Embed Size (px)

DESCRIPTION

ppt presentation on short run & long runby saju thomas dit school of business (g.noida, up , india)

Citation preview

PRESENTED BY :-SAJU THOMAS

SARANSH ANAND

ROHAN SINGH

DIT SCHOOL OF BUSINESSPRESENTATION ON

SHORT RUN & LONG RUN COST CURVES

Cost:-Sum of the inputs may multiplied by their

respective prices and added together give the money value of the inputs, that is the cost of production.

TYPES OF COST

Opportunity and actual costExplicit and implicit costOut of pocket and book costFixed, variable and marginal cost Short term and long term costIncremental and sunk costHistorical cost and replacement costPrivate and social cost

Opportunity cost and actual costOpportunity cost –It may be defined as the

expected returns form the second best use of the resources which are forgone due to the scarcity of resources.

Actual cost –The total money expenses recording in the books of accounts.

Business cost and Full costBusiness cost –Business cost include all the

expenses which are incurred to carry out a business.

Full cost –It includes business cost ,opportunity and normal profit.

Explicit cost and Implicit costExplicit cost –Explicit cost are those cost

which fall under actual or business costs entered in the books of accounts.

Implicit cost –Implicit cost do not take the form of cash outlays

Out of pocket cost and Book costOut of pocket cost –The items of

expenditure which involve cash payments or cash transfer are known as out of pocket costs.

Book cost –Book cost which are entered in the books of accounts

Fixed cost and variable costFixed cost –Fixed cost are those which are

fixed in volume for a certain given output/scale of production.

Variable cost –Variable cost are those which vary according to the level of production.

Marginal cost –It is the addition to total cost due to the addition of one unit of output.

Short run cost –short run cost are those cost which vary according to the variation in output

Incremental cost -It arises due to change in scale of production, introduction of a new product and replacement of a worn out plant and machinery.

Sunk cost – sunk cost are those cost which can not be changed.

Historical cost –It includes all the past expenditure incurred for the production of goods and services.

Replacement cost –It refers to the outlay which has to be made for replacing an old asset.

Private cost –private cost are those which are incurred by an individual/firm on the purchase of goods and services from the market.

Private cost =explicit cost +implicit costSocial cost – it is the total cost borne by the

society due to production of a commodity.

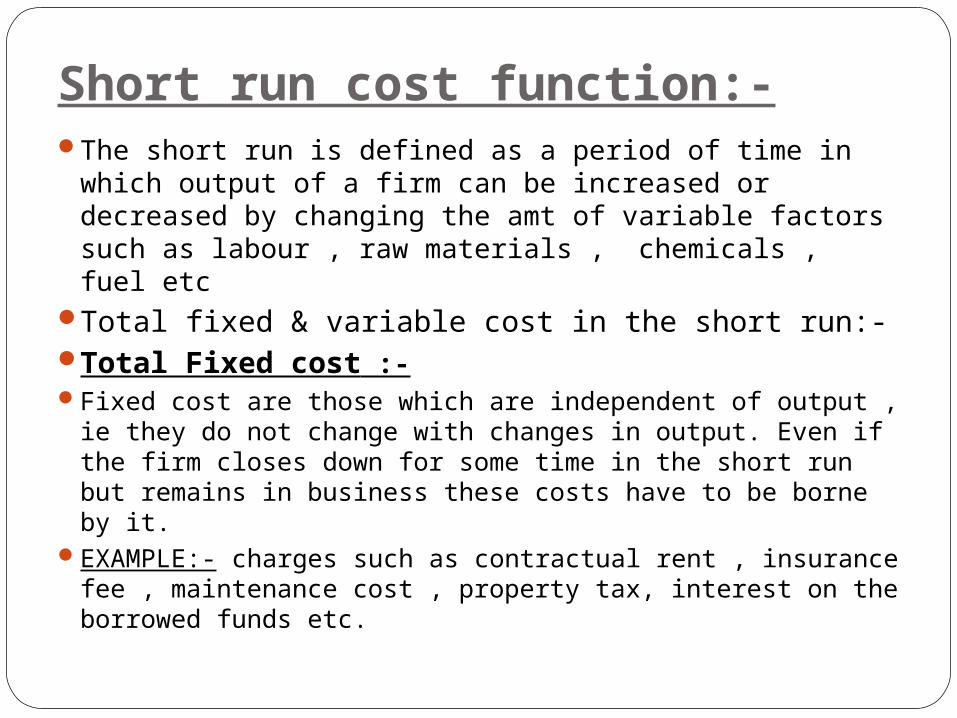

Short run cost function:-The short run is defined as a period of time in

which output of a firm can be increased or decreased by changing the amt of variable factors such as labour , raw materials , chemicals , fuel etc

Total fixed & variable cost in the short run:-Total Fixed cost :-Fixed cost are those which are independent of output ,

ie they do not change with changes in output. Even if the firm closes down for some time in the short run but remains in business these costs have to be borne by it.

EXAMPLE:- charges such as contractual rent , insurance fee , maintenance cost , property tax, interest on the borrowed funds etc.

Total Variable cost:-

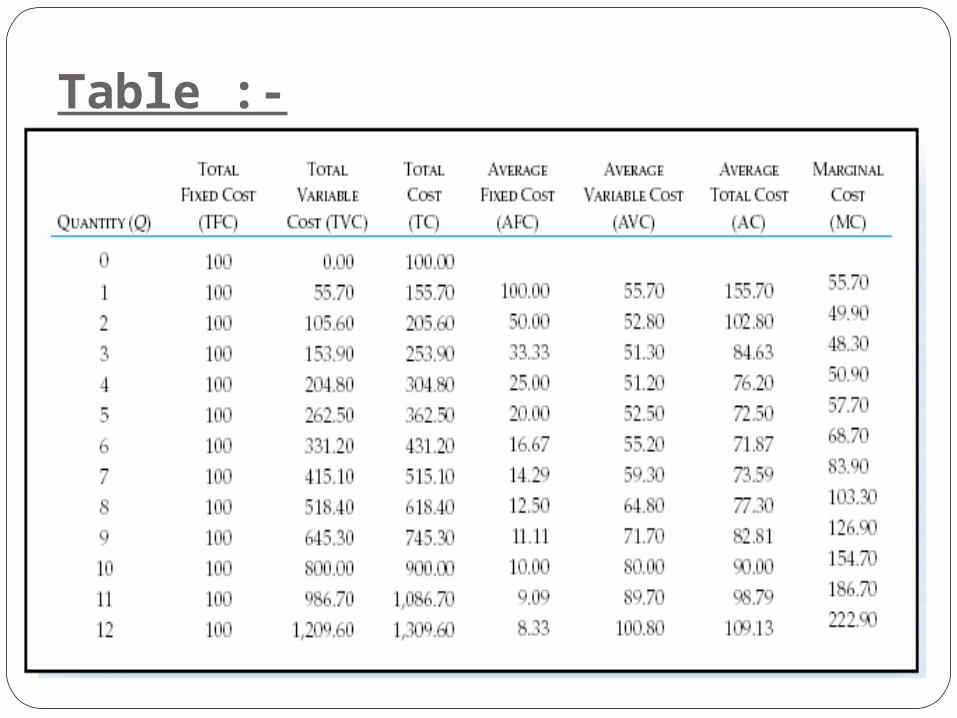

