Embed Size (px)

Citation preview

Senior Housing Properties Trust REITWeek 2017: NAREIT's Investor Forum® June 2017

11 Fan Pier Boulevard & 50 Northern Avenue, Boston, MA. Biotech Medical Office Buildings. Primary Tenant: Vertex Pharmaceuticals.

Senior Housing Properties Trust

Disclaimer THIS PRESENTATION CONTAINS FORWARD LOOKING STATEMENTS WITHIN THE MEANING OF

THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 AND OTHER SECURITIES LAWS.

ALSO, WHENEVER WE USE WORDS SUCH AS "BELIEVE," "EXPECT," "ANTICIPATE," "INTEND,"

"PLAN," "ESTIMATE," "WILL,” “MAY” AND NEGATIVES OR DERIVATIVES OF THESE OR SIMILAR

EXPRESSIONS, WE ARE MAKING FORWARD LOOKING STATEMENTS. THESE FORWARD

LOOKING STATEMENTS ARE BASED UPON OUR PRESENT INTENT, BELIEFS OR EXPECTATIONS.

FORWARD LOOKING STATEMENTS ARE NOT GUARANTEED TO OCCUR AND MAY NOT OCCUR.

ACTUAL RESULTS MAY DIFFER MATERIALLY FROM THOSE CONTAINED IN OR IMPLIED BY OUR

FORWARD LOOKING STATEMENTS AS A RESULT OF VARIOUS FACTORS. YOU SHOULD NOT

PLACE UNDUE RELIANCE UPON ANY FORWARD LOOKING STATEMENT. EXCEPT AS REQUIRED

BY APPLICABLE LAW, WE UNDERTAKE NO OBLIGATION TO UPDATE OR REVISE ANY FORWARD

LOOKING STATEMENT AS A RESULT OF NEW INFORMATION, FUTURE EVENTS OR OTHERWISE.

2 Note: Unless otherwise stated, data in this presentation is as of March 31, 2017.

Senior Housing Properties Trust

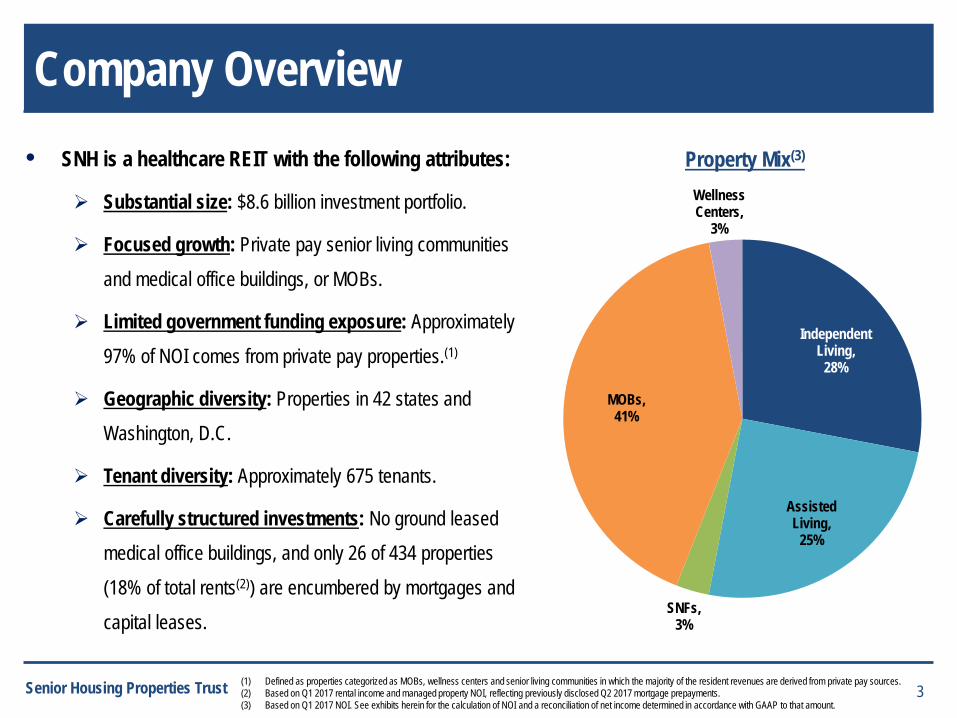

Company Overview

• SNH is a healthcare REIT with the following attributes:

Substantial size: $8.6 billion investment portfolio.

Focused growth: Private pay senior living communities and medical office buildings, or MOBs.

Limited government funding exposure: Approximately 97% of NOI comes from private pay properties.(1)

Geographic diversity: Properties in 42 states and Washington, D.C.

Tenant diversity: Approximately 675 tenants.

Carefully structured investments: No ground leased medical office buildings, and only 26 of 434 properties (18% of total rents(2)) are encumbered by mortgages and capital leases.

3 (1) Defined as properties categorized as MOBs, wellness centers and senior living communities in which the majority of the resident revenues are derived from private pay sources. (2) Based on Q1 2017 rental income and managed property NOI, reflecting previously disclosed Q2 2017 mortgage prepayments. (3) Based on Q1 2017 NOI. See exhibits herein for the calculation of NOI and a reconciliation of net income determined in accordance with GAAP to that amount.

Independent Living,

28%

Assisted Living,

25%

SNFs, 3%

MOBs, 41%

Wellness Centers,

3%

Property Mix(3)

Senior Housing Properties Trust

Why Invest in SNH? • High quality portfolio.

Predominantly private pay assets with limited exposure to government reimbursement.

Diversification across geography, tenant and asset mix.

Actively maintain a high quality portfolio through regular investment and active asset management.

• Healthcare supply and demand fundamentals are positive and growing.

Long term demand for senior housing exceeds supply.

10,000 Baby Boomers turning 65 every day.(1)

• Secure dividend payment.

Current annualized dividend of $1.56 per share.

Secure normalized FFO payout ratio of 83% for the trailing twelve months.

• Conservative financial approach.

Financial flexibility with a strong balance sheet.

Investment grade ratings by Moody’s (Baa3) and S&P (BBB-).

4 (1) Source: U.S. Census Bureau.

Senior Housing Properties Trust

Geographic Diversification

5

$8.6 billion invested in 434 properties located in 42 states and Washington, D.C.

Property Type No. of Properties % of NOI(2)

Independent living 68 28.5%

Assisted living 197 24.8%

Skilled nursing facilities 39 2.6%

Medical office buildings 120 41.3%

Wellness centers 10 2.8%

Total 434 100%

Note: Blue colored states represent states where SNH owns properties. (1) Based on 3/31/17 gross book value of real estate assets. Gross book value of real estate assets is real estate properties at cost, before depreciation and purchase price

allocations, less impairment writedowns, if any. (2) Based on Q1 2017 NOI. See exhibits herein for the calculation of NOI and a reconciliation of net income determined in accordance with GAAP to that amount.

MA 14% CA 10%

FL 10%

TX 7%

GA 5%

MD 4%

WI 4%

NC 3% VA 3% NY 3%

32 Other States + D.C. 37%

Geographic Diversification(1)

Senior Housing Properties Trust

Boston Seaport Joint Venture

6

In March 2017, SNH formed its first ever joint venture by selling a minority interest in two life-science MOB’s in Boston’s Seaport District to a sovereign institutional investor.

Structure: Joint Venture partner contributed $261 million for a 45% equity interest. Investment amount is based on a valuation of $1.2 billion, less $620 million of secured debt.

Highlights: Transaction reduced SNH’s concentration in the property and improved the balance sheet by reducing overall leverage and increasing liquidity.

Property Snapshot: Location: 11 Fan Pier & 50 Northern Avenue, Boston, MA Description: Two 15 story, Class A LEED® Gold Certified, life-science MOB’s Rentable Square Feet: 1.13 million Price Per Square Foot: $1,059 Major Tenant: Vertex Pharmaceuticals (Nasdaq: VRTX)

SNH will continue to consolidate the assets in the financial statements.

