Embed Size (px)

Citation preview

SFA amendment requestMarch 2014

Contains forward looking statements

DisclaimerIMPORTANT: You must read the following before continuing. The following applies to the confidential information following this page as well as to any further information disclosed by WIND, whether in writing orother tangible form, or orally, that is identified as confidential when disclosed (collectively, the “Confidential Information”), and you are therefore advised to read this carefully before reading, accessing or making anyother use of the Confidential Information. In accessing the Confidential Information, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive anyinformation from us as a result of such access.

This presentation is provided to you (each referred to hereafter as a “Recipient”) for information purposes only and should not be relied upon by the Recipients and no liability, responsibility, or warranty of any kindis expressed, assumed or implied by WIND for the accuracy, inaccuracy, interpretation, misinterpretation, application, misapplication, use or misuse of any statement, claim, purported fact or financial amount,prediction or expectation and does not constitute an offer to sell shares or other securities or the solicitation of an offer to buy shares or other securities, nor shall there be any offer or sale of shares or othersecurities in any jurisdiction in which such offer or sale would be unlawful prior to registration or qualification under the securities laws of such jurisdiction. In addition, we also draw each Recipients attention to thefact that this presentation contains “forward-looking statements” regarding WIND and its future business. Such statements are not historical facts and may include opinions and expectations about management’sconfidence and strategies as well as details of management’s expectations of new and existing programs, technology and market conditions. Although WIND believes its opinions and expectations are based onreasonable assumptions, these forward-looking statements are subject to numerous risks and uncertainties, not all of which will be exhaustively explored in this presentation or elsewhere. Accordingly, theRecipients should not regard such statements as representations as to whether such anticipated events will occur nor that expected objectives will be achieved. The Recipients are reminded that all forward-lookingstatements in this presentation are made so on the date hereof and for the avoidance of doubt WIND does not undertake to update any such statement made to reflect events or circumstances after the date hereofor to reflect the occurrence of unanticipated events. For the avoidance of doubt, WIND does not accept any liability in respect of any such forward-looking statements.

You are reminded that this Confidential Information has been delivered to you on the basis that you are a person into whose possession this Confidential Information may be lawfully delivered in accordance with thelaws of the jurisdiction in which you are located and, except as set forth hereinafter, you may not, nor are you authorised to, deliver or disclose (whether in writing, orally or otherwise) the contents of thisConfidential Information to any other person, including but not limited to any investor, vendor, customer, manufacturer or independent contractor, without prior written approval of WIND, but only to the extent of andsubject to such conditions as may be imposed in such written authorization. You shall handle, use, treat and utilize the Confidential Information as follows: (a) hold all Confidential Information in strict confidence;(b) use the Confidential Information only for the purpose of your consideration of the amendment and waiver requests (“Permitted Purpose”); (c) reproduce the Confidential Information only to the extent necessaryfor Permitted Purpose; and (d) restrict disclosure of the Confidential Information to your employees or advisors with a need to know and advise such employees and advisors of the undertakings assumed herein.

All Confidential Information shall remain the sole property of WIND, and all materials containing any such Confidential Information (including all copies made by the Recipient), upon request of WIND, shall bereturned to WIND immediately upon the Recipient’s determination that it no longer has a need for such Confidential Information.

No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or reliability of the Confidential Information and no reliance should be placed on it. In no case shall thedisclosure or receipt of Confidential Information be construed as creating any obligation of WIND to furnish Confidential Information to the Recipient.

No license to the Recipient of any trademark, patent, copyright, or any other intellectual property right is either granted or implied by the disclosure to the Recipient of any Confidential Information, including, but notlimited to, any license to make, use, import or sell any product embodying any Confidential Information. No representation, warranty or assurance is made by WIND with respect to the non-infringement oftrademarks, patents, copyrights, or any other intellectual property rights or other rights of third persons.

WIND may be irreparably harmed by the breach of the confidentiality obligations assumed herein and damages may not be an adequate remedy; WIND may be granted an injunction or specific performance relieffor any threatened or actual breach of such obligations. In the event WIND shall bring any action to enforce or protect any of its rights hereunder, it shall be entitled to recover, in addition to damages, its reasonableattorneys' fees and costs incurred in connection therewith.

The foregoing rights and obligations in respect of the Confidential Information shall be governed by the laws of Italy without regard to conflict of laws principles. All disputes, controversies, or claims arising out of,relating to or in connection with such rights and obligations shall be finally settled by the courts of Rome, Italy.

2

Executive summary

• Wind Telecomunicazioni (“WIND”, or the “Company”) and Wind Acquisition Finance (“WAF”) is seeking amendments to the Senior Facilities Agreement (“SFA”) that will allow the Company to obtain the necessary operational flexibility to implement a multi-step refinancing plan aimed at addressing the PIK overhang and putting in place a stable, manageable and efficient capital structure (the “Multi-Step Refinancing” or the “Transaction”)

• In light of WIND’s strong operational performance (relative to the market) and positive momentum in the debt capital markets, WIND, WAF and its shareholder VimpelCom Ltd. (“VIP”) are considering improving the capital structure of WIND Group via a Multi-Step Refinancing plan which will entail:

Full refinancing of the existing PIK notes

Refinancing of the expensive senior unsecured cash-pay bonds with lower cost bonds in order to reduce the interest costs

Explore selective tower disposals to accelerate deleveraging

• In order to facilitate the implementation of the Multi-Step Refinancing, VIP is considering a substantial cash injection of €500m into Wind Acquisition Holdings Finance (“WAHF”) to create groundwork for refinancing the expensive callable existing debt at cheaper rates to generate substantial interest cost savings. VIP contribution along with the proceeds from an additional, lower interest, senior notes issuance will be used to refinance in full the PIK Notes within WIND restricted group

