Embed Size (px)

Citation preview

1

LINE OF

SIGHT

Choosing the Factor: Not Which But When Michael Hunstad, PhD Head of Quantitative Research, Global Equity Meggan Friedman Senior Investment Strategist, Global Equity Hosted by Brendan Maton

The Equity Imperative

© 2015 Northern Trust Corporation

2

Your Speakers

Meggan Friedman Senior Investment Strategist, Global Equity

• Meggan helps to create current thought leadership for global investors and to deliver comprehensive investment solutions across the equity spectrum.

• Meggan has been with Northern Trust since 2011 and has 19 years of industry experience.

• Meggan has a bachelor degree from Northwestern University and an M.B.A from Harvard Business School.

• Meggan was named “Best on the Street” by Wall Street Journal in 2010 and 2011.

Michael Hunstad, PhD Head of Quantitative Research, Global Equity

• Michael leads Quantitative research within the Global Equity Team. • Michael has been with Northern Trust since 2012 and has 15 years

industry experience. • He holds a PhD in applied mathematics as well as an MBA in

quantitative finance and an MA in econometrics.

3

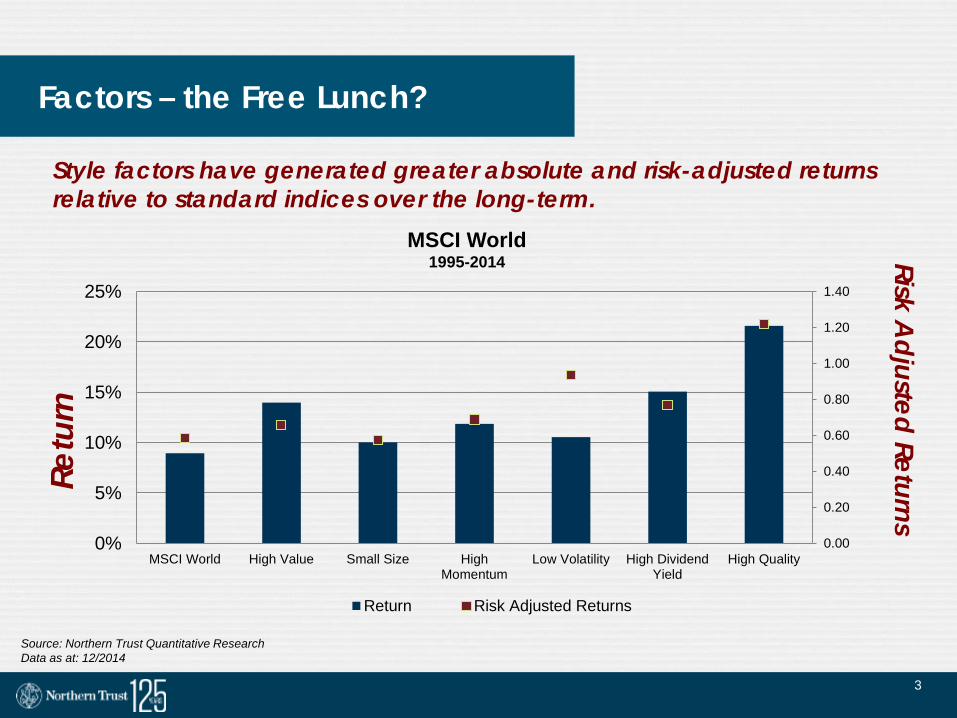

Factors – the Free Lunch? Re

turn

Risk A

djusted Returns

MSCI World 1995-2014

Source: Northern Trust Quantitative Research Data as at: 12/2014

Style factors have generated greater absolute and risk-adjusted returns relative to standard indices over the long-term.

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

0%

5%

10%

15%

20%

25%

MSCI World High Value Small Size HighMomentum

Low Volatility High DividendYield

High Quality

Return Risk Adjusted Returns

4

Factor Cycles

5

Source: Bloomberg and Northern Trust Quantitative Research Each month from January 1979 to June 2014 all stocks in the Russell 3000 universe were ranked on the MSCI Barra definition of Value and put into equally weighted quintiles. The subsequent return for each quintile is computed with the resultant value factor return defined as the first quintile (highest value) return minus the benchmark return.

