Embed Size (px)

Citation preview

Services Sector Liberalization, Employment and Growth: A

CGE AnalysisBased on Shantong LI, Yan WANG, and Fan

ZHAI’s [email protected]

Prepared for the Senior Policy Seminar on “China’s Service Sector in the Post WTO Era”

Beijing, ChinaSeptember 22-24, 2003

2

Outline• Why liberalize the service sector?• Trade in services a part of growth and poverty

reduction strategy, China

• How have other countries committed / liberalized? Thailand and China

• Impact of China’s service liberalization-CGE analysis

• Summary• Annex on banking services

3

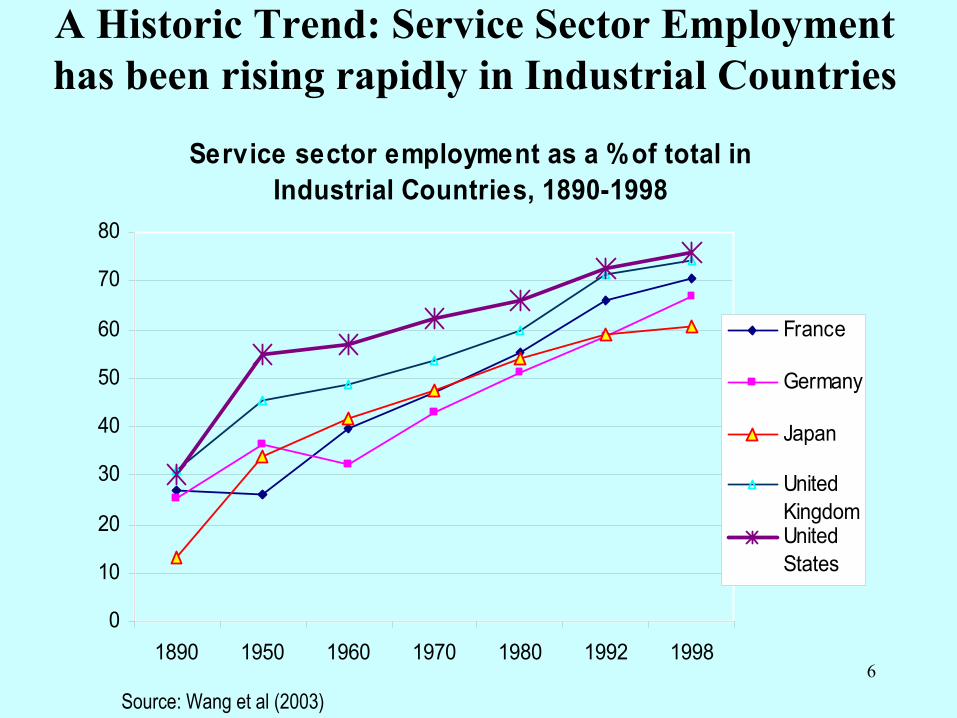

I. Why do services matter?• Services account for more than 50 percent of

output and employment. These ratios are higher for industrial countries (see charts)

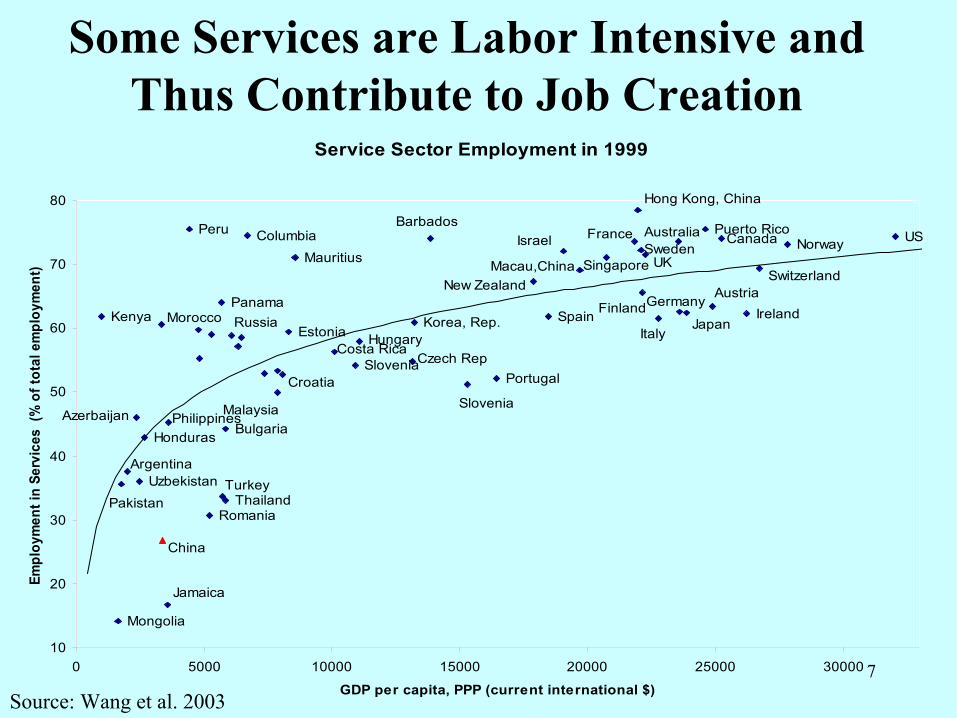

• Some services are low-skilled labor intensive such as tourism and personal services. Thus the expansion of these services are conducive to job creation and poverty reduction.

• Producer and distributive services are crucial for the competitiveness of the goods-export sector, as well as for the economic growth in general.

4

A classification of servicesElfring(1989) divided services into 4 categories: • Producer Services(business and professional

services, financial services, insurance services and real estate services, etc.),

• Distributive Services(retail trade, wholesale trade, transport and communications, etc.),

• Personal Services(hotels, restaurants, tourism, recreation and amusements, etc.) and

• Social Services(government proper, health services, educational services and miscellaneous social services).

5

Why open the service sector• The service sector has the ability to absorb more labor,

as some subsectors are labor intensive and can employ more low- or high-skilled workers.

• Services as engine of growth: since deeper division of labor and specialization contribute to competitiveness and higher productivity

• Liberalization in service may generate sizable gains– A) Standard gains from trade and specialization;– B) Services as intermediate input—better services for the

goods sector; – C) Gains from FDI as a means for trade --learning-by-doing.

6

A Historic Trend: Service Sector Employment has been rising rapidly in Industrial Countries

Service sector employment as a % of total in Industrial Countries, 1890-1998

0

10

20

30

40

50

60

70

80

1890 1950 1960 1970 1980 1992 1998

France

Germany

Japan

UnitedKingdomUnitedStates

Source: Wang et al (2003)

7

Some Services are Labor Intensive and Thus Contribute to Job Creation

Source: Wang et al. 2003

Service Sector Employment in 1999

Kenya MoroccoPanamaRussia

EstoniaCosta Rica

Slovenia

Portugal

Korea, Rep.

AzerbaijanBulgaria

RomaniaThailand

UzbekistanArgentina

Pakistan

Mongolia

IrelandJapan

ItalySpain

Mauritius

Peru

Singapore UK

Puerto Rico

Hong Kong, China

Switzerland

Norway US

Macau,ChinaNew Zealand

Turkey

Philippines

Croatia

Czech RepSlovenia

ColumbiaBarbados

Israel Canada

Honduras

AustraliaFranceSweden

Malaysia

China

Germany Austria

Hungary

Finland

Jamaica

10

20

30

40

50

60

70

80

0 5000 10000 15000 20000 25000 30000

GDP per capita, PPP (current international $)

Empl

oym

ent i

n Se

rvic

es (

% o

f tot

al e

mpl

oym

ent)

8

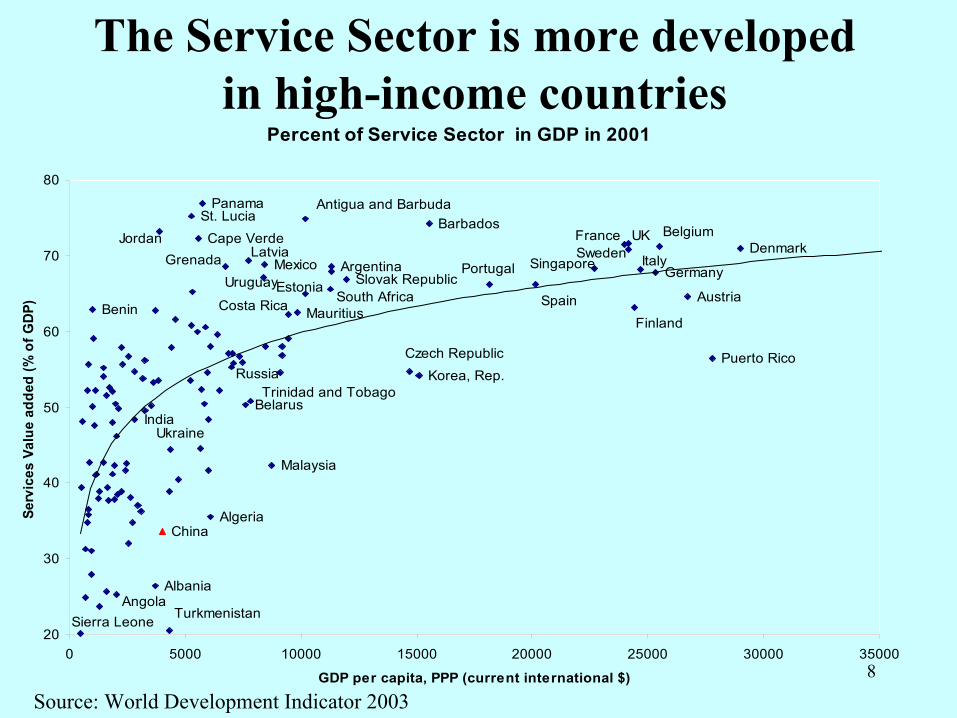

The Service Sector is more developed in high-income countries

Source: World Development Indicator 2003

Percent of Service Sector in GDP in 2001

India

Russia

Ukraine

Belarus

AngolaAlbania

Algeria

Malaysia

Benin

Grenada LatviaMexico

Cape VerdeJordanSt. Lucia

Panama

Estonia

Czech Republic

Costa Rica MauritiusSpain

Portugal SingaporeSweden

UK

ItalySlovak Republic

South Africa

Sierra Leone

France

China

Denmark

Germany

Finland

Belgium

Antigua and BarbudaBarbados

Argentina

Trinidad and Tobago

Turkmenistan

Puerto Rico

Austria

Korea, Rep.

Uruguay

20

30

40

50

60

70

80

0 5000 10000 15000 20000 25000 30000 35000

GDP per capita, PPP (current international $)

Serv

ices

Val

ue a

dded

(% o

f GDP

)

9

II. Liberalizing services a part of growth &poverty reduction strategy

Services account for 33% of GDP in China, 29% of total employment in 2002, lagging behind other industrial and developing countries.

• Expanding Job opportunities– Facilitating the private sector development– Expanding export (both goods and services)– Expanding tourism (a part of services)

• Maintaining Macro Stability– by Deepening banking reform

• Improving Capacities– education and health

• Strengthening governance, etc

10

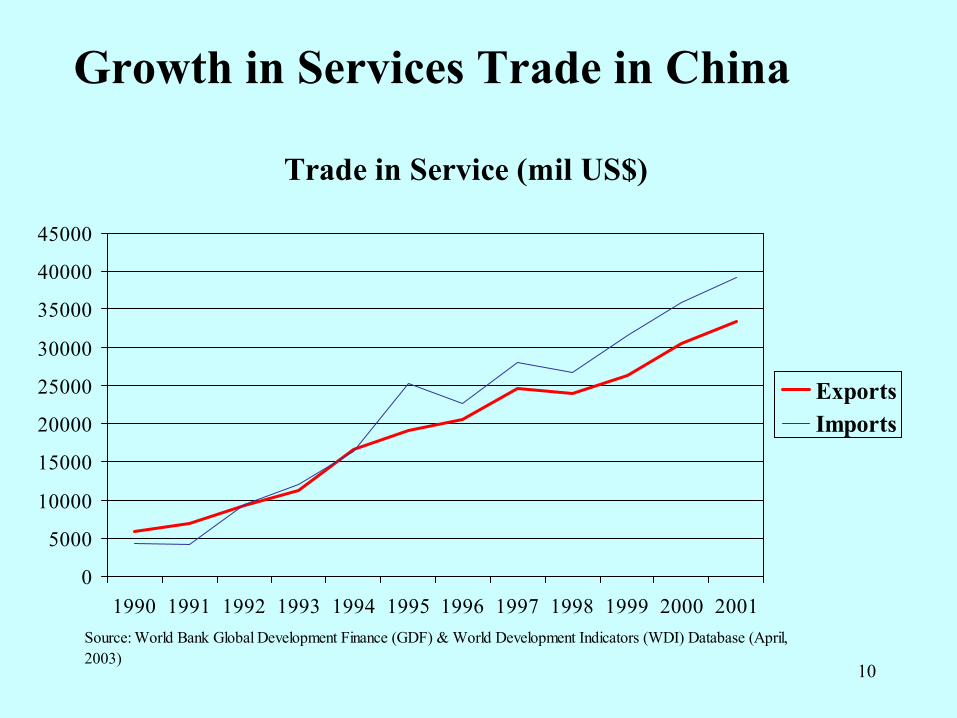

Growth in Services Trade in China

Trade in Service (mil US$)

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001Source: World Bank Global Development Finance (GDF) & World Development Indicators (WDI) Database (April, 2003)

ExportsImports

11

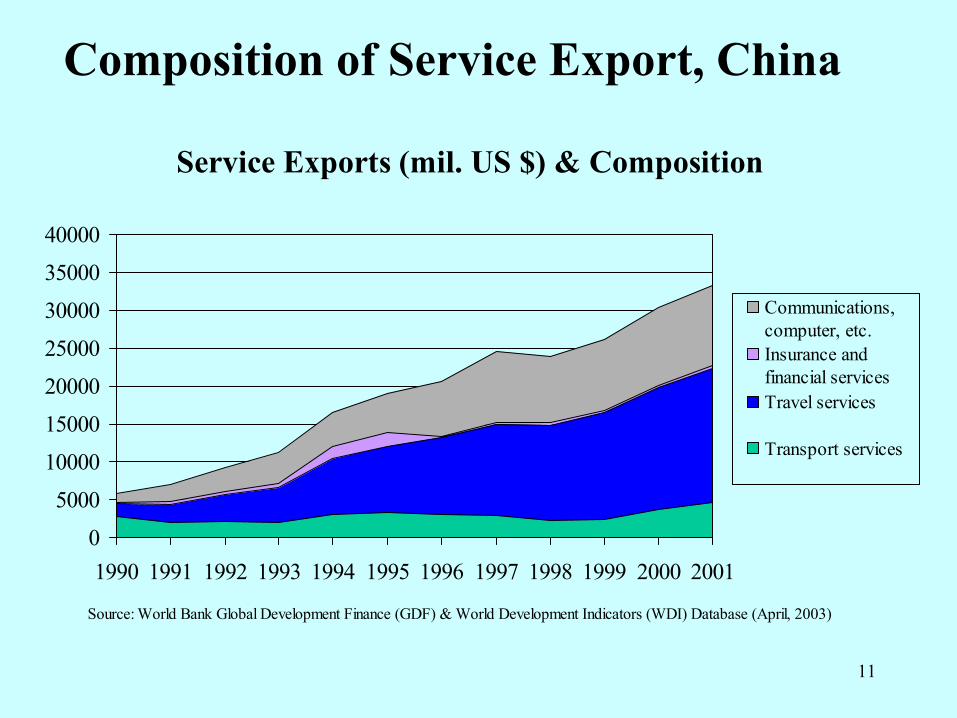

Composition of Service Export, China

Service Exports (mil. US $) & Composition

0

5000

10000

15000

20000

25000

30000

35000

40000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Source: World Bank Global Development Finance (GDF) & World Development Indicators (WDI) Database (April, 2003)

Communications,computer, etc. Insurance andfinancial servicesTravel services

Transport services

12

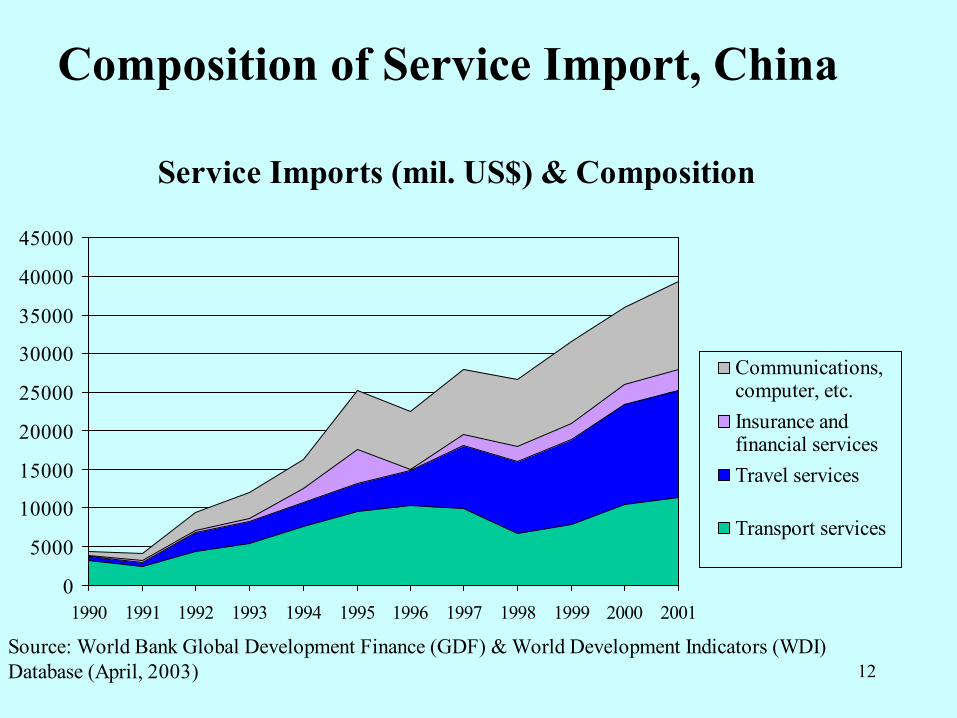

Composition of Service Import, China

Service Imports (mil. US$) & Composition

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Source: World Bank Global Development Finance (GDF) & World Development Indicators (WDI) Database (April, 2003)

Communications,computer, etc.Insurance andfinancial servicesTravel services

Transport services

13

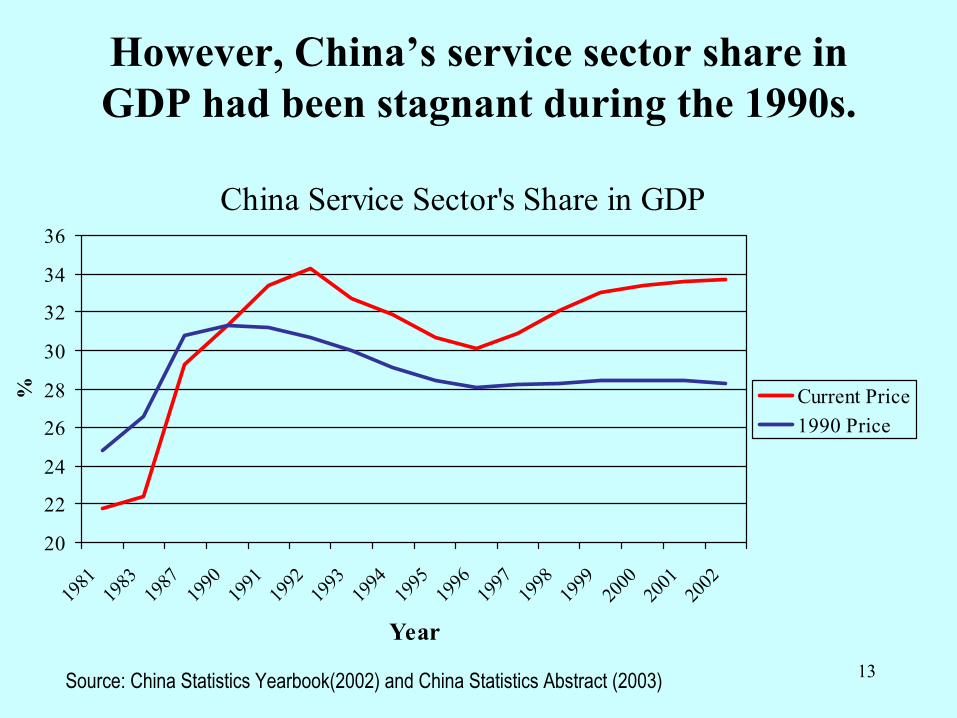

However, China’s service sector share in GDP had been stagnant during the 1990s.

