Embed Size (px)

Citation preview

Show Me the Keys: Tax Levy Settingpresented by Jim Smith

Information adapted fromBoone County Assessor’s web site

and presentations by Nathan Nickolaus,

City Counselor, Jefferson City;Joshua Payton with Cunningham,

Vogel & Rost, P.C.; and Mark Grimm, Gilmore and Bell

Goal

The goal of this presentation is to discuss the property tax calculation, the tax rate setting process, impact of the Hancock Amendment, impact of Senate Bill 711, and to touch on other legislation that can impact assessed valuation.

DBRL Operating Revenue 2008

$7,919,878 , 92%

$139,897 , 2%$361,606 , 4% $129,766 , 1%

$89,022 , 1%

DBRL Operating Revenue

Property Tax

State Aid

Investment Income

Contributions

Other

Presentation

• PART 1: Overview of the Property Tax Calculation

• PART 2: Overview of Property Tax Rate Setting and Impact of Legislation such as Hancock Amendment and Senate Bill 711

• PART 3: Overview of Legislation that can Impact Property Tax Valuation

PART 1: Property Tax Calculation

ASSESSMENT

County Assessor Calculates Market Value

“Actual Value” is Market Value:

What an ordinary willing buyer would pay an ordinary willing seller

Market Value to Assessed Value

Multiply the actual value by apercentage based on the type ofproperty

The Percentages Are

• Residential: 19% of value• Agricultural: 12% of value• Commercial & Other: 32% of value• Manufactured Homes: 19% of value• Farm Machinery 12%: of value• Historic Cars, Planes: 5% of value• Crops (grain): 0.5% of value• Other Vehicles: 33.3% of value

County Collector Applies the Tax Rate

• ($ Actual Value X Assessment % / 100) X Tax Rate %

• You divide the assessed value by 100, since the rate is per $100 of Assessed Valuation

• You multiply the result by the tax rate approved by the voters

Example

Thus if the tax rate levy is 10¢, and a house isworth $100,000, the calculation wouldbe:• $100,000 (market value) x 19% =

$19,000 (assessed value)• $19,000 ÷100 = $190• $190 x 0.10 (levy rate) = $19 (the tax

due)

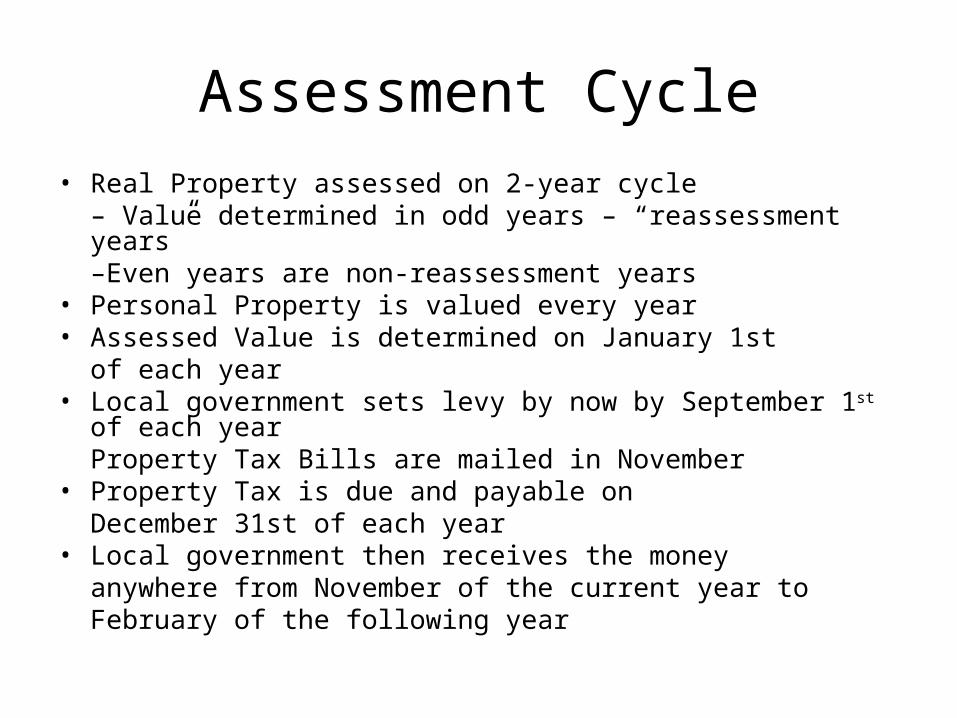

Assessment Cycle• Real Property assessed on 2-year cycle

– Value determined in odd years – “reassessment years”–Even years are non-reassessment years

• Personal Property is valued every year• Assessed Value is determined on January 1st

of each year• Local government sets levy by now by September 1st of each year

Property Tax Bills are mailed in November• Property Tax is due and payable on

December 31st of each year• Local government then receives the money

anywhere from November of the current year to February of the following year

Other Considerations

Exempt Property– Some Personal Property– Some Real Estate

• Government property• Property used as nonprofit cemeteries• Property used exclusively for religious worship, schools

and college• Property for purely charitable purposes

PART 2: Rate Setting

Rate Setting

Overview:– Each political subdivision must set its

own levy rates (§ 67.110.1 RSMo)– Formula: Levy Rate ×Assessed Value/100 =

Tax Amount Owed

Procedures for Rate Setting• Missouri State Auditor’s Office (SAO) requests information

to be sent to the County Clerk’s Office• County Clerks provide assessed valuation and other

information to the SAO to prepare the tax rate calculation for each political subdivision (137.245.3 RSMo)

• Library staff uses the information from the County Clerk and SAO to provide the board with all information necessary as required by 67.110.1 RSMo.

• Library staff prepares a proper notice to the public about the public hearing for setting the tax rate (137.055.2 RSMo)

• Once each individual board approves the tax rate, the SAO form is filled out and filed with the County Clerk.

Hancock Amendment

Who?– Businessman fromSpringfield, MissouriWhat?– Constitutionalamendments (Art. X §§ 16-24) that limit state andlocal government taxesWhen?– November 4, 1980 – voterapproved initiative

Hancock Amendment• Requires voter approval for new or increase in existing

taxes above previously voter approved rate• Reduces tax rate levy when tax base expands or allows

increases to tax rate levy when tax base declines (but not above the voted tax rate limit)

• Rollbacks (tax rate adjustments) to voter approved rates occur when assessed value of property increases to above the previous year’s tax revenue collections (total tax revenue) plus the lesser of CPI or actual growth (a.k.a. “Hancock Ceiling”)

• Impacts only the Operating Levy.

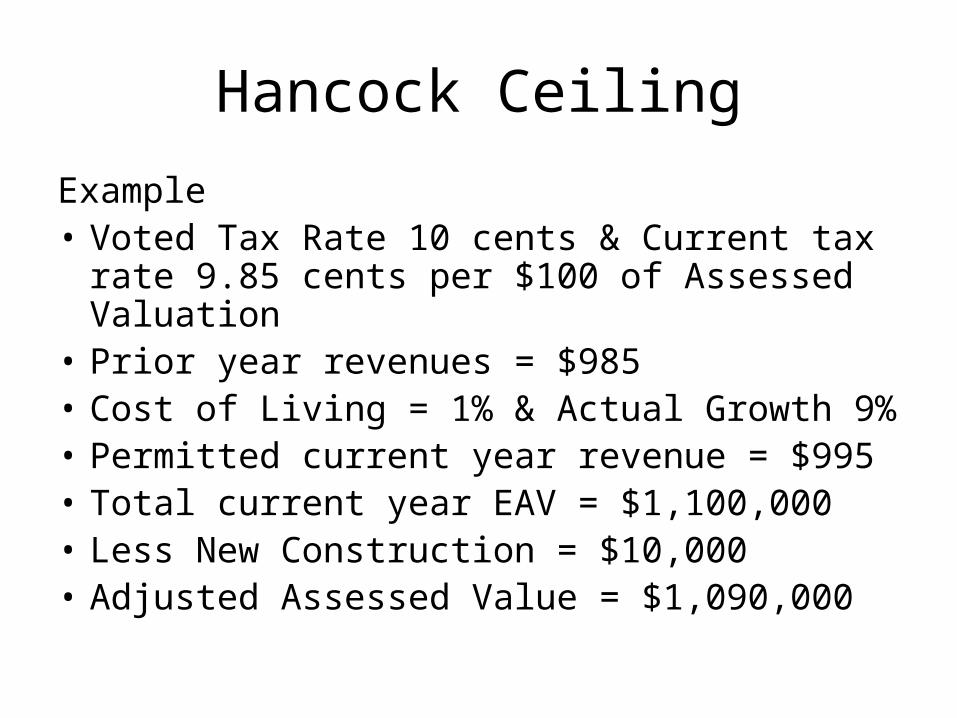

Hancock Ceiling

Example• Voted Tax Rate 10 cents & Current tax rate 9.85

cents per $100 of Assessed Valuation• Prior year revenues = $985• Cost of Living = 1% & Actual Growth 9%• Permitted current year revenue = $995• Total current year EAV = $1,100,000• Less New Construction = $10,000• Adjusted Assessed Value = $1,090,000

Hancock Ceiling

Formula:– Permitted Current Year Revenues ÷ Adjusted

Assessed Valuation = Maximum AuthorizedLevy

$995 ÷ ($1,090,000/100) = $0.0913$.0913 × $1,100,000/100 =$1,004 (Actual Tax Revenue) This

results in a required rollback to new rate.If the EAV was changed to $900,000, their would be no growth

and the maximum rate would be $0.1000, the tax rate ceiling

Senate Bill 711

• Changes Rate Setting Procedures• The purpose of SB 711 is to target increased

taxes resulting from rising assessed values.