Table :-

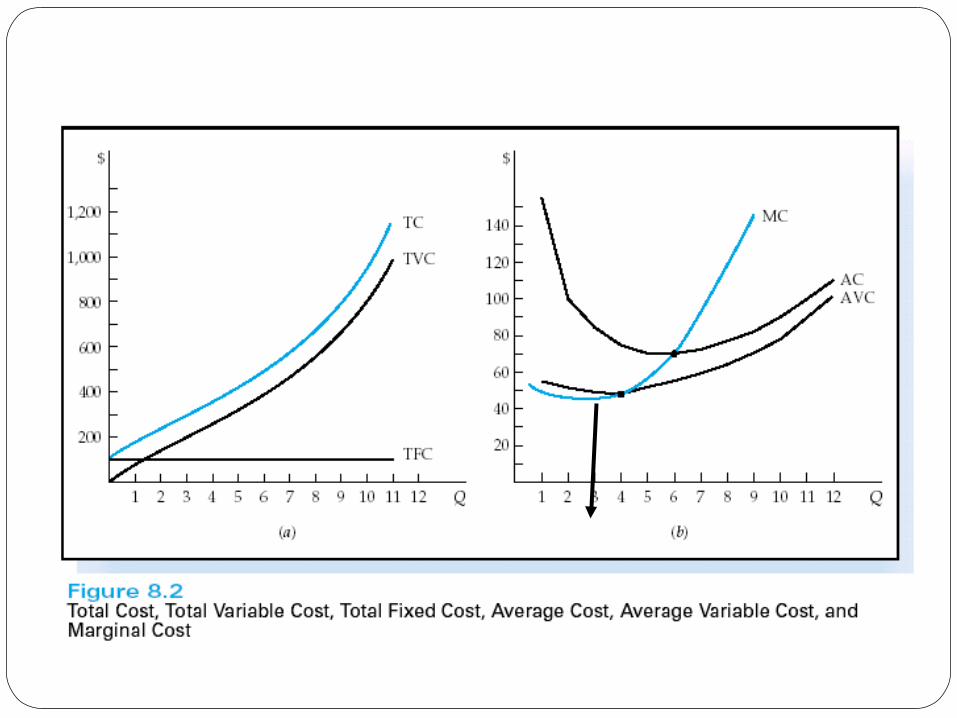

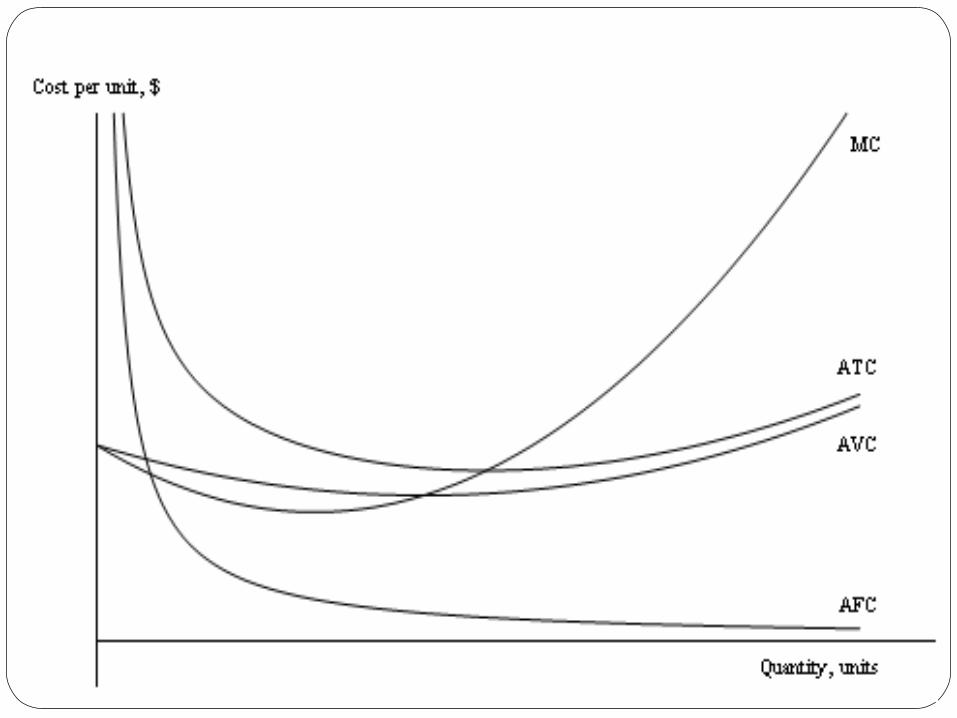

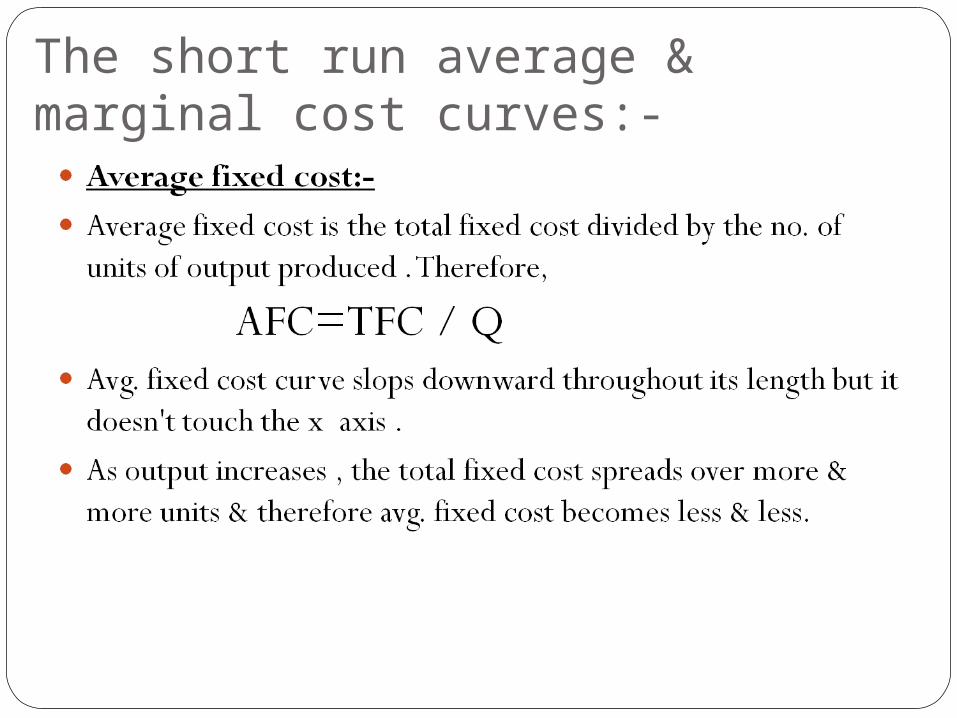

The short run average & marginal cost curves:-

