Embed Size (px)

Citation preview

Annual Report 2011Shizuoka Bank Group

1

Shizuoka Bank Group at a Glance

ContentsShizuoka Bank Group at a Glance . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Consolidated Financial Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

To Our Stakeholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

Message from the President . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Our 11th Medium-Term Business Plan (FY2011-2013) . . . . . . . . . . . .5

Support for Overseas Market Entry and Business . . . . . . . . . . . . . . . .7

Business Performance in Fiscal 2010 . . . . . . . . . . . . . . . . . . . . . . . . .8

Results of Recent Achievement . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

Management Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11

Risk Management Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

Our Operational Base: Shizuoka Prefecture . . . . . . . . . . . . . . . . . . .15

Independent Auditors’ Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Consolidated Balance Sheets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Consolidated Statements of Income . . . . . . . . . . . . . . . . . . . . . . . . .19

Consolidated Statement of Comprehensive Income . . . . . . . . . . . . .19

Consolidated Statements of Changes in Equity . . . . . . . . . . . . . . . .20

Consolidated Statements of Cash Flows . . . . . . . . . . . . . . . . . . . . 21

Notes to Consolidated Financial Statements . . . . . . . . . . . . . . . . . .22

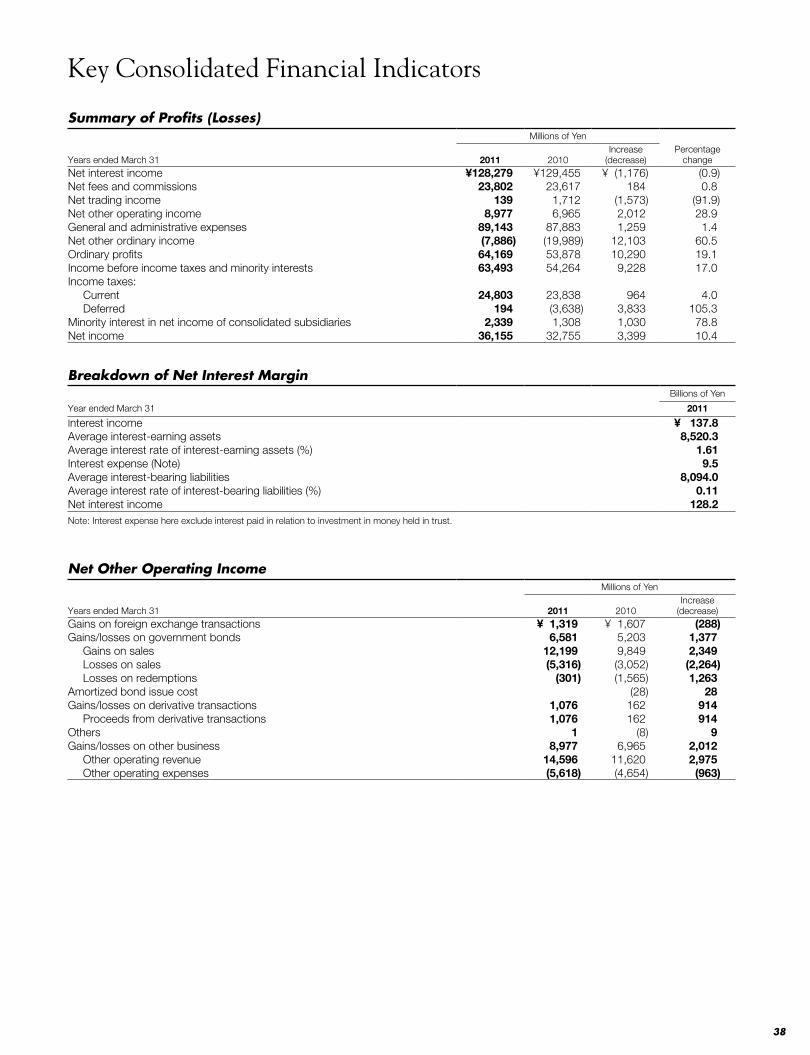

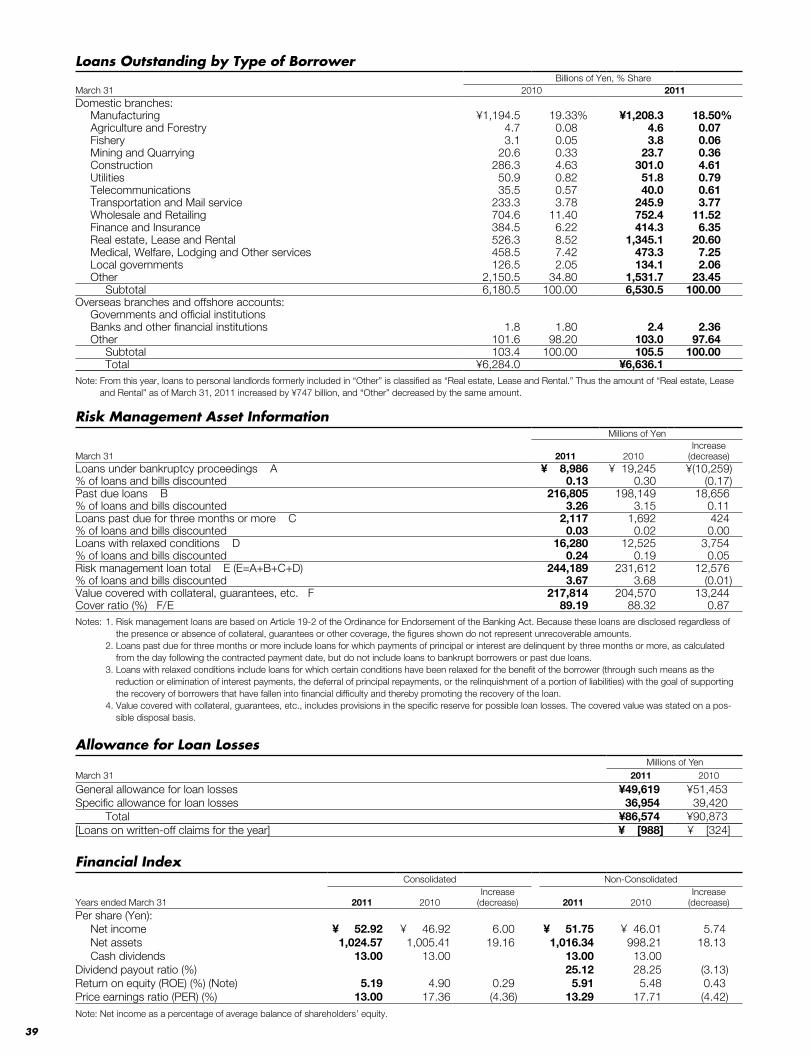

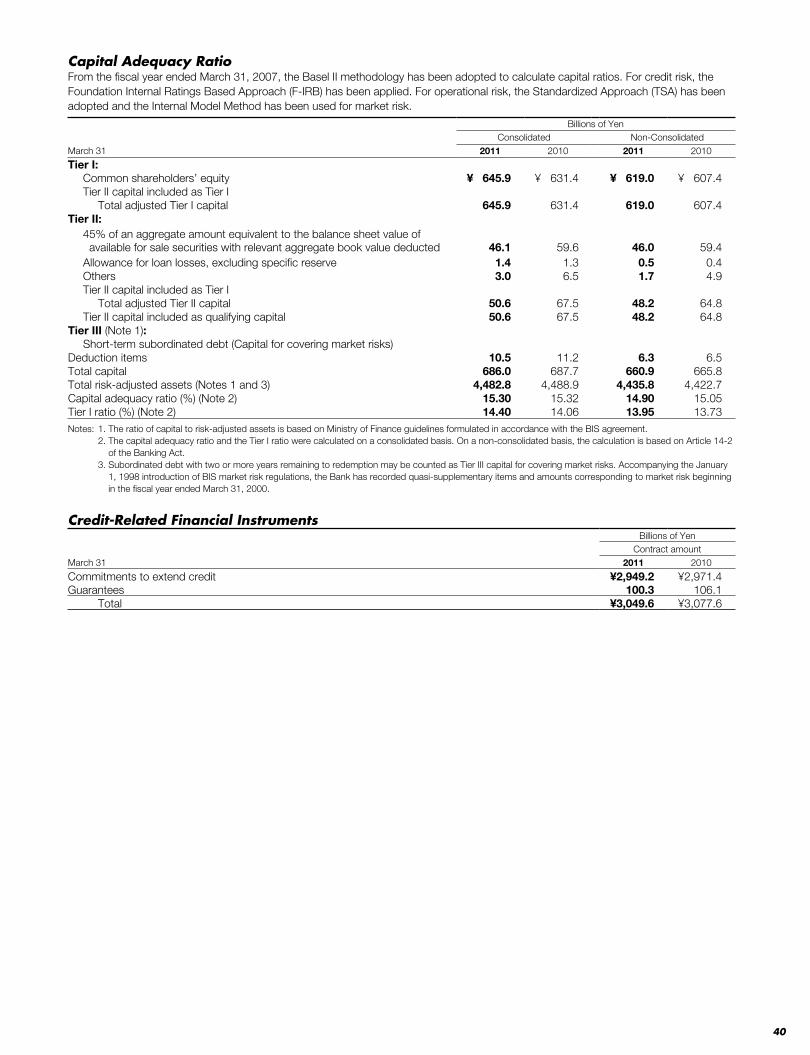

Key Consolidated Financial Indicators . . . . . . . . . . . . . . . . . . . . . . . .38

