revenues. While we have yet to put the purported benefits of Best World’s Dr’s Secret range of skincare to the test, we have noticed visible improvements to the skin condition of our acquaintance, who is a relatively new user: Before/After Using Dr’s Secret

From left: Before use, after 1 month, after 2 months

Source: DBS Bank (2) Credibility

Brand equity from Mainboard listing helps differentiate Best World from other fly-by-night schemes. Cases of pyramid schemes posing as direct sales programmes have led to concerns over the legitimacy of direct selling companies. In this regard, we see value in Best World’s SGX Mainboard listing as the supervision and indirect endorsement of the exchange through stringent listing/reporting requirements provides credibility to the legitimacy of its business. Skepticism over its direct selling model could be dispelled over time. We believe that Best World has demonstrated the resilience of its operating model through its established record of consistent profits and positive cash flows over the last 15 years. With time, we believe that concerns over its direct selling business – especially in China, which is now in focus, will be gradually dispelled if the group remains cash flow-generative while delivering earnings growth in China.

Page 25

ASIAN INSIGHTS VICKERS SECURITIES Page 8

Company Focus

Best World International

(3) Start-up cost for distributors

Start-up costs kept at a minimum. Initial investments for direct sellers typically include membership fees and inventory costs. In line with recommendations by the Direct Selling Association (DSA), start-up costs for Best World’s distributors are generally modest and include (i) a nominal membership fee, and (ii) reasonable inventory costs as its distributors (to prevent inventory loading) are not under compulsion to hold large amounts of inventory. (4) Compensation plan

Compensation plans should be attractive, yet sustainable. We believe that an effective compensation plan should facilitate the meeting of the following objectives: (i) motivate distributors to work hard at growing their product sales and network, and in return, (ii) reward their efforts through long-lasting residual income. Importantly, compensation should also be exclusively derived from commissions earned based on sales of actual products and not on recruitment. Best World practices a hierarchical commission structure under which distributors (members who purchase Best World products for sale to their network contacts, and further develop their network by introducing new members to the group) who achieve a minimum prescribed sales target will be accorded benefits and bonuses. As a distributor rises up the ranks, his/her benefits will increase. Promotions are hinged upon the sales volume generated by the distributor and his downlines (members recruited by the distributor) within a specified time period. Commissions paid out to distributors vary with product type and rank (among other factors), and are paid up to approximately 35-40% of sales value. (5) Holistic support structure

Comprehensive training. In line with its holistic approach, Best World has developed a comprehensive series of courses that are focused on personal wellbeing and equipping members with essential skills for success in the direct selling industry – such as product knowledge, entrepreneurial skills and business skills. While these courses are made available to members across its 12 markets and are usually self-funded (to cover overheads), attendance is not compulsory. The company has also often stressed that they do not profit from such events. Building a culture of mentorship and peer support. Independent sharing sessions hosted and sponsored by distributors are a regular feature at Best World. Each small group session is usually led by a senior, higher-ranked distributor (upline) who is primarily responsible for guiding

and grooming junior members (downlines) through close mentorship. Additionally, through brainstorming and sharing of experiences, these events are a viable platform for peer support and learning. System and tools. To help facilitate the sales process, Best World recently developed and launched a WeChat micro-site for its China market, which provides users with comprehensive information on its Dr’s Secret range, web-based membership enrolment (if desired) and the option to make purchases via the app. According to the company, sales made via the app will still go directly to the respective sales representatives. Best World’s WeChat Micro-site

Source: Company

Page 26

ASIAN INSIGHTS VICKERS SECURITIES Page 9

Company Focus

Best World International

Business model displays superior sales-to-cost growth relationship Best World’s Current Business Process for Direct Selling and Export Segments

