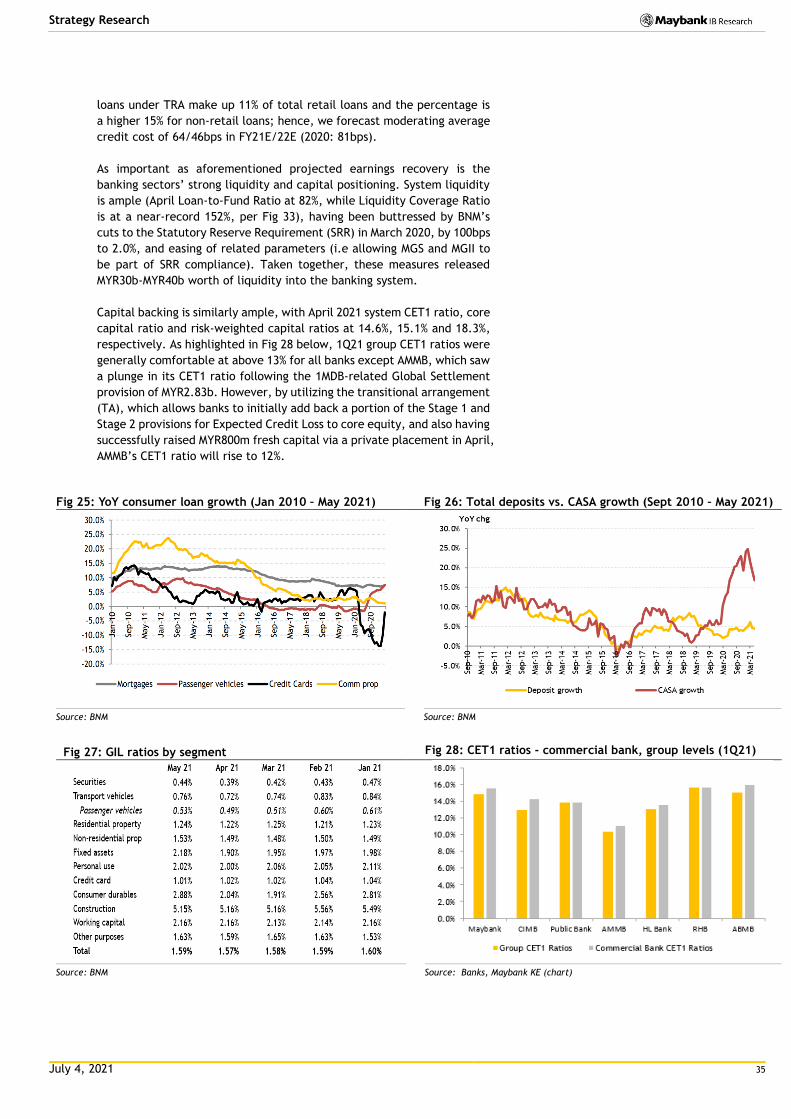

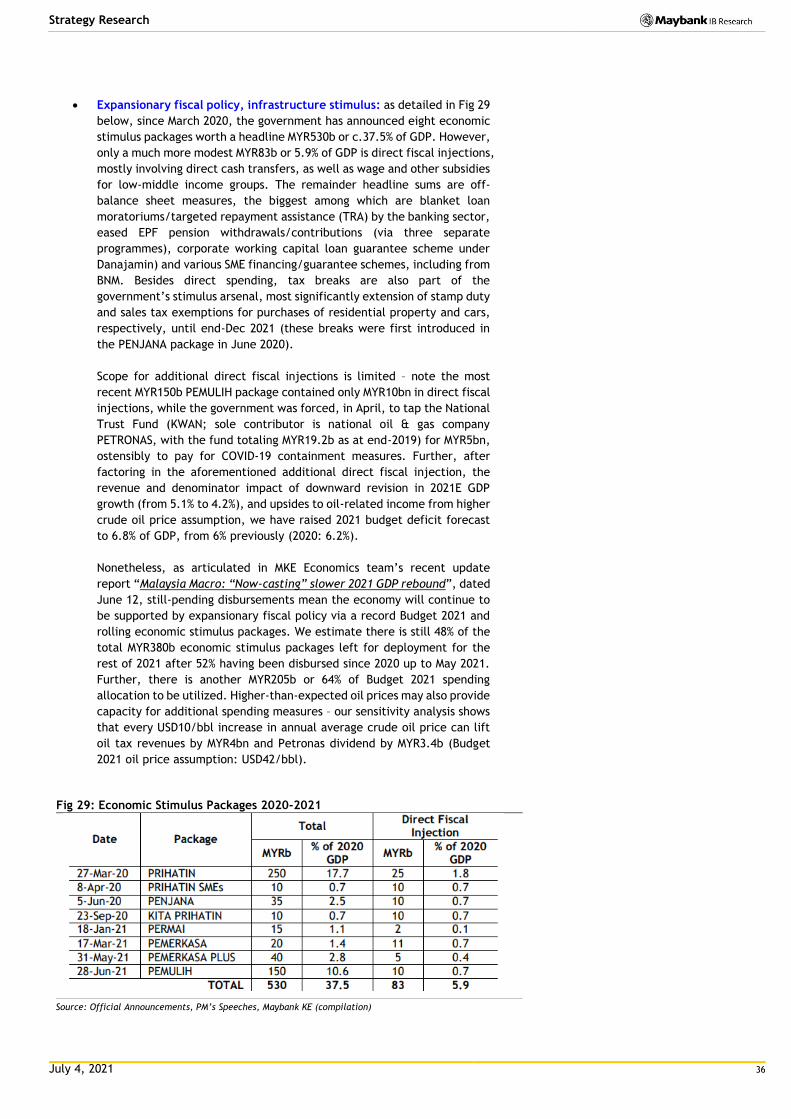

Embed Size (px)

Citation preview

July 4, 2021

ST

RAT

EG

Y

Mala

ysi

a

THIS REPORT HAS BEEN PREPARED BY MAYBANK INVESTMENT BANK BERHAD

SEE PAGE 114 FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS PP16832/01/2013 (031128)

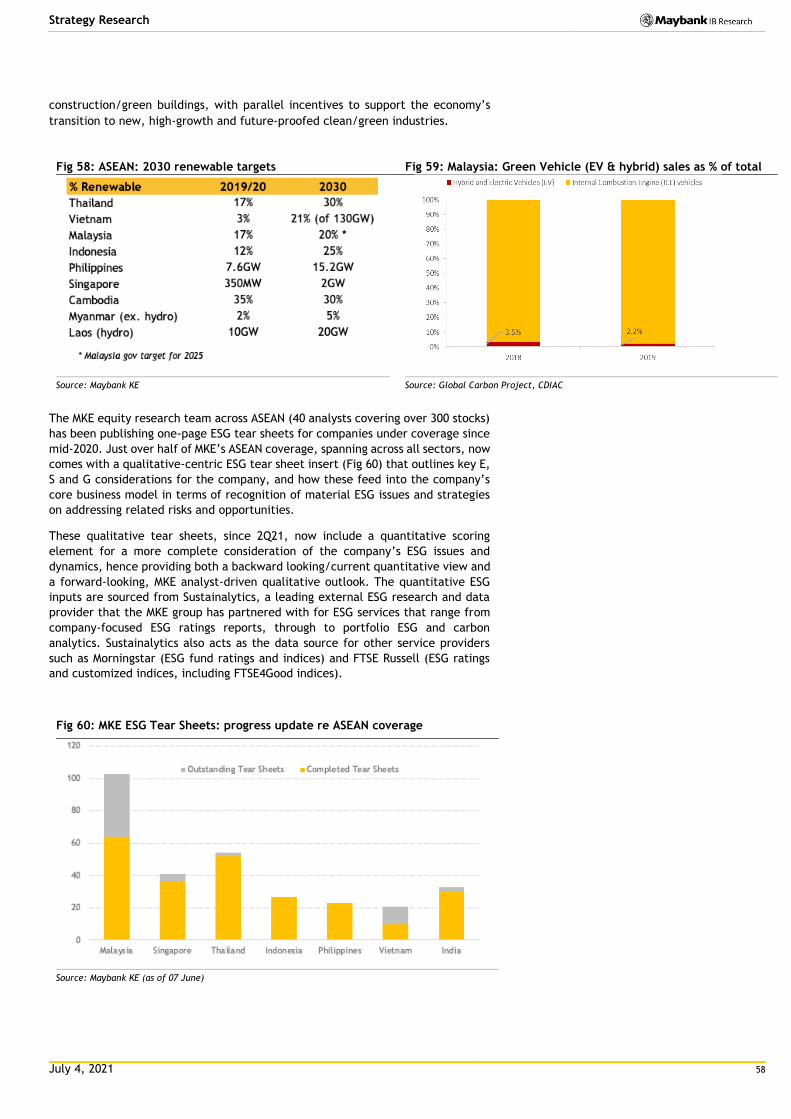

Malaysia 2H21 Outlook and Lookouts

Silver linings amidst the pandemic cloud

For Malaysia macro, we reiterate our revised 2021 real GDP growth

forecast of +4.2% (+5.1% previously); 2020: -5.6%) due to tighter restriction

in May 2021 and lockdown since June 2021. We cut growth forecasts for

non-manufacturing sectors on the supply side, and private expenditure on

the demand side. Global economic recovery plus higher commodity ASPs

cushioned downside to GDP via upgrades in manufacturing and external

trade growth forecasts. Sizeable positive impulse from economic stimulus

– and direct fiscal injection – remains given the additional PEMULIH

package that adds to the yet to be utilized parts of earlier stimulus and

Budget 2021 spending allocation, thus upward revision to Government

consumption expenditure growth and unchanged outlook with regards

anticipated public investment rebound.

We raised 2021 budget deficit/GDP forecast to 6.8%, from 6.0%, and

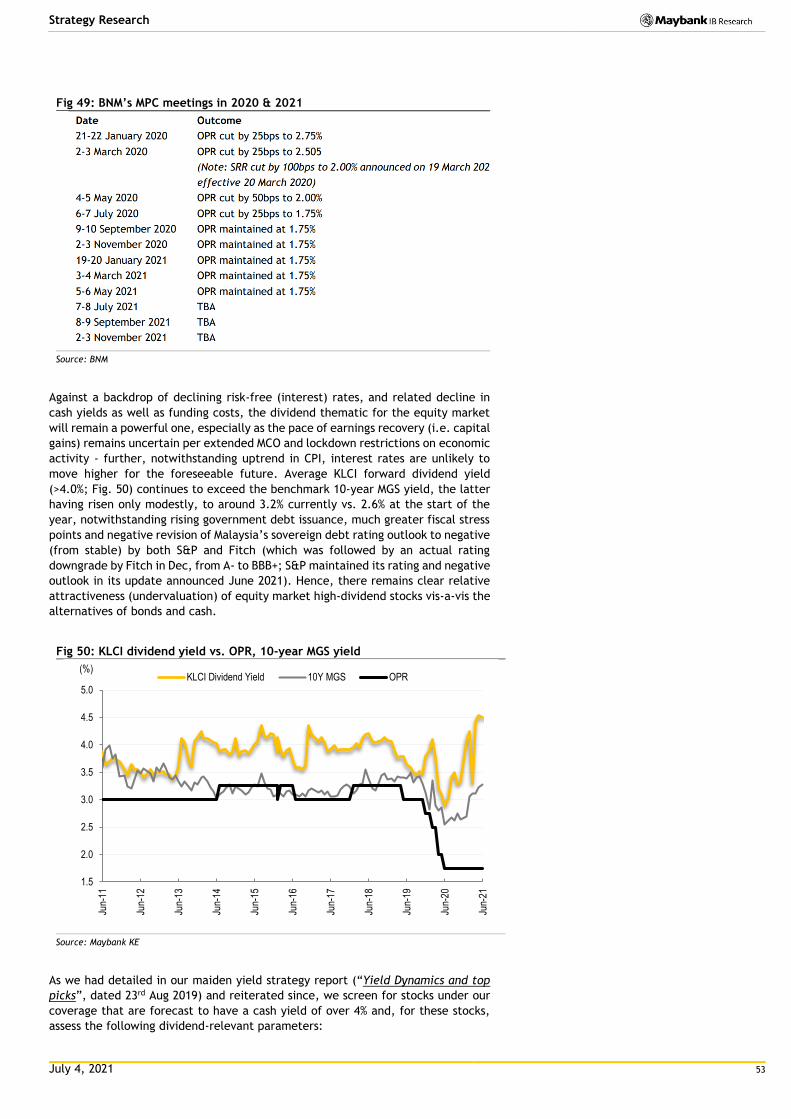

expect no change in current record-low 1.75% Overnight Policy Rate (OPR).

A silver lining amid the pandemic cloud is the acceleration in COVID-19

vaccinations hence rising share of population fully-vaccinated, which is

one of the conditions for exit from the current full lockdown,

easing/lifting of restrictions, and re-opening of the economy.

For Malaysia equities, bucking our bullish expectations, as articulated in

our 2021 Strategy report (“Malaysia 2021 Market Outlook: Goldilocks makes

a comeback”, dated Dec 14), of sustained recovery following broad uptrend

over 4Q20, the KLCI’s momentum stalled into Jan, brought up short by the

twin shocks of a renewed national Movement Control Order (MCO) and

Proclamation of Emergency. Fiscal limitations and sustained institutional

selling have also weighed negatively. However, while the path to full re-

opening from the current lockdown (since June 1) looks to be an extended

one, corporate earnings have proven resilient, and rapidly rising vaccination

rates should allow investors to refocus on equities-supportive positives into

4Q21 i.e. accelerated earnings recovery, continued albeit moderated fiscal

and monetary support, ample liquidity, commodities price recovery and

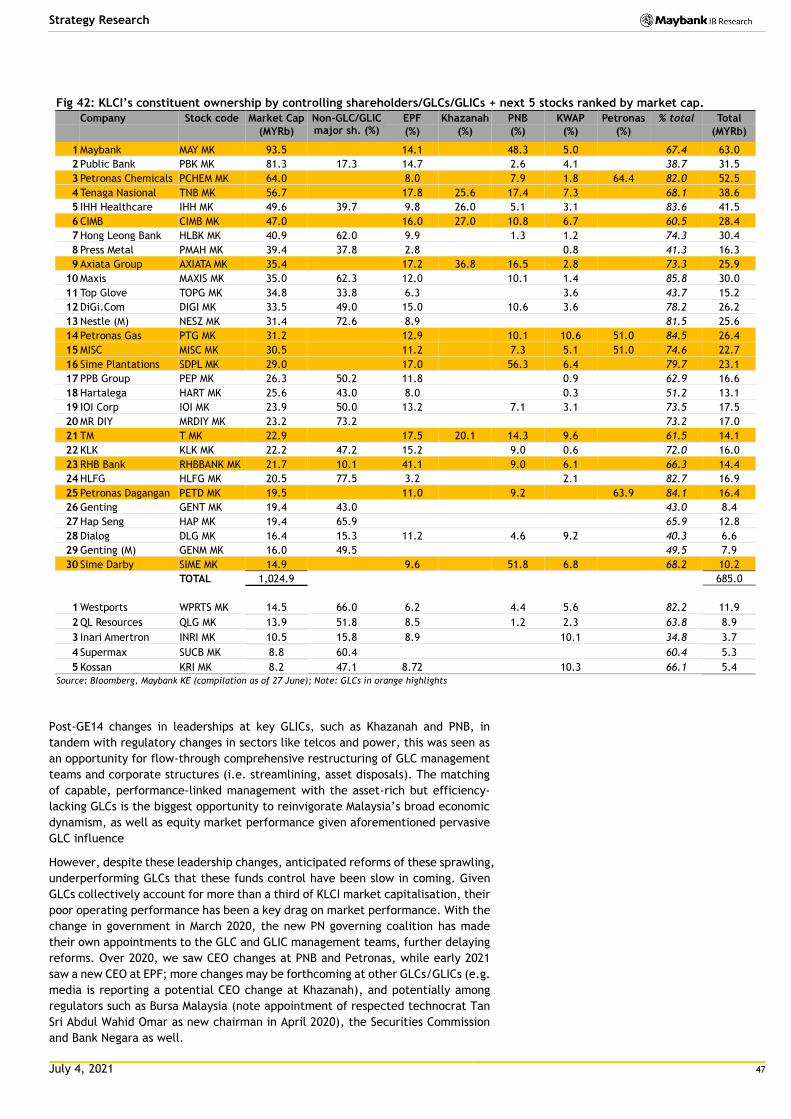

relative attraction vs. fixed income. Re thematics, GLC restructuring is

unlikely to gain traction (though revival of the Axiata-DiGi merger is

welcome) given backdrop of political volatility and continuing GLC/GLIC

management changes. The dividend yield and supply chain relocation

thematics offer much greater structural investability, as does sustainability

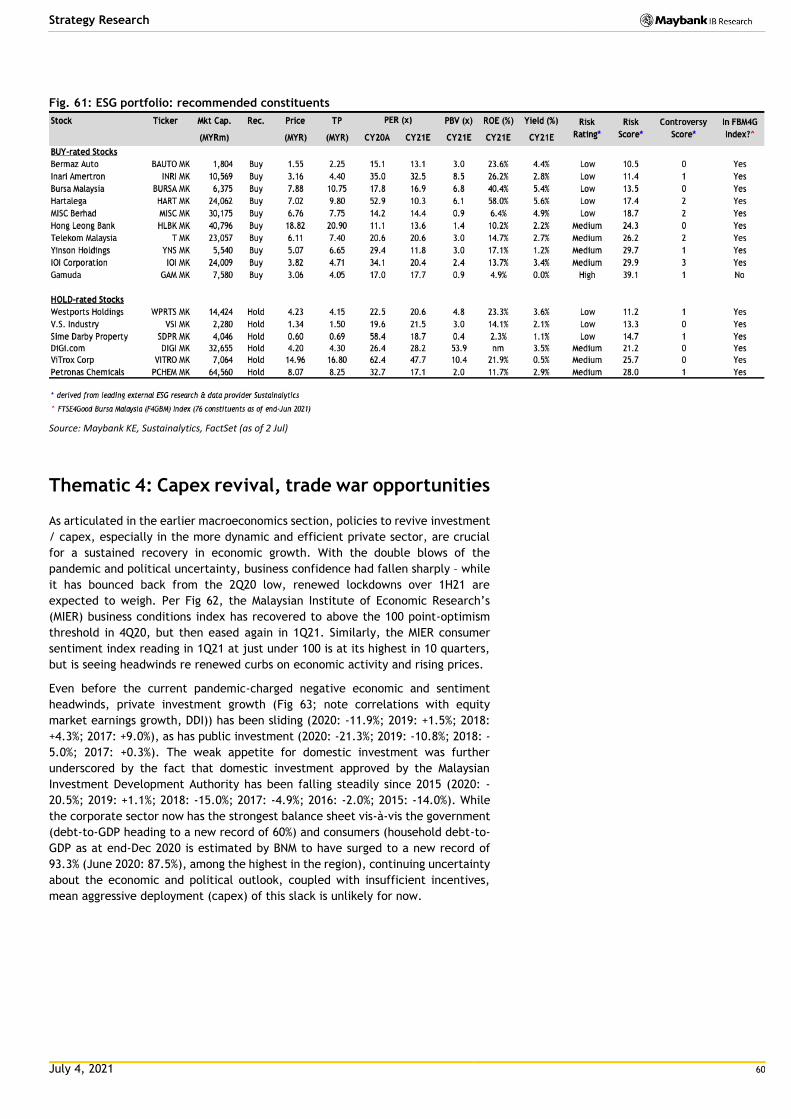

/ ESG investing, as detailed in our recently-published Malaysia ESG

Compendium (“Sustainability: No longer optional”, dated April 8).

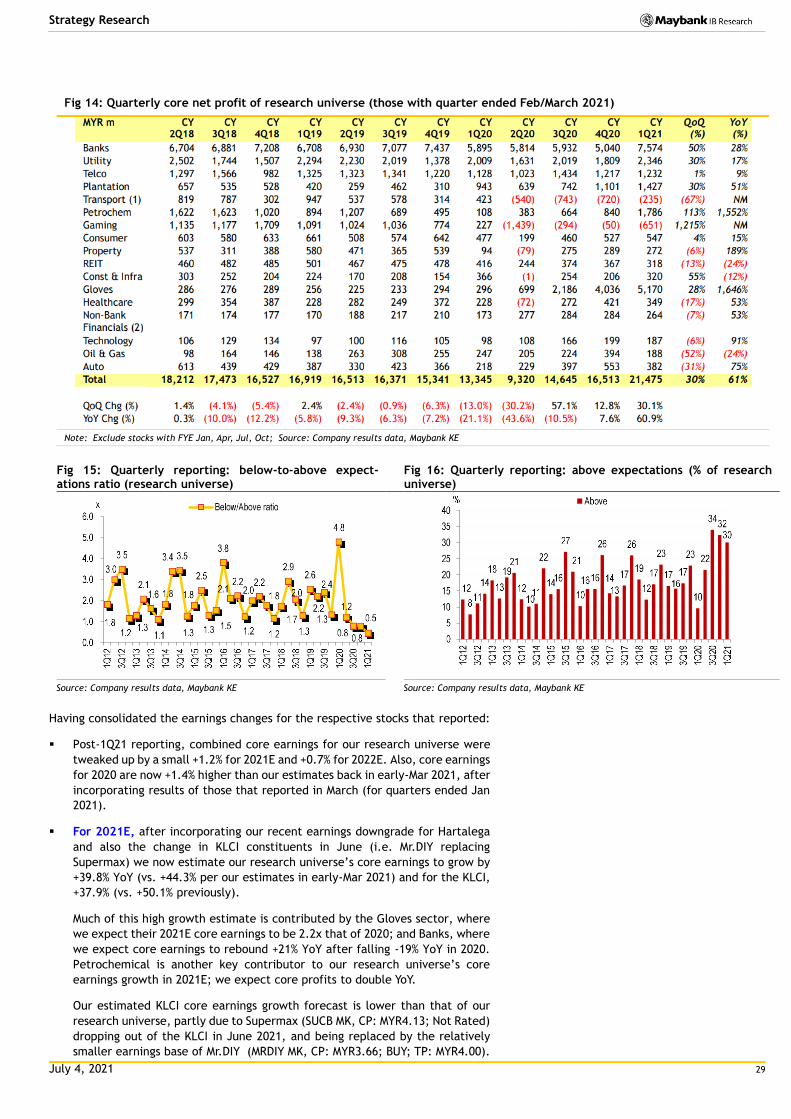

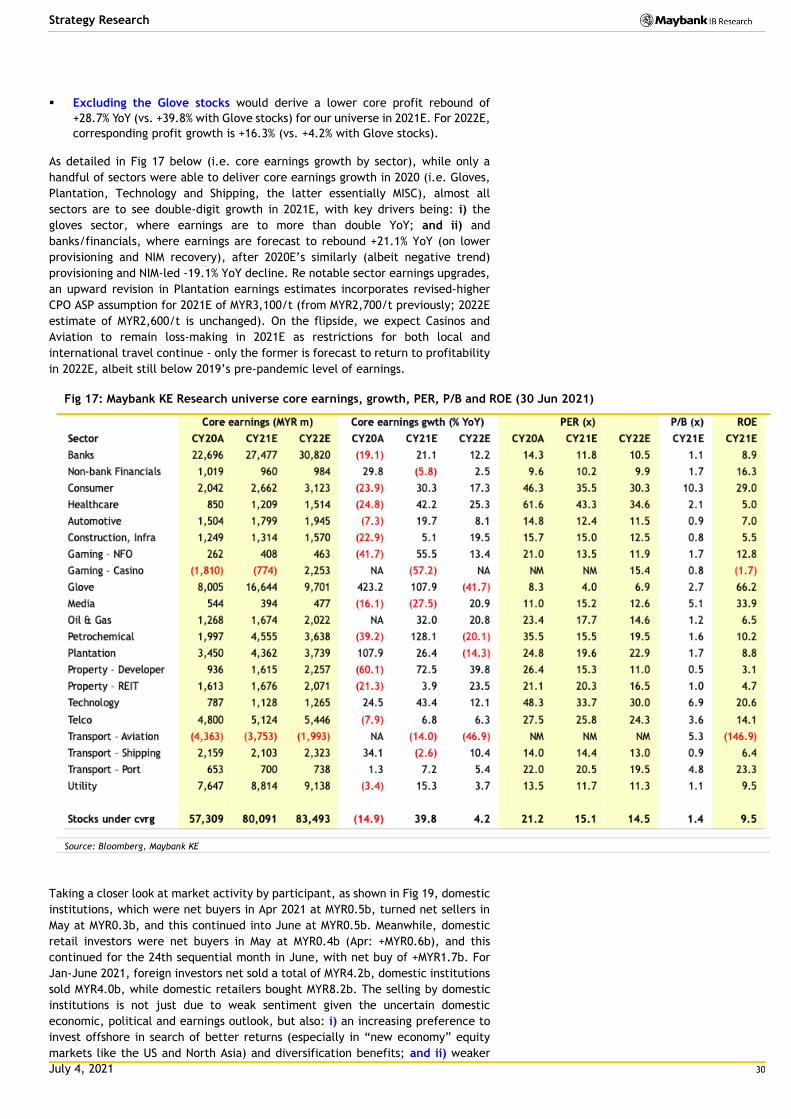

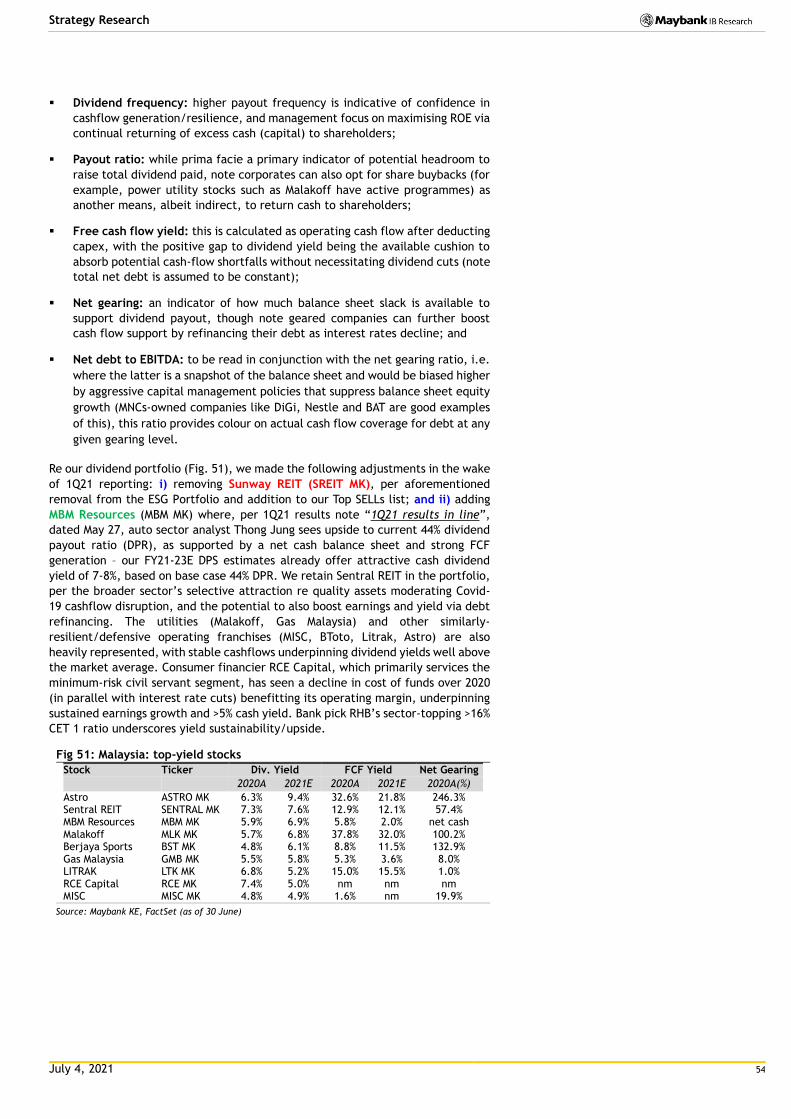

In the wake of 1Q21 reporting, we continue to expect the KLCI to see sharp

earnings recovery in 2021 (2020/2021F: -11.9%/+49.0%; if excluding glove

stocks, adjusted 2021F: +35% YoY) after three straight years of earnings

contraction. However, in factoring in extended NRP and political risks, we

moderate end-2021 KLCI target to 1,720 (15x forward earnings, -0.5 SD vs.

