Embed Size (px)

Citation preview

www.europeanpaymentscouncil.eu

SEPA goes Mobile

Dr. Marijke De Soete

ETSI Security Workshop 2011

19-20 January 2011

Sophia Antipolis, France

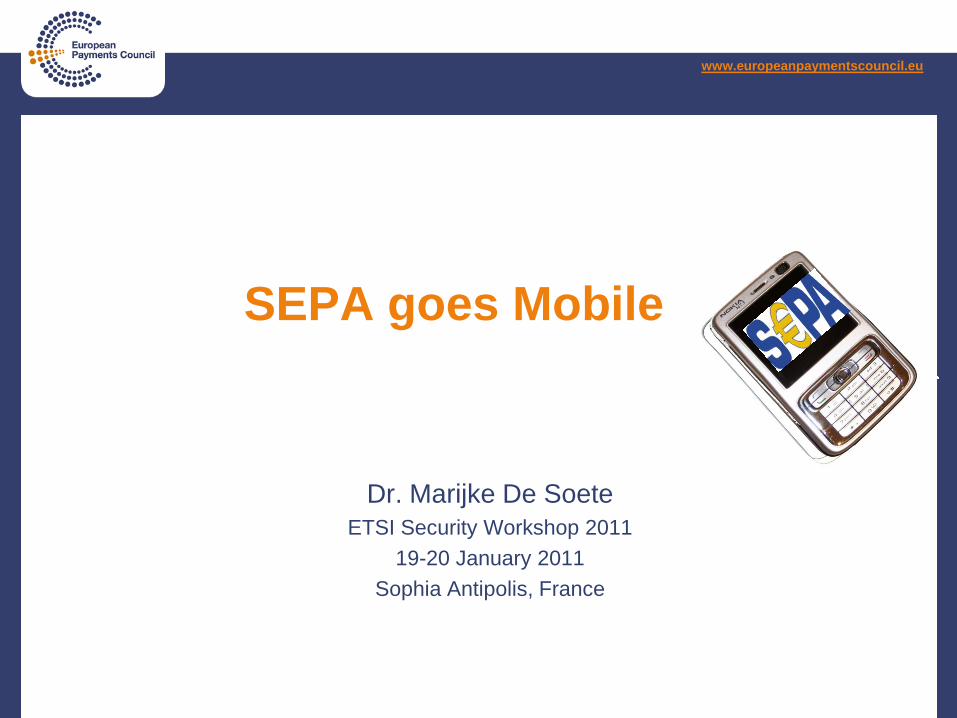

Mobile phone: some statistics

• Over a million new subscribers a day

• Many developed countries over 100% penetration

• Rising fast in developing countries

Data source: Wireless Intelligence

1 billion

subscribers

2 billion

subscribers

4 billion

subscribers

Actual Projected

Estimated 4.5

billion

subscribers

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2003 2004 2005 2006 2007 2008 2009 2010 2011

Glo

bal m

ob

ile s

ub

scri

bers

(m

illio

ns)

Most successful communication device in history

18 January 2011

Mobile phones: an interactive access device

for financial services

A personal device…..

…. that gives instant communications to everyone, anytime, any place

…. that supports multimedia

.... that supports a variety of interactive services

…. that is easy to use

The mobile is expected to become one of the strongest

channels for accessing payments and bank services in

the future .

Need for cooperation on standards, security features and

business models across industries (banks, MNOs, etc).

Convenience for end-users is absolutely key!