Serious Risk

Sustained underperformance is a primary risk in factor investing

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

Value Factor Cumulative Returns US Broadcap Benchmark

6

Value Cycles

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

% o

f Tot

al V

aria

tion

Months

High Value

Source: Bloomberg, MSCI Barra and Northern Trust Quantitative Research

The value cycle lasts for approximately

47 months

7

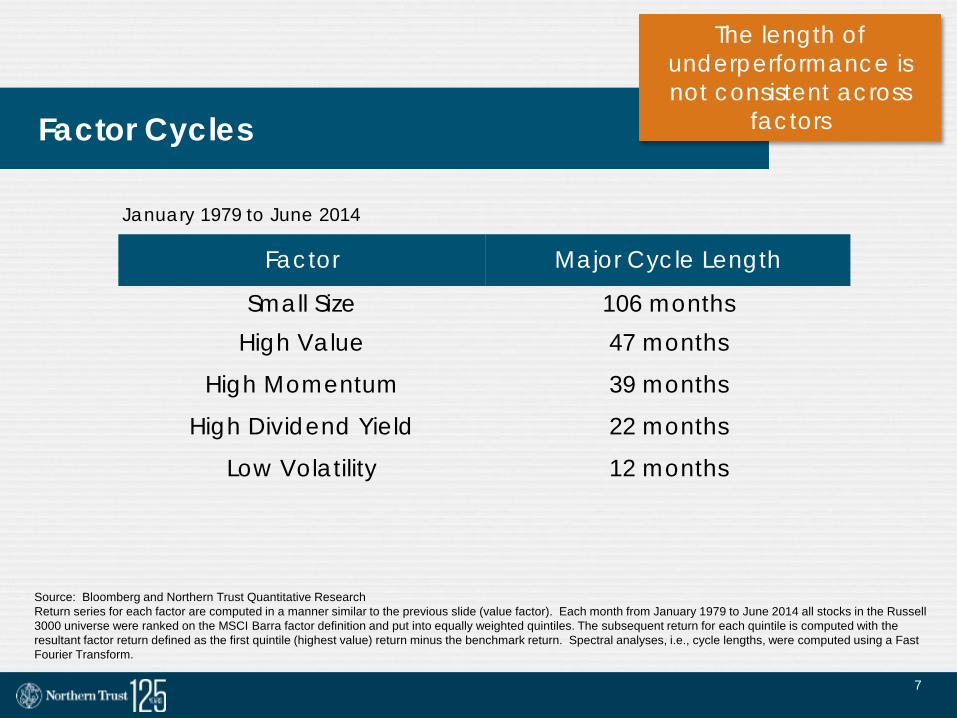

Factor Cycles

Factor Major Cycle Length

Small Size 106 months High Value 47 months

High Momentum 39 months

High Dividend Yield 22 months

Low Volatility 12 months

Source: Bloomberg and Northern Trust Quantitative Research Return series for each factor are computed in a manner similar to the previous slide (value factor). Each month from January 1979 to June 2014 all stocks in the Russell 3000 universe were ranked on the MSCI Barra factor definition and put into equally weighted quintiles. The subsequent return for each quintile is computed with the resultant factor return defined as the first quintile (highest value) return minus the benchmark return. Spectral analyses, i.e., cycle lengths, were computed using a Fast Fourier Transform.

The length of underperformance is not consistent across

factors

January 1979 to June 2014

8

Source: Bloomberg and Northern Trust Quantitative Research For full details of the multi-period optimization see the NTAM white paper Choosing Factors: Not ‘Which?’ but ‘When?’

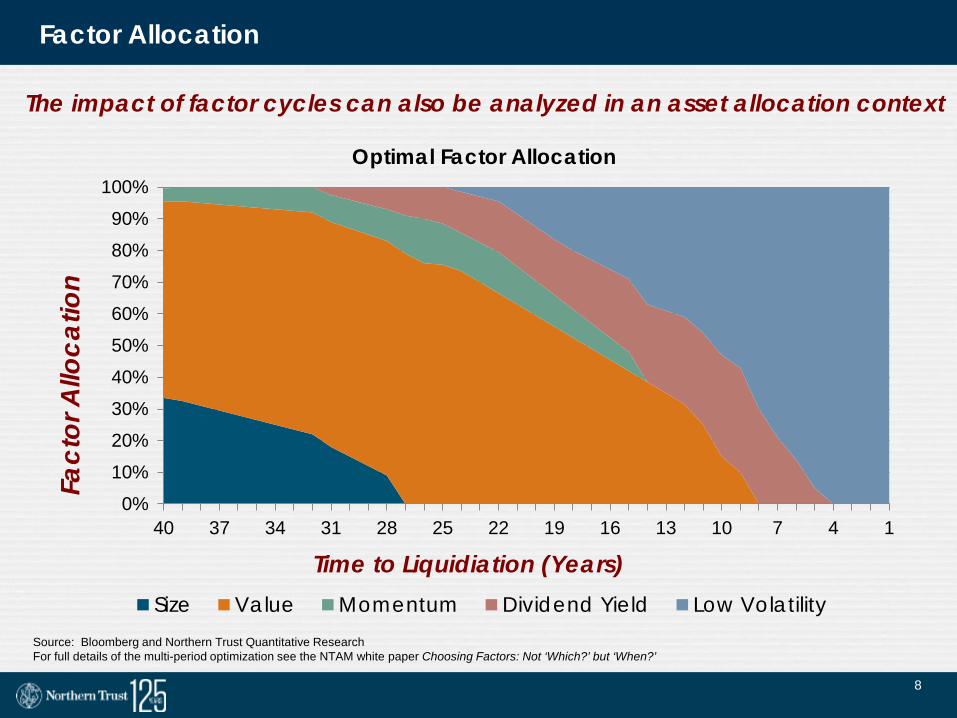

Factor Allocation

The impact of factor cycles can also be analyzed in an asset allocation context

0%10%20%30%40%50%60%70%80%90%

100%

40 37 34 31 28 25 22 19 16 13 10 7 4 1

Fact

or A

lloca

tion

Time to Liquidiation (Years)

