Embed Size (px)

Citation preview

1

Investment OutlookSummary

Uncertain outlook justifies caution. Declining global growth, combined with political turmoil in the form of trade wars and Brexit, is lowering the stock market outlook. We have thus chosen to underweight equities for the first time since 2016.

September 2019

How different asset classes have performed

The chart shows returns on the broad MSCI AC World equity index, Sweden’s OMX equity index and OMRX bond index and the Pan-European High Yield Index currency-hedged to SEK.

Source: Bloomberg/Macrobond

Investors thrown between hope and despairAfter last autumn’s turbulence, the stock market year began in an upbeat mood, driven by a shift in central bank policies towards interest rate cuts and other stim-ulus measures. In addition, hopes that China and the United States could reach a new trade agreement fairly soon helped drive the stock market upturn. As the year progressed, earlier worries about weaker growth were increasingly confirmed, and global economic growth forecasts were lowered. Together with tougher rhetoric in the trade talks, this derailed the summer share price rally. The stock market mood is now dominated by uncertainty and defensive investor behaviour. As uncertainty rose during the summer, this year’s trend towards falling bond yields accentuated greatly. Lower yields in themselves are positive for the stock market, but this time around the sharp decline from already low levels can be interpreted as a signal of increased recession risks.

Weaker economic conditions = weak stock exchanges Macro statistics show that the world economic slowdown is continuing, but the picture is much calmer than signalled by financial markets and the political arena. After a long period of growth, the economic cycle is showing signs of fatigue, especially in the US. Labour shortages and weaker world trade are squeezing manufacturing activity, while the service sector and households have so far shown resilience. We expect slower growth, but see no recession in the cards during the foreseeable future.

However, the weakness in the economy is sufficient to create question marks about future growth and corpo-rate profit levels. Earnings forecasts have been adjusted downward, especially for cyclical industries. We (and the market) now predict unchanged earnings for the full year 2019. The consensus forecast for 2020 points to earnings increases of about 10 per cent, which we consider a bit too optimistic. In light of this, and given the strong upturn in share prices earlier this year, it is no wonder that stock exchanges are becoming more volatile.

We have reduced the risk in our investmentsIt will probably take time before today’s question marks are resolved – given the more uncertain growth picture, and since few breakthroughs have occurred on trade is-sues and Brexit. This year’s stock market rallies also drove up valuations to stretched levels. There is currently a risk of continued market turmoil. In early August we thus chose to reduce the weight of equities in the portfolios we man-age, and our general recommendation is to hold a slightly smaller proportion of equities than in a normal situation.

In fixed income investments, we prefer corporate and emerging market bonds The supportive policies of central banks have benefited investments that have interest rate risk as well as credit risk. The big question is whether central banks can lower key interest rates as much as the market wishes, in order to prevent weaker economic conditions. We predict three more key interest rate cuts by the US Federal Reserve (Fed) and expect the European Central Bank to lower its key rate slightly and re-introduce bond purchases and oth-er easing. We also foresee stable core inflation of around 1.5 per cent in the United States and the euro area. All in all, a situation which suggests that long-term bond yields will also remain ultra-low. In Sweden, this means we no longer expect key rate hikes by the Riksbank but instead foresee an unchanged repo rate both this year and next. We see some advantages in holding corporate bonds, both with lower risk (investment grade) and higher risk (high yield).

In particular, the Fed’s dovish policy stance will enable continued good performance by emerging market bonds (EM debt) for another while, although there is greater uncertainty about these than before. EM debt performed well during the late spring and summer, thanks to relative-ly higher yields in emerging markets and as an effect of stronger EM currencies.

Investment Outlook

2

This document produced by SEB contains general marketing information about its investment products. SEB is the global brand name of Skandinaviska Enskilda Banken AB (publ) and its subsidiaries and branches. Neither the material nor the products described herein are intended for distribution or sale in the United States of America or to persons resident in the United States of America, so-called US persons, and any such distribution may be unlawful. Although the content is based on sources judged to be reliable, SEB will not be liable for any omissions or inaccuracies, or for any loss what-soever which arises from reliance on it. If investment research is referred to, you should if possible read the full report and the disclosures contained within it, or read the disclosures relating to specific companies found on www.seb.se/mb/disclaimers. Information relating to taxes may become outdated and may not fit your individual circumstances. Investment products produce a return linked to risk. Their value may fall as well as rise, and historic returns are no guarantee of future returns; in some cases, losses can exceed the initial amount invested. Where either the underlying funds or you invest in funds or securities denominated in a foreign currency, changes in exchange rates can impact the return. You alone are responsible for your investment decisions and you should always obtain detailed information before taking them. For more information please see inter alia the Key Investor Information Document for funds and the information brochure for funds and for structured products, available at www.seb.se. If necessary, you should seek advice tailored to your individual circumstances from your SEB advisor.

Information about taxation. As a client of our International Private Banking offices in Luxembourg and/or Singapore you are obliged to keep yourself informed of the tax rules applicable in the countries of your citizenship, residence or domicile with respect to bank accounts and financial transactions. You must yourself provide concerned authorities with information as and when required.

Investment Strategy SEB SE-106 40 Stockholm, Sweden

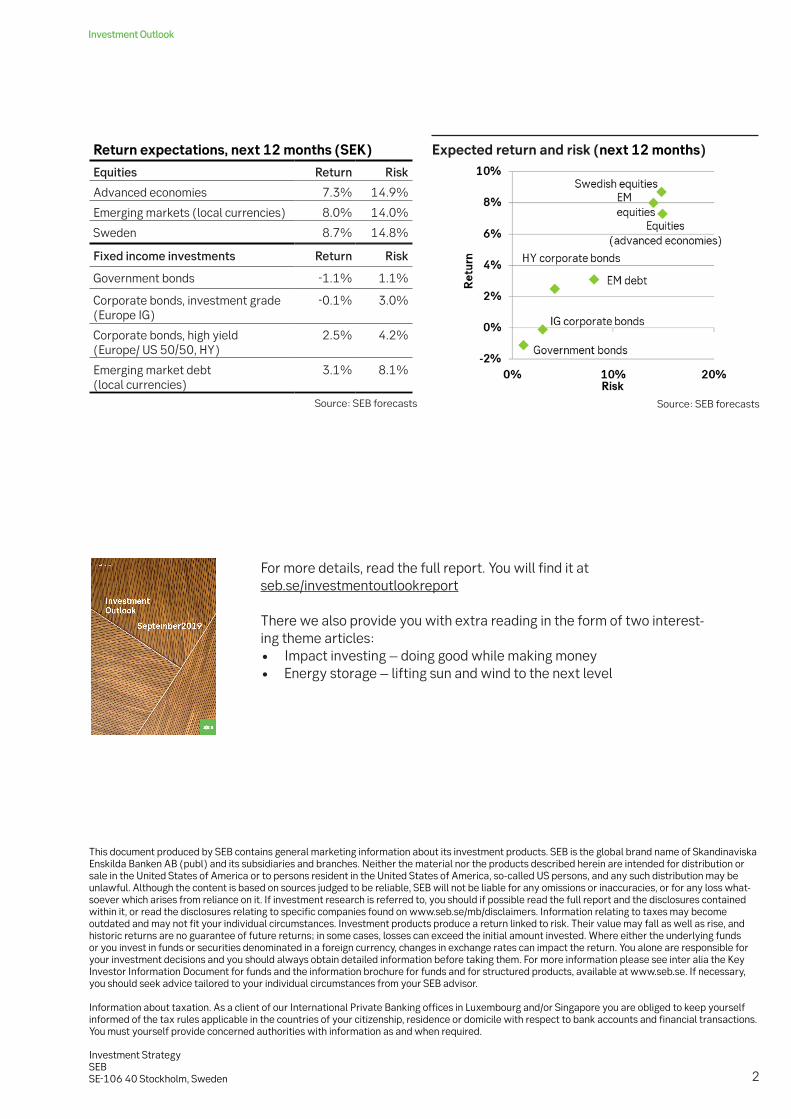

Expected return and risk (next 12 months)Return expectations, next 12 months (SEK)

Equities Return Risk

Advanced economies 7.3% 14.9%

Emerging markets (local currencies) 8.0% 14.0%

Sweden 8.7% 14.8%

Fixed income investments Return Risk

Government bonds -1.1% 1.1%

Corporate bonds, investment grade (Europe IG)

-0.1% 3.0%

Corporate bonds, high yield (Europe/ US 50/50, HY)

2.5% 4.2%

Emerging market debt (local currencies)

3.1% 8.1%

Source: SEB forecasts Source: SEB forecasts

For more details, read the full report. You will find it at seb.se/investmentoutlookreport

There we also provide you with extra reading in the form of two interest-ing theme articles: • Impact investing – doing good while making money• Energy storage – lifting sun and wind to the next level