18 January 2011

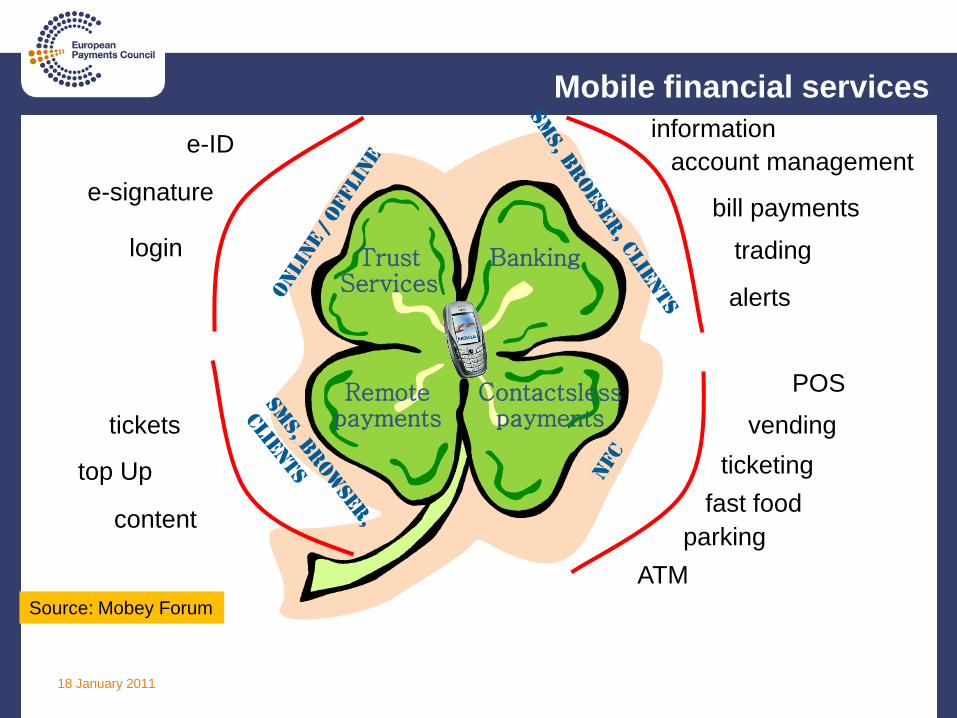

Mobile financial services

Banking

information

account management

bill payments

trading

alerts

Contactslesspayments

POS

vending

ticketing

fast food

parking

ATM

Remotepaymentstickets

top Up

content

TrustServices

e-ID

e-signature

login

Source: Mobey Forum

74 members from 32 countries represent all credit sectors on payments

(approximately 8000 banks)

see www.europeanpaymentscouncil.eu

IS THE DECISION-MAKING AND COORDINATION BODY

OF THE EUROPEAN BANKING INDUSTRY IN RELATION

TO PAYMENTS

EPC develops the payment schemes and frameworks necessary

to realise the Single Euro Payments Area (SEPA)

Specifies business and security requirements and standards

to facilitate the initiation of SEPA payments via e- & mobile

channels

EUROPEAN PAYMENTS COUNCIL (EPC)

REPRESENTS THE EUROPEAN BANKING INDUSTRY IN PAYMENTS

Who are EPC?

6

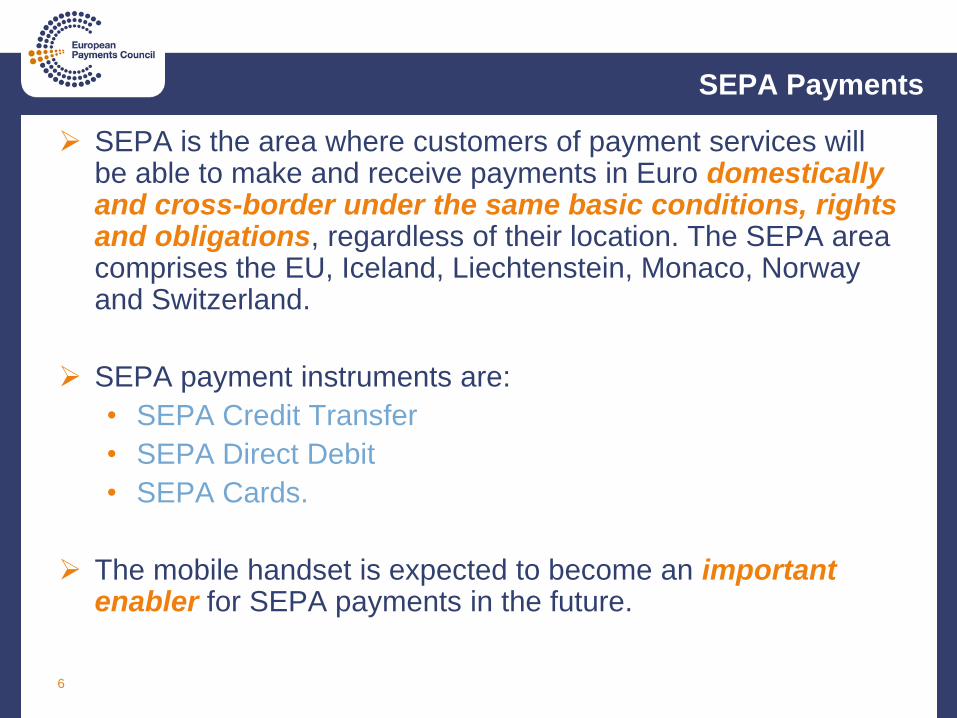

SEPA Payments

SEPA is the area where customers of payment services will be able to make and receive payments in Euro domestically and cross-border under the same basic conditions, rights and obligations, regardless of their location. The SEPA area comprises the EU, Iceland, Liechtenstein, Monaco, Norway and Switzerland.

SEPA payment instruments are:

• SEPA Credit Transfer

• SEPA Direct Debit

• SEPA Cards.

The mobile handset is expected to become an important enabler for SEPA payments in the future.

