Embed Size (px)

Citation preview

Shaping Up for the AEC and New Generation Trade Agreements

Cielito F. Habito

Chief of PartyTrade-Related Assistance for Development (TRADE) Project

Forum onAEC Gameplan & Industry Roadmaps Localization

Hotel Roma, Tuguegarao CityMay 12, 2016

Four Observations

1. It’s more about complementation, less of competition.

2. There’s much more to AEC than ASEAN itself.

3. AEC and other agreements have pushed us to do the right things.

4. The Philippines is well-positioned for AEC (and other ‘new-generation’ FTAs)

1. More complementation, less ofcompetitionMore trade happening within the same industries (‘intra-industry trade’)

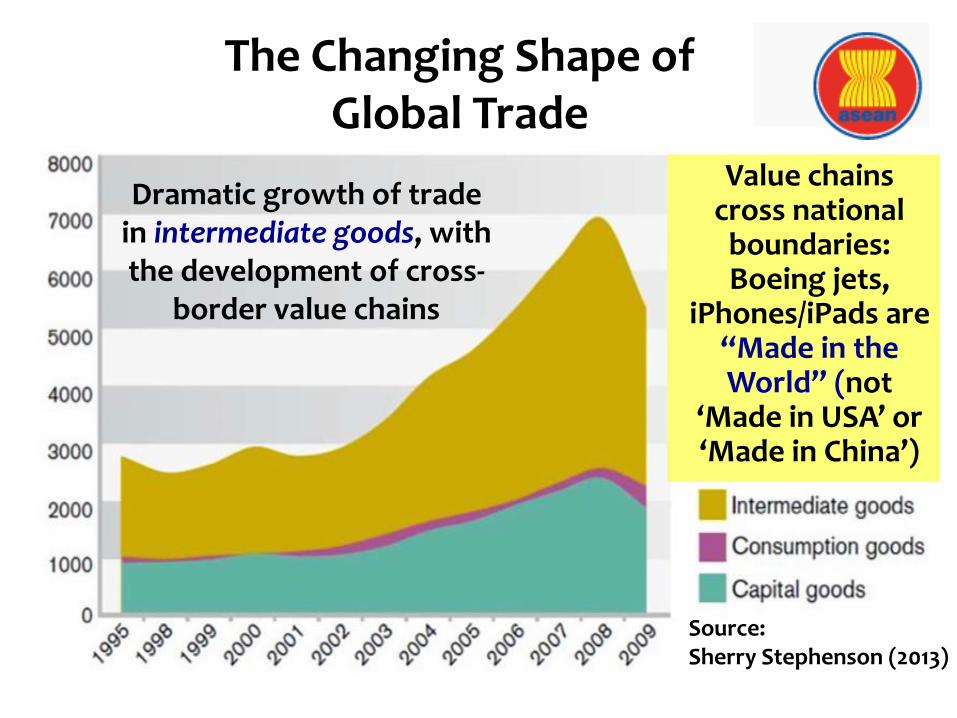

Dramatic growth of trade in intermediate goods, with the development of cross-

border value chains

Source: Sherry Stephenson (2013)

The Changing Shape of Global Trade

Value chains cross national

boundaries: Boeing jets,

iPhones/iPads are “Made in the World” (not

‘Made in USA’ or ‘Made in China’)

Philippine Trade with ASEAN Partners

With ThailandTop imports: Motor vehicles, electronics, petroleum and chemicalsTop exports: Motor vehicle parts, electronics &electricals, and minerals

With SingaporeTop imports: Electronics, machinery and petroleumTop exports: Electronics & electricals, machinery, and petroleum

With MalaysiaTop imports: Electronics, petroleum and chemicalsTop exports: Electronics, coconut oil, petroleum

Trade in ASEAN/AECFeatures

Largely intra-industry in nature (trade in products within the same industries, e.g. electronics, vehicles, chemicals)

Trade relationships are increasingly complementary rather than competitive; trade protection can be self-penalizing

Opportunities lie in positioning in regional and global value chains (aka production networks)

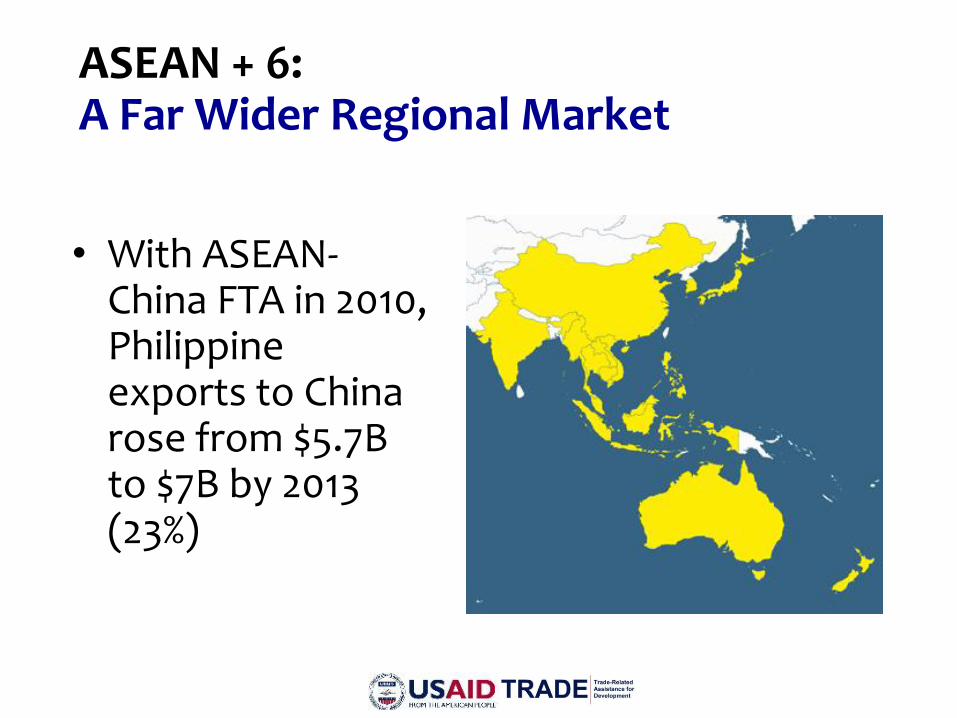

2. There’s much more to AEC than ASEAN itself.Membership in ASEAN opens access to six other large economies

ASEAN FTAs • ASEAN Free Trade Area (1992)• ASEAN – Korea FTA (2007)• ASEAN – Japan FTA (2008)• ASEAN – Australia+New Zealand FTA (2009)• ASEAN – China FTA (2010)• ASEAN – India FTA (2010)

ASEAN membership also means free access to Australia, China, India, Japan, Korea and New Zealand markets

ASEAN’s combined market = 600 million

ASEAN+6 combined market = 3.45 billion

• With ASEAN-China FTA in 2010, Philippine exports to China rose from $5.7B to $7B by 2013 (23%)

ASEAN + 6: A Far Wider Regional Market

New Generation Trade Agreements

• Regional Comprehensive Economic Partnership (RCEP) - to combine the ASEAN+6 FTAs; negotiations ongoing

• Trans Pacific Partnership (TPP) – 12 members so far, with 4 from ASEAN: Brunei, Malaysia, Singapore & Viet Nam; agreement signed on February 4, 2016

Trans Pacific Partnership: What is it?

An ambitious ‘new generation’, ‘high-standard’ trade agreement

Currently composed of 12 countries on both sides of the Pacific having:

• Combined population of 800 million

• GDP of $28 trillion (40% of global GDP)

• $9 trillion in merchandise trade; $2 trillion trade of services (30% of world trade)

TPP: Who are in it?

• Brunei (2005)

• Chile (2005)

• New Zealand (2005)

• Singapore (2005)

• Peru (2008)

• Australia (2008)

• United States (2008)

• Vietnam (2008)

• Malaysia (2010)

• Canada (2012)

• Mexico (2012)

• Japan (2013)

TPP: Who hope to come in?‘Second Wave’ Countries

• South Korea

• Philippines

• Taiwan

• Thailand

• Colombia

• Indonesia

• India

• Sri Lanka

3. AEC and other agreements are pushing us to do the right things.Membership entails compliance with certain policy commitments

Selected Stories

• My long, long wait for a phone land line

• A night at the movies

• Local cement monopolies

Common thread:

Restrained Competition

‘Right Things’ We’ve Been/We’re Being Led to

DoLegal/Policy Reforms

• Competition (Antitrust) Law - Done

• Customs Modernization & Tariff Act - Done

• Ease foreign investment restrictions - ??

Administrative Reforms

• Streamline customs processes

• Remove unnecessary & duplicating import clearances and permits (e.g., Toblerone)

The Philippine AEC Game Plan

Built on a Four C’s Strategy

• Competitiveness

• Compliance

• Collaboration

• Communication

Toward AEC-Enabled Enterprises

Competitiveness Agenda

PPP Infrastructure Program

Industry Road Maps (BOI)

Clustering Initiatives; Shared Service Facilities; Roving Academy (DTI, DOST)

Financial Inclusion Agenda (BSP)

Competition Law, CMTA (Congress)

Halal Industry Support (DTI, Bangsamoro)

Trade Facilitation Measures (Customs)

Climate Change & Disaster Resilience ++

4. The Philippines is in a strong position for AEC.

Now the strongest economy in ASEAN; PH firms are already AEC-engaged.

How is the Economy Doing?“PiTiK Test”

The Essential Yardsticks (P-T-K):

Price Stability (Presyo)

Jobs (Trabaho)

Incomes (Kita)

The Economy In 2015Good News on All 3 Counts

Prices: Inflation rate down to record low (Oct ’15 – 0.4%; 2015 Ave – 1.4%; Now: 1.1%)

Jobs: Unemployment rate finally breaks 6% barrier, down to 5.8%

Incomes/Output: Q4-2015 GDP growth of 6.3% (full year 2015 – 5.8%) among the fastest in ASEAN and globally

Signs of a BreakoutPiTiK Then (2004-09) & Now (2010-15)

Source: PSA

Latest: 1.1%

Latest: 5.8%

PH has moved ahead in ASEAN…

Source: WB

…and quality of growth is improving

Source: NEDA

2.8%

4.5%

6.3%Growing Investment

Contribution

2.8%

4.5%

6.3%Growing Industry

Contribution

Many PH firms are already AEC-engaged

Large: Jollibee, Oishi (Liwayway),

Golden ABC (Penshoppe), ICTSI, URC,

Mama Sita, KLT Fruits, Pointwest,

Splash, many more

Medium: Fountainhead, Manila Catering

Small: Human Nature, Great Women

Micro: Tubigon Loomweavers

Common Thread: Proactive, not Defensive

The Philippines & AEC Expressed concerns and fears are mostly due

to long-standing government failures, not inherent to AEC itself (e.g., weak support for agriculture)

Historically, policy of protection has fostered complacency and inaction

FTAs are pushing us into the long-needed policy reforms (open skies, competition law)

Making the most of AEC and new FTAs is a matter of attitude and mindset, i.e., proactiveness vs. defensiveness

From fearing threats to seizing opportunities

From creating ghosts to finding gold mines

Wanted:A Change in Mindset: