Embed Size (px)

Citation preview

Corporate Profile

April 2011

ShriramCity Union Finance Limited

SHRIRAM CITY UNION FINANCE LIMITED

Corporate profile

1 Corporate History and Company Overview

2 Financial performance over the years

3 Unique positioning and analysis

4 Competitive positioning

5 Shriram Group Eco-System

6 Future Growth

Company Overview

ShriramCity – Company Overview

ShriramCity is a major organized lender in

the Retail and Micro & small enterprises

credit space with leading market share in the

southern region.

Strategically present in multiple products,

with expertise in loan origination, valuation

and collection.

Unique access on Shriram Eco-system, viz.

Shriram Chits and Shriram Transport, which

provide a massive infrastructure, built over

time to ensure better financial productivity.

Large customer base of 3.55 million and

growing everyday.

Eminent Board and experienced management

team.

Listed on National Stock Exchange and

Bombay Stock Exchange with a market cap of

Rs. 25 Billion

Capital infusion by pedigree investors – ICICI

Ventures, Bessemer and Chrys Capital and

TPG

Large distribution network and AUM

Pan India presence through a network of over

1000 branches (includes 350 locations

offering only loan against gold)

Over 10000+ dedicated workforce

Total AUM of Rs. 71.29 billion as at Dec

2010

Company overview

Last twelve months share price performance

300

350

400

450

500

550

600

650

700

750

31-Mar-10 30-Jun-10 29-Sep-10 29-Dec-10 31-Mar-11

Shar

e p

rice

in R

up

ee

s(r

eb

ase

d to

SC

UF)

Shriram City Union SENSEX

CMP – Rs. 503 (31-Mar-11)Mcap – 2,491 crores

Corporate History

ShriramCitywas established

2005

1st preferential Allotment of equity shares to PE Investors @ Rs. 160/- per share

1986

Focus on Retail Financing

Listed on National Stock Exchange

2006

2nd preferential Allotment of equityshares to Private Equity Investors @ Rs.400/- per share. TPG invests in theholding Company

2008

2010

ShriramCity’s Net Worth touchesRs. 1000 Crore

2007

Launches – Small Business Loans

Launches Loan Against gold

2003 Listed on Bombay Stock Exchange

Vision platform

Our Mission “Striving to serve the largest number of common people”

Brand Promise “Trusted brand built over four decades”

Values Trustworthy

We are one of the

most trusted brands

in India

Responsive

We deliver

thoughtful, timely

and high quality

solutions to empower

common man

Creative

We continuously

improve the way

we work

Bold

We are not afraid

of venturing into

uncharted

territories

Competitive

Positioning

Delivery

Collaborating to combine

our group‟s network and

capabilities to provide

innovative & cost

effective solutions

Customers

We build long term

personal relationship with

our customers… Striving

to bring prosperity to their

lives

Discipline

Disciplined approach

towards wealth creation,

for all our stakeholders

balancing risk and rewards

Commitment to

stakeholders

Our people

Dedicated

workforce with an

extra ordinary

employee retention

Communities

Trusted and

caring.. Growth

through inclusion

Investors

Proven track

record, delivering

consistently

superior returns

Regulators

Demonstrating

exemplary ethical

and governance

standards

Strong Business Model

Retail and Small Business Loans financing Model

Small Business Loans Retail Loans

Personal LoansTwo wheeler

LoansAuto Loans

Localized

Presence

Field force drawn locally

Advantage of domain knowledge & personal knowledge of the customers

Quick Credit

Approvals

Centralized broad policy formulation; Decentralized decision making authority

Speedy approvals - superior turn around time in loan processing

Collection /

Recovery skills

Credit team responsible for monitoring early warning signals

Deal originators being responsible for the portfolio quality

No outsourcing

Focus Market 80% of the branch network focuses on rural and semi - urban areas

Pan India presence with an existing concentration in South India; expanding into other geographies

Origination & credit evaluation through own team

Loan against gold

With a strong financial track record

Total Income (Rs. Mns) Net profit (Rs. Mns)

Earnings Per Share Book value per share

10.9

16.5

22.025.8

41.2

0.0

10.0

20.0

30.0

40.0

50.0

2006 2007 2008 2009 2010

33

83104

155

203

0

50

100

150

200

250

2006 2007 2008 2009 2010EPS for 9M FY 2011 is Rs. 33.2 Book value per share as at Dec 2010 is Rs. 233

(Rs. Mns)

(Rs.) (Rs.)

