Embed Size (px)

Citation preview

Market UpdateSeptember Quarter

14 November 2016

Mission:

To be a leading

player in the

global online

classifieds

industry

For

per

sona

l use

onl

y

Page 1

This presentation includes “forward-looking statements.” These can be identified by words such as “may”, “should”, “anticipate”, “believe”, “intend”,“estimate” and “expect”. Statements which are not based on historic or current facts may be forward-looking statements.

Forward-looking statements are based on assumptions regarding Mitula Group’s financial position, business strategies, plans and objectives of

management for future operations and development and the environment in which Mitula Group will operate.

Forward-looking statements are based on current views, expectations and beliefs as at the date they are expressed and which are subject to

various risks and uncertainties. Actual results, performance or achievements of Mitula Group could be materially different from those expressed in,

or implied by, these forward-looking statements. The forward-looking statements contained in this presentation are not guarantees or assurances offuture performance and involve known and unknown risks, uncertainties and other factors, many of which are beyond the control of Mitula Group,

which may cause the actual results, performance or achievements of Mitula Group to differ materially from those expressed or implied by the

forward-looking statements. For example, the factors that are likely to affect the results of Mitula Group include general economic conditions in

Australia; exchange rates; competition in the markets in which Mitula Group does and will operate and the inherent regulatory risks in the

businesses of Mitula Group. The forward-looking statements contained in this presentation should not be taken as implying that the assumptions on

which the projections have been prepared are correct or exhaustive.

Mitula Group disclaims any responsibility for the accuracy or completeness of any forward-looking statement. Mitula Group disclaims anyresponsibility to update or revise any forward-looking statement to reflect any change in Mitula Group’s financial condition, status or affairs or any

change in the events, conditions or circumstances on which a statement is based, except as required by law.

The projections or forecasts included in this presentation have not been audited, examined or otherwise reviewed by the independent auditors of

Mitula Group. Unless otherwise stated, all amounts are based on A-IFRS and are in Australian Dollars. Certain figures may be subject to rounding

differences. Any market share information in this presentation is based on management estimates based on internally available information unless

otherwise indicated.

You must not place undue reliance on these forward-looking statements.

This presentation is not an offer or invitation for subscription or purchase of, or a recommendation of securities. The securities referred to in these

materials have not been and will not be registered under the United States Securities Act of 1933 (as amended) and may not be offered or sold in

the United States absent registration or an exemption from registration.

This presentation is unaudited.

Important Notice and Disclaimer

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 2

High Growth Global Online Classifieds CompanyIntroducing Mitula Group

November 2016 Analyst Presentation

Note: Prepared on a statutory basis. Lokku Limited acquired 8 May 2015, Nuroa acquired 28 February 2016, and DotProperty acquired 2 September 2016. Revenue projection does not include any M&A outcomes and EBITDA includes costs any associated with IPO, share based payments and M&A work.

Source: Internal Management Reports.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

CY 2012 CY 2013 CY 2014 CY 2015 CY 2016

(fcst)

CY 2017

(fcst)

AU

D M

illio

ns $38.0m -

$41.0m

$28.0m -$29.0m

$3.8m

$5.3m

$10.7m

$20.6m

• Leading online classifieds

company operating in 49 countries

• Diversified across four verticals:

property, employment, motoring,

fashion; generating more than 70

million monthly visits

• High calibre management and

board with decades of online

classifieds experience

• Consistent revenue growth, high-

margin, generating strong positive

cash flow (>A$1m/month)

• Significant opportunity for strong

growth through launch of new

products and synergistic M&A to

increase yield per visit

25.3% 35.2% 50.8% 46.8% 41.0% -

45.0%

42.0% -

46.0%

EBITDA

For

per

sona

l use

onl

y

Page 3

Operating in 51 Countries

EUROPESpain, UK, Italy, France,

Germany, Netherlands,

Portugal, Belgium, Austria,

Russia, Switzerland,

Poland, Romania,

Turkey, Ireland

Denmark, Sweden,

Ukraine

AMERICASUS, Canada, Mexico,

Chile, Brazil, Argentina,

Colombia, Peru, Venezuela,

Ecuador, Panama

AFRICAMorocco, South Africa,

Kenya, Tunisia, Nigeria

APACIndia, Hong Kong,

Malaysia, Singapore,

Philipines, China,

Indonesia, Pakistan,

UAE, Vietnam, Thailand,

Cambodia, Laos,

Myanmar, Australia, New

Zealand, Japan

Introducing Mitula Group

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

mitulagroup.com

Business Overview

Mission:

To be a leading

player in the global online classifieds

industry

For

per

sona

l use

onl

y

Page 5

Multiple Intermediaries in the Classifieds Transaction

Vertical

Search

Po

rtal +

Ge

ne

ral C

lassifie

ds

Site

s

(Site

s w

ith lis

ting

s)

Re

cru

iter / A

ge

nt / D

ea

ler

/

Pro

ject M

ark

ete

r Site

s

~20,000 agents /

developers

~100 portals / general

classifieds / specialist

sites

<5 main vertical

search sites

Se

llers

of C

ars

/ Jo

bs /

Ho

me

s / F

ash

ion

Bu

ye

rs

November 2016 Analyst Presentation

Business Overview

General

Search

Italian Real Estate

Example

Traditional Focus of Mitula Group in Red

For

per

sona

l use

onl

y

Page 6

Revenue Generation in the Classifieds Transaction

Trans-

action

(Commission)

Listings

Display

Advertising

Software

ClicksCPC / AdSense

Display

Advertising

November 2016 Analyst Presentation

Business Overview

Revenue Streams

Revenue Potential within a Given Market

x1 x10+ x100+ ILLUSTRATIVE

Traditional Focus of Mitula Group in Red

Vertical

Search

Po

rtal +

Ge

ne

ral C

lassifie

ds

Site

s

(Site

s w

ith lis

ting

s)

