Embed Size (px)

Citation preview

Serving Up the “Starbucks Experience” and Energizing Growth through Value Chain Optimization

Presented by:

GMA Executive Conference I August 27, 2012

Daryl Brewster Founder & CEO Brookside Management, LLC

Kate Newlin Principal & Founder Kate Newlin Consulting

Ric Schneider SVP, Global Procurement Starbucks Coffee Company

Dr. Mary Wagner SVP, Global R&D/ Quality & Regulatory Starbucks Coffee Company

Growing in Slow Growth Economy

“Low Growth in

Earnings is Expected” – Christine Hauser, April 5, 2012

The Brookside Growth Council

“Fed Officials Sees Lower U.S.

Growth, Slow Progress On Jobs”

“Slow growth predicted

for U.S. economy”

2

Agenda

Growth Benchmarking

Growth Drivers

Growth Case Study

Q&A

The Brookside Growth Council 3

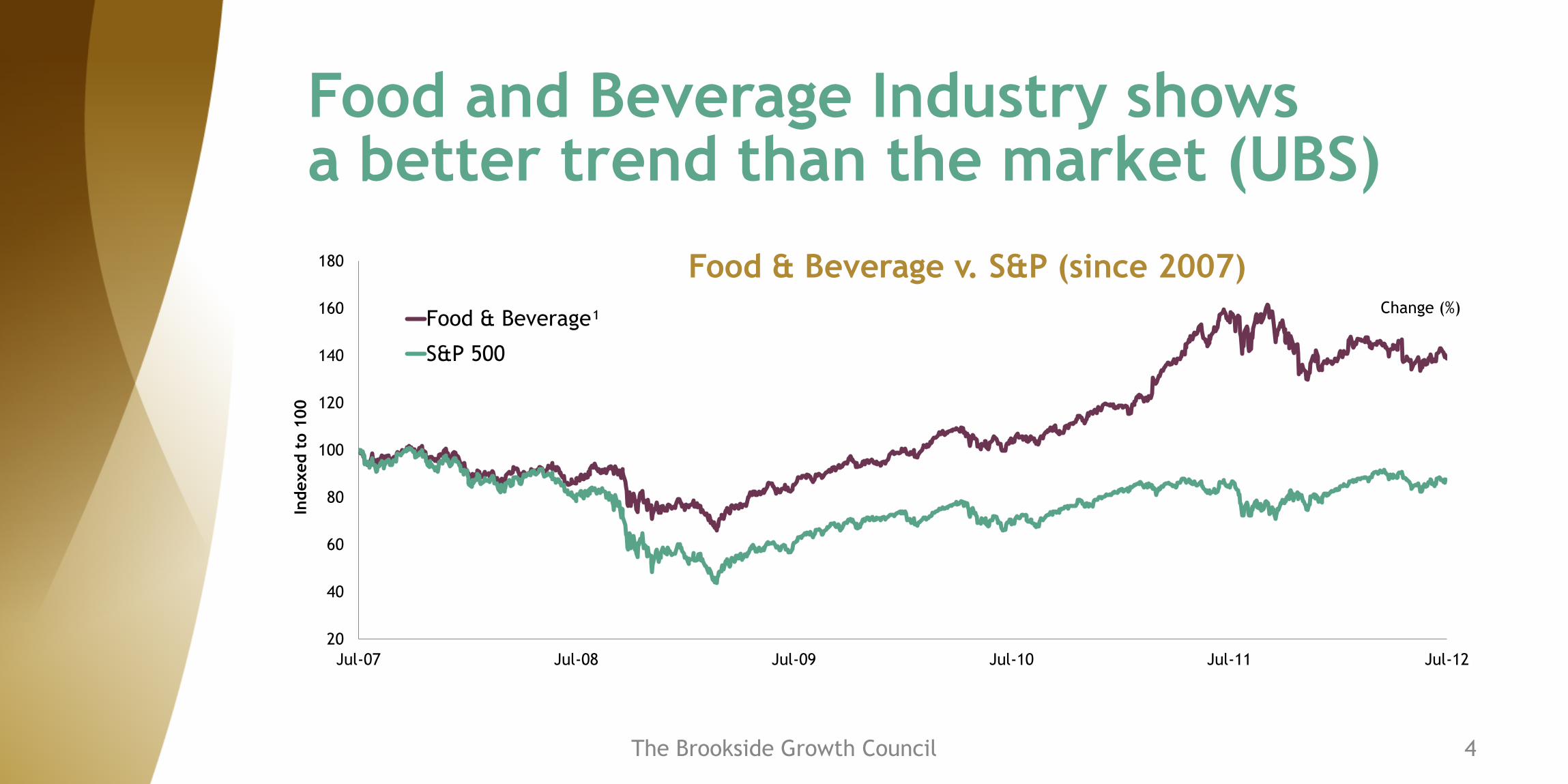

Food and Beverage Industry shows a better trend than the market (UBS)

Change (%)

20

40

60

80

100

120

140

160

180

Jul-07 Jul-08 Jul-09 Jul-10 Jul-11 Jul-12

Indexed t

o 1

00

Food & Beverage v. S&P (since 2007)

Food & Beverage¹

S&P 500

The Brookside Growth Council 4

Five Delivered Gold-Medal Growth More than 5 X Total Shareholder Return (TSR= stock appreciation + dividends since 2000; F&B, Other CPG, Retailers)

The Brookside Growth Council 5

5 More Earned Growth Silvers 3 to 5 X Total Shareholder Return (TSR= stock appreciation + dividends since 2000; F&B, other CPG, Retailers)

The Brookside Growth Council 6

Key Drivers of Growth Champions

Passion for Growth

From the Top

Entrepreneurial spirit throughout the Value Chain

Internal & External

The Brookside Growth Council 7

Key Drivers of Growth Champions

Passion for Growth

Aligned with Consumer Trends

Growing Global Middle Class (Nestle, Coke)

Bifurcation in US (Ralcorp & Hain; DG & WF)

Responsive to Consumer Trends throughout the Value Chain

Expansion: channels, geographies

Marketing

M&A

The Brookside Growth Council 8

Key Drivers of Growth Champions

Passion for Growth

Aligned with Consumer Trends

Innovation (incremental & breakthrough)

New ways of looking at old categories (IRI Pacesetters ‘06-’11)