Optimal Factor Allocation

Size Value Momentum Dividend Yield Low Volatility

9

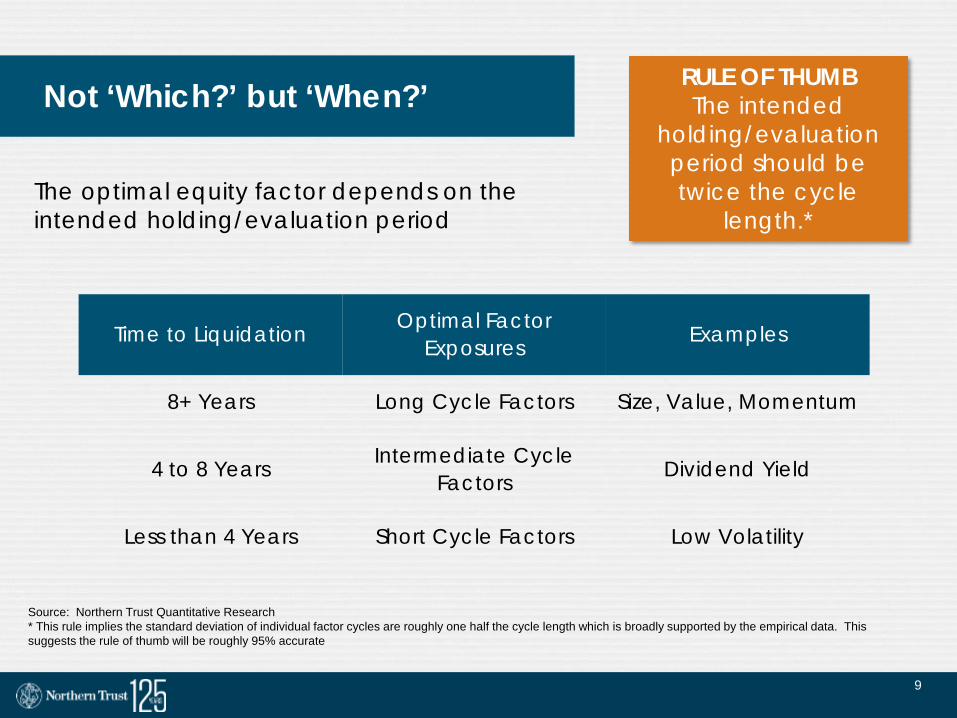

Time to Liquidation Optimal Factor Exposures Examples

8+ Years Long Cycle Factors Size, Value, Momentum

4 to 8 Years Intermediate Cycle Factors Dividend Yield

Less than 4 Years Short Cycle Factors Low Volatility

Not ‘Which?’ but ‘When?’

The optimal equity factor depends on the intended holding/evaluation period

Source: Northern Trust Quantitative Research * This rule implies the standard deviation of individual factor cycles are roughly one half the cycle length which is broadly supported by the empirical data. This suggests the rule of thumb will be roughly 95% accurate

RULE OF THUMB The intended

holding/evaluation period should be twice the cycle

length.*

10

Multi-factor Portfolios

11

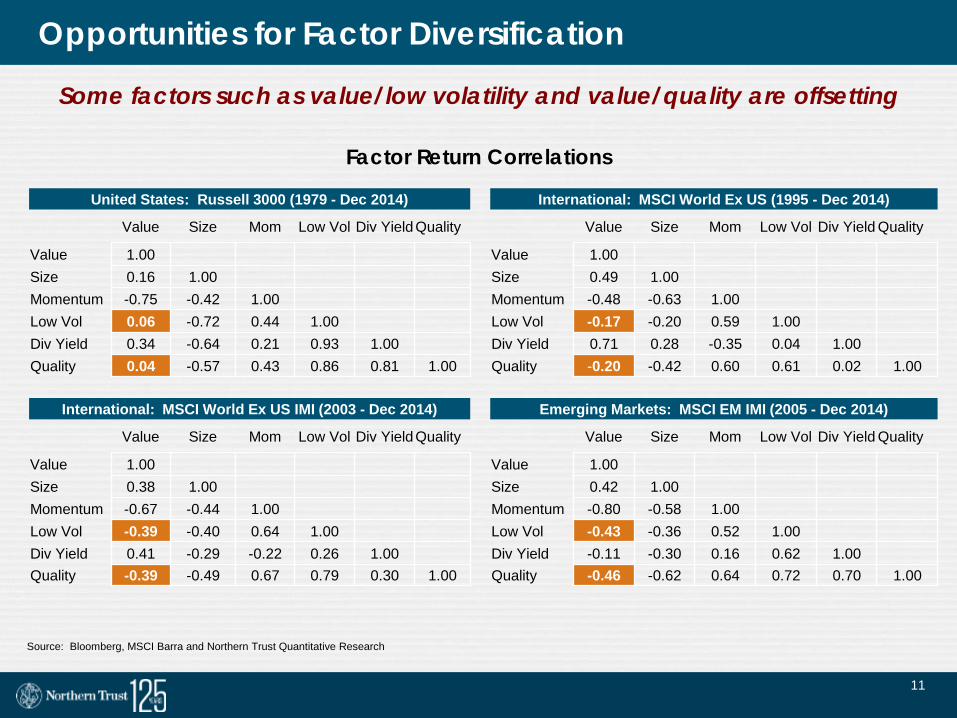

Opportunities for Factor Diversification

Some factors such as value/low volatility and value/quality are offsetting

Source: Bloomberg, MSCI Barra and Northern Trust Quantitative Research

Factor Return Correlations

United States: Russell 3000 (1979 - Dec 2014) International: MSCI World Ex US (1995 - Dec 2014)

Value Size Mom Low Vol Div Yield Quality Value Size Mom Low Vol Div Yield Quality

Value 1.00 Value 1.00 Size 0.16 1.00 Size 0.49 1.00 Momentum -0.75 -0.42 1.00 Momentum -0.48 -0.63 1.00 Low Vol 0.06 -0.72 0.44 1.00 Low Vol -0.17 -0.20 0.59 1.00 Div Yield 0.34 -0.64 0.21 0.93 1.00 Div Yield 0.71 0.28 -0.35 0.04 1.00 Quality 0.04 -0.57 0.43 0.86 0.81 1.00 Quality -0.20 -0.42 0.60 0.61 0.02 1.00

International: MSCI World Ex US IMI (2003 - Dec 2014) Emerging Markets: MSCI EM IMI (2005 - Dec 2014)

Value Size Mom Low Vol Div Yield Quality Value Size Mom Low Vol Div Yield Quality

Value 1.00 Value 1.00 Size 0.38 1.00 Size 0.42 1.00 Momentum -0.67 -0.44 1.00 Momentum -0.80 -0.58 1.00 Low Vol -0.39 -0.40 0.64 1.00 Low Vol -0.43 -0.36 0.52 1.00 Div Yield 0.41 -0.29 -0.22 0.26 1.00 Div Yield -0.11 -0.30 0.16 0.62 1.00 Quality -0.39 -0.49 0.67 0.79 0.30 1.00 Quality -0.46 -0.62 0.64 0.72 0.70 1.00

12

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

426

.0 1

42.0

85.

2 6

0.9

47.

3 3

8.7

32.

8 2

8.4

25.

1 2

2.4

20.

3 1

8.5

17.

0 1

5.8

14.

7 1

3.7

12.

9 1

2.2

11.

5 1

0.9

10.

4

% o

f Tot

al V

aria

tion

Months

Quality and Value Spectrums

Value Quality

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

426

.0 1

42.0

85.

2 6

0.9

47.

3 3

8.7

32.

8 2

8.4

25.

1 2

2.4

20.

3 1

8.5

17.

0 1

5.8

14.

7 1

3.7

12.

9 1

2.2

11.

5 1

0.9

10.

4

% o

f Tot

al V

aria

tion

Months

Low Volatility and Value Spectrums

Value Volatility

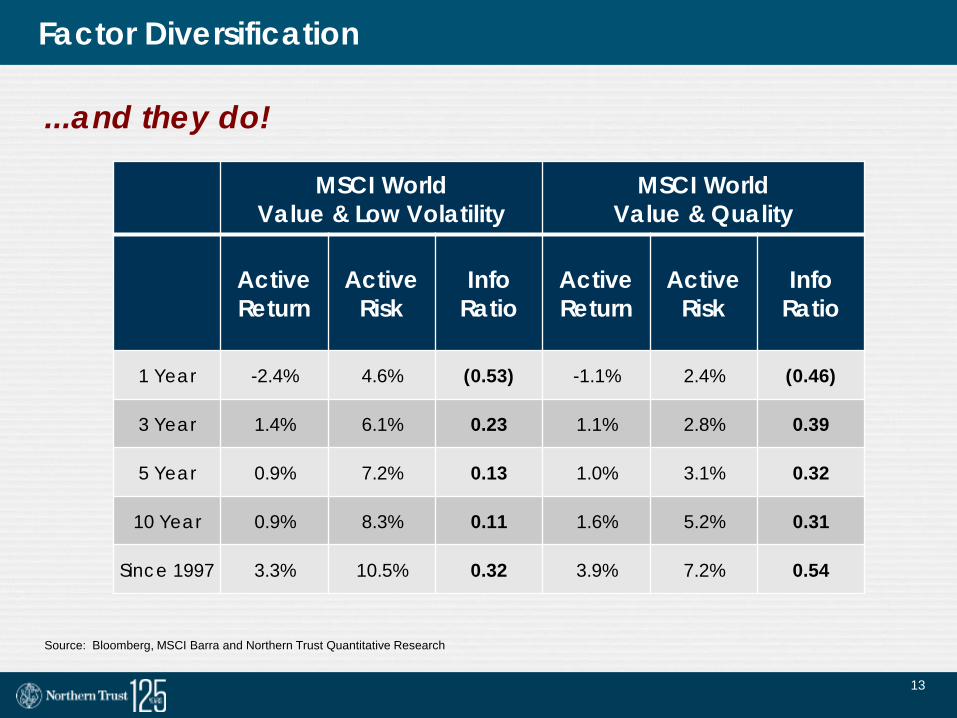

Factor Diversification

Multi-factor portfolios composed of factors of similar frequency should generate better diversification and higher risk adjusted returns...

Source: Bloomberg, MSCI Barra and Northern Trust Quantitative Research

13

Factor Diversification

MSCI World Value & Low Volatility

MSCI World Value & Quality

Active Return

Active Risk

Info

Ratio

Active Return

Active Risk

Info Ratio

1 Year -2.4% 4.6% (0.53) -1.1% 2.4% (0.46)

3 Year 1.4% 6.1% 0.23 1.1% 2.8% 0.39

5 Year 0.9% 7.2% 0.13 1.0% 3.1% 0.32

10 Year 0.9% 8.3% 0.11 1.6% 5.2% 0.31

Since 1997 3.3% 10.5% 0.32 3.9% 7.2% 0.54

...and they do!

Source: Bloomberg, MSCI Barra and Northern Trust Quantitative Research

14

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

426

.0 2

13.0

142

.0 1

06.5

85.

2 7

1.0

60.

9 5

3.3

47.

3 4

2.6

38.

7 3

5.5

32.

8 3

0.4

28.

4 2

6.6

25.

1 2

3.7

22.

4 2

1.3

20.

3 1

9.4

18.

5 1

7.8

17.

0 1

6.4

15.

8 1

5.2

14.

7 1

4.2

13.

7 1

3.3

12.

9 1

2.5

12.

2 1

1.8

11.

5 1

1.2

10.

9 1

0.7

10.

4 1

0.1

% o

f Tot

al V

aria

tion

Months

Quality Spectrum

Quality as a Diversifier

Quality is an excellent diversifier as it operates at multiple frequencies

Source: Bloomberg, MSCI Barra and Northern Trust Quantitative Research

15

Factor Cycles and Stock Specific Risk

16

Stock Specific Risk – A Natural Habitat??