Source: Company, DBS Bank

(1) Significant cost and time savings from the use of third-

party manufacturing

Enhancing consumer appeal through product innovation and improvement. Leveraging on insights from its vast member network and anticipating trends in the consumer/lifestyle space, Best World continuously seeks to introduce new, innovative products and improve on the existing formulae and packaging of its products to enhance its consumer appeal. Formulations are done in-house. Once a new product idea is initiated, Best World would first formulate the product in-house before appointing third-party manufacturers to develop prototypes. These efforts are usually led by the President, Dr Doreen Tan, who is a qualified nutritionist and CEO, Mr Huan Ban Chin, who is a biochemist and microbiologist by training. Low capex requirements as proprietary products are manufactured by contract manufacturers... The outsourcing of its manufacturing function allows Best World to mass produce without incurring substantial capex charges. The company’s current contract manufacturers are mainly based in Taiwan, Korea and the US. …but quality checks and packaging are done in-house. The group’s quality control process requires that finished products

be sent for sample inspections upon delivery. They are then sent to the group’s packaging facility in Singapore before they are distributed via the direct selling and export channels.

(2) Direct selling among the most scalable retail channels

Direct selling vs conventional retail. Unlike conventional retail, direct selling is a socially-based sales process where distributors – which are not confined to a permanent retail location, play a primary role in raising brand awareness. Eliminating the need for various costly overheads - such as rental, staff and advertising, the advantage of Best World’s direct selling model as opposed to traditional brick-and-mortar sales formats lies in its scalability given its ability to grow sales quickly without a commensurate increase in costs. This is evidenced by:

FY10 FY15 CAGR Membership 229,498 402,422 11.9%

Revenue (S$ m)

49.55 S$101.7 15.5%

NPAT (S$ m) 2.45 4.05 32.8%

Source: Company, DBS Bank

Product Initiation

Product Conceptualisation and Development

Receipt of Products, Quality Assurance and Packaging

3rd Party Manufacturing, New Product Registration and Marketing

Sales through Distribution Channels Direct Selling Export

Page 27

ASIAN INSIGHTS VICKERS SECURITIES Page 10

Company Focus

Best World International

A glimpse into Best World’s China operations

Best World’s 102 Product Workshop in Changsha, China (10-11 Dec 2016)

Source: DBS Bank Large-scale recruitment event attracting over 1,000 attendees. We had the opportunity to visit Best World’s operations in Changsha (Hunan province), where we attended a large-scale event from 10-11 December 2016 – which the company refers to as the “102 Product Workshop”, aimed at recruiting sales representatives. Over the course of two days, we spoke to key members of Best World’s China operations who were seconded from the company to China some years ago to lay the foundation and build awareness for the group’s products ahead of its application for a direct selling licence. We saw a good mix of both existing and potential sales representatives at the event, most of whom were traditional business owners. Of over a thousand attendees, we had the opportunity to interact closely with at least 60-70 individuals, including: (1) pioneer members/sales representatives, (2) existing users of Best World products exploring opportunities in direct selling, and (3) potential customers/users. Key items on the agenda included an introduction to Best World and its culture – led by co-founder Dr Dora Hoan, educational sessions focused on the philosophy behind its products and brands and improving product knowledge, managing expectations for upcoming events (such as the potential conversion to the direct selling model in China and shifting of manufacturing operations for Dr’s Secret products from the US to Singapore), as well as the sharing of inspirational success stories by some of the group’s top sales representatives. Thereafter, attendees would then break into smaller groups (led by their respective uplines), where they would take turns to share their takeaways, personal experiences (both as product users and as sales representatives) as well as their sales goals. At a Small-group Sharing Session

Source: DBS Bank

From the horse’s mouth. Through our interactions with attendees and sitting in at several small-group sharing sessions, we found that majority came to know about Best World’s products indirectly, after noticing and making enquiries about improvements to the physical appearance of a friend/acquaintance. Individuals who were once less financially independent felt that they benefitted from the low start-up costs and “having a product that sells itself”, which allowed them to “start small” and gradually grow their passive income. Encouraged by the success stories, several attendees (existing users) also made the leap to join Best World as a sales representative. Participants were generally most excited about the prospect of having a first-mover advantage in their respective cities, and looked forward to leveraging on the new WeChat micro-site to optimise their sales and networking efforts. Due to geographical dispersion, distributors located farther from the local headquarters in Changsha cited longer delivery lead-times as a challenge.