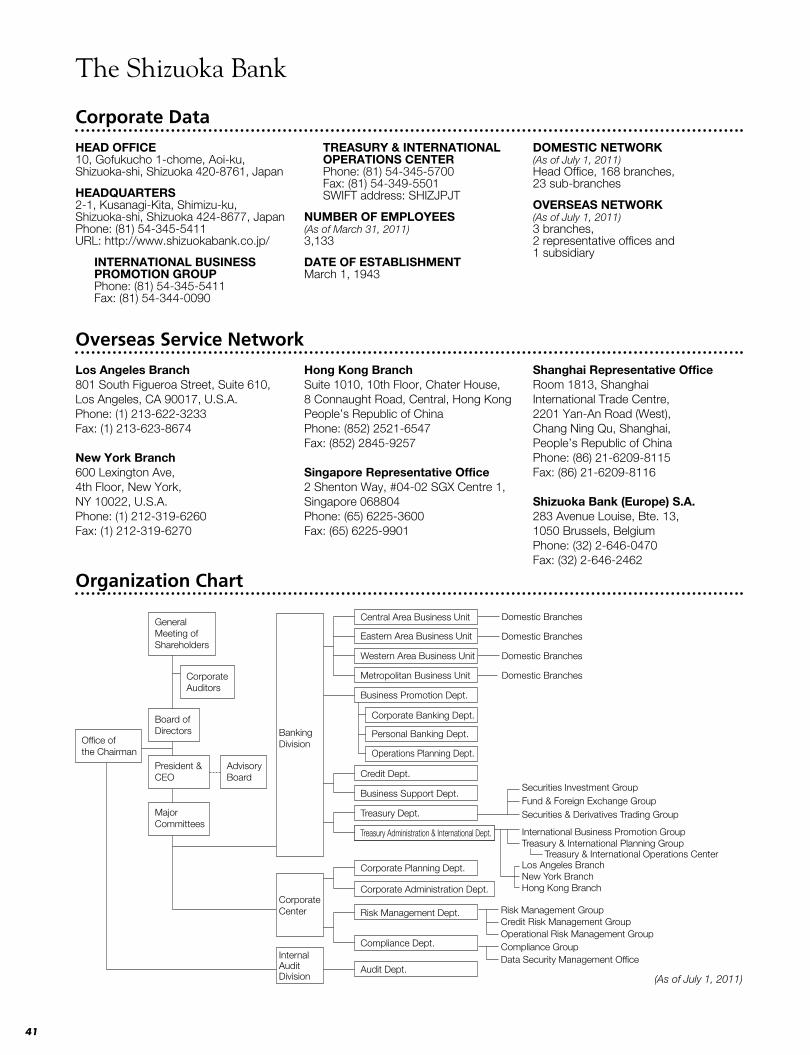

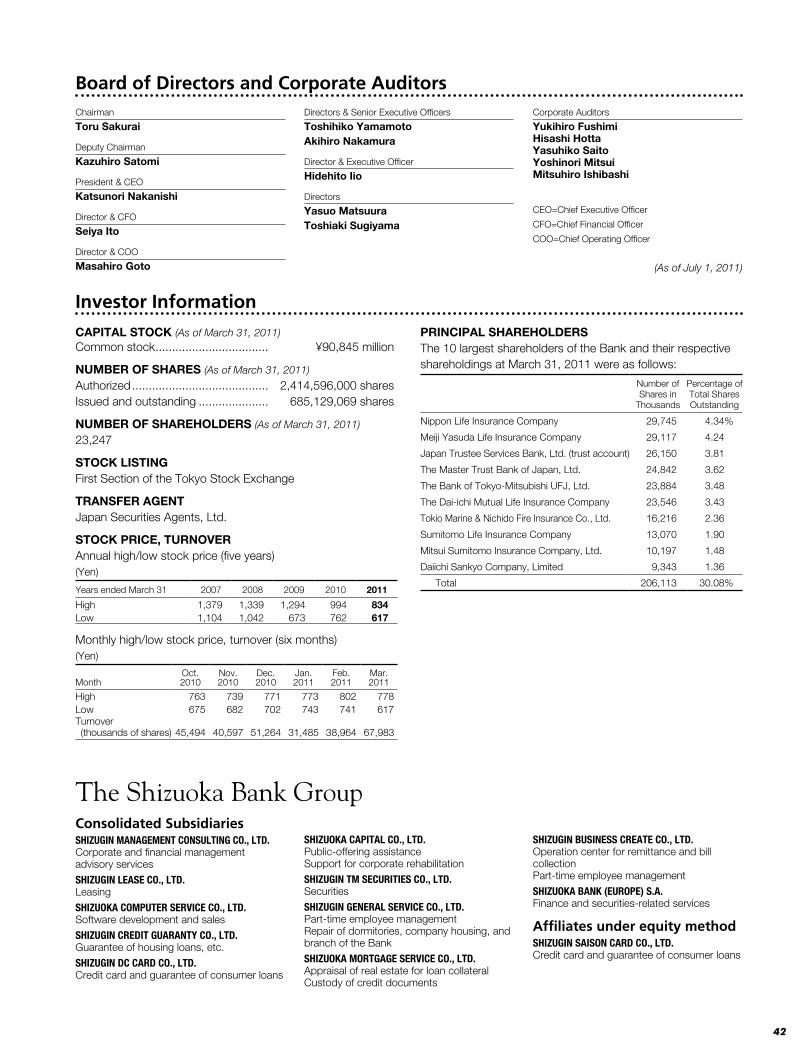

Corporate Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .41

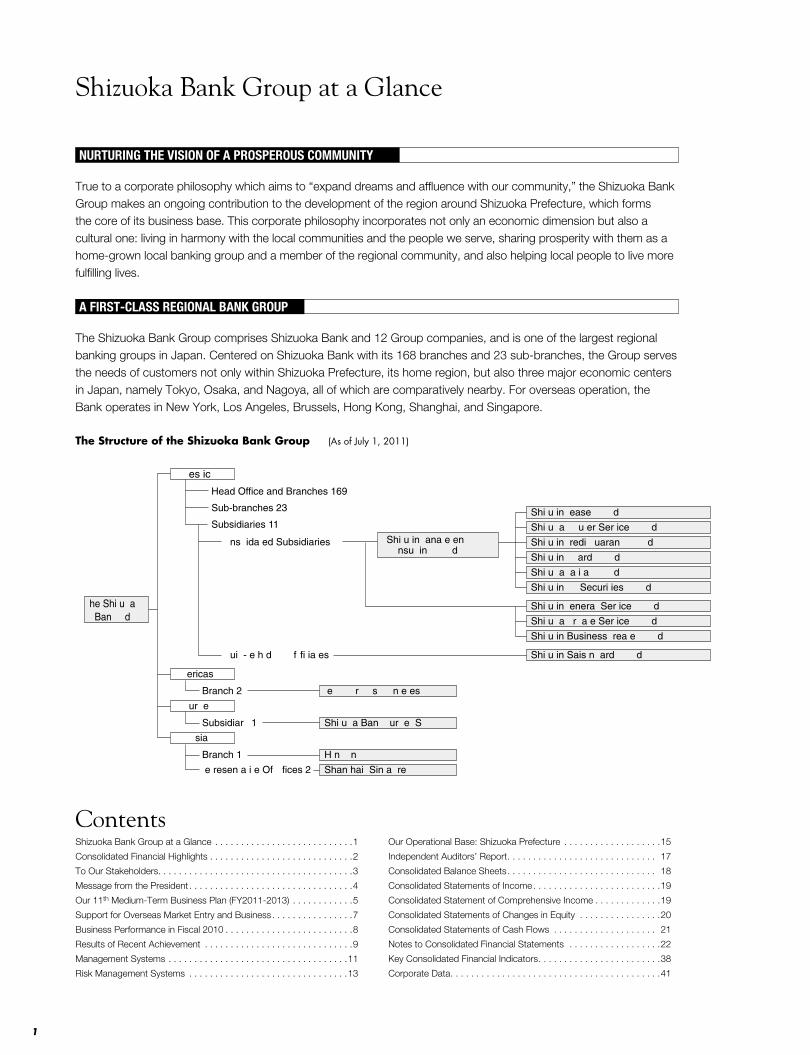

Head Office and Branches 169

Sub-branches 23

Subsidiaries 11

��ns��ida�ed Subsidiaries

��ui��-�e�h�d �f fi�ia�es

���es�ic

�he Shi�u��aBan�� ��d�

Shi�u�in �ease ���� ��d�

Shi�u��a ����u�er Ser�ice ���� ��d�

Shi�u�in �redi� �uaran�� ���� ��d�

Shi�u�in �� �ard ���� ��d�

Shi�u��a �a�i�a� ���� ��d�

Shi�u�in �� Securi�ies ���� ��d�

Shi�u�in �enera� Ser�ice ���� ��d�

Shi�u��a ��r��a�e Ser�ice ���� ��d�

Shi�u�in Business �rea�e ���� ��d�

��ericas

Shi�u�in �ana�e�en���nsu��in� ���� ��d�

Shi�u�in Sais�n �ard ���� ��d�

�e� � �r�� ��s �n�e�esBranch 2

Subsidiar� 1

Branch 1

�e�resen�a�i�e Of fices 2

�ur��e

�sia

Shi�u��a Ban� ��ur��e� S���

H�n� ��n�

Shan�hai� Sin�a��re

The Structure of the Shizuoka Bank Group (As of July 1, 2011)

NURTURING THE VISION OF A PROSPEROUS COMMUNITY

True to a corporate philosophy which aims to “expand dreams and affluence with our community,” the Shizuoka Bank Group makes an ongoing contribution to the development of the region around Shizuoka Prefecture, which forms the core of its business base . This corporate philosophy incorporates not only an economic dimension but also a cultural one: living in harmony with the local communities and the people we serve, sharing prosperity with them as a home-grown local banking group and a member of the regional community, and also helping local people to live more fulfilling lives .

A FIRST-CLASS REGIONAL BANK GROUP

The Shizuoka Bank Group comprises Shizuoka Bank and 12 Group companies, and is one of the largest regional banking groups in Japan . Centered on Shizuoka Bank with its 168 branches and 23 sub-branches, the Group serves the needs of customers not only within Shizuoka Prefecture, its home region, but also three major economic centers in Japan, namely Tokyo, Osaka, and Nagoya, all of which are comparatively nearby . For overseas operation, the Bank operates in New York, Los Angeles, Brussels, Hong Kong, Shanghai, and Singapore .

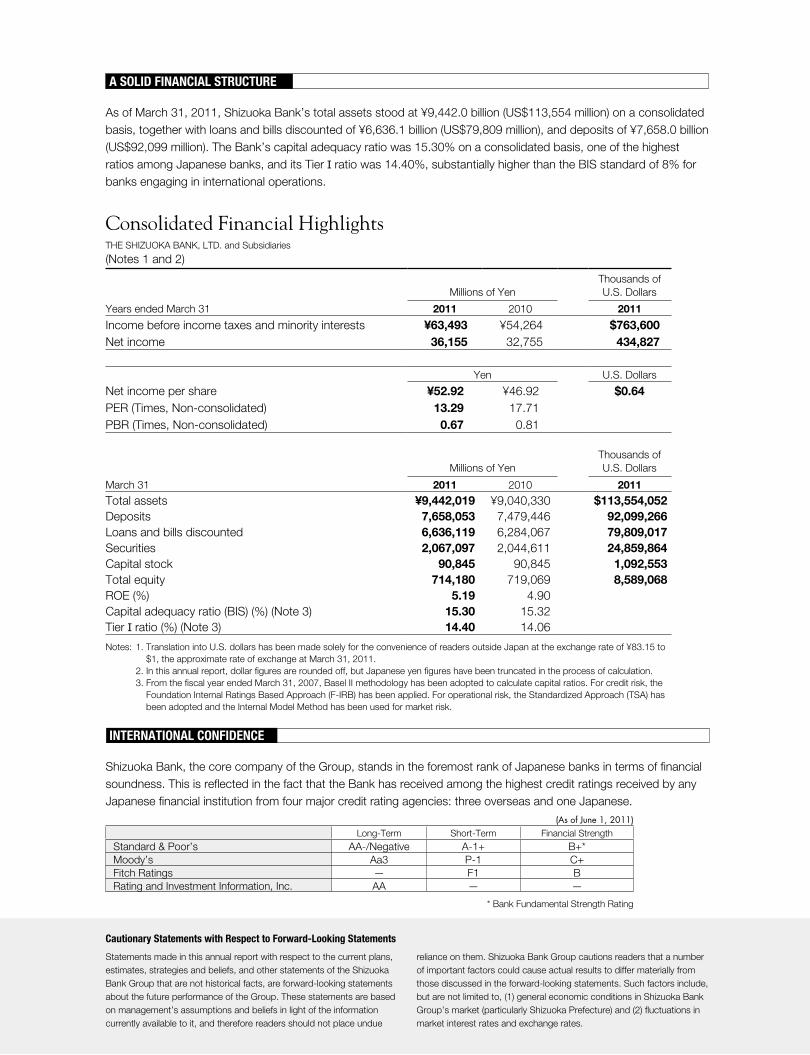

Consolidated Financial HighlightsTHE SHIZUOKA BANK, LTD. and Subsidiaries

(Notes 1 and 2)

Cautionary Statements with Respect to Forward-Looking Statements

Statements made in this annual report with respect to the current plans, estimates, strategies and beliefs, and other statements of the Shizuoka Bank Group that are not historical facts, are forward-looking statements about the future performance of the Group. These statements are based on management’s assumptions and beliefs in light of the information currently available to it, and therefore readers should not place undue

reliance on them. Shizuoka Bank Group cautions readers that a number of important factors could cause actual results to differ materially from those discussed in the forward-looking statements. Such factors include, but are not limited to, (1) general economic conditions in Shizuoka Bank Group’s market (particularly Shizuoka Prefecture) and (2) fluctuations in market interest rates and exchange rates.

A SOLID FINANCIAL STRUCTURE

As of March 31, 2011, Shizuoka Bank’s total assets stood at ¥9,442.0 billion (US$113,554 million) on a consolidated basis, together with loans and bills discounted of ¥6,636.1 billion (US$79,809 million), and deposits of ¥7,658.0 billion (US$92,099 million). The Bank’s capital adequacy ratio was 15.30% on a consolidated basis, one of the highest ratios among Japanese banks, and its Tier I ratio was 14.40%, substantially higher than the BIS standard of 8% for banks engaging in international operations.

Millions of YenThousands of U.S. Dollars

Years ended March 31 2011 2010 2011

Income before income taxes and minority interests ¥63,493 ¥54,264 $763,600 Net income 36,155 32,755 434,827

Yen U.S. Dollars

Net income per share ¥52.92 ¥46.92 $0.64 PER (Times, Non-consolidated) 13.29 17.71PBR (Times, Non-consolidated) 0.67 0.81

Millions of YenThousands of U.S. Dollars

March 31 2011 2010 2011

Total assets ¥9,442,019 ¥9,040,330 $113,554,052 Deposits 7,658,053 7,479,446 92,099,266 Loans and bills discounted 6,636,119 6,284,067 79,809,017 Securities 2,067,097 2,044,611 24,859,864 Capital stock 90,845 90,845 1,092,553 Total equity 714,180 719,069 8,589,068 ROE (%) 5.19 4.90Capital adequacy ratio (BIS) (%) (Note 3) 15.30 15.32Tier I ratio (%) (Note 3) 14.40 14.06

Notes: 1. Translation into U.S. dollars has been made solely for the convenience of readers outside Japan at the exchange rate of ¥83.15 to $1, the approximate rate of exchange at March 31, 2011.

2. In this annual report, dollar figures are rounded off, but Japanese yen figures have been truncated in the process of calculation. 3. From the fiscal year ended March 31, 2007, Basel II methodology has been adopted to calculate capital ratios. For credit risk, the

Foundation Internal Ratings Based Approach (F-IRB) has been applied. For operational risk, the Standardized Approach (TSA) has been adopted and the Internal Model Method has been used for market risk.

INTERNATIONAL CONFIDENCE

Shizuoka Bank, the core company of the Group, stands in the foremost rank of Japanese banks in terms of financial soundness. This is reflected in the fact that the Bank has received among the highest credit ratings received by any Japanese financial institution from four major credit rating agencies: three overseas and one Japanese.

(As of June 1, 2011)Long-Term Short-Term Financial Strength

Standard & Poor’s AA-/Negative A-1+ B+*Moody’s Aa3 P-1 C+Fitch Ratings — F1 BRating and Investment Information, Inc. AA — —

* Bank Fundamental Strength Rating

To Our Stakeholders

Thank you for your continued patronage of the Shizuoka

Bank Group.

Please allow us to extend our deepest sympathies to

everyone who has been affected by the Great East

Japan Earthquake of March 2011. The Great East

Japan Earthquake caused untold damage to stricken

areas and has cast a dark shadow over the future of

Japan’s economy with its shattering impact, which

disrupted the nation’s supply chain and forced con-

sumption to plunge.

The Shizuoka Bank Group, above all, stresses the

importance of interacting with customers and respond-

ing sincerely to all inquires and requests. As a regional

financial institution, the Group fulfills its mission by

supporting the regional economy through the smooth

supply of funds.

In April 2011, the Shizuoka Bank Group embarked

on its 11th medium-term business plan “MIRAI—

FUTURE” under the vision of “A comprehensive financial

group that goes along with customers to open up a

future with the region – Challenge for the Future.” As a

comprehensive financial group, under this new medium-

term business plan, we will continue to further meet the

expectations of all of our stakeholders including custom-

ers, the local community, shareholders, and employees.

We hope that our shareholders and other stakehold-

ers will continue to favor us with their support and

encouragement in the future.

September 2011

Toru Sakurai

Chairman

Katsunori Nakanishi

President & Chief Executive Officer

Toru Sakurai, Katsunori Nakanishi, Chairman President & Chief Executive Officer

3

Business Creation that Enhances our GrowthIn fiscal 2010, the final year of our 10th three-year medium-term business plan “Dream TEN – New Challenges,” we made a concerted effort to achieve our vision of “Nurturing the dreams of everyone in the region and growing as a comprehensive financial group.” In addition, to create business that enhances our growth, we pursued our three basic strate-gies of: 1) establishing the solid operational base required to achieve sustained growth in tandem with the region, 2) achiev-ing a group management capable of high productivity and 3) establishing the “Shizugin” brand. Under our fundamental principle of “growing our dreams and prosperity together with the region,” we worked hard to provide financial services that contribute to the development of the region’s economy, indus-try, society, and culture to fulfill our social responsibility and public mission as a Bank. In the area of corporate banking, we promoted regional finance, the Shizuoka Bank Group’s specialty, based on the three core pillars, 1) “business match-ing,” which supports our customer’s business expansion by increasing their sales channels, 2) “Shizuginship,” our learning and networking opportunity for younger managers, who will contribute to for the community’s future, and 3) “support for management improvement and business revitalization” to stabilize the region’s economy. As a result, in fiscal 2010, we achieved a loan market share of 30% in Shizuoka Prefecture, which was one of the targets in our 10th medium-term business plan, and we recorded our second consecutive year increase in both ordinary profit and net income. I want to express my sincere appreciation for our custom-ers and shareholders because the results in 2010 were due entirely to their support.

Seeking Further Increase in Corporate ValueSeeking to have a management that is supported by all of its shareholders, the Bank twice repurchased and cancelled 20 million shares of treasury stock in fiscal 2010. In line with our basic policy of maintaining a dividend payout ratio of 25% and one of the highest dividends paid among major regional banks, we paid an annual dividend of ¥13 per share as a token of our appreciation to shareholders for their recent sup-port. Based on the stock buyback and dividend payout, we achieved shareholder returns (combined amount of treasury stock repurchased and dividend paid) of ¥23.8 billion and a shareholder return ratio of 67.22% in fiscal 2010. In fiscal 2011 as well, by June we had already repurchased 20 million shares of treasury stock and we will take steps to raise corporate value through appropriate capital policies to win our shareholders’ and the market’s trust.

11th Medium-Term Business PlanIn April 2011, we began our 11th medium-term business plan, “MIRAI—Future,” which seeks to make the best use of the business foundation established in the 10th medium-term business plan and embarked on a new stage of growth. The plan sets out to fulfill the Bank’s vision of becoming “A comprehensive financial group that goes along with customers to open up a future with the region” by promoting balance between its three basic strategies: 1) grow through innova-tion and problem-solving ability, 2) build a robust operating structure with high productivity, and 3) increase the value of the Shizugin brand. We established the following declaration of action that expresses how we should act in order to fulfill our vision, “We always try to be the best partner for customers, so that we can contribute to regional development and growth for the future.” Most importantly, the Bank, a regional financial institution, is in the service industry and cannot survive without winning the trust of its customers. Let us once again return to these roots and under this declaration of action become “the Shizugin Bank Group, advancing together with the region” and fostering a greater sense of unity with the regional community.