FY 2006 FY 2007 FY 2008 FY 2009 FY 2010

2048 3490

6232

9339

11028

For the nine months ending Dec 2010 - Rs. 9197 Millions

FY 2006 FY 2007 FY 2008 FY 2009 FY 2010

317516

876

1,1701,943

As at Half year ending SeptFor the nine months ending Dec 2010 - Rs. 1634 Millions

Superior return on Networth

Net worth (Rs. Mns)

Return on Equity (%)

36.83%

23.97%

22.86%20.47%

22.72%

0.00%

10.00%

20.00%

30.00%

40.00%

2006 2007 2008 2009 2010

FY 2006 FY 2007 FY 2008 FY 2009 FY 2010

905

3257 4265

7097

10000

As at Dec 2010, Net Worth – Rs. 11538 Millions

Driven by Fast Growth in AUM with Low NPAs

AUM (Rs Mns)

NPA levels

3.66%

2.30%1.52%

2.07%2.27%

1.79%2.29%

1.47%

0.90%

0.96%0.71%

0.43%

0.00%

1.00%

2.00%

3.00%

4.00%

2006 2007 2008 2009 2010 Dec-10

FY 2006 FY 2007 FY 2008 FY 2009 FY 2010

12107

25069

33689

46295 52155

As at Dec 2010, AUM is at Rs 71285 Millions

Strengths of ShriramCity

Why ShriramCity

Diversified Product Portfolio

Seasoned Credit Policy & Process

Well developed & large infrastructure and Pan India Presence

Healthy Asset Quality & strong profitability

Best in Class – Corporate Governance

1

3

2

4

7

Strong management backed by eminent board 8

Has attracted Quality Investors5

Optimum borrowing mix6

Sound risk management systems9

1. Diversified Product Portfolio

A Balanced Mix of High Yield and Low Risk Portfolio

Split of AUM – Rs 71.29 billion

Loans to Small Business Units

Key financials (9M FY 2011)

Average Tenor: 36 Months

Average Yield: 22 – 24%

Disbursement: 9809 Mn

Retail Loans

Personal Loans

Key financials (9M FY 2011)

Average Tenor : 30 Months

Average Yield: 24 – 27%

Disbursement: 3832 Mn

Two Wheelers

Key financials (9M FY 2011)

Average Tenor: 24 Months

Average Yield: 24 – 26%

Disbursement: 9973 Mn

Auto Loans

Key financials (9M FY 2011)

Average Tenor : 30 months

Average Yield: 22 – 24%

Disbursement: 7873 Mns

29% 15% 10%

21%

Gold Loans

Key financials (9M FY 2011)

Average Tenor : 4 Months

Average Yield: 18- 20%

Disbursement: 22778 Mn

25%

Seasoning of Product Portfolio

Note: CAGR calculated on the disbursement in the month of launch and disbursement for the month of March 2010

Dec 2002Two

wheeler

Oct 2005Auto Loans

Dec 2005Small

Business Loans

Jan 2006Personal

Loans

Oct 2006Loan

Against Gold

CAGR 71%

CAGR 399%

CAGR 97%

CAGR 399%

CAGR 525%

Avg Tenor-

24 Months

Avg Tenor-

30 Months

Avg Tenor-

35 Months

Avg Tenor-

24 Months

Avg Tenor- 4 Months

Business concentration has been to Southern India, however now the Company is expanding into other geographies

The Company slowly introduces all its products after a thorough study of the location and demand for products

As a policy, every business location has to offer the entire range of the Company‟s product in due course

Around 200 business outlets are yet to introduce the complete range of products.

The Company plans to extend all the products to 650 outlets by March 2012.

2 Pan India Presence

Branch Network is Adequately Capturing Growth Corridors of the Country

Presence (1-10 branches)

Deep penetration (>50 branches)

18

4

650 branches

112

6

1

1

1

19

25

12

9 11

205

166

91

68

No Presence

Some presence (10-50 branches)

Points of Business of Company State wise GDP Growth FY05-09*State wise FY09 GDP contribution*

