Embed Size (px)

Citation preview

Should I Trust You? Earnings Quality as a Signal in Earnout Agreements

Authors:

Annalisa Prencipe Department of Accounting

Università Bocconi [email protected]

Luca Viarengo* Department of Accounting

Università Bocconi [email protected]

This draft: March 2016 Preliminary, please do not quote

Comments Welcome

*Corresponding Author

2

Should I Trust You? Earnings Quality as a Signal in Earnout Agreements

Abstract

This paper aims to test whether past earnings quality of the acquirer serves as a signal of its

trustworthiness in view of the inclusion of an earnout agreement in an acquisition contract. Earnouts

are contractual agreements that link part of the payment of an acquisition to the future performance

of the acquired company. In the US, above 12% of the corporate acquisitions over the period 2002-

2014 include earnout agreements, and this percentage raises to over 20% in some industries.

Typically, earnouts are contractual solutions aimed at bridging valuation disagreement between the

potential acquirer and the seller of the target firm. Prior studies have highlighted earnouts’

usefulness in reducing adverse selection problems and the acquirer’s valuation risk in M&A

transactions. However, from the seller’s perspective, such agreements are subject to moral hazard

issues as the acquirer may not exert effort to achieve pre-determined benchmarks, as originally

contracted. Moreover, many earnouts are based on accounting performance measures, which may

be affected by accounting measurement issues. Consequently, earnouts agreements are often settled

in courts of law.

To reduce the probability of a litigation process, the uncertainty and costs associated with it, we

expect the sellers to explore and investigate the quality type of the acquirer, in particular of its

trustworthiness, prior to entering into an earnout agreement. A possible indicator of trustworthiness

is the acquirer’s past earnings quality. Based on a sample of 9,178 acquisition deals completed in

the US between 2002 and 2014, we find that the acquirer’s past earnings management is negatively

associated to the probability of inclusion of an earnout in acquisition contracts.

Keywords: Earnouts, acquisitions, earnings quality, earnings management.

3

1. Introduction

An earnout is a contractual agreement that links part of an acquisition price to the future

performance of the acquired company. Earnouts are fairly common in acquisition deals. In the US,

over 12% of the corporate acquisitions, during the period 2002-2014, include earnout agreements.

Earnout deals are also significant in terms of nominal value. Over the same period, the annual

average value of earnout deals is close to 3 billion dollars, compared to the annual average of non-

earnout deals of 32.6 billion dollars.

Earnouts aim at bridging a valuation gap between the acquirer and the sellers, thus making the deal

possible. When the negotiating parties are unable to reach an agreement on the value of the target

company, earnouts contracts facilitate the closing of the deal by linking part of the acquisition price

to the certain milestones, such as hitting target levels of performance of the acquired company.

Earnouts are advantageous for acquirers as they allow risk sharing and reduce information

asymmetry that typically affects acquisitions. In other words, earnouts allow to share the valuation

risk between acquirer and sellers, and act as a mechanism of partial verification of the quality of the

target company, as the sellers are willing to accept a deferred payment contingent on the

performance of their firm only if they believe that the agreed-upon benchmarks, which trigger the

additional payment, will be met.

Earnouts are valuable also to the sellers, as they reduce the adverse selection risk for the target firm,

thus allowing to negotiate a higher consideration. However, this benefit is costly, because, after the

closing of the deal, the sellers bear not only the risk that the acquired company will not meet the

pre-specified earnout requirements, but also the risk that the acquirer will behave opportunistically

in the attempt to reduce, or avoid, the contingent payment. Such opportunism can be implemented

by either ‘managing’ the (reported and/or real) accounting results, or by reducing effort made to

reach the target’s benchmarks.

The sellers of the target firm may be aware of the risk of opportunistic behavior by the acquirer,

thereby introducing stringent rules on how to measure performance benchmarks. Such measurement

4

rules are applied in the attempts to reduce possible costly litigations. Nonetheless, legal disputes on

the actual realization of the performance levels stated by the earnout are frequent1. Trevis Laster, a

judge who had to decide on a dispute related to an earnout payment, once said "an earnout often

converts today's disagreement over price into tomorrow's litigation over outcome"2. A survey

conducted by the law firm Morrison & Foerster LLP (2012) on a sample of acquisitions in the high-

tech sector – an industry where earnouts are used the most3 – with over 300 respondents reports that

almost three-quarters of those who have used earnouts claimed that such clauses led to subsequent

disputes or litigation, and nearly one-fifth of respondents estimated there had been post-deal

conflicts over earnouts up to half of the times. In fact, practitioners warn M&A dealers to carefully

define the accounting measures or entries to be included or excluded from the computation of the

earnout4. Recent anecdotal evidence helps clarifying this issue5. In 2007 3M acquired Acolyte

Biomedica, a pharmaceutical company owned by Porton Capital, for an upfront payment of £10.4m

and an earnout of £41m, contingent on net sales targets. In 2011, 3M was sued in the UK Court of

Law by Porton Capital. The former owners of Acolyte Biomedica requested the Courts to rule for

a higher earnout payment than that offered by 3M, accusing 3M for applying a highly

“conservative” recognition approach for recording net sales.6

Apparently, once the earnout acquisition deal is agreed and ownership has passed to the acquirer,

only the target’s former owners face transaction risk. That risk is associated with the acquirer

incentive to either shirk and/or employ tactics to reduce the earnout payment. The target firm is

1 Some examples of earnout disputes ended up in litigation are Comet Systems Inc Shareholders’ Agent v. MIVA Inc, 980 A.2d 1024 (Del. Ch. 2008); Chambers v. Genesee & Wyoming Inc, 2005 WL 2000765 (Del. Ch. Aug. 11, 2005); William J. LaPoint v. AmerisourceBergen Corp, 2007 WL 2565709 (Del. Ch. Sept. 4, 2007), aff’d, 956 A.2d 642 (Del. 2008). 2 Airborne Health, Inc. and Weil, Gotshal & Manges LLP v. Squid Soap, LP, C.A. No. 4410-VCL (Del. Ch. Nov. 23, 2009). 3 Datar, Frankel and Wolfson (2001) report that earnout in the high tech sector are more than one third of the total. 4 See, for example, Fox and Wolf (2010), Crimmins, Gray, Waller, Brown (2010) or Shannon and Reilly (2011). 5 Porton Capital Technology Funds & Ors v 3M UK Holdings Ltd & Anor [2011] EWHC 2895 (Comm), 07 November 2011. 6 The trial, however, ended largely in favor of 3M.

5

likely to be aware of the asymmetric risk inherited with that transaction.7

Following this line of reasoning, we hypothesize that the decision to include an earnout agreement

in an acquisition contract is positively (negatively) related to the acquirer’s past earnings quality

(earnings management).

Therefore, we expect

that, during negotiations, both sides to the negotiations attempt to study the counterparty’s quality,

including its reliability, honesty, and trustworthiness, part of which depends on that party’s past

‘behavior’. One possible signal of reliability and honesty is the firms’ financial reporting practices.

Put differently, the sellers may gain additional insights into the degree of honesty by observing the

acquirer’s financial reporting quality in terms of earnings management, serving as an indication of

trustworthiness. Following Healy and Whalen (1999) definition, earnings management occurs when

managers use judgment in financial reporting and in structuring transactions to alter financial

reports to either mislead some stakeholders about the underlying economic performance of the

company or to influence contractual outcomes that depend on reported accounting numbers. Target

owners may assume that, if the acquirer has the tendency to act opportunistically through earnings

management to affect contractual outcomes, it is likely that it will act opportunistically also after

the acquisition to deceive the target’s owners. Therefore, sellers’ decision whether to accept an

earnout agreement may depend on their perceived probability that the acquirer will use

opportunistic tactics to avoid the contingent payment. The extent to which the acquirer manages

earnings in the past may be used as a signal of such probability, i.e. the greater the earnings

management, the higher the probability of future opportunistic behavior by the acquirer.

We test this hypothesis on a sample of 9,178 deals completed in the US over the period 2002-2014.

In order to capture the quality of earnings of the bidder, we rely on an earnings management proxy,

7 In Appendix A we provide an example of an earnout agreement (Source: https://www.sec.gov/Archives/edgar/data/56978/000119312508162770/dex103.htm).

6

computed using a version of the modified Jones’ model (Dechow, Sloan and Sweeney, 1995). A

lower earnings management proxy indicates a higher level of earnings quality, and therefore a

higher acquirer’s trustworthiness.

While controlling for earnouts’ determinants as reported by prior studies, we provide statistical

evidence of a significantly negative association between the acquirer’s past earnings management

and the likelihood of inclusion of an earnout in an acquisition deal. Overall, our results validate the

hypothesis that the acquirer’s past earnings quality is used as a signal by the seller to evaluate the

former’s reliability.

Our paper contributes to the literature on earnouts by showing that the acquirer’s reporting quality

is used as a signal of the acquirer’s trustworthiness and is a significant determinant of the decision

by the seller to accept such contractual agreements. Our paper contributes also to the literature on

the relation between M&As and earnings management, that so far has mainly been focused on the

managerial incentives to manage earnings around the acquisition time to enhance the results of the

negotiation. As far as we know, our study is the first to show that past earnings quality of the

counterparty is a relevant determinant of the structure of acquisition contracts.

The remainder of the paper is organized as follows. The next section provides a review of the

relevant literature on earnouts and earnings management. In Section 3 we develop our hypothesis,

and in Section 4 we describe the sample and data used in the empirical analysis. In Section 5 we

describe our model, while in Section 6 we report our empirical results. In Section 7 we discuss

some robustness tests. Section 8 concludes.

