Embed Size (px)

Citation preview

Performance creates trust

CFO Martin Sieg Castagnola

London, 23 May 2014

Sell-Side Analysts’ Breakfast

Caution regarding forward-looking statements

This document may contain projections or other forward-looking statements

related to the Vontobel Group that are subject to known and unknown risks,

uncertainties and other important factors. These projections and forward-

looking statements reflect management’s current views and estimates. They

involve certain risks and uncertainties that could cause actual results to

differ materially from those contained in the projections and forward-

looking statements. Potential risks and uncertainties include factors such as

general economic conditions, foreign exchange, share price and interest rate

fluctuations as well as legal and regulatory developments.

Slide 2

Looking at the past….to understand the future

Slide 3

A consistent, improving and solid business case…

CHF mns

� Solidity, reliability and respect of all stakeholders are fundamental to us

� No single year without profit through the entire financial crisis

0

200

400

600

800

1000

Total operating income Operating expenses

102 81183 256 264

113 139 148 114 124 122

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Slide 4

Group

net

profit

1.10 1.20

1.602.00 2.00

1.20

1.40 1.40

1.10

1.20 1.30

3.9%

4.5%

4.0% 3.8% 3.7%

5.5%

4.7%

3.9%

5.2%

4.3%

3.5%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

DPS (in CHF) Dividend yield in %

…underpinned by sustainable dividend yield of over 4%

� Since 2003 dividend yield has been below the financial sector average only in the absolute boom years

� Consistent long-term dividend policy / high payout ratio

Avg. 10Y

Dividend yield

4.2%

Payout ratio 64% 89% 56% 50% 48% 67% 61%65% 62% 62% 68%Payout ratio

mostly

over 50%

Slide 5

The most

senior

person of the current

management team started

in October

2002; average

seniority of members is

of over 6

years

ROE is strong, but it is an ‘R on a lot of E’

� Base case remains very solid, ROE adjusted for current excess capital position some 3pp higher

� We deliberately mantain our excess capital position

939

1'0771'199

1'287

1'421

1'370

1'484 1'504

1'448

1'5521'626

11.4

8.5

16.2

21.619.2

8.1

9.7 9.8

7.5

8.4 8.9

0

5

10

15

20

25

30

35

40

0

200

400

600

800

1000

1200

1400

1600

1800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Shareholders’ equity

(in CHF mns)