Re

cru

iter / A

ge

nt / D

ea

ler

/

Pro

ject M

ark

ete

r

Se

llers

of C

ars

/ Jo

bs /

Ho

me

s / F

ash

ion

Bu

ye

rs

General

Search

For

per

sona

l use

onl

y

Page 7

Business Overview

How Vertical Search WorksListings from

advertiser sent to

Mitula

1

2

3

4

5

User makes

a search

request

User reviews search

results and clicks

AdSense or listing

User clicks on AdSense

User clicks on listing and

redirected to source details

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 8Page 8

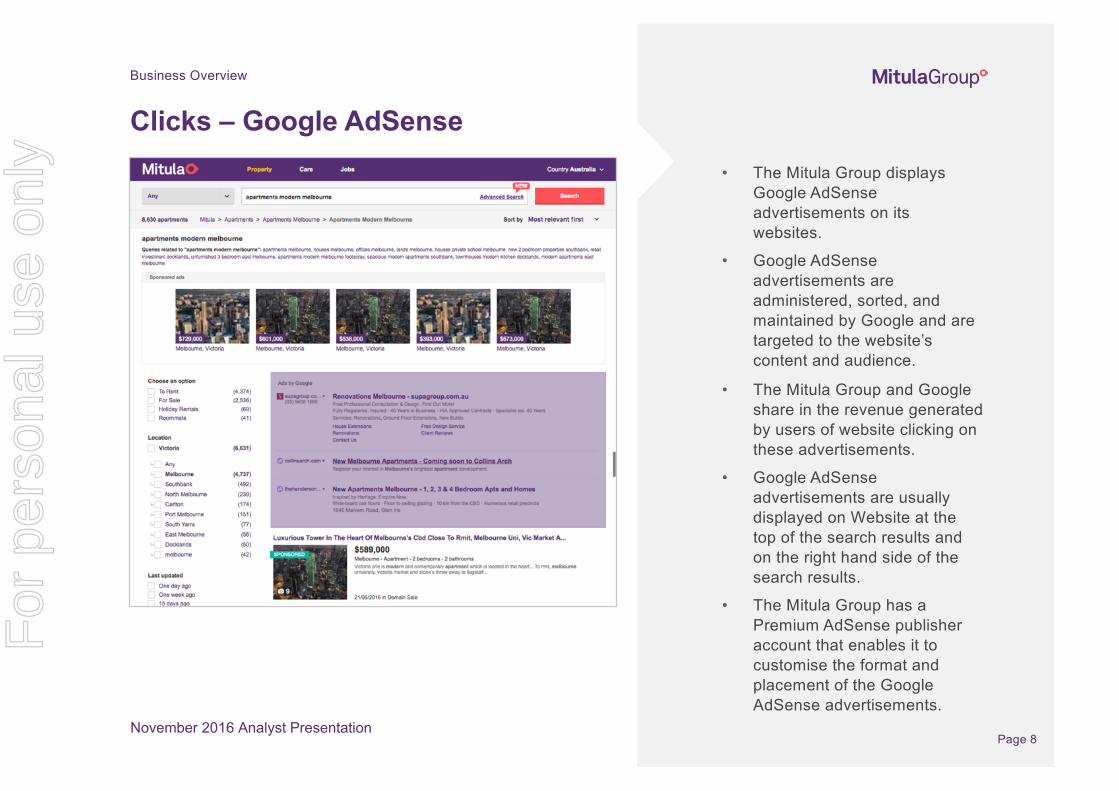

Business Overview

Clicks – Google AdSense• The Mitula Group displays

Google AdSense

advertisements on its

websites.

• Google AdSense

advertisements are

administered, sorted, and

maintained by Google and are

targeted to the website’s

content and audience.

• The Mitula Group and Google

share in the revenue generated

by users of website clicking on

these advertisements.

• Google AdSense

advertisements are usually

displayed on Website at the

top of the search results and

on the right hand side of the

search results.

• The Mitula Group has a

Premium AdSense publisher

account that enables it to

customise the format and

placement of the Google

AdSense advertisements.

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 9Page 9

Business Overview

Clicks – Cost per Click (CPC)• The Mitula Group displays

advertisers’ listings on its websites,

initially free of charge. Those

listings may only receive a limited

number of click outs.

• If an advertiser would like to receive

more click outs than the limited

number provided free of charge, the

advertiser must pay the Mitula

Group, on a ‘cost-per-click’ basis, to

receive those additional click outs.

This is referred to as Direct CPC

Revenue, contributed by a paying

advertiser.

• The amount paid per click out by a

paying advertiser varies by vertical

(real estate, employment, motoring)

and by country.

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 10

Segmentation of Mitula Group Markets

Yield per Visit for Mitula Group

Visits to Mitula Group Sites in the Country

Tier 1 – Established Markets

• Mature countries with clear online classifieds structure (portals and general classified sites)

• Major and minor players invest in marketing (brand building and traffic generation)

• Vertical search seen as a legitimate source of traffic

• Mitula monetising well with clear growth potential

• Example: UK, AU, UAE, DE, FR

Tier 3 – Early Stage Markets

• No clear online classifieds structure

• Rapid growth but off a low base

• Long term potential

• Mitula not monetising beyond AdSense

• Example: PK, NG, KE

Tier 2 – Emerging Markets

• Strong growth countries

• Online classifieds structure not settled

• Vertical search material source of traffic

• Mitula slow to monetise

• Example: MX, PH, CO, BR, ID

November 2016 Analyst Presentation

Business Overview

For

per

sona

l use

onl

y

Page 11

Value Creation by Segment (September Quarter)

Visits (m)

Clicks (m)

% Tier Clicks Sold

Revenue (AUD 000’s)

Yield/ Visit

(c)Strategic Implications

Tier 1

Established

Markets

56.1 78.7 65.7% 3,386 6.0

• Stable driver of revenues

• Focus on growing visitation as

able to sell majority of clicks

• Roll out of additional products

and services to existing

customers

• Find ways of selling more

clicks (up to around 80%)

Tier 2Emerging Markets

133.3 185.6 33.4% 3,529 2.6

• Value being “left of the table”

• Low yield per visit driven by low number of clicks sold & lower CPC rate

• Look for new ways to monetise visitation and increase yield per visit

Tier 3

Early Stage12.2 14.8 27.0% 310 2.5

• No real short term value for

Mitula Group

• Allow to grow naturally and

revisit if / when scale achieved

Source: Internal Management Reports (Sep Quarter 2016)

November 2016 Analyst Presentation

Focus on driving

new methods of

increasing yield per visit –

primarily around

greater sale of

direct to end

customer products

Business Overview

For

per

sona

l use

onl

y

Page 12

Strategic Approach for Mitula Group

November 2016 Analyst Presentation

Business Overview

Listings

Display

Advertising

Software

ClicksCPC/AdSense

Display

Advertising

Revenue Streams

Tier 1Tier 2 Markets

New Focus of Mitula Group in

Red

Vertical

Search

Po

rtal +

Ge

ne

ral C

lassifie

ds

Site

s

(Site

s w

ith lis

ting

s)

