Embed Size (px)

Citation preview

04/14/08 10:38 AM SIC 602

1

INDUSTRY SYNOPSIS

SIC 6023 - STATE AND FEDERAL COMMERCIAL BANKING

TABLE OF CONTENTS

1. SCOPE OF SYNOPSIS A. Industry Definition Page 2 B. Contextual Overview Page 6

2. INDUSTRY OVERVIEW

A. Number of Establishments and Companies Page 8 B. Size and Type of Production by- Size Page 8 C. Concentration and Major Service Providers Page 9 D. Stability of the Industry Page 10 E. Geographic Dispersion Page 10 F. Sample Information Page 11 G. Value of Shipments Per Employee Information Page 11

3. PRODUCT INFORMATION

A. Service Delivery Process Page 11 B. Types of Services and Estimated Value of Output Page 21 C. Price Determining Characteristics Page 21 D. Custom Services Page 26 E. Seasonality Page 27 F. Service Substitution Page 27

4. MARKET AND TRANSACTION INFORMATION

A. Interplant and Intraindustry Payments Page 28 B. Price Behavior Page 28 C. Types of Prices Page 30 D. Types of Buyers Page 32 E. Discounts Page 33 F. Additional Charges Page 33 G. Size of Purchase Page 34 H. Contracts Page 34 I. Other Variables Affecting Prices Page 34

04/14/08 10:38 AM SIC 602

1

5. INDUSTRY INFORMATION AND RELATIONS

A. Industry Relations Page 35 B. Currently Available Price Data Page 35 C. Litigation and Other Cooperation Problems Page 35 D. Service Identification Problems Page 36 E. Checklist Clarifications Page 36 F. Industry Specific Questions and Procedures Page 37 G. Presurvey and Pretest Contacts Page 41

6. PUBLICATION GOALS Page 42

1. SCOPE OF SYNOPSIS

A. INDUSTRY DEFINITION

According to the 1987 Standard Industrial Classification Manual, SIC 6021, National Commercial Banks, and SIC 6022, State Commercial Banks, are banks and trust companies (accepting deposits) that are chartered under the National Bank Act (SIC 6021) or by one of the States or territories (SIC 6022). Trust companies engaged in fiduciary business, but not regularly engaged in deposit banking, are classified in Industry 6097. SIC 6023 consist of the following services:

Commercial banks, National Trust companies (accepting deposits) Commercial banks, State Trust companies (accepting deposits)

For purposes of this study SIC 6021 and SIC 6022 have been combined to form SIC 6023 which correlates to the 1997 North American Industrial Classification System (NAICS) definition of Commercial Banking. NAICS defines this industry as establishments primarily engaged in accepting demand and other deposits and making commercial, industrial, and consumer loans. The NAICS classification for commercial banks will consist of portions of four separate SICs. NAICS 52211 Commercial Banking SIC 6021 National Commercial Banks excluding credit card issuing services (NAICS 52221) SIC 6022 State Commercial Banks excluding credit card issuing services (NAICS 52221) SIC 6029 Commercial Banks, Not Elsewhere Classified SIC 6081 Branches and Agencies of Foreign Banks excluding international trade financing (NAICS 52229) and all other non-depository credit intermediation (NAICS 52229) SIC 6023 will include establishments classified under NAICS 52211, in particular foreign banking and branches and agencies of foreign banks. For the purpose of this study, commercial banks that issue credit cards will be included. NOTE: The possibility exists for confusion between commercial banks and what is known as bank holding companies. Bank holding companies are companies that control 25 percent or more voting stock of two or more banks, and are allowed to engage in other non-bank activities such as investment banking and insurance. Bank holding companies are classified in SIC 6712. Output The primary output of commercial banking is financial intermediation. That is, commercial banks function to gather and allocate funds in the economy. Financial intermediaries such as commercial banks transform financial claims in ways that make them more attractive to the ultimate investor. Commercial banks purchase direct claims (IOUs) with one set of characteristics (e.g., term to maturity) from a deficit spending unit (DSU) and transform them into indirect claims

2

04/14/08 10:38 AM SIC 602

3

(IOUs) with a different set of characteristics, which they then sell to a surplus spending unit (SSU). This transformation process is called intermediation. Therefore, households (SSUs) deposit excess cash balances in deposit accounts of a commercial bank, which in turn makes business loans to businesses (DSUs). The primary service lines of this industry are: Deposits Loans Trust Operations Other services including off Balance Sheet Banking Outputs in this industry that will be repriced are deposit accounts (using financial intermediation services indirectly measured, or FISIM, described below) that can be demand, savings, or time deposit accounts; loans that can be consumer, commercial and industrial, agricultural or real estate; estate portfolios that are managed, administered and settled by trust managers; other services such as standby letters of credit by banks engaged in off-balance sheet banking. Deposits have bundled products associated with their outputs. These bundled services include account closing service, account inquiries, telephone banking representative, ATM, check card, check cashing, check copies, check orders, counter item (withdrawal, deposits slips, etc), deposited item return, deposit verification, dormant account service, official checks, overdraft protection, returned check, insufficient funds, uncollected funds, statements, stop payment request or renewal, research services, and tax levies or garnishments. Loans also have bundled products associated with their outputs. These bundled services or outputs include loan origination and loan servicing activities. Other services rendered in this industry include correspondence banking, leasing, sales of treasury securities, cash management services such as payroll, cash forecasts, pension and profit sharing plan administration, investment administration, automatic bill paying, home banking through personal computer, lock box service, and the sale of foreign exchange, travelers checks, certified checks, money orders, bond coupon collection, bond redemption, bond coupon collection returned, safe deposit box, subpoenas or summonses, wire transfers, and tax reporting.

Financial Intermediation Services Indirectly Measured (FISIM) Banks are able to provide services for which they do not charge explicitly by paying or charging different rates of interest to borrowers and lenders. They pay lower rates of interest than would otherwise be the case to those who lend them money and charge higher rates of interest to those who borrow from them. The resulting net revenues of interest are used to defray their expenses and provide an operating surplus. This scheme of interest rates avoids the need to charge their customers individually for services provided and leads to the pattern of interest rates observed in practice. Therefore, these unpriced services are referred to as financial intermediation services indirectly measured. Interest is only indirectly relevant to measuring unpriced services. One of the primary revenues that a bank receives is interest. They take in money and lend out money and earn

interest. The difficulty is allocating the interest earned on loans between the two outputs, the loans and the deposits. Therefore, a reference rate methodology is used to allocate the interest between loans and deposits. The reference rate to be used represents the pure cost of borrowing funds- that is, a rate from which the risk premium has been eliminated to the greatest extent possible and which does not include any intermediation services. Reference rates and how they will be used to price the output of the industry will be explained in detail in Price Determining Characteristics, Checklist Clarifications and Industry Specific Questions and Procedures sections of this synopsis. Other Industry Exclusions SIC 603 Savings Institutions SIC 6035 consists of the following savings institutions: -Federal savings and loan associations -Savings banks, Federal -Savings and loan associations, federally chartered SIC 6036 consists of the following savings institutions: -Savings and loan associations, not federally chartered -Savings banks, State: not federally chartered SIC 606 Credit Unions -SIC 6061 Cooperative thrift and loan associations (accepting deposits) organized under Federal charter to finance credit needs of their members ---Federal Credit Unions. -SIC 6062 Cooperative thrift and loan associations (accepting deposits) organized under other than Federal charter to finance credit needs of their members ---State credit unions, not federally chartered.

SIC 609 Functions Related to Depository Banking -SIC 6091 Non-deposit Trust companies that engage in fiduciary business, but do not regularly engage in deposit banking ---Non-deposit trust companies -SIC 6099 Establishments primarily engaged in performing functions related to depository banking, not elsewhere classified. SIC 6712 Offices of Bank Holding Companies -Establishments primarily engaged in holding or owning the securities of banks for the sole purpose of exercising some degree of control over the activities of bank companies whose securities they hold. Companies holding securities of banks, but which are predominantly operating the banks, are classified according to the kind of bank operated.

B. CONTEXTUAL OVERVIEW

4

04/14/08 10:38 AM SIC 602

5

The number of banks in the Commercial Banking industry has shrunk significantly over the years as a result of consolidation in the form of mergers and acquisitions. The consolidation in the industry is not a result of diminished profits, but as a result of intensified competition. According to Standard and Poor's Banking Industry Surveys, the intensified competition has put added pressure on banks to expand market share, to increase efficiency, and to offer a broader range of financial services.

