Embed Size (px)

Citation preview

maam

SENIOR RESOURCE ASSOCIATION, INC.

Financial Statements and Single Audit Reports

June 30, 2019

(With Independent Auditors' Report Thereon)

SENIOR RESOURCE ASSOCIATION, INC.

Independent Auditors' Report

Financial Statements:

Statement of Financial Position

Statement of Activities

Statement of Functional Expenses

Statement of Cash Flows

Notes to Financial Statements

Single Audit Reports:

Table of Contents

June 30, 2019

Independent Auditors' Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards

Independent Auditors' Report on Compliance for Each Major Federal Program and State Project and on Internal Control over Compliance Required by the Uniform Guidance and Chapter 10.650, Rules of the Auditor General of the State of Florida

Schedule of Expenditures of Federal Awards and State Projects

Notes to Schedule of Expenditures of Federal Awards and State Projects

Schedule of Findings and Questioned Costs

1-2

3

4

5-6

7

8-16

17 -18

19-20

21-22

23

24-25

11am Morgan• Jacoby• Thurn• Boyle & Associates, P.A.

Certified Public Accountants

Independent Auditors' Report

The Board of Directors Senior Resource Association, Inc.:

Report on the Financial Statements

We have audited the accompanying financial statements of Senior Resource Association, Inc. ( the Association) which comprise the statement of financial position as of June 30, 2019, and the related statements of activities, functional expenses, and cash flows for the year then ended, and the related notes to the financial statements.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to the financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, that financial statements referred to above present fairly, in all material respects, the financial position of Senior Resource Association, Inc. as of June 30, 2019, and the changes in its net assets and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

( Continued) 700 - 20th Street • Vero Beach, Florida 32960 Phone 772-562-4158 Telefax 772-563-2024 • www.mjtbcpa.com

maam Other Matters

Other Information

2

Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The accompanying schedule of expenditures of federal awards and state projects, as required by Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and Chapter 10.650, Rules of the Auditor General of the State of Florida, is presented for purposes of additional analysis and is not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated, in all material respects, in relation to the financial statements as a whole.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report December 13, 2019, on our consideration of the Association's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part on an audit performed in accordance with Government Auditing Standards in considering the Association's internal control over financial reporting and compliance.

Report on Summarized Comparative Information

We have previously audited the Association's June 30, 2018 financial statements, and we expressed an unmodified audit opinion on those audited financial statements in our report dated November 8, 2018. In our opinion, the summarized comparative information presented herein as of and for the year ended June 30, 2018 is consistent, in all material respects, with the audited financial statements from which it has been derived.

Emphasis of Matter

As discussed in note 2 to the financial statements, in 2019 the Association adopted new accounting guidance ASU 2016-14. Our opinion is not modified with respect to this matter.

December 13, 2019

3

SENIOR RESOURCE ASSOCIATION, INC.

Statement of Financial Position

June 30, 2019 (with summarized information as of June 30, 2018)

2019 2018 Without With

Restrictions Restrictions Total Total Assets

Current assets: Cash and cash equivalents $ 469,019 163,437 632,456 763,557 Investments 15,166 Grants receivable 672,407 672,407 554,679 Contributions receivable 615,076 615,076 96,450 Accounts receivable 85,319 85,319 108,711 Other receivables 3,345 3,345 624 Other assets 302A36 302A36 269,926

Total current assets 2,147,602 163,437 2,311,039 1,809,113

Contributions receivable, noncurrent 52,670 Assets restricted for capital projects 37,720 . 37,720 90,891 Property and equipment, net 1,526,828 2,730,839 4,257,667 4,760,976

Total assets $ 3.674.430 2.931.996 6.606.426 6.713.650

Liabilities and Net Assets

Current liabilities: Note payable under line of credit Accounts payable 393,174 393,174 370,260 Accrued expenses 234,565 234,565 194,745 Deferred revenue 237,821 237,821 218,255

Total current liabilities 865,560 865,560 783,260

Net assets: Without donor restrictions 2,808,870 2,808,870 2,424,090 With donor restrictions 2,931,996 2,931,996 3,506,300

Total net assets 2,808,870 2,931,996 5,740,866 5,930,390

Total liabilities and net assets $ 3.674.430 2.931.996 6.606.426 6,713.650

See accompanying notes to financial statements.

4

SENIOR RESOURCE ASSOCIATION, INC.

Statement of Activities

Year ended June 30, 2019 (with summarized information for the year ended June 30, 2018)

2019 2018 Without With

Restrictions Restrictions Total Total Revenues and other support:

Governmental fees and grants - operating $ 5,638,840 5,638,840 5,174,527 Governmental fees and grants - capital 440,807 406,780 847,587 1,599,180 Contributions 802,624 322,399 1,125,023 562,129 Program service fees 468,375 468,375 596,699 United Way 141,500 141,500 134,250 Fundraising, net of direct costs of

$130,646 and $70,975, respectively 272,239 272,239 253,369 Investment return, net 7,241 7,241 3,792 Other revenue 2,450 2,450 34,214 Gain (loss) on disposal of property and

equipment 16,002 16,002 (80,084) 7,790,078 729,179 8,519,257 8,278,076

Nets assets released from restrictions 1,303,483 (1,303,483) Total revenues and other support 9,093,561 (574,304) 8,519,257 8,278,076

Expenses and losses: Program services:

Transportation 5,074,245 5,074,245 4,937,955 Adult day services 809,673 809,673 808,726 Case management services 800,222 800,222 686,016 Nutrition 776,762 776,762 683,924 Guardian pro gram 10,394 10,394

Total program services 7,471,296 7,471,296 7,116,621

Supporting services: Management and general 1,045,828 1,045,828 831,090 Fundraising 191,657 191,657 141,120 Rental activity 21,890

Total supporting services 1,237,485 1,237,485 994,100

Total expenses 8,708,781 8,708,781 8,110,721

Change in net assets 384,780 (574,304) (189,524) 167,355

Net assets, beginning of year 2,424,090 3,506,300 5,930,390 5,763,035

Net assets, end of year $ 2,808.870 2,931.996 5.740.866 5.930.390

See accompanying notes to financial statements.