Page 28

ASIAN INSIGHTS VICKERS SECURITIES Page 11

Company Focus

Best World International

Earnings growth a driver of share price Historical Relationship Between Earnings Growth and Best World’s Share Price

Strong historical correlation between share price and trailing 12-month earnings per share price (T12M EPS). We attempt to study the longer–term relationship between BEST’s share price performance against T12M EPS as we compute the correlation between the two from FY2012. The pair displayed a positive correlation of 0.940, which suggests that BEST’s 12-month EPS performance for the past five years was closely correlated to changes in the underlying share prices. Best World mostly traded range-bound between 2012 and most of 2015, but saw an uptick at end-2015 after the company reported a good set of results – earnings for the quarter nearly doubled m-o-m. Apart from strong earnings momentum, the share’s impressive 400% run-up in 2016 from 26.8 Scts to S$1.34 (as at 31 December) also appears to be driven by optimism surrounding

the counter in anticipation of the award of its direct selling licence in China:

Quarterly EPS T12M EPS

3Q15 0.0077 0.02008

4Q15 0.0146 0.03064

1Q16 0.0135 0.03672

2Q16 0.0217 0.05752

3Q16 0.0268 0.07664

% Chg: +248% +282%

Source: DBS Bank, Bloomberg Finance L.P.

Source: DBS Bank, Bloomberg Finance L.P.

