Embed Size (px)

Citation preview

SEPA card schemes, can they happen?

Stephan Becker, Payfair

click here to add main title

click here to add sub title

New and innovative payment solutions

payfair

SEPA Card Schemes, can they happen?

EPCA Brussels, March 21, 2013

2

click here to add main title

click here to add sub title

New and innovative payment solutions

payfair's outgoing position

22/03/2013 3

click here to add main title

click here to add sub title

New and innovative payment solutions

-There are/were 3 Payment • SEPA concept for cards has been introduced • Authorities requested more competition and pushing for European Scheme

• EAPS • Bank and Domestic Scheme driven • Protecting existing business and players • None profit – none innovative

• Monnet • Bank driven • Protecting existing revenues and players

• payfair • neutral initiative

• Innovative • Visa - Vpay

• Will Visa Europe be part of Visa Inc. in 2013? .

What has happened?

22/03/2013 4

click here to add main title

click here to add sub title

New and innovative payment solutions

• European Commission and SEPA authorities claim that less 2% of the work for SDD (which should be completed by 2014) has been accomplished

• Mobile Payments drive growth in other regions and become more and more important in the SEPA region

• New technologies require modern infrastructure and legacy systems (NFC, QR….)

• Retailers are looking for “European Solution” and push for BPA

• Mobile Operators are moving into Payments

• New players from new industries move into Payment (Google, Apple,…)

An ever changing environment…

22/03/2013 5

click here to add main title

click here to add sub title

New and innovative payment solutions

The evolution of stock

prices between 2006 and

today - suggests that (de-

mutualised) card

schemes prosper in a

period that banks

struggle ....

Banks and card schemes – are interests still aligned?

-59,47%

+1.102,79%

Time for a new approach?

22/03/2013 6

click here to add main title

click here to add sub title

New and innovative payment solutions

• Global Schemes have strengthened their positions

• Domestic Schemes disappear or need costly investment for upgrade

• Competition has not really “increased”

• No open market yet

• Prices for consumers have not decreased the opposite - in

some areas the increased

• New entrants have failed

• Innovation is blocked

The result of regulatory changes so far…..

22/03/2013 7

click here to add main title

click here to add sub title

New and innovative payment solutions

click here to add main title

click here to add sub title

New and innovative payment solutions

Is it reasonable to upgrade this original but ‘veteran’ version with today’s new ‘standard’ features and characteristics ? At what final cost ? Image reputation ? Uncertainty about final performances, life cycle and investments and about future developments ...

2013: normal & ‘mandatory’ features & characteristics Consumption 3,7 l/100km, CO² 99 gr/km ABS-EPS-DCS-Airbags ***** EuroNCap (anti collision test) GPS-MP3-Electronics...

(VW Golf I, 1977) (VW Golf VII, 2011)

Better to opt straight for the new and better one with cost reductions & latest new technologies

Legacy – just a comparison …

Fiscal status :

if >25 years old

« vintage car ! »

22/03/2013 9

click here to add main title

click here to add sub title

New and innovative payment solutions

Global schemes want to protect their stronghold over the payment value chain and integrate mobile as an ingredient in the payment proposition and brand. Mobile network operators want to leverage their infrastructure and expand their offering to their customers and integrate payments as an ingredient of a mobile phone proposition under their own brand. Since in payments as well as in mobile interoperability is key the Telco’s will need to set up new multilateral brands / schemes.

Knowing that Mobile payments will change the industry

Banks – especially in emerging markets - will have the opportunity to co-operate with Telco’s under new brands and schemes to offer new

innovative payment solutions to their customers

22/03/2013 10

click here to add main title

click here to add sub title

New and innovative payment solutions

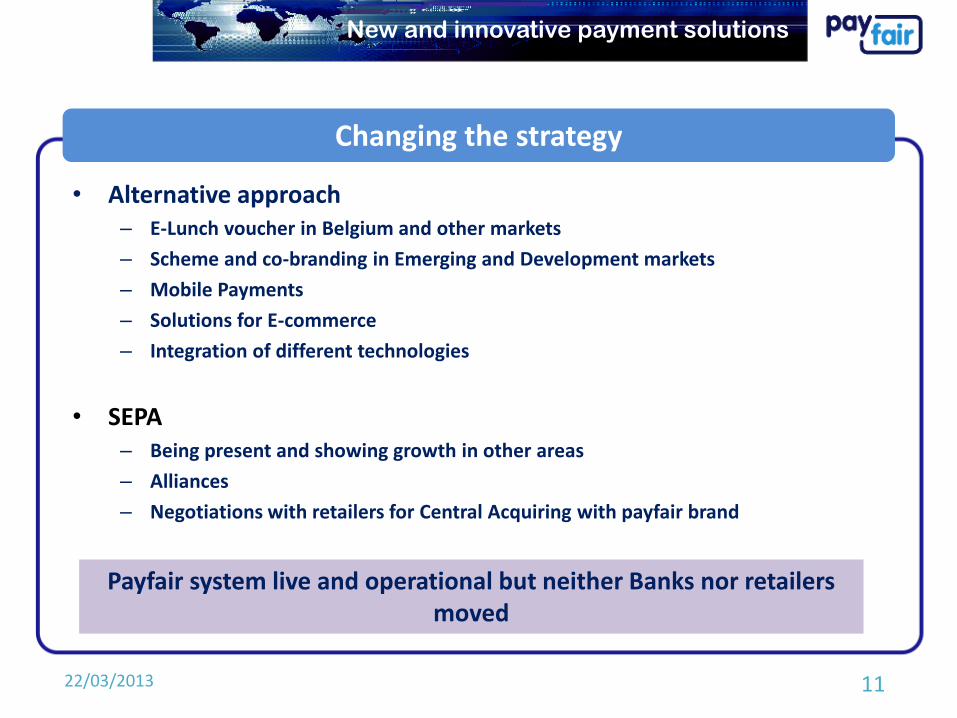

Changing the strategy

Payfair system live and operational but neither Banks nor retailers moved

22/03/2013 11

• Alternative approach – E-Lunch voucher in Belgium and other markets

– Scheme and co-branding in Emerging and Development markets

– Mobile Payments

– Solutions for E-commerce

– Integration of different technologies

• SEPA – Being present and showing growth in other areas

– Alliances

– Negotiations with retailers for Central Acquiring with payfair brand

click here to add main title

click here to add sub title

New and innovative payment solutions

1. Payment scheme solutions

2. Merchant acquiring solutions

3. Technology solutions

payfair – 3 lines of business addressing the needs of the changing payment landscape

12 22/03/2013

click here to add main title

click here to add sub title

New and innovative payment solutions

Robust industry with growing volumes and revenues Limited legacy systems – opportunities for innovative solutions and business models Market entry for new players in the payment business

Payfair’s focus: CEE and MENA – fast growth requires market specific solutions

• High penetration of mobile phones – high usage of mobile banking and payments

• Markets with no legacy payment infrastructure: opportunity to immediately move to next generation of payments

• Low penetration of bank accounts, cards ...

• Limited payment infrastrucure demanding new ways of value transfer – funding, transferring, collecting, cashing ...

• Growing importance of prepaid, mobile payments, virtual money, ewallets ... • Expectation to have (secure) payment convenience at ‘finger tip’ and ubiquituous access

22/03/2013 13

click here to add main title

click here to add sub title

New and innovative payment solutions

Technology – the Payfair Edge

22/03/2013 14

Payfair technology enables customers to significantly expand their electronic payments offering

In certain emerging markets 80% of the populations have a mobile phone, but only 20% a bank account - already up to 80% of the monthly salaries are paid to mobile accounts

In most market more young people have mobile Phones than Bank Accounts

Immediate opportunity for: P2P payments Internet purchases Contactless terminals – often mass

transit Digital media purchases

Unbanked

New Merchants

Community New merchant categories and regions can be obtained easily with existing mobile infrastructure and low cost devices

Merchants not connected to existing payment networks can process payfair payments via existing GPRS or Mobile network connections

Payfair and payfair partners offer end-to-end solutions for e- and m-commerce – including merchant acquiring if required

Payfair solutions fit into many governments modernization and efficiency agendas

Payfair and partners offer merchant solutions integrating payment with tax and accounting data reporting

click here to add main title

click here to add sub title

New and innovative payment solutions

22/03/2013 15

The payfair Retail offer

• Central European (or more) payfair brand acquiring – Only 1 technical connection

– Same service and fees in all countries

• Integration of different and new payment solution – Mobile with NFC, Sound, SMS +PIN, QR

• Independency – Not driven by banks

– Not owned by any party

• Flexibility – Rules & Regulations reflect changing environment

• Innovation – Mobile payments allow new and cheaper infrastructure

– New technologies (QR….) allow new types of transactions

click here to add main title

click here to add sub title

New and innovative payment solutions

• Mobile ATM Solution – Withdraw cash with mobile phone at ATMs

• Mobile POS Solutions – Pay at merchant terminals with mobile phone

• E-commerce solutions – Pay online with mobile phone

– Virtual cards

• Example – [email protected] cash at ATM service in Russia

• Partnership with one of the largest ATM networks in the country

• Rosbank (part of the major international banking group) – and one of the major acquirers in Russia - supports the solution

• Partnership with two of the major mobile and prepaid networks

22/03/2013 16

The payfair Technology Offer

click here to add main title

click here to add sub title

New and innovative payment solutions

Scheme for flexible top-up and top-down transactions Acquirer of the web-merchants -sites Virtual / plastic cards with ATM access / usage if required Interface through webservices MCC blocking per account type Turnover limits per account type Reporting per Sub-BIN range API to selected card bureaus Support of multiple card designs Fraud management

payfair (prepaid) card – virtual or real EMV – that can be used by the consumer to buy online

Specialized to meet the needs of Internet gambling / gaming Supporting responsible gambling/ gaming Offering flexible top-up options Offering a connected bank account and support instant transfer (top-down) Offering various withdrawal options including ATM-based pay outs and Online Shopping

Product Requirements Payfair Proposition

The payfair E-commerce offer

22/03/2013 17

click here to add main title

click here to add sub title

New and innovative payment solutions

Key point – broadening proprietary payment propositions

The payfair Co-Branding offer

22/03/2013 18

The purpose is to integrate payFair methods of payment (cards and other) into the PAY

national payments system operated by Liberty bank by co-

hosting of PAY and payfair methods of payments on the

same instrument.

Liberty bank to issue co-branded payfair / PAY cards with co-hosted PAY and payfair applications. Transaction with a PAY/ Payfair method of payment

• carried out within the PAY network s a PAY transaction. • carried out outside the PAY network is a payfair transaction

Liberty bank to open PAY merchants for payfair acceptance. PAY merchants will be enabled to accept other payfair methods of payment (i.e. not issued in combo with a PAY method of payment) via the PAY gateway also.

click here to add main title

click here to add sub title

New and innovative payment solutions

The purpose is to create the Azerbaijan National Payment System. Azerbaijan Banks will

have direct access to the governance and will have a

decisive role for such elements that are critical to the fair functioning of a scheme.

Key point – domestic card with international acceptance

The payfair (Regional) Scheme offer

22/03/2013 19

• Managed by Azerbaijan authorities, • Open Governance and possibility for Azerbaijan banks to participate in decision process • Transparent and easy scheme and fee model managed by Azerbaijan authority. • Issuing business is open for non-bank Issuers • Reduce scheme and connection costs (maintenance and operations) • International acceptance • Transparent and low transaction costs generate substantial cost savings.

No investment for acceptance. Productivity gain: by combining loyalty + payment functions on the same card

• Operations will be based on the best of breed of existing card schemes standards (EMV, ISO 8583, ISO 20022).

click here to add main title

click here to add sub title

New and innovative payment solutions

Thank you!

Stephan Becker, CEO payfair Group 4-Bras Building Mechelsesteenweg 455/19 1950 Kraainem (Belgium)

T: +32 2 767 66 66 M: +32 479 81 66 45 [email protected]

22/03/2013 20