Factor neutrality may be difficult for managers that take specific risk

Source: Northern Trust Quantitative Research, Factset, BARRA Represents average specific risk for Russell 1000 from 1979 to March 2015

Volatility Size Value Growth

Quintile Specific Risk Standard

Deviation Specific Risk Standard

Deviation Specific Risk Standard

Deviation Specific Risk Standard

Deviation

High 42.0 16.0 20.9 9.4 27.8 14.6 34.8 16.9 2 29.8 9.8 24.3 11.3 24.1 11.5 27.5 12.5 3 24.4 7.7 26.7 12.0 25.1 11.7 24.3 10.6 4 20.6 6.6 27.7 12.4 26.3 12.3 22.7 9.7

Low 16.6 5.3 33.8 16.3 30.2 14.7 23.4 10.8

Q1 - Q5 25.4 (12.9) (2.3) 11.4

Momentum Quality Dividend Yield

Quintile Specific Risk Standard

Deviation Specific Risk Standard

Deviation Specific Risk Standard

Deviation

High 29.7 13.6 20.8 11.2 19.0 8.1

2 23.5 10.8 24.3 11.1 22.1 8.6

3 22.8 10.3 25.4 12.5 24.9 10.0

4 24.4 11.2 27.2 13.8 31.9 16.5

Low 23.0 16.2 32.2 17.0 34.5 14.2

Q1 - Q5 6.6 (11.3) (15.4)

17

The Consequences of Specific Risk

-0.70

-0.50

-0.30

-0.10

0.10

0.30

0.50

0.70

DividendYield

Quality Momentum Size Value Volatility Growth

BARR

A F

acto

r Exp

osur

e

Example Fundamental Manager

In pursuing stock specific risk, fundamental managers often find it in its natural habitat

Threshold of Materiality

Threshold of Materiality

Source: Northern Trust Quantitative Research, Factset, BARRA As of May 2015 – manager generates appox. 9% tracking error against benchmark and holds about 25 names

18

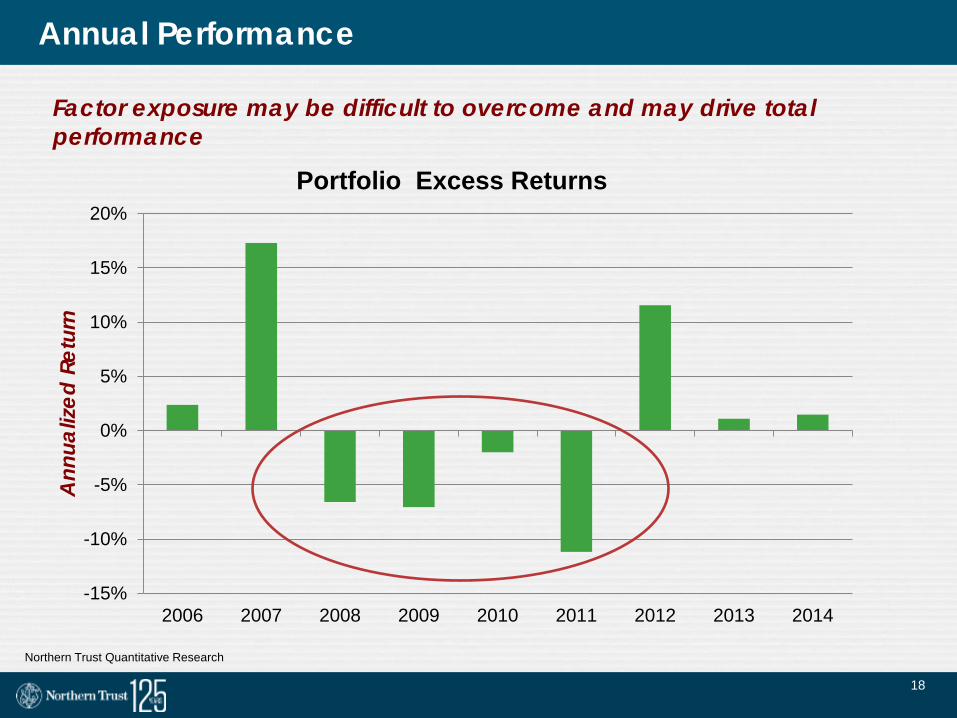

Annual Performance

-15%

-10%

-5%

0%

5%

10%

15%

20%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Ann

ualiz

ed R

etur

n

Portfolio Excess Returns

Factor exposure may be difficult to overcome and may drive total performance

Northern Trust Quantitative Research

19

A Repeated Pattern

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

3 Year Pre-hire 3 Year Post-hire 3 Year Post-fire

Info

rmat

ion

Ratio

3 Year Pre and Post Hire and Fire IRs

From Goyal, A. and Wahal, S., “The Selection and Termination of Investment Managers by Plan Sponsors,” Journal of Finance 63(4) 1805‒1847, 2008

These cycles may strongly influence the hiring and firing of active equity managers

20

Engineering Equity: Product Design

21

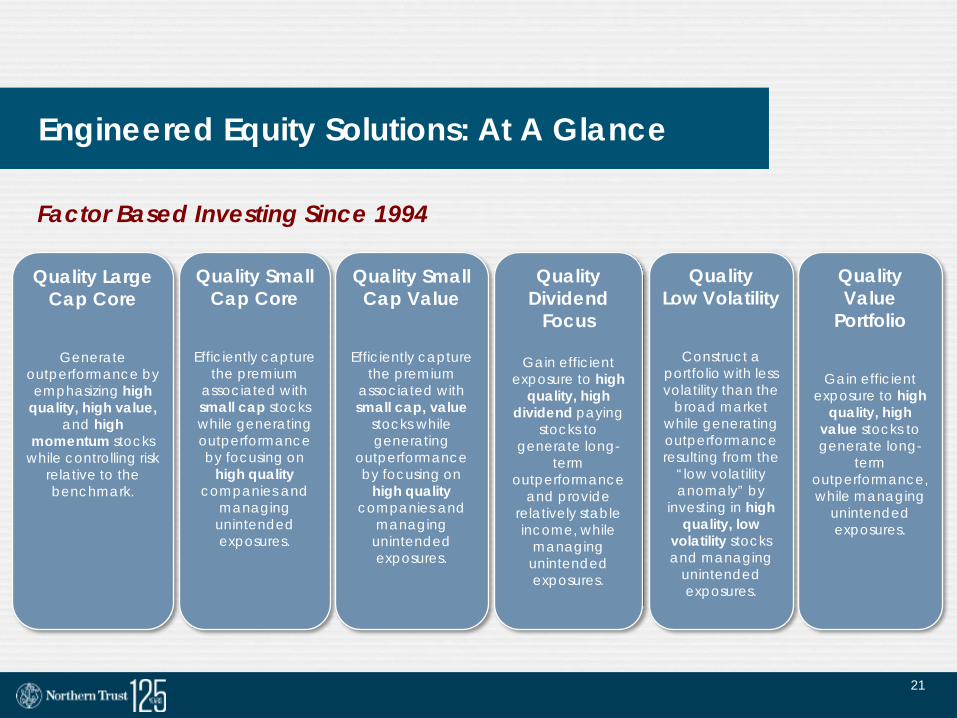

Factor Based Investing Since 1994

Quality Small Cap Core

Efficiently capture the premium

associated with small cap stocks while generating outperformance by focusing on

high quality companies and

managing unintended exposures.

Quality Small Cap Value

Efficiently capture the premium

associated with small cap, value

stocks while generating

outperformance by focusing on

high quality companies and

managing unintended exposures.

Quality Large Cap Core

Generate outperformance by emphasizing high

quality, high value, and high

momentum stocks while controlling risk

relative to the benchmark.

Quality Dividend

Focus

Gain efficient exposure to high

quality, high dividend paying

stocks to generate long-

term outperformance

and provide relatively stable income, while

managing unintended exposures.

Quality Low Volatility

Construct a portfolio with less volatility than the

broad market while generating outperformance resulting from the

“low volatility anomaly” by

investing in high quality, low

volatility stocks and managing

unintended exposures.

Quality Value

Portfolio

Gain efficient exposure to high

quality, high value stocks to generate long-

term outperformance, while managing

unintended exposures.

Engineered Equity Solutions: At A Glance

Factor Based Investing Since 1994

22

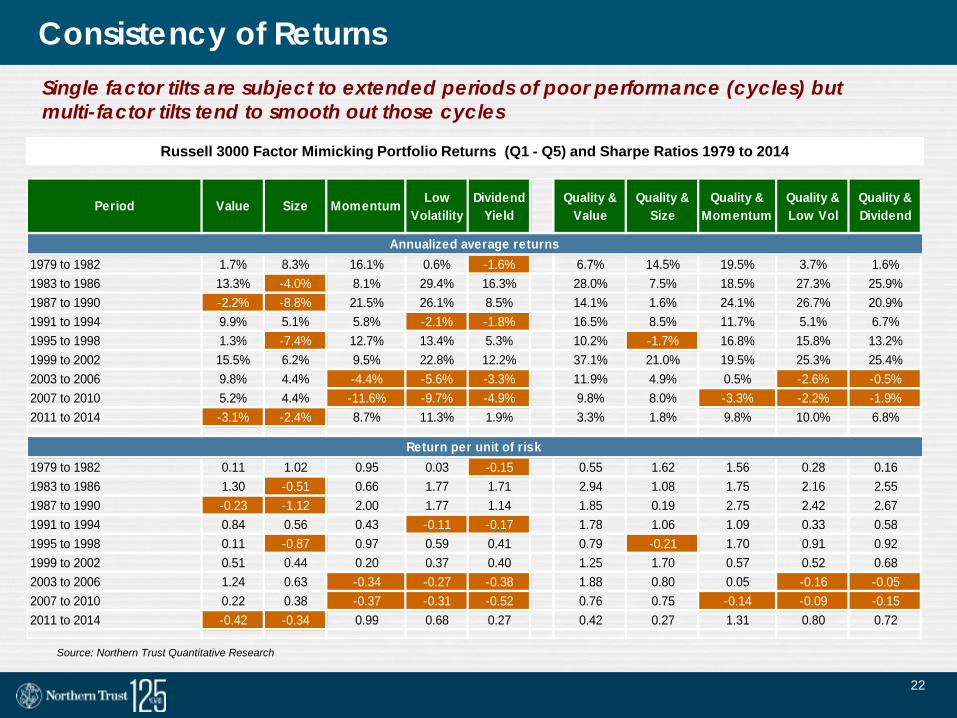

Consistency of Returns Single factor tilts are subject to extended periods of poor performance (cycles) but multi-factor tilts tend to smooth out those cycles

Russell 3000 Factor Mimicking Portfolio Returns (Q1 - Q5) and Sharpe Ratios 1979 to 2014

Source: Northern Trust Quantitative Research

Period Value Size Momentum LowVolatility

DividendYield

Quality &Value

Quality &Size

Quality &Momentum

Quality &Low Vol

Quality &Dividend

1979 to 1982 1.7% 8.3% 16.1% 0.6% -1.6% 6.7% 14.5% 19.5% 3.7% 1.6%1983 to 1986 13.3% -4.0% 8.1% 29.4% 16.3% 28.0% 7.5% 18.5% 27.3% 25.9%1987 to 1990 -2.2% -8.8% 21.5% 26.1% 8.5% 14.1% 1.6% 24.1% 26.7% 20.9%1991 to 1994 9.9% 5.1% 5.8% -2.1% -1.8% 16.5% 8.5% 11.7% 5.1% 6.7%1995 to 1998 1.3% -7.4% 12.7% 13.4% 5.3% 10.2% -1.7% 16.8% 15.8% 13.2%1999 to 2002 15.5% 6.2% 9.5% 22.8% 12.2% 37.1% 21.0% 19.5% 25.3% 25.4%2003 to 2006 9.8% 4.4% -4.4% -5.6% -3.3% 11.9% 4.9% 0.5% -2.6% -0.5%2007 to 2010 5.2% 4.4% -11.6% -9.7% -4.9% 9.8% 8.0% -3.3% -2.2% -1.9%2011 to 2014 -3.1% -2.4% 8.7% 11.3% 1.9% 3.3% 1.8% 9.8% 10.0% 6.8%