Taking on the Challenge of Growing TogetherIn the environment surrounding the Bank, amid the urgent tasks of recovery and reconstruction in the aftermath of the Great East Japan Earthquake, structural changes, such as an aging population with declining birthrate, are taking place in a wide range of social domains. In addition to political disarray, we now stand at a time in which we can no longer see a bright future. Nevertheless, it is precisely at times like these that we must face difficulties with courage and believe that there are endless options for everything. That we persist in our efforts to open up new possibilities is more important than anything. To deal with the structural changes of the regional commu-nity, the Shizuoka Bank has already formed business alliances with banks in Thailand, Indonesia, and Vietnam and has strengthened its support system for regional companies enter-ing the Asian market. Moreover, we have started a “growth area support project,” which supports efforts in new fields that have a bearing on the region’s economic future, such as medicine, nursing care, the environment, and agriculture. The Bank will continue to take on bold challenges to grow with the region and with its customers over the next 10 to 20 years and beyond under its new medium-term business plan. We look forward to your continued support.

Message from the PresidentA comprehensive financial group that goes along with customers to open up a future with the region — Challenge for the future

4

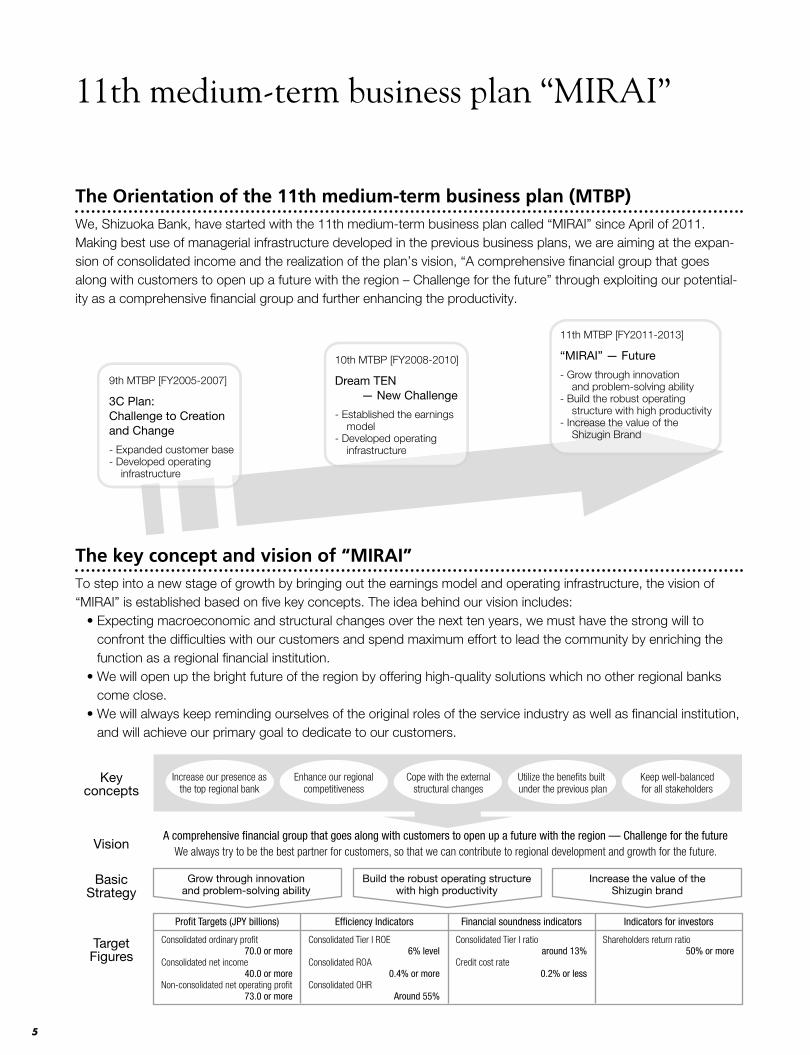

11th medium-term business plan “MIRAI”

The Orientation of the 11th medium-term business plan (MTBP)We, Shizuoka Bank, have started with the 11th medium-term business plan called “MIRAI” since April of 2011. Making best use of managerial infrastructure developed in the previous business plans, we are aiming at the expan-sion of consolidated income and the realization of the plan’s vision, “A comprehensive financial group that goes along with customers to open up a future with the region – Challenge for the future” through exploiting our potential-ity as a comprehensive financial group and further enhancing the productivity.

The key concept and vision of “MIRAI”To step into a new stage of growth by bringing out the earnings model and operating infrastructure, the vision of “MIRAI” is established based on five key concepts. The idea behind our vision includes:

• Expecting macroeconomic and structural changes over the next ten years, we must have the strong will to confront the difficulties with our customers and spend maximum effort to lead the community by enriching the function as a regional financial institution.

• We will open up the bright future of the region by offering high-quality solutions which no other regional banks come close.

• We will always keep reminding ourselves of the original roles of the service industry as well as financial institution, and will achieve our primary goal to dedicate to our customers.

9th MTBP [FY2005-2007]

3C Plan:Challenge to Creationand Change

- Expanded customer base- Developed operating infrastructure

10th MTBP [FY2008-2010]

Dream TEN — New Challenge

- Established the earnings model- Developed operating infrastructure

11th MTBP [FY2011-2013]

“MIRAI” — Future

- Grow through innovation and problem-solving ability- Build the robust operating structure with high productivity- Increase the value of the Shizugin Brand

Keyconcepts

Vision

BasicStrategy

TargetFigures

Increase our presence asthe top regional bank

Grow through innovationand problem-solving ability

Consolidated ordinary prot 70.0 or moreConsolidated net income 40.0 or moreNon-consolidated net operating prot 73.0 or more

Consolidated Tier I ROE 6% levelConsolidated ROA 0.4% or moreConsolidated OHR Around 55%

Consolidated Tier I ratio around 13%Credit cost rate 0.2% or less

Shareholders return ratio 50% or more

Pro�t Targets (JPY billions) Indicators for investorsFinancial soundness indicatorsEf�ciency Indicators

Build the robust operating structurewith high productivity

Increase the value of theShizugin brand

A comprehensive �nancial group that goes along with customers to open up a future with the region — Challenge for the futureWe always try to be the best partner for customers, so that we can contribute to regional development and growth for the future.

Enhance our regionalcompetitiveness

Keep well-balancedfor all stakeholders

Utilize the benets built under the previous plan

Cope with the externalstructural changes

5

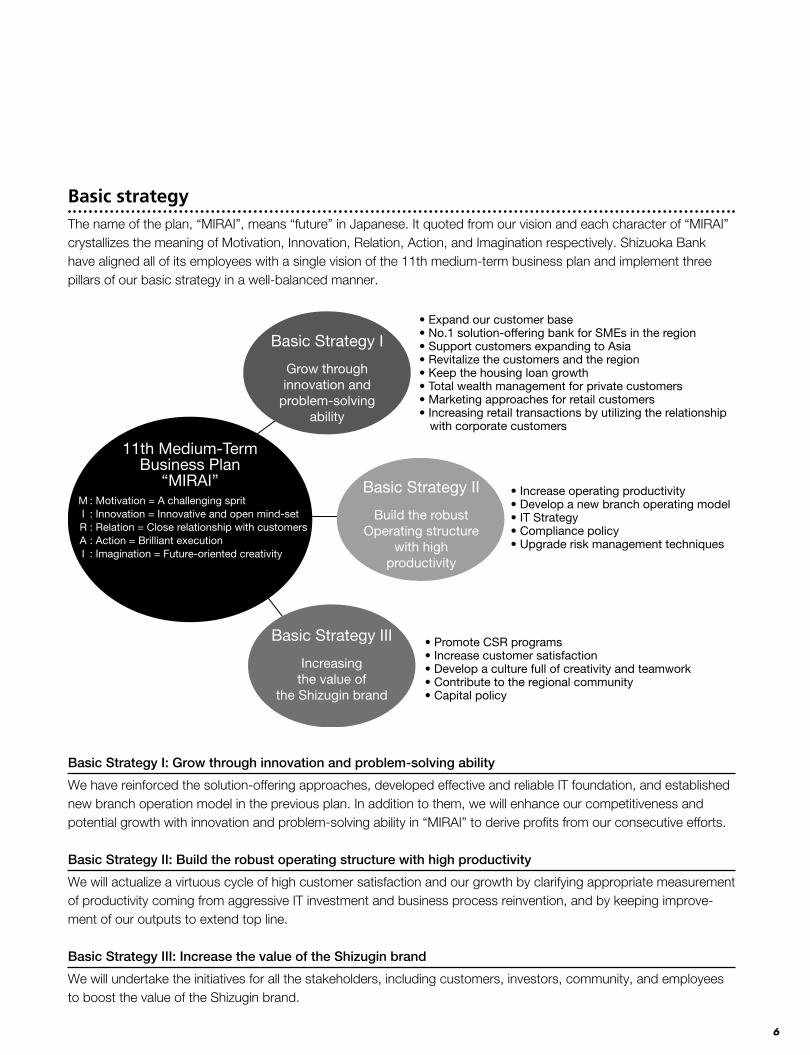

Basic strategyThe name of the plan, “MIRAI”, means “future” in Japanese. It quoted from our vision and each character of “MIRAI” crystallizes the meaning of Motivation, Innovation, Relation, Action, and Imagination respectively. Shizuoka Bank have aligned all of its employees with a single vision of the 11th medium-term business plan and implement three pillars of our basic strategy in a well-balanced manner.

Basic Strategy I: Grow through innovation and problem-solving ability

We have reinforced the solution-offering approaches, developed effective and reliable IT foundation, and established new branch operation model in the previous plan. In addition to them, we will enhance our competitiveness and potential growth with innovation and problem-solving ability in “MIRAI” to derive profits from our consecutive efforts.

Basic Strategy II: Build the robust operating structure with high productivity

We will actualize a virtuous cycle of high customer satisfaction and our growth by clarifying appropriate measurement of productivity coming from aggressive IT investment and business process reinvention, and by keeping improve-ment of our outputs to extend top line.

Basic Strategy III: Increase the value of the Shizugin brand

We will undertake the initiatives for all the stakeholders, including customers, investors, community, and employees to boost the value of the Shizugin brand.

11th Medium-TermBusiness Plan

“MIRAI”

Basic Strategy I

Grow throughinnovation and

problem-solvingability

Basic Strategy II

Build the robustOperating structure

with highproductivity

Basic Strategy III

Increasingthe value of

the Shizugin brand

M : Motivation = A challenging sprit I : Innovation = Innovative and open mind-set R : Relation = Close relationship with customers A : Action = Brilliant execution I : Imagination = Future-oriented creativity

• Expand our customer base• No.1 solution-offering bank for SMEs in the region• Support customers expanding to Asia• Revitalize the customers and the region• Keep the housing loan growth• Total wealth management for private customers• Marketing approaches for retail customers• Increasing retail transactions by utilizing the relationship

with corporate customers

• Increase operating productivity• Develop a new branch operating model• IT Strategy• Compliance policy• Upgrade risk management techniques

• Promote CSR programs• Increase customer satisfaction• Develop a culture full of creativity and teamwork• Contribute to the regional community• Capital policy

6

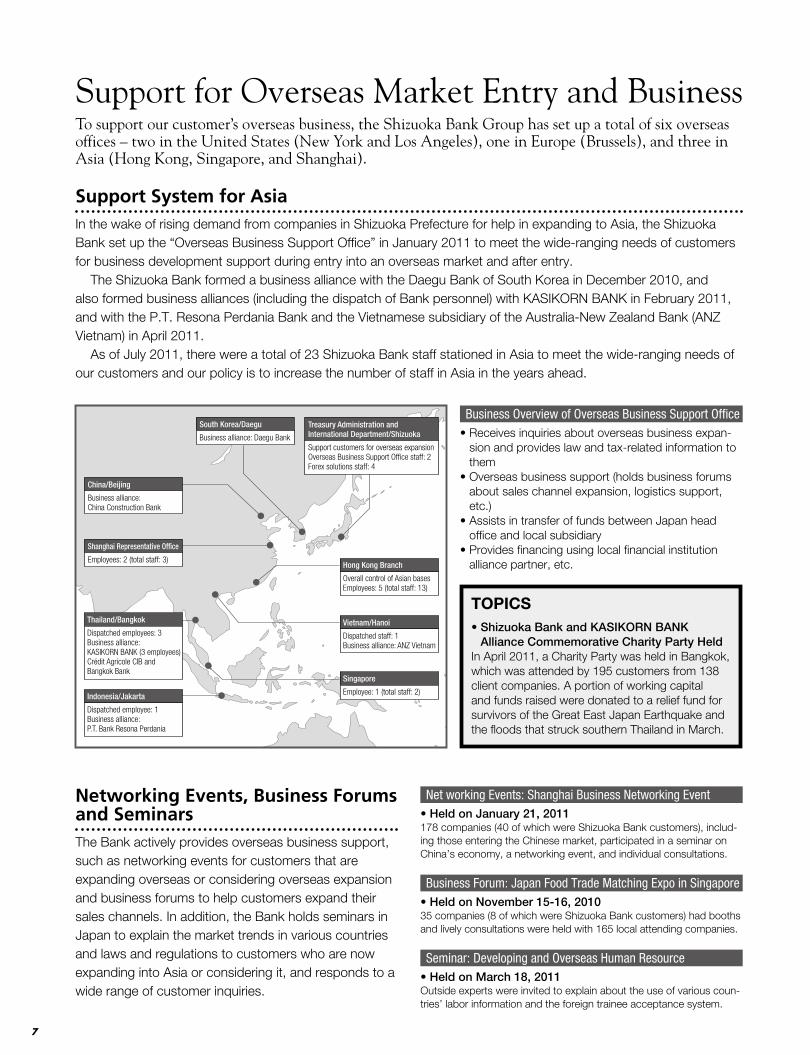

Support for Overseas Market Entry and BusinessTo support our customer’s overseas business, the Shizuoka Bank Group has set up a total of six overseas offices – two in the United States (New York and Los Angeles), one in Europe (Brussels), and three in Asia (Hong Kong, Singapore, and Shanghai).

Support System for AsiaIn the wake of rising demand from companies in Shizuoka Prefecture for help in expanding to Asia, the Shizuoka Bank set up the “Overseas Business Support Office” in January 2011 to meet the wide-ranging needs of customers for business development support during entry into an overseas market and after entry. The Shizuoka Bank formed a business alliance with the Daegu Bank of South Korea in December 2010, and also formed business alliances (including the dispatch of Bank personnel) with KASIKORN BANK in February 2011, and with the P.T. Resona Perdania Bank and the Vietnamese subsidiary of the Australia-New Zealand Bank (ANZ Vietnam) in April 2011. As of July 2011, there were a total of 23 Shizuoka Bank staff stationed in Asia to meet the wide-ranging needs of our customers and our policy is to increase the number of staff in Asia in the years ahead.

Networking Events, Business Forums and SeminarsThe Bank actively provides overseas business support, such as networking events for customers that are expanding overseas or considering overseas expansion and business forums to help customers expand their sales channels. In addition, the Bank holds seminars in Japan to explain the market trends in various countries and laws and regulations to customers who are now expanding into Asia or considering it, and responds to a wide range of customer inquiries.

Net working Events: Shanghai Business Networking Event• Held on January 21, 2011178 companies (40 of which were Shizuoka Bank customers), includ-ing those entering the Chinese market, participated in a seminar on China’s economy, a networking event, and individual consultations.

Business Forum: Japan Food Trade Matching Expo in Singapore• Held on November 15-16, 201035 companies (8 of which were Shizuoka Bank customers) had booths and lively consultations were held with 165 local attending companies.

Seminar: Developing and Overseas Human Resource• Held on March 18, 2011Outside experts were invited to explain about the use of various coun-tries’ labor information and the foreign trainee acceptance system.

Business Overview of Overseas Business Support Office• Receives inquiries about overseas business expan-

sion and provides law and tax-related information to them

• Overseas business support (holds business forums about sales channel expansion, logistics support, etc.)

• Assists in transfer of funds between Japan head office and local subsidiary

• Provides financing using local financial institution alliance partner, etc.

TOPICS• Shizuoka Bank and KASIKORN BANK

Alliance Commemorative Charity Party HeldIn April 2011, a Charity Party was held in Bangkok, which was attended by 195 customers from 138 client companies. A portion of working capital and funds raised were donated to a relief fund for survivors of the Great East Japan Earthquake and the floods that struck southern Thailand in March.

China/Beijing

Business alliance:China Construction Bank

Shanghai Representative Of�ce

Employees: 2 (total staff: 3)

Thailand/Bangkok

Dispatched employees: 3Business alliance: KASIKORN BANK (3 employees)Crédit Agricole CIB and Bangkok Bank

Indonesia/Jakarta

Dispatched employee: 1Business alliance: P.T. Bank Resona Perdania

South Korea/Daegu

Business alliance: Daegu Bank

Treasury Administration andInternational Department/Shizuoka

Support customers for overseas expansionOverseas Business Support Of�ce staff: 2Forex solutions staff: 4

Hong Kong Branch

Overall control of Asian basesEmployees: 5 (total staff: 13)

Vietnam/Hanoi

Dispatched staff: 1 Business alliance: ANZ Vietnam

Singapore

Employee: 1 (total staff: 2)

7

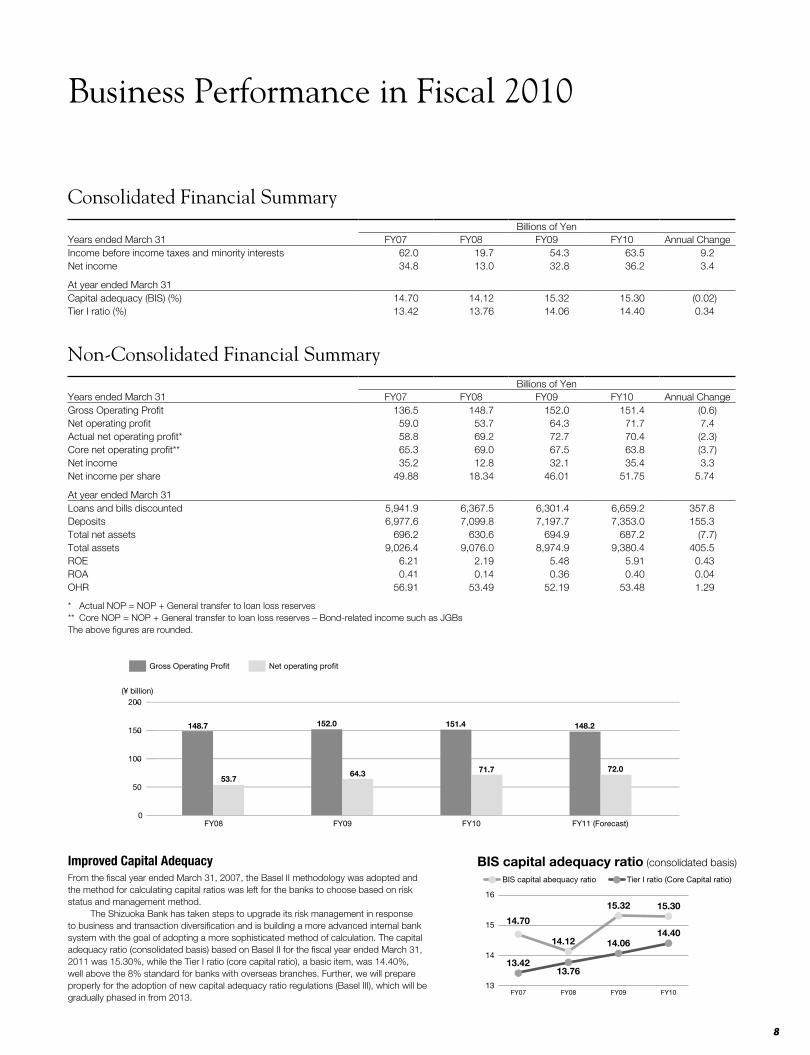

Business Performance in Fiscal 2010

Consolidated Financial SummaryBillions of Yen

Years ended March 31 FY07 FY08 FY09 FY10 Annual ChangeIncome before income taxes and minority interests 62.0 19.7 54.3 63.5 9.2Net income 34.8 13.0 32.8 36.2 3.4

At year ended March 31Capital adequacy (BIS) (%) 14.70 14.12 15.32 15.30 (0.02)Tier I ratio (%) 13.42 13.76 14.06 14.40 0.34

Non-Consolidated Financial SummaryBillions of Yen

Years ended March 31 FY07 FY08 FY09 FY10 Annual ChangeGross Operating Profit 136.5 148.7 152.0 151.4 (0.6)Net operating profit 59.0 53.7 64.3 71.7 7.4Actual net operating profit* 58.8 69.2 72.7 70.4 (2.3)Core net operating profit** 65.3 69.0 67.5 63.8 (3.7)Net income 35.2 12.8 32.1 35.4 3.3Net income per share 49.88 18.34 46.01 51.75 5.74

At year ended March 31Loans and bills discounted 5,941.9 6,367.5 6,301.4 6,659.2 357.8Deposits 6,977.6 7,099.8 7,197.7 7,353.0 155.3Total net assets 696.2 630.6 694.9 687.2 (7.7)Total assets 9,026.4 9,076.0 8,974.9 9,380.4 405.5ROE 6.21 2.19 5.48 5.91 0.43ROA 0.41 0.14 0.36 0.40 0.04OHR 56.91 53.49 52.19 53.48 1.29

* Actual NOP = NOP + General transfer to loan loss reserves** Core NOP = NOP + General transfer to loan loss reserves – Bond-related income such as JGBsThe above figures are rounded.

13

14

15

16

FY07 FY08 FY09 FY10

BIS capital adequacy ratio (consolidated basis)

Tier I ratio (Core Capital ratio)

14.40

15.30

14.12

13.76

15.32

14.06

13.42

14.70

BIS capital abequacy ratio

Improved Capital AdequacyFrom the fiscal year ended March 31, 2007, the Basel II methodology was adopted and the method for calculating capital ratios was left for the banks to choose based on risk status and management method. The Shizuoka Bank has taken steps to upgrade its risk management in response to business and transaction diversification and is building a more advanced internal bank system with the goal of adopting a more sophisticated method of calculation. The capital adequacy ratio (consolidated basis) based on Basel II for the fiscal year ended March 31, 2011 was 15.30%, while the Tier I ratio (core capital ratio), a basic item, was 14.40%, well above the 8% standard for banks with overseas branches. Further, we will prepare properly for the adoption of new capital adequacy ratio regulations (Basel III), which will be gradually phased in from 2013.

100

50

150

200

00

50

100

150

200

0

5050

000000

500050

200000000

Balance of deposits (average; non-consolidated)

FY08 FY09 FY10

(¥ billion)

Gross Operating Pro�t Net operating pro�t

FY11 (Forecast)

148.7

53.7

148.2

72.0

151.4

71.7

152.0

64.3

8

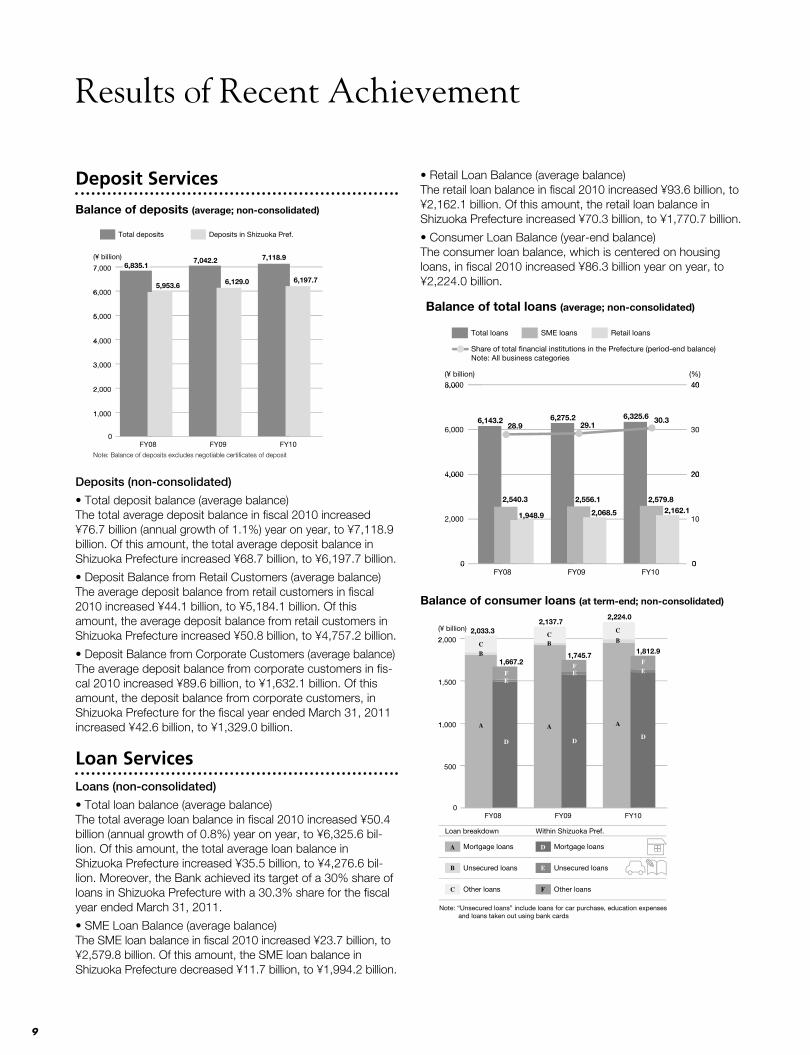

Deposit Services

1,000

2,000

4,000

3,000

5,000

6,000

7,000

00

1001,1,

2002,2,

3003,3,

4004,4,

5005,5,

6006,6,

7007,7,

0

10000000

20000000

30000000

40000000

50000000

60000000

7000000

C

B

A

F

E

DMortgage loans

Unsecured loans

Loan breakdown

Mortgage loans

Unsecured loans

Within Shizuoka Pref.

Other loans Other loans

Note: “Unsecured loans” include loans for car purchase, education expenses and loans taken out using bank cards

Balance of deposits (average; non-consolidated)

FY08 FY09

(¥ billion)

Total deposits Deposits in Shizuoka Pref.

FY10

6,835.1

5,953.6

7,118.9

6,197.7

Note: Balance of deposits excludes negotiable certi�cates of deposit

7,042.2

6,129.0

Deposits (non-consolidated)

• Total deposit balance (average balance)The total average deposit balance in fiscal 2010 increased ¥76.7 billion (annual growth of 1.1%) year on year, to ¥7,118.9 billion. Of this amount, the total average deposit balance in Shizuoka Prefecture increased ¥68.7 billion, to ¥6,197.7 billion.

• Deposit Balance from Retail Customers (average balance)The average deposit balance from retail customers in fiscal 2010 increased ¥44.1 billion, to ¥5,184.1 billion. Of this amount, the average deposit balance from retail customers in Shizuoka Prefecture increased ¥50.8 billion, to ¥4,757.2 billion.

• Deposit Balance from Corporate Customers (average balance)The average deposit balance from corporate customers in fis-cal 2010 increased ¥89.6 billion, to ¥1,632.1 billion. Of this amount, the deposit balance from corporate customers, in Shizuoka Prefecture for the fiscal year ended March 31, 2011 increased ¥42.6 billion, to ¥1,329.0 billion.

Loan ServicesLoans (non-consolidated)

• Total loan balance (average balance)The total average loan balance in fiscal 2010 increased ¥50.4 billion (annual growth of 0.8%) year on year, to ¥6,325.6 bil-lion. Of this amount, the total average loan balance in Shizuoka Prefecture increased ¥35.5 billion, to ¥4,276.6 bil-lion. Moreover, the Bank achieved its target of a 30% share of loans in Shizuoka Prefecture with a 30.3% share for the fiscal year ended March 31, 2011.

• SME Loan Balance (average balance)The SME loan balance in fiscal 2010 increased ¥23.7 billion, to ¥2,579.8 billion. Of this amount, the SME loan balance in Shizuoka Prefecture decreased ¥11.7 billion, to ¥1,994.2 billion.

• Retail Loan Balance (average balance)The retail loan balance in fiscal 2010 increased ¥93.6 billion, to ¥2,162.1 billion. Of this amount, the retail loan balance in Shizuoka Prefecture increased ¥70.3 billion, to ¥1,770.7 billion.

• Consumer Loan Balance (year-end balance)The consumer loan balance, which is centered on housing loans, in fiscal 2010 increased ¥86.3 billion year on year, to ¥2,224.0 billion.

2,000

4,000

6,000

8,000

0

10

20

30

40

00.000000

1333.333333

2666.666667

4000.00000

5333.333333

6666.666667

8000.00000

0.00000000000

1333.3333333333333333

2666.6666676666766667

000 00,000,0000000000004,4,4,4,

5333.3333333333333333

6666.6666676666766667

8,0008,000000000008,8,8,8,

0.00000000000000

1333.33333333333333333

2666.66666676666766667

4000.00000000000000000000000000000000

5333.33333333333333333

6666.6666676666766667

0.0000000000000000000000000

00

2020

4040

C

B

A

F

E

D

2,540.3

28.9 29.130.3

1,948.9

Mortgage loans

Unsecured loans

Loan breakdown

Mortgage loans

Unsecured loans

Within Shizuoka Pref.

Other loans Other loans

Note: “Unsecured loans” include loans for car purchase, education expenses and loans taken out using bank cards

Balance of total loans (average; non-consolidated)

FY08 FY09

(¥ billion) (%)

Total loans SME loans Retail loans

FY10

6,143.2

2,579.82,162.1

6,325.6

2,556.1

2,068.5

6,275.2

Share of total �nancial institutions in the Prefecture (period-end balance) Note: All business categories

900

1,100

1,300

1,500

0

0

(¥ billion)

500

1,000

1,500

2,000

FY08 FY09 FY10

FY04 FY05

(¥ billion)

FY06

0

500

1001,1,

1501,1,

2002,2,

0

5005000

10000000

15005000

20000000

0

500

1000

1500

2000

0

5000

10000

15000

2000

C

B

A

F

F

E

E

D

D

DA

B

C

1,253.7

F

E

A

B

C

1,617.6

1,363.7

A

B

C

1,765.0

F

E

D

1,480.4

1,474.0

1,667.2

A

B

C

FE

D

Balance of consumer loans (at term-end; non-consolidated)

Mortgage loans

Unsecured loans

Loan breakdown

Mortgage loans

Unsecured loans

Within Shizuoka Pref.

Other loans Other loans

Note: “Unsecured loans” include loans for car purchase, education expenses and loans taken out using bank cards

2,033.3

1,812.9

A

B

C

FE

D

2,224.0

1,745.7

A

BC

FE

D

2,137.7

Results of Recent Achievement

9

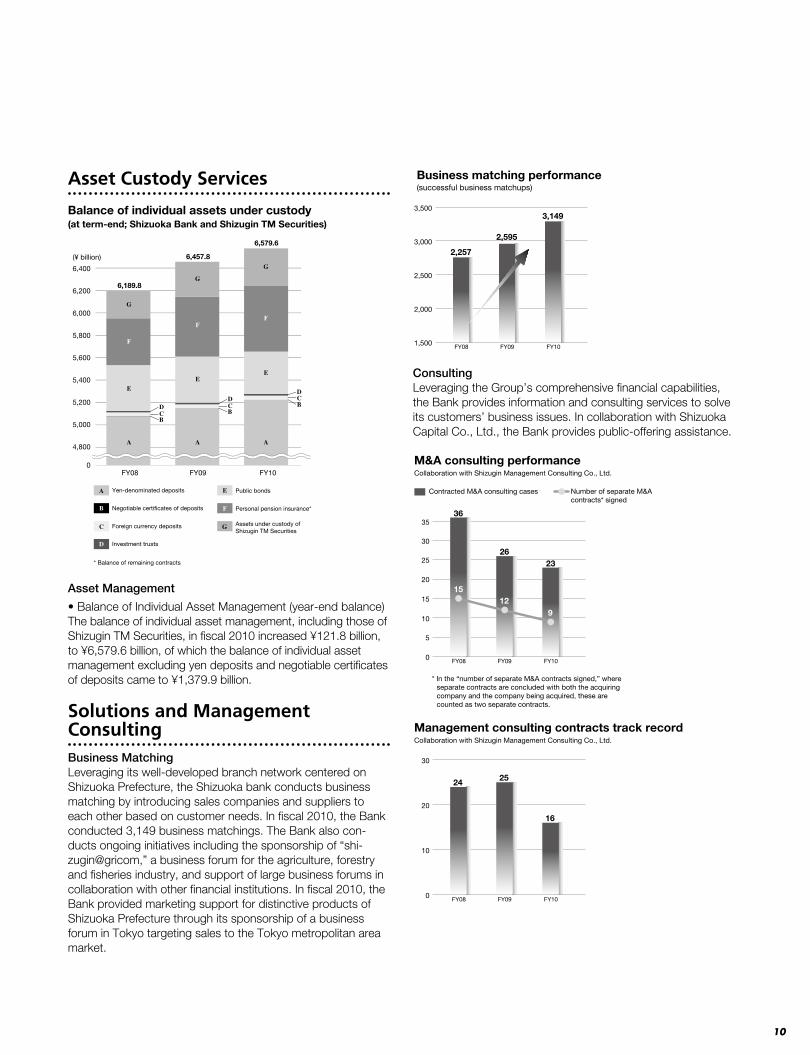

Asset Custody Services

4600

6400

4400

6200

Personal pension insurance*

Foreign currency deposits

Investment trusts

F

F

E

A

G

6,189.8

CD

0

4,800

5,000

5,200

5,400

5,600

5,800

6,000

6,200

6,400

(¥ billion)

Yen-denominated deposits

Assets under custody of Shizugin TM Securities

Negotiable certi�cates of deposits

Public bonds

B

E

F

A

D

C G

B

E

A

G

6,579.6

BCD

Balance of individual assets under custody(at term-end; Shizuoka Bank and Shizugin TM Securities)

FY08 FY09 FY10

* Balance of remaining contracts

F

E

A

G

6,457.8

CD

B

Asset Management

• Balance of Individual Asset Management (year-end balance)The balance of individual asset management, including those of Shizugin TM Securities, in fiscal 2010 increased ¥121.8 billion, to ¥6,579.6 billion, of which the balance of individual asset management excluding yen deposits and negotiable certificates of deposits came to ¥1,379.9 billion.

Solutions and Management ConsultingBusiness MatchingLeveraging its well-developed branch network centered on Shizuoka Prefecture, the Shizuoka bank conducts business matching by introducing sales companies and suppliers to each other based on customer needs. In fiscal 2010, the Bank conducted 3,149 business matchings. The Bank also con-ducts ongoing initiatives including the sponsorship of “shi-zugin@gricom,” a business forum for the agriculture, forestry and fisheries industry, and support of large business forums in collaboration with other financial institutions. In fiscal 2010, the Bank provided marketing support for distinctive products of Shizuoka Prefecture through its sponsorship of a business forum in Tokyo targeting sales to the Tokyo metropolitan area market.

2,500

2,000

1,500

3,000

3,500

FY08 FY09 FY10

Business matching performance

3,149

2,595

2,257

(successful business matchups)

ConsultingLeveraging the Group’s comprehensive financial capabilities, the Bank provides information and consulting services to solve its customers’ business issues. In collaboration with Shizuoka Capital Co., Ltd., the Bank provides public-offering assistance.

5

10

0

15

25

20

30

35

FY08 FY09 FY10

Collaboration with Shizugin Management Consulting Co., Ltd.

M&A consulting performance

Contracted M&A consulting cases Number of separate M&A contracts* signed

2326

36

912

15

* In the “number of separate M&A contracts signed,” where separate contracts are concluded with both the acquiring company and the company being acquired, these are counted as two separate contracts.

10

0

20

30

FY08 FY09 FY10

Management consulting contracts track record

2524

16

Collaboration with Shizugin Management Consulting Co., Ltd.

10

Management Systems

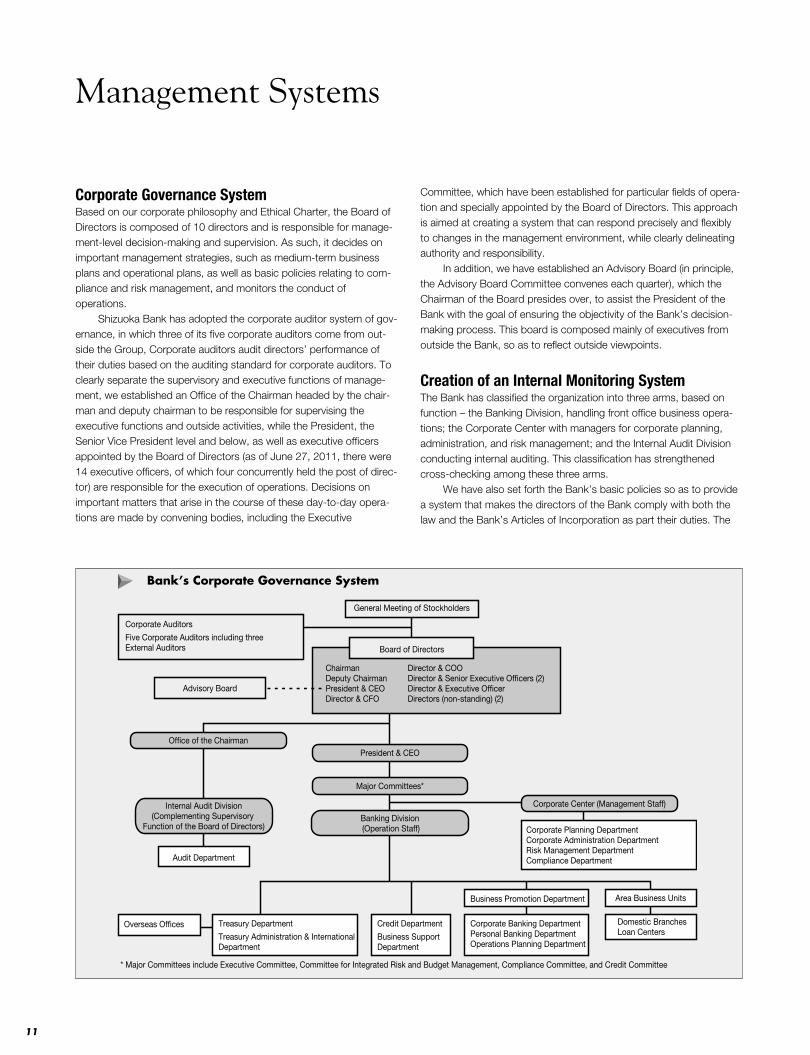

Corporate Governance SystemBased on our corporate philosophy and Ethical Charter, the Board of Directors is composed of 10 directors and is responsible for manage-ment-level decision-making and supervision. As such, it decides on important management strategies, such as medium-term business plans and operational plans, as well as basic policies relating to com-pliance and risk management, and monitors the conduct of operations.

Shizuoka Bank has adopted the corporate auditor system of gov-ernance, in which three of its five corporate auditors come from out-side the Group, Corporate auditors audit directors’ performance of their duties based on the auditing standard for corporate auditors. To clearly separate the supervisory and executive functions of manage-ment, we established an Office of the Chairman headed by the chair-man and deputy chairman to be responsible for supervising the executive functions and outside activities, while the President, the Senior Vice President level and below, as well as executive officers appointed by the Board of Directors (as of June 27, 2011, there were 14 executive officers, of which four concurrently held the post of direc-tor) are responsible for the execution of operations. Decisions on important matters that arise in the course of these day-to-day opera-tions are made by convening bodies, including the Executive

Committee, which have been established for particular fields of opera-tion and specially appointed by the Board of Directors. This approach is aimed at creating a system that can respond precisely and flexibly to changes in the management environment, while clearly delineating authority and responsibility.

In addition, we have established an Advisory Board (in principle, the Advisory Board Committee convenes each quarter), which the Chairman of the Board presides over, to assist the President of the Bank with the goal of ensuring the objectivity of the Bank’s decision-making process. This board is composed mainly of executives from outside the Bank, so as to reflect outside viewpoints.

Creation of an Internal Monitoring SystemThe Bank has classified the organization into three arms, based on function – the Banking Division, handling front office business opera-tions; the Corporate Center with managers for corporate planning, administration, and risk management; and the Internal Audit Division conducting internal auditing. This classification has strengthened cross-checking among these three arms. We have also set forth the Bank’s basic policies so as to provide a system that makes the directors of the Bank comply with both the law and the Bank’s Articles of Incorporation as part their duties. The

General Meeting of Stockholders

Chairman Deputy Chairman President & CEODirector & CFO

Director & COODirector & Senior Executive Of�cers (2) Director & Executive Of�cerDirectors (non-standing) (2)

Board of Directors

Credit Department

Business Support Department

Treasury Department

Treasury Administration & International Department

Area Business Units

Domestic BranchesLoan Centers

Overseas Of�ces

Business Promotion Department

Corporate Banking DepartmentPersonal Banking DepartmentOperations Planning Department

Banking Division (Operation Staff)

Of�ce of the Chairman

Major Committees*

Audit Department

* Major Committees include Executive Committee, Committee for Integrated Risk and Budget Management, Compliance Committee, and Credit Committee

Internal Audit Division(Complementing Supervisory

Function of the Board of Directors) Corporate Planning DepartmentCorporate Administration DepartmentRisk Management DepartmentCompliance Department

Corporate Center (Management Staff)

Bank’s Corporate Governance System

Corporate Auditors

Five Corporate Auditors including three External Auditors

Advisory Board

President & CEO

11

system also enables management to ensure appropriate business operations across the board. Based on these policies, we are cur-rently working to create an effective system of internal control.

Prompt and Appropriate DisclosureTo ensure the prompt and appropriate provision of corporate informa-tion to the Bank’s stakeholders, the Bank discloses information in accordance with Banking Law and the Financial Instruments and Exchange Act and the securities listing regulations of the Japanese stock exchanges. It also conducts voluntary proactive disclosure by appropriately disclosing information in a consistent, transparent and impartial manner. The Corporate Planning Department centrally manages a variety of information generated by each group. Once it has decided that the information falls under the category of prompt disclosure, that informa-tion is, in principle, disclosed after Executive Committee approval is received. To maintain prompt and appropriate disclosure, when nec-essary, the Compliance Department and the auditing firm confer, while the Internal Audit Division routinely verifies the appropriateness and effectiveness of overall disclosure.

Basic Compliance Policy and Organizational StructureThe Shizuoka Bank Group has always regarded ethical and legal com-pliance as a priority issue for management, and is taking measures to consolidate and strengthen its compliance structure under its Ethical Charter, which sets out the Bank’s basic policy. These measures are governed by the Compliance Program, a specific set of compliance measures drawn up by the Board of Directors each fiscal year. Meetings of the Compliance Committee, chaired by the Bank’s president and composed of directors and other top executives, are held monthly to deliberate on important compliance-related matters and assess the operation of the compliance system across the whole Shizuoka Bank Group – including progress being made in achieving the goals of the Compliance Program. The system is revised when deemed necessary. In addition to acting as the central body for the unified manage-ment of compliance-related information throughout the Group, the Compliance Group of the Compliance Department takes prime responsibility for monitoring the functioning of the compliance system, devises preventive measures against possible compliance violations, and works to improve the whole compliance system. In addition, Compliance Officers and officers responsible for the management of risk-involved products assigned to the Compliance Group carry out on-site checks of the Bank’s branches to strengthen our monitoring systems at the branch level. Persons responsible for compliance have been assigned to all Bank branches, head office departments, and Group companies where they conduct compliance inspections and draft reports on day-to-day business operations, which are verified by the Audit Department of the Internal Audit Division.

Creating a Compliance-Centered Corporate CultureBy getting management actively involved in compliance activities, such as by taking the opportunity to participate in the branch managers’ meeting and visit branch offices and having directors directly give compliance instructions, the entire Group seeks to enhance compli-ance awareness. In addition to the above-mentioned efforts, we are implementing measures to foster and raise compliance awareness including the following.

Basic PolicyAs a member of the local community, the Shizuoka Bank Group com-plies with laws, regulations, and social norms and embraces a spirit of fair play. To develop as a bank while maintaining harmony with the community, the Bank has established an Ethical Charter, which sets out the Bank’s basic compliance policy. Ethical CharterGaining Trust

We are constantly aware of the Bank’s heavy social responsibility and its public mission. As a banking group, we strive to build unshakable trust through sound business management.

Compliance with Laws, Regulations and RulesIn the conduct of our business, we comply with laws, regulations, and Company rules and on the basis of honesty and fairness, we maintain social norms as a member of society.