5

SENIOR RESOURCE ASSOCIATION, INC.

Statement of Functional Expenses

Year ended June 30, 2019 (with summarized information for the year ended June 30, 2018)

Program Services Adult Case Day Management

Transgortation Services Services Nutrition

Salaries and wages $ 1,703,663 387,441 167,756 156,563 Fringe benefits 175,728 54,721 19,075 13,960 Payroll taxes 144,271 32,071 12,962 13,041 Employment expenses 47,210 14,426 2,165 15,079 Retirement 5A52 18 1~603 881

Total employee related 2,076,324 488,677 203,561 199,524

Maintenance 531,389 12,229 3,265 29,585 Fuel 518,908 8,381 Client expenses 348,497 566,403 Meals 17,202 456,077 Insurance 290,769 13,800 3,105 14,319

Occupancy 296,721 44,444 2,985 8,364 Professional fees 96,024 21,160 7,047 11,293 Advertising 29,847 19,902 942 5,929 Supplies 19,385 22,584 979 11,327 Utilities 18,727 22,518 1,691 6,159

Subcontract services 23,761 Telephone 4,062 4,559 253 1,275 Community outreach 2,942 6,953 1,733 2,142 Interest expense and bank charges 433 71 311 Travel 1,049 1,027 2,844 1,466

Printing 1,758 1,200 128 38 Fundraising expense Postage 2,651 14 520 913 Dues and subscriptions 3,925 1,671 246 583 Equipment 9,094 737 796 6,401

Other 10,212 1,384 Licenses and fees 1,398 230 1,158

4,253,470 713,313 796,569 766,629

Depreciation and amortization 820~775 96~360 3~653 10~133

Total expenses $ 520742245 8092673 8002222 7762762

See accompanying notes to financial statements.

6

Su~~orting Services Management

Guardian and 2019 2018 Program Total General Fundraising Total Total

$ 2,415,423 672,939 50,866 3,139,228 3,185,045 263,484 57,349 6,668 327,501 320,532 202,345 52,748 4,160 259,253 272,433

7,255 86,135 10,737 9,072 105,944 91,259 7,954 10,458 18,412 14,097

7,255 2,975,341 804,231 70,766 3,850,338 3,883,366

576,468 53,682 14,390 644,540 662,696 527,289 527,289 558,144 914,900 914,900 518,661 473,279 473,279 400,718

175 322,168 2,030 324,198 295,544

352,514 9,101 2,979 364,594 357,169 936 136,460 70,464 37,696 244,620 110,948 693 57,313 41,996 20,238 119,547 99,527

9 54,284 3,278 18,153 75,715 87,827 49,095 10,566 534 60,195 63,285

23,761 6,733 30,494 51,972 3 10,152 9,585 113 19,850 21,992

13,770 6,861 20,631 20,959 815 815 14,541

874 7,260 8,541 328 16,129 13,435

3,124 1,717 456 5,297 12,548 9,259 9,259 10,020

44 4,142 3,882 1,638 9,662 9,296 325 6,750 1,436 292 8,478 7,337

17,028 2,147 333 19,508 6,398

11,596 5,259 16,855 5,781 80 2,866 267 332 3,465 2,916

10,394 6,540,375 1,027,626 191,657 7,759,658 7,215,080

930,921 18,202 949,123 895,641

$ 10~394 7A71~296 1~045~828 191~657 8~708~781 8~110)21

7

SENIOR RESOURCE ASSOCIATION, INC.

Statement of Cash Flows

Year ended June 30, 2019 (with summarized information for the year ended June 30, 2018)

2019 Cash flows from operating activities:

Change in net assets $ (189,524) Adjustments to reconcile change in net assets to net cash flows

provided by (used in) operating activities: Depreciation 949,123 Amortization of debt issuance costs Grants and contributions restricted to capital projects (472,228) Gain on investments, net (2,007) (Gain) loss on disposal of property and equipment (16,002) (Increase) decrease in:

Grants receivable (117,728) Contributions receivable (465,956) Accounts receivable 23,392 Other receivables (2,721) Other assets (32,510)

Increase (decrease) in: Accounts payable (3,501) Accrued expenses 39,820 Deferred revenue 19l566

Net cash provided by (used in) operating activities (270)76)

Cash flows from investing activities: Proceeds from sale of investments 17,173 Increase in assets restricted for capital projects (65,448) Proceeds from assets restricted for capital projects 80,619 Proceeds from sale of property and equipment 141,537 Capital expenditures (544l934)

Net cash used in investing activities (371l053)

Cash flows from financing activities: Grants and contributions restricted to capital projects 510,228 Proceeds from line of credit, net of repayments Principal loan payments

Net cash provided by financing activities 510)28

Net increase (decrease) in cash and cash equivalents (131,101)

Cash and cash equivalents, at beginning of year 763l557

Cash and cash equivalents, at end of year $ 632.456

Supplemental schedule of noncash investing and financing activities:

2018

167,355

895,641 2,043

(997,058) (2,375) 80,084

(7,742) 198,309

2,262 409

(16,093)

(43,581) 260

(43l643) 235l871

233 (112,000) 112,773 354,718

(ll151l940) (796)16)

959,058 210,000 (19)15)

ll149l843

589,498

174l059

763,557

During the year ended June 30, 2019, the Association acquired certain equipment totaling $26,415 with trade accounts payable.

During the year ended June 30, 2018, the Association sold property and repaid related notes payable totaling $681,598.

See accompanying notes to financial statements. ·

(1) Organization

8

SENIOR RESOURCE ASSOCIATION, INC.

Notes to Financial Statements

June 30, 2019

The Senior Resource Association promotes independence and dignity in our community by providing services to older adults and transportation to all. Senior Resource Association, Inc. (the Association) was incorporated as a nonprofit organization under Internal Revenue Code Section 50l(c)(3) in January 1974 to provide programs and services designed to support an active, healthy, independent life for older adults. The Association assists seniors and their families in finding the resources they seek, delivers quality, professional services that meet a senior's individual needs, and provides programs and volunteer opportunities for active older adults. Key programs include: Nutrition Services, Adult Day Care, Case Managed Services, Information and Referral, and Transportation. The Association is recognized as the lead agency in Indian River County for home and community based services for older adults. In addition, the Association is contracted by the Indian River County as the Community Transportation Coordinator operating GoLine, a public transit system, and Community Coach, a door-to-door transportation program.

(2) Summary of Significant Accounting Policies

( a) Basis of Presentation

On August 18, 2016, FASB issued ASU 2016-14, Not-for-Profit Entities (Topic 958) - Presentation of Financial Statements of Not-for-Profit Entities. The update addresses the complexity and understandability of net asset classification, deficiencies in information about liquidity and availability of resources, and the lack of consistency in the type of information provided about expenses and investment return. The Association has adjusted the presentation of these statements accordingly. The ASU has been applied retrospectively to all periods presented.

To ensure observance of limitations and restrictions placed on the use of resources available to the Association, the accounts of the Association are maintained in accordance with the principles of fund accounting. This is the procedure by which resources are classified for accounting and reporting into funds established according to their nature and purpose and in accordance with activities or objectives specified by donors.

Fund balances and transactions have been classified into two classes of net assets -without donor restrictions or with donor restrictions as follows:

Net assets without donor restrictions - Net assets that are not subject to donorimposed restrictions and may be expended for any purpose in performing the primary objectives of the Association. These net assets may be used at the discretion of the Association's management and Board of Directors.

Net assets with donor restrictions - Net assets subject to stipulations imposed by donors and grantors. Some donor restrictions are temporary in nature; those restrictions will be met by actions of the Association or by the passage of time. Other donor restrictions are perpetual in nature, whereby the donor has stipulated the funds be maintained in perpetuity.

(Continued)

9

SENIOR RESOURCE ASSOCIATION, INC.

Notes to Financial Statements

(b) Revenue Recognition

All contributions/ donations are considered available for unrestricted use unless specifically restricted by the donor. Contributions/donations are considered restricted if a donor imposes a restriction that may be satisfied by the passage of time or the actions of the Association.

When a donor restriction expires, that is, when a stipulated time restriction ends or purpose restriction is accomplished, net assets with donor restrictions are reclassified to net assets without donor restrictions and reported in the statement of activities as net assets released from restrictions. Support that is restricted by the donor is reported as an increase in net assets w-ithout donor restrictions if the restriction expires in the reporting period in which the support is recognized.

The Association has contracted to provide non-emergency transportation services and in-home services such as homemaking, respite, and case management, to all eligible Medicaid clients. Reimbursement from Medicaid is based on units of service provided.

(c) Cash Equivalents

For purposes of the statement of cash flows, the Association considers all highly liquid debt instruments purchased with original maturities of three months or less to be cash equivalents. As of June 30, 2019, cash equivalents includes money market funds of $44,333.

( d) Investments

Investments are reported at fair value. Donated investments are recorded at fair market value on the date of donation and adjusted for changes in market value at year end.

(e) Property and Equipment

Property and equipment are recorded at cost for purchased items and fair value for contributed items. Maintenance and repairs are charged to expense as incurred. Depreciation is provided on the straight-line method over the estimated useful life of the assets, which ranges from 4 to 3 0 years.

(I) Debt Issuance Costs

Debt issuance costs are presented as a direct deduction from the carrying amount of the related debt liability and amortization of such costs are presented as interest expense. Debt issuance costs are amortized on a straight-line basis over the term of the related agreement.

(Continued)

10

SENIOR RESOURCE ASSOCIATION, INC.

N ates to Financial Statements

(g) Contributed Use of Long-Lived Assets

Indian River County (the County) has received on behalf of the Association, Department of Transportation (the DOT) Section 5307, Federal Transit Capital and Operation Assistance Formula Grants. Under the grants, the County is the grantee and the Association is a sub-recipient. The DOT requires certain capital acquisitions purchased under the grants to be titled to the grantee (the County). The County has given the use of these long-lived assets to the Association, for as long as the Association remains the County's Community Transportation Coordinator.

