Embed Size (px)

Citation preview

7/23/2019 Silver Brochure

http://slidepdf.com/reader/full/silver-brochure 1/8

SILVERHEDGING PRICE RISK

“Purge the dross from the silver, and the material for a vessel comes forth for the silversmith”. The Bible

7/23/2019 Silver Brochure

http://slidepdf.com/reader/full/silver-brochure 2/8

OVERVIEW

PRICE RISK MANAGAMENT

Silver is a brilliant grey-white metal that

is soft and malleable. Its unique

properties include its strength,

malleability, ductility, electrical and

thermal conductivity, sensitivity, high

reflectance of light, and reactivity. Silver

is found in native form, as an alloy with

gold (electrum), and in ores containing

sulphur, arsenic, antimony or chlorine.

Risk management techniques are of

critical importance for participants, such

as producers, exporters, marketers,

processors, and SMEs. Modern

ilver has been used for thousands of years for ornaments and utensils,trade, and as the basis for many monetary systems. Its value as aS precious metal was long considered second only to gold. Silver and

silver alloys are used in the construction of high-quality musical windinstruments of many types. Silver's catalytic properties make it ideal for useas a catalyst in oxidation reactions, for example, the production of

formaldehyde from methanol and air by means of silver screens or crystallitescontaining a minimum 99.95 weight-percent silver. Silver (upon somesuitable support) is probably the only catalyst available today to convertethylene to ethylene oxide (later hydrolyzed to ethylene glycol used for making

polyesters—an important industrial reaction). It is also used in the Oddytest to detect reduced sulphur compounds and carbonyl sulfides. Because silverreadily absorbs free neutrons, it is commonly used to make control rods toregulate the fission chain reaction in pressurized water nuclear reactors,

generally as an alloy containing 80% silver, 15% indium, and 5%cadmium. Silver is used to make solder and brazing alloys, and as a thinlayer on bearing surfaces can provide a significant increase in gallingresistance and reduce wear under heavy load, particularly against steel.

Source: Wikipedia, Silver Institute

SILVER : HEDGING PRICE RISK

techniques and strategies, including

market-based risk management

financial instruments like 'Silver Futures',

offered on the MCX platform can

improve efficiencies and consolidate

competitiveness through price risk

management. The importance of risk

management cannot be overstated; the

government too has set up high-level

committees to suggest steps for

fulfilling the objectives of price

discovery and price risk management oncommodity derivative exchanges. The

role of commodity futures in risk

management consists of anticipating

price movement and shaping resource

allocations, and these ends can be

achieved through hedging.

Hedging is the process of reducing or

controlling risk. It involves taking equal

and opposite positions in two different

markets (such as spot and futures market),

with the objective of reducing or limiting

risks associated with price change. It is a

two-step process, where a gain or loss in

the physical position due to changes inprice will be offset by changes in the value

on the futures platform, thereby reducing

or limiting risks associated with

unpredictable changes in price.

HEDGING MECHANISM

Price Movement

CME Parity ` /Kg MCX /Kg `

2

30000

33000

36000

39000

42000

45000

48000

51000Firm US Dollar, fear of

hike in US interest ratesFed tapering

Possibililty hikeby US FED by September

of rate

Supply tightness

US Fed announces interestrates to remain low

Euro zone worries,safe haven buying

Feb 14 Apr 14 Jun 14 Aug 14 Oct 14 Dec 14 Feb 15 Apr 15 Jun 15 Aug 15

7/23/2019 Silver Brochure

http://slidepdf.com/reader/full/silver-brochure 3/8

3

Siemens India Limited

Endeavour Silver Corp.

Odyssey Marine Exploration,Inc

“The Company uses Commodity FutureContracts to hedge against fluctuation incommodity prices.”

Source: Annual Report, 2013.

Source: Annual Report, 2013.

Source: Odyssey's Gairsoppa Silver Monetization

Strategy Results.

Parko Commodities

Parker Bullion

Johnson Matthey

Larsen and Toubro Limited

“As hedgers we use these contracts to manageprice risk on an expected purchase or sale of th ephysical metal.”

“Price Risk Management is an important aspectin managing our balance sheet and futurestrading has been of immense importance to ourindustry considering the volatile price scenario.”

“Fluctuations in precious metal prices can h avea significant impact on Johnson Matthey'sfinancial results, our policy for allmanufactuiring businesses is to limit thisexposure by hedging against future pricechanges where such hedging can be done atacceptable cost.”

“In line with the Company's risk managementpolicy, the various financial risks mainly relatingto changes in the exchange rates, interest ratesand commodity prices are hedged by using acombination of forward contracts, swaps andother derivative contracts, besides the naturalhedges.”

“The Company has not engaged in any hedgingactivities, other than short term metal

derivative transactions less than 90 days, toreduce its exposure to commodity price risk.”

“Odyssey Marine Exploration, Inc., a pioneer inthe field of deep-ocean exploration has to-datemonetized over 900,000 troy ounces of the

silver recovered from the Gairsoppa shipwreckin July 2013 at an average price per ounce of$23.56 for a gross total of $21.5 million. Thecompany estimates that the monetization andhedging program generated total grossproceeds of approximately $39 million from the2013 recovery, in addition to approximately$41 million generated in the prior year from the2012 recovery.”

Source: Annual Report, 2013.

Source: Annual Report 2013 -14.

SILVER : HEDGING PRICE RISK

Hedging ExperienceIn the international arena, hedging in

Silver futures takes place on a number of

exchanges, the major ones being

Chicago Mercantile Exchange (CME),

Multi Commodity Exchange of India Ltd.

(MCX), Shanghai Futures Exchange

(SHFE) and Tokyo Commodity Exchange

(TOCOM).

Hedging is critical for stabilizing

incomes of corporations and individuals.

Reducing risks may not always improve

earnings, but failure to manage risk will

have direct repercussion on the risk

bearers' long-term income.

To gain most from hedging, it is

essential to identify and understand the

objectives behind hedging. A good

hedging practice, hence, encompassesefforts by companies to get a clear

picture of their risk profile and benefit

from hedging techniques.

MCX offers a transparent hedging

platform, besides bringing about

economic and financial efficiencies by

de-risking production, processing, and

trade. The Exchange's engagement has

led to large efficient gains in supply

chains, with exporters gaining a larger

IMPORTANCE OF HEDGING

PARTICIPANT HEDGERS

share of global prices, and producers

getting better prices and much better

access to markets.

All those who have or intend to take

positions in physical silver are

participant hedgers. These are:

l

Importersl Exporters

l Refiners

l Jewellers

l Designers

l Market intermediaries

l Merchandisers

l Prices ruling in the international

markets

l Currency exchange rate movements,

especially US Dollar

l Economic factors: industrial growth,

global financial crisis, recession and

inflation

l Government trade policies (import

duties, penalties, and quotas)

l Geopolitical events

l Interest rate movements and prices of

gold

FACTORS AFFECTING PRICE

VARIATIONS

The mining of silver began some 5000 years

ago. Silver was first mined in about 3000 B.C.

in Anatolia (modern day Turkey). The

principal sources of silver are the ores of silver,

silver-nickel, lead, and lead-zinc obtained from Peru,

Bolivia, Mexico, China, Australia, Chile, Poland, and

Serbia. Peru, Bolivia, and Mexico have been mining

silver since 1546, and are still major world producers.

The top three silver-producing mines are Cannington

(Australia), Fresnillo (Mexico), and San Cristobal(Bolivia), In Central Asia, Tajikistan is known to have

some of the largest silver deposits in the world. The

metal is primarily produced as a byproduct of

electrolytic silver refining, gold, nickel, and zinc

refining, and by application of the Parkes process on lead metal obtained from lead ores

that contain small amounts of silver. Secondary silver sources include coin melt, scrap

recovery, and dis-hoarding from countries where export is restricted. Secondary sources

are price sensitive.

Source: Wikipedia, Silver Institute

7/23/2019 Silver Brochure

http://slidepdf.com/reader/full/silver-brochure 4/8

4

SILVER : HEDGING PRICE RISK

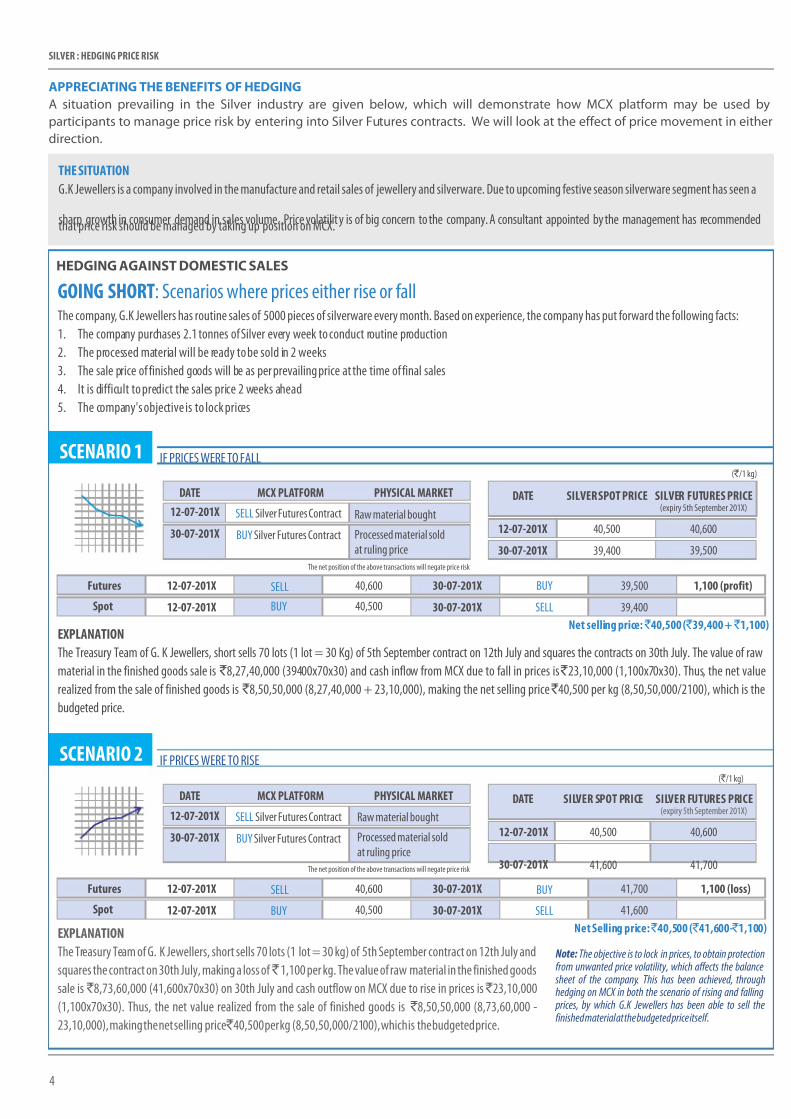

APPRECIATING THE BENEFITS OF HEDGING

A situation prevailing in the Silver industry are given below, which will demonstrate how MCX platform may be used by

participants to manage price risk by entering into Silver Futures contracts. We will look at the effect of price movement in either

direction.

SCENARIO 2

SCENARIO 1

THE SITUATION

G.K Jewellers is a company involved in the manufacture and retail sales of jewellery and silverware. Due to upcoming festive season silverware segment has seen a

sharp growth in consumer demand in volume. Price volatility is of big concern to the company. A consultant appointed by the management has recommendedthat price risk should be managed by taking up position on MCX.sales

EXPLANATION

The Treasury Team of G. K Jewellers, short sells 70 lots (1 lot = 30 Kg) of 5th September contract on 12th July and squares the contracts on 30th July. The value of raw

material in the finished goods sale is ` 8,27,40,000 (39400x70x30) and cash inflow from MCX due to fall in prices is 23,10,000 (1,100x70x30). Thus, the net value

realized from the sale of finished goods is ` 8,50,50,000 (8,27,40,000 + 23,10,000), making the net selling price ` 40,500 per kg (8,50,50,000/2100), which is the

budgeted price.

`

EXPLANATION

The Treasury Team of G. K Jewellers, short sells 70 lots (1 lot = 30 kg) of 5th September contract on 12th July and

squares the contract on 30th July, making a loss of ` 1,100 per kg. The value of raw material in the finished goods

sale is ` 8,73,60,000 (41,600x70x30) on 30th July and cash outflow on MCX due to rise in prices is ` 23,10,000

(1,100x70x30). Thus, the net value realized from the sale of finished goods is ` 8,50,50,000 (8,73,60,000 -

23,10,000), making the net selling price ` 40,500 per kg (8,50,50,000/2100), which is the budgeted price.

The company, G.K Jewellers has routine sales of 5000 pieces of silverware every month. Based on experience, the company has put forward the following facts:

1. The company purchases 2.1 tonnes of Silver every week to conduct routine production

2. The processed material will be ready to be sold in 2 weeks

3. The sale price of finished goods will be as per prevailing price at the time of final sales

4. It is difficult to predict the sales price 2 weeks ahead

5. The company's objective is to lock prices

GOING SHORT: Scenarios where prices either rise or fall

IF PRICES WERE TO RISE

IF PRICES WERE TO FALL

DATE

SELL Silver Futures Contract

Processed material soldat ruling price

MCX PLATFORM PHYSICAL MARKET

DATE

BUY Silver Futures Contract

SELL Silver Futures Contract

The net position of the above transactions will negate price risk

MCX PLATFORM PHYSICAL MARKET

Futures

Futures

12-07-201X

12-07-201X

30-07-201X

30-07-201X

40,600

40,600

39,500

41,700

1,100 (profit)

1,100 (loss)

39,400

41,600

12-07-201X

12-07-201X

30-07-201X

30-07-201X

Spot

Spot

SELL

SELL

SELL

SELL

BUY

BUY

( ` /1 kg)

DATE

12-07-201X

30-07-201X

40,500 40,600

39,50039,400

SILVER SPOT PRICE SILVER FUTURES PRICE(expiry 5th September 201X)

( ` /1 kg)

DATE

12-07-201X

30-07-201X

40,500 40,600

41,70041,600

SILVER SPOT PRICE SILVER FUTURES PRICE(expiry 5th September 201X)

Net Selling price: 40,500 ( 41,600- 1,100) ` ` `

Net selling price: 40,500 ( 39,400 + 1,100) ` ` `

HEDGING AGAINST DOMESTIC SALES

Note: The objective is to lock in prices, to obtain protectionfrom unwanted price volatility, which affects the balance sheet of the company. This has been achieved, throughhedging on MCX in both the scenario of rising and falling prices, by which G.K Jewellers has been able to sell thefinished material at the budgeted price itself.

BUY Silver Futures Contract

Raw material bought

BUY 40,500

Processed material soldat ruling price

Raw material bought

BUY 40,500

12-07-201X

30-07-201X

The net position of the above transactions will negate price risk

12-07-201X

30-07-201X

7/23/2019 Silver Brochure

http://slidepdf.com/reader/full/silver-brochure 5/8

5

SILVER : HEDGING PRICE RISK

THE SITUATION

Bharat Silver Ltd primarily a silver importer, who imports, stocks and sells silver in various denominations to a host of users. The silver market has been extremely

unpredictable due to price volatility, which is a reflection of international and domestic factors and currency movements. Bharat Silver imports large quantities of silver

and sells them in a staggered manner to the physical market at the prevailing prices. The huge stock of imported silver it holds over a long time-period exposes Bharat

Silver to very high risks as silver prices are highly volatile. The company hedges on MCX to effectively manage its commodity and currency risk.

Hedging against Staggered Sales

Bharat Silver Ltd, imports silver in huge quantities and sells it in a staggered manner in the physical market, at the prevailing market prices

1. The company imports on 20th October 5,000 kg of Silver

2. The company imports and caters to the physical demand of the buyers at the prevailing market price

3. The company manages to sell 500 kg of the imported 5,000 kg on 20th October itself. Thus, there is no price risk in the sale of the first lot.

4. The remaining 4,500 kg will be sold in subsequent days at ruling prices

5. The company hedges for 4,500 kg

GOING SHORT: Scenarios where prices either rise or fall

The Treasury Team of Bharat Silver Ltd, short sells 4,500 kg (1 lot = 30 kg) of 5th December contract on 20th October and squares the position in a staggered

manner on subsequent days, whenever the company sells Silver to the physical market at the prevailing spot market price. The company by hedging its position

and making a staggered exit from the futures contract makes the net selling price at ` 40,550 per kg, which is the budgeted price.

DATE

SELL 1500 kg

IMPORTSELL 5000 kg and500 kg

MCX PLATFORMPHYSICAL MARKET

( ` /1 kg)

DATE

20-10-201X27-10-201X

40,550 40,60040,90040,850

SILVER SPOT PRICE SILVER FUTURES PRICEth

(expiry 5 December 201X)

Open Interest

in lots on MCX

SELL 2100 kg

SELL 900 kg

BUY 50 lots of Silver Futures

BUY 70 lots of Silver Futures

BUY 30 lots of Silver Futures

150

100

30

0

SELL 150 lots of Silver Futurescontract (30 kg each)

04-11-201X

11-11-201X

40,150 40,200

41,40040,350

DATE SPOT MARKET

ACTION

NET SELLING PRICE

per kg

PROFIT/LOSS per kg

on MCX

FUTURES MARKET

ACTIONS

20-10-201X

27-10-201X

04-11-201X

11-11-201X

SELL

SELL

SELL

BUYSELL

BUY

BUY

BUY

SELL

IMPORT5000 kg

Sell 500 kg@ ` 40,550

Sell 1500 kg@ ` 40,850

Sell 2100 kg@ ` 40,150

Sell 900 kg@ ` 41,350

150 lots@ ` 40,600

50 lots@ ` 40,900

70 lots@ ` 40,200

30 lots@ ` 41,400

` 300 Loss)(

` 400 (Profit)

` 800 (Loss)

` 40,550

`

( ` `

40,55040,850 - 300)

` 40,550( ` 40,150 + ` 400)

` 40,550( ` 41,350 - ` 800)

Explanation

SILVER FACTS

Silver has innumerable applications in art, science, industry and beyond. At the highest level, though, demand for silver

breaks down into three important categories: silver in industry, investment, and silver jewellery and décor. Together, these

three areas represent more than 95% of the annual silver demand. With unique properties, including its strength,

malleability, and ductility; its electrical and thermal conductivity; its sensitivity to and high reflectance of light; and the

ability to endure extreme temperature; it is an element without substitution. Islam permits Muslim men to wear silver

rings on the little finger of either hand. In the Americas, high temperature silver-lead cupellation technology was

developed by pre-Inca civilizations as early as AD 60–120. Silver plays no known natural biological role in humans, and

possible health effects of silver are a disputed subject. Commercial-grade fine silver is at least 99.9% pure, and purities

greater than 99.999% are available.

20-10-201X

27-10-201X

04-11-201X

11-11-201X

7/23/2019 Silver Brochure

http://slidepdf.com/reader/full/silver-brochure 6/8

6

How much Volatility Risk are you Exposed to?

SILVER : HEDGING PRICE RISK

Daily Average Volatility Silver MCX (Near Month Continuous Prices)

REGULATORY BOOST TO HEDGERS

1. Income tax exemptions for

hedging. The Finance Act, 2013, has

provided for coverage of commodity

derivatives transactions undertaken in

recognized commodity exchanges

under the ambit of Section 43(5)

of the Income Tax Act, 1961, on thelines of the benefit available

to transactions undertaken in

recognized stock exchanges.

This effectively means that business

profits / losses can be offset by losses/

profits undertaken in commodity

derivatives transactions. This

enhances the attractiveness of risk

management on recognized

commodity derivative exchanges and

incentivizes hedging. Hedgers are no

longer forced to undertake physical

delivery of commodities to prove that

their transactions are in the nature of

hedging and not 'speculation'.

2. Limit on open position as against

hedging. This enables hedgers totake positions to the extent of their

exposure on the physical market and

are allowed to take position over and

above prescribed position limits on

approval by the exchange.

3. Early pay-in benefit. If a hedger

makes an early pay-in of commodity,

he is exempted from paying all

applicable margins.

BENEFITS OF HEDGING ON MCX

l India's no. 1 commodity exchange totrade Silver futures

l Highly liquid contracts

l Highly efficient and transparentmarket

l Low impact costs (trading costs)because of tight bid-ask spreads

l Deliverable contract withinternationally accepted silver bars

l Flexibility to choose from differentcontract sizes

l The market is operational during theday and evening session, enablingparticipants to take part in pricediscovery when global markets areactive.

Year

AnnualisedVolatility

2009

2010

2011

2012

2013

25%

21%

37%

19%

29%

Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-15

15.00%

10.00%

5.00%

0.00%

-5.00%

-10.00%

-15.00%

-20.00%

Aug-14

2014 21%

Silver: Witnessed annualized price volatility of about 23% in 2014

Are you prepared for volatility risk?Adoption of a risk management practice, such as hedging on the MCX, can help shield againstthe perils of price volatility.

Which means

A firm in the silver business, with an annual turnover of ` 100 crore was exposed to a price riskof 23 crore in 2014.

India, with an annual silver market size of 5000 tonnes, worth about 23,000 crore, is exposedto price volatility risk of about 5,300 crore (i.e. 23% of the holding value).