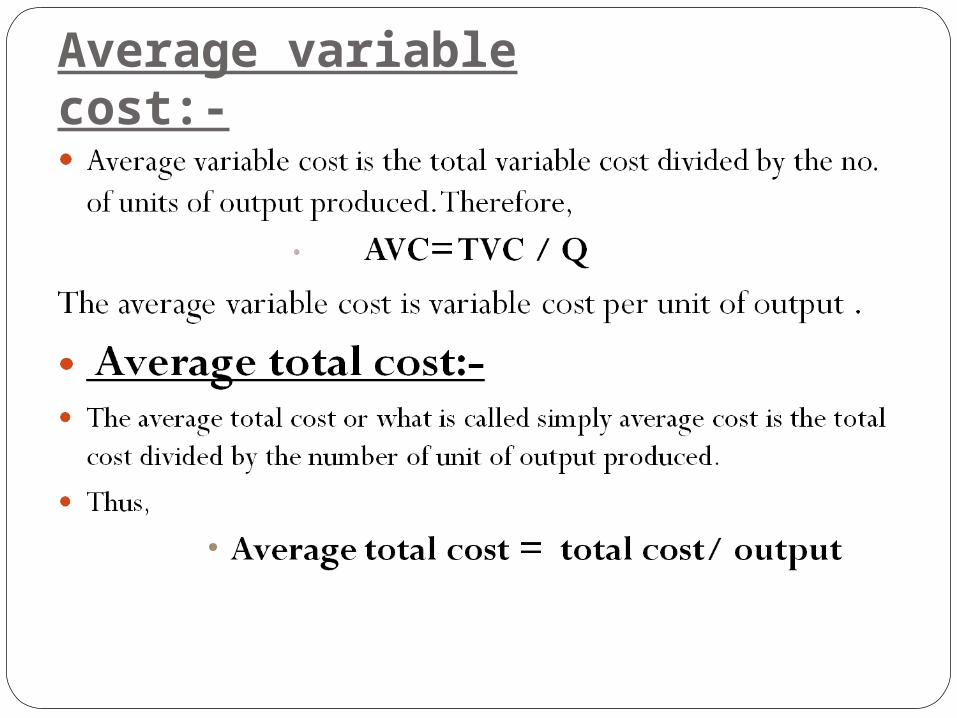

Average variable cost:-

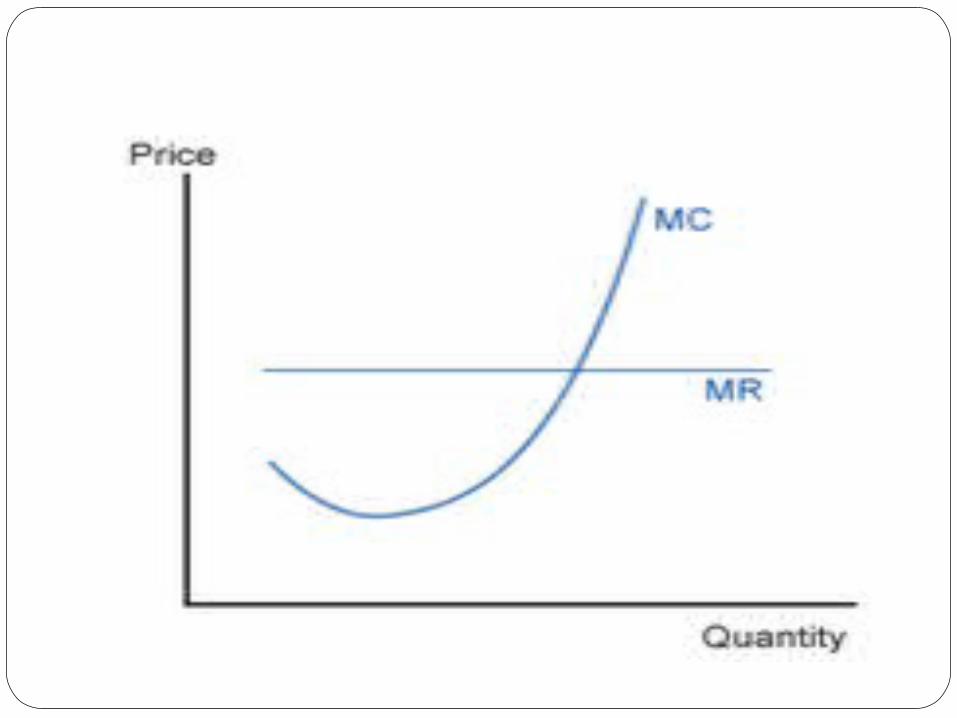

The marginal cost curve (MC)A marginal cost that graphically represents the relation