7.5%

Contributes: 1-2%

Contributes > 5%

Contributes: <1%

Contributes 2-5%

0.1%

1.6%3.1%

1.6%

0.4%

6.8%

3.3%

0.8%

0.7%

1.6%

5.4%

4.0%

13.3%

3.3%

0.1%0.2%

0.1%

2.5%

3.1%

4.3%0.1%

6.8%

0.3%

8.1%

0.8%

7.1%

0.1%

0.3%

3.5%

0.2%

9.3%

Growth: 4 - 6%

Growth: >9%

Growth: 0-4%

Growth: 6-9%

5.2%

12.2%

10.7%

11.8%

10.0%

8.4%

6.2%

9.7%

9.6%

5.5% 5.0%

9.4%

6.3%

9.0%

8.0%

5.2%

6.5%

7.4%

8.8%

11.5%

12.9%

19.0%

6.7%

7.9%

5.4%

5.6%

8.4%

10.9%

7.8%

*Source: MOSPI; GDP split and growth at constant prices 1999-2000

3 Seasoned Credit Policy & Process

Credit team responsible for monitoring early warning signals

Proprietary integrated ERP – Linking business from the origination point to the final accounts

Average LTV lower/ equal to the industry average

Immovable assets & personal guarantees as collateral for personal & small business loans

Centralized broad policy formulation

Decentralized decision making authority

Speedy approvals -superior turn around time in loan processing

Pre lending Field Investigation (FI) & the post lending appraisal by dedicated teams

Origination & credit evaluation through own team

Deal originators being responsible for the portfolio quality

Systematized Controls Loan to

Value (LTV)

Quick Credit Approvals

FI & Post Lending Verification

“No Outsourcing

” Policy

Credit policy & process

Assigning Responsibility

4 Healthy Asset Quality

Enables decentralized decision making

Ensures quick turn around time

Systematized controls

Well defined incentive plan for field

officers to ensure low default rates

50% of the compensation is by way of

performance based incentives.

3.66%

2.30%1.52%

2.07%2.27%

1.79%2.29%

1.47%

0.90%

0.96%0.71%

0.43%

2006 2007 2008 2009 2010 Dec-10

38%

37%

41%

54%

69% 74%

2006 2007 2008 2009 2010 Dec-10

Deal originators being responsible for

monitoring early warning signals

Customized repayment structures

Localized presence – field force being

drawn locally.

Prudent Credit norms

Reasons for Low Delinquency

Incentive Schemes

Asset Quality

Asset Coverage Ratio

…and Strong Profitability

Spread Analysis FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 Dec-10

Interest from Financing Operations /

Average AUM 18.0% 18.0% 20.8% 23.1% 21.8% 20.11%

Interest Expenses / Average AUM 8.9% 7.1% 8.5% 10.8% 9.4% 7.78%

Gross Spread 9.1% 10.9% 12.3% 12.3% 12.4% 12.33%

OPEX / Average AUM 4.0% 6.1% 6.6% 6.2% 4.8% 5.31%

Provisions & Write offs **/ Average

AUM 1.5% 1.3% 1.7% 1.9% 2.4% 1.99%

Net Spread 3.6% 3.5% 3.9% 4.2% 5.2% 5.03%

** Provisions include the standard assets provisioning @ 0.25%

4

…Has attracted Strong Interest from Quality Investors

Directly & Indirectly PE Investors hold 64% in ShriramCity

Key Shareholder*

Shareholding

(millions) % of o/s

Shriram Enterprise Holdings* 17.92 36.2

Shriram Retail Holdings* 8.56 17.3

Van Gogh Ltd (Chrys Capital) 6.63 13.4

Norwest Venture Partners 4.34 8.8

IDBI Trusteeship (ICICI Ventures) 3.70 7.5

Bessemer Venture Partners 2.50 5.1

Acacia Partners LP 1.56 3.1

Asiabridge Fund LLC 1.18 2.4

Acacia Institutional 0.54 1.1

Others 2.54 5.2

Total 49.46 100.0

Consistent track record and high

growth potential has attracted reputed

institutional and Private Equity

investors to infuse growth capital

Details of Shares capital issues

Asia Bridge - Invested in May „08 @ Rs. 400/- per share [0.58 mn shares]

Bessemer Venture partners - Invested in May „08 @ Rs. 400/- per share [1.25 mn shares]

Chrys Capital - Dec ‟06 @ Rs.160/-and May „08 @ Rs. 400/- per share. [6.625 mn shares in total]

ICICI Ventures - Invested in May „08 –Rs. 400/- per share [0.75 mn shares]