`

`

`

7/23/2019 Silver Brochure

http://slidepdf.com/reader/full/silver-brochure 7/8

Commodity Silver Silver Mini Silver Micro

Contracts Available

th th st stContract Start Day 16 day of contract launch month. I f16 day is a holiday then the following 1 day of contract launch month. I f 1 day

working day. is a holiday then the following Day

th thLast Trading Day 5 day of contract expiry month. I f 5 day Last calendar day of the contract month. I f last calendar day is a holiday then

is a holiday then preceding working day. preceding working day.

Trading Period Monday through Friday (10.00 a.m. to 11.30 / 11.55 p.m.)

Trading Unit 30 kg 5 kg 1 kg

Quotation/ Base Value 1 kg

Maximum Order Size 600 kg

Price Quote Ex-Ahmedabad ( inclusive of a ll taxes and levies relating to import duty, customs i f applicable but excluding sales tax / VAT,

any other additional tax or surcharge on sales tax, local taxes and octroi)

Tick Size ` 1 per kg

Daily Price Limit The base price limit will be 4%. Whenever the base daily price limit is breached, the relaxation will be allowed upto 6% without anycooling off period in the trade. In case the daily price limit of 6% is also breached, then after a cooling off period of 15 minutes, the

daily price limit will be relaxed upto 9%

In case price movement in international markets is more than the maximum daily price limit (i.e 9%), the same may be further

relaxed in steps of 3% beyond the maximum permitted limit, and inform the Commission immediately.

Initial Margin Minimum 5 % or based on SPAN whichever is higher

Additional and / or Special Margin In case of additional volatility, an additional margin (on both buy & sell side) and/ or special margin (on either buy or sell side) at

such percentage, as deemed fit; will be imposed in respect of all outstanding positions.

Maximum Allowable Open Position For individual clients 100 MT or 5% of the market wide open position, whichever is higher for all silver contracts combined together

For a member collectively for all clients: 1000 MT or 20% of the market wide open position, whichever is higher for all silver contracts

combined together

Delivery Unit 30 kg

Delivery Centres Ahmedabad at designated Clearing House facilities

Quality Specifications Grade: 999 and Fineness: 999 (as per IS 2112: 1981)

• No negative tolerance on the minimum fineness shall be permitted.

• If it is below 999 purity, it is rejected.

It should be serially numbered silver bars supplied by LBMA approved suppliers or other suppliers as may be approved by MCX

Due Date Rate Due Date Rate is calculated on the Sett lement rate is f ixed by the Exchange on the last working day of contract

expiry day of the contract. This is expiry month. The settlement rate will be the official closing price on that day

calculated by way of taking simple fixed by the system for Silver 30 kg contract of immediate expiry.

average of last 3 days s pot market

prices of Ahmedabad.

Delivery Logic Compulsory Both Option

Note: Please refer to the exchange circulars for latest contract specifications

* Genuine hedgers having underlying exposure that exceed the prescribed OI limits given in the contract specifications can be allowed higher limits based on approvals.