Social Etiquette and Fair PlayAs executives and employee of the Shizuoka Bank Group, we con-tribute to the development of the local community by fostering a strong social etiquette and a spirit of fair play.

Breaking Contact with Anti-Social ForcesThe Shizuoka Bank Group adamantly rejects the unreasonable demands made by anti-social forces and groups that offend public order and morals and absolutely refuses to deal with such groups.

Active CommunicationWe will actively communicate with stakeholders and will cooperate with them to build a strong compliance system.

Shizugin Compliance BookThe Bank has established standards of conduct vis-à-vis laws and rules that must be observed in the execution of day-to-day business activities. It has also compiled the Shizugin Compliance Book. These laws and rules are written in easy-to-understand language in the recently published Shizugin Compliance Book, which is distributed to all employees and executives.

“Opinion Box” Internal Reporting SystemThe Bank has set up reporting counters for Compliance Officers in the Compliance Department and in attorneys’ offices so that executives and employees can directly report compliance-related issues. In this way, we seek to encourage more self-reporting within the organization.* Reporting can be made by phone, in writing, or by email.

Compliance Education and TrainingThe Bank conducts ongoing educational activities for the practice of compliance by training executives and employees and holding monthly study groups in branches.

12

Risk Management Systems

Integrated Risk Management SystemsAt the Shizuoka Bank Group, we established a basic frame-work consisting of defining risk, setting up an organizational structure for risk management, and following specific risk con-trol procedures based on the “Basic Risk Management Regulations” which lay down the fundamental principles that underlie our approach to risk management. To ensure an appropriate balance between raising earn-ings levels and financial sustainability, the Bank’s risk manage-ment is based upon the allocation of risk capital as an integral part of its integrated risk management system. The “allocation of risk capital” is a mechanism to ensure the soundness of management by keeping risk within a man-ageable range. Shizuoka Bank defines core shareholder’s equity(*) as capital for allocation, and allocates it to all depart-ments involved in business execution. Even if market risk, credit risk and other risks were to materialize, the resulting losses would be controlled within the bounds of shareholders’ equity.(*) Ordinary equity + retained earnings – funds due to be paid outside the com-

pany – intangible fixed assets – prepaid pension expenses, etc.

Credit Risk Management SystemThe Credit Risk Management Group of the Risk Management Department manages all credit risk relating to the Shizuoka Bank Group’s operations both in Japan and overseas in order to maintain and enhance the soundness of the Group’s loan asset portfolio. In the Bank’s internal rating system, including its borrower credit rating system, which is the foundation stone of its credit risk management, responsibility for the design of the system and supervision of its function belongs to the Credit Risk Management Group; responsibility for the day-to-day application of the credit rating system belongs to the Ratings Assessment Group of the Credit Department; and responsibility for verification of the system belongs to the Risk Management Group of the Risk Management Department. These three units exercise a system of checks and balances, thereby facilitating greater precision and proper functioning of the Bank’s internal ratings system. In addition, the self-assessment process – overseen by the Asset Auditing Group of the Audit Department, which is organizationally independent of the sales division and credit department as well as risk management units – is used to verify that the rules of credit risk management are being properly observed. The Credit Risk Management Group also uses statistical methods to quantify latent credit risk in the Bank’s loan portfo-lio. In this way, the Bank accurately assesses the amount of future risk, monitors the concentration of loans to particular large borrowers or specific industries, and thus controls the portfolio to avoid excessive credit risk.

Compliance Group

Major Committees Executive Committee Compliance Committee Committee for Integrated Risk & Budget Management Credit Committee

Credit Risk Market Risk Liquidity RiskOperational Risk

Administrative Risk System Risk Other Risks

Domestic & overseas branches, head of�ce departments, Group companies, overseas subsidiaries, and signi�cant outsource

Board of Directors

Of�ce of the Chairman

Compliance

Compliance and Risk Management Systems

Independent Auditor

Corporate Auditors

Internal AuditDivision

(AuditDepartment)

Risk Management DepartmentCompliance Department

Veri�cation of risk management effectiveness Risk monitoring

13

Borrowers’ Credit Rating SystemThe Shizuoka Bank Group employs a borrowers’ credit rating system to gain an accurate picture of the creditworthiness of borrowers and ensure meticulous credit risk management. Borrowers are rated on a scale of 1 to 12 according to finan-cial indicators, including the borrowers’ financial standing and cash flows. To keep the ratings objective, we place more weight on quantitative information in this system. Borrowers’ credit ratings form the basis for classification in self-assessment, which is implemented as part of capital ratio calculations based on the Banking Act. They are also widely used as a standard for calculating the general reserve for possi-ble loan losses, and as a standard for the management of prob-lem loans. In principle, the Bank assigns borrower ratings to all borrow-ers and routinely reviews these ratings each year based on the borrowers’ financial statements and other relevant data. In the event that it becomes necessary to change the rating, a review will be conducted as needed. By monitoring the current financial status of borrowers, we can improve our screening ability.

Market Risk Management SystemIn market transactions, the Shizuoka Bank Group limits the amount of risk capital allocated as well as sets various restric-tions, such as on gains or losses from valuation of investment securities, and on the amount of exposure or loss depending upon the risk profile of each transaction or financial instrument. In this way, we keep market risk within certain defined levels. For banking account transactions, especially deposits, loans, and investment securities, the ALM group of the Corporate Planning Department formulates the hedging poli-cies based on current risk conditions and on the outlook for interest rates so as to keep risk volume within a certain range, and discusses these policies at the Committee for Integrated Risk and Budget Management. The organization of the market divisions is strictly divided between departments conducting transactions (front office: Treasury Department) and administrative and control depart-ments (back office: Treasury Administration & International Department, Treasury & International Operations Center). In addition, an independent risk management department (mid-dle office: Risk Management Department, Risk Management Group) that provides for mutual checks and balances has been established. Moreover, the effectiveness of the mutual checks and balances between these three departments is ver-ified through inspections by the Audit Department, which is independent of the departments responsible for executing transactions.

Liquidity Risk Management SystemThe Shizuoka Bank Group has established separate yen and foreign currency-denominated financing management depart-ments (Treasury Department, Fund & Foreign Exchange Group, Treasury Administration & International Department, Treasury & International Operations Center etc.), and has established a liquidity risk management department (Risk Management Department, Risk Management Group) that is entirely inde-pendent of the financing management departments. In this way, we set up a system that provides mutual checks and bal-ances. The Fund & Foreign Exchange Group of the Treasury Department, which is one of the financing management departments, controls fundraising requirements within procura-ble levels to avoid excessive fundraising. We also conduct sta-ble fund management activities, paying close attention to

market conditions. Moreover, the liquidity risk management department monitors the status of financing management departments and assesses the stability of the assets-liabilities structure. To handle unforeseen circumstances, emergency fundrais-ing management is divided into four stages: “Stage 1 (preven-tive stage)”; “Stage 2 (attention required stage)”; “Stage 3 (liquidity concern stage)”; and “Stage 4 (insufficient liquidity stage)”; with each stage having its own person in charge and predefined countermeasures, thereby forming a structure capable of swiftly responding to issues should they arise. As for market liquidity risk, the liquidity risk management department routinely monitors the status of highly liquid asset holdings that can be easily monetized. The front office addresses market liquidity risk by selecting investment assets based on their liquidity and setting limits on specific stocks and holding periods.

Operational Risk Management SystemEach risk category is managed by a dedicated unit of the Bank, while the Operational Risk Management Group of the Risk Management Department is the central unit responsible for overseeing and managing operational risk throughout the entire Shizuoka Bank Group. In line with our basic policies on operational risk management, we are taking steps to strengthen our operational risk management system through a range of measures including the compilation and analysis of internal loss data and the implementation of a risk control self-assessment. The effectiveness of this risk management sys-tem is verified by on-site audits conducted by the Audit Department, which is organizationally independent from any of the units that it audits.

Business Continuity PlanBecause of the highly public nature of banking services, such as the withdrawing of deposits and account settlement, there are strong demands for banks to ensure business continuity as a fulfillment of their social responsibility. To prepare itself against an outbreak of a state of emer-gency, the Shizuoka Bank has established the Contingency Plan as its business continuity plan. The Plan enables the Bank to continually carry out its critically important operations or to resume them as soon as possible after an interruption, even in the case of a major natural disaster like the Tokai earthquake, which had been predicted as Suruga Bay is a seismic center, or an outbreak of a highly dangerous new strain of bird influenza. When necessary, the Bank reviews its disaster counter-measures, such as responding to stronger tsunami counter-measures in the wake of the massive tsunami that the struck coastal area, particularly in the Tohoku Region, as a result of the Great East Japan Earthquake of March 2011. In addition to making our computer and training centers and some of our branches earthquake-proof, and reinforcing the earthquake-resistance of some of our buildings, we have installed uninterruptible power supplies (UPS) and private power generation equipment. We have also installed a wide range of disaster prevention countermeasure equipment including telecommunications equipment for emergent situa-tions, a duplicate communications network and a backup sys-tem, which ensures that we will be able to resume business soon after disaster strikes. In addition, as a more practical measure, we routinely carry out disaster drills, backup center operation drills and other drills based on the Contingency Plan.

14

Tokyo

Shizuoka

Osaka

Economic ScaleWith a nominal annual economic output of ¥16.4 trillion

(US$166.51 billion) in fiscal 2008, Shizuoka Prefecture,

our main operational base, would comes after the GDP of

Singapore, Rumania and Philippine. In terms of economic

indicators, Shizuoka Prefecture has a share of the national

economy amounting to roughly 3%, putting it at around 10th

place among the country’s 47 prefectures. For this reason, it is

sometimes called “the 3% economy.”

Industrial CharacteristicsShizuoka Prefecture is situated midway between the two

major consumer markets and industrial centers of Japan —

the Nagoya region plus the Osaka-Kyoto region to the west,

and the Yokohama-Tokyo region to the east. Because of this

location at a busy “crossroads” of the nation, it has historically

developed into a significant center of manufacturing industry.

The convenient location of Shizuoka Prefecture in transporta-

tion terms has caused the growth of a strong industrial base.

The prefecture ranks first among Japan’s 47 prefectures for

the establishment of new factories, and is one of the country’s

leading manufacturing areas. Moreover, the wide variety of

industries represented within Shizuoka has led to it being

dubbed “the industrial department store.” Corporations active

in Shizuoka include world-leading enterprises such as Toyota,

Honda, Suzuki, and Yamaha, and the prefecture is renowned

for its concentration of export-oriented manufacturing compa-

nies. Many of these firms have set up production subsidiaries

overseas, which is creating a growing international aspect to

the regional economy. In addition, Mt. Fuji Shizuoka Airport

opened in June 2009, and we expect that Shizuoka prefecture

will be more internationalized, stimulating the interchange of

people and ideas with the major urban centers of Eastern

Asia, and act as an important driving force for the regional

economy.

In recent years the prefectural authorities have been operat-

ing a number of schemes to encourage companies in the

medical treatment, pharmaceuticals, chemicals, and optical

technology industries, among others, to set up operations in

the so-called “Shizuoka Triangle Research Cluster” (spread

across the prefecture’s eastern, central, and western districts)

as a means of developing a next-generation industrial base.

Eastern ShizuokaThis part of the prefecture is characterized by the traditional paper and

pulp industry, which developed to take advantage of the abundant

underground water resources near Mt. Fuji, as well as a number of

plants and research facilities that have more recently relocated to the

area from Tokyo and its vicinity. The Izu Peninsula boasts wonderful

natural scenery that is magically transformed with the changing

seasons, as well as a wealth of hot springs. For these reasons, it is

one of the most popular yen-round holiday resort areas in Japan.

The Pharma Valley ProjectIn anticipation of a massive increase in demand for medical treatment

and nursing care services against the background of a growing

lifespan, a project is being pursued to encourage research activities in

the field of wellness.

Central ShizuokaThis region has a wide variety of retailing companies and a concentra-

tion of other service industries. Traditional craft manufacturing (primar-

ily furniture), plastic models and other toy manufacturing, and food

processing industries (tea, canned foods) are also active in this part of

Shizuoka. The famous ports of Yaizu and Shimizu are also located in

this region. The former is well-known as a base for large-scale com-

mercial fishing operations, and the latter as a trading port.

The Food-Science Hills ProjectThis project seeks to develop the local industrial base by efforts to

overcome lifestyle-related diseases through scientific progress in the

fields of foods and pharmaceutical products.

Western ShizuokaThis part has a high concentration of manufacturing companies, such

as makers of motorcycles and musical instruments, among which are

many world-renowned companies. This is one of the main reasons

why Shizuoka Prefecture ranks third among Japan’s 47 prefectures in

terms of the value of manufactured goods shipments, accounting for

5.7% of the value of nation’s total manufacturing output in 2008. It is

to this area that Shizuoka Prefecture owes its reputation as a heavily

industrialized prefecture with a high proportion of export-oriented

companies.

The Photon Valley projectThe project aims to develop a next-generation industrial base centered

on optical technology, and assist in practical industrial applications of

new technologies.

Our Operational Base:Shizuoka Prefecture

15

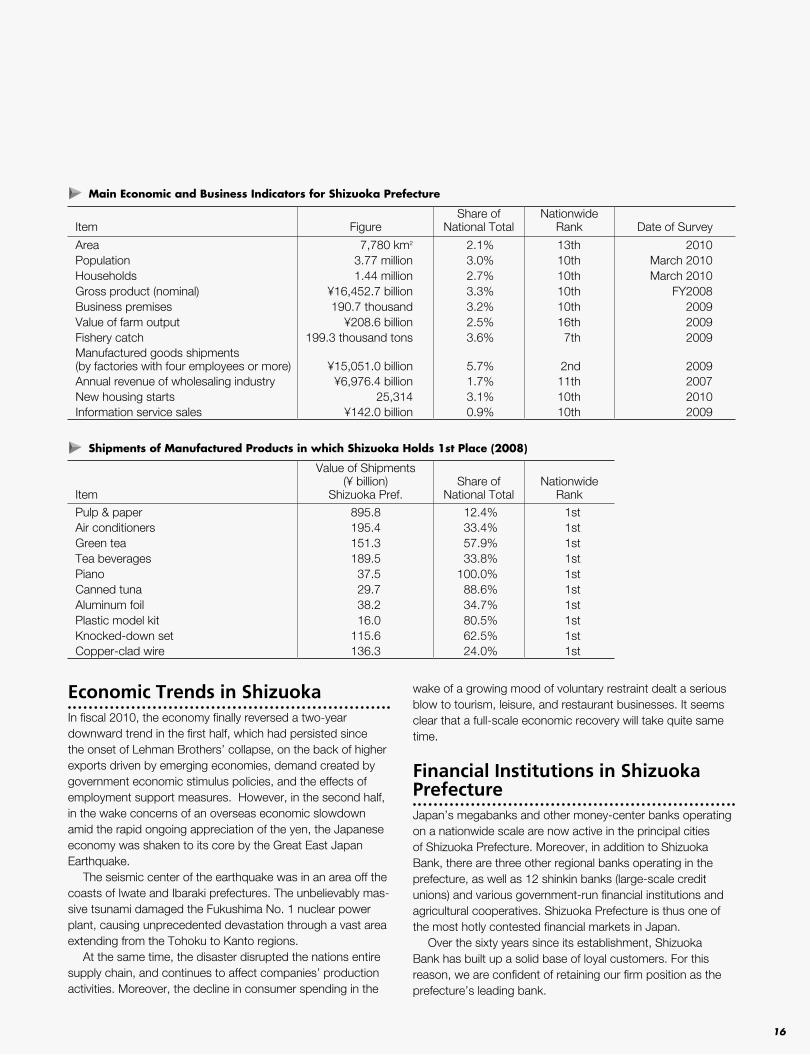

Shipments of Manufactured Products in which Shizuoka Holds 1st Place (2008)

Main Economic and Business Indicators for Shizuoka Prefecture

Economic Trends in ShizuokaIn fiscal 2010, the economy finally reversed a two-year downward trend in the first half, which had persisted since the onset of Lehman Brothers’ collapse, on the back of higher exports driven by emerging economies, demand created by government economic stimulus policies, and the effects of employment support measures. However, in the second half, in the wake concerns of an overseas economic slowdown amid the rapid ongoing appreciation of the yen, the Japanese economy was shaken to its core by the Great East Japan Earthquake. The seismic center of the earthquake was in an area off the coasts of Iwate and Ibaraki prefectures. The unbelievably mas-sive tsunami damaged the Fukushima No. 1 nuclear power plant, causing unprecedented devastation through a vast area extending from the Tohoku to Kanto regions. At the same time, the disaster disrupted the nations entire supply chain, and continues to affect companies’ production activities. Moreover, the decline in consumer spending in the

wake of a growing mood of voluntary restraint dealt a serious blow to tourism, leisure, and restaurant businesses. It seems clear that a full-scale economic recovery will take quite same time.

Financial Institutions in Shizuoka PrefectureJapan’s megabanks and other money-center banks operating on a nationwide scale are now active in the principal cities of Shizuoka Prefecture. Moreover, in addition to Shizuoka Bank, there are three other regional banks operating in the prefecture, as well as 12 shinkin banks (large-scale credit unions) and various government-run financial institutions and agricultural cooperatives. Shizuoka Prefecture is thus one of the most hotly contested financial markets in Japan. Over the sixty years since its establishment, Shizuoka Bank has built up a solid base of loyal customers. For this reason, we are confident of retaining our firm position as the prefecture’s leading bank.

Item

Value of Shipments(¥ billion)

Shizuoka Pref.Share of

National Total

Nationwide

Rank

Pulp & paper 895.8 12.4% 1stAir conditioners 195.4 33.4% 1stGreen tea 151.3 57.9% 1stTea beverages 189.5 33.8% 1stPiano 37.5 100.0% 1stCanned tuna 29.7 88.6% 1stAluminum foil 38.2 34.7% 1stPlastic model kit 16.0 80.5% 1stKnocked-down set 115.6 62.5% 1stCopper-clad wire 136.3 24.0% 1st

Item FigureShare of

National TotalNationwide

Rank Date of Survey

Area 7,780 km2 2.1% 13th 2010Population 3.77 million 3.0% 10th March 2010Households 1.44 million 2.7% 10th March 2010Gross product (nominal) ¥16,452.7 billion 3.3% 10th FY2008Business premises 190.7 thousand 3.2% 10th 2009Value of farm output ¥208.6 billion 2.5% 16th 2009Fishery catch 199.3 thousand tons 3.6% 7th 2009Manufactured goods shipments (by factories with four employees or more) ¥15,051.0 billion 5.7% 2nd 2009Annual revenue of wholesaling industry ¥6,976.4 billion 1.7% 11th 2007New housing starts 25,314 3.1% 10th 2010Information service sales ¥142.0 billion 0.9% 10th 2009

16

17

18

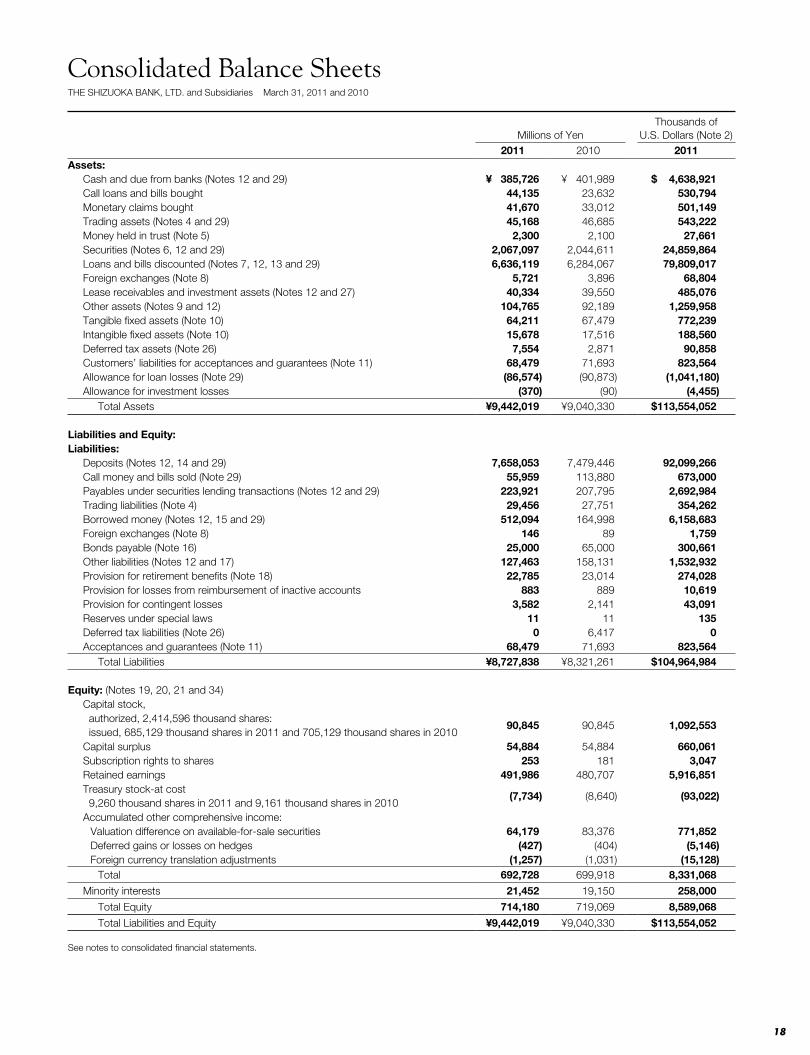

Consolidated Balance SheetsTHE SHIZUOKA BANK, LTD. and Subsidiaries March 31, 2011 and 2010

Millions of Yen

Thousands of U.S. Dollars (Note 2)

2011 2010 2011Assets:

Cash and due from banks (Notes 12 and 29) ¥ 385,726 ¥ 401,989 $ 4,638,921 Call loans and bills bought 44,135 23,632 530,794 Monetary claims bought 41,670 33,012 501,149 Trading assets (Notes 4 and 29) 45,168 46,685 543,222 Money held in trust (Note 5) 2,300 2,100 27,661 Securities (Notes 6, 12 and 29) 2,067,097 2,044,611 24,859,864 Loans and bills discounted (Notes 7, 12, 13 and 29) 6,636,119 6,284,067 79,809,017 Foreign exchanges (Note 8) 5,721 3,896 68,804 Lease receivables and investment assets (Notes 12 and 27) 40,334 39,550 485,076 Other assets (Notes 9 and 12) 104,765 92,189 1,259,958 Tangible fixed assets (Note 10) 64,211 67,479 772,239 Intangible fixed assets (Note 10) 15,678 17,516 188,560 Deferred tax assets (Note 26) 7,554 2,871 90,858 Customers’ liabilities for acceptances and guarantees (Note 11) 68,479 71,693 823,564 Allowance for loan losses (Note 29) (86,574) (90,873) (1,041,180)Allowance for investment losses (370) (90) (4,455)

Total Assets ¥9,442,019 ¥9,040,330 $113,554,052

Liabilities and Equity:Liabilities:

Deposits (Notes 12, 14 and 29) 7,658,053 7,479,446 92,099,266 Call money and bills sold (Note 29) 55,959 113,880 673,000 Payables under securities lending transactions (Notes 12 and 29) 223,921 207,795 2,692,984 Trading liabilities (Note 4) 29,456 27,751 354,262 Borrowed money (Notes 12, 15 and 29) 512,094 164,998 6,158,683 Foreign exchanges (Note 8) 146 89 1,759 Bonds payable (Note 16) 25,000 65,000 300,661 Other liabilities (Notes 12 and 17) 127,463 158,131 1,532,932 Provision for retirement benefits (Note 18) 22,785 23,014 274,028 Provision for losses from reimbursement of inactive accounts 883 889 10,619 Provision for contingent losses 3,582 2,141 43,091 Reserves under special laws 11 11 135 Deferred tax liabilities (Note 26) 0 6,417 0 Acceptances and guarantees (Note 11) 68,479 71,693 823,564

Total Liabilities ¥8,727,838 ¥8,321,261 $104,964,984

Equity: (Notes 19, 20, 21 and 34)Capital stock, authorized, 2,414,596 thousand shares: issued, 685,129 thousand shares in 2011 and 705,129 thousand shares in 2010

90,845 90,845 1,092,553

Capital surplus 54,884 54,884 660,061 Subscription rights to shares 253 181 3,047 Retained earnings 491,986 480,707 5,916,851 Treasury stock-at cost 9,260 thousand shares in 2011 and 9,161 thousand shares in 2010

(7,734) (8,640) (93,022)

Accumulated other comprehensive income:Valuation difference on available-for-sale securities 64,179 83,376 771,852 Deferred gains or losses on hedges (427) (404) (5,146)Foreign currency translation adjustments (1,257) (1,031) (15,128)

Total 692,728 699,918 8,331,068

Minority interests 21,452 19,150 258,000

Total Equity 714,180 719,069 8,589,068

Total Liabilities and Equity ¥9,442,019 ¥9,040,330 $113,554,052

See notes to consolidated financial statements.

19

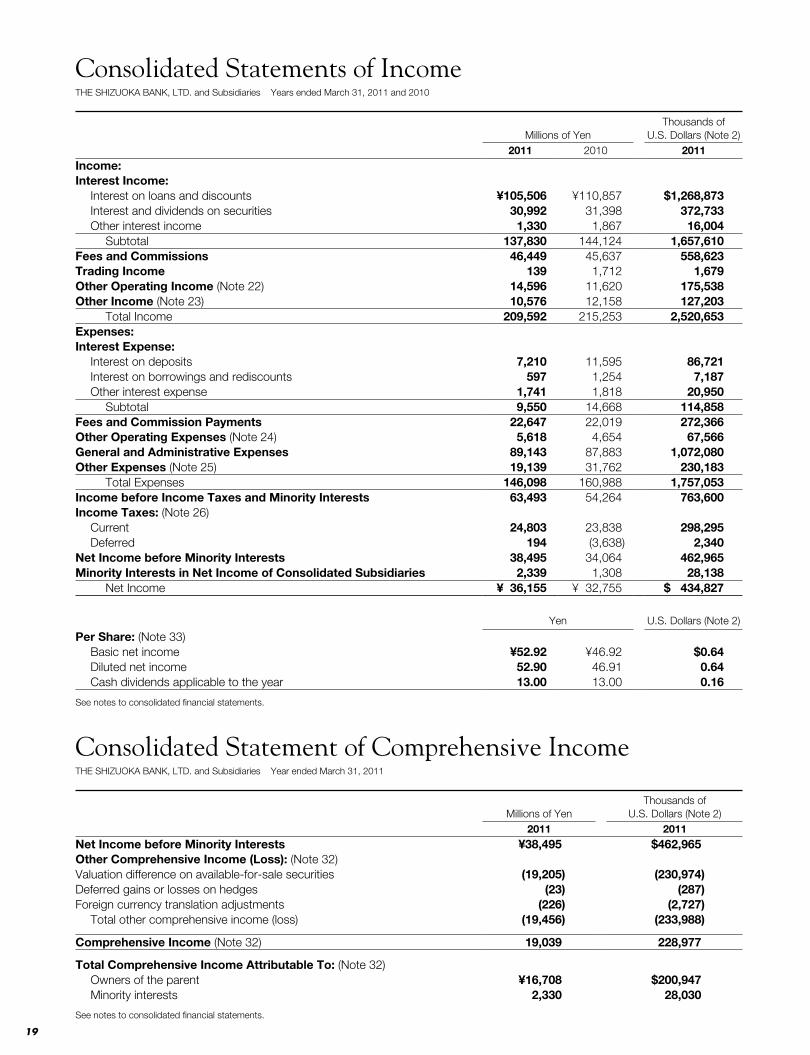

Consolidated Statements of IncomeTHE SHIZUOKA BANK, LTD. and Subsidiaries Years ended March 31, 2011 and 2010

Consolidated Statement of Comprehensive IncomeTHE SHIZUOKA BANK, LTD. and Subsidiaries Year ended March 31, 2011

Millions of Yen

Thousands of U.S. Dollars (Note 2)

2011 2010 2011Income:Interest Income:

Interest on loans and discounts ¥105,506 ¥110,857 $1,268,873 Interest and dividends on securities 30,992 31,398 372,733 Other interest income 1,330 1,867 16,004

Subtotal 137,830 144,124 1,657,610 Fees and Commissions 46,449 45,637 558,623 Trading Income 139 1,712 1,679 Other Operating Income (Note 22) 14,596 11,620 175,538 Other Income (Note 23) 10,576 12,158 127,203

Total Income 209,592 215,253 2,520,653 Expenses:Interest Expense:

Interest on deposits 7,210 11,595 86,721 Interest on borrowings and rediscounts 597 1,254 7,187 Other interest expense 1,741 1,818 20,950

Subtotal 9,550 14,668 114,858 Fees and Commission Payments 22,647 22,019 272,366 Other Operating Expenses (Note 24) 5,618 4,654 67,566 General and Administrative Expenses 89,143 87,883 1,072,080 Other Expenses (Note 25) 19,139 31,762 230,183

Total Expenses 146,098 160,988 1,757,053 Income before Income Taxes and Minority Interests 63,493 54,264 763,600Income Taxes: (Note 26)

Current 24,803 23,838 298,295Deferred 194 (3,638) 2,340

Net Income before Minority Interests 38,495 34,064 462,965 Minority Interests in Net Income of Consolidated Subsidiaries 2,339 1,308 28,138

Net Income ¥ 36,155 ¥ 32,755 $ 434,827

Yen U.S. Dollars (Note 2)

Per Share: (Note 33)Basic net income ¥52.92 ¥46.92 $0.64 Diluted net income 52.90 46.91 0.64 Cash dividends applicable to the year 13.00 13.00 0.16

See notes to consolidated financial statements.

Millions of Yen

Thousands of U.S. Dollars (Note 2)

2011 2011Net Income before Minority Interests ¥38,495 $462,965 Other Comprehensive Income (Loss): (Note 32)Valuation difference on available-for-sale securities (19,205) (230,974)Deferred gains or losses on hedges (23) (287)Foreign currency translation adjustments (226) (2,727)

Total other comprehensive income (loss) (19,456) (233,988)

Comprehensive Income (Note 32) 19,039 228,977

Total Comprehensive Income Attributable To: (Note 32)Owners of the parent ¥16,708 $200,947 Minority interests 2,330 28,030

See notes to consolidated financial statements.

20

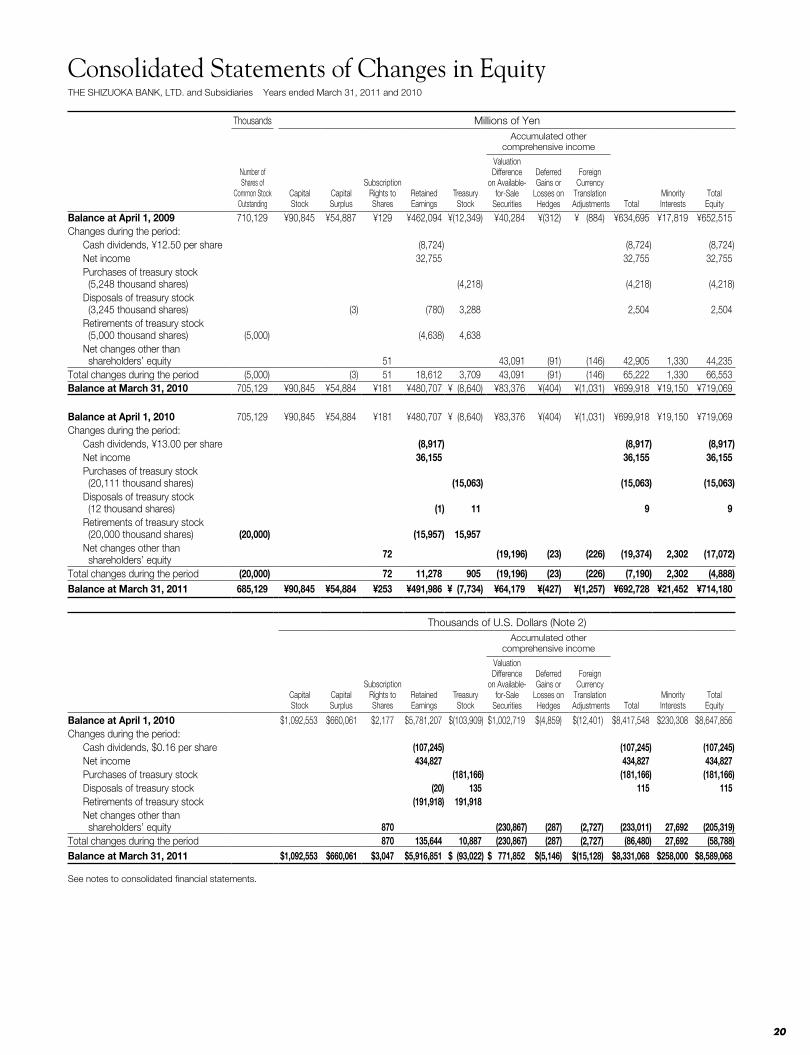

Consolidated Statements of Changes in EquityTHE SHIZUOKA BANK, LTD. and Subsidiaries Years ended March 31, 2011 and 2010

Thousands Millions of YenAccumulated other

comprehensive income

Number of Shares of

Common StockOutstanding

CapitalStock

CapitalSurplus

SubscriptionRights to Shares

Retained Earnings

Treasury Stock

Valuation Difference

on Available-for-Sale

Securities

Deferred Gains or

Losses on Hedges

Foreign Currency

Translation Adjustments Total

Minority Interests

TotalEquity

Balance at April 1, 2009 710,129 ¥90,845 ¥54,887 ¥129 ¥462,094 ¥(12,349) ¥40,284 ¥(312) ¥ (884) ¥634,695 ¥17,819 ¥652,515Changes during the period:

Cash dividends, ¥12.50 per share (8,724) (8,724) (8,724)Net income 32,755 32,755 32,755 Purchases of treasury stock (5,248 thousand shares) (4,218) (4,218) (4,218) Disposals of treasury stock (3,245 thousand shares) (3) (780) 3,288 2,504 2,504Retirements of treasury stock (5,000 thousand shares) (5,000) (4,638) 4,638 Net changes other than shareholders’ equity 51 43,091 (91) (146) 42,905 1,330 44,235

Total changes during the period (5,000) (3) 51 18,612 3,709 43,091 (91) (146) 65,222 1,330 66,553Balance at March 31, 2010 705,129 ¥90,845 ¥54,884 ¥181 ¥480,707 ¥ (8,640) ¥83,376 ¥(404) ¥(1,031) ¥699,918 ¥19,150 ¥719,069

Balance at April 1, 2010 705,129 ¥90,845 ¥54,884 ¥181 ¥480,707 ¥ (8,640) ¥83,376 ¥(404) ¥(1,031) ¥699,918 ¥19,150 ¥719,069Changes during the period:

Cash dividends, ¥13.00 per share (8,917) (8,917) (8,917)Net income 36,155 36,155 36,155 Purchases of treasury stock (20,111 thousand shares) (15,063) (15,063) (15,063) Disposals of treasury stock (12 thousand shares) (1) 11 9 9 Retirements of treasury stock (20,000 thousand shares) (20,000) (15,957) 15,957 Net changes other than shareholders’ equity 72 (19,196) (23) (226) (19,374) 2,302 (17,072)

Total changes during the period (20,000) 72 11,278 905 (19,196) (23) (226) (7,190) 2,302 (4,888)Balance at March 31, 2011 685,129 ¥90,845 ¥54,884 ¥253 ¥491,986 ¥ (7,734) ¥64,179 ¥(427) ¥(1,257) ¥692,728 ¥21,452 ¥714,180

Thousands of U.S. Dollars (Note 2) Accumulated other

comprehensive income

CapitalStock

CapitalSurplus

SubscriptionRights to Shares

Retained Earnings

Treasury Stock

Valuation Difference

on Available-for-Sale

Securities

Deferred Gains or

Losses on Hedges

Foreign Currency

Translation Adjustments Total

Minority Interests

TotalEquity

Balance at April 1, 2010 $1,092,553 $660,061 $2,177 $5,781,207 $(103,909) $1,002,719 $(4,859) $(12,401) $8,417,548 $230,308 $8,647,856Changes during the period:

Cash dividends, $0.16 per share (107,245) (107,245) (107,245)Net income 434,827 434,827 434,827 Purchases of treasury stock (181,166) (181,166) (181,166)Disposals of treasury stock (20) 135 115 115Retirements of treasury stock (191,918) 191,918 Net changes other than shareholders’ equity 870 (230,867) (287) (2,727) (233,011) 27,692 (205,319)

Total changes during the period 870 135,644 10,887 (230,867) (287) (2,727) (86,480) 27,692 (58,788)Balance at March 31, 2011 $1,092,553 $660,061 $3,047 $5,916,851 $ (93,022) $ 771,852 $(5,146) $(15,128) $8,331,068 $258,000 $8,589,068

See notes to consolidated financial statements.

21

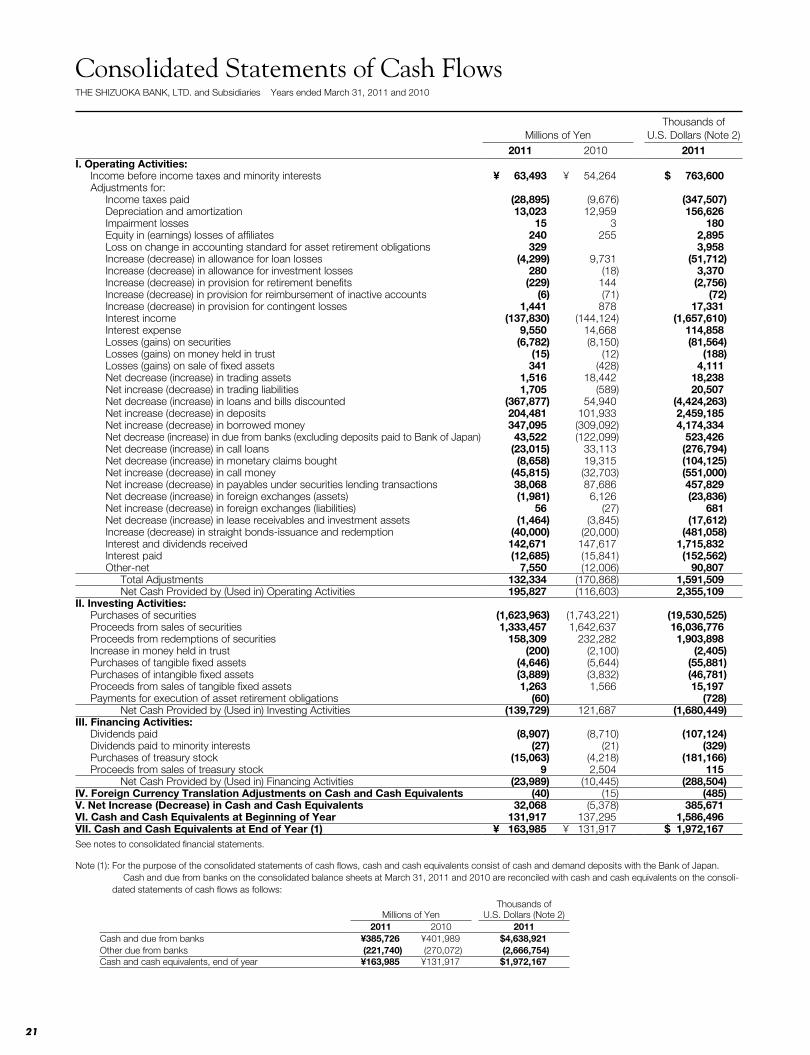

Consolidated Statements of Cash FlowsTHE SHIZUOKA BANK, LTD. and Subsidiaries Years ended March 31, 2011 and 2010

Millions of Yen

Thousands of U.S. Dollars (Note 2)

2011 2010 2011I. Operating Activities:

Income before income taxes and minority interests ¥ 63,493 ¥ 54,264 $ 763,600 Adjustments for:

Income taxes paid (28,895) (9,676) (347,507)Depreciation and amortization 13,023 12,959 156,626 Impairment losses 15 3 180 Equity in (earnings) losses of affiliates 240 255 2,895 Loss on change in accounting standard for asset retirement obligations 329 3,958 Increase (decrease) in allowance for loan losses (4,299) 9,731 (51,712)Increase (decrease) in allowance for investment losses 280 (18) 3,370 Increase (decrease) in provision for retirement benefits (229) 144 (2,756)Increase (decrease) in provision for reimbursement of inactive accounts (6) (71) (72)Increase (decrease) in provision for contingent losses 1,441 878 17,331 Interest income (137,830) (144,124) (1,657,610)Interest expense 9,550 14,668 114,858Losses (gains) on securities (6,782) (8,150) (81,564)Losses (gains) on money held in trust (15) (12) (188)Losses (gains) on sale of fixed assets 341 (428) 4,111 Net decrease (increase) in trading assets 1,516 18,442 18,238 Net increase (decrease) in trading liabilities 1,705 (589) 20,507 Net decrease (increase) in loans and bills discounted (367,877) 54,940 (4,424,263)Net increase (decrease) in deposits 204,481 101,933 2,459,185 Net increase (decrease) in borrowed money 347,095 (309,092) 4,174,334Net decrease (increase) in due from banks (excluding deposits paid to Bank of Japan) 43,522 (122,099) 523,426 Net decrease (increase) in call loans (23,015) 33,113 (276,794)Net decrease (increase) in monetary claims bought (8,658) 19,315 (104,125)Net increase (decrease) in call money (45,815) (32,703) (551,000)Net increase (decrease) in payables under securities lending transactions 38,068 87,686 457,829 Net decrease (increase) in foreign exchanges (assets) (1,981) 6,126 (23,836)Net increase (decrease) in foreign exchanges (liabilities) 56 (27) 681 Net decrease (increase) in lease receivables and investment assets (1,464) (3,845) (17,612)Increase (decrease) in straight bonds-issuance and redemption (40,000) (20,000) (481,058)Interest and dividends received 142,671 147,617 1,715,832Interest paid (12,685) (15,841) (152,562)Other-net 7,550 (12,006) 90,807

Total Adjustments 132,334 (170,868) 1,591,509 Net Cash Provided by (Used in) Operating Activities 195,827 (116,603) 2,355,109

II. Investing Activities:Purchases of securities (1,623,963) (1,743,221) (19,530,525)Proceeds from sales of securities 1,333,457 1,642,637 16,036,776 Proceeds from redemptions of securities 158,309 232,282 1,903,898 Increase in money held in trust (200) (2,100) (2,405)Purchases of tangible fixed assets (4,646) (5,644) (55,881)Purchases of intangible fixed assets (3,889) (3,832) (46,781)Proceeds from sales of tangible fixed assets 1,263 1,566 15,197 Payments for execution of asset retirement obligations (60) (728)

Net Cash Provided by (Used in) Investing Activities (139,729) 121,687 (1,680,449)III. Financing Activities:

Dividends paid (8,907) (8,710) (107,124)Dividends paid to minority interests (27) (21) (329)Purchases of treasury stock (15,063) (4,218) (181,166)Proceeds from sales of treasury stock 9 2,504 115

Net Cash Provided by (Used in) Financing Activities (23,989) (10,445) (288,504)IV. Foreign Currency Translation Adjustments on Cash and Cash Equivalents (40) (15) (485)V. Net Increase (Decrease) in Cash and Cash Equivalents 32,068 (5,378) 385,671 VI. Cash and Cash Equivalents at Beginning of Year 131,917 137,295 1,586,496 VII. Cash and Cash Equivalents at End of Year (1) ¥ 163,985 ¥ 131,917 $ 1,972,167 See notes to consolidated financial statements.

Note (1): For the purpose of the consolidated statements of cash flows, cash and cash equivalents consist of cash and demand deposits with the Bank of Japan. Cash and due from banks on the consolidated balance sheets at March 31, 2011 and 2010 are reconciled with cash and cash equivalents on the consoli-dated statements of cash flows as follows:

Millions of Yen

Thousands of U.S. Dollars (Note 2)

2011 2010 2011Cash and due from banks ¥385,726 ¥401,989 $4,638,921 Other due from banks (221,740) (270,072) (2,666,754)Cash and cash equivalents, end of year ¥163,985 ¥131,917 $1,972,167

22

1. BASIS OF PRESENTATIONThe accompanying consolidated financial statements have been prepared from the accounts maintained by The Shizuoka Bank, Ltd. (the “Bank”) and its subsidiaries (the “Group”) in accordance with the provisions set forth in the “Companies Act,” the Japanese Financial Instruments and Exchange Act, the Banking Act of Japan and the Accounting Guideline for Banks in Japan stated by the Japanese Bankers’ Association and accounting principles generally accepted in Japan (“Japanese GAAP”), which are different in certain respects as to the application and disclosure requirements of International Financial Reporting Standards (“IFRS”).