Embed Size (px)

Citation preview

Sheffield and Leeds City Regions:

Post-HS2 Timetable Option Study

Technical Report

Report

July 2013

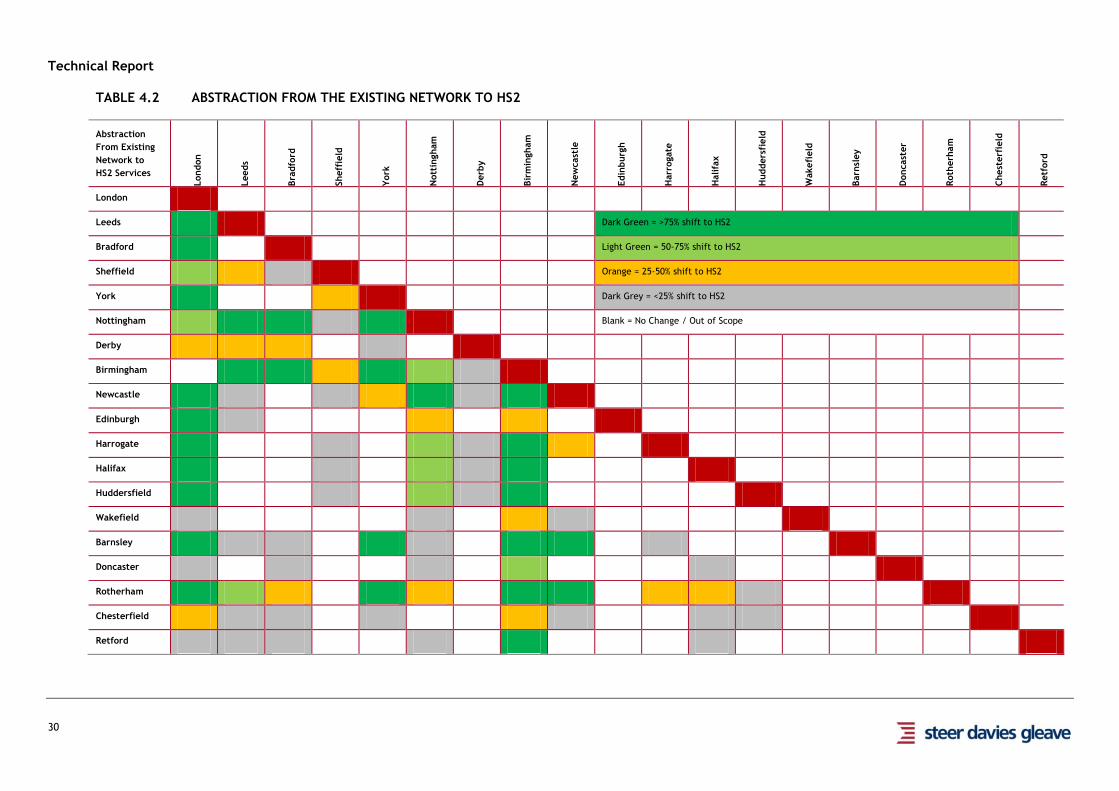

Prepared for: Prepared by:

SYPTE and Metro

Steer Davies Gleave

West Riding House

67 Albion Street

Leeds LS1 5AA

+44 (0)113 389 6400

www.steerdaviesgleave.com

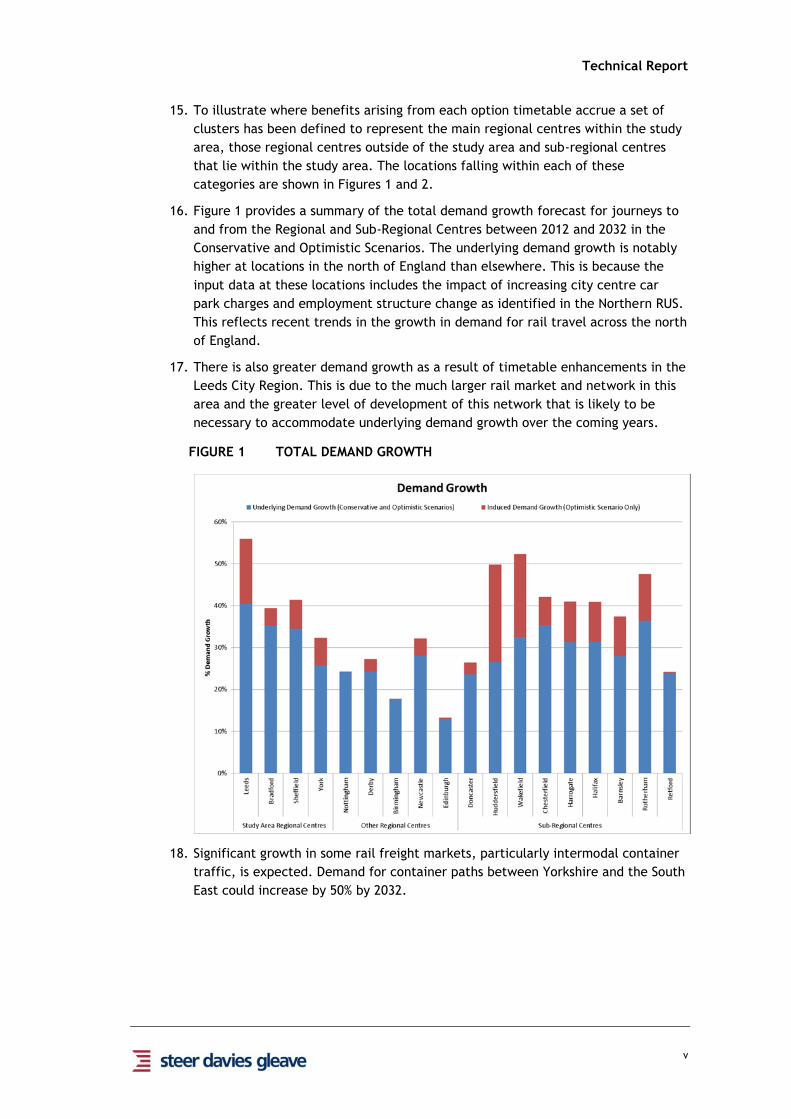

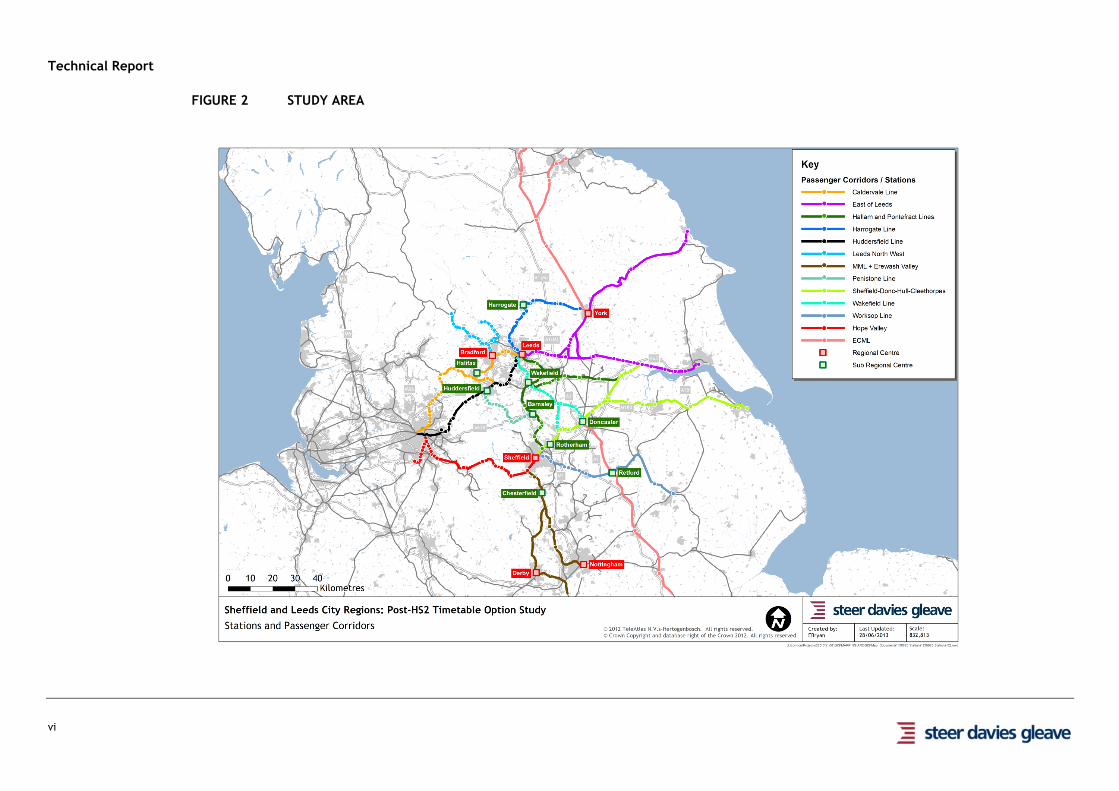

Technical Report

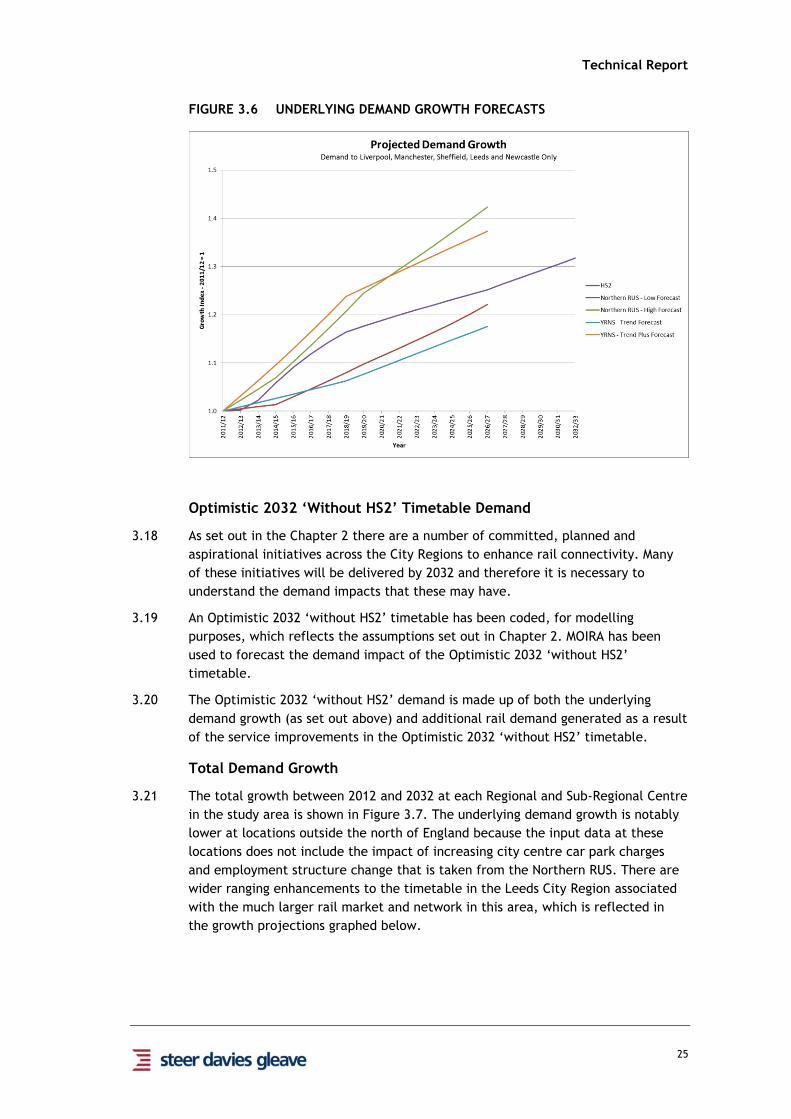

Contents

CONTENTS

EXECUTIVE SUMMARY ...................................................................................... I

Key Messages .......................................................................................... i

Introduction .......................................................................................... ii

Strategic Context and Guiding Principles ....................................................... iii

Demand Growth to 2032 ........................................................................... iv