7

2. Literature review

2.1 Earnouts

Compared to other areas in the disciplines of finance and accounting, research on earnouts is fairly

recent. The seminal papers on the topic focus on the role of earnout contracts as mechanisms to

reduce information asymmetry. Kohers and Ang (2000) analyze acquisitions of US companies over

the period 1984-1996. They report that earnouts are mainly used in acquisitions of private

companies and subsidiaries – due to the absence of a market price which increases the uncertainties

on the value of the target – and in acquisitions of companies operating in the service or high-tech

sectors, characterized by higher uncertainty due to issues related to market demand for the target

company products, human capital and growth opportunities. They also suggest that the likelihood of

using earnout contracts is increasing in the size of the target, while it is decreasing in the size of the

acquirer, and that the likelihood increases when the target firm operates in a different industry than

the acquirer’s. A later study by Datar, Frankel and Wolfson (2001) reaffirm Kohers and Ang’s

results, using international acquisitions over the period 1990-1996.

More recently, Ragozzino and Reuer (2009) analyze acquisitions of private target firms, pointing

out that earnouts are used more frequently when the target is young, and when it operates in an

industry that requires different expertise than that of the acquirer. Barbopulos and Sudarsanam

(2012) focus on UK acquisitions, suggesting that when earnouts are optimally applied to reduce

information asymmetry the acquirer experiences higher market returns compared to non-earnout

transactions. Similar results are found by Kohers and Ang (2000). Using a sample of US deals over

the period 1994-2003, Cain, Denis and Denis (2011) show that the performance parameters used in

earnouts agreement are chosen in order to discover the actual value of the target firm. Cain et al.

also suggest that the time period over which the earnout-related performance benchmark is

measured tends to increase with the relevance of R&D costs and to decrease with the return

volatility in the target’s industry.

8

However, research on accounting or reporting issues related to earnouts is fairly limited. Allee and

Wangerin (2013) study the impact of changes in accounting regulation on the use of earnouts. More

specifically, they analyze the effects of the revised US accounting standards on business

combinations (i.e. FASB ASC 805, formerly SFAS 141(R)), which modified the accounting

recognition and valuation of contingent payments. While there was no obligation to recognize

earnouts in financial statements prior to the revision, as of the fiscal year beginning after December

15, 2008, it is mandatory to value contingent payments at their fair value, and to evaluate these

contingent payments each year until their expiration. Consistent with a financial reporting cost

hypothesis, Allee and Wangerin (2013) report less frequent use of earnouts after the adoption of the

new standard. However, the presence of a high-quality auditor tends to decrease such an effect.

Based on a sample of deals carried out over the period July 1, 2006 – June 30, 2011, Cadman,

Carrizosa, and Faurel (2014) arrive at different conclusions, showing that the percentage of deals

including earnouts did not change significantly after the new standard adoption.

2.2 Earnings management in M&As

Although literature on earnings quality and earnings management is vast, evidence on the relation

between M&A transactions and earnings management is rather limited. Using a sample of stock-

for-stock deals completed between 1985 and 1990, Erickson and Wang (1999) suggest that earnings

are managed upward by acquirers in the quarters preceding the deal, and it is proportional to the

economic benefit for the acquirer, as captured by the relative size of the deal compared to the value

of the acquirer’s capitalization. The rationale behind this type of earnings management is that

acquirers attempt to increase their stock price, thus reducing the relative cost of acquiring the target.

Studying UK acquisition deals, Botsari and Meeks (2008) report similar results. Based on a US

sample of acquisitions during 1992 - 2000, Louis (2004) reports that the effect of pre-acquisition

earnings management on the acquirer’s stock prices is reversed after closing the deal. Indeed, the

9

study reports a negative correlation between the level of earnings management and both short and

the long term post-acquisition returns to the acquirer. Jensen (2005) contends that overvalued firms

tend to inflate earnings and to undertake stock acquisitions to create the illusion of growth to satisfy

market expectations. However, Ball and Shivakumar (2008) claim that, because large corporate

events are characterized by higher than usual litigation and regulatory risk from inflating earnings,

managers should be dissuaded from manipulating their reported earnings around these events.

Gong, Louis and Sun (2008) reports that pre-merger abnormal accruals are a strong determinant of

post-merger lawsuits. The effect of abnormal accruals is significant even after controlling for the

post-merger abnormal return, which suggests that pre-merger earnings management has a first-order

effect on the likelihood of a lawsuit.

To the best of our knowledge, there are no prior studies that examine the acquirer’s earnings

management as an ex-ante signal of its reliability and at its consequences on the structure of

acquisition contracts.

3. Hypothesis development

As mentioned above, if an acquisition contract includes an earnout, the payment of part of the

consideration is postponed to the future, and that part of payment depends on the achievement of

pre-established benchmarks by the target company. Such benchmarks are often based on

performance measures.

The presence of an earnout reverses the “information asymmetry” problem that usually

characterizes acquisitions. While before the closing the sellers have perfect monitoring over their

company, and the bidder faces an information asymmetry problem which can be only partially

unveiled through a due diligence process, the situation is reversed afterwards. Indeed, at the deal

closing the bidder acquires the ownership and the control of the target company. As a consequence,

10

it is now the acquirer who potentially possesses more information on the acquired company, while

the sellers (of the target company) face the issues and the consequences of information asymmetry.

By acquiring control, the buyer becomes in-charge of measuring and reporting the post-acquisition

performance of the acquired company. However, there is a risk of opportunistic behavior aimed at

reducing or avoiding the contractual payment to the sellers. Indeed, the acquirer may affect the

reported performance of the acquired company either by reducing the exerted effort or through

accounting policies aimed at reducing the reported performance. The risk that the acquirer will

engage in opportunistic behavior is increased by the sellers’ limited monitoring ability and lack of

ability to influence the decisions of the acquirer itself.

In case of disagreement about the benchmark outcomes, due to an alleged opportunistic behavior by

the acquirer, the sellers may revert to a judicial court. However, the judges themselves may be

affected by an information asymmetry that an investigation process may not completely resolve.

Also, the judges may be called to decide on matters like the computation of accounting numbers,

which are subject to discretion.

The limited ex-post monitoring and enforcement possibilities, along with the risk to bear

deadweight litigation cost in case of unsuccessful legal trial, will induce the sellers to engage in a

rigorous and accurate ex-ante screening of their counterparties before accepting an earnout

agreement.

We hypothesize that bidder’s past earnings quality is one of the signals employed by sellers to

evaluate the bidder’s trustworthiness. Using earnings management as an inverse proxy for earnings

quality, we expect that a higher level of earnings management in the bidder’s past financial

statements will be assumed by the sellers as an indicator of higher risk of opportunistic behavior

after the closing of the deal. Thus, the sellers would be more inclined to accept an agreement

including an earnout when their counterparty showed low level of past earnings management.

Based on this line of reasoning, we formulate our hypothesis as follows:

11

The likelihood of inclusion of earnouts in acquisition deals is negatively associated with the level of

earnings management in the acquirer’s past financial statements.

In the next section we provide a description of the sample and the data used to test our hypothesis.

4. Data and variable description

4.1. Sample composition

We collect acquisitions data over the period January 1st, 2002 – December 31st, 2014 from Thomson

ONE Banker, provided by SDC. This initial sample is merged with Compustat to retrieve the

relevant accounting information. The final sample includes deals completed during the selected

period, and for which the acquirer is a non-financial public company. Information on the total

consideration paid, market value of the acquirer prior to the acquisition, and the accounting

numbers required for estimating the abnormal accrual measure (i.e. our earnings management

proxy) must be available.

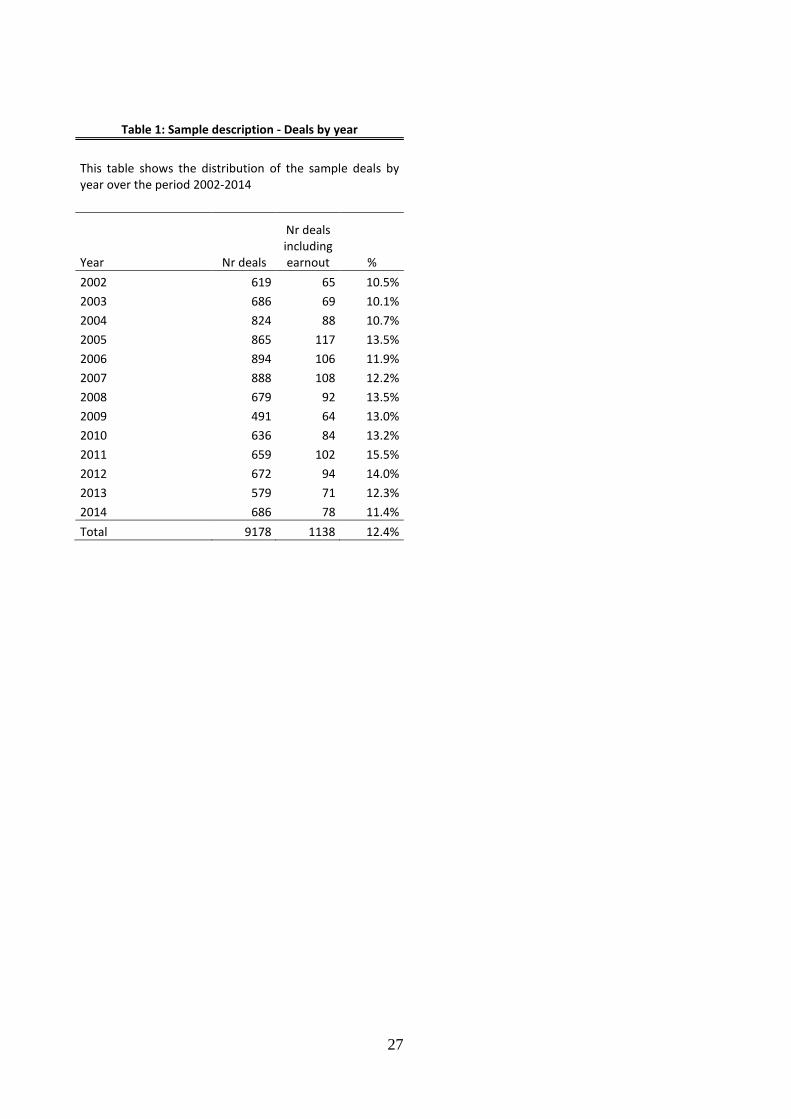

Table 1 provides details on the composition of the sample. The sample comprises 9,178 deals, out

of which 1,138 deals include earnout agreements, i.e. 12.4% of total deals, a significantly higher

proportion than the 9% reported by Cadman, et. al. (2014). There is a substantial variation in the

number of earnout deals over the sample years, from 64 in 2009 to 117 earnout deals in 2005. The

sample exhibits also a variation of the earnout deals proportion over the sample period, from 10.1%

in 2003 to 15% in 2011.

