Embed Size (px)

DESCRIPTION

Income Tax Accounting SFAS 109 (ASC 740-10)

Citation preview

Income Tax Accounting SFAS 109 (ASC 740-10)

2

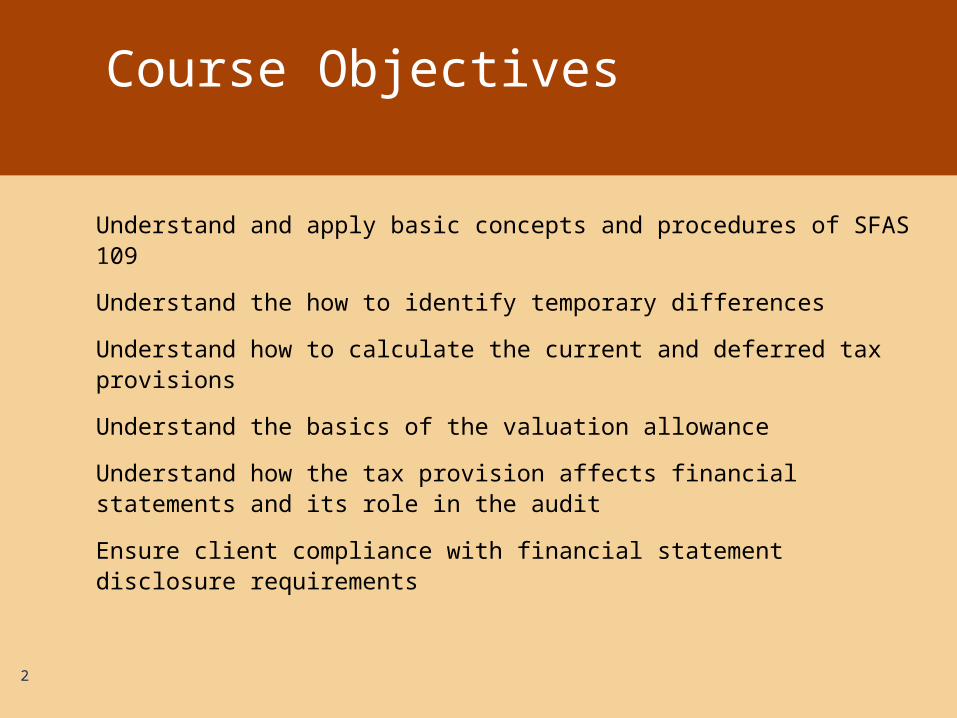

Course Objectives

Understand and apply basic concepts and procedures of SFAS 109

Understand the how to identify temporary differences

Understand how to calculate the current and deferred tax provisions

Understand the basics of the valuation allowance

Understand how the tax provision affects financial statements and its role in the audit

Ensure client compliance with financial statement disclosure requirements

3

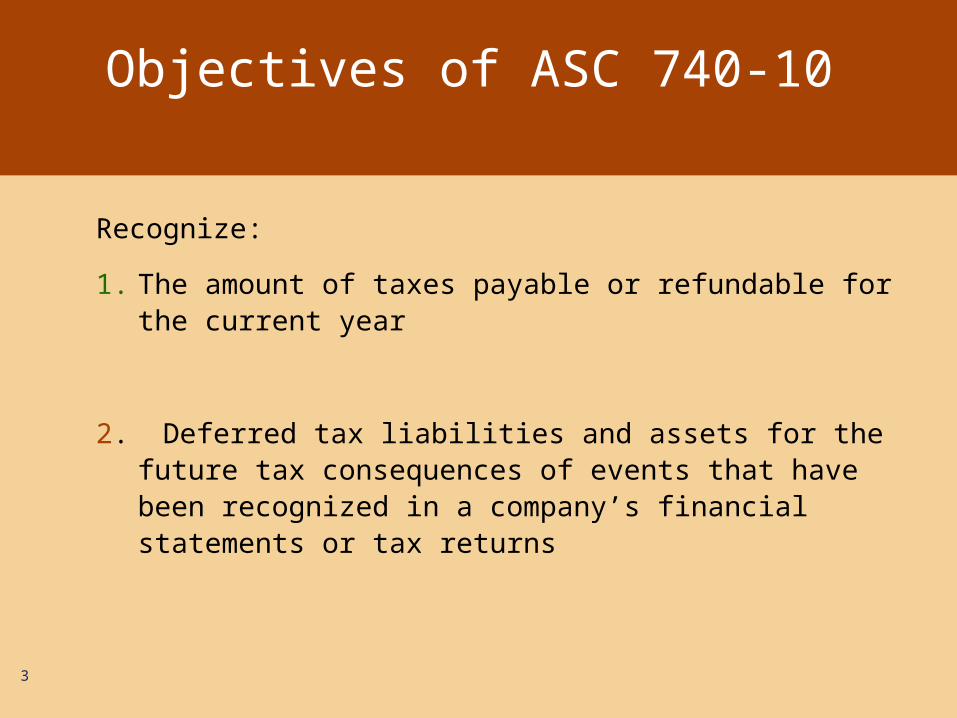

Recognize:

1. The amount of taxes payable or refundable for the current year

2. Deferred tax liabilities and assets for the future tax consequences of events that have been recognized in a company’s financial statements or tax returns

Objectives of ASC 740-10

4

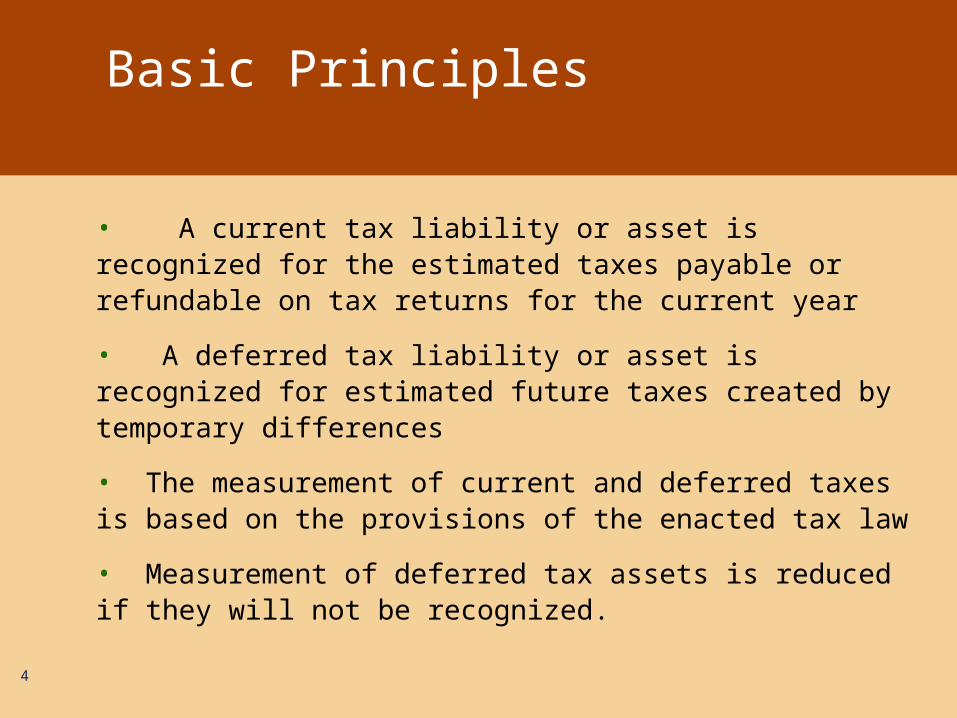

• A current tax liability or asset is recognized for the estimated taxes payable or refundable on tax returns for the current year

• A deferred tax liability or asset is recognized for estimated future taxes created by temporary differences

• The measurement of current and deferred taxes is based on the provisions of the enacted tax law

• Measurement of deferred tax assets is reduced if they will not be recognized.

Basic Principles

5

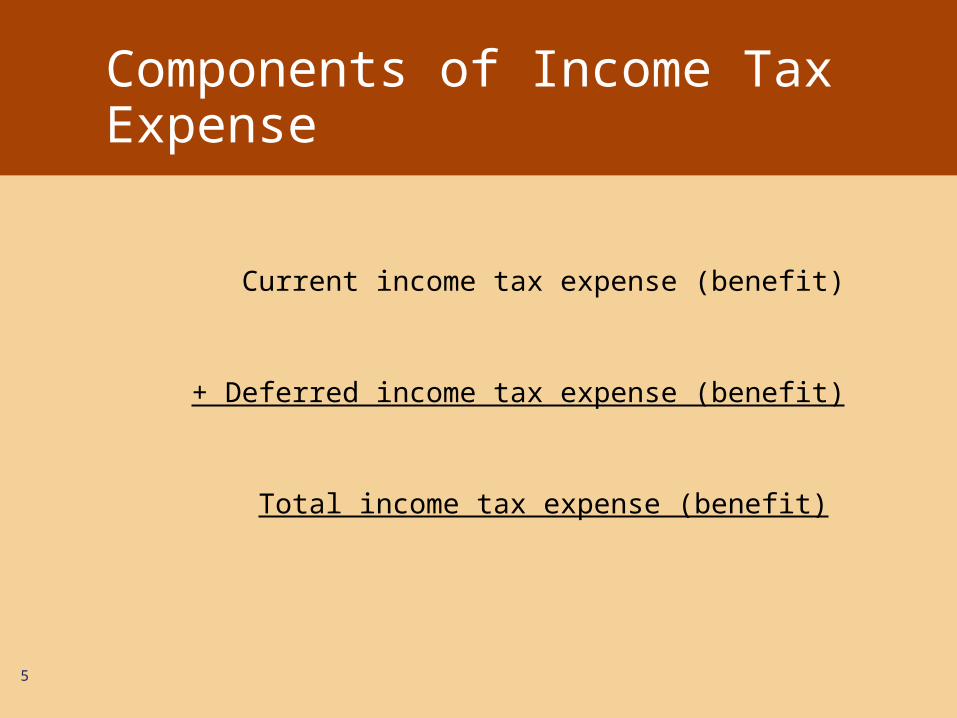

Current income tax expense (benefit)

+ Deferred income tax expense (benefit)

Total income tax expense (benefit)

Components of Income Tax Expense

6

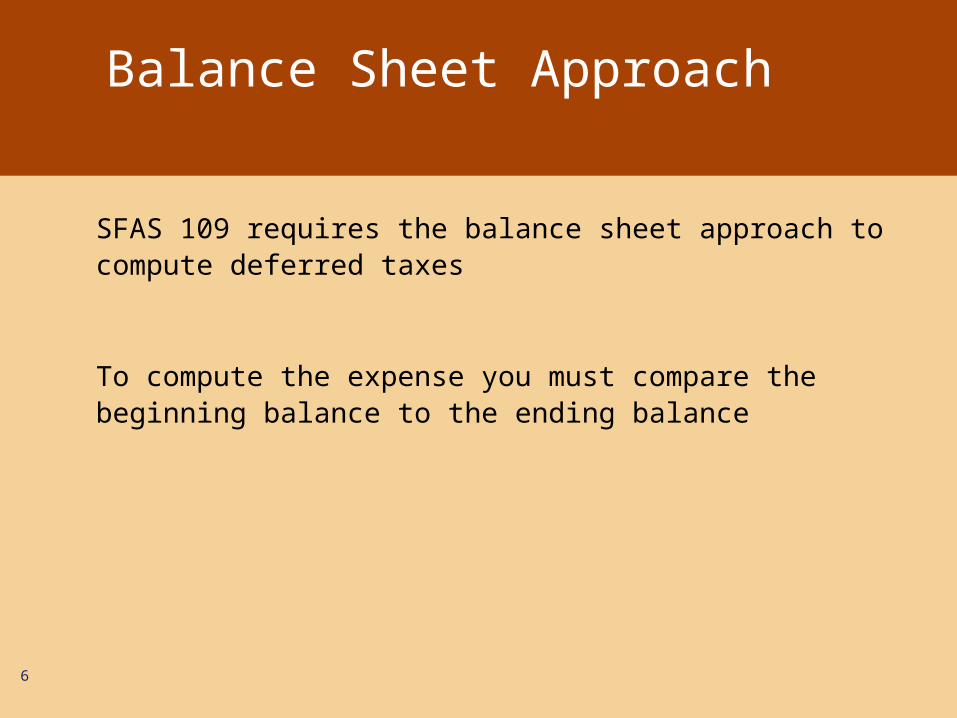

Balance Sheet Approach

SFAS 109 requires the balance sheet approach to compute deferred taxes

To compute the expense you must compare the beginning balance to the ending balance

Balance Sheet Approach

7

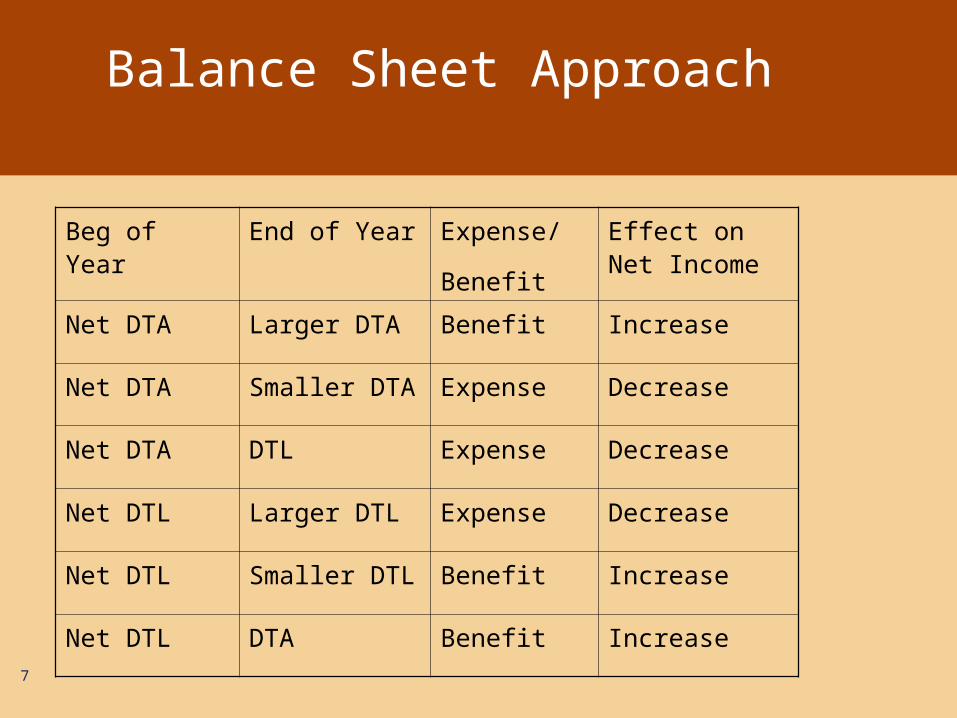

Balance Sheet Approach

Beg of Year End of Year Expense/

Benefit

Effect on Net Income

Net DTA Larger DTA Benefit Increase

Net DTA Smaller DTA Expense Decrease

Net DTA DTL Expense Decrease

Net DTL Larger DTL Expense Decrease

Net DTL Smaller DTL Benefit Increase

Net DTL DTA Benefit Increase

8

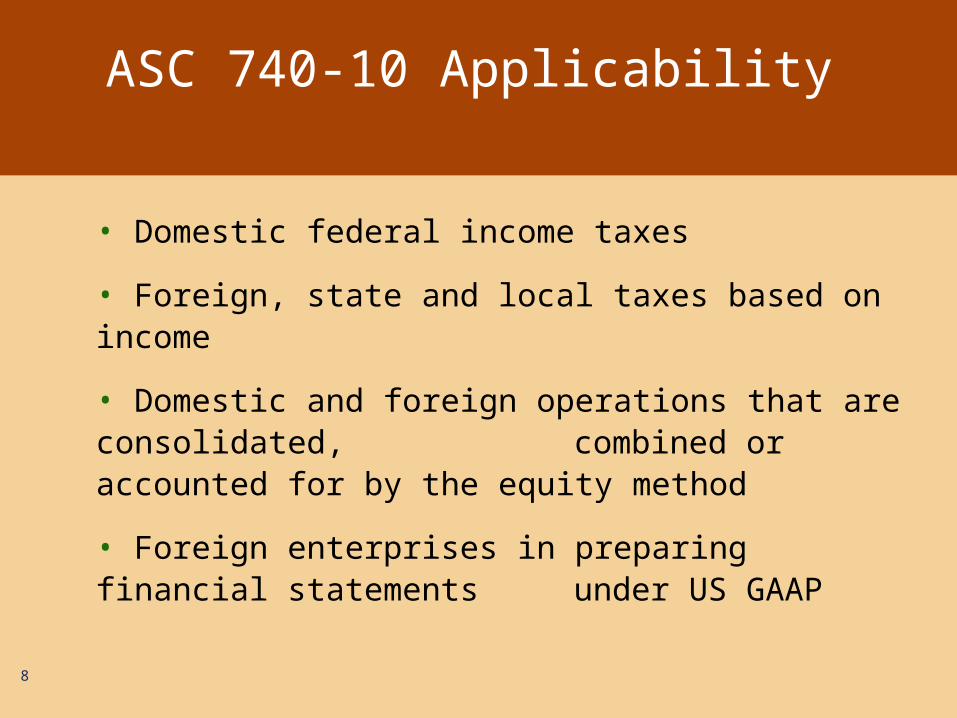

• Domestic federal income taxes

• Foreign, state and local taxes based on income

• Domestic and foreign operations that are consolidated, combined or accounted for by the equity method