The Association has recorded these assets as capital additions and recognized expenses in the period the long-lived assets are used. Additionally, the contribution is reported as restricted support that increases net assets with donor restrictions. Expense for depreciation is recognized over the asset's useful life, and net assets are periodically reclassified from net assets with donor restrictions to net assets without donor restrictions as these expenses are recognized.

(h) Donated services

The Association does not record donated services for any volunteers working in a nonprofessional capacity since the volunteers' time does not meet the criteria for recognition.

(i) Functional Allocation of Expenses

The Association allocates its expenses on a functional basis among its various programs and support services. Expenses that can be identified with a specific program or support service are allocated directly according to their natural expenditure classification. Other expenses that are common to several functions are allocated based on an analysis of personnel time or square footage utilized for the related activities.

0) Income Taxes

The Association is generally exempt from federal and state income taxes under Section 501(c)(3) of the Internal Revenue Code and is not considered a private foundation under Section 509(a)(2) of the Internal Revenue Code. The Association has unrelated business income resulting from rental activities that may result in taxable income. As of June 30, 2019, the Association has approximately $175,000 of unused net operating loss carryforwards available to be applied to future taxable income that expire 2026 through 2035. The Association's income tax filings are subject to audit by various taxing authorities. The Association's open audit periods are 2016 - 2019.

(k) Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make . estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

(Continued)

11

SENIOR RESOURCE ASSOCIATION, INC.

Notes to Financial Statements

([) Concentrations of Credit Risk

Financial instruments that potentially subject the Association to concentrations of credit risk consist principally of cash, investments, pledges receivable, and assets restricted to capital projects. Cash balances maintained in financial institutions may at times be in excess of the FDIC limit. The Association has not experienced any losses on such amounts and does not believe it is exposed to any significant risk with respect to such balances.

The Association had no significant concentrations of credit risk with respect to contributions receivable and collateral is not required to support contributions receivable.

(m) Prior Period Information

The financial statements include certain prior-year summarized comparative information in total but not by net asset class. Such information does not include sufficient detail to constitute a presentation in conformity with accounting principles generally accepted in the United States of America. Accordingly, such information should be read in conjunction with the Association's financial statements for the year ended June 30, 2018 from which the summarized information was derived.

(3) Liquidity and Availability of Resources

The following represents the Association's financial assets as of June 30, 2019 and 2018.

Financial assets: Cash and cash equivalents Investments Current receivables

Total financial assets

Less amounts not available to be used for general expenditures

Financial assets available to meet general expenditures during the next twelve months

2019 2018

$ 469,019 625,361 15,166

1,376,147 760,464

1~845,166 1,400~991

$ 1,845.166 1,400.991

Financial assets are available for general expenditures within one year of the balance sheet date, other than noted above. Grants receivable subject to time restrictions are considered available as they will be collected within one year.

Additionally, the Association maintains a $300,000 line of credit, as discussed in more detail in note 5, which is available to meet cash flow needs.

(Continued)

12

SENIOR RESOURCE ASSOCIATION, INC.

Notes to Financial Statements

(4) Property and Equipment

As of June 30, 2019 and 2018, the Association's property and equipment consisted of the following:

2019 2018

Land $ 217,101 218,409 Buildings and improvements 2,487,957 2,709,682 Vehicles 1,070,301 1,088,892 Vehicles - title restricted 5,573,866 6,043,430 Furniture and computer equipment 649,337 589,981 Furniture and computer equipment - FT A restricted 1~587~882 1A75~094

11,586,444 12,125,488 Less accumulated depreciation 7~328~777 7~364~512

$ 4~257~667 4~760~976

Depreciation expense amounted to $949,123 and $895,641 for the years ended June 30, 2019 and 2018, respectively.

The cost of vehicles and equipment contributed to the Association for their use amounted to $7,161,748 at June 30, 2019, and was originally acquired under Federal Transit Administration (FT A) or Florida Department of Transportation (FDOT) grants awarded to the County in the current and prior years. Disposal of restricted vehicles and equipment with individual values greater than $5,000, or disposed of before the end of service lives, requires reimbursement of the sales proceeds to the granting agency in an amount proportionate to its original percentage participation in the grant. Alternatively, the proceeds may be used to offset the costs of replacement equipment subject to the approval of the granting agency. The net book value of vehicles and equipment acquired under FTA and FDOT grants totaled $2,596,998 and $133,841, respectively at June 30, 2019. During the year ended June 30, 2019, proceeds received on disposal of these assets were appropriately reinvested. There were no disposals of these assets during the year ended June 30, 2018.

(5) Note Payable under Line of Credit

The Association maintains a $300,000 line of credit providing for interest at the prime rate (5.5% at June 30, 2019) and is due on demand. The line of credit agreement requires an annual thirty-day resting period with a zero balance prior to each anniversary date of the loan. As of June 30, 2019, the outstanding balance on the line of credit was $-0- and the Association was in compliance with the provisions of the loan agreement.

(Continued)

13

SENIOR RESOURCE ASSOCIATION, INC.

Notes to Financial Statements

(6) Commitments and Contingencies

Leases

The Association leased land and buildings from the County under an agreement that terminates on May 31, 2021 and provides for a total rental of $7 due in advance. The lease is cancelable in the event the Association ceases acting as the County's Transit Service Provider under its transportation operations.

The Association subleased additional land and buildings from the County under a lease agreement that terminates on May 31, 2022 and provides for a total rental of $5 due in advance. The lease is cancelable in the event the Association ceases acting as the County's transit service provider under its transportation operations.

The estimated fair value of the support from the County associated with these leases has been reflected in the accompanying statement of activities as contribution revenue and lease expense of $232,000 for the year ended June 30, 2019.

The Association leases certain office equipment under an operating lease that expires in 2020. The committed annual payments as of June 30, 2019 for 2020 totals $12,592.

Lease expense totaled $28,883 and $27,206 for the years ended June 30, 2019 and 2018, respectively.

Federal and State Grants

The Association has received federal and state grants for specific purposes that are subject to audit by the grantor agencies. Entitlements to these resources are generally conditional upon compliance with the terms and conditions of grant agreements and applicable federal and state regulations, including the expenditure of resources for allowable purposes. Any disallowance resulting from a grantor audit may become a liability of the Association. No provision for any liability that may result has been recognized in the Association's financial statements.

(Continued)

14

SENIOR RESOURCE ASSOCIATION, INC.

Notes to Financial Statements

(7) Governmental Fees and Grants

The Association received governmental fees and grants during the years ended June 30, 2019 and 2018 under the following programs:

Area Agency on Aging Grants: Community Care for the Elderly $ 517,168

6,260 187,472 56,570

452,001 2,723

175,115 58,287

Home Care for the Elderly Alzheimer's Respite Services Nutrition Services Incentive Program Special Programs for the Aging:

Title III, Part B - Supportive Services and Senior Centers

Title III, Part C - Nutrition Services National Family Caregiver Support - Title III, Part

E - Supportive Services Emergency Home Energy Assistance

Florida Commission for the Transportation Disadvantaged Trip and Equipment Grant Program

Federal Department of Transportation Grants: Federal Transit Capital Assistance Federal Transit Operating Assistance Public Transportation for Non urbanized Areas Bus and Bus Facilities Formula Program

Florida Department of Transportation Grants: Block Grants Transit Corridor Operating Grant Service Development Grant Elderly and Persons with Disabilities Capital

Assistance Pro gram Regional Mobility Management Facilitator Program

Grant Enhanced Mobility for Seniors and Individuals with

Disabilities Operating Assistance Grant

Indian River County

Martin County

Total governmental fees and grants

-176,243 350,905

54,937 36,352

757,491

716,027 1,145,853

67,718

494,625 100,642 340,267

131,560

80,446

58,718

1,173,879

33,294

124,177 339,797

58,012 44,964

386,973

962,091 1,465,328

66,695 196,717

512,137 133,145 298,900

72,946

79,650

47,784

1,296,265

$ 6.486,427 6,773.707

As of June 30, 2019, the Association had $3,850,008 in unearned operating revenues and $2,131,979 in unearned capital revenues available for future expenditures under these grants through June 30, 2019. The Association has expenditures of $163,875 in prepaid insurance along with the corresponding deferred revenue.

(Continued)

15

SENIOR RESOURCE ASSOCIATION, INC.

Notes to Financial Statements

(8) Net Assets With Donor Restrictions

Net assets with donor restrictions as of June 30, 2019 and 2018 are available for the following specific purposes:

2019 2018

Vehicles and equipment - title restricted $ 2,730,839 3,211,093 Meals On Wheels programs 123,832 126,406 Charitable remainder trust 52,670 Adult day care scholarships 30,000 22,540 Capital projects 37,720 90,891 Guardianship program 9,605 Time restricted promise to give 2l700

Total $ 2~931 ~996 3~506~300

In June 2019, the Association was awarded a $141,500 grant from United Way. A portion of the grant will be funded on a census-based reimbursement basis and the remainder will be for the Association's meals on wheels program.

Net assets were released from donor restrictions by incurring expenses or by otherwise satisfying restrictions during the years ended June 30, 2019 and 2018 related to the following:

Vehicles and equipment - title restricted Meals On Wheels programs Capital projects Adult day care scholarships Time restricted promise to give Silvertones music program Guardianship program

Total

(9) Retirement Plan

$

$

2019

887,034 181,319 118,619 22,540 57,526 26,050 10395

1~303~483

2018

731,645 122,994 112,773

38,740 2,700

26,843

1 ~035~695

The Association has established a tax sheltered annuity plan for the benefit of its employees in accordance with Section 403(b) of the Internal Revenue Code. Under the plan, a contribution is made to the account of each participating employee, based on their compensation. Employer contributions represent a 5 0% match of the employee contribution, up to a maximum of 4% of the employee's wages. Employees can request that an additional voluntary deduction from their gross wages be contributed to the plan.

(Continued)

16

SENIOR RESOURCE ASSOCIATION, INC.

Notes to Financial Statements

Employees hired on or after October 1, 2007 vest in employer contributions over a five year vesting schedule. The plan was amended and restated in May 2019 to comply with current law and did not result in significant changes to the benefits under the plan.

For the years ended June 30, 2019 and 2018, the Association contributed $18,412 and $14,097, respectively, on behalf of the employees.

(10) Subsequent Events

In preparing these financial statements, the Association has evaluated events and transactions for potential recognition or disclosure through December 13, 2019, the date the financial statements were available to be issued.

Subsequent to June 30, 2019, the Association was awarded the following grants:

Indian River County (October 1, 2019 to September 30, 2020) $ 1,285,927 Community Care for the Elderly 2019/20 annual award (July 1,

2019 to June 30, 2020 grant period) 458,683 Home Care for the Elderly 2019/20 annual award (July 1, 2019 to

June 30, 2020 grant period) 75,638 Alzheimer's Disease Initiative 2019/20 annual award (July 1, 2019

to June 30, 2020 grant period) 206,212 Florida Commission for the Transportation Disadvantaged Trip and

Equipment Grant Program (July 1, 2019 to June 30, 2020 grant period) - Indian River County 417,367

Florida Commission for the Transportation Disadvantaged Trip and Equipment Grant Program (July 1, 2019 to June 30, 2020) -Martin County 389,473

Public Transit Block, Florida Department of Transportation (July 1, 2019 to June 30, 2020) 580,817

Formula Grants for Rural Areas, Florida Department of Transportation (July 1, 2019 to June 30, 2020) 76,178

Florida Commission for the Transportation Disadvantaged - Shirley Conroy Rural Area Capital Assistance Program Grant (July 1, 2019 to June 30, 2020)-Martin County 31,108

Florida Department of Elder Affairs (October 1, 2019 to June 30, 2021) 69,472

Indian River County Hospital District (October 1, 2019 to September 30, 2020) 30,000

Florida Commission for the Transportation Disadvantage -Innovation and Service Development Grant (December 1, 2019 to June 30, 2020) - Indian River County 121,680

Florida Commission for the Transportation Disadvantage -Innovation and Service Development Grant (December 1, 2019 to June 30, 2020) - Martin County 196,200

Area Agency on Aging - Emergency Home Energy Assistance Program (October 1, 2019 to September 30, 2020) 46,796

Total grants $ 329852551

11am Morgan• Jacoby• Thurn• Boyle 17 & Associates, P.A.

Certified Public Accountants

Independent Auditors' Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an

Audit of Financial Statements Performed in Accordance with Government Auditing Standards

The Board of Directors Senior Resources Association, Inc.:

We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of Senior Resources Association, Inc. (the Association), which comprise the statement of financial position as of June 30, 2019 and the related statements of activities, functional expenses, and cash flows for the year then ended, and the related notes to the financial statements, and have issued our report thereon dated December 13, 2019.

Internal Control over Financial Reporting

In planning and performing our audit of the financial statements, we considered the Association's internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Association's internal control. Accordingly, we do not express an opinion on the effectiveness of the Association's internal control.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the Association's financial statements will not be prevented, or detected and corrected, on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Association's financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

( Continued) 700 - 20th Street • Vero Beach, Florida 32960 • Phone 772-562-4158 • Telefax 772-563-2024 ° www.mjtbcpa.com

maam 18

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the Association's internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Association's internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

December 13, 2019

11am Morgan• Jacoby• Thurn• Boyle 19 & Associates, P.A.

Certified Public AccOLmtants

Independent Auditors' Report on Compliance for Each Major Federal Program and State Project and on

Internal Control over Compliance Required by the Uniform Guidance and Chapter 10.650, Rules of the Auditor General of the State of Florida

The Board of Directors Senior Resources Association, Inc.:

Report on Compliance for Each Major Federal Program and State Project

We have audited Senior Resource Association, Inc.' s (the Association) compliance with the types of compliance requirements described in the 0MB Compliance Supplement and the requirements described in the Florida Department of Financial Services' State Projects Compliance Supplement that could have a direct and material effect on each of the Association's major federal programs and major state projects for the year ended June 30, 2019. The Association's major federal programs and major state projects are identified in the summary of auditors' results section of the accompanying schedule of findings and questioned costs.

Management's Responsibility

Management is responsible for compliance with compliance with federal and state statutes, regulations, and the terms and conditions of its federal awards and state projects applicable to its federal programs and state projects.

Auditor's Responsibility

Our responsibility is to express an opinion on compliance for each of the Association's major federal programs and state projects based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and audit requirements of Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), and Chapter 10.650, Rules of the Auditor General of the State of Florida. Those standards, the Uniform Guidance, and Chapter 10.650 require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program or state project occurred. An audit includes examining, on a test basis, evidence about the Association's compliance with those requirements and performing such other procedures as we considered necessary in the circumstances.

We believe that out audit provides a reasonable basis for our opinion on compliance for each major federal program and state project. However, our audit does not provide a legal determination of the Association's compliance.

Opinion on Each Major Federal Program and State Project

In our opinion, the Association complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs and major state projects for the year ended June 30, 2019.

(Continued) 700 - 20th Street• Vero Beach, Florida 32960 • Phone 772-562-4158 • Telefax 772-563-2024 • www.mjtbcpa.com

maam 20

Report on Internal Control over Compliance

Management of the Association is responsible for establishing and maintaining effective internal control over compliance with the types of compliance requirements referred to above. In planning and performing our audit, we considered the Association's internal control over compliance with the types of requirements that could have a direct and material effect on a major federal program or state project in order to determine the auditing procedures for the purpose of expressing our opinion on compliance, and to test and report on internal control over compliance in accordance with the Uniform Guidance and Chapter 10.650, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of the Association's internal control over compliance.

A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program or state project on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program or state project will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program or state project that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance.

Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be deficiencies, significant deficiencies, or material weaknesses. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses, as defined above.

The purpose of this report on internal control over compliance is solely to describe the scope of our testing of internal control over compliance and the results of that testing based on the requirements of the Uniform Guidance and Chapter 10.650. Accordingly, this report is not suitable for any other purpose.

December 13, 2019

21

SENIOR RESOURCE ASSOCIATION, INC.