[Insert Table 1 here]

Panel A of Table 2 provides additional descriptives of the sample. Using Fama-French 12 industries

classification, we note a high proportion of earnouts deals in several industries: 22.4% in

healthcare, followed by consumer durables (15.3%) and Computers (14.6%). Panel B of Table 2

12

classifies the sample according to the target’s industry. Also here we note similar industrial

concentration: 22,1% in healthcare, and 14.6% in computers. This sample attributes are similar to

those reported by Datar et al. (2001).

[Insert Tables 2 here]

4.2 Earnings management proxy

To estimate the level of the acquirers’ earnings management we apply the modified-Jones model

as in Dechow et. al. (1995), adding ROA to the model as suggested by Kothari, Leone and Wasley

(2005). We use a cross-sectional specification of the model by time and industry (i.e. quarter or

year, consistently with the definition of the time variable). We follow Peasnell, Pope and Young

(2000) and Jeter and Shivakumar (1999), who suggest that cross-sectional models seem to be better

specified and have higher power than time series estimation models.

The model used to estimate accruals is the following:

ACCRj,t/TAj,t-1 = α[1/TAj,t-1] + β1[(ΔREVj,t - ΔRECj,t)/ TAj,t-1] + β2[PPEj,t/TAj,t-1] + β3ROAj,t

+ εj,t

(1)

Where j and t designate firm and time, respectively, ACCR is the total accruals, ΔREV is the

change in revenues, ΔREC is the change in accounts receivable, PPE designates property, plants

and equipment, ROA is return on assets, and TA stands for total assets.

Quarterly data are used to estimate the model, defining industries according to the Fama-French 12

industry classification. Abnormal accruals are defined as the actual accruals not explained by the

expectation as estimated by model (1), i.e.,

EMj,t = |ACCRj,t/TAj,t-1 – E(ACCRj,t/TAj,t-1)|

13

We apply the absolute abnormal accruals of the acquirer averaged over the four quarters preceding

the acquisition, which we label EM. We opt for an absolute measure because we are more interested

in the reliability of earnings rather than in the direction of their effects. We compute the average of

the four quarters in order to capture a behavior that is consistent in time, rather than occasional.

However, for robustness tests, we resort to variations of EM measures to validate the reported

results.

4.3 Explanatory variables

To test our hypothesis, we perform both a univariate and a multivariate analyses. In the latter case,

we use the model that includes control variables as reported in prior studies, i.e., Kohers and Ang

(2000), Datar et al. (2001), Barbopulos and Sudarsanam (2012), and Cadman et al. (2014). They

suggest that earnouts are more frequently used in deals involving private companies and

subsidiaries, for which the problem of asymmetry of information is relevant, also because of the

absence of a market price for the target. Similarly, earnouts are more likely used for the acquisitions

of targets operating in the service or high-tech industries, due to the high growth opportunities and

relevant uncertainties related to the role of human capital that characterizes these industries. The

presence of a toehold in the target company reduces the probability of an earnout, because the

acquirer possibly possesses information on the target, and thus the valuation risk is less relevant

than when a toehold is absent. Moreover, the likelihood of observing an earnout in a deal is

positively associated with the size of the deal, and negatively associated with the value of the

acquirer. We control also for whether the bidder and the target operate in same industry.8

Our model also controls for known determinants of earnings quality which may also affect the

likelihood of an earnout. In particular, we control for the audit firm size, typically reported to be

8 There is a lack of consensus on the association between diversifying acquisitions, that is, deals in which the acquirer and the target operate in different industries, and the use of earnouts. Focusing on the US market, Kohers and Ang (2000) and Datar et al. (2001), who focus on acquisitions during the 80’s and the 90’s, report a positive association between cross-industry deals and the use of earnouts. Instead, Cadman et al. (2014), who focus on a more recent sample, find opposite results.

14

positively (negatively) associated with earnings quality (earnings management) (e.g., DeAngelo,

1981), and for ROA (e.g., McNichols, 2000; Kothari et al., 2005). In additional tests we control also

for the quality of corporate governance, measured as the proportion of non-executive directors of

the total number of board directors. We add the corporate governance variable for two reasons: it

has been reported to be positively (negatively) associated to earnings quality (earnings

management) (e.g., Beasley, 1996; Klein, 2002), and may be argued that corporate governance

quality is an indicator of the acquirer reliability.

5. The logit model

Since the decision to include an earnout in a deal is a dichotomous variable, a logit model is

employed to test our hypothesis. We define and estimate the following model:

Logit{Prob(Earnoutit=1)} = β0 + β1EMit + Σ βi Controlsit + εit (2)

Our dependent variable is Earnout, a dummy variable that takes value 1 if an earnout agreement is

part of the deal, zero otherwise.

The model includes the following controls:

HighTech = a dummy variable that takes value 1 if the target operates in the high-tech sector, 0

otherwise;

Service = a dummy variable that takes value 1 if the target operates in the service industry, 0

otherwise;

DealValue = log of the transaction price of the deal, including the earnout;

MVacquirer = the log of the market value of the acquirer prior to the deal announcement;

Subsidiary = a dummy variable that takes value 1 if the target is a subsidiary, 0 otherwise;

Private = a dummy variable that takes value 1 if the target is a private company, 0 otherwise;

15

SameIND = a dummy variable that takes value 1 if bidder and target have the same two-digits SIC

code;

Toehold = a dummy variable that takes value 1 if the bidder holds a stake in the target before the

acquisition, 0 otherwise;

Stock = a dummy variable that takes value 1 if the upfront payment is at least partly in stocks, 0

otherwise;

ROA = the return on assets of the acquirer calculated as the ratio of net income to total assets in the

quarter (year) preceding the acquisition ;

Big4 = a dummy variable that takes value 1 if the bidder’s financial statements are audited by one

of the big 4 audit firms, 0 otherwise;

CorpGov = Acquirer’s ratio of non-executive directors over total number of directors at the

acquisition time.

We also include year fixed effects to control for possible trends or changes in the regulatory or

economic environment over time.

6. Empirical analysis

6.1 Descriptive statistics

Table 3 provides descriptive statistics for the variables used in our study. Panel A compares the

variables’ statistics between earnout and non–earnout deals. The proportion of deals in which the

target is a high-tech or a service company is significantly higher in the earnout group (34.6% vs.

22.7%, and 40.0% vs. 31.9%, respectively), consistent with prior literature. The table also exhibits

that earnout transactions tend to be characterized by smaller-size acquirers (7.27 vs. 6.46,

respectively). Moreover, when the acquisition involves contingent payments, the frequency of

private companies is much higher than for the non-earnout sample (75.9% vs. 46.9%, respectively).

The opposite seems to hold if we look at the proportion of subsidiaries (22% vs. 37.1%). However,

16

filtering out the relative presence of private companies, we notice that among non-private

companies the frequency of subsidiaries is higher in deals involving earnouts. Earnout deals seem

also to be characterized by a higher frequency of transactions in the same industry (63.9% vs.

60.7%), and by a higher proportion of acquisitions that include common stocks in the upfront

payment (26.4% vs. 18.4%, respectively). The frequency of bidders having a toehold in the target

company, instead, is significantly lower for earnout deals. Finally, if we compare the average value

of our earnings management variable, we observe that it is rather similar in earnout and non-earnout

deals (0.043 vs. 0.045, respectively).

Panel B provides the Pearson correlation matrix. The first column of the table reports correlations in

line with prior literature. Indeed, earnouts are positively correlated with high-tech and service

industries, with the target being a private firm and (weakly) with the target being in the same

industry as the acquirer. Earnouts are negatively correlated with the deal value and the market value

of the acquirer, with the target being a subsidiary, and with the acquirer having a toehold in the

target., Earnouts seem to be (weakly) negatively correlated with the acquirer’s auditor size and its

corporate governance measure. Such correlation, however, is most probably associated with the

high correlations of these variables with the acquirer’s size (MVacquirer), as shown in column 6.

The table reveals that earnings management (EM) is significantly negatively correlated to the

acquirer’s size (-0.337), with auditor size (-0.296), with ROA (-0.274) and the corporate

governance variable (-0.110). These correlations are in line with those reported in the earnings

management literature. The panel also indicates that earnings management is positively correlated

with cases where deals include a payment partly with stocks (0.115), consistent with the extant

literature (e.g., Erickson and Wang, 1999; Botsari and Meeks, 2008).

[Insert Table 3 here]

17

6.2 Results

The results of our main logit regression models are reported in Table 4.

The table provides coefficients values of four versions of Model (2), where different controls are

applied as explanatory variables. These regressions are based on 9,178 acquisitions and all four

regressions are significant with all Chi2 values above 500.

