Embed Size (px)

Citation preview

Session Three

Next Generation Supply Chain

Blockchain: new payment system for the sharing economy

Matthew Key Head of Customer Innovation at BT

Global Services

Understanding the Blockchain Matthew Key – Head of Customer Innovation FS- BT 06/07/16

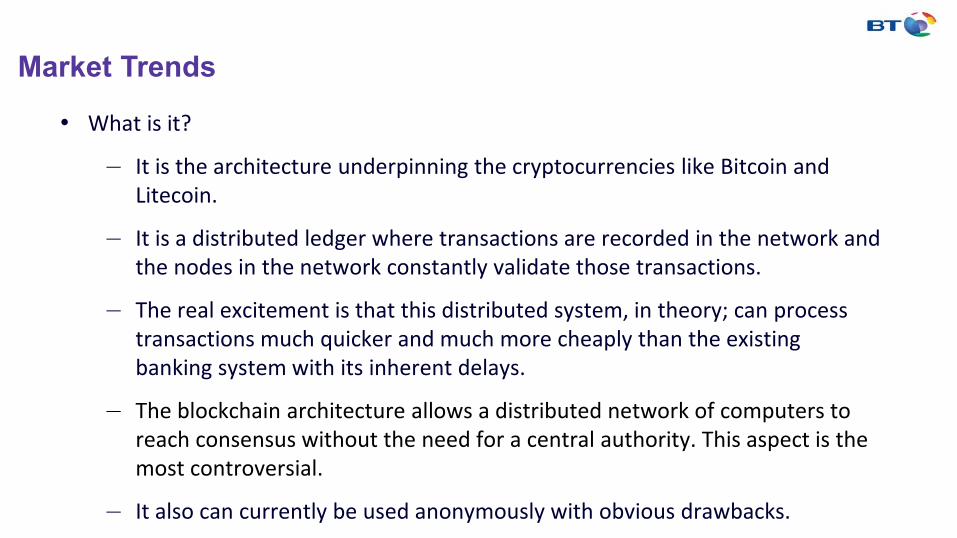

Market Trends

• What is it?

– It is the architecture underpinning the cryptocurrencies like Bitcoin and Litecoin.

– It is a distributed ledger where transactions are recorded in the network and the nodes in the network constantly validate those transactions.

– The real excitement is that this distributed system, in theory; can process transactions much quicker and much more cheaply than the existing banking system with its inherent delays.

– The blockchain architecture allows a distributed network of computers to reach consensus without the need for a central authority. This aspect is the most controversial.

– It also can currently be used anonymously with obvious drawbacks.

Market Trends ‘Distributed ledger technology has the

potential to transform the delivery of public and private services. It has the potential to redefine the relationship between government and the citizen.. and trust and make a leading contribution to the government’s digital transformation plan.

Any new technology creates challenges, but with the right mix of leadership, collaboration and sound governance, distributed ledgers could yield significant benefits for the UK’

Sir Mark Walport HMG Chief Scientific Advisor 19/01/2016

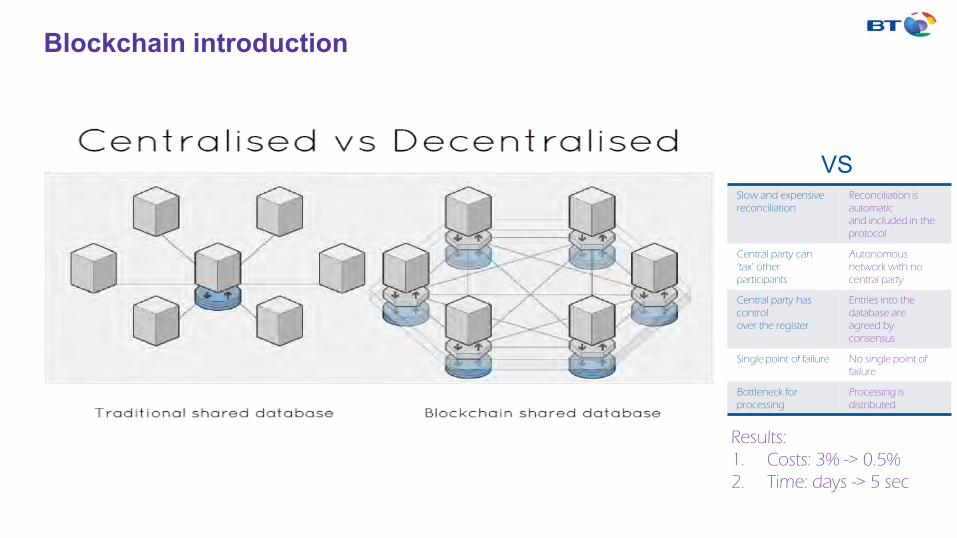

Blockchain introduction

Slow and expensive

reconciliation

Reconciliation is

automatic

and included in the

protocol

Central party can

‘tax’ other

participants

Autonomous

network with no

central party

Central party has

control

over the register

Entries into the

database are

agreed by

consensus

Single point of failure No single point of

failure

Bottleneck for

processing

Processing is

distributed

Results:

1. Costs: 3% -> 0.5%

2. Time: days -> 5 sec

VS

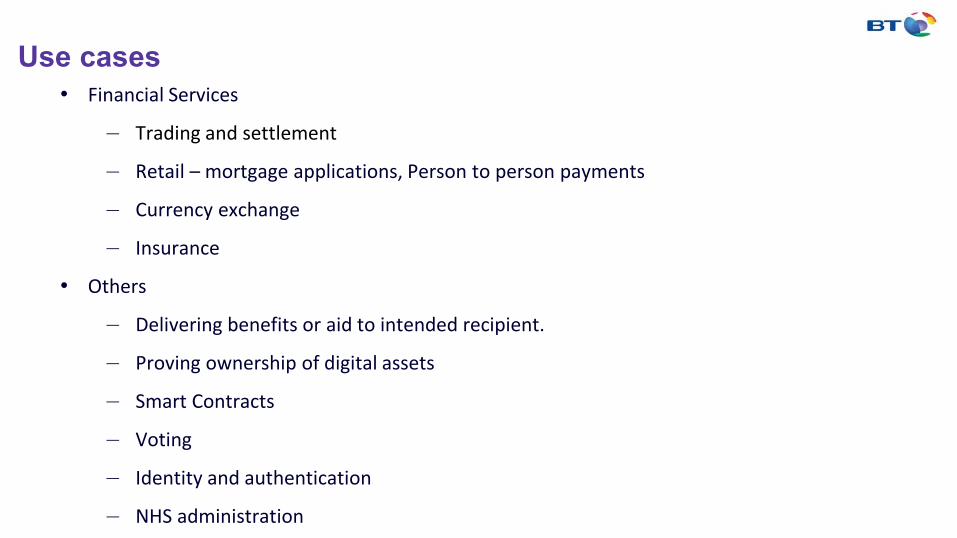

Use cases • Financial Services

– Trading and settlement

– Retail – mortgage applications, Person to person payments

– Currency exchange

– Insurance

• Others

– Delivering benefits or aid to intended recipient.

– Proving ownership of digital assets

– Smart Contracts

– Voting

– Identity and authentication

– NHS administration

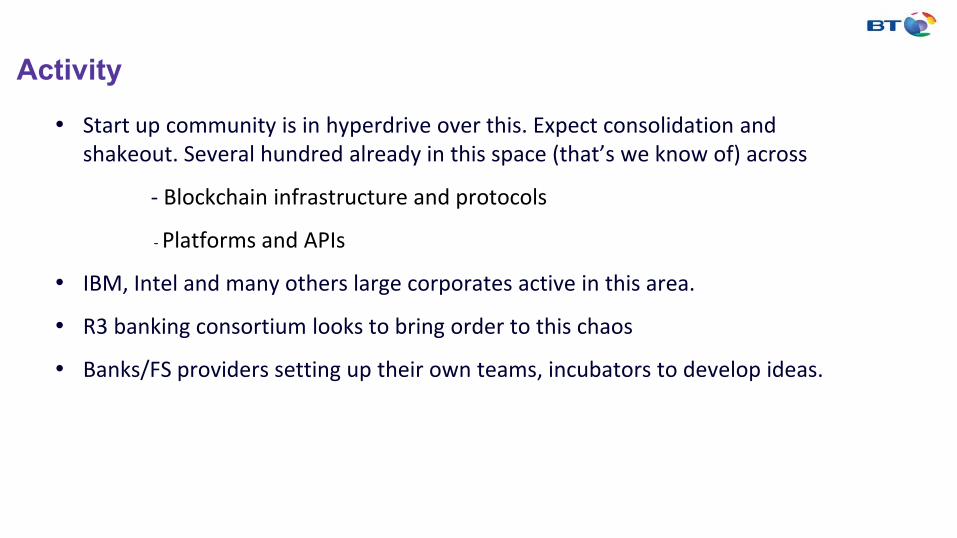

Activity

• Start up community is in hyperdrive over this. Expect consolidation and shakeout. Several hundred already in this space (that’s we know of) across

- Blockchain infrastructure and protocols

- Platforms and APIs

• IBM, Intel and many others large corporates active in this area.

• R3 banking consortium looks to bring order to this chaos

• Banks/FS providers setting up their own teams, incubators to develop ideas.

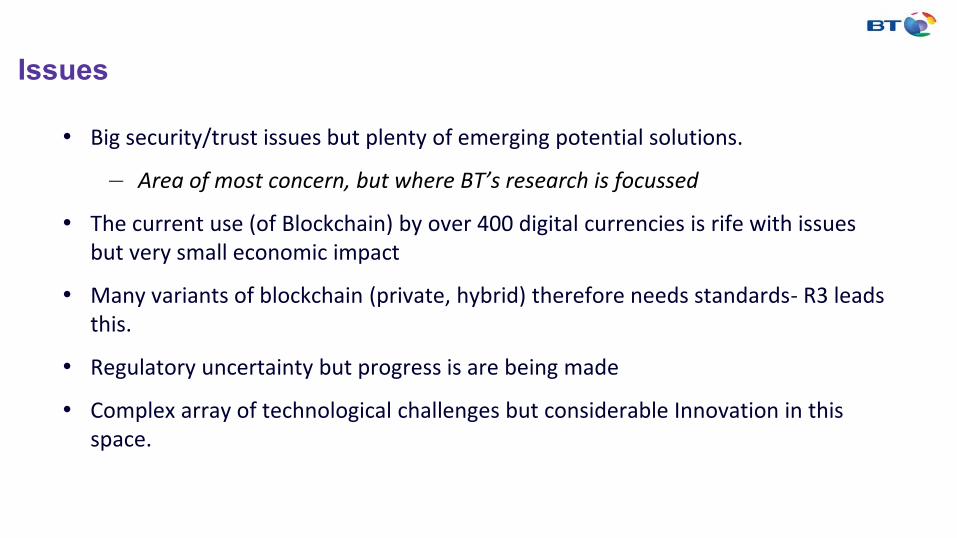

Issues

• Big security/trust issues but plenty of emerging potential solutions.

– Area of most concern, but where BT’s research is focussed

• The current use (of Blockchain) by over 400 digital currencies is rife with issues but very small economic impact

• Many variants of blockchain (private, hybrid) therefore needs standards- R3 leads this.

• Regulatory uncertainty but progress is are being made

• Complex array of technological challenges but considerable Innovation in this space.

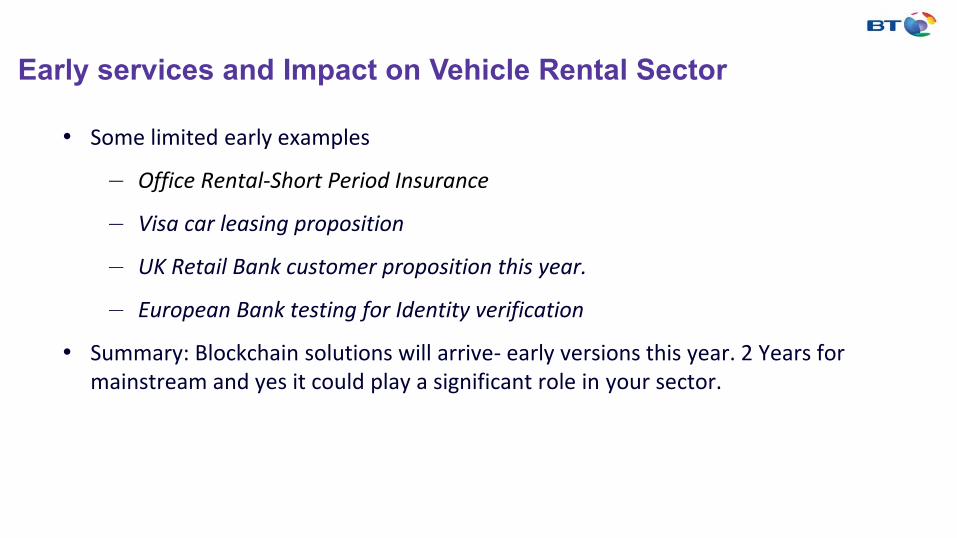

Early services and Impact on Vehicle Rental Sector

• Some limited early examples

– Office Rental-Short Period Insurance

– Visa car leasing proposition

– UK Retail Bank customer proposition this year.

– European Bank testing for Identity verification

• Summary: Blockchain solutions will arrive- early versions this year. 2 Years for mainstream and yes it could play a significant role in your sector.

Delivering Mobility as a Service

Martin Drake Product Director at Drive Software

Solutions

The Market To Date

• Principle Products – Contract hire – Personal Leasing – Fleet management – Short term Rental

• Increasing Services • Low interest rates • Green Policies

Current Changes

• Connected Cars – Driver Behaviour – Lots of Data – Vehicle Condition Monitoring – Location Tracking – Journeys – Logistics

• “Mobility” – Car Sharing – Incident Management – Travel

• Electric Vehicles • Salary Sacrifice • Financial Changes

– Negative Interest Rates – IFRS16 Imposition

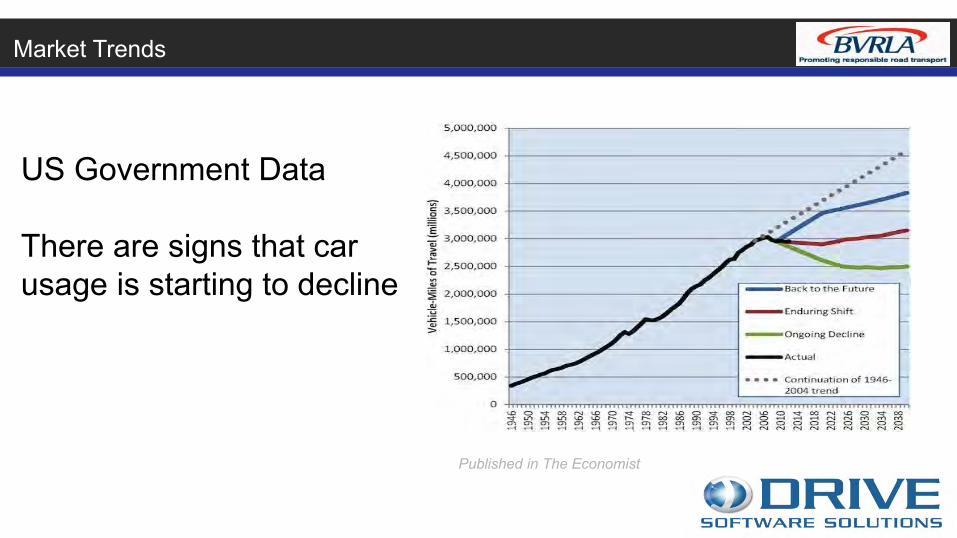

Market Trends

US Government Data There are signs that car usage is starting to decline

Published in The Economist

Market Trends

Users expect interactions to be mobile and efficient

The Effect

• Mobility becomes a reality – Flexible Contracts – Assetless Contracts – Car Sharing – Incident Management – Travel Administration – Car Policy becomes Mobility Policy

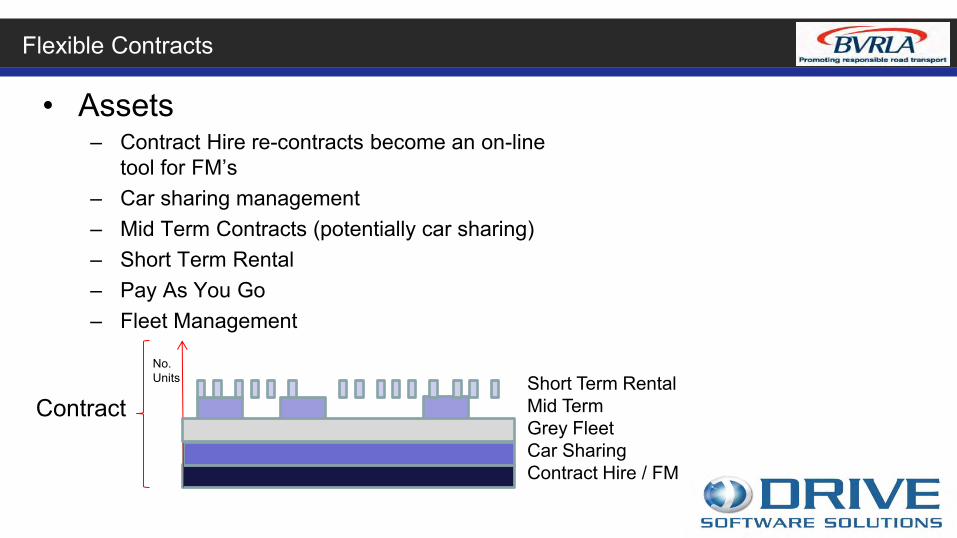

Flexible Contracts

• Assets – Contract Hire re-contracts become an on-line

tool for FM’s – Car sharing management – Mid Term Contracts (potentially car sharing) – Short Term Rental – Pay As You Go – Fleet Management

No. Units

Contract Short Term Rental Mid Term Grey Fleet Car Sharing Contract Hire / FM

Asset Less Contracts

• Equally Flexible – Flexible Service Choices restricted by grade / role – Usual Flexible Billing

• Hierarchy splits • Drivers • Consolidated with Asset Billing • Integrated with rental / incident management etc

– Expenses Management – Travel Cards / Management

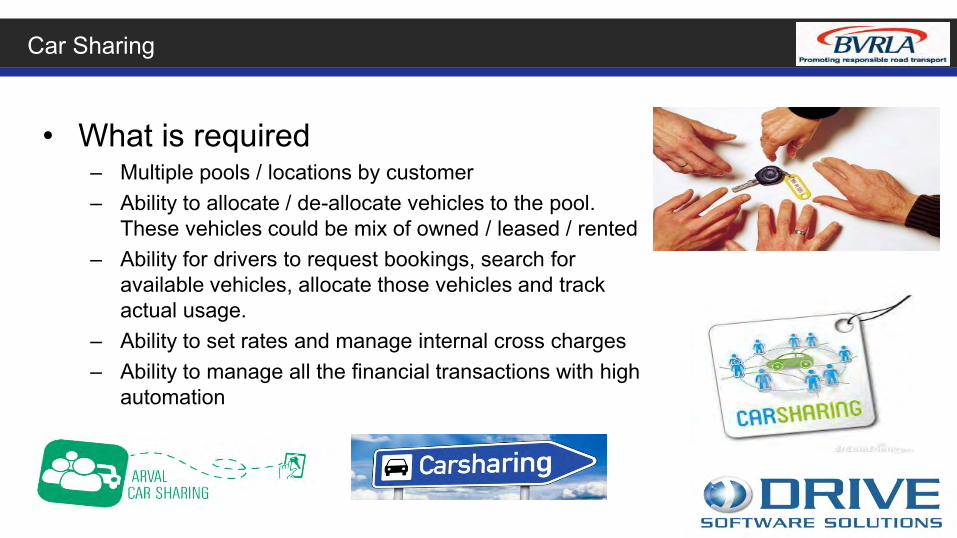

Car Sharing

• What is required – Multiple pools / locations by customer – Ability to allocate / de-allocate vehicles to the pool.

These vehicles could be mix of owned / leased / rented – Ability for drivers to request bookings, search for

available vehicles, allocate those vehicles and track actual usage.