Schedule of Expenditures of Federal Awards and State Projects

Year ended June 30, 2019

CFDAI Federal/State Agency CSFA Grant

Federal Award/State Project No. No.

U.S. Department of Health and Human Services: Pass-through from Florida Department of Elder

Affairs, Area Agency on Aging: Aging Cluster:

Nutrition Services Incentive Program 93.053 IU016-9300 93.053 IA019-9300

Special Programs for the Aging - Title III, Part B - Supportive Services and Senior Centers 93.044 IA016-9300

93.044 IA019-9300 Special Programs for the Aging- Title III,

Part C - Nutrition Services 93.045 IA016-9300 93.045 IA019-9300

Total Aging Cluster

National Family Caregiver Support - Title III, Part E - Supportive Services 93.052 IA016-9300

93.052 IA019-9300 Emergency Home Energy Assistance 93.568 IP015-9300

93.568 IP018-9300

Total U.S. Department of Health and Human Services

U.S. Department of Transportation: Pass-through from Indian River County, Florida:

Federal Transit Cluster: Federal Transit Capital and Operating

Assistance (Section 5307)* 20.507 FL-90

Public Transportation for Non urbanized Areas (Section 5 311) 20.509 ARQ46

20.509 G1462 Transit Services Program Cluster:

Elderly and Persons with Disabilities Capital Assistance Program (Section 5310) 20.513 YR42

Regional Mobility Management Facilitator Program (Section 531 OM) 20.513 GO891

Enhanced Mobility for Seniors and Individuals with Disabilities Operating Assistance (Section 5310) 20.513 GO178 Total Transit Services Program Cluster

Total U.S. Department of Transportation

Total expenditures of Federal awards

* - denotes major pro gram

Total Expenditures

$ 28,525 28,045

79,795 96,448

179,351 171~554 583,718

25,468 29,469 13,365 22~986

675~006

1,861,881

33,342 34,376

116,942

71,508

58,718 247)-68

2~176,767

2~851~773

(Continued)

22

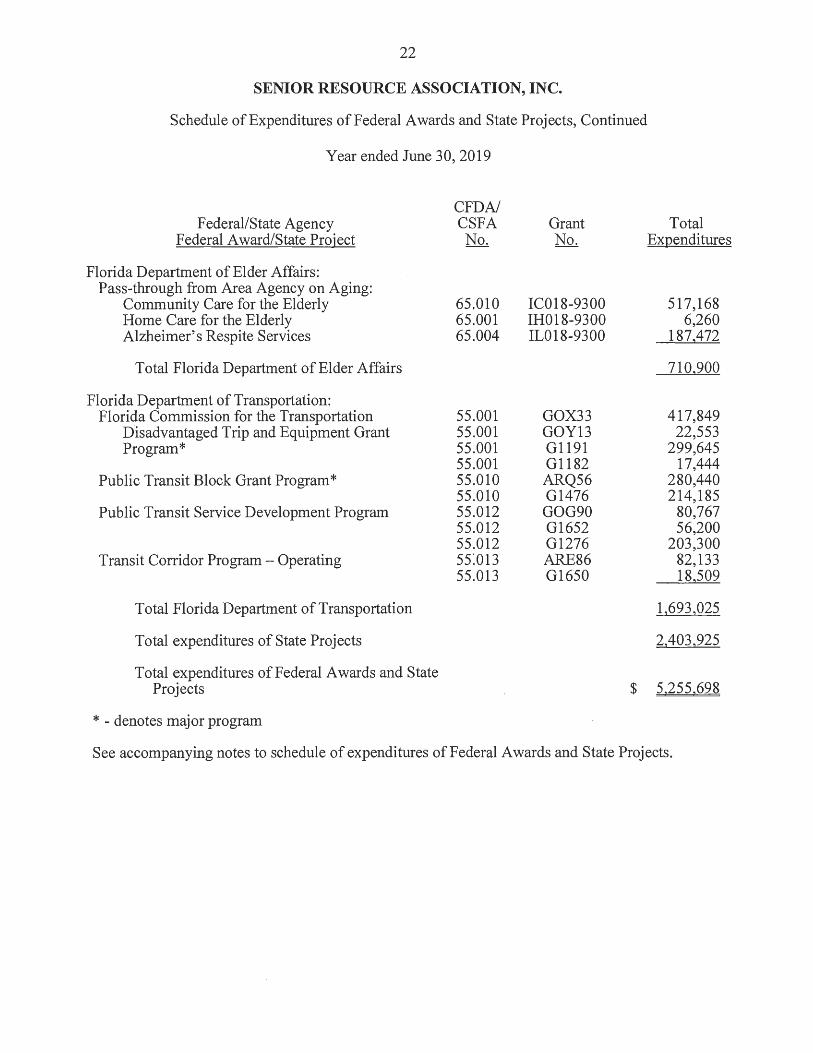

SENIOR RESOURCE ASSOCIATION, INC.

Schedule of Expenditures of Federal Awards and State Projects, Continued

Year ended June 30, 2019

CFDA/ Federal/State Agency CSFA Grant Total

Federal Award/State Project No. No. Expenditures

Florida Department of Elder Affairs: Pass-through from Area Agency on Aging:

Community Care for the Elderly 65.010 IC018-9300 517,168 Home Care for the Elderly 65.001 IH018-9300 6,260 Alzheimer's Respite Services 65.004 IL018-9300 187,472

Total Florida Department of Elder Affairs 710,900

Florida Department of Transportation: Florida Commission for the Transportation 55.001 GOX33 417,849

Disadvantaged Trip and Equipment Grant 55.001 GOY13 22,553 Program* 55.001 Gl 191 299,645

55.001 G1182 17,444 Public Transit Block Grant Program* 55.010 ARQ56 280,440

55.010 G1476 214,185 Public Transit Service Development Program 55.012 GOG90 80,767

55.012 G1652 56,200 55.012 G1276 203,300

Transit Corridor Program- Operating 55:013 ARE86 82,133 55.013 G1650 18,509

Total Florida Department of Transportation 1,693,025

Total expenditures of State Projects 2,403,925

Total expenditures of Federal Awards and State Projects $ 5.255.698

* - denotes major pro gram

See accompanying notes to schedule of expenditures of Federal Awards and State Projects.

23

SENIOR RESOURCE ASSOCIATION, INC.

Notes to Schedule of Expenditures of Federal Awards and State Projects

Year ended June 30, 2019

(1) Basis of Presentation

The accompanying schedule of expenditures of Federal Awards and State Projects (the Schedule) includes the federal and state grant activity of Senior Resource Association, Inc. and is presented on the accrual basis of accounting. The information in this Schedule is presented in accordance with the requirements of Title 2 U.S. Code of Federal Regulations Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and Chapter 10.650, Rules of the Auditor General of the State of Florida. Therefore, some amounts presented in this Schedule may differ from amounts presented in, or used in the preparation of, the basic financial statements.

(2) Summary of Significant Accounting Policies

Expenditures reported on the Schedule are reported on the accrual basis of accounting. Such expenditures are recognized following the cost principles contained in the Uniform Guidance, wherein certain types of expenditures are not allowable or are limited as to reimbursement. Negative amounts, if any, shown on the Schedule represent adjustments or credits made in the normal course of business to amounts reported as expenditures in prior years.

(3) Indirect Cost Rate

The Association has elected not to use the 10 percent de minimis indirect cost rate allowed under the Uniform Guidance.

(4) Matching Funds

The following matching expenditures during 2019 are not subject to Section 215.97 Florida Statutes:

Federal/State Agency Federal Award/State Project

Florida Department of Transportation: Elderly and Persons with Disabilities Capital Assistance

Program (Section 5310) Regional Mobility Management Facilitator Program

(Section 531 OM)

Total matching expenditures

(5) Contingency

Grant No.

YR42

G0891

$

Matching Expenditures

14,618

8,938

23.556

The Association has received federal and state grants fot specific purposes that are subject to audit by the grantor agencies. Entitlements to these resources are generally conditional upon compliance with the terms and conditions of grant agreements and applicable federal and state regulations, including the expenditure of resources for allowable purposes. Any disallowance resulting from a grantor audit may become a liability of the Association. In the opinion of management, all grant and contract expenditures are in compliance with the terms of the grants and contract agreements, applicable federal and state laws, and other applicable regulations.

24

SENIOR RESOURCE ASSOCIATION, INC.

Schedule of Findings and Questioned Costs

Year ended June 30, 2019

Section I - Summary of Auditors' Results

Financial Statements: Type of auditors' report issued

Internal control over financial reporting: Material weaknesses identified?

Significant deficiencies identified?

Noncompliance material to financial statements noted?

Federal A wards:

Unmodified

No

None reported

No

Identification of major federal awards - U.S. Department of Transportation, Federal Transit Capital and Operating Assistance - CFDA No. 20.507.

Internal control over major programs: Material weaknesses identified?

Significant deficiencies identified?

Type of auditors' report issued on compliance for major federal awards?

Any audit findings disclosed that are required to be reported in accordance with CFR 200.516(a)?

Dollar threshold used to distinguish between Type A and Type B Awards

Auditee qualified as low-risk auditee?

State Projects:

No

None reported

Unmodified

No

$ 750.000

Yes

Identification of major state projects - Florida Department of Transportation, Public Transit Block Grant Program - CSFA No. 55.010; Florida Department of Transportation, Florida Commission for the Transportation Disadvantaged Trip and Equipment Grant Program -CSFA No. 55.001.

Internal control over major programs: Material weaknesses identified? No

Significant deficiencies identified? None reported

Type of auditors' report issued on compliance for major state projects? Unmodified Any audit findings disclosed that are required to be reported in accordance

with Chapter 10.650, Rules of the Auditor General of the State of Florida? No

Dollar threshold used to distinguish between Type A and Type B Awards $ 721.178

(Continued)

25

SENIOR RESOURCE ASSOCIATION, INC.

Schedule of Findings and Questioned Costs, Continued

Year ended June 30, 2019

Section II - Financial Statement Findings

There were no findings related to the financial statements which are required to be reported in accordance with Government Auditing Standards.

Section III - Federal Awards Findings and Questioned Costs

There were no findings related to the state projects which are required to be reported in accordance with CFR 200.516(a).

Section IV - State Projects Findings and Questioned Costs

There were no findings related to the state projects which are required to be reported in accordance with Chapter 10.650, Rules of the Auditor General of the State of Florida.

Section V - Summary of Prior Year Audit Findings Relating to State Projects

There were no prior year audit findings related to the state projects which are required to be reported in accordance with Chapter 10.650, Rules of the Auditor General of the State of Florida.

Section VI - Management Letter Relating to State Projects

NIA - There were no matters relating to State Projects that were required to be reported in a management letter.