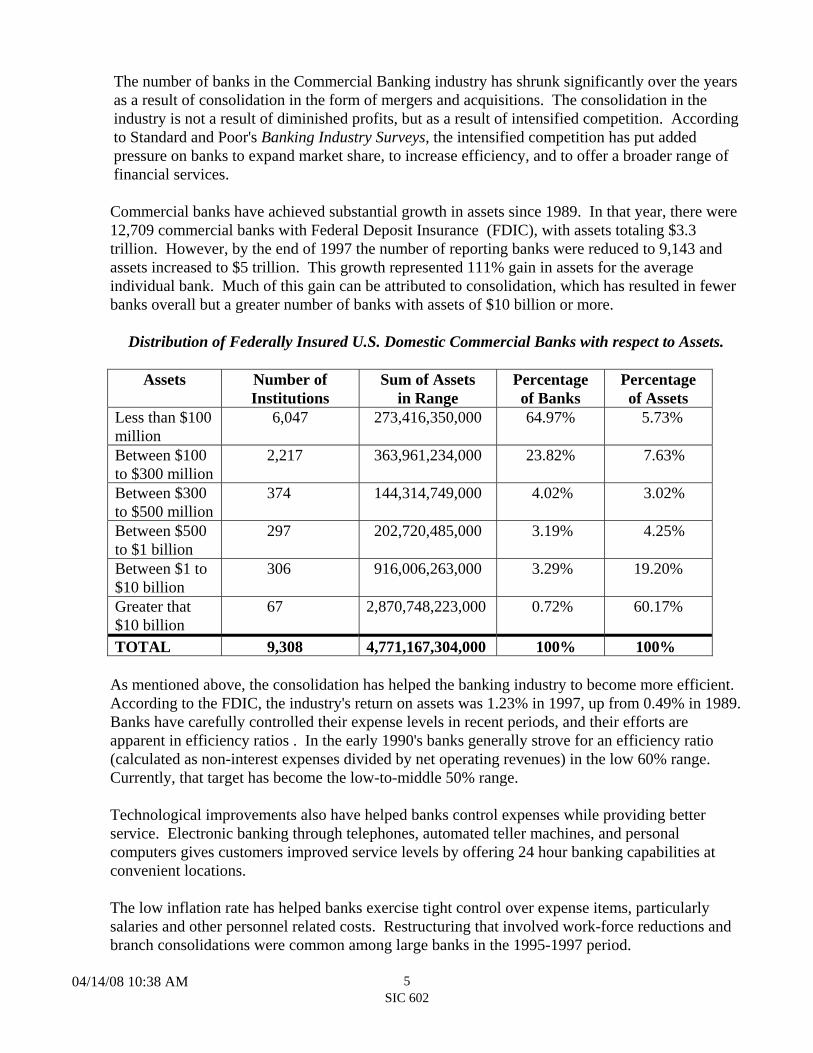

Commercial banks have achieved substantial growth in assets since 1989. In that year, there were 12,709 commercial banks with Federal Deposit Insurance (FDIC), with assets totaling $3.3 trillion. However, by the end of 1997 the number of reporting banks were reduced to 9,143 and assets increased to $5 trillion. This growth represented 111% gain in assets for the average individual bank. Much of this gain can be attributed to consolidation, which has resulted in fewer banks overall but a greater number of banks with assets of $10 billion or more.

Distribution of Federally Insured U.S. Domestic Commercial Banks with respect to Assets.

Assets Number of

Institutions Sum of Assets

in Range Percentage of Banks

Percentage of Assets

Less than $100 million

6,047 273,416,350,000 64.97% 5.73%

Between $100 to $300 million

2,217 363,961,234,000 23.82% 7.63%

Between $300 to $500 million

374 144,314,749,000 4.02% 3.02%

Between $500 to $1 billion

297 202,720,485,000 3.19% 4.25%

Between $1 to $10 billion

306 916,006,263,000 3.29% 19.20%

Greater that $10 billion

67 2,870,748,223,000 0.72% 60.17%

TOTAL 9,308 4,771,167,304,000 100% 100% As mentioned above, the consolidation has helped the banking industry to become more efficient. According to the FDIC, the industry's return on assets was 1.23% in 1997, up from 0.49% in 1989. Banks have carefully controlled their expense levels in recent periods, and their efforts are apparent in efficiency ratios . In the early 1990's banks generally strove for an efficiency ratio (calculated as non-interest expenses divided by net operating revenues) in the low 60% range. Currently, that target has become the low-to-middle 50% range. Technological improvements also have helped banks control expenses while providing better service. Electronic banking through telephones, automated teller machines, and personal computers gives customers improved service levels by offering 24 hour banking capabilities at convenient locations. The low inflation rate has helped banks exercise tight control over expense items, particularly salaries and other personnel related costs. Restructuring that involved work-force reductions and branch consolidations were common among large banks in the 1995-1997 period.

In addition, consolidation has forced banks to become more competitive in the way they do business. In the long term, it will be the lowest-cost providers that not only survive, but also thrive.

2. INDUSTRY OVERVIEW

A. NUMBER OF ESTABLISHMENTS AND COMPANIES

As of March 1999, there are 8,776 Commercial Banks that are registered with the FDIC. A database from the FDIC will be utilized. The database includes information such as the institution's name, the address and telephone numbers of the institutions and the total assets of the institutions. Data on the commercial banking industry is available from the Unemployment Insurance File (UI file). However, size measurements based on revenue in the FDIC frame along with the completeness of the FDIC frame were felt to be superior to the UI file based on employment as size.

B. SIZE AND TYPE OF PRODUCTION BY SIZE

Services in the banking industry depend on size. The larger the bank the more services the bank will provide. For example, demand deposits which is defined as a deposit that is payable on demand or issued with an original maturity of less than seven days are closely associated with consumer transactions. Therefore, demand deposits are relatively more important as a source of funds for small consumer-oriented banks than for large banks. On the other hand, Certificate of Deposits, CDs, which are very large unsecured liabilities of commercial banks issued in denominations of $100,000 or more to business firms or individuals are issued by large, well-known commercial banks of the highest credit standing. Also, Borrowed Funds that are short-term borrowing by commercial banks from the wholesale money markets or a Federal Reserve Bank are a source of funds primarily for large banks. Other services such as Eurodollars and Banker's Acceptance are sources of revenues mainly for large commercial banks. In terms of investments, treasury securities are more important to the portfolio of smaller banks than to those of larger banks. Larger banks have access to many more sources of liquid funds than do smaller banks. Note that treasury securities provide banks with liquidity. Also, they provide banks with diversification beyond that possible with only a loan portfolio. Also, small banks have a higher proportion of fixed assets than do large banks. Small banks with a greater consumer/retail emphasis require more collateral than large banks for loans. In terms of loans, business loans reflect the composition of a bank's customers and are typically more important to large banks than to small retail banks. Agricultural loans on the other hand, represents an important source of lending at many small rural banks. Small banks (banks with less than $100 million of assets) account for almost 50 percent of agricultural lending by all commercial banks. There are also loans made to other financial institutions, and large banks usually make these loans for a variety of purposes. Sales finance companies that engage primarily

6

04/14/08 10:38 AM SIC 602

7

in consumer lending obtain a large proportion of their funds from commercial banks. Large banks also lend to stock brokerage firms and dealers in the U.S. government securities. Consumer loans on the other hand, account for about 12 percent of total bank assets and are an important source of lending for small retail banks. For services such as bank credit cards, currently about 3,000 banks issue credit cards. These banks tend to be large banks and are banks that have developed a comparative advantage in offering credit cards. It is usually the case for banks to merge or buy other banks that have comparative advantages in offering services such as credit cards, mortgage lending, large deposits etc. This is so as to become specialists in providing that particular service in which there is comparative advantage. It is also usually the case that larger banks tend to charge for services that are otherwise free for smaller banks. For example, some smaller banks do not charge for ATM transactions. For services such as money orders, travelers' checks, certified checks etc., some small banks rarely charge a fee, whereas larger banks tend to charge fees, sometimes depending on the relationship the bank has with the client. In order to retain customers, smaller banks usually waive the fees on some services especially those mentioned above. Additionally, banks that have customers with deposits or accounts over a certain amount obtain certain services for free. Large banks, however, tend to be the price setters and price leaders for many services such as loans, deposits etc. Because large banks enjoy economies of scale, the prices for their services tend to be lower. To retain customers at smaller banks, these smaller banks cannot afford to charge higher prices than larger banks.