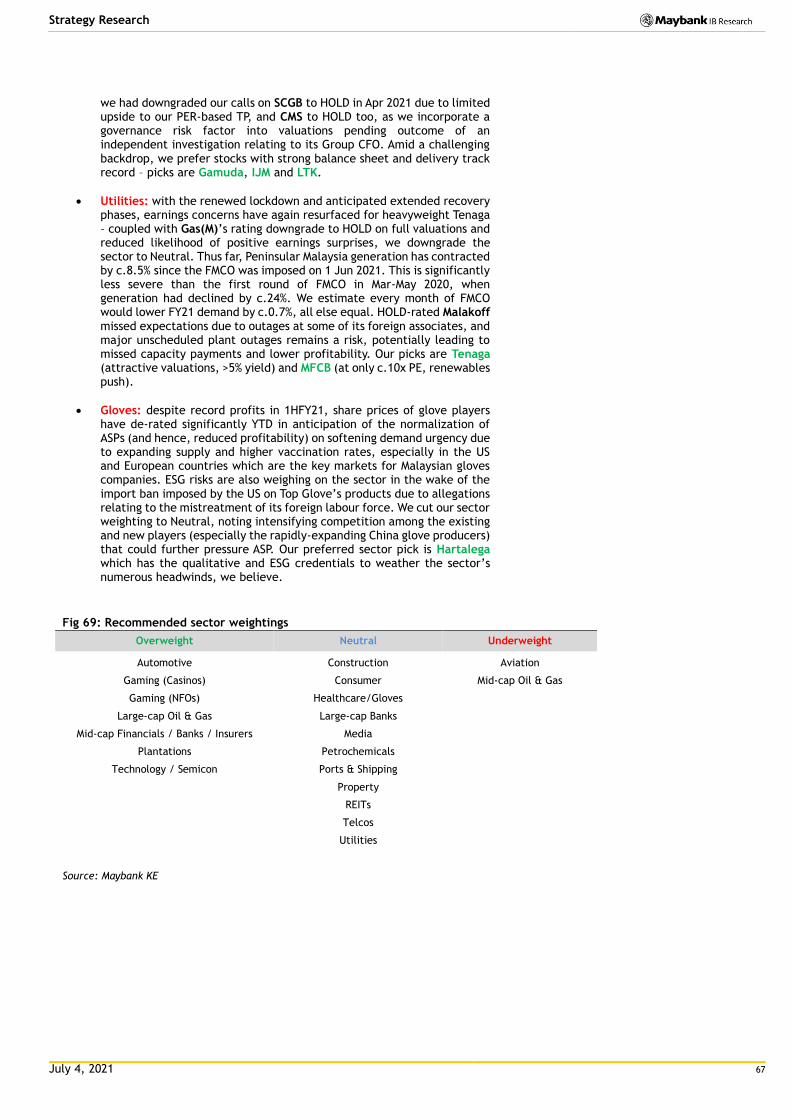

mean), from 1,830 (16x, in line with historical mean) previously. Re sector

positioning changes, we downgrade Construction (preferred sector picks are

Gamuda, IJM), Utilities (Tenaga, MFCB) and Gloves (Hartalega) to Neutral

(Fig 69), and raise Gaming to overweight (GENM, BST). We continue to like

Mid-cap Financials (HLBK, RHB, Allianz), Tech/Semicon (Inari, Greatech),

Large-cap Oil & Gas (Dialog, Yinson), Plantations (KLK, BPlant) and Auto

(BAuto). We are selective on Telcos (Telekom), REITs (Axis), Property (SP

Setia) and Logistics (MISC); we stay Underweight Aviation and Mid-cap O&G.

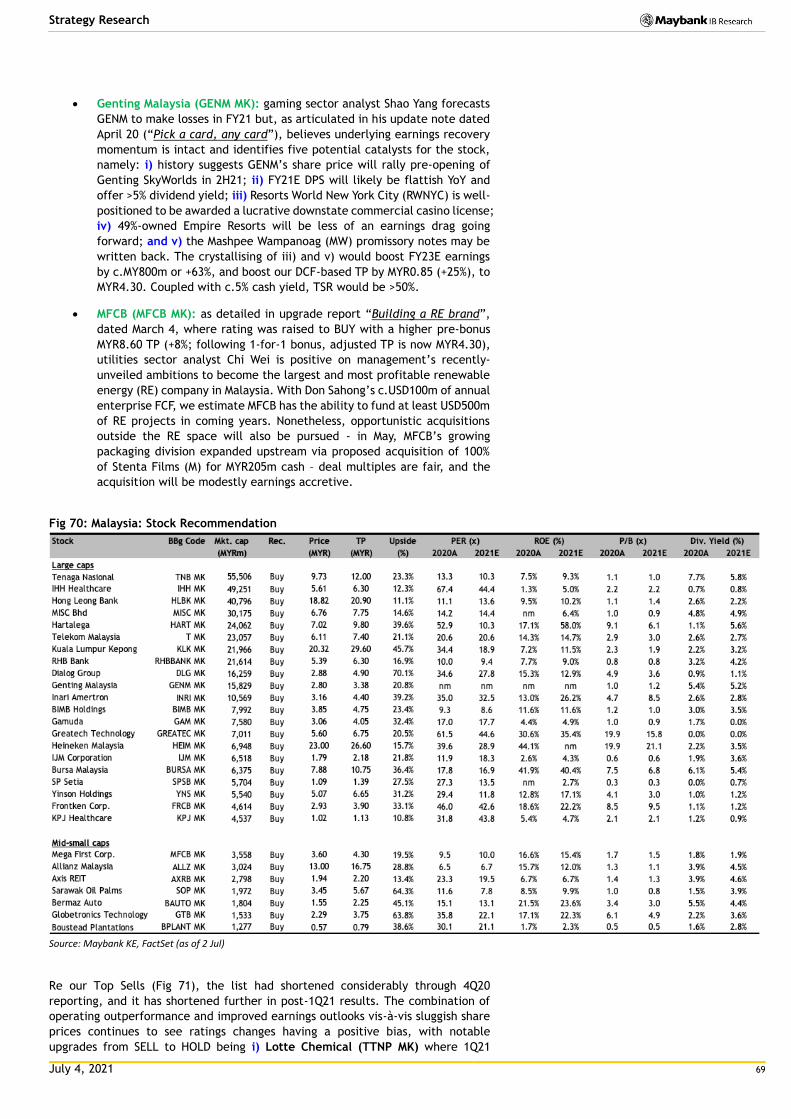

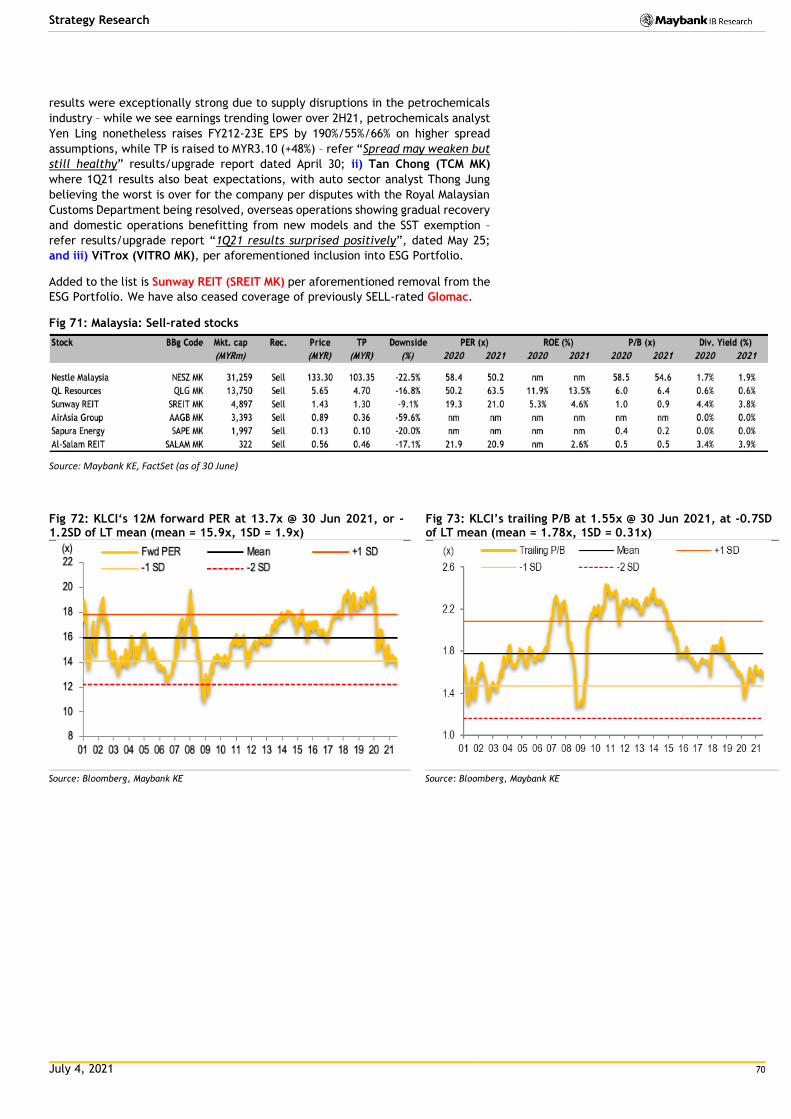

Top BUYs (Fig 70) and Top SELLs (Fig 71) are detailed on pages 68-70,

recommended ESG stock picks are per Fig 61, while conviction dividend picks

(providing 5-9% cash yield) are in Fig 51.

Analysts

Suhaimi Ilias (Economics)

(+603) 2297 8682

Anand Pathmakanthan (Equity Strategy)

(+603) 2282 3730

Wong Chew Hann (Equity Research)

(+603) 2297 8686

Malaysia Economics, FX, Fixed Income and

Equities Research Teams

(please refer to backpages for the full list)

July 4, 2021 2

Strategy Research

Table of Contents

Malaysia Macro Update ................................................................................................................ 3

2H 2021 Outlook and Lookouts .................................................................................................... 21

Thematic 1: GLC Restructuring .................................................................................................... 46

Thematic 2: Interest rates vs. dividend yields ................................................................................. 52

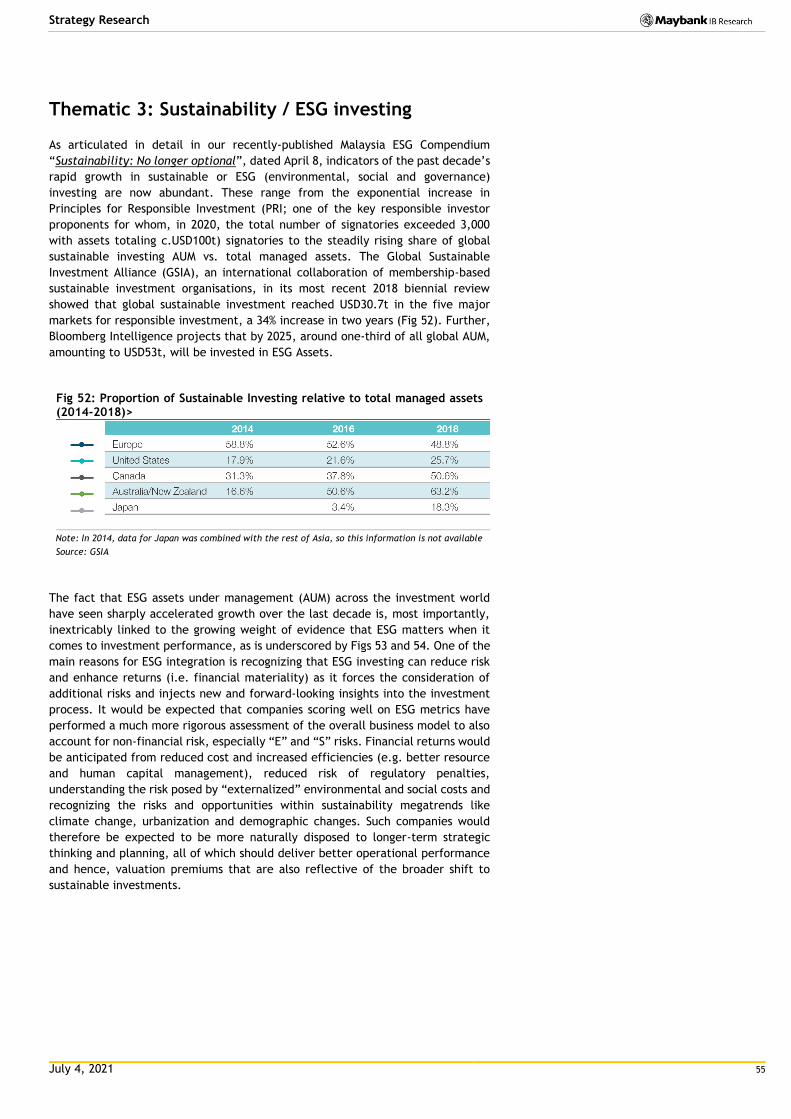

Thematic 3: Sustainability / ESG investing ...................................................................................... 55

Thematic 4: Capex revival, trade war opportunities ......................................................................... 60

Balanced positioning, with ESG and yield overlays ............................................................................ 65

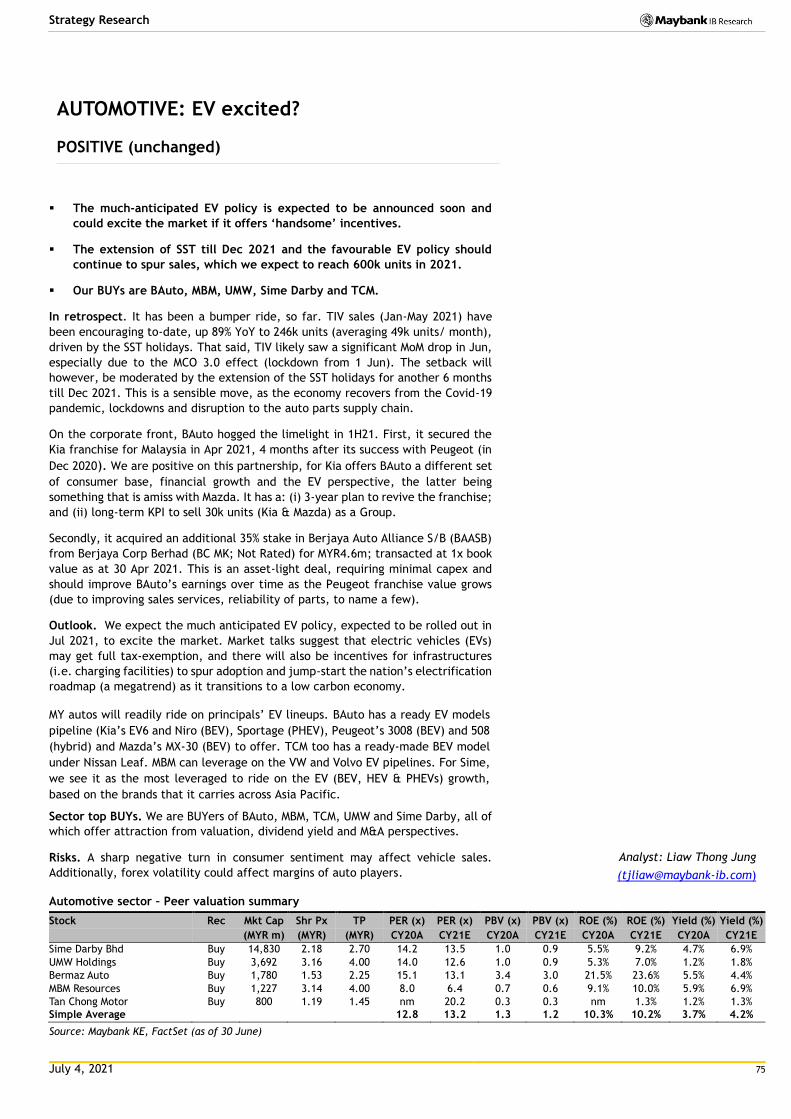

AUTOMOTIVE: EV excited? .......................................................................................................... 75

AVIATION: Worst may be over but still tough ................................................................................... 77

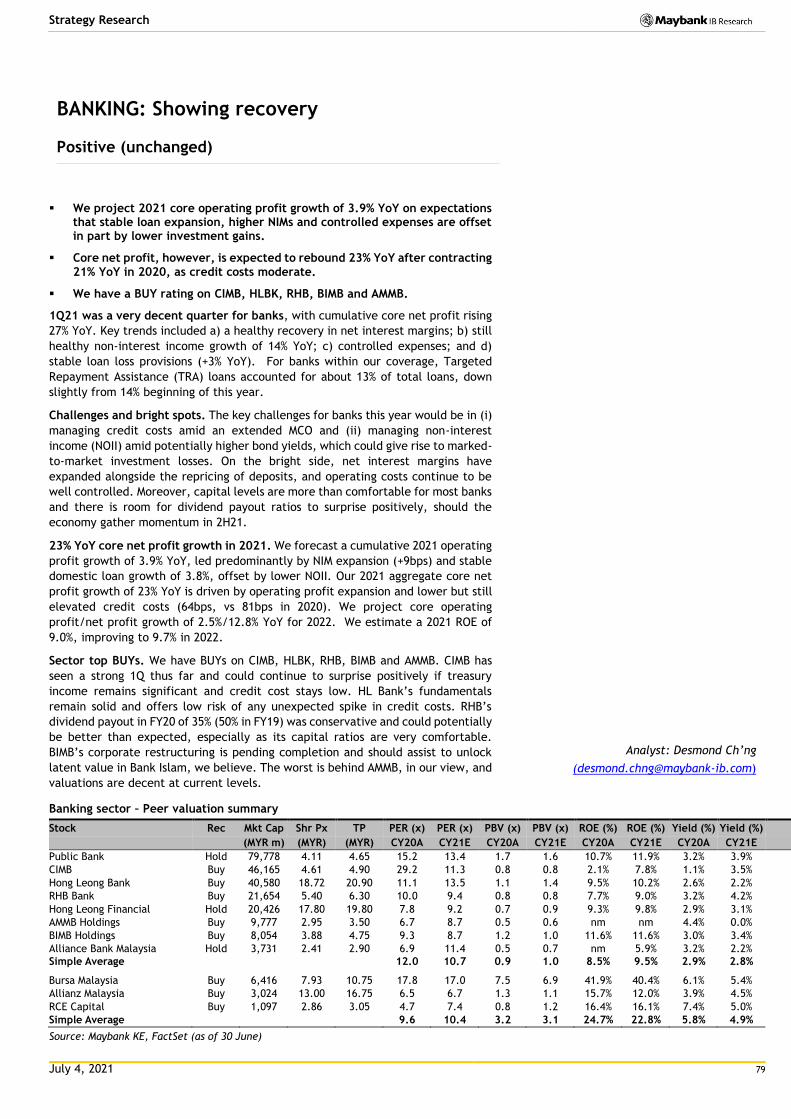

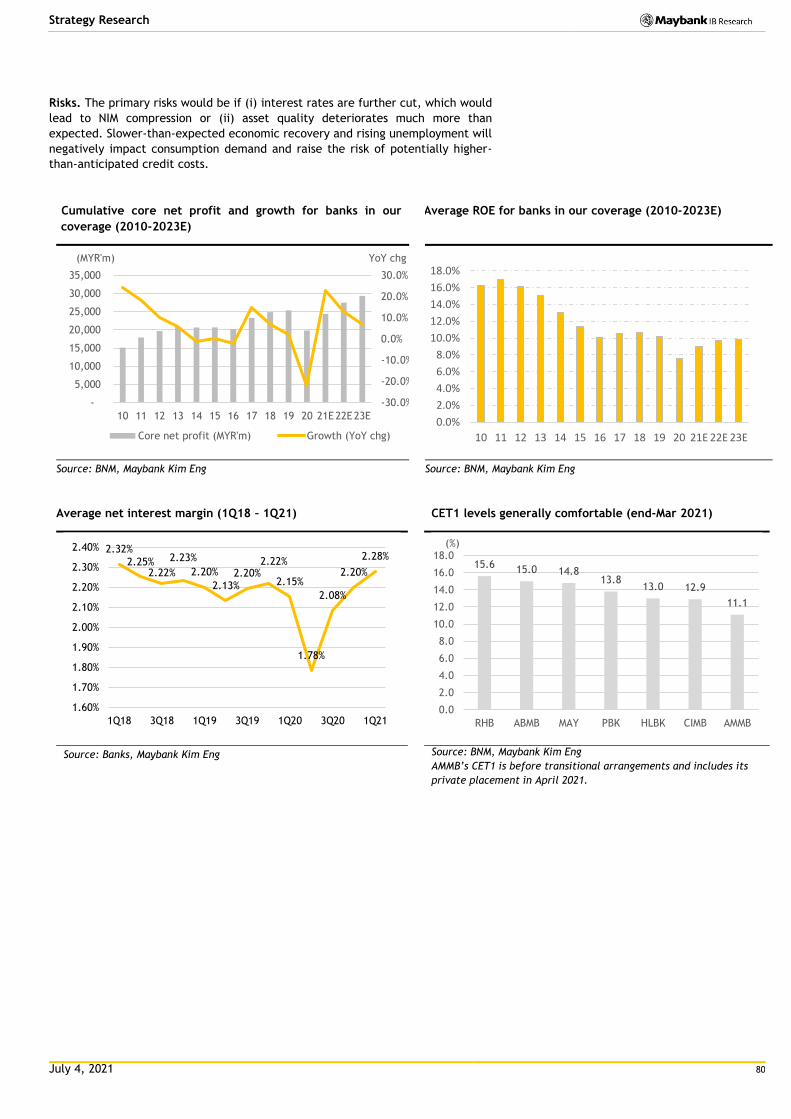

BANKING: Showing recovery ........................................................................................................ 79

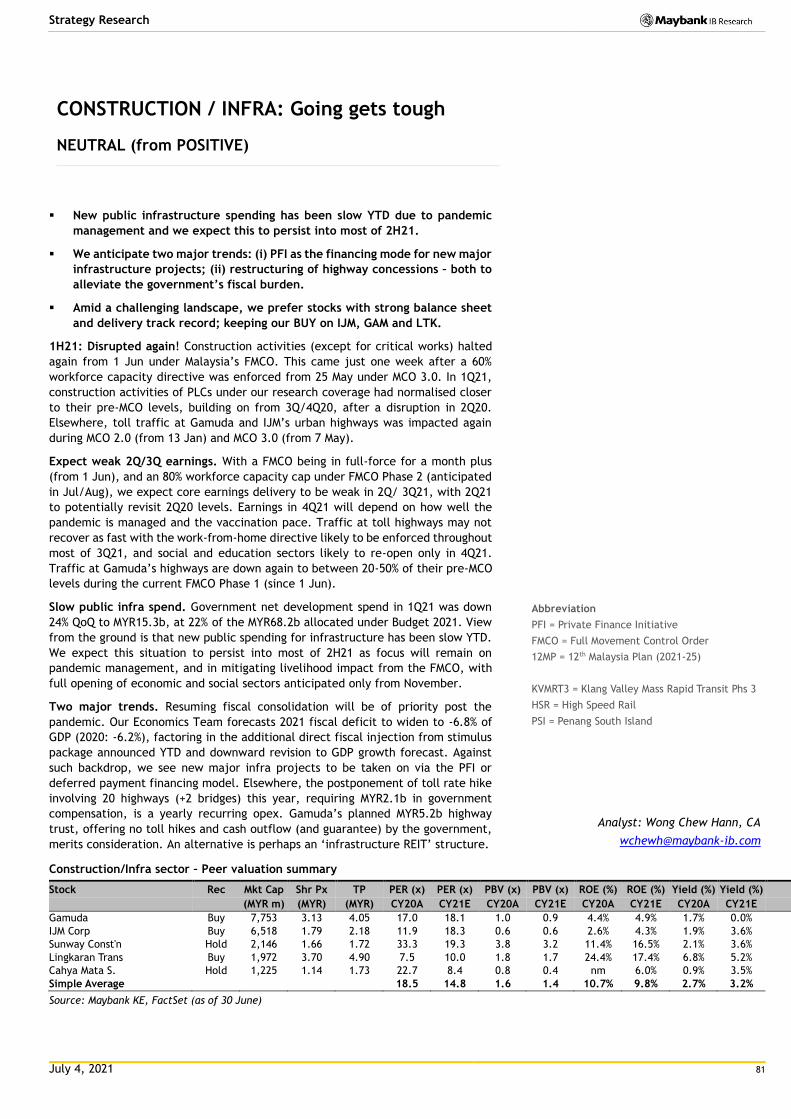

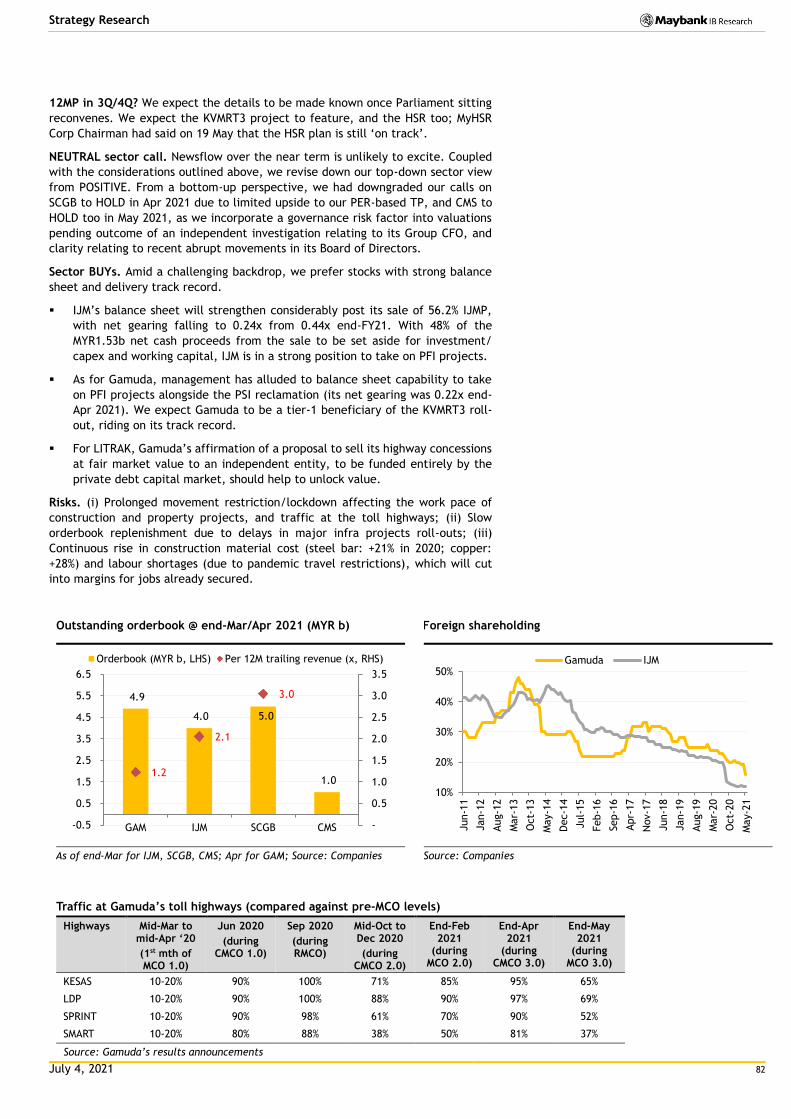

CONSTRUCTION / INFRA: Going gets tough ...................................................................................... 81

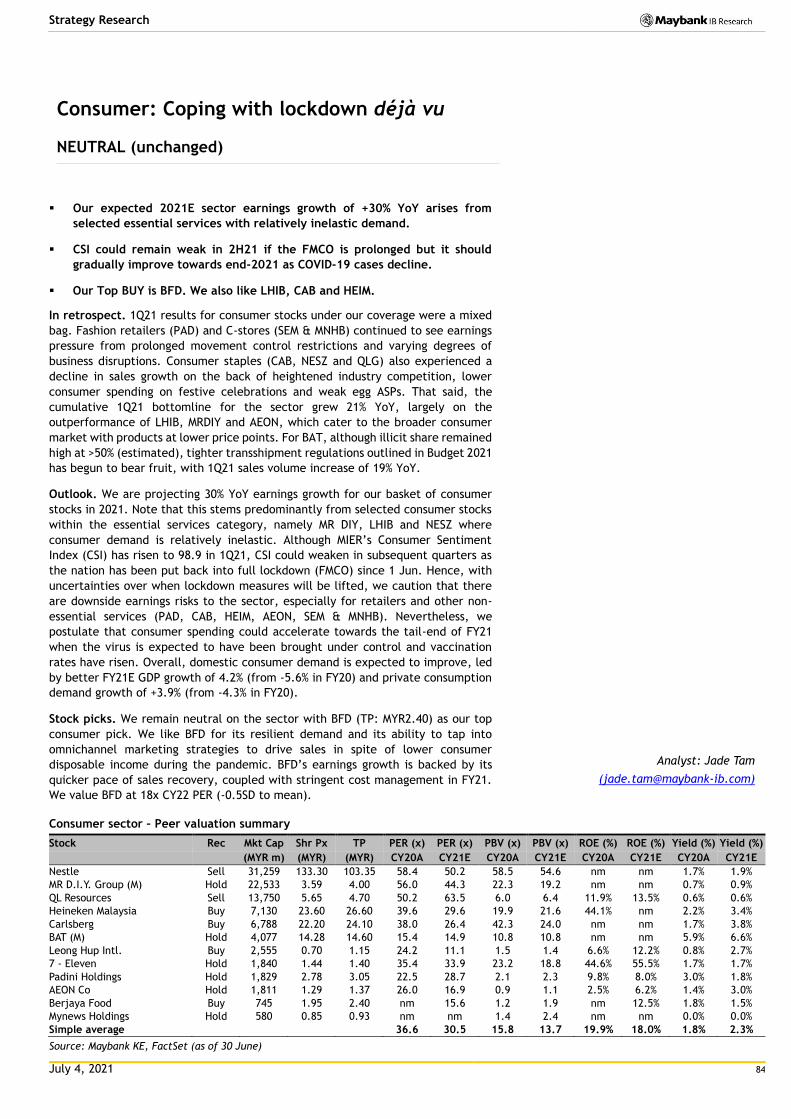

Consumer: Coping with lockdown déjà vu ...................................................................................... 84