Re

cru

iter / A

ge

nt / D

ea

ler

/

Pro

ject M

ark

ete

r

Se

llers

of C

ars

/ Jo

bs /

Ho

me

s / F

ash

ion

Bu

ye

rs

General

Search

Trans-

action

(Commission)

For

per

sona

l use

onl

y

Page 13

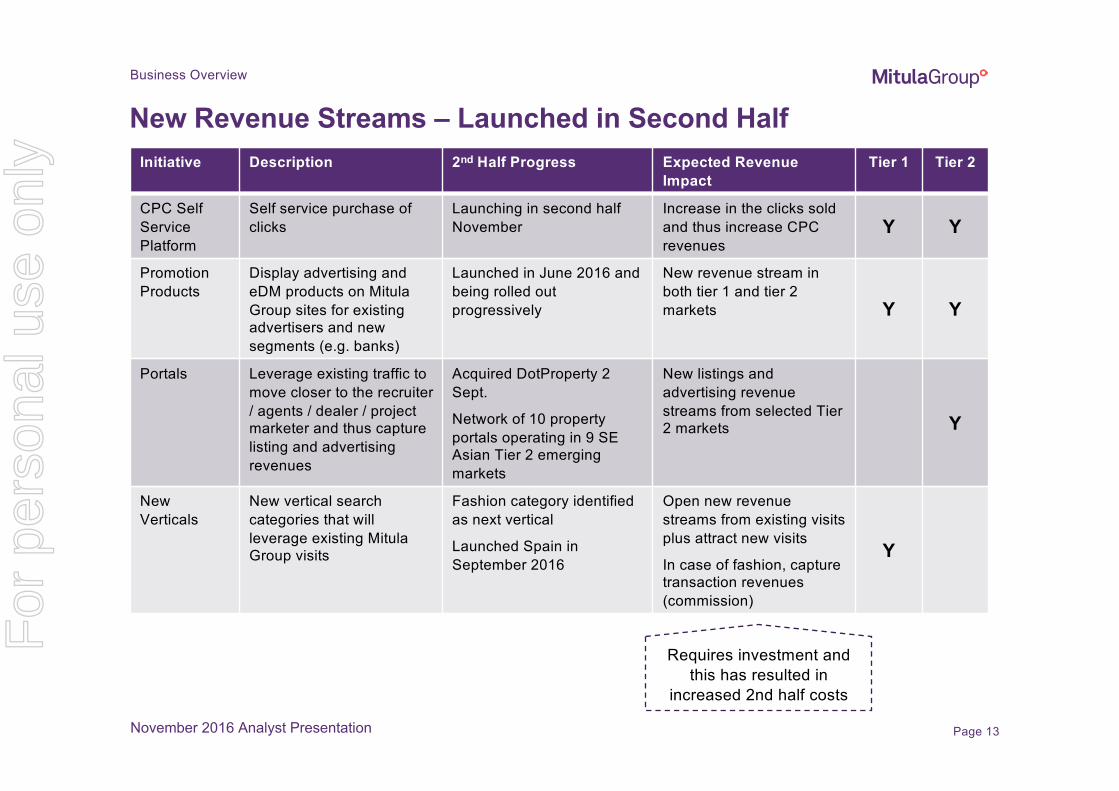

New Revenue Streams – Launched in Second Half

November 2016 Analyst Presentation

Initiative Description 2nd Half Progress Expected Revenue Impact

Tier 1 Tier 2

CPC Self

Service

Platform

Self service purchase of

clicks

Launching in second half

November

Increase in the clicks sold

and thus increase CPC

revenues

Y Y

Promotion

Products

Display advertising and

eDM products on Mitula

Group sites for existing

advertisers and new

segments (e.g. banks)

Launched in June 2016 and

being rolled out

progressively

New revenue stream in

both tier 1 and tier 2

markets Y Y

Portals Leverage existing traffic to

move closer to the recruiter

/ agents / dealer / project

marketer and thus capture

listing and advertising

revenues

Acquired DotProperty 2

Sept.

Network of 10 property

portals operating in 9 SE

Asian Tier 2 emerging

markets

New listings and

advertising revenue

streams from selected Tier

2 markets Y

New

Verticals

New vertical search

categories that will

leverage existing Mitula

Group visits

Fashion category identified

as next vertical

Launched Spain in

September 2016

Open new revenue

streams from existing visits

plus attract new visits

In case of fashion, capture

transaction revenues

(commission)

Y

Business Overview

Requires investment and

this has resulted in

increased 2nd half costs

For

per

sona

l use

onl

y

mitulagroup.com

September QuarterPerformance

Mission:

To be a leading

player in the global online classifieds

industry

For

per

sona

l use

onl

y

Page 15

Note: Prepared on a statutory basis. Lokku Limited acquired on 8 May 2015, Nuroa on 28 February 2016 and DotProperty acquired 2 September 2016.

Source: Internal Management Reports.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

AU

D M

illio

ns

CPC AdSense New Products

Quarterly Revenue Growth20.5% Year on Year

Revenue Growth

$7.2 m$6.0 m

September Quarter Performance

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 16

Quarterly Revenue by Product

AUD 000’s Sep 2016 Quarter

Sep 2015 Quarter Growth

AdSense 2,643 1,992 32.7%

Cost-per-Click 4,165 4,004 4.0%

New Products(1) 417 0 n/a

Totals 7,225 5,996 20.5%

Tier 1 CPC revenues grew

at 15.8% year on year

Tier 2 CPC revenues

decreased by 8.0% year

on year due to a tightening

of marketing spend by

customers

In addition, currency

movements had a negative

impact (see appendix p32)

(1) New products commenced launch in June 2016. These include promotion products on Mitula Group sites, listings and promotion products on DotProperty sites, transaction revenue on the fashion vertical, and data products across the Group.

Note: Prepared on a statutory basis. Lokku Limited acquired on 8 May 2015, Nuroa on 28 February 2016 and DotProperty on 2 September 2016.

Source: Internal Management Reports.