• The multi-step refinancing will allow WIND Group to create a sustainable capital structure with important benefits:

Permanent resolution of PIK overhang and any risk of CoC triggered by PIK holders

Substantial run-rate interest cost savings (c.€200m per annum)

Stronger cashflow generation and deleveraging trajectory

Extended maturity profile with no meaningful amortisations over the next few years

Additional operational flexibility and adequate covenant headroom

3

Executive summary (continued)

• As part of the implementation of the Multi-Step Refinancing, WIND and WAF requires certain amendments and waivers from the SFA and Senior Secured Notes (“SSNs”) lenders:

• The required SFA amendments will be split into 2 separate requests:

Request A (Refinancing amendments)*: Aimed primarily to provide the necessary covenant headroom and debt incurrence and distribution flexibility to put in place the Transaction. Request A requires Majority SFA lenders consent

Request B (Maturity extension by 2 years): Aimed at extending the maturity profile of the Group whereby the consenting lenders will roll into new extended SFA tranches. Request B to be implemented via structural adjustment requiring Majority and Affected Lenders consent. Lenders consenting to Request B must also accept Request A

• The Multi-Step Refinancing will demonstrate that WIND is an important asset for VIP and completely resolve the PIK overhang and near term WIND financing requirements whilst achieving a more efficient debt allocation within the VIP Group

• Secured Lenders are expected to benefit substantially as a result of i) unchanged senior secured leverage multiple with attractive junior debt/equity cushion; ii) significantly lower cash-pay and total interest cost; iii) improved deleveraging profile; iv) cash injection support from strong listed parent; and v) permanent resolution of PIK overhang and risk of CoC triggered by PIK holders

4* Certain of the Refinancing amendments are subject to the VIP cash contribution as outlined later in this presentation

Transaction overview

5

Target structure post TransactionCurrent simplified structure

* Plus associated transaction costs incl call premium and accrued interest

WAHF SA

WAF SA

Wind Telecom

WAHF

€2.4bnSFA

€1.3bnPIK

€3.8bn SSNs

€2.7bn SNs

+€0.5bn cash

€0.8bn*

€1.3bnPIK

Seek and obtain SFA and SSNs amendments

€500m VIP cash injection to part repay PIK

Subsequently use tower sale proceeds to repay partly SFA debt and partly new SNs

Launch refinancing of PIK and SNs via new SNs within the Restricted Group

WAHF SA

WAF SA

Wind Telecom

WAHF

€3.8bn SSNs

Tower proceeds in excess of 5xEBITDA

€2.4bnSFA

5x EBITDA tower proceeds

1

2

4

3

1

1

2

3

4

4

€3.7bn New SNs

Transaction overview (continued)

6* Plus associated transaction costs incl call premium and accrued interest

Step Overview Indicative timing Considerations

SFA and SSNs consent • Seek consent of SFA lenders and SSNs holders in order to implement the contemplated refinancing March-April 2014

No change in senior secured leverage

Economic incentive

€500m cash injection• Inject €500m cash contribution

• Use the proceeds to refinance part of the existing PIK notes

2014Support from VIP in order for WIND to implement its long term strategy

Substantial fresh cash injection

Refinancing of PIK and SNs via new SNs

• Launch a refinancing of the existing Senior Notes and PIK with newly issued Senior Notes within the Restricted Group

• Upstream part of the new Senior Notes issuance proceeds in order to refinance c.€800m PIK notes at WAHF*

2014

Permanent resolution of PIK overhang and any risk of CoC triggered by PIK holders

Significant interest savings event vs. existing cash-pay interest costs

Further deleveraging via tower sale proceeds

• Disposal of tower assets

• Use disposal proceeds to part repay existing SFA and newly issued Senior Notes

2014

Further reduction of senior secured and total leverage e.g. 10x EBITDA valuation would imply 5x repayment of SFA debt and remaining used to repay junior debt

TOTAL INTEREST SAVINGS ~€50m pa cash interest; ~€200m pa total interest incl. PIK

1

2

3

4

Transaction rationale

7

Take advantage of excellent debt capital market conditions to put in place a sustainable long-term capital structure

Permanent elimination of PIK overhang / risk of CoC triggered by PIK holders

Substantial cash injection from VIP highlighting confidence in WIND

Facilitate refinancing of existing bonds to provide substantial interest cost savings

Improved cashflows and deleveraging profile

Adequate covenant headroom

Improved liquidity position

Extended debt maturity profile

Enable management to focus on business strategy and value creation

Create a viable and efficient capital structure for WIND – core VIP asset providing earnings diversification and ~25% of Group EBITDA

€500m cash injection to deliver ~€200m annual interest cost savings (c. 2 years payback)

WIND will continue to be financially self-supporting

Facilitate exploration of strategic options for WIND (tower sale/ sharing, M&A etc)

Sources and uses

8

Group sources of funds €m Group uses of funds €m

New Senior Notes 3,709 Refinancing of 2017 SNs 2,678

VIP cash injection 500 Refinancing of PIK notes 1,277

Use of cash on BS 51 Call premiums (2017 SNs and PIK notes) 118

Unwinding of cross currency swaps on 2017 SNs 20

Other costs* 167

Total sources 4,260 Total uses 4,260

* Includes SFA and SSN consent fees, other fees and certain accrued interest

Manageable capital structure

9

Pro forma for refinancing (FY 2013PF)Status quo (FY 2013A)€m xEBITDA

Cash (141) (0.1)x

Term Loans 2,420 1.2x

2018 SSNs 3,133 1.6x

2019 and 2020 SSNs 550 0.3x

Total net senior secured debt 5,962 3.1x

2017 SNs 2,779 1.4x

Other debt*** 404 0.2x

Total net cash pay debt 9,145 4.7x

PIK notes 1,277 0.7x

Total net debt 10,422 5.4x

LTM EBITDA 1,944

Indicative cash-pay interest 770

Indicative PIK interest 155

Indicative total interest****** 925

€m xEBITDA

Cash (90) (0.0)x

Existing term loan* - -

Extended term loan* 2,420 1.2x

2018 SSNs 3,133 1.6x

2019 and 2020 SSNs 550 0.3xTotal net senior secured debt 6,013 3.1x ~3.0x

New SNs** 3,709 1.9x

Other debt*** 384 0.2x

Total net cash pay debt 10,106 5.2x

PIK notes**** - -

Total net debt 10,106 5.2x ~5.0x

LTM EBITDA 1,944

Pro forma cash-pay interest 720

Pro forma PIK interest -

Pro forma total interest 720

Note: Debt shown at book value* Assuming 100% extension rate for the SFA lenders** Includes the impact of call premium, consent fee payable to SFA and SSN lenders, transaction costs and unwinding of certain hedges*** Includes LTE debt and mark-to-market on derivatives**** PIK repaid via c.€500m cash contribution from VIP and new SNs issued at WIND restricted group***** Assumes the proceeds from tower sale for illustrative reasons

Illustrative impact of potential tower sale

proceeds to repay existing debt*****

3402,015

2,678

1,277

81 81 421

5,970

3,216

150 425

2014 2015 2016 2017 2018 2019 2020 2021

TLA TLB 2018 SSNs 2019 FRNs 2020 SSNs 2017 SNs PIK notes Ministry loan

3402,015

3,216 150

81 81 81 0

3,556

2,165

425

3,709

2014 2015 2016 2017 2018 2019 2020 2021

TLA TLB 2018 SSNs 2019 FRNs 2020 SSNs New SNs Ministry loan

No meaningful amortisations over the next few years

10

Status quo (FY 2013A)

Pro forma for refinancing (FY 2013PF)

(€m)Average maturity: ~4 yearsBlended total WACD: ~8.9%

Available liquidity: €441m

(€m)Average maturity: ~6 yearsBlended total WACD: ~7.1%

Available liquidity: €590m**

Note: Maturity of new SNs to be confirmed at the time of refinancing though maturity to be beyond SFA maturity. Assumes 100% extension rate for SFA lenders. Extended SFA lenders to have springing maturity vis-à-vis existing SSNs 2018 and SNs 2017. Debt shown at nominal value.

* Expected size of new Senior Notes factoring in the impact of call premium, consent fee payable to SFA and SSN lenders, transaction costs and unwinding of certain hedges

** Including the effect of the Transaction and €200m uncommitted RCF accordion

*

Section 1

WIND credit highlights

Clear outperformer in Italian mobile market

• Consistent market outperformer steadily increasing revenue and subscriber market share

• Smart Value for Money operator delivering good network quality on all technologies

• State of the art commercial proposition:

“All Inclusive” extended across the board: fixed & mobile as well as consumer & SME/SoHo

Innovative and attractive pricing: clear and transparent proposition

Simplified options portfolio with selected price increase in order to defend margins

12* Excluding MVNO: Vodafone Italia, TIM and 3 Italia estimation on official declaration

Mobile customer base

Mobile market share*

(millions)

(%)

19.9

21.0

21.6

22.3

2010 2011 2012 2013

34.2% 34.9% 34.7% 34.1%

33.8% 32.4% 31.7% 31.0%

10.0% 9.9% 10.3% 10.6%

22.0% 22.8% 23.3% 24.3%

2010 2011 2012 2013

Fixed strategy focused on value proved to be successful

• Effectiveness of the LLU focused strategy focused on value, demonstrated by sharp increase in EBITDA margin +6.2 p.p. in 2013

• Focus on LLU subscribers coupled with defocus on lower gross margins and indirect customers determined a slight reduction in customer base and market shares

• Defocus on more expensive push sales channels coupled with increased utilization of pull sales channels has contributed to the margin increase

13

Fixed broadband market shares*

Fixed EBITDA trend

(%)

(€m/%)

Others

297 303 332384

20.1% 20.3%22.6%

28.8%

2010 2011 2012 2013

53.9% 52.9% 51.9% 50.6%

11.9% 13.1% 12.6% 12.8%

12.9% 11.8% 13.1% 14.2%6.9% 6.4% 6.1% 6.3%14.4% 15.8% 16.3% 16.0%

2010 2011 2012 2013

* Source: Internal estimation on official declaration

WIND outperformance achieved in the backdrop of a difficult market environment

• Price war started in Q2 2013 reaching the highest level of aggressiveness during summer:

1. TIM directly attacked WIND lowering its price, adding You&Me unlimited, 1000 SMS and increasing the internet size bucket to 2GB

2. VOD reacted aligning its offer to TIM

3. WIND after unsuccessfully trying to defend previous pricing models reacted with a new offer lowering price and calls/SMS cap, increasing internet to 2GB as well

• Current commercial proposals by main competitors indicate return to more robust pricing strategies (See page 17)

• Hutchison is continuing its price undercutting approach, maintaining a -50/60% gap versus WIND’s current price level

14

Weak Italian macro scenario* Unemployment rate*

Intense price competition

(%) GDP trend (%)

* Source: ISTAT

1.3

(2.5)

(1.8)

0.7

2010 2011 2012 2013 2014E

Current Forecast

8.4

10.7

12.1 12.4

2010 2011 2012 2013 2014E

Current Forecast

WIND is now well-positioned to mitigate the adverse macro, regulatory and competitive environment going forward

15

MTR cuts impact fully factored-in1

Stabilising competitive environment2

WIND strong competitive positioning highlighted by consistent market outperformance3

Win in mobile data with significant upside potential4

Strong network supporting growth with limited future capex requirements5

Cost saving initiatives6

Potential towers sale targeted for 20147

1,573 1,6061,503 1,464

1,292 1,312 1,280 1,255

1,700 1,6711,572

1,4941,389 1,349 1,286

1,204

933 954 899 890815 828 839 800

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13

Tim Vodafone Wind

(0.1)%(3.0)%

(7.8)% (6.8)%(12.6)%(13.2)%

(6.7)%(10.1)%

5.0%2.1% 0.1% 2.3% 1.0% 1.7% 0.1%

(2.6)%

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13

Svc Rev Rep Exc MTR

MTR cuts impact is fully factored-in

• MTR cuts were the main cause of voice ARPU decline accounting for approximately 50% in 2011 and for more than 60% in 2012 and in 2013

2013 impact coming from MTR cuts estimated at approximately €400m decrease of total revenues and €100m of EBITDA decline vs. 2012

• Italy MTR value as of today is one of the lowestin Europe

• As of today no further MTR cuts are envisaged

• Any further cut would have a limited impact on P&L given the current MTR value lower than 1 €cent

16

WIND mobile service revenues

Mobile service revenues trend*

(YoY change)

(€m)

1

Excl MTR

Reported

(29)%(20)%

(14)%

Total change

* Source: Vodafone Italia estimation on official declaration, TIM as from official declaration

Signs of mobile market reverting to rational competition

• According to the commercial offers proposed in the market in September/October 2013, and given the recent Christmas campaigns, main competitors are focusing on more robust pricing models

• Hutchison is continuing its price undercutting approach, maintaining a -50/60% gap versus WIND’s current price level, slowly gaining market share but maintaining a higher churn due to its lack of nationwide mobile coverage and poor quality of service perception

17

2

February 2014

• Unlimited minutes on-net for Telecom Italia fixed customers

• Additional 1 GB and first month for free for customers signing

on-line

550 min550 SMS

1 GBUnlimited minutes on-net

17€

250 min250 SMS

1 GBUnlimited minutes on-net

12€

400 min400 SMS

2 GB

10€

800 min800 SMS

2 GB

14€

200 min200 SMS

1 GB

15€

200 min200 SMS

1 GB

14,9€

Summer 2013

400 min400 SMS

1 GB

10€

300 min350 SMS

1 GB

9.9€

460 min460 SMS

2 GB

10€

300 min300 SMS

2 GB

7€

400 min1000 SMS

Unl to 1 VO2 GB10€

400 min400 SMS

1 GB

15€

400 min1000 SMSUnl to TIM

2 GB10€

800 min800 SMS

1 GB

10€

WIND has better network with high

quality LTE spectrum and full national

coverage

Feb/Mar 2013

800 min/SMS and 2 GB for Telecom Italia fixed customers

( 70% of fixed market)

120 min120 SMS

1 GB

4€

240 min240 SMS

1 GB

8€

400 min400 SMS

1 GB

10€

600 min600 SMS

1 GB

20€

WIND strong competitive positioning highlighted by consistent market outperformance

• Clear positioning strategy as “Smart value for money provider”, coupled with strong commercial proposition, based on simplicity and transparency

• Further increase in both subscriber and revenue market shares in mobile

• “All Inclusive” umbrella proposition extended to all market segments including mobile consumer, fixed consumer, small/medium business and ethnic

18

3

Quality of serviceBrand positioning

InnovationSmart efficiency• Smart efficiency measures adopted

on all costs, including Advertising (single testimonial, “All Inclusive” brand ), Real Estate, Power and Rental costs

• Anti-crisis positioning with “minuto vero” concept (pay per effective second utilised instead of 30 seconds blocks)

• Strong performance on smartphones, reaching 30% penetration on WIND’s customer base

• Adopted revenue share model with Google play

• WIND best performance on “Facebook Top Brands” by BlogMeter as the fastest company on answering customers via Facebook

• MyWIND App for smart-phones and tablets(more than three million downloads)

Q3-12 Q4-12 Q1-13 Q2-13 Q3-13 Q4-13

3,965 4,4795,541

8,296

2010 2011 2012 2013

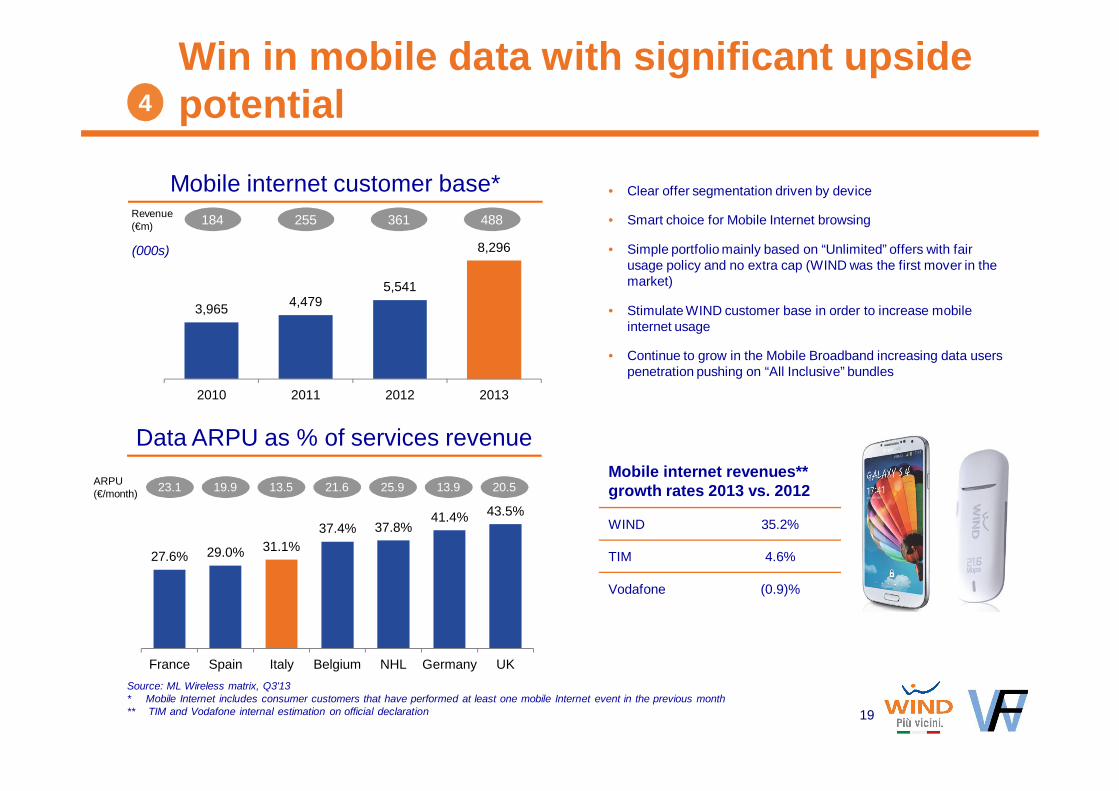

Win in mobile data with significant upside potential

• Clear offer segmentation driven by device

• Smart choice for Mobile Internet browsing

• Simple portfolio mainly based on “Unlimited” offers with fair usage policy and no extra cap (WIND was the first mover in the market)

• Stimulate WIND customer base in order to increase mobile internet usage

• Continue to grow in the Mobile Broadband increasing data users penetration pushing on “All Inclusive” bundles

19

4

Mobile internet customer base*

Source: ML Wireless matrix, Q3'13* Mobile Internet includes consumer customers that have performed at least one mobile Internet event in the previous month** TIM and Vodafone internal estimation on official declaration

Data ARPU as % of services revenueMobile internet revenues**growth rates 2013 vs. 2012

WIND 35.2%

TIM 4.6%

Vodafone (0.9)%

Revenue (€m) 184 255 361 488

ARPU (€/month)

27.6% 29.0% 31.1%37.4% 37.8%

41.4% 43.5%

France Spain Italy Belgium NHL Germany UK

23.1 19.9 13.5 21.6 25.9 13.9 20.5

(000s)

905

789

16.7%15.8%

2012 2013

Strong network supporting growth with limited future capex requirements

• GSM network completed: reached 99.85% population coverage with GPRS/EDGE nationwide coverage

• HSPA+ network fully developed: 96.34% population coverage, with 21 Mbps being rolled out in all Italian cities, 42 Mbps being deployed in largest cities

• Double digit increase YoY in data traffic on WIND’s network

• LTE hotspots launched in Rome and Milan in 4Q 13 as well as in main Italian airports

• LTE plan: available in 17 largest Italian cities by the end of 2014 utilizing the 800 MHz frequencies

20

5

Capex* Mobile network

• 1,458 LLU sites: c. 60% direct population coverage in all major Italian cities

Fixed network

• Solid fibre optic backbone of 21,647 km, supporting both fixed and mobile businesses

Backbone• 2013 capex mainly dedicated to further expansion of HSPA+

coverage and capacity as well as strengthening the backbone to support data growth

• Capex expected to remain stable despite the LTE rollout plan that will substitute current HSPA+ investments

• Capex spend not expected to change materially vs previous 2-3 years

As of December 2013* Capex excludes LTE costs. Capex 2013 excludes €134m of non-cash increase in Intangible Assets related to the contract with Terna in

relation to the Right of Way of WIND’s backbone

Capex/Revenues*

WIND executing on cost saving initiatives

21

6

• Cost efficiency program recurring waves in order to optimize all P&L’s OPEX cost lines (e.g. commercial, staff, technology, procurement)

Description

Cost efficiency program

Initiative

• Advertising optimization in order to improve efficiency and effectiveness of media spending thanks to strong synergies: same format and same testimonial for the entire product portfolio and across all segments, without impacting on communication efficiency

Advertising Optimization

• Established dedicated organization to optimize Rental and Power costs management through BTS modernization, suppliers renegotiations and data center consolidation

• Strong focus on site rental optimization through launch of new sites negotiation model and push on mobile sites sharing (already increased by 30% in last twelve months from 2.0k to 2.6k)

Rental & Power

• Re-design and simplify IT systems framework to improve time to market and analysis effectiveness for a fast product development and 360° customer response

• In-sourcing activities and maintenance optimization in order to maximize productivityTechnology

• Build The Network project signed in 2013 will allow WIND in coming years to install same quantity of equipment developed in 2012Network

• Network Transformation Project executed: achieved in 2013 a saving of approximately €50m in costs (mainly from HR) compared with 2012NTP

Potential upside from towers sale

• WIND is evaluating various options for a stand alone towers sale including the upfront monetizing of the long-term commitment on-site rental management with a Tower operator

• The value of the potential initiative derives from the sum of the discounted cash flows to the TowerCo driven by the fees paid by WIND for the long term passive site management service on the contributed sites and by commercial exploitation of the spare space available for third parties hosting

• WIND benefits from the incremental value related to tower operator market premium deriving from EBITDA multiple (tower multiples are still in the range of 10x – 15x vs. ~6x for Telecoms)

• The possible transaction perimeters considered include a subset of WIND’s sites (5,000 – 7,000 sites) mainly situated in rural areas (of which about 20% with at least another mobile network operator hosted) selected in order to (i) have no or very limited impact on WIND’s LTE roll-out plans and (ii) provide a potential upside for the TowerCo to host other operators on the sites without Electromagnetic radiation limitations issues

• Based on a preliminary valuation, considering 5,000 – 7,000 rural sites as initiative perimeter, the Enterprise Value of this potential initiative is estimated in the range of €350 – 550 million. WIND proceeds, based on its retaining a 10% – 15% stake, are in the range of €300 – 500 million

• A potentially larger perimeter can be evaluated although it increases deal size and complexity

• Towers sale is already allowed under current SFA documentation; amendments to be solicited to facilitate the transaction

• Under the SFA, proceeds of the towers sale can be reinvested in the business within the following 12 months or applied to prepay Senior debt; amendments to be solicited to allow a portion of such transaction to be used to partly repay new senior notes subject to threshold

• The transaction is targeted to be completed in 201422

7

Section 2

Amendment request

Overview of SFA Amendment – Request A (1/2)• Amendments to create a stable long-term capital structure for WIND

• Require majority lenders consent

24

Note: Selected and key SFA Amendments* Plus PIK Refinancing Transaction Cost which includes associated transaction costs, call premium and accrued interest** Debt incurrence technically not conditional on VIP Cash Injection, although use of proceeds exclusively for Existing PIK refinancing which

can only occur post VIP Cash Injection

SFA item Description RationaleContingent on VIP

Cash Injection

Debt incurrence

• Permit incurrence of €800m* junior debt exclusively to refinance PIK within the restricted group

• VIP support with €500m cash injection

• Elimination of PIK overhang

• ~5.0x PF leverage (incl tower sale proceeds impact) well inside WIND valuation

• Develop positive momentum to execute existing bonds refinancing with substantial interest cost savings

• Unchanged senior secured leverage with adequate junior debt/equity cushion

• Attractive bank debt margins considering current market conditions and issue ratings

Distribution to WAHF (PIKCO)

• Permit €800m* distribution exclusively to facilitate PIK refinancing

• Distribution flexibility construct purely to facilitate PIK refinancing

**

Overview of SFA Amendment – Request A (2/2)• Amendments to create a stable long-term capital structure for the WIND Group

• Require majority lenders consent

25

Note: Selected and key SFA Amendments* Effective headroom lower considering the call premium payable upon existing bonds refinancing

SFA item Description RationaleContingent on VIP

Cash Injection

Financial covenants

reset

• Reset leverage (senior secured and total debt) and interest cover covenants*

• Adequate but not excessive headroom*

• Reset leverage covenants with appropriate step-downs

• WIND continues to consistently outperform in a challenging market

RCF accordion

• Permit €200m RCF accordion • Uncommitted RCF accordion

• Provides further liquidity

Tower sale

• Permit tower sale proceeds in excess of 5.0x EBITDA tower valuation as certified by CFO to repay the junior debt (incl PIK) e.g. 10x valuation would imply 5x repayment of SFA debt and remaining used to repay Senior Notes/PIK Notes

• Consents to align the requirements of Permitted Tower Agreement with prevailing market terms

• Facilitate tower transaction under SFA

• De-leveraging event

• Interest cost saving via most expensive debt repayment

• Reduced senior secured leverage with improved cashflows

Escrow / Alternative

Issuers

• Allow WAF to issue new refinancing debt into escrow ahead of effective refinancing

• Flexibility to issue notes out of an Italian entity

• Defined escrow conditions so that proceeds can only be released for repayment of debt

• Alternative issuer of HY Notes and SSNs to provide flexibility on jurisdiction and entity, without prejudice to rights of existing secured creditors

Overview of SFA Amendment – Request B• Extension of maturity profile for the WIND Group• Request B implementation via Structural Amendment requiring Majority Lenders and each affected lender consent• Lenders consenting to Request B must also consent to Request A

26* Subject to existing SSNs 2018 and SNs 2017 maturity** Mobile telephony license holder in EU, Canada, Switzerland and/or the US with market capitalization at the time of sale or merger

announcement in excess of VimpelCom market capitalization at the time of PIK Consent Request Letter

SFA item Description RationaleContingent on VIP

Cash Injection

Maturity extension

• Extend maturity of existing RCF, TLA and TLB by 2 years

• TLA amortization profile extended by 2 years

• Request B contingent on successful approval of Request A that will provide platform for a stable long-term capital structure for the WIND Group

Demonstration of VIP support via €500m cash injection

Removal of PIK overhang

Improved cashflows driven by refinancing

Unchanged senior secured leverage

Adequate junior debt/equity cushion despite higher cashpay leverage

• Request B to further enhance capital structure via

Maturity extension with no material debt amortization until 2018

Enable management to focus on business strategy and value creation

• Extended SFA lenders to benefit from springing maturity*

• Dividend flexibility represents

Material de-leveraging required to reach 4.0x threshold with adequate equity cushion and improved cashflows

Facilitates materially faster deleveraging via stronger parent (ie with higher market cap) in return for dividends post this material deleveraging to 4.0x

Change of control

flexibility

• Extended tranches to have CoC linked to (i) Eligible Acquirer** having a market capitalization in excess of VimpelCom or (ii) pro-forma total net and senior secured leverage is 4.25x and 3.0x respectively or (iii) either (i) or (ii) are satisfied and merger / acquisition

Dividends

• In case of CoC Acquisition linked to Eligible Acquirer** then the dividend threshold is increased from 3.5x to 4.0x

Currentmaturity

Extendedmaturity

RCF Nov-16 Nov-18

TLA Nov-16 Nov-18

TLB Nov-17 Nov-19

Request B – Change of Control (‘CoC’)

27

• Flexibility applicable to New RCF and New TL (A3, A4, B3, B4) extended tranches following:Positive Request B consentVIP €500m cash injection

• Change of Control mandatory prepayment provisions are not triggered if one of the below alternatives is satisfied

Market cap not worse than VIP market cap Pro Forma Net Leverage below 4.25x (deleveraging transaction)1 2

• Amend the definition of “Principal Investor” to include:Any publicly listed company which holds a licence to provide mobile telephony services in the European Union, Canada, Switzerland and/or the United States Market Capitalisation greater than or equal to VimpelCom’s Market Capitalisation*

• If this Option 1 is utilised, then dividend test is raised from 3.5x to 4.0x Pro Forma Total Net Leverage Ratio (note significant deleveraging to 4.0x and well capitalised new owner profile; provision facilitates event driven deleveraging)

• No Change of Control only if:Pro Forma Net Total and Senior Secured Leverage following the acquisition is 4.25x and 3.0x respectivelyPro Forma test to include only limited amount of reasonably anticipated synergies and cost savings to be certified by the CEO and CFO and with a cap of 10% of the Pro Forma Consolidated EBITDA

99.5

59.221.3 15.7

Vodafone H3G TI VIP

Alternative key conditions which are credit enhancing for lenders

Illustrative: market cap of Italian operators ($bn)

83.8 43.5 5.6Difference to VIP Market Cap ($bn)

By way of illustration, all three major Italian players would comply with the

proposed Principal Investor Definition

* “Market Capitalisation” for Eligible Acquirer calculated at the time of the announcement of the sale or merger transaction while VimpelCom market capitalization is as of PIK Consent Request Letter

** Moody’s and S&P, respectively

Illustrative example

Pro forma net leverage post refinancing and tower sale

Required net leverage

~5.0x 4.25x

Change of Control No Change of Control

Corporate rating** A3/A- A3/A- Ba1/BB+ Ba3/BB

OR

In market consolidation1b

• Satisfaction of either 1 or 2 above• Also permits a merger or an acquisition for an in-market

consolidation

OR 2b/

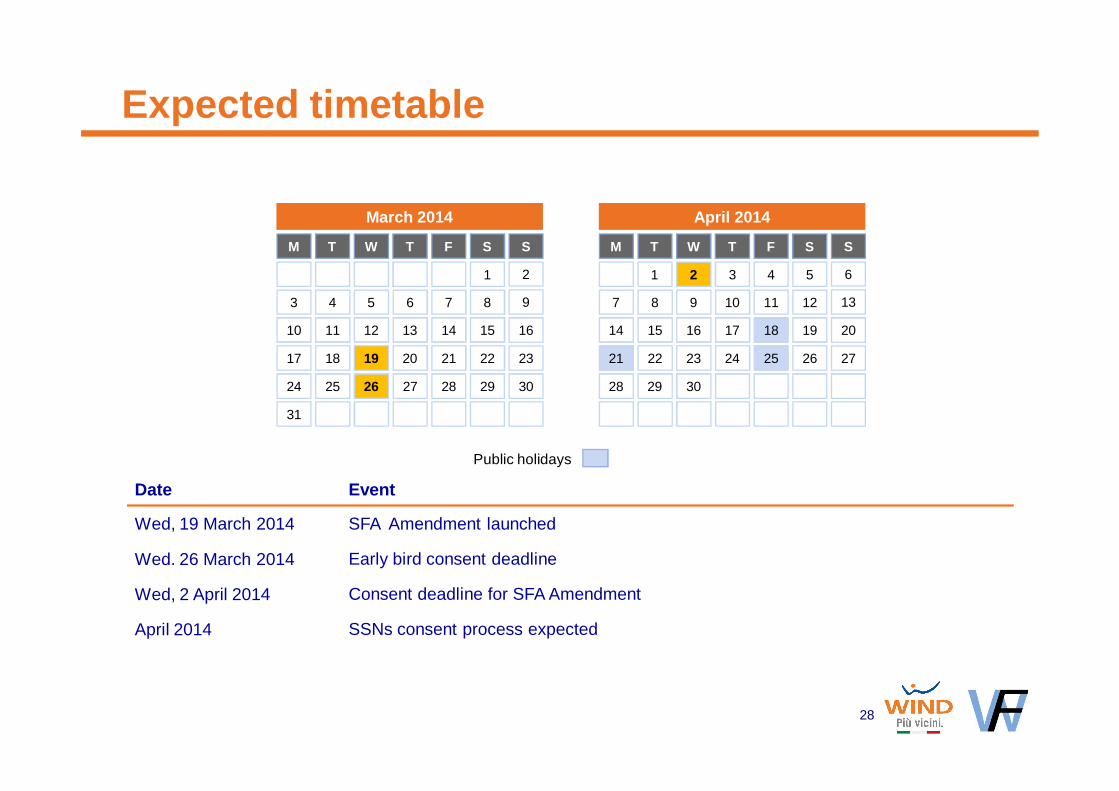

Expected timetable

28

Date Event

Wed, 19 March 2014 SFA Amendment launched

Wed. 26 March 2014 Early bird consent deadline

Wed, 2 April 2014 Consent deadline for SFA Amendment

April 2014 SSNs consent process expected

Public holidays

April 2014

SW T F STM

27

3028 29

13

20

6

24

1

7

21

10 11 128

17 18 191615

2322

3 4 52

14

25 26

9

March 2014

SW T F STM

23

26 2927 2824 25

9

16

2

20

3

17

6 7 84

13 14 151211

1918

1

10

21 22

5

30

31

Appendix I

Additional materials

Alternative refinancing structure

• The WIND Group may also consider an alternative refinancing structure in which the remaining PIK notes (post €500m cash injection) are refinanced with new PIK toggle notes

• The structure may be implemented:

In case Senior Secured Noteholders consent to a refinancing of the PIK/SNs is not economical

Potentially better call features available at PIK level

In case flexibility is required for potential M&A

• The outlined refinancing structure would be characterized by:

Lower cash-pay leverage at the WIND Group level

Relatively similar interest cost vs. base case refinancing structure

• €80m per annum distribution to WAHF subject to 5.25x proforma leverage to become effective in this alternative refinancing structure*

30

* WIND to have ability to bring €800m of debt plus any associated transaction and call costs into WIND restricted group as long as the per annum basket is reduced pro-rata

Appendix II

Update on FY2013 performance

8.1 8.7

2012 2013

(mln)

10.48.0

3.94.3

14.412.3

2012 2013

(€) 21.6 22.3

2012 2013

(mln)

32

+7.6%

Customer Base ARPU

Gross Adds

+3.0%

Data

Voice

• WIND’s customer base up 3.0% YoY driven by the significant growth of gross additions in first part of the year, despite competitive environment

• Data ARPU increases 9.6% reaching 35.2% of total ARPU; voice ARPU declines as a result of the intense price competition coupled with the MTR cuts

• Voice traffic continues to grow double digit as a result of increasing penetration of “All Inclusive” bundles

Strong Mobile Commercial Performance

(14.5)%

+9.6%

5,541

8,296

2012 2013

('000)

33

Mobile Internet CB*Internet & Data Revenues

* Mobile Internet includes consumer customers that have performed at least one mobile Internet event in the previous month

+49.7%

• Internet and Data revenues confirm to be future

proof with double digit growth driven by

increase in data users penetration via “All

Inclusive” bundles and specific data offerings

coupled with increase in penetration of

smartphones

Impressive Mobile Internet Performance

1,007

127

(5)

21 1,150

2012 Mobile Internet

Traditional Data

Content 2013

(€m)

+35.2%

+14.2%

645 548

2,466 2,415

3,110 2,963

2012 2013

34

Voice Subscribers

ARPU

• Fixed voice subscribers decrease by 4.7% as a

result of strategy focused on LLU and pull

channels, in order to switch acquisition from

quantity to quality and generate a positive

growth in EBITDA and margin

• Fixed-line ARPU declines marginally with the

voice component decrease partially offset by the

double digit growth in data ARPU driven by

broadband

Indirect

Direct

Fixed-Line Performance Delivering on LLU Strategy

(4.7)%

(2.0)%

(1.7)%

(15.0)%

(‘000)

31.2 30.7

2012 2013

(€/month)

1,848 1,866

2012 2013

('000)

92.9% 92.9%

2,210 2,191

2012 2013

('000)

35

Broadband Subscribers

Dual-play Subscribers

Broadband ARPU

Strategic Highlights

Flat

Pay x use

• Fixed Broadband customer base stable, in line with the strategy focused on acquisition of higher value LLU customers and increasing utilization of inbound sales channels

• BB ARPU increases as a result of growing penetration of customers with a dual play bundles driven by convergence options between fixed and mobile both covered by the common “All Inclusive” umbrella

Solid Fixed Broadband Performance

(0.9)%

+1.0%

19.1

20.2 20.220.4 20.5

Q4-12 Q1-13 Q2-13 Q3-13 Q4-13

(€/month)

2,063 1,944

38.0% 39.0%

2012 2013

(€m)

5,053 4,577

374406

5,4274,983

2012 2013

(€m)

36

(8.2)%

Total Revenues

(9.4)%

Other revenues + CPE

TLC service revenues

EBITDA / Margin

(5.8)%

• Total revenues decline 8.2% with service revenues

down 9.4% mainly due to the aggressive price

competition coupled with double MTR cuts.

Excluding MTR impact total revenues are stable

(-0.9%)

• From September promotional pressure reduced but

cannibalization effect on customer base remains an

issue

• EBITDA declines 5.8% YoY with positive impact

coming from the optimization in all P&L cost lines

partially compensating pressure on top line

• EBITDA margin at 39.0% up 1.0 percentage point

versus 2012

Revenues and EBITDA – Total

(9.9)%

EBITDA / Margin

Total Revenues

(7.8)%

(10.7)%

Other rev. + CPE

TLC service rev.

• Total mobile revenues in 2013 decline 7.8% as a

combined result of:

Strong performance in mobile Internet & data

revenues, growing 14.2%, driven by impressive

growth in mobile Internet, up 35.2%

Decline in mobile voice revenues mainly driven

by fierce price competition and reduction of

incoming revenues due to the MTR cuts

• 2013 EBITDA declines 9.9% to €1,559 million mainly

due to the pressure on service revenues

37

Revenues and EBITDA – Mobile

3,677 3,282

281366

3,9583,648

2012 2013

(€m)

1,731 1,559

43.7% 42.7%

2012 2013

(€m)

332 384

22.6%

28.8%

2012 2013

(€m)

1,376 1,295

9340

1,4691,335

2012 2013

(€m)

Total Revenues

EBITDA / Margin

Other rev. + CPE

TLC service rev.

• Fixed-line total revenues in 2013 decline 9.1% YoY

mainly due to lower service revenues, down 5.9%,

driven by the LLU strategy focused on higher

value subscribers, and fixed to mobile

substitution

• EBITDA increases 15.8% YoY to €384 mln driven

by strategy focused on higher margin LLU

customers and pull channels leading to significant

increase in margin

38

Revenues and EBITDA – Fixed-Line

(9.1)%

+15.8%

(5.9)%