Model 1 is similar to the models applied in prior studies, with the inclusion of the auditor size

(Big4) as an additional control variable. The regression coefficient of Big4 is insignificant, possibly

due to the lack of variation in the sample, once considered its high correlation with the acquirer

size. The variable SameIND, which controls for deals done in the same industry, is found

insignificantly different from zero. This is not surprising as prior literature report conflicting results

regarding this variable. All other variables in the model are consistent with prior findings. In

particular, the negative coefficient of the acquirer size (MVacquirer) (-0.191) suggests that large

firms are less inclined to use earnouts in acquisition deals, perhaps because they can likely afford

higher misvaluation risk. The probability of a deal to include earnouts is increasing with the target

being in the service (0.638) or high-tech (1.046) industries, with deal size (0.102), with the target

being either private firms (2.507) or subsidiaries of other firms (1.589). All these results are

consistent with those reported by Kohers and Ang (2000), Datar et al. (2001), Barbopulos and

Sudarsanam (2012), and Cadman et al. (2014).

Model 2 includes the earnings management variable (EM). Consistently with our hypothesis, the

coefficient is significantly negative (coefficient of -1.472, with s.e. of 0.549), suggesting that the

higher the acquirer’s earnings management in the four quarters preceding the deal, the less likely

the sellers to accept an earnout agreement to be included in the transaction. In Model 3 we control

also for the presence of a toehold. We find that it is negatively associated with the probability of

inclusion of an earnout, significant at the 10% confidence level (coefficient of -0.376 and s.e. of

0.200). In model 4 we include the variable Stock, which captures the fact that part of the upfront

payment is made in stocks. The latter variable shows a significant positive coefficient (0.268, with

18

s.e. of 0.0843), suggesting that common stocks and earnouts tend to be used as complementary tools

for risk sharing purposes. In both Models 3 and 4, the coefficient on the earnings management

variable remains negative and significant, and very close in their magnitude to that in Model 2. This

empirical evidence supports our expectation that the sellers do a ‘reverse due diligence’ on the

acquirers, to screen the acquirer trustworthiness.

In Table 5 we include an additional control for the corporate governance quality, proxied by the

ratio between non-executive directors and total number of board members. The idea behind this

inclusion is that the quality of the firm corporate governance may be considered as a ‘corporate’

quality sign. Therefore it may serve either as a substitute or as a complement to the earnings

management signal. The inclusion of this control reduces the sample size to 7,831 deals.

Nonetheless, the results are very similar to those reported in Table 4. The corporate governance

coefficient is negative but it lacks statistical significance, thus it does not seem to affect the

likelihood of the inclusion of an earnout in the acquisition contract.

[Insert Table 4 and Table 5 here]

In the next section, we test the robustness of our results to various definition of earnings

management (applying variations of window period estimations), and to stricter requirements on the

sample selection process.

7. Robustness tests

7.1 Changing the time horizon for the measurement of earnings management

In our main analysis we measure earnings management over the four quarters preceding the

acquisition. Prior literature suggests that acquirers have the incentive to manage earnings upwards

in the quarters preceding the deal in order to increase the stock price of their company, and thus to

19

reduce the cost of acquiring the target (e.g., Erickson and Wang, 1999; Botsari and Meeks, 2008).

Therefore, the quarters immediately preceding the acquisitions may be considered a good indicator

of the tendency to carry out earnings management in the presence of a contractual incentive.

However, one may question the sellers’s ability to observe the last quarter’s results before deciding

on the inclusion of an earnout in the agreement. In order to address this concern, we first repeat our

logit models excluding the last quarter, i.e. the quarter just prior to the completion of the deal. Our

results (untabulated) remain qualitatively unchanged, confirming that earnings management is

negatively related to the likelihood of inclusion of an earnout in the acquisition contract. We repeat

these analyses after calculating our test variable as the average of the earnings management proxy

over a longer time horizon, i.e. the six quarters preceding the deal (both including and excluding the

last quarter). The results (untabulated) remain qualitatively unchanged.

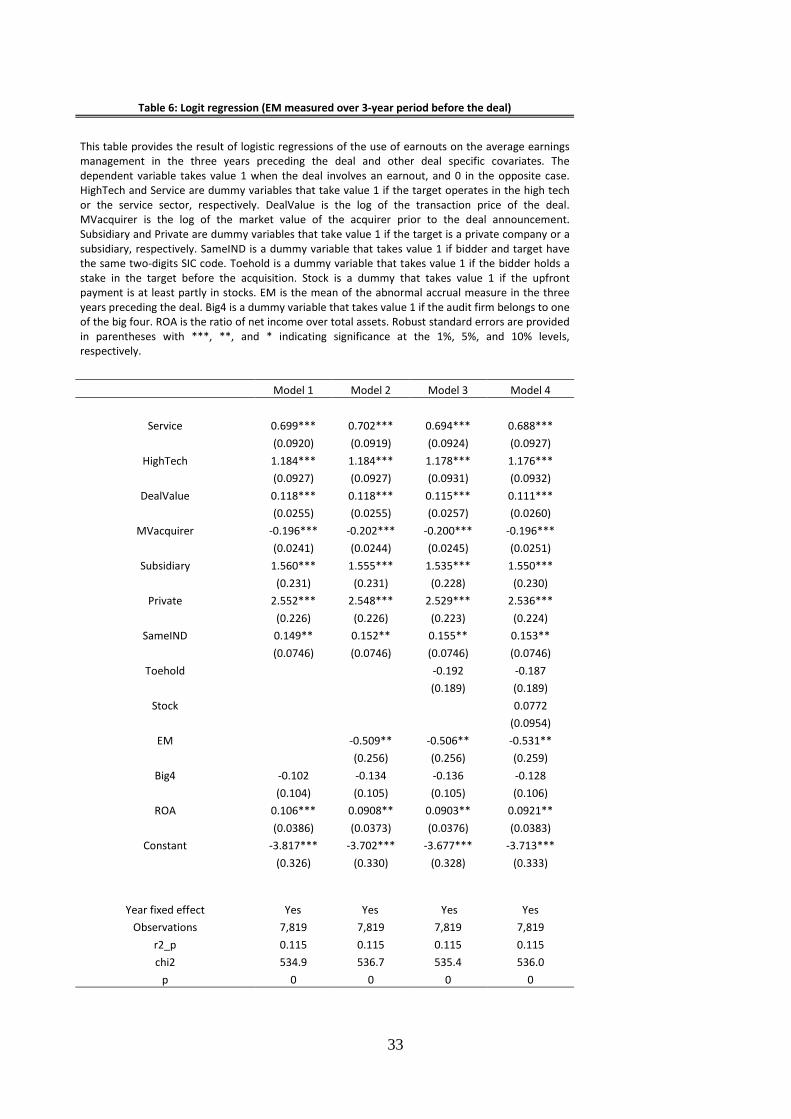

In further tests, we check whether using annual data to measure the attitude to manage earnings by

the bidder alters our main findings. Table 6 reports the results of the logit regressions when earnings

management is estimated using annual data over a 3-year period preceding the deal. Basically, these

revised definitions of earnings management measures do not alter our reported results. The earnings

management variable is found to be negatively and significantly related to the likelihood of

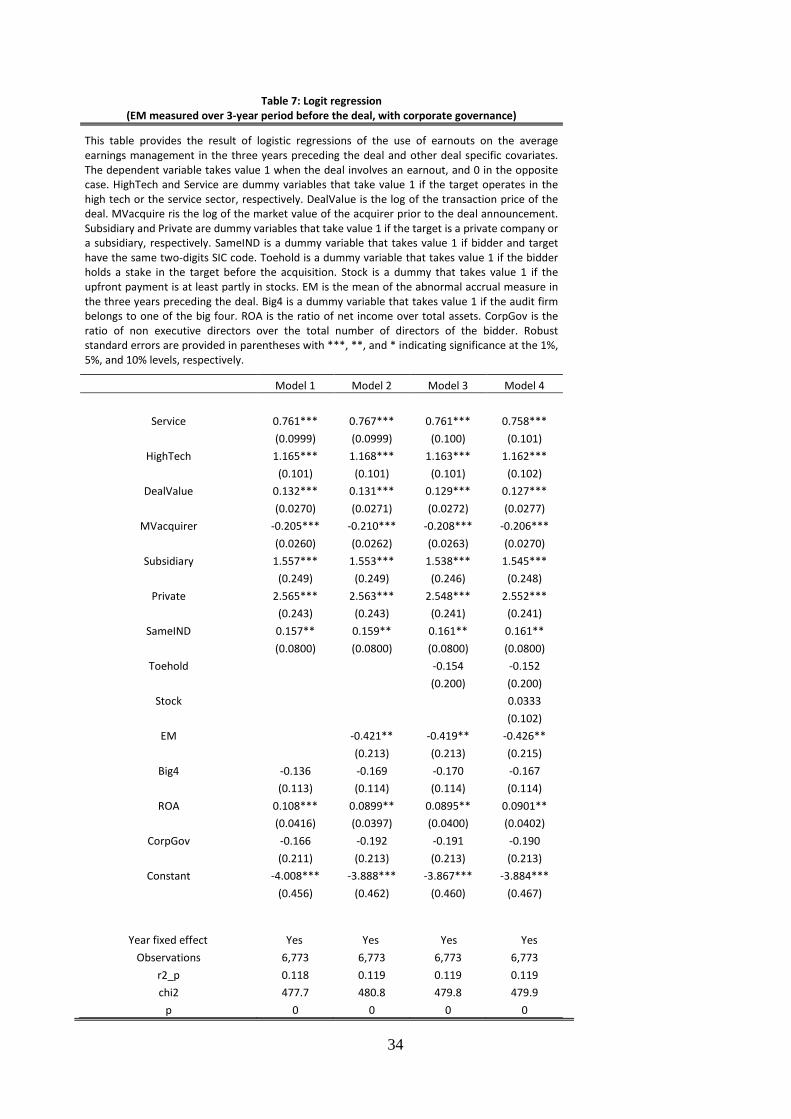

inclusion of an earnout in the contract (-0.509, s.e. 0.256). Similar results are shown when we also

control for the corporate governance quality (Table 7).