7

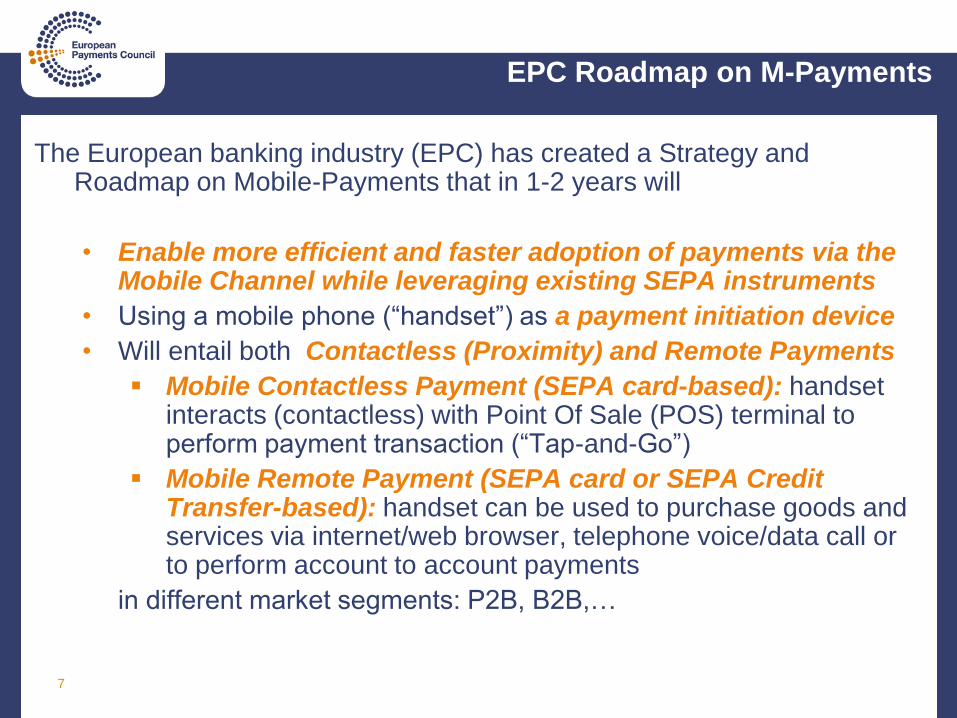

EPC Roadmap on M-Payments

The European banking industry (EPC) has created a Strategy and Roadmap on Mobile-Payments that in 1-2 years will

• Enable more efficient and faster adoption of payments via the Mobile Channel while leveraging existing SEPA instruments

• Using a mobile phone (“handset”) as a payment initiation device

• Will entail both Contactless (Proximity) and Remote Payments

Mobile Contactless Payment (SEPA card-based): handset interacts (contactless) with Point Of Sale (POS) terminal to perform payment transaction (“Tap-and-Go”)

Mobile Remote Payment (SEPA card or SEPA Credit Transfer-based): handset can be used to purchase goods and services via internet/web browser, telephone voice/data call or to perform account to account payments

in different market segments: P2B, B2B,…

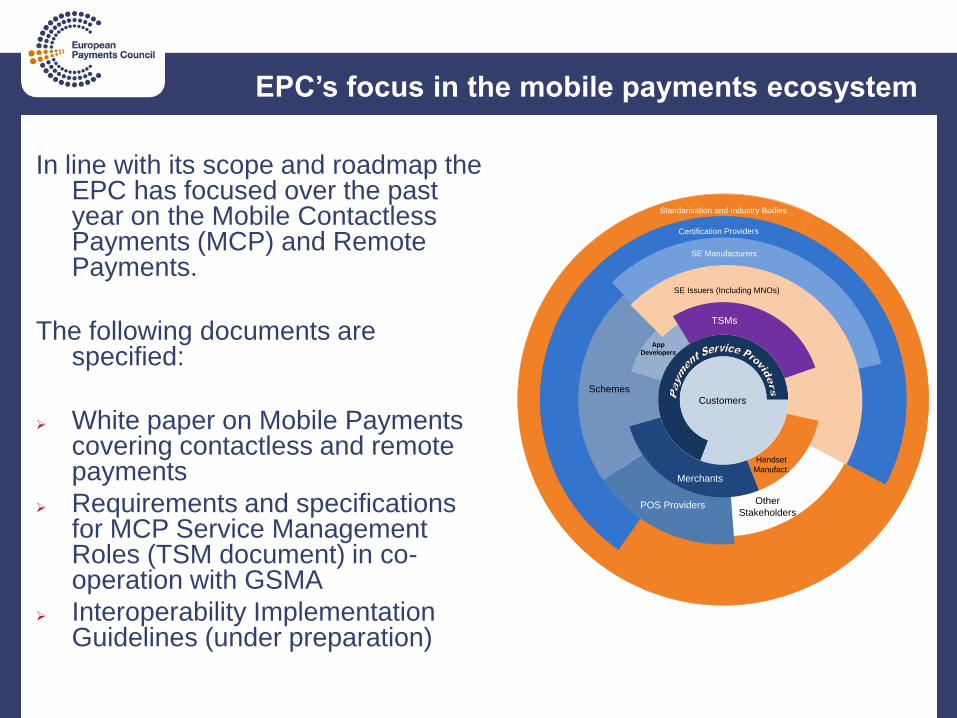

EPC’s focus in the mobile payments ecosystem

In line with its scope and roadmap the EPC has focused over the past year on the Mobile Contactless Payments (MCP) and Remote Payments.

The following documents are specified:

White paper on Mobile Payments covering contactless and remote payments

Requirements and specifications for MCP Service Management Roles (TSM document) in co-operation with GSMA

Interoperability Implementation Guidelines (under preparation)

Other

Stakeholders

Standarisation and Industry Bodies

App

Developers

Certification Providers

POS Providers

Schemes

SE Manufacturers

Customers

SE Issuers (Including MNOs)

Handset

Manufact.

TSMs

Merchants

EPC White paper on M-payments

EPC published a White paper on M-Payments aimed to create

awareness on the subject in the banking community and beyond.

http://www.europeanpaymentscouncil.eu/knowledge_bank_detail.cf

m?documents_id=402

The 1st release includes a high level overview on M-payments as

new channel to existing SEPA payment instruments.

• Through the description of use cases in a daily life of a customer with a

mobile phone it is shown how m-payments can provide efficiency,

convenience and cost-effectiveness.

• Also introduced are the main characteristics of the m-payments

categories (contactless and remote payments) as prioritised by EPC as

well as the payment service provisioning.

• A further section provides more details on MCP

including some business, technical infrastructure,

user experience and standardisation aspects.

9

EPC-GSMA collaboration

30th June 2008: EPC and GSMA announced a co-operation agreement

(http://www.europeanpaymentscouncil.eu/news_detail.cfm?news_id=65)

Cross Industry cooperation

enable banks to deliver more efficiently mobile payments services

leveraging the mobile operator's infrastructure

for the benefits of customers of the banks and MNOs

Initial focus of GSMA-EPC co-operation is

on Mobile Contactless Payments (MCPs)

MCP Service Management (1)

Joint work has focused initially on developing a set of requirements

and specifications for MCP Service Management Roles (SMRs)

and related processes covering functional, technical, security and

legal aspects while ensuring interoperability.

Hereby the MCP, issued by the Banks (Issuers) is stored on the

UICC into the mobile phone.

These SMRs cover the full life cycle management of MCP

applications including loading, personalisation, activation,

maintenance, blocking, etc... and deletion of the MCP.

These SMRs can be fulfilled by MNOs, Issuers or dedicated Third

Parties: “Trusted Service Managers” (TSMs), or a combination

thereof.

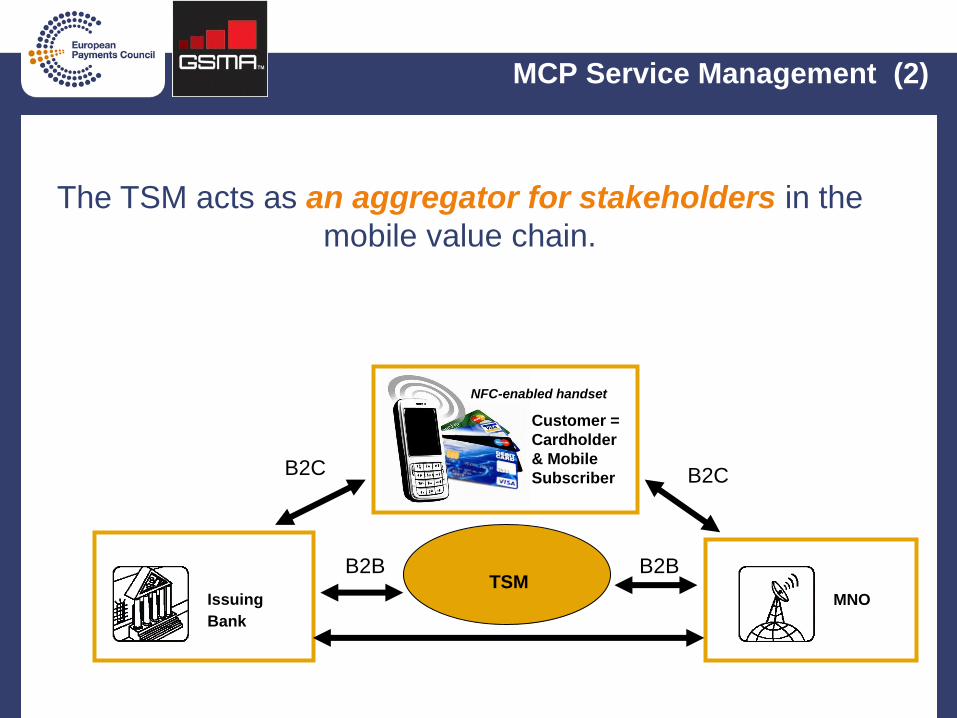

MCP Service Management (2)

MNOIssuing

Bank

NFC-enabled handset

Customer =

Cardholder

& Mobile

Subscriber B2C

TSM

B2C

B2B B2B

The TSM acts as an aggregator for stakeholders in the

mobile value chain.

MCP Service Management (3)

The joint work aims to facilitate the development of commercial

relationships between the MNOs, Issuers and TSMs which are the key

stakeholders in the MCP ecosystem.

EPC and GSMA published the document October 21st 2010 with a

press release.

http://www.europeanpaymentscouncil.eu/knowledge_bank_detail.cfm?d

ocuments_id=423

smooth and safe, quickly built-up

MCP ecosystem

from chaotic, slow MCP

ecosystem development

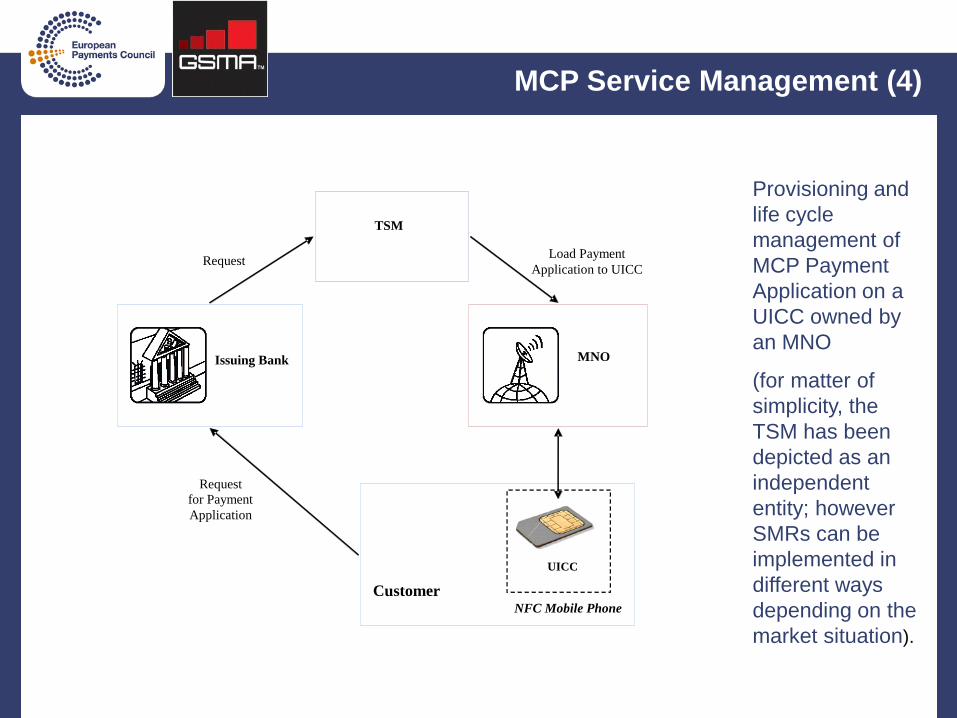

Provisioning and

life cycle

management of

MCP Payment

Application on a

UICC owned by

an MNO

(for matter of

simplicity, the

TSM has been

depicted as an

independent

entity; however

SMRs can be

implemented in

different ways

depending on the

market situation).

MCP Service Management (4)