November 2016 Analyst Presentation

September Quarter Performance

For

per

sona

l use

onl

y

Page 17

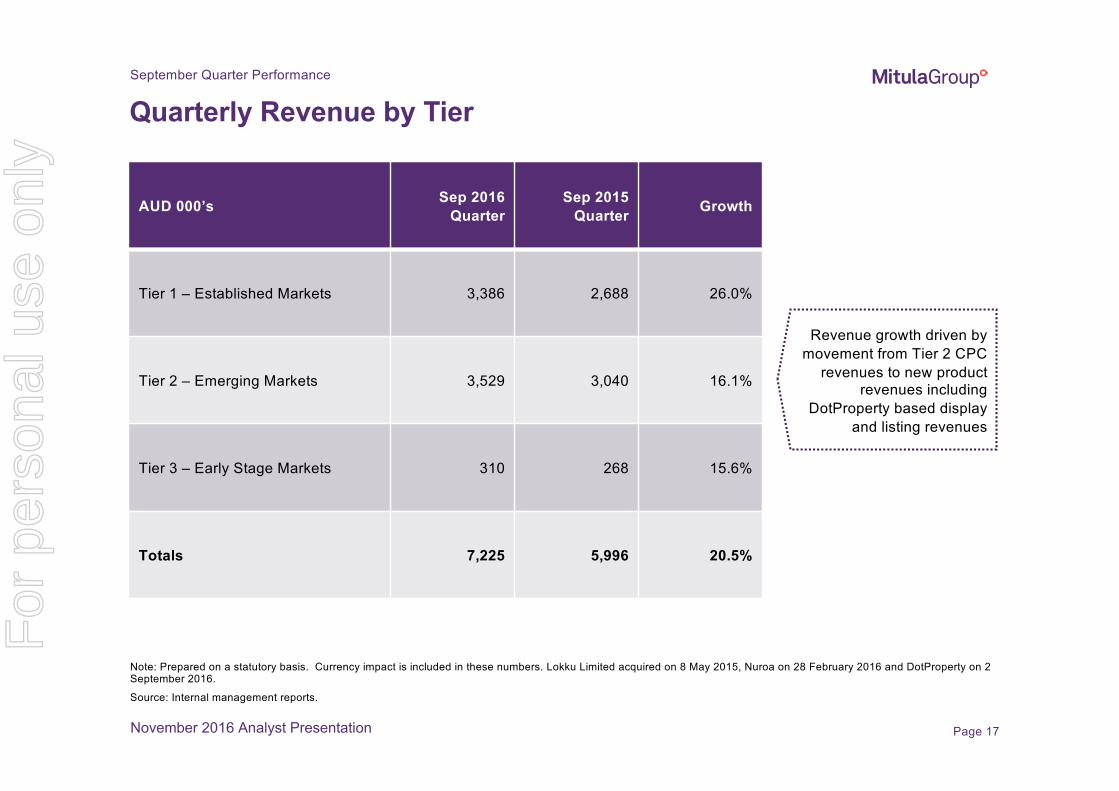

Quarterly Revenue by Tier

AUD 000’s Sep 2016 Quarter

Sep 2015 Quarter Growth

Tier 1 – Established Markets 3,386 2,688 26.0%

Tier 2 – Emerging Markets 3,529 3,040 16.1%

Tier 3 – Early Stage Markets 310 268 15.6%

Totals 7,225 5,996 20.5%

Revenue growth driven by

movement from Tier 2 CPC

revenues to new product

revenues including

DotProperty based display

and listing revenues

Note: Prepared on a statutory basis. Currency impact is included in these numbers. Lokku Limited acquired on 8 May 2015, Nuroa on 28 February 2016 and DotProperty on 2 September 2016.

Source: Internal management reports.

September Quarter Performance

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 18

Note: Prepared on a statutory basis. Revenues and KPI’s from Nestoria included from acquisition on 8 May 2015, Nuroa from acquisition on 28 February 2016 and DotProperty from acquisition on 2 September 2016. Will vary from historically published KPI’s that were prepared on a pro-forma basis.

Source: Internal Management Reports.

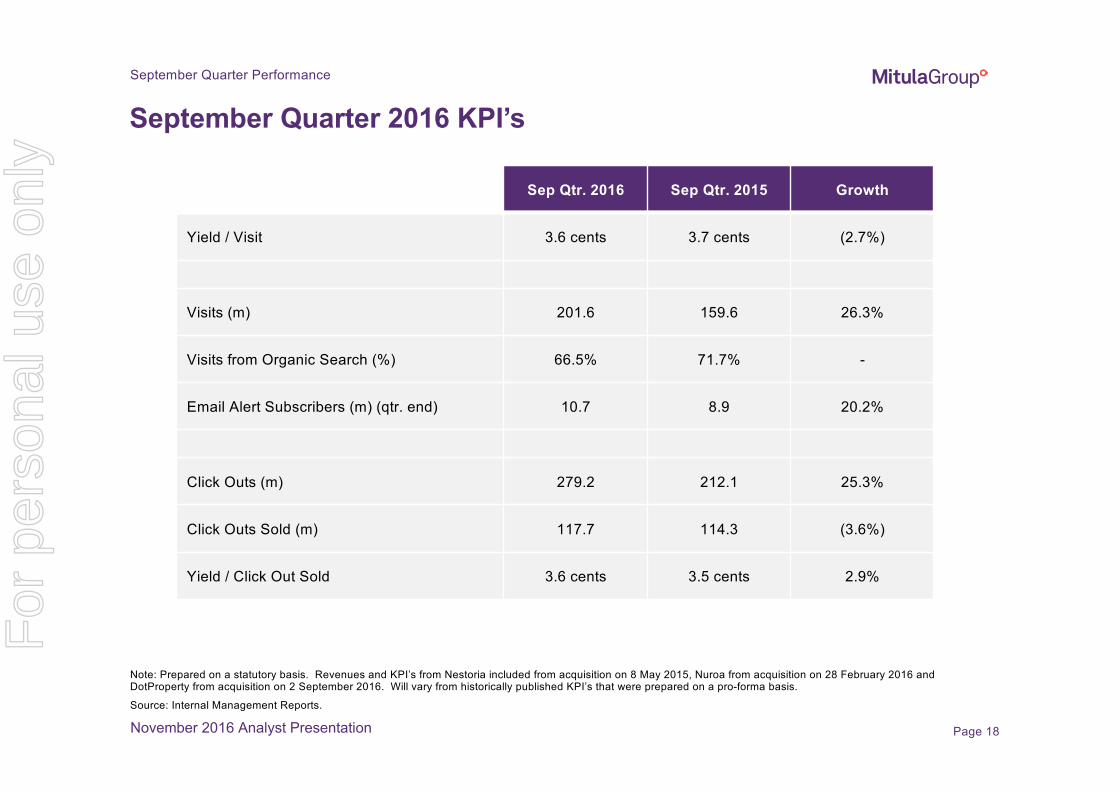

September Quarter 2016 KPI’s

Sep Qtr. 2016 Sep Qtr. 2015 Growth

Yield / Visit 3.6 cents 3.7 cents (2.7%)

Visits (m) 201.6 159.6 26.3%

Visits from Organic Search (%) 66.5% 71.7% -

Email Alert Subscribers (m) (qtr. end) 10.7 8.9 20.2%

Click Outs (m) 279.2 212.1 25.3%

Click Outs Sold (m) 117.7 114.3 (3.6%)

Yield / Click Out Sold 3.6 cents 3.5 cents 2.9%

September Quarter Performance

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 19

Yield per Visit (Quarterly)

0.000

0.005

0.010

0.015

0.020

0.025

0.030

0.035

0.040

0.045

AU

D c

en

ts

Note: Prepared on a statutory basis. Revenues and visits from Nestoria included from acquisition on 8 May 2015, Nuroa from acquisition on 28 February 2016 and DotProperty from acquisition on 2 September 2016.

Source: Internal Management Reports.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

AU

D M

illio

ns

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

millio

ns

Revenue

Visits

Yield per visit

September Quarter Performance

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 20

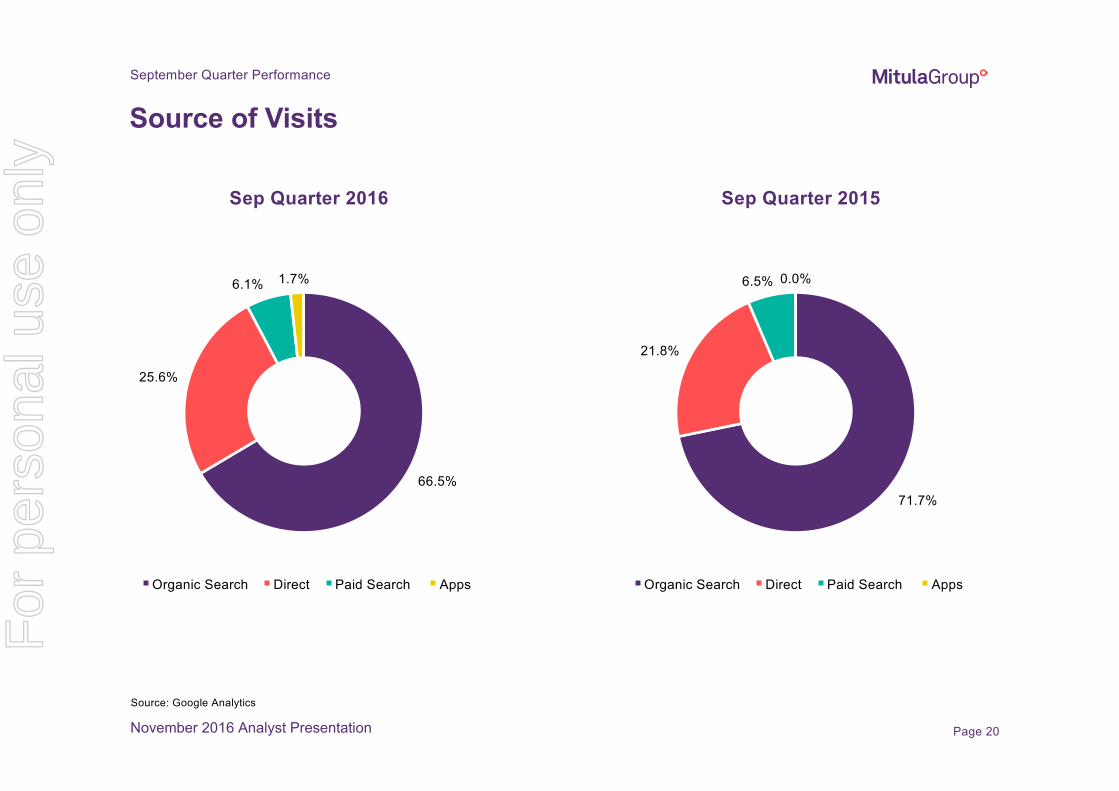

Source: Google Analytics

Source of Visits

Sep Quarter 2016

71.7%

21.8%

6.5% 0.0%

Organic Search Direct Paid Search Apps

Sep Quarter 2015

66.5%

25.6%

6.1% 1.7%

Organic Search Direct Paid Search Apps

September Quarter Performance

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 21

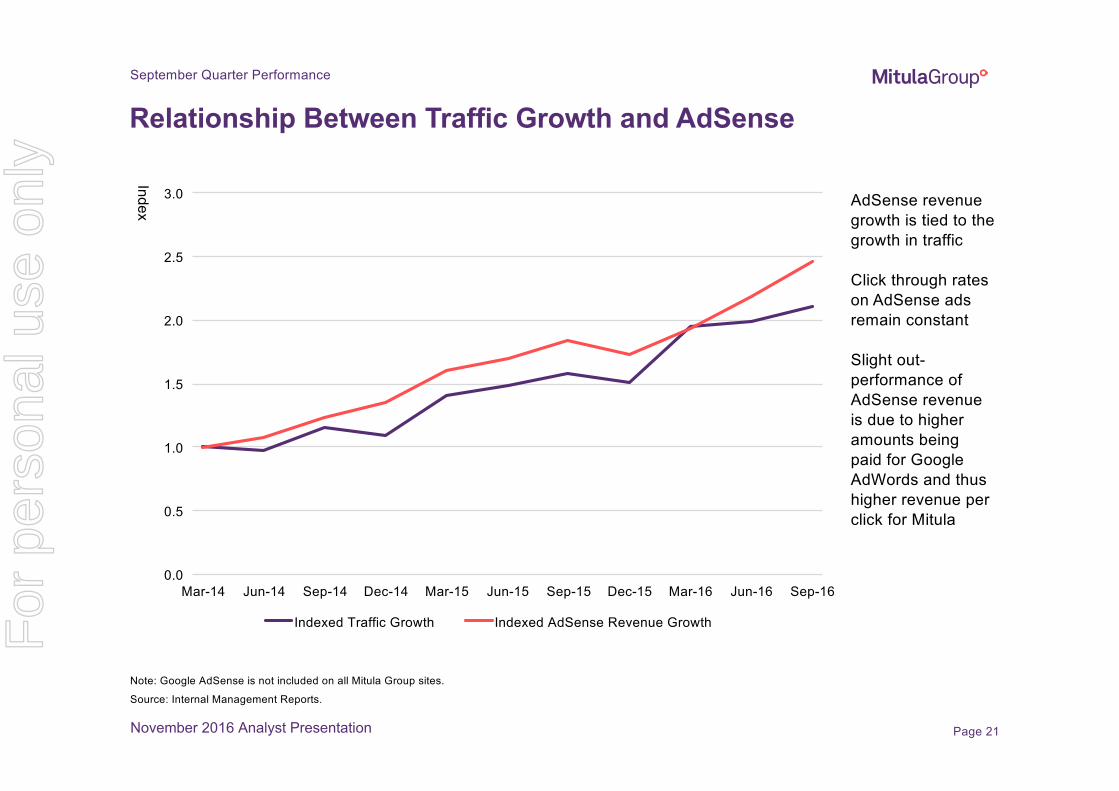

Relationship Between Traffic Growth and AdSense

Note: Google AdSense is not included on all Mitula Group sites.

Source: Internal Management Reports.

September Quarter Performance

November 2016 Analyst Presentation

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Indexed Traffic Growth Indexed AdSense Revenue Growth

AdSense revenue

growth is tied to the

growth in traffic

Click through rates

on AdSense ads

remain constant

Slight out-

performance of

AdSense revenue

is due to higher

amounts being

paid for Google

AdWords and thus

higher revenue per

click for Mitula

Ind

ex

For

per

sona

l use

onl

y

Page 22

0.0

50.0

100.0

150.0

200.0

250.0

300.0

millio

ns

Click Outs Generated and Sold (Quarterly)31.6% vs

PCP

Growth

Note: All numbers prepared on a statutory basis. Clicks generated and sold from Nestoria included from acquisition on 8 May 2015 and Nuroa from acquisition on 28 February 2016.

Source: Internal Management Reports.

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

millio

ns

3.1% vs

PCP

Growth

Click Outs Generated Click Outs Sold

Sep 163.6 cents per

