Embed Size (px)

Citation preview

GUIDE TO PROPERTY INVESTING

2ND EDITION

1

INTRODUCTION

There are many times in our life that we dread to look at our bank balance. We are also facing difficult times in regards to jobs for life (which no longer exist), continuous bouts of recession (are we ever out of it?), pensions that seem to be worthless (when was the last time you looked at its value?) and people on the whole wonder where their fortunes will come from.

If any of the above sounds like your current position, then maybe this article is for you. I am writing a basic guide to property investing without too much of the waffle (or at least I will try).

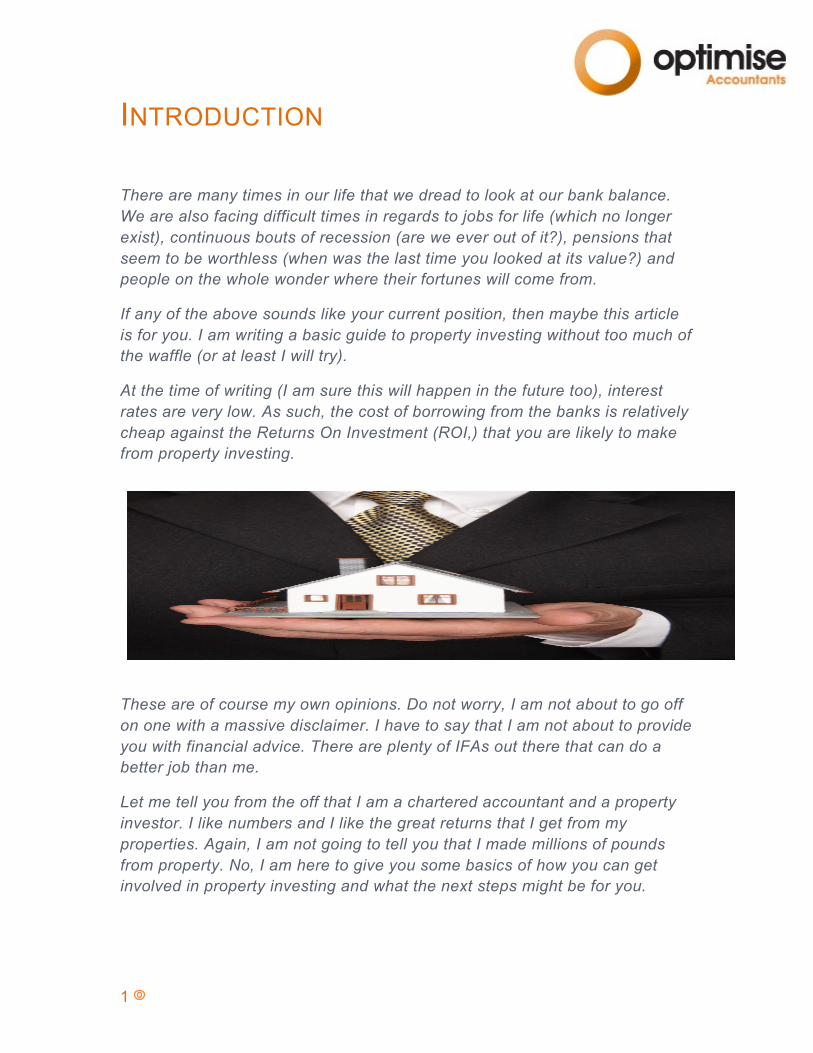

At the time of writing (I am sure this will happen in the future too), interest rates are very low. As such, the cost of borrowing from the banks is relatively cheap against the Returns On Investment (ROI,) that you are likely to make from property investing.

These are of course my own opinions. Do not worry, I am not about to go off on one with a massive disclaimer. I have to say that I am not about to provide you with financial advice. There are plenty of IFAs out there that can do a better job than me.

Let me tell you from the off that I am a chartered accountant and a property investor. I like numbers and I like the great returns that I get from my properties. Again, I am not going to tell you that I made millions of pounds from property. No, I am here to give you some basics of how you can get involved in property investing and what the next steps might be for you.

2

BEFORE YOU GET STARTED IN PROPERTY

Before you go into property investing it is always worth spending a few hours, days or even weeks going through your goals and objectives.

I am not here to sell you life coaching sessions. You could not afford me anyway (just kidding). On a serious note you would not start a journey in your car without knowing where you are headed, right?

What are your goals?

Think about what your goals are financially for the next 12 months, then 3 years and finally 5 years? After that it will be pure guesswork, (in my opinion of course). There may be people that say to me “but Simon I have planned the next 30 years”. For the purposes of this report, let us stick with 5.

Before you look into the future though you need to truly understand where you are today. So write down how much money you earn per month and the value of your net assets. Once done, start to write down the amount of money that you would like to be earning per month, after three months. Finally write down the value of the net assets you will have in three years.

3

THE PROPERTY MARKET

At the time of writing, house prices were beginning to steadily increase. Not a lot but there was certainly an increase. What does this mean? In my opinion for what it is worth, this could mean two things:

• House prices will continue to increase because there is more demand, fuelled by a recovery from recession or government backed mortgages. (1)

• It is a temporary blip and house prices will continue to decrease over the long term because of a bigger recession.

You may have noticed that the above points are contradictory and may appear that I am sitting on the fence. Well I like splinters up my backside, so yes I am sitting on the fence.

Quite honestly, I do not know if house prices will increase. The so-called experts have been caught out already.

People have complained bitterly that the government have not supported buyers. Now that they have with the government backed mortgages, people are claiming that house prices will increase and will result in another bubble.

Brian Murphy, managing director of the Mortgage Advice Bureau, said: "What comes next in the development of Help to Buy, will determine just how many people can join the rush to secure a good deal on property, whether or not they are first-time buyers or second-steppers”.

"We are still waiting to see how the mortgage guarantee will work in practice, but in the meantime the competition between lenders means there is plenty of reason to shop around and seek advice to secure a favourable offer." (2)

4

Therefore, I am not sure if house prices are going to go up, or down and I do not know what will happen to house prices in the future. What is the point of me writing this article?

I can safely say that house prices have increased every 15 years without fail. and yes, you may see good growth in the future. Is this likely to increase in the same way over the next 15 -20 years? That I cannot say, other than taking an educated guess by looking at the historic chart. In my view, house prices will continue to rise, why?

There are more and more people living in the UK and this country is not getting any bigger. Supply and demand. The demand for houses will continue to increase and the construction of property is not enough to cope with demand. (4)

5

GETTING STARTED So, what is the first thing that you must do?

I am hoping that you have done this already. You should have written down your goals and committed to making them happen. If you have not done that then please go back and re-read the first section.

The first thing that I would say about property investing is education, the second thing about property investing is networking and the third is experience.

Before you start though, please do begin learning from books, videos, courses etc to get you to know the basics. I am going to provide you with some great tips but there is nothing better than learning new skills, listening to people that have made a success of it and will also tell you the mistakes that they have made along the way.

Would it not be better to listen to others that have made mistakes so that you can put in place safeguards to reduce your risks?

There are plenty of courses around and if you Google people like Simon Zutshi (5) and Rob Moore (6) then you will find, in my opinion, the best courses on the market for property investing. Not only that, but you may also see me at one of their networking meetings.

One of the key learning’s I have found, was listening to other people. I would suggest that talking and listening with property investors who have been there and done it, might show you some quick paths to success. I will also say that there are many property investors that genuinely want to help you on your journey.

6

KNOW THE MARKET House prices are more likely to increase if it is in a good area and people want to live there. The more sought after an area is, the more demand there will be for the property. As a result, the house prices are likely to increase. (7)

Here are some great ways to know if an area is worth investing in:

• Great transport links into a town or city centre. Even more so, if there are transport links direct to London.

• The crime rate in the area is low and therefore considered safe.