between marginal cost incurred by a firm in the short-run product of a good or service and the quantity of output produced. This curve is constructed to capture the relation between marginal cost and the level of output, holding other variables, like technology and resource prices, constant. The marginal cost curve is U-shaped. Marginal cost is relatively high at small quantities of output, then as production increases, declines, reaches a minimum value, then rises. The marginal cost is shown in relation to marginal revenue, the incremental amount of sales that an additional product or service will bring to the firm. This shape of the marginal cost curve is directly attributable to increasing, then decreasing marginal returns (and the law of diminishing marginal returns - Diminishing returns). Marginal cost equal w/MPL. For most production processes the marginal product of labor initially rises, reaches a maximum value and then continuously falls as production increases. Thus marginal cost initially falls, reaches a minimum value and then increases.

Theory of long run cost:-The long run refers to a time period during which

full adjustment to a change in environment can be made by the firm by varying all inputs , including capital equipment & factory building.

Long run avg. cost curve :-The long run as noted above is period of time during

which the firm can vary all its inputs. The long run production function has therefore no fixed factors & the firm has no fixed cost in the long run.

In the short run, some inputs are fixed & others are varied to increase the level of output .while in the long run none of the factors is fixed and all can be varied to expand output.

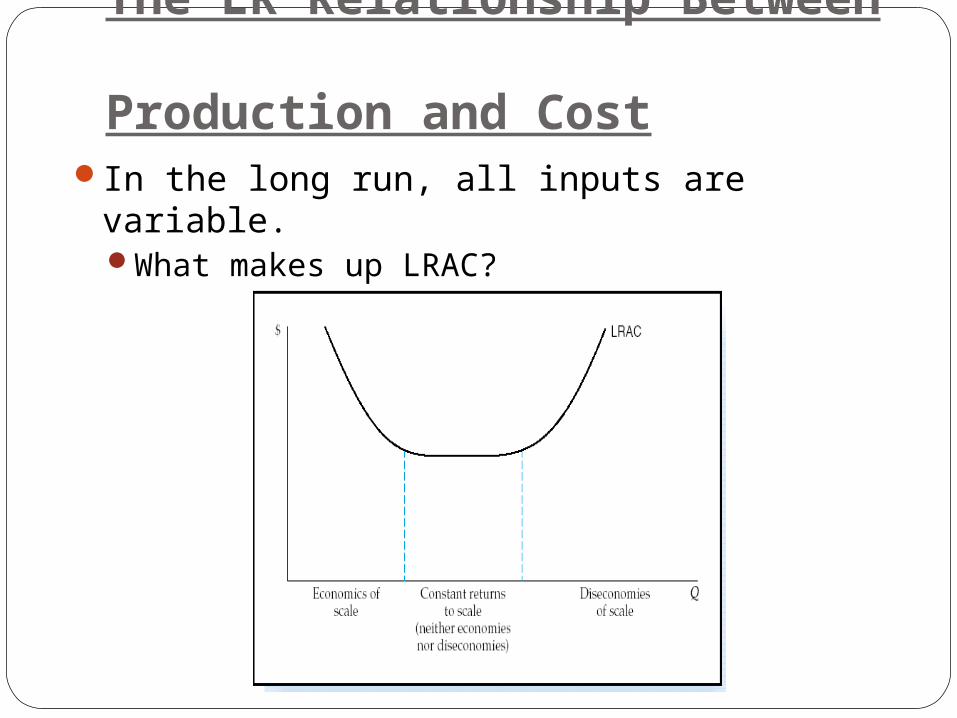

The LR Relationship Between

Production and CostIn the long run, all inputs are variable.

What makes up LRAC?

The Long-Run Cost Function :-

Reasons for Economies of Scale…

Use of technically efficient machineDivision of labourInvisibility & economies of scaleFinancial economyEconomies of scope.

The Long-Run Cost Function :-Reasons for Diseconomies of Scale…

Decreasing returns to scale Input market imperfections Management coordination and control

problems