[Insert Table 6 and Table 7 here]

Our main findings (untabulated) hold also when we exclude the last year prior to the acquisition

and, therefore, consider only the earnings management carried out in years t-2 and t-3.

20

7.2 Propensity Score Matching

In order to further check the validity of our hypothesis, we compute a t-test for the differences in the

mean level of earnings management for the group of deals in which earnouts are included and for

those in which they are not, using a Propensity Score Matching procedure (PSM), as described in

Becker and Ichino (2002). The idea behind this methodology is to compare the level of earnings

management (our outcome variable) between a group of treated subjects (earnout users) and a group

of non-treated subjects (non-earnout users) selected as similar as possible to the treated

observations. We follow this procedure to reduce the possibility that the comparison of subjects that

are inherently different could bias the results.

The propensity score is computed taking into consideration the following deal characteristics: the

acquirer size, defined as total assets, the deal value , that is the total value of the transaction, the

target operating in the high tech or service industry, and a dummy variable for the period before the

financial crisis of 20079. The model is parsimonious, yet it satisfies the balancing hypothesis10

.

Moreover, in order to improve the quality of the match, only the observations belonging to the

common support of the treated and non-treated are used in the comparison.

[Insert Table 8 here]

The results of the PSM analysis, performed using the nearest neighbor method, are shown in Table

8. The level of earnings management is estimated over the four quarters preceding the deal, as in

our main analysis. Consistently with our hypothesis, the acquirers of deals in which earnouts are

9 The size of the acquirer and the size of the deal are defined in terms of terciles of their sample distribution. Each observation is assigned to one of three groups: high, medium or small bidder size, and high, medium or small deal size. This partitioning is used for the computation of the propensity score. 10 If the balancing hypothesis is satisfied, treated observations and non-treated observations with the same propensity score share the same distribution of observable and unobservable characteristics.

21

used show a lower level of earnings management compared to their matched peers (i.e. non-users).

The difference is significant at the 1% level (t-values of -3.759 to -2.922).

7.3 Introducing additional filters

In line with Datar et al. (2001) and Cadman et al. (2014), in our main analyses we did not impose

any restriction on the percentage of shares acquired in the deal. By using more restrictive filters on

the sample, however, our results remain qualitatively the same.

[Insert Tables 9 and 10 here]

Table 9 reports the results obtained considering only the subsample of deals in which at least 20%

of the shares of the target is acquired. In a setting like the US, in which ownership is generally

fragmented, such percentage is usually sufficient to gain control on a company. The results in terms

of signs and levels of significance remain substantially the same.

In table 10 we apply an even more stringent filter, as we consider only deals in which the toehold in

the target before the acquisition is lower than 50%, and the ownership of the acquirer after the

acquisition is at least 90%. Our main results confirm to be robust, suggesting that past earnings

management of the acquirer is negatively associated with the probability of inclusion of an earnout

in the deal.

8. Conclusions

Earnouts are contractual agreements that condition part of the payment of an acquisition to the

future performance of the acquired company.

22

Earnouts are beneficial for acquirers as they reduce the information asymmetry that typically affects

acquisitions, and act as a selection mechanism on the quality of the target company. They are

advantageous also to the sellers, as they reduce the risk of adverse selection for the target company,

thus allowing to negotiate a higher consideration. However, this benefit comes at a price, because,

after the closing of the deal, the sellers bear not only the risk that the acquired company will not

meet the earnout requirements, but also the risk that the acquirer will act opportunistically to

reduce, or even avoid, the accounting based benchmarks for determining the contingent payment.

Such opportunism can be implemented by either managing the accounting numbers, or by reducing

the effort in directing the target’s activities.

Legal disputes on the actual realization of the performance levels stated by the earnout are indeed

frequent. However, anecdotal evidence indicates that the risk to lose the legal case and to bear the

cost of the litigation for the sellers is not trivial.

Given the above-mentioned risks related to the ex post enforcement of earnout contracts, sellers

who intend to agree for earnout contracts are likely to engage in ex-ante screening of the

trustworthiness of their counterparties. To this purpose, past earnings quality of the acquirer may

be used by the sellers as a signal of the former’s reliability. Therefore, we hypothesize that the

decision to include an earnout agreement in an acquisition contract is positively related to the

acquirer’s past earnings quality.

We test this hypothesis on a sample of 9,178 deals completed in US between 2002 and 2014. In

order to capture the quality of earnings of the acquirer, we rely on the absolute value of the earnings

management proxy, computed using a variation of the modified Jones’ model (Dechow et al.,

1995). A lower absolute value of our earnings management proxy indicates a higher level of

earnings quality, and therefore of higher level of trustworthiness.

After controlling for the determinants that prior studies have associated with the use of earnouts,

through a logit model we show that there is a negative and significant relation between earnings

management and the likelihood of inclusion of an earnout in an acquisition deal. Overall, our results

23

validate the hypothesis that the acquirer’s past earnings quality is used as a signal by the seller to

evaluate the former’s reliability.

Our paper contributes to the literature on earnouts by showing that the bidder’s trustworthiness is a

significant determinant of the decision by the seller to accept such contractual agreements. Our

paper contributes also to the literature on the relation between M&As and earnings management,

that so far has mainly been focused on the managerial incentives to manage earnings around the

acquisition time to improve the results of the negotiation. Our study is the first to show that past

earnings quality of the counterparty is a relevant determinant of the structure of acquisition

contracts.

References

Allee, K., Wangerin, D. (2013). Auditors’ Role in Financial Contracting: Evidence from SFAS 141

(R). Working paper.

Ball, R., Shivakumar, L. (2008). Earnings quality at initial public offerings: managerial

opportunism or public-firm conservatism. Journal of Accounting and Economics, 45, 324-

349.

Beasley, M. S. (1996). An Empirical Analysis of the Relation between the Board of Director

Composition and Financial Statement Fraud. The Accounting Review, 71, 443–465.

Becker, S. O., Ichino, A. (2002). Estimation of average treatment effects based on propensity

scores. The Stata Journal 2(4).

Barbopoulos, L., Sudarsanam, S. (2012). Determinants of earnout as acquisition payment currency

and bidder’s value gains. Journal of Banking & Finance, 36(3).

Botsari, A., Meeks, G. (2008). Do acquirers manage earnings prior to a share for share bid?.

Journal of Business Finance & Accounting, 35(5‐6).

Cadman, B., Carrizosa, R., Faurel, L. (2014). Economic Determinants and Information

Environment Effects of Earnouts: New Insights from SFAS 141 (R). Journal of Accounting

Research, 52(1).

Cain, M. D., Denis, D. J., Denis, D. K. (2011). Earnouts: A study of financial contracting in

acquisition agreements. Journal of Accounting and Economics, 51(1).

Crimmins, P. M., Gray, B, Waller, J., Brown, M. (2010). Earn-outs in M&A Transactions. The

M&A Journal, 10(10).

Datar, S., Frankel, R., Wolfson, M. (2001). Earnouts: The effects of adverse selection and agency

costs on acquisition techniques. Journal of Law, Economics, and Organization, 17(1).

DeAngelo, L.E. (1981). Auditor size and audit quality. Journal of Accounting and Economics, 3,

183-199.

25

Dechow, P. M., Sloan, R. G., Sweeney, A. P. (1995). Detecting earnings management. Accounting

Review, 70(2).

DuCharme, L. L., Malatesta, P. H., Sefcik, S. E. (2004). Earnings management, stock issues, and

shareholder lawsuits. Journal of financial economics, 71(1).

Erickson, M., Wang, S. (1999). Earnings management by acquiring firms in stock for stock

mergers. Journal of Accounting and Economics, 27(2).

Fox, D., Wolf, D. E. (2010). An Earnout Is In the Eye of the Beholder. Investment Dealers' Digest,

76(4).

Gong, G., Louis, H., Sun A. (2008). Earnings management, lawsuits, and stock-for-stock acquirers’

market performance. Journal of Accounting and Economics, 46, 62-77.

Healy, P. and J. Whalen, (1999). A Review of the Earnings Management Literature and its

Implication for Standard Setting, Accounting Horizons 13, 365–383.

Jensen, M. (2005). Agency costs of overvalued equity. Financial Management, 34, 5–19.

Jeter, D. C., Shivakumar, L. (1999). Cross-sectional estimation of abnormal accruals using quarterly

and annual data: Effectiveness in detecting event-specific earnings management. Accounting

and Business Research, 29(4).

Jones, J. J. (1991). Earnings management during import relief investigations. Journal of Accounting

Research, 29(2).

Klein, A. (2002). Audit Committee, Board of Director Characteristics and Earnings Management.

Journal of Accounting and Economics, 33, 375–400.

Kohers, N., Ang, J. (2000). Earnouts in Mergers: Agreeing to Disagree and Agreeing to Stay. The

Journal of Business, 73(3).

Kothari, S., Leone, A., Wasley, C., (2005), Performance Matched Discretionary Accrual Measures,

Journal of Accounting & Economics 39, 163-197.

Louis, H. (2004). Earnings management and the market performance of acquiring firms. Journal of

Financial Economics, 74(1).

26

McNichols, M.F. (2000). Research design issues in earnings management studies. Journal of

Accounting and Public Policy, 19, 313-345.

Morrison and Foerster LLP (2012). M&A Leaders Survey. Press Releases 5/15/2012. Available at:

www.mofo.com

Peasnell, K. V., Pope, P. F., Young, S. (2000). Detecting earnings management using cross-

sectional abnormal accruals models. Accounting and Business Research, 30(4).

Ragozzino, R., Reuer, J. J. (2009). Contingent earnouts in acquisitions of privately held targets.

Journal of Management, 35(4).

Shannon, K., Reilly, M. (2011). Post-Closing Earnouts in M&A Transactions: Avoiding Common

Disputes. American Bar Association Newsletter.