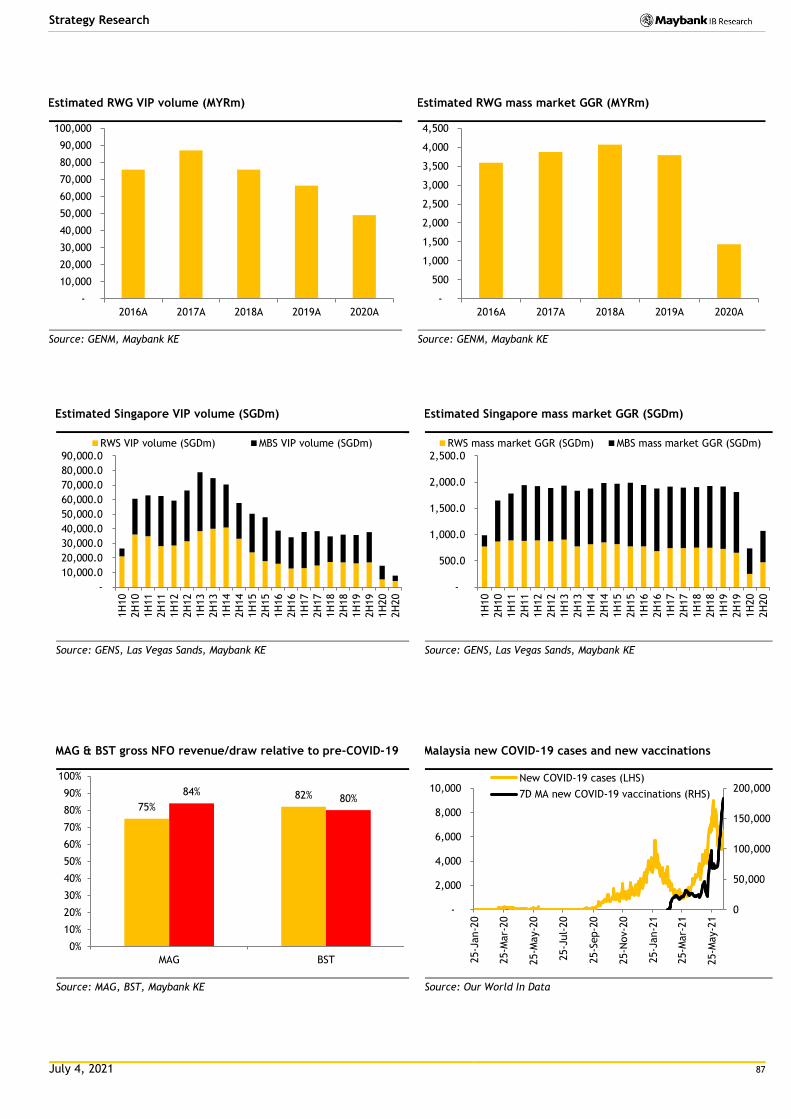

GAMING: Vaccination is key ......................................................................................................... 86

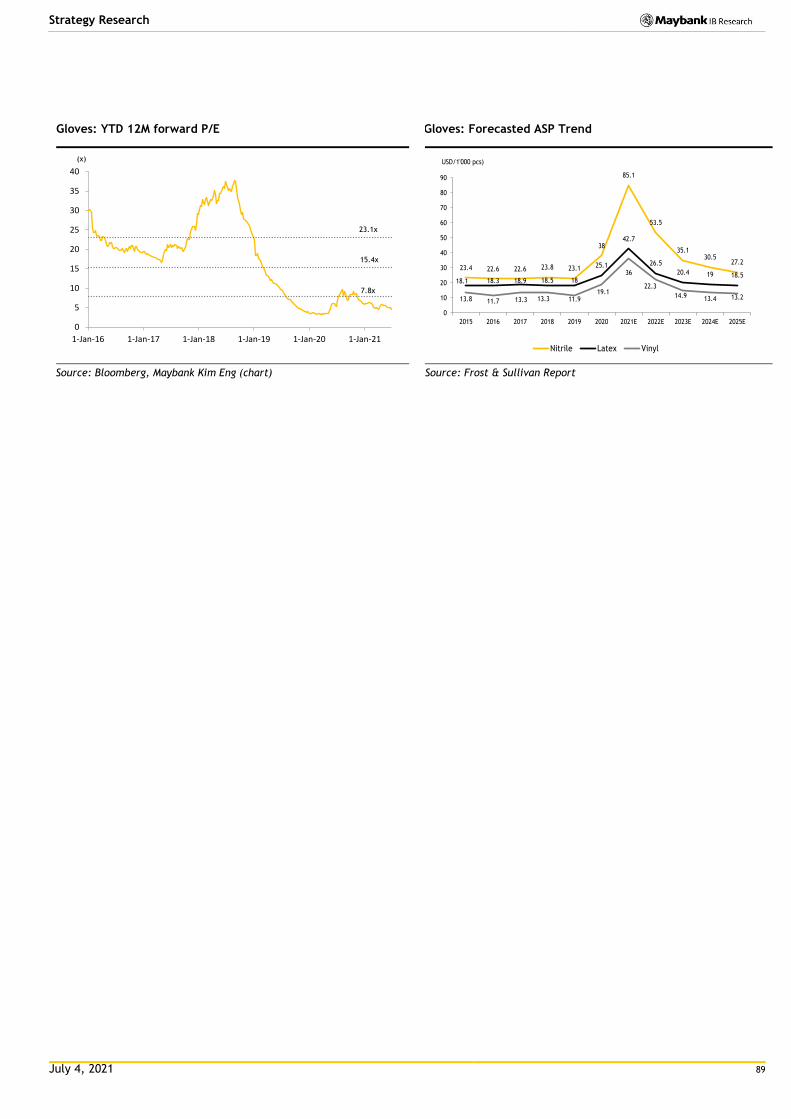

GLOVES: Entering a phase of declining ASP trend ............................................................................. 88

Media: We have growth! ............................................................................................................. 90

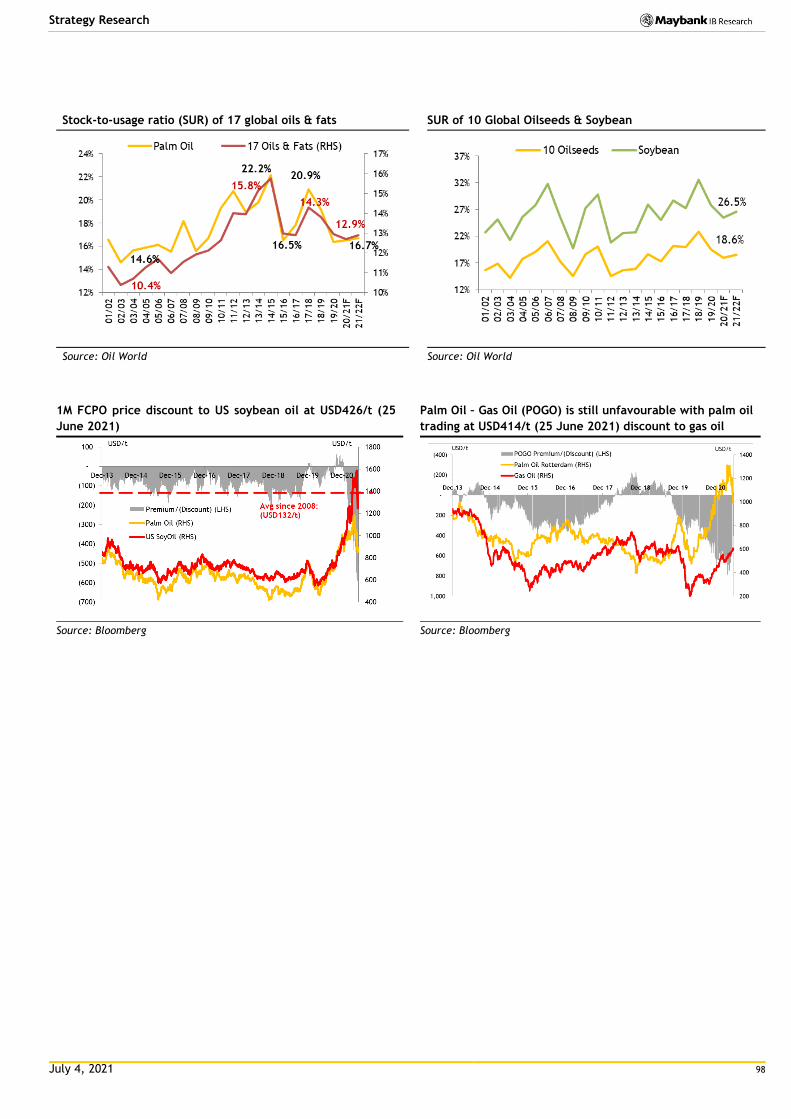

OIL & GAS: Commodity super-cycle? .............................................................................................. 92

PETROCHEMICAL: A Regression to the Mean .................................................................................... 94

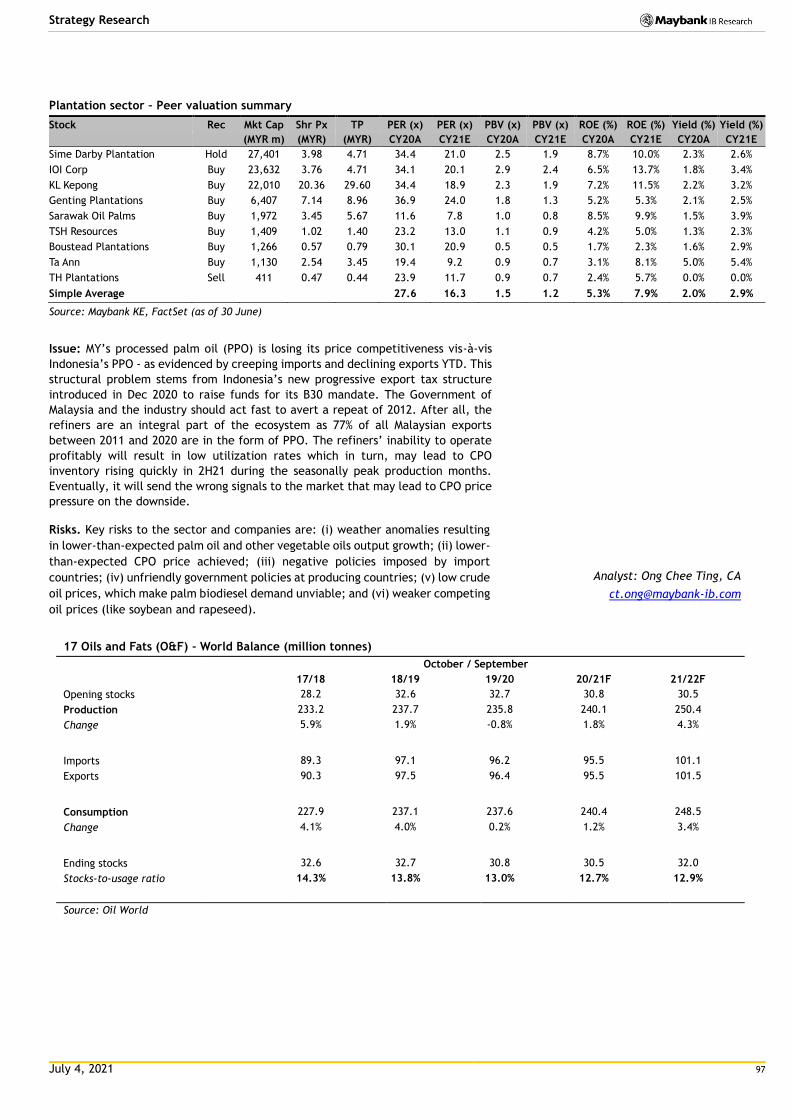

PLANTATION: Higher HoH output in 2H21 to buffer anticipated weaker CPO ASP ..................................... 96

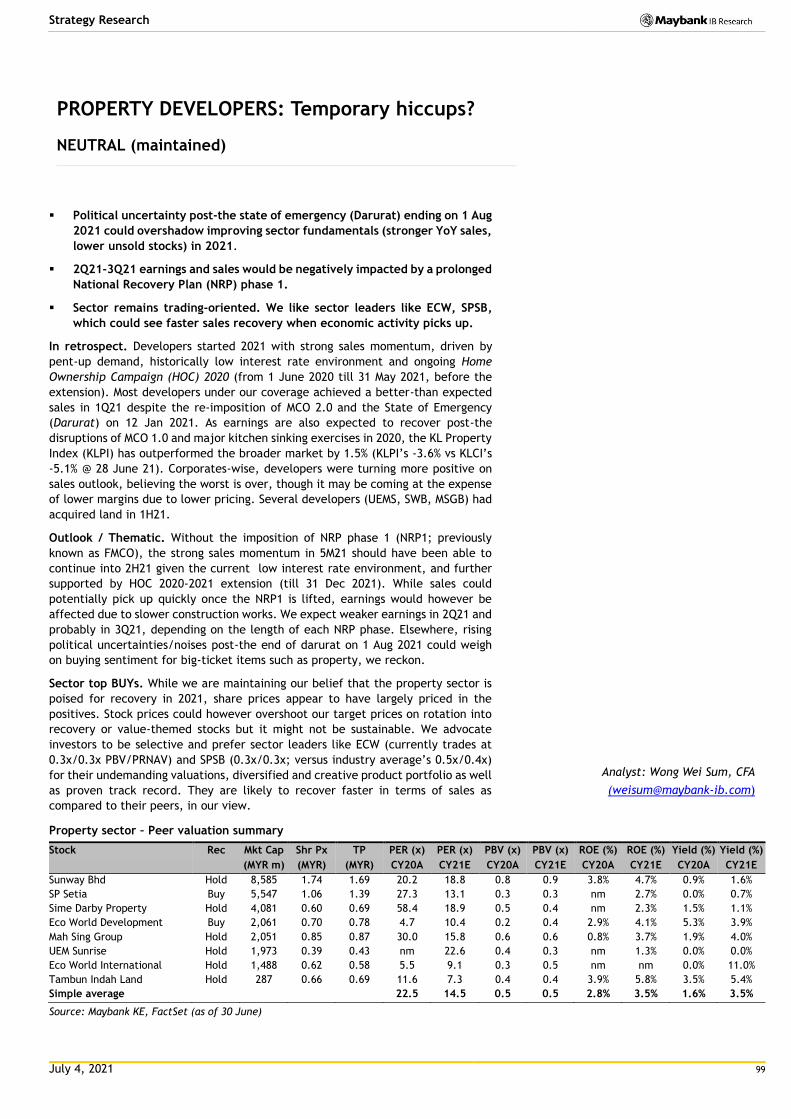

PROPERTY DEVELOPERS: Temporary hiccups? .................................................................................. 99

REITs: Awaiting recovery .......................................................................................................... 101

SHIPPING & PORTS: A Mixed Bag ................................................................................................. 103

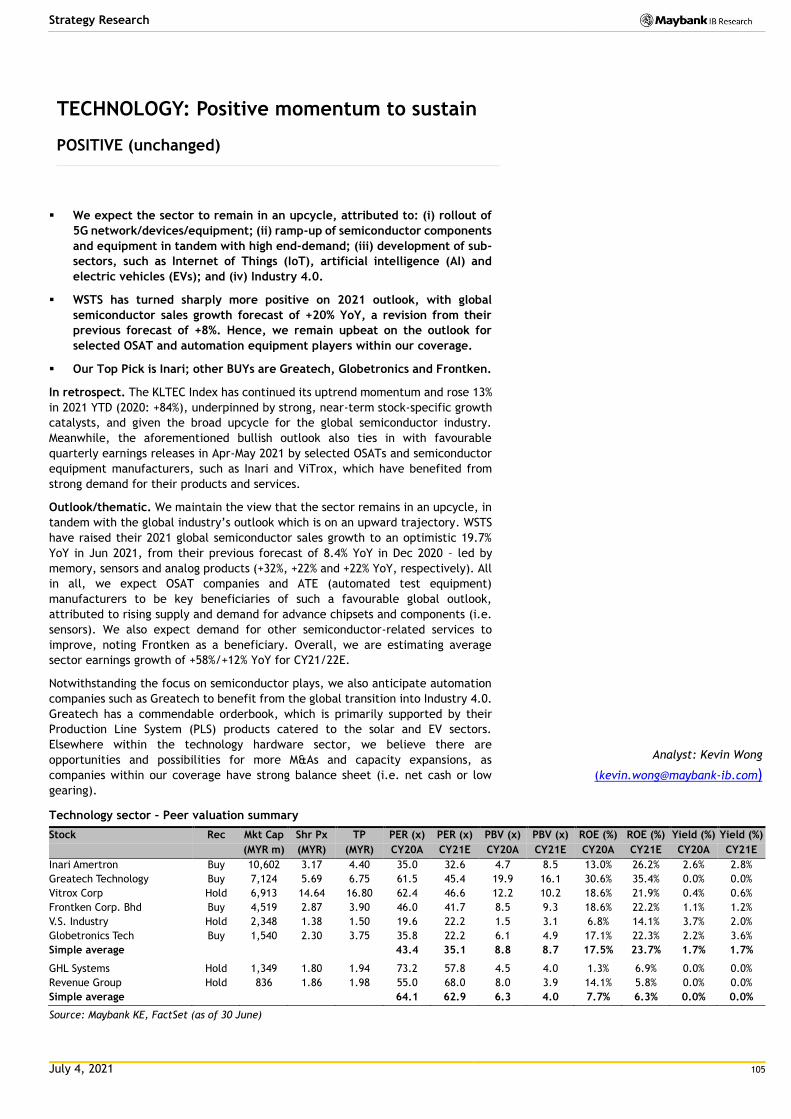

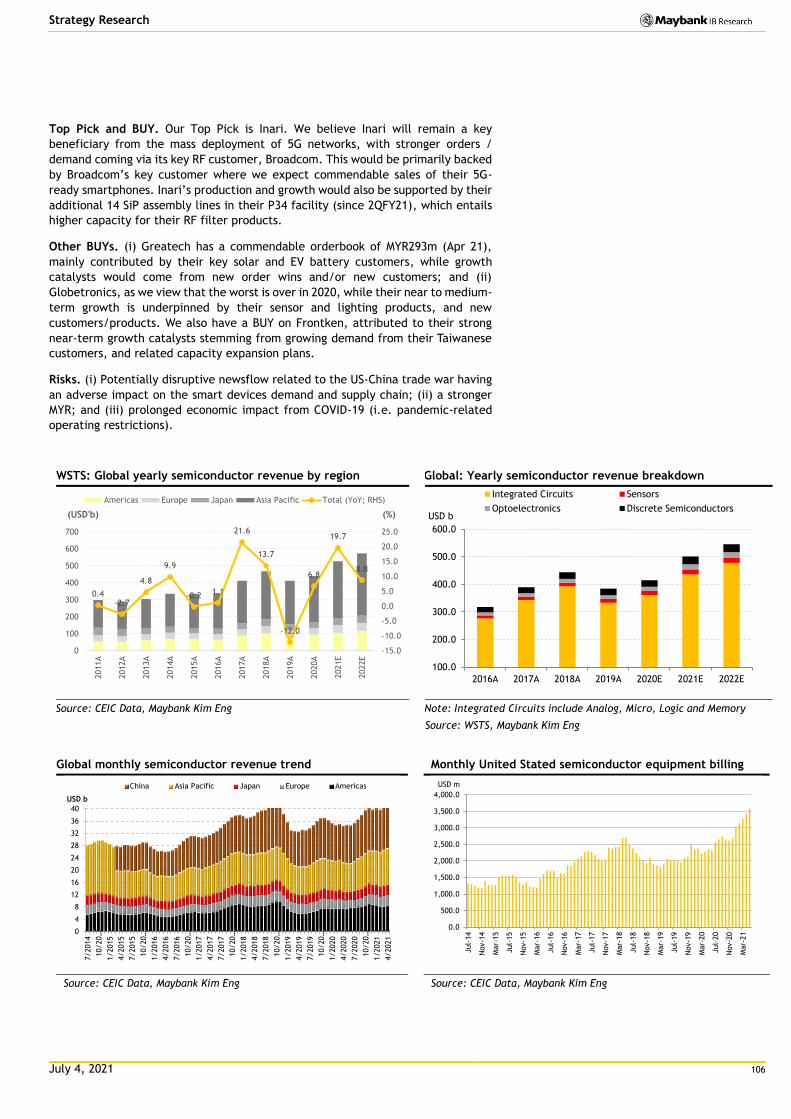

TECHNOLOGY: Positive momentum to sustain ................................................................................ 105

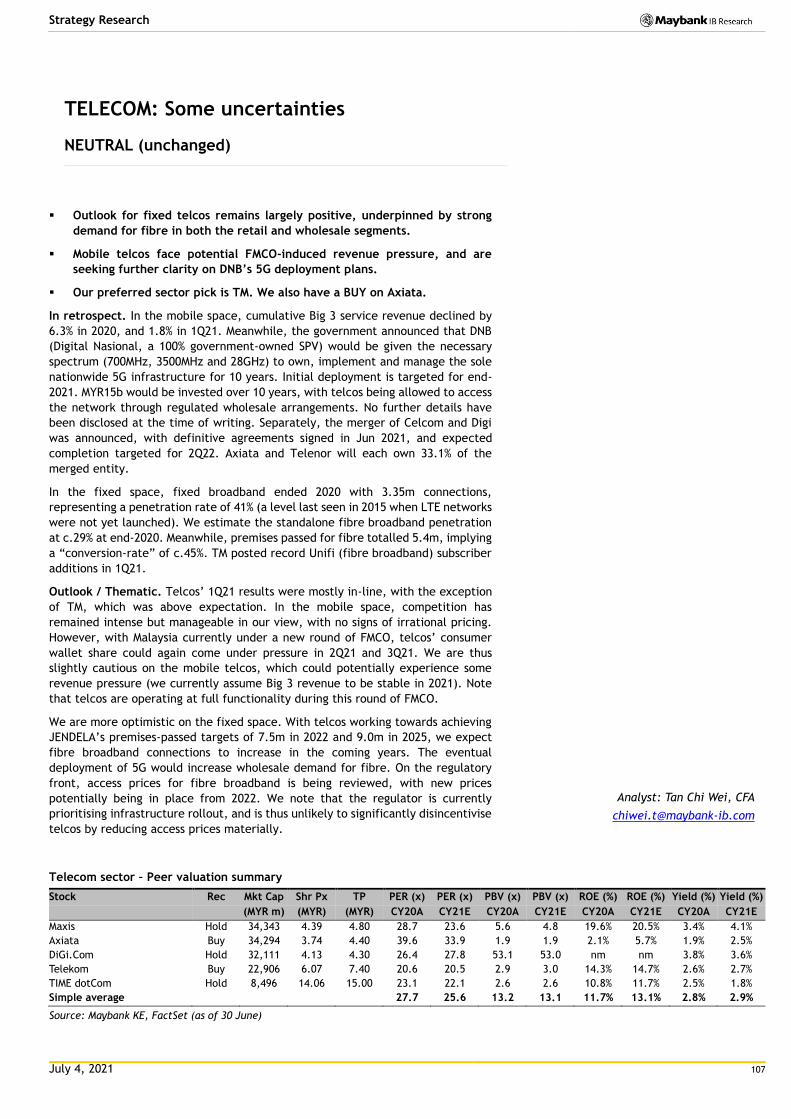

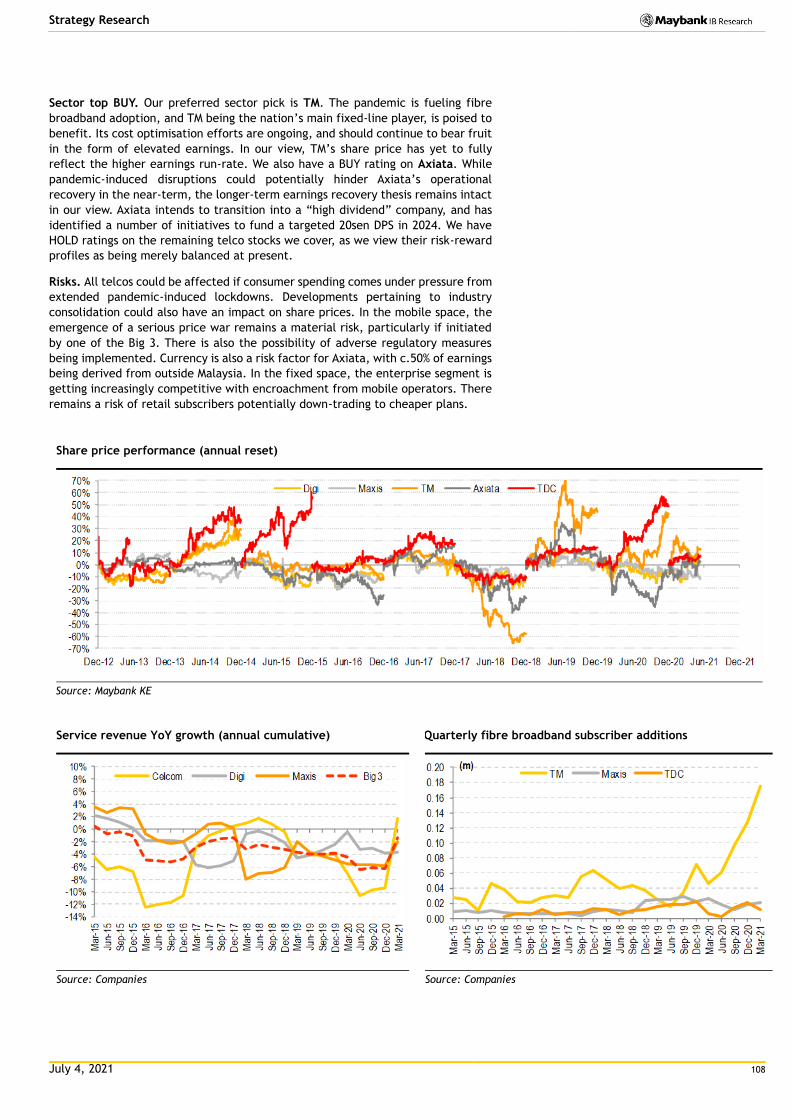

TELECOM: Some uncertainties ................................................................................................... 107

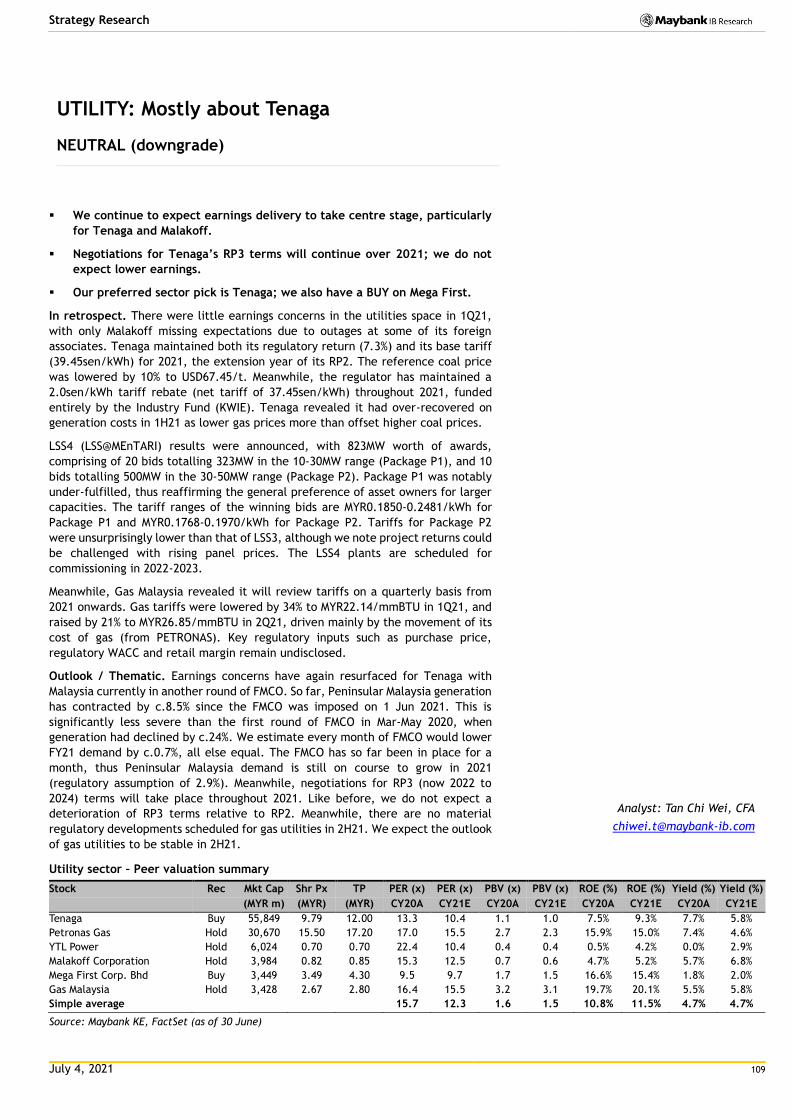

UTILITY: Mostly about Tenaga .................................................................................................... 109

APPENDIX: Foreign shareholding trend ......................................................................................... 111

July 4, 2021

ST

RAT

EG

Y

Mala

ysi

a

July 4, 2021 3

Malaysia Macro Update

Slower 2021 GDP rebound

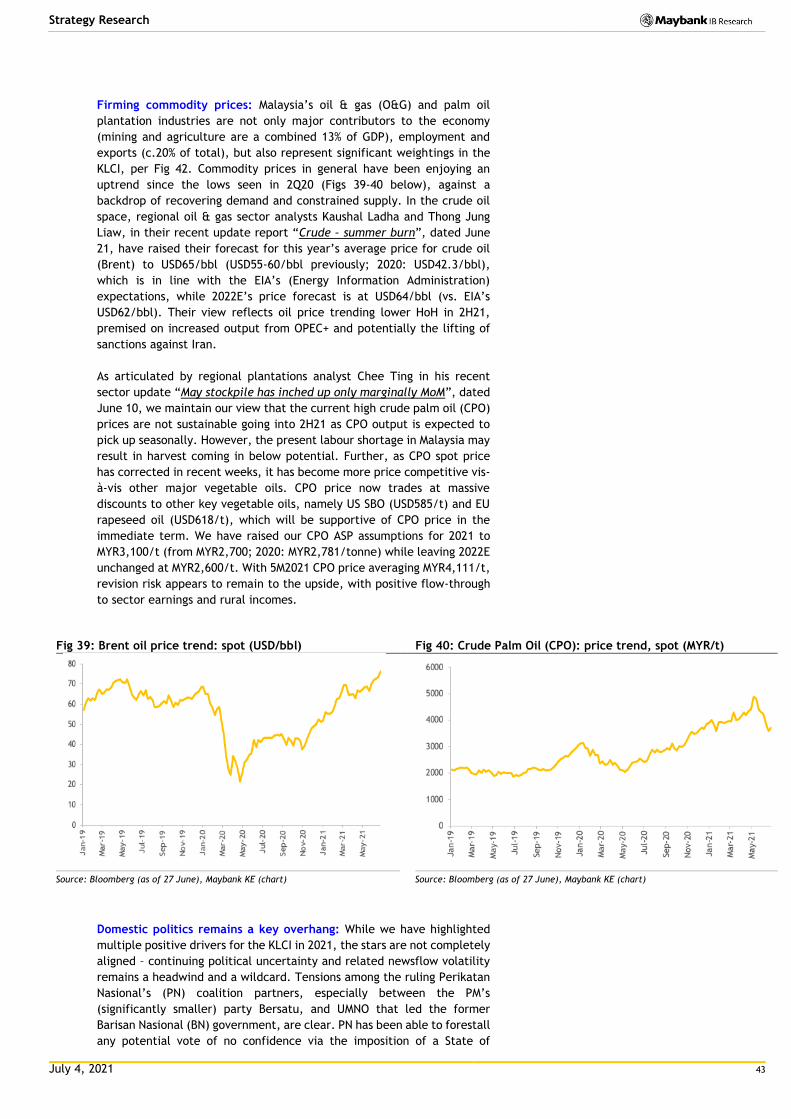

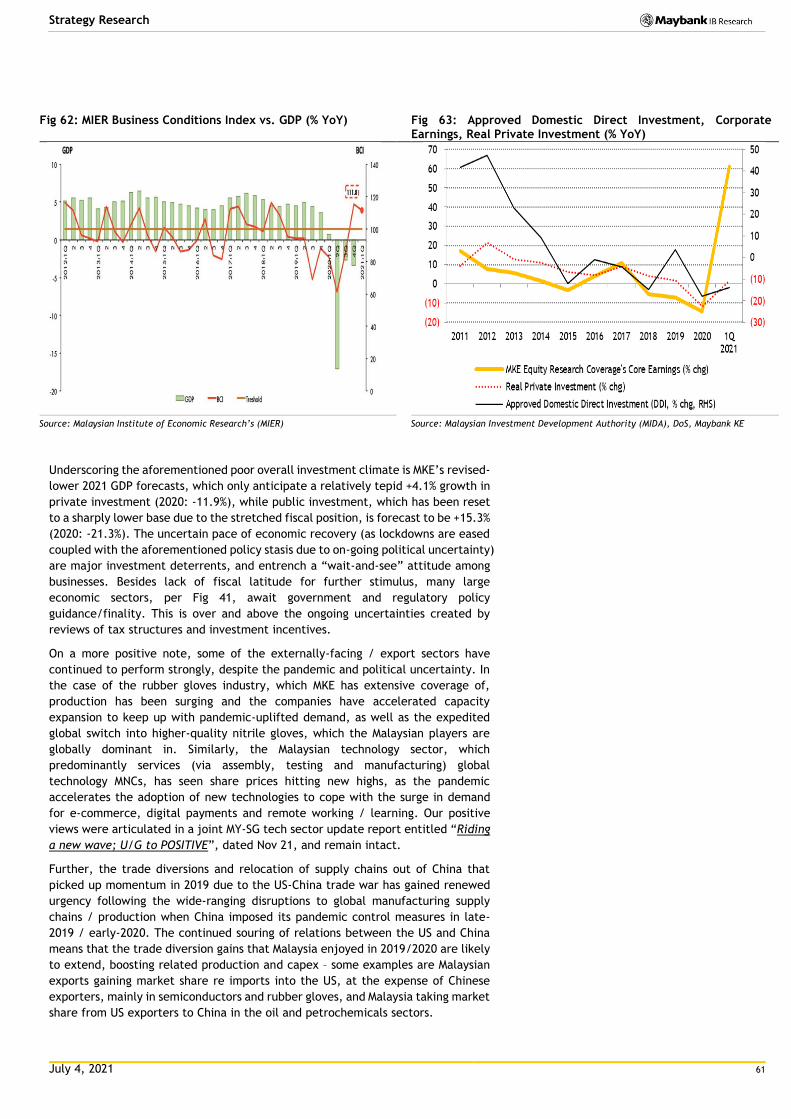

With the country into tighter restrictions in May 2021 and lockdown since 1 June 2021, we cut 2021 real GDP growth forecast to +4.2% from +5.1% previously (2020: -5.6%). This mainly reflects lower growth forecasts for the largest segment of supply-side and demand-side of the economy i.e. services sector (2021E: to +4.2% from +5.1% previously; 1Q 2021: -2.3% YoY; 2020: -5.5%) and private consumption (2021E: to +3.9% from +5.9% previously; 1Q 2021: -1.5% YoY; 2020: -4.3%). Both are 58% and 59.5% of 2020 GDP respectively. Cushioning the downside to the revised 2021 GDP growth forecast is global economic recovery (2021E +6.1%; 1Q 2021 +2.8% YoY; 2020: -3.3%) which is positive for the export-oriented manufacturing and external trade, hence the upgrades in this year’s growth forecasts for manufacturing sector (2021E: to +6.3% from +5.2% previously; 1Q 2021: +6.6% YoY; 2020: -2.6%), exports of goods and services (2021E: to +15.5% from +7.5% previously; 1Q 2021: +11.9% YoY; 2020: -8.9%), and imports of goods & services (2021E: to +18.0% from +8.0% previously; 1Q 2021: +13.0% YoY; 2020: -8.4%). Upward revisions in external trade growth forecasts also reflect upgrades in the in-house forecasts for this year’s ASPs for crude oil (Brent) to USD65/bbl (USD55-60/bbl previously; 2020: USD42.3/bbl) and crude palm oil (CPO) to MYR3,100/tonne (MYR2,700/tonne previously; 2020: MYR2,781/tonne).

Acknowledging the challenging business and operating environment given the ins-and-outs of restrictions and lockdowns, we lowered this year’s private investment growth forecast to +4.1% from +6.3% (2020: -11.9%). Positively, 1Q 2021 private investment grew for the first time since 4Q 2019 by +1.3% YoY (4Q 2020: -6.6% YoY), driven by the first quarterly growth of “machinery & equipment” segment after nine quarters of contractions, signaling positive impact of budget incentives and economic stimulus measures to spur capital expenditure in technology adoption, automation and digitalization. Furthermore, corporate earnings rebounded since 4Q 2020 and total approved investment recovered strongly by +95.6% YoY in 1Q 2021 (2020: -19.5%), which augurs well for private investment outlook.

There are still sizeable positive impulse left from economic and fiscal stimulus i.e. around 60% of the eight economic stimulus packages totaling MYR530b and of Budget 2021’s MYR322.5b spending allocation, as well as around a quarter of the MYR65b COVID-19 Fund, to be spent. Thus we raised Government consumption growth forecast (2021E: to +5.0% from +2.8% previously; 1Q 2021: +5.9% YoY; 2020: +3.9%) and maintain public investment’s double-digit growth outlook (2021E: no change at +15.3%; 1Q 2021: -18.6% YoY; 2020: -21.4%) amid on-going major infrastructure projects and rollout of digital infrastructure capex.

Silver linings amid the pandemic clouds are rising trends in registrations for vaccinations, daily vaccinations and vaccinated population; as well as ramp up in vaccine supplies since June 2021.

We raised our 2021 budget deficit/GDP forecast to 6.8% from 6.0% previously, factoring in the additional direct fiscal injections from the economic stimulus packages year-to-date; revenue and denominator impact of slower GDP growth forecast; and upsides to commodity-related revenues from higher crude oil and CPO price assumptions.

We are sticking to our call of no change in current record-low 1.75% Overnight Policy Rate (OPR) this year amid “passive easing” from negative real OPR; easing in financial condition indicators (i.e. yield and credit spreads); the above-mentioned remaining positive impulse in economic/fiscal stimulus; and active use of other BNM policy tools e.g. loan moratorium; SME financing and microcredit schemes.

Click here to enter text.

Click here to enter text.

Click here to enter text.

Analysts

Suhaimi Ilias (Economics)

(+603) 2297 8682

Dr Zamros Dzulkafli

(603) 2082 6818

Ramesh Lankanathan

(603) 2297 8685

July 4, 2021 4

Strategy Research

Economic indicators jumped in Apr 2021

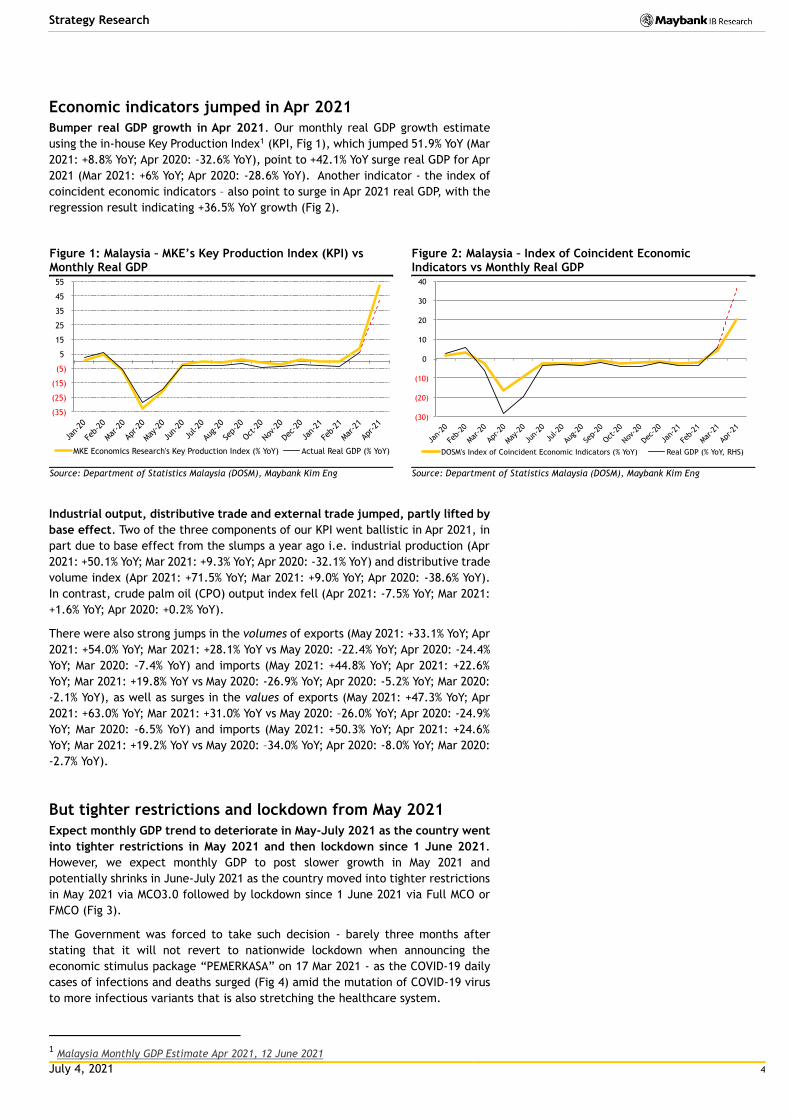

Bumper real GDP growth in Apr 2021. Our monthly real GDP growth estimate

using the in-house Key Production Index1 (KPI, Fig 1), which jumped 51.9% YoY (Mar

2021: +8.8% YoY; Apr 2020: -32.6% YoY), point to +42.1% YoY surge real GDP for Apr

2021 (Mar 2021: +6% YoY; Apr 2020: -28.6% YoY). Another indicator - the index of

coincident economic indicators – also point to surge in Apr 2021 real GDP, with the

regression result indicating +36.5% YoY growth (Fig 2).

Figure 1: Malaysia – MKE’s Key Production Index (KPI) vs Monthly Real GDP

Figure 2: Malaysia – Index of Coincident Economic Indicators vs Monthly Real GDP

Source: Department of Statistics Malaysia (DOSM), Maybank Kim Eng Source: Department of Statistics Malaysia (DOSM), Maybank Kim Eng

Industrial output, distributive trade and external trade jumped, partly lifted by

base effect. Two of the three components of our KPI went ballistic in Apr 2021, in

part due to base effect from the slumps a year ago i.e. industrial production (Apr

2021: +50.1% YoY; Mar 2021: +9.3% YoY; Apr 2020: -32.1% YoY) and distributive trade

volume index (Apr 2021: +71.5% YoY; Mar 2021: +9.0% YoY; Apr 2020: -38.6% YoY).

In contrast, crude palm oil (CPO) output index fell (Apr 2021: -7.5% YoY; Mar 2021:

+1.6% YoY; Apr 2020: +0.2% YoY).

There were also strong jumps in the volumes of exports (May 2021: +33.1% YoY; Apr

2021: +54.0% YoY; Mar 2021: +28.1% YoY vs May 2020: -22.4% YoY; Apr 2020: -24.4%

YoY; Mar 2020: -7.4% YoY) and imports (May 2021: +44.8% YoY; Apr 2021: +22.6%

YoY; Mar 2021: +19.8% YoY vs May 2020: -26.9% YoY; Apr 2020: -5.2% YoY; Mar 2020:

-2.1% YoY), as well as surges in the values of exports (May 2021: +47.3% YoY; Apr

2021: +63.0% YoY; Mar 2021: +31.0% YoY vs May 2020: –26.0% YoY; Apr 2020: -24.9%

YoY; Mar 2020: -6.5% YoY) and imports (May 2021: +50.3% YoY; Apr 2021: +24.6%

YoY; Mar 2021: +19.2% YoY vs May 2020: –34.0% YoY; Apr 2020: -8.0% YoY; Mar 2020:

-2.7% YoY).

But tighter restrictions and lockdown from May 2021

Expect monthly GDP trend to deteriorate in May-July 2021 as the country went

into tighter restrictions in May 2021 and then lockdown since 1 June 2021.

However, we expect monthly GDP to post slower growth in May 2021 and

potentially shrinks in June-July 2021 as the country moved into tighter restrictions

in May 2021 via MCO3.0 followed by lockdown since 1 June 2021 via Full MCO or

FMCO (Fig 3).

The Government was forced to take such decision - barely three months after

stating that it will not revert to nationwide lockdown when announcing the

economic stimulus package “PEMERKASA” on 17 Mar 2021 - as the COVID-19 daily

cases of infections and deaths surged (Fig 4) amid the mutation of COVID-19 virus

to more infectious variants that is also stretching the healthcare system.

1 Malaysia Monthly GDP Estimate Apr 2021, 12 June 2021

(35)

(25)

(15)

(5)

5

15

25

35

45

55

Jan-

20

Feb-

20

Mar

-20

Apr-20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct

-20

Nov-20

Dec-

20

Jan-

21

Feb-

21

Mar

-21

Apr-21

MKE Economics Research's Key Production Index (% YoY) Actual Real GDP (% YoY)

(30)

(20)

(10)

0

10

20

30

40

Jan-

20

Feb-

20

Mar

-20

Apr-20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct-2

0

Nov-2

0

Dec-

20

Jan-

21

Feb-

21

Mar

-21

Apr-21

DOSM's Index of Coincident Economic Indicators (% YoY) Real GDP (% YoY, RHS)

July 4, 2021 5

Strategy Research

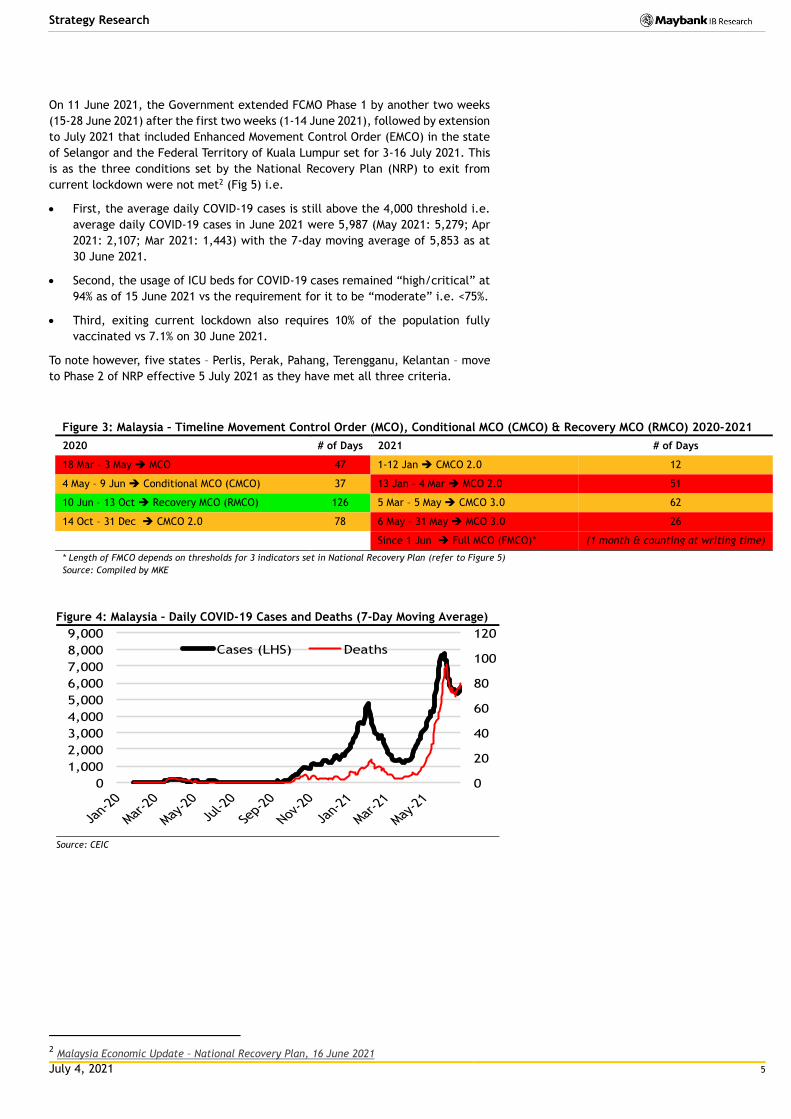

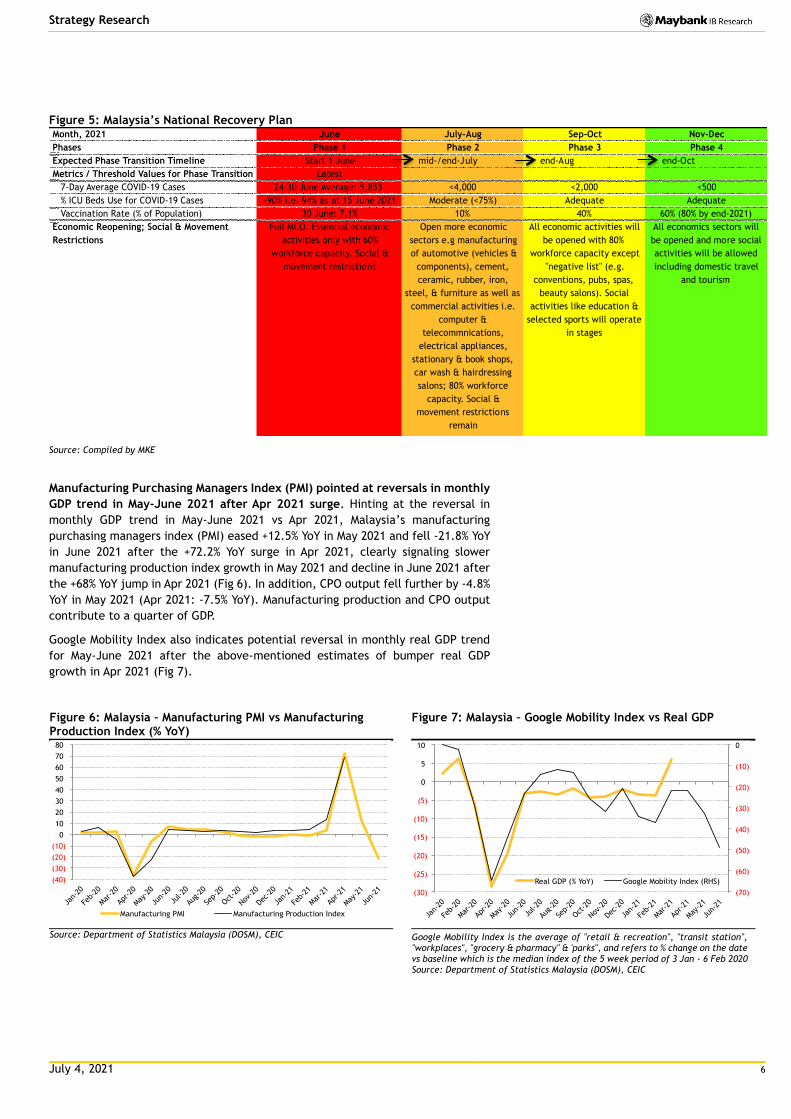

On 11 June 2021, the Government extended FCMO Phase 1 by another two weeks

(15-28 June 2021) after the first two weeks (1-14 June 2021), followed by extension

to July 2021 that included Enhanced Movement Control Order (EMCO) in the state

of Selangor and the Federal Territory of Kuala Lumpur set for 3-16 July 2021. This

is as the three conditions set by the National Recovery Plan (NRP) to exit from

current lockdown were not met2 (Fig 5) i.e.

First, the average daily COVID-19 cases is still above the 4,000 threshold i.e.

average daily COVID-19 cases in June 2021 were 5,987 (May 2021: 5,279; Apr

2021: 2,107; Mar 2021: 1,443) with the 7-day moving average of 5,853 as at

30 June 2021.

Second, the usage of ICU beds for COVID-19 cases remained “high/critical” at

94% as of 15 June 2021 vs the requirement for it to be “moderate” i.e. <75%.

Third, exiting current lockdown also requires 10% of the population fully

vaccinated vs 7.1% on 30 June 2021.

To note however, five states – Perlis, Perak, Pahang, Terengganu, Kelantan – move

to Phase 2 of NRP effective 5 July 2021 as they have met all three criteria.

Figure 3: Malaysia – Timeline Movement Control Order (MCO), Conditional MCO (CMCO) & Recovery MCO (RMCO) 2020-2021

2020 # of Days 2021 # of Days

18 Mar – 3 May MCO 47 1-12 Jan CMCO 2.0 12

4 May – 9 Jun Conditional MCO (CMCO) 37 13 Jan – 4 Mar MCO 2.0 51

10 Jun – 13 Oct Recovery MCO (RMCO) 126 5 Mar – 5 May CMCO 3.0 62

14 Oct – 31 Dec CMCO 2.0 78 6 May – 31 May MCO 3.0 26

Since 1 Jun Full MCO (FMCO)* (1 month & counting at writing time)

* Length of FMCO depends on thresholds for 3 indicators set in National Recovery Plan (refer to Figure 5)

Source: Compiled by MKE

Figure 4: Malaysia – Daily COVID-19 Cases and Deaths (7-Day Moving Average)

Source: CEIC

2 Malaysia Economic Update – National Recovery Plan, 16 June 2021

0

20

40

60

80

100

120

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan-

20

Mar-2

0

May-2

0

Jul-2

0

Sep-

20

Nov-2

0

Jan-

21

Mar-2

1

May-2

1

Cases (LHS) Deaths

July 4, 2021 6

Strategy Research

Figure 5: Malaysia’s National Recovery Plan

Source: Compiled by MKE

Manufacturing Purchasing Managers Index (PMI) pointed at reversals in monthly

GDP trend in May-June 2021 after Apr 2021 surge. Hinting at the reversal in

monthly GDP trend in May-June 2021 vs Apr 2021, Malaysia’s manufacturing

purchasing managers index (PMI) eased +12.5% YoY in May 2021 and fell -21.8% YoY

in June 2021 after the +72.2% YoY surge in Apr 2021, clearly signaling slower

manufacturing production index growth in May 2021 and decline in June 2021 after

the +68% YoY jump in Apr 2021 (Fig 6). In addition, CPO output fell further by -4.8%

YoY in May 2021 (Apr 2021: -7.5% YoY). Manufacturing production and CPO output

contribute to a quarter of GDP.

Google Mobility Index also indicates potential reversal in monthly real GDP trend

for May-June 2021 after the above-mentioned estimates of bumper real GDP

growth in Apr 2021 (Fig 7).

Figure 6: Malaysia – Manufacturing PMI vs Manufacturing Production Index (% YoY)

Figure 7: Malaysia – Google Mobility Index vs Real GDP

Source: Department of Statistics Malaysia (DOSM), CEIC Google Mobility Index is the average of "retail & recreation", "transit station", "workplaces", "grocery & pharmacy" & 'parks", and refers to % change on the date vs baseline which is the median index of the 5 week period of 3 Jan - 6 Feb 2020 Source: Department of Statistics Malaysia (DOSM), CEIC

Month, 2021 June July-Aug Sep-Oct Nov-Dec

Phases Phase 1 Phase 2 Phase 3 Phase 4

Expected Phase Transition Timeline Start 1 June mid-/end-July end-Aug end-Oct

Metrics / Threshold Values for Phase Transition Latest

7-Day Average COVID-19 Cases 24-30 June Average: 5,853 <4,000 <2,000 <500

% ICU Beds Use for COVID-19 Cases >90% i.e. 94% as at 15 June 2021 Moderate (<75%) Adequate Adequate

Vaccination Rate (% of Population) 30 June: 7.1% 10% 40% 60% (80% by end-2021)

Economic Reopening; Social & Movement

Restrictions

Full MCO. Essential economic

activities only with 60%

workforce capacity. Social &

movement restrictions

Open more economic

sectors e.g manufacturing

of automotive (vehicles &

components), cement,

ceramic, rubber, iron,

steel, & furniture as well as

commercial activities i.e.

computer &

telecommnications,

electrical appliances,

stationary & book shops,

car wash & hairdressing

salons; 80% workforce

capacity. Social &

movement restrictions

remain

All economic activities will

be opened with 80%

workforce capacity except

"negative list" (e.g.

conventions, pubs, spas,

beauty salons). Social

activities like education &

selected sports will operate

in stages

All economics sectors will

be opened and more social

activities will be allowed

including domestic travel

and tourism

(40)

(30)

(20)

(10)

0

10

20

30

40

50

60

70

80

Jan-

20

Feb-

20

Mar

-20

Apr-20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct-2

0

Nov-2

0

Dec-

20

Jan-

21

Feb-

21

Mar

-21

Apr-21

May

-21

Jun-

21

Manufacturing PMI Manufacturing Production Index

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

(30)

(25)

(20)

(15)

(10)

(5)

0

5

10

Jan-

20

Feb-

20

Mar

-20

Apr-20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct

-20

Nov-2

0

Dec-

20

Jan-

21

Feb-

21

Mar

-21

Apr-21

May

-21

Jun-

21

Real GDP (% YoY) Google Mobility Index (RHS)

July 4, 2021 7

Strategy Research

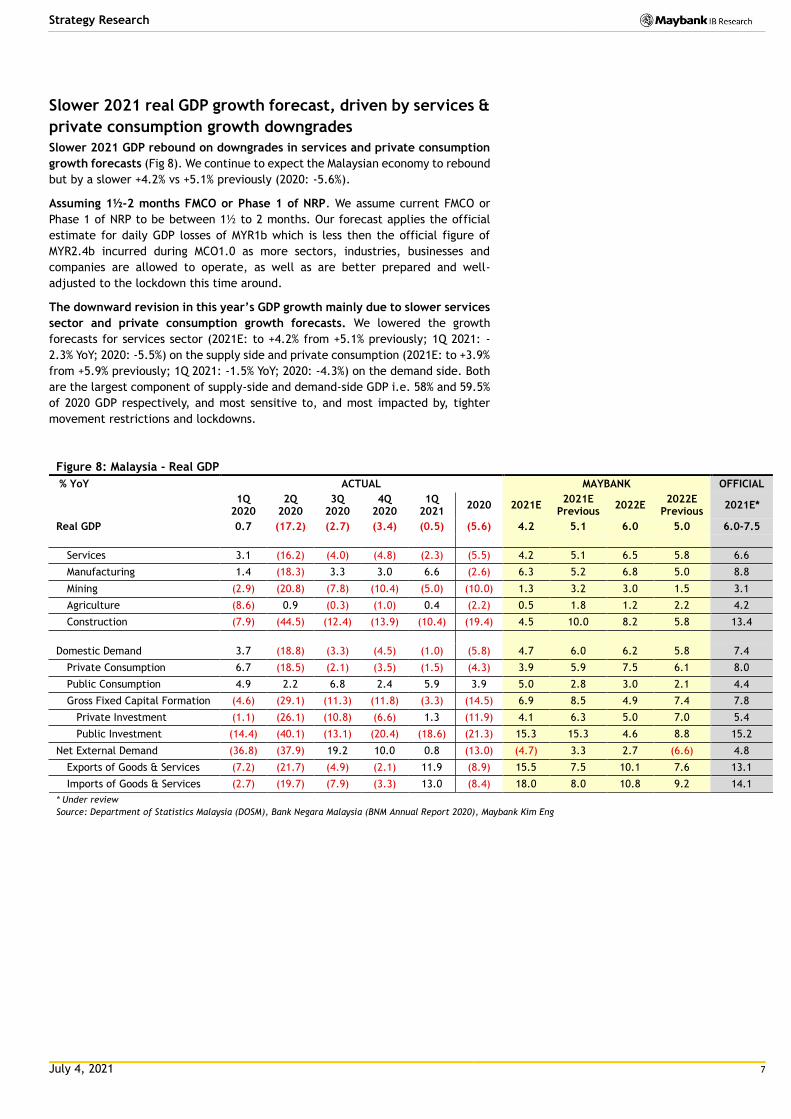

Slower 2021 real GDP growth forecast, driven by services &

private consumption growth downgrades

Slower 2021 GDP rebound on downgrades in services and private consumption

growth forecasts (Fig 8). We continue to expect the Malaysian economy to rebound

but by a slower +4.2% vs +5.1% previously (2020: -5.6%).

Assuming 1½-2 months FMCO or Phase 1 of NRP. We assume current FMCO or

Phase 1 of NRP to be between 1½ to 2 months. Our forecast applies the official

estimate for daily GDP losses of MYR1b which is less then the official figure of

MYR2.4b incurred during MCO1.0 as more sectors, industries, businesses and

companies are allowed to operate, as well as are better prepared and well-

adjusted to the lockdown this time around.

The downward revision in this year’s GDP growth mainly due to slower services

sector and private consumption growth forecasts. We lowered the growth

forecasts for services sector (2021E: to +4.2% from +5.1% previously; 1Q 2021: -

2.3% YoY; 2020: -5.5%) on the supply side and private consumption (2021E: to +3.9%

from +5.9% previously; 1Q 2021: -1.5% YoY; 2020: -4.3%) on the demand side. Both

are the largest component of supply-side and demand-side GDP i.e. 58% and 59.5%

of 2020 GDP respectively, and most sensitive to, and most impacted by, tighter

movement restrictions and lockdowns.

Figure 8: Malaysia - Real GDP

% YoY ACTUAL MAYBANK OFFICIAL

1Q

2020 2Q

2020 3Q

2020 4Q

2020 1Q

2021 2020 2021E

2021E Previous

2022E 2022E

Previous 2021E*

Real GDP 0.7 (17.2) (2.7) (3.4) (0.5) (5.6) 4.2 5.1 6.0 5.0 6.0-7.5

Services 3.1 (16.2) (4.0) (4.8) (2.3) (5.5) 4.2 5.1 6.5 5.8 6.6

Manufacturing 1.4 (18.3) 3.3 3.0 6.6 (2.6) 6.3 5.2 6.8 5.0 8.8

Mining (2.9) (20.8) (7.8) (10.4) (5.0) (10.0) 1.3 3.2 3.0 1.5 3.1

Agriculture (8.6) 0.9 (0.3) (1.0) 0.4 (2.2) 0.5 1.8 1.2 2.2 4.2

Construction (7.9) (44.5) (12.4) (13.9) (10.4) (19.4) 4.5 10.0 8.2 5.8 13.4

Domestic Demand 3.7 (18.8) (3.3) (4.5) (1.0) (5.8) 4.7 6.0 6.2 5.8 7.4

Private Consumption 6.7 (18.5) (2.1) (3.5) (1.5) (4.3) 3.9 5.9 7.5 6.1 8.0

Public Consumption 4.9 2.2 6.8 2.4 5.9 3.9 5.0 2.8 3.0 2.1 4.4

Gross Fixed Capital Formation (4.6) (29.1) (11.3) (11.8) (3.3) (14.5) 6.9 8.5 4.9 7.4 7.8

Private Investment (1.1) (26.1) (10.8) (6.6) 1.3 (11.9) 4.1 6.3 5.0 7.0 5.4

Public Investment (14.4) (40.1) (13.1) (20.4) (18.6) (21.3) 15.3 15.3 4.6 8.8 15.2

Net External Demand (36.8) (37.9) 19.2 10.0 0.8 (13.0) (4.7) 3.3 2.7 (6.6) 4.8

Exports of Goods & Services (7.2) (21.7) (4.9) (2.1) 11.9 (8.9) 15.5 7.5 10.1 7.6 13.1

Imports of Goods & Services (2.7) (19.7) (7.9) (3.3) 13.0 (8.4) 18.0 8.0 10.8 9.2 14.1

* Under review

Source: Department of Statistics Malaysia (DOSM), Bank Negara Malaysia (BNM Annual Report 2020), Maybank Kim Eng

July 4, 2021 8

Strategy Research

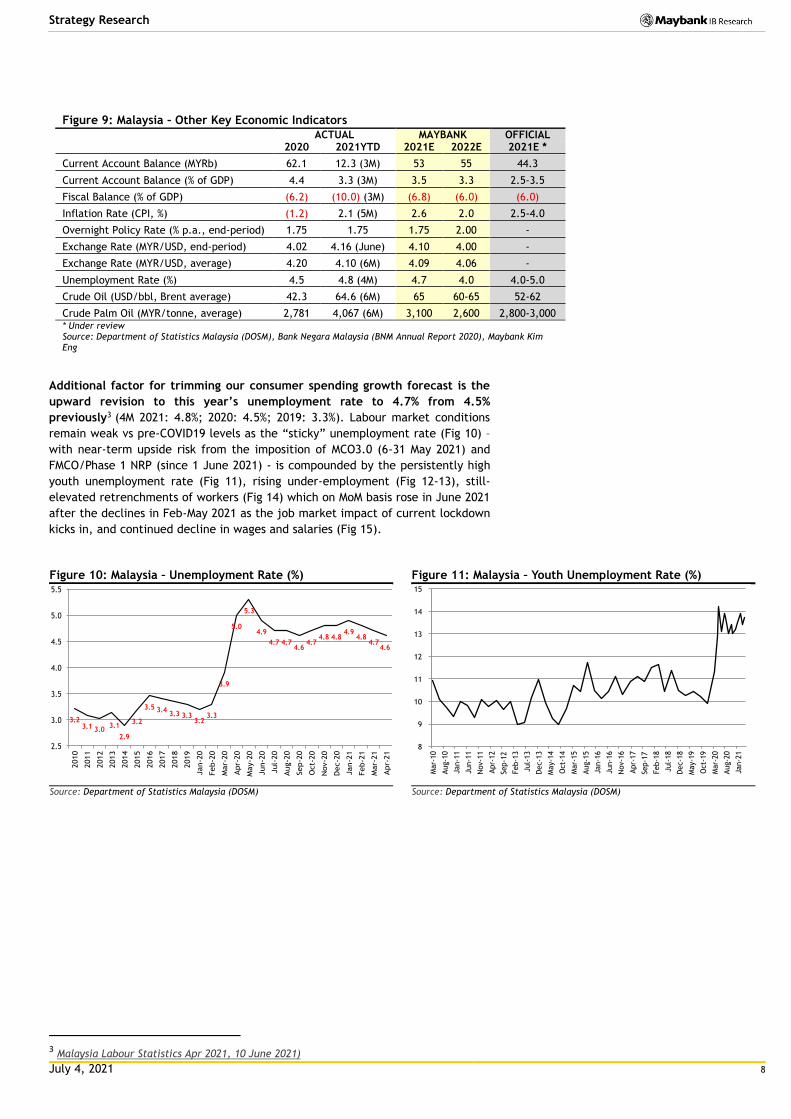

Figure 9: Malaysia – Other Key Economic Indicators

ACTUAL MAYBANK OFFICIAL 2020 2021YTD 2021E 2022E 2021E *

Current Account Balance (MYRb) 62.1 12.3 (3M) 53 55 44.3

Current Account Balance (% of GDP) 4.4 3.3 (3M) 3.5 3.3 2.5-3.5

Fiscal Balance (% of GDP) (6.2) (10.0) (3M) (6.8) (6.0) (6.0)

Inflation Rate (CPI, %) (1.2) 2.1 (5M) 2.6 2.0 2.5-4.0

Overnight Policy Rate (% p.a., end-period) 1.75 1.75 1.75 2.00 -

Exchange Rate (MYR/USD, end-period) 4.02 4.16 (June) 4.10 4.00 -

Exchange Rate (MYR/USD, average) 4.20 4.10 (6M) 4.09 4.06 -

Unemployment Rate (%) 4.5 4.8 (4M) 4.7 4.0 4.0-5.0

Crude Oil (USD/bbl, Brent average) 42.3 64.6 (6M) 65 60-65 52-62

Crude Palm Oil (MYR/tonne, average) 2,781 4,067 (6M) 3,100 2,600 2,800-3,000 * Under review Source: Department of Statistics Malaysia (DOSM), Bank Negara Malaysia (BNM Annual Report 2020), Maybank Kim Eng

Additional factor for trimming our consumer spending growth forecast is the

upward revision to this year’s unemployment rate to 4.7% from 4.5%

previously3 (4M 2021: 4.8%; 2020: 4.5%; 2019: 3.3%). Labour market conditions

remain weak vs pre-COVID19 levels as the “sticky” unemployment rate (Fig 10) –

with near-term upside risk from the imposition of MCO3.0 (6-31 May 2021) and

FMCO/Phase 1 NRP (since 1 June 2021) - is compounded by the persistently high

youth unemployment rate (Fig 11), rising under-employment (Fig 12-13), still-

elevated retrenchments of workers (Fig 14) which on MoM basis rose in June 2021

after the declines in Feb-May 2021 as the job market impact of current lockdown

kicks in, and continued decline in wages and salaries (Fig 15).

Figure 10: Malaysia – Unemployment Rate (%) Figure 11: Malaysia – Youth Unemployment Rate (%)

Source: Department of Statistics Malaysia (DOSM) Source: Department of Statistics Malaysia (DOSM)

3 Malaysia Labour Statistics Apr 2021, 10 June 2021)

3.2 3.1 3.0

3.1

2.9

3.2

3.5 3.4 3.3 3.3

3.2 3.3

3.9

5.0

5.3

4.9

4.7 4.7 4.6

4.7 4.8 4.8

4.9 4.8

4.7 4.6

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Jan-2

0

Feb-2

0

Mar-

20

Apr-

20

May-2

0

Jun-2

0

Jul-

20

Aug-2

0

Sep-2

0

Oct-

20

Nov-2

0

Dec-2

0

Jan-2

1

Feb-2

1

Mar-

21

Apr-

21 8

9

10

11

12

13

14

15

Mar-

10

Aug-1

0

Jan-1

1

Jun-1

1

Nov-1

1

Apr-

12

Sep-1

2

Feb-1

3

Jul-

13

Dec-1

3

May-1

4

Oct-

14

Mar-

15

Aug-1

5

Jan-1

6

Jun-1

6

Nov-1

6

Apr-

17

Sep-1

7

Feb-1

8

Jul-

18

Dec-1

8

May-1

9

Oct-

19

Mar-

20

Aug-2

0

Jan-2

1

July 4, 2021 9

Strategy Research

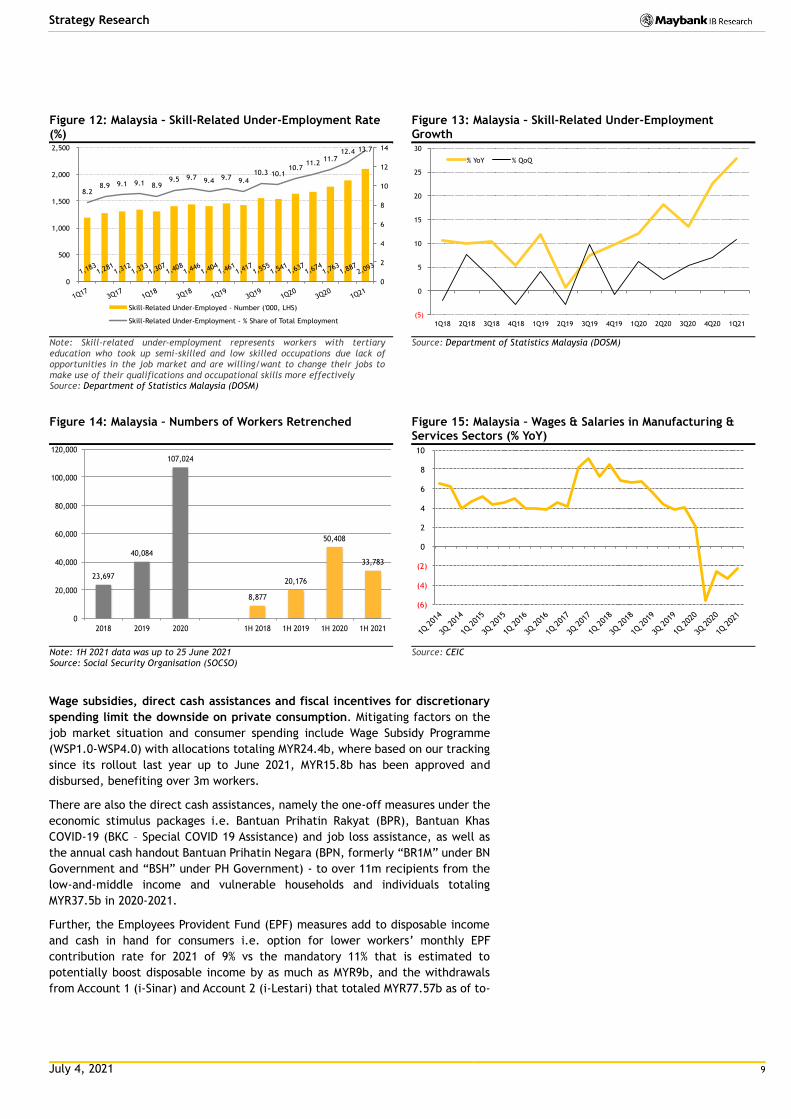

Figure 12: Malaysia – Skill-Related Under-Employment Rate (%)

Figure 13: Malaysia – Skill-Related Under-Employment Growth

Note: Skill-related under-employment represents workers with tertiary education who took up semi-skilled and low skilled occupations due lack of opportunities in the job market and are willing/want to change their jobs to make use of their qualifications and occupational skills more effectively Source: Department of Statistics Malaysia (DOSM)

Source: Department of Statistics Malaysia (DOSM)

Figure 14: Malaysia – Numbers of Workers Retrenched Figure 15: Malaysia – Wages & Salaries in Manufacturing & Services Sectors (% YoY)

Note: 1H 2021 data was up to 25 June 2021 Source: Social Security Organisation (SOCSO)

Source: CEIC

Wage subsidies, direct cash assistances and fiscal incentives for discretionary

spending limit the downside on private consumption. Mitigating factors on the

job market situation and consumer spending include Wage Subsidy Programme

(WSP1.0-WSP4.0) with allocations totaling MYR24.4b, where based on our tracking

since its rollout last year up to June 2021, MYR15.8b has been approved and

disbursed, benefiting over 3m workers.

There are also the direct cash assistances, namely the one-off measures under the

economic stimulus packages i.e. Bantuan Prihatin Rakyat (BPR), Bantuan Khas

COVID-19 (BKC – Special COVID 19 Assistance) and job loss assistance, as well as

the annual cash handout Bantuan Prihatin Negara (BPN, formerly “BR1M” under BN

Government and “BSH” under PH Government) - to over 11m recipients from the

low-and-middle income and vulnerable households and individuals totaling

MYR37.5b in 2020-2021.

Further, the Employees Provident Fund (EPF) measures add to disposable income

and cash in hand for consumers i.e. option for lower workers’ monthly EPF

contribution rate for 2021 of 9% vs the mandatory 11% that is estimated to

potentially boost disposable income by as much as MYR9b, and the withdrawals

from Account 1 (i-Sinar) and Account 2 (i-Lestari) that totaled MYR77.57b as of to-

1,183 1,281

1,312 1,333

1,307 1,408

1,446 1,404

1,461 1,417

1,555 1,541

1,637 1,674

1,763 1,887

2,093

8.2 8.9 9.1 9.1 8.9

9.5 9.7 9.4 9.7 9.4 10.3 10.1

10.7 11.2

11.7 12.4 13.7

0

2

4

6

8

10

12

14

0

500

1,000

1,500

2,000

2,500

1Q17 3Q17

1Q18 3Q18

1Q19 3Q19

1Q20 3Q20

1Q21

Skill-Related Under-Employed - Number ('000, LHS)

Skill-Related Under-Employment - % Share of Total Employment (5)

0

5

10

15

20

25

30

1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21

% YoY % QoQ

23,697

40,084

107,024

8,877

20,176

50,408

33,783

0

20,000

40,000

60,000

80,000

100,000

120,000

2018 2019 2020 1H 2018 1H 2019 1H 2020 1H 2021

(6)

(4)

(2)

0

2

4

6

8

10

1Q 201

4

3Q 201

4

1Q 201

5

3Q 201

5

1Q 201

6

3Q 201

6

1Q 201

7

3Q 201

7

1Q 201

8

3Q 201

8

1Q 201

9

3Q 201

9

1Q 202

0

3Q 202

0

1Q 202

1

July 4, 2021 10

Strategy Research

date4 i.e. MYR19.6b under i-Lestari and MYR57.97b under i-Sinar, with potential

additional MYR30b from the latest withdrawal scheme i-Citra.

At the same time, household income in the plantation sector is buoyed by the high

crude palm oil (CPO) prices (6M2021: MYR4,067 per tonne; 2020: MYR2,781 per

tonne).

In addition, to boost discretionary consumer spending, the Government extended

for the second time the stamp duty and sales tax exemptions for purchases of

residential property and cars respectively until end-Dec 2021. These exemptions

were first introduced under the “PENJANA” economic stimulus package back in

June 2020. And under the “PERMAI” economic stimulus package in Jan 2021, the

Government extended the special MYR2,500 personal income tax relief for

purchases of mobile phones, computers and tablets until 31 Dec 2021 following its

expiry on 31 Dec 2020.

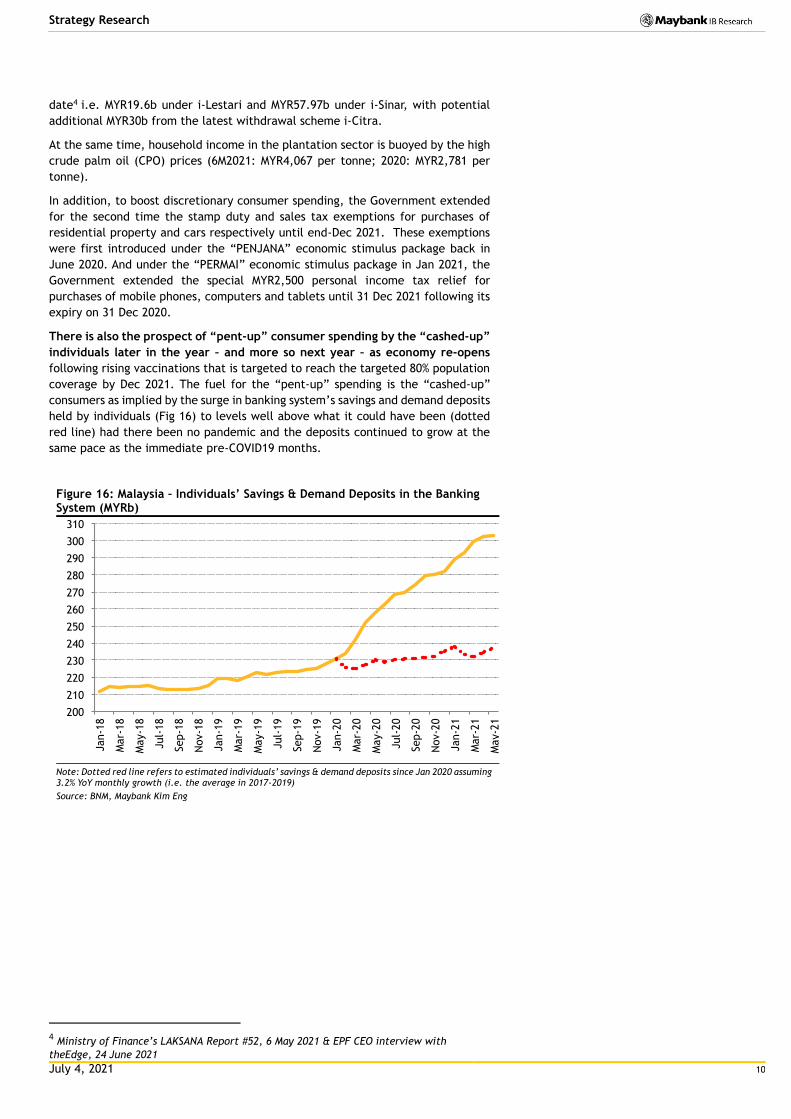

There is also the prospect of “pent-up” consumer spending by the “cashed-up”

individuals later in the year – and more so next year – as economy re-opens

following rising vaccinations that is targeted to reach the targeted 80% population

coverage by Dec 2021. The fuel for the “pent-up” spending is the “cashed-up”

consumers as implied by the surge in banking system’s savings and demand deposits

held by individuals (Fig 16) to levels well above what it could have been (dotted

red line) had there been no pandemic and the deposits continued to grow at the

same pace as the immediate pre-COVID19 months.

Figure 16: Malaysia – Individuals’ Savings & Demand Deposits in the Banking System (MYRb)

Note: Dotted red line refers to estimated individuals’ savings & demand deposits since Jan 2020 assuming 3.2% YoY monthly growth (i.e. the average in 2017-2019)

Source: BNM, Maybank Kim Eng

4 Ministry of Finance’s LAKSANA Report #52, 6 May 2021 & EPF CEO interview with

theEdge, 24 June 2021

200

210

220

230

240

250

260

270

280

290

300

310

Jan-1

8

Mar-

18

May-1

8

Jul-

18

Sep-1

8

Nov-1

8

Jan-1

9

Mar-

19

May-1

9

Jul-

19

Sep-1

9

Nov-1

9

Jan-2

0

Mar-

20

May-2

0

Jul-

20

Sep-2

0

Nov-2

0

Jan-2

1

Mar-

21

May-2

1

July 4, 2021 11

Strategy Research

Positive impact on manufacturing & external trade from

global economic rebound provide some cushion

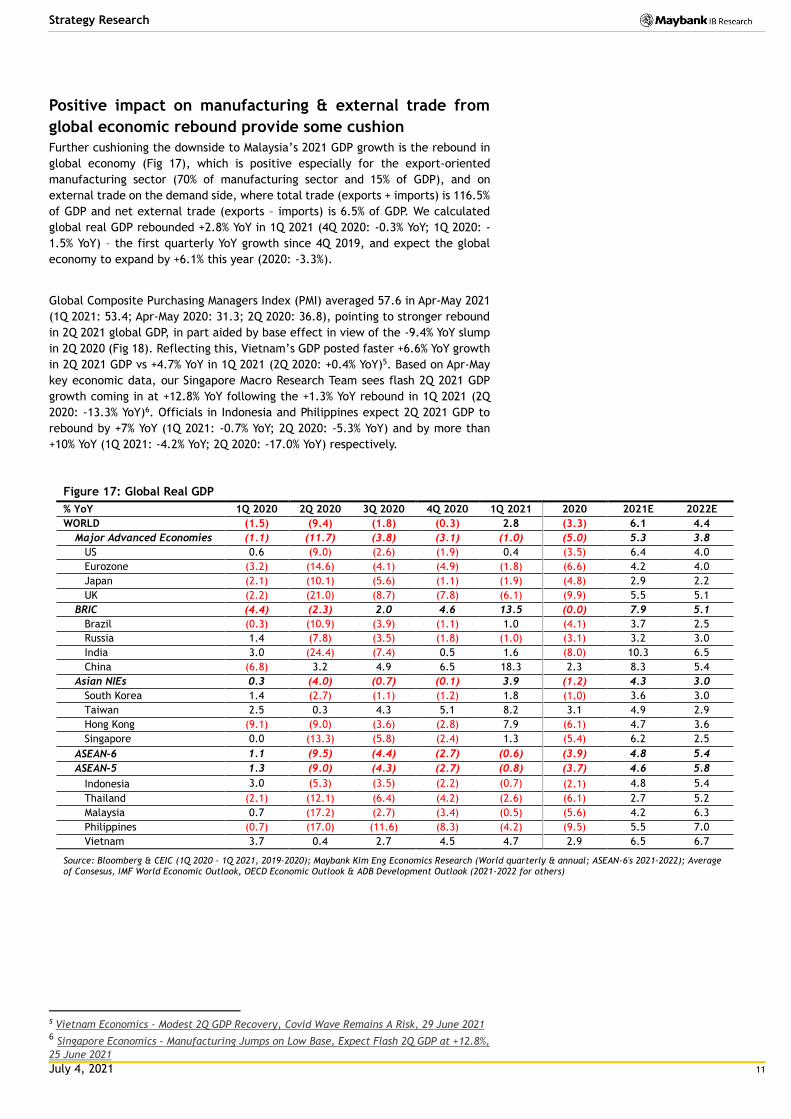

Further cushioning the downside to Malaysia’s 2021 GDP growth is the rebound in

global economy (Fig 17), which is positive especially for the export-oriented

manufacturing sector (70% of manufacturing sector and 15% of GDP), and on

external trade on the demand side, where total trade (exports + imports) is 116.5%

of GDP and net external trade (exports – imports) is 6.5% of GDP. We calculated

global real GDP rebounded +2.8% YoY in 1Q 2021 (4Q 2020: -0.3% YoY; 1Q 2020: -

1.5% YoY) – the first quarterly YoY growth since 4Q 2019, and expect the global

economy to expand by +6.1% this year (2020: -3.3%).