MNO

Request

for Payment

Application

Load Payment

Application to UICCRequest

NFC Mobile Phone

Customer

UICC

Issuing Bank

TSM

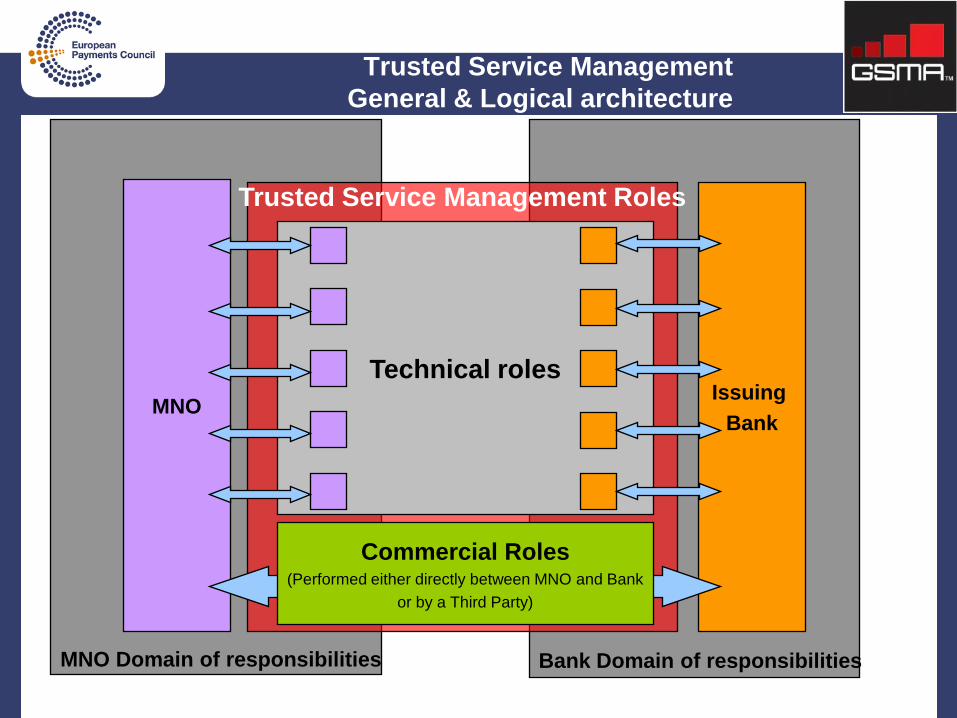

Trusted Service Management

General & Logical architecture

Bank Domain of responsibilitiesMNO Domain of responsibilities

Trusted Service Management Roles

-

Technical roles

MNOIssuing

Bank

Commercial Roles(Performed either directly between MNO and Bank

or by a Third Party)

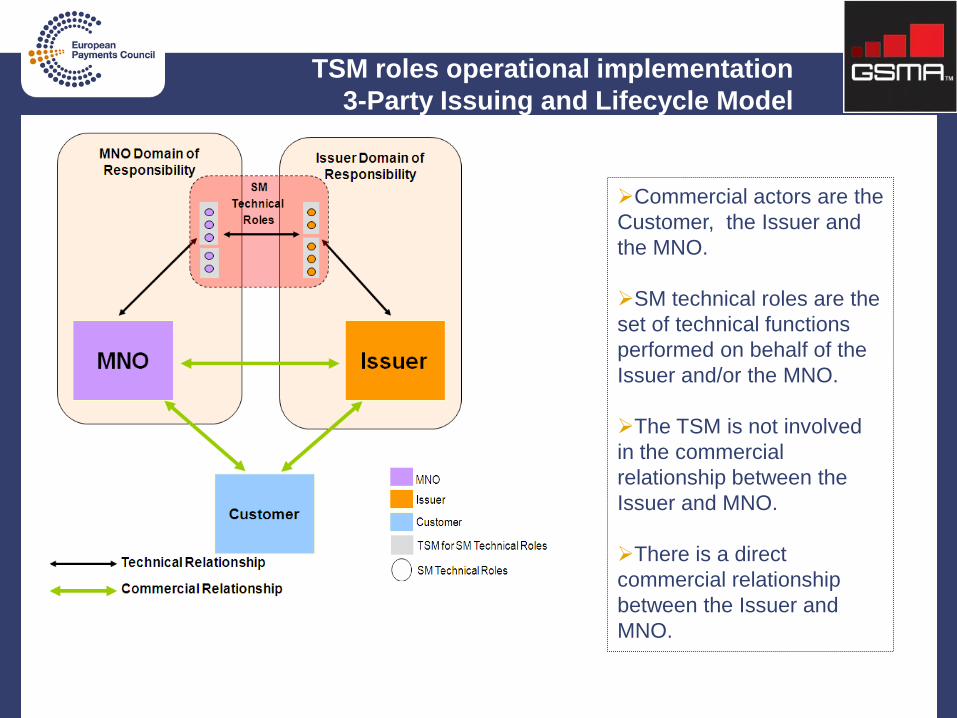

TSM roles operational implementation

3-Party Issuing and Lifecycle Model

Commercial actors are the

Customer, the Issuer and

the MNO.

SM technical roles are the

set of technical functions

performed on behalf of the

Issuer and/or the MNO.

The TSM is not involved

in the commercial

relationship between the

Issuer and MNO.

There is a direct

commercial relationship

between the Issuer and

MNO.