Subramanyam, K. R. (1996). The pricing of discretionary accruals. Journal of Accounting and

Economics, 22(1).

27

Table 1: Sample description - Deals by year

This table shows the distribution of the sample deals by year over the period 2002-2014

Year Nr deals

Nr deals including earnout %

2002 619 65 10.5% 2003 686 69 10.1% 2004 824 88 10.7% 2005 865 117 13.5% 2006 894 106 11.9% 2007 888 108 12.2% 2008 679 92 13.5% 2009 491 64 13.0% 2010 636 84 13.2% 2011 659 102 15.5% 2012 672 94 14.0% 2013 579 71 12.3% 2014 686 78 11.4% Total 9178 1138 12.4%

28

Table 2: Sample description - Deals by industry

This table provides descriptive statistics on the sample deals by industry. In panel A deals are classified according to the industry of the acquirer, while in panel B deals are classified according to the industry of the target. Deals in which the acquirer operates in the financial industry are excluded.

Panel A: Acquirer's industry

Industry Nr deals

Nr deals including earnout %

Consumer NonDurables 428 42 9.8% Consumer Durables 157 24 15.3% Manufacturing 1155 71 6.1% Oil, Gas, and Coal Extraction and Products 776 25 3.2% Chemicals and Allied Products 188 13 6.9% Computers, Software, and Electronic Equipment 2846 415 14.6% Telephone and Television Transmission 373 16 4.3% Utilities 247 3 1.2% Services and Retail 694 74 10.7% Healthcare, Medical Equipment, and Drugs 1139 255 22.4% Other (Mines, Constr, Entertainment, Transp) 1175 200 17.0% Total 9178 1138 12.4%

Panel B: Target's industry

Industry Nr deals

Nr deals including earnout %

Consumer NonDurables 389 46 11.8% Consumer Durables 181 20 11.0% Manufacturing 944 67 7.1% Oil, Gas, and Coal Extraction and Products 720 20 2.8% Chemicals and Allied Products 205 12 5.9% Computers, Software, and Electronic Equipment 2790 407 14.6% Telephone and Television Transmission 347 16 4.6% Utilities 239 3 1.3% Services and Retail 655 48 7.3% Healthcare, Medical Equipment, and Drugs 1139 252 22.1% Financial 142 13 9.2% Other (Mines, Constr, Entertainment, Transp) 1427 234 16.4% Total 9178 1138 12.4%

Table 3: Descriptive statistics and correlations

This table provides descriptive statistics on the main variables used in the analysis. HighTech and Service are dummy variables that take value 1 if the target operates in the high tech or the service sector, respectively. DealValue is the log of the transaction price of the deal. MVacquirer is the log of the market value of the acquirer prior to the deal announcement. Subsidiary and Private are dummy variables that take value 1 if the target is a private company or a subsidiary, respectively. SameIND is a dummy variable that takes value 1 if bidder and target have the same two-digits SIC code. Toehold is a dummy variable that takes value 1 if the bidder holds a stake in the target before the acquisition. Stock is a dummy that takes value 1 if the upfront payment is at least partly in stocks. EM is the mean of the abnormal accrual measure in the four quarters preceding the deal. Big4 is a dummy variable that takes value 1 if the audit firm is belongs to one of the big four. ROA is the ratio of net income over total assets. CorpGov is the ratio of non-executive directors over the total number of directors of the bidder. Panel A provides, for each variable, mean and standard deviation, detailed for the subsample of earnout users, non earnout users, and in the whole sample. Panel B provides correlations. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Panel A: Means and standard deviations

Non-earnout users Earnout users Total

Mean SD Mean SD Sign. Mean SD HighTech 22.70% 41.90% 34.60% 47.60% *** 24.10% 42.80% Service 31.90% 46.60% 40.00% 49.00% *** 32.90% 47.00% DealValue 3.964 1.884 3.516 1.540 *** 3.908 1.851 MVacquirer 7.276 2.124 6.460 1.997 *** 7.170 2.126 Subsidiary 37.10% 48.30% 22.00% 41.40% *** 35.20% 47.80% Private 46.90% 49.90% 75.90% 42.80% *** 50.50% 50.00% SameIND 60.70% 48.80% 63.90% 48.10% ** 61.10% 48.70% Toehold 6.50% 24.60% 2.50% 15.80% *** 6.00% 23.70% Stock 18.40% 38.80% 26.40% 44.10% *** 19.40% 39.60% Big4 80.60% 39.60% 73.10% 44.40% *** 79.60% 40.30% ROA -0.50% 47.30% 0.30% 6.80% -0.40% 44.30% CorpGov 38.20% 37.90% 39.20% 37.20% 38.30% 37.80% EM 0.043 0.06 0.045 0.047 0.043 0.059

30

Panel B: Pearson Correlations

Earnout HighTech Service DealValue MVacquirer Subsidary Private SameIND Toehold Stock Big4 ROA CorpGov EM

Earnout

1 HighTech

0.104*** 1

Service

0.011*** -0.392*** 1 DealValue -0.077*** 0.018* -0.127*** 1

MVacquirer -0.125*** 0,006 0.057*** 0.619*** 1 Subsidiary -0.054*** 0.024*** -0.176*** 0.056*** -0.032*** 1

Private 0.085*** -0.064*** 0.208*** -0.269*** -0.026*** -0.83*** 1 SameIND 0.028*** 0.041*** 0.037*** 0.024*** -0.065*** 0,004 -0.016** 1

Toehold

-0.039*** -0,003 -0.069*** 0,001 0.041*** -0.021*** -0.106*** 0,009 1 Stock

0.128*** 0.033*** 0,006 -0.016* -0.226*** -0.085*** 0,003 0.034*** -0.031*** 1

Big4

-0.053*** 0.02*** 0,006 0.326*** 0.556*** 0.027*** -0.061*** 0,01 0.019*** -0.186*** 1 ROA

0,007 -0.017** 0,01 0.042*** 0.073*** -0,001 -0,002 0.017** -0,009 -0.046*** 0.058*** 1

CorpGov

-0.016** -0,009 0.025*** 0.162*** 0.222*** -0.031*** 0.034*** -0,004 0,004 -0.102*** 0.052*** 0.019*** 1 EM 0,008 -0.022*** -0.013* -0.2*** -0.337*** -0,008 0.015** -0,006 -0,001 0.115*** -0.296*** -0.274*** -0.11*** 1

Table 4: Logit regression (EM measured over 4 quarters before the deal)

This table provides the result of logistic regressions of the use of earnouts on the average earnings management in the four quarters preceding the deal and other deal specific covariates. The dependent variable takes value 1 when the deal involves an earnout, and 0 in the opposite case. HighTech and Service are dummy variables that take value 1 if the target operates in the high tech or the service sector, respectively. DealValue is the log of the transaction price of the deal. MVacquirer is the log of the market value of the acquirer prior to the deal announcement. Subsidiary and Private are dummy variables that take value 1 if the target is a private company or a subsidiary, respectively. SameIND is a dummy variable that takes value 1 if bidder and target have the same two-digits SIC code. Toehold is a dummy variable that takes value 1 if the bidder holds a stake in the target before the acquisition. Stock is a dummy that takes value 1 if the upfront payment is at least partly in stocks. EM is the mean of the abnormal accrual measure in the four quarters preceding the deal. Big4 is a dummy variable that takes value 1 if the audit firm belongs to one of the big four. ROA is the ratio of net income over total assets. Robust standard errors are provided in parentheses with ***, **, and * indicating significance at the 1%, 5%, and 10% levels, respectively.

Model 1 Model 2 Model 3 Model 4

Service 0.638*** 0.633*** 0.620*** 0.596***

(0.0829) (0.0829) (0.0833) (0.0837)

HighTech 1.046*** 1.038*** 1.028*** 1.017***

(0.0851) (0.0852) (0.0855) (0.0857)

DealValue 0.102*** 0.102*** 0.0978*** 0.0841***

(0.0236) (0.0236) (0.0238) (0.0241)

MVacquirer -0.191*** -0.202*** -0.198*** -0.183***

(0.0216) (0.0223) (0.0224) (0.0229)

Subsidiary 1.589*** 1.580*** 1.544*** 1.604***

(0.221) (0.221) (0.218) (0.220)

Private 2.507*** 2.501*** 2.465*** 2.495***

(0.216) (0.216) (0.213) (0.215)

SameIND 0.0795 0.0762 0.0810 0.0735

(0.0685) (0.0686) (0.0686) (0.0687)

Toehold

-0.376* -0.360*

(0.200) (0.200)

Stock

0.268***

(0.0843)

EM

-1.472*** -1.463*** -1.609***

(0.549) (0.547) (0.555)

Big4 0.0443 0.0101 0.00687 0.0406

(0.0947) (0.0946) (0.0946) (0.0957)

ROA 0.0904* 0.105** 0.105** 0.105**

(0.0492) (0.0423) (0.0425) (0.0446)

Constant -3.926*** -3.740*** -3.693*** -3.876***

(0.291) (0.301) (0.300) (0.310)

Year fixed effect Yes Yes Yes Yes

Observations 9,178 9,178 9,178 9,178 r2_p 0.0997 0.101 0.101 0.103 chi2 529.6 534.3 530.6 541.8

p 0 0 0 0

32

Table 5: Logit regression controlling for corporate governance quality

This table provides the result of logistic regressions of the use of earnouts on the average earnings management in the four quarters preceding the deal and other deal specific covariates. The dependent variable takes value 1 when the deal involves an earnout, and 0 in the opposite case. HighTech and Service are dummy variables that take value 1 if the target operates in the high tech or the service sector, respectively. DealValue is the log of the transaction price of the deal. MVacquirer is the log of the market value of the acquirer prior to the deal announcement. Subsidiary and Private are dummy variables that take value 1 if the target is a private company or a subsidiary, respectively. SameIND is a dummy variable that takes value 1 if bidder and target have the same two-digits SIC code. Toehold is a dummy variable that takes value 1 if the bidder holds a stake in the target before the acquisition. Stock is a dummy that takes value 1 if the upfront payment is at least partly in stocks. EM is the mean of the abnormal accrual measure in the four quarters preceding the deal. Big4 is a dummy variable that takes value 1 if the audit firm belongs to one of the big four. ROA is the ratio of net income over total assets. CorpGov is the ratio of non executive directors over the total number of directors of the bidder. Robust standard errors are provided in parentheses with ***, **, and * indicating significance at the 1%, 5%, and 10% levels, respectively.