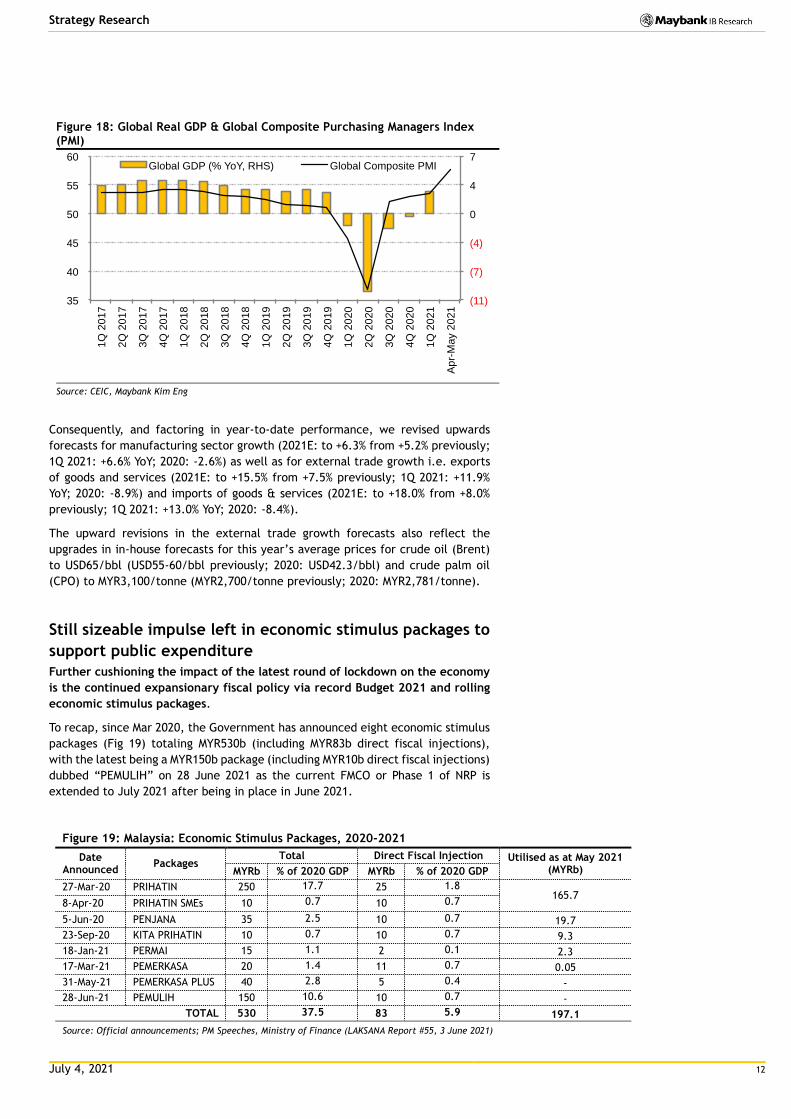

Global Composite Purchasing Managers Index (PMI) averaged 57.6 in Apr-May 2021

(1Q 2021: 53.4; Apr-May 2020: 31.3; 2Q 2020: 36.8), pointing to stronger rebound

in 2Q 2021 global GDP, in part aided by base effect in view of the -9.4% YoY slump

in 2Q 2020 (Fig 18). Reflecting this, Vietnam’s GDP posted faster +6.6% YoY growth

in 2Q 2021 GDP vs +4.7% YoY in 1Q 2021 (2Q 2020: +0.4% YoY)5. Based on Apr-May

key economic data, our Singapore Macro Research Team sees flash 2Q 2021 GDP

growth coming in at +12.8% YoY following the +1.3% YoY rebound in 1Q 2021 (2Q

2020: -13.3% YoY)6. Officials in Indonesia and Philippines expect 2Q 2021 GDP to

rebound by +7% YoY (1Q 2021: -0.7% YoY; 2Q 2020: -5.3% YoY) and by more than

+10% YoY (1Q 2021: -4.2% YoY; 2Q 2020: -17.0% YoY) respectively.

Figure 17: Global Real GDP

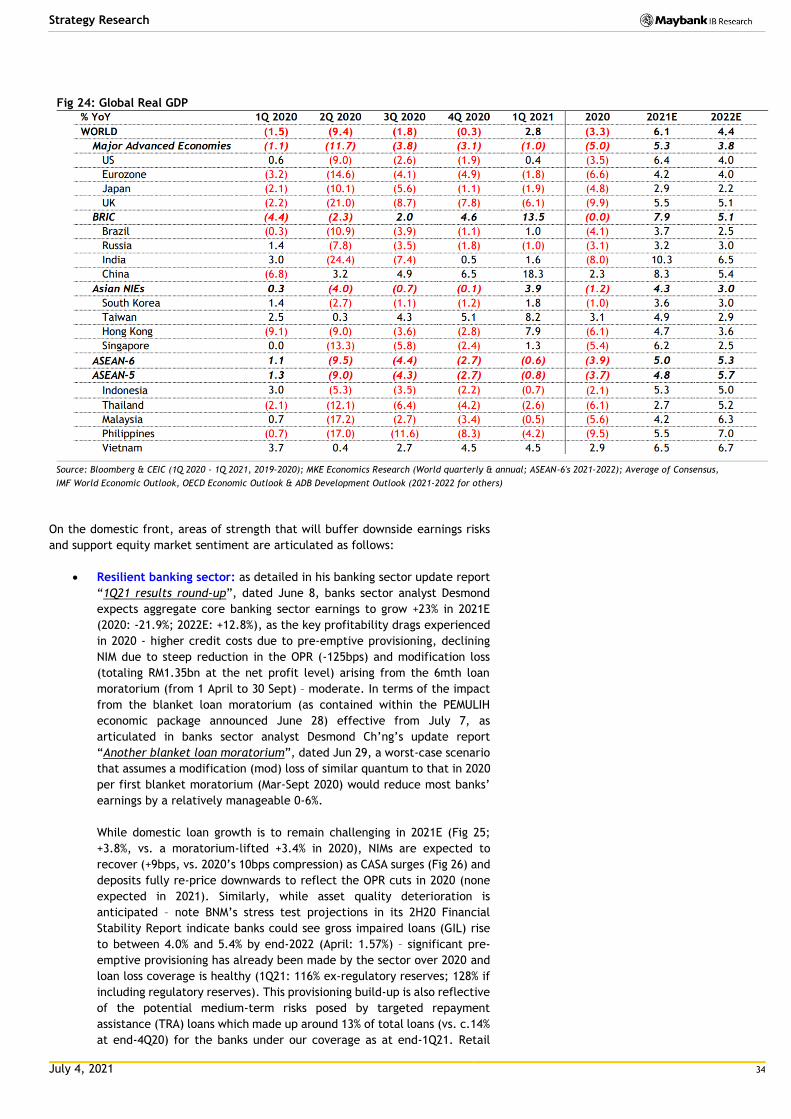

% YoY 1Q 2020 2Q 2020 3Q 2020 4Q 2020 1Q 2021 2020 2021E 2022E

WORLD (1.5) (9.4) (1.8) (0.3) 2.8 (3.3) 6.1 4.4

Major Advanced Economies (1.1) (11.7) (3.8) (3.1) (1.0) (5.0) 5.3 3.8

US 0.6 (9.0) (2.6) (1.9) 0.4 (3.5) 6.4 4.0

Eurozone (3.2) (14.6) (4.1) (4.9) (1.8) (6.6) 4.2 4.0

Japan (2.1) (10.1) (5.6) (1.1) (1.9) (4.8) 2.9 2.2

UK (2.2) (21.0) (8.7) (7.8) (6.1) (9.9) 5.5 5.1

BRIC (4.4) (2.3) 2.0 4.6 13.5 (0.0) 7.9 5.1

Brazil (0.3) (10.9) (3.9) (1.1) 1.0 (4.1) 3.7 2.5

Russia 1.4 (7.8) (3.5) (1.8) (1.0) (3.1) 3.2 3.0

India 3.0 (24.4) (7.4) 0.5 1.6 (8.0) 10.3 6.5

China (6.8) 3.2 4.9 6.5 18.3 2.3 8.3 5.4

Asian NIEs 0.3 (4.0) (0.7) (0.1) 3.9 (1.2) 4.3 3.0

South Korea 1.4 (2.7) (1.1) (1.2) 1.8 (1.0) 3.6 3.0

Taiwan 2.5 0.3 4.3 5.1 8.2 3.1 4.9 2.9

Hong Kong (9.1) (9.0) (3.6) (2.8) 7.9 (6.1) 4.7 3.6

Singapore 0.0 (13.3) (5.8) (2.4) 1.3 (5.4) 6.2 2.5

ASEAN-6 1.1 (9.5) (4.4) (2.7) (0.6) (3.9) 4.8 5.4

ASEAN-5 1.3 (9.0) (4.3) (2.7) (0.8) (3.7) 4.6 5.8

Indonesia 3.0 (5.3) (3.5) (2.2) (0.7) (2.1) 4.8 5.4

Thailand (2.1) (12.1) (6.4) (4.2) (2.6) (6.1) 2.7 5.2

Malaysia 0.7 (17.2) (2.7) (3.4) (0.5) (5.6) 4.2 6.3

Philippines (0.7) (17.0) (11.6) (8.3) (4.2) (9.5) 5.5 7.0

Vietnam 3.7 0.4 2.7 4.5 4.7 2.9 6.5 6.7

Source: Bloomberg & CEIC (1Q 2020 - 1Q 2021, 2019-2020); Maybank Kim Eng Economics Research (World quarterly & annual; ASEAN-6's 2021-2022); Average of Consesus, IMF World Economic Outlook, OECD Economic Outlook & ADB Development Outlook (2021-2022 for others)

5 Vietnam Economics - Modest 2Q GDP Recovery, Covid Wave Remains A Risk, 29 June 2021 6 Singapore Economics - Manufacturing Jumps on Low Base, Expect Flash 2Q GDP at +12.8%,

25 June 2021

July 4, 2021 12

Strategy Research

Figure 18: Global Real GDP & Global Composite Purchasing Managers Index (PMI)

Source: CEIC, Maybank Kim Eng

Consequently, and factoring in year-to-date performance, we revised upwards

forecasts for manufacturing sector growth (2021E: to +6.3% from +5.2% previously;

1Q 2021: +6.6% YoY; 2020: -2.6%) as well as for external trade growth i.e. exports

of goods and services (2021E: to +15.5% from +7.5% previously; 1Q 2021: +11.9%

YoY; 2020: -8.9%) and imports of goods & services (2021E: to +18.0% from +8.0%

previously; 1Q 2021: +13.0% YoY; 2020: -8.4%).

The upward revisions in the external trade growth forecasts also reflect the

upgrades in in-house forecasts for this year’s average prices for crude oil (Brent)

to USD65/bbl (USD55-60/bbl previously; 2020: USD42.3/bbl) and crude palm oil

(CPO) to MYR3,100/tonne (MYR2,700/tonne previously; 2020: MYR2,781/tonne).

Still sizeable impulse left in economic stimulus packages to

support public expenditure

Further cushioning the impact of the latest round of lockdown on the economy

is the continued expansionary fiscal policy via record Budget 2021 and rolling

economic stimulus packages.

To recap, since Mar 2020, the Government has announced eight economic stimulus

packages (Fig 19) totaling MYR530b (including MYR83b direct fiscal injections),

with the latest being a MYR150b package (including MYR10b direct fiscal injections)

dubbed “PEMULIH” on 28 June 2021 as the current FMCO or Phase 1 of NRP is

extended to July 2021 after being in place in June 2021.

Figure 19: Malaysia: Economic Stimulus Packages, 2020-2021

Date Announced

Packages Total Direct Fiscal Injection Utilised as at May 2021

(MYRb) MYRb % of 2020 GDP MYRb % of 2020 GDP

27-Mar-20 PRIHATIN 250 17.7 25 1.8 165.7

8-Apr-20 PRIHATIN SMEs 10 0.7 10 0.7

5-Jun-20 PENJANA 35 2.5 10 0.7 19.7

23-Sep-20 KITA PRIHATIN 10 0.7 10 0.7 9.3

18-Jan-21 PERMAI 15 1.1 2 0.1 2.3

17-Mar-21 PEMERKASA 20 1.4 11 0.7 0.05

31-May-21 PEMERKASA PLUS 40 2.8 5 0.4 -

28-Jun-21 PEMULIH 150 10.6 10 0.7 -

TOTAL 530 37.5 83 5.9 197.1

Source: Official announcements; PM Speeches, Ministry of Finance (LAKSANA Report #55, 3 June 2021)

(11)

(7)

(4)

0

4

7

35

40

45

50

55

60

1Q

20

17

2Q

20

17

3Q

20

17

4Q

20

17

1Q

20

18

2Q

20

18

3Q

20

18

4Q

20

18

1Q

20

19

2Q

20

19

3Q

20

19

4Q

20

19

1Q

20

20

2Q

20

20

3Q

20

20

4Q

20

20

1Q

20

21

Ap

r-M

ay 2

021

Global GDP (% YoY, RHS) Global Composite PMI

July 4, 2021 13

Strategy Research

62% of the total MYR530b economic stimulus packages still available after 38%

disbursed since 2020 up to June 2021. According to the Ministry of Finance, as

of May 2021, almost 60% of the measures and initiatives in the first six economic

stimulus packages totaling MYR340b have been implemented and MYR197.1b have

been disbursed7, with the latest tally at over MYR200b as of June 2021 according

to PM Speech when announcing the PEMULIH economic stimulus package on 28

June 2021. Thus there are around MYR330b left the total MYR530b from the eight

stimulus packages announced to-date.

Plus MYR185.5b or 57.5% of Budget 2021 spending allocation - and MYR17b or

26% of COVID-19 Fund - to be utilized. Further, of the record-high MYR322.5b

Budget 2021 total expenditure allocation, with MYR137b or 42.5% spent in Jan-May

2021, there are still MYR185.5b or 57.5% left for the rest of the year. In addition,

on the approved total for COVID-19 Fund of MYR65b, after the MYR38b spent in

2020 and MYR10b used in Jan-Apr 2021, there are MYR17b available which we

expect to be fully utilized by end-2021.

We estimated every MYR100b of these stimuli can boost GDP by 1.1-1.2 ppts.

Consequently, in view of the still sizeable positive impulse left from Budget

2021, economic stimulus packages and COVID-19 Fund, we raised our growth

forecasts for Government consumption (2021E: to +5.0% from +2.8% previously;

1Q 2021: +5.9% YoY; 2020: +3.9%) and maintain the mid-teen public investment

growth projection (2021E: +15.3%; 1Q 2021: -18.6% YoY; 2020: -21.4%). These take

into account of the implied acceleration in growth of Federal Government’s

operating and development expenditures in 2Q-4Q 2021 averaging +16.2% YoY (1Q

2021: +0.2% YoY) and +68.6% YoY per quarter (1Q 2021: +34.9% YoY) respectively.

Public investment is also supported by the on-going major infrastructure projects

as well as the rollout of digital infrastructure capex.

We also changed our 2021 budget deficit forecast to 6.8% of GDP from 6.0% of

GDP previously (note: original Budget 2021 target was 5.4% of GDP), factoring

in the additional direct fiscal injection from the latest economic stimulus package;

revenue and denominator impact of the downward revision in this year’s GDP

growth; and upsides to oil-related income from higher crude oil price assumption

(note: our sensitivity analysis showed every USD10/bbl increase in annual average

crude oil price can lift Government’s oil tax revenues by MYR4b and Petronas

dividend by MYR3.4b).

Private investment on the mend

We cut our private investment growth forecast for this year to +4.1% from

+6.3% previously (2020: -11.9%) amid the challenging business and operating

environment given the ins-and-outs of MCOs.

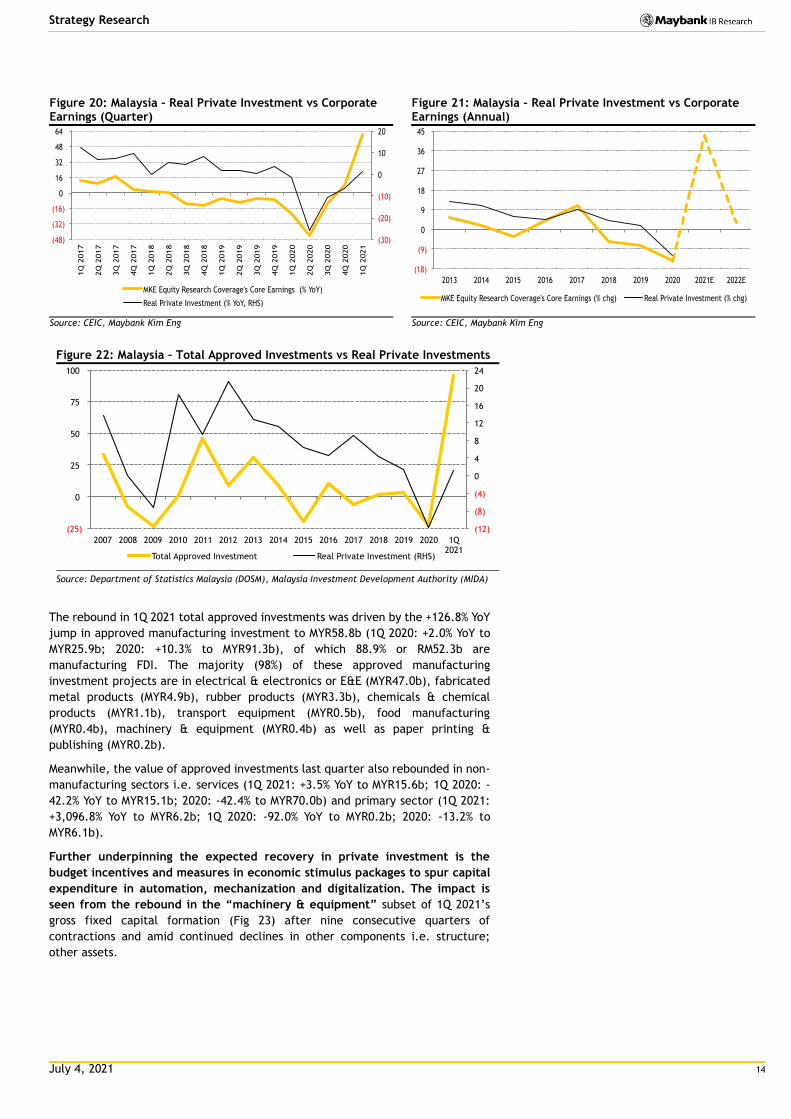

Positively though – and supporting our outlook of rebound this year, private

investment posted its first quarterly YoY growth in 1Q 2021 amid recovery in a

key indicator i.e. corporate earnings (Fig 20-21). Earnings of our Equity Research

Team’s stock coverage are projected to bounce back by +43.1% in 2021 (2020: -

14.4%).

In addition, total approved investments surged +95.6% YoY in 1Q 2021 to

MYR80.6b (1Q 2020: -29.4% YoY to MYR38.1b; 2020: -19.5% to MYR167.4b),

which augurs well for real private investment outlook (Fig 22). According to the

Malaysian Investment Development Authority (MIDA), there are MYR54.4b worth of

manufacturing and services investment applications in the pipeline pending

approvals.

7 Ministry of Finance’s LAKSANA Report #55, 3 June 2021

July 4, 2021 14

Strategy Research

Figure 20: Malaysia – Real Private Investment vs Corporate Earnings (Quarter)

Figure 21: Malaysia – Real Private Investment vs Corporate Earnings (Annual)

Source: CEIC, Maybank Kim Eng Source: CEIC, Maybank Kim Eng

Figure 22: Malaysia – Total Approved Investments vs Real Private Investments

Source: Department of Statistics Malaysia (DOSM), Malaysia Investment Development Authority (MIDA)

The rebound in 1Q 2021 total approved investments was driven by the +126.8% YoY

jump in approved manufacturing investment to MYR58.8b (1Q 2020: +2.0% YoY to

MYR25.9b; 2020: +10.3% to MYR91.3b), of which 88.9% or RM52.3b are

manufacturing FDI. The majority (98%) of these approved manufacturing

investment projects are in electrical & electronics or E&E (MYR47.0b), fabricated

metal products (MYR4.9b), rubber products (MYR3.3b), chemicals & chemical

products (MYR1.1b), transport equipment (MYR0.5b), food manufacturing

(MYR0.4b), machinery & equipment (MYR0.4b) as well as paper printing &

publishing (MYR0.2b).

Meanwhile, the value of approved investments last quarter also rebounded in non-

manufacturing sectors i.e. services (1Q 2021: +3.5% YoY to MYR15.6b; 1Q 2020: -

42.2% YoY to MYR15.1b; 2020: -42.4% to MYR70.0b) and primary sector (1Q 2021:

+3,096.8% YoY to MYR6.2b; 1Q 2020: -92.0% YoY to MYR0.2b; 2020: -13.2% to

MYR6.1b).

Further underpinning the expected recovery in private investment is the

budget incentives and measures in economic stimulus packages to spur capital

expenditure in automation, mechanization and digitalization. The impact is

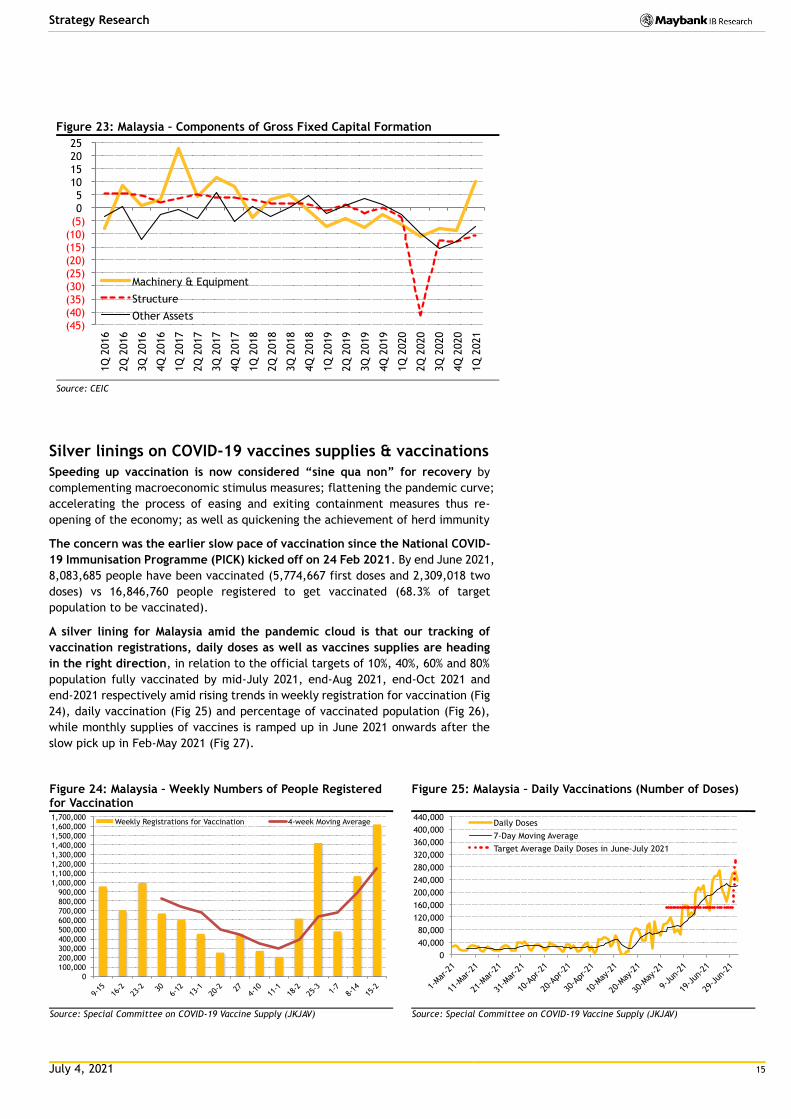

seen from the rebound in the “machinery & equipment” subset of 1Q 2021’s

gross fixed capital formation (Fig 23) after nine consecutive quarters of

contractions and amid continued declines in other components i.e. structure;

other assets.

(30)

(20)

(10)

0

10

20

(48)

(32)

(16)

0

16

32

48

64

1Q

2017

2Q

2017

3Q

2017

4Q

2017

1Q

2018

2Q

2018

3Q

2018

4Q

2018

1Q

2019

2Q

2019

3Q

2019

4Q

2019

1Q

2020

2Q

2020

3Q

2020

4Q

2020

1Q

2021

MKE Equity Research Coverage's Core Earnings (% YoY)

Real Private Investment (% YoY, RHS)

(18)

(9)

0

9

18

27

36

45

2013 2014 2015 2016 2017 2018 2019 2020 2021E 2022E

MKE Equity Research Coverage's Core Earnings (% chg) Real Private Investment (% chg)

(12)

(8)

(4)

0

4

8

12

16

20

24

(25)

0

25

50

75

100

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 1Q 2021

Total Approved Investment Real Private Investment (RHS)

July 4, 2021 15

Strategy Research

Figure 23: Malaysia – Components of Gross Fixed Capital Formation

Source: CEIC

Silver linings on COVID-19 vaccines supplies & vaccinations

Speeding up vaccination is now considered “sine qua non” for recovery by

complementing macroeconomic stimulus measures; flattening the pandemic curve;

accelerating the process of easing and exiting containment measures thus re-

opening of the economy; as well as quickening the achievement of herd immunity

The concern was the earlier slow pace of vaccination since the National COVID-

19 Immunisation Programme (PICK) kicked off on 24 Feb 2021. By end June 2021,

8,083,685 people have been vaccinated (5,774,667 first doses and 2,309,018 two

doses) vs 16,846,760 people registered to get vaccinated (68.3% of target

population to be vaccinated).

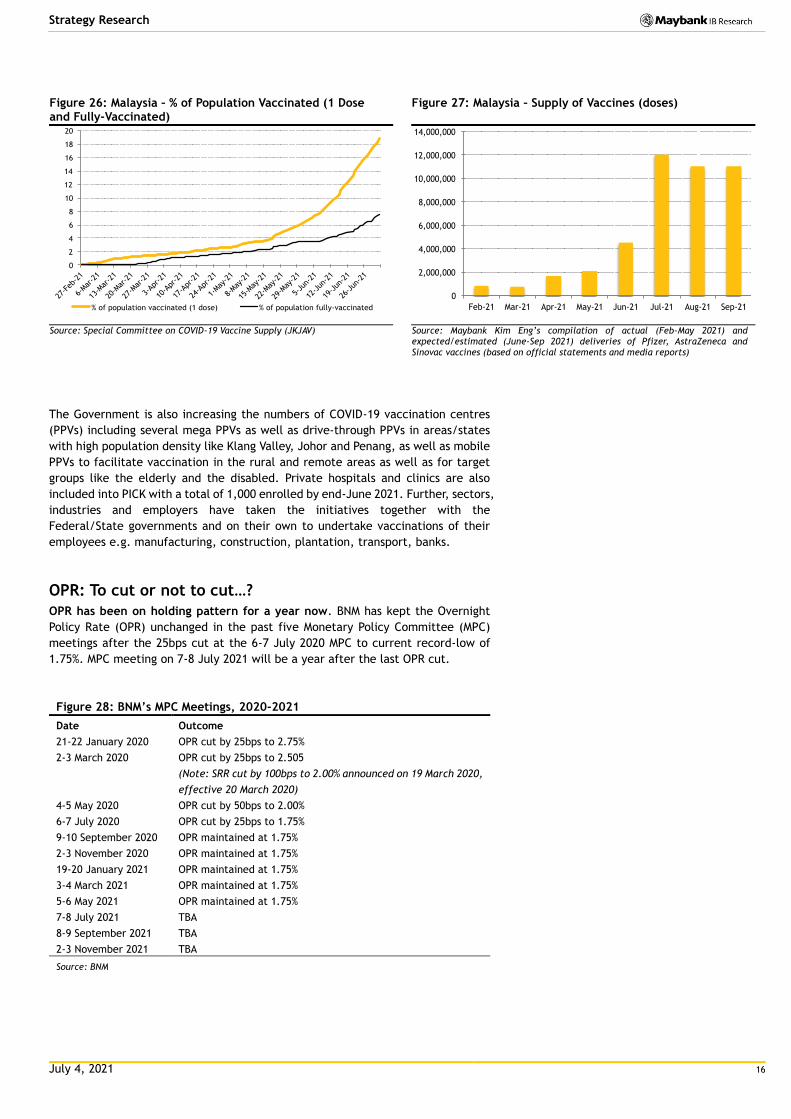

A silver lining for Malaysia amid the pandemic cloud is that our tracking of

vaccination registrations, daily doses as well as vaccines supplies are heading

in the right direction, in relation to the official targets of 10%, 40%, 60% and 80%

population fully vaccinated by mid-July 2021, end-Aug 2021, end-Oct 2021 and

end-2021 respectively amid rising trends in weekly registration for vaccination (Fig

24), daily vaccination (Fig 25) and percentage of vaccinated population (Fig 26),

while monthly supplies of vaccines is ramped up in June 2021 onwards after the

slow pick up in Feb-May 2021 (Fig 27).