click sold

Sep 153.5 cents per

click sold

2.9%

Growth

September Quarter Performance

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 23

New Revenue Streams – Progress and Impact on BusinessSeptember Quarter Performance

November 2016 Analyst Presentation

Initiative Progress September Quarter Impact

CPC Self Service

Platform

Expected to launch in second half

November

Additional costs incurred by the business during the build out

of the self service platform

No revenues generated as not launched in September

quarter

Promotion

Products

Initial products launched in June and

being refined

Sales and marketing approach being

rolled out

Generated approximately 50% of the new product revenues

in the September quarter

Additional costs (vs first half) were incurred as product

development continued and promotion was rolled out

DotProperty

Acquisition

DotProperty growing inline with

business plan

Mitula implementing traffic sharing

initiatives to help accelerate growth

Generated approximately 50% of the new product revenues

in September quarter

Added additional costs to the business as it operated at an

EBTIDA loss in September

Fashion Vertical Launched Spain in September 2016

Commencing cross platform marketing

Initial revenue streams emerging

Initial, but small, revenues generated in September quarter

Costs being incurred as still in the set up phase

Overall impact has been an increase in operating

costs to fund new revenue stream development

and thus a reduction in EBITDA margin from the

first half. This will continue into the December

quarter.

For

per

sona

l use

onl

y

mitulagroup.com

Outlook Mission:

To be a leading

player in the global online classifieds

industry

For

per

sona

l use

onl

y

Page 25

CY 2016 Revenue Forecast

AUD 000’sCY16

1st Half(Actual)

CY162nd Half

(Forecast)

CY16Total

(Forecast)

CY15Total

(Actual)

Annual Growth

(Forecast)

CY15 2nd Half (Actual)

Half Year Growth

(Forecast)

Revenue (High) 13,587 15,413 29,000 20,568 41.0% 11,670 32.1%

Revenue (Low) 13,587 14,413 28,000 20,568 36.1% 11,670 23.5%

Source: Internal Management Reports

November 2016 Analyst Presentation

Outlook

For

per

sona

l use

onl

y

Page 26

Outlook

For display purposes, uses mid point data for Dec 2016 quarter forecast of between $6.8 m and $7.8 m in revenues.

Source: Internal Management Reports.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

(fcst)