Model 1 Model 2 Model 3 Model 4

Service 0.699*** 0.693*** 0.683*** 0.664***

(0.0906) (0.0906) (0.0910) (0.0915)

HighTech 1.043*** 1.033*** 1.026*** 1.018***

(0.0934) (0.0936) (0.0938) (0.0940)

DealValue 0.115*** 0.115*** 0.112*** 0.101***

(0.0254) (0.0254) (0.0256) (0.0259)

MVacquirer -0.197*** -0.207*** -0.204*** -0.192***

(0.0236) (0.0241) (0.0242) (0.0249)

Subsidiary 1.614*** 1.607*** 1.579*** 1.628***

(0.242) (0.242) (0.239) (0.242)

Private 2.571*** 2.568*** 2.540*** 2.565***

(0.237) (0.237) (0.234) (0.235)

SameIND 0.0857 0.0837 0.0874 0.0819

(0.0741) (0.0741) (0.0741) (0.0742)

Toehold

-0.306 -0.293

(0.209) (0.209)

Stock

0.216**

(0.0908)

EM

-1.544** -1.535** -1.645***

(0.625) (0.623) (0.630)

Big4 -0.0162 -0.0530 -0.0554 -0.0282

(0.107) (0.107) (0.107) (0.108)

ROA 0.0743 0.0978** 0.0976** 0.0968**

(0.0476) (0.0431) (0.0432) (0.0447)

CorpGov -0.173 -0.223 -0.223 -0.205

(0.194) (0.197) (0.197) (0.198)

Constant -3.923*** -3.735*** -3.697*** -3.846***

(0.314) (0.325) (0.324) (0.333)

Year fixed effect Yes Yes Yes Yes

Observations 7,831 7,831 7,831 7,831 r2_p 0.106 0.106 0.107 0.108 chi2 476.1 480.2 477.8 484.8

p 0 0 0 0

33

Table 6: Logit regression (EM measured over 3-year period before the deal)

This table provides the result of logistic regressions of the use of earnouts on the average earnings management in the three years preceding the deal and other deal specific covariates. The dependent variable takes value 1 when the deal involves an earnout, and 0 in the opposite case. HighTech and Service are dummy variables that take value 1 if the target operates in the high tech or the service sector, respectively. DealValue is the log of the transaction price of the deal. MVacquirer is the log of the market value of the acquirer prior to the deal announcement. Subsidiary and Private are dummy variables that take value 1 if the target is a private company or a subsidiary, respectively. SameIND is a dummy variable that takes value 1 if bidder and target have the same two-digits SIC code. Toehold is a dummy variable that takes value 1 if the bidder holds a stake in the target before the acquisition. Stock is a dummy that takes value 1 if the upfront payment is at least partly in stocks. EM is the mean of the abnormal accrual measure in the three years preceding the deal. Big4 is a dummy variable that takes value 1 if the audit firm belongs to one of the big four. ROA is the ratio of net income over total assets. Robust standard errors are provided in parentheses with ***, **, and * indicating significance at the 1%, 5%, and 10% levels, respectively.

Model 1 Model 2 Model 3 Model 4

Service 0.699*** 0.702*** 0.694*** 0.688***

(0.0920) (0.0919) (0.0924) (0.0927)

HighTech 1.184*** 1.184*** 1.178*** 1.176***

(0.0927) (0.0927) (0.0931) (0.0932)

DealValue 0.118*** 0.118*** 0.115*** 0.111***

(0.0255) (0.0255) (0.0257) (0.0260)

MVacquirer -0.196*** -0.202*** -0.200*** -0.196***

(0.0241) (0.0244) (0.0245) (0.0251)

Subsidiary 1.560*** 1.555*** 1.535*** 1.550***

(0.231) (0.231) (0.228) (0.230)

Private 2.552*** 2.548*** 2.529*** 2.536***

(0.226) (0.226) (0.223) (0.224)

SameIND 0.149** 0.152** 0.155** 0.153**

(0.0746) (0.0746) (0.0746) (0.0746)

Toehold

-0.192 -0.187

(0.189) (0.189)

Stock

0.0772

(0.0954)

EM

-0.509** -0.506** -0.531**

(0.256) (0.256) (0.259)

Big4 -0.102 -0.134 -0.136 -0.128

(0.104) (0.105) (0.105) (0.106)

ROA 0.106*** 0.0908** 0.0903** 0.0921**

(0.0386) (0.0373) (0.0376) (0.0383)

Constant -3.817*** -3.702*** -3.677*** -3.713***

(0.326) (0.330) (0.328) (0.333)

Year fixed effect Yes Yes Yes Yes

Observations 7,819 7,819 7,819 7,819 r2_p 0.115 0.115 0.115 0.115 chi2 534.9 536.7 535.4 536.0

p 0 0 0 0

34

Table 7: Logit regression (EM measured over 3-year period before the deal, with corporate governance)

This table provides the result of logistic regressions of the use of earnouts on the average earnings management in the three years preceding the deal and other deal specific covariates. The dependent variable takes value 1 when the deal involves an earnout, and 0 in the opposite case. HighTech and Service are dummy variables that take value 1 if the target operates in the high tech or the service sector, respectively. DealValue is the log of the transaction price of the deal. MVacquire ris the log of the market value of the acquirer prior to the deal announcement. Subsidiary and Private are dummy variables that take value 1 if the target is a private company or a subsidiary, respectively. SameIND is a dummy variable that takes value 1 if bidder and target have the same two-digits SIC code. Toehold is a dummy variable that takes value 1 if the bidder holds a stake in the target before the acquisition. Stock is a dummy that takes value 1 if the upfront payment is at least partly in stocks. EM is the mean of the abnormal accrual measure in the three years preceding the deal. Big4 is a dummy variable that takes value 1 if the audit firm belongs to one of the big four. ROA is the ratio of net income over total assets. CorpGov is the ratio of non executive directors over the total number of directors of the bidder. Robust standard errors are provided in parentheses with ***, **, and * indicating significance at the 1%, 5%, and 10% levels, respectively.

Model 1 Model 2 Model 3 Model 4

Service 0.761*** 0.767*** 0.761*** 0.758***

(0.0999) (0.0999) (0.100) (0.101)

HighTech 1.165*** 1.168*** 1.163*** 1.162***

(0.101) (0.101) (0.101) (0.102)

DealValue 0.132*** 0.131*** 0.129*** 0.127***

(0.0270) (0.0271) (0.0272) (0.0277)

MVacquirer -0.205*** -0.210*** -0.208*** -0.206***

(0.0260) (0.0262) (0.0263) (0.0270)

Subsidiary 1.557*** 1.553*** 1.538*** 1.545***

(0.249) (0.249) (0.246) (0.248)

Private 2.565*** 2.563*** 2.548*** 2.552***

(0.243) (0.243) (0.241) (0.241)

SameIND 0.157** 0.159** 0.161** 0.161**

(0.0800) (0.0800) (0.0800) (0.0800)

Toehold

-0.154 -0.152

(0.200) (0.200)

Stock

0.0333

(0.102)

EM

-0.421** -0.419** -0.426**

(0.213) (0.213) (0.215)

Big4 -0.136 -0.169 -0.170 -0.167

(0.113) (0.114) (0.114) (0.114)

ROA 0.108*** 0.0899** 0.0895** 0.0901**

(0.0416) (0.0397) (0.0400) (0.0402)

CorpGov -0.166 -0.192 -0.191 -0.190

(0.211) (0.213) (0.213) (0.213)

Constant -4.008*** -3.888*** -3.867*** -3.884***

(0.456) (0.462) (0.460) (0.467)

Year fixed effect Yes Yes Yes Yes

Observations 6,773 6,773 6,773 6,773 r2_p 0.118 0.119 0.119 0.119 chi2 477.7 480.8 479.8 479.9

p 0 0 0 0

35

Table 8: Propensity Score Matching

This table provides the results of the ATT procedure performed on our sample. The analisys is performed on the observations belonging to the region of common support, so to improve the quality of the matching. Standard errorrs are computed analytically. T-stats are reported with the associated significance level, with ***, **, and * indicating significance at the 1%, 5%, and 10% levels, respectively. Panel A shows results using as outcome variable the mean of the abnormal accrual measure in the four quarters preceding the deal. Panel B restricts the analysis to the two quarters preceding the deal, Panel C extends it to the six quarters preceding the deal.

Panel A Nr. Treated 1138

Nr. Controls 7942

ATT -0.005

Std. Err. 0.002

t-stat -3.331*** Panel A Nr. Treated 1138

Nr. Controls 7942

ATT -0.007

Std. Err. 0.002

t-stat -3.759*** Panel C Nr. Treated 1138

Nr. Controls 7522

ATT -0.004

Std. Err. 0.001

t-stat -2.922***

36

Table 9: Logit regression (EM measured over 4 quarters before the deal) Subsample of deals with acquisitions of at least 20% of the capital of the target firm

This table provides the result of logistic regressions of the use of earnouts on the average earnings management in the four quarters preceding the deal and other deal specific covariates. The dependent variable takes value 1 when the deal involves an earnout, and 0 in the opposite case. HighTech and Service are dummy variables that take value 1 if the target operates in the high tech or the service sector, respectively. DealValue is the log of the transaction price of the deal. MVacquirer is the log of the market value of the acquirer prior to the deal announcement. Subsidiary and Private are dummy variables that take value 1 if the target is a private company or a subsidiary, respectively. SameIND is a dummy variable that takes value 1 if bidder and target have the same two-digits SIC code. Toehold is a dummy variable that takes value 1 if the bidder holds a stake in the target before the acquisition. Stock is a dummy that takes value 1 if the upfront payment is at least partly in stocks. EM is the mean of the abnormal accrual measure in the four quarters preceding the deal. Big4 is a dummy variable that takes value 1 if the audit firm belongs to one of the big four. ROA is the ratio of net income over total assets. Robust standard errors are provided in parentheses with ***, **, and * indicating significance at the 1%, 5%, and 10% levels, respectively.