– Ability to set rates and manage internal cross charges – Ability to manage all the financial transactions with high

automation

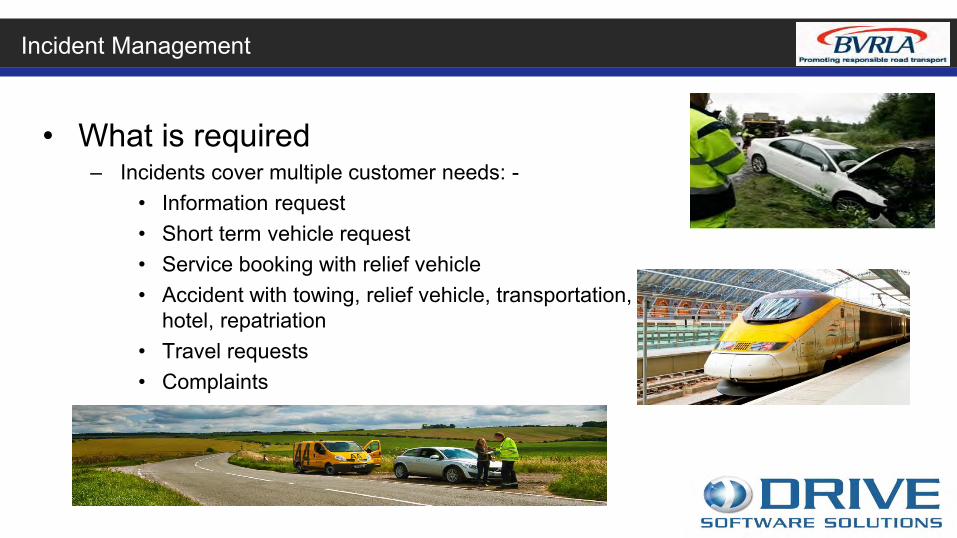

Incident Management

• What is required – Incidents cover multiple customer needs: -

• Information request • Short term vehicle request • Service booking with relief vehicle • Accident with towing, relief vehicle, transportation,

hotel, repatriation • Travel requests • Complaints

Mobility Policy

• Customers have many choices – Permanent lease vehicles – Fleet Management – Electric Vehicles – Car share – Salary Sacrifice option requiring grey fleet

management – Rentals and Mid Term contracts – Non Vehicle Transport (Bus / Taxi / Train)

Capitalising on the Opportunity

• To capitalise on the opportunity the key is technology

• It needs to combine traditional leasing and associated services with rental, driver services, connections to external travel tools all delivered through seamless user interfaces

• It needs to have very high levels of customer specificity and automation based on these rules

• It needs to leverage high volumes of collected data becoming intuitive for users (they are used to services such as Google and Amazon knowing what you want before you do)

Or…

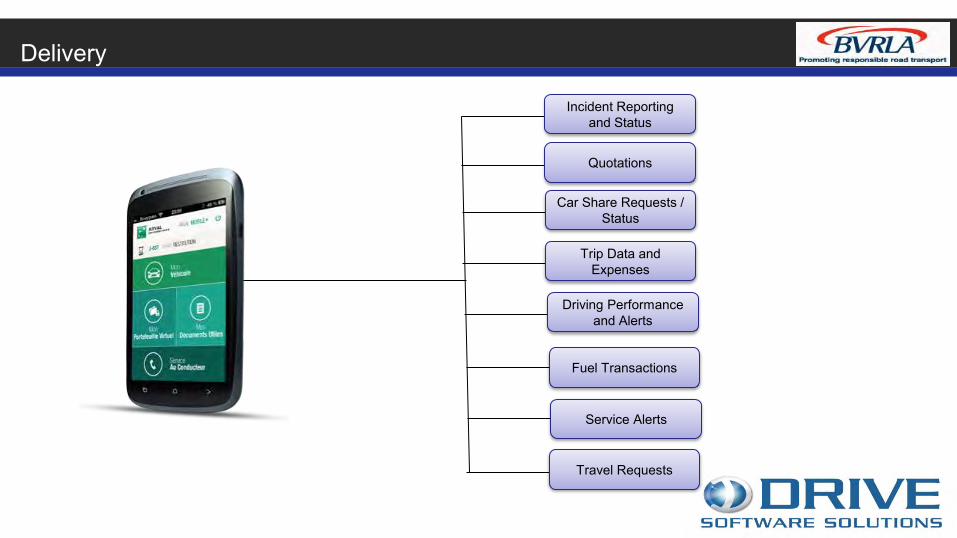

Delivery

Incident Reporting and Status

Quotations

Car Share Requests / Status

Trip Data and Expenses

Driving Performance and Alerts

Fuel Transactions

Travel Requests

Service Alerts

What does this mean?

• More Transactions. • Greater Complexity. • More IT Interfaces. • More Functions. • More Data.

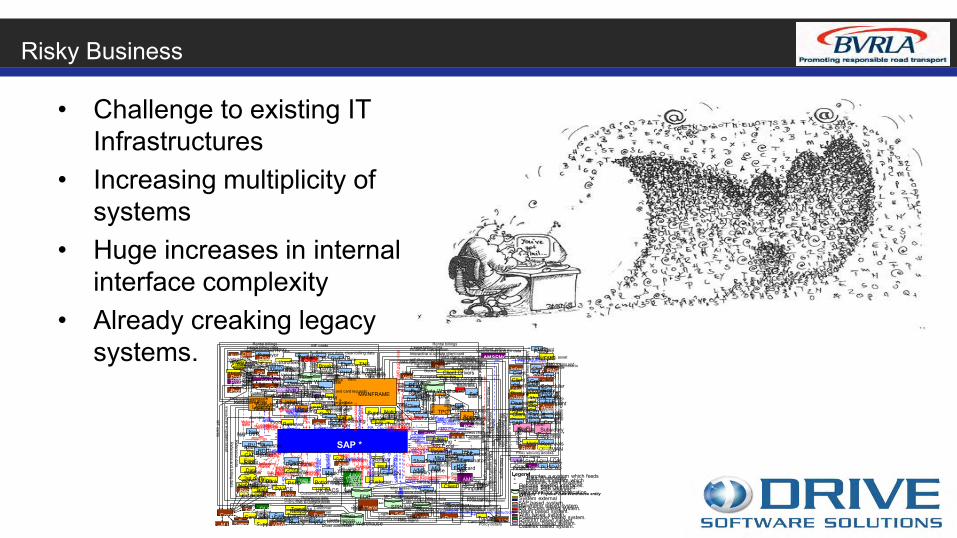

Risky Business

• Challenge to existing IT Infrastructures

• Increasing multiplicity of systems

• Huge increases in internal interface complexity

• Already creaking legacy systems.

SAP *

Quotes

Interest adjustment

NVR inc. CAS/PCP

Fuel (including Leasing * + and Networks +)

Customer Rental Billing AR/GL

EPOS

manual fuel vouchers

MAINFRAME

Mini Lease lease billing *

Local Account Card (LAC) * Purchasing Card * (makes own payments)

Certegy

Bank

CHOS

AMS

Client Invoicing *

To AR

Capita

Irish Fuel * (aka Eirecaps)

PRICING Policy data

Pinpoint

Car Hire companies Vehicle Rental

Client MAP Info.

Magic Box

Fleetcom Centracall

Reference and billing data

Interactive

Reference data

Eurofleet

Reference data, clean billing data

Interactive e-update asset

Interactive e-update client card

Customer and vendor reference data Reference data

1Link Relicensing

Policy Financial suppression

Financial suppression

Rectify

TPOT Lease billing data

VDIS

Roa

d ta

x du

e

Breakdown company Breakdown vehicles

DRP CBA*

Rental policy Valid codes

Booking

Bookings/E

xtensions

Reference data

Financial suppression

Clients and vendors

Mini Lease Allocations

Supplier

MS Excel Matisse GL Manual GL

To GL

KeyFleets (Prolease) * Subsidery (Prolease) *

Eiger Account Validation lookup

Customer

AR files

Outstanding balances Bottomline

Fuel

tran

satio

ns

Cha

rges

Val

id to

tax

Veh

icle

tax

deta

ils

I & O

AR

Customer ref data

Bill

ed

trans

actio

ns

Ren

tal t

rans

actio

ns

Fuel and SMR billing data

Bill

ed tr

ansa

ctio

ns

Vendor, custom

er, asset data Mini Lease hire details

Bill

ing

Dat

a S

MR

eve

nt d

ata

Mas

ter D

ata

Policy data

Client, contract, specs, vendors

Data supplier

Collection balance Supplier Payments

Invoices (into AR)

Supplier

payment

Supp Payments

BA

CS

C

heques

Supp Payments

UK BACS Irish Bank PAYCE

N6, N7, N8, N9 to GL

MS Access based system. Web based system.

Assets To Bill

AP Reimb Invoicing *

GL

AR

Powerbuilder based system.

Questionnaires

EDB

SPIN

NVR assets/fittings and card requests

Data Warehouse

Data Warehouse

Some reference data

Data Warehouse

3rd party authorisation

Det

ail C

odin

g Vehicle Ref Data (including Residual Values (RVs))

RS6000 based system. Dataflex based system.

Glass Transactions Glass Payments Incident transactions/charges

TMS

Shredder

Epyx/1Link (Translease) Vehicle Service histories SMR vendor invoices

Supplier Invoices (into AP)

Customer Invoices (into AR) Includes: RDDD, ADDACS, AUDDIS, Bank Statement

Self Registration Logins

Client

data

MCS Card data

Maintbook Vehicle lines data

Reporting Reference and billing data

SMR event data

Refunder Expected refunds

OLA Cards MF cards

MF cards

CardClear Hotlisted cards

Supplier

Txns for authorisation/ authorised txns

TNS

Progress based system.

Pol

led

txns

Unvalidated txns

Reference data

Legend + Denotes a system which feeds Data Warehouse. * Denotes a system which produces client Invoices. Denotes existing interfaces. Denotes SAP inbound. Denotes SAP Outbound.

System external Mainframe based system.

Data store not an application (NB Only 1 Physical Data Warehouse entity exists)

Delphi based system.

Customer profiles

Client Drivers Acceptance/check in

Mileage readings

AMS client, supplier, card, asset reference data

AM

S client, supplier, card, asset reference data

FMG AMS client, supplier, card, asset reference data

FMG Policy Client policy Client policy

Tranzline Laptop Customer

Clients, vendors, service histories

Reference data

Unvalidated txns

Invoice prints Ta

x di

sk re

fund

s

Eve

nt in

form

atio

n

Financial suppression

Client data

Interactive e-upate client card M

F Reference data

MF Reference data

MF Reference data

Reference data

Reference data

Reference data Client data

Interactive e-update asset Reference and biling data

Logins

Matchstick Vehicle lines and RV data Vehicle lines and RV data

Vehicle lines and RV data

Vehicle lines data

Vehicle lines and RV data

Vehicle lines and RV data Vehicle lines and RV data

SMR txns

Supplier reference data

Vehicle lines data Sold assets

ED

I invoices

Paper invoices

Customer, card and daily txns

Centrefile

Vehicle, card and vendor data

To GL

eRetriever Vendor RA Invoice details

Retriever Invoice details Vendor RA

Customer payments & assets from AR, GL Invoice prints

Key - for-key

Customer policy data

Returned DD file DD

Reference data

Interactive e-update client card

Manual

PCP Reference data Pricing data

Interactive Security Security access Security access

SM

R vendor

invoices

Billings and text

CLIENT Txns

Drivers and vehicles

DEW/ STAR

Client

Suspect txns

Valid txns

Fuel Rebates Payments Fuel txns

DWP FAMIS Vehicles and txns

ICI Vehicles, billed txns

VMS Enquiry Collections

Cheque RA Fleetcard special outputs Fuel brand analysis

DMS Rental billings

New LVR

Journals

Postings

Infrascan

Archiver

Change of Name Copy Voucher

FTE Headcount

Compass

Charger

Blueprint

Dimensions

Profile Calculator Profiles Profile Loader Quotes

Client profile quotes

IBM EDI Purchase orders IBM

RV Reserves

Job codes, labour times

NatWest Bankline Bank statements and CHAPS

Adjuster

Asset data

CAP RVs

RVs

Client

OPX2 CCH

Bookem Farmer

Errors VMD

Surf

VMM Tracker

Tranzline Networked Customer

Fuel Voucher Voucher details

Terminator Early terminations

VTAR Addresses Driver addresses

Allstar Online Txn, copy voucher and client data

National Supplier

REIMS

EDI invoice types Glass txns

EDI invoices

Parts & price catalogue

Invoice types, glass, parts & price catalogue

Oracle Financials

Abacus

Payroll Deductions

IRIS OROS PWA

PHHBatch Various data

Self Billing

Billed txns

RDD Receipts System Letters, mailmerge Reaper Casper Sundry invoice lookup

CAS PCP

Scribler Snap

Car

Hire

da

ta

Balancer GL account movements

Stanley Oliver

AMSFMGdatarep AMS client, supplier, card, asset reference data

Solimar Car Hire

EDI (Tradacom) RA Electronic payment

Electronic payment Forecast Model

Peugeot SMR txns

CAS PCP AR

PAS PUS

Fuel Voucher Checking Voucher details

P11D

Payroll

P11D

Bank details

FleetSN

CC

, car sales

Sapencer CSV converter

Topcall SMS messages

Unique .co.uk

Online. co.uk

Credit DB Client

OFISMAN

FMGUser Daemon FMG logins and security access to Interactive

Fees

Incidents

Incidents

FMG Payments

FMG Payments

FMG security access

FMG security access

FMG

security access

FMG logins

FMG logins FMG

logins

FMG logins

ePCP Pricing data

eQuotes Policy data

Suppression File

Capwin Vehicle ref data

Sel

l and

SM

R p

olic

y da

ta

Estimated valuations and work instructions ePresentment

Registered users

email address changes

email address changes

HSE Fleetcard Disk Billed data

Surveys

Crackle

Client MF reference data

MF R

eference data

MF reference data

MF reference data

Governer Cards

Depreciator

Ass

ets

Client

Dealer Directory

M I Reporting

Tax Calc

Reco Report

GIS location data Policy details

PCSO

Special Outputs Special outputs

Vehicle lines

Bookings

Policy details

Policy details Policy details

Policy details

FMG

logins FM

G security access

Rental nillings

Rental billings

Rental billings

Lease billing data Lease billing data

Lease billing data Financial suppression

Financial suppression Rental billings

MF cards

Vehicle lines and R

V data

Renewals Vehicle data

Vehicle data

Vehicle data

Scheduler Monitor

Vehicle lines and RV data

Client Asset data

Asset data

Profile Loader Client profile quotes

SAP based system.

Client

Client

P & R SMR

Ezine Surveyor

Orange User Recognition

CAP

FAS

Root Cause Management

Disposals vat Buying Agency

Driver Interactive

P & R SMR Current asset position Current asset position

Account Managers Lib

• Key Point 1: Enabling Software

• Single Database architecture & technical environment

• Normalised data for high quality and low maintenance overhead

• Fully Coded Data

• Automated processes for operational activities to avoid poor data qualit

• Fully Auditable

• Rich suite of business rules configuration to meet specific customer needs

• Integrated eBusiness tools exploiting configuration / automation

Enablement

• Key Point 2: People Skills

• Top management have to be involved and committed

• This is business change management not just technology change

• Significant expertise is required to be successful • People development is intrinsic

Enablement

Project Key points

• Software ability to reach this step • Embedded in the top management

process

• Change management project

• Evolution of the models / processes becomes BAU

Project Key points Under estimated

Summary

Digital Parking Services

Lee Hudson Chief Operating Officer at AppyParking

Lee Hudson - COO

What Is A Smart City?

“A place where information is shared to create an ideal environment resulting in happy citizens.”

Drivers Are Currently Lost

660 £ M

FINES ISSUED EACH YEAR

30 %

CONGESTION FROM VEHICLES LOOKING FOR PARKING

Wasted Time And Money

AVERAGE BRIT IN THEIR LIFETIME WASTES

347 LOOKING FOR A SPACE

DAYS 37 ON FUEL TRYING TO PARK

K £

AppyParking’s Mission

“To make parking a truly forgettable experience.”

AppyParking Products

App/White Label Website Parking API AppyPetrol

REAL TIME BAY SENSORS

AppyParking™ has teamed up with Nwave to show drivers which bays are available and to reduce congestion, parking times and pollution.

Sparkit Sensor Nwave Base Station

Real time bay availability

Application Server

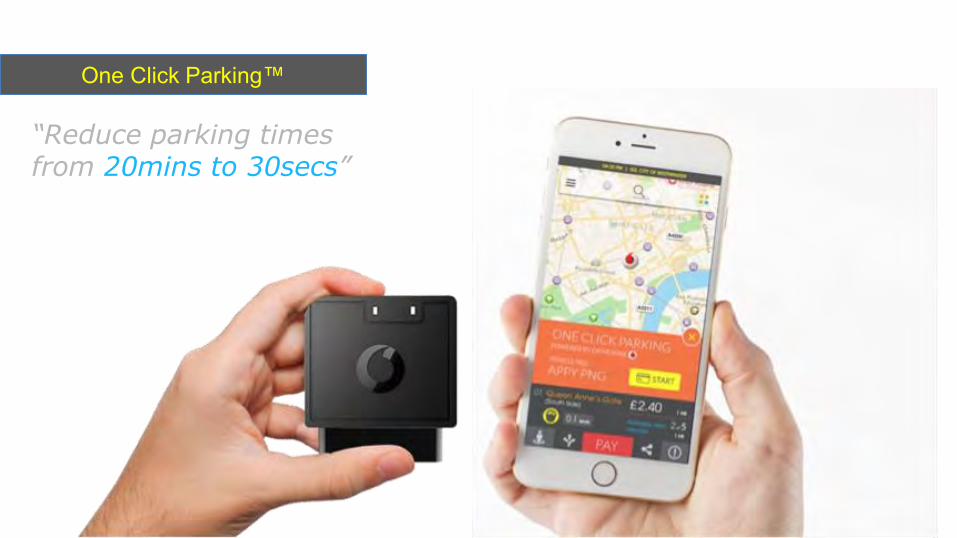

One Click Parking™

“Reduce parking times from 20mins to 30secs”

AppyParking Next Steps

“To supply autonomous vehicles with Last Meter Navigation ”

High Definition Data

London’s favourite parking app is now national.

WHERE DO WE COVER?

CURRENT PARTNERS

THANK YOU

Remarketing and De-Fleet

Rupert Pontin Director of Valuations at Glass’s

07/07/2016

Glass’s View on Technology in the Remarketing and Defleet Process Rupert Pontin – Director of Valuations

July 6th 2016

Reproduction and commercial distribution is strictly prohibited

Agenda

The Defleet Process

Defleet to Remarketing

Working Smarter

How Does Data Help

Summary

Reproduction and commercial distribution is strictly prohibited 207 07/07/2016

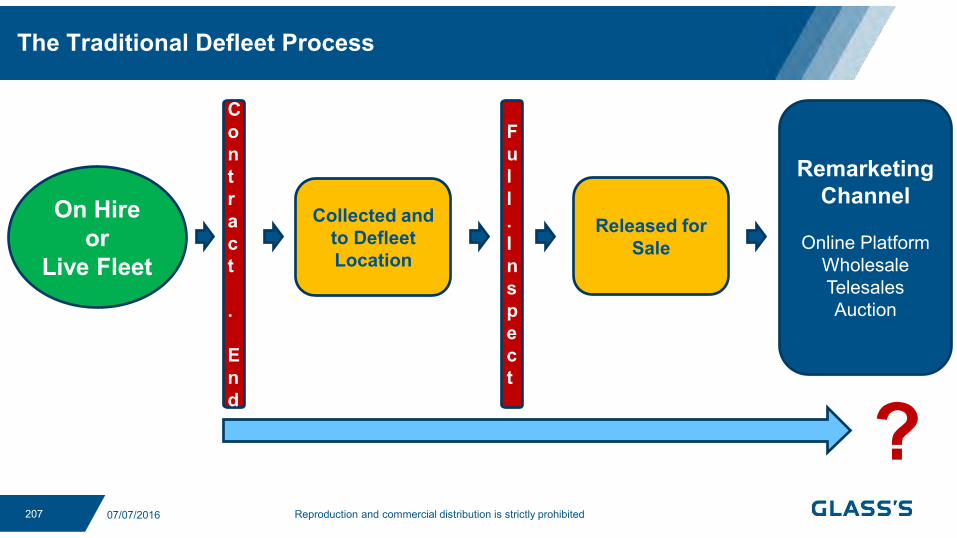

The Traditional Defleet Process

On Hire or

Live Fleet

Contract . End

Collected and to Defleet Location

Full.Inspect

Released for Sale

Remarketing Channel

Online Platform

Wholesale Telesales Auction

?

Reproduction and commercial distribution is strictly prohibited 208 07/07/2016

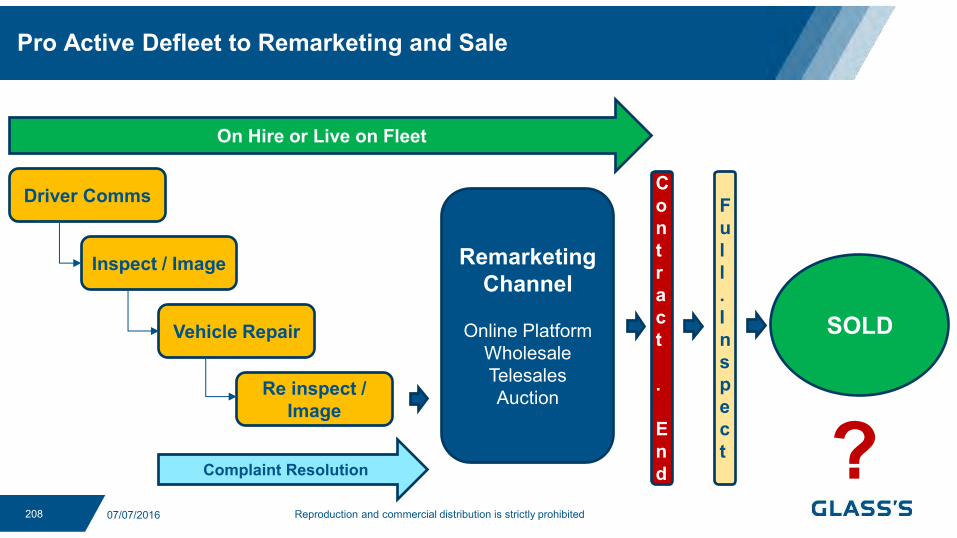

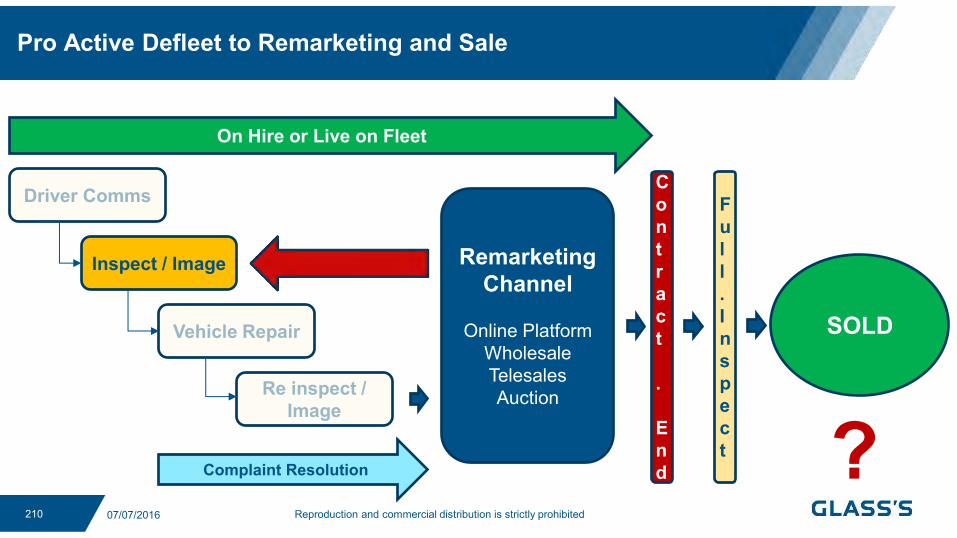

Pro Active Defleet to Remarketing and Sale

SOLD

Contract . End

Full.Inspect

Driver Comms

Remarketing Channel

Online Platform

Wholesale Telesales Auction

On Hire or Live on Fleet

?

Inspect / Image

Vehicle Repair

Re inspect / Image

Complaint Resolution

Reproduction and commercial distribution is strictly prohibited 209 07/07/2016

Choose Remarketing Partner Wisely Review Market Intelligence Technology Drives Success Professional Inspection Resource Online Automated Approval Processes Link Defleet and Wholesale Remarketing

to Retail Sale

Defleet to Remarketing and Sale

Reproduction and commercial distribution is strictly prohibited 210 07/07/2016

Pro Active Defleet to Remarketing and Sale

SOLD

Contract . End

Full.Inspect

Remarketing Channel

Online Platform

Wholesale Telesales Auction

On Hire or Live on Fleet

?

Inspect / Image

Complaint Resolution

Reproduction and commercial distribution is strictly prohibited 211 07/07/2016

Working Smarter – the full picture

Trade Sale

Retail Sale

Remarketing Channel

Online Platform

Wholesale Telesales Auction

Days to Sale – 42.9

Reproduction and commercial distribution is strictly prohibited 213 07/07/2016

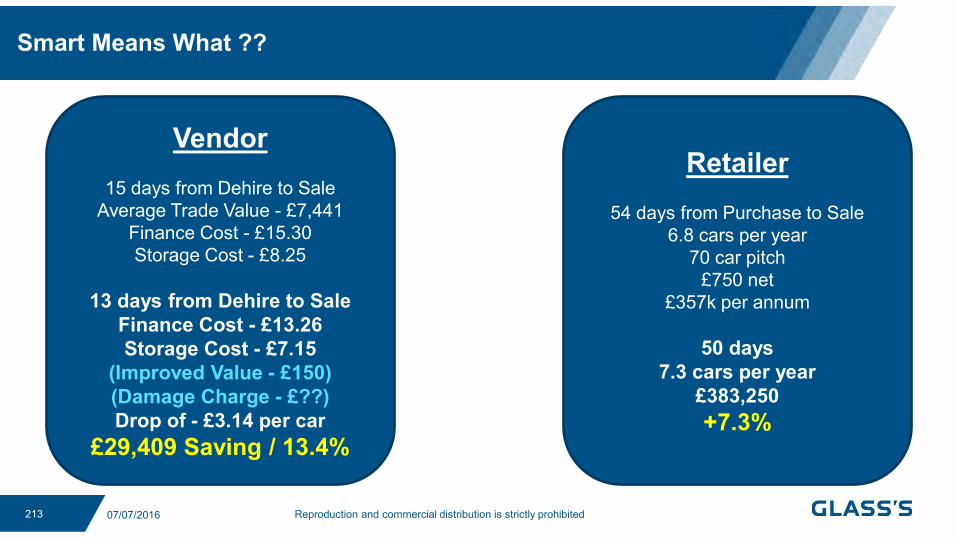

Smart Means What ??

Vendor

15 days from Dehire to Sale Average Trade Value - £7,441

Finance Cost - £15.30 Storage Cost - £8.25

13 days from Dehire to Sale

Finance Cost - £13.26 Storage Cost - £7.15

(Improved Value - £150) (Damage Charge - £??) Drop of - £3.14 per car

£29,409 Saving / 13.4%

Retailer

54 days from Purchase to Sale 6.8 cars per year

70 car pitch £750 net

£357k per annum

50 days 7.3 cars per year

£383,250 +7.3%

Reproduction and commercial distribution is strictly prohibited 214 07/07/2016

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2014 2015 2016

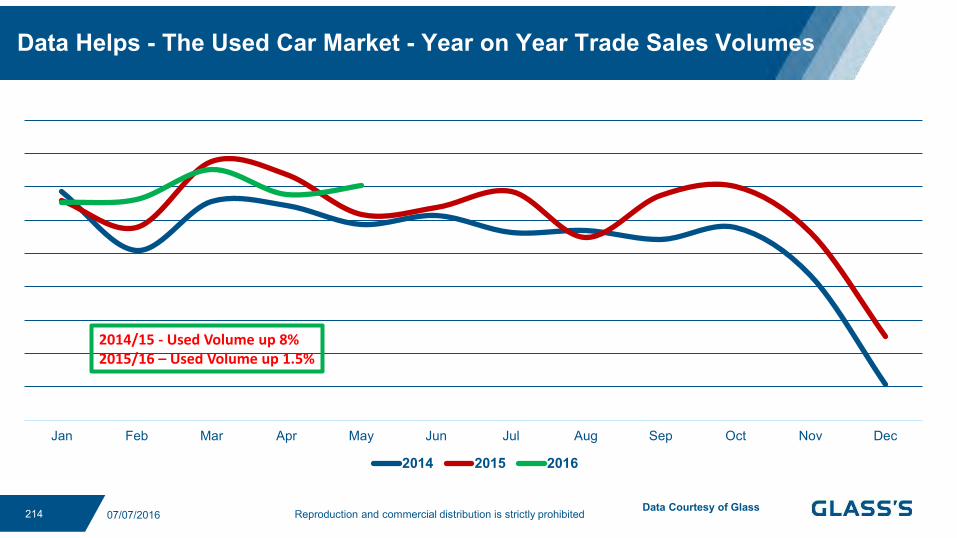

Data Helps - The Used Car Market - Year on Year Trade Sales Volumes

Data Courtesy of Glass

2014/15 - Used Volume up 8% 2015/16 – Used Volume up 1.5%

Reproduction and commercial distribution is strictly prohibited 215 07/07/2016

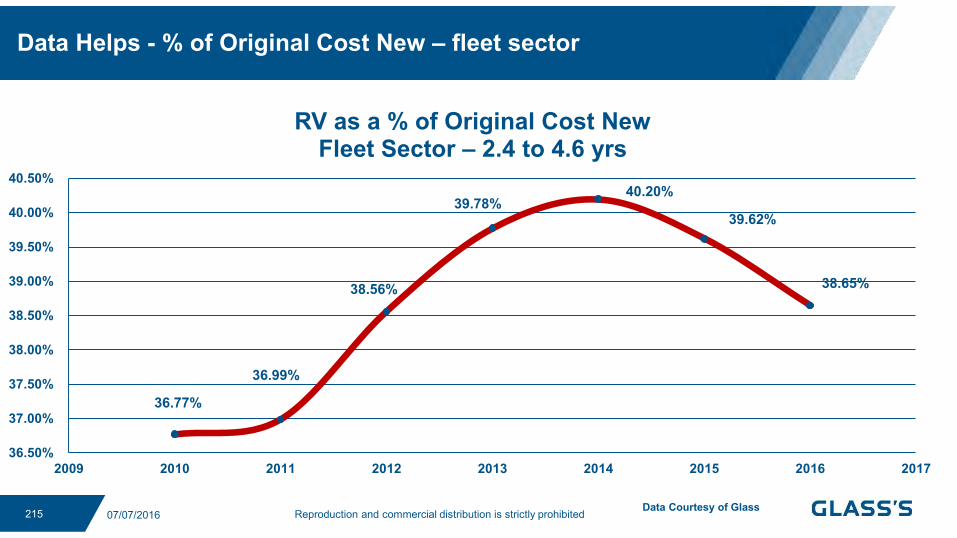

Data Helps - % of Original Cost New – fleet sector

36.77%

36.99%

38.56%

39.78% 40.20%

39.62%

38.65%

36.50%

37.00%

37.50%

38.00%

38.50%

39.00%

39.50%

40.00%

40.50%

2009 2010 2011 2012 2013 2014 2015 2016 2017

RV as a % of Original Cost New Fleet Sector – 2.4 to 4.6 yrs

Data Courtesy of Glass

Reproduction and commercial distribution is strictly prohibited 216 07/07/2016

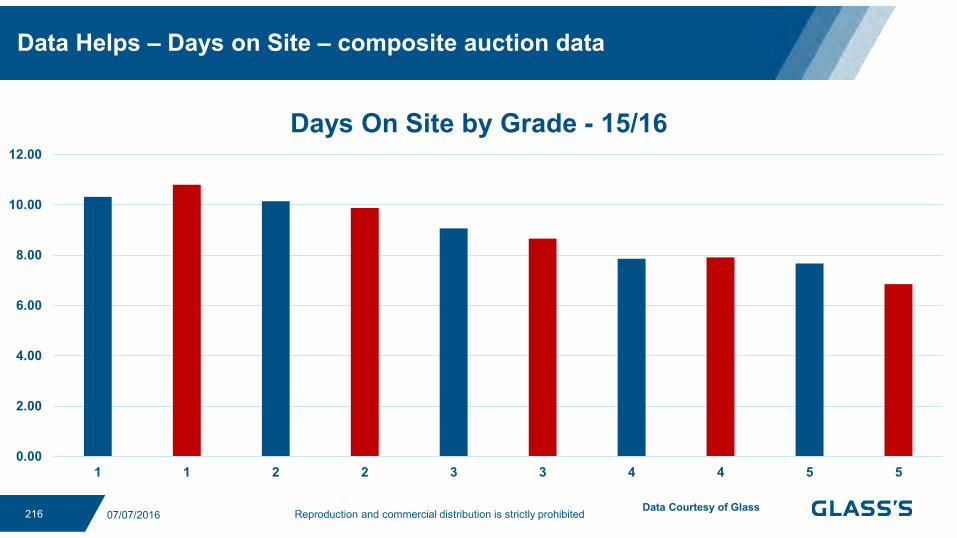

Data Helps – Days on Site – composite auction data

0.00

2.00

4.00

6.00

8.00

10.00

12.00

1 1 2 2 3 3 4 4 5 5

Days On Site by Grade - 15/16

Data Courtesy of Glass

Reproduction and commercial distribution is strictly prohibited 217 07/07/2016

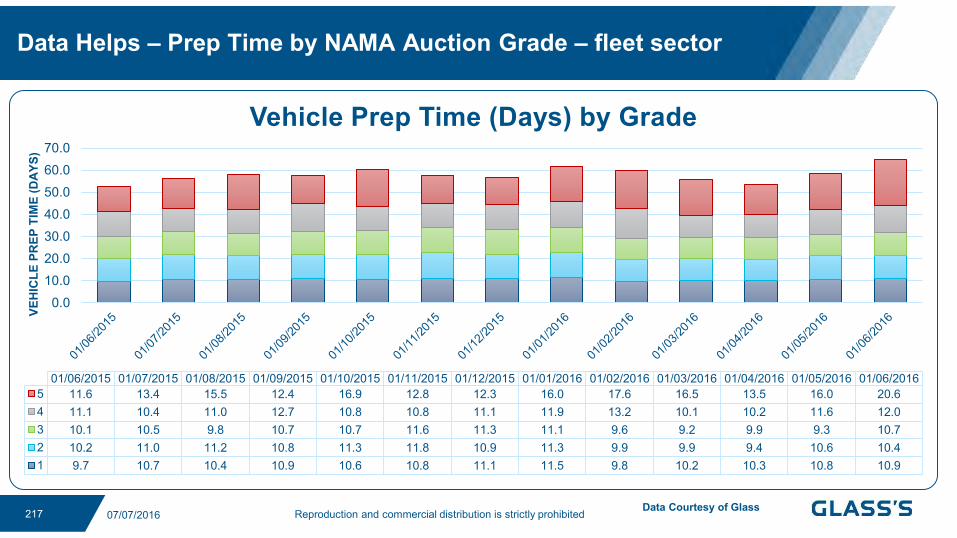

Data Helps – Prep Time by NAMA Auction Grade – fleet sector

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

VEH

ICLE

PR

EP T

IME

(DA

YS)

01/06/2015 01/07/2015 01/08/2015 01/09/2015 01/10/2015 01/11/2015 01/12/2015 01/01/2016 01/02/2016 01/03/2016 01/04/2016 01/05/2016 01/06/20165 11.6 13.4 15.5 12.4 16.9 12.8 12.3 16.0 17.6 16.5 13.5 16.0 20.64 11.1 10.4 11.0 12.7 10.8 10.8 11.1 11.9 13.2 10.1 10.2 11.6 12.03 10.1 10.5 9.8 10.7 10.7 11.6 11.3 11.1 9.6 9.2 9.9 9.3 10.72 10.2 11.0 11.2 10.8 11.3 11.8 10.9 11.3 9.9 9.9 9.4 10.6 10.41 9.7 10.7 10.4 10.9 10.6 10.8 11.1 11.5 9.8 10.2 10.3 10.8 10.9

Vehicle Prep Time (Days) by Grade

Data Courtesy of Glass

Reproduction and commercial distribution is strictly prohibited 219 07/07/2016

Trade to Retail Journey – June 2016

Trade Sale £7,441

Prep Time 10.9

Retail Asking £9,382

Stock Days 42.9

Retail Transacted £9,164

Retail Margin 23.1%

Journey from trade auction to retail forecourt sale*

June 2016

Data Courtesy of Glass

Reproduction and commercial distribution is strictly prohibited 220 07/07/2016

Summary

• Remarketing Partners Drive Defleet Speed

• Technology Advances – better linking and partnerships

• Brexit Impact is NOT Evident

• Downward Pressure on Values from Volume

• Recession is a Possibility

Quicker Defleet Processes and Market Insight are Critical for Success as we head Post Brexit……

Volvo Car UK: Connected Car Vision

Kevin Meeks Head of Internal Communication and

New Car Launches

Volvo vision 2020 SAFETY IN A CONNECTED WORLD

Kevin Meeks

Volvo Car UK Limited

"Cars are driven by people. The guiding principle behind everything we make at Volvo, therefore, is – and must remain – safety.” Assar Gabrielsson and Gustav Larsson,1927

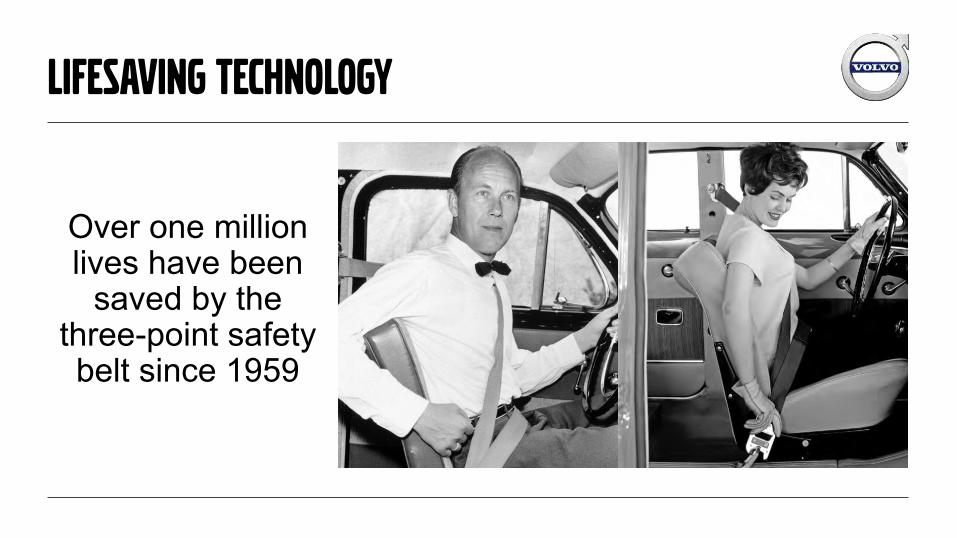

Over one million lives have been

saved by the three-point safety belt since 1959

Lifesaving technology

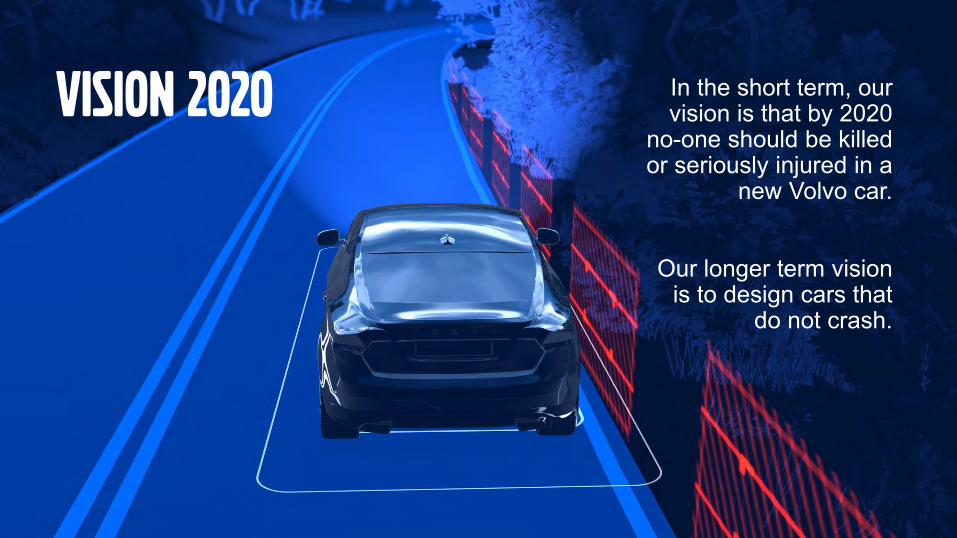

Vision 2020 In the short term, our vision is that by 2020

no-one should be killed or seriously injured in a

new Volvo car.

Our longer term vision is to design cars that

do not crash.

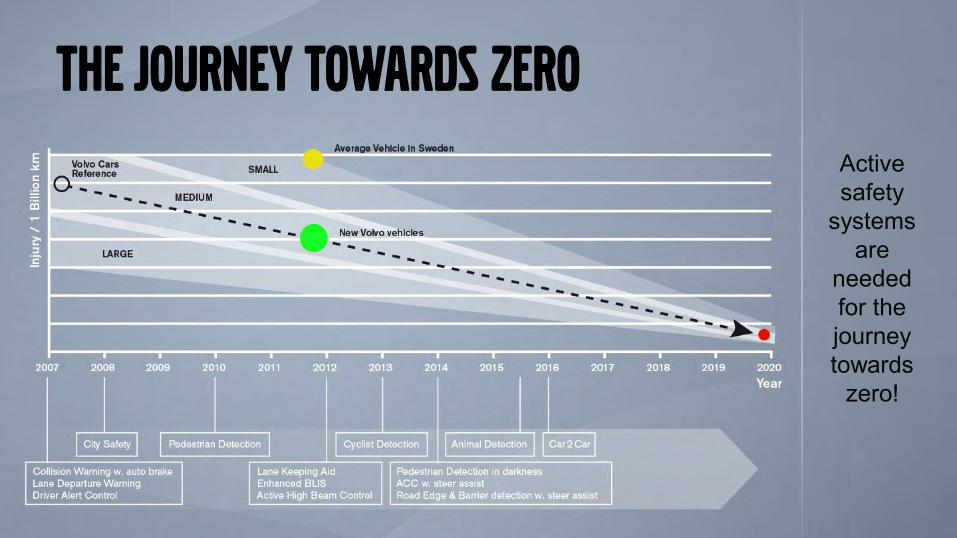

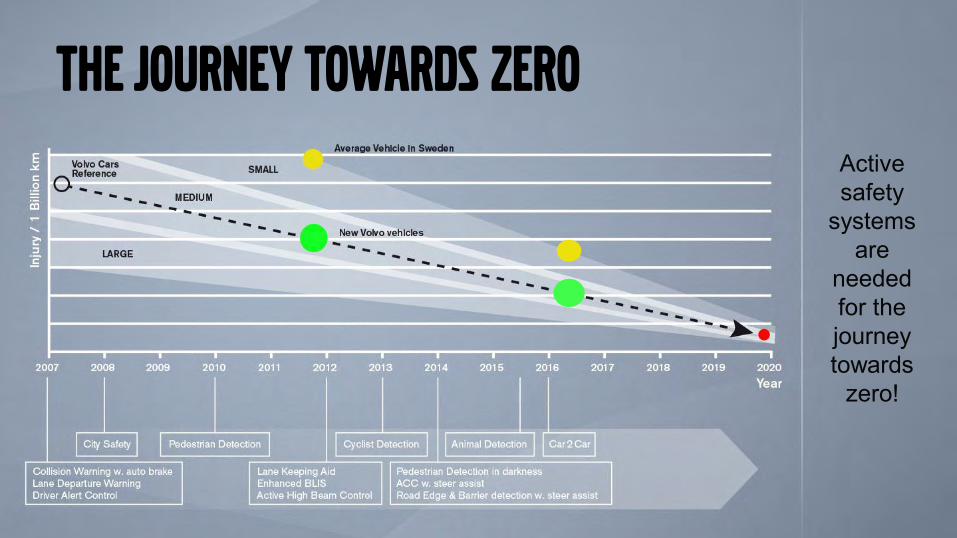

The journey towards zero

Active safety

systems are

needed for the journey towards

zero!

The journey towards zero

Active safety

systems are

needed for the journey towards

zero!

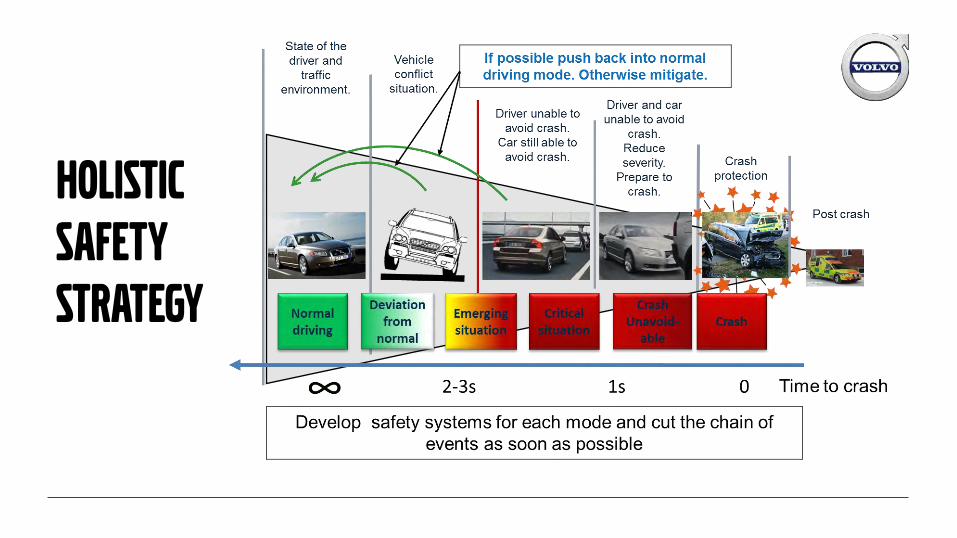

holistic

safety

strategy

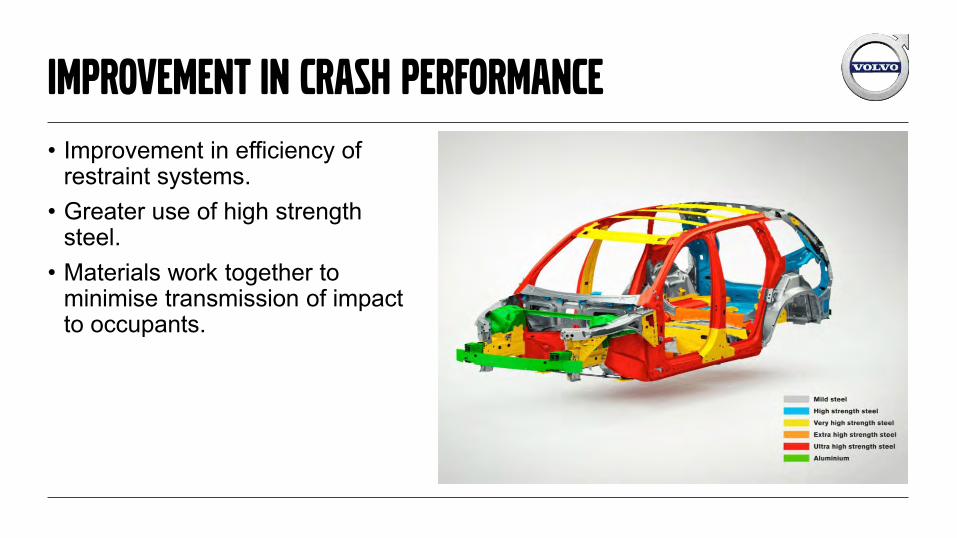

• Improvement in efficiency of restraint systems.

• Greater use of high strength steel.

• Materials work together to minimise transmission of impact to occupants.

Improvement in crash performance

• Road accidents are reducing. • Statistical analysis becomes more difficult. • Unusual types of accident gain higher priority

for analysis. • For example – run off road accidents.

Accidents are changing

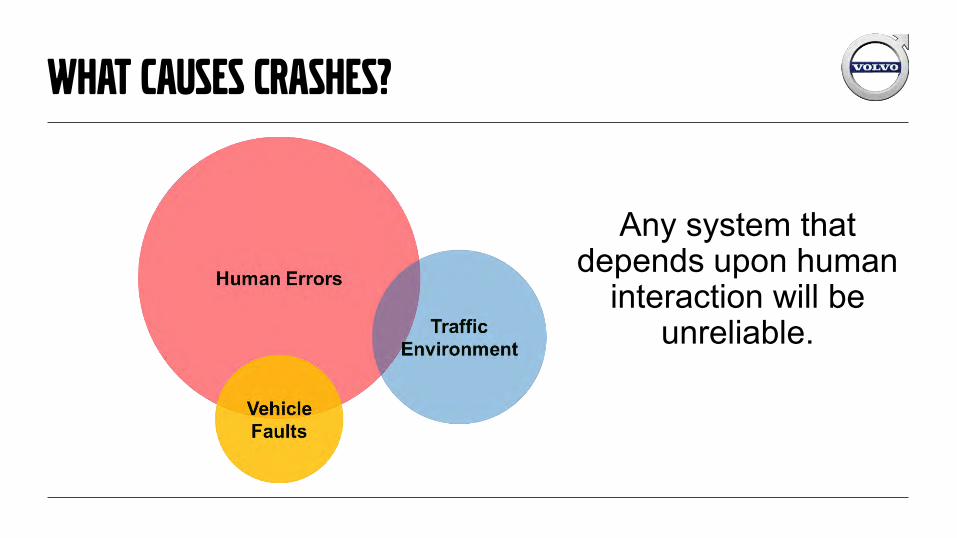

Any system that depends upon human

interaction will be unreliable.

What causes crashes?

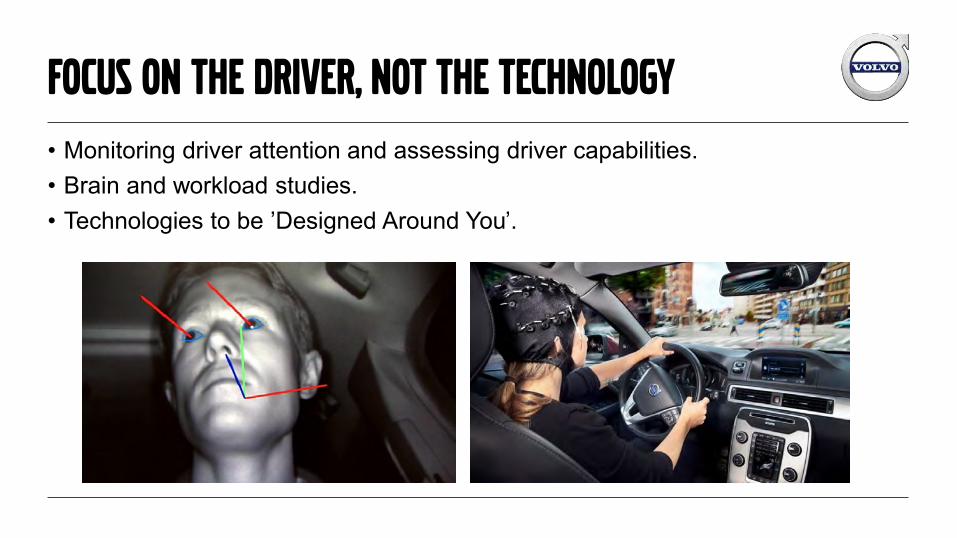

• Monitoring driver attention and assessing driver capabilities. • Brain and workload studies. • Technologies to be ’Designed Around You’.