C. CONCENTRATION AND MAJOR SERVICE PROVIDERS

In the past several years, the pace of consolidation among banks has accelerated. Efforts to increase efficiency, service levels, and product depth are behind much of the merger trend. According to the FDIC, FDIC-insured banks numbered 14,628 in 1975; 14,500 in 1984, and 10,451 in 1994. The decline has continued, with 9,940 such banks in 1995, 9,143 in 1997, and as of March 3, 1999 there were 8,776 banks. Currently, the smallest 7,000 banks (or about 70 percent of all banks) in this country hold only 8 percent of the total assets of the banking industry. Most of these banks are located in small one- or two-bank towns. In contrast, the largest 195 bank (about 2 percent of all banks) control 67 percent of the total assets of the industry.

D. STABILITY OF THE INDUSTRY

It is expected that the commercial banking industry will continue to experience more consolidations and mergers, thus causing the number of banks to decline.

Strong capital levels, healthy loan loss reserves, respectable loan growth, diversification into additional fee-based business, and expansion and cost cutting, through consolidation are expected to continue to boost earnings. A more accommodating interest rate policy by the Federal Reserve and a relaxed regulatory environment will preserve the important underpinnings that have served the banking industry well in recent years. However, some sources of bank earnings are less robust. Specifically, large banks with trading and international credit exposure are likely to see a slowdown in earnings. This reflects a more difficult equity market environment and more conservative credit underwriting, which could cause loan loss provisions to increase.

3. PRODUCTION INFORMATION

A. SERVICE DELIVERY PROCESS

The most important role of commercial banks is financial intermediation. That is, commercial banks are prepared to assume the risk of agreeing to pay depositors for their excess funds (usually with interest, sometimes with services) and then finding others who are willing to pay amounts in excess of the expenses of the intermediaries for the use of the funds. Financial intermediation occurs in the form of loan origination, loans, standby letters of credit, asset backed financing, trust, checking accounts, saving accounts, etc. There are also services that may be considered as ancillary services such as ATM transactions, lockbox and the sale of traveler's checks, money orders etc. Revenues derived from commercial banking activities are differentiated according to the type of service rendered. That is, revenues can be from interest or fees. For example, revenue from loans is in the form of interest, while revenue from letters of credit is in the form of fees. Consumers often pay for services in the form of interest and/or fees, and are the primary market of many banks. To serve that market, a wide variety of transactions and savings deposits are offered, as well as a similarly large variety of investment loan and trust products. These products and services are directed at different market segments, and are tailored in ways that satisfy each of them.

B. TYPES OF SERVICES AND ESTIMATED VALUE OF OUTPUT

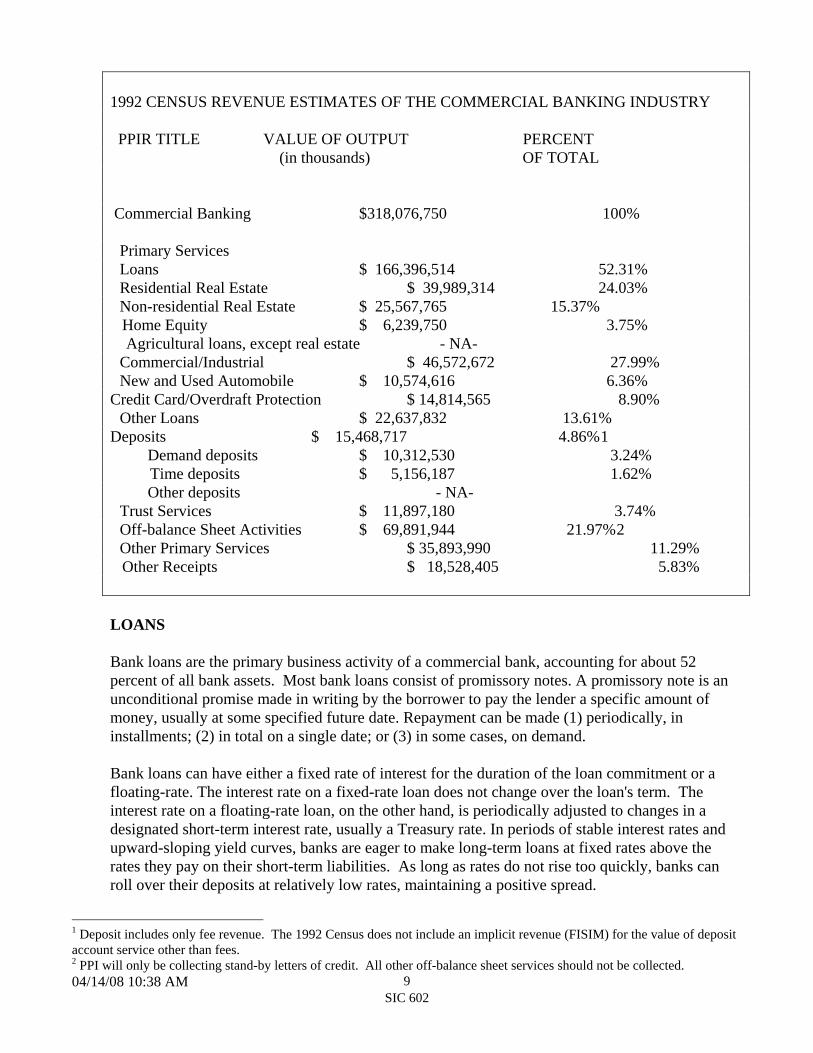

The commercial banking industry provides financial intermediation. That is, the commercial banks function to gather and allocate funds in the economy. The following pages describe the major service lines of the commercial banking industry. The table below shows the value of receipts for each major service line with in SIC 6023 and the percentage of total industry revenue that each service line represents.

8

04/14/08 10:38 AM SIC 602

9

1992 CENSUS REVENUE ESTIMATES OF THE COMMERCIAL BANKING INDUSTRY PPIR TITLE VALUE OF OUTPUT PERCENT (in thousands) OF TOTAL Commercial Banking $318,076,750 100% Primary Services Loans $ 166,396,514 52.31% Residential Real Estate $ 39,989,314 24.03% Non-residential Real Estate $ 25,567,765 15.37% Home Equity $ 6,239,750 3.75% Agricultural loans, except real estate - NA- Commercial/Industrial $ 46,572,672 27.99% New and Used Automobile $ 10,574,616 6.36% Credit Card/Overdraft Protection $ 14,814,565 8.90% Other Loans $ 22,637,832 13.61% Deposits $ 15,468,717 4.86%1 Demand deposits $ 10,312,530 3.24% Time deposits $ 5,156,187 1.62% Other deposits - NA- Trust Services $ 11,897,180 3.74% Off-balance Sheet Activities $ 69,891,944 21.97%2 Other Primary Services $ 35,893,990 11.29% Other Receipts $ 18,528,405 5.83% LOANS Bank loans are the primary business activity of a commercial bank, accounting for about 52 percent of all bank assets. Most bank loans consist of promissory notes. A promissory note is an unconditional promise made in writing by the borrower to pay the lender a specific amount of money, usually at some specified future date. Repayment can be made (1) periodically, in installments; (2) in total on a single date; or (3) in some cases, on demand. Bank loans can have either a fixed rate of interest for the duration of the loan commitment or a floating-rate. The interest rate on a fixed-rate loan does not change over the loan's term. The interest rate on a floating-rate loan, on the other hand, is periodically adjusted to changes in a designated short-term interest rate, usually a Treasury rate. In periods of stable interest rates and upward-sloping yield curves, banks are eager to make long-term loans at fixed rates above the rates they pay on their short-term liabilities. As long as rates do not rise too quickly, banks can roll over their deposits at relatively low rates, maintaining a positive spread.

1 Deposit includes only fee revenue. The 1992 Census does not include an implicit revenue (FISIM) for the value of deposit account service other than fees. 2 PPI will only be collecting stand-by letters of credit. All other off-balance sheet services should not be collected.