• There are good schools that are performing well against the national average.

• There are good quality shops that are close to the area.

• The local authorities are looking to make improvements to the area such as parks and additional amenities that will attract more people.

There may be other points that you can think of too. This article is here to make you think and for you to make a more informed decision.

The very best way to get to know the market is to go and look. Get in the car, take the bus and get moving. You will be the best judge to determine if a market is right for you.

I would also suggest that you speak with the local letting agents to find out if the letting market is good.

7

KNOW THE NUMBERS Ok I am a bean counter (accountant) and you may say numbers are the most important aspect of property investing. You would be correct!

There are many things to consider when buying a property investment:

• Purchase price: is the price of the property correct in comparison to the sold prices in recent months (do not just compare the house prices to other “For Sale” prices – these are not sold yet)?

• The amount of deposit that you will have to invest. At the time of writing, mortgage lenders were asking for 25% of the property value. (2)

• Depending on the amount of work that is required on the property will determine the amount of money that you will spend on refurbishment. I would always advise you take another property investor or a builder who can give you a rough estimate, do not take a chance by estimating it yourself.

• Professional fees such as legal costs - some mortgage brokers are charging a fee on top of the mortgage arrangement fee that banks are charging (again, at the time of writing).

• Bank interest. There are different types of mortgages that you can go for. You can opt to pay just the interest on an “Interest Only” mortgage and pay the capital at the end of the term or “Capital repayment” whereby you pay off the loan during the term.

There are other costs to consider, but for me, these are the major costs, apart from your accountancy costs of course. No, honestly mine are very reasonable – just in case you were wondering

8

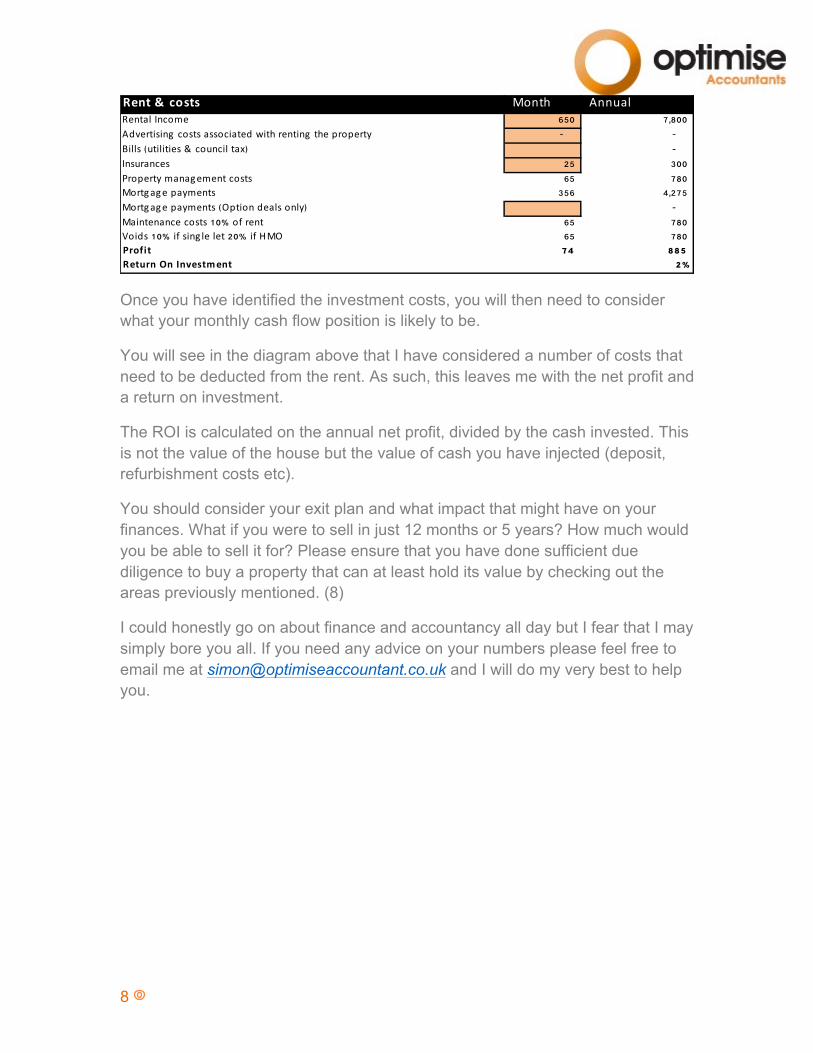

Rent & costs Month AnnualRental Income 650 7,800

Advertising costs associated with renting the property - -

Bills (utilities & council tax) -

Insurances 25 300

Property management costs 65 780

Mortgage payments 356 4,275

Mortgage payments (Option deals only) -

Maintenance costs 10% of rent 65 780

Voids 10% if sing le let 20% if HMO 65 780

Profit 74 885

Return On Investment 2%

Once you have identified the investment costs, you will then need to consider what your monthly cash flow position is likely to be.

You will see in the diagram above that I have considered a number of costs that need to be deducted from the rent. As such, this leaves me with the net profit and a return on investment.

The ROI is calculated on the annual net profit, divided by the cash invested. This is not the value of the house but the value of cash you have injected (deposit, refurbishment costs etc).

You should consider your exit plan and what impact that might have on your finances. What if you were to sell in just 12 months or 5 years? How much would you be able to sell it for? Please ensure that you have done sufficient due diligence to buy a property that can at least hold its value by checking out the areas previously mentioned. (8)

I could honestly go on about finance and accountancy all day but I fear that I may simply bore you all. If you need any advice on your numbers please feel free to email me at [email protected] and I will do my very best to help you.

9

AXE THE TAX Many people are buying properties as an investment. There are many landlords and property investors that have accountants. The sad thing is that their accountants could be of greater use if landlords and property investors involved them in the buying process.

As it is a tax question whether expenditure is capital or revenue, accountancy has no role in deciding whether or not an expense is allowable. Accountancy is important as the accounts prepared in accordance with GAAP, determine when relief is given for tax purposes. (9)

There are two types of costs that we will consider throughout this article:

o Capital costs

o Revenue costs

As you may appreciate, revenue costs may be offset against your profit and therefore reduces your tax liability. A capital cost is an asset and is therefore part of your balance sheet. These costs are depreciated over a number of years but only where it is a commercial property. Residential properties are not allowed to depreciate their assets to reduce future tax liabilities (4).

So what are capital costs and revenue costs? (10)

Capital costs (depreciated over a number of years).

Replacing assets if you are replacing an entire asset rather than repairing assets such as kitchen suites, bathrooms suites, fencing etc, and these costs are not considered a repair and therefore needs to be capitalised as an asset. (11)

Improvement / alteration / technology cost: Where any improvements are made to an asset such as a new kitchen with greater features or a conservatory, then these costs are an improvement of the asset as a whole and are therefore capitalised costs that benefit from 18% capital allowances each year. Examples of improvements are: double glazed windows from single glaze, electrical system with alarms that did not have one before.

If something is ‘a fixture’ then it has become part of the building and not an asset in its own right. (9)

10

The type of costs that are considered to be capital costs of a residential building are:

o Boilers

o Radiators

o Kitchen suites

o Bathroom suites

o Electrical systems

o Lifts

o Revenue costs (tax deductible)

o Replacing assets: whereby you are replacing an element of an asset such as an oven door, parts of existing brickwork, replacing tiles on a roof (12) as these examples are part of the an existing asset and not an asset in its own right.

o Repairs: There are times when repairs will be required on the property itself and these may be deducted, (15)

o Exterior and interior painting and decorating,

o Stone cleaning,

o Damp and rot treatment,

o Mending broken windows, doors, furniture and machines such as cookers or lifts,

o Re-pointing, and

o Replacing roof slates, flashing and gutters.

o Integral features: are sometimes repaired or replaced. Items such as kitchens, bathrooms suites, fencing whereby the total cost of the replacement / repair is more than 50% of the original cost are to be considered a capital cost.

o The following items of costs cannot be considered as a repair or capital if they are used by a tenant in a residential setting. (14)

o Fridges / freezers

11

o Furniture and related fixtures

o Temporary fixtures

o Carpets and soft furnishings

Here are some examples given by HMRC: (9)

Example 1

Amy owns a Victorian building that has been divided into student flats.

The electrician recommends that the building needs re-wiring. Amy decides to take the opportunity and have the building modernised.

The whole house is rewired, the heating system is partially replaced; the kitchens in all flats are replaced, together with two of the bathrooms. Three windows are replaced and the property re-decorated inside and out.

As a result of the work, Amy still has a property divided into the same number of student flats, capable of providing the same standard of accommodation for the same number of students.

Looked at, as a whole, the character of the asset has not changed as a result of the work. There may be small items of alterations, but the overall programme is simply a repair. As the property is a dwelling house, it does not qualify for capital allowances and so the integral features rules do not need to be considered.

For further guidance on the meaning of ‘dwelling house’ see the capital allowances manual CA11520.

Amy’s property lies in an area that is attracting investment. Rather than refurbishing the property as student accommodation, Amy has the same work carried out to a higher standard and converts the building into flats suitable for long term letting to people in a high income bracket.

Looked at as a whole, the character of the asset has changed, from short let student accommodation to up-market long term lettings.

It is important to recognise that a considerable amount of work that can be carried out without changing the character of the asset.

12

Example 2

Sophia owns a number of residential properties that she lets. The properties are not furnished lettings.

The boiler in one property needs replacing. As the new boiler has to be located in a different position, Sophia decides to modernise the kitchen as a whole.

All the existing base units, wall units and sink etc are stripped out and replaced, as is the fitted cooker and hob. New units of an equivalent quality are installed but in a different layout to allow for the re-location of the boiler, finally the kitchen is re-plastered and re-tiled.

The entirety is the house, not the fitted kitchen. The new kitchen is slightly different but it does the same job as before. Sophia has simply replaced the old kitchen with a modern equivalent. This is a repair and allowable expenditure.

Shortly afterwards, the fridge freezer breaks down and has to be replaced.

This is not part of the building but is an asset in its own right. Sophia has not repaired an asset; she had incurred capital expenditure on a new asset. As the fridge freezer is used in a dwelling house, it is not qualifying expenditure for capital allowances purposes.

Example 3

A Ltd company trades from premises that consist of a showroom and warehouse. They decide to modernise their premises. They completely renew the roof; refurbish the staff kitchen; they extend the showroom by demolishing an interior wall and building a new one and installing a new floor and false ceiling to modernise the extended showroom area.

The new roof simply returns the roof to original condition. It is neither an alteration nor improvement; it is simply a repair of the building. In the same way, the refurbishment of the staff kitchen is simply a repair of the building. These are allowable expenses.

Example 4:

Rosemary runs a property business. One of the houses needs repairs to the roof. Rosemary takes the opportunity to convert the attic into an additional bedroom.

13

Rosemary has chosen not to simply repair the property; she has altered the property by converting unusable space into another room. The whole of the cost is disallowable.

Example 5:

Helena has a property business. She is advised that the boiler in one property needs to be replaced.

Helena is told that she cannot simply replace the boiler with one of the same type because since 1st April 2007 it has been a legal requirement (in England and Wales) that all gas boilers installed must be a condensing model. In addition, the old boiler was rated in imperial units and boilers are now measured in the equivalent metric unit.

Helena chooses to replace the boiler with a condensing boiler that is the closest equivalent in capability.

The new boiler is smaller and has to be installed on a different wall, so that it can condense outside. Helena takes the opportunity to install additional kitchen units as tenants have commented about the lack of storage space.

Although the tank is slightly larger, the reality is that Helena has simply used the modern equivalent of the original tank. The result is that the cost of the boiler is still revenue expenditure. The cost of the additional kitchen units is an improvement and not an allowable expense.

End of examples.

There are many examples that demonstrates that any cost associated with a property falls into:

Capitalised expenditure (adds value or is new to the property).

Revenue expenditure to reduce tax (direct replacement / repair).

Non capital / revenue expenditure (fridge example).

HMRC remind you that it is not the responsibility of your accountant to understand or apply the above rules.

14

You can easily pay no tax on your property investment if you follow these simple steps:

o Buy Below Market Value (say 75% or lower).

o Refurb that is repairs / replacement to reduce your tax.

o Re-finance the property to pull money out and do the next property.

I used this strategy for many years until I decided to develop properties. It was a sound way of minimising my tax liability and to generate more cash for bigger projects, which I am now working on.

15

ALLOWABLE ONGOING EXPENSES Keeping expenditure receipts

It is imperative that you keep all receipts. These ought to be recorded on a spreadsheet or accounting software, whilst making sure that you check that the bank balances in your spreadsheet / accounting system agrees at all times.

There will be times when you need to use cash to buy goods and services but these ought to be kept to a minimum to make it easier for you to account for the costs.

The following types of costs may be accounted for to help you reduce your tax. This list is not complete but it gives you an idea of what costs may be accounted for in your limited company.

o Repairs: exterior and interior painting, damp treatment, stone cleaning, roof repairs, furniture repairs

o Rents and leases

o Business rates

o Council tax

o Water rates

o Ground rents

o Insurance

o Maintenance: cleaning, gardening

o Loan interest and finance charges

o Legal and professional costs

o Utilities (if the tenants are not paying for them)

o Stationery

o Phone

o Travel: to the house and associated companies managing the property

o Car journeys

16

o Train journeys

o Flights

o Hotels

o Subsistence (whilst away on business)

o Environment energy saving technologies

o Membership and subscriptions (Property related or management related)

o Education for employees

o Claiming mileage

17

WHAT IS NEXT Take action, go!!!

Now you are set, motivated and ready to earn your millions by buying lots of property. Maybe, before you do anything go and find your local property investment networking meeting and start your education.

Please drop me a line with any questions that you may have in relation to property investing (especially the geeky numbers with my many geeky spreadsheets). Email is [email protected].

You can also contact me as follows:

Web: www.optimiseaccountants.co.uk

Facebook: https://www.facebook.com/OptimiseAccountants

Twitter: https://twitter.com/Si_Accountant

Good luck and have fun

Simon Misiewicz ACCA MBA

Optimise Accountants

Helping you make more money and profit from property

18

REFERENCES:

(1) http://moneyfacts.co.uk/news/mortgages/rise-in-house-prices-during-may30513/

(2) http://moneyfacts.co.uk/news/mortgages/mortgage-applications-increase-by-5421513/

(3) http://www.marketoracle.co.uk/Article4926.html

(4) http://www.guardian.co.uk/society/2012/may/17/government-failing-homes-built

(5) http://www.propertyinvestingquickstart.co.uk/

(6) http://www.progressiveproperty.co.uk/

(7) http://www.thisismoney.co.uk/money/mortgageshome/article-1596759/Ten-tips-buy-let.html

(8) https://www.moneyadviceservice.org.uk/en/articles/investing-in-property

(9) http://www.hmrc.gov.uk/briefs/income-tax/brief0513.htm

(10) http://www.hmrc.gov.uk/briefs/income-tax/draft-guidance.pdf

(11) http://www.hmrc.gov.uk/manuals/bimmanual/bim46910.htm

(12) http://www.accountingweb.co.uk/press/hmrc-brings-manuals-date-repairs-expenditure

(13) http://www.hmrc.gov.uk/manuals/pimmanual/PIM3010.htm

(14) http://www.hmrc.gov.uk/manuals/pimmanual/PIM2020.htm