ROE in %

Slide 6

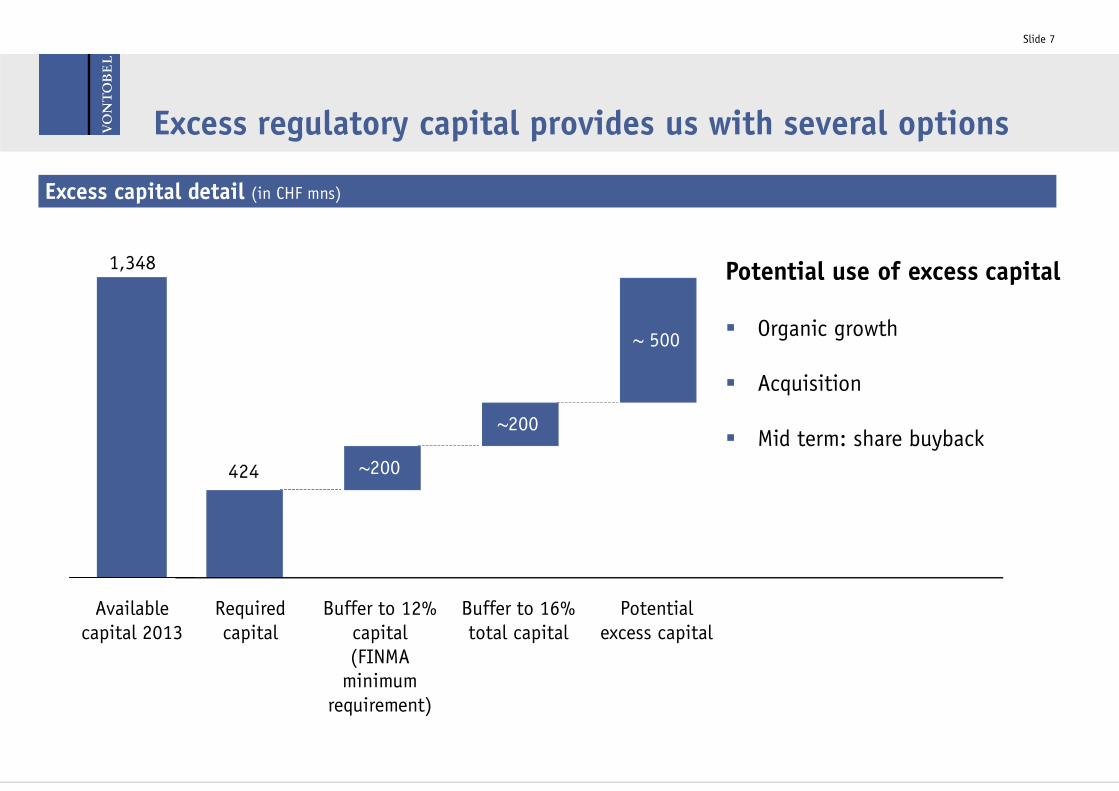

Excess regulatory capital provides us with several options

Excess capital detail (in CHF mns)

~ 500

~200

Buffer to 16%

total capital

Buffer to 12%

capital

(FINMA minimum

requirement)

Potential

excess capital

Required

capital

~200

Available

capital 2013

1,348

Slide 7

Potential use of excess capital

� Organic growth

� Acquisition

� Mid term: share buyback

Stronger capital base, controlled risks and top discipline

939

2013

1,497

2010

1,504

2009

1,626

2011

1,552

2008

1,484

2012

1,199

2006

6,281

2003

1,287

4,948

4,186

1,099

5,292

2004 2005

1,421

2007

1,370

4,969

5,895 5,6905,019

5,294

2,4522,972

Total risk weighted positions (CHF mns)

Total equity (CHF mns)

CAGR: 5.6%

CAGR: 8.0%

Regulatory changes

continuing to demand

more capital for lower effective exposure

It is a key concern for

us to have enough

capital to cope with this additional capital

burden and to not

bother shareholders

with tedious capital

increases

� Leverage ratio under FINMA rules not defined yet

� Basel II and Basel III increased our capital requirements

� Uncertainity in market prevails

Slide 8

Looking at the present to understand the future

Slide 9

Strong business fundamentals –total client assets increase by average 11% per year…

16%

10%

8%

2013201220112010200920082007200620052004

CAGR 11%

2003

AuM non-discretionary

AuM discretionaryCustody assets

Structured products outstanding

Total client assets (in CHF bns)

10Y CAGR

Slide 10

2%

…leading to consistent earnings pattern

6136 46

2014 2013

122

76

2012

124

63

2011

114

78 <761H

2H

Group reported net profit (in CHF mns)

23.3% 27.2% 25.5%

Slide 11

BIS tier

1 ratio

Brand value and reputation increased sharply during the crisis

Slide 12

in CHF mns

� Interbrand and Bilanz regularly assess the brand value of companies

� The brand value has doubled up since 2009, but the market multiples barely reflect this

� Vontobel is in a strong position to further build up trust and reputation

� New hiring is the best proof of increased trust and reputation

1 Brand value of 2009

Our most important message of this morning to you

Shareholders are our focus - we are driven by total return to shareholders

Slide 13

Vontobel: 10% Banking Sector: 2%1

TSR, annualized as from 1/10/2002 to end 2013

1 DJ EURO STOXX Banks Index

Contact Details

Fabrizio Croce, Head Investor Relations

Slide 14

Susanne Borer, Deputy Head Investor Relations

Vontobel Gotthardstrasse 43

CH-8022 Zürich +41 (0)58 283 7329

Vontobel Gotthardstrasse 43

CH-8022 Zürich +41 (0)58 283 5126

The Vontobel Group

Slide 15