Embed Size (px)

Citation preview

Shining a Light on the SFT Regulation and an Update on Shadow Banking Reform

Teleconference

Tuesday, May 24, 2016 12:00PM – 1:00PM EDT

Presenters:

Peter J. Green, Partner, Morrison & Foerster LLP

Jeremy C. Jennings-Mares, Partner, Morrison & Foerster LLP

1. Presentation

2. Morrison & Foerster User Guide:

“The Long Long Game: The EU Financial Regulatory Agenda into 2016 and Beyond”

3. Morrison & Foerster Client Alert:

“Casting Light on Shadows: New Transparency Rules for Securities Finance Transactions”

4. Morrison & Foerster Client Alert:

“Possible Worlds Versus Probable Worlds − the Metaphysics of Systemic Risk: FSOC Revisits Asset Managers”

5. Fund Board Views Article:

“Derivatives Rule Proposal: More Work for Overburdened Fund Directors”

6. Morrison & Foerster Client Alert: “SEC Proposes Rules to Require Funds to Adopt Liquidity Risk Management Programs; Allow ‘Swing Pricing’”

©

2014 M

orr

ison &

Foers

ter

LLP

| A

ll R

ights

Reserv

ed | m

ofo

.com

Shining a Light on the SFT

Regulation and an Update on

Shadow Banking Reform

24 May 2016

Presented by:

Peter Green

Jeremy Jennings-Mares

LN2-12648

2

A Brief History of Shadow Banking Reform

• Financial crisis and concerns that crisis was partly caused and/or

exacerbated by banking activities carried out by non banks:

securitisation/CDOs

SIVs/ABCP conduits

credit derivatives

• Potential systemic risks arising from such activities

• G20 summit at Seoul in 2010 mandated FSB to develop oversight

and regulation of shadow banking system

• Various background papers, consultative documents and related

papers published by FSB

• FSB work now focussed on five workstreams

• EU Commission Green Paper published March 2012 and EU

Commission Communication published in September 2013

• Legislation in place or being developed in many areas

3

What is “Shadow Banking”?

• FSB background note – 12 April 2011:

no clear definition

activities outside the regular banking system that involve bank-

like functions

non-bank credit intermediation

focus on activities that give rise to systemic risks, in particular

through maturity or liquidity transformation, leverage and flawed

credit risk transfer

• FSB, EU Commission and other regulators have stressed

that any definition should not be rigid and should be

capable of adapting to changes and developments in the

financial markets

4

What is “Shadow Banking”? (cont.)

• EU Commission Green Paper published in March 2012 approved

FSB definition and set out non-exhaustive list of entities and activities

it believes fall within the ambit of shadow banking

Entities • Special purpose entities performing liquidity and / or maturity transformation (eg ABCP conduits,

securitisation SPVs, SIVs)

• Money market funds and similar vehicles with deposit-like characteristics making them vulnerable

to runs

• Investment funds providing credit or that are leveraged (eg ETFs)

• Finance companies / securities entities providing credit or guarantees or unregulated liquidity /

maturity transformation

• Insurance / reinsurance undertakings issuing or guaranteeing credit products

Activities

• Securitisation

• Securities lending and repos

5

Shadow Banking: FSB Monitoring and

Workstreams

• In conjunction with the G20 leaders, the FSB has adopted a two

pronged strategy to address financial stability risks in shadow

banking

• First, it has created a system-wide monitoring framework to track

developments in shadow banking and to identify the build up of

systemic risks with a view to taking necessary corrective action

• Secondly, it has developed five workstreams to strengthen the

oversight and regulation of shadow banking:

dampening procyclicality and other financial stability risks in securities financing

transactions such as repos and securities lending

reducing the susceptibility of money market funds to runs

mitigating risks in banks’ interactions with shadow banking entities

improving the transparency and aligning the incentives in securitisation

assessing and mitigating financial stability risks posed by other shadow banking

entities and activities

6

Regulation of Securities Lending and Repos

• FSB acknowledges securities and repo markets are vital in

supporting secondary market liquidity for many securities:

central to financial intermediaries’ ability to make markets and facilitate risk

management and collateral management strategies

core funding markets for some financial institutions

key to money market and refinancing operations in many jurisdictions

can, however, lead to bank-like activities including maturity and liquidity

transformation and leverage

7

Regulation of Securities Lending and Repos (cont.)

• FSB’s specific concerns include:

ensuring competent authorities have sufficient visibility on the build-up of leverage

and illiquidity

extent of reinvestment of cash collateral given for securities lending (and the

potential for maturity and liquidity transformation)

potential for securities financing to cause pro-cyclicality in the banking system

tendency of creditors in repo and securities lending sectors to sell collateral

securities immediately upon a counterparty default, potentially causing a

downwards spiral

possibility of re-hypothecation of client assets causing risks to financial stability if

there is uncertainty as to the treatment of re-hypothecated assets in the event of

an insolvency

8

Regulation of Securities Lending and Repos (cont.)

• FSB developed 11 policy recommendations for this workstream,

including:

improving regulatory reporting to obtain more granular information on exposures

improving collection of trade level data and regular snapshots of outstanding

balances for repo markets (particularly through trade repositories)

total national and regional data for repos and securities lending should be

aggregated by FSB

improving reporting by fund managers to end-investors

limiting risks associated with cash collateral reinvestment

addressing risks associated with re-hypothecation of client assets

strengthening collateral valuation and management practices

evaluating the establishment or wider use of central clearing

changing bankruptcy law treatment of repos and securities lending transactions

9

FSB Framework for Haircuts on Non-centrally cleared

SFTs

• FSB proposals for consultation on minimum standards for

methodologies in calculating haircuts and for a minimum haircut

framework

• In November 2013, FSB launched quantitative impact study on

detailed proposals for the haircut framework

• In October 2014 the FSB published its regulatory framework for

haircuts on non-centrally cleared securities financing transactions

contains FSB’s final recommendations on qualitative standards for methodologies

used by market participants to calculate haircuts

sets out numerical haircut floor framework

• FSB regulatory framework was revised in November 2015

10

FSB Framework for Haircuts on Non-centrally

cleared SFTs (cont.)

• Haircut methodologies:

framework sets out qualitative standards to be incorporated by regulatory

authorities

haircuts to be based on market risk of assets used as collateral and calibrated

over sufficiently long historical period (including at least one stress period)

regulatory authorities should set qualitative standards for methodologies used in

calculating collateral margins or haircuts, whether on an individual transaction or

portfolio basis, and should review those standards against FSB guidance by the

end of 2017

11

FSB Framework for Haircuts on Non-centrally

cleared SFTs (cont.)

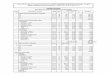

• The FSB sets out a table of numerical haircut floors:

12

FSB Framework for Haircuts on Non-centrally

cleared SFTs (cont.)

• FSB specific recommendations in relation to numerical floor are:

BCBS should review its capital treatment of non-centrally cleared securities

financing transactions and incorporate the framework of numerical framework

floors in the Basel framework by the end of 2015 (BCBS published a consultative

document in this regard on 5 November 2015)

national authorities should implement such framework of numerical haircut floors

by the end of 2018 (delay from previous recommendation of 2017)

national authorities should also introduce a framework of numerical haircut floors

on non-bank to non-bank transactions by the end of 2018. For jurisdictions with

larger securities financing activities this should be done using market regulation or

an entity-based approach (ideally market regulation in jurisdictions with the very

largest securities financing activities)

an initial assessment of the need and the implementation approach for introducing

the framework of numerical haircut floors on non-bank to non-bank transactions

should be conducted by national authorities by the end of 2018

13

FSB Standards for Data Collection and Aggregation

• In addition to its work on haircuts, the FSB has also developed

standards and processes for global securities financing data

collection and aggregation

• Finalised standards published in November 2015

implementation timetable aims at launching global data and aggregation in 2018

14

EU Regulation on SFTs - Overview

• European Commission Regulation on reporting and transparency of

securities financing transactions (SFTs) came into force on 12

January 2016

• Draft Regulation first proposed by EU Commission in January 2014

• Regulation focuses on transparency, disclosure and rehypothecation

(reuse of securities)

• Effective date for implementation of provisions is staggered as set out

further below

15

EU Regulation on SFTs - Scope

• Regulation applies to :

any counterparty to a SFT that is established in the EU or established outside the

EU if the SFT is concluded by a branch of that counterparty located in the EU

UCITS management companies and investment companies

managers of alternative investment funds authorised under the AIFMD

counterparties to “reuse” arrangements which are either established in the EU or

in a non-EU jurisdiction if the reuse is effected in the course of the operations of

an EU branch or the reuse concerns financial instruments provided as collateral

by a counterparty established in the EU or by an EU branch of a counterparty

established outside the EU

16

EU Regulation on SFTs – Scope (cont.)

• There is an exemption from the provisions of the Regulation relating

to the reporting and safeguarding obligations and the reuse of

financial instruments under a collateral arrangement for:

members of the European System of Central Banks and member state bodies

performing similar functions

EU public bodies charged with or intervening in the management of public debt

the Bank for International Settlements

17

EU Regulation on SFTs – Definition of SFT

• The Regulation defines a SFT under Article 3(11) as:

a repurchase transaction (including reverse repo transactions);

securities or commodities lending or borrowing;

a buy-sell back transaction or a sell-buy-back transaction; or

a margin lending transaction.

18

EU Regulation on SFTs – The Reporting Obligation

• Article 4 of the Regulation provides that counterparties to a SFT must

report, to a registered or recognised trade repository, the details of

any SFT that they have concluded, modified or terminated

reporting must be no later than the working day following the conclusion,

modification or termination of a transaction

details to be included in the reporting are to be specified in further RTS to be

developed by ESMA and adopted by the EU Commission (see further below)

the Regulation provides that reportable information must at least include details of

the parties to the SFT (and any beneficiaries), principal amount, currency, details

of collateral (including type, quality and value), whether the collateral is available

for reuse, repurchase rate, lending fee, margin lending rates, haircuts, value date

and maturity date

19

EU Regulation on SFTs – The Reporting

Obligation (cont.)

• Both counterparties have an obligation to report the details of a SFT

• A financial counterparty is responsible for reporting on behalf of both

counterparties where the other counterparty is:

a non financial counterparty

whose balance sheet does not exceed two of (i) EUR20m balance sheet total, (ii)

EUR 40m net turnover, (iii) 250 employee average during financial year

• Financial counterparty includes credit institutions, investment firms

authorised under MiFID, insurance undertakings authorised under

Solvency II, UCITS funds and an AIF whose manager is authorised or

registered under the AIFMD

• If a UCITS fund or AIF is the counterparty to a SFT, the UCITS

manager or the AIFM is responsible for reporting on behalf of the

UCITS fund or AIF

• Counterparties may delegate their reporting obligations but remain

liable in respect of the obligation

20

EU Regulation on SFTs – The Reporting Obligation

(cont.)

• Reporting is required to be made to a trade repository that is either:

located in the EU and registered under Article 5 of the Regulation or

located outside the EU and recognised under Article 19 of the Regulation

in either case, the relevant repository must meet the criteria for regulation

specified under EMIR

in the absence of a registered or recognised trade repository, reporting can be

made to ESMA

• Counterparties must keep records of any SFT they have concluded,

modified or terminated for least five years following termination of the

transaction

21

EU Regulation on SFTs – The Reporting Obligation

(cont.)

• The reporting requirement is to be phased in after adoption of the

relevant RTS

• The reporting requirement will apply on or after the relevant “phase-

in” date which will occur a specified number of months after the RTS

are adopted and enter into force – the number of months will vary

depending on the nature of the relevant counterparty:

12 months for EU investment firms or credit institutions or equivalent non-EU

entities

15 months for central counterparties and central securities depositories authorised

in the EU or equivalent non-EU entities

18 months for insurance and reinsurance undertakings, UCITS funds, AIFs,

institutions for occupational retirement provision and central counterparties, in

each case authorised in the EU (or equivalent non-EU entities)

21 months for non-financial counterparties established either in the EU or in a

non-EU jurisdiction

22

EU Regulation on SFTs – The Reporting Obligation

(cont.)

• In addition to SFTs traded on or after the applicable phase-in date,

back-loaded reporting of transactions will apply to transactions in

existence prior to the phase in date where:

the applicable SFT has a remaining maturity on the phase-in date of more than

180 days or

the applicable SFT has an open maturity and remains outstanding for 180 days

after the phase in date

• Back-loaded transactions shall be reported within 190 days of the

applicable phase-in date

23

EU Regulation on SFTs – Investor Transparency

• The Regulation contains provisions relating to transparency similar to

those contained in the UCITS V Directive and the AIFMD

• To enable investors to be made aware of the risks associated with the

use of SFTs, Articles 13 and 14 of the Regulation require fund

managers to provide pre-contractual and periodical information to

investors

24

EU Regulation on SFTs – Investor

Transparency (cont.)

• In the case of UCITS or AIF funds, pre-contractual information must

be provided to investors in either a UCITS prospectus or an AIF

disclosure, including:

a general description of the SFTs and total return swaps used by the fund and the

rationale for their use

in relation to each type of SFT and total return swaps used by the fund, data

relating to the types of assets subject to such transactions and the maximum and

expected proportion of assets under management to be the subject of such

transactions

criteria used to select counterparties (including legal statutes, country of origin and

minimum credit rating)

acceptable collateral

collateral valuation

a description of the risks linked to SFTs and total return swaps

specification of how assets subject to SFTs and total return swaps and collateral

received are kept safe

specification of any restrictions (regulatory or self-imposed) on the re-use of

collateral

25

EU Regulation on SFTs – Investor Transparency

(cont.)

• In relation to such funds, periodical information must be provided in a

UCITs half-yearly and annual reports and an AIF’s annual report:

global data relating to the amount of securities and commodities on loan as a

proportion of total lendable assets and the amount of assets engaged in each type

of SFT and total return swaps in absolute terms and as a proportion of funds

under management

concentration data relating to the top ten collateral issuers across all SFTs and

total return swaps and the top ten counterparties of each type of SFT and total

return swap

aggregate transaction data for each type of SFT and total return swap including

type and quality of collateral, maturity tenor of collateral and SFTs in specified

maturity buckets, currency of collateral and country of domicile of counterparty

data on the reuse of collateral, including the share of collateral received that is

reused compared to the maximum amount specified in pre-contractual information

provided to investors

26

EU Regulation on SFTs – Investor Transparency

(cont.)

• Obligation on UCITS and AIFMs to disclose their use of SFTs and

total return swaps in financial reports becomes effective 12 months

after the Regulation comes into force

• Obligation on UCITS and AIFMs to disclose use of SFTs and total

return swaps in prospectuses/pre-investment disclosure becomes

effective 18 months after the Regulation comes into force for AIFs

and UCITS funds that are constituted prior to the Regulation coming

into force

27

EU Regulation on SFTs – Reuse of Collateral

• Reuse of collateral is defined as:

the use of financial instruments by an entity receiving such instruments under a

collateral arrangement in its own name and on its own account, or on the account

of another counterparty, including a natural person (the “receiving counterparty”)

• The use can comprise transfer of title or exercise of a right of use in

accordance with a security financial collateral arrangement:

does not include the liquidation of a financial instrument in the event of default of

the entity providing the collateral

• Rules on re-use of collateral become effective 6 months after the

Regulation came into force (so 12 July 2016)

28

EU Regulation on SFTs – Reuse of Collateral (cont.)

• Article 15 of the Regulation specifies certain conditions that must be

complied with if a receiving counterparty has a right to reuse financial

instruments it receives as collateral:

the providing counterparty must be informed in writing of the risks and

consequences in (i) granting consent to a right of collateral under a security

financial collateral arrangement or (ii) concluding a title transfer collateral

arrangement

the providing party must (i) grant its prior express signed consent to the applicable

security financial collateral arrangement containing a right of use of collateral or (ii)

expressly agree to provide collateral by way of a title transfer collateral

arrangement

the reuse must be carried out in accordance with the terms of the applicable

collateral arrangement

the financial instruments received by the receiving counterparty must be

transferred from the account of the providing counterparty

29

EU Regulation on SFTs – Administrative Sanctions

• Member states are required to provide their competent authorities

with the power to impose administrative sanctions and other

administrative measures in respect of breaches of the reporting and

reuse obligations under the Regulation

• Sanctions available to competent authorities include:

cease and desist orders

public censure

withdrawal or suspension of authorisation

temporary banning orders

administrative fines

30

EU Regulation on SFTs – Third Country Issues

• The EU Commission may adopt implementing acts determining the

equivalence of non-EU reporting regimes:

such rules must ensure secrecy of information and be applied and enforced in a

manner commensurate with the rules under the Regulation

31

EU Regulation on SFTs - RTS

• On 11 March 2016, ESMA published draft RTS relating to the

Regulation

• RTS cover principally technical areas, including:

technical standards regarding the registration of trade repositories in respect of

the reporting obligation

the format of reports to be made under the Regulation including the content and

structure of the report

operational standards for data collection by trade repositories and data to be

provided to competent authorities

• RTS were open for consultation until 22 April 2016

• ESMA expect to produce a final report on the RTS by Q3 2016 for

endorsement by the EU Commission by 13 January 2017

32

Regulatory Reform of Money Market Funds

• FSB has stated that MMFs are an important element of the shadow

banking system:

provision of maturity and liquidity transformation

important source of short-term funding for banks

• Historically MMFs have been regarded as a safe investment with a

stable NAV

• During financial crisis some MMFs suffered large losses due to

holdings of ABS and other financial instruments:

significant drop in NAVs of some funds

prompted investor redemptions and instability

in 2008, the Prime Reserve Fund in the US “broke the buck” due to large holdings

in Lehman Brothers paper

• IOSCO Reports: April 2012 and October 2012

33

Regulatory Reform of Money Market Funds (cont.)

• IOSCO identified on-going vulnerabilities of MMFs which could

destabilise the financial system:

stable NAV features gives impression of safety but MMFs are subject to credit,

interest rate and liquidity risk

“first mover advantage” for investors who redeem MMF shares at first sign of

market distress – stable NAV feature means losses are borne by remaining

shareholders

discrepancies between published NAV and realisable value of assets

implicit support from sponsors results in investors perceiving MMFs as less risky

than they are

importance of ratings in MMF regulations

34

Regulatory Reform of Money Market Funds (cont.)

• IOSCO final report made 15 policy recommendations, which have

been endorsed by the FSB, including:

MMFs should be explicitly defined in regulation of collective investment schemes

need for compliance with general principles of fair value when valuing securities in

portfolio

holding of a minimum amount of liquid assets to meet redemptions and prevent

fire sales

MMFs that offer a stable NAV should be subject to measures designed to reduce

specific risks associated with the stable NAV feature

MMF regulation should strengthen internal credit risk assessment practices

documentation should disclose the absence of a capital guarantee

regulators should, where necessary, develop guidelines strengthening the

framework applicable to the use of repos by MMFs

35

SEC Regulation of Money Market Funds (cont.)

• In July 2014, following a consultation on previous proposals, the SEC

voted 3-2 to adopt amended rules relating to MMFs

• Rule amendments comprised of two principal components:

floating NAV requirement for MMFs other than retail and government funds

liquidity fees and gates

36

SEC Regulation of Money Market Funds (cont.)

• Floating NAV:

institutional MMFs (other than government MMFs) must fix NAV based on the

current market value of their underlying securities rounded to four decimal places

funds may value fixed income securities with remaining maturity of 60 days or less

at amortised cost (rather than current market value) when the fund can reasonably

conclude, each time it makes a value determination, that amortised cost is

approximately the same as the fair value of the security as determined without the

use of amortised cost valuation

retail MMFs may continue to use amortised cost

retail MMFs are defined as funds that limit beneficial owners to natural persons

retail MMFs must adopt policies reasonably designed to enforce limitation to

natural persons

governmental MMF is one that invests at least 99.5% of its total assets in cash,

government securities and/or repurchase agreements collateralised by cash or

government securities

37

SEC Regulation of Money Market Funds (cont.)

Liquidity fees and redemption gates:

• Liquidity fees:

if non-government MMF’s “weekly liquid assets” fall below 30% of total assets,

the fund board has discretion to impose a liquidity fee of 2% on all redemptions if it

determines that fee is in the best interests of the MMF

the fund board can impose a lesser or no fee if determined to be in the fund’s best

interests

all non-government MMFs must impose a liquidity fee of 1% if weekly liquid assets

fall below 10% of total assets unless the board determines such a fee is not in the

MMF’s best interests MMF’s best interests - fund directors may impose fees of up

to 2% on redemptions

• Redemption gates:

if weekly liquid assets fall below 30%, the board may also suspend redemptions

for up to 10 days in any 90 day period

• Government MMFs are not bound by fee and gate requirements but

could impose them if disclosed in the prospectus

38

SEC Regulation of Money Market Funds (cont.)

• Other requirements of the amended rules include:

enhanced registration statement and website disclosure about any financial

support provided by fund’s sponsor or an affiliate and daily reporting of NAV per

share

additional disclosure requirements re net inflows and outflows and daily and

weekly liquidity levels

new form N-CR which must be filed within one business day of certain events,

e.g. imposition or lifting of redemption gates, defaults in an underlying security and

decline in NAV below $0.9975 for stable NAV fund

removal of 25% bucket for guarantees or demand features from a single

institution. Up to 15% of a tax-exempt MMF’s total assets may be subject to

guarantees or demand features from a single institution provided that any demand

feature or guarantee acquisition in excess of 10% of fund’s total assets must be a

demand feature or a guarantee issued by a non-controlled person

other amendments which promote greater diversification

additional stress testing requirements

39

SEC Regulation of Money Market Funds (cont.)

• Effective date of SEC Amendments:

floating NAV fees and gates: October 14, 2016 (2 years after the Effective Date)

reporting requirements: July 14, 2015 (9 months after the Effective Date)

diversification, stress testing etc: April 14, 2016 (18 months after the Effective

Date)

• Fall out from new MMF regulations:

some observers believe that fees and gates will increase the likelihood of pre-

emptive runs

will federal banking regulators, through FSOC, require additional protections?

40

Draft EU Money Market Fund Regulation

• In December 2012 the European Systemic Risk Board published four

broad recommendations in relation to MMFs:

a mandatory move to variable NAV in most cases

greater requirements for monitoring of liquidity risks and having measures in place

to deal with liquidity constraints

greater public disclosure of absence of capital guarantee, valuation practices and

redemption procedures

enhanced reporting requirements

41

Draft EU Money Market Fund Regulation

• Draft Regulation published by EU Commission on 4 September 2013

• Departed from a number of the ESRB recommendations

• Draft Regulation proposes to limit investment by MMFs to: money market instruments (with high internal credit rating)

deposits of no more than 12 months (or on demand) with eligible credit institutions

financial derivatives (for hedging maturity and fx risks only)

reverse repos (maximum close-out facility of two working days)

• Subsequent negotiation during EU legislative process has been

detailed and time consuming: concerns in particular raised by EU parliament over requirement that constant NAV MMFs

should have a 3% capital buffer in place

concerns also on restrictions on permitted investments

• EU parliament has voted in favour of amendments to the draft

Regulation and the EU Council of Ministers subsequently published a

comprise proposal on 10 May 2016

• Following slides reflect current Council Compromise proposal

42

Draft EU Money Market Fund Regulation (cont.)

• Current compromise draft envisages that MMFs may be established

in the EU as either:

Variable Net Asset Value MMF (VNAV)

Constant Net Asset Value MMF (CNAV)

Low Volatility Net Asset Value MMF (LVNAV)

• CNAV must:

seek to maintain an unchanging NAV per unit or share

accrue income in the fund to either be paid to the investor or be used to purchase

more fund units or shares

generally value assets according to the amortised cost method and/or round the

NAV to the nearest percentage point

invest at least 99.5% of its assets in specified assets and cash (see below)

43

Draft EU Money Market Fund Regulation (cont.)

• LVNAV MMFs must comply with specific requirements including:

LVNAV may be valued using the amortised cost method only if it has a residual

maturity up to 75 days (and provided such value does not deviate from a mark to

market or mark to model valuation by more than 10 basis points)

calculate a constant NAV per share on at least a daily basis on the basis specified

in the Regulation

the LVNAV must also calculate a mark to market or mark to model valuation and

continuously monitor the difference between such value and the constant NAV

value

the units or shares of a LVNAV may be issued or redeemed at a price equal to the

constant NAV provided such value does not deviate from the NAV per share or

unit calculated on a mark to market or mark to model valuation by more than 20

basis points

potential investors must be clearly warned of the circumstances in which shares or

units will not be redeemed on a constant NAV basis

44

Draft EU Money Market Fund Regulation (cont.)

• Investment restrictions provide that a MMF may only invest in:

high quality money market investments (“high quality” is to be assessed by an

internal credit quality procedure in accordance with the Regulation)

eligible securitisations and asset backed commercial paper (ABCP)

financial derivative instruments

repurchase agreements and reverse repurchase agreements

units or shares of other MMFs

• Eligible securitisations and ABCP comprise:

securitisations eligible to be included in the LCR under CRD IV

an ABCP which is fully supported by a credit institution under CRD IV that covers

all liquidity, credit and material dilution risks as well as transaction and programme

wide costs

securitisations designated as a “simple, transparent and standardised”

securitisations under the forthcoming Securitisation Regulation

45

Draft EU Money Market Fund Regulation (cont.)

• Further criteria are specified for the other categories of permitted

investments.

• Certain investment activities are expressly prohibited by the

Regulation:

short-selling

taking direct or indirect exposure to equity or commodities, including through

derivatives or indices

entering into securities lending or borrowing agreements or other agreements that

would encumber the assets of the MMF

borrowing and lending cash

46

Draft EU Money Market Fund Regulation (cont.)

• The Regulation imposes diversification requirements on an MMF:

maximum 5% issuer limit for money market instruments (for VNAV MMFs the limit

is 10% provided the aggregate value of instruments held above 5% in any

instrument does not exceed 40%)

10% limit on deposits with a single credit institution

aggregate 15% limit on permitted securitisation exposures

cap on value of assets transferred under permitted repurchase agreements of

10% of MMF’s assets

maximum risk exposure to same counterparty in respect of OTC derivatives of 5%

aggregate cash provided to same counterparty to reverse repos not to exceed

20% of MMF’s assets

• In addition to limits above, a MMF may not combine investments in

money market instruments, deposits and OTC derivative exposures to

the same body if that would exceed 20% of the MMFs assets

• A MMF must not hold more than 10% of the money market instruments

issued by a single body

47

Draft EU Money Market Fund Regulation (cont.)

• The Regulation will also impose portfolio rules for standard MMFs

(does not include CNAV or LVNAV MMFs):

portfolio not to have a weighted average maturity (WAM) of more than 6 months

portfolio to have a weighted average life (WAL) of no more than 12 months at any

time

at least 10% of assets to be comprised of daily maturing assets (including reverse

repos that can be terminated on one business day’s notice)

• Different rules for short-term MMF portfolios (which must have a legal

or residual maturity of 397 days or less and meet other criteria

specified in the Regulation):

WAM of no more than 60 days

WAL of no more than 120 days

48

Draft EU Money Market Fund Regulation (cont.)

• Regulation imposes specific rules relating to liquidity fees and/or redemption gates

and/or suspension of redemptions for CNAV and LVNAV MMFS

• Manager of a CNAV or LVNAV MMF must establish, implement and consistently apply

prudent and rigorous liquidity management procedures for controlling the weekly

liquidity thresholds applicable to such funds

• Where the proportion of weekly maturing assets falls below a 30% threshold of the

assets of the MMF, the manager must inform the Board of the MMF which must make

a “documented and well-reasoned” assessment of the situation and, acting in the best

interests of investors, decide whether to apply one more of the following measures:

liquidity fees on redemptions up to 2%

redemption gates limiting the amount of shares or units to be redeemed on any

dealing day to a maximum of 10% (for up to 15 dealing days)

suspension of redemptions for up to 15 days

49

Draft EU Money Market Fund Regulation (cont.)

• If the proportion of weekly maturing asset falls below 10% of total

assets, the manager shall inform the Board which, following a

documented and well-reasoned assessment of the situation, shall,

acting in the best interests of investors, impose

liquidity fees of at least 1% (not exceeding 2%) on redemptions

suspension of redemptions for any period up to 15 days

• If within a period of 90 days, aggregated suspensions exceed 15

days, a CNAV or LVNAV MMF shall automatically cease to be a

CNAV or LVNAV MMF and shall be prohibited from using the

amortised cost or rounding method

50

Draft EU Money Market Fund Regulation (cont.)

• The Regulation imposes various transparency and reporting

obligations:

MMF must indicate what type of MMF it is and whether it is a short-term or

standard MMF

MMF must report information to its competent authority on at least a quarterly

basis

documents used for marketing purposes must contain certain statements including

that the MMF is not a guaranteed investment, that it does not rely on external

support for guaranteeing the liquidity of the MMF or stabilising the NAV per unit or

share and that the risk of loss of the principal has to be borne by the investor

51

Draft EU Money Market Fund Regulation (cont.)

• The Regulation provides that a MMF shall not receive external

support

• External support is stated to be any direct or indirect support offered

by a third party that is intended for or in effect would result in

guaranteeing the liquidity of the MMF or stabilising the NAV per unit

or share including:

cash injections

purchase of assets at an inflated price

purchase by a third party of units or shares of the MMF

issuance of any kind of explicit or implicit guarantee, warranty or letter of support

for the benefit of the MMF

52

Draft EU Money Market Fund Regulation (cont.)

• Previous proposal for a 3% capital buffer is removed from the latest

compromise draft

• Existing MMFs will have 2 years to comply with the Regulation after it

comes into force

• Regulation is still subject to further negotiation and change

53

Interaction of Regular Banking System with Shadow

Banking

• Various amendments have been made to banks’ capital requirements

under Basel II.5 and III. Measures that have been or are in the

process of being adopted include:

increased capital requirements for banks’ exposures to resecuritisations and

liquidity facilities provided to securitisation vehicles

increased capital requirements under the IRB approach for exposures to regulated

financial institutions whose total assets are equal to or greater than US$100bn

and to unregulated financial institutions

enhanced banks’ internal capital adequacy process under Pillar 2 for securitisation

risk, reputational risk and implicit support

enhanced Pillar 3 disclosure requirements in relation to securitisation

• BCBS is continuing to develop guidance to improve international

consistency of consolidation for prudential regulatory purposes

54

Interaction of Regular Banking System with Shadow

Banking (cont.)

• In December 2013, BCBS published final policy framework for

calculating capital requirements for banks’ equity investments in

funds held in their banking book:

financial standard will apply from 1 January 2017

BCBS aims for consistent approach between banking book and trading book

• In April 2014, BCBS published its final standards for the framework

for measuring and controlling banks’ large exposures seeking to take

account of risks arising from shadow banking:

to apply from 1 January 2019

overall limit on large exposures of 25% of Tier 1 capital (15% for G-SIBs)

EBA published Guidelines on exposures to shadow banking entities in December

2015

55

Regulation of other Shadow Banking Entities

• FSB has examined the extent to which non-bank financial entities (other than

MMFs) pose systemic risks:

policy framework published in August 2013

• Focus on economic functions carried out by relevant entities rather than

focussing purely on legal names or forms

• FSB recommends that regulatory authorities identify shadow banking risks in

non-financial entities by focussing on a framework of five economic functions:

management of cash pools with features making them susceptible to runs

loan provision that is dependent on short term funding

intermediation of market activities dependent on short term funding or on secured

funding of client assets

facilitation of credit creation

securitisation and funding of financial entities

56

Regulation of other Shadow Banking Entities

(cont.)

• FSB has launched an information-sharing exercise among all its

member jurisdictions to exchange information on the status of

national authorities’ implementation of the framework

• In July 2015 the FSB also launched a thematic peer review to

evaluate progress in implementing the policy framework

57

Regulation of other Shadow Banking Entities (cont.)

• In January 2014 FSB/IOSCO published a consultation paper on

assessment methodologies for identifying non-bank, non-insurer Global

SIFIs:

basic set of impact factors included size, interconnectedness, substitutability,

complexity and cross-jurisdictional activities

assessment methodologies to measure impact of entity’s failure on global financial

system and wider economy

establishment of international oversight group

sector-specific methodologies

• Further FSB/IOSCO consultation paper expected shortly

• In US under Dodd-Frank, FSOC has already designated four non-banks

as SIFIs: GE Capital, AIG, Prudential and Met Life

on March 30, 2016 – US federal court overturned FSOC’s designation of Met Life

including calling such designation “arbitrary and capricious”.

58

Regulation of other Shadow Banking Entities (cont.)

• FSOC has, with SEC, considered whether asset management firms

could pose a systemic risk and potentially be designated as SIFIs

SEC consultation in 2013

• In December 2014 the SEC chair outlined three initiatives for the

investment management industry:

expanded data reporting for registered investment companies and investment

advisers

enhanced controls on risks relating to portfolio composition

improved transition planning and stress testing

• In December 2014 the FSOC issued a public consultation on whether

asset management products and activities may pose potential risks to

the US financial system:

liquidity and redemptions – FSOC asks whether pooled investment vehicles that

provide for liquidity (e.g. mutual funds) have a greater incentive to redeem in times

of market stress than if investors held the underlying securities directly

59

Regulation of other Shadow Banking Entities (cont.)

whether leverage by pooled investment vehicles increases the potential for forced

asset sales or exposes lenders or other counterparties to losses or unanticipated

market risks and the potential impact for US financial stability

potential risks to the US financial system resulting from operational risks

the extent to which the failure or closure of an asset manager, fund counterparty

or financial intermediary could have an adverse impact on financial markets or the

economy

• September 2015, SEC proposed rules to require investment

companies to adopt comprehensive liquidity risk management

programmes which would include among other things:

classification of the liquidity of fund portfolio assets

assessment, periodic review and management of a fund’s liquidity risk

establishment of a three day liquid asset minimum

board approval and review

proposal would also allow funds to use “swing pricing” to add on the cost of large

purchases and redemptions to shareholders that create costs

60

Regulation of other Shadow Banking Entities (cont.)

• December 2015, SEC proposed rules to limit investment company

use of derivatives and leverage

• Funds would be required to comply with one of two tests:

exposure-based portfolio limit – fund’s aggregate exposure to derivatives cannot

exceed 150% of net assets

risk-based portfolio limit – fund could limit exposure to 300% of net assets,

provided investments are subject to less market risk than if the fund did not use

derivatives, evaluated using a valuation at risk (VAR) analysis

• Funds must segregate cash to cover obligations from derivative

transactions

• Funds that use more than a limited amount of derivatives would be

required to implement a derivatives risk programme and designate a

derivatives risk manager

61

Securitisation and Excess Leverage

• FSB has accepted that securitisation can have benefit to real

economy:

resumption of orderly securitisation markets stated to be a goal of the wider

financial reform programme

• Concerns, however, that certain complex structures gave rise to

various risks:

misaligned incentives as between originators and investors

imperfect credit risk transfers leading to concentration of risk in banking system

opaqueness of structures led to lack of transparency

some structures were specifically designed to circumvent Basel capital

requirements

• BCBS/IOSCO undertook investigation of requirements relating to

transparency and risk retention

• IOSCO policy recommendations published in November 2012

62

Securitisation and Excess Leverage (cont.)

• IOSCO recommendations include:

enhanced monitoring of incentives / retention requirements and the impact of

differences in approach, particularly between EU and US

improving disclosure by issuers on stress testing and scenario analysis of pooled

assets

encouraging standardisation of securitisation products, particularly in relation to

disclosure templates

• In July 2015, BCBS/IOSCO published criteria for identifying simple,

transparent and comparable securitisations

• In the EU, in September 2015, the EU Commission published a draft

Securitisation Regulation with a view to setting out common rules on

securitisation and creating on EU framework for “simple, transparent

and standardised” securitisations which would attract preferred

regulatory capital treatment for institutional investors

THE LONG LONG GAME:

THE EU FINANCIAL REGULATORY AGENDA INTO 2016 AND BEYONDFEBRUARY 2016

A pig in a poke. Whist, whist’ (Sir Joseph Mawbey, 1st Bt), by James Gillray, publisher Samuel William Fores (floruit 1841), published 1788.

2016 will mark the eighth anniversary of the collapse of Lehman Brothers and the raft of regulatory reforms introduced in the aftermath of that event and the wider financial crisis will continue to be implemented during the year and in the coming years. Although many of these reforms have now been in the pipeline for a number of years, some new regulation does however continue to be worked on. In particular, in 2015, we saw the initiative to develop a Capital Markets Union (“CMU”) in the European Union (“EU”) which focused on a number of issues including reform of the Prospectus Directive and the introduction of a new regime for simple, transparent and standardised securitisations. Some major pieces of legislation, including the Market Abuse Regulation and the PRIIPs Regulation (both referred to in more detail below), will come into effect during or at the end of 2016 and this coming year will see the finalisation of many regulatory technical standards (“RTS”) and Implementing Technical Standards (“ITS”) in connection with such legislation. Although it looks like implementation of MiFID II will be delayed from 2017 to 2018 (as described more fully below), work will continue in relation to developing the vast number of RTS and ITS that need to be prepared in connection with this legislation.

Although the EU continues to push through its regulatory reform agenda, the cumulative effect of all the new regulation on the financial markets remains uncertain and there are some concerns that there may be unintended and unforeseen consequences arising from the reform agenda. On 20 January 2016, the European Parliament published a resolution on stocktaking and challenges of EU financial regulation.1 The resolution calls on the EU Commission to pursue an integrated approach to the CMU, pay attention to other relevant policy agendas including the development of a digital single market and threats to cyber security and provide regular (at least annual) “coherence and consistency” checks on a cross-sectoral basis on draft and adopted legislation. The resolution also calls on the EU Commission to publish a green paper exploring new approaches to promoting proportionality in financial regulation and to provide, at least every five years, a comprehensive qualitative and quantitative assessment of the cumulative impact of EU financial services regulation on financial markets and participants, both at EU and member state level. The EU Commission has yet to formally respond to this resolution but the points raised by the EU Parliament in the resolution echo many concerns already raised by market participants.

We have set out below a summary of some of the main regulatory developments we expect to see in the EU during 2016.

TABLE OF CONTENTS

I. EMIR Implementation ................................... 2

II. Capital Markets Union ................................. 4

III. PD III (Prospectus Regulation) .................. 4

IV. EU Securitisation Regulation ..................... 5

V. MiFID II Implementation.............................. 6

VI. PRIIPS Implementation ............................. 9

VII. EU Benchmark Regulation ....................... 9

VIII. BRRD Implementation ........................... 10

IX. TLAC/MREL ............................................. 11

X. CRD IV/Basel III ........................................ 13

XI. UK Ring-fencing ............................................. 16

XII. Possible EU Banking Reform........................ 16

XIII. FCA Senior Managers Regime .................... 17

XIV. AIFMD .......................................................... 18

XV. Shadow Banking ........................................... 19

XVI. MAR/MAD II Implementation ....................... 21

XVII. UCITS V...................................................... 22

XVIII. SRM Regulation ........................................ 23

XIX. EU Deposit Insurance Regulation ............... 24

XX. PSD II ........................................................... 25

1 http://www.europarl.europa.eu/RegData/seance_pleniere/textes_adoptes/provisoire/2016/01-19/0006/P8_TA-PROV(2016)0006_EN.pdf

2

I. EMIR Implementation

The European Market Infrastructure Regulation (“EMIR”)2 regulating derivatives transactions in the EU entered into force on 16 August 2012, but some of its requirements have yet to come into effect. Further delegated acts, RTS and ITS are required for many of EMIR’s provisions to be effected.

Reporting

Although the trade reporting regime was introduced in February 2014 and expanded in August 2014, recommendations for changes to the RTS and ITS have been made to address practical implementation concerns. In November 2015, the European Securities and Market Authority (“ESMA”) published a Final Report3 setting out new draft RTS and ITS on data reporting under Article 9 of EMIR.

The RTS include a list of reportable fields with prescriptions of what the content should include. The RTS explain how to report in the situation when one counterparty reports on behalf of the other counterparty to the trade, the information required for the reporting of trades cleared by a CCP and the conditions and start date for reporting valuations and information on collateral.

The ITS include a list of reportable fields prescribing formats and standards for the content of the fields. The ITS define the frequency of valuation updates and various modifications that can be made to the report and a waterfall approach to the identification of counterparties and the product traded. Finally, they describe the timeframe by which all trades should be reported (including historic trades that will need to be backloaded). ESMA has sent the final draft technical standards to the EU Commission for endorsement, which is likely to occur in early 2016.

ESMA published a Consultation Paper4 in December 2015 on draft RTS relating to data access, and aggregation and comparison of data. It proposed amendments to the current RTS5 on data access. The draft RTS aim to allow the authorities to better fulfil their responsibilities, in particular in the context of monitoring systemic risk and increased OTC derivatives transparency.

Clearing

The implementation of clearing requirements continues to be progressed. After some back and forth between ESMA and the EU Commission at draft stage, the first RTS on clearing Interest Rate Swaps was published in the Official Journal of the EU on 1 December 2015.6 The classes of interest rate swaps that will need to be cleared are:

• fixed-to-float (Plain Vanilla) swaps denominated in Euro, GBP, JPY and USD;

• float-to-float (Basis) swaps denominated in Euro, GBP, JPY and USD;

• forward rate agreements denominated in Euro, GBP and USD; and

• overnight index swaps denominated in Euro, GBP and USD.

2 http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32012R0648&from=EN 3 https://www.esma.europa.eu/sites/default/files/library/2015/11/2015-esma-1645_-_final_report_emir_article_9_rts_its.pdf 4 https://www.esma.europa.eu/sites/default/files/library/esma-2015-1866_-_consultation_paper_on_access_aggregation_and_comparison_of_tr_data.pdf 5 Commission Delegated Regulation (EU) No 148/2013, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2013:052:0001:0010:en:PDF 6 Commission Delegated Regulation (EU) 2015/2205, http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32015R2205.

3

The RTS divide market participants into categories in order to ensure the most active market participants are required to clear first. The phase-in schedule is as follows:

• 21 June 2016 - Category 1: counterparties that are clearing members of an authorised CCP.

• 21 December 2016 - Category 2: financial counterparties and alternative investment funds (“AIFs”) that belong to a group that exceeds a threshold of EUR 8 billion aggregate month-end average outstanding gross notional amount of non-centrally cleared derivatives.

• 21 June 2017 - Category 3: financial counterparties and other AIFs with a level of activity in uncleared derivatives below the threshold of EUR 8 billion aggregate month-end average outstanding gross notional amount of non-centrally cleared derivatives.

• 21 December 2018 - Category 4: non-financial counterparties above the clearing threshold.

The contract date against which the minimum remaining maturity is calculated for Category 1 and Category 2 counterparties was adjusted to allow counterparties time to determine their categorisation and make any necessary arrangements.

ESMA published a Final Report7 setting out final draft RTS in November 2015 establishing a mandatory clearing obligation on two further classes of interest rate swaps, being:

• fixed-to-float interest rate swaps denominated in CZK, DKK, HUF, NOK, SEK and PLN; and

• forward rate agreements denominated in NOK, SEK and PLN.

As with the first RTS, these RTS propose that the clearing obligation will be phased in depending on counterparty category.

Risk Mitigation – Collateral

Article 11(3) of EMIR requires financial counterparties to adopt procedures with respect to the timely, accurate and appropriately segregated exchange of collateral with respect to non-cleared derivatives. The European Supervisory Authorities (“ESAs”) (being ESMA, the European Banking Authority (“EBA”) and the European Insurance and Occupational Pensions Authority (“EIOPA”)) are required to develop RTS as to the necessary procedures, levels and type of collateral and segregation arrangements. In April 2014, the ESAs published their first joint consultation on draft RTS8 and their second Consultation Paper on draft RTS9 was published in June 2015 which, among other provisions, prescribed the regulatory amount of initial and variation margin to be posted and collected, and the methodologies by which that minimum amount would be calculated.

The ESAs propose that variation margin be collected over the life of the trade to cover the mark - to-market exposure of OTC derivative contracts. For initial margin, counterparties will be able to choose between a standard pre-defined schedule based on the notional value of the contracts and a more complex internal approach, where the initial margin is determined based on the modelling of the exposures. Assets provided as collateral are subject to eligibility criteria. Once received, margin must be segregated from proprietary assets of the relevant custodian, and initial margin cannot be rehypothecated.

7 https://www.esma.europa.eu/sites/default/files/library/2015/11/esma-2015-1629__final_report_clearing_obligation_ irs_other_currencies.pdf 8http://www.eba.europa.eu/documents/10180/655149/JC+CP+2014+03+%28CP+on+risk+mitigation+for+OTC+derivatives%29.pdf 9 http://www.eba.europa.eu/documents/10180/1106136/JC-CP-2015-002+JC+CP+on+Risk+Management+Techniques+for+OTC+derivatives+.pdf

4

The second consultation revised the phase-in schedule so that variation margin requirements for uncleared trades are expected to come into effect from 1 September 2016 for major market participants (market participants that have an aggregate month-end average notional amount of non-centrally cleared derivatives exceeding EUR 3 trillion) and on 1 March 2017 for all other counterparties. Initial margin requirements are expected to be phased in between 1 September 2016 and 1 September 2020.

II. Capital Markets Union

In September 2015, the EU Commission launched its Capital Markets Union (“CMU”) Action Plan10, intended to cover the 28 EU member states. The CMU initiative was first suggested in response to concerns that, compared with the US and other jurisdictions, capital markets-based financing in Europe is fragmented and underdeveloped, with significant reliance on banks to provide sources of funding. For example, compared with the US, European small and medium-sized enterprises (“SMEs”) receive five times less funding from capital markets.

The hope is that this single market for capital will unlock more investment from the EU and the rest of the world by removing barriers to cross-border investment, whilst channeling capital and investment from developed capital markets into smaller markets with higher growth potential. It is intended to provide more options and better returns for savers and investors through cross-border risk-sharing and more liquid markets, with the ultimate aim of both lowering the cost and increasing the sources of funding available.

Based on consultations which began in February 2015, the EU Commission has confirmed that, rather than establishing the CMU through a single measure, it will be achieved through a range of initiatives. These will be targeted towards specific sectors, as well as more generally towards the EU supervisory structure, in each case with the aim of removing the barriers which stand between investors’ money and investment opportunities.

The following measures have been designated as priorities: providing greater funding choice for Europe’s businesses and SMEs; ensuring an appropriate regulatory environment for long-term and sustainable investment and financing of Europe’s infrastructure; increasing investment and choice for retail and institutional investors; enhancing the capacity of banks to lend; and bringing down cross-border barriers and developing markets for all 28 member states.

The EU Commission declares this to be a long-term project, with its ultimate goal being a fully functioning CMU by 2019. In order to achieve this, the Action Plan provides that the EU Commission will continuously work to identify the main inefficiencies and barriers to deeper capital markets in Europe and, alongside the annual reports it intends to publish, the EU Commission is also proposing to do a ‘comprehensive stock-take’ in 2017 to decide whether any further measures are required.

The next stage of the CMU implementation will occur in early 2016 when the EU Commission receives responses to two public consultations on (1) access to European venture capital and social entrepreneurship funds and (2) the creation of a pan-European covered bonds market. Also during the course of 2016, the European Parliament and the EU Council of Ministers will consider amendments to the Solvency II Delegated Regulation, as well as proposals for a Securitisation Regulation creating an EU framework for simple and transparent securitisation (see section on EU Securitisation Regulation) as described further below.

III. PD III (Prospectus Regulation)

As part of its implementation of the CMU Action Plan, on 30 November 2015, the EU Commission published a legislative proposal11 for a new Prospectus Regulation (“PD III”) which will repeal and replace the current Prospectus Directive 2003/71/EC and its implementing measures. As set out in the EU 10 http://ec.europa.eu/finance/capital-markets-union/docs/building-cmu-action-plan_en.pdf 11 http://eur-lex.europa.eu/resource.html?uri=cellar:036c16c7-9763-11e5-983e-01aa75ed71a1.0006.02/DOC_1&format=PDF

5

Commission’s Consultation Document12 published in February 2015, the EU Commission concludes that the barriers to accessing capital in the EU need lowering and the mandatory disclosure requirements under the Prospectus Directive are particularly burdensome. Therefore, the hope is that implementation of PD III will make it easier and cheaper for SMEs to access capital markets, whilst also simplifying the process for all companies wishing to issue debt or shares.

The key proposals involve the following:

• introducing a higher threshold for determining when a prospectus is required for smaller capital raisings (proposed to be increased from €100,000 to €500,000, with the ability for member states to increase the threshold further in their domestic markets);

• doubling the firm size threshold under which SMEs are allowed to submit a ‘lighter’ prospectus (to include SMEs with a market capitalisation of up to €200 million);

• a simpler prospectus for secondary issuances by listed companies to reflect the reduced risk posed by such issuances;

• shorter, clearer prospectus summaries emphasising only material risk factors;

• fast-track approvals for frequent issuers via a ‘Universal Registration Document’ (the “URD”) (similar to a shelf registration concept); and

• the creation of a free searchable online portal which will act as a single access point for all prospectuses approved in the EEA.

Most other exemptions from the requirement to produce a prospectus, such as for offerings to qualified investors only and to fewer than 150 persons per member state, are proposed to remain unchanged.

As we move further into 2016, the draft PD III will be reviewed by the European Parliament and the EU Council of Ministers. Once approved by all relevant EU institutions, several delegated acts will need to be adopted and ESMA will need to publish draft RTS and guidance. This timetable process is uncertain and it is therefore not presently known when PD III will take effect. The current draft of PD III contemplates that ESMA will produce annual reports on its impact and, in particular, the extent to which the simplified disclosure regimes for SMEs and secondary issuances and the URD are used. The new rules will be evaluated five years after they enter into force.

IV. EU Securitisation Regulation

Securitisations have continued to be criticised in some quarters for the product’s perceived role in causing and/or exacerbating the effects of the recent financial crisis. However during the last couple of years, there have been increasing signs that the securitisation market is viewed by EU regulators as having an important part to play in creating well-functioning capital markets. This is principally due to the role such structures can play in diversifying funding sources and allocating risk more efficiently within the financial system.

On 30 September 2015, the EU Commission published a legislative proposal for a “Securitisation Regulation”13 with a view to setting out common rules on securitisation and creating an EU framework for simple, transparent and standardised (“STS”) securitisations. In effect, these are securitisations that satisfy certain criteria and are therefore able to benefit from the resulting STS label (for example, through reduced capital charges). This concept is not dissimilar to the idea that a fund might qualify for the

12 http://ec.europa.eu/finance/consultations/2015/prospectus-directive/docs/consultation-document_en.pdf 13 http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52015PC0472&from=EN

6

UCITS label. According to the EU Commission, the development of a STS market is a key building block of the CMU and contributes to the priority objectives of supporting job creation and sustainable growth. At the same time, the EU Commission also published a draft Regulation to amend the CRR (referred to and defined below) to provide more favourable regulatory capital treatment for STS securitisations.

The draft Securitisation Regulation has two main goals, the first being to harmonise EU securitisation rules applicable to all securitisation transactions, while the second is to establish a more risk-sensitive prudential framework for STS securitisations in particular. The first goal is to be achieved through repealing the separate, and often inconsistent, disclosure, due diligence and risk retention provisions found across EU legislation, such as the CRR, the Alternative Investment Fund Managers Directive and the Solvency II Directive, and replacing them with a single, shorter set of provisions consisting of uniform definitions and rules which will apply across financial sectors.

The second part of the Securitisation Regulation is focused on the objective of creating the framework for STS securitisations and aims to provide clear criteria for transactions to qualify as STS securitisations. These include RMBS, auto loans/leases and credit card transactions, whereas actively managed portfolios (for example, CLOs), resecuritisations (for example, CDOs and SIVs) and structures which include derivatives as investments have been specifically prohibited. Those transactions which qualify as STS securitisations will result in preferential regulatory capital treatment for institutional investors. The EU Commission’s hope is that in recognising the different risk profile of STS and non-STS securitisations, investing in safer and simpler securitisation products will become more attractive for credit institutions established in the EU and will thus release additional capital for lending to businesses and individuals.

However, market concern exists in relation to the classification of STS securitisations. This, in part, arises as a result of the lengthy list of STS criteria which need to be satisfied and which may be interpreted in different ways. The burden of such interpretation is currently proposed to reside with the issuers and investors, which may introduce uncertainty and a lack of clarity that could ultimately defeat the purpose of the exercise. Some commentators have suggested that a third-party approval mechanism may be beneficial, although it remains to be seen who would be willing to assume this role and whether it is something that EU regulators wish to pursue.

The proposed Securitisation Regulation has been sent to the European Parliament and the EU Council of Ministers who need to agree and approve a final text. It is likely to be subject to considerable debate and scrutiny and it is therefore unlikely to become effective before the end of 2016. That said, market participants are likely to start responding to the proposal by considering whether their transactions fit the criteria for preferential regulatory capital treatment in time for when the Regulation does become effective.

V. MiFID II Implementation

MiFID II is the commonly used term for the overhaul of the Markets in Financial Instruments Directive which originally came into force in 2007. The primary MiFID II legislation comprises a Regulation (“MiFIR”)14 and recast Directive15 (together with MiFIR referred to as “MiFID II”). MiFID II was published in the Official Journal of the EU on 12 July 2014 and entered into force 20 days after that date.

MiFID II currently provides that its provisions will start to become effective in the EU in January 2017. However, during 2015, concerns increased as to the work required in relation to the implementation of MiFID II, both in terms of finalising the vast number of delegated acts, RTS and ITS required to be published under MiFID II and in relation to firms putting in place the necessary systems to comply with all of the requirements. ESMA has recommended a delay in the implementation of MiFID II. In November 2015, the European Parliament announced that it is prepared to accept a one-year delay to MiFID II, subject to certain conditions. It is expected that the EU Commission will shortly make a formal legislative proposal to defer the date of implementation to January 2018 but this has not yet been published. It is

14 Regulation (EU) No 600/2014, http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014R0600&from=EN 15 Directive 2014/65/EU, http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014L0065&from=EN

7

not clear whether the EU Commission will also propose a deferral of the deadline for member states transposing relevant parts of MiFID II into their national laws. This deadline is currently 3 July 2016.

MiFID II significantly expands the scope of the existing MiFID legislation, including:

• some amendments to the investor protection provisions including a narrowing of the execution-only exemption so that structured UCITS are now outside the exemption, together with bonds or other forms of securitised debt that incorporate a structure which makes it difficult to understand the risk involved;

• structured deposits are now subject to a number of the provisions of MiFID II;

• the extension of many provisions of MiFID II to “organised trading facilities” or “OTFs” which will cover many forms of organised trading (not being regulated markets or multilateral trading facilities (“MTFs”)) on which bonds, structured finance products and derivatives are traded;

• requiring all derivatives that are subject to the clearing obligation under EMIR, and that ESMA determines to be sufficiently liquid, to be traded on a regulated market, MTF or OTF;

• extending the pre- and post- trade transparency regime (which currently only applies to shares) to bonds, structured finance instruments and derivatives traded on a trading venue;

• wider product intervention powers granted to ESMA and competent authorities including the ability to temporarily prohibit or restrict marketing of certain products in the EU;

• increased regulation of algorithmic and high frequency trading; and

• significantly expanding the scope of the regulation of commodities and commodity derivatives.

In addition to the level 1 legislation referred to above, MiFID II requires a significant number of delegated acts of the EU Commission to be prepared, mostly comprising RTS and ITS to be drafted by ESMA and the other ESAs. This has resulted in a significant number of consultation papers and discussion papers to be published, including:

(a) in May 2014, a Consultation Paper16 and a Discussion Paper17 from ESMA outlining its initial thinking on many aspects of MiFID II;

(b) in December 2014, Technical Advice from ESMA to the EU Commission18 and a second Consultation Paper on MiFID II19 dealing principally with regulation of secondary markets (including a detailed consideration of what constitutes a liquid market for the purpose of granting waivers of pre-trade transparency requirements for bonds, structured finance instruments and bonds and derivatives);

(c) in February 2015, an Addendum Consultation Paper from ESMA20 relating to MiFID II, dealing in particular with the transparency rules for non-equity financial instruments including the specification of thresholds for large-in-scale and size-specific waivers for pre- and post-trade transparency requirements for certain derivative transactions;

16 ESMA 2014/549, http://www.esma.europa.eu/system/files/2014-549_-_consultation_paper_mifid_ii_-_mifir.pdf 17 ESMA 2014/548, http://www.esma.europa.eu/system/files/2014-548_discussion_paper_mifid-mifir.pdf 18 http://www.esma.europa.eu/system/files/2014-1569_final_report__esmas_technical_advice_to_the_commission_ on_mifid_ii_and_mifir.pdf 19 http://www.esma.europa.eu/system/files/2014-1570_cp_mifid_ii.pdf 20 https://www.esma.europa.eu/sites/default/files/library/2015/11/2015-319_cp_addendum_mifid_ii-mifir.pdf

8

(d) in April 2015, a Consultation Paper from ESMA21 on draft guidelines for the assessment of knowledge and competence of persons in investment firms providing investment advice or information about financial instruments, investment services or ancillary services to clients under Article 24 and 25 of the MiFID II Directive;

(e) in June 2015, an ESMA Final Report22 on draft ITS and RTS relating to authorisation, passporting, registration of third-country firms and co-operation between competent authorities;

(f) in August 2015, an ESMA Consultation Paper23 on various ITS and RTS to be published under MiFID II that it had not previously consulted on, including the suspension and removal of financial instruments from trading on a trading venue and notification and provision of information for data reporting services providers;

(g) in September 2015, an ESMA Final Report24 setting out the final versions of ITS and RTS it consulted on pursuant to its May 2014 papers referred to above;

(h) in November 2015, an ESMA Final Report25 setting out Guidelines on complex debt instruments and structured deposits in respect of the MiFID II “execution only” exemption;

(i) in December 2015, Final Reports from ESMA on Guidelines26 for cross-selling practices under the MiFID II Directive and on draft ITS27 relating to various matters including position reporting and format and timing of weekly position reports; and

(j) in December 2015, a Consultation Paper from ESMA28 on Guidelines on its draft RTS on transaction reporting, reference data, order record keeping and clock synchronisation.

It is expected that the EU will move to adopt the various delegated acts necessary in connection with the relevant ITS and RTS detailed above. It was expected that this would occur before the July 2016 transposition deadline. As mentioned, if the MiFID II timetable is delayed, it remains to be seen if the transposition deadline is also amended.

In the United Kingdom, on 15 December 2015, the FCA published the first of two Consultation Papers29 on changes to its Handbook necessary to implement MiFID II. This first consultation focused on secondary trading of financial instruments including the rules relating to pre- and post-trade transparency. This consultation is open until 8 March 2016, following which the FCA will publish a Policy Statement. The FCA’s second Consultation Paper on changes to its Handbook dealing with other relevant matters under MiFID II is expected during the first half of 2016.