Norwest Venture Partners - July „09 –Secondary Market Purchase

Capital Adequacy ratio as of December

31, 2010: 21.01%

* TPG has stake in Shriram Enterprise Holdings and Shriram Retail Holdings

5

Optimum borrowing mix

Segment wise Borrowings as at 31st Dec 2010

Segment FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 Dec-10

Total Borrowings (Rs. Mns) 8652 15224 29992 43228 46671 54180

Retail Borrowings 81.1% 54.4% 32.4% 33.0% 40.1% 34%

Institutional Borrowings 18.9% 45.6% 64.9% 60.8% 55.6% 55%

Market Borrowings - - 2.7% 6.2% 4.3% 11%

Retail NCD25%

Retail Sub Debts9%Utilised Cash Credit

Limits25%

Term Loans30%

Institutional NCD7%

Commercial Papers4%

Retail Liability

Long Term Rating of “AA- “ by Fitch, Care & Crisil.

Highest rating in Short term by all three rating agencies

*Unutilized Cash Credit limits as at Dec 2010 were Rs. 10730 Millions

6

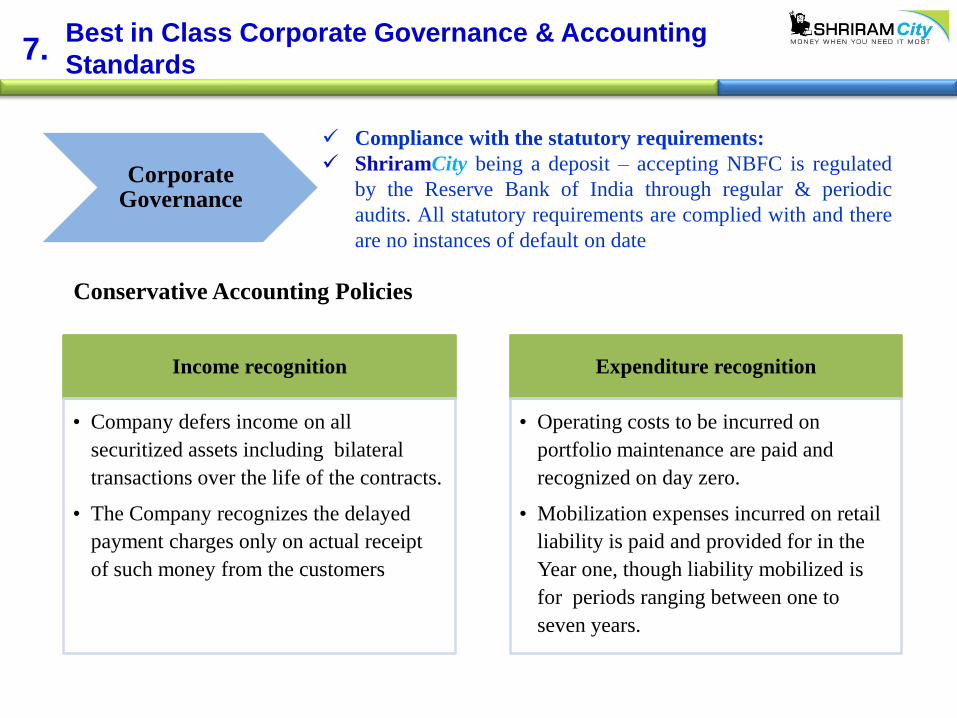

7.Best in Class Corporate Governance & Accounting

Standards

Compliance with the statutory requirements:

ShriramCity being a deposit – accepting NBFC is regulated

by the Reserve Bank of India through regular & periodic

audits. All statutory requirements are complied with and there

are no instances of default on date

Income recognition

• Company defers income on all

securitized assets including bilateral

transactions over the life of the contracts.

• The Company recognizes the delayed

payment charges only on actual receipt

of such money from the customers

Expenditure recognition

• Operating costs to be incurred on

portfolio maintenance are paid and

recognized on day zero.

• Mobilization expenses incurred on retail

liability is paid and provided for in the

Year one, though liability mobilized is

for periods ranging between one to

seven years.