CPC AdSense Advertising/Listing

Quarterly Revenue Growth – December Quarter Forecast

Forecast 19.3% -

36.8% PCP

Revenue Growth

November 2016 Analyst Presentation

AU

D M

illion

s

Driven by a

combination of new

promotion revenues

on Mitula Group sites

+ DotProperty Group

revenues

$5.7m $6.8m-$7.8m

Expected CPC

revenues to return to

previous levels driven

by launch of self

service platform and

a strengthening of

the CPC market

For

per

sona

l use

onl

y

Page 27

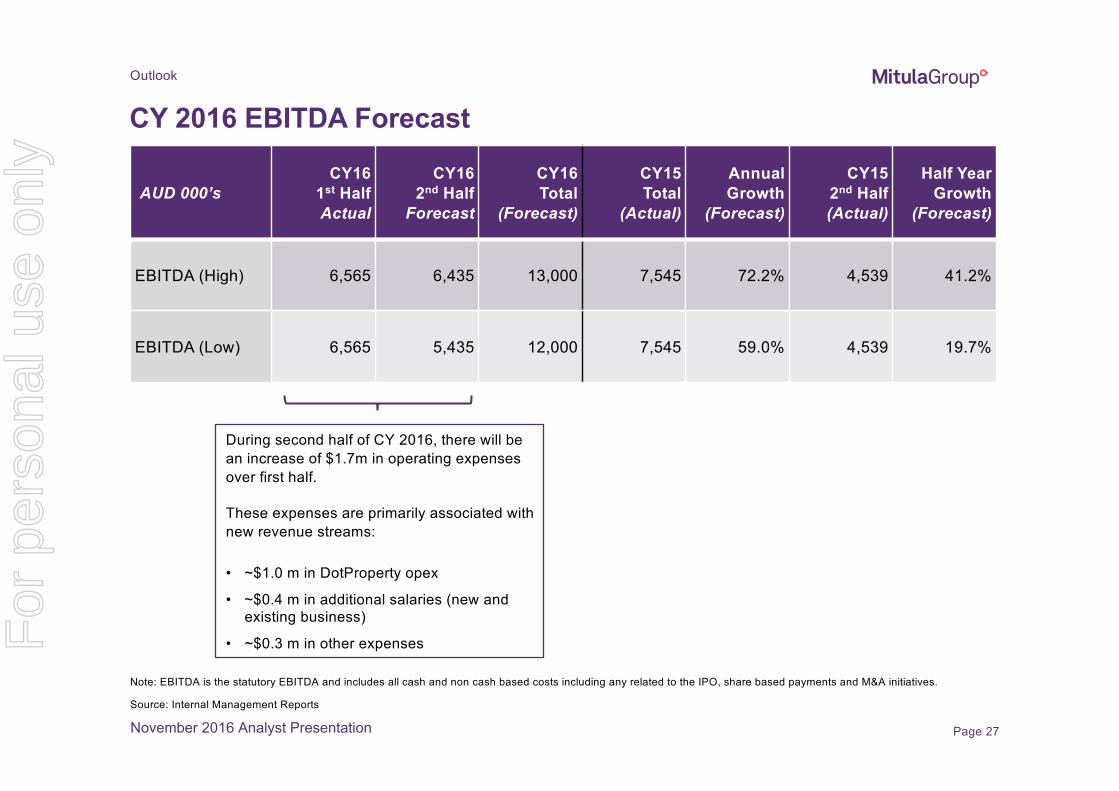

CY 2016 EBITDA Forecast

AUD 000’sCY16

1st HalfActual

CY162nd HalfForecast

CY16Total

(Forecast)

CY15Total

(Actual)

Annual Growth

(Forecast)

CY15 2nd Half (Actual)

Half Year Growth

(Forecast)

EBITDA (High) 6,565 6,435 13,000 7,545 72.2% 4,539 41.2%

EBITDA (Low) 6,565 5,435 12,000 7,545 59.0% 4,539 19.7%

November 2016 Analyst Presentation

Note: EBITDA is the statutory EBITDA and includes all cash and non cash based costs including any related to the IPO, share based payments and M&A initiatives.

Source: Internal Management Reports

During second half of CY 2016, there will be

an increase of $1.7m in operating expenses

over first half.

These expenses are primarily associated with

new revenue streams:

• ~$1.0 m in DotProperty opex

• ~$0.4 m in additional salaries (new and

existing business)

• ~$0.3 m in other expenses

Outlook

For

per

sona

l use

onl

y

Page 28

Outlook

Note: Prepared on a statutory basis. Lokku Limited acquired 8 May 2015, Nuroa acquired 28 February 2016, and DotProperty acquired 2 September 2016. Revenue projection does not include any M&A outcomes and EBITDA includes any costs associated with IPO, share based payments and M&A initiatives.

Source: Internal Management Reports.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

CY 2012 CY 2013 CY 2014 CY 2015 CY 2016 (fcst) CY 2017 (fcst)

AU

D M

illio

ns

Annual Revenue Growth – CY 2017 Guidance

$38.0m -$41.0m

$28.0m -$29.0m

November 2016 Analyst Presentation

EBITDA

expected to be

between

$17.0m and

$19.0m for

CY 2017

$3.8m$5.3m

$10.7m

$20.6m

For

per

sona

l use

onl

y

mitulagroup.com

Appendix

Mission:

To be a leading

player in the global online classifieds

industry

For

per

sona

l use

onl

y

Page 30

Vertical Search Display Advertising ProductsSpecial Branding Options

300x600

300x250

Display / Banners

Appendix

November 2016 Analyst Presentation

For

per

sona

l use

onl

y

Page 31

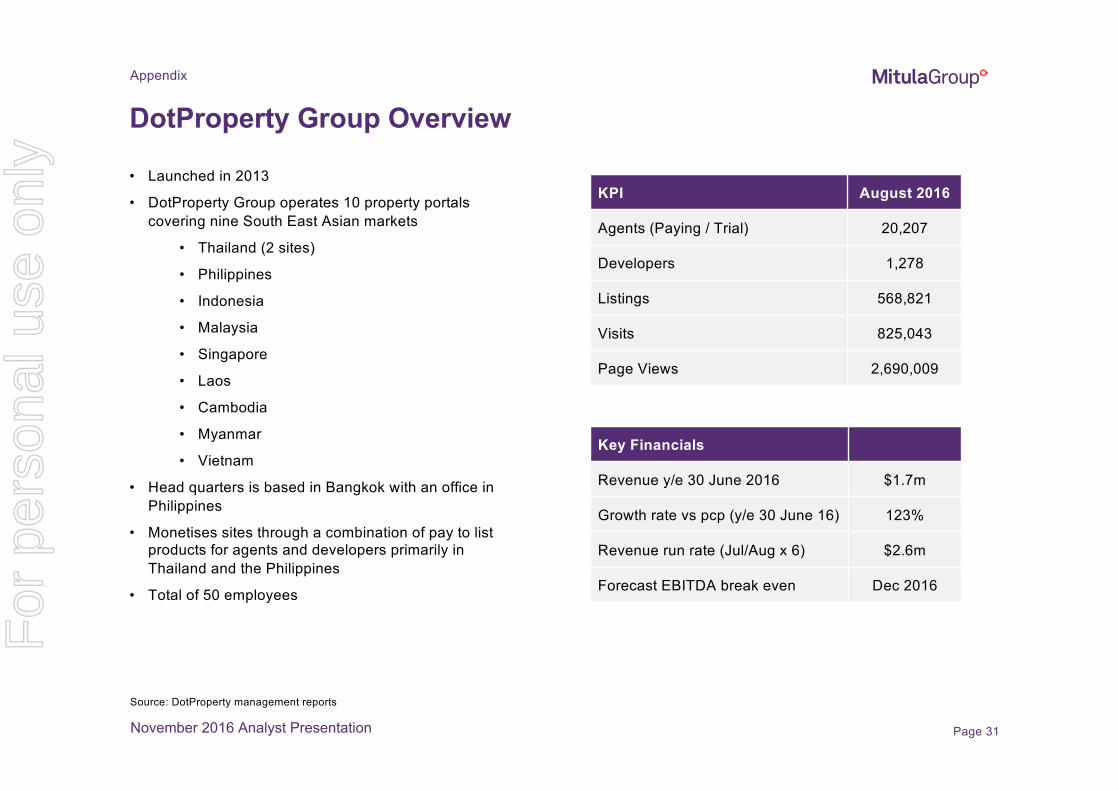

DotProperty Group Overview

• Launched in 2013

• DotProperty Group operates 10 property portals

covering nine South East Asian markets

• Thailand (2 sites)