Focus on the driver, not the technology

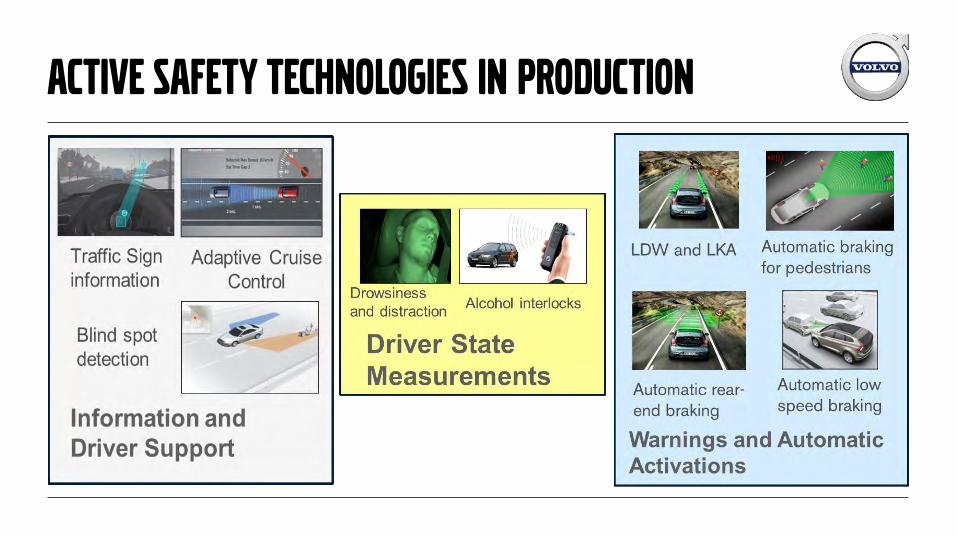

Active safety technologies in production

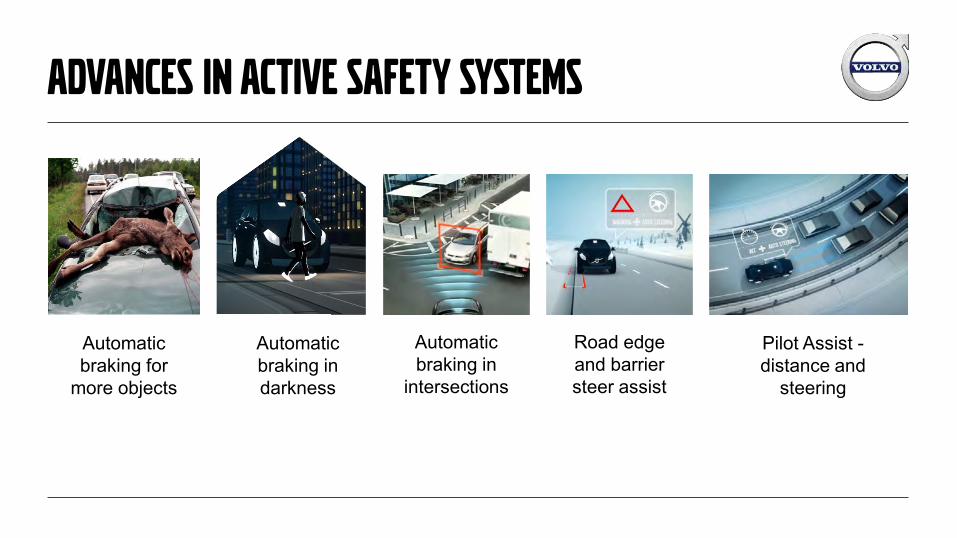

Advances in active safety systems

Automatic braking for

more objects

Automatic braking in darkness

Automatic braking in

intersections

Road edge and barrier steer assist

Pilot Assist - distance and

steering

Pilot assist Semi-autonomous driving

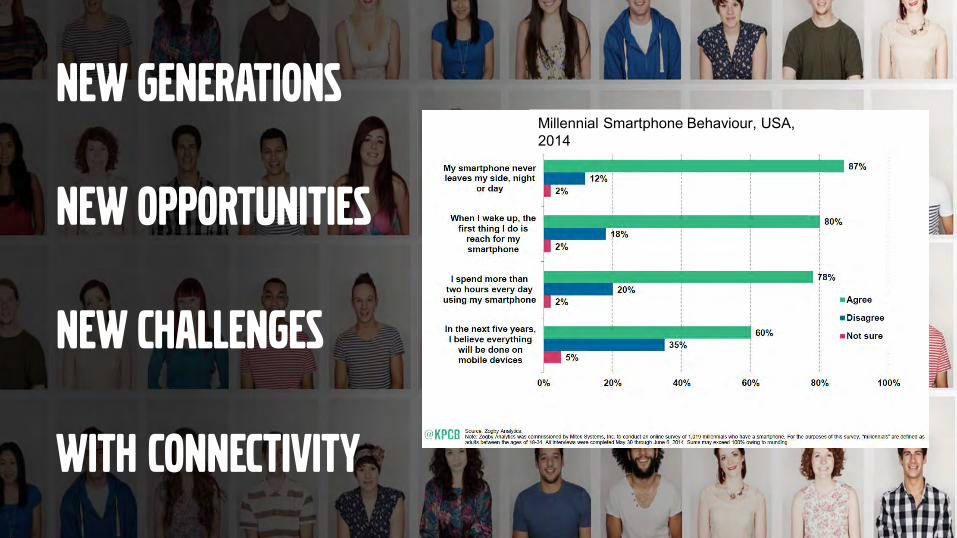

New generations

new opportunities

new challenges

with connectivity

New generations

new opportunities

new challenges

with connectivity

Millennial Smartphone Behaviour, USA, 2014

Autonomous driving The future

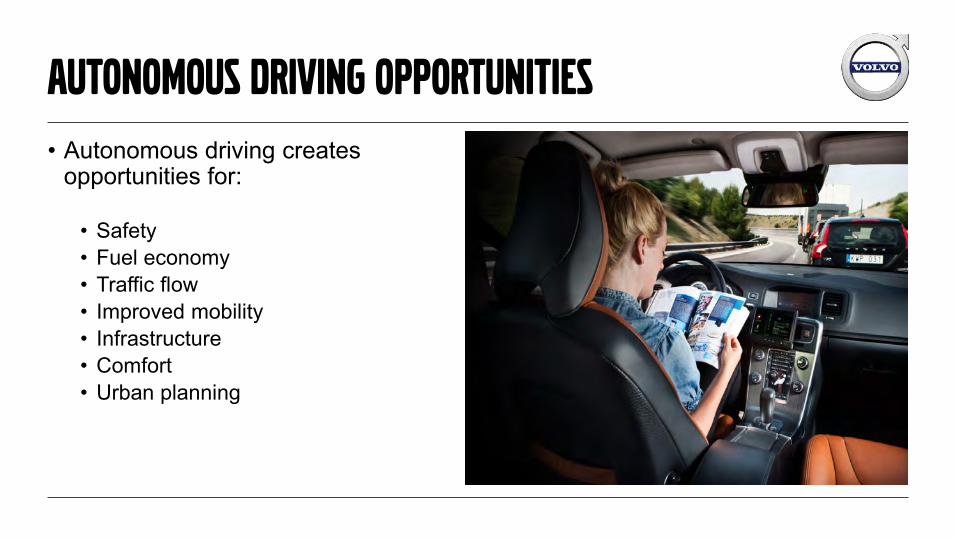

• Autonomous driving creates opportunities for:

• Safety • Fuel economy • Traffic flow • Improved mobility • Infrastructure • Comfort • Urban planning

Autonomous driving opportunities

• The world’s first large scale project for self-driving cars

• Project started in 2014 • Self-driving cars on public

roads in 2017 • 100 customer cars • 30 miles highway / max

speed 50 mph

Drive me project

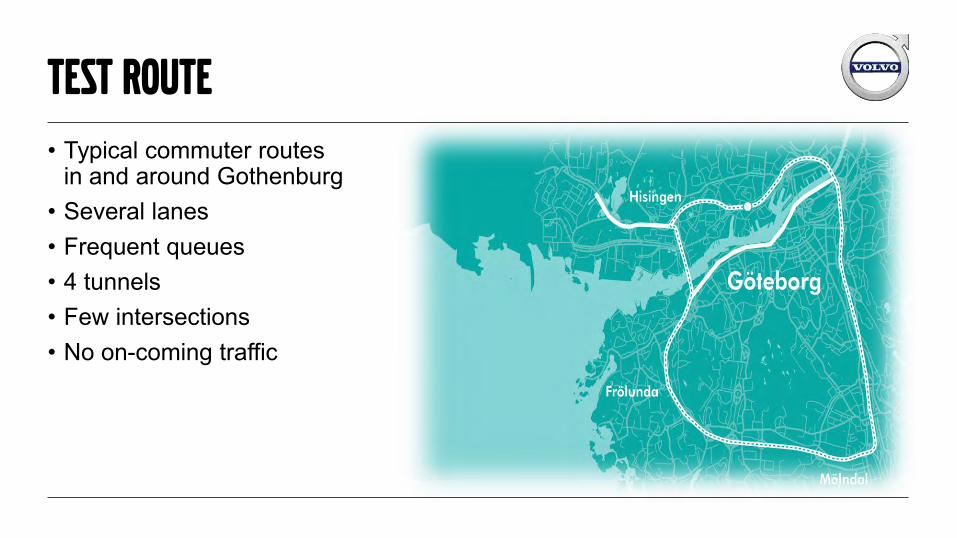

• Typical commuter routes in and around Gothenburg

• Several lanes • Frequent queues • 4 tunnels • Few intersections • No on-coming traffic

Test route

• Commencing 2017. • Initially a limited number of semi-autonomous cars. • Expanding in 2018 to include autonomous cars. • The largest and most extensive AD test programme on UK roads.

• So what could the future hold?

Drive me london

• Can be steered actively with the farmer in full control.

• Can handle situations where the farmer is out of the loop and still find its way home.

• Won’t accept being steered into a tree or off a cliff.

The car of tomorrow – like the farmer’s horse

Thank you

Chairman’s Closing Comments

Peter Cakebread Managing Director at Marshall Leasing

Conference Close Tea / Coffee and Networking

Thank you to all our speakers, sponsors

and exhibitors for contributing to this event.

Safe journey home.