• Foreign enterprises in preparing financial statements under US GAAP

ASC 740-10 Applicability

9

Hi Course Objectives story

• APB 11– Issued in 1967

– Used the Deferred Method

– Calculation was a “with” and without” method

History of Accounting for Income Taxes

10

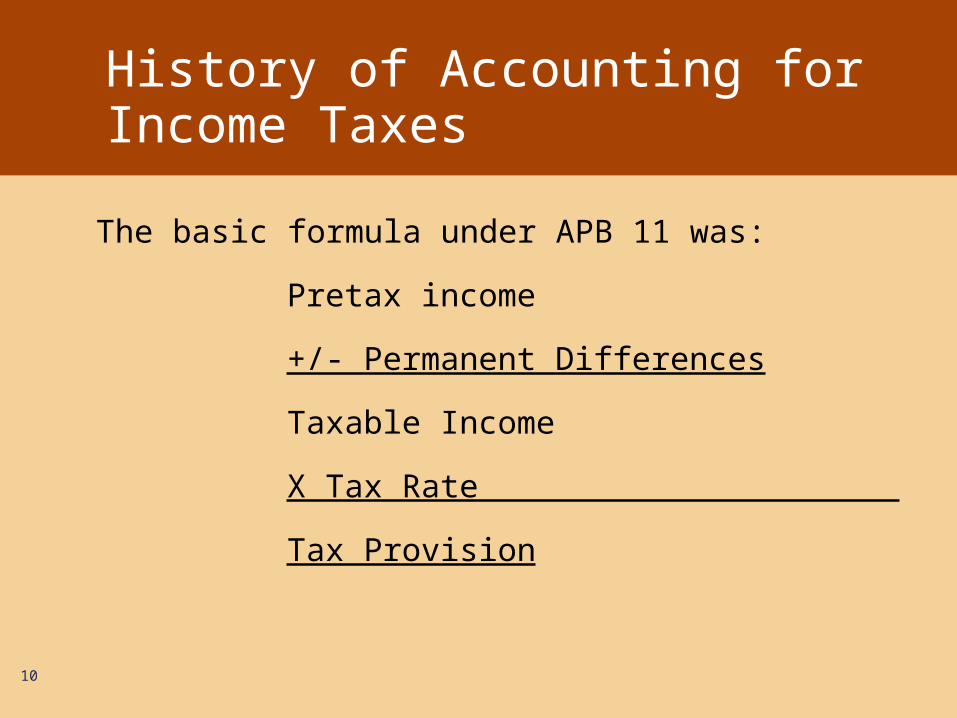

The basic formula under APB 11 was:

Pretax income

+/- Permanent Differences

Taxable Income

X Tax Rate

Tax Provision

History of Accounting for Income Taxes

11

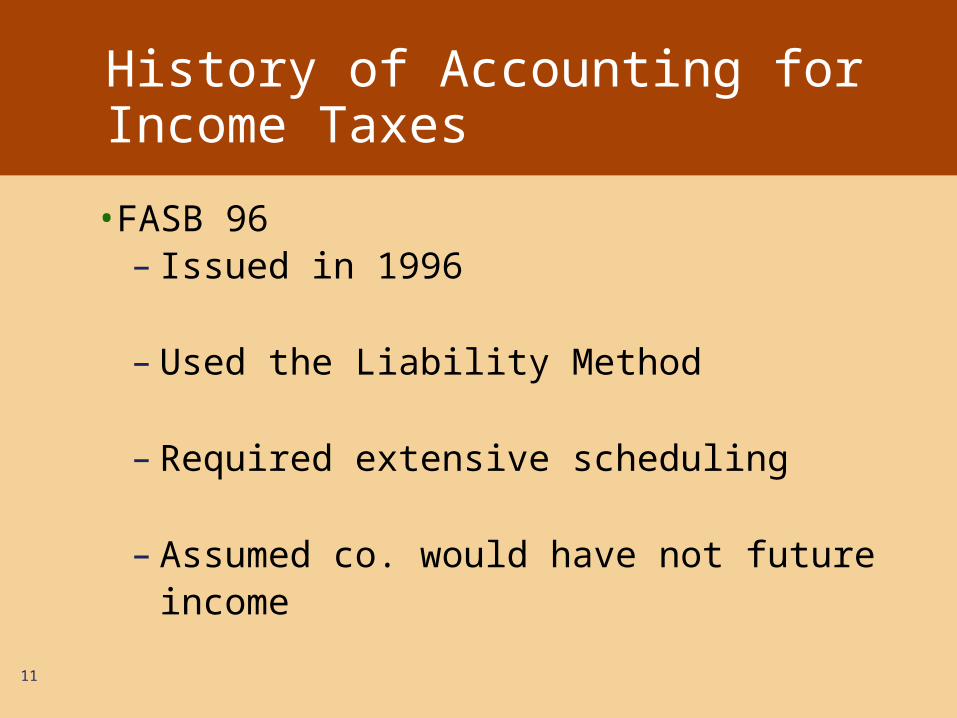

•FASB 96– Issued in 1996

– Used the Liability Method

– Required extensive scheduling

– Assumed co. would have not future income

History of Accounting for Income Taxes

12

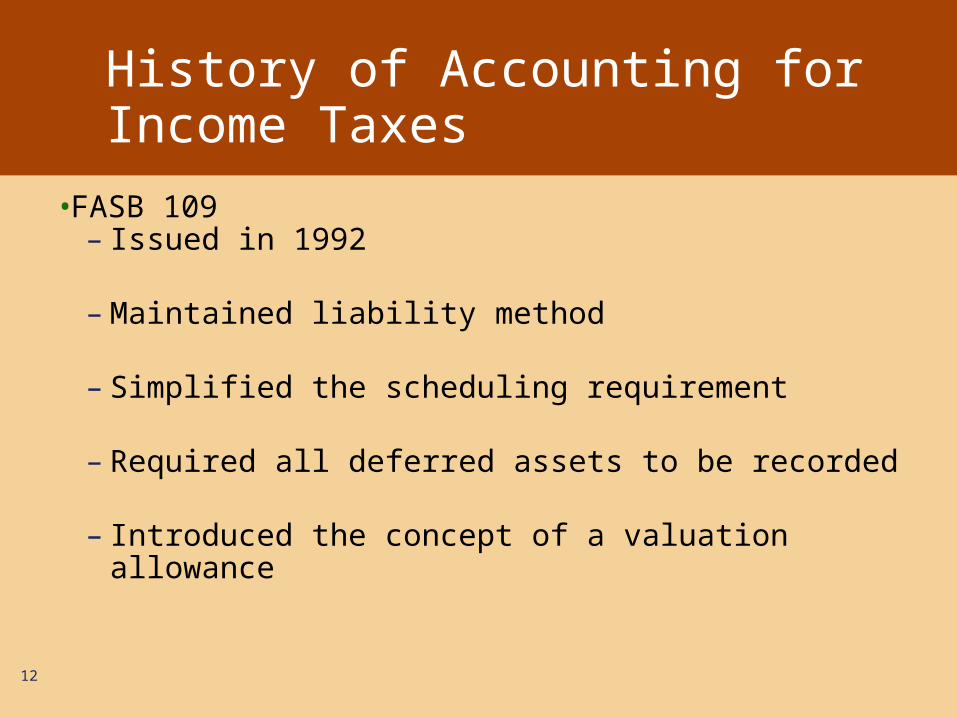

•FASB 109– Issued in 1992

– Maintained liability method

– Simplified the scheduling requirement

– Required all deferred assets to be recorded

– Introduced the concept of a valuation allowance

History of Accounting for Income Taxes

Temporary Differences

13

The difference between the tax basis of an asset or liability and its reported amount in the financial statements that will result in taxable or deductible amounts in future years when the reported amount of the asset or liability is recovered or settled, respectively.

Types of Temporary Differences

14

Taxable Temporary Differences Differences that will result in taxable amounts in future years when the related asset or liability is recovered or settled.

Deductible Temporary DifferencesDifferences that will result in deductible amounts in future years when the related asset or liability is recovered or settled

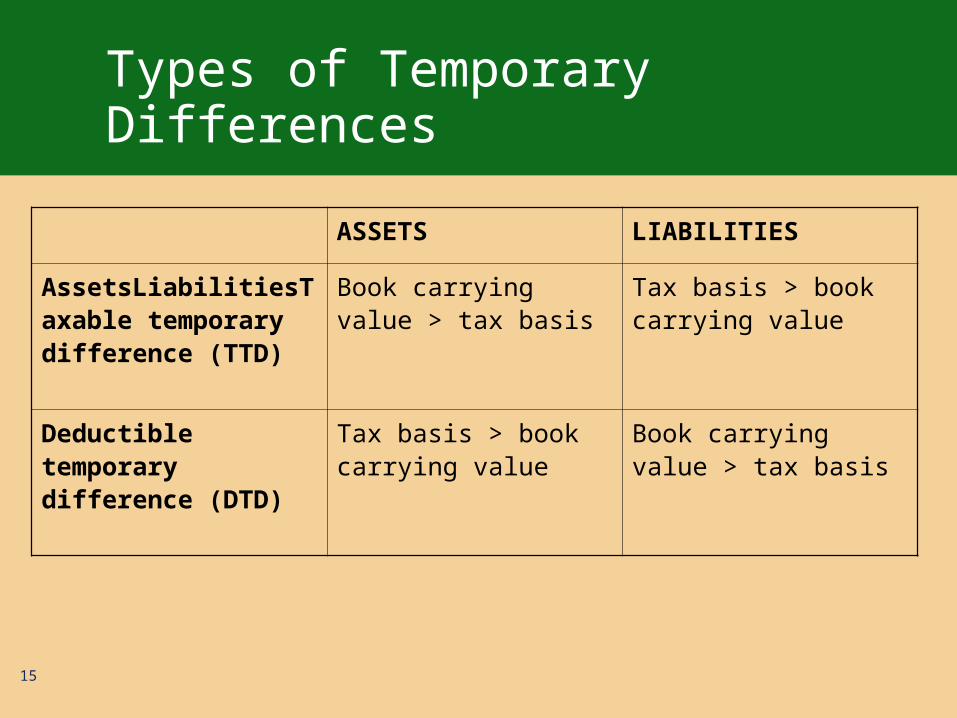

Types of Temporary Differences

ASSETS LIABILITIES

AssetsLiabilitiesTaxable temporary difference (TTD)

Book carrying value > tax basis

Tax basis > book carrying value

Deductible temporary difference (DTD)

Tax basis > book carrying value

Book carrying value > tax basis

15

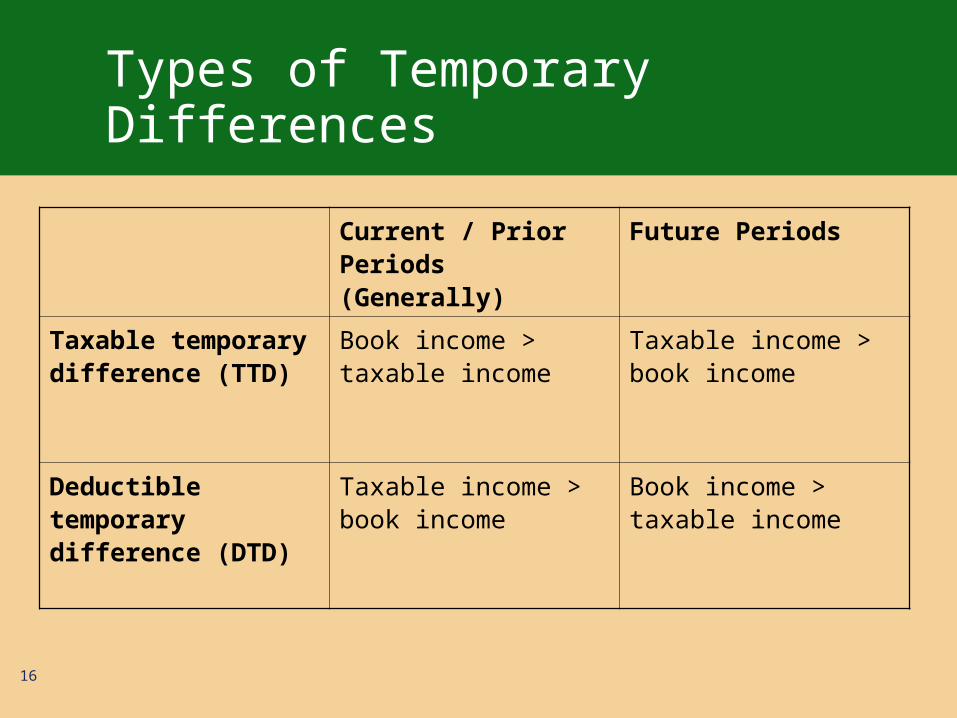

Types of Temporary Differences

Current / Prior Periods (Generally)

Future Periods

Taxable temporary difference (TTD)

Book income > taxable income

Taxable income > book income

Deductible temporary difference (DTD)

Taxable income > book income

Book income > taxable income

16

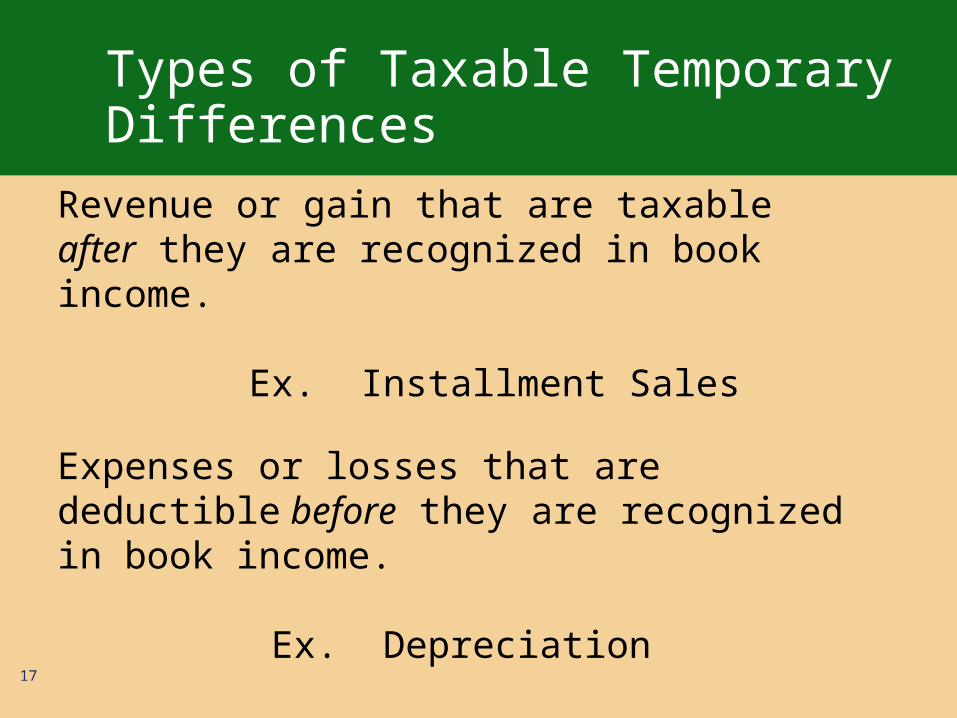

Types of Taxable Temporary Differences

17

Revenue or gain that are taxable after they are recognized in book income.

Ex. Installment Sales

Expenses or losses that are deductible before they are recognized in book income.

Ex. Depreciation

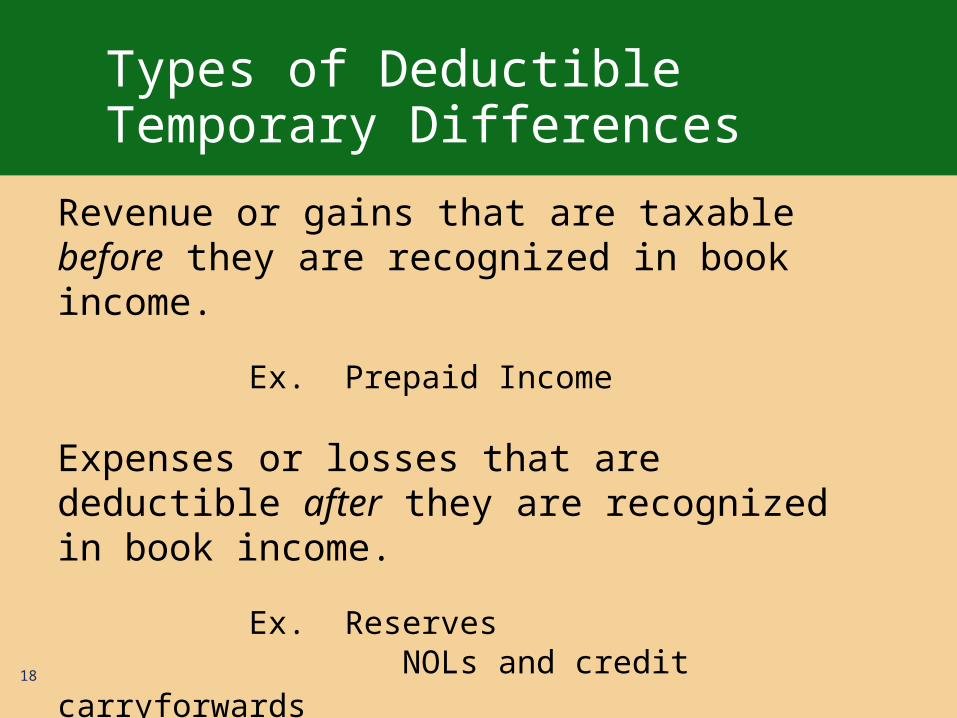

Types of Deductible Temporary Differences

18

Revenue or gains that are taxable before they are recognized in book income.