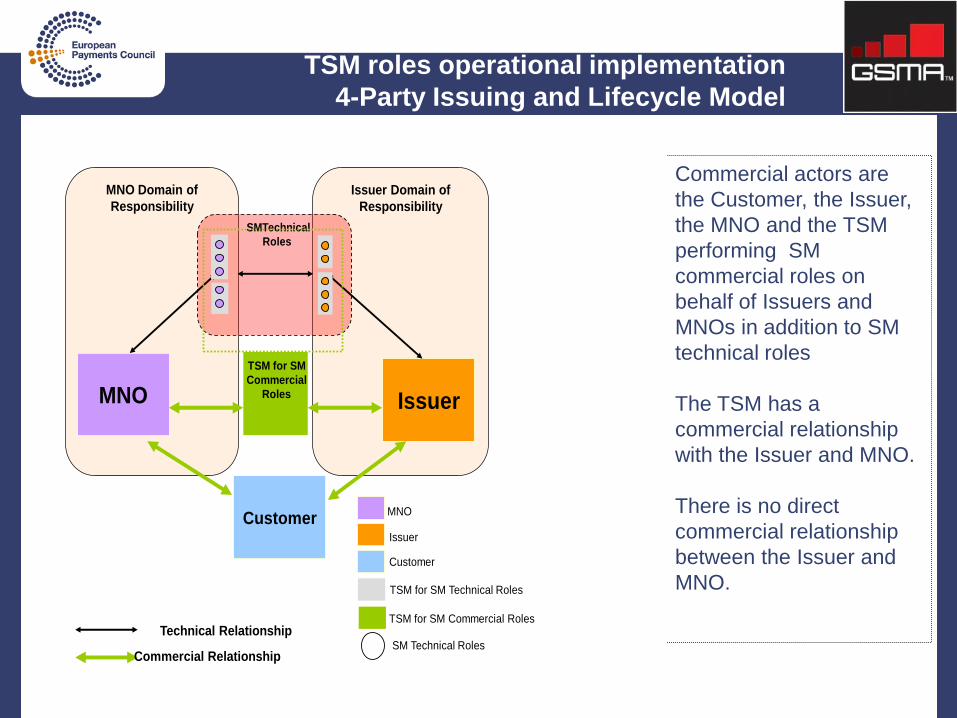

TSM roles operational implementation

4-Party Issuing and Lifecycle Model

Commercial actors are

the Customer, the Issuer,

the MNO and the TSM

performing SM

commercial roles on

behalf of Issuers and

MNOs in addition to SM

technical roles

The TSM has a

commercial relationship

with the Issuer and MNO.

There is no direct

commercial relationship

between the Issuer and

MNO.

.

MNO Domain of

Responsibility

Issuer Domain of

Responsibility

-

Customer

MNO Issuer

Technical Relationship

Commercial Relationship

MNO

Issuer

Customer

TSM for SM Technical Roles

TSM for SM Commercial Roles

SM Technical Roles

TSM for SM

Commercial

Roles

SMTechnical

Roles

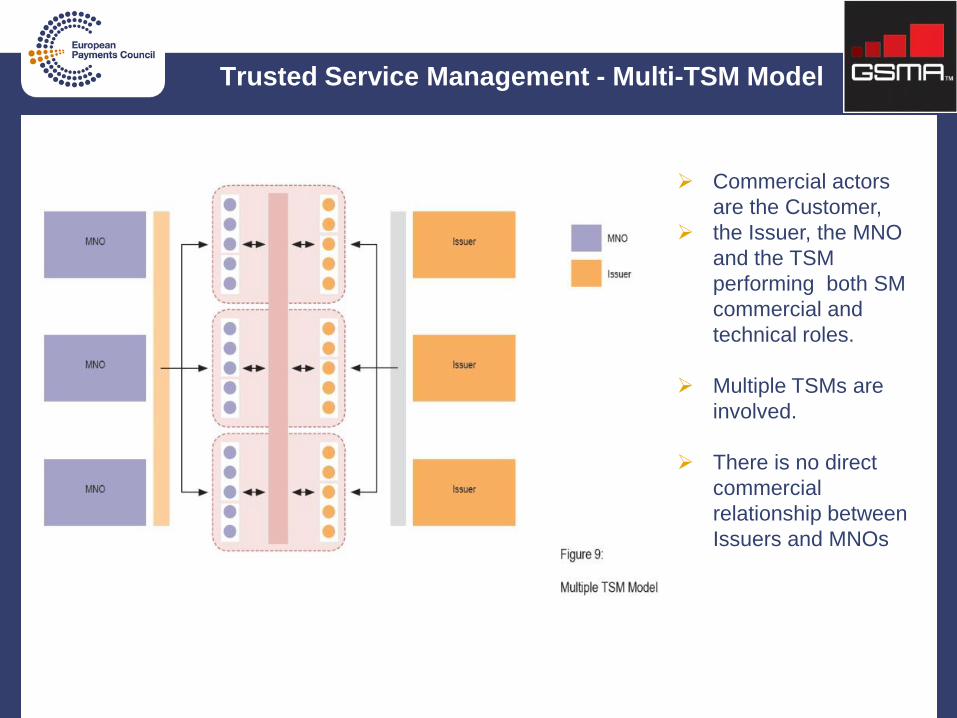

Trusted Service Management - Multi-TSM Model

Commercial actors

are the Customer,

the Issuer, the MNO

and the TSM

performing both SM

commercial and

technical roles.

Multiple TSMs are

involved.