China Service Sector's Share in GDP

20

22

24

26

28

30

32

34

36

1981

1983

1987

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Year

% Current Price1990 Price

Source: China Statistics Yearbook(2002) and China Statistics Abstract (2003)

14

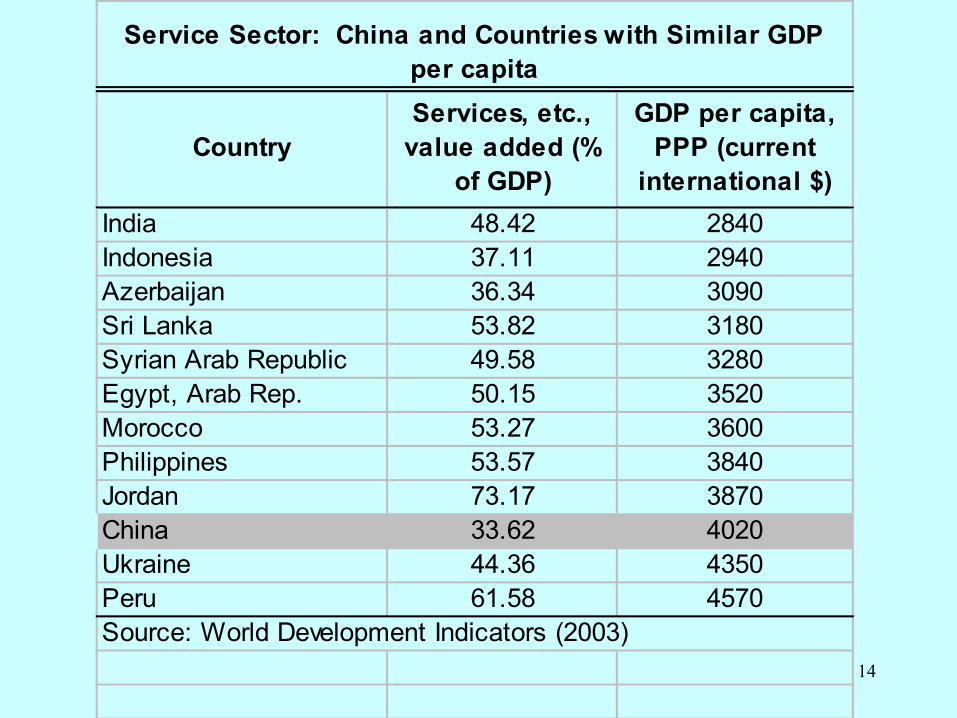

CountryServices, etc.,

value added (% of GDP)

GDP per capita, PPP (current

international $) India 48.42 2840Indonesia 37.11 2940Azerbaijan 36.34 3090Sri Lanka 53.82 3180Syrian Arab Republic 49.58 3280Egypt, Arab Rep. 50.15 3520Morocco 53.27 3600Philippines 53.57 3840Jordan 73.17 3870China 33.62 4020Ukraine 44.36 4350Peru 61.58 4570Source: World Development Indicators (2003)

Service Sector: China and Countries with Similar GDP per capita

15

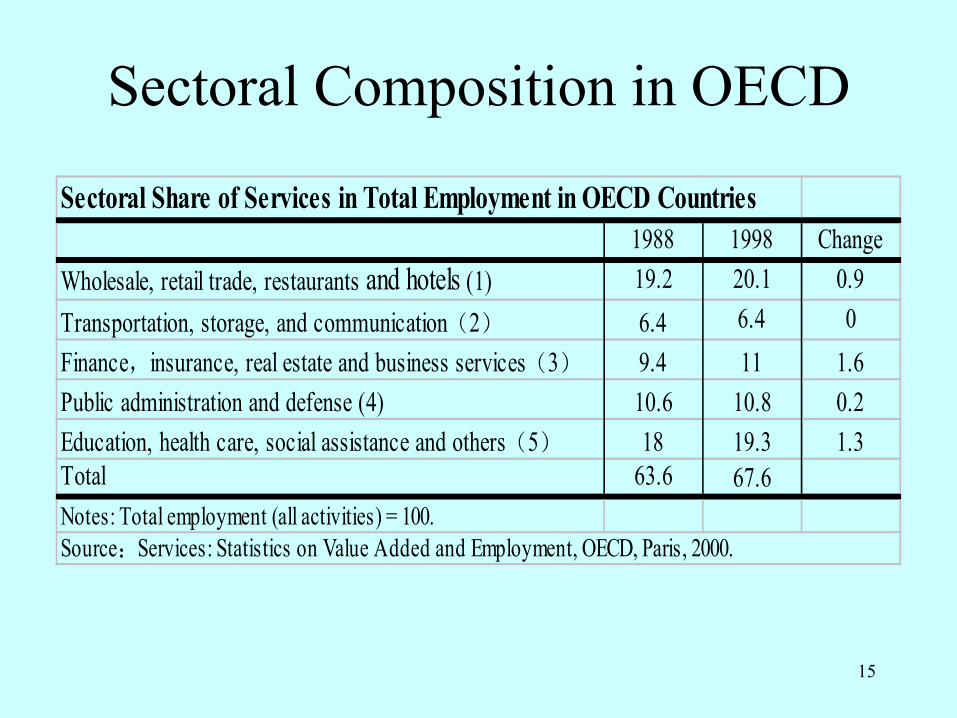

Sectoral Share of Services in Total Employment in OECD Countries1988 1998 Change

Wholesale, retail trade, restaurants and hotels (1) 19.2 20.1 0.9Transportation, storage, and communication(2) 6.4 6.4 0Finance,insurance, real estate and business services(3) 9.4 11 1.6Public administration and defense (4) 10.6 10.8 0.2Education, health care, social assistance and others(5) 18 19.3 1.3Total 63.6 67.6Notes: Total employment (all activities) = 100.Source:Services: Statistics on Value Added and Employment, OECD, Paris, 2000.

Sectoral Composition in OECD

16

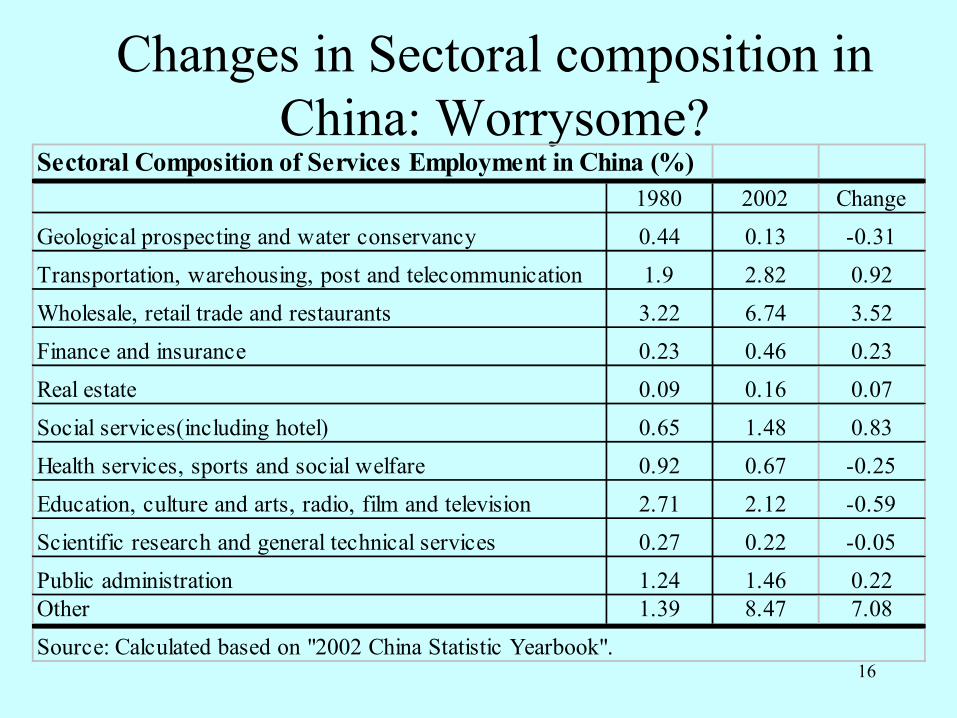

Changes in Sectoral composition in China: Worrysome?