Corporate Governance

Conservative Accounting Policies

Each product is an exclusive vertical, headed by a product head

strong management team8

Chief Operating

Officer-

Mr. Y. S. Chakravarti

Managing Director

Mr. R. Kannan

Board of Directors

Chief Technical &

Accounts Officer-

Mr. R. Chandrasekhar

Chief Financial

Officer-

Ms. Subhasri Sriram

Product

managementCredit

Legal Recovery

Enterprise

finance

Accounts

Information

Technology

& innovation

Talent Engagement

& Development

Finance

Strategic Planning

& Risk

Management

Back OfficeCustomer

Care

Audit

Management

Information

System

Administration

…Backed by Eminent board…

Board of Directors

Mr. Arun Duggal Chairman

• Former MD & CEO, Bank of America (India)

• Former CFO, HCL Technologies

Mr. R. KannanManaging Director

• Around 3 decades of experience in Shriram

• Former ED, Shriram Chits

Mr. S. VenkatakrishnanDirector

• Retired senior bureaucrat from Civil Services. He has served in senior finance, audit & accounts posts in the Government and Public sector undertakings

• Has been strategic advisor to the group for over a decade

Mr. G.S. Sundararajan

Director

• Current MD of Shriram Capital

• Former CEO & MD Fullerton India Credit Company

• Former MD and head of Citibank's SME and asset based finance business in India

Mr. Puneet BhatiaDirector

• Managing Director and Country Head - India for TPG Asia

• Served as Chief Executive, Private Equity Group for GE Capital India (“GE Capital”)

Mr. Ranvir DewanDirector

• Head of Financial Institutions Group Operations- TPG Capital

• Served as Executive Vice President and Chief Financial Officer of Standard Chartered First Bank (formerly Korea First Bank) in Seoul, Korea.

8

Board of Directors – Independent Directors

Mr. Vipen KapurDirector

• Has held senior positions at multiple banks and corporate houses across the world

• Has been associated with Grindlays, Bank of America, JP Morgan and Al Rushaid

Mr. Sunil VermaDirector

• Extensive consulting experience spanning over 30 years with Price Waterhouse Management Consultants and the IBM Consulting Group

Mr. S. KrishnamurthiDirector

• Former Senior banker with RBI

• Former Chairman & CEO – Tamilnad Mercantile Bank

• Former General Manager (Vigilance & Inspection/Audit) with Indian Overseas Bank

Mr. Mukund Govind DiwanDirector

• Former Chairman of Life Insurance Corporation (LIC) of India

• Experience in carrying out management and actuarial consultant assignments

Mr. K.R.RamamoorthyDirector

• Senior banker, with over 40 years of commercial and banking experience in India.

• Served as CMD of Corporation Bank and CEO of ING Vysya

Mrs. Lakshmi PraneeshDirector

• Former Chief Secretary to the Government of Tamil Nadu

• Has served as ex-officio Chairman of the Tamil Nadu Civil Supplies Corporation, Overseas Manpower Corporation, Women's Economic Development Corporation

…Backed by Eminent board…8

Type of Risk ShriramCity Model

Concentration Risk Multiple products ensure risk diversification.

optimum mix of retail & institutional borrowings

Interest Rate Risk Balanced mix of fixed / floating rate loans.

Loan assets are at Fixed rates and the borrowings are an equal mix of fixed

and floaters

The entire retail liability constituting 34% of the total borrowings, are all at

fixed rates with the average balance maturity of approx. 30 months.

Liquidity Risk Adequate liquidity back up in the form of unutilized working capital limits,

fixed deposits with banks.

Unutilized Cash Credit limits and balances in bank accounts as at 31st Dec

2010, was at Rs. 14102 Millions

ALM Risk Positive cumulative mismatch in all the buckets – assets being of short tenors

(18 – 24 months) and borrowings of longer tenors (24 – 36 months)

Sound Risk management Systems9

Competitive Positioning

Competitive positioning

Company

Consumer

Durables Car 2 wheeler 3 wheeler

Commercial

Vehicles* Personal

SME/

Business Gold

Housing /

property*

Shriram City

Bajaj

Sundaram

Future Cap

Manappuram

Muthoot

Chola

TATA CAPITAL

Magma

ShriramCity offers most diverse and complete product offerings among

major Retail NBFCs in India…

Product / service offered by the Company

* Finances commercial vehicles with a vintage of more than 12 years. Housing finance to be launched soon

Shriram Group Eco-system

Legacy of Shriram Group

“Helping Create Wealth. Empowering people through prosperity.

Resulting in inclusive growth”

Shiram Group has a four decade legacy of

creating business which have strived for

the empowerment of common man

The relentless pursuit of this mission has

given the group its distinct identity

The Group‟s reputation for effectiveness,

transparency and integrity has helped it to

become one of India‟s largest Financial

Services Network.

Currently the Group manages assets

exceeding Rs.400 billion, has 6.5 million

clients, served by 1,00,000 Agents and

36,000 employees, through 2700 Branches

across India.

Our commitment to inclusive growth:

Shriram Chits is the largest Chit fund

entity in India

Shriram Transport Finance Co. (STFC) is

the largest & only organized player in

financing pre-owned and small truck

owners, with a market share of 20-25%

STFC, which is the flagship company of

the group has delivered superior returns

to investors with a net profit CAGR of

58% since 2006

Future Growth

Strategy for Future Growth

Product Expansion across Branches

Increase reach

Franchising through network of

group Companies –

especially for Loan against Gold

Focus on Small Business Loans-

In particular to the “Under Banked Community”

in MSME sector

Product Expansion – Small Business Loans

Financial inclusion has become a national and a government imperative in the last few years..

Many believe that fastest and most efficient way to ensure economic development of financially

excluded is by improving the bankability and thereby competitiveness of Micro, Small & Medium

Businesses (MSMEs)

MSMEs – Some statistics

Constituting around 26 million units

Contributes to 45% of industrial output

40% of exports are fromMSMEs

Employs 60 million people

Creates 1.3 million jobs every year

Currently 21% of SCUF’s loan portfolio is

towards MSME loans

Lending is largely addressed by unorganized

sector

Expertise of Shriram Group

Localized presence - loans are to be processed

and delivered at the customers doorsteps

Ability to understand the customer’s business

model and provide tailor made loans

Lending to this segment, cannot be based

purely on collaterals - this is where

ShriramCity scores over competition

Shriram Chits has years of expertise in this

segment. We have an extensive borrower

database of Shriram Chits – which is

combined with our own borrower database

Gives us an edge over competition in assessing

customers’ requirements and ability to repay

the loan

Product Expansion – Gold Loans

Gold-backed lending to households presents a good opportunity, given the safety of gold as

collateral and high levels of accumulated gold stock among Indian households…

South India is the largest market for Gold

ShriramCity is better positioned compared to large banks in the gold loan segment:

Source: Broker research, IMACS Report on Gold Loans Market in India 2009 and Updated Report on Gold Loans Market In India 2010

0

100

200

300

400

500

600

FY 02 FY 07 FY 09 FY 10 FY 11

Rs.bn

Size of Gold Loans Market in India

Targeting Non – bankable Customers

Perhaps the only product where customers

assess lender‟s brand equity and goodwill

Minimum documentation formalities

Better operating structures compared to banks

Brand name and trust of Shriram Brand

Ability to use the existing infrastructure of

group companies

Average yield on gold loans of SCUF is 18-

20%, which is much higher than average

yields enjoyed by banks (10-12%)

Disclaimer

This presentation is for information purposes only and does not constitute an offer, solicitation or advertisement with respect tothe purchase or sale of any security of Shriram City Union Finance Limited (the “Company”) and no part of it shall form the basisof or be relied upon in connection with any contract or commitment whatsoever. No offering of securities of the Company will bemade except by means of a statutory offering document containing detailed information about the Company.

This presentation is not a complete description of the Company. Certain statements in the presentation contain words or phrasesthat are forward looking statements. All forward-looking statements are subject to risks, uncertainties and assumptions that couldcause actual results to differ materially from those contemplated by the relevant forward looking statement. Any opinion,estimate or projection herein constitutes a judgment as of the date of this presentation, and there can be no assurance thatfuture results or events will be consistent with any such opinion, estimate or projection. The information in this presentation issubject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed and it may not contain allmaterial information concerning the Company. We do not have any obligation to, and do not intend to, update or otherwise reviseany statements reflecting circumstances arising after the date of this presentation or to reflect the occurrence of underlyingevents, even if the underlying assumptions do not come to fruition.

All information contained in this presentation has been prepared solely by the Company. No information contained herein hasbeen independently verified by anyone else. No representation or warranty (express or implied) of any nature is made nor is anyresponsibility or liability of any kind accepted with respect to the truthfulness, completeness or accuracy of any information,projection, representation or warranty (expressed or implied) or omissions in this presentation. Neither the Company nor anyoneelse accepts any liability whatsoever for any loss, howsoever, arising from any use or reliance on this presentation or its contentsor otherwise arising in connection therewith. This presentation may not be used, reproduced, copied, distributed, shared, ordisseminated in any other manner. The distribution of this document in certain jurisdictions may be restricted by law and personsinto whose possession this presentation comes should inform themselves about, and observe, any such restrictions.