Banks loans may be secured or unsecured. The security or collateral, may consist of merchandise, inventory, accounts receivable, plant and equipment, and, in some instances, even stocks and bonds. Unsecured loans are available for certain customers with excellent credit ratings and history. There are three types of loan commitments that may be agreed upon by business borrowers and commercial banks: line of credit, term loan, and revolving credit. Consumers usually do not enter into these types of arrangements. The purpose of the loan commitment is to (1) provide some assurance to the borrower that the funds will be available if and when they are needed and (2) provide the lender with a basic format for structuring the customer's loan request properly. A line of credit is an agreement under which a bank customer can borrow up to a predetermined limit on a short-term basis (less than one year). The line of credit is a moral obligation and not a legal commitment on the part of a bank. Thus, if a company's circumstance change, a bank may cancel or change the amount of the limit at any time. A term loan is a formal legal agreement under which a bank will lend a customer a certain dollar amount for a period exceeding one year. The loan may be amortized over the life of the loan or paid in a lump sum at maturity. Revolving credit is a formal legal agreement under which a bank agrees to lend up to a certain limit for a period exceeding one year. A company has the flexibility to borrow, repay, or re-borrow as it sees fit during the revolving credit period. At the end of the period, all outstanding loan balances are payable, or, if stipulated, they may be converted into a term loan. In a sense, revolving credit is a long-term, legally binding line of credit. In addition to the loan criteria mentioned above, there are three basic types of business loans, depending on the borrower's need for funds and source of repayment. A bridge loan supplies cash for a specific transaction, and repayment is made from cash flows from an identifiable source. Usually, the purpose of the loan and the source of repayment are related; hence the term "bridge loan". A seasonal loan provides term financing to take care of temporary discrepancies between business revenues and expenses that are due to the manufacturing or sales cycle of a business. For example, a retail business may borrow money to build inventory in anticipation of heavy Christmas sales and may expect to repay it after the new year begins. Long-term asset loans are seasonal loans with a longer term. An example would be a manufacturing company purchasing new production equipment with a seven year expected life. The new equipment should increase the firm's cash flow in future years. The loan would then be repaid over seven years from the firm's yearly cash flow. Bank's long-term asset loans typically have maturities ranging between one and ten years. REAL ESTATE: RESIDENTIAL AND NON RESIDENTIAL Mortgage loans finance the purchase, construction, and remodeling of both residential housing and commercial facilities. Mortgage loans are collateralized by the real estate they finance. They are

10

04/14/08 10:38 AM SIC 602

11

long term loans with an average maturity of about 25 years, but maturities may vary between 10 and 30 years. Historically, mortgages had a fixed interest rate, with borrowers paying the loans back in fixed monthly installments. In recent years, more mortgage loans have been variable-rate mortgages, in which the interest rate and monthly payments vary with the market index, usually within a prescribed range. The amount of down payment affects the interest rate charged on a mortgage loan. Higher down payments reduce the risk of loss to the mortgage holder in the event that the home must be repossessed for the owner's failure to make mortgage payments or for some other breach of contract. Down payments range from 10 to 30 percent of the purchase price.

HOME EQUITY LOANS

Home equity lines of credit are usually arranged at the time a customer signs his/her mortgage. The bank sets a fixed amount of borrowing power, ranging from $5,000 to $250,000, that is available to customer in the next 5 to 10 years. During that time a customer can take a loan any time s/he wants, with no additional approval required from the bank. Home-equity loans are accessed in different ways, depending on the lender. Banks may supply checks credit or debit cards, or attach the line of credit to the customer's checking account. The customer may pay interest only on the money that s/he actually uses, at a variable rate. The minimum loan is usually $250 to $500.

AGRICULTURAL LOANS In addition to the loans mentioned above, there are also loans for certain clients. There are agricultural loans that are both short-term and long-term to farmers to finance farming activities. These loans represent an important source of lending at many small rural banks. Small banks (assets less than $100 million) account for almost 50 percent of agricultural lending by all commercial banks. Short-term agricultural loans are generally seasonal and are made primarily to provide farmers with funds to purchase seed, fertilizer, and livestock. In making these loans, specialized knowledge of farm products is required, and the lending officer usually inspects the applicant's farming operation once a year.

COMMERCIAL LOANS Commercial, industrial or business loans are also both short-terms and long term to small businesses, and corporations. Most of these loans are secured by merchandise, inventory, accounts receivable, and plant and equipment. There are three types of loan commitments that may be agreed upon by business borrowers and commercial banks: line of credit, term loan, and revolving credit. Consumers usually do not enter into these types of arrangements. The purpose of the loan commitment is to (1) provide some assurance to the borrower that the funds will be available if and when they are needed and (2) provide the lender with a basic format for structuring the customer's loan request properly.

A line of credit is an agreement under which a bank customer can borrow up to a predetermined limit on a short-term basis (less than one year). The line of credit is a moral obligation and not a legal commitment on the part of a bank. Thus, if a company's circumstance change, a bank may cancel or change the amount of the limit at any time. A term loan is a formal legal agreement under which a bank will lend a customer a certain dollar amount for a period exceeding one year. The loan may be amortized over the life of the loan or paid in a lump sum at maturity. Revolving credit is a formal legal agreement under which a bank agrees to lend up to a certain limit for a period exceeding one year. A company has the flexibility to borrow, repay, or re-borrow as it sees fit during the revolving credit period. At the end of the period, all outstanding loan balances are payable, or, if stipulated, they may be converted into a term loan. In a sense, revolving credit is a long-term, legally binding line of credit. In addition to the loan criteria mentioned above, there are three basic types of business loans, depending on the borrower's need for funds and source of repayment. A bridge loan supplies cash for a specific transaction, and repayment is made from cash flows from an identifiable source. Usually, the purpose of the loan and the source of repayment are related; hence the term "bridge loan". A seasonal loan provides term financing to take care of temporary discrepancies between business revenues and expenses that are due to the manufacturing or sales cycle of a business. For example, a retail business may borrow money to build inventory in anticipation of heavy Christmas sales and may expect to repay it after the new year begins. Long-term asset loans are seasonal loans with a longer term. An example would be a manufacturing company purchasing new production equipment with a seven year expected life. The new equipment should increase the firm's cash flow in future years. The loan would then be repaid over seven years from the firm's yearly cash flow. Bank's long-term asset loans typically have maturities ranging between one and ten years. CONSUMER LOANS AND OTHER LOAN SERVICES Bank loans to individuals are known as consumer loans. Their maturities and conditions vary widely with the type of purchase. Maturities can be as short as one month or as long as five years for automobile loans. Longer-term loans, which are typically paid on an installment basis, are generally secured by the item purchased, as in the case of the automobile loans. Shorter-term loans are usually single-payment loans. New and Used Auto and Truck Loans As was mentioned above, automobile loans often have maturities for five years, and are typically paid on an installment basis. Credit Cards

12

04/14/08 10:38 AM SIC 602

13

The most ubiquitous of all loans, however, is the credit card loan. These cards are presented to merchants who accept them as a draft, which they can present to the issuing bank and be paid the amount advanced by the merchant for the purchase. For most credit card customers, the card is the equivalent of money borrowed without any hassle. Credit cards are a menu of products. Different customers will qualify for or will want different combination from the menu, and for that will pay different prices in the form of different annual fees, interest rates on balances, grace periods, etc. For the consumer, the holder of a credit is guaranteed a credit limit at the time the card is issued. The dollar amount of the credit lines varies with the cardholder's income and employment record. In general, credit lines to individuals are limited to one month's income. The bank sets a minimum monthly payment that must be paid. The interest charged for credit card installments usually varies between 1 and 2 percent per month (12 and 24 percent annum) on the unpaid balance. The cardholder may receive the card free or may pay an annual membership fee between $15 and $300, depending on the services the card offers to the cardholder Rates on credit cards vary, depending upon the credit profile of the customer, what features in addition to the basic credit function are available to the cardholder through the card, the history and forecast for credit and fraud losses to the issuer, the rate paid on money used to fund the credit card loans, the existence or amount of an annual fee, and a number of other variables. Over Draft Protection A checking account associated with a line of credit that allows a person to write checks for more than the actual balance in the account, with a finance charge on the overdraft. Commercial banks derive fees from a reserve of funds accessible to creditworthy customers with demand deposits. This reserve of funds is an indirect line of credit available to customers when checks drawn an their account are not covered by the customer's deposits.