Sectoral Composition of Services Employment in China (%)1980 2002 Change

Geological prospecting and water conservancy 0.44 0.13 -0.31

Transportation, warehousing, post and telecommunication 1.9 2.82 0.92

Wholesale, retail trade and restaurants 3.22 6.74 3.52

Finance and insurance 0.23 0.46 0.23

Real estate 0.09 0.16 0.07

Social services(including hotel) 0.65 1.48 0.83

Health services, sports and social welfare 0.92 0.67 -0.25

Education, culture and arts, radio, film and television 2.71 2.12 -0.59

Scientific research and general technical services 0.27 0.22 -0.05

Public administration 1.24 1.46 0.22Other 1.39 8.47 7.08

Source: Calculated based on "2002 China Statistic Yearbook".

17

Factors for China’s lagging Services• Is service a “nonproductive” sector?• Lack of competition—entry barriers in many sectors

such as banking, telecom, civil aviation, and railways, and restrictions on non-state capital and foreign capital investment

• Low level of marketization• Low level of urbanization• Inadequate human resources in many services: legal,

accounting, financing, multimode distribution, E-commerce, computer software, R & D, market service, corporate management service, etc.

• Therefore, reform and liberalization is needed for the development of the service sector.

18

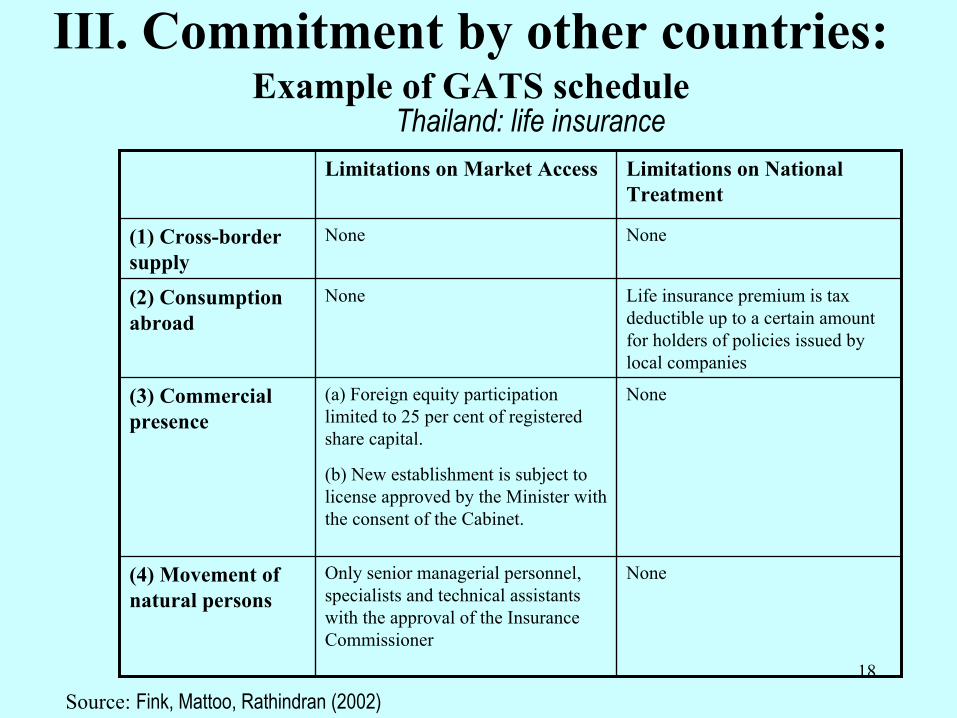

III. Commitment by other countries:Example of GATS schedule

NoneOnly senior managerial personnel, specialists and technical assistants with the approval of the Insurance Commissioner

(4) Movement of natural persons

None(a) Foreign equity participation limited to 25 per cent of registered share capital.

(b) New establishment is subject to license approved by the Minister with the consent of the Cabinet.

(3) Commercial presence

Life insurance premium is tax deductible up to a certain amount for holders of policies issued by local companies

None(2) Consumption abroad

NoneNone(1) Cross-border supply

Limitations on National Treatment

Limitations on Market Access

Thailand: life insurance

Source: Fink, Mattoo, Rathindran (2002)

19

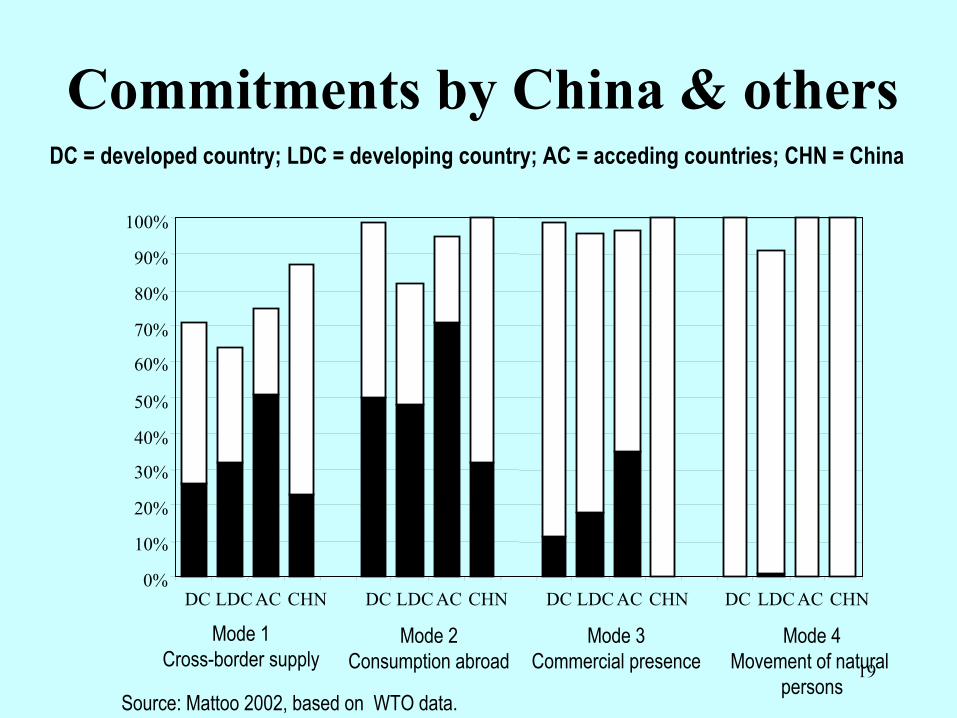

Commitments by China & others

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

DC LDC AC CHN DC LDC AC CHN DC LDC AC CHN DC LDC AC CHN

Mode 1Cross-border supply

Mode 2Consumption abroad

Mode 3Commercial presence

Mode 4Movement of natural

personsSource: Mattoo 2002, based on WTO data.

DC = developed country; LDC = developing country; AC = acceding countries; CHN = China

20

IV. Macro impact of liberalizing the service sector—CGE analysis

A Computable General Equilibrium(CGE) model of China

• 52 productive sectors and 2 households by urban and rural

• Productive factors– agricultural land, capital, labor by rural/urban and skill

• monopolistic competition – Transportation, communication, finance, insurance, real estate,

social service, education, health and cultural service

21

Simulations Design• Base case projection for 2000-2010• Service liberalization case – incorporated four

aspects of policy or institutional changes.– Promote the competition in service sector – Increased foreign investment resulted from reduction of

barriers– Productivity increases in service sector induced by

service liberalization– Halving the barriers to services trade

• All policy changes will be phased in over the period from 2003-2010

22

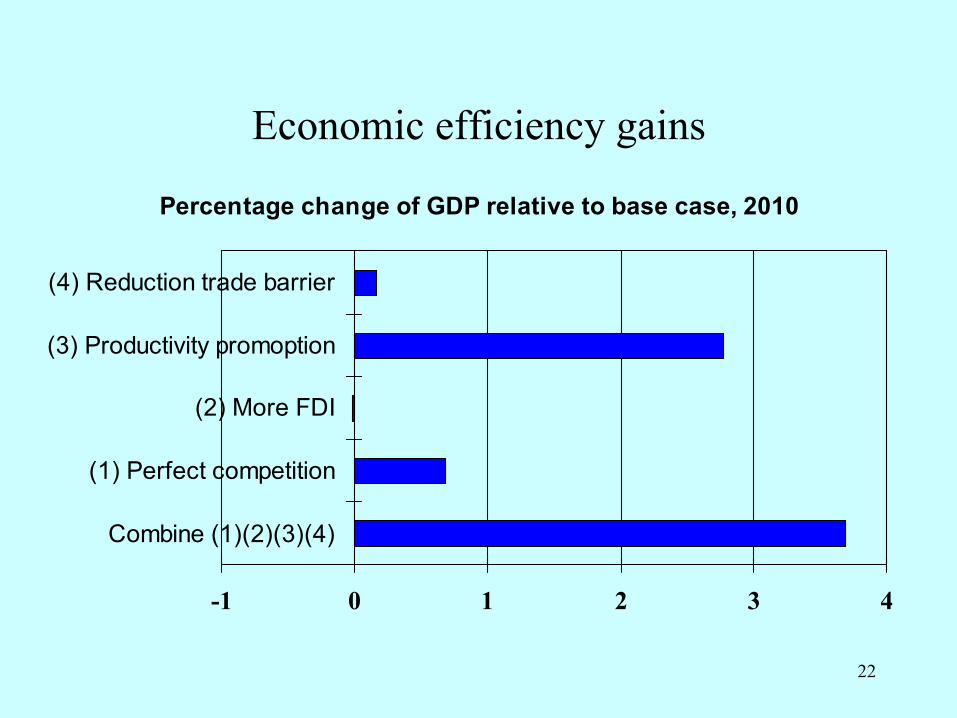

Economic efficiency gains

Percentage change of GDP relative to base case, 2010

-1 0 1 2 3 4

Combine (1)(2)(3)(4)

(1) Perfect competition

(2) More FDI

(3) Productivity promoption

(4) Reduction trade barrier

23

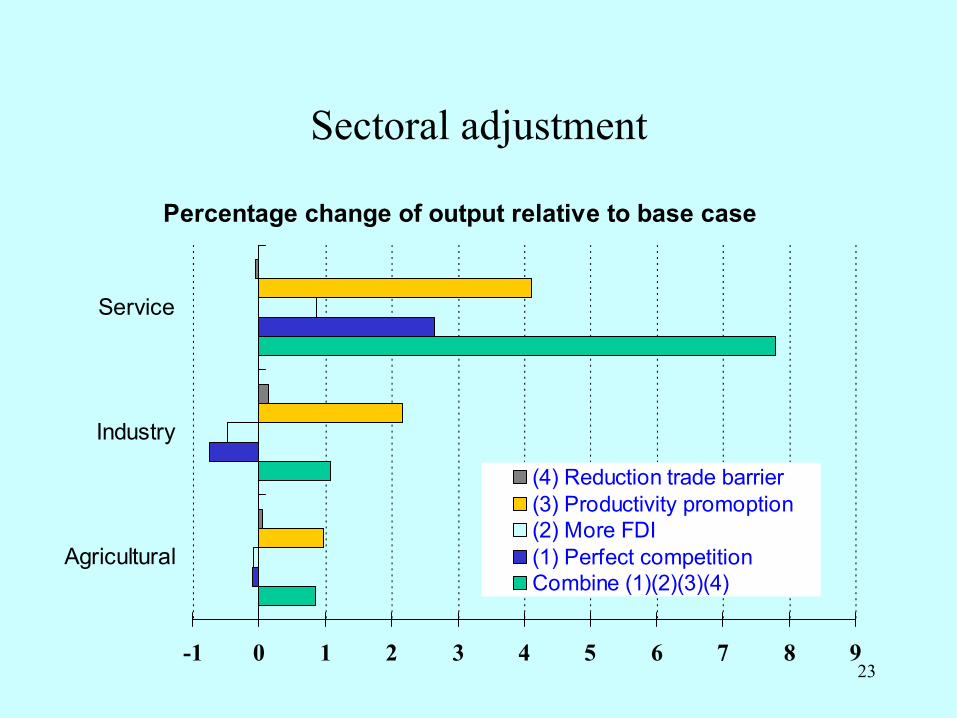

Sectoral adjustment

Percentage change of output relative to base case

-1 0 1 2 3 4 5 6 7 8 9

Agricultural

Industry

Service

(4) Reduction trade barrier(3) Productivity promoption(2) More FDI(1) Perfect competitionCombine (1)(2)(3)(4)