1979 to 1982 0.11 1.02 0.95 0.03 -0.15 0.55 1.62 1.56 0.28 0.161983 to 1986 1.30 -0.51 0.66 1.77 1.71 2.94 1.08 1.75 2.16 2.551987 to 1990 -0.23 -1.12 2.00 1.77 1.14 1.85 0.19 2.75 2.42 2.671991 to 1994 0.84 0.56 0.43 -0.11 -0.17 1.78 1.06 1.09 0.33 0.581995 to 1998 0.11 -0.87 0.97 0.59 0.41 0.79 -0.21 1.70 0.91 0.921999 to 2002 0.51 0.44 0.20 0.37 0.40 1.25 1.70 0.57 0.52 0.682003 to 2006 1.24 0.63 -0.34 -0.27 -0.38 1.88 0.80 0.05 -0.16 -0.052007 to 2010 0.22 0.38 -0.37 -0.31 -0.52 0.76 0.75 -0.14 -0.09 -0.152011 to 2014 -0.42 -0.34 0.99 0.68 0.27 0.42 0.27 1.31 0.80 0.72

Annualized average returns

Return per unit of risk

23

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Northern Trust Quality Low Volatility S&P 500 Low Volatility MSCI USA Minimum Volatility

Low Volatility Strategies: Sector Exposure Comparison

Sector Weights vs. Russell 1000

Source: Northern Trust Quantitative Research. Data as of 3/31/2015.

24

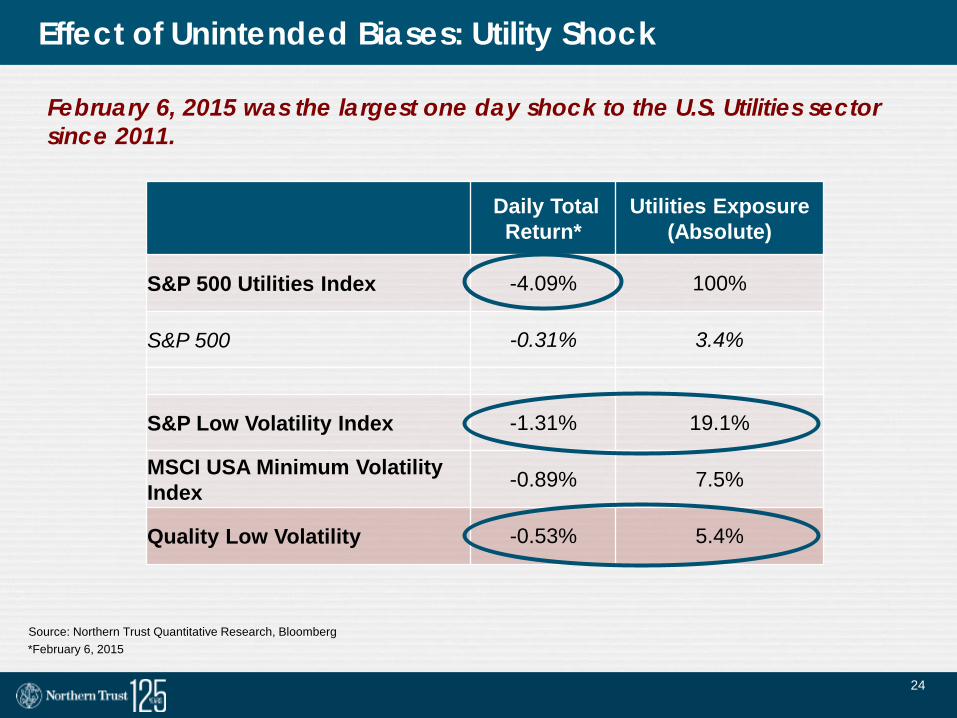

Effect of Unintended Biases: Utility Shock

February 6, 2015 was the largest one day shock to the U.S. Utilities sector since 2011.

Daily Total Return*

Utilities Exposure (Absolute)

S&P 500 Utilities Index -4.09% 100%

S&P 500 -0.31% 3.4%

S&P Low Volatility Index -1.31% 19.1%

MSCI USA Minimum Volatility Index -0.89% 7.5%

Quality Low Volatility -0.53% 5.4%

*February 6, 2015 Source: Northern Trust Quantitative Research, Bloomberg

25

Top Quartile

2nd

Quartile

3rd Quartile

Bottom Quartile

Excess Return Tracking Error Batting Average Information Ratio

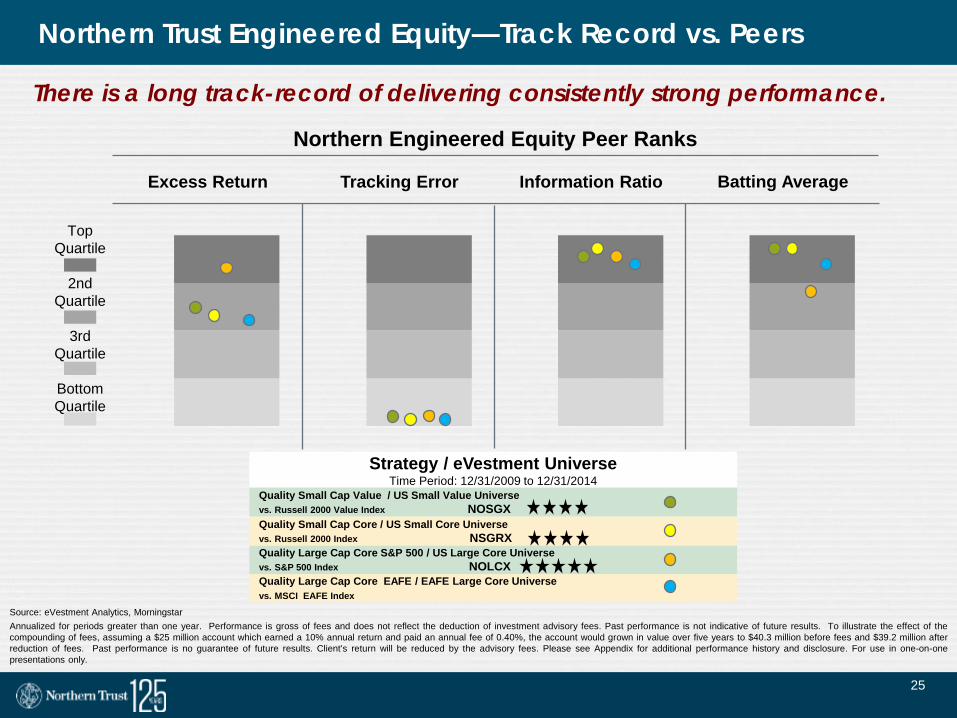

Northern Engineered Equity Peer Ranks

Strategy / eVestment Universe Time Period: 12/31/2009 to 12/31/2014

Quality Small Cap Value / US Small Value Universe vs. Russell 2000 Value Index NOSGX Quality Small Cap Core / US Small Core Universe vs. Russell 2000 Index NSGRX Quality Large Cap Core S&P 500 / US Large Core Universe vs. S&P 500 Index NOLCX Quality Large Cap Core EAFE / EAFE Large Core Universe vs. MSCI EAFE Index

Source: eVestment Analytics, Morningstar Annualized for periods greater than one year. Performance is gross of fees and does not reflect the deduction of investment advisory fees. Past performance is not indicative of future results. To illustrate the effect of the compounding of fees, assuming a $25 million account which earned a 10% annual return and paid an annual fee of 0.40%, the account would grown in value over five years to $40.3 million before fees and $39.2 million after reduction of fees. Past performance is no guarantee of future results. Client’s return will be reduced by the advisory fees. Please see Appendix for additional performance history and disclosure. For use in one-on-one presentations only.

Northern Trust Engineered Equity—Track Record vs. Peers

There is a long track-record of delivering consistently strong performance.

26

Questions?

Michael Hunstad

Meggan Friedman

27

Read the paper.

See more research.

Speak to us.

northerntrust.com/ engineeredequity

USA: +1 312 557 6117 Europe: +44 207 982 3988 Asia Pacific: +852 2918 9884

Paper will be emailed once

published

28

Important Information

This material is directed to eligible counterparties and professional clients only and should not be relied upon by retail investors. This presentation is intended only for the exclusive benefit and use of our clients. Northern Trust and its affiliates may have positions in, and may effect transactions in, the markets, contracts and related investments described herein, which positions and transactions may be in addition to, or different from, those taken in connection with the investments described herein. Important Information Regarding Hypothetical Returns – Where hypothetical portfolio data is presented, the portfolio analysis assumes the hypothetical portfolio maintained a consistent asset allocation (rebalanced monthly) for the entire time period shown. Hypothetical portfolio data is based on publicly available index information. All information is assumed to be accurate and complete but is not guaranteed. Hypothetical portfolio data contained herein does not represent the results of an actual investment portfolio but reflects the historical index performance of the strategy described which were selected with the benefit of hindsight. Components of the hypothetical portfolio were selected primarily utilizing actual historic market risk and return data. If the hypothetical portfolio would have been actively managed, it would have been subject to market conditions that could have materially impacted performance and possibly resulted in a significant decline in portfolio value. The information in this presentation reflects prevailing market conditions and our judgment as of this date, which are subject to change. Past performance is no guarantee of future results. All material has been obtained from sources believed to be reliable, but the accuracy, completeness and interpretation cannot be guaranteed. The information does not constitute investment advice or a recommendation to buy or sell any security and is subject to change without notice Issued in the UK by Northern Trust Global Investments Limited (NTGIL). NTGIL is authorised and regulated by the Financial Conduct Authority in the United Kingdom. Registered in England 03929218. Registered Office: 50 Bank Street, London E14 5NT. Northern Trust Global Investments (NTGI) comprises Northern Trust Investments, N.A. (NTI), Northern Trust Global Investments Limited (NTGIL), Northern Trust Global Investments Japan, K.K. (NTGIJ), the investment advisor division of The Northern Trust Company (TNTC) and Northern Trust Global Advisors, Inc. (NTGA), and its subsidiaries to offer investment products and services to personal and institutional markets. As of 03/31/2015, NTGI had assets under management totaling $960.1 billion. For purposes of compliance with the Global Investment Performance Standards (GIPS®), we have defined our firm as Northern Trust Global Investments Services (NTGIS, a subset of NTGI) that includes those investment products managed by NTI, NTGIL, NTGIJ, and TNTC that are distributed through national channels. 03/31/2015 Northern Trust Asset Management Services had assets under management totaling $791.8 billion.

![lr V≤ Xmg]m{Y - samarthramdas400.in/cite>MaUHù_cr](https://img.pdfslide.us/doc/110x75/5af7c1867f8b9a44658b7d2d/lr-v-xmgmy-.jpg)

![ekuuh; v/;{k egksn;]finance.rajasthan.gov.in/docs/budget/statebudget/2018...VISION-2020](https://img.pdfslide.us/doc/110x75/5ab6d01e7f8b9ab7638e1dfe/ekuuh-vk-egksn.jpg)