Ex. Prepaid Income

Expenses or losses that are deductible after they are recognized in book income.

Ex. Reserves

NOLs and credit carryforwards

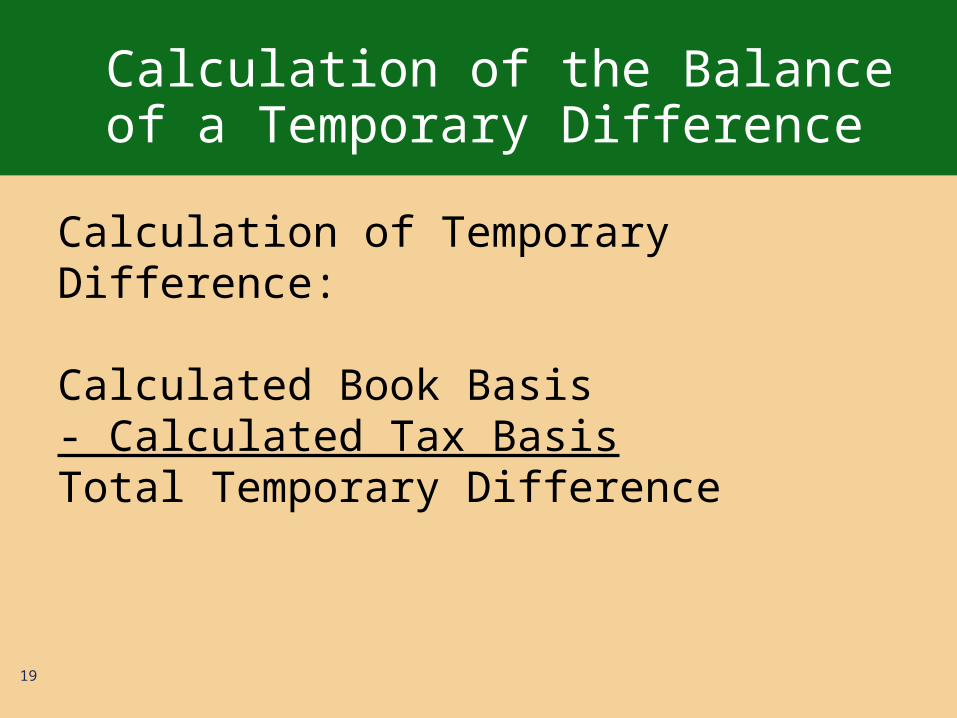

Calculation of the Balance of a Temporary Difference

19

Calculation of Temporary Difference:

Calculated Book Basis- Calculated Tax BasisTotal Temporary Difference

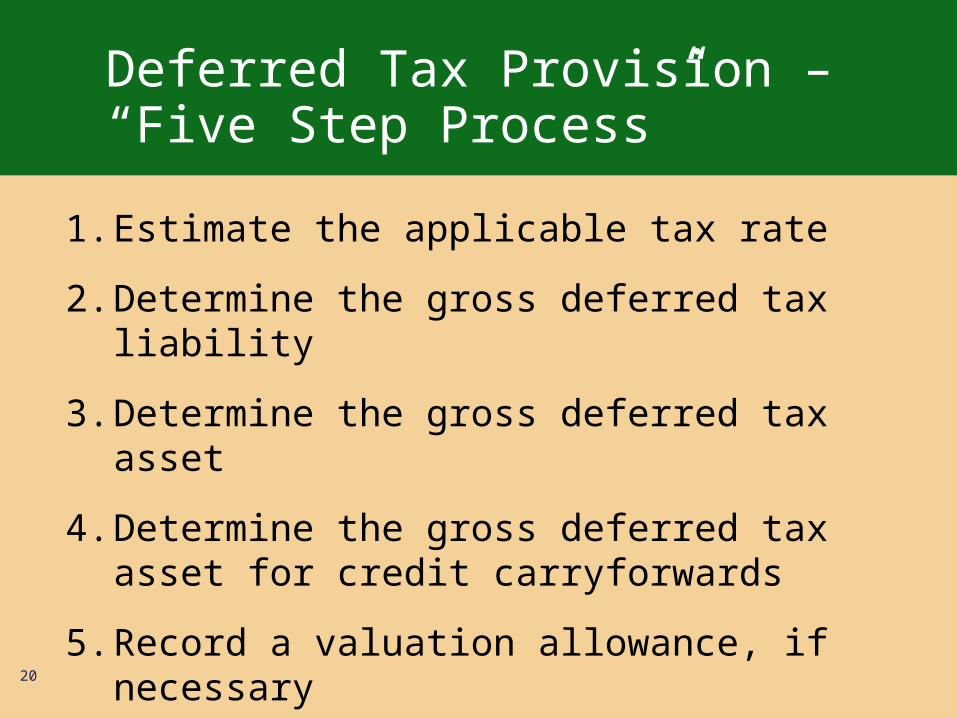

Deferred Tax Provision – “Five Step Process”

20

1. Estimate the applicable tax rate

2. Determine the gross deferred tax liability

3. Determine the gross deferred tax asset

4. Determine the gross deferred tax asset for credit carryforwards

5. Record a valuation allowance, if necessary

Tax Rates Used

•U.S. Federal Income Tax Rate– Regular– AMT

• State Income Taxes– Blended Tax Rate

• Foreign Income Taxes

21

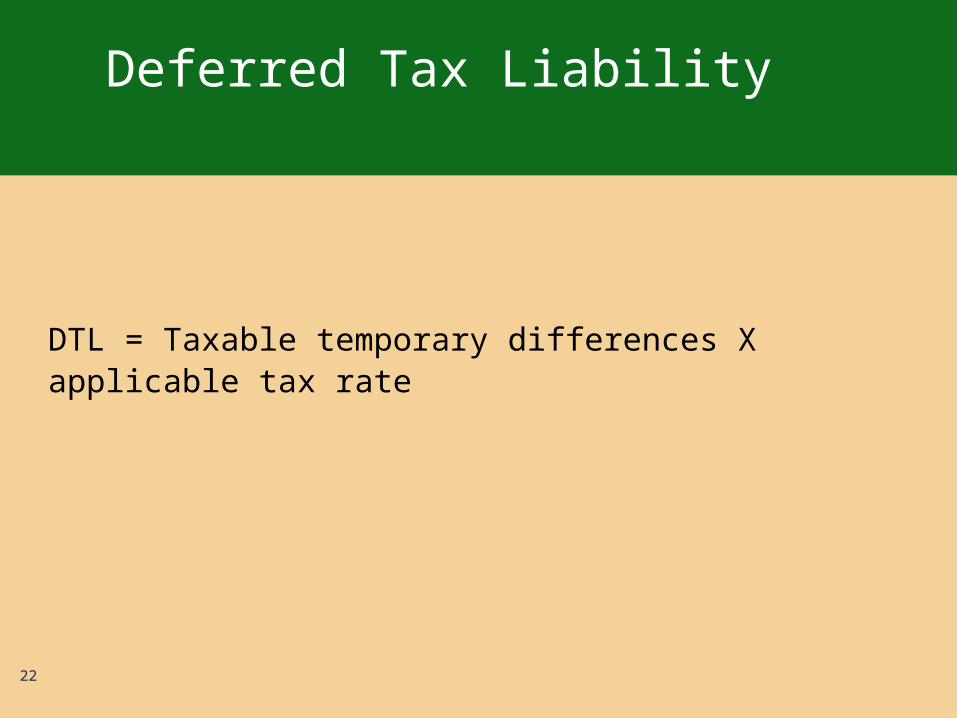

Deferred Tax Liability

DTL = Taxable temporary differences X applicable tax rate

22

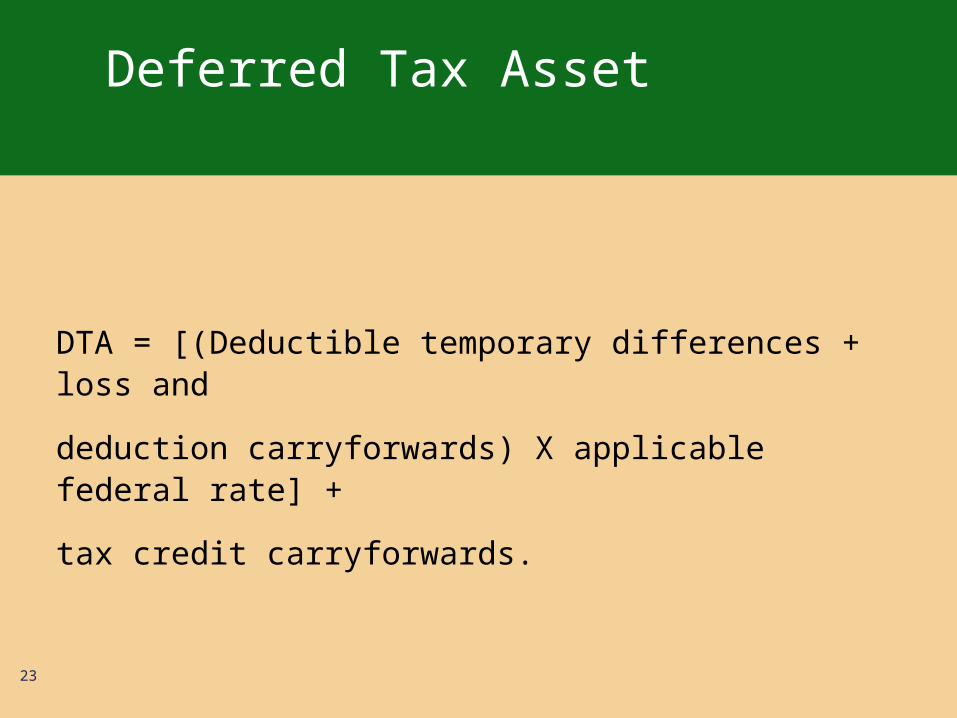

Deferred Tax Asset

DTA = [(Deductible temporary differences + loss and

deduction carryforwards) X applicable federal rate] +

tax credit carryforwards.

23

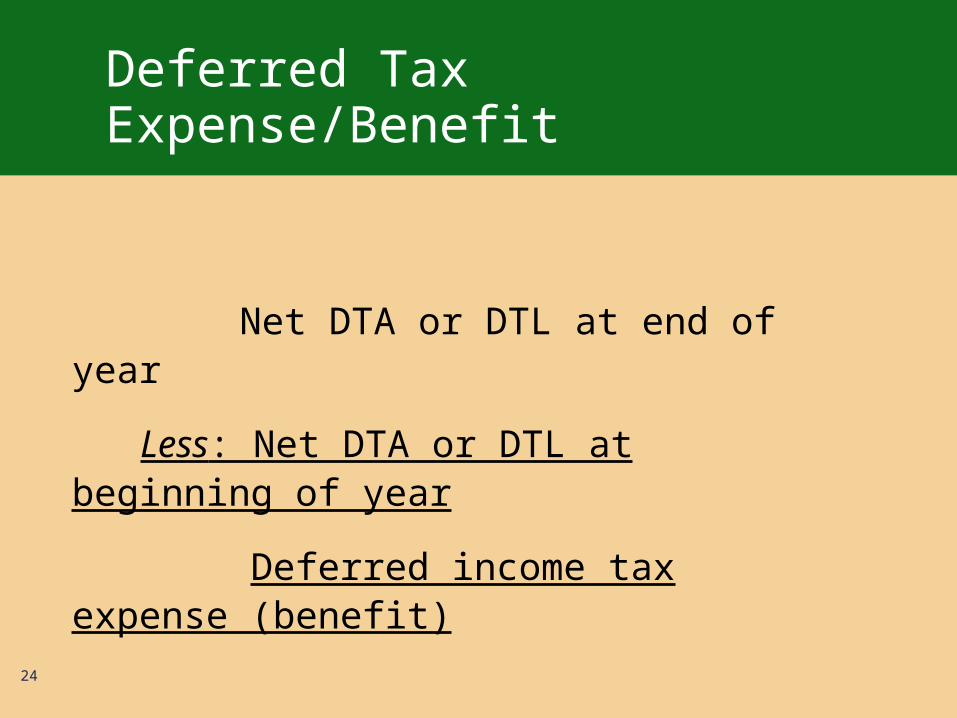

Deferred Tax Expense/Benefit

Net DTA or DTL at end of year

Less: Net DTA or DTL at beginning of year

Deferred income tax expense (benefit)

24

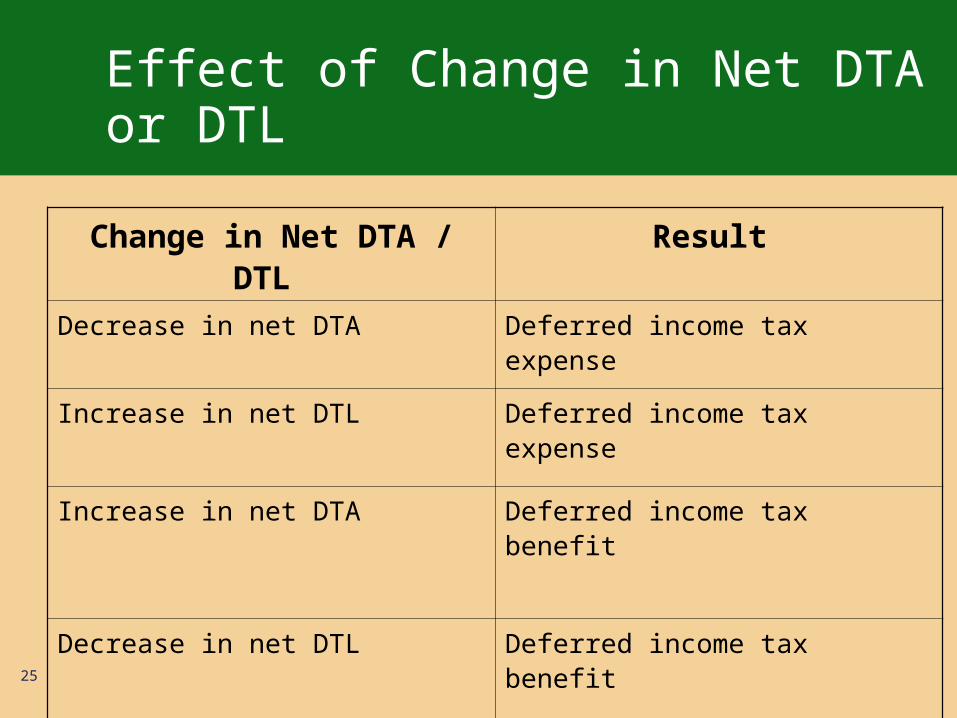

Effect of Change in Net DTA or DTL

Change in Net DTA / DTL Result

Decrease in net DTA Deferred income tax expense

Increase in net DTL Deferred income tax expense

Increase in net DTA Deferred income tax benefit

Decrease in net DTL Deferred income tax benefit

25

Exception to the General Rule

APB 23 – Permanently reinvested earnings in a foreign subsidiary

26

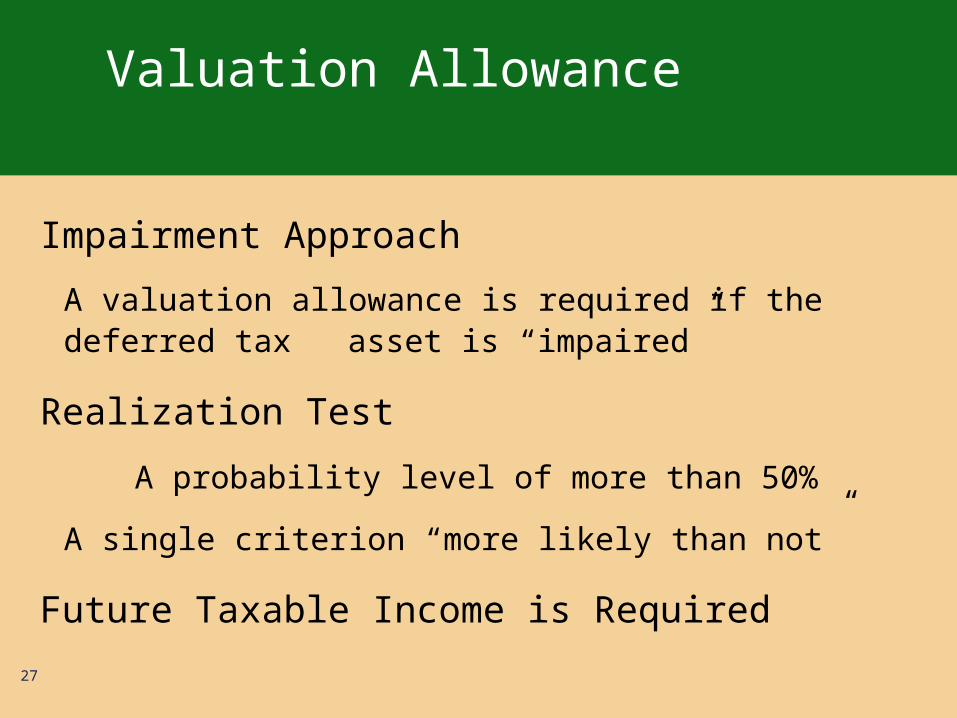

Valuation Allowance

Impairment Approach

A valuation allowance is required if the deferred tax asset is “impaired”