Figure 24: Malaysia – Weekly Numbers of People Registered for Vaccination

Figure 25: Malaysia – Daily Vaccinations (Number of Doses)

Source: Special Committee on COVID-19 Vaccine Supply (JKJAV) Source: Special Committee on COVID-19 Vaccine Supply (JKJAV)

(45)

(40)

(35)

(30)

(25)

(20)

(15)

(10)

(5)

0

5

10

15

20

25

1Q

2016

2Q

2016

3Q

2016

4Q

2016

1Q

2017

2Q

2017

3Q

2017

4Q

2017

1Q

2018

2Q

2018

3Q

2018

4Q

2018

1Q

2019

2Q

2019

3Q

2019

4Q

2019

1Q

2020

2Q

2020

3Q

2020

4Q

2020

1Q

2021

Machinery & Equipment

Structure

Other Assets

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1,100,000

1,200,000

1,300,000

1,400,000

1,500,000

1,600,000

1,700,000

9-15

16-2

23-2 30

6-12

13-1

20-2 27

4-10

11-1

18-2

25-3 1-

7

8-14

15-2

Weekly Registrations for Vaccination 4-week Moving Average

0

40,000

80,000

120,000

160,000

200,000

240,000

280,000

320,000

360,000

400,000

440,000

1-Mar

-21

11-M

ar-2

1

21-M

ar-2

1

31-M

ar-2

1

10-A

pr-2

1

20-A

pr-2

1

30-A

pr-2

1

10-M

ay-2

1

20-M

ay-2

1

30-M

ay-2

1

9-Ju

n-21

19-J

un-2

1

29-J

un-2

1

Daily Doses

7-Day Moving Average

Target Average Daily Doses in June-July 2021

July 4, 2021 16

Strategy Research

Figure 26: Malaysia – % of Population Vaccinated (1 Dose and Fully-Vaccinated)

Figure 27: Malaysia – Supply of Vaccines (doses)

Source: Special Committee on COVID-19 Vaccine Supply (JKJAV) Source: Maybank Kim Eng’s compilation of actual (Feb-May 2021) and expected/estimated (June-Sep 2021) deliveries of Pfizer, AstraZeneca and Sinovac vaccines (based on official statements and media reports)

The Government is also increasing the numbers of COVID-19 vaccination centres

(PPVs) including several mega PPVs as well as drive-through PPVs in areas/states

with high population density like Klang Valley, Johor and Penang, as well as mobile

PPVs to facilitate vaccination in the rural and remote areas as well as for target

groups like the elderly and the disabled. Private hospitals and clinics are also

included into PICK with a total of 1,000 enrolled by end-June 2021. Further, sectors,

industries and employers have taken the initiatives together with the

Federal/State governments and on their own to undertake vaccinations of their

employees e.g. manufacturing, construction, plantation, transport, banks.

OPR: To cut or not to cut…?

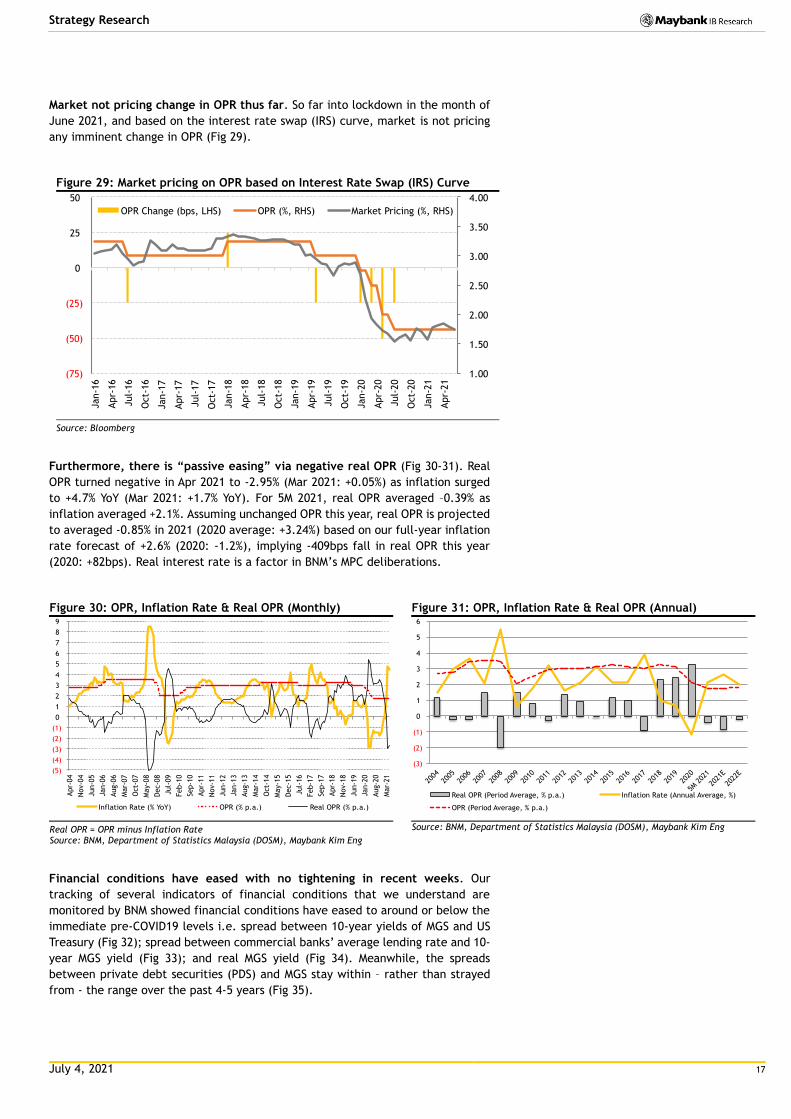

OPR has been on holding pattern for a year now. BNM has kept the Overnight

Policy Rate (OPR) unchanged in the past five Monetary Policy Committee (MPC)

meetings after the 25bps cut at the 6-7 July 2020 MPC to current record-low of

1.75%. MPC meeting on 7-8 July 2021 will be a year after the last OPR cut.

Figure 28: BNM’s MPC Meetings, 2020-2021

Date Outcome

21-22 January 2020 OPR cut by 25bps to 2.75%

2-3 March 2020 OPR cut by 25bps to 2.505

(Note: SRR cut by 100bps to 2.00% announced on 19 March 2020,

effective 20 March 2020)

4-5 May 2020 OPR cut by 50bps to 2.00%

6-7 July 2020 OPR cut by 25bps to 1.75%

9-10 September 2020 OPR maintained at 1.75%

2-3 November 2020 OPR maintained at 1.75%

19-20 January 2021 OPR maintained at 1.75%

3-4 March 2021 OPR maintained at 1.75%

5-6 May 2021 OPR maintained at 1.75%

7-8 July 2021 TBA

8-9 September 2021 TBA

2-3 November 2021 TBA

Source: BNM

0

2

4

6

8

10

12

14

16

18

20

27-F

eb-2

1

6-Mar

-21

13-M

ar-2

1

20-M

ar-2

1

27-M

ar-2

1

3-Ap

r-21

10-A

pr-2

1

17-A

pr-2

1

24-A

pr-2

1

1-May

-21

8-May

-21

15-M

ay-2

1

22-M

ay-2

1

29-M

ay-2

1

5-Ju

n-21

12-J

un-2

1

19-J

un-2

1

26-J

un-2

1

% of population vaccinated (1 dose) % of population fully-vaccinated

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21

July 4, 2021 17

Strategy Research

Market not pricing change in OPR thus far. So far into lockdown in the month of

June 2021, and based on the interest rate swap (IRS) curve, market is not pricing

any imminent change in OPR (Fig 29).

Figure 29: Market pricing on OPR based on Interest Rate Swap (IRS) Curve

Source: Bloomberg

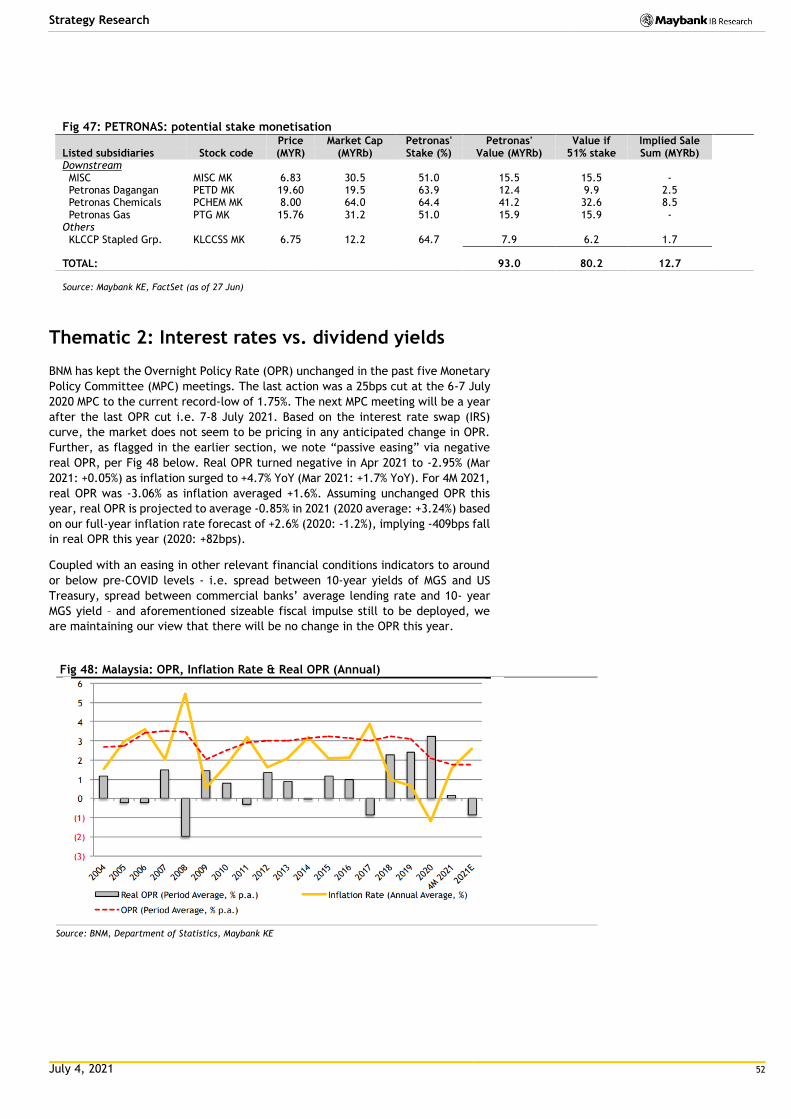

Furthermore, there is “passive easing” via negative real OPR (Fig 30-31). Real

OPR turned negative in Apr 2021 to -2.95% (Mar 2021: +0.05%) as inflation surged

to +4.7% YoY (Mar 2021: +1.7% YoY). For 5M 2021, real OPR averaged –0.39% as

inflation averaged +2.1%. Assuming unchanged OPR this year, real OPR is projected

to averaged -0.85% in 2021 (2020 average: +3.24%) based on our full-year inflation

rate forecast of +2.6% (2020: -1.2%), implying -409bps fall in real OPR this year

(2020: +82bps). Real interest rate is a factor in BNM’s MPC deliberations.

Figure 30: OPR, Inflation Rate & Real OPR (Monthly) Figure 31: OPR, Inflation Rate & Real OPR (Annual)

Real OPR = OPR minus Inflation Rate Source: BNM, Department of Statistics Malaysia (DOSM), Maybank Kim Eng

Source: BNM, Department of Statistics Malaysia (DOSM), Maybank Kim Eng

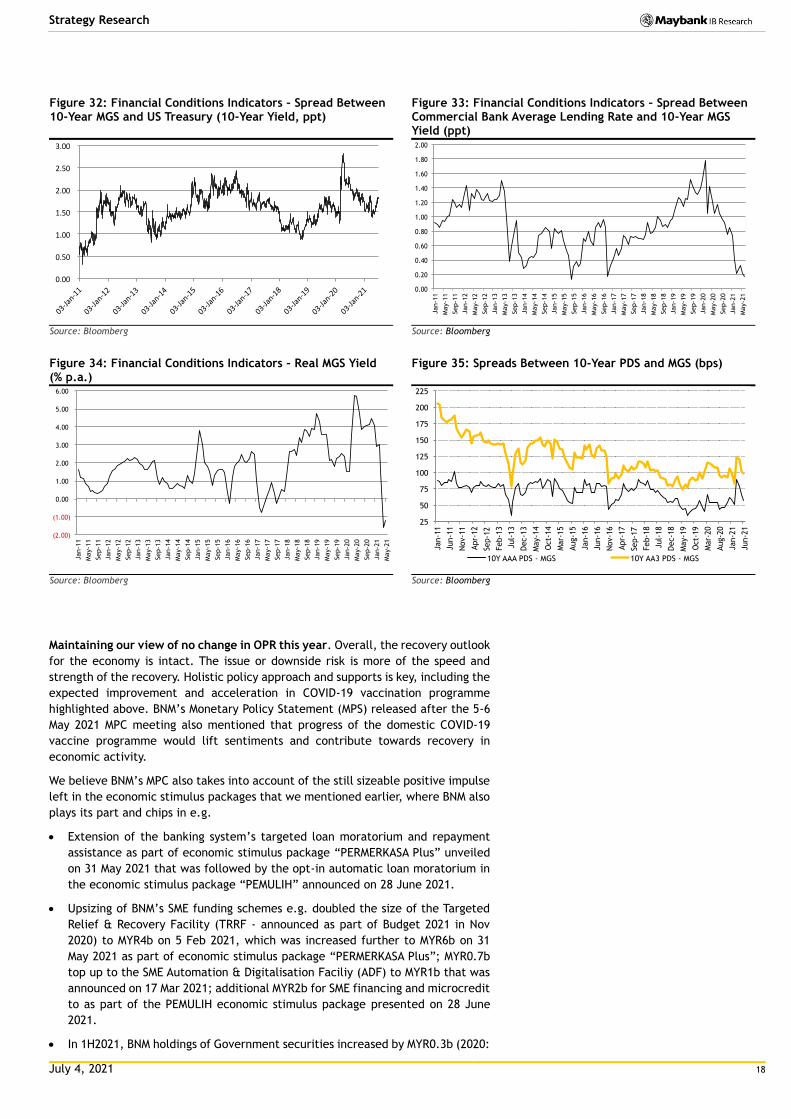

Financial conditions have eased with no tightening in recent weeks. Our

tracking of several indicators of financial conditions that we understand are

monitored by BNM showed financial conditions have eased to around or below the

immediate pre-COVID19 levels i.e. spread between 10-year yields of MGS and US

Treasury (Fig 32); spread between commercial banks’ average lending rate and 10-

year MGS yield (Fig 33); and real MGS yield (Fig 34). Meanwhile, the spreads

between private debt securities (PDS) and MGS stay within – rather than strayed

from - the range over the past 4-5 years (Fig 35).

1.00

1.50

2.00

2.50

3.00

3.50

4.00

(75)

(50)

(25)

0

25

50

Jan-1

6

Apr-

16

Jul-

16

Oct-

16

Jan-1

7

Apr-

17

Jul-

17

Oct-

17

Jan-1

8

Apr-

18

Jul-

18

Oct-

18

Jan-1

9

Apr-

19

Jul-

19

Oct-

19

Jan-2

0

Apr-

20

Jul-

20

Oct-

20

Jan-2

1

Apr-

21

OPR Change (bps, LHS) OPR (%, RHS) Market Pricing (%, RHS)

(5)

(4)

(3)

(2)

(1)

0

1

2

3

4

5

6

7

8

9

Apr-

04

Nov-

04

Jun-0

5

Jan-0

6

Aug-0

6

Mar-

07

Oct-

07

May-0

8

Dec-0

8

Jul-

09

Feb-1

0

Sep-1

0

Apr-

11

Nov-

11

Jun-1

2

Jan-1

3

Aug-1

3

Mar-

14

Oct-

14

May-1

5

Dec-1

5

Jul-

16

Feb-1

7

Sep-1

7

Apr-

18

Nov-

18

Jun-1

9

Jan-2

0

Aug-2

0

Mar-

21

Inflation Rate (% YoY) OPR (% p.a.) Real OPR (% p.a.)

(3)

(2)

(1)

0

1

2

3

4

5

6

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

5M 202

1

2021

E

2022

E

Real OPR (Period Average, % p.a.) Inflation Rate (Annual Average, %)

OPR (Period Average, % p.a.)

July 4, 2021 18

Strategy Research

Figure 32: Financial Conditions Indicators – Spread Between 10-Year MGS and US Treasury (10-Year Yield, ppt)

Figure 33: Financial Conditions Indicators – Spread Between Commercial Bank Average Lending Rate and 10-Year MGS Yield (ppt)

Source: Bloomberg Source: Bloomberg

Figure 34: Financial Conditions Indicators – Real MGS Yield (% p.a.)

Figure 35: Spreads Between 10-Year PDS and MGS (bps)

Source: Bloomberg Source: Bloomberg

Maintaining our view of no change in OPR this year. Overall, the recovery outlook

for the economy is intact. The issue or downside risk is more of the speed and

strength of the recovery. Holistic policy approach and supports is key, including the

expected improvement and acceleration in COVID-19 vaccination programme

highlighted above. BNM’s Monetary Policy Statement (MPS) released after the 5-6

May 2021 MPC meeting also mentioned that progress of the domestic COVID-19

vaccine programme would lift sentiments and contribute towards recovery in

economic activity.

We believe BNM’s MPC also takes into account of the still sizeable positive impulse

left in the economic stimulus packages that we mentioned earlier, where BNM also

plays its part and chips in e.g.

Extension of the banking system’s targeted loan moratorium and repayment

assistance as part of economic stimulus package “PERMERKASA Plus” unveiled

on 31 May 2021 that was followed by the opt-in automatic loan moratorium in

the economic stimulus package “PEMULIH” announced on 28 June 2021.

Upsizing of BNM’s SME funding schemes e.g. doubled the size of the Targeted

Relief & Recovery Facility (TRRF - announced as part of Budget 2021 in Nov

2020) to MYR4b on 5 Feb 2021, which was increased further to MYR6b on 31

May 2021 as part of economic stimulus package “PERMERKASA Plus”; MYR0.7b

top up to the SME Automation & Digitalisation Faciliy (ADF) to MYR1b that was

announced on 17 Mar 2021; additional MYR2b for SME financing and microcredit

to as part of the PEMULIH economic stimulus package presented on 28 June

2021.

In 1H2021, BNM holdings of Government securities increased by MYR0.3b (2020:

0.00

0.50

1.00

1.50

2.00

2.50

3.00

03-Jan-11

03-Jan-12

03-Jan-13

03-Jan-14

03-Jan-15

03-Jan-16

03-Jan-17

03-Jan-18

03-Jan-19

03-Jan-20

03-Jan-21 0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Jan-1

1

May-1

1

Sep-1

1

Jan-1

2

May-1

2

Sep-1

2

Jan-1

3

May-1

3

Sep-1

3

Jan-1

4

May-1

4

Sep-1

4

Jan-1

5

May-1

5

Sep-1

5

Jan-1

6

May-1

6

Sep-1

6

Jan-1

7

May-1

7

Sep-1

7

Jan-1

8

May-1

8

Sep-1

8

Jan-1

9

May-1

9

Sep-1

9

Jan-2

0

May-2

0

Sep-2

0

Jan-2

1

May-2

1

(2.00)

(1.00)

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Jan-1

1

May-1

1

Sep-1

1

Jan-1

2

May-1

2

Sep-1

2

Jan-1

3

May-1

3

Sep-1

3

Jan-1

4

May-1

4

Sep-1

4

Jan-1

5

May-1

5

Sep-1

5

Jan-1

6

May-1

6

Sep-1

6

Jan-1

7

May-1

7

Sep-1

7

Jan-1

8

May-1

8

Sep-1

8

Jan-1

9

May-1

9

Sep-1

9

Jan-2

0

May-2

0

Sep-2

0

Jan-2

1

May-2

1

25

50

75

100

125

150

175

200

225

Jan-1

1

Jun-1

1

Nov-

11

Apr-

12

Sep-1

2

Feb-1

3

Jul-

13

Dec-1

3

May-1

4

Oct-

14

Mar-

15

Aug-1

5

Jan-1

6

Jun-1

6

Nov-

16

Apr-

17

Sep-1

7

Feb-1

8

Jul-

18

Dec-1

8

May-1

9

Oct-

19

Mar-

20

Aug-2

0

Jan-2

1

Jun-2

1

10Y AAA PDS - MGS 10Y AA3 PDS - MGS

July 4, 2021 19

Strategy Research

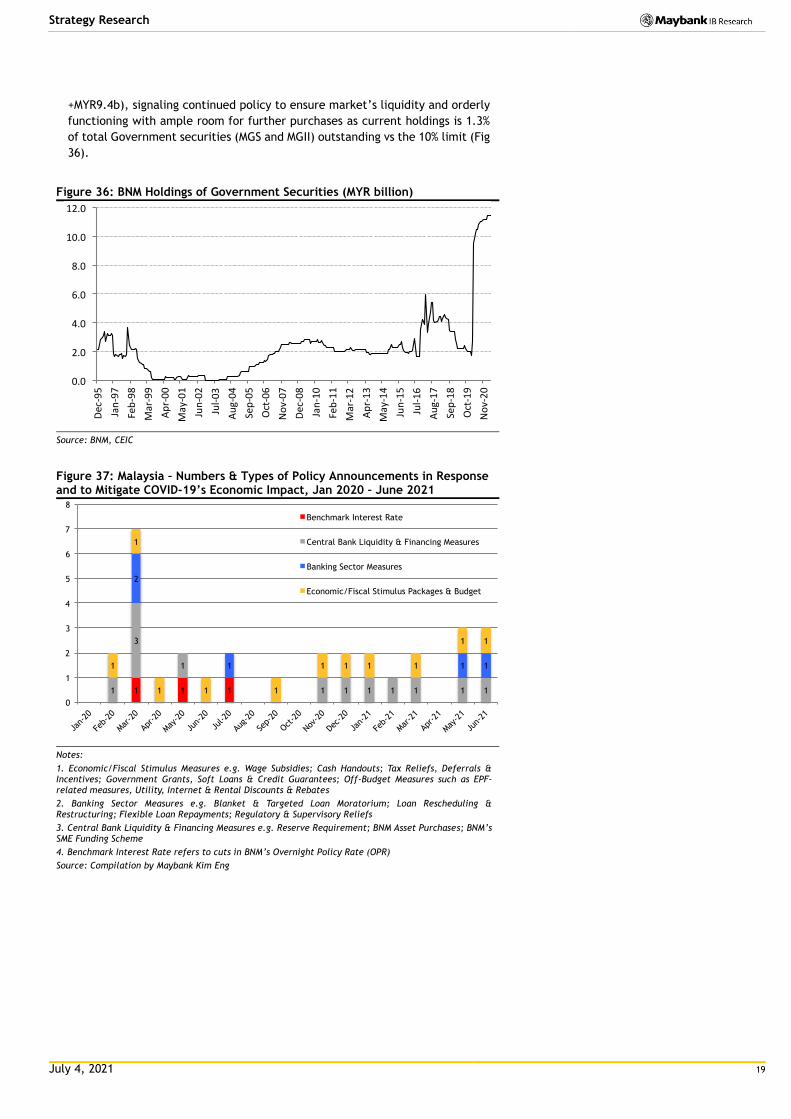

+MYR9.4b), signaling continued policy to ensure market’s liquidity and orderly

functioning with ample room for further purchases as current holdings is 1.3%

of total Government securities (MGS and MGII) outstanding vs the 10% limit (Fig

36).

Figure 36: BNM Holdings of Government Securities (MYR billion)

Source: BNM, CEIC

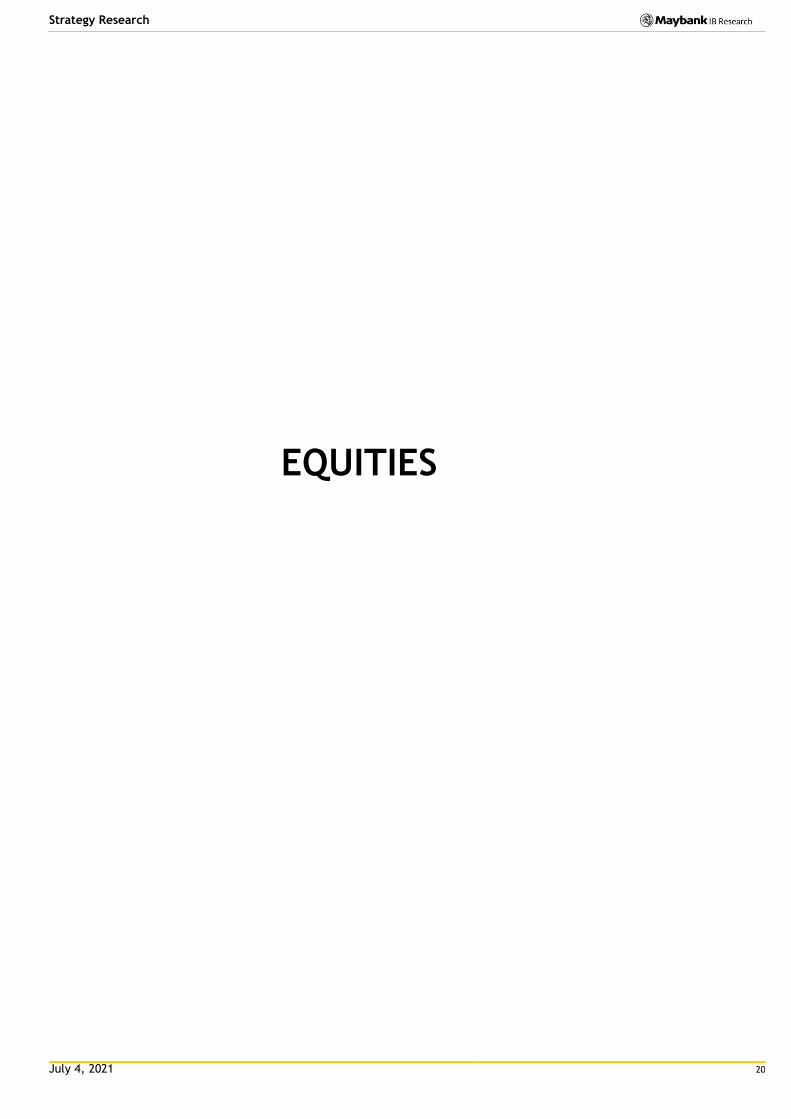

Figure 37: Malaysia – Numbers & Types of Policy Announcements in Response and to Mitigate COVID-19’s Economic Impact, Jan 2020 – June 2021

Notes:

1. Economic/Fiscal Stimulus Measures e.g. Wage Subsidies; Cash Handouts; Tax Reliefs, Deferrals & Incentives; Government Grants, Soft Loans & Credit Guarantees; Off-Budget Measures such as EPF-related measures, Utility, Internet & Rental Discounts & Rebates

2. Banking Sector Measures e.g. Blanket & Targeted Loan Moratorium; Loan Rescheduling & Restructuring; Flexible Loan Repayments; Regulatory & Supervisory Reliefs

3. Central Bank Liquidity & Financing Measures e.g. Reserve Requirement; BNM Asset Purchases; BNM’s SME Funding Scheme

4. Benchmark Interest Rate refers to cuts in BNM’s Overnight Policy Rate (OPR)

Source: Compilation by Maybank Kim Eng

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Dec-95

Jan-97

Feb-98

Mar-99

Apr-00

May-01

Jun-02

Jul-03

Aug-04

Sep-05

Oct-06

Nov-07

Dec-08

Jan-10

Feb-11

Mar-12

Apr-13

May-14

Jun-15

Jul-16

Aug-17

Sep-18

Oct-19

Nov-20

1 1 1 1

3

1

1 1 1 1 1 1 1

2

1 1 1 1

1

1 1 1

1 1 1 1

1 1

0

1

2

3

4

5

6

7

8

Jan-

20

Feb-

20

Mar

-20

Apr-20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct-2

0

Nov-2

0

Dec-

20

Jan-

21

Feb-

21

Mar

-21

Apr-21

May

-21

Jun-

21

Benchmark Interest Rate

Central Bank Liquidity & Financing Measures

Banking Sector Measures

Economic/Fiscal Stimulus Packages & Budget

July 4, 2021 20

Strategy Research

EQUITIES

July 4, 2021

ST

RAT

EG

Y

Mala

ysi

a

July 4, 2021 21

2H 2021 Outlook and Lookouts

Deferred, not derailed

COVID-centric setbacks = delayed market recovery

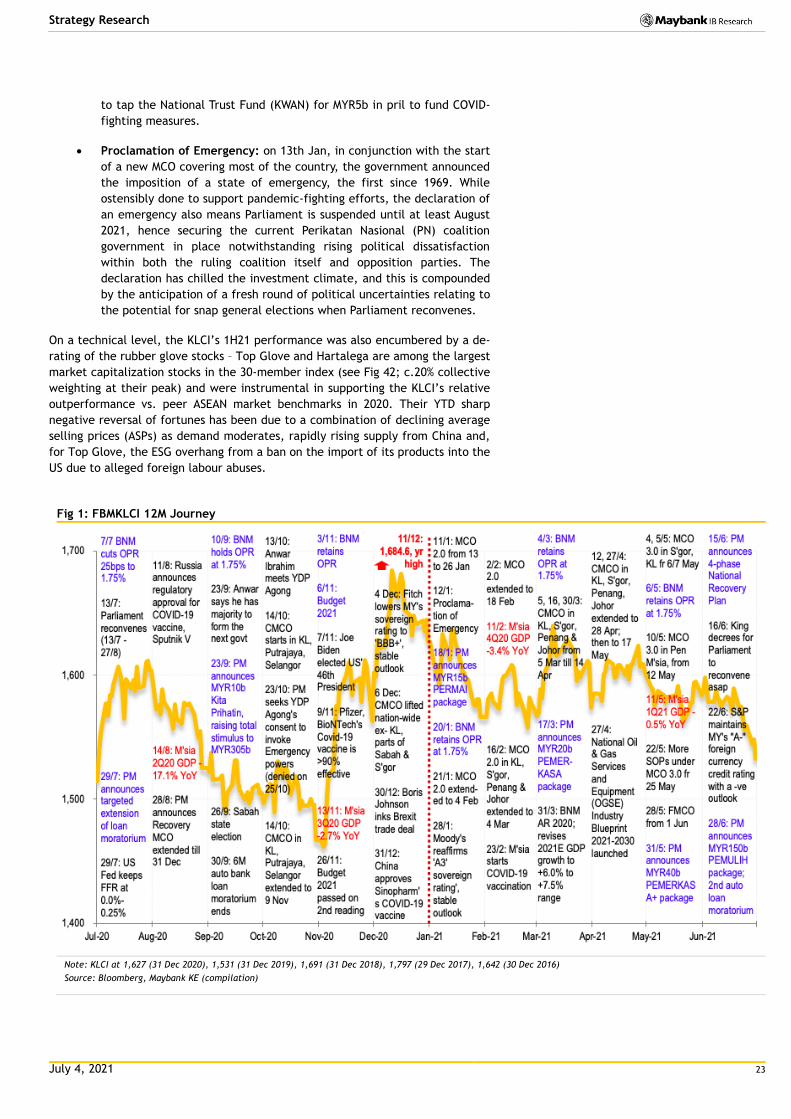

Bucking our bullish expectations, as articulated in our 2021 Strategy report (“Malaysia 2021 Market Outlook: Goldilocks makes a comeback”, dated Dec 14), of sustained recovery following broad uptrend over 4Q20, the KLCI’s momentum stalled into Jan, brought up short by the twin shocks of a renewed national Movement Control Order (MCO) and Proclamation of Emergency. Fiscal limitations and sustained institutional selling, both foreign and domestic, have also weighed negatively. However, while the path to full re-opening from the current lockdown (since June 1) looks to be an extended one, corporate earnings have proven largely resilient, and rapidly rising vaccination rates should allow investors to refocus on equities-supportive positives into 4Q21 i.e. accelerated earnings recovery, continued albeit moderated fiscal and monetary support, ample liquidity, commodities price recovery and relative attraction vs. fixed income. We retain a balanced positioning, via a mix of value and growth stocks, and continuing yield focus. Top BUYs (Fig 70) and Top SELLs (Fig 71) are detailed on pages 68-70, recommended ESG stock picks are per Fig 61, while conviction dividend picks (providing 5-9% cash yield) are in Fig 51.