Financial Institutional loans

Banks make loans to other financial institutions, such as their respondent banks, sales finance companies, savings and loan associations, and brokers and dealers in securities. Large banks usually make these loans for a variety of purposes. Sales finance companies that engage primarily in consumer installment lending obtain a large proportion of their funds from commercial banks. Large banks also lend to stock brokerage firms and dealers in U.S. government securities. Brokerage firms may extend credit to customers up to a certain percentage of the purchase price of the stock. These loans -called margin loans are collateralized by the securities purchased.

Loan Origination

Most mortgage lenders charge a substantial origination fee (often 1- percent of the mortgage balance) on mortgage loans that they make or arrange. The fee compensates them for the time and effort needed to ensure that the mortgage does not involve excessive credit risk and for evaluating and preparing a loan. Revenue from this service originates from residential real estate loans, non-residential real estate loans, and other loans. Closing costs such as discount points, title insurance,

escrow fees, attorney fees, recording fees, appraisal fees, notary fees, and so forth, are sometimes included in this fee based services category. Loan Servicing In order to maintain correspondence between the borrower and the lender concerning a loan,

the following activities are involved: Preparation and mailing to borrower of monthly loan payment coupons. Collection of monthly payments from borrowers and disbursement to investors within 10 days

of receipt. Mailing of late notices to borrowers when necessary. Preparation and submission of payoff demands. Tracking of status of senior loan and fire insurance; letters to investors if action is required. All telephone and written communication to borrowers and investor. Maintenance of trust account. Immediate referral to in-house foreclosure department of all loans which become 40 days

delinquent. If necessary, immediate referral to on-line legal staff of all files in which the trustor files

bankruptcy or assignment of rent action is required. Preparation and filing of required 1099 and 1098 reports to the IRS and Franchise Tax Board.

Leasing Banks, upon the request of customers, purchase properties and lease them back to the customers. Bank leasing activities for large banks involve big-ticket items such as commercial aircraft, ocean-going tankers, computers, and nuclear generators for utilities. Other items leased by both large and small banks include office equipment, automobiles, trucks and machinery. The majority of bank leasing activities is with business firms, although leasing of automobiles to individuals is gaining in popularity.

DEPOSITS The principal source of funds for most banks is deposit accounts: demand, time, savings, and NOW deposits. Individuals may now choose from among a number of deposit products, including the traditional demand deposit account on which the law prohibits payment of interest; regular savings account on which interest is paid but withdrawals are sometimes limited; Negotiable Order of Withdrawal (NOW) accounts, or other negotiable withdrawal accounts upon which interest is paid and checks are drawn; various kinds of time or certificate accounts which bear interest and which mature at a specific time and on which, until maturity, withdrawals are limited or require the customer to forfeit a penalty; and Individual Retirement Account (IRA) or Keogh accounts which are designed for individual retirement purposes. Some accounts have been specifically established to serve consumers who need only a limited number of checks a month, and whose account balances will not be large. Efforts to explain basic

14

04/14/08 10:38 AM SIC 602

15

banking services and requirements to consumers who have not had bank accounts are part of the services provided to many of those customers. Banks are creative, and are offering their individual customers a variety of interest rate options coupled with these basic deposit products. Some, for example, have paid a varying rate of interest on an account depending upon variation in the rate of money market instruments. Others will vary the rate depending upon the length of time that the depositor leaves the deposit in the bank, or the number of transactions which are permitted monthly. For the individual consumer, therefore, the decision now is not whether he or she will deposit their funds in a bank, it is rather what deposit instrument should he or she select. More recently, so as to accommodate the need of small businesses, commercial banks have developed 'sweep accounts', which is basically a deposit account with a minimum balance. Amounts over the minimum balance are swept into investments accounts overnight or for a certain period of time so as to earn interest.

Automated Teller Machine Services (ATM) Associated with deposit services are ATM services that facilitate customers deposit transactions. Shared remote terminals can accommodate cross transfers of funds between institutions or withdrawals of funds from any of several institutions. Cross transfers of funds or pooled use of joint terminals require communications networks to be established to verify that customers have sufficient funds in their accounts so that they can be transferred according to customers' request. Such operations are facilitated when institutions link their account balance verification information through a single electronic switch. ATM services are collected as a part of the deposit price. ATM services are considered as bundled services. That is, an ATM transaction does not exist unless there is a deposit account. TRUST OPERATIONS Trust operations involve the bank's acting in a fiduciary capacity for an individual or a legal entity, such as a corporation or the estate of a deceased person. This typically involves holding and managing trust assets for the benefit of a third party. Equity investment constitute about two thirds of the total assets of bank trust departments, and the banks administer these securities rather than own them. Nearly one-half of all trust assets are managed for individual accounts. This frequently involves the settlement of estates. The trust assures that the terms and conditions of the will are fulfilled, sees that claims against the estate are settled, and manages the assets of the estate during the interim period. Banks also administer personal trusts for those not wishing or unable to undertake this responsibility for themselves. The second largest group of trust assets managed by banks is for pension funds. Bank trust departments also perform functions other than managing or investing assets. They frequently act as transfer agents, registrars, dividend disbursement agents, trustees, seeing that the conditions of the bond contract are carried out by the issuer on behalf of the bondholders.

OTHER BANKING SERVICES Standby Letters of Credit A standby letter of credit (SLC) is a contractual agreement issued by a bank that involves three parties: the bank, the bank's customer, and a beneficiary. In an SLC transaction, the bank acts as a third party in a commercial transaction between the bank's customer and the beneficiary substituting the bank's creditworthiness for that of its customer. Thus, if the bank's customer fails to meet the terms and conditions of the commercial contract, the bank guarantees the performance of the contact stipulated by the terms of the SLC. The bank's obligation under an SLC is a contingent liability, because no funds are advanced unless the contract is breached by the bank's customer and the bank has to make good on its guarantee. For example, a corporation needing to finance inventory for three months decides to obtain money through the sale of commercial paper with an SLC rather than through a commercial bank loan. The SLC guarantees principal and interest payments to investors who buy the commercial paper in the event that the corporation defaults on its obligation. The SLC is payable only upon presentation of evidence of default or nonperformance on the part of the corporation. Large, well-known banks of the highest credit standing issue most SLCs. There are SLCs associated with export or import. In this case SLC guarantees the payment of a customer's drafts up to a stated amount for a specified period, which is used primarily in trade and insurance transactions, and between U.S. and foreign individuals. There is also an SLC assuring performance on a contract, for example, a real estate contract, and SLC assuring performance on bonds, taxable or tax-exempt, used by municipalities to obtain higher credit rating on bond issuance.

Correspondent Banking Correspondent banking involves the sale of bank services to other banks and to non-bank financial institutions. Correspondent banks typically act as agents for respondent banks in check clearing, and collection, purchase of securities, purchase and sale of foreign exchange, and participation in large loans. Correspondent banks also provide electronic data processing for deposit accounts, installment loans, and payroll. They provide investment and trust department advice, prepare reports on economic and financial market conditions. Correspondent banks buy and sell government securities, foreign exchange, Federal Funds, and other financial securities for respondent banks. They may also serve as a clearing house for job applicants, assist in forming holding companies or opening new branches, or help respondents find sources of equity capital or other long-term funds. The check clearing process works in the following manner: when a check drawn on Bank A is cashed by a merchant, the merchant, the merchant's bank (bank B) the clearinghouse or the Federal Reserve, and any correspondent banks for Bank A and B all accept the check subject to final payment. Once the check passes through the hands of all these entities and reaches Bank A, Bank A (if there are sufficient funds in the check writer's account) subtracts the balance from the check writer's account and transfers funds to the party that presented Bank A with the check. If