SB 711

Summary of Changes• Creation of Second “Gibbons” Ceiling• New methodology for calculating voter

approved levy rate increases

SB 711Second “Gibbons” Ceiling-When does Gibbons Ceiling apply?– When political subdivisions levy a tax rate voluntarily

below Hancock Ceiling in even year (non-reassessment), then

– In odd-numbered year (reassessment) the new Gibbons Ceiling applies

– Why?– Limits tax revenues to previous year plus cost of living

Increase– Targets increases in tax revenues due solely to rising

assessed values

SB 711Second “Gibbons” Ceiling• Potential Long-Term Affect– Never achieve Hancock Ceiling

• Can “bust” through Gibbons Ceiling– When?

In even-numbered years– How?

Hold a Public HearingGoverning body passes ordinance/resolution/policy

statement justifying increaseNO vote of qualified voters required

Property Tax Elections

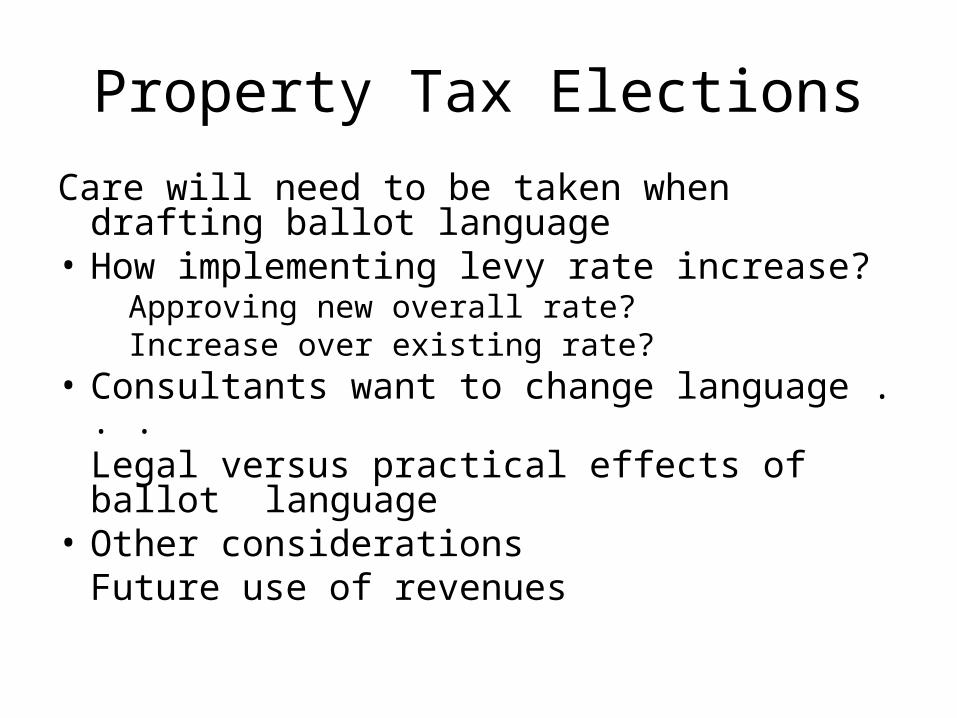

Care will need to be taken when drafting ballot language

• How implementing levy rate increase?Approving new overall rate?Increase over existing rate?

• Consultants want to change language . . .Legal versus practical effects of ballot

language• Other considerations

Future use of revenues

Delinquent Taxes and Appeals

• Property Tax is due and payable on December 31st of each year.

• Tax becomes delinquent January 1st • Liens are created for Real Estate Tax• Personal Property Taxes are collected by civil suitThree Steps to contesting an assessment• Informal adjustment• Board of Equalization• Appeal to Tax Commission

(From here can go to court)

PART 3: Other Legislation

• Economic Development Methods Impacting Library– Tax Increment Financing (TIF)– Chapter 100 Property Tax AbatementOthers Methods Available – MODESA– MODESA “Light”– Chapter 353 Urban Redevelopment Corporations

Tax Increment Financing (TIF)

• Creates a special district to make public improvements to generate private sector development

• Tax base is frozen and any new development is used to pay project costs

• Tax freeze lasts for a defined period of time no more than 23 years

• Done to stimulate areas that would not grow without action

Chapter 100

• Gives cities, counties and other governments authority to issue revenue bonds to companies wishing to move into or expand in the area

• Company buys the bonds, gives title to the government and leases the property

• Property is exempt from taxation and company makes payment in lieu of taxes (PILT)

Property Tax

Questions and Answers