• Philippines

• Indonesia

• Malaysia

• Singapore

• Laos

• Cambodia

• Myanmar

• Vietnam

• Head quarters is based in Bangkok with an office in

Philippines

• Monetises sites through a combination of pay to list

products for agents and developers primarily in

Thailand and the Philippines

• Total of 50 employees

KPI August 2016

Agents (Paying / Trial) 20,207

Developers 1,278

Listings 568,821

Visits 825,043

Page Views 2,690,009

Key Financials

Revenue y/e 30 June 2016 $1.7m

Growth rate vs pcp (y/e 30 June 16) 123%

Revenue run rate (Jul/Aug x 6) $2.6m

Forecast EBITDA break even Dec 2016

Source: DotProperty management reports

November 2016 Analyst Presentation

Appendix

For

per

sona

l use

onl

y

Page 32

Appendix

Currency Impact on Revenues

Note: Constant currency approach based on using a constant set of currency exchange rates for the complete period rather than monthly average exchange rates. The Mitula Group does not undertake any currency hedging

Source: Internal Management Information.

November 2016 Analyst Presentation

AUD 000’s Sep 2016 Quarter

Sep 2015 Quarter Growth

Revenues (Actual Currency) 7,225 5,996 20.5%

Revenues (Constant Currency) 7,560 5,996 26.1%

Negative exchange rate

movements resulted in

a decrease in year on

year growth of 5.6

percentage points

For

per

sona

l use

onl

y

Page 33

Appendix

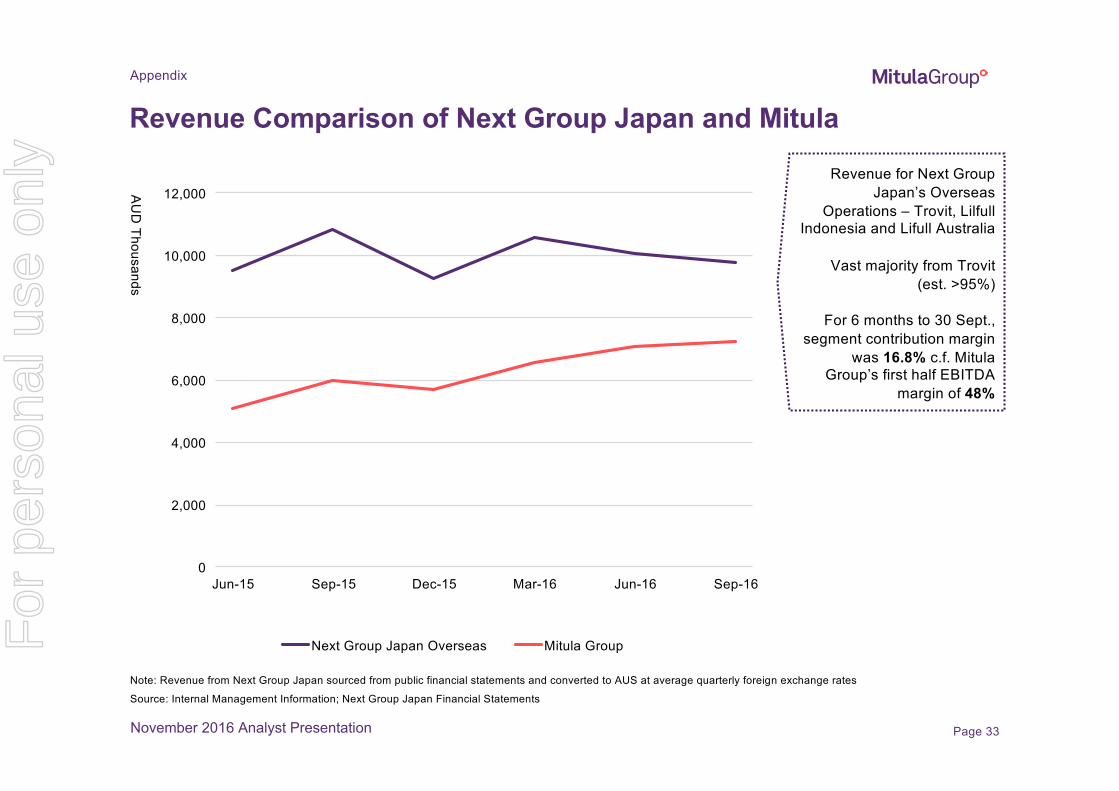

Revenue Comparison of Next Group Japan and Mitula

Note: Revenue from Next Group Japan sourced from public financial statements and converted to AUS at average quarterly foreign exchange rates

Source: Internal Management Information; Next Group Japan Financial Statements

November 2016 Analyst Presentation

0

2,000

4,000

6,000

8,000

10,000

12,000

Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Next Group Japan Overseas Mitula Group

AU

D T

ho

usa

nd

s

Revenue for Next Group

Japan’s Overseas

Operations – Trovit, Lilfull

Indonesia and Lifull Australia

Vast majority from Trovit

(est. >95%)

For 6 months to 30 Sept.,

segment contribution margin

was 16.8% c.f. Mitula

Group’s first half EBITDA

margin of 48%

For

per

sona

l use

onl

y

Gonzalo del Pozo

CEO

Contact us

HQ:

Mitula Group Ltd.

Enrique Granados 6, edif. B

28224 Pozuelo de Alarcón

Madrid, Spain

+34 917 082 147

Simon Baker

Chairman

Contact us

For

per

sona

l use

onl

y

![[Pick the date] - WordPress.com · [Pick the date] [FB ADSENSE NINJA (MAGIC TRICK)] [Pick the date] Surefire Way To Make Money With Adsense | Adsense Labs ADSENSELABS.COM FB ADSENSE](https://img.pdfslide.us/doc/110x75/5ce055df88c993d22e8dc2e8/pick-the-date-pick-the-date-fb-adsense-ninja-magic-trick-pick-the.jpg)