16

04/14/08 10:38 AM SIC 602

17

there are not sufficient funds in the depositer's account to pay the check, it is marked "NSF" and bounced or returned, by the way it came, to the merchant who initially accepted it. Almost every important bank in the world maintains an operating office in New York, and almost every large bank in the U.S. maintains a correspondent relationship with at least one large bank in that city. Chicago is the second most important correspondent banking city. Sale of Securities Commercial banks are the most important sellers of money market instruments. Banks sell money market instruments such as treasury bills, notes and bonds, agency securities, commercial paper, banker's acceptances, federal funds and repurchase agreements. During periods of cyclical boom, banks are typically faced with the problem of reserve deficiencies because of heavy loan demand. Therefore, needed reserves can be obtained by selling securities, such as short term securities from their investment portfolio. CASH MANAGEMENT SERVICES Banks handle payroll, cash forecasts, transfer of funds between accounts, pension and profit sharing plan administration, investment administration, automatic bill paying, check information, home banking through personal computer, lock box service, and sell foreign exchange, travelers checks, certified checks and money orders. Cash forecast Banks have established systems so that their customers can know, throughout the course of a business day, the precise status of collected and uncollected checks. Other bank systems control disbursements for the customer, thereby avoiding lapses in the customer's cash management program. Check information Information on checks paid or not paid can be provided to customers. When checks clear through the banking system, they carry substantial information, including who paid whom and for what financial institutions assisted in their clearing. This information provides proof of payment for tax and legal purposes (in case someone claims that a contract was not fulfilled). Automatic bill payment There are a wide variety of uses of electronic funds transfer technologies. One of the first uses was for the transfer of computerized credit card clearing information. Other uses often require automated clearinghouses (ACHs). ACHs can provide either credit transfers, in which the initiating institution sends funds through the system to be deposited in the recipient's account, or debit transfers, in which the initiating institution withdraws funds from the depositor's account.

Major examples of credit transfers are automatic deposits of payrolls, and bill payments by telephone. Examples of debit transfers are preauthorized bill payments, transfers initiated by point-of-sale (POS) transactions, check truncation, and cash withdrawals from ATMs. Regular payments to the same individual can be made efficiently through automated clearinghouses. The bank of the paying organization gives the ACH a computer tape that provides information on the banks and account numbers of a firm's or agency employees (or government pension and Social Security recipients) who are to be paid. The clearinghouse then credits the account of the receiving bank (or other financial institutions) with the total due and provides data indicating which depositor's accounts should be credited. The bank that submits the tape provides funds to the clearinghouse if its payments exceed its receipts at the clearinghouse from other sources. Bill payment can be made efficiently through ACHs using telephone or cable television lines. To make payment, the depositor dials the bank, enters his or her account number, the amount he or she wishes to pay, and the coded bank and account numbers of the recipient of the payment. If the depositor provides data electronically (as with a touch-tone phone), the payment information can be verified and entered directly on a magnetic tape for submission to an ACH, which will make the appropriate credit transfers. Verbal information cannot be handled as cheaply or with few errors as touch-tone information. Consumers can authorize their banks or other depository institutions to make payments on their mortgages, utilities, rent, insurance, or other regularly recurring bills when they come due. Under such as system, the institution that is to receive the payment creates a tape indicating what amount it is to receive, from whom, and when. It sends the tape to an ACH to receive payment. The ACH obtains the funds from its customers' bank, which in turn subtract them from their customer's accounts. Check Truncation works like computerized billing of debit or credit card payment. When a check is cashed, it is held by the institution that received it (or, more commonly, that institution's bank). Then, by electronic means, the account on which the consumer wrote the check is debited, and the account of the merchant who deposited the check is credited. Because electronic impulses travel faster than paper, check truncation is widely used with NOW accounts. Banks offer customer access to Fedwire, an electronic funds transfer system administered by the Federal Reserve, by which transfers of trillions of dollars of deposits a day are made electronically throughout the banking system. Purchases and sales of securities for customers and for their own accounts are made over Fedwire. Home Banking The reduced cost of computer and communications technology has also made home banking feasible. Home banking computers use connections over telephone lines or cable television networks to access a depository institution's account records. Most allow people to check their account balances, pay their bills and transfer funds among accounts. Many also allow people to keep home budget, accounting, and tax records in an organized fashion. Lock Box Service

18

04/14/08 10:38 AM SIC 602

19

Lock box service, for example, operates with a corporate customer, through use of a post office box serviced by the bank. These are usually in more than one geographic location at which payments can be made. They have increased the ability of many corporate treasurers to expedite collections and minimize cash and borrowing needs. In addition to the above services, there are also brokerage, insurance and advisory services that are rendered by commercial banks which are regarded as “other receipts.”

C. PRICE DETERMINING CHARACTERISTICS

DEPOSITS Different customers have different deposit accounts. Some of these customers are individuals, government (state, local and U.S. Treasury Department), small banks small businesses and large corporations or institutions. Demand Deposit Efficiency or budget checking, student checking, regular checking, money market, small business checking (sweep account) and Interest on Lawyers' Trust Account (IOLTA) are some of the price determining characteristics for demand deposits. In order to have a checking account with one of the criteria above, a minimum balance is usually required. For example, a budget checking requires no minimum balance whereas regular checking account requires a minimum balance. Other price determining price characteristics are based on the restrictions of the demand deposit account. There are restrictions such as how many checks can be written per month, and if the demand account is a money market account, there is restriction or limitation on the number of withdrawals. Intuitively, budget checking accounts have most restrictions. Savings Account There are different kinds of savings accounts such as passbook savings, Negotiable Order of Withdrawals (NOW), and Money Market Deposit Account (MMDA). MMDAs have a minimum balance requirement. In addition to individuals, non-profit organizations are the major customers. Time Deposits Examples of time deposits are Certificate of Deposits (CDs), savings certificates, Money Market Certificates (MMC), Individual Retirement Account (IRA), and Keogh. Consumers or other small depositors primarily hold savings certificates. These certificates are issued in a designated amount, specifying a fixed rate of interest and maturity date. MMCs are designed primarily to service consumers and small businesses. Banks can issue 91-day as well as six-month maturity deposit certificates with a minimum balance of $7,500 and an interest rate tied

to the 13-week Treasury bill rate. CDs are issued in denominations of $100,000 or more to business firms and individuals. They have a fixed maturity date, pay an explicit rate of interest, and are negotiable if they meet certain legal specifications. Negotiable CDs are issued by large, well-known commercial banks of the highest credit standing and are traded actively in an well-organized secondary market. CDs can be redeemed at any time in the secondary market without loss of deposit funds to the bank. The interest rate on CDs is competitive with the rates on comparable money market instruments. For IRA accounts, an individual has to be less than 70 1/2 years of age. Individuals can make contributions up to $2,000. The amount of pretax funds that an individual is eligible to invest in IRAs is reduced if the individual is a participant in an employer-maintained fund. There is also a self directed IRA in which the customer can move funds from money market accounts into mutual funds, CDs, or securities.

LOANS All loans in general have the following price determining characteristics. Consumer: individual or retail, small business, non-profit, business, financial institution, real estate Repayments: periodically, installments, in total, on demand Interest Rate: fixed rate, floating rate Collateral: secured, unsecured Length of Loan: short term, long term Loan Commitment: line of credit, term loan, revolving credit Business Loan: bridge loan, seasonal loan, long-term asset loan Thus, based on the above characteristics, a small business can have a long term unsecured line of credit loan with a fixed rate of interest. Price determining characteristics based on the type of client or a particular sector are as follow: Real Estate Loan Price determining characteristics for real-estate loans depends on the purchase, construction or remodeling of residential housing or commercial facilities. The loan maturity will typically vary between 10 and 30 years. The amount of down payment is also a characteristic that affects the price of the loan. Down payments typically range from 5 to 30 percent of the purchase price. Another type of real-estate loan is the home equity loan or line of credit. There is a fixed amount of funds that can be borrowed. For example, the fixed amount varies between $5,000 to $25,000. This line of credit may be available to the client for the next 5 to 10 years after obtaining the loan. Banks may supply checks, credit or debit cards, or attach a line of credit to the customer's checking account.

Agricultural Loans Short-term agricultural loans to farmers tend to be seasonal.

20

04/14/08 10:38 AM SIC 602

21

Financial Institutional Loans Financial institutions are respondent banks, sales finance companies, savings and loan associations, investment banks, and brokers and dealers. Loans made to brokers and dealers are called margin loans, and are collaterilized by securities. Consumer Loans Consumer loans can be any type of loans. More commonly, consumer loans are automobile loans. Maturities on consumer loans can be as short as one month or as long as five years. Most ubiquitous of all consumer loans is the credit card loan. Price determining characteristics for credit card loans are as follows: type of customer annual fees interest rates balances credit limit grace period

cardholder's income cardholder's employment record membership fee type of credit card (regular, gold, platinum) credit profile of cardholder cardholders payment history

Over draft protection is another type of consumer loan. A checking account is associated with this type of loan. This loan allows the consumer to write checks for more than the actual balance in the customer's deposit account. TRUST OPERATIONS The types of client can determine the price determining characteristics for trust operations. Clients can be corporation, organizations, pension funds or individuals. The value or amount placed in trust, and procedures on how to settle the trusts are also price determining. Banks can administer the trust or have customers administer their own trust. In addition, clarifications should be made whether the bank also performs transfer, registration, dividend disbursement, or trustee services. OFF BALANCE SHEET SERVICES For standby letters of credit (only service priced in this category), the value of the asset is the primary price determining characteristic.

D. CUSTOM SERVICE

Almost all the primary services such as deposits, loans, trust and off-balance sheet activities tend to be customer service oriented, and are therefore custom in this sense. These services are products specifically produced for a given buyer. In this sense, there are rarely any standardized products in the banking industry.

Service such as deposits and ATM transactions require more than one visit from the consumer and these services charge a fee based on the per item transacted. Other services however, require on average just one visit from the customer, and the customer is able to specify the services.

E. SEASONALITY Certain services provided in the banking industry are seasonal. The seasonality of the industry depends to a larger extent on the U.S. and to some extent on the global economy. For example, products such as loans, money market, and derivative instruments are interest rate sensitive. A lower interest rate will increase demand for loans and decrease the demand for money market instruments. Services such as the off-balance sheet activities, in particular derivatives financial futures, are influenced by global economic conditions since banks derive revenue based on the spread between countries' interest rates. Because the bulk of bank profits is derived from net interest income (the interest income received on loans minus the interest expense for borrowed funds), interest rates determine to a large extent how profitable a bank can be. Also, net interest margin (a bank's net interest income divided by its average earnings assets) is a common measure of a bank's ability to squeeze profits from its loans. Net interest margins widen or narrow depending on the direction of interest rates, the mix of funding sources underlying loans, and the duration, or time period until expiration, on the investment portfolio. Falling interest rates have a positive effect on banks for several reasons. One is that net interest rate margins can expand, at least in the short term. They can do so because banks are still earning a higher than market yield on loans to customers, while the cost of funds goes down more quickly in response to the new, lower loan rates. Second, declining rates enhance the value of a bank's fixed-rate investment portfolio, since a bond with a higher stated interest rate becomes more valuable as prevailing rates drop. Noninterest income such as, trust income, securities processing, mortgage banking and brokerage income, has become a favorite avenue of revenue growth for banks since this income is not dependent on interest rates.

F. SERVICE SUBSTITUTION It is anticipated that there will be few items to quality adjust in the commercial banking industry, with most relating to characteristics of the loan or deposit service. These characteristics are the number of accounts in the portfolio and average number of transactions per account. Because of the constant changes in the industry in terms of efficiency and technology, it is anticipated that services such as deposits, loans, and correspondent banking may change. Currently, more and more banks are experimenting with Internet banking in which customers can conduct all of their deposit transactions on line. This Internet service will eliminate certain bundled services that are associated with deposit services. For example, services such as account inquiry, telephone banking, check orders, deposit verification, statements etc., will be eliminated. Banks are hoping to get the majority of their customers to bank online.

2

04/14/08 10:38 AM SIC 602

3

Service such as loan servicing that is associated with loans may be eliminated due to better technology in which customers can make loan payments and correspondence concerning their loan via the computer. Also, because of better computers and more affordable computers, smaller banks may be able to conduct most of their services themselves without relying on larger correspondent banks to perform services for them. In the future, customers who have deposit accounts plus mortgages and portfolios may receive one statement which explain the activities of all the services instead of one statement per account. This one statement may explain how funds were automatically transferred from the checking account to pay the mortgage, and how the dividends earned from the portfolio were transferred to the checking account.

4. MARKET AND TRANSACTION INFORMATION

A. INTERPLANT AND INTRAINDUSTRY PAYMENTS Through correspondent banking, banks are involved in the sale of bank services to other banks. As was mentioned above, correspondent banks usually act as agents for respondent banks in check clearing and collection, purchase of securities, purchase and sale of foreign exchange, and participation in large loans. In the U.S. there are more than 8,000 banks, most of which are small and operating only one office. These banks find it either impossible or inefficient to produce certain types of services needed by their customers. Small rural banks often maintain correspondent banking with five or more larger banks in regional financial centers. Regional financial center banks maintain correspondent balances with 30 or more banks in national financial centers as well as with banks in other regional financial centers. The center for American correspondent banking is New York City. This is because New York is the nation's financial center, with its short-term money markets, foreign exchange markets, and long-term capital markets. Almost every important bank in the United States maintains a correspondent relationship with at least one large bank in that city. Chicago is the second most important banking city. Nevertheless, in addition to check clearing, correspondent banks often participate in loans arranged by respondents. The respondent bank may want outside help with some loans because demand outstrips regional supplies of funds or because the loan exceeds the bank's legal lending limit. Loan participation also helps respondents diversify their loan portfolios and reduce overall risk on their loans. Correspondent banks also provide electronic data processing for deposit accounts, installment loans, and payrolls. They provide investment and trust department advice, and prepare reports on economic and financial market conditions. Correspondent banks also buy and sell government securities, foreign exchange, Federal Funds, and other financial securities for respondent banks. They may also serve as clearinghouses for job applicants, assist in forming holding companies or opening new branches, or help respondents find sources of equity capital or other long-term funds.

B. PRICE BEHAVIOR

The explicit (fee) prices for deposits have been increasing over the last few years due to banks need to increase profits. Mundane services associated with a checking account that used to be free are now charged to customers. These are services such as access to teller, and the use of deposit/withdrawal slips etc. In the past a customer could go to a teller to make a deposit and ask for a deposit slip. Now there is a charge just for a visit to the teller and another charge for the deposit slip. Banks are now finding many creative ways of charging customers. It should be pointed out however, that most banks practice price discrimination in the sense that the case presented above only applies to a customer that has a basic checking account. There are other types of checking accounts that charge for a few services, and some that do not charge for any services. The type of checking account a customer has depends on the amount placed in deposit and maintaining a minimum balance. Other services such as loan origination, loan servicing, leasing, trust operations, and cash management services prices are stable. The prices for services such as correspondent banking, off-balance sheet activities, and brokerage and advisory services tend to vary depending on the negotiations between the bank and the customers who purchase these services. Large banks tend to sometimes charge more for some services, and even charge for some services that are offered free at other smaller banks. The rationale for this is the case that they have higher overhead costs. Small banks usually offer some of their services for free to attract new customers and to retain customers they already have. Because of more services offered by larger banks such as internet banking for example, customers from these small banks tend to open accounts at these larger banks. Therefore, to retain customers small banks will provide, free checking, for example. Some banks are experts in construction lending, while some are experts in agricultural lending. Therefore, there would be an inelastic supply of agricultural loans in non-farming areas. Smaller banks frequently serve the less densely populated areas of the country, with most of them located in states in which farming still plays an important role in the economy. Without these banks, however, those communities and business, which are served by those communities, would not prosper. The balance sheets of large and small banks will tend to be different. Generally, smaller banks will invest more in government securities (buying and selling more treasury bonds and bills) as much as 40-50% compared with under 20% for larger banks. Smaller banks will lend a smaller percent of their deposits than will larger banks. Larger banks service more of the larger businesses. The largest banks, particularly the super-regionals or those in the money centers such as New York City or Chicago, have a different set of customers since those communities are home to international companies with worldwide businesses, and securities and investment banking firms that frequently need very large advances from their banks. A very few of the largest banks have moved almost entirely into wholesale banking, engaging in large trading activities and foreign exchange activities, a broad range of risk management

4

04/14/08 10:38 AM SIC 602

5

functions for corporate clients, and through affiliates, in significant underwriting activity. Some of these banks, for example, have almost entirely withdrawn from the retail market, in some cases holding less than 10 percent of their deposits in accounts of a size small enough to be fully insured by the FDIC. Finally, an even smaller number of the largest banks have continued a strategy in which they provide the greatest variety of financial services to a variety of customers. Thus, commercial banks throughout the country are facing a marketplace filled with tough competitors and demanding customers, and both the competitors and the customers might be from foreign countries, even if the banks are relatively small in size. Banks in small towns, in Nebraska, for example, may have developed products that are desired by companies in a number of countries, thereby necessitating an understanding by their banker of foreign laws, rules, and customs, export restrictions and procedures, currency exchange markets government programs available for export assistance, the possibility of joint ventures with complementary firms, etc. As was previously mentioned, the effects of interest rates have a significant effect on the price of products such as loans and deposits offered in the banking industry.