March, May, July, September, December February, April, June, August, November

7

SALIENT CONTRACT SPECIFICATIONS OF SILVER FUTURES CONTRACTS

SILVER : HEDGING PRICE RISK

7/23/2019 Silver Brochure

http://slidepdf.com/reader/full/silver-brochure 8/8

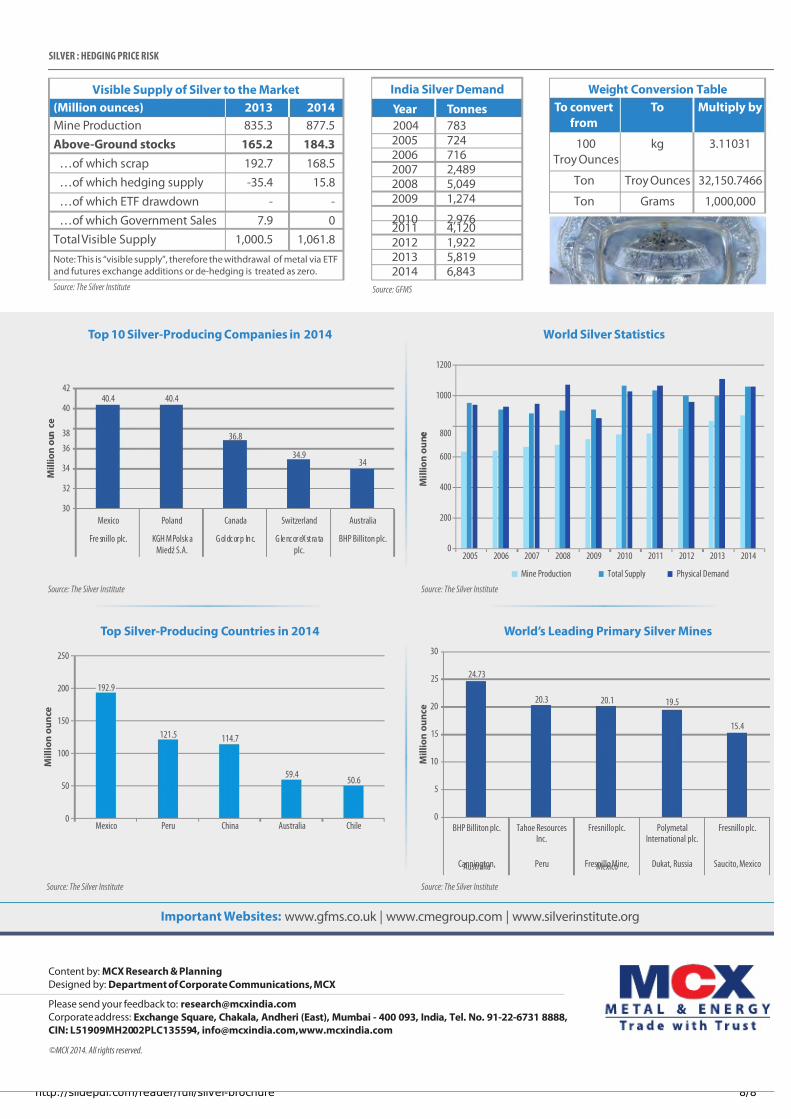

Weight Conversion Table

100 kg 3.11031

Ton Troy Ounces 32,150.7466

Ton Grams 1,000,000

To convert To Multiply by

from

Troy Ounces

©MCX 2014. All rights reserved.

Content by: MCX Research & Planning

Designed by: Department of Corporate Communications, MCX

Please send your feedback to: [email protected]

Corporate address: Exchange Square, Chakala, Andheri (East), Mumbai - 400 093, India, Tel. No. 91-22-6731 8888,

CIN: L51909MH2002PLC135594, [email protected], www.mcxindia.com

World Silver Statistics

Important Websites: www.gfms.co.uk | www.cmegroup.com | www.silverinstitute.org

SILVER : HEDGING PRICE RISK

Top 10 Silver-Producing Companies in 2014

Top Silver-Producing Countries in 2014 World’s Leading Primary Silver Mines

Visible Supply of Silver to the Market

(Million ounces) 2013 2014

Mine Production 835.3 877.5

Above-Ground stocks 165.2 184.3

…of which scrap 192.7 168.5

…of which hedging supply -35.4 15.8

…of which ETF drawdown - -

…of which Government Sales 7.9 0

Total Visible Supply 1,000.5 1,061.8

Note: This is “visible supply”, therefore the withdrawal of metal via ETFand futures exchange additions or de-hedging is treated as zero.

Source: The Silver Institute Source: GFMS

India Silver Demand

Year Tonnes

2004 7832005 7242006 7162007 2,4892008 5,0492009 1,274

2010 2,9762011 4,1202012 1,9222013 5,8192014 6,843

40.4 40.4

36.8

34.934

30

32

34

36

38

40

42

Mexico Poland Canada Switzerland Australia

Fre snillo plc. KGH M Polsk aMiedź S.A.

G oldc orp Inc. G lenc oreXstrataplc.

BHP Billiton plc.

192.9

121.5 114.7

59.4

50.6

0

50

100

150

200

250

Mexico Peru China Australia Chile0

5

10

15

20

25

30

24.73

BHP Billiton plc.

Cannington,Australia

20.3

Tahoe ResourcesInc.

Peru

20.1

Fresnillo plc.

Fresnillo Mine,Mexico

19.5

PolymetalInternational plc.

Dukat, Russia

15.4

Fresnillo plc.

Saucito, Mexico

0

200

400

600

800

1000

1200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

M i l l i o n o u n c e

Mine Production Total Supply Physical Demand

Source: The Silver Institute

M i l l i o n o u n c e

Source: The Silver Institute

Source: The Silver Institute Source: The Silver Institute

M i l l i o n o u n c e

M i l l i o n o u n c e