Calorie counts: Nabisco 100, MGD 64, Bud 55, Trop 50

Category X-Overs: Cracker Chips, M&M Pretzels, Bailey’s Creamers

Restaurant to Retail: SBUX, Dunkin’ Donuts, PF Chang Meals

The Brookside Growth Council 9

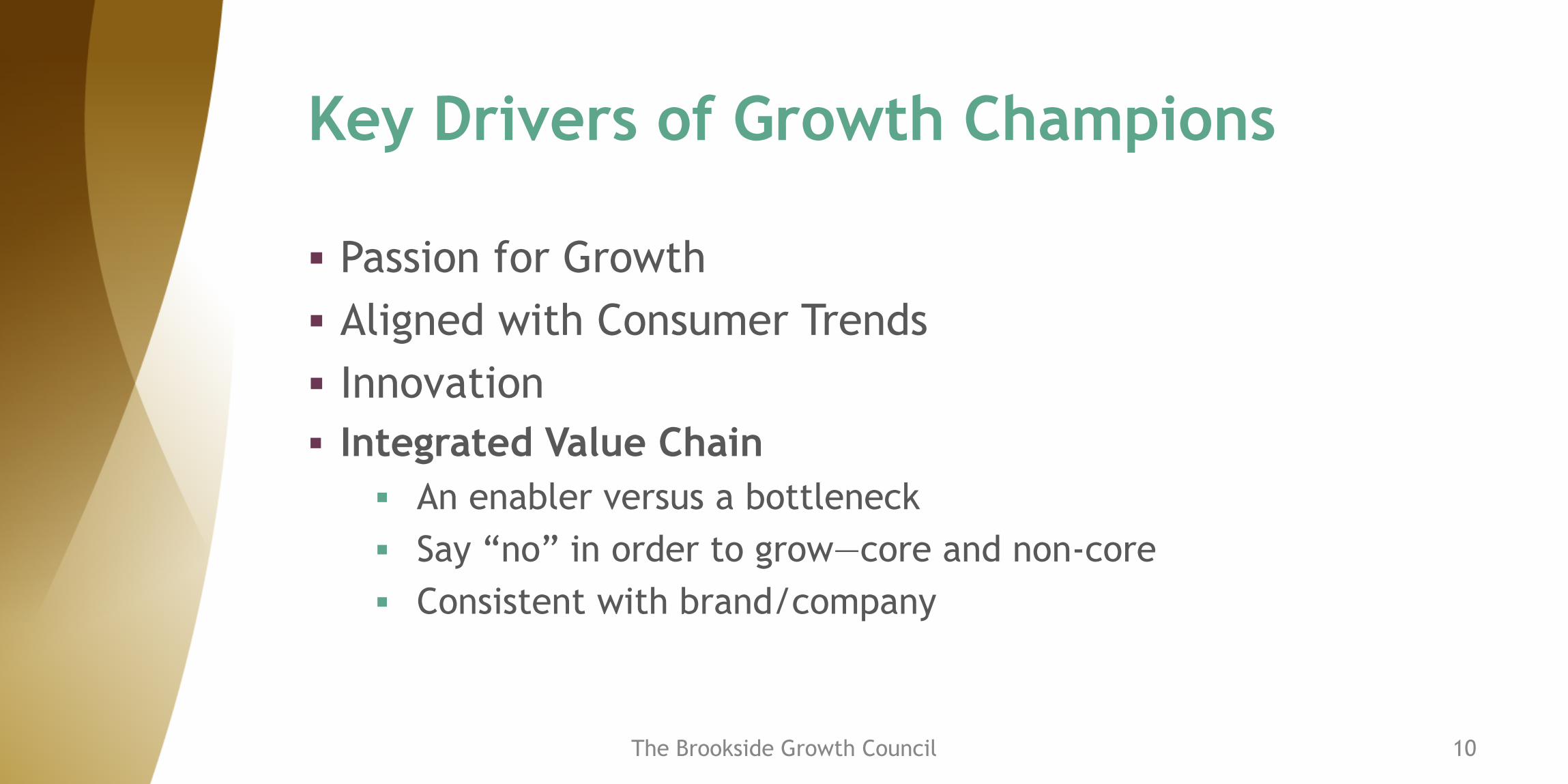

Key Drivers of Growth Champions

Passion for Growth

Aligned with Consumer Trends

Innovation

Integrated Value Chain

An enabler versus a bottleneck

Say “no” in order to grow—core and non-core

Consistent with brand/company

The Brookside Growth Council 10

Case Study – Starbucks

The Brookside Growth Council 11

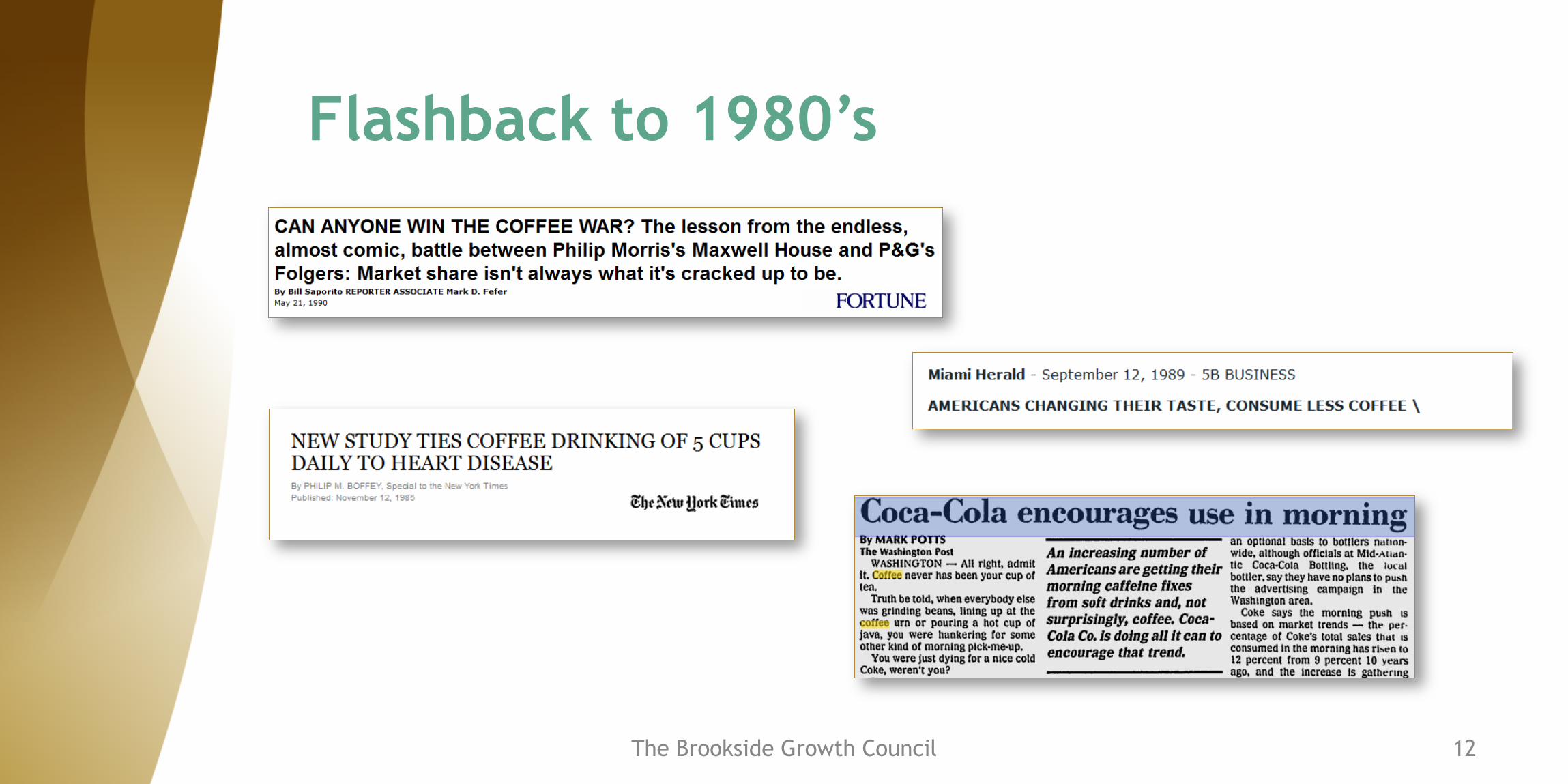

Flashback to 1980’s

The Brookside Growth Council 12

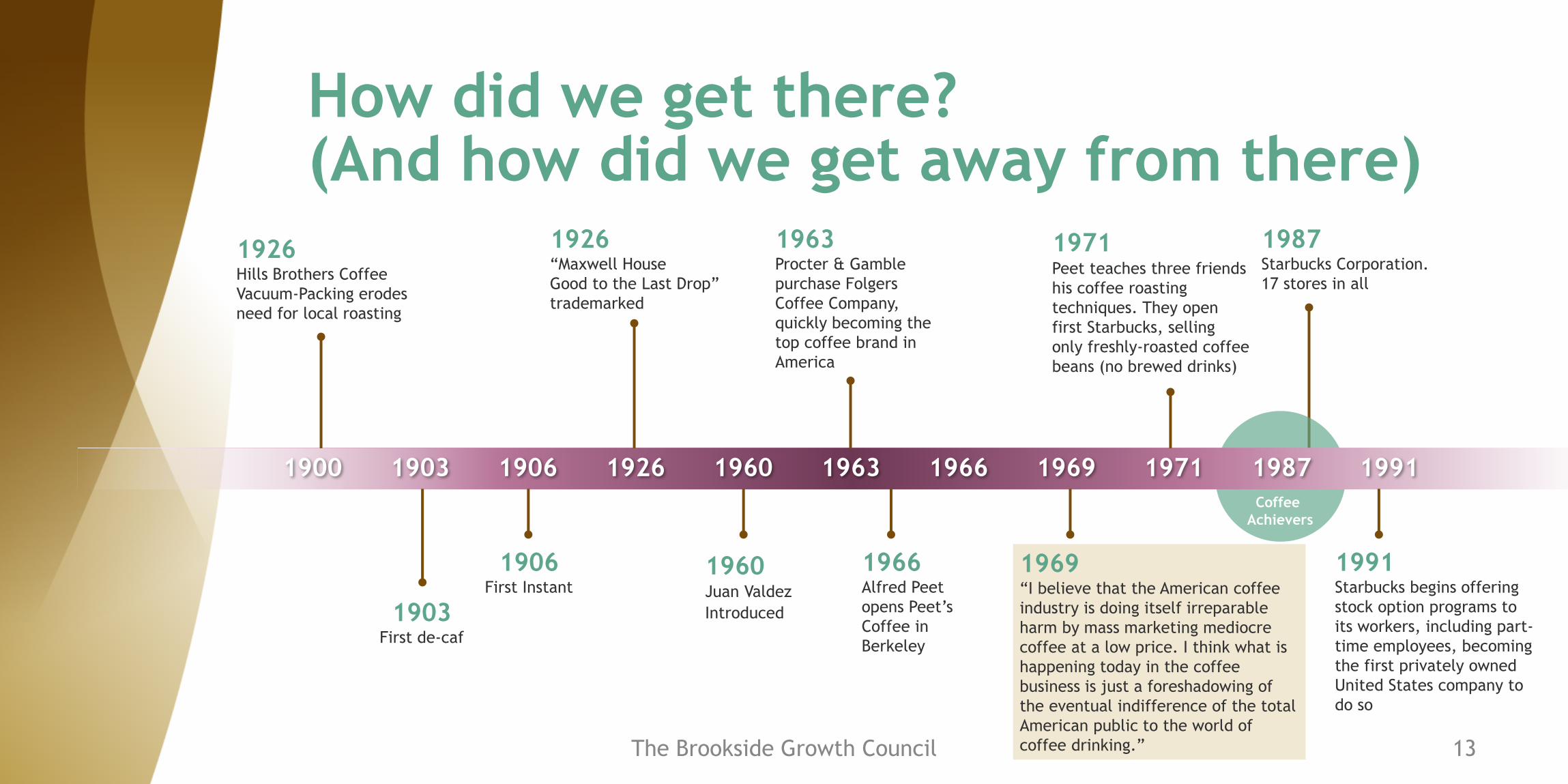

How did we get there? (And how did we get away from there)

1926 Hills Brothers Coffee

Vacuum-Packing erodes

need for local roasting

1900 1903

1926 “Maxwell House

Good to the Last Drop”

trademarked

1960 Juan Valdez

Introduced

1963 Procter & Gamble

purchase Folgers

Coffee Company,

quickly becoming the

top coffee brand in

America

1969 “I believe that the American coffee

industry is doing itself irreparable

harm by mass marketing mediocre

coffee at a low price. I think what is

happening today in the coffee

business is just a foreshadowing of

the eventual indifference of the total

American public to the world of

coffee drinking.”

1966 Alfred Peet

opens Peet’s

Coffee in

Berkeley

1971 Peet teaches three friends

his coffee roasting

techniques. They open

first Starbucks, selling

only freshly-roasted coffee

beans (no brewed drinks)

1987 Starbucks Corporation.

17 stores in all

1991 Starbucks begins offering

stock option programs to

its workers, including part-

time employees, becoming

the first privately owned

United States company to

do so

1903 First de-caf

1906

1906 First Instant

1926 1960 1963 1966 1969 1971 1987 1991

Coffee

Achievers

The Brookside Growth Council 13

Coffee Achiever’s Campaign

The Brookside Growth Council 14

“Personality is an unbroken series of

successful gestures; see also Starbucks”

- F. Scott Fitzgerald

The Brookside Growth Council 15

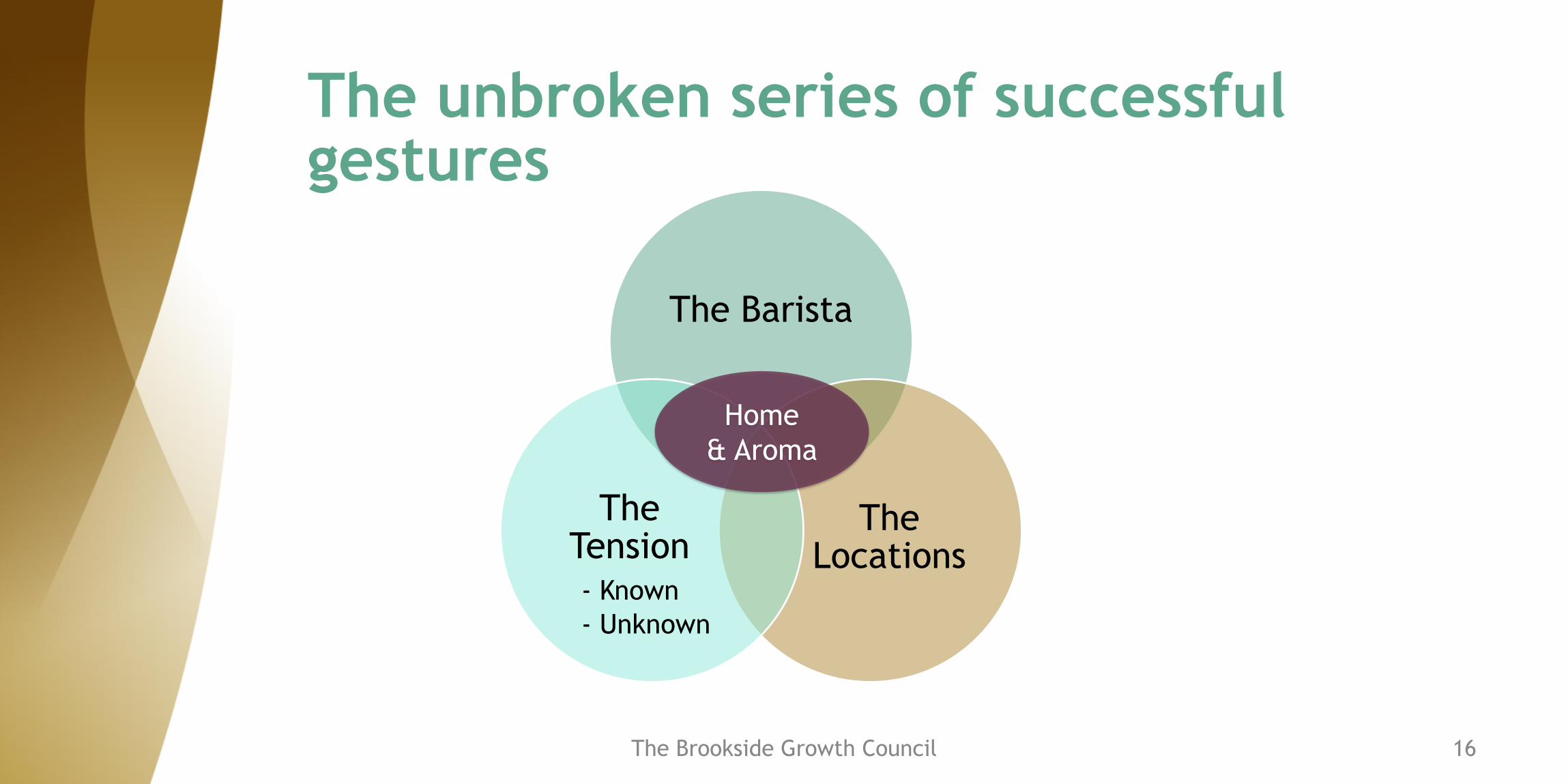

The unbroken series of successful gestures

The Barista

The Locations

The Tension

- Known

- Unknown

Home

& Aroma

The Brookside Growth Council 16