C. TYPES OF PRICES

REFERENCE RATE A reference rate is used in calculating in order to allocate earned income on loans between loans and implicit services on deposits The reference rate to be used represents the pure cost of borrowing funds- that is, a rate from which the risk premium has been eliminated to the greatest extent possible and which does not include any intermediation services. This rate is calculated by the Washington office TYPE OF PRICES FOR DEPOSITS “Interest less fees” All deposits will be priced at the portfolio level on a monthly basis. The following formula will be used to determine the deposit price:

{Reference Rate - Interest payments - Earned deposit fees } * $1,000 Average deposit balance The reference rate is calculated by the Washington Office as annual rate of 6.0%. It is preprinted on the checklist as a monthly rate of 0.50%, which is 6.0% divided by twelve. The respondent is to provide total interest payments made for the selected deposit portfolio for the calendar month, deposit fees earned for the month, and the average deposit balance for the month. The average deposit balance is to be calculated by dividing the sum of the ending daily balances for the calendar month by the number of days in the month.

A worksheet to assist in this calculation is provided in the checklist. LOANS “Interest income plus fees” All loans will be priced at the portfolio level on a monthly basis. The following formula will be used to determine the loan price:

{Earned interest income + Fees - Reference Rate } * $1,000 Average loan balance The reference rate is calculated by the Washington Office as annual rate of 6.0%. It is preprinted on the checklist as a monthly rate of 0.50%, which is 6.0% divided by twelve. The respondent is to provide total earned interest income for the selected loan portfolio for the calendar month, fees earned for the month, and the average loan balance for the month. The average deposit balance is to be calculated by dividing the sum of the ending daily balances for the calendar month by the number of days in the month. A worksheet to assist in this calculation is provided in the checklist.

NOTE: The Annual Percentage Rate (APR) incorporates loan origination and loan servicing fees that are associated with real estate, commercial, industrial, and home equity loans. Thus, for all real estate, commercial, industrial, and home equity loans, the loan yield (quoted interest rate) will be used in the estimation of the loan price. NOTE: If the bank does not separate loan servicing fees for loans that they do not hold from those fees earned on loans they do hold, they should be included as part of the fee component of this price. If fees for loans not held can be separated, price these services on fee basis as described below. TYPE OF PRICE FOR ALL OTHER SERVICES “Fee” The remaining services are price on a fee basis. Loan Servicing for loans not held (if separate records) : Banks can pool loans together and sell them to third parties. Banks may choose to continue to service the loans, such as handling loan payments, correspondence, and other services, while the third party collects interest payments. For this service, collect the percentage charged to third parties for loan servicing. When banks service their own loans, this income is captured in their interest earnings. Trust Operations: The fees that banks charge for trust operations are usually determined by a percent of the market value of the assets in custody at the banks. For example, a mutual fund may

6

04/14/08 10:38 AM SIC 602

7

place in custody assets valuing $1,000,000, and the bank may charge .05% to safeguard the assets. Therefore, the bank's fee is $1,000,000 times .05% or $5,000. Standby Letter of Credit: The fee for this service is based on a flat fee. The flat fee is determined in a contractual agreement between the bank and its customer. The price is calcalated as a percentage of the value of the assets. Cash management services The service can be provided on a flat fee or cost per item basis.

D. TYPES OF BUYERS It should be kept in mind that almost all individuals and organizations of the U.S. economy employ the services of commercial banks; however, the following will provide a more specific list of the types of buyers of SIC 6023 services: Retail: Banks depends on individuals for their deposits into transaction accounts. Some banks also target certain individuals to obtain their business such as senior citizens and students. Small businesses: Many small business and entrepreneurs rely on banks as a source of funding. Banks also have specialists available to work with only small businesses. Farmers: In agricultural areas, farmers are the main customers for banks that service their areas. Non-profit organizations: Because of their tax status, many banks provide special accounts for non-profit organizations. Trusts: Trust funds and accounts are managed, administered and executed by commercial banks. Mutual Fund: Most mutual funds assets are safeguarded in trusts at commercial banks. These banks also act as transfer agents and custodians for the mutual funds. Savings and Loan Associations: These banks employ the correspondence services of commercial banks. Non-bank financial institutions: These include credit unions, industrial loan associations, financing companies and loans associations who also employ correspondence services. Government: Municipal, state and federal government sell their bonds and/or treasury bills through the commercial banking system. Corporations: Large corporations such as investment banking firms, brokerages, multinational corporations employ the services of large well-established banks. Also certain banks only cater to these large institutional clients.

Many banks often differentiate between retail, business and corporate clients. As stated above retail clients are individuals. The major difference between business clients and corporate clients is the level of account activity. It is presumed that corporate clients have a higher level of account activity.

E. DISCOUNTS

Discounts are common in the commercial banking industry. A common type of discount that is granted is discount for customers who have several accounts with the bank. For example, some customers may have their deposit accounts, their mortgage account, their money market account, and their portfolio under management by the bank. For having these accounts, the bank may waive service fees or any number of fees for these kinds of customers. For deposits, discounts are given to students and senior citizens for demand deposits. Usually service charge or limitations on the account such as the number of checks written are waived. Discounts are also granted to large corporate clients because of the volume of transactions in their account. The discount granted in this case is usually unlimited check writing and no charge for additional services associated with corporate checking accounts. It is sometimes the case that discounts are granted on loans to institutional clients. In most cases fees are waived for origination, and in the case of real estate, closing costs. For trust operations, banks that perform additional services besides safeguarding assets sometimes waive the fees for those additional services. Some discounts are also given to bank customers who have their portfolio managed by the bank. Discounts are generally in the form of reduced management fees.

F. ADDITIONAL CHARGES

Because of the changing nature of the commercial banking industry in which new products are added, or existing products take on a new twist, additional charges can be incurred in the banking industry. In addition, banks are continuously expanding their services because of H.R. 10 (see litigation section below). Because of H.R. 10, underwriting and investment banking activities will be offered in some banks. These activities are not considered primary to the commercial banking industry thus they will be collected in other SICs such as 6282, Investment Advice and 6211, Securities, Brokers and Dealers.

G. SIZE OF PURCHASE In the commercial banking industry, service lines such as deposit accounts, no minimum purchase or balance is required. A savings account can be opened with just a few dollars at certain banks. For some checking accounts no minimum balance is required. This is the case for budget checking accounts. For all other service lines, a minimum purchase is required. Individual or retail customers who purchase deposit accounts, money market instruments such as bonds, and other items such as travelers checks, money orders, etc. at the commercial banks spend the smallest amount on the banks' products. Other clients such as businesses and other institutions spend large amounts at the commercial banks. For service lines such as off-balance sheet banking only large institutional clients with millions to trade can utilize the banks trading services.

8

04/14/08 10:38 AM SIC 602

9

H. CONTRACTS

To varying degrees all the services rendered in the commercial banking industry require a contract. For a simplistic service such as a demand deposit, a contractual agreement is reached between the bank and the customer. In this contract the customer agrees to the services the bank will provide for having a demand deposit, services such as ATM policies, overdraft fees, bounce fees etc. This contract usually terminates once the customer closes the account with the bank. Services such as loans, loan origination, and loan servicing involve long and extensive contracts specifying the terms and conditions of the loan to the borrower. These contracts usually last the length of the loan. For example, a contract for a mortgage lasts for 30 years if it is a 30-year mortgage. For other services such as leasing, trust operations, correspondent banking, brokerage and advisory, and cash management services, contracts are drawn which dictates the terms and conditions between the bank and the customer. Some of these contracts may have special criteria specified in the contract. For example, a correspondent and a respondent bank may make some special agreement on how the correspondent bank will be compensated. As an aside, some correspondent banks are paid in kind as oppose to fees. The contract for these services listed above are usually for one year.

I. OTHER VARIABLES AFFECTING PRICE