There is no direct

commercial

relationship between

Issuers and MNOs

18 January 2011

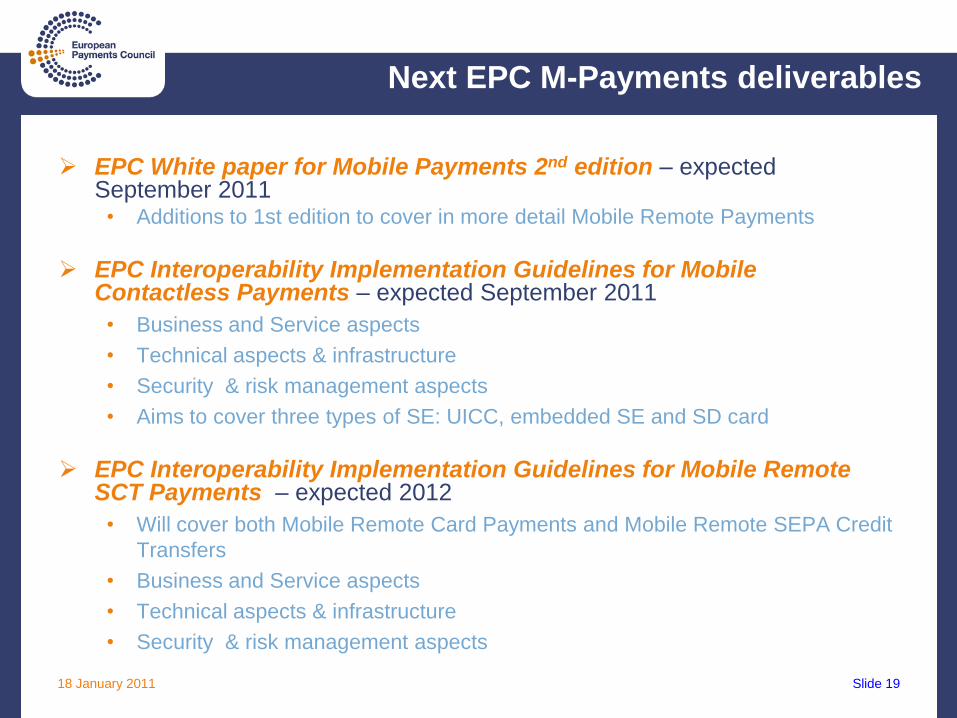

Next EPC M-Payments deliverables

EPC White paper for Mobile Payments 2nd edition – expected September 2011

• Additions to 1st edition to cover in more detail Mobile Remote Payments

EPC Interoperability Implementation Guidelines for Mobile Contactless Payments – expected September 2011

• Business and Service aspects

• Technical aspects & infrastructure

• Security & risk management aspects

• Aims to cover three types of SE: UICC, embedded SE and SD card

EPC Interoperability Implementation Guidelines for Mobile Remote SCT Payments – expected 2012

• Will cover both Mobile Remote Card Payments and Mobile Remote SEPA Credit

Transfers

• Business and Service aspects

• Technical aspects & infrastructure

• Security & risk management aspects

Slide 19

18 January 2011

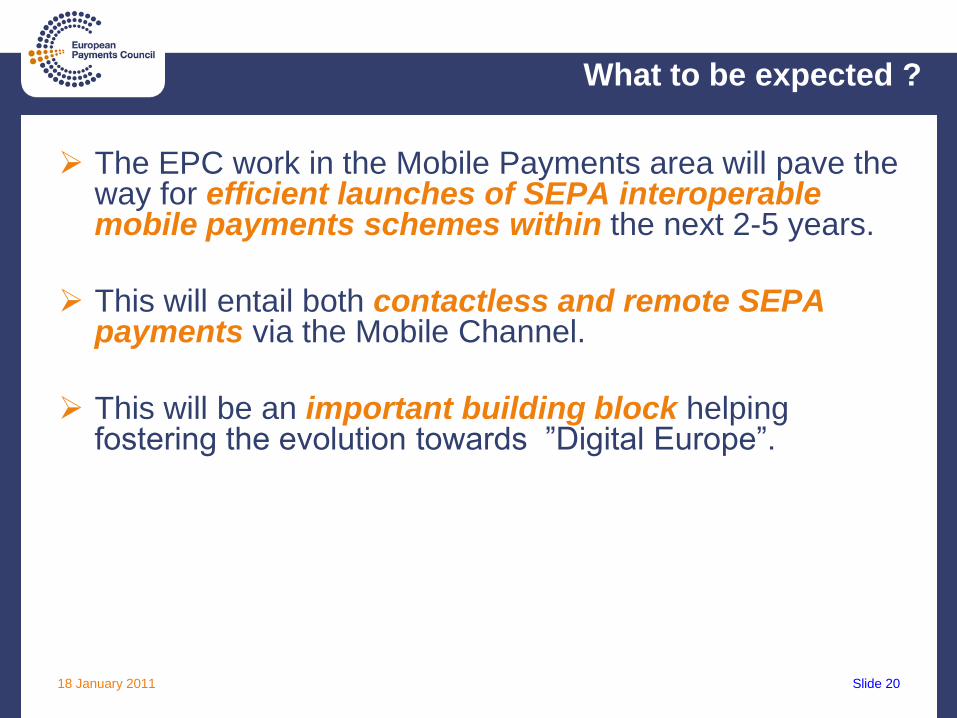

What to be expected ?

The EPC work in the Mobile Payments area will pave the way for efficient launches of SEPA interoperable mobile payments schemes within the next 2-5 years.

This will entail both contactless and remote SEPA payments via the Mobile Channel.

This will be an important building block helping fostering the evolution towards ”Digital Europe”.

Slide 20

Information

21

EPC website: http://www.europeanpaymentscouncil.eu/

All documentation can be freely downloaded

or contact: