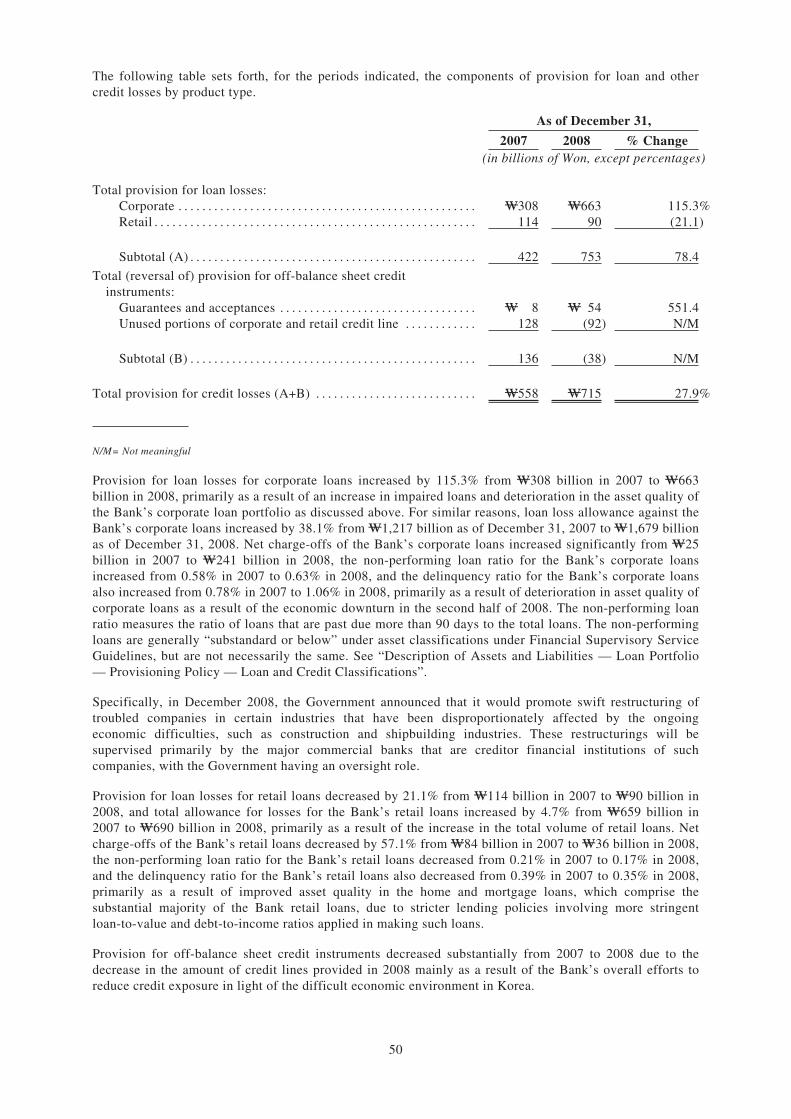

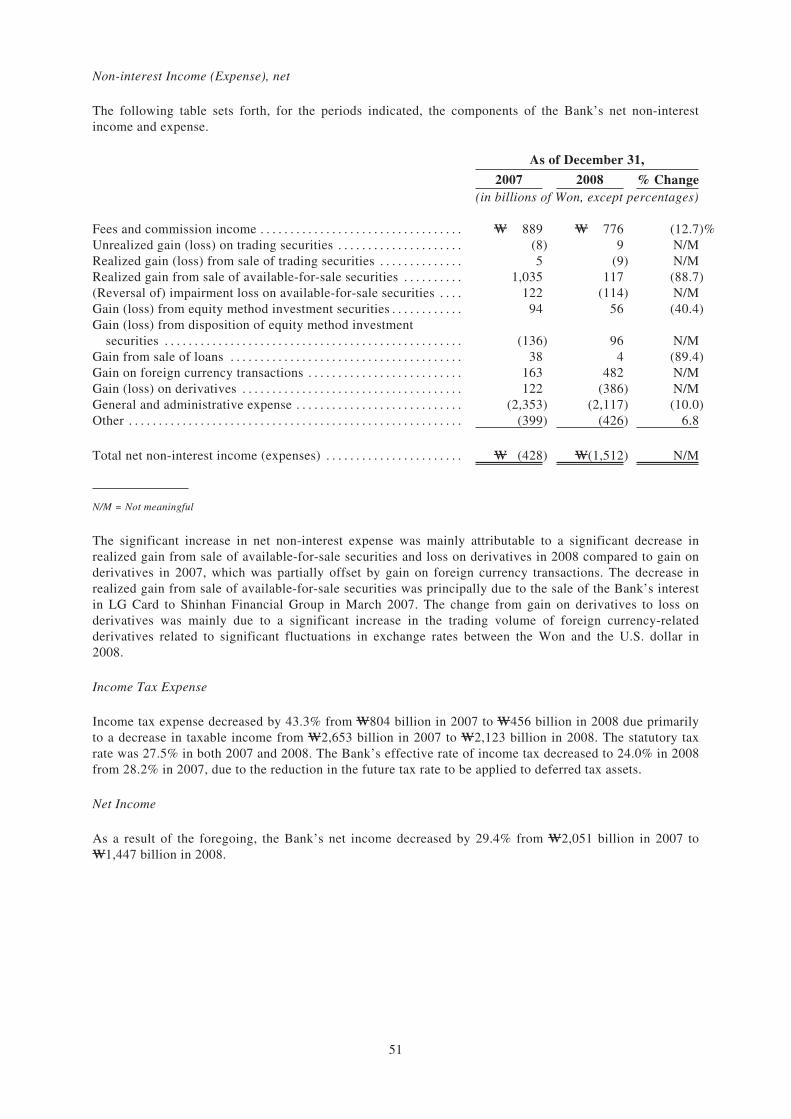

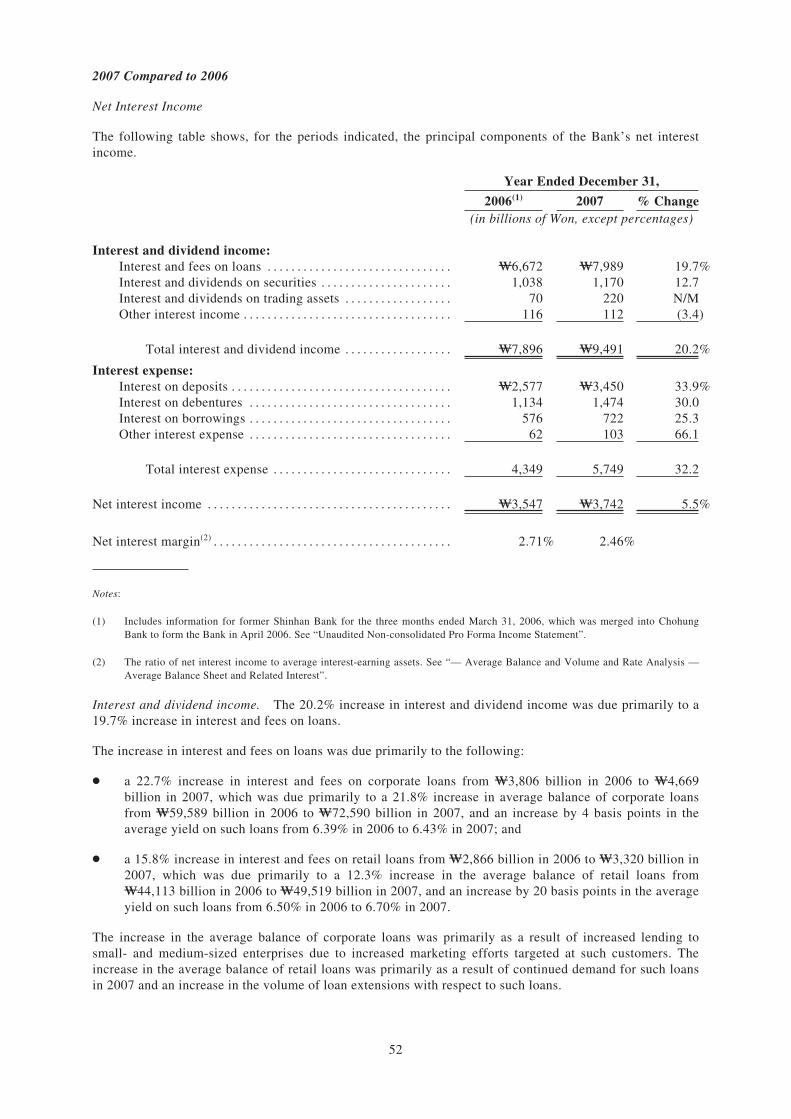

Embed Size (px)

Citation preview

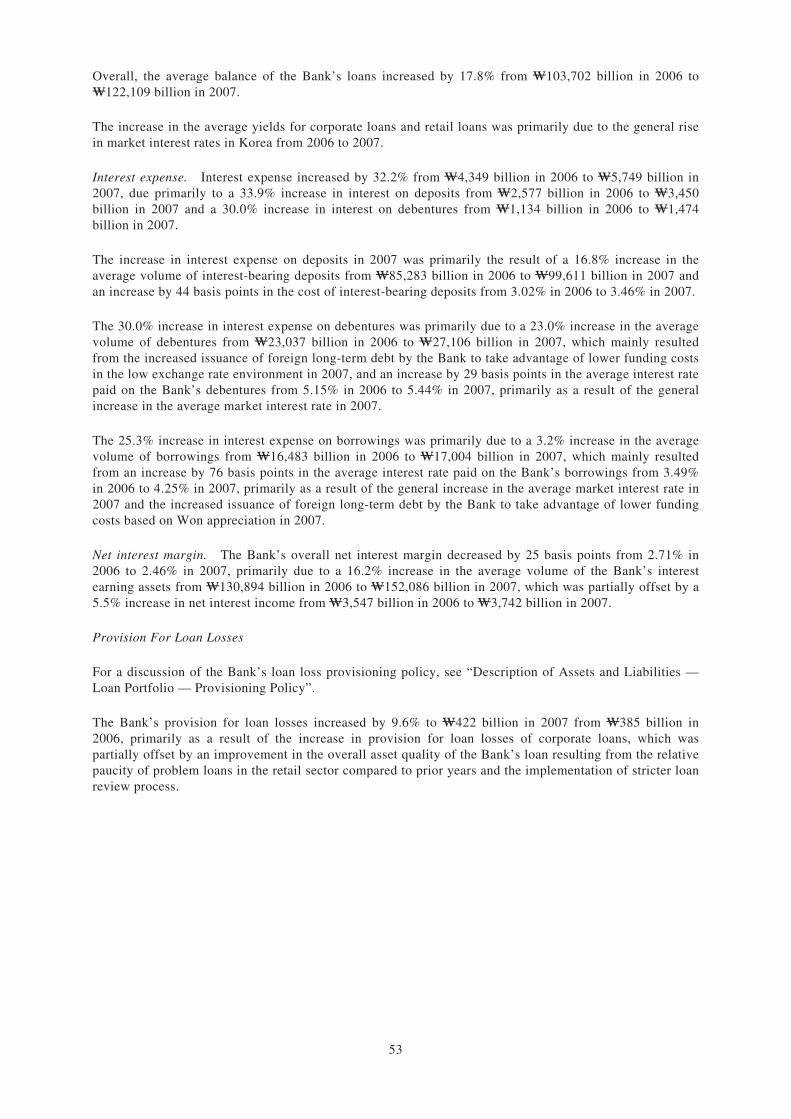

OFFERING CIRCULAR

US$500,000,000

(incorporated with limited liability under the laws of the Republic of Korea)

6.0% Senior Notes due 2012

Issue Price: 99.835%

Shinhan Bank (the “Bank”) will issue an aggregate principal amount of US$500,000,000 of 6.0% Senior Notesdue 2012 (the “Notes”). The Notes will bear interest semi-annually in arrears on June 29 and December 29 ofeach year, commencing June 29, 2009 until redemption or maturity. The Notes will mature on June 29, 2012.The Bank may not redeem the Notes in whole or in part prior to maturity except upon the occurrence of certainevents related to Korean tax law as described herein. The Notes will be issued in registered form indenominations of US$100,000 and integral multiples of US$1,000 in excess thereof.

The Notes will be the Bank’s direct, unconditional and unsecured senior obligations and will rank pari passuwith all of its other unsecured senior indebtedness, except as may be required by mandatory provisions of law.

There is currently no market for the Notes. Application has been made to list the Notes on the SingaporeExchange Securities Trading Limited (the “Singapore Stock Exchange”). The Singapore Stock Exchangeassumes no responsibility for the correctness of any statements made, opinions expressed or reports containedherein. The approval in-principle from, and the admission of the Notes to the Official List of, the SingaporeStock Exchange are not to be taken as an indication of the merits of the Issuer or the Notes.

The Notes are expected to be rated A2 by Moody’s Investors Service, Inc. (“Moody’s”) and A- by Standard &Poor’s Rating Services, a division of The McGraw-Hill Companies, Inc. (“S&P”). Such ratings do notconstitute a recommendation to buy, sell or hold the Notes and may be subject to revision or withdrawal at anytime by such rating organizations.

Investing in the Notes involves risks. See “Risk Factors” beginning on page 11 for a discussion of certainfactors to be considered in connection with investing in the Notes.

The Notes have not been and will not be registered under the United States Securities Act of 1933 (the“Securities Act”) or any state securities laws and may not be offered or sold within the United Statesexcept pursuant to an exemption from, or in a transaction not subject to, the registration requirementsof the Securities Act. Accordingly, the Notes may be offered for sale only (i) in the United States, toqualified institutional buyers (“QIBs”) within the meaning of, and in reliance on, Rule 144A under theSecurities Act; or (ii) outside the United States in reliance on, and in accordance with, Regulation S, ineach case, in compliance with applicable laws, regulations and directives. See “Plan of Distribution —Selling Restrictions” and “Notice to Investors”.

Delivery of the Notes in book-entry form will be made on or about June 29, 2009. The Global Notes will bedeposited with a custodian for and registered in the name of a nominee of The Depository Trust Company(“DTC”). Except as described herein, interests in the Global Notes will be shown on, and transfers thereof willbe effected only through, records maintained by DTC and its participants, including Euroclear Bank S.A./N.V.(“Euroclear”) and Clearstream Banking, société anonyme (“Clearstream”) and their accountholders. Definitivecertificates in respect of beneficial interests in the Notes will not be issued except as described herein.

Joint Bookrunners and Joint Lead Managers

BNP PARIBAS Deutsche Bank HSBC Merrill Lynch & Co. The Royal Bank of Scotland

Joint Lead Manager

Goodmorning Shinhan Securities

The date of this offering circular is June 22, 2009.

TABLE OF CONTENTS

Page

CERTAIN DEFINED TERMS AND CONVENTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iv

PRESENTATION OF FINANCIAL AND OTHER INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . iv

ENFORCEABILITY OF CIVIL LIABILITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

AVAILABLE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

FORWARD-LOOKING STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vi

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

USE OF PROCEEDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

EXCHANGE RATES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

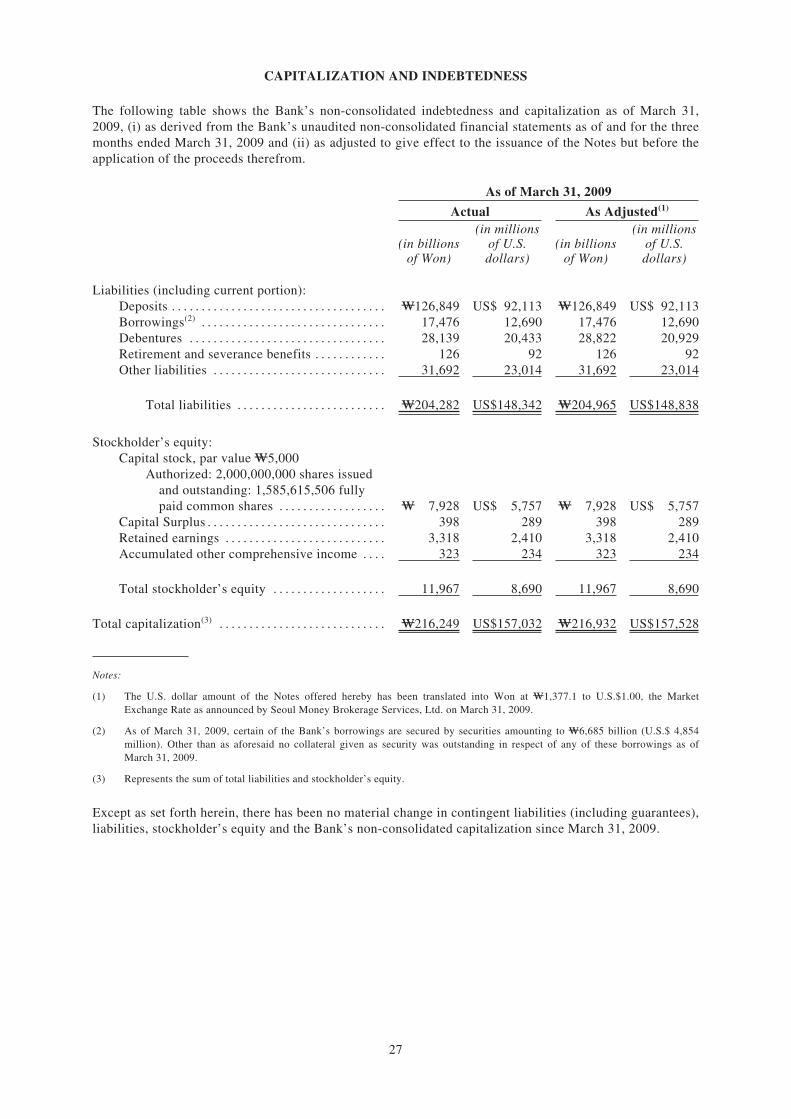

CAPITALIZATION AND INDEBTEDNESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

SELECTED FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

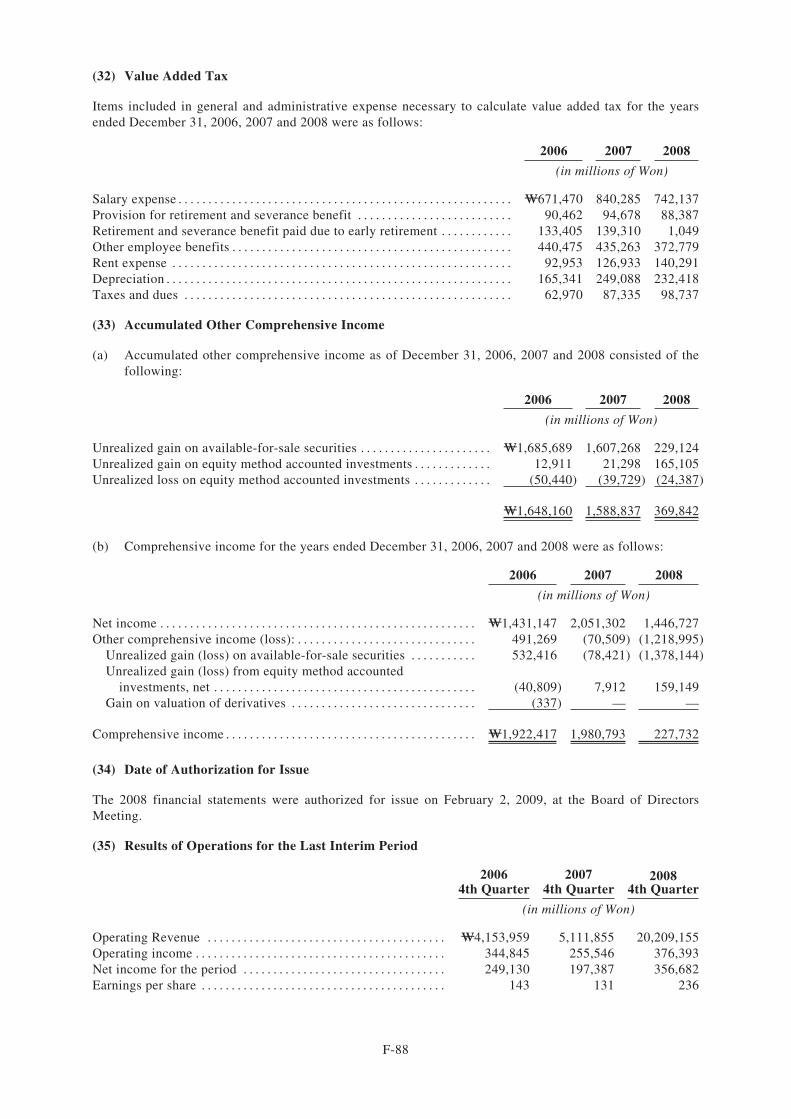

UNAUDITED NON-CONSOLIDATED PRO FORMA INCOME STATEMENT . . . . . . . . . . . . . . . . 30

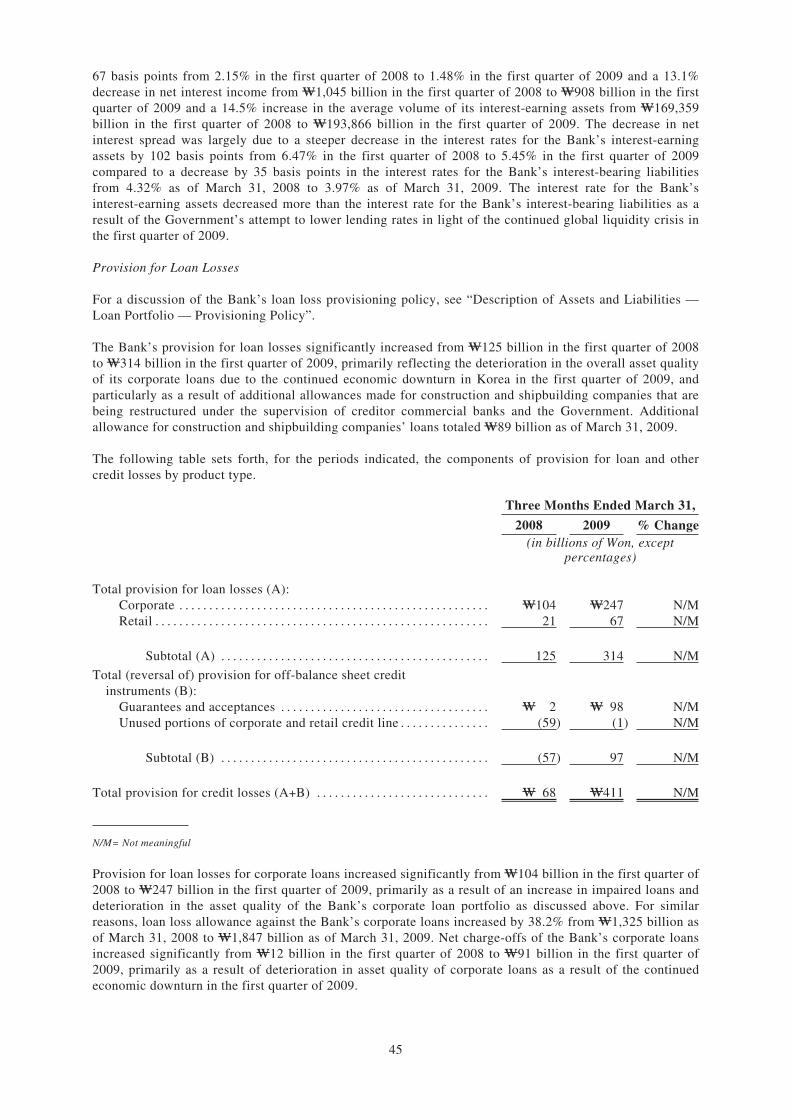

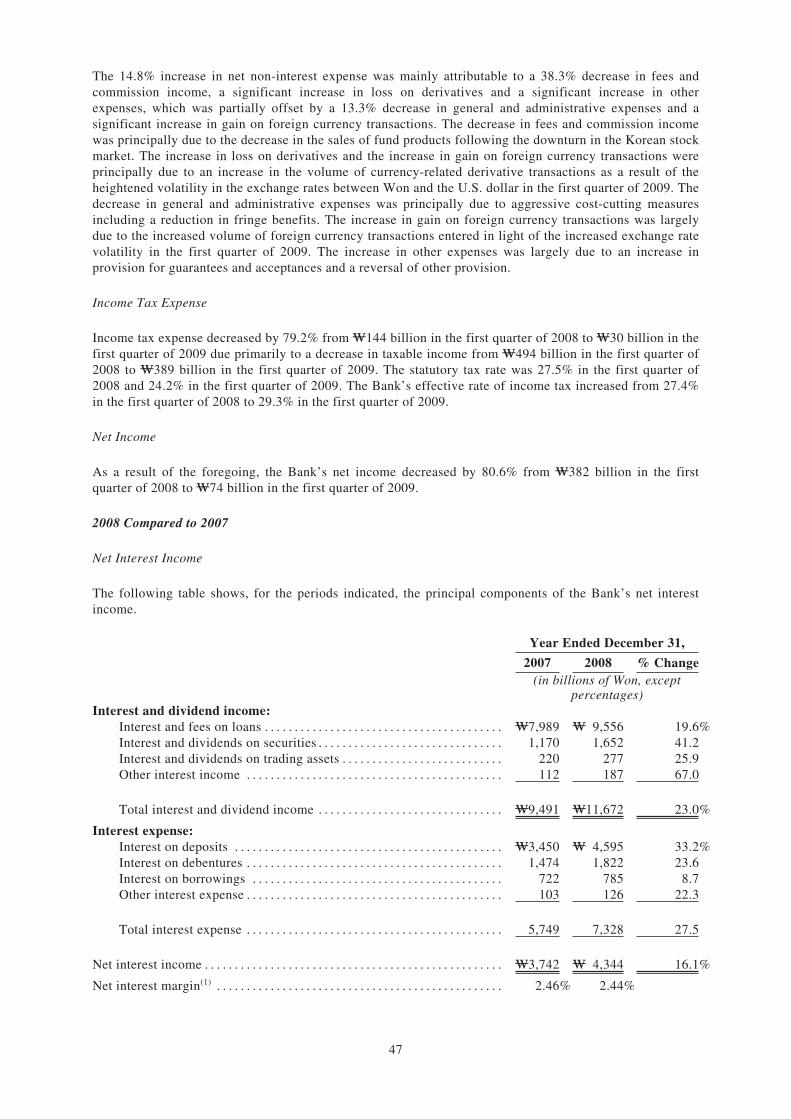

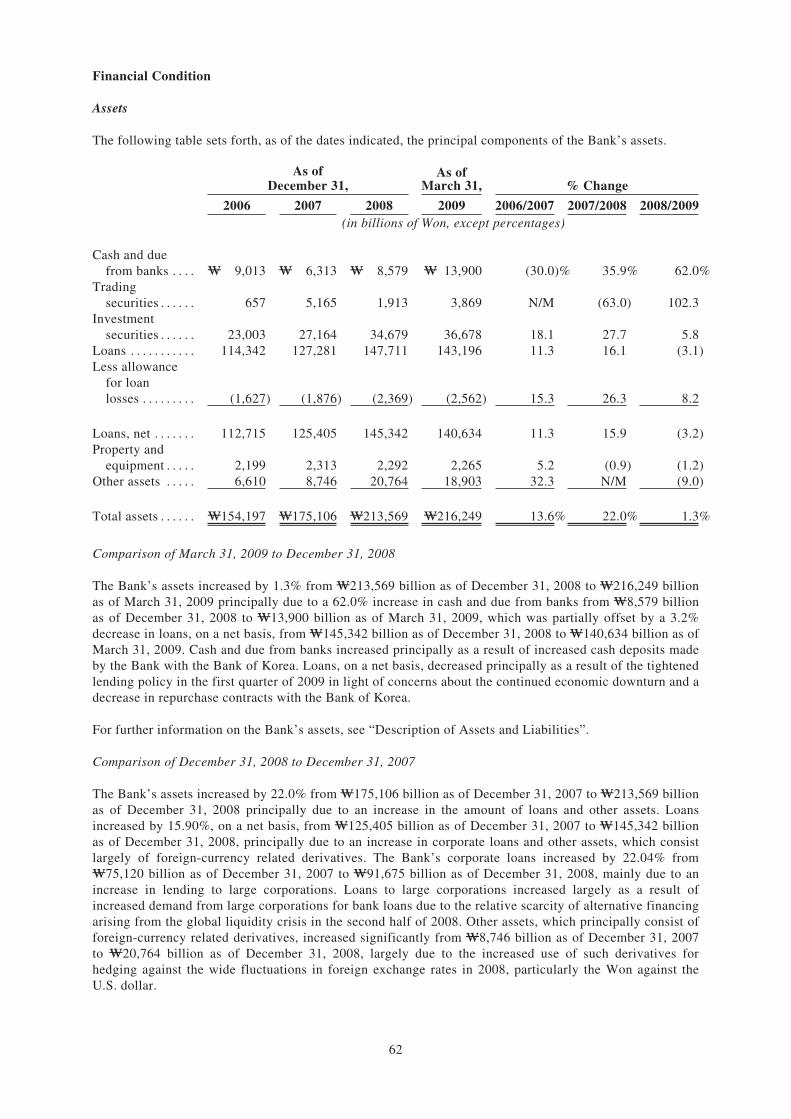

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION ANDRESULTS OF OPERATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

THE KOREAN BANKING INDUSTRY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

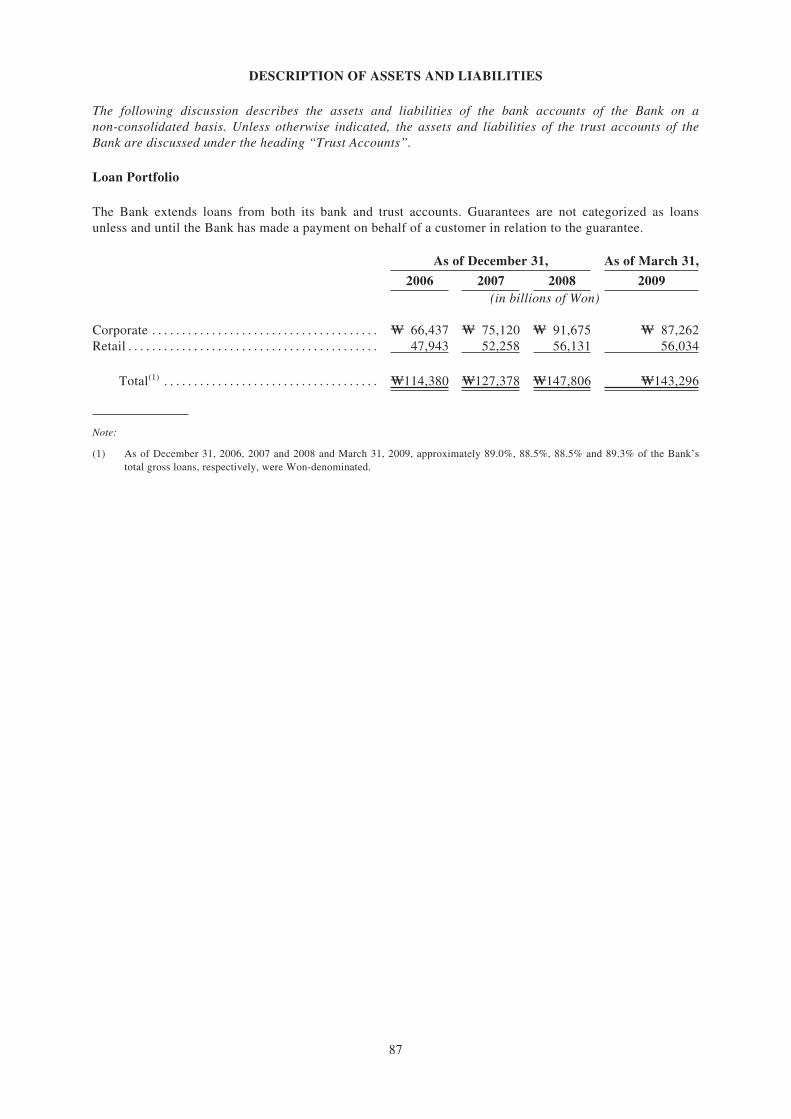

DESCRIPTION OF ASSETS AND LIABILITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

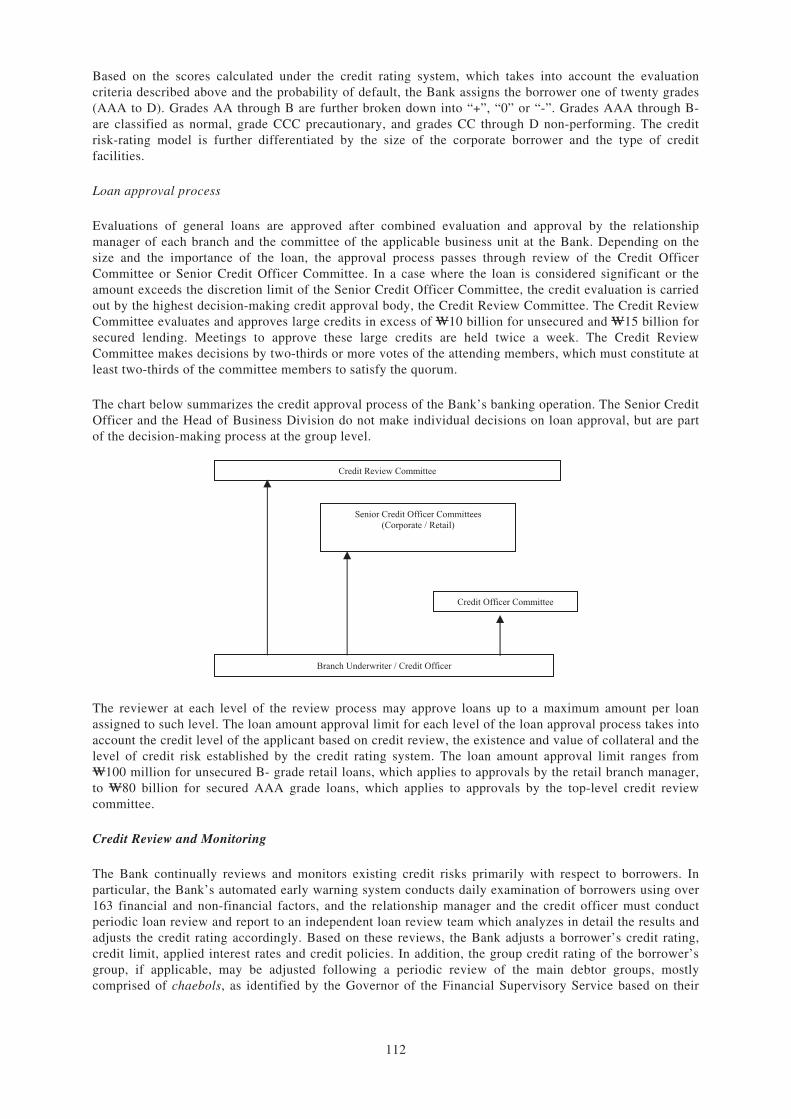

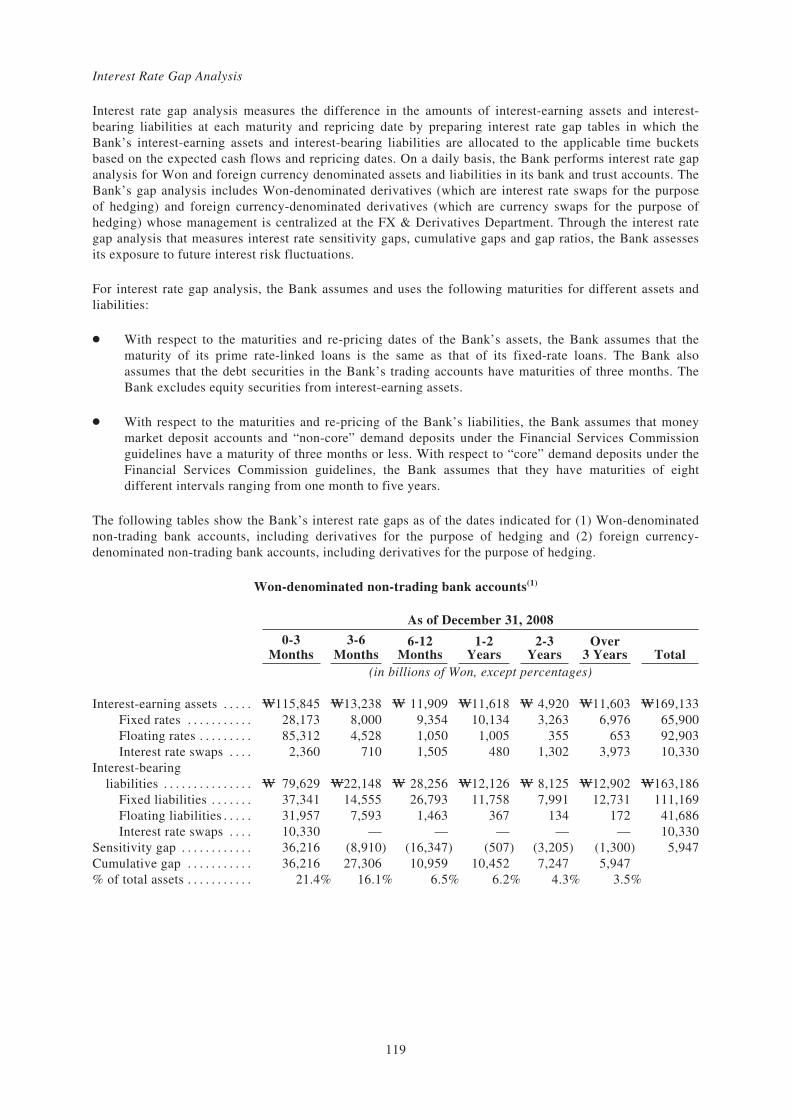

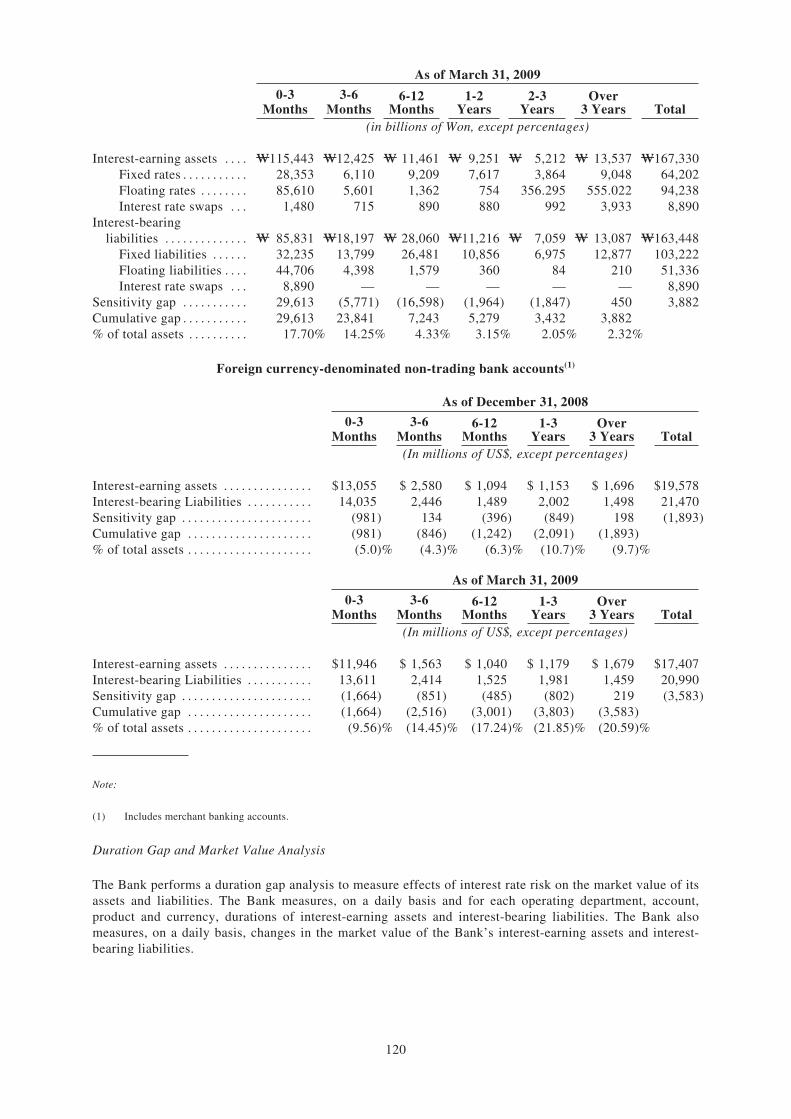

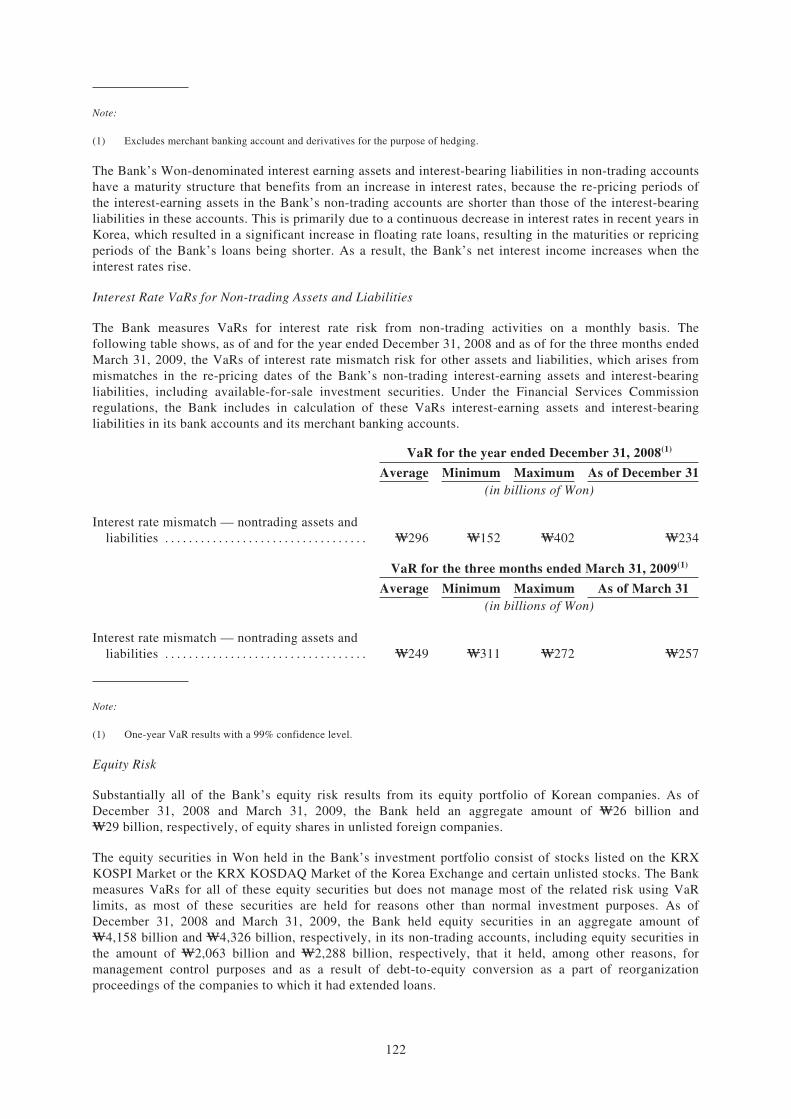

RISK MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

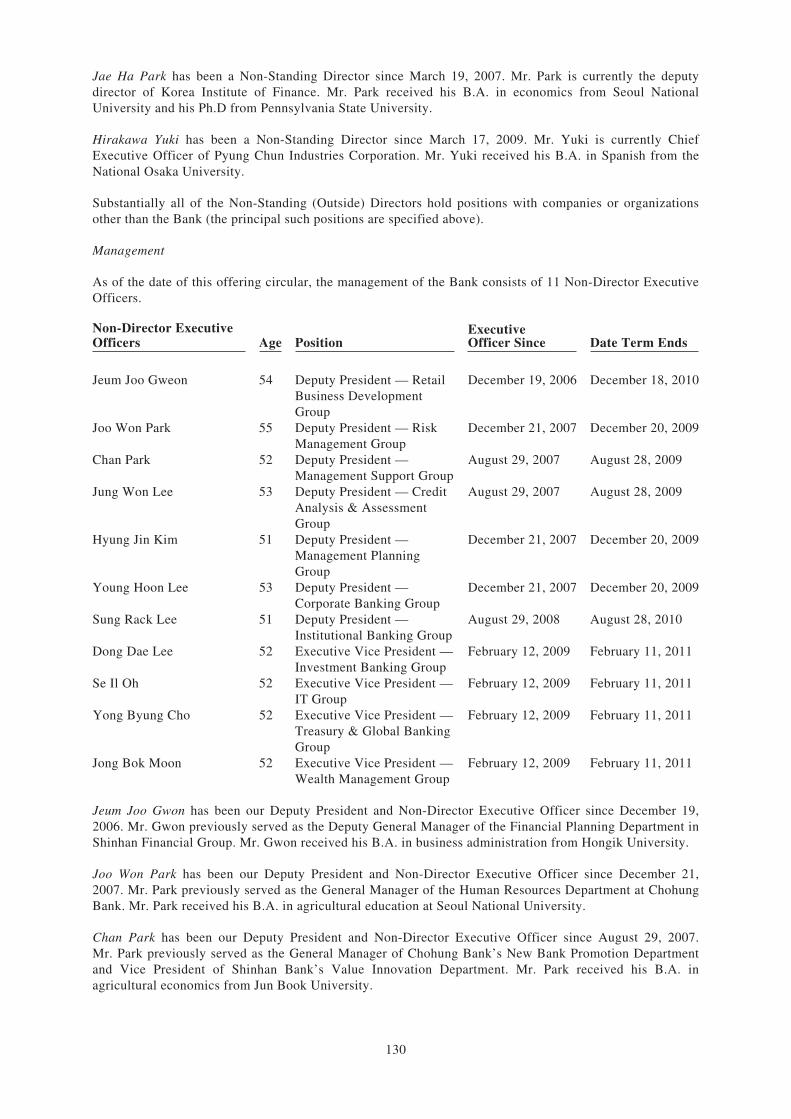

MANAGEMENT AND EMPLOYEES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128

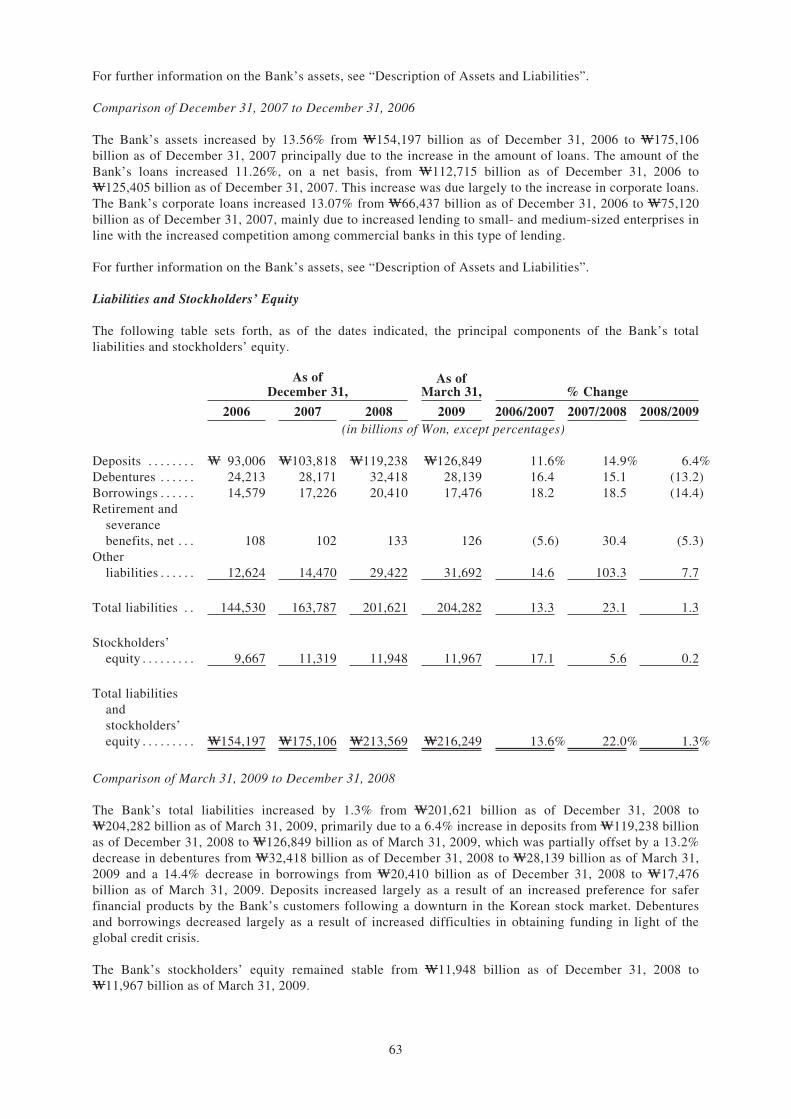

CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS . . . . . . . . . . . . . . . . . . . . 135

SHINHAN FINANCIAL GROUP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 136

SUPERVISION AND REGULATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141

DESCRIPTION OF THE NOTES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154

TAXATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 165

PLAN OF DISTRIBUTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170

NOTICE TO INVESTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174

CERTAIN ERISA CONSIDERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 177

LEGAL MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

INDEPENDENT ACCOUNTANTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

SUMMARY OF CERTAIN DIFFERENCES BETWEEN KOREAN GAAP AND U.S. GAAP . . . 180

INDEX TO FINANCIAL STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F-1

i

You should rely only on the information contained in this offering circular or to which the Bank hasreferred you. We have not authorized anyone to provide you with information that is different. Thisoffering circular may only be used where it is legal to sell the Notes. You should not assume that theinformation in this offering circular is accurate as of any date other than the date at the front of thisoffering circular. This offering circular is confidential. You are authorized to use this offeringcircular solely for the purpose of considering the purchase of the Notes described in this offeringcircular. You may not reproduce or distribute this offering circular in whole or in part, and you maynot disclose any of the contents of this offering circular or use any information herein for any purposeother than considering a purchase of the Notes. You agree to the foregoing by accepting delivery ofthis offering circular.

IN CONNECTION WITH THIS OFFERING, MERRILL LYNCH, PIERCE, FENNER & SMITHINCORPORATED OR ANY PERSON ACTING FOR OR ON ITS BEHALF, TO THE EXTENTPERMITTED BY APPLICABLE LAWS AND REGULATIONS, MAY OVERALLOT OR EFFECTTRANSACTIONS WITH A VIEW TO SUPPORTING THE MARKET PRICE OF THE NOTES AT ALEVEL HIGHER THAN THAT WHICH MIGHT OTHERWISE PREVAIL FOR A LIMITED PERIOD OFTIME AFTER THE ISSUE DATE. HOWEVER, THERE IS NO ASSURANCE THAT MERRILL LYNCH,PIERCE, FENNER & SMITH INCORPORATED OR ITS AGENT WILL UNDERTAKE SUCHSTABILIZATION. SUCH STABILIZATION, IF COMMENCED, MAY BE DISCONTINUED AT ANYTIME AND MUST BE BROUGHT TO AN END AFTER A LIMITED PERIOD. SEE “PLAN OFDISTRIBUTION”.

The Bank, having made all reasonable inquiries, confirms that this offering circular contains all informationwith respect to it and the Notes which is material in the context of the issue and offering of the Notes, thatthe information contained in this offering circular is true and accurate in all material respects and is notmisleading in any material respect, that the opinions and intentions expressed in this offering circular arehonestly held and have been reached after considering all relevant circumstances and are based onreasonable assumptions, and that there are no other facts, the omission of which would, in the context of theissue and offering of the Notes, make this offering circular as a whole or any information or the expressionof any opinions or intentions expressed in this offering circular misleading in any material respect. TheBank accepts responsibility accordingly. Information provided in this offering circular with respect toKorea, its political status and economy, has been derived from information published by the Governmentand other public sources, and the Bank accepts responsibility only for the accurate extraction of informationfrom such sources.

In making an investment decision, prospective investors must rely on their own examination of us and theterms of the offering of Notes, including the merits and risks involved. We are not making anyrepresentation to any purchaser of the Notes regarding the legality of an investment in the Notes by suchpurchaser under any legal investment or similar laws or regulations. The contents of this offering circularshould not be construed as providing legal, business, accounting or tax advice. An investor should bear theeconomic risk of an investment in the Notes.

This offering circular is based on the information provided by the Bank. Accordingly, no representation,warranty or undertaking, express or implied, is made and no responsibility or liability is accepted by theInitial Purchasers as to the accuracy or completeness of the information contained in this offering circularor any other information provided by us in connection with the offering of the Notes.

No person is authorized in connection with any offering of the Notes to give any information or make anyrepresentation other than as contained in this offering circular and, if given or made, that information orrepresentation must not be relied upon as having been authorized by us or by the Initial Purchasers (asdefined in “Plan of Distribution”). This offering circular does not constitute an offer to sell or a solicitationof an offer to buy any Notes by any person except in compliance with all applicable laws and regulations.Neither the delivery of this offering circular nor any sale made in connection with this offering circularshall under any circumstances imply that the information in this offering circular is correct as of any datesubsequent to the date of this offering circular or constitute a representation that there has been no changeor development reasonably likely to involve a material adverse change in our affairs since the date of thisoffering circular.

ii

The distribution of this offering circular and the offering of the Notes in certain jurisdictions may berestricted by law. It may not be used for or in connection with any offer to, or solicitation by, anyone in anyjurisdiction in which it is unlawful to make such an offer or solicitation. Persons into whose possession thisoffering circular may come are required by us and the Initial Purchasers to inform themselves about and toobserve the relevant restrictions. No action is being taken in any jurisdiction to permit an offering to thegeneral public of Notes or the distribution of this offering circular in any jurisdiction where action would berequired for those purposes.

A REGISTRATION STATEMENT FOR THE OFFERING AND SALE OF THE NOTES HAS NOTBEEN FILED WITH THE FINANCIAL SERVICES COMMISSION OF KOREA. ACCORDINGLY,THE NOTES MAY NOT BE OFFERED, SOLD OR DELIVERED, DIRECTLY OR INDIRECTLY,IN KOREA OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, ANY RESIDENT OF KOREA (ASSUCH TERM IS DEFINED UNDER THE FOREIGN EXCHANGE TRANSACTION LAW ANDREGULATION OF KOREA AND ITS ENFORCEMENT DECREE), FOR A PERIOD OF ONEYEAR FROM THE DATE OF ISSUANCE OF THE NOTES, EXCEPT AS OTHERWISEPERMITTED BY APPLICABLE KOREAN LAWS AND REGULATIONS. FURTHERMORE, AHOLDER OF THE NOTES SHALL BE PROHIBITED FROM OFFERING, DELIVERING ORSELLING ANY NOTES, DIRECTLY OR INDIRECTLY, IN KOREA OR TO, OR FOR THEACCOUNT OR BENEFIT OF, ANY RESIDENT OF KOREA OTHER THAN CERTAINQUALIFIED PROFESSIONAL INVESTORS AS SET FORTH IN ARTICLE 11, PARAGRAPH 1,ITEM 1, SUB-ITEMS KA AND NA OF THE PRESIDENTIAL DECREE OF THE FINANCIALINVESTMENT SERVICES AND CAPITAL MARKETS ACT FOR A PERIOD OF ONE YEARFROM THE DATE OF ISSUANCE OF THE NOTES, EXCEPT AS OTHERWISE PERMITTED BYAPPLICABLE KOREAN LAWS AND REGULATIONS.

NOTICE TO PROSPECTIVE INVESTORS IN THE UNITED STATES

NEITHER THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION (THE “SEC”)NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THENOTES OR DETERMINED IF THIS OFFERING CIRCULAR IS TRUTHFUL OR COMPLETE.ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

THE NOTES ARE SUBJECT TO RESTRICTIONS ON TRANSFERABILITY AND RESALE ANDMAY NOT BE TRANSFERRED OR RESOLD EXCEPT AS PERMITTED UNDER THESECURITIES ACT AND THE APPLICABLE STATE SECURITIES LAWS PURSUANT TOREGISTRATION OR EXEMPTION THEREFROM. AS A PROSPECTIVE PURCHASER, YOUSHOULD BE AWARE THAT YOU MAY BE REQUIRED TO BEAR THE FINANCIAL RISKS OFTHIS INVESTMENT FOR AN INDEFINITE PERIOD OF TIME. PLEASE REFER TO THESECTIONS IN THIS OFFERING CIRCULAR ENTITLED “PLAN OF DISTRIBUTION” AND“NOTICE TO INVESTORS”.

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR ALICENSE HAS BEEN FILED UNDER RSA 421-B WITH THE STATE OF NEW HAMPSHIRE NORTHE FACT THAT A SECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSEDIN THE STATE OF NEW HAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OFSTATE OF NEW HAMPSHIRE THAT ANY DOCUMENT FILED UNDER CHAPTER 421-B ISTRUE, COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACTTHAT AN EXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR ATRANSACTION MEANS THAT THE SECRETARY OF STATE HAS PASSED IN ANY WAY UPONTHE MERITS OR QUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO,ANY PERSON, SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TOBE MADE, TO ANY PROSPECTIVE PURCHASER, CUSTOMER OR CLIENT ANYREPRESENTATION INCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

iii

CERTAIN DEFINED TERMS AND CONVENTIONS

Unless otherwise specified or the context otherwise requires, in this offering circular:

Š all references to “we”, “us”, “our”, “Shinhan Bank” and the “Bank” shall mean the surviving entityfollowing the merger of former Shinhan Bank into Chohung Bank, effective April 3, 2006;

Š all references to “former Shinhan Bank” shall mean Shinhan Bank as in existence prior to its mergerwith Chohung Bank, effective April 3, 2006;

Š all references to “Chohung Bank” shall mean Chohung Bank as in existence prior to its merger withformer Shinhan Bank, effective April 3, 2006; and

Š all references to “Shinhan Financial Group Co., Ltd.,” “Shinhan Financial Group” and “our holdingcompany” shall mean Shinhan Financial Group Co., Ltd., of which the Bank is a wholly-ownedsubsidiary.

All references to “Korea” and the “Republic” contained in this offering circular shall mean The Republic ofKorea. All references to the “Government” shall mean the government of The Republic of Korea. The“Financial Supervisory Service” is the executive body of the Financial Services Commission, which wasrenamed as such as of February 29, 2008, from the Financial Supervisory Commission.

All references to “Won” or “W” in this offering circular are to the lawful currency of Korea; all referencesto “Dollars”, “$” or “US$” are to the lawful currency of the United States of America; and all references to“Yen” or “¥” are to the lawful currency of Japan.

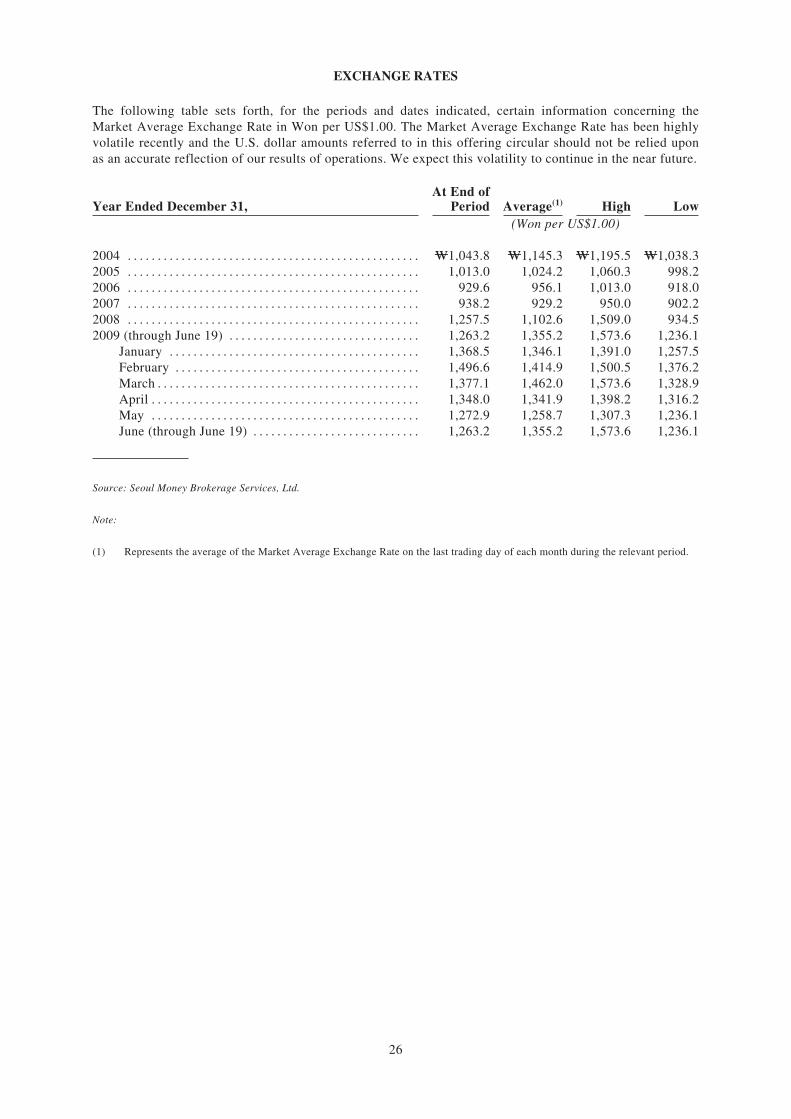

For convenience only, certain Won amounts have been translated into U.S. dollars. Unless otherwisespecified, all such conversions were made at the market average exchange rate announced by SeoulMoney Brokerage Services, Ltd. in Seoul for U.S. dollars against Won (the “Market Average ExchangeRate”). Unless otherwise stated, the translations of Won into U.S. dollars as of March 31, 2009 weremade at the Market Average Exchange Rate in effect on such date, which was W1,377.1 = U.S.$1.00. TheMarket Average Exchange Rate has been highly volatile recently and the U.S. dollar amounts referred toin this offering circular should not be relied upon as an accurate reflection of our results of operations.We expect this volatility to continue in the near future. No representation is made that the Won or U.S.dollar amounts referred to herein could have been or could be converted into U.S. dollars or Won, as thecase may be, at any particular rate or at all. The Market Average Exchange Rate on June 19, 2009 wasW1,263.2 = U.S.$1.00.

Any discrepancies in any table between totals and the sums of the amounts listed are due to rounding.References to billions are to thousands of millions.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

We prepare our financial statements in Won in accordance with generally accepted accounting principles inKorea (“Korean GAAP”), together with, where applicable, accounting and reporting guidelines underKorean accounting standards applicable to the banking industry, which differ in certain important respectsfrom generally accepted accounting principles in certain other countries, including the United States. For adiscussion of certain differences between Korean GAAP and generally accepted accounting principles in theUnited States (“U.S. GAAP”) as they relate to the Issuer, see “Summary of Certain Differences betweenKorean GAAP and U.S. GAAP”. We have made no attempt to identify or quantify the impact of thesedifferences.

All financial information contained in this offering circular is presented on a non-consolidated basis, unlessstated otherwise. Financial and other information contained in this offering circular regarding individualborrowers, groups or categories of borrowers or classifications by industry, geography, size or other factors,including information as to loans, credits, total exposures, allowances, collateral values, non-performingloans and other items, is derived solely from our internal management information systems.

iv

Under the Korean Banking Act of 1950, as amended (the “Banking Act”), assets accepted in trust by a bankin Korea must be segregated from its other assets in the accounts of that bank. Accordingly, banks,including the Bank, engaged in the banking and trust businesses must maintain two separate accounts, thebank account and the trust account, and two separate sets of records, which provide details of theirrespective banking and trust businesses. All financial information contained in this offering circular relatingto the Bank is presented with respect to the Bank’s bank account only, unless stated otherwise.

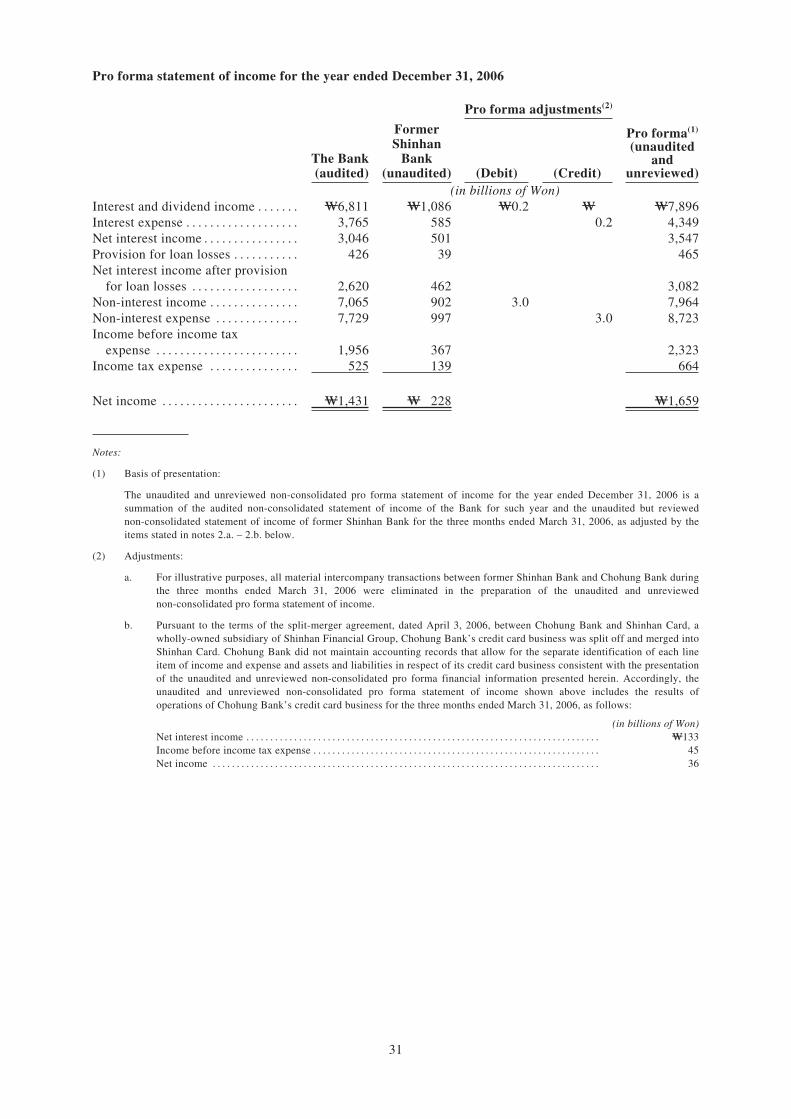

On August 19, 2003, Shinhan Financial Group acquired 80.04% of Chohung Bank’s common shares.Subsequently, Shinhan Financial Group acquired additional common shares of Chohung Bank, and in June2004, acquired all remaining common shares of Chohung Bank. As of April 3, 2006, Shinhan FinancialGroup merged former Shinhan Bank into Chohung Bank, with the latter being the surviving legal entity, andsplit-merged the credit card business of Chohung Bank into Shinhan Card Co., Ltd. (“Shinhan Card”), asubsidiary of Shinhan Financial Group. On the same date, the surviving entity from the merger of formerShinhan Bank and Chohung Bank changed its name to Shinhan Bank. Accordingly, unless otherwise stated,the financial and statistical information of the Bank for the year ended December 31, 2006 contained in thisoffering circular does not include information for former Shinhan Bank prior to the merger on April 3,2006. See also “Unaudited Non-consolidated Pro Forma Income Statement”.

ENFORCEABILITY OF CIVIL LIABILITIES

The Bank is a corporation organized under the laws of Korea. All of the Bank’s directors and officers andcertain other persons named in this offering circular reside in Korea, and all or a significant portion of theassets of the directors and officers and certain other persons named in this offering circular andsubstantially all of the Bank’s assets are located in Korea. As a result, it may not be possible for you toeffect service of process within the United States upon such persons or to enforce against them or against usin U.S. courts judgments predicated upon the civil liability provisions of the federal securities laws of theUnited States. There is doubt as to the enforceability in Korea, either in original actions or in actions forenforcement of judgments of U.S. courts, of civil liabilities predicated on the U.S. federal securities laws.

AVAILABLE INFORMATION

To permit compliance with Rule 144A under the Securities Act in connection with sales of the Notes, theBank will be required under the Fiscal Agency Agreement to be entered into as of the closing date of thisoffering (the “Fiscal Agency Agreement”) between the Bank and The Bank of New York Mellon, as thefiscal agent (the “Fiscal Agent”), to furnish, upon request, to a Holder (as defined in “Description of theNotes — General”) of a Note and a prospective investor designated by such Holder, the informationrequired to be delivered under Rule 144A(d)(4) under the Securities Act unless at the time of the request weare a reporting company under Section 13 or Section 15(d) of the United States Securities Exchange Act of1934, as amended (the “Exchange Act”), or the Bank is exempt from the registration requirements ofSection 12(g) of the Exchange Act (and therefore are required to publish on its Web site, in English, certaininformation pursuant to Rule 12g3-2(b) under the Exchange Act). In accordance with the Fiscal AgencyAgreement, the Fiscal Agent also will make available for inspection by Holders of the Notes or, in certaincases, arrange for the mailing to such Holders, certain reports or communications received from us. See“Description of the Notes — Notices”.

Copies of the Bank’s articles of incorporation and the Fiscal Agency Agreement are available free of chargefrom the specified offices of the Fiscal Agent. We prepare audited annual financial statements andunaudited interim financial statements in accordance with generally accepted accounting principles in Korea(“Korean GAAP”), which will be available at the office of the Fiscal Agent.

v

FORWARD-LOOKING STATEMENTS

This offering circular contains certain “forward-looking statements” that are based on the Bank’s currentexpectations, assumptions, estimates and projections about it and its industry. The forward-lookingstatements are subject to various risks and uncertainties. Generally, these forward-looking statements can beidentified by the use of forward-looking terminology such as “anticipate”, “believe”, “estimate”, “expect”,“intend”, “target”, “seek”, “aim”, “contemplate”, “project”, “plan”, “goal”, “should” and similarexpressions or the negatives thereof. Those statements include, among other things, the discussions of theBank’s business strategy and expectations concerning its market position, future operations, cash flows,margins, profitability, liquidity and capital resources. The Bank cautions you that reliance on any forward-looking statement involves risks and uncertainties, and that although the Bank believes that the assumptionson which its forward-looking statements are based are reasonable, any of those assumptions could prove tobe inaccurate, and, as a result, the forward-looking statements based on those assumptions could beincorrect. The uncertainties in this regard include, but are not limited to, those identified in the risk factorsdiscussed elsewhere in this offering circular. See the section entitled “Risk Factors” beginning on page 11.In light of these and other uncertainties, you should not conclude that the Bank will necessarily achieve anyplans and objectives or projected financial results referred to in any of the forward-looking statements. TheBank does not undertake to release the results of any revisions of these forward-looking statements toreflect future events or circumstances, except as required by law.

vi

SUMMARY

You should read the following summary as an introduction to and in conjunction with the more detailedinformation about the Bank and its financial statements contained elsewhere in this offering circular.

The Bank

Introduction

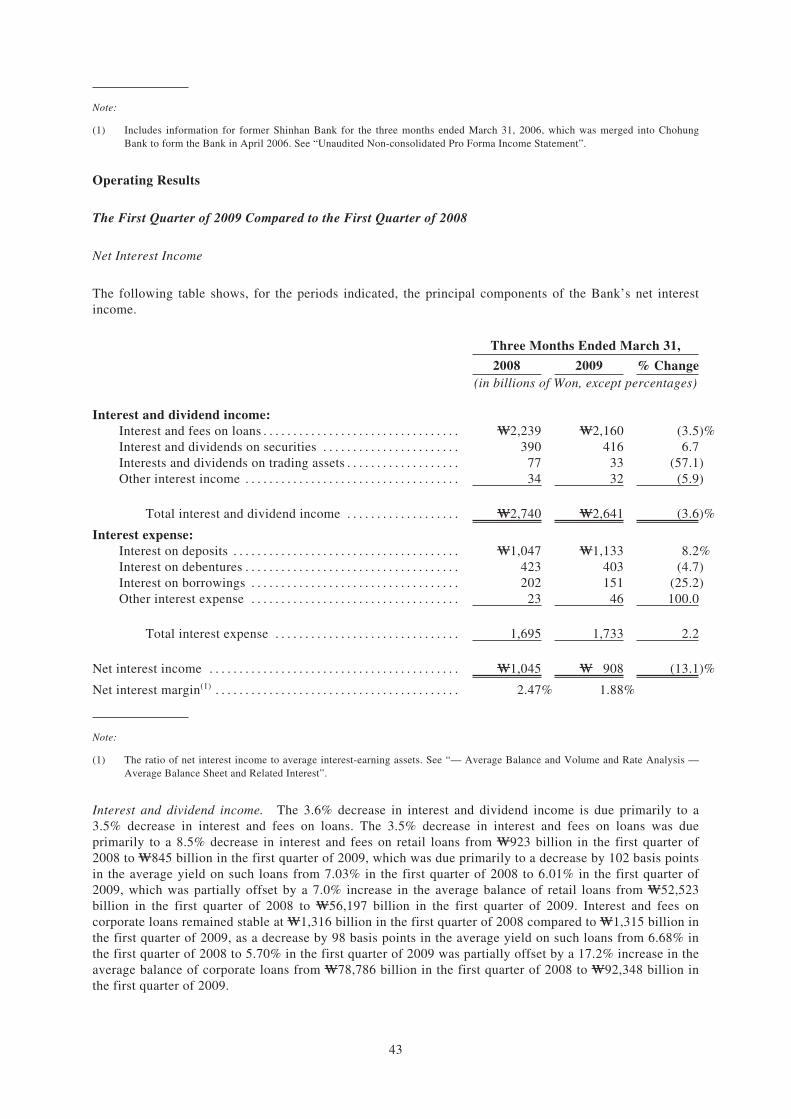

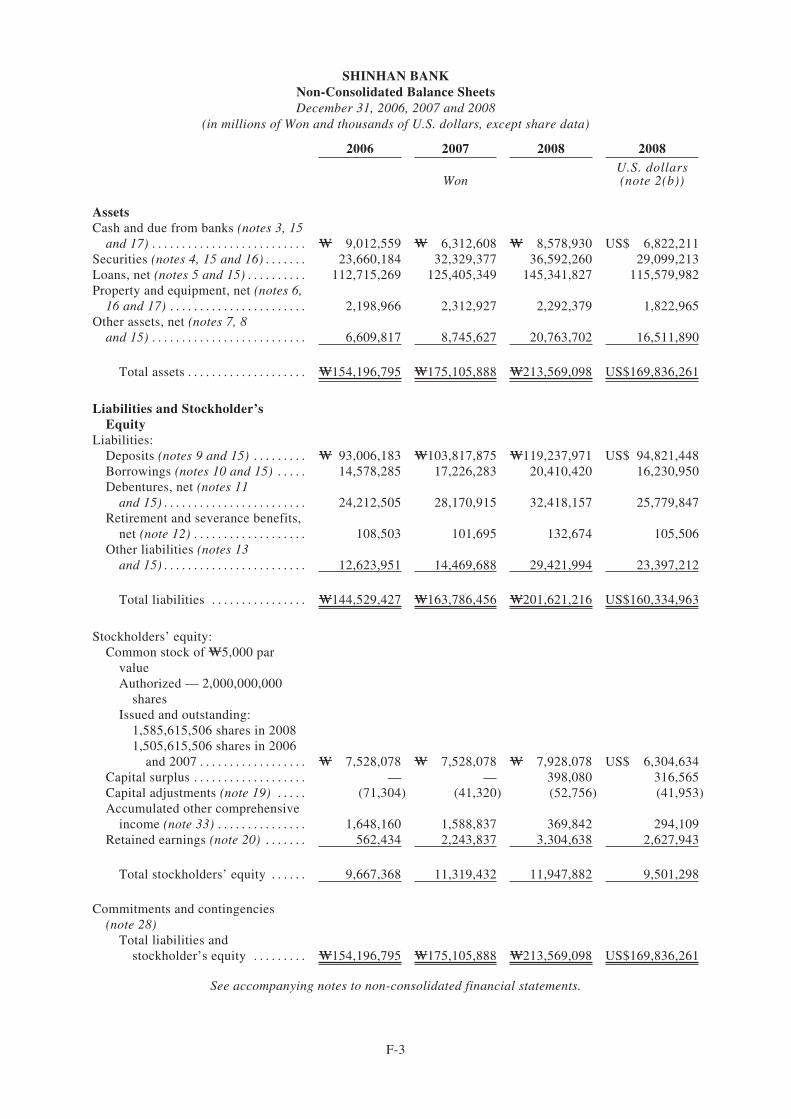

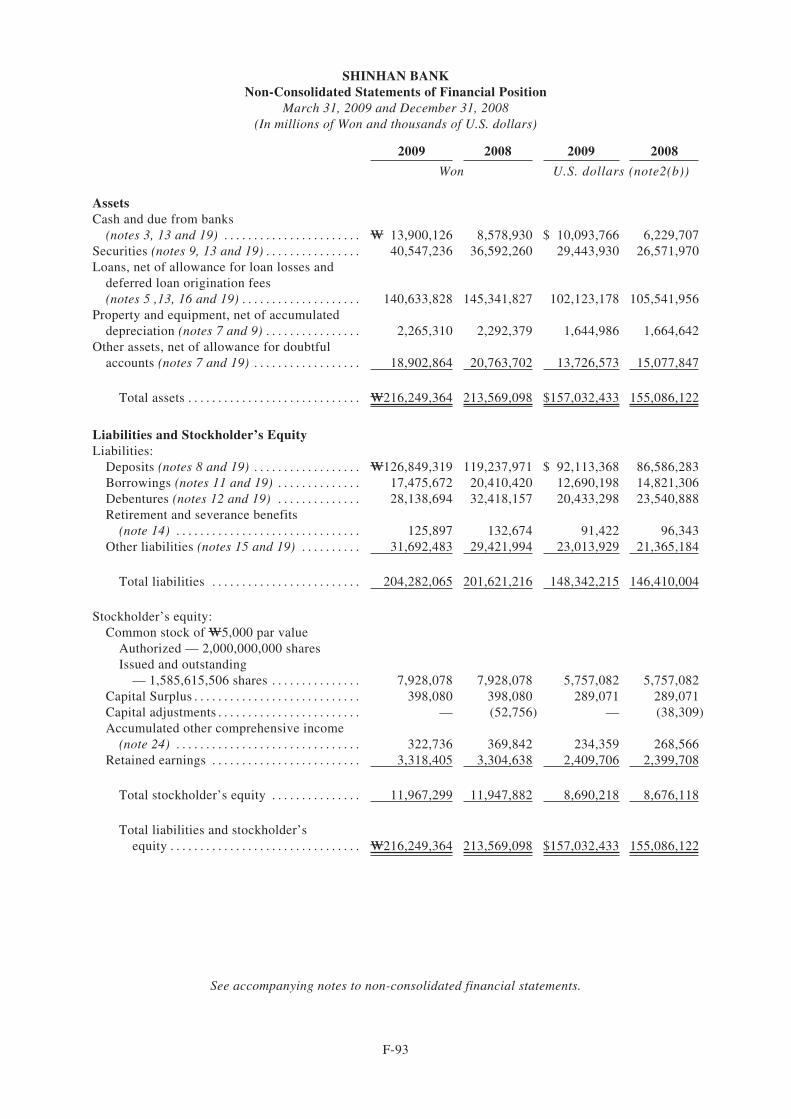

The Bank is the third largest commercial bank in Korea in terms of total assets as of March 31, 2009. TheBank provides a wide range of banking products and services to small- and medium-sized enterprises, largecorporations and individuals in Korea. As of March 31, 2009, the Bank served approximately 5.2 millionactive customers (meaning customers who maintain a monthly average deposit balance of W300,000 ormore or who have a positive monthly average loan balance with the Bank), through a nationwide network of944 branches and 7,147 automated banking terminals, as well as fixed line, mobile telephone and Internetbanking. As of March 31, 2009, the Bank’s non-consolidated total assets, net loans (after deductingallowance for loan losses) and bank account deposits, which do not include the assets and liabilities of trustaccounts, were W216,249 billion, W140,634 billion and W126,849 billion, respectively.

Lending to small- and medium-sized enterprises in Korea has been a principal focus of the Bank’soperations and the Bank remains one of the largest lenders in Korea to these customers. As of March 31,2009 and December 31, 2008, the Bank’s loans to small- and medium-sized enterprises totaled W62,144billion and W61,813 billion, respectively, which accounted for 43.4 % and 41.8% of the Bank’s total loans.This customer segment represents a broad spectrum of corporations in Korea, both by type of lending andtype of customer. The Bank believes that its extensive branch network facilitates its customer-orientedapproach to service this diversified group of customers.

Since its inception, prudent risk management has been one of the highest priorities of the Bank’s operations.As of March 31, 2009, the Bank’s capital adequacy ratio, as reported to the Korean Financial SupervisoryService, was 14.46%, which was highest among Korean commercial banks.

The Bank is the largest subsidiary of Shinhan Financial Group, which is the first privately establishedfinancial holding company in Korea. Shinhan Financial Group is one of the three largest financial servicesproviders in Korea as measured by total assets as of March 31, 2009 and, through its subsidiaries, providesa wide range of financial products and services, including banking, credit card services, brokerage,insurance and asset management services, including the largest credit card operation in Korea. The Bankbelieves that its business has benefited from the cross-selling and other synergy opportunities with othermember companies of Shinhan Financial Group. For more information on the financial holding companystructure, see “Shinhan Financial Group”.

Former Shinhan Bank was established in 1982 as the first privately funded commercial bank in Korea.Chohung Bank was established in 1897 and was the oldest financial institution in Korea. Former ShinhanBank and Chohung Bank were merged on April 3, 2006 and the new bank was named “Shinhan Bank”. TheBank’s headquarters is located at 120, 2-Ka, Taepyung-ro, Chung-Ku, Seoul, Korea. As of March 31, 2009,the Bank had nine consolidated subsidiaries, located in Seoul, Hong Kong, New York, Los Angeles,Toronto, Frankfurt, Phnom Penh, Beijing and Almaty.

Strategy

Prior to the onset of the current turmoil in the financial services industry and macro-economy in Korea aswell as globally, the Bank’s primary strategic focus has been on enhancing its market position in the Koreanbanking industry, achieving economy of scale in each major business segment, and integrating the businessunits of former Shinhan Bank and Chohung Bank.

1

The Bank believes that the level of uncertainty and volatility presented by the ongoing market andeconomic conditions presents a unique set of challenges and opportunities that requires it to realign itsstrategic priorities in order to ensure that it positions itself to best weather the current market crisis as wellas to capture the opportunities that emerge from it. Accordingly, the Bank plans to take a more “back tobasics” approach in protecting and strengthening the fundamentals of, and synergy among, its core businesslines, which will serve as the platform for pursuing sustainable growth group-wide and further solidifyingits competitive leadership, notwithstanding the difficult prospects in the global and domestic market andeconomic conditions.

More specifically, the Bank’s “back to basics” approach in light of the current crisis will focus on thefollowing fundamentals of its core businesses:

Further strengthen risk management. The Bank plans to make its risk management system morecomprehensive and pre-emptive in detecting and assessing any known and potential risks throughearly alerts and multiple contingency management plans. The Bank will also seek to improve itsoverall asset quality and minimize any reputational risk by reassessing the risk profile of its corebusinesses and realigning their respective asset portfolios by reducing exposure to high-risk assets.

Strengthen the profit structure. In order to improve the Bank’s profitability, it plans, among others,to adopt greater differentiation in risk-profiling its products to price them more accurately,aggressively restructure low-profit and overlapping product lines and loss-leaders, conservativelydiversify its revenue streams by taking advantage of market openings allowed by regulatory changes,deepen its banking customer relationships by capturing a greater market share of auto payroll depositaccounts and further expand cross-selling opportunities across the group-wide business units.

Capture maximum synergy. The Bank plans to continue to assist in building out, in conjunction withShinhan Financial Group’s group-wide efforts, informational networks and shared databases in orderto maximize opportunities for target marketing, up-selling and cross-selling as well as deepeningcustomer loyalty and relationships at the group level.

The Bank plans to use its strong business fundamentals as described above to become a world-class bankthat ranks among the leaders of the banking industry in Asia and globally. The Bank aims to achieve suchobjective by implementing the following strategies and focusing on the following objectives and initiatives:

Pursue new customer-oriented marketing to enhance customer loyalty. To further develop andenhance the loyalty of the Bank’s customers across all business segments, the Bank will (i) developcomprehensive banking services for each customer segment, (ii) formulate customized marketing andbusiness strategies for each customer segment, (iii) strengthen its direct marketing efforts, (iv) explorenew businesses to meet changes in customers’ needs, (v) seek to develop innovative products andservices, such as ubiquitous banking and foreign financial product investment services, and (vi) offerdiversified investment products to customers. In particular, the Bank is focusing on the developmentof its mass-market customer basis. In addition, the Bank plans to combine its commercial bankingchannels with its investment banking products to create a unique commercial investment bankingmodel in Korea and simultaneously seek investment banking opportunities in the overseas markets.

Establish an optimal earnings structure for corporate sustainability. The Bank aims to strengthen itsfoundation of income sources, with particular efforts to increase its non-interest income. Furthermore,the Bank aims to secure a sound management structure to improve risk management, achieve anoptimal balance of funding and funds operations and strengthen its infrastructure and systems tomaximize earnings from cross-selling products and services of its affiliates.

Establish a sound foundation to compete globally. To enable the Bank to compete in the globalfinancial markets, it aims to (i) improve its brand value, (ii) continue to create customer-orientedoperating systems and processes, (iii) establish a system to create, accumulate, utilize and shareintellectual property among the Bank and its affiliates, (iv) create a flexible organizational culture that

2

embraces changes in market conditions and customers’ demands and (v) establish a platform to enablethe Bank to strengthen its strategic co-operation with foreign financial institutions and create a globalnetwork to exchange information and ideas.

Creating synergies within the holding company structure of Shinhan Financial Group. Since theestablishment of a financial holding company, Shinhan Financial Group, in 2001, the Bank hasfocused on achieving synergy through cross-selling of products and services of the other subsidiariesof Shinhan Financial Group. The Bank and its affiliates, Goodmorning Shinhan Securities andShinhan Life Insurance, together serve as the primary distribution channel for Shinhan FinancialGroup while the other non-bank members of the Shinhan Financial Group are focusing on developingcompetitive products and services. Examples of the principal products for cross-selling in the retailsegment include bancassurance, credit cards, beneficiary certificates and “Financial NetworkAccounts”, which are integrated accounts for banking, brokerage and insurance services. In particular,the Bank intends to capitalize on the synergistic benefits of the acquisition by Shinhan FinancialGroup of LG Card and its substantial customer base. See “Shinhan Financial Group”.

Establishing and Consolidating the One Portal Network. In order to provide total financial solutionsto the customers of the Bank and other members of the Shinhan Financial Group on a real-time basis,the Bank, together with other members of the Shinhan Financial Group, is continuing to develop aone-portal network for the Shinhan Financial Group. The one-portal network refers to the ability of acorporate or retail customer to have access to a total financial solution through any single point ofcontact with any member of Shinhan Financial Group.

3

Summary Financial Data

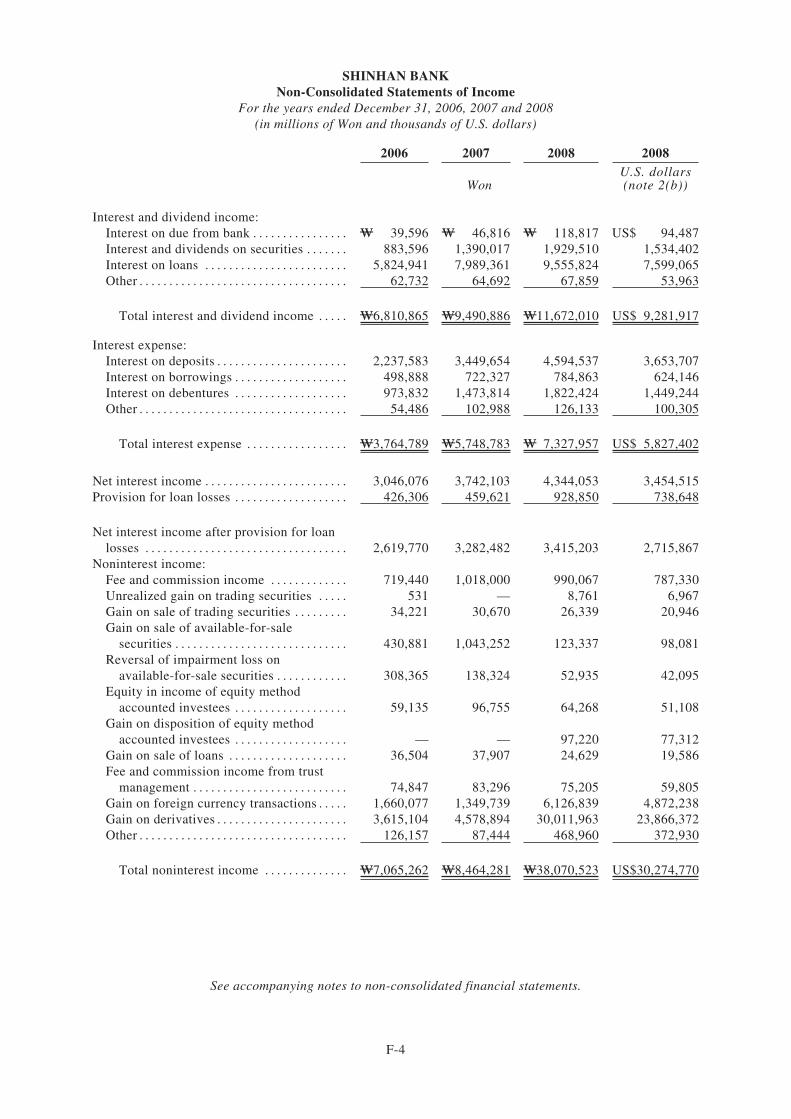

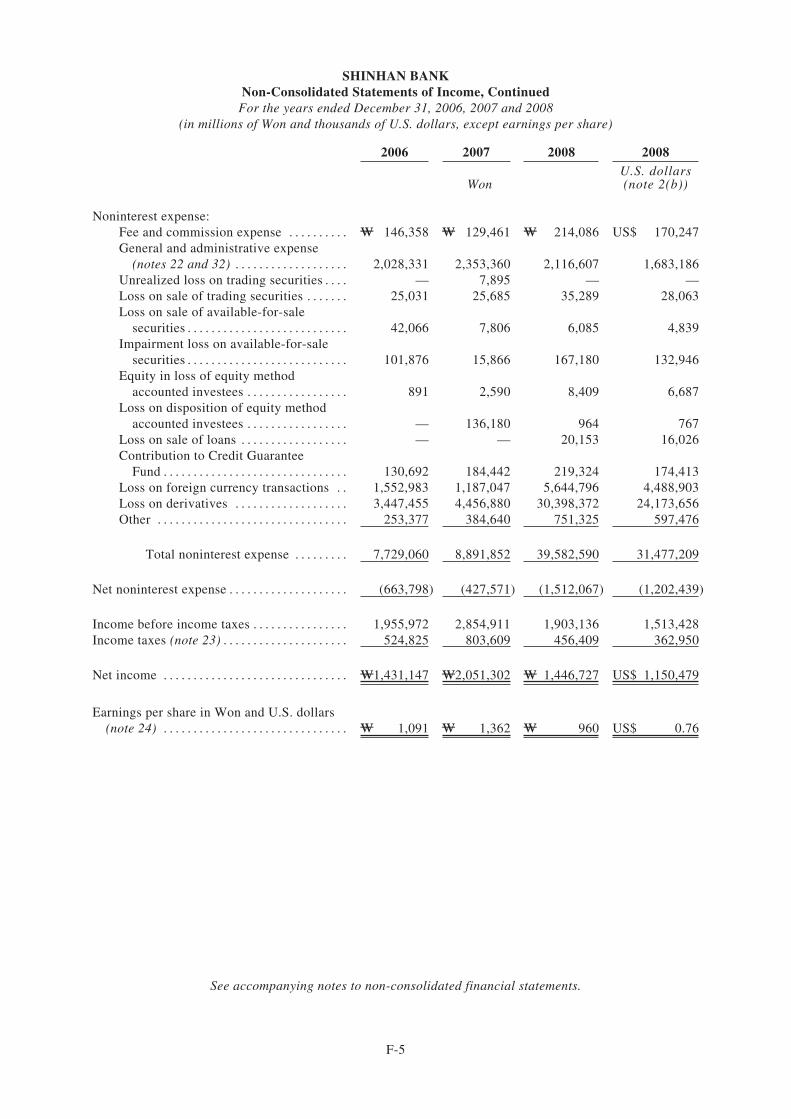

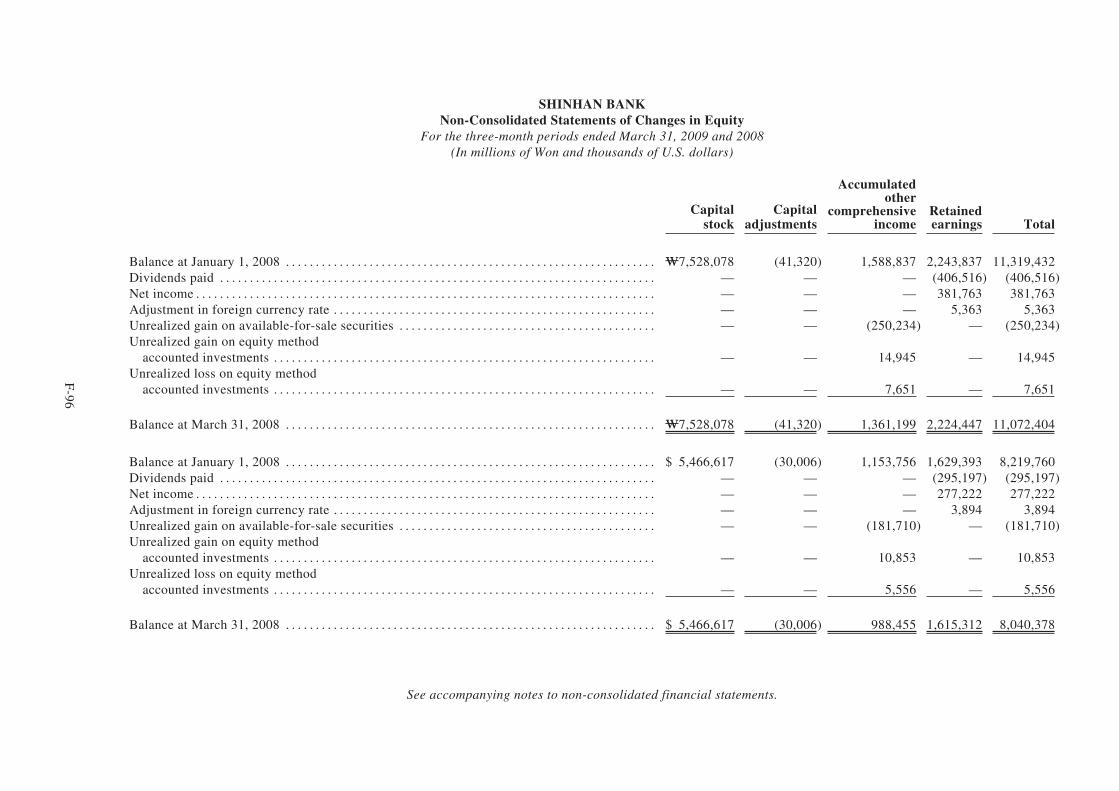

The following tables set forth summary non-consolidated income statement and balance sheet data withrespect to the Bank as of and for the years ended December 31, 2006, 2007 and 2008, which have beenderived from the Bank’s audited non-consolidated financial statements as of such dates and for suchperiods, and as of March 31, 2009 and for the three months ended March 31, 2008 and 2009, which havebeen derived from the Bank’s unaudited non-consolidated interim financial statements as of such date andfor such periods.

The non-consolidated financial statements exclude the accounts of all of the Bank’s subsidiaries (exceptthat the value of the Bank’s equity investments in their respective consolidated subsidiaries is included) andtheir respective trust account management business. The non-consolidated financial statements have beenprepared in accordance with Korean GAAP and, where applicable, the Korean Bank Accounting Guidelines,which differ in certain material respects from U.S. GAAP, and have not been intended to present thefinancial position, results of operations, cash flows and changes in equity in accordance with generallyaccepted accounting policies and practices in countries and jurisdictions other than Korea. For a discussionof certain differences between Korean GAAP and U.S. GAAP, see “Summary of Certain Differencesbetween Korean GAAP and U.S. GAAP” in this offering circular.

Certain financial information contained in “Business” and “Description of Assets and Liabilities of theBank” was not derived directly from the Bank’s unaudited non-consolidated interim financial statements asof March 31, 2009 and for the three months ended March 31, 2008 and 2009 or from the Bank’s auditednon-consolidated financial statements as of and for the years ended December 31, 2006, 2007 and 2008 butwas derived from certain accounting records, which were unaudited but were subject to the Bank’s internalcontrol over financial reporting.

On August 19, 2003, Shinhan Financial Group acquired 80.04% of Chohung Bank’s common shares.Subsequently, Shinhan Financial Group acquired additional common shares of Chohung Bank, and in June2004, acquired all remaining common shares of Chohung Bank. As of April 3, 2006, Shinhan FinancialGroup merged former Shinhan Bank into Chohung Bank, with the latter being the surviving legal entity, andsplit-merged the credit card business of Chohung Bank into Shinhan Card, a subsidiary of ShinhanFinancial Group. On the same date, the surviving entity from the merger of former Shinhan Bank andChohung Bank changed its name to Shinhan Bank. Accordingly, unless otherwise stated, the financial andstatistical information of the Bank for the year ended December 31, 2006 contained in this offering circulardoes not include information for former Shinhan Bank prior to the merger on April 3, 2006.

4

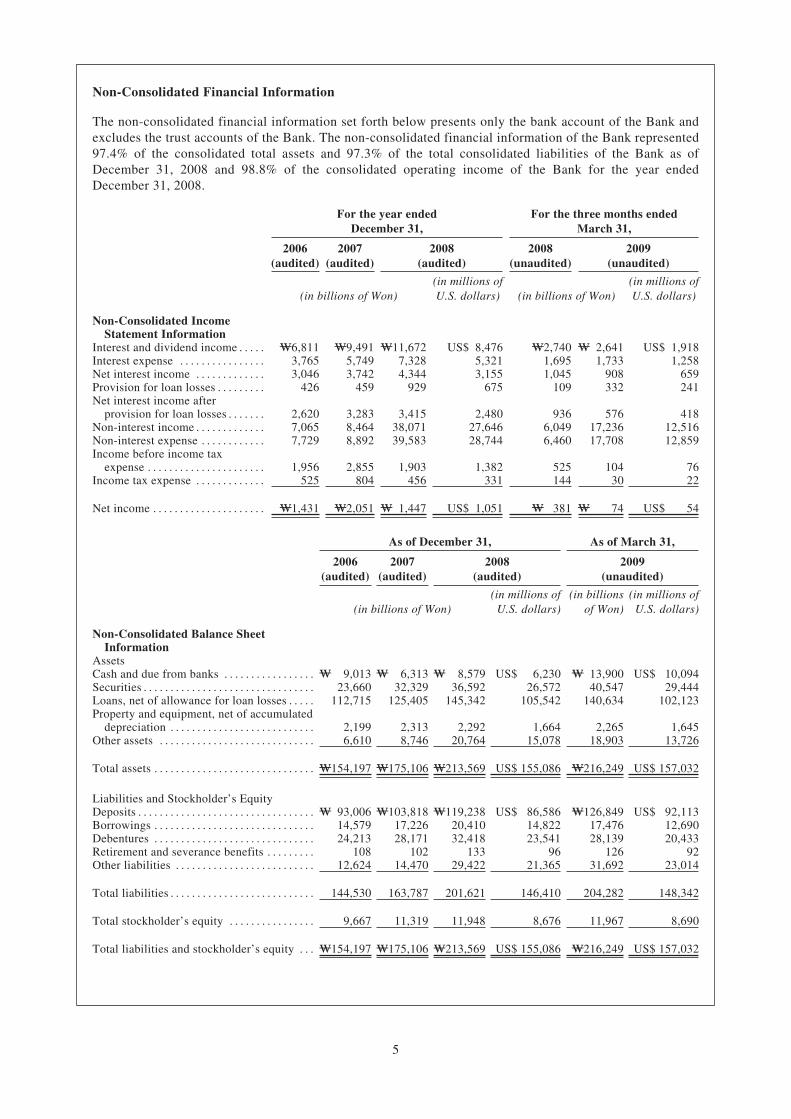

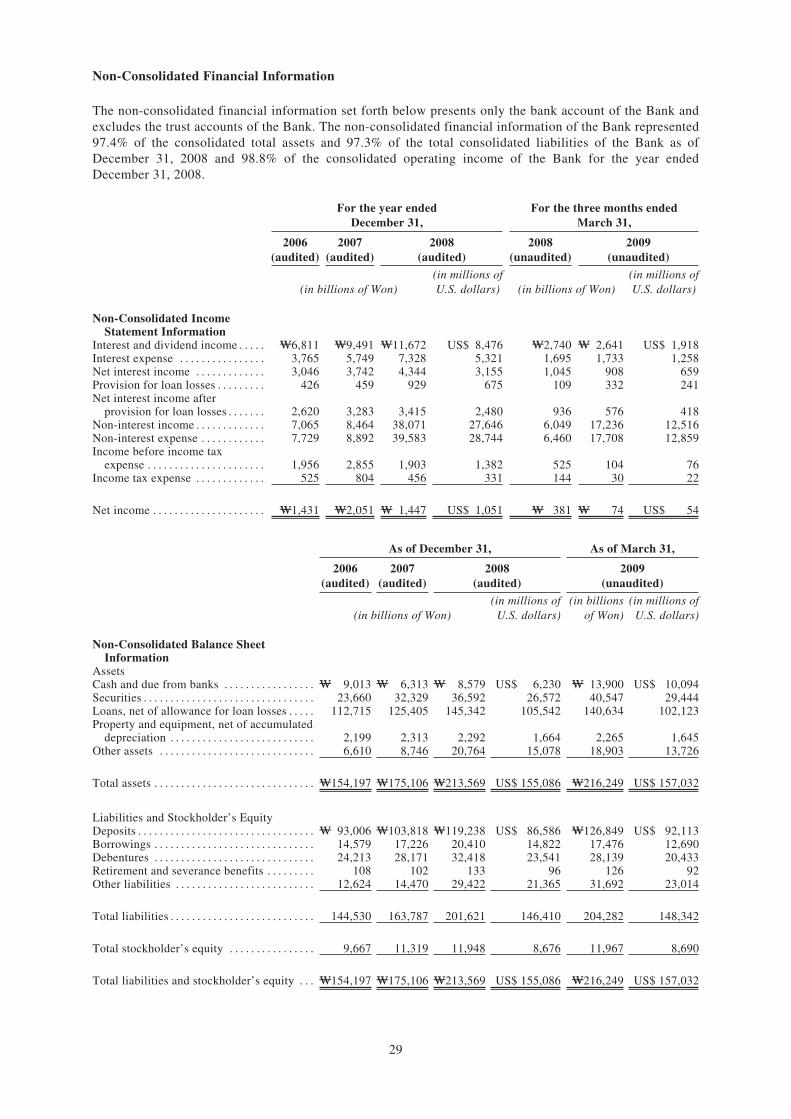

Non-Consolidated Financial Information

The non-consolidated financial information set forth below presents only the bank account of the Bank andexcludes the trust accounts of the Bank. The non-consolidated financial information of the Bank represented97.4% of the consolidated total assets and 97.3% of the total consolidated liabilities of the Bank as ofDecember 31, 2008 and 98.8% of the consolidated operating income of the Bank for the year endedDecember 31, 2008.

For the year endedDecember 31,

For the three months endedMarch 31,

2006(audited)

2007(audited)

2008(audited)

2008(unaudited)

2009(unaudited)

(in billions of Won)(in millions ofU.S. dollars) (in billions of Won)

(in millions ofU.S. dollars)

Non-Consolidated IncomeStatement Information

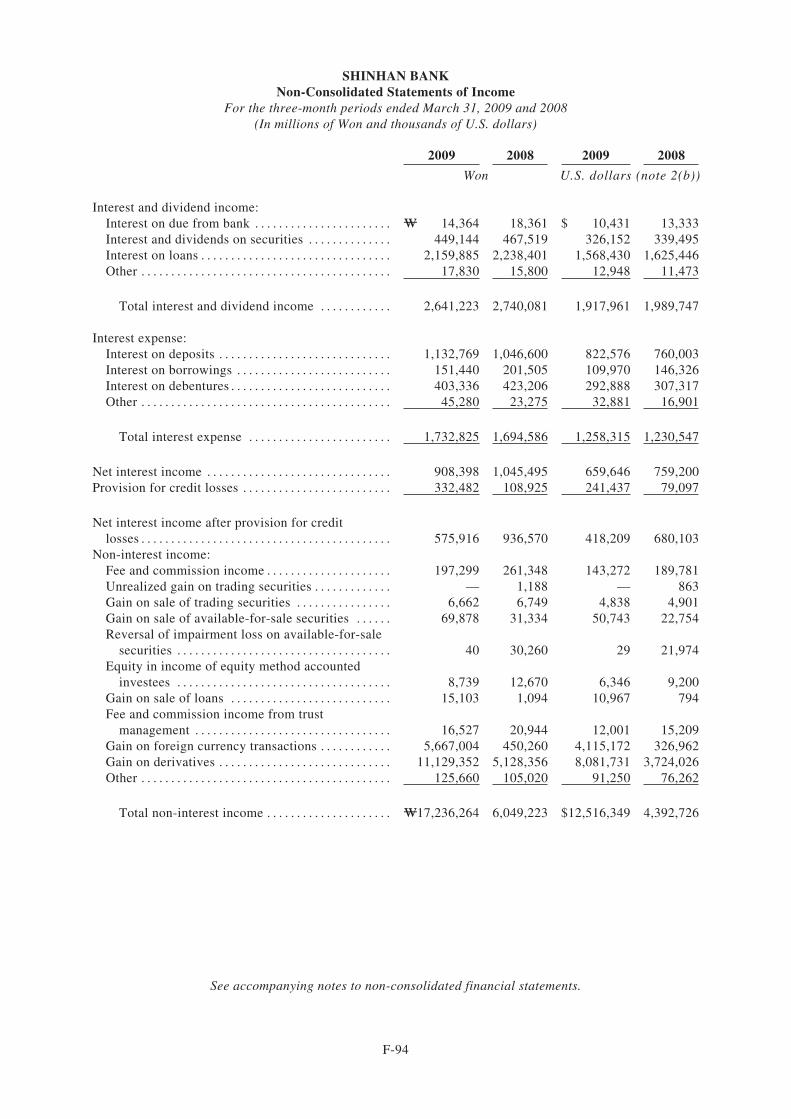

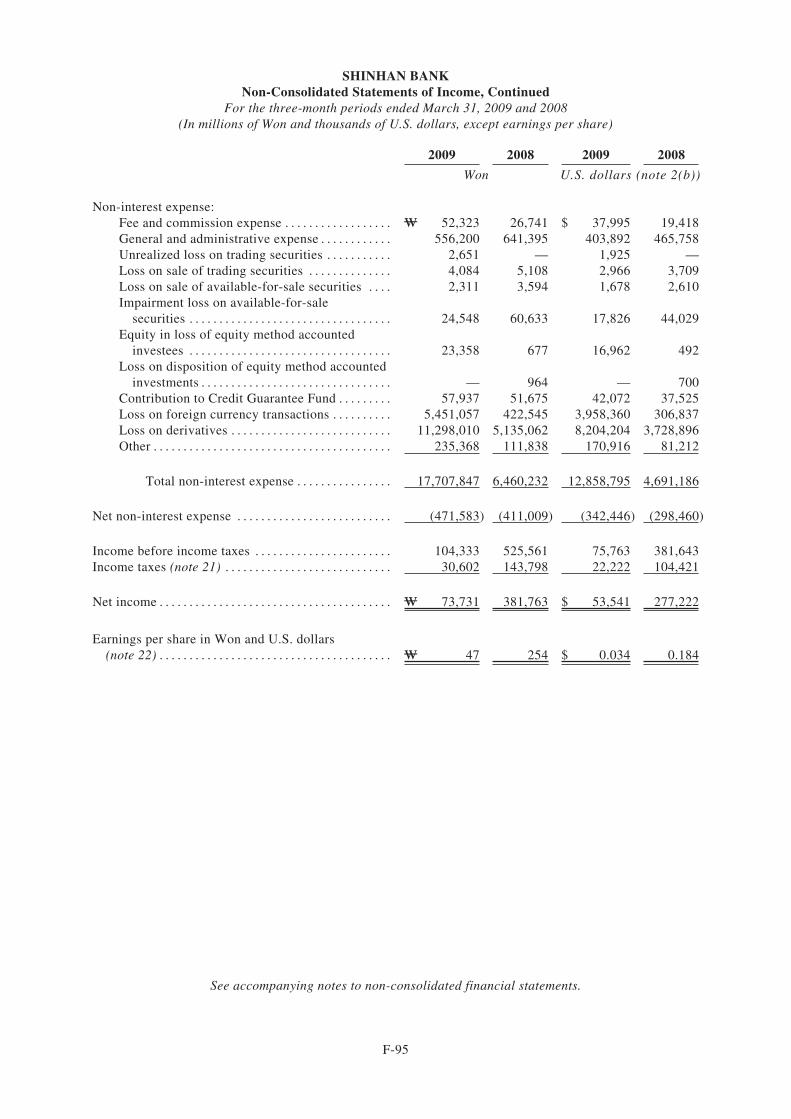

Interest and dividend income . . . . . W6,811 W9,491 W11,672 US$ 8,476 W2,740 W 2,641 US$ 1,918Interest expense . . . . . . . . . . . . . . . . 3,765 5,749 7,328 5,321 1,695 1,733 1,258Net interest income . . . . . . . . . . . . . 3,046 3,742 4,344 3,155 1,045 908 659Provision for loan losses . . . . . . . . . 426 459 929 675 109 332 241Net interest income after

provision for loan losses . . . . . . . 2,620 3,283 3,415 2,480 936 576 418Non-interest income . . . . . . . . . . . . . 7,065 8,464 38,071 27,646 6,049 17,236 12,516Non-interest expense . . . . . . . . . . . . 7,729 8,892 39,583 28,744 6,460 17,708 12,859Income before income tax

expense . . . . . . . . . . . . . . . . . . . . . . 1,956 2,855 1,903 1,382 525 104 76Income tax expense . . . . . . . . . . . . . 525 804 456 331 144 30 22

Net income . . . . . . . . . . . . . . . . . . . . . W1,431 W2,051 W 1,447 US$ 1,051 W 381 W 74 US$ 54

As of December 31, As of March 31,

2006(audited)

2007(audited)

2008(audited)

2009(unaudited)

(in billions of Won)(in millions of

U.S. dollars)(in billions

of Won)(in millions of

U.S. dollars)

Non-Consolidated Balance SheetInformation

AssetsCash and due from banks . . . . . . . . . . . . . . . . . W 9,013 W 6,313 W 8,579 US$ 6,230 W 13,900 US$ 10,094Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23,660 32,329 36,592 26,572 40,547 29,444Loans, net of allowance for loan losses . . . . . 112,715 125,405 145,342 105,542 140,634 102,123Property and equipment, net of accumulated

depreciation . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,199 2,313 2,292 1,664 2,265 1,645Other assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,610 8,746 20,764 15,078 18,903 13,726

Total assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . W154,197 W175,106 W213,569 US$ 155,086 W216,249 US$ 157,032

Liabilities and Stockholder’s EquityDeposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . W 93,006 W103,818 W119,238 US$ 86,586 W126,849 US$ 92,113Borrowings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14,579 17,226 20,410 14,822 17,476 12,690Debentures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24,213 28,171 32,418 23,541 28,139 20,433Retirement and severance benefits . . . . . . . . . 108 102 133 96 126 92Other liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . 12,624 14,470 29,422 21,365 31,692 23,014

Total liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . 144,530 163,787 201,621 146,410 204,282 148,342

Total stockholder’s equity . . . . . . . . . . . . . . . . 9,667 11,319 11,948 8,676 11,967 8,690

Total liabilities and stockholder’s equity . . . W154,197 W175,106 W213,569 US$ 155,086 W216,249 US$ 157,032

5

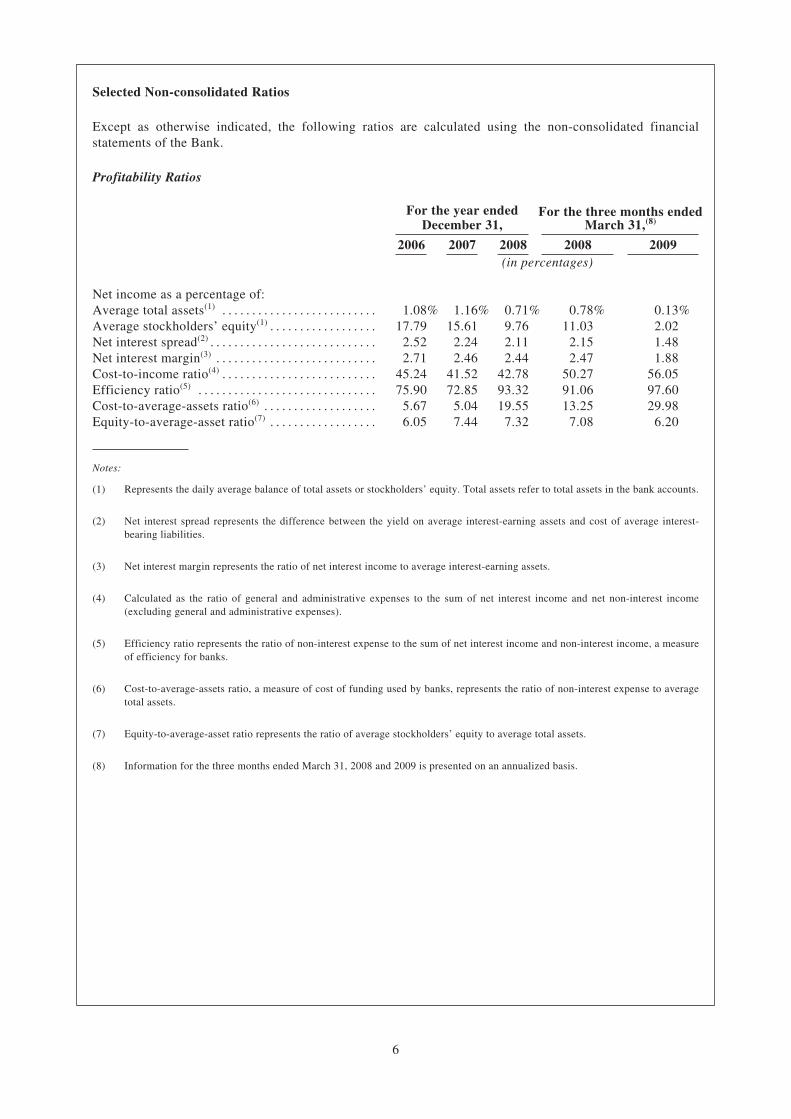

Selected Non-consolidated Ratios

Except as otherwise indicated, the following ratios are calculated using the non-consolidated financialstatements of the Bank.

Profitability Ratios

For the year endedDecember 31,

For the three months endedMarch 31,(8)

2006 2007 2008 2008 2009(in percentages)

Net income as a percentage of:Average total assets(1) . . . . . . . . . . . . . . . . . . . . . . . . . . 1.08% 1.16% 0.71% 0.78% 0.13%Average stockholders’ equity(1) . . . . . . . . . . . . . . . . . . 17.79 15.61 9.76 11.03 2.02Net interest spread(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.52 2.24 2.11 2.15 1.48Net interest margin(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.71 2.46 2.44 2.47 1.88Cost-to-income ratio(4) . . . . . . . . . . . . . . . . . . . . . . . . . . 45.24 41.52 42.78 50.27 56.05Efficiency ratio(5) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75.90 72.85 93.32 91.06 97.60Cost-to-average-assets ratio(6) . . . . . . . . . . . . . . . . . . . 5.67 5.04 19.55 13.25 29.98Equity-to-average-asset ratio(7) . . . . . . . . . . . . . . . . . . 6.05 7.44 7.32 7.08 6.20

Notes:

(1) Represents the daily average balance of total assets or stockholders’ equity. Total assets refer to total assets in the bank accounts.

(2) Net interest spread represents the difference between the yield on average interest-earning assets and cost of average interest-bearing liabilities.

(3) Net interest margin represents the ratio of net interest income to average interest-earning assets.

(4) Calculated as the ratio of general and administrative expenses to the sum of net interest income and net non-interest income(excluding general and administrative expenses).

(5) Efficiency ratio represents the ratio of non-interest expense to the sum of net interest income and non-interest income, a measureof efficiency for banks.

(6) Cost-to-average-assets ratio, a measure of cost of funding used by banks, represents the ratio of non-interest expense to averagetotal assets.

(7) Equity-to-average-asset ratio represents the ratio of average stockholders’ equity to average total assets.

(8) Information for the three months ended March 31, 2008 and 2009 is presented on an annualized basis.

6

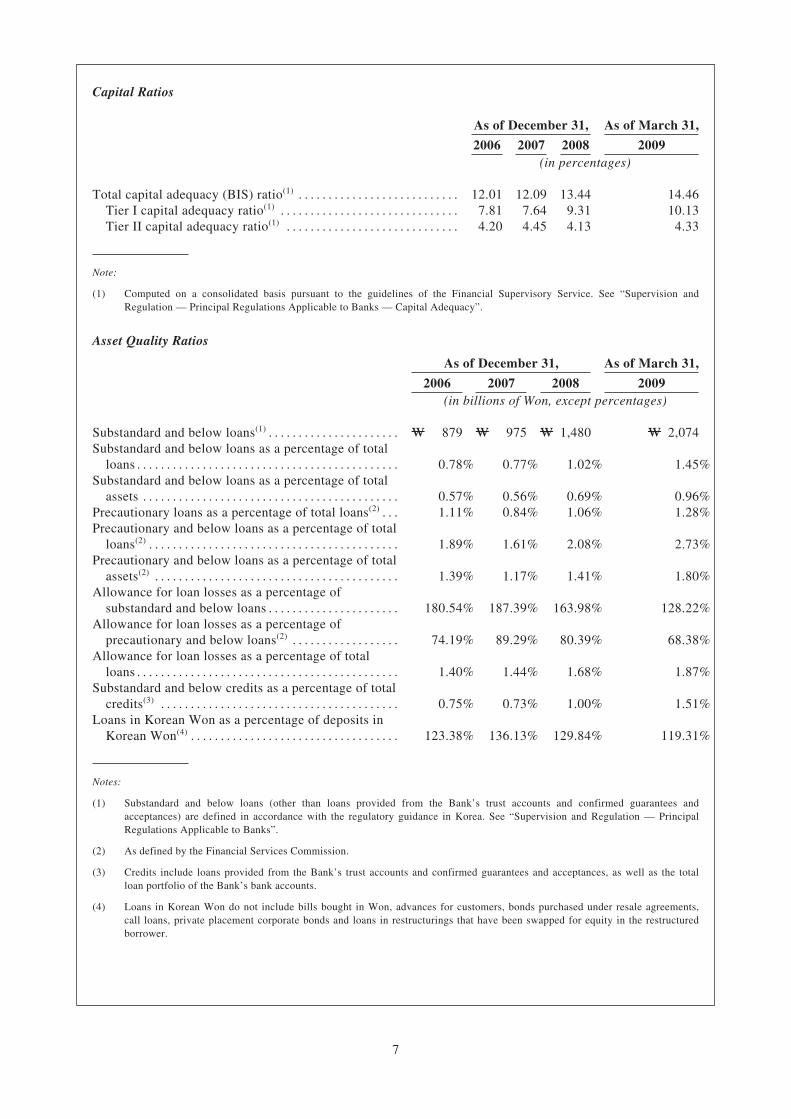

Capital Ratios

As of December 31, As of March 31,

2006 2007 2008 2009(in percentages)

Total capital adequacy (BIS) ratio(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . 12.01 12.09 13.44 14.46Tier I capital adequacy ratio(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7.81 7.64 9.31 10.13Tier II capital adequacy ratio(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.20 4.45 4.13 4.33

Note:

(1) Computed on a consolidated basis pursuant to the guidelines of the Financial Supervisory Service. See “Supervision andRegulation — Principal Regulations Applicable to Banks — Capital Adequacy”.

Asset Quality Ratios

As of December 31, As of March 31,

2006 2007 2008 2009(in billions of Won, except percentages)

Substandard and below loans(1) . . . . . . . . . . . . . . . . . . . . . . W 879 W 975 W 1,480 W 2,074Substandard and below loans as a percentage of total

loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.78% 0.77% 1.02% 1.45%Substandard and below loans as a percentage of total

assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.57% 0.56% 0.69% 0.96%Precautionary loans as a percentage of total loans(2) . . . 1.11% 0.84% 1.06% 1.28%Precautionary and below loans as a percentage of total

loans(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.89% 1.61% 2.08% 2.73%Precautionary and below loans as a percentage of total

assets(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.39% 1.17% 1.41% 1.80%Allowance for loan losses as a percentage of

substandard and below loans . . . . . . . . . . . . . . . . . . . . . . 180.54% 187.39% 163.98% 128.22%Allowance for loan losses as a percentage of

precautionary and below loans(2) . . . . . . . . . . . . . . . . . . 74.19% 89.29% 80.39% 68.38%Allowance for loan losses as a percentage of total

loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.40% 1.44% 1.68% 1.87%Substandard and below credits as a percentage of total

credits(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.75% 0.73% 1.00% 1.51%Loans in Korean Won as a percentage of deposits in

Korean Won(4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123.38% 136.13% 129.84% 119.31%

Notes:

(1) Substandard and below loans (other than loans provided from the Bank’s trust accounts and confirmed guarantees andacceptances) are defined in accordance with the regulatory guidance in Korea. See “Supervision and Regulation — PrincipalRegulations Applicable to Banks”.

(2) As defined by the Financial Services Commission.

(3) Credits include loans provided from the Bank’s trust accounts and confirmed guarantees and acceptances, as well as the totalloan portfolio of the Bank’s bank accounts.

(4) Loans in Korean Won do not include bills bought in Won, advances for customers, bonds purchased under resale agreements,call loans, private placement corporate bonds and loans in restructurings that have been swapped for equity in the restructuredborrower.

7

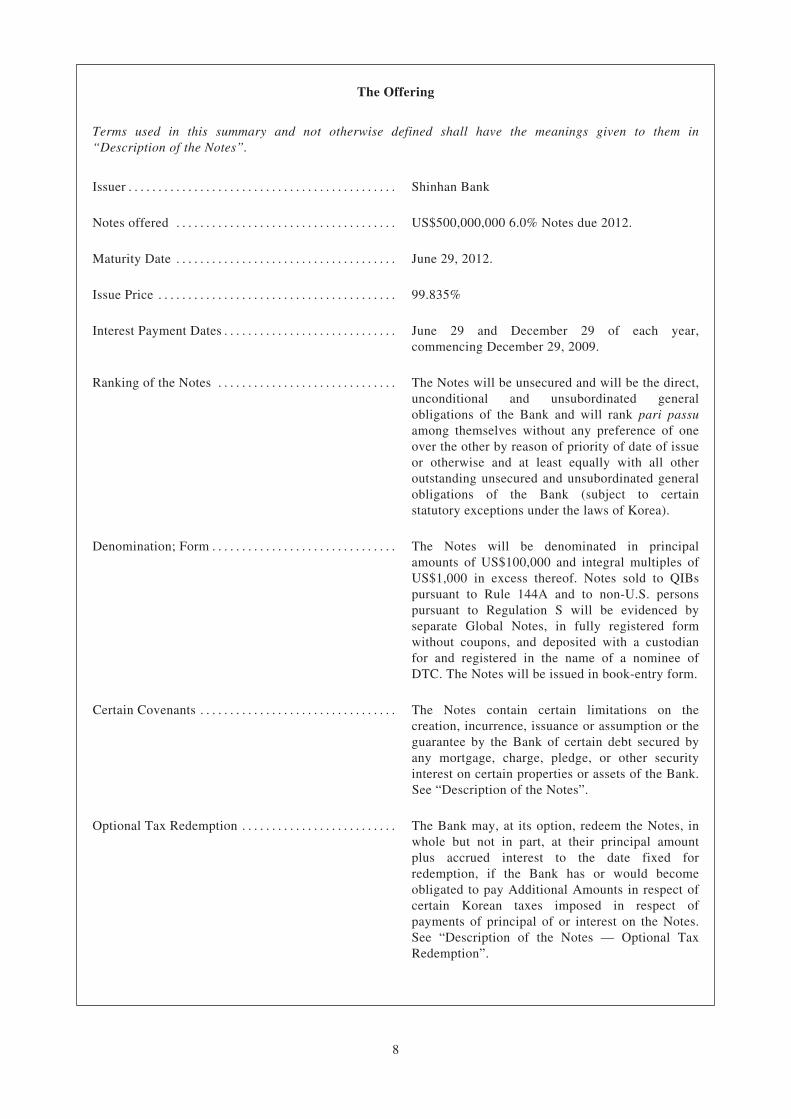

The Offering

Terms used in this summary and not otherwise defined shall have the meanings given to them in“Description of the Notes”.

Issuer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Shinhan Bank

Notes offered . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . US$500,000,000 6.0% Notes due 2012.

Maturity Date . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . June 29, 2012.

Issue Price . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99.835%

Interest Payment Dates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . June 29 and December 29 of each year,commencing December 29, 2009.

Ranking of the Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . The Notes will be unsecured and will be the direct,unconditional and unsubordinated generalobligations of the Bank and will rank pari passuamong themselves without any preference of oneover the other by reason of priority of date of issueor otherwise and at least equally with all otheroutstanding unsecured and unsubordinated generalobligations of the Bank (subject to certainstatutory exceptions under the laws of Korea).

Denomination; Form . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . The Notes will be denominated in principalamounts of US$100,000 and integral multiples ofUS$1,000 in excess thereof. Notes sold to QIBspursuant to Rule 144A and to non-U.S. personspursuant to Regulation S will be evidenced byseparate Global Notes, in fully registered formwithout coupons, and deposited with a custodianfor and registered in the name of a nominee ofDTC. The Notes will be issued in book-entry form.

Certain Covenants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . The Notes contain certain limitations on thecreation, incurrence, issuance or assumption or theguarantee by the Bank of certain debt secured byany mortgage, charge, pledge, or other securityinterest on certain properties or assets of the Bank.See “Description of the Notes”.

Optional Tax Redemption . . . . . . . . . . . . . . . . . . . . . . . . . . The Bank may, at its option, redeem the Notes, inwhole but not in part, at their principal amountplus accrued interest to the date fixed forredemption, if the Bank has or would becomeobligated to pay Additional Amounts in respect ofcertain Korean taxes imposed in respect ofpayments of principal of or interest on the Notes.See “Description of the Notes — Optional TaxRedemption”.

8

Use of Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . The aggregate net proceeds from the offering ofthe Notes are expected to be approximatelyUS$496 million, after deducting underwritingcommissions and certain out-of-pocket expensesrelating to the offering. The net proceeds from theoffering will be used for repayment of existingdebt and other general corporate purposes.

Rating of the Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . The Notes are expected to be rated A2 by Moody’sand A- by S&P. Such ratings do not constitute arecommendation to buy, sell or hold the Notes andmay be subject to revision or withdrawal at anytime by such rating organizations. Each such ratingshould be evaluated independently of any otherrating of the Notes.

Listing and Trading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Application has been made to list the Notes on theSingapore Stock Exchange. The Notes will betraded on the Singapore Stock Exchange in aminimum board lot size of US$200,000 for so longas the Notes are listed on the Singapore StockExchange.

Further Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . The Bank may from time to time, without theconsent of the existing holders of the Notes, createand issue additional notes under the Fiscal AgencyAgreement having the same terms and conditionsas the Notes in all respects except for issue dateand issue price. Additional notes issued in thismanner may be consolidated with and form asingle series with the Notes outstanding at the timeof such further issuance, provided that suchadditional notes must be issued with no more thana de minimis amount of original issue discount orbe part of a “qualified reopening” for U.S. federalincome tax purposes.

Selling Restrictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . There are certain restrictions on the offer, sale andtransfer of the Notes in the United States, UnitedKingdom, Korea, Hong Kong, Singapore andJapan. See “Plan of Distribution — SellingRestrictions”.

Notice to Investors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . The Notes have not been and will not be registeredunder the Securities Act or any state securitieslaws and may not be offered or sold within theUnited States except pursuant to an exemptionfrom, or in a transaction not subject to, theregistration requirements of the Securities Act.Accordingly, the Notes may be offered for saleonly (i) in the United States, to QIBs within themeaning of, and in reliance on, Rule 144A; or(ii) outside the United States in reliance on, and inaccordance with, Regulation S, in each case, incompliance with applicable laws, regulations anddirectives. See “Plan of Distribution — SellingRestrictions” and “Notice to Investors”.

9

Governing Law . . . . . . . . . . The Notes and the Fiscal Agency Agreement will be governed by New Yorklaw.

Risk Factors . . . . . . . . . . . . . See “Risk Factors” and the other information in this offering circular for adiscussion of factors that you should carefully consider before deciding toinvest in the Notes.

Fiscal Agent . . . . . . . . . . . . . The Bank of New York Mellon.

Paying and TransferAgent . . . . . . . . . . . . . . . . . The Bank of New York Mellon. For so long as the Notes are listed on the

Singapore Stock Exchange and the rules of the Singapore Stock Exchange sorequire, the Bank will appoint and maintain a paying agent in Singapore,where the Notes may be presented or surrendered for payment or redemption,in the event that the Bank issues definitive Notes. In addition, in the eventthat any of the Global Notes is exchanged for definitive Notes, anannouncement of such exchange will be made by or on behalf of the Bankthrough the Singapore Stock Exchange and such announcement will includeall material information with respect to the delivery of the definitive Notes,including details of the paying agent in Singapore.

Security Codes . . . . . . . . . . . Rule 144A Notes Regulation S Notes

CUSIPISIN

824589 AC9US824589AC99

Y77488 AA5USY77488AA51

10

RISK FACTORS

In addition to other information contained in this offering circular, you should consider carefully the risksdescribed below. These risks are not the only ones that the Bank faces. Additional risks not currently knownto the Bank or those which the Bank currently believes are immaterial may also impair its businessoperations. The Bank’s business, financial condition or results of operations could be materially adverselyaffected by any of these risks.

Risks Relating to the Current Economic and Market Crisis

The recent difficulties in the global financial markets and their contagion effect on the overall economycould adversely affect the Bank’s asset quality and results of operations.