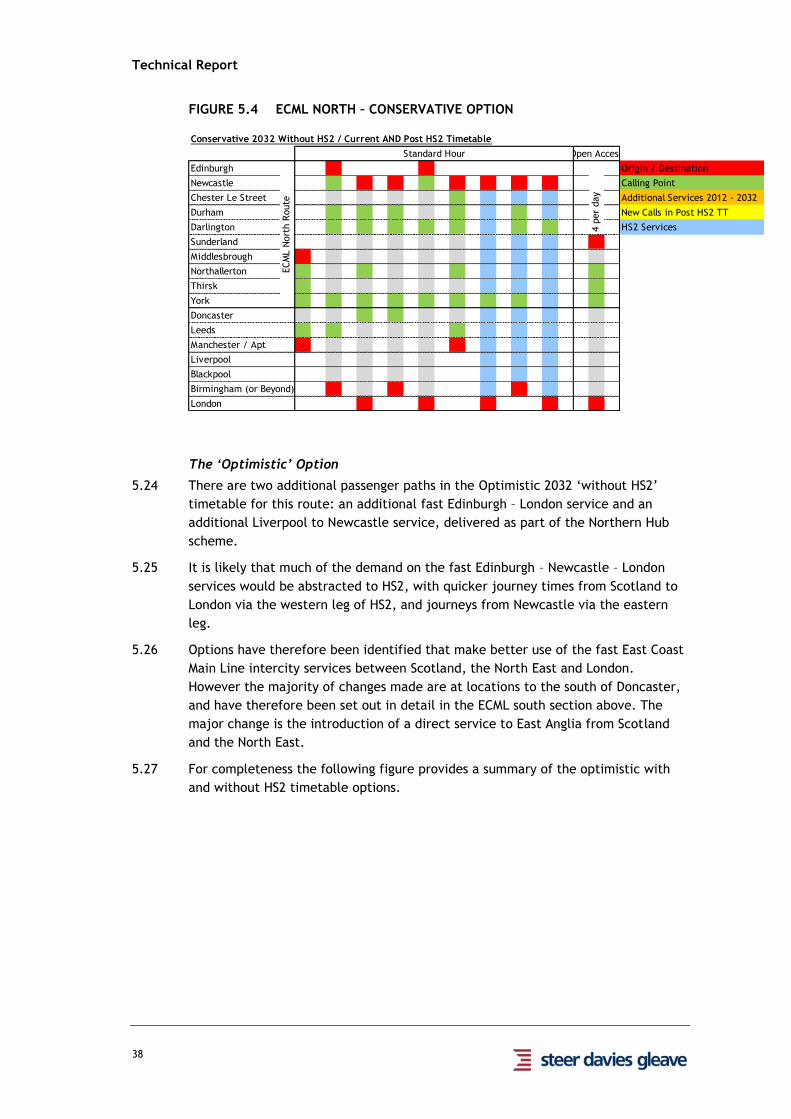

Impact of HS2 ....................................................................................... vii

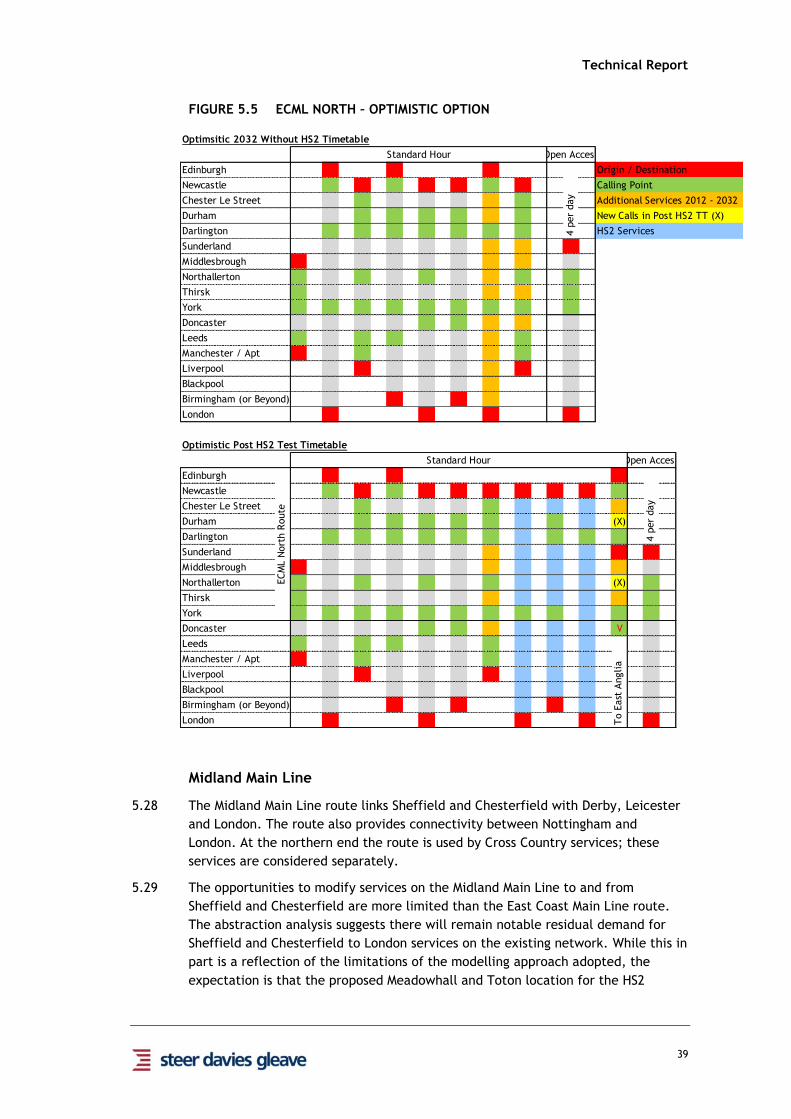

Developing a Post-HS2 Timetable .............................................................. viii

Distribution of the Economic Benefits........................................................... ix

Conclusions ............................................................................................ x

Next Steps ............................................................................................ xi

1 INTRODUCTION ..................................................................................... 1

Study Context ......................................................................................... 1

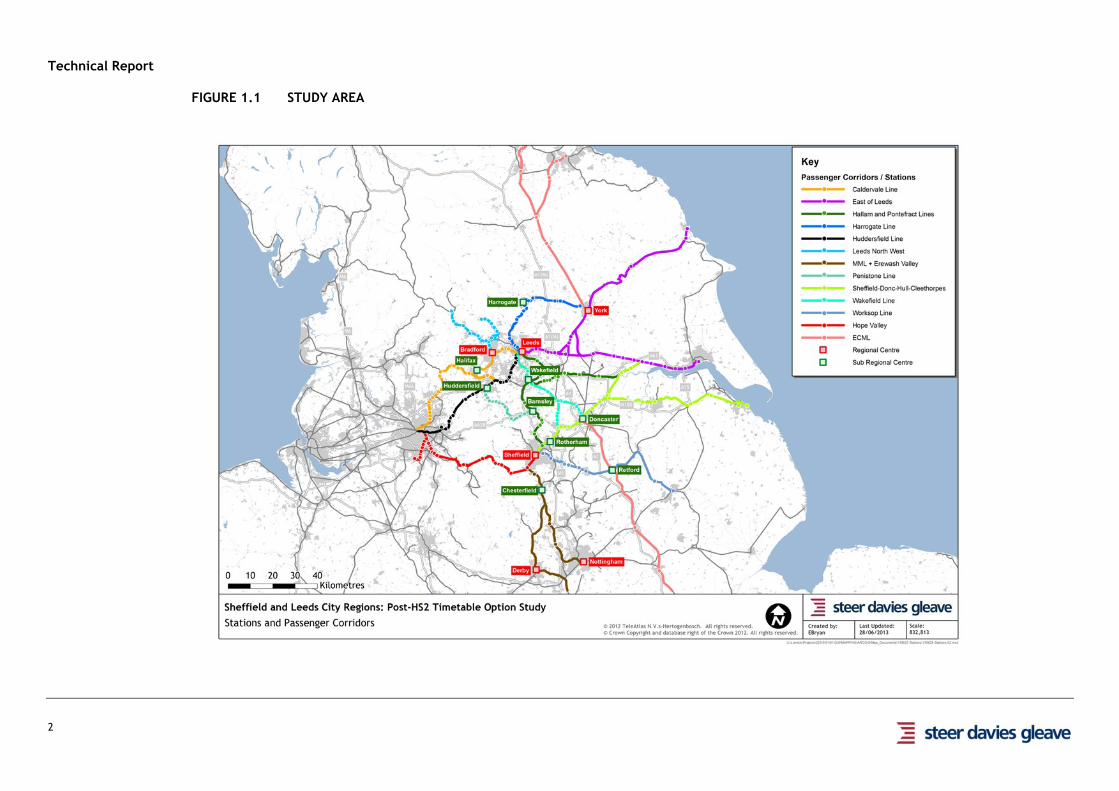

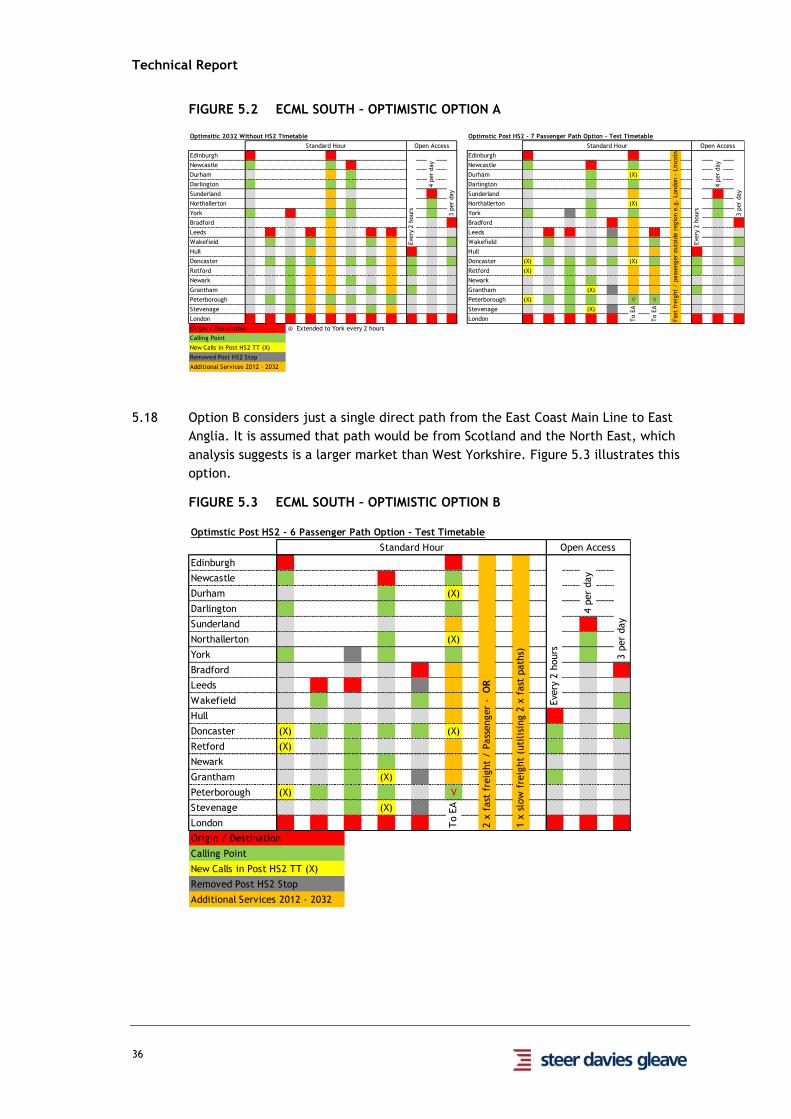

Study Area ............................................................................................. 1

Study Approach ....................................................................................... 3

Caveats ................................................................................................ 5

Report Structure ..................................................................................... 5

2 STRATEGIC CONTEXT AND GUIDING PRINCIPLES ............................................. 7

Introduction ........................................................................................... 7

Rail Strategies Covering the Sheffield and Leeds City Regions .............................. 7

Network Rail’s Long Term Planning Process .................................................. 14

Assumed Enhancements in the Optimistic 2032 ‘Without HS2’ Timetable .............. 16

‘Guiding Principles’ Underpinning Development of Post-HS2 Scenarios ................. 17

3 ESTABLISHING THE 2032 ‘WITHOUT HS2’ DEMAND ........................................ 19

Introduction ......................................................................................... 19

Underlying Passenger Demand Growth ......................................................... 19

Optimistic 2032 ‘Without HS2’ Timetable Demand .......................................... 25

Total Demand Growth ............................................................................. 25

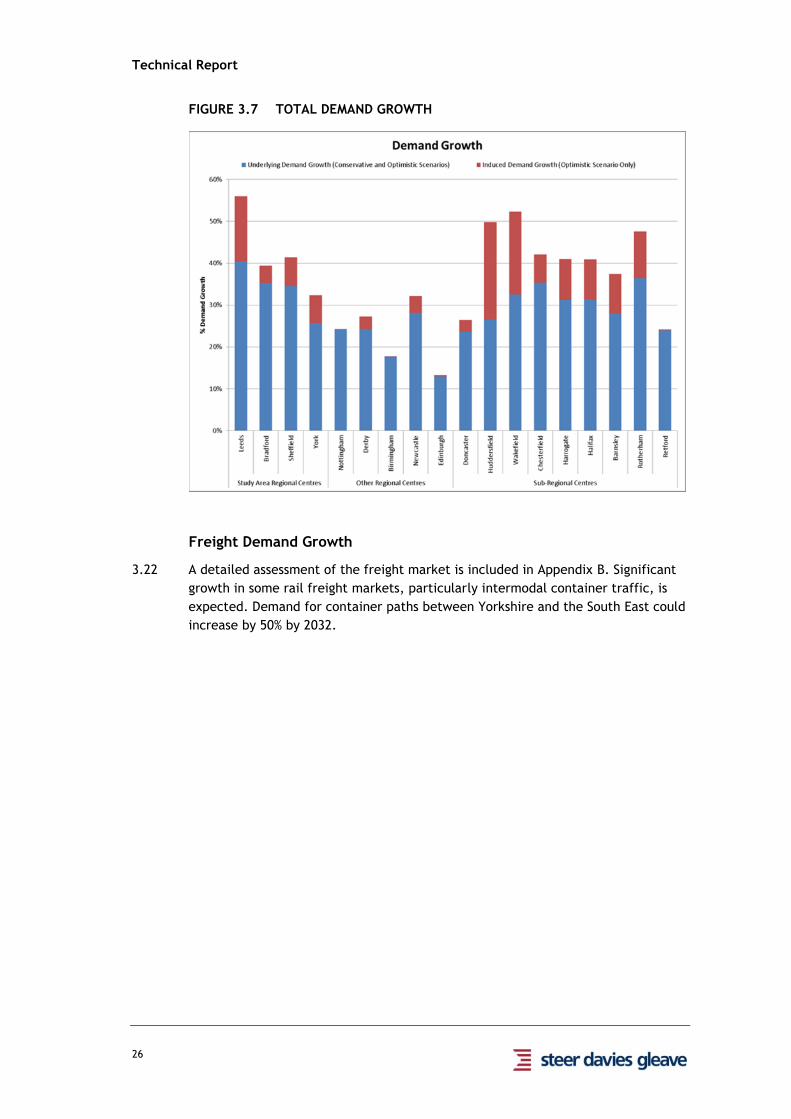

Freight Demand Growth .......................................................................... 26

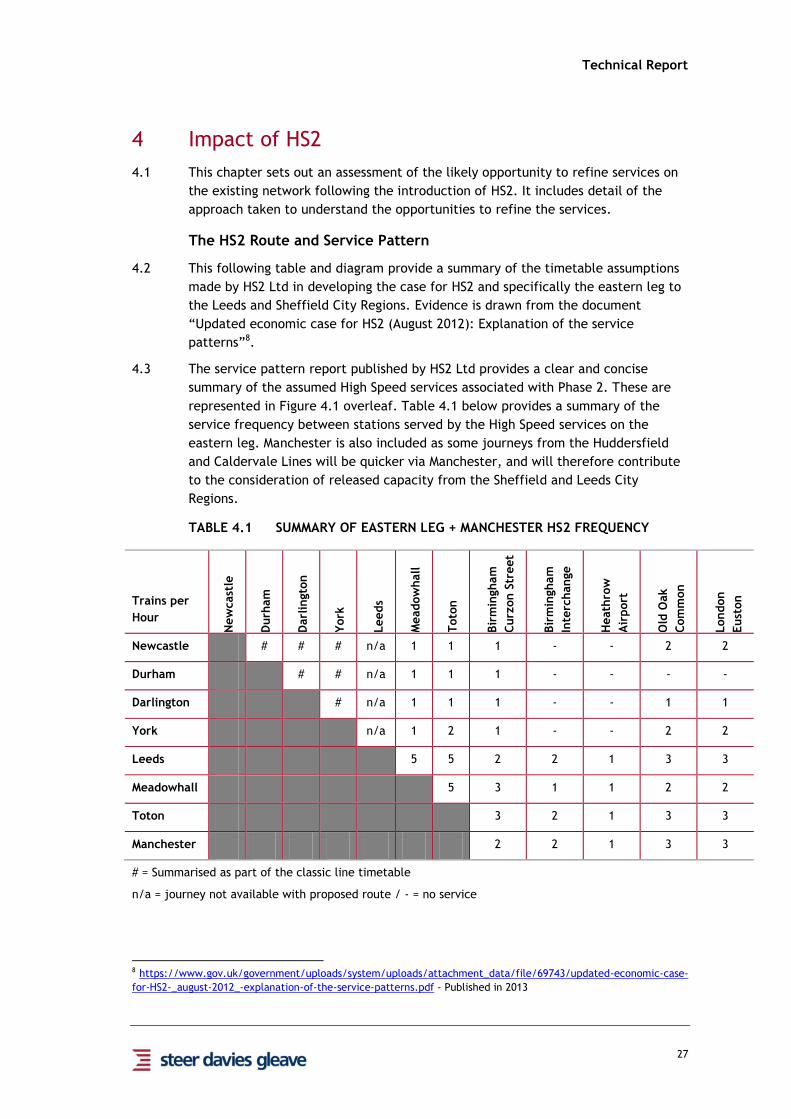

4 IMPACT OF HS2 .................................................................................... 27

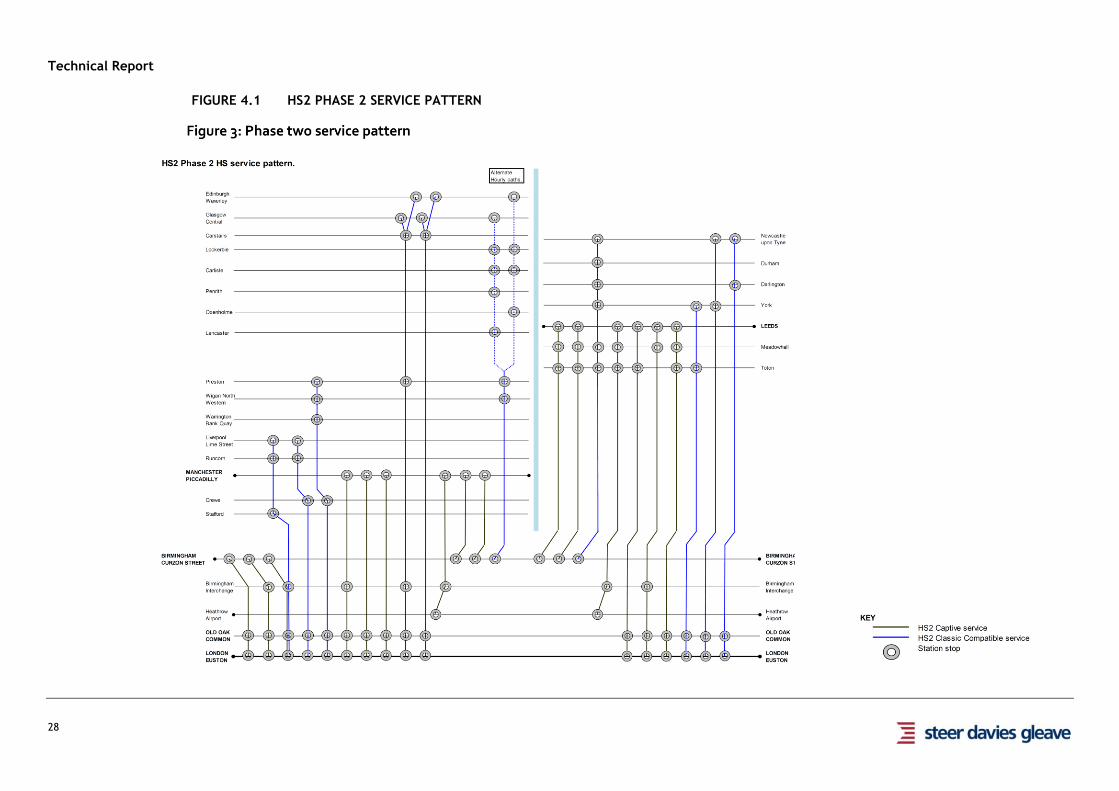

The HS2 Route and Service Pattern ............................................................. 27

Approach to Assessing the Released Capacity Opportunities .............................. 29

5 OPTIONS FOR A POST-HS2 TIMETABLE ....................................................... 33

Contents

Introduction ......................................................................................... 33

East Coast Main Line – south of Doncaster ..................................................... 34

East Coast Main Line - north of York ........................................................... 37

Midland Main Line .................................................................................. 39

Cross Country ....................................................................................... 40

Feeder Services..................................................................................... 43

6 ECONOMIC IMPACT ASSESSMENT ............................................................... 45

Introduction ......................................................................................... 45

Calculating Economic Impact .................................................................... 45

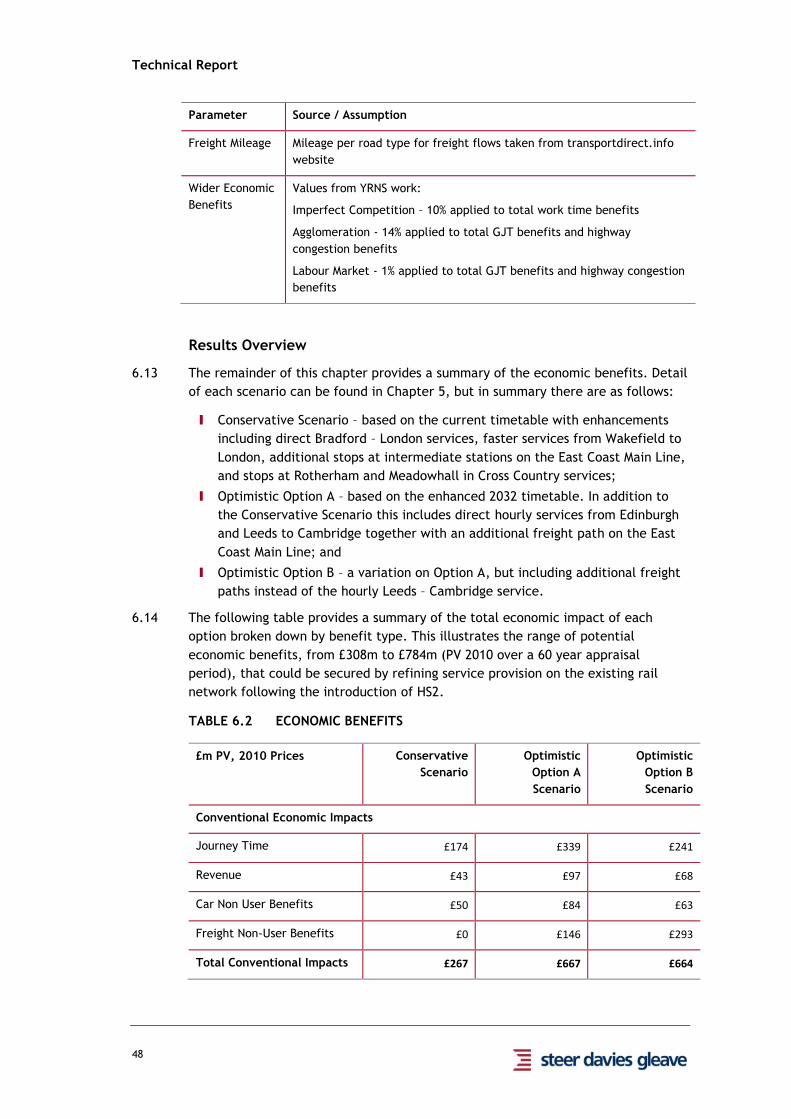

Results Overview ................................................................................... 48

7 CONCLUSIONS AND NEXT STEPS ................................................................ 53

Conclusions .......................................................................................... 53

Next Steps ........................................................................................... 53

FIGURES

Figure 1 Total Demand Growth ....................................................... v

Figure 2 Study Area .................................................................... vi

Figure 1.1 Study Area ..................................................................... 2

Figure 3.1 GVA Per Capita Growth ................................................... 22

Figure 3.2 Employment Growth ....................................................... 22

Figure 3.3 Population Growth ......................................................... 23

Figure 3.4 Households With No Car Growth ......................................... 23

Figure 3.5 Fuel Cost Growth ........................................................... 24

Figure 3.6 Underlying Demand Growth Forecasts .................................. 25

Figure 3.7 Total Demand Growth ..................................................... 26

Figure 4.1 HS2 Phase 2 Service Pattern .............................................. 28

Figure 5.1 ECML South – Conservative Option ...................................... 34

Figure 5.2 ECML South – Optimistic Option A ....................................... 36

Figure 5.3 ECML South – Optimistic Option B ....................................... 36

Figure 5.4 ECML North – Conservative Option ...................................... 38

Figure 5.5 ECML North – Optimistic Option ......................................... 39

Figure 5.6 Midland Main Line – Conservative and Optimistic Base Timetable 40

Figure 5.7 Cross Country – Conservative Option .................................... 41

Figure 5.8 Cross Country – Optimistic Option ....................................... 43

Technical Report

Contents

Figure 6.1 Benefit by Flow (Excluding Freight) ..................................... 50

Figure 6.2 Benefit by Regional and Sub Regional Centre (Excluding Freight). 51

Figure A.1 Freight Corridors ........................................................... 66

TABLES

Table 1.1 Option Terminology .......................................................... 4

Table 3.1 RIFF-Lite Model Inputs ..................................................... 20

Table 4.1 Summary of Eastern Leg + Manchester HS2 Frequency .............. 27

Table 4.2 Abstraction from the Existing Network to HS2 ........................ 30

Table 6.1 Economic Benefit Appraisal Assumptions .............................. 47

Table 6.2 Economic Benefits .......................................................... 48

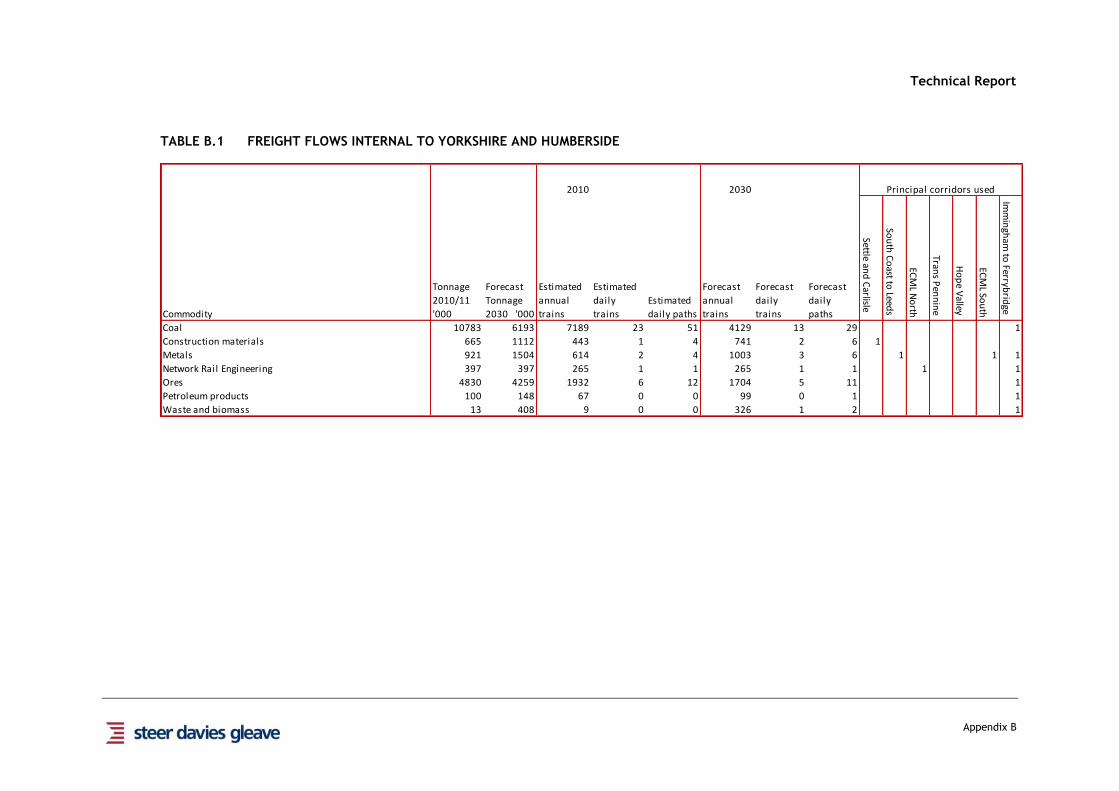

Table B.1 Freight Flows Internal to Yorkshire and Humberside ................ 69

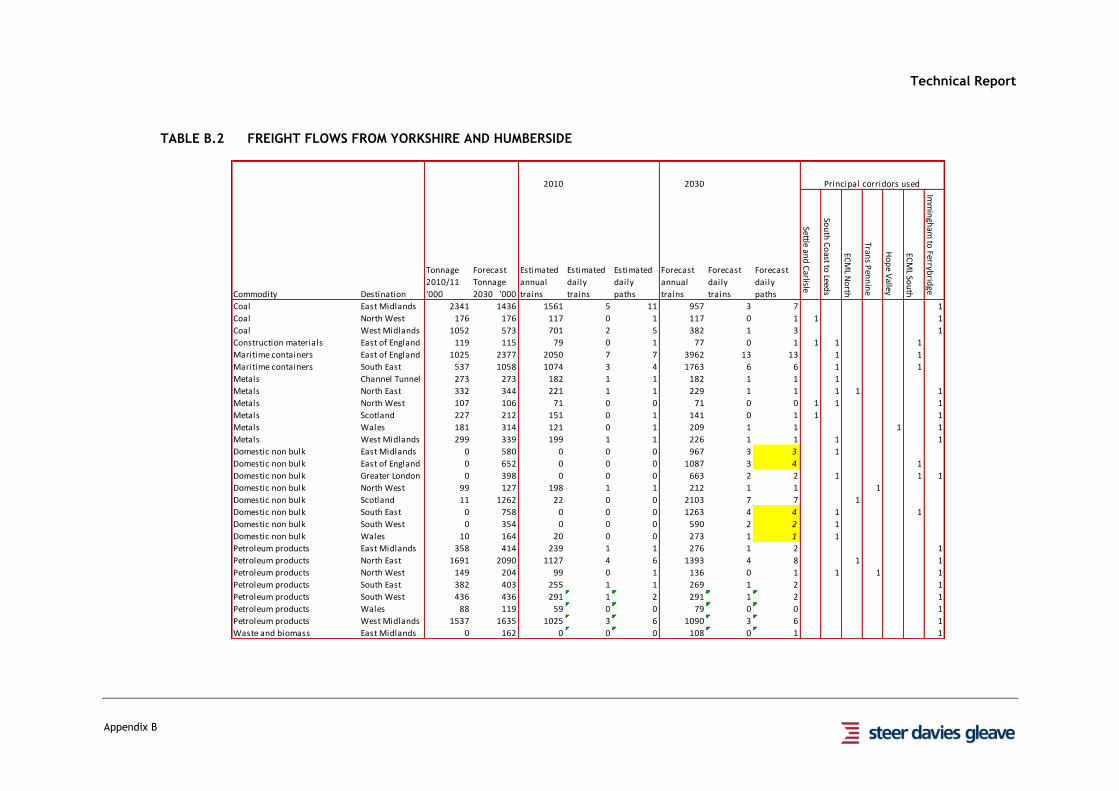

Table B.2 Freight flows From Yorkshire and Humberside ........................ 70

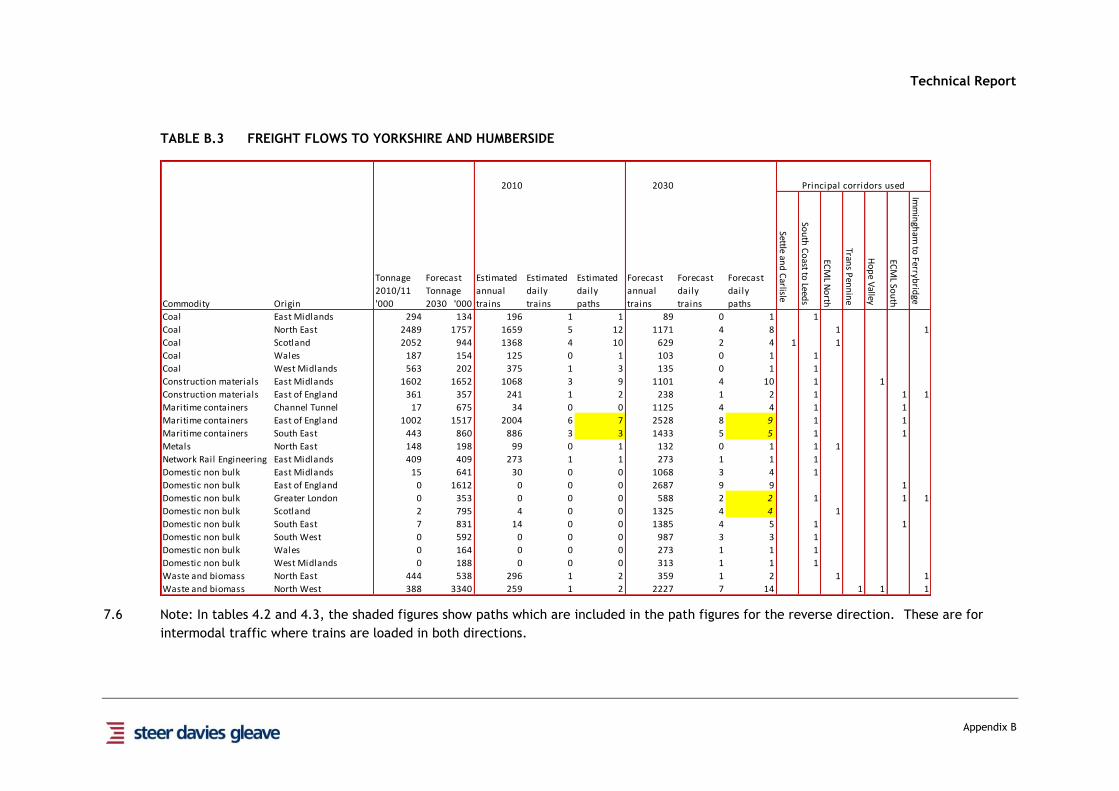

Table B.3 Freight flows To Yorkshire and Humberside ........................... 71

Table B.4 Freight flows Through Yorkshire and Humberside .................... 72

Table B.5 Summary of Forecast Path Requirements (Northern RUS) .......... 73

APPENDICES

A OPTIMISTIC 2032 ‘WITHOUT HS2’ TIMETABLE ASSUMPTIONS

B FREIGHT MARKET ASSESSMENT

Technical Report

i

Executive Summary

Key Messages

The Government is planning to build a national high speed rail network, known as High

Speed 2 (HS2). This will significantly reduce rail journey times from London and Birmingham

to Leeds, Sheffield and York and also provide an opportunity to modify service provision on

the existing rail network.

To support development of the business case, HS2 Ltd has made initial assumptions as to

how services on the existing network could be modified following the introduction of HS2.

These include reducing some service frequencies and re-routeing some services in ways that

may worsen connectivity to and from locations in the Sheffield and Leeds City Regions (SCR

and LCR). This study has considered an alternative approach to modifying services on the

existing network that has the potential to:

I Generate economic benefits of between £300m and £800m (2010 present value); and

I Provide benefits that are distributed across the SCR and LCR areas.

These benefits relate solely to enhanced passenger and freight connectivity on the existing

network following the introduction of HS2. They are additional to the direct benefits

generated by HS2 itself. The benefits could be secured largely through refining how services

on the existing network operate and making use of available capacity. They could therefore

be realised with minimal additional operating and capital cost.

The study has identified indicative timetable scenarios and used these to value an envelope

of potential benefits. There is scope to refine and develop these scenarios to allow overall

benefits to be maximised and the distribution of benefits for SCR and LCR to be improved.

Further development will need to reflect stakeholder aspirations and the on-going

development of the existing rail network and HS2. Investment in the existing network

beyond 2019 should be targeted to ensure the infrastructure required to realise the wider

opportunities that HS2 brings is in place in advance of 2032.

As currently proposed, HS2 infrastructure in Yorkshire will be lightly used compared to the

capacity that will be available on the high speed network. Existing parallel routes will be

operating at or close to capacity. Consideration should be given to making better use of the

HS2 infrastructure.

The study suggests there are worthwhile economic benefits to be gained as a result of

providing enhanced passenger and freight services on the existing network post-HS2. Given

this opportunity the following actions for stakeholders are suggested:

I Respond positively to the consultation on the wider HS2 propositions;

I Engage with HS2 Ltd/Network Rail to consider alternative options for use of the existing

network to those currently included by HS2 Ltd in the economic case;

I In due course, undertake further work to refine the post-HS2 timetable options as more

detail on the development of the existing and HS2 networks becomes available; and

I Make the case for an “existing network investment funding pot – post-HS2” for 2019 and

beyond, geared at ensuring maximum benefits can be derived from the existing network.

Technical Report

ii

Introduction

1. The Government is planning to build a national high speed rail network. This will

significantly reduce rail journey times from London and Birmingham to Leeds,

Sheffield and York. It will also significantly increase passenger capacity for these

intercity flows. It will have a dramatic impact on rail travel. The direct benefits

of significantly quicker journey times are self-evident for point-to-point flows

from York, Leeds and Sheffield (Meadowhall) to London and Birmingham. What is

less clear at present are the opportunities that the introduction of High Speed 2

(HS2) might offer to improve services on the existing network.

2. This study considers the opportunities to enhance services on the existing rail

network following the introduction of HS2, and makes an initial valuation of the

potential economic benefits. The study covers:

I The potential impact of HS2 on demand for services on the existing network;

I How service provision on the existing network might be refined in order to

serve the residual markets following the start of HS2 services; and

I An initial estimate of the potential economic benefits such refinements might

generate.

3. A range of possible economic benefits have been identified reflecting

Conservative and Optimistic Scenarios. Assuming there is no development of the

rail network between now and 2032, the analysis suggests that economic benefits

of £300m could be secured by revising the service pattern on the existing

network.

4. However, this could increase to £800m should government policy favour on-going

investment in rail network capability up to 2032. The additional benefit is created

as a result of greater underlying rail demand generated by the enhanced 2032

timetable, more opportunities to enhance the service pattern post-HS2 including

providing new direct journey opportunities, and the opportunity to accommodate

additional freight traffic.

5. While the volume of this potential benefit equates to a small proportion of the

total benefit of HS2, £63.6bn1 for the full network and £40bn2 for the Leeds and

Manchester legs, it does reflect a much larger volume of benefit for the regions

specifically. Further it is likely that a significant proportion of the benefits could

be delivered with relatively small levels of additional infrastructure and operating

costs being incurred.

6. The remainder of this Study Overview provides a summary of the work programme

that has been followed to identify the post-HS2 service options and the potential

economic benefits that these may generate. It is structured as follows:

I Summarises the strategic context and guiding principles;

I Comments on how rail demand is projected to grow between now and 2032;

I Presents an overview of an initial assessment of demand that HS2 might

abstract from the existing rail network;

1 Updated Economic Case for HS2, HS2 Ltd, August 2012 – Table 1, row 6 -

http://assets.hs2.org.uk/sites/default/files/inserts/Updated%20economic%20case%20for%20HS2.pdf 2 Updated Economic Case for HS2, HS2 Ltd, August 2012 – Table 1, row 6 less Table 2, row 6

Technical Report

iii

I Summarises options for a post-HS2 timetable;

I Provides a summary of how benefits are distributed through the Sheffield and

Leeds City Regions; and

I Presents the key conclusions and next steps.

Strategic Context and Guiding Principles

7. There are a variety of plans and strategies that will influence the development of

rail network capability and rail service outputs between now and 2032, the

proposed opening date for Phase 2 of HS2, and also provide direction as to how

the rail network ought to be developed beyond 2032. These include:

I Network Rail’s Route Utilisation Strategies (RUSs)

I The Northern Hub strategy

I The Department for Transport’s High Level Output Statement and in response

Network Rail’s Strategic Business Plan;

I Plans for electrification, including the Electric Spine, Midland Main Line and

Trans Pennine routes;

I The Yorkshire Rail Network Study;

I West Yorkshire RailPlan 7 and the Sheffield City Region Transport Strategy;

I The draft Long Term Rail Strategy for the North of England; and

I Emerging conclusions from Network Rail’s Long Term Planning Process,

including specifically at this point in time, the Long Distance Market Study.

8. The strategic context is important to this study for two reasons. It helps define

what the service provision and network capability might be in 2032, against which

we can consider the benefits of a refined post-HS2 timetable. It also helps define

the guiding principles that underpin our assumptions of how the post-HS2

timetable might be developed.

Timetable Development to 2032

9. The strategies and plans identified above set out a wide range of planned and

aspirational service enhancements that may be delivered between now and 2032.

These include enhancements that are committed such as the Northern Hub and

aspirations that still require significant development, such as those set out in the

draft Long Term Rail Strategy for the North.

10. The extent to which these are delivered will have a direct impact on the nature

of the residual rail market post-HS2 and the network capability for residual

passenger and freight services. Reflecting the range of possible enhancements

between now and 2032, two scenarios for the ‘without HS2’ existing rail network

in 2032 have been modelled. These scenarios, developed in consultation with

industry partners, reflect the extremities of likely development in the rail

network over the next 20 years. The two 2032 ‘without HS2’ scenarios that have

been modelled are as follows:

Technical Report

iv

I The Conservative Scenario - based on the current (December 2012) timetable.

It is acknowledged that some infrastructure enhancement and additional

rolling stock is committed. However, the resulting service enhancements will

be determined as part of the franchising process and are not currently

confirmed; and

I The Optimistic Scenario – based on planned enhancements and other

aspirations as set out in the informing strategies, plans and industry views. It

considers an optimistic view of likely infrastructure and service

enhancements, including specifically three additional hourly services

throughout the day on the East Coast Main Line to London and an additional

hourly York – Leeds - Birmingham cross country service.

11. It is likely that infrastructure and service enhancement between now and 2032

will lie somewhere between these two scenarios, hence our analysis provides an

‘envelope of opportunity’. The eventual 2032 ‘without HS2’ scenario will need to

be reviewed and defined as the existing network and HS2 proposition is developed

over the coming years.

Guiding Principles

12. The review of the existing strategies and plans provides a clear and consistent

view on rail development affecting the Sheffield and Leeds City Regions. It

identifies that there are material economic benefits to be gained by enhancing

connectivity to, from and within the Sheffield and Leeds City Regions. If benefits

are to be maximised it is therefore essential that any refinement of passenger

services on the existing network serve to enhance this connectivity. Conversely,

there is also a clear guiding principle that the options developed for a post-HS2

timetable on the existing network should not result in an overall worsening in

connectivity compared to the current timetable. It is essential that changes in

passenger use of the network must not preclude freight growth where this is

forecast.

Demand Growth to 2032

13. To support the valuation of potential economic benefits it is necessary to forecast

the level of demand on the existing network by 2032. There are two distinct

elements that make up demand growth to 2032:

I Underlying demand growth - driven by factors external to the rail industry

such as economic, population and employment growth. These assumptions are

included in both the Conservative and Optimistic Scenarios; and

I Induced demand growth – additional rail demand generated as a result of

enhancements to rail services. This only applies in the Optimistic Scenario.

14. The underlying demand growth forecasting has been undertaken using the RIFF-

Lite (Rail Industry Forecasting Framework) model. The additional induced demand

in the Optimistic Scenario has been estimated using MOIRA, the rail industry’s

standard tool for forecasting the impact of timetable changes. Both models adopt

the methodology and parameters set out in the Passenger Demand Forecasting

Handbook (PDFH).

Technical Report

v

15. To illustrate where benefits arising from each option timetable accrue a set of

clusters has been defined to represent the main regional centres within the study

area, those regional centres outside of the study area and sub-regional centres

that lie within the study area. The locations falling within each of these

categories are shown in Figures 1 and 2.

16. Figure 1 provides a summary of the total demand growth forecast for journeys to

and from the Regional and Sub-Regional Centres between 2012 and 2032 in the

Conservative and Optimistic Scenarios. The underlying demand growth is notably

higher at locations in the north of England than elsewhere. This is because the

input data at these locations includes the impact of increasing city centre car

park charges and employment structure change as identified in the Northern RUS.

This reflects recent trends in the growth in demand for rail travel across the north

of England.

17. There is also greater demand growth as a result of timetable enhancements in the

Leeds City Region. This is due to the much larger rail market and network in this

area and the greater level of development of this network that is likely to be

necessary to accommodate underlying demand growth over the coming years.

FIGURE 1 TOTAL DEMAND GROWTH

18. Significant growth in some rail freight markets, particularly intermodal container

traffic, is expected. Demand for container paths between Yorkshire and the South

East could increase by 50% by 2032.

Technical Report

vi

FIGURE 2 STUDY AREA

Technical Report

vii

Impact of HS2

19. The study has undertaken analysis to understand the impact of HS2 on demand on

the existing rail network. This analysis uses MOIRA to compare the Conservative

and Optimistic Scenarios with and without the HS2 service specification, as set

out in HS2 Ltd’s document “Updated Economic Case for HS2 (August 2012):

Explanation of the Service Patterns”. This allows analysis of the demand using HS2

services and the existing rail network on a flow by flow basis.

20. The modelling shows that the flows where HS2 will abstract most demand is, as

expected, those directly served by HS2 (i.e. from York, Leeds and Sheffield to

London and Birmingham) and from the Regional and Sub-Regional Centres that

already use these hub stations as an interchange point for journeys to London and

Birmingham, e.g. Bradford and Barnsley.

21. An important finding, however, is that there will remain a large residual market

on the existing network for inter and intra-regional flows between locations not

directly served by HS2. The analysis suggests that journeys from Leeds to

Sheffield city centre, Wakefield to York/Sheffield and Chesterfield to

Nottingham/Derby/Sheffield will be relatively unaffected by the introduction of

HS2. There will also remain a market for longer distance inter-regional flows such

as Leeds to Peterborough and Sheffield to Leicester.

22. Consideration has been given to options to refine services to, from or within the

Sheffield and Leeds City Regions. This suggests that the opportunity to remove

services, and therefore release capacity on the existing network, would appear

quite limited. The extent to which the existing rail network no longer needs to

provide services is limited to services between Leeds, York, Sheffield and

London/Birmingham. This, however, is challenging because in most cases services

on these routes also provide connectivity from other Centres in the City Regions.

For example:

I All services from Leeds to London stop at Wakefield and most also call at

Doncaster;

I Some services from York to London also serve Doncaster;

I Cross Country services from York and the North East to and beyond

Birmingham also serve Chesterfield and Wakefield or Doncaster.

23. The analytical work suggests that HS2 will not be the preferred route for those

travelling from Wakefield, Doncaster and Chesterfield to Birmingham and London.

This is because the additional time taken to access and interchange at a High

Speed station is likely to offset the journey time saving compared to the direct

services that are available in the 2032 ‘without HS2’ timetable. However, it is

acknowledged that rail heading may distort this conclusion and that a proportion

of passengers who currently use stations such as Wakefield to access London-

bound trains may well switch to a HS2 station. For this analysis, no fare

differential between classic line and HS2 services is assumed.

24. The conclusion from this part of the study is that opportunities to maximise the

benefits from the existing rail network needs to focus on refining services on the

existing network, rather than through wholesale removal of service patterns and

replacement with different services.

Technical Report

viii

Developing a Post-HS2 Timetable

25. We have adopted the overarching principle that overall connectivity should not be

materially worsened as a result of changes to the existing rail network following

the introduction of HS2.

26. In following the principle that existing network services should not be withdrawn

if this leads to poorer connectivity, it might be observed that the current services

from London to Wakefield and Chesterfield ought to be retained but need not

serve Leeds and Sheffield respectively. Similarly the Cross Country services should

be retained, but would not need to provide today’s connectivity from Leeds and

York to Birmingham. This, however, poses a particular challenge in that these

services also provide connections from Leeds, Sheffield and York to important

intermediate destinations such as Wakefield and Doncaster, and locations outside

the Regions, such as Peterborough, Stevenage, Derby, Tamworth and Darlington.

27. This analysis indicates that the opportunity and scope to remove services from the

existing network is limited. Instead it is likely that the timetable on the existing

rail network would need to be refined through smaller incremental amendments

to specific services rather than wholesale removal and replacement of services.

28. Reflecting these considerations, ‘post-HS2’ timetable options for the existing

network have been developed for both the Conservative and Optimistic Scenarios.

The key features of these timetable options are summarised below.

29. Currently a primary role of the East Coast Main Line is to provide fast connectivity

to London from Edinburgh, Newcastle, York and Leeds. Post 2032 such services

would not need to be provided in the same way as they would pre-HS2, since

these flows would be catered for by services that use HS2 in full or in part. For

the purpose of this assessment it has been assumed in the Conservative and

Optimistic Scenarios that these fast London paths could be used to:

I Provide a direct hourly fast Bradford to London service;

I Maintain connectivity between Leeds and intermediate stations to London;

I Retain a half hourly Wakefield Westgate - London services with journey times

faster than today;

I Provide more frequent and quicker journeys from Doncaster to London than

today; and

I Enhance connectivity from Retford and Doncaster to intermediate stations on

the East Coast Main Line including direct services to Newcastle and Edinburgh.

30. The higher capacity on the existing network assumed in the Optimistic Scenario

would enable additional opportunities for the East Coast Main Line. This

additional capacity could be used to provide a combination of direct services from

the Leeds and Sheffield City Regions (and the North East/Scotland) to East Anglia.

It would also offer additional capacity for additional freight services. Two

Optimistic Scenarios are assumed, summarised as follows:

I Option A – An hourly Edinburgh to Cambridge and Leeds to Cambridge service

together with thee freight paths per day between the South East and West

Yorkshire; and

Technical Report

ix

I Option B – An hourly Edinburgh to Cambridge service together with six freight

paths per day between the South East and West Yorkshire.

31. There are more limited opportunities to refine timetables on the Midland Main

Line and Cross Country routes. This is simply because HS2 will abstract a lower

proportion of overall demand on these two routes. The timetable option includes

additional stops in Cross Country services:

I At Rotherham in services via Leeds – to provide enhanced inter-regional

connectivity including fast services to Leeds; and

I At Meadowhall in services via Doncaster - to provide enhanced inter-regional

connectivity from the park and ride site at Meadowhall.

32. In the Optimistic timetable scenario it is assumed that there is an additional Cross

Country type service via Leeds that would provide Rotherham with a half hourly

fast service to Leeds and other regional and sub-regional centres on the route.

33. The timetable options identified are used purely to underpin the modelling work.

They are designed to allow a reasonable estimation of the likely economic

benefits of a post-HS2 timetable option. The test timetable does not represent

any firm commitment to change services in a specific manner. Significant

timetable development will need to be undertaken before a firm post-HS2

timetable could be ascertained, which is outside the scope of this study.

Distribution of the Economic Benefits

34. An important conclusion from this study is that there is potential for the benefits

of a refined post-2032 timetable to be distributed across the City Regions and not

focussed solely on the major regional centres that directly benefit from HS2. The

following points summarise the key observations from the analysis that has been

undertaken:

I Wakefield benefits in the Conservative Scenario from quicker journeys to

London, while retaining the current two train per hour frequency. In the

Optimistic Scenario 2032 pre-HS2 timetable it is assumed that there would be

three trains per hour from Wakefield to London. In the assumed post-HS2

timetable this reduces to two trains per hour to London, which results in a

disbenefit when compared to the 2032 pre-HS2 optimistic timetable, even

though in the case of Wakefield, the service offer for journeys to London in

the Optimistic timetable is an improvement on the current service provision.

I Bradford, Doncaster and Retford benefit as a result of quicker connections to

London via the existing network. In the case of Bradford this is a result of an

hourly direct service to London. Doncaster and Retford also benefit from

improved direct connectivity to the North East and Scotland.

I York benefits from improved connectivity to intermediate locations on the

East Coast Main Line in the Conservative Scenario. The benefits are enhanced

in the Optimistic Scenario as this also includes direct connectivity to East

Anglia.

I Rotherham benefits as a result of the direct fast services to Leeds and longer

distance connectivity to the North East and South West, as well as a more

frequent heavy rail connection to Meadowhall and Sheffield.

Technical Report

x

I Leeds sees a disbenefit because of slower services to intermediate locations

on the East Coast Main Line. However in Optimistic Option A this is

outweighed by the benefit of a direct service to East Anglia. While there are

disbenefit at Leeds as a result of service changes on the existing network

these, will be relatively minor compared to the benefits of High Speed 2

itself.

I London sees a large disbenefit in the Optimistic Scenarios as these include

paths from Yorkshire and the North East being used for passenger services to

East Anglia and/or freight rather than passenger services to London. However

the disbenefit on flows to and from London is offset by the benefit at

intermediate stations on the East Coast Main Line, and is small in context of

the wider benefits of HS2.

I Other centres in the City Regions will see marginal impacts as a result of

changes on the existing network. Outside the City Regions, Newcastle and

Edinburgh benefit as a result of enhanced connections to intermediate

stations on the East Coast Main Line, and in the case of the Optimistic

Scenarios, to East Anglia too.

35. What is clear from the analysis is that the volume and location of economic

benefits will be sensitive to development of the existing rail network over the

coming years and the assumed use of the network following the introduction of

HS2 services. Development of the existing network will need to be undertaken in

cognisance with the development of HS2 and the post-HS2 timetable proposition

for the existing network will need to be carefully developed to maximise the

potential benefits to as many locations as possible.

Conclusions

36. The analysis suggests that significant economic benefits could be generated by

refining timetables on the existing rail network following the introduction of HS2.

These timetable refinements could bring important local benefits to the Sheffield

and Leeds City Regions and, because the timetable scenarios primarily revise

likely pre-HS2 services patterns, could be achieved at relatively low cost. Further

efficiencies and cost savings may also be possible, for example alternative train

configurations or fuel costs.

37. In general, the locations that benefit are the Regional and Sub-Regional Centres,

including Bradford, York, Wakefield, Doncaster, Rotherham and Retford. In the

case of Wakefield, there are potential benefits compared to the current service,

but the analysis reaffirms the importance of maintaining direct connections to

London. This is because Wakefield sees a net economic disbenefit in the modelled

scenario where services on the East Coast Main Line operate to East Anglia rather

than London.

38. HS2 is a high capacity railway and there may be opportunity for classic services to

make use of the HS2 infrastructure to improve connectivity and generate

economic benefit

39. High level analysis that has demonstrated the scope for released capacity

afforded by the introduction of HS2 to be used to refine existing service patterns

and define new services to create economic benefit.

Technical Report

xi

Next Steps

40. The study suggests that there are worthwhile economic benefits to be realised

from refining the services on the existing network to, from and within the

Sheffield and Leeds City Regions following the introduction of HS2. It is

recommended that the City Regions and other interested stakeholders work to

realise these benefits by:

I Respond positively to the forthcoming consultation on the wider HS2

propositions for the Phase 2 route to Yorkshire;

I Engage with HS2 Ltd/Network Rail to consider alternative options for use of

the existing network to those currently included by HS2 Ltd in the economic

case for HS2, since an alternative option may generate a greater level of

benefits for the Sheffield and Leeds City Regions;

I In due course, undertake further work to refine the post-HS2 timetable

options as more detail on the development of the existing and HS2 networks

becomes available; and

I Stakeholders should make the case for development of a “existing network

investment pot post-HS2” for 2019 and beyond, geared at ensuring maximum

benefits can be derived from the existing network post-HS2.

Technical Report

1

1 Introduction

Study Context

1.1 The government is planning to build a national high speed rail network. This will

significantly reduce rail journey times from London and Birmingham to Leeds,

Sheffield and York. It will also significantly increase passenger capacity for these

intercity flows. It will have a dramatic impact on rail travel. The direct benefits of

significantly quicker journey times are self-evident for point-to-point flows from

York, Leeds and Sheffield (Meadowhall) to London and Birmingham. What is less

clear at present are the opportunities that the introduction of High Speed 2 (HS2)

might offer to improve services on the existing network.

1.2 HS2 Ltd has made initial assumptions as to how services on the existing network

could be modified following the introduction of HS2, to support development of

the business case. These include reducing some service frequencies and re-

routeing some services in ways that may worsen connectivity to and from locations

in the Sheffield and Leeds City Regions (SCR and LCR).

1.3 This study considers alternative opportunities to enhance services on the existing

rail network following the introduction of HS2, and makes an initial valuation of

the potential economic benefits. The study covers:

I The potential impact of HS2 on demand for services on the existing network;

I How service provision on the existing network might be refined in order to

serve the residual markets following the start of HS2 services; and

I An initial estimate of the potential economic benefits such refinements might

generate.

Study Area

1.4 The study is focused on the rail services to, from and within the Sheffield and

Leeds City Regions. To facilitate the analysis and presentation of the economic

benefits stations within the City Regions (and some key locations outside the City

Regions) have been split into three groups. These are:

I The Regional Centres – which consist of the major rail centres within and

outside the City Regions and include: Leeds, Bradford, York, Sheffield,

Nottingham, Derby, Birmingham, Newcastle, Edinburgh and London;

I The Sub Regional Centres – which consist of other important rail centres

within the City Region and include: Doncaster, Huddersfield, Wakefield,

Chesterfield, Harrogate, Halifax, Barnsley, Rotherham and Retford; and

I Local Stations - which have been split into number of specific routes as

summarised in the map overleaf.

1.5 Figure 1.1 overleaf illustrates the regional, sub-regional and local stations for

which specific outputs have been considered as part of the study.

Technical Report

2

FIGURE 1.1 STUDY AREA

Technical Report

3

Study Approach

1.6 The following paragraphs present an overview of the approach that has been

adopted for this study; more detail is provided in the subsequent chapters of this

report. To provide a clear audit trail and evidence base to underpin the study a

staged approach was adopted:

I Stage 1 – Establishing the strategic context and ‘base case’ scenario;

I Stage 2 – Identifying the impact of HS2;

I Stage 3 – Developing timetable options; and

I Stage 4 – Assessing the economic benefits.

1.7 Each stage is summarised in more detail below.

Stage 1 – Establishing the Strategic Context and ‘Base Case’ Scenario

1.8 The strategic context is important to this study for two reasons. It helps define

what a ‘reasonable to assume’ service provision and network capability might be in

2032. This forms the base case scenario against which we can consider the benefits

of a refined post-HS2 timetable. It also helps define the guiding principles that

underpin our assumptions of how the post-HS2 timetable might be developed. This

is covered in Chapter 2.

1.9 At this stage the projected demand growth between now and 2032 has been

established using standard industry demand forecasting tools and assumptions. This

is set out in Chapter 3.

Stage 2 – Identifying the Impact of HS2

1.10 At this stage analysis was undertaken to compare the identified pre-HS2 timetable

scenarios with a scenario that includes HS2 services. The analysis allows

identification of those flows where demand might be abstracted to HS2, and

therefore where there is an opportunity to consider ways to refine services on the

residual network. This stage is detailed in Chapter 4.

Stage 3 – Developing Timetable Options

1.11 Service options have been developed to represent opportunities to refine services

on the existing network following the introduction of HS2. The options draw on the

evidence identified during Stages 1 and 2. These options are set out in Chapter 5.

1.12 There is a wide variety of committed, planned and aspirational enhancements to

the rail network. The extent to which these are delivered will have a direct impact

on the nature of the residual rail market post-HS2 and the network capability for

residual passenger and freight services. Reflecting the range of possible

enhancements between now and 2032 two scenarios for the ‘without HS2’ existing

rail network in 2032 have been modelled. These scenarios, developed in

consultation with industry partners, reflect the extremities of likely development

in the rail network over the next 20 years. The two scenarios that have been

modelled are as follows:

Technical Report

4

I The Conservative Scenario - based on the current (December 2012) timetable.

It is acknowledged that some infrastructure enhancement and additional

rolling stock is committed. However, the resulting service enhancements will

be determined as part of the franchising process and are not currently

confirmed; and

I The Optimistic Scenario – based on planned enhancements and other

aspirations as set out in the informing strategies, plans and industry views. It

considers an optimistic view of likely infrastructure and service

enhancements, including specifically three additional hourly services

throughout the day on the East Coast Main Line to London and an additional

hourly York – Leeds - Birmingham cross country service.

1.13 Post-HS2 timetable options for the existing network have been developed for both

the Conservative and Optimistic Scenarios. The higher capacity on the existing

network assumed in the Optimistic Scenario would enable additional opportunities.

Two post-HS2 Optimistic Scenarios are assumed, which represent different options

for passenger and freight services.

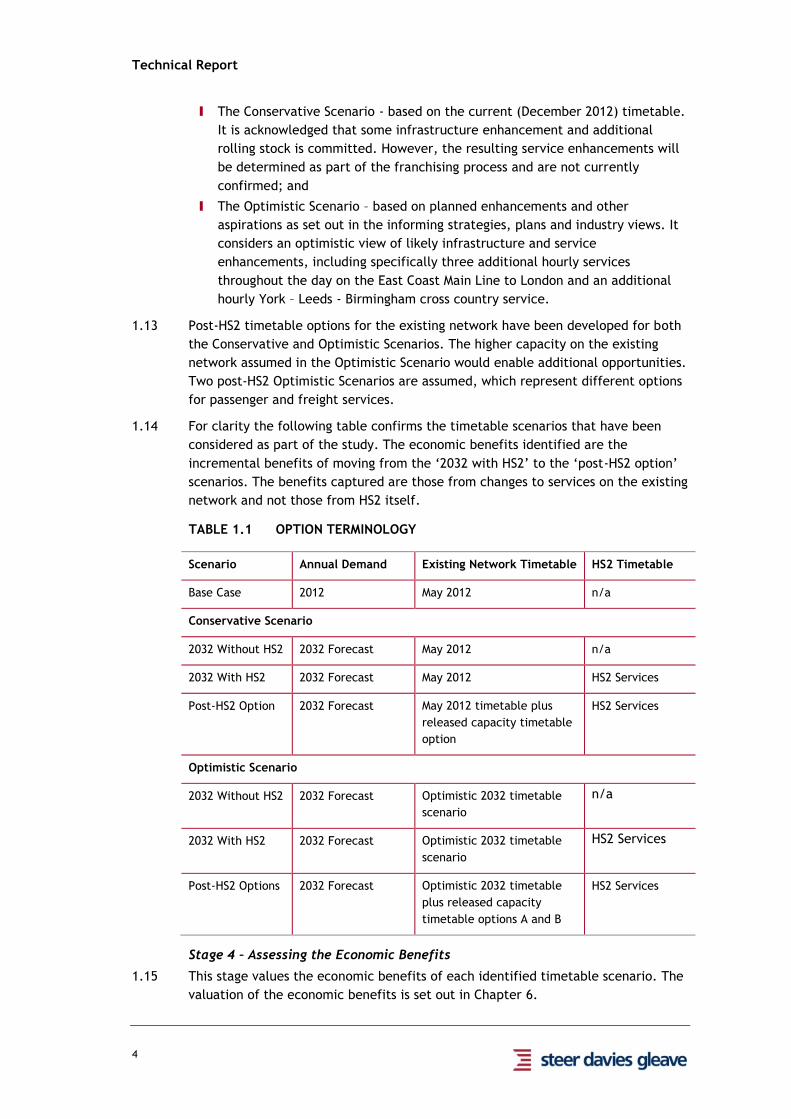

1.14 For clarity the following table confirms the timetable scenarios that have been

considered as part of the study. The economic benefits identified are the

incremental benefits of moving from the ‘2032 with HS2’ to the ‘post-HS2 option’

scenarios. The benefits captured are those from changes to services on the existing

network and not those from HS2 itself.

TABLE 1.1 OPTION TERMINOLOGY

Scenario Annual Demand Existing Network Timetable HS2 Timetable

Base Case 2012 May 2012 n/a

Conservative Scenario

2032 Without HS2 2032 Forecast May 2012 n/a

2032 With HS2 2032 Forecast May 2012 HS2 Services

Post-HS2 Option 2032 Forecast May 2012 timetable plus

released capacity timetable

option

HS2 Services

Optimistic Scenario

2032 Without HS2 2032 Forecast Optimistic 2032 timetable

scenario

n/a

2032 With HS2 2032 Forecast Optimistic 2032 timetable

scenario

HS2 Services

Post-HS2 Options 2032 Forecast Optimistic 2032 timetable

plus released capacity

timetable options A and B

HS2 Services

Stage 4 – Assessing the Economic Benefits

1.15 This stage values the economic benefits of each identified timetable scenario. The

valuation of the economic benefits is set out in Chapter 6.

Technical Report

5

Caveats

1.16 It should be recognised that, with around 20 years until the opening of HS2

Phase 2, there is considerable uncertainty over how service provision and

infrastructure will evolve. This report is based on a reasonable assessment of the

potential future service provision and infrastructure enhancements and this point

in time.

1.17 The timetable options identified are used purely to underpin the modelling work.

They are designed to allow a reasonable estimation of the likely economic benefits

of a post-HS2 timetable option. The options do not represent any firm commitment

to change service in specific manner. Significant timetable development will need

to be undertaken before a firm post-HS2 timetable could be ascertained, which is

outside the scope of this study.

Report Structure

1.18 The remainder of this report is structured as follows:

I Chapter 2 - Strategic Context / Guiding Principles: Provides the strategic

context underpinning the timetable development assumptions informing the

2032 ‘without HS2’ timetable and used to define the guiding principles that

informs future timetable development;

I Chapter 3 - Establishing the 2032 ‘Without HS2’ Demand: Describes the

process of forecasting 2032 ‘without HS2’ demand, including underlying

demand growth and impact of timetable enhancement delivered by 2032;

I Chapter 4 - Impact of HS2: - Gives details of HS2 timetable proposals and the

HS2 impact on demand on the existing network;

I Chapter 5 - Developing a Post-HS2 Timetable: Sets out the process for

developing post-HS2 passenger timetable and freight opportunities.

I Chapter 6 - Economic Benefits of Post-HS2 Timetable Development:

provides a description of the valuation of the economic benefits of a post-HS2

timetable; and

I Chapter 7 – Conclusions and Next Steps.

Technical Report

7

2 Strategic Context and Guiding Principles

Introduction

2.1 There are a variety of strategies and plans that set out the desired direction of

development of the rail network in the Sheffield and Leeds City Regions. These

cover periods ranging from the remainder of this control period (2014) to longer

term plans including to 2029 and beyond.

2.2 This chapter sets out the pertinent strategies and plans to the development of the

rail network in the Sheffield and Leeds City Regions and, moreover, to the

opportunity that HS2 might afford in developing rail services on the existing

network. Such plans and strategies are important in the context of this study for

two reasons:

I They provide insight into how the existing rail network may develop between

now and 2032, which informs the Optimistic 2032 ‘without HS2’ Scenario; and

I They give guidance as to what the priorities might be in the post-HS2

timetable options.

2.3 In presenting the strategic context this chapter:

I Sets out the plans and strategies that are important to the Sheffield and

Leeds City Regions;

I Summarises the principles underpinning development of the rail network

between now and 2032, as modelled in the Optimistic 2032 ‘without HS2’

timetable scenario; and

I Confirms the principles that guided the development of options for a post-HS2

timetable scenario.

Rail Strategies Covering the Sheffield and Leeds City Regions

2.4 Below is set out the studies, plans and strategies that will influence the

development of rail network capability and rail service outputs between now and

2032, and will also influence longer term development of the network beyond.

Route Utilisation Strategies (RUSs)

2.5 There are four Network Rail geographic RUSs of relevance to this study dating from

2008 onwards: East Coast, Yorkshire and Humberside, East Midlands and two

versions of a Northern RUS. There are also two nationwide RUSs that are of

interest, for Electrification and Freight. These strategies are managed and

published by Network Rail with support from the wider rail industry.

2.6 The RUS process follows a standard approach of reviewing general developments

and commitments in the study area, identifying gaps between demand and rail

service provision and network capability, considering options to address these gaps

and then working forward through business case development to make

recommendations.

2.7 In the identified RUS reports the following themes emerge:

Technical Report

8

I Insufficient route capacity on the East Coast Main Line, especially to the

south of Peterborough, on the two track section between Doncaster and

Peterborough and north of York towards Newcastle. Pathing slower freight

and faster passenger services is a major constraint;

I Proposals to improve services towards London on both the East Coast Main

Line (through additional infrastructure to enhance capacity) and the Midland

Main Line (through electrification);

I Recommendations and suggestions on improvements to a wide range of non–

London longer distance services (Yorkshire to Thames Valley and South Coast);

I Regional and local train service crowding on the routes leading into the major

cities, but especially into Leeds and Sheffield;

I The need to identify a strategy to electrify the most advantageous routes,

alongside the geographic RUS process; and

I The delivery of a Strategic Freight Network which protects and develops the

coal supply routes and the capability and capacity of longer haul container

and intermodal routes.

2.8 The RUS programme has now effectively been superseded by the Long Term

Planning Process market led studies based on long distance and regional needs,

summarised later. However, the underlying RUS work remains both valid and

important in shaping strategic decisions with many of the RUS recommendations

being reflected in the High Level Output Statement (HLOS) for Control Period 5.

Northern Hub

2.9 Alongside the RUS process Network Rail, working closely with Local Authorities and

wider stakeholders across the north of England, has developed the Northern Hub

strategy. The purpose of the strategy is to unlock the key capacity constraints in,

and on radial routes from, central Manchester that restrict the development of

inter-regional rail services more widely across the north of England. The strategy

identified a strong case for investing in additional capacity schemes and line speed

improvements. These specifically include:

I In central Manchester: Ordsall Chord linking Manchester Victoria, Oxford Road

and Piccadilly stations allowing trains via Manchester Victoria to serve

Manchester Airport and enhanced capacity on the Castlefield Corridor to allow

more frequent services to Manchester Airport;

I Caldervale Line: Line speed improvements to allow quicker services between

Bradford and Manchester. Ordsall Chord also allows direct services to

Manchester Airport;

I Huddersfield Line: Electrification to provide additional capacity and quicker

services as well as faster journeys to Liverpool via Manchester Victoria; and

I Hope Valley Line: Line speed improvements and additional capacity to allow

two additional longer distance services.

Technical Report

9

High Level Output Statement and Strategic Business Plan

2.10 Many of the recommendations of the Route Utilisation Strategies and the full

Northern Hub Strategy have been adopted by the rail industry and are planned for

delivery in Control Period 5 (2014-2019). This includes options include in the High

Level Output Statement (HLOS) for Control Period 5 and in response included in

Network Rail’s Strategic Business Plan.

Electrification

2.11 The HLOS makes provision for the electrification of the Midland Main Line north of

Bedford to Sheffield via Derby and Nottingham in Control Period 5 (or in the early

years of Control Period 6). The work is contingent on the completion of route re-

signalling and to take place either following major station remodelling (as in

Nottingham in 2013), or in parallel with these works to reduce disruption and

reduce costs.

2.12 A very significant investment in the future has been the agreement by the DfT to

proceed with a major programme of electrification for the North Trans Pennine

route from Manchester to York via Huddersfield and Leeds, and an extension to

Selby and the East Coast Main Line. It is planned for completion by 2019 and will

give a major capacity and service boost to a wide range of service groups across

Northern England.

2.13 Recommendations on options for further electrification are being considered by

Network Rail. It is considered likely that this will include extensions from Sheffield

to Doncaster via Rotherham and Mexborough, and Sheffield to Leeds via

Moorthorpe, along with the route south of Derby towards Birmingham via Burton on

Trent. At a future date there are options for extending the Leeds to Selby scheme

(approved for CP5) to Hull, giving more connectivity for inter-urban operations.

There is also strong stakeholder support for electrification to Middlesbrough.

2.14 The primary outputs from electrification are higher train speeds and quicker

acceleration resulting in reduced journey times and better use of track capacity as

well as significant cost savings.

Re-signalling and Route Control

2.15 Network Rail are developing a national signalling and control strategy for delivery

from 2014 onwards which will remove a significant number of older electronic and

manual signal boxes from service and concentrate 80% of national rail operations

on 14 Route Operational Control locations by 2030. In the study area, operations

will be concentrated on the two new locations at Derby (East Midlands – replacing

as a minimum Leicester, Trent and Derby signal centres) and York which will

control much of the East Coast main line, Sheffield and Leeds. Other lines not

classified as trunk routes will be encompassed within these new centres,

potentially going through a transition period. The development of modular

signalling will reduce costs on lighter trafficked lines. New signalling facilities will

be compliant with the gradual national fitment of ERTMS (European Rail Traffic

Management System) for installation in a future rollout as compatible rolling stock

is built or retro-fitted.

Technical Report

10

2.16 The outputs of the new generation of signalling control is driven by general

efficiency of rail operations (for example giving control staff total oversight of

train operations on a discrete area), centralised control for information and train

running information and service supervision. During the design and planning of new

facilities, many options and opportunities are available for the industry to improve

route capacity through the removal of obsolete infrastructure and replacement

with new capacity (for example signal spacing and section headways) - more

attuned to the 21st Century railway and emerging traffic needs.

Rolling Stock and Train Management System (ERTMS)

2.17 The industry has developed a cross member Rolling Stock Strategy (February 2013)

which sets out a vision for the future fleet size, and a broad platform to enable

operators and manufacturers to consider the requirements in planning a strategy

to deal with growth and passenger requirements (this excludes non-franchised and

freight operators). The key message is that by the 2030s much of the present

rolling stock fleet will have been extensively refurbished and re-engineered and

there will have been considerable augmentation by the building of new electric

trains for all operating types including trains for the High Speed route operations.

The national use of diesel traction will be much reduced, with 80% of traffic

handled by electric trains by the 2030s.

2.18 IEP trains will be delivered during Control Period 5 replacing the current long

distance diesel fleet on East Coast Main Line services. The formation of these

trains, in five and ten car sets, will allow more flexibility in serving locations away

from the core East Coast route. The necessary infrastructure to support IEP roll

out, particularly power supply equipment, will be provided during Control

Period 5.

2.19 A complex area is the phasing in of ERTMS on a regional basis with suitably fitted

rolling stock – a national plan which will spread over several decades is being

prepared at the moment. All trains for operation on high speed lines will be a

priority for fitment as operation without the facility will not be allowed.

Capacity enhancements in Control Period 5

2.20 DfT and the rail industry have identified a series of infrastructure improvements

and enhancements in the region as an aid to managing passenger and freight

growth in the period 2014 to 2019 as identified in the illustrative HLOS solutions.

These include new platform capacity at Leeds at the west end, the provision of

additional terminating facilities for local services at Horsforth and Micklefield

(giving more efficient operation of peak hour services) and a series of suburban

platform extensions across the area.

Technical Report

11

Yorkshire Rail Network Study

2.21 The longer term objective of the Yorkshire Rail Network Study3 was to set the

foundation for an assessment of the medium term investment needs for rail routes

in Yorkshire in order to support the identification of schemes for delivery beyond

2019. Specifically, the Yorkshire Rail Network Study establishes an evidence base

that allows targeted proposals to enhance the rail network to be developed with

the goal of maximising economic returns.

2.22 The primary purpose of the study was to develop a “Conditional Output

Statement”. With the goal of supporting economic growth in the Leeds and

Sheffield City Regions, the Conditional Outputs codify what the rail industry should

strive to deliver. The Conditional Outputs have been developed considering the

established evidence base complemented by bespoke analysis of the potential

economic benefits of enhancing current train capacity and facilitating more

frequent services with lower journey times. They are described as “conditional”

because realisation of each output will be subject to an affordable and value for

money solution being identified and delivered by the rail industry.

2.23 Four of the Conditional Outputs identified by the Yorkshire Rail Network Study are

of specific importance for the purpose of developing the optimistic 2032 ‘without

HS2’ timetable. These are the Conditional Outputs for connectivity, capacity,

freight and north-south links as summarise below:

I Connectivity - Rail journey times should be quicker than off peak car

journeys and there should be a minimum frequency of two trains per hour all

day operating on a clock face timetable with additional peak services as

required to meet demand. Specific targets were identified for connectivity

between the major regional centres as follows:

Leeds – Manchester: 40 minutes, six trains per hour;

Sheffield – Manchester: 40 minutes, four trains per hour;

Leeds – Sheffield: 35 minutes, two trains per hour (and two semi-fast trains

which provide a viable alternative to the fast trains);

Bradford – Manchester: 50 minutes, two trains per hour;

Bradford – Leeds: 15 minutes, six trains per hour, from a single station;

and

Leeds – York: 20 minutes, six trains per hour;

I Capacity - Sufficient capacity, by providing longer or more frequent trains, to

accommodate forecast demand growth to 2027;

I Freight - Sufficient network capacity and capability to maintain the region’s

electricity generating capacity and deliver forecast growth in rail freight,

particularly inter-modal container traffic; and

I North-South Links - Service improvements should not preclude HS2

implementation or vice versa. Local rail services should maximise the

distribution of HS2 benefits around the region.

3 http://www.wymetro.com/news/projects/projectdetails/YRNS

Technical Report

12

West Yorkshire RailPlan 7

2.24 RailPlan 7 seeks to build on the Local Transport Plan (LTP3) 2011-26 and the

Yorkshire Rail Network Study by setting out Metro’s approach to deliver sustainable

economic growth by improving the rail network in West Yorkshire. It sets the

overall vision for rail in West Yorkshire:

“For West Yorkshire to have the best railway in the country by 2026 - A rail

network that connects people and places in a way that supports the economy, the

environment and quality of life while delivering the best service reliability and

customer satisfaction in the country.”

2.25 To deliver this vision and support the LTP3 and wider rail objectives, Metro has

developed four Rail Objectives that RailPlan should help to deliver for West

Yorkshire. These are:

I To double annual rail patronage;

I To improve passenger satisfaction scores;

I To develop a rail network that secures better value for money for passengers

and tax payers; and

I To exploit the benefits of high speed rail when it arrives in West Yorkshire in

the 2030s.

2.26 Through gap analysis, RailPlan considers where the current and planned capability

of the rail network might prevent the RailPlan objectives being achieved. The

strategy then identifies what will need to be addressed to deliver the rail vision

and achieve the rail objectives. The evidence, gap analysis and strategy is set out

in seven categories. Those that are pertinent to developing the optimistic 2032

‘without HS2’ timetable are as summarised as follows:

I Connectivity - Provide improved connectivity through quicker and more

frequent services between the key economic centres within West Yorkshire

and across the North of England. The Connectivity outputs are consistent with

those set by the Yorkshire Rail Network Study.

I Demand and Crowding - Provide sufficient capacity to meet continuing

passenger growth; and

I Freight - Ensure sufficient network capacity and capability to enable forecast

freight growth in West Yorkshire.

Sheffield City Region Transport Strategy

2.27 The Sheffield City Region Transport Strategy is based on the achievement of the

following four goals:

I To support economic growth;

I To enhance social inclusion and health;

I To reduce emissions; and

I To maximise safety.

2.28 The transport strategy goes on to identify 26 policy areas in order to achieve the

goals. The policy that is of particular relevance to this work is:

“To improve rail services and access to stations, focusing on interventions that

can be delivered in the short term.”

Technical Report

13

2.29 The strategy sets out the Local Enterprise Partnership will work with Network Rail

to improve rail services to London and to neighbouring City Regions: Manchester,

Leeds and Nottingham. Improvements that are strongly supported include:

I Journey time and capacity improvements on the Hope Valley line to

Manchester;

I Electrification and journey time improvements on the Midland Main Line

(MML) between Sheffield and Barnsley, and from both of these to London and

Leeds;

I Journey time and capacity improvements to the East Coast Main Line (ECML),

including links to the south (London) and the north (York, Newcastle and

Scotland); and

I Journey time and capacity improvements for Swinton Junction and Holmes

Chord.

Draft Long Term Rail Strategy for the North of England

2.30 The draft Long Term Rail Strategy (LTRS) has been developed jointly by local

transport authorities across the north of England to help provide a consistent

strategy for developing the rail network. There are three over-arching objectives

that drive the Strategy for the North’s rail services:

I Supporting sustainable economic growth;

I Enhancing service quality, improving the appeal of rail and, by encouraging

more rail use, reducing environmental impacts and carbon emissions; and

I Improving efficiency, reducing the cost per passenger carried.

2.31 The draft LTRS builds on previous work: the City Region transport/rail strategies,

DfT’s DaSTS programme and Network Rail’s Long Term Planning Process. Having

formulated a Vision together as the North’s transport authorities a review was

undertaken to identify the strategic gaps between the ambitions of the Vision and

the reality that is likely to be delivered by current rail industry plans. In response

to the gaps a series of outputs have been identified that the rail industry and local

authorities need to work together to deliver in order to realise the Vision and

overarching objectives identified above.

2.32 As a Vision the draft LTRS identifies that across the North rail use is growing – and

more strongly than on other transport modes. The Vision wants to see this

continue and rail market share to double over the next fifteen or so years,

extending its reach and relevance across the north. The central proposition is that

attention is turned to creating a European-style connected network. The focus is

on broadening the appeal of rail to address a wider set of markets. Additional rail

usage means more revenue and better value from committed and future

investments. The strategy goes on to identify that sustainable economic growth

will be supported by improving connectivity:

I Between the cities of the North;

I By expanding commuter networks;

I Connecting areas of economic disadvantage with areas of economic

opportunity;

I Provide capacity to accommodate the expected growth in freight by rail;

Technical Report

14

I Addressing the differing needs of the North’s evolving and rebalanced

economy; and

I Providing direct and efficient links to London, the other major centres of the

UK, the international airports and ports.

2.33 This will be achieved through a focus on an easy-to-use network, integrated across

the modes, with a connecting timetable of local and express city to city services

and a transformed fares system. The strategy identifies a number of high level

outputs that are of interest in developing an optimistic 2032 ‘without HS2’

timetable. The pertinent outputs are summarised as follows:

I Service Connectivity Between Centres4 - in vehicle rail journey time for

services between these centres that are quicker than the off peak car journey

time and a minimum frequency of two trains per hour. Where possible direct

connections should be available to at least the five key centres, and where

interchange is necessary the connection time should be minimised;

I Commuter Journeys - A minimum peak period frequency in urban areas of

two trains per hour is required with a minimum hourly frequency for

commuter routes in more rural areas. The timetable must allow morning

arrivals in the key urban centres earlier than 07:00 and evening departures

later than 20:00;

I To International Gateways - An hourly direct service from each major

town/city to Manchester Airport. At a minimum each should have access to

Manchester Airport requiring a single interchange;

I Access to London and other UK Centres - Wherever possible there should be

provision of direct services from each centre to London in some hours. And

there should be a half hourly journey opportunity requiring a single

interchange; and

I Capacity – Sufficient capacity needs to be provided to facilitate growth in

passenger and freight demand.

Network Rail’s Long Term Planning Process

2.34 Network Rail, representing rail industry partners, is leading the Long Term

Planning Process (LTPP). This represents a new approach to strategic planning of

the rail network and is designed to take into consideration the views of the rail

industry, funders, specifies and customers. This process fulfils Network Rail’s

licence obligations to plan the future capability of the network, and will replace

the existing RUS process.

2.35 There are three key elements to the LTPP, summarised as follows:

I Market Studies – articulate strategic goals for each particular market sector,

forecast future rail demand, and develop ‘conditional outputs’;

I Cross-Boundary analysis - considers options for services that run across

multiple routes; and

I Route Studies - develop options for future services and for development of

the rail network.

4 Defined as the Inter Connected Matrix

Technical Report

15

2.36 The LTPP is still at the early stage of development. The four draft Market Studies

were published for consultation in April 2013. They are currently being reviewed

by the rail industry and wider stakeholders and therefore subject to revision.

Importantly in the context of this study they are considered broadly consistent

with other existing strategies and plans. Of these studies three are of particular

interest to the Sheffield and Leeds City Regions. These are the studies for: Long

Distance, Regional Urban and Freight. The fourth is for London and the South East.

2.37 Each study has been developed using an assessment of how to deliver the following

three strategic goals. A fourth strategic gaol, affordability, will be considered in

subsequent stages of the planning process.

I Enabling economic growth;

I Reducing carbon and the transport sector’s impact on the environment; and

I Improving the quality of life for communities and individuals.

Long Distance

2.38 In the context of the Sheffield and Leeds City Regions this includes travel between

Leeds and Sheffield, and from these stations to other major centres around the

UK, including: Bristol, Cardiff, Edinburgh, Glasgow, Leicester, Liverpool, London,

Manchester, Newcastle, and Nottingham. The conclusion of the Long Distance

Market Study is a set of Conditional Outputs, which are aspirations for

development of the rail network up to 2043. These are summarised in the

following points:

I The rail industry can help create the conditions to improve economic growth,

the environment, and the quality of life for communities and individuals by

improving the long distance services between the major regional centres;

I The largest improvements against these goals are likely to be generated by

providing very fast services between London and the other principal regional

centres, and between some of the other principal regional centres of around

100 miles in separation such as Birmingham and Leeds;

I Very large improvements against these goals are also likely to be generated

by providing high frequency interurban services between a number of the

principal regional centres in the north of England;

I Service improvements between other regional centres and principal regional

centres in other regions will also be of benefit;

I Provision of improved opportunities to travel between a number of locations

that are not currently directly served would be beneficial; and

I Significant additional capacity is likely to be required over the next 30 years

to accommodate the growth in economically productive travel.

Regional Urban

2.39 The Regional Urban market relates to an area less than 50 miles from a regional

centre where people travel in large numbers primarily for the purpose of

commuting and leisure. In the context of the Market Study and the Sheffield and

Leeds City Regions the regional centres are: Barnsley, Bradford, Doncaster,

Halifax, Huddersfield, Leeds, Sheffield, Wakefield and York.

Technical Report

16

2.40 The Regional Urban study acknowledges that the services covered by the study,

particularly in the commuter markets, are subject to many location specific

considerations. At this stage West Yorkshire has been used as a case study to

understand Regional Urban markets in other areas.

2.41 The key conclusion from the Regional Urban Market Study is that improving

transport links for commuters into commercial and employment centres will help

to drive economic growth through improved supply of labour to employment.

2.42 The study identifies that most people are typically willing to commute where the

generalised journey time5 is less than 20 minutes, and very few are willing to

commute where the generalised journey time is greater than 60 minutes. The

focus in developing service in the Regional Urban area should therefore be in

reducing generalised journey times that are within this 20 – 60 minute range.

Development should also focus on linking locations where the number of people in

the population catchment of the origin station and the number of jobs in the

catchment of the destination station are high.

Freight

2.43 The Freight Market Study presents a summary of the projected growth in rail

freight nationally. The forecasts are broadly consistent with other forecasts that

have been reviewed for this study, as set out in Appendix B.

Assumed Enhancements in the Optimistic 2032 ‘Without HS2’ Timetable

2.44 The following points provide a summary of the underlying assumptions that have

been observed in determining an Optimistic 2032 ‘without HS2’ timetable

scenario. These are informed by the plans and strategies set out previously. A

summary of the assumed timetable changes in the Optimistic 2032 ‘without HS2’

timetable on a route by route basis is provided in Appendix A. In summary it is

assumed that:

I Committed CP5 infrastructure investment is delivered (including Northern

Hub, Trans Pennine and Midland Main Line Electrification, capacity

enhancements) that will allow the HLOS illustrative service options to be

delivered;

I There is a rolling programme of electrification beyond CP5. This could include

the Calder Valley Line, Harrogate Line, Selby – Hull, Sheffield to South Kirby

Junction/Doncaster and ECML to Middlesbrough. Electrification may result in

modest journey time savings, but the detail of these is yet to be confirmed

and no time savings have been modelled;

I In general the headline frequency outputs identified by the

YRNS/RailPlan 7/draft LTRS are delivered. i.e. a minimum 2 trains per hour

frequency across the network;

I Generally limited frequency enhancement on already higher frequency routes,

but rather additional capacity through train lengthening / higher capacity

trains;

5 Generalised journey time is a measure of journey time used by the rail industry. It includes the station to station

journey time, a service frequency penalty and, if appropriate, an interchange penalty.

Technical Report

17

I Roll out of ERTMS signalling and concentration of signalling operations in

major signalling centres. This will generate cost savings and some capacity

enhancements but no direct service output as a result of change;

I An assumption that freight growth (based on RFG / MDS Transmodal report)

would be accommodated; and

2.45 Enhancements between now and 2032 will only be delivered if there is a robust

business and funding case. It is accepted that there may not currently be a robust

case for some of the enhancements included but it is assumed that favourable cost

and revenue growth by 2032 will make the enhancements viable.

‘Guiding Principles’ Underpinning Development of Post-HS2 Scenarios

2.46 Finally, this chapter sets out the guiding principles that have been considered in

developing scenarios to develop rail services on the existing network post-HS2. The

guiding principles reflect the identified plans and strategies that set out the

objectives for transport, and rail specifically, in the Sheffield and Leeds City

Regions.