24

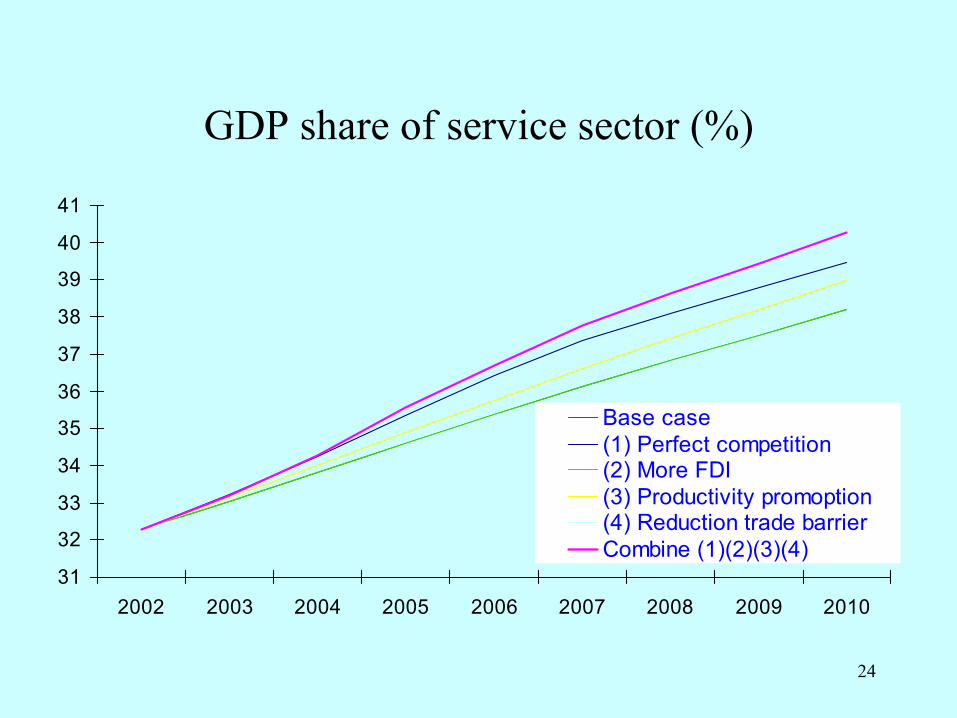

GDP share of service sector (%)

31

32

33

34

35

36

37

38

39

40

41

2002 2003 2004 2005 2006 2007 2008 2009 2010

Base case(1) Perfect competition(2) More FDI(3) Productivity promoption(4) Reduction trade barrierCombine (1)(2)(3)(4)

25

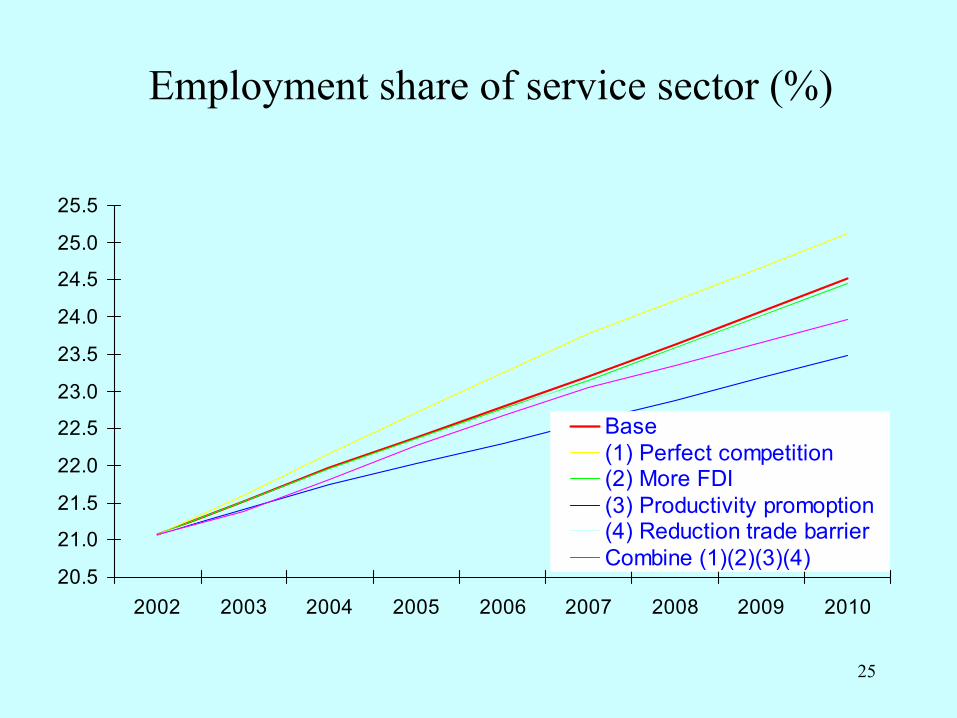

Employment share of service sector (%)

20.5

21.0

21.5

22.0

22.5

23.0

23.5

24.0

24.5

25.0

25.5

2002 2003 2004 2005 2006 2007 2008 2009 2010

Base(1) Perfect competition(2) More FDI(3) Productivity promoption(4) Reduction trade barrierCombine (1)(2)(3)(4)

26

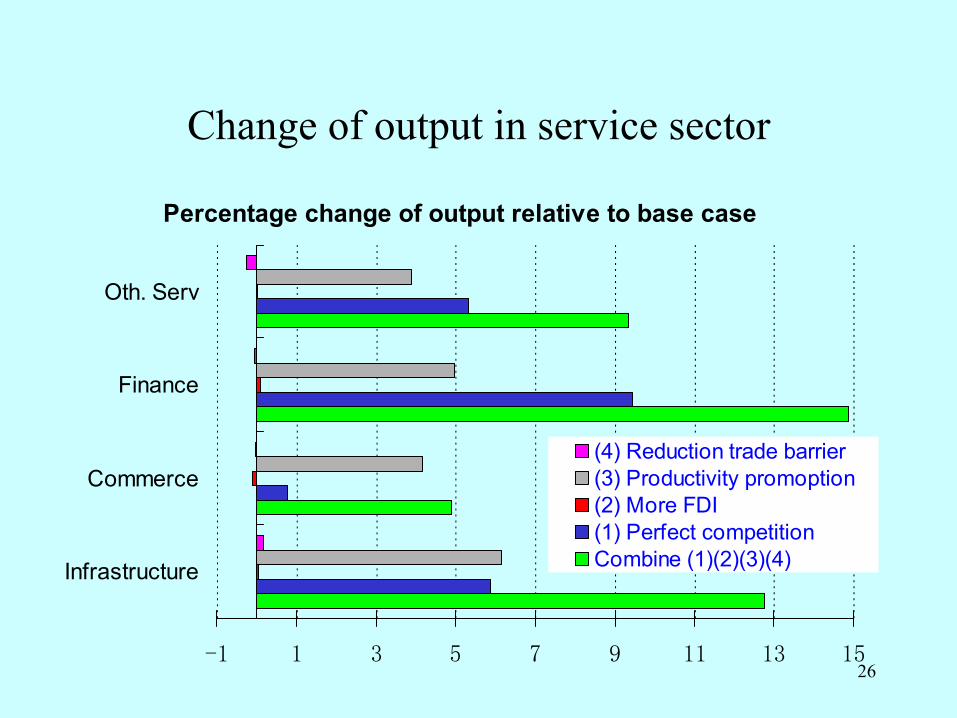

Change of output in service sector

Percentage change of output relative to base case

-1 1 3 5 7 9 11 13 15

Infrastructure

Commerce

Finance

Oth. Serv

(4) Reduction trade barrier(3) Productivity promoption(2) More FDI(1) Perfect competitionCombine (1)(2)(3)(4)

27

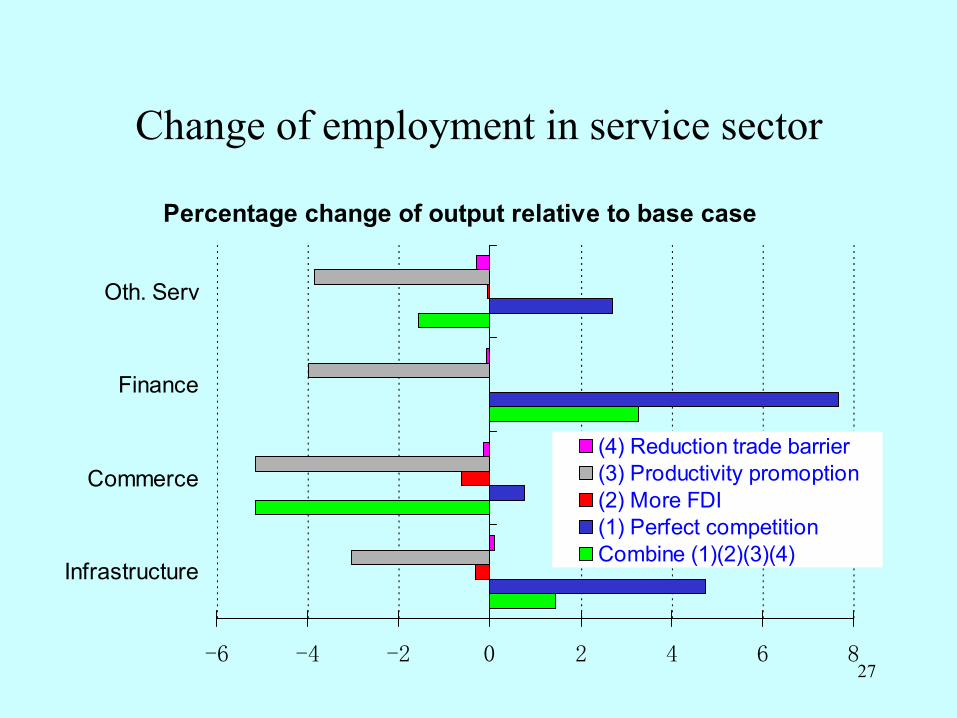

Change of employment in service sector

Percentage change of output relative to base case

-6 -4 -2 0 2 4 6 8

Infrastructure

Commerce

Finance

Oth. Serv

(4) Reduction trade barrier(3) Productivity promoption(2) More FDI(1) Perfect competitionCombine (1)(2)(3)(4)

28

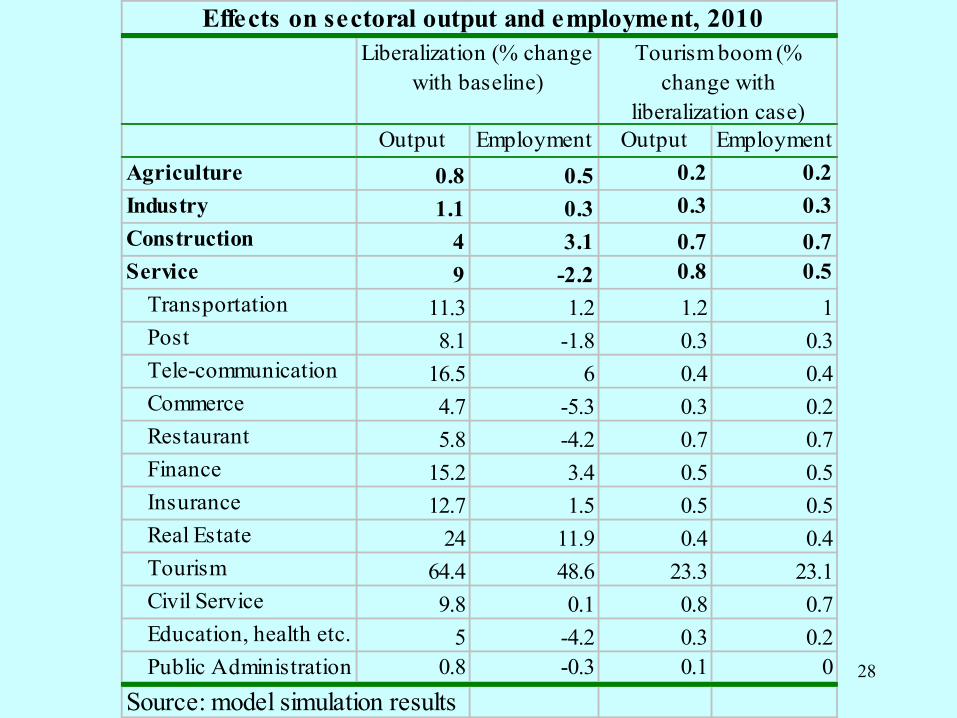

Effects on sectoral output and employment, 2010

Output Employment Output EmploymentAgriculture 0.8 0.5 0.2 0.2Industry 1.1 0.3 0.3 0.3Construction 4 3.1 0.7 0.7Service 9 -2.2 0.8 0.5

Transportation 11.3 1.2 1.2 1Post 8.1 -1.8 0.3 0.3Tele-communication 16.5 6 0.4 0.4Commerce 4.7 -5.3 0.3 0.2Restaurant 5.8 -4.2 0.7 0.7Finance 15.2 3.4 0.5 0.5Insurance 12.7 1.5 0.5 0.5Real Estate 24 11.9 0.4 0.4Tourism 64.4 48.6 23.3 23.1Civil Service 9.8 0.1 0.8 0.7Education, health etc. 5 -4.2 0.3 0.2Public Administration 0.8 -0.3 0.1 0

Source: model simulation results

Liberalization (% change with baseline)

Tourism boom (% change with

liberalization case)

29

Effects of service liberalization• Service liberalization will boost economic

efficiency and have shared benefits• Annual GDP growth rates will increase by 0.48

percentage point in 2003-2010• Welfare gains amount to 827 bn yuan or 4.2% of

GDP in 2010• Real consumption rises by 6.8 % and real

investment by 3.8 %• Overall employment will not rise significantly but

wages for skilled and unskilled labor will rise by 3-6%, benefiting both rural and urban HHs.

30

Sectoral and Employment Results• Output will expand in all service sectors,

especially in highly regulated subsectors such as telecom, insurance, and banking

• Tourism and real estate will experience big output booms and significant increases in their employment

• Employment in the service sector will decline but it will increase in sectors such as construction, automobile and other industrial sectors

• In the case of a foreign tourist boom, both employment and output will increase significantly by 0.8 and 0.5 percent over the baseline.

31

Conclusions• China’s service sector is lagging behind• One of the reasons was lack of competition• Opening service trade could lead to substantial

benefits in growth and consumer welfare• In the case of service liberalization alone,

employment will not rise, but in the case of foreign tourism boom, both output and employment rise significantly

• Complementary measures are needed to reduce strains in labor market

![JBICI Discussion Paper Series - JICA · capital account liberalization should follow current account and domestic financial sector liberalization (McKinnon [1973]). This sequence](https://img.pdfslide.us/doc/110x75/5eaca35f778aaf228459eea6/jbici-discussion-paper-series-jica-capital-account-liberalization-should-follow.jpg)