Realization Test

A probability level of more than 50%

A single criterion “more likely than not”

Future Taxable Income is Required

27

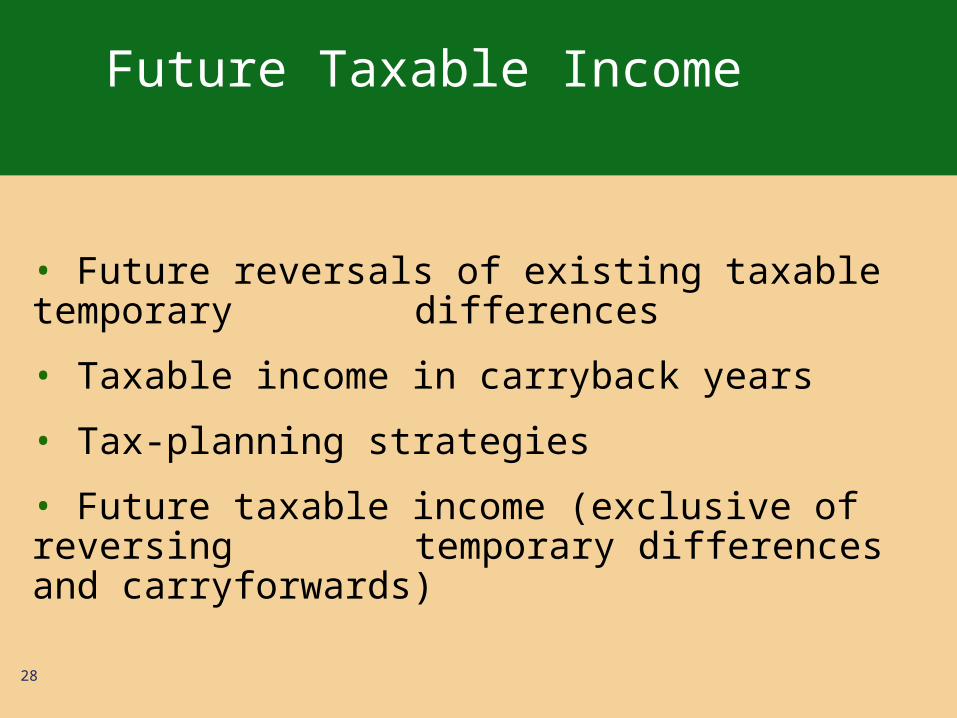

Future Taxable Income

• Future reversals of existing taxable temporary differences

• Taxable income in carryback years

• Tax-planning strategies

• Future taxable income (exclusive of reversing temporary differences and carryforwards)

28

Tax Planning Strategies

Tax-planning strategies will accelerate income so that the company can take advantage of future deductible differences.

Tax-planning strategies must be prudent and feasible.

The company does not have to actually implement the strategy.

29

Tax Planning Strategies

Sale of operating assets

Change of inventory method

Elect out of the installment method

Elect the alternative depreciation system

30

Positive and Negative Evidence

Negative Evidence

• Cumulative losses

• History of expiring tax benefits

• Expectation of future losses

• Unsettled circumstances

• Brief carryback or carryforward period

31

Positive Evidence

• Existing contracts or sales backlog

• Appreciated asset value over tax basis

• Strong earnings history

Valuation Allowance

RECOGNITION OF AN OPERATING LOSS OR ADJUSTMENTS TO BEGINNING-OF-YEAR VALUATION ALLOWANCE

• When incurred - source of loss

• Subsequently– Operations if based on future income– Source of income if based solely on current year

income

32

Valuation Allowance - Change

EFFECT OF A CHANGE IN THE VALUATION ALLOWANCE THAT RESULTS FROM A CHANGE IN CIRCUMSTANCES MUST BE INCLUDED IN INCOME FROM CONTINUING OPERATIONS.

33

Valuation Allowance - Change

CHANGE IN JUDGMENT ABOUT REALIZABILITY

• Affects Current Quarter If For Future Years

• Affects Remaining Interim Periods If For Future Interim Periods

34

Valuation Allowance – Change at Interim Date

DECREASE IN VALUATION ALLOWANCE IS SEGREGATED INTO TWO COMPONENTS

• Portion related to a change in estimate regarding the current year's income– Taken into income by prospectively adjusting effective

tax rate for current year

• Portion related to a change in estimate about future years' income– Taken into income as a discrete event in the quarter of

the change in estimate

35

Tax Effect of a Change in Tax Law

MEASURED AND RECORDED ON THE ENACTMENT DATE

– May be necessary to estimate temporary difference at interim dates

RETROACTIVE APPLICATION - EITF ISSUE 93-13– Impact on disc. operations, extraordinary and

cumulative effect items

REQUIRED DISCLOSURES

36

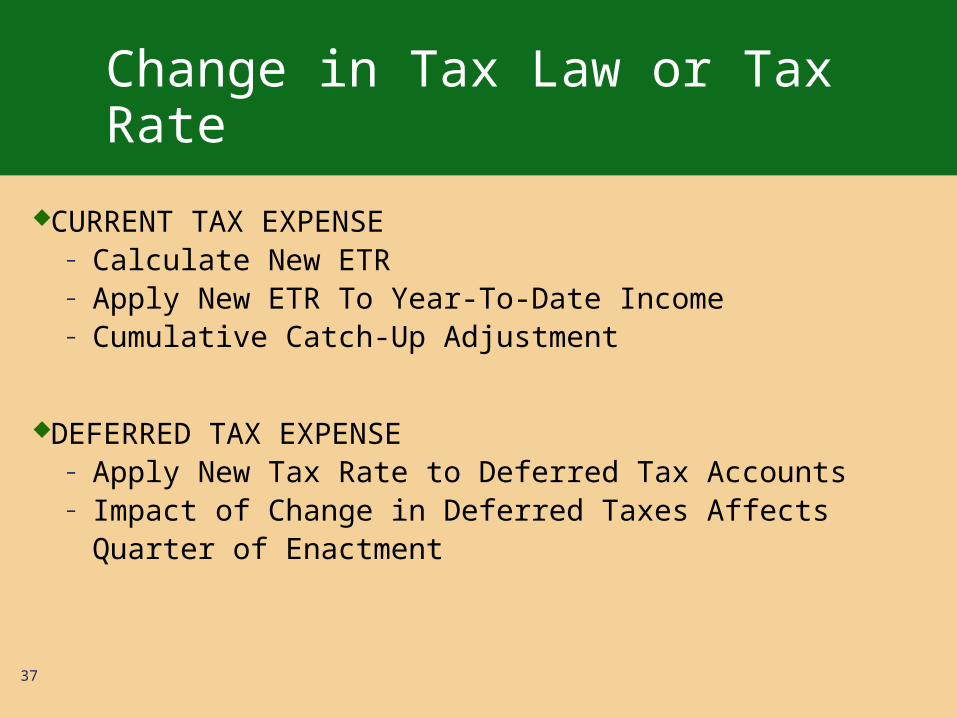

Change in Tax Law or Tax Rate

CURRENT TAX EXPENSE– Calculate New ETR– Apply New ETR To Year-To-Date Income– Cumulative Catch-Up Adjustment

DEFERRED TAX EXPENSE– Apply New Tax Rate to Deferred Tax Accounts– Impact of Change in Deferred Taxes Affects Quarter of

Enactment

37

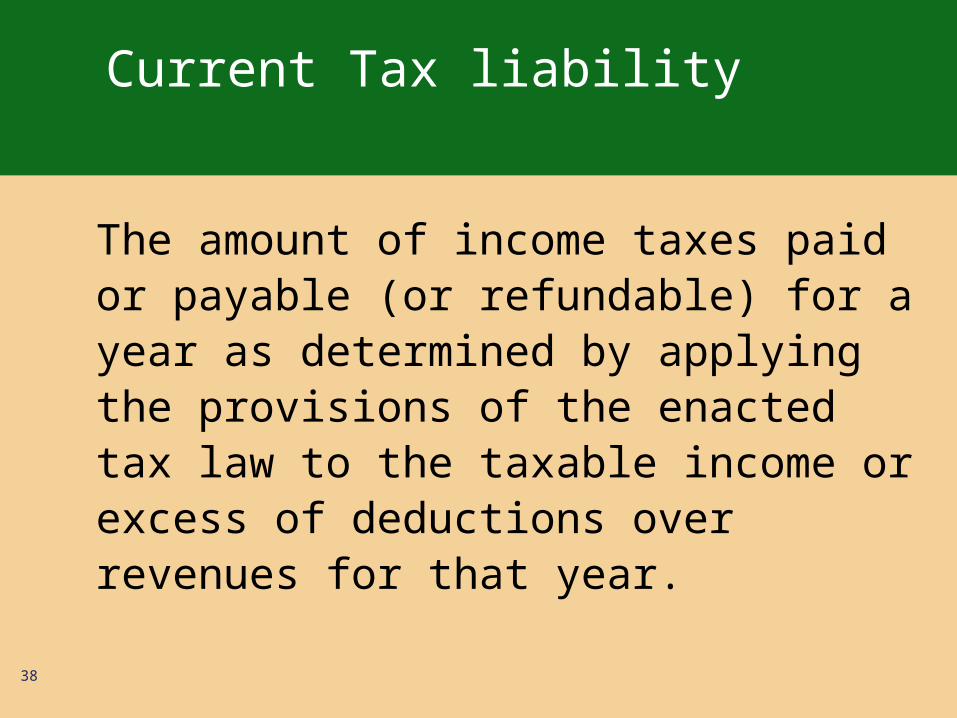

Current Tax liability

The amount of income taxes paid or payable (or refundable) for a year as determined by applying the provisions of the enacted tax law to the taxable income or excess of deductions over revenues for that year.

38

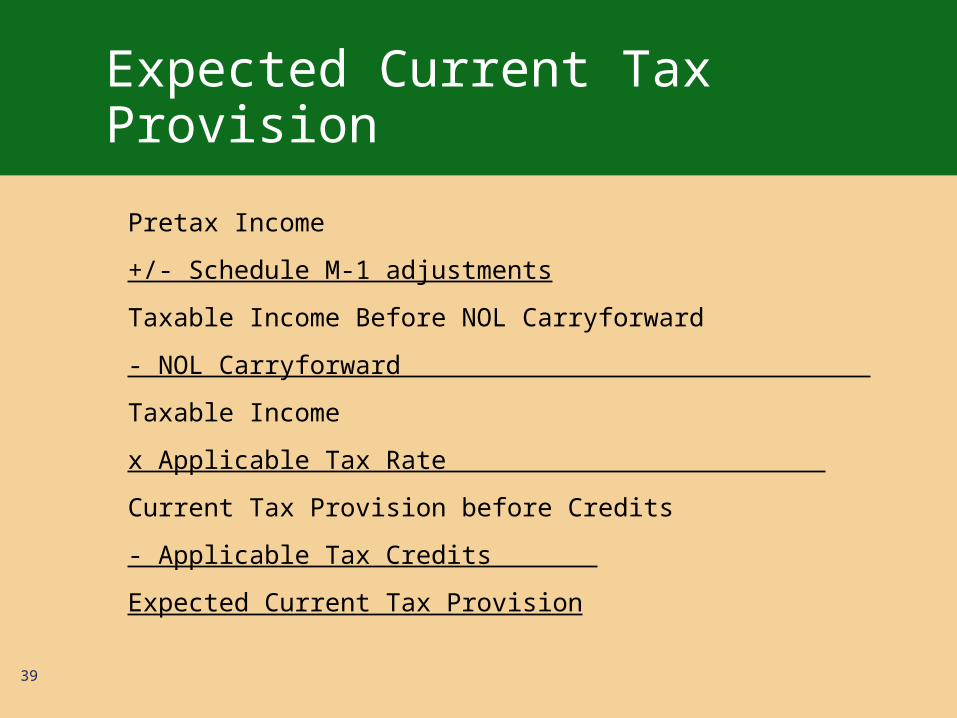

Expected Current Tax Provision

Pretax Income

+/- Schedule M-1 adjustments

Taxable Income Before NOL Carryforward

- NOL Carryforward

Taxable Income

x Applicable Tax Rate

Current Tax Provision before Credits

- Applicable Tax Credits

Expected Current Tax Provision39

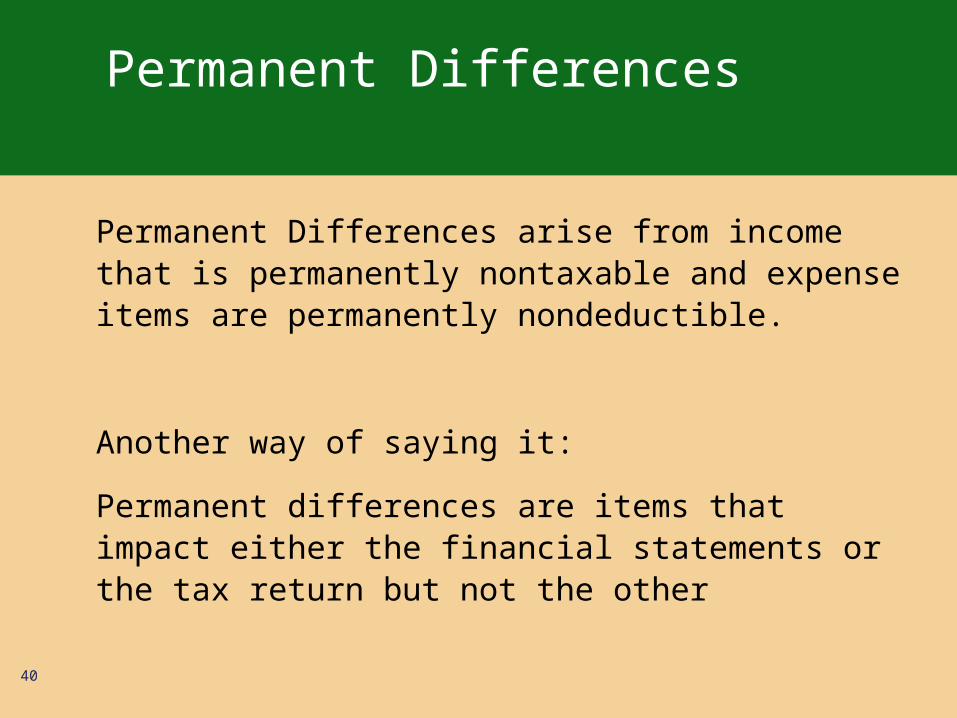

Permanent Differences

Permanent Differences arise from income that is permanently nontaxable and expense items are permanently nondeductible.

Another way of saying it:

Permanent differences are items that impact either the financial statements or the tax return but not the other

40

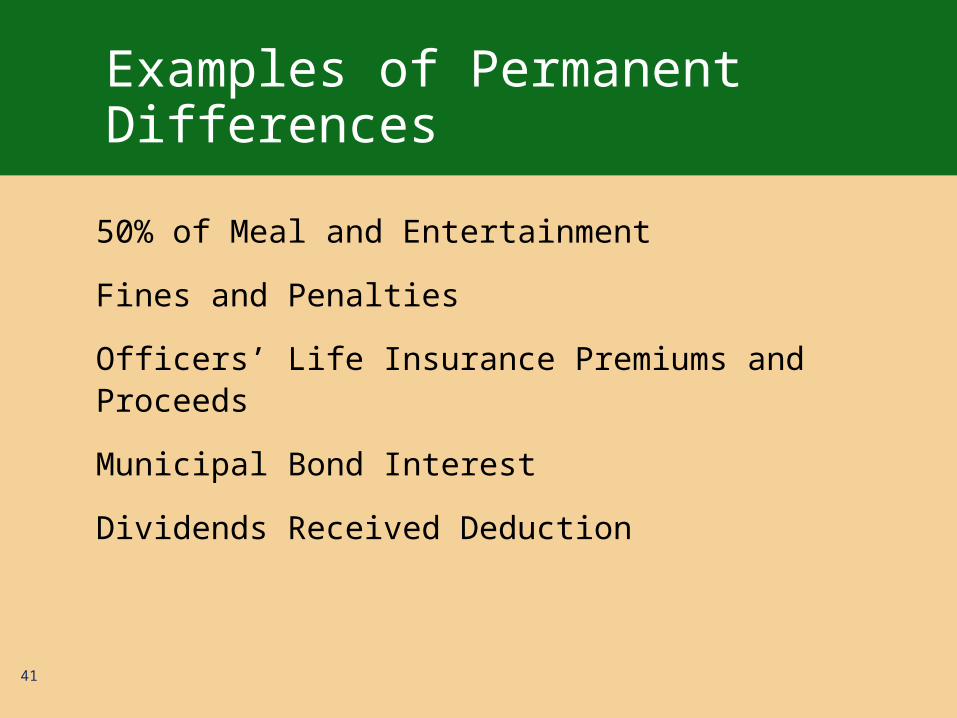

Examples of Permanent Differences

50% of Meal and Entertainment

Fines and Penalties

Officers’ Life Insurance Premiums and Proceeds

Municipal Bond Interest

Dividends Received Deduction

41

Cases

42

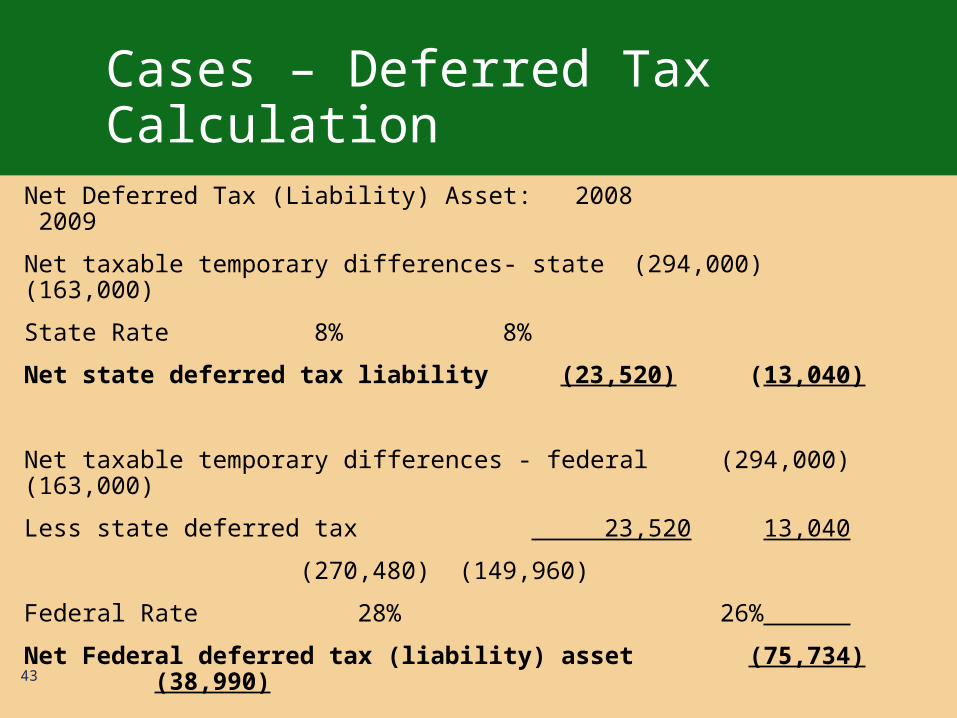

Cases – Deferred Tax Calculation

Net Deferred Tax (Liability) Asset: 2008 2009

Net taxable temporary differences- state (294,000) (163,000)

State Rate 8% 8%

Net state deferred tax liability (23,520) (13,040)

Net taxable temporary differences - federal (294,000) (163,000)

Less state deferred tax 23,520 13,040

(270,480) (149,960)

Federal Rate 28% 26%

Net Federal deferred tax (liability) asset (75,734) (38,990)43

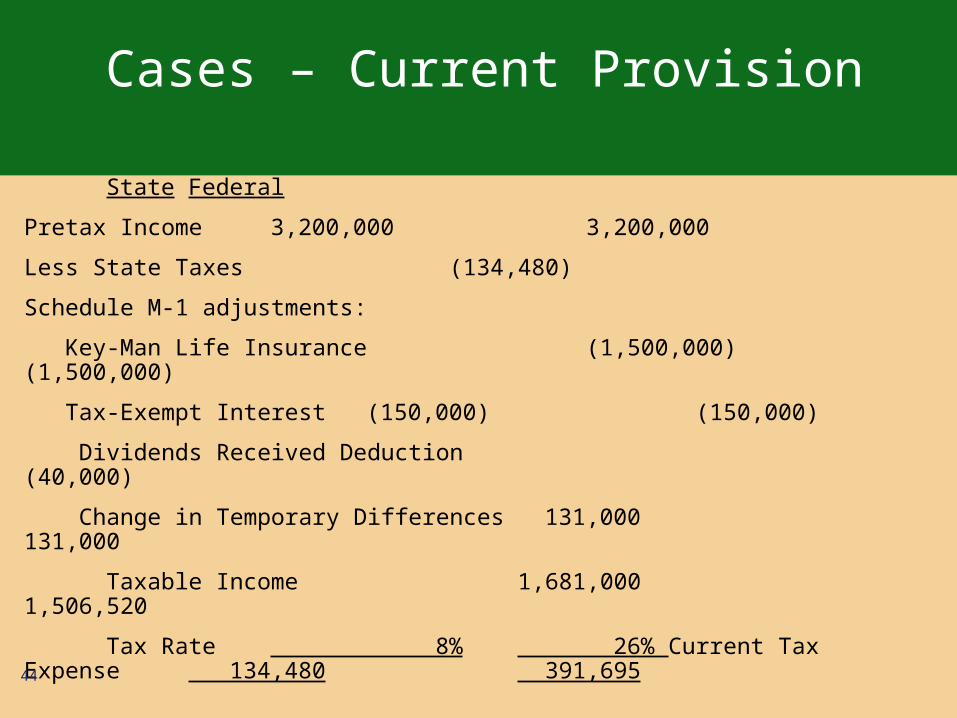

Cases – Current Provision

State Federal

Pretax Income 3,200,000 3,200,000

Less State Taxes (134,480)

Schedule M-1 adjustments:

Key-Man Life Insurance (1,500,000) (1,500,000)

Tax-Exempt Interest (150,000) (150,000)

Dividends Received Deduction (40,000)

Change in Temporary Differences 131,000 131,000

Taxable Income 1,681,000 1,506,520

Tax Rate 8% 26% Current Tax Expense 134,480 391,69544

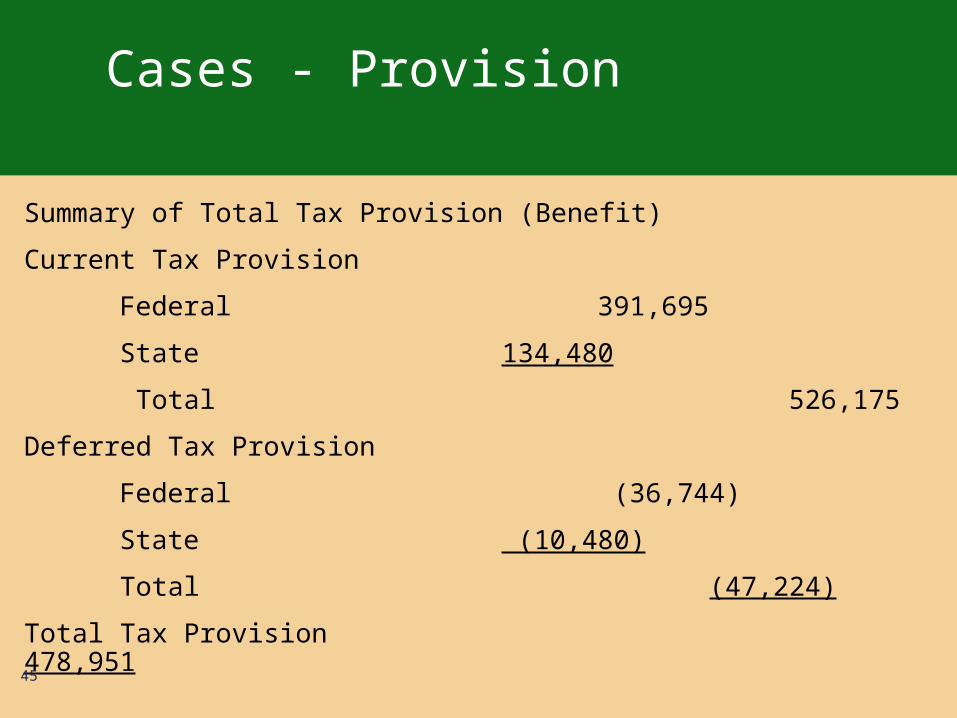

Cases - Provision

Summary of Total Tax Provision (Benefit)

Current Tax Provision

Federal 391,695

State 134,480

Total 526,175

Deferred Tax Provision

Federal (36,744)

State (10,480)

Total (47,224)

Total Tax Provision 478,951

45

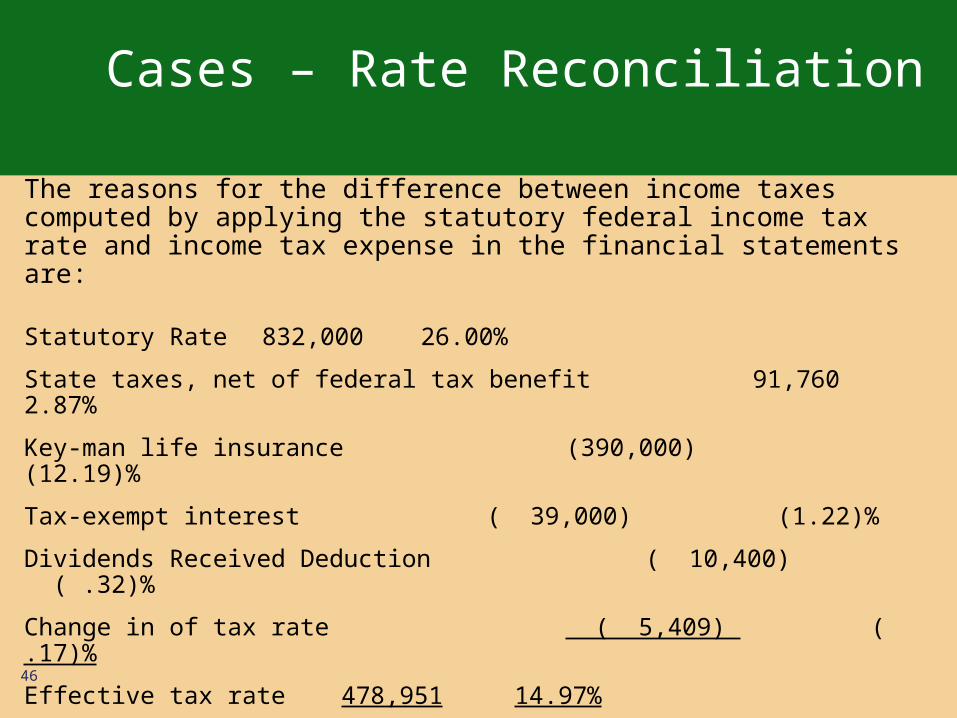

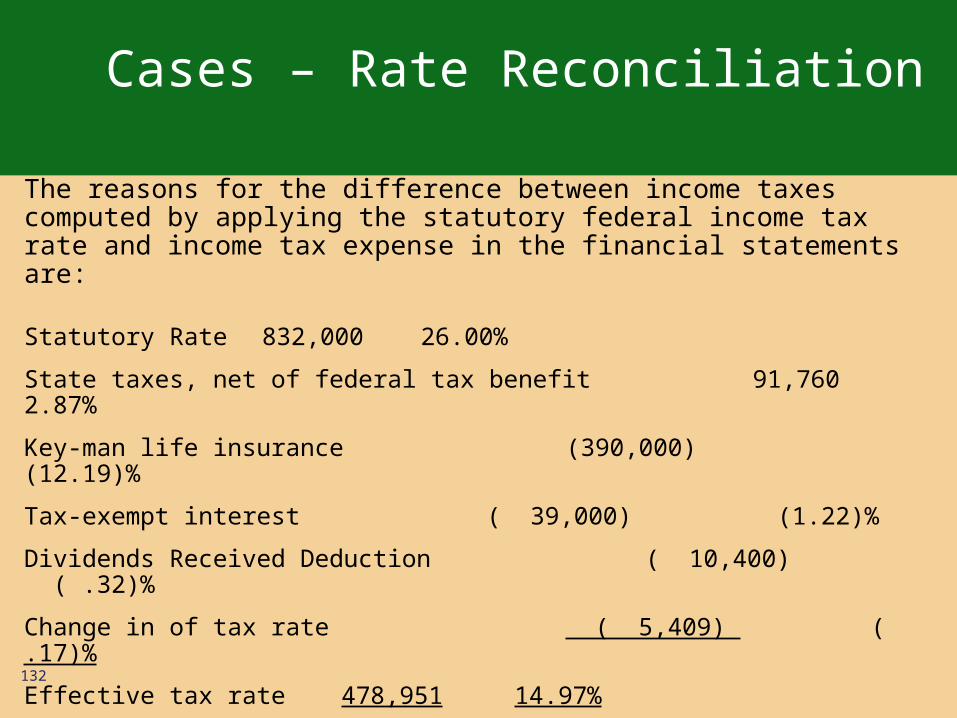

Cases – Rate Reconciliation

The reasons for the difference between income taxes computed by applying the statutory federal income tax rate and income tax expense in the financial statements are:

Statutory Rate 832,000 26.00%

State taxes, net of federal tax benefit 91,760 2.87%

Key-man life insurance (390,000) (12.19)%

Tax-exempt interest ( 39,000) (1.22)%

Dividends Received Deduction ( 10,400) ( .32)%

Change in of tax rate ( 5,409) ( .17)%

Effective tax rate 478,951 14.97%46

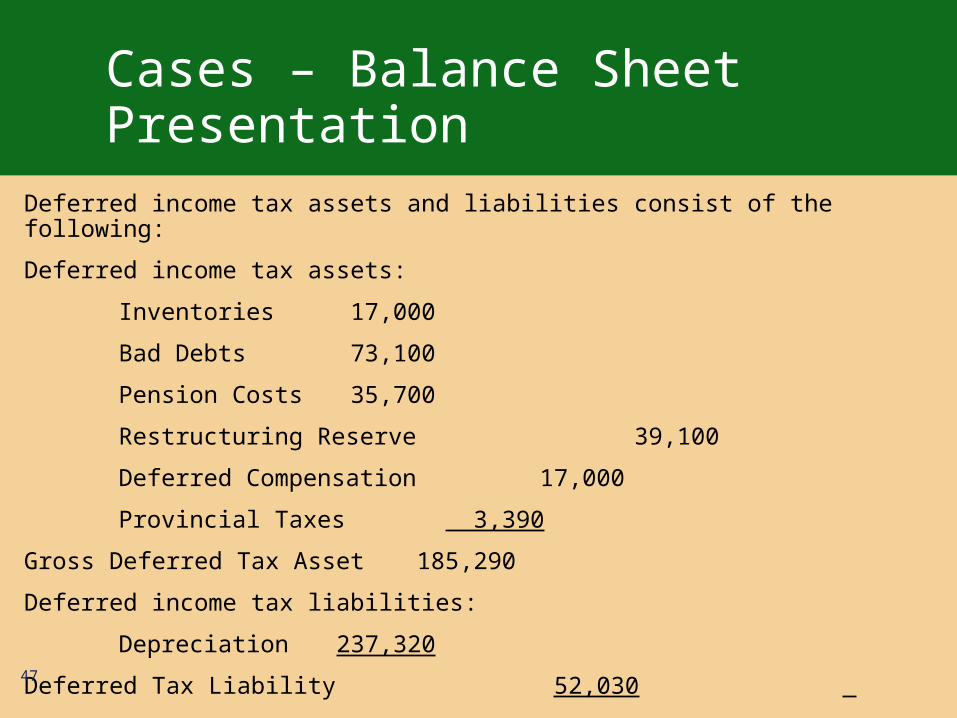

Cases – Balance Sheet Presentation

Deferred income tax assets and liabilities consist of the following:

Deferred income tax assets:

Inventories 17,000

Bad Debts 73,100

Pension Costs 35,700

Restructuring Reserve 39,100

Deferred Compensation 17,000

Provincial Taxes 3,390

Gross Deferred Tax Asset 185,290

Deferred income tax liabilities:

Depreciation 237,320

Deferred Tax Liability 52,030 47

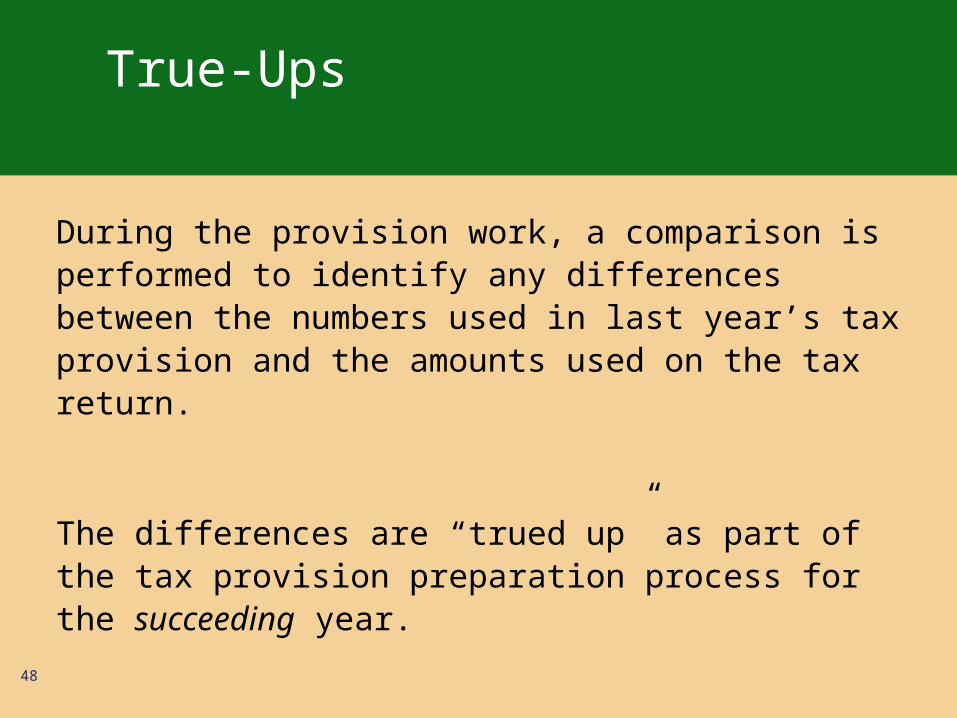

True-Ups

During the provision work, a comparison is performed to identify any differences between the numbers used in last year’s tax provision and the amounts used on the tax return.