Page 29

ASIAN INSIGHTS VICKERS SECURITIES Page 12

Company Focus

Best World International

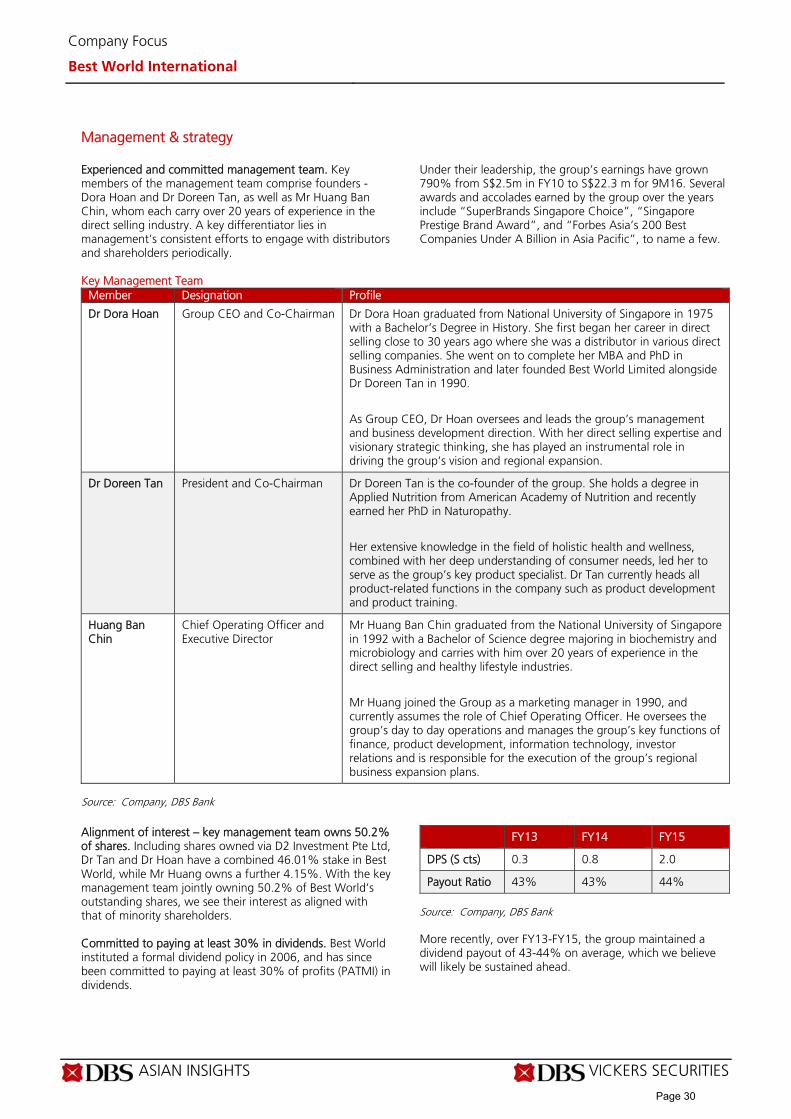

Management & strategy Experienced and committed management team. Key members of the management team comprise founders - Dora Hoan and Dr Doreen Tan, as well as Mr Huang Ban Chin, whom each carry over 20 years of experience in the direct selling industry. A key differentiator lies in management’s consistent efforts to engage with distributors and shareholders periodically.

Under their leadership, the group’s earnings have grown 790% from S$2.5m in FY10 to S$22.3 m for 9M16. Several awards and accolades earned by the group over the years include “SuperBrands Singapore Choice”, “Singapore Prestige Brand Award”, and “Forbes Asia’s 200 Best Companies Under A Billion in Asia Pacific”, to name a few.

Key Management Team Member Designation Profile

Dr Dora Hoan Group CEO and Co-Chairman Dr Dora Hoan graduated from National University of Singapore in 1975 with a Bachelor’s Degree in History. She first began her career in direct selling close to 30 years ago where she was a distributor in various direct selling companies. She went on to complete her MBA and PhD in Business Administration and later founded Best World Limited alongside Dr Doreen Tan in 1990.

As Group CEO, Dr Hoan oversees and leads the group’s management and business development direction. With her direct selling expertise and visionary strategic thinking, she has played an instrumental role in driving the group’s vision and regional expansion.

Dr Doreen Tan President and Co-Chairman Dr Doreen Tan is the co-founder of the group. She holds a degree in Applied Nutrition from American Academy of Nutrition and recently earned her PhD in Naturopathy.

Her extensive knowledge in the field of holistic health and wellness, combined with her deep understanding of consumer needs, led her to serve as the group’s key product specialist. Dr Tan currently heads all product-related functions in the company such as product development and product training.

Huang Ban Chin

Chief Operating Officer and Executive Director

Mr Huang Ban Chin graduated from the National University of Singapore in 1992 with a Bachelor of Science degree majoring in biochemistry and microbiology and carries with him over 20 years of experience in the direct selling and healthy lifestyle industries.

Mr Huang joined the Group as a marketing manager in 1990, and currently assumes the role of Chief Operating Officer. He oversees the group’s day to day operations and manages the group’s key functions of finance, product development, information technology, investor relations and is responsible for the execution of the group’s regional business expansion plans.

Source: Company, DBS Bank

Alignment of interest – key management team owns 50.2% of shares. Including shares owned via D2 Investment Pte Ltd, Dr Tan and Dr Hoan have a combined 46.01% stake in Best World, while Mr Huang owns a further 4.15%. With the key management team jointly owning 50.2% of Best World’s outstanding shares, we see their interest as aligned with that of minority shareholders. Committed to paying at least 30% in dividends. Best World instituted a formal dividend policy in 2006, and has since been committed to paying at least 30% of profits (PATMI) in dividends.

FY13 FY14 FY15

DPS (S cts) 0.3 0.8 2.0

Payout Ratio 43% 43% 44% Source: Company, DBS Bank More recently, over FY13-FY15, the group maintained a dividend payout of 43-44% on average, which we believe will likely be sustained ahead.

Page 30

ASIAN INSIGHTS VICKERS SECURITIES Page 13

Company Focus

Best World International

(1) Focusing on its fastest-growing market, China Direct selling licence for Hangzhou now effective. Best World was granted its direct selling licence by the Ministry of Commerce, the People’s Republic of China (MOFCOM) on 30 June 2016. Having fulfilled the condition of setting up nine service centres in Hangzhou city (one per district), Best World is now permitted to commence direct selling in Hangzhou city. Shift to direct selling model in 2017 unlikely. We do not expect to see a complete shift from the export to direct selling model in China for 2017 as (i) the direct selling licence was only awarded for Hangzhou city, while Best World’s stronghold is in the Hunan (Changsha), Zhejiang, Guangdong, Sichuan (Chongqing) and Heilongjiang (Harbin) provinces, and (ii) differing direct selling regulatory frameworks between China and its other direct selling markets. To successfully navigate China’s regulatory environment, we reckon that it will take a further 8-10 months (or longer) for Best World to finetune its direct sales model for China, before making a formal shift away from its current export model. Ahead of this, we believe that the company will still continue to grow the geographical coverage under its direct selling licence. Similar to Hangzhou, the extension will entail setting up one service outlet per district per city. We think Best World will likely kick-start the process by focusing on cities and provinces where it has established its presence. Strategies to drive growth in China. Leveraging on its heightened brand/product awareness following MOFCOM’s indirect endorsement, we believe Best World will continue to employ the following strategies to drive growth: (a) Increasing the frequency of large-scale recruitment events

(much like the one we attended in Changsha) from one to two/three per quarter, especially in Tier 2 and Tier 3 cities where the competitive landscape tends to be more favourable

(b) Rolling out more promotional events and introducing more complementary products into China – subject to successful product registrations

(c) Recent launch of Best World’s official WeChat micro-site,

an informative in-app order platform, should help raise the productivity of its sales representatives

(2) Driving sales across markets through higher member engagement levels Upside potential when customers exercise option to also distribute. As Best World is primarily focused on growing user base, before ultimately converting them to distributors. We see significant potential just from Best World’s current membership base alone as c.95% of its membership pool comprises users who have fulfilled the criteria to be distributors, and have the flexibility to do so if desired. Further beefing up its product portfolio. Best World typically introduces an average of 3-4 new products each year. From

2017, to better engage and incentivise members to achieve their prescribed maintenance amounts – the level at which rebates/bonuses kick in, the group plans to supplement new product offerings with a series of more generic, day-to-day products (such as toiletries and instant beverages). (3) Setting up a skincare manufacturing facility in Singapore Motivations for shifting operations back to Singapore. The company typically has an average lead time of six months for its purchase orders with its OEM manufacturer in the US, and as a result, has had to hold considerable amounts of inventory on its balance sheet. In addition to hopes of reducing its inventory lead time, the group’s strategic decision to shift its skincare manufacturing operations back to Singapore was also to allow for greater control over procurement of raw materials and production quality. While it is not a key priority, this initiative could also lead to eventual cost-savings (i.e. freight costs) for the group over the longer term. Tuas facility to be operational by end-2017. Best World acquired a 4,550-sqm facility in Tuas (Singapore) for S$10m in 2016. By the end of 2017, half of Best World’s skincare products are expected to be manufactured out of Tuas, with the shift in operations back to Singapore likely to be completed by early 2019. (4) Net cash of S$30.2m could be deployed towards acquisitions

M&A opportunities. Best World will likely utilise some of its net cash of c.S$30.2m as at 9M16, to accelerate growth inorganically. Potential candidates include direct selling companies which provide immediate access to new markets (such as Japan and Europe), or complementary products and services that could be further marketed via Best World’s distribution network – similar to its proposed acquisition of stem cell banking service provider, Prolife Biobank in 2016 (which has since lapsed as conditions precedent in the joint venture agreement were not met).