Model 1 Model 2 Model 3 Model 4

Service 0.602*** 0.598*** 0.600*** 0.577***

(0.0834) (0.0834) (0.0835) (0.0840)

HighTech 1.016*** 1.008*** 1.012*** 1.002***

(0.0856) (0.0858) (0.0861) (0.0862)

DealValue 0.0884*** 0.0886*** 0.0890*** 0.0756***

(0.0240) (0.0241) (0.0241) (0.0243)

MVacquirer -0.182*** -0.193*** -0.193*** -0.178***

(0.0220) (0.0227) (0.0227) (0.0233)

Subsidary 1.589*** 1.582*** 1.597*** 1.657***

(0.230) (0.230) (0.224) (0.226)

Private 2.514*** 2.509*** 2.525*** 2.556***

(0.226) (0.226) (0.220) (0.221)

SameIND 0.0854 0.0823 0.0808 0.0733

(0.0690) (0.0690) (0.0691) (0.0692)

Big4 0.0429 0.0109 0.0120 0.0450

(0.0952) (0.0951) (0.0951) (0.0962)

ROA 0.0891* 0.104** 0.104** 0.104**

(0.0496) (0.0430) (0.0430) (0.0450)

Toehold

0.154 0.167

(0.242) (0.243)

Stock

0.261***

(0.0845)

EM

-1.400*** -1.398** -1.540***

(0.543) (0.544) (0.551)

Constant -3.902*** -3.727*** -3.746*** -3.927***

(0.300) (0.310) (0.305) (0.315)

Year fixed effect Yes Yes Yes Yes Observations 8,830 8,830 8,830 8,830

r2_p 0.0969 0.0978 0.0978 0.0993 chi2 513.3 517.2 534.7 545.3

p 0 0 0 0

37

Table 10: Logit regression (EM measured over 4 quarters before the deal) Subsample of acquisition with ownership passing from less than 50% to at least 90%

This table provides the result of logistic regressions of the use of earnouts on the average earnings management in the four quarters preceding the deal and other deal specific covariates. The dependent variable takes value 1 when the deal involves an earnout, and 0 in the opposite case. HighTech and Service are dummy variables that take value 1 if the target operates in the high tech or the service sector, respectively. DealValue is the log of the transaction price of the deal. MVacquirer is the log of the market value of the acquirer prior to the deal announcement. Subsidiary and Private are dummy variables that take value 1 if the target is a private company or a subsidiary, respectively. SameIND is a dummy variable that takes value 1 if bidder and target have the same two-digits SIC code. Toehold is a dummy variable that takes value 1 if the bidder holds a stake in the target before the acquisition. Stock is a dummy that takes value 1 if the upfront payment is at least partly in stocks. EM is the mean of the abnormal accrual measure in the four quarters preceding the deal. Big4 is a dummy variable that takes value 1 if the audit firm belongs to one of the big four. ROA is the ratio of net income over total assets. Robust standard errors are provided in parentheses with ***, **, and * indicating significance at the 1%, 5%, and 10% levels, respectively.

Model 1 Model 2 Model 3 Model 4

Service 0.615*** 0.611*** 0.613*** 0.590***

(0.0854) (0.0854) (0.0855) (0.0860)

HighTech 1.028*** 1.021*** 1.023*** 1.013***

(0.0875) (0.0876) (0.0877) (0.0878)

DealValue 0.0800*** 0.0802*** 0.0800*** 0.0675***

(0.0244) (0.0245) (0.0245) (0.0246)

MVacquirer -0.178*** -0.188*** -0.188*** -0.174***

(0.0226) (0.0231) (0.0231) (0.0237)

Subsidary 1.857*** 1.851*** 1.862*** 1.927***

(0.273) (0.273) (0.272) (0.274)

Private 2.771*** 2.768*** 2.776*** 2.812***

(0.270) (0.270) (0.269) (0.270)

SameIND 0.0844 0.0821 0.0800 0.0730

(0.0703) (0.0703) (0.0703) (0.0703)

Big4 -0.00799 -0.0389 -0.0385 -0.00558

(0.0965) (0.0964) (0.0964) (0.0976)

ROA 0.142 0.159* 0.159* 0.165*

(0.133) (0.0848) (0.0849) (0.0912)

Toehold

0.286 0.284

(0.343) (0.346)

Stock

0.250***

(0.0861)

EM

-1.367** -1.365** -1.514***

(0.567) (0.568) (0.578)

Constant -4.078*** -3.910*** -3.922*** -4.103***

(0.340) (0.349) (0.348) (0.358)

Year fixed effect Yes Yes Yes Yes Observations 8,268 8,268 8,268 8,268

r2_p 0.0977 0.0985 0.0986 0.0999 chi2 495.7 501.2 506.8 516.8

p 0 0 0 0

38

APPENDIX A

SAMPLE EARNOUT AGREEMENT

(Bold added) This EARNOUT AGREEMENT (this “Agreement”) is entered into this 31st day of July, 2008 by and between

Orthodyne Electronics Corporation (“Orthodyne”) and Kulicke and Soffa Industries, Inc. (the “Company,” and together with Orthodyne, the “Parties”). The Parties are entering into this Agreement in connection with Orthodyne’s sale of the Purchased Assets to the Company, pursuant to an Asset Purchase Agreement, dated as of July 31, 2008, by and among Orthodyne and the Company (the “Purchase Agreement”). Capitalized terms used herein without definition shall have the meanings ascribed to such terms in the Purchase Agreement.

WHEREAS, as part of the transactions contemplated in the Purchase Agreement, Orthodyne shall be entitled to certain payments in addition to those set forth in the Purchase Agreement based upon the financial performance of the Business.

WHEREAS, Orthodyne and the Company have agreed that calculation and payment of such earnout amounts is to be made in accordance with the terms of this Agreement.

NOW, THEREFORE, in consideration of the premises and of the respective covenants and provisions contained herein, Orthodyne and the Company agree as follows: 1. Definitions.

“Additional Earnout” means, with respect to the three-year period following the Commencement Date, up to an aggregate of $10 million, the payment of which shall be made in cash based on the formula set forth on Exhibit A hereto.

“Base Earnout” means, with respect to each of the twelve-month periods ending on the first, second and third anniversary of the Commencement Date, up to an aggregate of $30 million, the payment of which shall be made in cash based on the formula set forth on Exhibit A hereto.

“Budgeted Gross Profit” means, for each Earnout Period, the amount set forth on Exhibit A. “Commencement Date” shall mean the Closing Date if the Closing Date coincides with the first day of a fiscal

quarter of the Company or, if the Closing Date does not coincide with the first day of a fiscal quarter of the Company, the Commencement Date shall be the first day of the fiscal quarter succeeding the Closing Date.

“Earnout Payment” means each payment made pursuant to Section 2(a) below on account of Base Earnout and Additional Earnout.

“Earnout Periods” means the twelve-month periods ending on the first, second and third anniversaries of the Commencement Date, respectively.

“Forecast” means the forecast provided by Orthodyne to the Company on which the Company’s valuation of the Business was based, which is set forth on Exhibit C.

“Gross Profit” shall have the meaning assigned to such term in Section 3(a). “Gross Profit Statement” shall have the meaning assigned to such term in Section 3(b)(i). “Independent Accounting Firm” shall have the meaning assigned to such term in Section 3(b)(ii). “Maximum Aggregate Earnout Amount” means $40 million. “Term” means the period commencing on the Commencement Date and ending on the third anniversary thereof.

2. Earnout Payment.

(a) Period for Payment. The Budgeted Gross Profit, Base Earnout and Additional Earnout for each of the Earnout Periods shall be as set forth on Exhibit A.

(b) Earnout Payment.

39

(i) For each Earnout Period during the Term, the Company shall, pursuant to Section 3, calculate the Gross Profit for such period and shall pay to Orthodyne the Base Earnout that corresponds to the amount of Gross Profit set forth in the Base Earnout table on Exhibit A with respect to such Earnout Period; provided that the Base Earnout for the first Earnout Period shall not exceed $10 million and the aggregate Base Earnout for the first and second Earnout Periods shall not exceed $20 million.

(ii) If the cumulative Gross Profit during the Term, as determined pursuant to Section 3, exceeds the Budgeted Gross Profit for the Term, the Company shall pay to Orthodyne the Additional Earnout attributable to such amount of Gross Profit set forth in the Additional Earnout table on Exhibit A.

(iii) The Earnout Payment with respect to each Earnout Period shall be paid to Orthodyne as soon as practicable after the amount of the Earnout Payment has been determined and any dispute with respect thereto has been settled pursuant to Section 3.

(iv) Orthodyne shall not be entitled to any interest on any payments under this Agreement. (v) For the sake of clarity, Exhibit A hereto sets forth examples of the application of this Section 2

to different amounts of Gross Profit. (c) Right of Setoff. The Company shall have the right to withhold and set off, against any amount due

Orthodyne hereunder, any amount owed by Orthodyne to the Company or the Company pursuant to any claim for indemnification or payment of damages to which the Company may be entitled under the Purchase Agreement or any other agreement entered into in connection with the transactions contemplated therein.