Since July 2007, significant adverse developments in the U.S. sub-prime mortgage sector have createdsignificant disruption and volatility in financial markets globally. The ensuing contraction of liquidity andcredit and deteriorations in asset values have had contagion effects on the overall economy. Starting in thesecond half of 2008, the world’s largest economies, including the United States, Europe and Japan, arewidely considered to be in the midst of significant economic recessions, and export-driven emergingeconomies such as China and Korea have also suffered substantial weakness in their economies. Forexample, the Korean economy experienced a contraction in real gross domestic product by 3.4% in thefourth quarter of 2008 compared to the fourth quarter of 2007. The weakening economies in Korea andglobally may create further shocks to the global financial markets, which in turn could cause a furtherdownward spiral in global economic and financial conditions.

In Korea, where most of the Bank’s assets are located and where it generates most of its income, there aresigns that, due to the recent significant difficulties in global economic and financial conditions, key macro-and microeconomic indicators such as exports, personal expenditures and consumption, unemploymentrates, demand for business products and services, debt service burden of households and businesses, thegeneral availability of credit and the asset value of real estate and securities may further deteriorate. Any ora combination of the foregoing factors may result in an increase in non-performing loans and worsen theasset quality of the Bank’s loans.

The Bank’s substandard or below credits, as classified according to the Financial Services Commissionguidelines, increased to W2,294 billion as of March 31, 2009 and W1,531 billion as of December 31, 2008,from W981 billion as of December 31, 2007, while the ratio of the Bank’s substandard or below credits tototal credits increased to 1.51% and 1.00% from 0.73% as of the same dates. The Bank’s delinquent loansas reported to the Financial Services Commission, which represent loans whose principals are past due forone day or more, increased to W1,608 billion as of March 31, 2009 and W1,172 billion as of December 31,2008, from W790 billion as of December 31, 2007, while its delinquency ratio increased to 1.12% and0.79% from 0.62% as of the same dates, respectively. Such increases were largely due to the deterioratingasset quality of the Bank’s loans to small- and medium-sized enterprises, which amounted to W62,144billion as of March 31, 2009 and W61,813 billion as of December 31, 2008, compared to W53,512 billionas of December 31, 2007. The delinquency ratio for such loans increased to 1.98% and 1.33% from 0.85%as of the same dates. The asset quality of the Bank’s loans, particularly the loans to small- and medium-sized enterprises, may further deteriorate, especially if the current economic and financial conditions inglobal and Korean markets continue to worsen, which would have a material adverse effect on its business,financial condition and results of operation.

The disruptions and volatility in the global and Korean financial markets and economies may also adverselyaffect the Bank’s business and results of operation in other ways. Specifically, the availability of credit maybecome limited, causing some of its counterparties to default. Moreover, negative developments in theglobal credit markets may cause significant fluctuations in stock markets globally and foreign currencyexchange rates, which in turn may affect the Bank results of operation. If credit market conditions continueto deteriorate, the Bank’s capital funding structure may need to be adjusted, its funding costs may increase,its credit rating may be further downgraded, or its loan and other credit losses may increase, all of whichcould have a material adverse effect on its business, financial condition and results of operation.

11

Systemic risk resulting from failures in the financial services industry could adversely affect the Bank.

Within the financial services industry, the default of any institution could lead to defaults by otherinstitutions. Concerns about, or a default by, one institution could lead to significant liquidity problems,losses or defaults by other institutions because the commercial soundness of many financial institutions maybe closely related as a result of their credit, trading, clearing or other relationships. This risk is sometimesreferred to as “systemic risk” and may adversely affect financial intermediaries, such as clearing agencies,clearinghouses, banks, securities firms and exchanges with which the Bank interacts on a daily basis, whichcould have an adverse effect on the Bank’s ability to raise new funding, and in turn, its business, financialcondition and results of operation. Furthermore, the Bank could be perceived to be facing the same issues asother financial institutions that hold assets with limited market liquidity or with significantly depressedvalues due to significantly negative views about the financial services sector in general as a result of recenteconomic and market developments, including the recent failures of major global financial institutions.Such perceptions of the Bank, even if false, could adversely affect its business, financial condition andresults of operation.

Risks Relating to the Bank’s Business

Competition in the Korean financial services industry is intense, and may further intensify as a result ofrecent deregulation.

Competition in the Korean financial services industry is, and is likely to remain, intense. The Bankcompetes principally with other major Korean commercial banks and major global banks operating inKorea, as well as government-run banks, specialized banks and regional banks. Some of the Bank’scompetitors, particularly the major global financial institutions, have greater experience and resources thanit does. As the Korean economy further develops, more competitors may enter the industry. In addition,potential consolidation among the Bank’s rival institutions may make the competitive landscape moreadverse to the Bank.

The Korean financial industry continues to be deregulated, which has lowered the barriers to entry. InFebruary 2009, the Financial Investment Services and Capital Markets Act became effective, which, byremoving regulatory barriers between securities brokerage, asset management, derivative financial servicesand trust services, has enabled financial investment companies (which have replaced the pre-existingsecurities companies and asset management companies) to engage in a broader sphere of financial activitiesthan the securities companies were previously allowed to, as well as offer a wider range of depositaryservices. Accordingly, the new law enables the creation of large financial institutions that can offer bothcommercial and investment banking services modeled after the major global financial institutions based inthe United States and Europe.

If the Bank is unable to compete effectively in this more competitive and deregulated business environment,its profit margin and market share may erode and its further growth opportunities may become limited,which could adversely affect its business, results of operation and financial condition.

The Bank is required to maintain its capital ratios above a minimum required level, and the failure to doso could result in the suspension of some or all of its operations.

The Bank, like other commercial banks in Korea, is required to maintain a minimum Tier I capital adequacyratio of 4.0% and a BIS ratio of 8.0%, each on a consolidated basis. These ratios measure the respectiveregulatory capital as a percentage of risk-weighted assets on a consolidated basis and are determined basedon guidelines of the Financial Services Commission. As of December 31, 2008, the Tier I capital adequacyratio and the BIS ratio of the Bank on a consolidated basis were 9.3% and 13.4%, respectively, and as ofMarch 31, 2009, the Tier I capital adequacy ratio and the BIS ratio of the Bank on a consolidated basis were10.13% and 14.46%, respectively.

The Bank may not be able to continue to satisfy its capital adequacy requirements for a number of reasons,including an increase in risky assets and provisioning expenses; substitution costs related to the disposal ofproblem loans; declines in the value of its securities portfolio; adverse changes in foreign currency

12

exchange rates; changes in the capital ratio requirements, the guidelines regarding the computation ofcapital ratios, or the framework set by the Basel Committee on Banking Supervision upon which theguidelines of the Financial Services Commission are based; or other adverse developments affecting theBank’s asset quality or equity capital as discussed in this section or due to other reasons.

If the Bank’s capital adequacy ratios fall below the required levels, the Financial Services Commission mayimpose penalties ranging from a warning to suspension or revocation of its business licenses. In order tomaintain the capital adequacy ratios above the required levels, the Bank may be required to raise additionalcapital through equity financing or capital injections from Shinhan Financial Group, but there is noassurance that it will be able to do so on commercially favorable terms or at all, or that Shinhan FinancialGroup may provide a capital injection in a sufficient amount or at all.

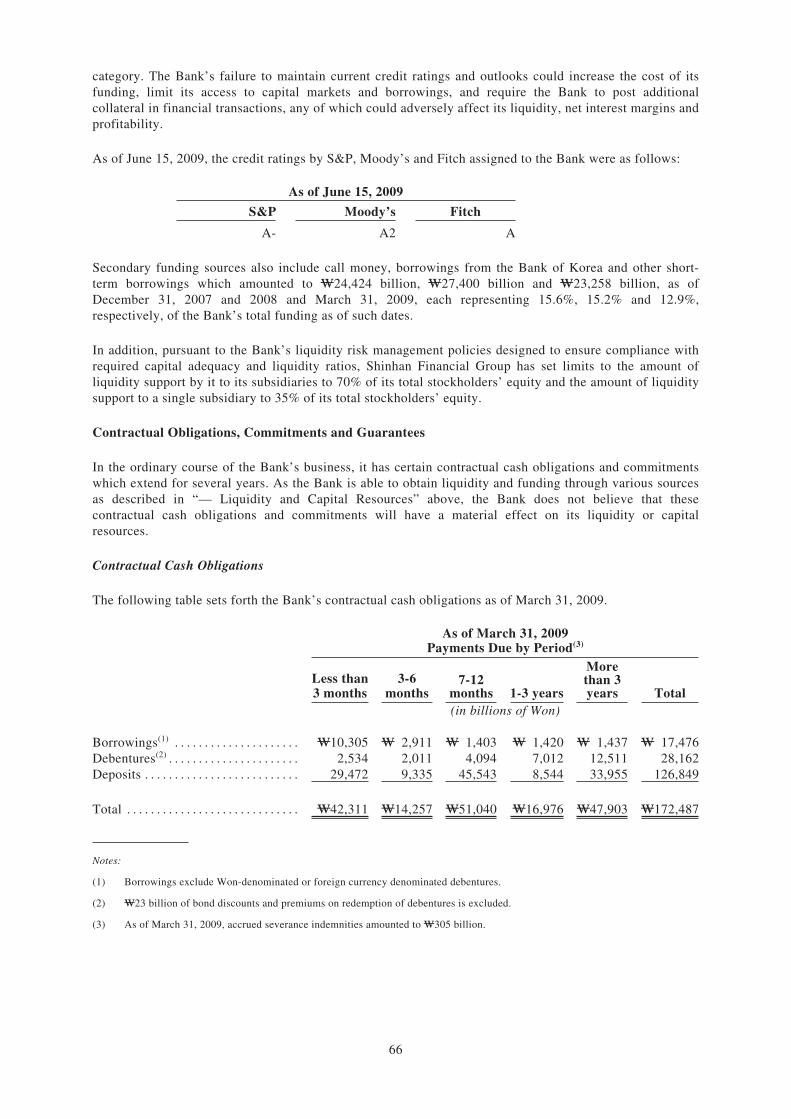

Liquidity, funding management and credit ratings are critical to the Bank’s ongoing performance.

Liquidity is essential to the Bank’s business as a financial intermediary, and the Bank may seek additionalfunding in the near future to satisfy liquidity needs, meet regulatory requirements, enhance its capital levelsor fund the growth of its operations as opportunities arise. A substantial part of the liquidity and fundingrequirements for the Bank is met using short-term customer deposits. While the volume of the Bank’scustomer deposits has generally been stable, there have been times when customer deposits declinedsubstantially due to the popularity of other, higher-yielding investment opportunities, namely stocks andmutual funds. During those times, the Bank was required to obtain alternative funding at higher costs. Inaddition, following the deregulation of depositary and settlement services as a result of the FinancialInvestment Services and Capital Markets Act, the Bank may experience a decrease in customer deposits dueto intensified competition for such deposits. The Bank also raises funds in the capital markets and borrowsfrom other financial institutions, the cost of which depends on the market rates and the general availabilityof credit, the terms of which may limit its ability to make acquisitions or subject itself to other restrictivecovenants. In addition, during times of sudden and significant devaluations of Korean Won against the U.S.dollar as was the case recently amid the global liquidity crisis, Korean commercial banks, including theBank, had difficulties from time to time in refinancing or obtaining optimal amounts of foreign currency-denominated funding on terms commercially acceptable to the Bank. While the Bank currently is not facingliquidity difficulties in any material respect, if the Bank is unable to obtain the funding that it needs onterms commercially acceptable to it for an extended period of time for reasons of Won devaluation orotherwise, it may not be able to ensure its financial viability, meet regulatory requirements, implement itsstrategies or compete effectively.

Credit ratings affect the cost and other terms upon which the Bank is able to obtain funding. Domestic andinternational rating agencies regularly evaluate the Bank, and their ratings of the Bank’s long-term debt arebased on a number of factors, including its financial strength as well as conditions affecting the financialservices industry generally and in Korea. In light of the ongoing difficulties in the financial servicesindustry and the financial markets, there can be no assurance that the rating agencies will maintain theBank’s current ratings or outlooks. For example, in February 2009, Moody’s Investors Service, Inc.(“Moody’s”) downgraded credit ratings on eight banks in Korea, including the Bank, as a result of whichthe Bank’s foreign currency-denominated long-term unsecured senior debt credit rating was downgradedfrom A1 to A2, which is the corresponding credit rating currently assigned to the Government. Other ratingagencies may decide to follow suit or place the Bank in a lower credit rating category. Additionaldowngrades in the credit ratings and outlooks of the Bank will likely increase the cost of its funding, limitits access to capital markets and borrowings, or require it to post additional collateral in financialtransactions, any of which could adversely affect its liquidity, net interest margins and profitability, and inturn, its business, financial condition and results of operation.

Changes in interest rates, foreign exchange rates, bond and equity prices, and other market factors haveaffected and will continue to affect the Bank’s business.

The most significant market risks that the Bank faces are interest rate, foreign exchange and bond andequity price risks. Changes in interest rate levels, yield curves and spreads may affect the interest ratemargin realized between lending and borrowing costs. Changes in currency rates, particularly in the KoreanWon-U.S. dollar exchange rates, affect the value of the Bank’s assets and liabilities denominated in foreign

13

currencies, the reported earnings of the Bank’s non-Korean subsidiaries and income from foreign exchangedealings. The performance of financial markets may affect bond and equity prices and, therefore, causechanges in the value of the Bank’s investment and trading portfolios. While the Bank has implemented riskmanagement methods to mitigate and control these and other market risks to which it is exposed, it isdifficult to predict with accuracy changes in economic or market conditions and to anticipate the effects thatsuch changes could have on the Bank’s business, financial condition and results of operation.

The Bank may incur losses associated with its counterparty exposures.

The Bank faces the risk that counterparties will be unable to honor contractual obligations. These partiesmay default on their obligations to the Bank due to bankruptcy, lack of liquidity, operational failure or otherreasons. This risk may arise, for example, from entering into swaps or other derivative contracts underwhich counterparties have obligations to make payments to the Bank or in executing currency or othertrades that fail to settle at the required time due to non-delivery by the counterparty or systems failure byclearing agents, exchanges, clearinghouses or other financial intermediaries. Counterparty risk hasincreased especially in light of the recent credit crisis and global economic downturn.

The Bank has significant exposure to small- and medium-sized enterprises, and financial difficultiesexperienced by such enterprises may result in a deterioration of its asset quality.

One of the Bank’s core banking businesses has historically been and continues to be lending to small- andmedium-sized enterprises (as defined in “Business — Business Overview — The Bank’s PrincipalActivities — Corporate Banking Services — Small- and Medium-sized Enterprises Banking”). The Bank’sloans to such enterprises increased from W44,330 billion as of December 31, 2006, to W53,512 billion as ofDecember 31, 2007, W61,813 billion as of December 31, 2008 and W62,144 billion as of March 31, 2009,representing 38.8%, 42.0%, 41.8% and 43.4%, respectively, of its total loan portfolio as of such dates.

Compared to loans to large corporations, which tend to be better capitalized and able to weather businessdownturns with greater ease, or loans to individuals and households, which tend to be secured with homesand with respect to which the borrowers are therefore less willing to default, loans to small- and medium-sized enterprises have historically had a relatively higher delinquency ratio. Prior to the onset of the globalfinancial crisis, loans to such enterprises were the targets of aggressive lending by Korean banks, includingthe Bank, as part of their campaigns to increase their respective market shares. As of December 31, 2006,2007 and 2008 and March 31, 2009, the Bank’s delinquent loans to small- and medium-sized enterpriseswere W318 billion, W453 billion, W820 billion and W1,231 billion, respectively, representing delinquencyratios (net of charge-offs and loan sales) of 0.72%, 0.85%, 1.33% and 1.98%, respectively. If the currentbusiness downturn further deepens in terms of length and severity, the delinquency ratio for the Bank’sloans to small- and medium-sized enterprises is likely to rise significantly at least in the near future.

Of particular concern is the significant exposure that the Bank has to small- and medium-sized enterprisesin the real estate and leasing industry and the construction industry. As of March 31, 2009, the Bank’s loansto the real estate and leasing industry and the construction industry was W12,444 billion and W4,349billion, representing 8.68% and 3.04%, respectively, of its total loan portfolio as of such dates with adelinquency ratio (net of charge-offs and loan sales) of 1.50% and 3.88%, respectively. In comparison, as ofDecember 31, 2008, the Bank’s loans to the real estate and leasing industry and the construction industrywas W13,619 billion and W4,266 billion, representing 9.21% and 2.89%, respectively, of its total loanportfolio as of such dates with a delinquency ratio (net of charge-offs and loan sales) of 1.08% and 2.51%,respectively. The small- and medium-sized enterprises in the real estate development and constructionindustries are concentrated in the housing market, which has been particularly affected by declining assetprices as a result of the global credit crisis as well as sustained efforts by the Government to stemspeculation in the housing market. The Bank also has significant exposure to construction companies thathave built residential units in provinces outside the metropolitan Seoul area, which have experienced arelatively low rate of pre-sales, the proceeds from which the construction companies primarily rely on as asource for their liquidity and cash flow. In addition, the Bank also has significant exposure to theshipbuilding industry, which has also been disproportionately hurt by the recent economic downturnfollowing a particularly robust period, largely due to the rapid slowdown in world trade, which hassubstantially diminished shipbuilding orders.

14

The delinquency ratio for small- and medium-sized enterprises in the construction and shipbuildingindustries is also likely to increase significantly if a restructuring program for troubled companies in theseindustries is implemented as currently planned by the government. Specifically, in December 2008, theGovernment announced that it would promote swift restructuring of troubled companies in certain industriesthat have been disproportionately affected by the ongoing economic difficulties, such as construction andshipbuilding industries. These restructurings will be supervised primarily by the major commercial banksthat are creditor financial institutions of such companies, with the Government having an oversight role. InFebruary 2009, 12 construction companies and four shipbuilding companies became subject to workoutfollowing review by their creditor financial institutions and the Government, and the Bank was one of thecreditor financial institutions for 11 construction companies and four shipbuilding companies. The Bank hasestablished an allowance for the loans and off-balance sheet credit instruments for such companiesamounting to W129 billion and W28 billion, respectively, as of December 31, 2008 and W204 billion andW123 billion, respectively, as of March 31, 2009. However, there is no assurance that the Bank’sallowances for such companies will be sufficient to cover all future losses arising from its exposure to suchcompanies.

The Bank is taking active steps to curtail delinquency among its small- and medium-sized enterprisecustomers, including by way of strengthening loan application review processes and closely monitoringborrowers in troubled sectors. Despite such efforts, there is no assurance that the delinquency ratio for theBank’s loans to small- and medium-sized enterprises will not rise in the future. The current adverseeconomic developments, which may deepen in terms of length and severity, are likely to cause deteriorationin the liquidity and cash flow of these enterprises and result in higher delinquency and impairment of loans.Furthermore, adverse structural changes or macroeconomic trends in the Korean economy may further hurtthe ability of such enterprises to generate revenues or service debt. A significant rise in the delinquencyratios among these borrowers would have a material adverse effect on the Bank’s business, financialcondition and results of operation.

A decline in the value of the collateral securing the Bank’s loans or the Bank’s inability to fully realizethe collateral value may adversely affect the Bank’s credit portfolio.