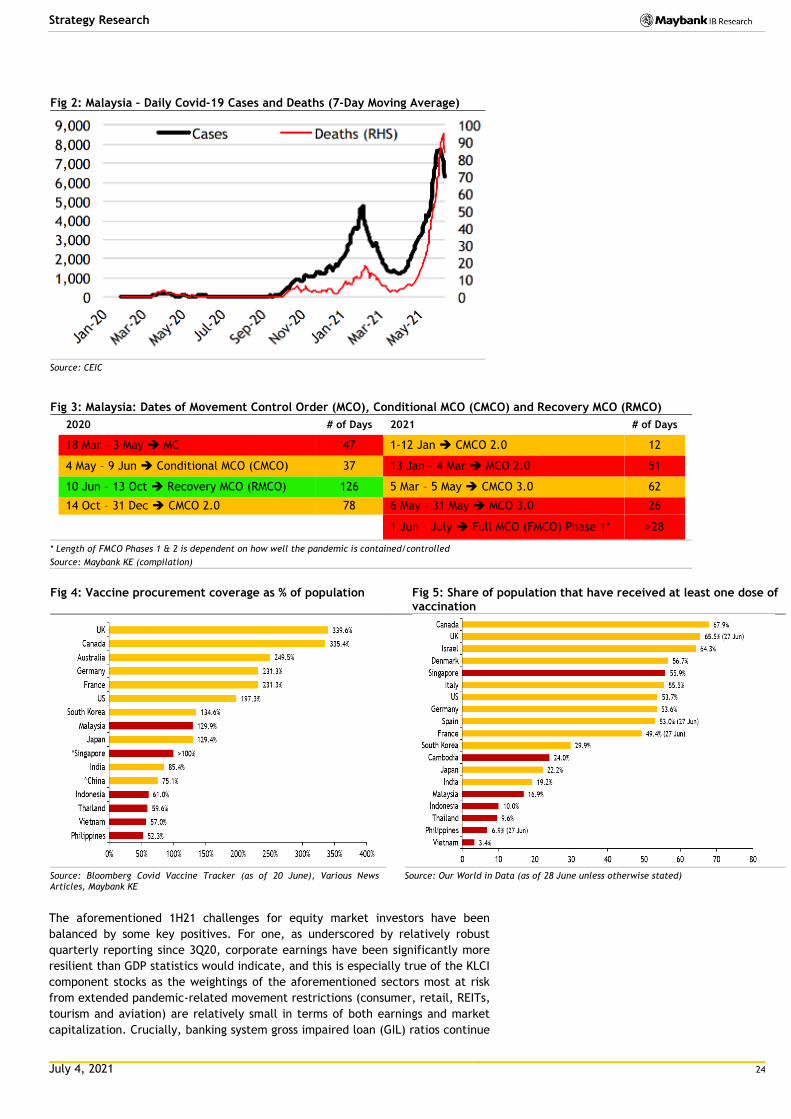

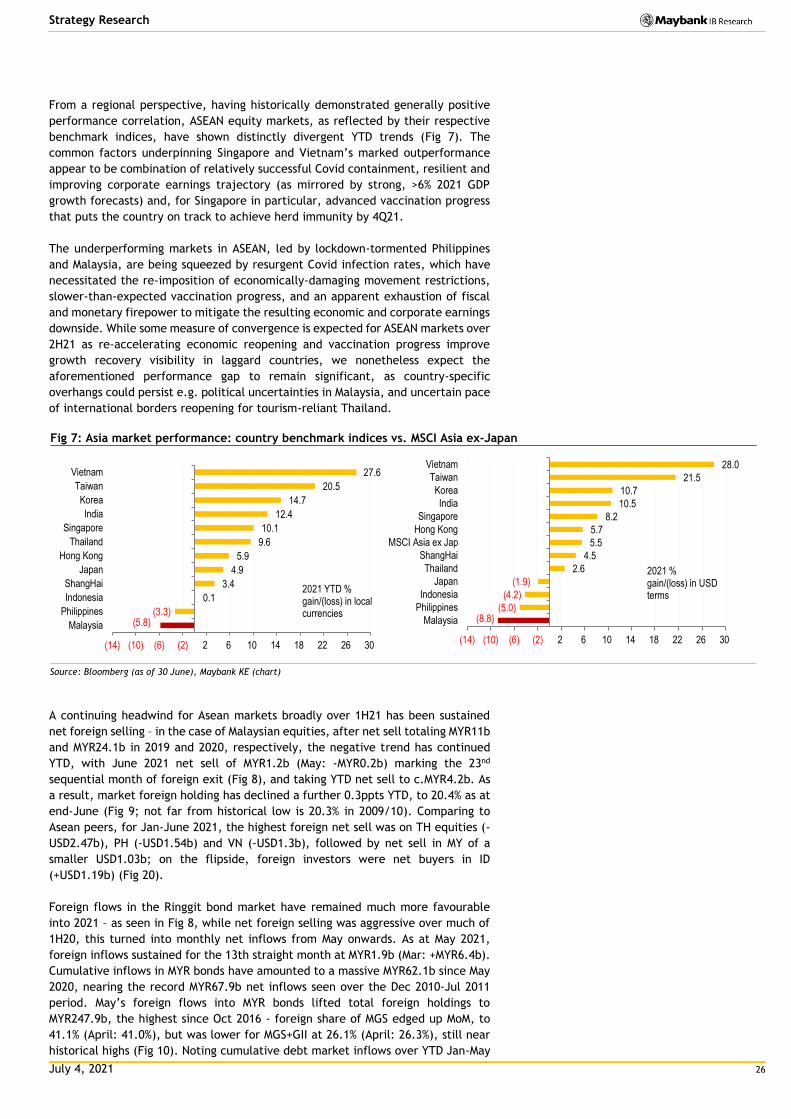

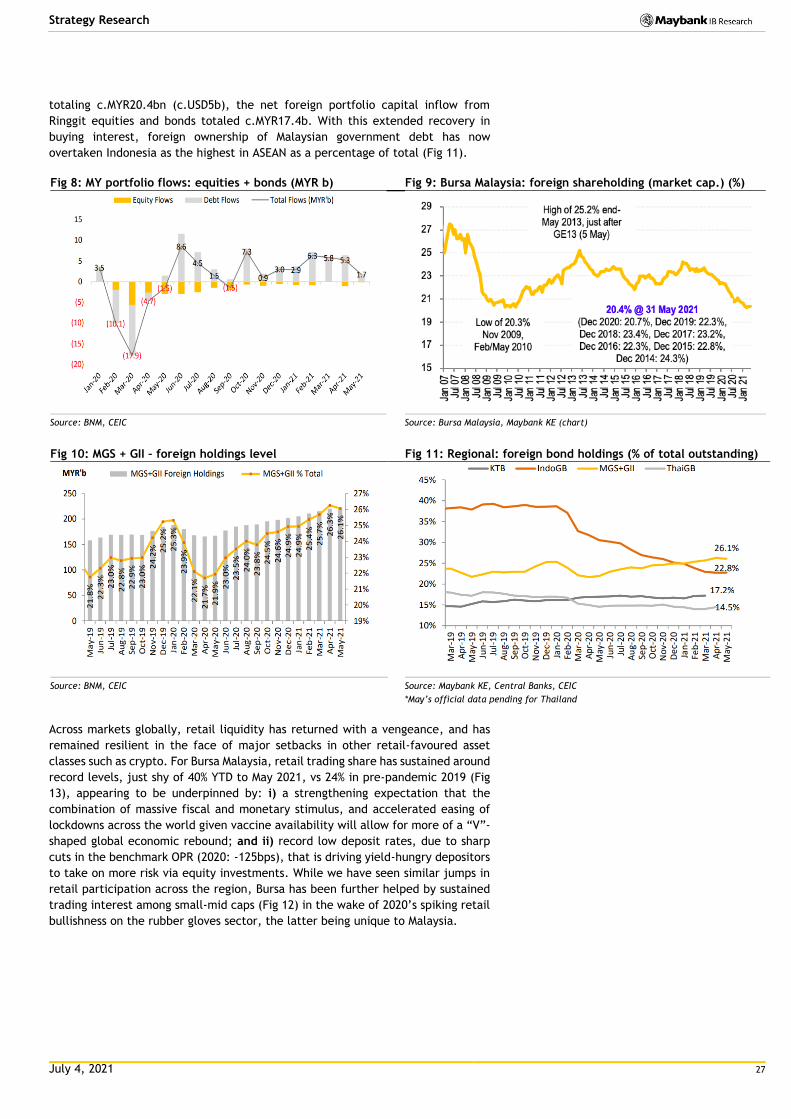

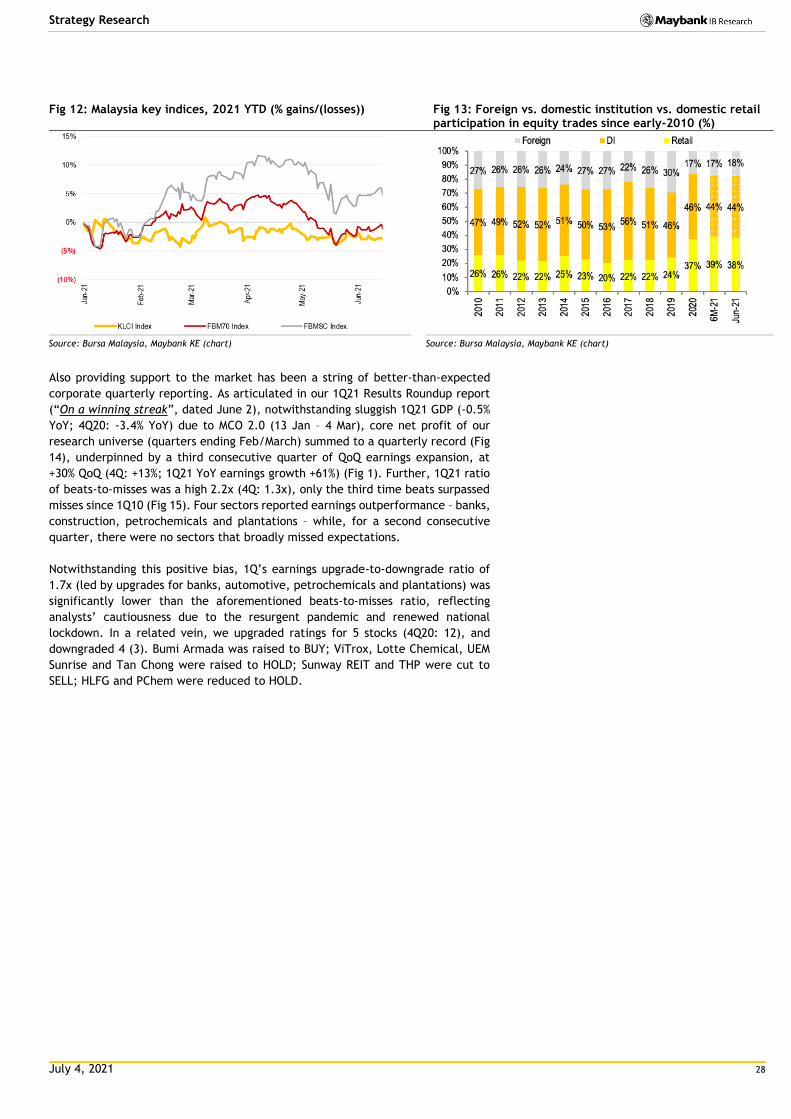

1H21 recap: renewed pandemic-led headwinds As captured by Fig 1, the KLCI has been range-bound through 1H21, as a combination of renewed uptrend in daily COVID cases (Fig 2) and slow pace of vaccinations resulted in disruptive Movement Control Orders (MCOs) of various intensities (Fig 3). Undershooting GDP and lack of fiscal space, as underscored by the government resorting to tapping the National Trust Fund, further dented sentiment and overshadowed some mitigating positives, the latter including generally robust corporate reporting (Fig 14), undershooting NPLs (Fig 27) and strength in the exports-oriented manufacturing and commodities sectors (crude oil, CPO). While retail participation remained near records (Fig 13), sustained net selling by both foreign and domestic institutional investors (Fig 19) resulted in the KLCI being the worst performing benchmark in ASEAN over 1H21 (Fig 7; -6% YTD).

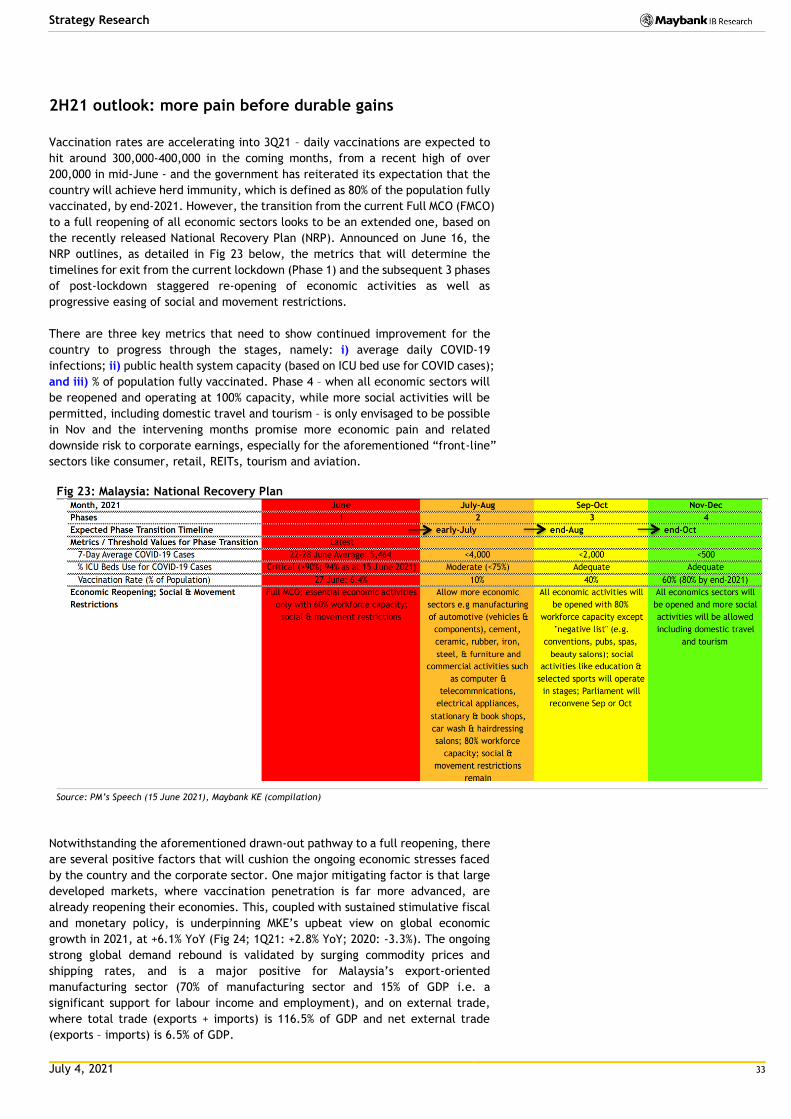

2H21 outlook: more pain before durable gains

Uncertain timeline for the National Recovery Plan (NRP; Fig 23), given the multiple preconditions necessary to enable phase transition, coupled with rising political risk ahead of the re-opening of Parliament, sets the market up for a difficult 3Q21. However, we see broadly improving visibility on these issues into 4Q21, with other equities-supportive factors including sharply higher vaccination rate, a more settled global economic recovery (Fig 24) and comparative asset class attraction vs. fixed income (Fig 35) and deposits, per negative real rates (Fig 31). Re thematics, GLC restructuring is unlikely to gain traction (though revival of the Axiata-DiGi merger is welcome; Figs 43-44) given backdrop of political volatility and continuing GLC/GLIC management changes. The dividend yield (Fig 50) and supply chain relocation (Figs 64-65) thematics offer much greater structural investability, as does sustainability / ESG investing (Figs 52-29; see our recently-published Malaysia ESG Compendium (“Sustainability: No longer optional”, dated April 8).

Balanced positioning, with ESG and yield overlays

In the wake of 1Q21 reporting, we continue to expect the KLCI to see sharp earnings recovery in 2021 (2020/2021F/2022F: -12.5%/+37.9%/+2.1%; if excluding glove stocks, adjusted 2021F/2022F: +28%/+14% YoY) after three straight years of earnings contraction. However, in factoring in extended NRP and political risks, we moderate end-2021 KLCI target to 1,720 (15x forward earnings, -0.5 SD vs. mean), from 1,830 (16x, in line with historical mean) previously. Re sector positioning changes, we downgrade Construction, Utilities and Gloves to Neutral (Fig 69), and raise Gaming to Overweight (GENT, BST). We continue to like Mid-cap Financials (HLBK, RHB, Allianz), Tech/Semicon (Inari, Greatech), Large-cap Oil & Gas (Dialog, Yinson), Plantations (KLK, BPlant) and Auto (BAuto). We are selective on Telcos (Telekom), REITs (Axis), Property (SP Setia) and Logistics (MISC); we are staying Underweight with regards the Aviation and Mid-cap O&G sectors.

KLCI vs. MSCI EM Index

Current KLCI: 1,533 (30-Jun-2021) YE KLCI target: 2021E 1,720 (15x forward PER)

Malaysia equities growth & valuation

2020A 2021E 2022E

KLCI @ 1,532.6 PE (x) 19.1 13.9 13.6 Earnings Growth (%) (12.5%) 37.9% 2.1

Research Universe PE (x) 21.2 15.1 14.5 Earnings Growth (%) (14.9%) 39.8% 4.2%

Top BUY picks

Stock BB Ticker Price TP Upside (%)

Large Caps Tenaga TNB MK 9.73 12.00 23.3% IHH IHH MK 5.61 6.30 12.3% HL Bank HLBK MK 18.82 20.90 11.1% MISC MISC MK 6.76 7.75 14.6% Hartalega HART MK 7.02 9.80 39.6% TM T MK 6.11 7.40 21.1% KLK KLK MK 20.32 29.60 45.7% RHB RHBBANK MK 5.39 6.30 16.9% Dialog DLG MK 2.88 4.90 70.1% Genting (M) GENM MK 2.80 3.38 20.8% Inari INRI MK 3.16 4.40 39.2% BIMB BIMB MK 3.85 4.75 23.4% Gamuda GAM MK 3.06 4.05 32.4% Greatech GREATEC MK 5.60 6.75 20.5% Heineken HEIM MK 23.00 26.60 15.7% IJM IJM MK 1.79 2.18 21.8% Bursa BURSA MK 7.88 10.75 36.4% SP Setia SPSB MK 1.09 1.39 27.5% Yinson YNS MK 5.07 6.65 31.2% Frontken FRCB MK 2.93 3.90 33.1% KPJ KPJ MK 1.02 1.13 10.8% Mid-small Caps Mega First MFCB MK 3.60 4.30 19.5% Allianz ALLZ MK 13.00 16.75 28.8% Axis REIT AXRB MK 1.94 2.20 13.4% Swk Oil Plm SOP MK 3.45 5.67 64.3% Bermaz BAUTO MK 1.55 2.25 45.1% Globetronic GTB MK 2.29 3.75 63.8% Bous. Plant BPLANT MK 0.57 0.79 38.6%

Source: Maybank KE, Factset (as of 2 Jul)

July 4, 2021 22

Strategy Research

1H21 recap: renewed pandemic-led headwinds

The KLCI enjoyed a strong, broad uptrend over the last two months of 2020 (Fig 1),

underpinned by rising optimism on the pace of economic reopening in the wake of

the multiple COVID-19 vaccine breakthroughs announced from early Nov, and the

expedited approvals and distribution in major economies from Dec. As articulated

in our 2021 Strategy report (“Malaysia 2021 Market Outlook: Goldilocks makes a

comeback”, dated Dec 14), we had anticipated sustained market recovery through

2021 given the equity-favouring investment backdrop of rapidly-improving vaccine

efficacy/availability, continuing accommodative fiscal and monetary policy,

rebounding commodity prices, and surging retail trading activity. A further

potential support for equities would be asset reallocation flows out of fixed income

per MKE’s mildly bearish outlook for Malaysian Government Securities (MGS) as

demand-supply dynamics broadly weaken following a period of extended

outperformance, and debt rating risk remains, as underscored by Fitch rating

downgrade in Dec 2020, and S&P retaining its negative outlook per June 2021

review.

Unfortunately, the KLCI’s momentum stalled into the New Year and the index has

been trading within a narrow range in 1H21, with the end-June close of 1,532

actually being a c.6% pullback from the end-2020 KLCI close of 1,627. Some of the

key headwinds that investors have had to contend with are as follows:

COVID resurgence: a combination of renewed uptrend in daily COVID

infection rate (Fig 2) and slower-than-expected pace of vaccinations

(Figs 4-5) resulted in renewed Movement Control Orders (MCOs) of

various intensities through 1H21 (Fig 3). Resulting restrictions on broad

economic activities and people movement have weighed on growth and

“return to normalcy” expectations, especially for the most directly-

impacted sectors such as consumer, retail, REITs, tourism and aviation.

Weak GDP traction: undershooting 4Q20 GDP, which shrank 3.4% YoY (3Q:

-2.6% YoY), resulted in 2020 GDP contraction of -5.6%, worse than both

official (-4.5%) and MKE (-5.4%) forecasts. With the re-imposition of MCOs

from early-Jan, culminating into Lockdown 1.0 from June 1 (no end date

as yet), the GDP outlook remains weak, as underscored by continued

contraction in 1Q21 GDP (-0.5% YoY) – in its recent update report

“Malaysia Macro:”Now-casting” slower 2021 GDP rebound”, dated June

12, the MKE economics team now expects the Malaysian economy to

rebound by a slower +4.2% in 2021, vs. +5.1% previously (official forecast

range: +6.0% to +7.5%).

Mounting fiscal stress: even as pandemic-related restrictions on

economic activities continue, the government’s ability to extend support

via fiscal spending packages appears to have reached its limit. While the

relatively modest MYR20b PEMERKASA package announced in March 2021

included MYR11b direct fiscal injections, the subsequent PEMERKASA Plus

package announced on May 31 (details in update report “MYR40b

stimulus package (PEMERKASA Plus) in response to “Lockdown 2.0””

dated June 1), while indicating double the headline stimulus amount of

MYR40b (see Fig 29 below), contains only around MYR5b worth of direct

fiscal injection, principally for public health, cash transfers, business

grants and wage subsidies. Most recently, the MYR150b PEMULIH

economic package (10.6% of GDP; see report “MYR150b economic

package (PEMULIH) as lockdown extended indefinitely”, dated June 29)

announced on June 28 contained just MYR10b direct fiscal injection, the

rest being off-balance sheet measures centered on a 6-month blanket

“opt-in” loan moratorium for individual borrowers, a new EPF withdrawal

scheme (i-Citra) and SME guarantees / funding by the government, Bank

Negara (BNM) and DFIs (Development Financial Institutions), as well as

GLCs (e.g. electricity bill discounts). Further, the government was forced

July 4, 2021 23

Strategy Research

to tap the National Trust Fund (KWAN) for MYR5b in pril to fund COVID-

fighting measures.

Proclamation of Emergency: on 13th Jan, in conjunction with the start

of a new MCO covering most of the country, the government announced

the imposition of a state of emergency, the first since 1969. While

ostensibly done to support pandemic-fighting efforts, the declaration of

an emergency also means Parliament is suspended until at least August

2021, hence securing the current Perikatan Nasional (PN) coalition

government in place notwithstanding rising political dissatisfaction

within both the ruling coalition itself and opposition parties. The

declaration has chilled the investment climate, and this is compounded

by the anticipation of a fresh round of political uncertainties relating to

the potential for snap general elections when Parliament reconvenes.

On a technical level, the KLCI’s 1H21 performance was also encumbered by a de-

rating of the rubber glove stocks – Top Glove and Hartalega are among the largest

market capitalization stocks in the 30-member index (see Fig 42; c.20% collective

weighting at their peak) and were instrumental in supporting the KLCI’s relative

outperformance vs. peer ASEAN market benchmarks in 2020. Their YTD sharp

negative reversal of fortunes has been due to a combination of declining average

selling prices (ASPs) as demand moderates, rapidly rising supply from China and,

for Top Glove, the ESG overhang from a ban on the import of its products into the

US due to alleged foreign labour abuses.

Fig 1: FBMKLCI 12M Journey

Note: KLCI at 1,627 (31 Dec 2020), 1,531 (31 Dec 2019), 1,691 (31 Dec 2018), 1,797 (29 Dec 2017), 1,642 (30 Dec 2016)