SNH will receive a credit from the joint venture partner for their portion of the business management fee.

Senior Housing Properties Trust

86%

87%

88%

89%

90%

91%

92%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Occu

panc

y

Units

Senior Housing Supply-Demand Trends (2)

Inventory Growth Absorption Occupancy

Senior Living Industry Dynamics

7

New supply mitigated by record absorption due to aging population and overall penetration rates.

The age 85 plus population is growing at a much faster rate than the rest of the population.(1)

(1) Source: U.S. Census Bureau, “2014 National Population Projections”. (2) Source: National Investment Center for the Seniors Housing and Care Industry (NIC), as of December 31, 2016.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0

2

4

6

8

10

12

14

16

18

20

2015 2019 2023 2027 2031 2035 2039 2043 2047

Millio

ns

Age 85 + Population (1)

85+ Population Growth Rate (%)

Senior Housing Properties Trust

Senior Living Portfolio

8

• 304 properties with 35,018 units located in 39 states. • Premier operators: Five Star Senior Living, Brookdale Senior Living,

Sunrise Senior Living, and 11 private senior living operators. • Weighted average rent coverage of 1.30x. • Weighted average occupancy of 85.5%.

The Stratford. Carmel, IN. 213 Units.

Note: Coverage ratio and occupancy are for the twelve months ended December 31, 2016.

Park Summit. Coral Springs, FL. 281 Units.

Remington Club. San Diego, CA.

405 Units.

Court at Palm Aire. Pompano Beach, FL. 295 Units.

The Jefferson. Arlington, VA. 422 Units.

The Gables. Winchester, MA. 125 Units.

Senior Housing Properties Trust

Senior Living Portfolio

9

Operator Unit Mix Number of Communities(1) Units(1) Occupancy(2) Rental

Coverage(2)

Five Star Senior Living IL, AL, ALZ, SNF 185 20,187 83.6% 1.19x

Sunrise Senior Living IL, AL, ALZ, SNF 4 1,619 91.8% 2.05x

Brookdale Senior Living AL, ALZ 18 894 84.5% 2.59x

11 Private Operators IL, AL, SNF 29 3,520 90.1% 1.28x

Managed Senior Living IL, AL, ALZ, SNF 68 8,798 87.2% N/A

Total Senior Living 304 35,018 85.5% 1.30x

(1) Number of communities and units are as of March 31, 2017. (2) Operator occupancy and rental coverage are presented for the twelve month period ended December 31, 2016. Rental Coverage is calculated as operating cash

flow from our tenants’ operations of properties, before subordinated charges, divided by rents payable to us.

Senior Housing Properties Trust

Medical Office Industry Dynamics

10

$0

$1,000

$2,000

$3,000

$4,000

$5,000

2007 2011 2015 2019 2023

National Health Expenditures ($ in billions)

Approximately 10,000 people are turning 65 each day.(1)

18.7 21.3 26.6 31.8 35.7 37.9 13.0 12.9

13.4 15.6

19.8 23.9

5.1 6.1 6.8

7.3 8.0

9.6 12.4% 13.0%

14.5% 16.3%

18.2% 19.7%

0%

5%

10%

15%

20%

25%

0102030405060708090

100

2005 2010 2015 2020 2025 2030

65+ Population Growth

65-75 75-85 85+ 65+ % of population

65+ A

ge g

roup

pop

ulat

ion (

milli

ons)

65+ Age group % of total population (U.S.)

In 2010, the number of seniors in the U.S. totaled 40 million, representing 13% of the population. By 2030, the number is expected to reach 71 million, or 19.7% of the population.(3)

National Healthcare Expenditures are expected to grow rapidly over the next decade.(2)

(1) Source: U.S. Census Bureau. (2) Source: www.cms.gov. (3) American Seniors Housing Association.

Senior Housing Properties Trust

High Quality MOB Portfolio • 11.6 million square feet in 120 properties located in 28 states and Washington, D.C. • Over 650 tenants. • Occupancy of 96.4% at March 31, 2017.

11

Durham, NC. Tenant: Duke University Health System.

Square feet: 126,225.

Concord, MA. Tenant: Harvard Vanguard.

Square feet: 49,250.

Los Angeles, CA. Tenant: Cedars-Sinai Medical Center. Square feet: 330,892.

Sheboygan, WI. Tenant: Aurora Healthcare, Inc. Square feet: 154,423.

Irving, TX. Tenant: Hospital Corporation of America.

Square feet: 94,137.

San Diego, CA. Tenant: The Scripps Research Institute. Square feet: 164,091.

Senior Housing Properties Trust 12

Largest MOB Tenants ($ in ‘000s) Square Feet Annualized Rental Income(1) %(1) Lease Expiration Vertex Pharmaceuticals, Inc.(2) 1,082,000 $90,215 11.8% 2028 Aurora Health Care, Inc. 643,000 $16,896 2.2% 2024 Cedars-Sinai Medical Center 137,000 $13,479 1.8% 2017 – 2025 The Scripps Research Institute 164,000 $10,177 1.3% 2019 Medtronic, Inc. 460,000 $8,217 1.1% 2017 – 2020 HCA Holdings, Inc. 254,000 $8,091 1.1% 2018 – 2025 Reliant Medical Group, Inc. 362,000 $7,595 1.0% 2019 Nanotherapeutics, Inc. 166,000 $7,384 1.0% 2031

The MOB weighted average remaining lease term (by annualized rental income) is 7.2 years.

Medical Office Building Portfolio

7% 7% 11% 9%

5% 5% 3%

10%

3%

40%

0%

15%

30%

45%

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026+

MOB Annualized Rental Income Expiring

(1) Annualized rental income is rents pursuant to existing leases as of March 31, 2017. Annualized rental income includes straight line rent adjustments and estimated recurring expense reimbursements for certain net and modified gross leases; excludes lease value amortization at certain of the MOBs.

(2) The property leased by this tenant is owned by a joint venture, in which we own a 55% equity interest. Rental income presented includes 100% of rental income as reported under GAAP.

Senior Housing Properties Trust

38%

11%

51% Life Science

• Laboratory and research space.

MOB Segment

13

Patient Care • Clinics, outpatient centers, and

doctor’s offices.

Other Medical Related • Medical equipment manufacturing. • Other medical related tenants.

Medical Office

Buildings

Senior Housing Properties Trust

Investment Grade Rated Balance Sheet

14

Market Value of Common Shares

58%

Unsecured Senior Notes

21%

Mortgage Debt 13%

Unsecured Term Loans

7% Unsecured Revolving

Credit Facility 1%

Total Market Capitalization(1)

Unsecured senior notes: • $1.75 billion of senior notes due in 2019, 2020, 2021, 2024, 2042 and 2046.

Mortgage debt & capital leases:(1)

• $1.1 billion secured by 45 properties (90% of properties are unencumbered).

Unsecured term loans: • $350 million non-revolving term loan.

Matures in January 2020.

• $200 million non-revolving term loan.

Matures in September 2022.

Unsecured credit facility: • $1 billion revolving credit facility.

$97 million outstanding as of March 31, 2017. LIBOR plus 130 basis points.

Matures in January 2018, with option to extend to 2019.

(1) As of March 31, 2017.

Senior Housing Properties Trust

40.5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Total Debt as a % of Gross Assets

SNH SNL US REIT Healthcare Index

Conservative Financial Profile

15

$-

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

Debt Maturity Schedule(2)

Unsecured Floating Unsecured Fixed Secured Fixed

($ in millions)

(1) Source for the Healthcare Index is SNL Financial; data is actual as of the most recent quarter reported. (2) As of March 31, 2017.

No derivatives, no off balance sheet liabilities and no material adverse change clauses or ratings triggers.

(1)

Senior Housing Properties Trust

Normalized FFO payout ratio of 83% for the trailing 12 months Q1 2017.

History of Providing Returns to Investors

16 (1) Excludes 13.2¢/share of RMR stock distributed in Q4 2015. (2) Source: SNL Financial, based on period from 3/31/2002 to 3/31/2017.

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%Total Return(2)

SNH SNL U.S. REIT Equity

$1.23

$1.24

$1.25

$1.28

$1.30

$1.38

$1.40

$1.42

$1.45

$1.49

$1.53

$1.56

$1.56

$1.56

$1.56

$1.56

78%

80%

82%

84%

86%

88%

90%

92%

94%

$1.15

$1.20

$1.25

$1.30

$1.35

$1.40

$1.45

$1.50

$1.55

$1.60Dividends Paid Per Share(1)

Annual Dividends Paid Normalized FFO Payout Ratio

334% total return over 15 years.

Senior Housing Properties Trust

Preferred Portfolio Composition

17 Source: Company filings and presentations. SNH, HCP, VTR, and HCN shown as a percentage of NOI. OHI shown as a percentage of revenue.

Portfolio Comparison of Five Largest Healthcare REITs

38%

12%

28% 26% 28%

15%

19% 31%

42% 3%

71%

4%

13%

6%

13%

41% 40%

25% 17%

3%

17% 7%

1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

SNH OHI HCP VTR HCN

Senior Housing - NNN Senior Housing - Managed Skilled Nursing Hospitals MOBs / Life Science Other

Senior Housing Properties Trust

Healthcare REIT Peer Comparison

18 Source: SNL Financial.

Senior Housing Properties Trust

Management Structure

19

SNH obtains high quality and cost-effective management services from The RMR Group for its real estate operating platform. RMR is an alternative asset management company with $27.6 billion of assets under management, including more than 1,400 real estate properties. The RMR managed companies combined have approximately $11 billion of annual revenues and approximately 53,000 employees.

Financial Services: Real Estate Services: Business Services:

Accounting Acquisitions / Dispositions Administration

Capital Markets Asset Management Human Resources

Compliance / Audit Construction Information Technology (IT)

Finance Engineering Investor Relations

Financial Planning Leasing Legal

Tax Property Management Risk Management

RMR’s Operations Include: Healthcare REIT G&A Expense Comparison

(1)

(1) Source: SNL Financial

Senior Housing Properties Trust

Management Fees and Aligned Interests

20

Revised Fee Structure

Business Management Fee: Principally consists of an annual fee based on 50 bps multiplied by the lower of: (1) SNH’s historical cost of real estate, or (2) SNH’s total market capitalization.

Incentive Fee: Equal to 12% of value generated by SNH in excess of benchmark index total returns per share over a three year period, subject to a cap (1.5% of equity market cap).

Property Management Fee: Principally consists of an annual fee based on 3.0% of gross rents collected at SNH’s MOB properties.

In June 2015 SNH, along with three other managed public REITs, acquired approximately half of The RMR Group. Further Aligned Interests The historical owners of RMR have become owners of a significant number of restricted shares of SNH and those shares are

subject to 10 year lock up agreements.

SNH and its shareholders own RMR shares and share in future profits from new businesses of the external manager.

There is greater transparency for SNHs’ shareholders into RMR management, including compensation practices as well as financial and operating results.

Senior Housing Properties Trust

Business Plan

21

• Remain focused on investing internally and active asset management to maintain high quality properties leased to strong credit tenants.

Expand private pay senior living communities that contain a mix of independent living, assisted living and memory care.

Continue to reinvest at our medical office buildings to attract high quality tenants.

• Maintain a strong, investment grade rated financial profile.

Continue to grow Normalized FFO.

Continue to monitor debt market and repayment opportunities.

Continue to evaluate alternatives to optimize our weighted average cost of capital.

Exhibits

22

Senior Housing Properties Trust

Financial Summary

23 (1) See following pages for reconciliation to nearest GAAP measures.

2017 2016Rental income 166,443$ 161,421$ Residents fees and services (managed properties) 98,118 96,954 Total revenues 264,561$ 258,375$

Property net operating income (NOI)(1) 163,504$ 160,426$ NOI margin % 61.8% 62.1%

Adjusted EBITDA(1) 152,984$ 150,222$

Normalized funds from operations (FFO)(1) 108,432$ 110,330$

Per share data:Common dividend 0.39$ 0.39$ Normalized FFO 0.46$ 0.46$ Normalized FFO payout ratio 84.8% 84.8%

For the three months endedMarch 31,($ in 000s, except per share data)

Senior Housing Properties Trust

Calculation and Reconciliation of Net Operating Income (NOI) and Cash Basis NOI(1)

24

($ in 000s)

(1) See slide 27 for a definition of NOI and Cash Basis NOI, a description of why we believe they are appropriate supplemental measures and a description of how we use these measures.

(2) We recorded a liability for the amount by which the estimated fair value for accounting purposes exceeded the price we paid for our investment in RMR common stock in June 2015. A portion of this liability is being amortized on a straight line basis through December 31, 2035 as a reduction to property management fees, which are included in property operating expenses.

Senior Housing Properties Trust

Calculation and Reconciliation of EBITDA and Adjusted EBITDA(1)

25

(1) See slide 27 for a definition of EBITDA and Adjusted EBITDA and a description of why we believe they are appropriate supplemental measures. (2) Amounts represent equity compensation awarded to our trustees, officers and certain other employees of The RMR Group LLC. (3) Incentive fees under our business management agreement are payable after the end of each calendar year, are calculated based on common share total return, as defined, and are included in general and administrative

expense in our condensed consolidated statements of income. In calculating net income in accordance with GAAP, we recognize estimated business management incentive fee expense, if any, in the first, second and third quarters. Although we recognize this expense, if any, in the first, second and third quarters for purposes of calculating net income, we do not include these amounts in the calculation of Adjusted EBITDA until the fourth quarter, when the amount of the business management incentive fee expense for the calendar year, if any, is determined.

($ in 000’s)

Senior Housing Properties Trust

Calculation and Reconciliation of Funds From Operations (FFO) and Normalized FFO(1)

26

(1) See slide 27 for a definition of FFO and Normalized FFO, a description of why we believe they are appropriate supplemental measures and a description of how we use these measures. (2) Incentive fees under our business management agreement are payable after the end of each calendar year, are calculated based on common share total return, as defined, and are included in general and administrative expense

in our condensed consolidated statements of income. In calculating net income attributable to common shareholders in accordance with GAAP, we recognize estimated business management incentive fee expense, if any, in the first, second and third quarters. Although we recognize this expense, if any, in the first, second and third quarters for purposes of calculating net income attributable to common shareholders, we do not include these amounts in the calculation of Normalized FFO until the fourth quarter, when the amount of business management incentive fee expense for the calendar year, if any, is determined.

($ in 000’s)

Senior Housing Properties Trust

Definitions of Certain Non-GAAP Financial Measures

27

NOI and Cash Basis NOI The calculations of NOI and Cash Basis NOI exclude certain components of net income in order to provide results that are more closely related to our property level results of operations. We calculate NOI and Cash Basis NOI as shown on page 24. We define NOI as income from our real estate less our property operating expenses. NOI excludes amortization of capitalized tenant improvement costs and leasing commissions because we record those amounts as depreciation and amortization. We define Cash Basis NOI as NOI excluding noncash straight line rent adjustments, lease value amortization, lease termination fee amortization, if any, and non-cash amortization included in property operating expenses. We consider NOI and Cash Basis NOI to be appropriate supplemental measures to net income because they may help both investors and management to understand the operations of our properties. We use NOI and Cash Basis NOI internally to evaluate individual and company wide property level performance, and we believe that NOI and Cash Basis NOI provide useful information to investors regarding our results of operations because these measures reflect only those income and expense items that are generated and incurred at the property level and may facilitate comparisons of our operating performance between periods and with other REITs. NOI and Cash Basis NOI do not represent cash generated by operating activities in accordance with GAAP and should not be considered as an alternative to net income or operating income as an indicator of our operating performance or as a measure of our liquidity. These measures should be considered in conjunction with net income and operating income as presented in our Condensed Consolidated Statements of Income. Other REITs and real estate companies may calculate NOI and Cash Basis NOI differently than we do.

EBITDA and Adjusted EBITDA We calculate EBITDA and Adjusted EBITDA as shown on page 25. We consider EBITDA and Adjusted EBITDA to be appropriate supplemental measures of our operating performance, along with net income, net income attributable to common shareholders and operating income. We believe that EBITDA and Adjusted EBITDA provide useful information to investors because by excluding the effects of certain historical amounts, such as interest, depreciation and amortization expense, EBITDA and Adjusted EBITDA may facilitate a comparison of current operating performance with our past operating performance. EBITDA and Adjusted EBITDA do not represent cash generated by operating activities in accordance with GAAP and should not be considered an alternative to net income or operating income as an indicator of operating performance or as a measure of our liquidity. These measures should be considered in conjunction with net income and operating income as presented in our Condensed Consolidated Statements of Income. Other REITs and real estate companies may calculate EBITDA and Adjusted EBITDA differently than we do.

FFO and Normalized FFO

We calculate FFO and Normalized FFO as shown on page 26. FFO is calculated on the basis defined by the National Association of Real Estate Investment Trusts, or NAREIT, which is net income attributable to common shareholders, calculated in accordance with GAAP, excluding any gain or loss on sale of properties and impairment of real estate assets, plus real estate depreciation and amortization and the difference between net income attributable to common shareholders and FFO attributable to noncontrolling interest, as well as certain other adjustments currently not applicable to us. Our calculation of Normalized FFO differs from NAREIT's definition of FFO because we include business management incentive fees, if any, only in the fourth quarter versus the quarter when they are recognized as expense in accordance with GAAP due to their quarterly volatility not necessarily being indicative of our core operating performance and the uncertainty as to whether any such business management incentive fees will be payable when all contingencies for determining such fees are determined at the end of the calendar year, and we exclude acquisition and certain other transaction related costs such as legal and professional fees associated with our acquisition and disposition activities, gains and losses on early extinguishment of debt, if any, and Normalized FFO from noncontrolling interest, net of FFO, if any. We consider FFO and Normalized FFO to be appropriate supplemental measures of operating performance for a REIT, along with net income attributable to common shareholders and operating income. We believe that FFO and Normalized FFO provide useful information to investors because by excluding the effects of certain historical amounts, such as depreciation and amortization expense, FFO and Normalized FFO may facilitate a comparison of our operating performance between periods and with other REITs. FFO and Normalized FFO are among the factors considered by our Board of Trustees when determining the amount of distributions to our shareholders. Other factors include, but are not limited to, requirements to maintain our qualification for taxation as a REIT, limitations in our revolving credit facility and term loan agreements and our public debt covenants, the availability to us of debt and equity capital, our expectation of our future capital requirements and operating performance and our expected needs and availability of cash to pay our obligations. FFO and Normalized FFO do not represent cash generated by operating activities in accordance with GAAP and should not be considered as alternatives to net income, net income attributable to common shareholders or operating income as an indicator of our operating performance or as a measure of our liquidity. These measures should be considered in conjunction with net income, net income attributable to common shareholders and operating income as presented in our Condensed Consolidated Statements of Income. Other REITs and real estate companies may calculate FFO and Normalized FFO differently than we do.

Senior Housing Properties Trust REITWeek 2017: NAREIT's Investor Forum® June 2017

11 Fan Pier Boulevard & 50 Northern Avenue, Boston, MA. Biotech Medical Office Buildings. Primary Tenant: Vertex Pharmaceuticals.