The differences are “trued up” as part of the tax provision preparation process for the succeeding year.

48

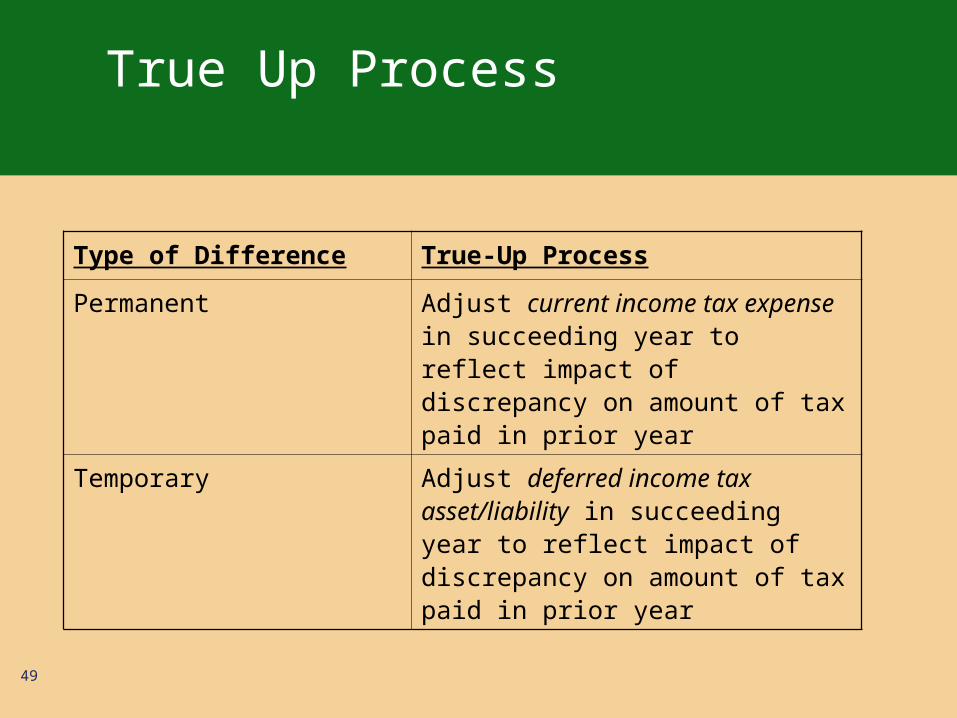

True Up Process

Type of Difference True-Up Process

Permanent Adjust current income tax expense in succeeding year to reflect impact of discrepancy on amount of tax paid in prior year

Temporary Adjust deferred income tax asset/liability in succeeding year to reflect impact of discrepancy on amount of tax paid in prior year

49

True Up Process

Temporary Difference

End of Year 20X1

True Up Beginning Year 20X2

50

True Up Process - Example

51

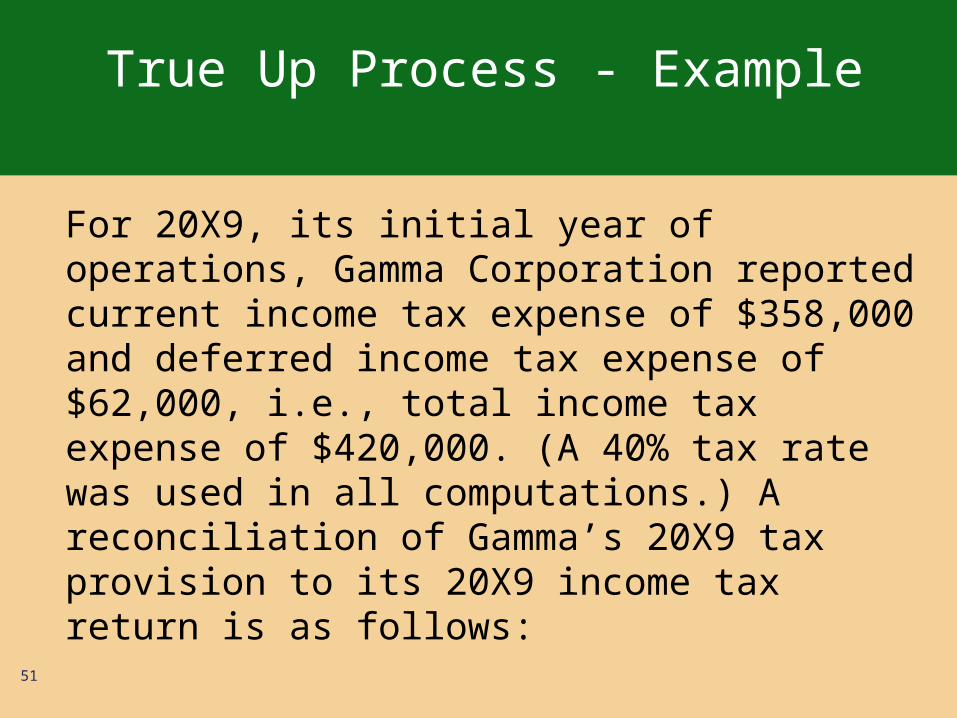

For 20X9, its initial year of operations, Gamma Corporation reported current income tax expense of $358,000 and deferred income tax expense of $62,000, i.e., total income tax expense of $420,000. (A 40% tax rate was used in all computations.) A reconciliation of Gamma’s 20X9 tax provision to its 20X9 income tax return is as follows:

True Up Process - Example

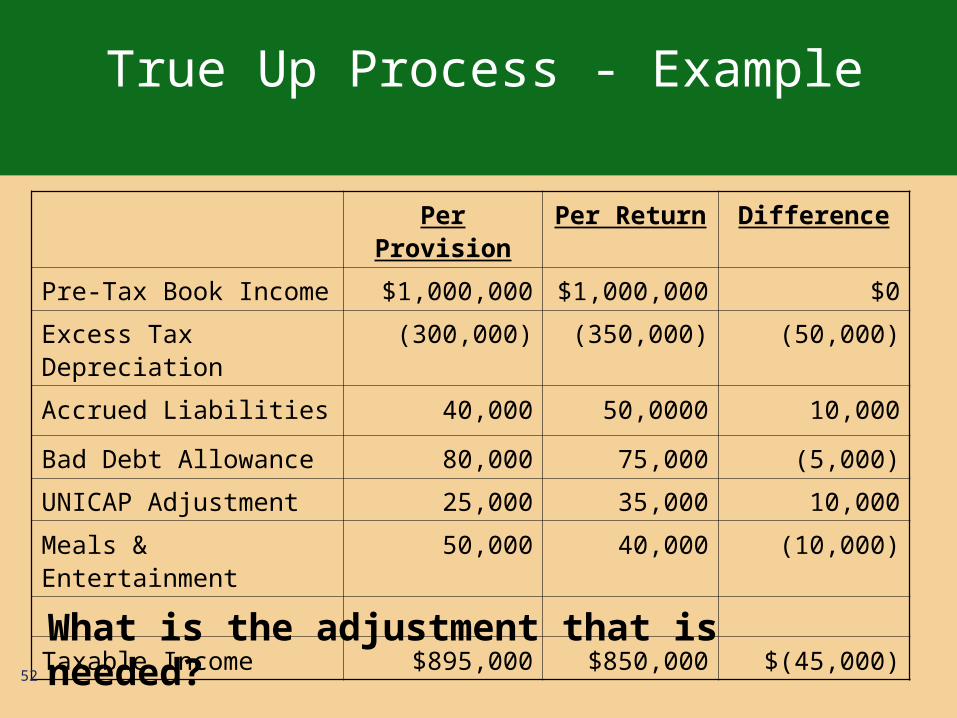

Per Provision Per Return Difference

Pre-Tax Book Income $1,000,000 $1,000,000 $0

Excess Tax Depreciation (300,000) (350,000) (50,000)

Accrued Liabilities 40,000 50,0000 10,000

Bad Debt Allowance 80,000 75,000 (5,000)

UNICAP Adjustment 25,000 35,000 10,000

Meals & Entertainment 50,000 40,000 (10,000)

Taxable Income $895,000 $850,000 $(45,000)

52

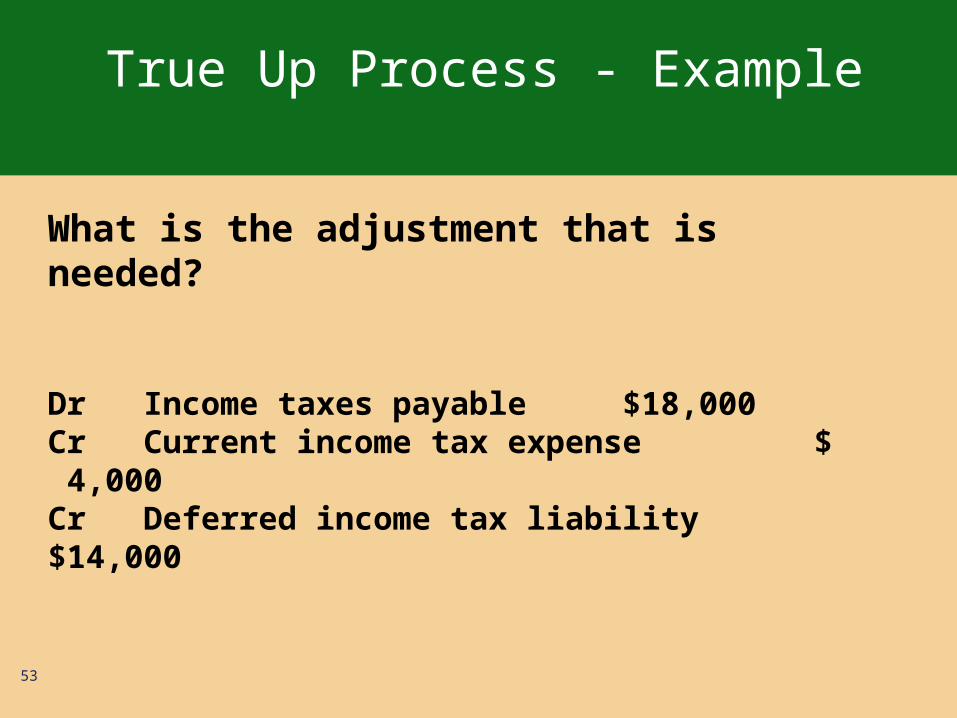

What is the adjustment that is needed?

True Up Process - Example

53

What is the adjustment that is needed?

Dr Income taxes payable $18,000Cr Current income tax expense $ 4,000Cr Deferred income tax liability $14,000

Uncertain Tax Positions

54

Tax issues created the most problems found under Sarbanes-Oxley and 404

Numerous restatements were required because of the tax provision

In response FASB undertook a project to govern how uncertain tax positions would be reported

Former Practices

55

Tax Contingencies or cushion were hid and not disclosed in detail

Tax Directors were very proprietary with the calculation and were reluctant to discuss with the auditors

Concern that if the information was included in the audit workpapers the IRS would have access to them

Former Practices

56

Tax Contingencies are reported using either:

“Loss Contingency” approach – SFAS 5“Best Estimate” approach – 50/50 “Tax Advantaged Transaction” approach – reverse SFAS 5

Former Practices

57

Had to use a consistent approach

The likelihood of a taxing authority discovering the issue on examination should not be considered

Support for each reserve amount and any change was required

FASB’s Concerns

58

Diversity of reporting of tax contingencies

Felt the standards needed strengthening

Use of tax contingencies had become too flexible and used to manipulate income

Reporting and disclosure lacked transparency

SEC’s Position

59

SEC also concerned about the reporting of tax contingencies

Many SEC letters were been issued on this matter in the 6 to 9 months prior to the issuance of FIN 48 (ASC 740-10)

Dealing with the SEC very different than FASB and IRS

FIN 48 (ASC 740-10)

60

Released July 13, 2006

“Benefit Recognition” Approach

“More likely than not” threshold

“Cumulative Probability”

Objectives of FIN 48 (ASC 740-10)

61

Clarify accounting for income taxes

Provide greater consistency in criteria used to recognize, derecognize, and measure benefits related to income taxes

Establish consistent thresholds, thereby improving relevance and comparability of financial statement reporting

Scope of FIN 48 (ASC 740-10)

62

Applies to all income tax positions

A tax position is defined as a position taken in a previously filed return or expected to be taken in a future return

A position can result in a permanent reduction of taxes (permanent differences), a deferral of taxes (temporary differences), or a change in the expected realizability of deferred tax assets

FIN 48 also encompasses decisions not to file an income tax return, jurisdictional allocations (i.e., transfer pricing) and characterization of income

FIN 48 (ASC 740-10)

63

Recognition criteria focuses primarily on technical tax law

“Widely understood” administrative procedures considered

Each position assessed separately

Detection risk not considered

Highly Certain Tax Positions

64

• FIN 48 applies to all income tax positionsDistinguishes between “highly certain” and “uncertain” tax positions

Highly certain tax positions Clearly meets the MLTN recognition standard and greater than 50% likely that 100% of benefit will be sustained based on clear and unambiguous tax law

FIN 48 (ASC 740-10)

65

Introduces concept of “Unit of Account”

Based on facts and circumstances• Aggregate or• Separate each project

Unit of Account

66

The appropriate unit of account for a tax position is a matter of judgment and requires consideration of

• The manner in which the enterprise prepares and supports its income tax return, and• The approach the enterprise anticipates the taxing authority will take during an examination

Once established, should be consistently applied to similar positions from period to period unless change in facts and circumstances indicates that a different unit of account is more appropriate

Two Step Process

67

The application of FIN 48 to an uncertain tax position (UTP) requires a two-step process that separates recognition from measurement

Step 1: Recognition Threshold

Step 2: Measurement of the Benefit

Step 1: Initial Recognition

68

A tax benefit is recognized when it is “more likely than not” to be sustained based on the technical merits of the position

• Conclusion regarding financial statement recognition takes into account technical merits and facts and circumstances

• Assumes that tax position will be examined by the taxing authority

• Each position must stand on its own merits

• Administrative practices and precedents deal with limited technical violations of the tax law

• Authority will not take issue with the tax position• Broad understanding in practice

Step 2: Measurement

69

A tax position that meets the MLTN recognition threshold shall initially and subsequently be measured as the largest amount of tax benefit that is greater than 50% likely of being realized (cumulative probability concept)

• Based upon facts and circumstances determined at the reporting date

Step 2: Measurement

70

Differences related to timing (deduction itself is not in question)

• Recognition threshold is achieved

Not all tax positions require detailed consideration of possible outcome amounts and percentage likelihood associated with each amount (cumulative probability approach)

Example – Step 1

71

A company takes a deduction that creates a tax benefit of $100. How likely of being sustained on technical merit must the deduction be before the company can record the benefit?

Under the first step the position must be more than 50% likely of being sustained on its technical merit to take the benefit. The amount that should be recognized will depend on the cumulative probability in the second step.

Example – Step 2

72

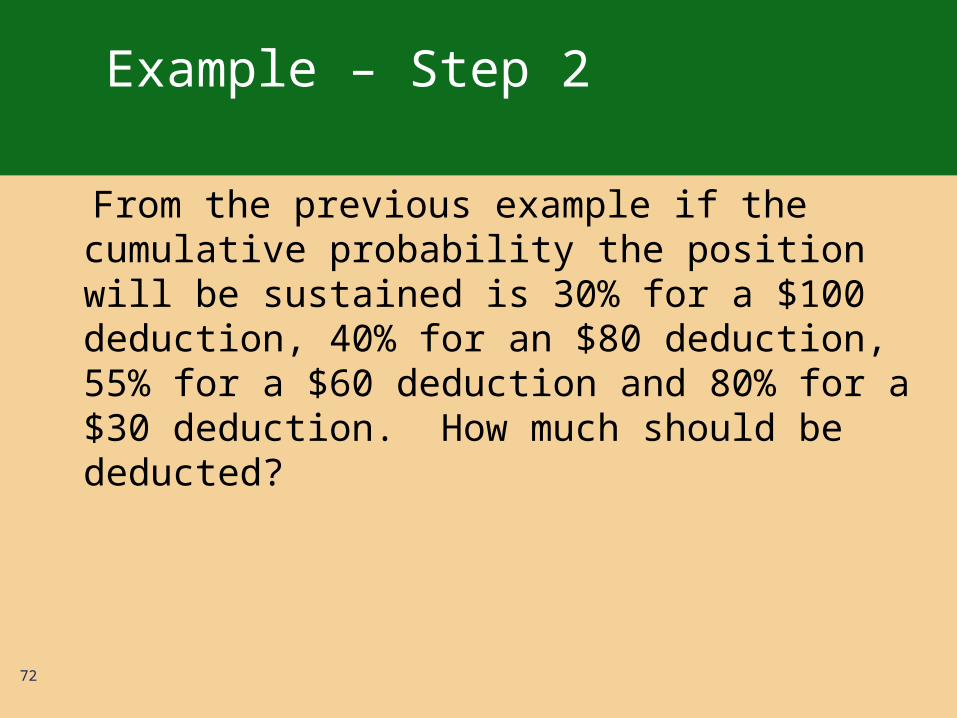

From the previous example if the cumulative probability the position will be sustained is 30% for a $100 deduction, 40% for an $80 deduction, 55% for a $60 deduction and 80% for a $30 deduction. How much should be deducted?

Example – Step 2

73

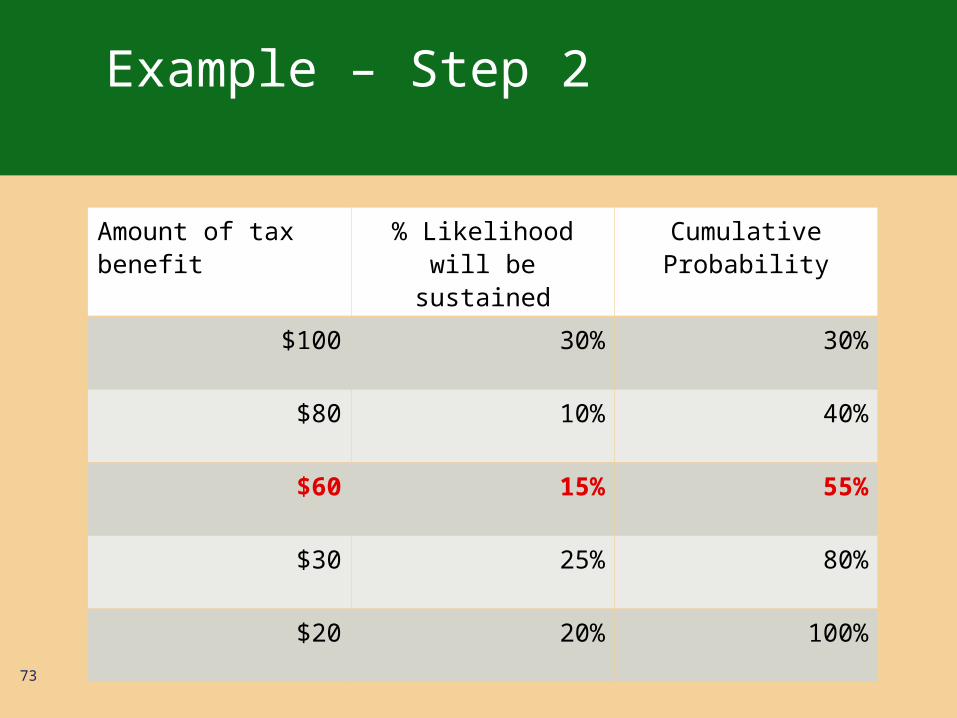

Amount of tax benefit % Likelihood will be sustained

Cumulative Probability

$100 30% 30%

$80 10% 40%

$60 15% 55%

$30 25% 80%

$20 20% 100%

Change in Judgment

74

Subsequent recognition, derecognition or change in measurement

• Requires new information vs. new evaluation

•Reporting date vs. financial statement issuance date

•Change from rules under FAS 5

Subsequent Recognition

75

Subsequent recognition occurs when any of the following conditions are met:

• The MLTN threshold is met by the reporting date

• The tax matter is effectively settled through examination, negotiation or litigation

• The statute of limitations expires

Subsequent Recognition

76

Applies to those positions not initially recognized

“Effectively settled” defined• Taxing authority completed all exam procedures

• No appeal or litigation is intended

• Enterprise considers it remote that the tax position would be subsequently examined or reexamined

• Presume taxing authority has full knowledge of all relevant information

Sources of New Information

77

• Developments in the audit

• Revenue Agent’s report

• Changes in the law

• Notice of Proposed Adjustment

• Experience in prior audits

• APA

• Taxing authority program changes

• Public statements by tax authority

Balance Sheet Presentation

78

Tax contingencies should be included in the current income tax payable for amounts expected to be paid within 12 months.

Amounts that are expected to be paid after 12 months should be in a long-term payable.

FIN 48 does not allow tax contingencies to be part of the deferred tax accounts or the valuation allowance.

Effective Date

79

FIN 48 applies to annual periods beginning after December 15, 2006 for public companies;

Effective for annual periods beginning after December 15, 2008 for private companies

Same rules apply for public and nonpublic companies

One-time disclosure of cumulative effect

Cumulative Effect

80

The cumulative effect of the change in net assets requires an adjustment to beginning retained earnings. If the adjustment relates to a business combination, the effect requires an adjustment to goodwill.

Disclosure Requirements

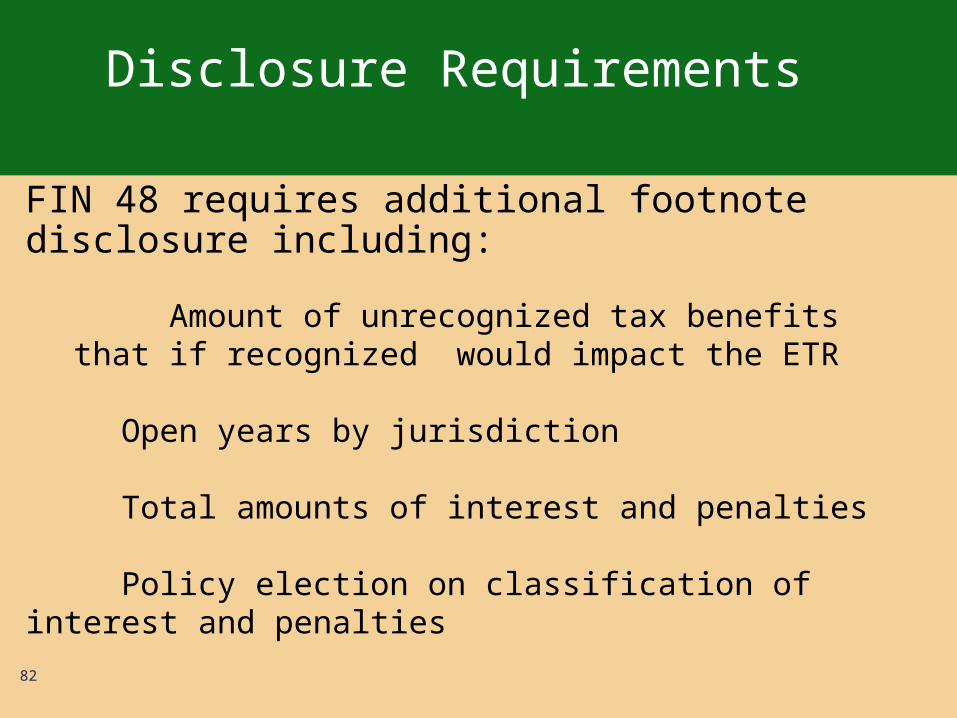

81

FIN 48 requires additional footnote disclosure including:

• An annual reconciliation of “unrecognized tax benefits” on an aggregated world-wise basis

• Gross amount of increases or decreases relating to prior period positions

• Gross amount of increases or decreases relating to the current period

• Amounts of decreases relating to settlements with taxing authorities

• Reductions due to expiration of statute of limitations

Disclosure Requirements

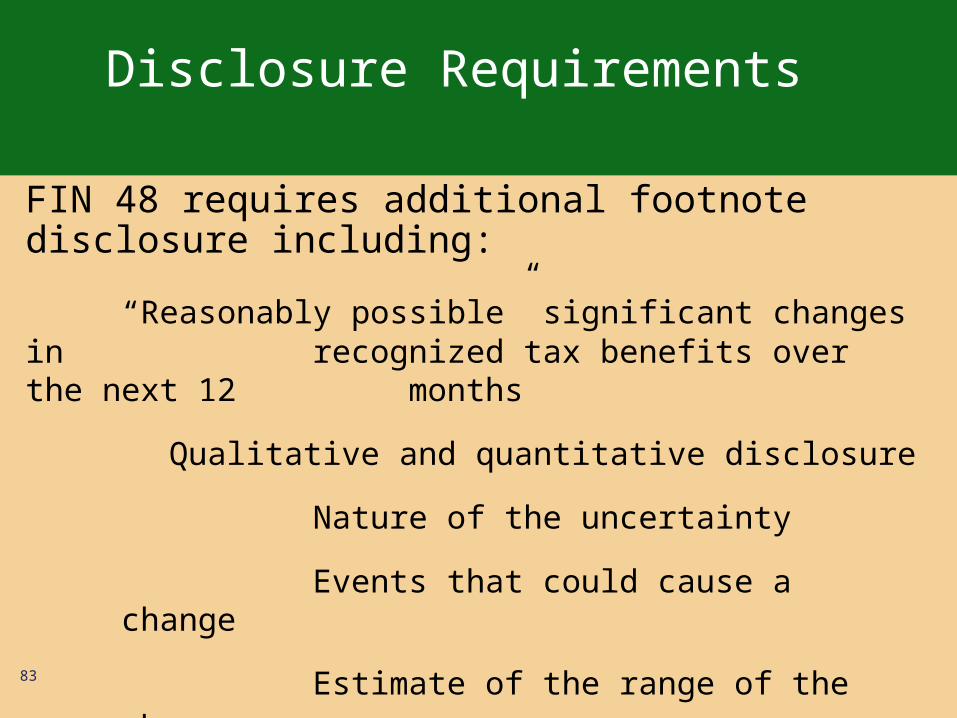

82

FIN 48 requires additional footnote disclosure including:

Amount of unrecognized tax benefits that if recognized would impact the ETR

Open years by jurisdiction

Total amounts of interest and penalties

Policy election on classification of interest and penalties

Disclosure Requirements

83

FIN 48 requires additional footnote disclosure including:

“Reasonably possible” significant changes in recognized tax benefits over the next 12

months

Qualitative and quantitative disclosure

Nature of the uncertainty

Events that could cause a change

Estimate of the range of the change

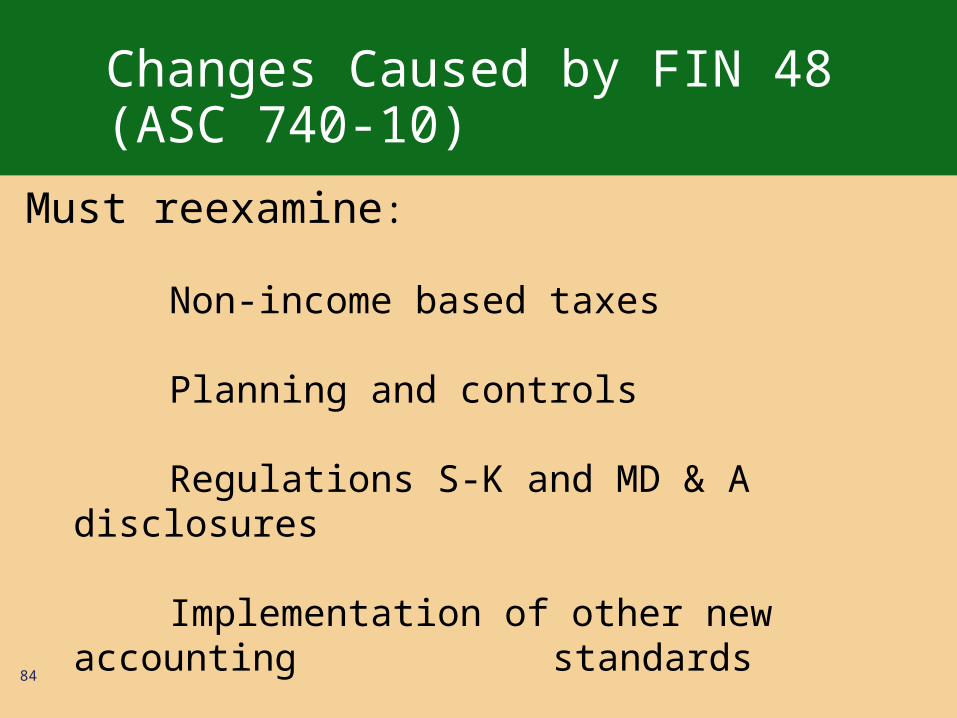

Changes Caused by FIN 48 (ASC 740-10)

84

Must reexamine:

Non-income based taxes

Planning and controls

Regulations S-K and MD & A disclosures

Implementation of other new accounting standards

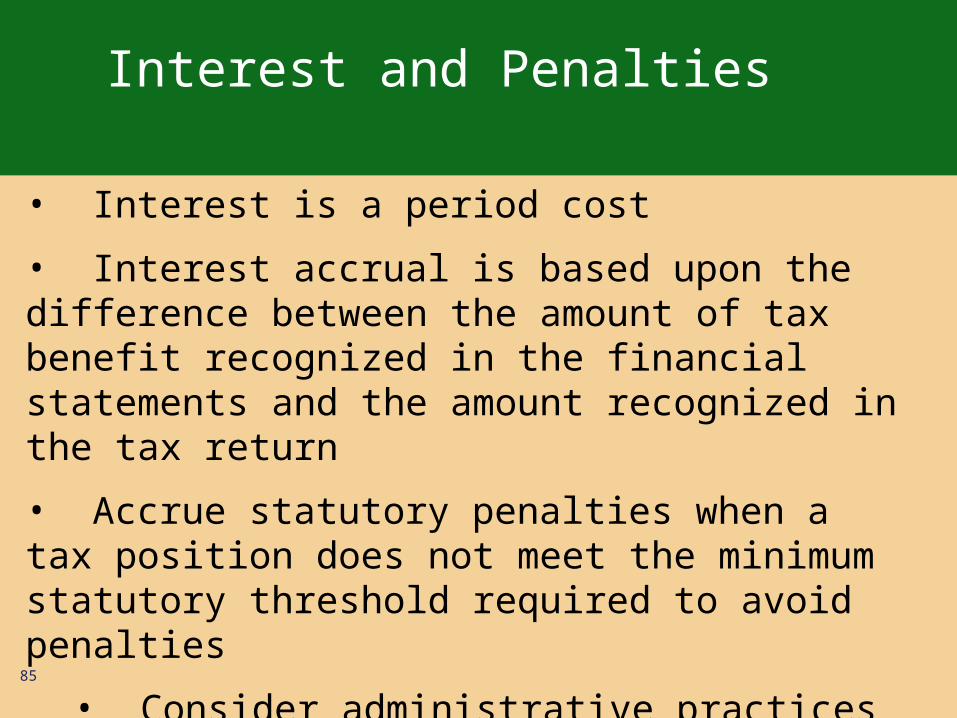

Interest and Penalties

85

• Interest is a period cost

• Interest accrual is based upon the difference between the amount of tax benefit recognized in the financial statements and the amount recognized in the tax return

• Accrue statutory penalties when a tax position does not meet the minimum statutory threshold required to avoid penalties

• Consider administrative practices and precedents of the tax authority

Interest and Penalties

86

Tax law provisions that address interest and penalties may vary between jurisdictions, periods

Classification of interest and penalties is an accounting policy election

Other Related Topics

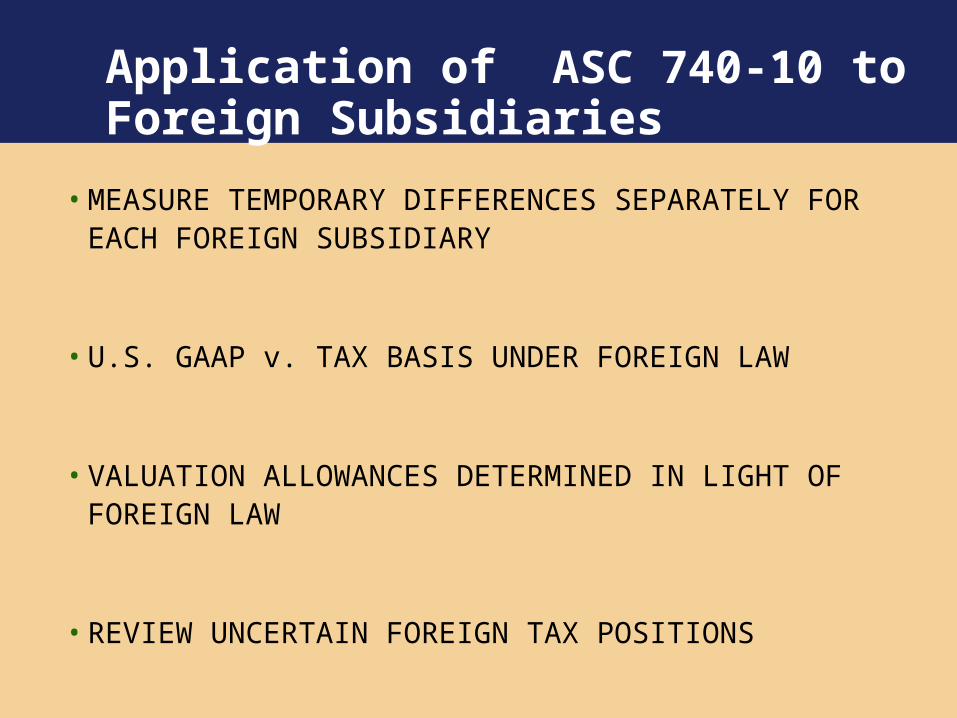

Application of ASC 740-10 to Foreign Subsidiaries

• MEASURE TEMPORARY DIFFERENCES SEPARATELY FOR EACH FOREIGN SUBSIDIARY

• U.S. GAAP v. TAX BASIS UNDER FOREIGN LAW

• VALUATION ALLOWANCES DETERMINED IN LIGHT OF FOREIGN LAW

• REVIEW UNCERTAIN FOREIGN TAX POSITIONS

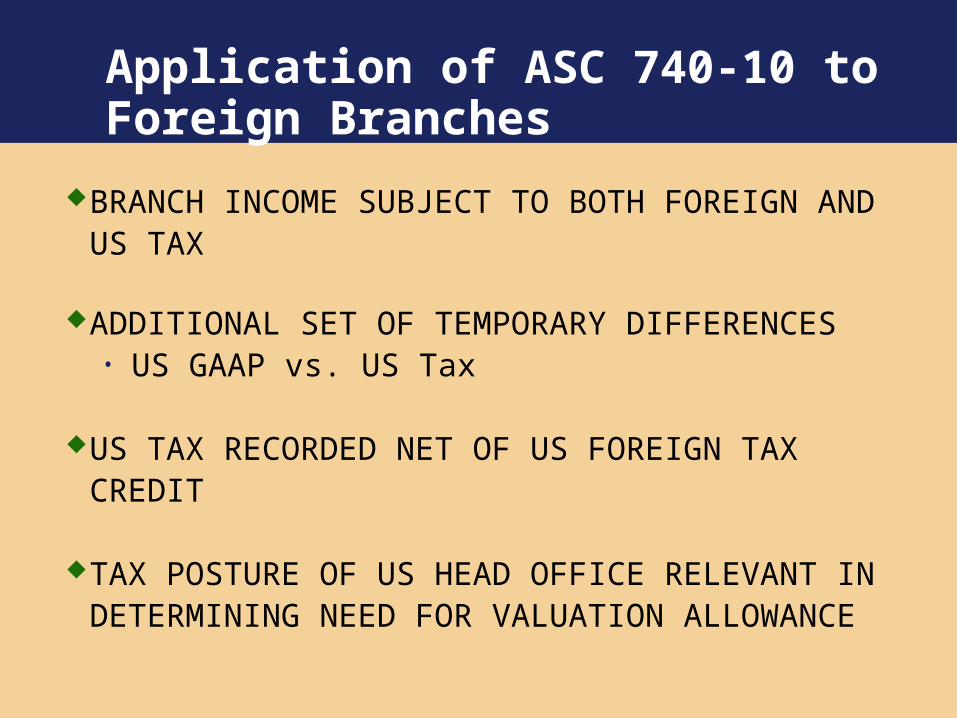

Application of ASC 740-10 to Foreign Branches

BRANCH INCOME SUBJECT TO BOTH FOREIGN AND US TAX

ADDITIONAL SET OF TEMPORARY DIFFERENCES• US GAAP vs. US Tax

US TAX RECORDED NET OF US FOREIGN TAX CREDIT

TAX POSTURE OF US HEAD OFFICE RELEVANT IN DETERMINING NEED FOR VALUATION ALLOWANCE

Inside Basis Temporary Difference

FAS 109 APPLIES TO DIFFERENCES IN FINANCIAL REPORTING CARRYING VALUE AND TAX BASIS OF FOREIGN SUBSIDIARIES’ ASSETS (i.e., INSIDE BASIS)

MEASURE TEMPORARY DIFFERENCES SEPARATELY FOR EACH FOREIGN SUBSIDIARY

US GAAP vs. TAX BASIS UNDER FOREIGN LAW

VALUATION ALLOWANCES DETERMINED IN LIGHT OF FOREIGN

LAW

“Outside” Basis Temporary Difference

• THE DIFFERENCE BETWEEN THE FINANCIAL REPORTING AMOUNT AND THE TAX BASIS OF THE INVESTMENT ON THE INVESTOR’S FINANCIAL STATEMENTS.

Methods Of Accounting For Investments

• COST

• EQUITY

• CONSOLIDATION

Cost Method Of Accounting

• INVESTMENT RECORDED AT INITIAL COST

• RECOGNIZE INCOME AS DIVIDENDS ARE RECEIVED

• NET ACCUMULATED EARNINGS OF THE INVESTEE SUBSEQUENT TO THE DATE OF INVESTMENT ARE RECOGNIZED BY THE INVESTOR TO THE EXTENT DISTRIBUTED AS DIVIDENDS

• DIVIDENDS RECEIVED IN EXCESS OF EARNINGS SUBSEQUENT TO THE DATE OF INVESTMENT ARE CONSIDERED A RETURN OF INVESTMENT AND ARE RECORDED AS REDUCTIONS OF THE COST OF THE INVESTMENT

Cost Method Of Accounting - Continued

• A DEFERRED TAX LIABILITY IS RECOGNIZED FOR AN EXCESS OF THE AMOUNT FOR FINANCIAL REPORTING OVER THE TAX BASIS OF AN INVESTMENT IN A LESS-THAN-20-PERCENT-OWNED FOREIGN INVESTEE.

• A DEFERRED TAX ASSET IS RECOGNIZED FOR AN EXCESS TAX BASIS OVER THE AMOUNT FOR FINANCIAL REPORTING OF AN INVESTMENT IN A LESS-THAN-20-PERCENT-OWNED FOREIGN INVESTEE.

Equity Method Of Accounting

• ONE-LINE CONSOLIDATION CONCEPT

• MUST BE FOLLOWED BY AN INVESTOR WHO HAS THE ABILITY TO EXERCISE SIGNIFICANT INFLUENCE OVER OPERATING AND FINANCIAL POLICIES OF AN INVESTEE EVEN THOUGH THE INVESTOR HOLDS 50 PERCENT OR LESS OF THE VOTING STOCK.

• 20 PERCENT OR MORE OF THE VOTING STOCK LEADS TO THE PRESUMPTION THAT, IN ABSENCE OF EVIDENCE TO THE CONTRARY, AN INVESTOR HAS THE ABILITY TO EXERCISE SIGNIFICANT INFLUENCE OVER AN INVESTEE.

Equity Method - Continued

• INVESTMENT ORIGINALLY RECORDED AT THE COST OF SHARES ACQUIRED.

• INVESTMENT’S CARRYING AMOUNT IS INCREASED OR DECREASED BY THE INVESTOR’S PROPORTIONATE SHARE OF EARNINGS OR LOSSES AND DECREASED BY ALL DIVIDENDS RECEIVED.

• REVENUE CONSISTS OF THE INVESTOR’S PROPORTIONATE SHARE OF EARNINGS AND AMORTIZATION OF ANY PURCHASED PREMIUM.

Equity Method - Continued

• IF EQUITY IS TO BE REALIZED IN THE FORM OF DIVIDENDS, INCOME TAXES SHOULD BE RECOGNIZED AS IF THE EARNINGS WERE DISTRIBUTED AS A DIVIDEND, APPLYING ANY APPLICABLE DIVIDENDS RECEIVED DEDUCTIONS, FOREIGN TAX CREDITS, TAXES TO BE WITHHELD, ETC.

• IF EQUITY IS TO BE REALIZED IN THE FORM OF A DISPOSITION, INCOME TAXES SHOULD BE ACCRUED AT THE APPROPRIATE RATES (CAPITAL GAIN RATES, IF APPLICABLE).

Foreign Subsidiaries

• A DEFERRED TAX LIABILITY IS NOT RECOGNIZED FOR THE EXCESS OF THE AMOUNT FOR FINANCIAL REPORTING OVER THE TAX BASIS OF AN INVESTMENT IN A FOREIGN SUBSIDIARY OR A FOREIGN CORPORATE JOINT VENTURE THAT IS ESSENTIALLY PERMANENT IN DURATION (i.e., THE OUTSIDE BASIS DIFFERENCE).

APB 23 (ASC 740-30) Exception vs. Election

• Not an election

• Exception applies if the specific facts and circumstances warrant

• Based on a company’s ability and intent to control the reversal of a taxable temporary difference (i.e. the outside basis difference in the stock of CFC due to unrepatriated earnings)

APB 23 (ASC 740-30) Issues

• FAS 109 INCORPORATES UNREMITTED EARNINGS IN THE “OUTSIDE BASIS” DIFFERENCE

• The ”outside basis" also includes–SAB 51 gains–Currency translation adjustments

SFAS 123R

• SFAS 123R applies to all transactions involving the issuance by a company of its own equity in exchange for goods or services

• Currently SFAS 123R does not apply to share-based payment transactions with non-employees or ESOPs.

SFAS 123R

• 123R requires all entities to recognize compensation expense in an amount equal to the fair value of share-based payments granted to employees.

Compensation Expense

• Compensation expense will be recognized over the requisite service period

• How the compensation is recorded depends on the vesting schedule– Cliff Vesting– Graded Vesting

Forfeitures

• 123R requires companies to estimate forfeitures on the date of grant

• In subsequent periods, estimates can be adjusted

• Changes in estimates will be a cumulative effect of a change in accounting estimate

Stock Compensation

• SFAS 123R requires companies to use fair value to measure share-based payments to employees

• Fair Value is determined at date of grant

• Value is never remeasured

Fair Value

If an observable market price exists for an option with the same or similar terms, companies should use that price

Otherwise, a valuation technique based on established financial economic theory should be used

Valuation Models

• Must be consistent with the fair value measurement objective and

• Capable of incorporating all the substantive characteristics unique to employee stock options

Factors Considered in Fair Value

• Exercise Price

• The expected term of the award

• Current Price

• Expected Volatility

• Expected Dividends

• Risk Free Interest Rate

Application of ASC 740-10 to Stock Options

• The compensation deduction on the financial statements give rise to a deferred tax asset under SFAS 109.

• The deferred tax is not remeasured for any future changes in the fair value before the tax deduction is taken

• A need for a valuation allowance should be considered

Effect on DTA – Tax Deduction

• At the time of the tax deduction is taken the DTA is written off

• If the tax deduction is larger than the book deduction the excess tax benefit is treated as an increase to paid-in capital

• If there is a tax benefit deficiency it is recorded as a decrease in paid-in capital if excess tax benefits exist

SFAS 123R

• A company should not recognize a credit to APIC for windfall tax benefits unless such windfall benefit reduces taxes payable. Therefore, a company would only be allowed to credit APIC when a benefit is received.

Effect of ASC 740-10 for ISOs

• Companies should not record a deferred tax asset for ISO’s because they cannot assume that these awards will result in a tax deduction

• A current tax benefit will result if there is a disqualifying dispostion

Accounting for Income Taxes - Interim

• FIN 18 “Accounting for Income Taxes in Interim Periods” amended APB 28

• Tackles how to measure the tax provision for interim reports when the actual tax expense is based on annual income.

• Allows estimates and judgments to determine the interim tax provision

Accounting for Income Taxes

• Income taxes for interim reporting is divided into:

1. Those applicable to income from continuing operations

2. Those applicable to significant, unusual or infrequently occurring items, discontinued items and extraordinary items

• Tax effect of the second set of items are calculated separately and added to tax expense for the quarter

Annual Effective Rate Method

• To calculate the provision under the annual effective rate method you must:

1. Determine the projected income, all permanent and temporary differences, credits and carryforwards for the entire year

2. Calculate the tax liability for the year

3. Calculate the ETR for the year; and

4. Apply the ETR to quarterly earnings

Annual Effective Rate Method

• Estimated ETR is applied to year-to-date income

• Prior quarter income taxes are deducted to compute the current quarterly income tax expense

Post Sarbanes-Oxley

• Prior to Sarbanes-Oxley many companies did not separate the income tax provision into current and deferred

–APB 11 approach

• Currently, a complete tax provision that shows a breakdown of current and deferred taxes are required for public companies

Updating the Annual Estimate

• A company must update its ETR each quarter

• An accurate projection of ETR is very important

• Because it is an estimate the amount may change during the year

• If ETR is miscalculated early in the year it is better to overstate taxes in the earlier quarter

Operating Losses in an Interim Period

• SFAS 109 addresses the case where a company has an operating loss for a quarter

• Under SFAS 109 realization of a tax benefit must be assured beyond a reasonable doubt before the benefit may be recognized in the financial statements

Operating Losses in an Interim Period

• A company can recognize a tax benefit of a to-date operating loss

• Prior periods of income are present against which the current loss can be applied

• Tax credits are available to offset the tax effect of the operating loss

• The company has established seasonal patterns of income in subsequent interim periods

Accounting Changes in Interim Periods

• SFAS 3 deals with how to report accounting changes in interim reports

• General recommendation is that changes should be made in the first quarter

• Cumulative effect of change – if change is made any a subsequent quarter all prior quarters must be restated

• Retroactive type change – if previous annual reports must be restates so do the interim reports

Intraperiod Tax Allocations

• Income tax expense or benefit must be allocated among– Continuing operations– Discontinued operations– Extraordinary items– Items charged or credited directly to

shareholder’s equity

Intraperiod Tax Allocations

• The tax effects of the following items are charged or credited directly to equity:

– Adjustments of opening RE for certain changes in accounting principles or a correction of an error

– Gains and losses included in comprehensive income but excluded from net income

– A change in contributed capital– Change in basis of tax assets in a pooling of interest– Dividends that are paid on unallocated shares held by an

ESOP– Deductible temporary differences that existed at the date

of a quasi reorganization

Intraperiod Tax Allocations

• Tax benefit of NOLs are reported in the same manner as the source of the income or loss in the current year

• Exceptions to this rule are:

• Tax effects of deductible temporary differences that existed at the date of a purchase business combination

• Tax effects of deductible temporary differences that are allocated directly to stockholder’s equity

Allocation Between Types of Income

• If there is only one item other than continuing operations, the portion of income tax expense or benefit that remains after the allocation to continuing operations is allocated to that item.– Use a with and without calculation

Allocation Between Types of Income

• If there are two or more other items, the amount of tax that remains after the allocation to continuing operations shall be allocated among the other items in proportion to their individual effect on income tax expense or benefit for the year.

• The sum of the separate tax effects may not equal the amount of income tax that remain to be allocated.

127

Balance Sheet Presentation

Classified Balance Sheet

• Break out current and noncurrent portions

Netting of Deferred Tax Assets and Liabilities of the Same Jurisdiction

No Netting of Deferred Tax Assets and Liabilities from Different Jurisdictions

128

Financial Statement Disclosures

Tax expense or benefit allocated to continuing operations and other categories

Significant components of income tax

Effective rate reconciliation

Gross deferred tax liabilities, gross deferred tax assets, the valuation allowance and the net change in the valuation allowance

129

Financial Statement Disclosure

Tax effect of each type of temporary difference and carryforward that gives rise to significant portions of the deferred tax liabilities or assets

Significant matters affecting comparability of information for all periods presented

Amounts and expiration dates of tax loss and credit carryforwards

130

Financial Statement Disclosure

Any portion of the valuation allowance or deferred tax assets for which subsequent recognition would be used to reduce goodwill or other noncurrent intangible assets of an acquired entity or would be allocated directly to equity

131

Rate Reconciliation

The objective of the rate reconciliation is to reconcile the “expected” US federal statutory income tax rate of 34% or 35% with the company’s “actual” or “effective” tax rate.

Items that Impact the Effective Tax Rate

State and foreign taxes (net of federal benefit)

Permanent Differences

Changes in the Valuation Allowance

Income Tax Credits

True Ups and changes in Cushion or change in prior year tax

Changes in Tax Rates

Cases – Rate Reconciliation

The reasons for the difference between income taxes computed by applying the statutory federal income tax rate and income tax expense in the financial statements are:

Statutory Rate 832,000 26.00%

State taxes, net of federal tax benefit 91,760 2.87%

Key-man life insurance (390,000) (12.19)%

Tax-exempt interest ( 39,000) (1.22)%

Dividends Received Deduction ( 10,400) ( .32)%

Change in of tax rate ( 5,409) ( .17)%

Effective tax rate 478,951 14.97%132

![Sfas dts help final[1]](https://img.pdfslide.us/doc/110x75/55858fb0d8b42aca7b8b46d5/sfas-dts-help-final1.jpg)