Embed Size (px)

Citation preview

William D. Coleman

Abstract: This article examines an important sector of the economy, securities dealing, and shows how it has come to be governed by a mix of state supervision and private interest government. An interest association has achieved a unique “public status” and has assumed responsibility for implementing policy and disciplining member firms. The development of self-regulatory modes of governance through private interest governments, the article suggests, is more likely in highly concentrat- ed sectors that offer specialized, technical services rather than those that manufac- ture goods. The argument is developed through a case study of the Investment Dealers Association of Canada and its role in the securities industry. Using a typology of policy networks, the article traces the historical path from an informal, primitive system of self-regulation, Tequiring little attention from government, to a highly formalized system, jointly managed by complex state and industry organizations.

Self-regulation in the Canadian securities industry : A study of the Investment Dealers Association of Canada

Sommaire: Cet article examine un secteur important de I’economie, le commerce des valeurs mobilieres, et decrit comment il en est arrive a Ctre regi par un melange de controle Ctatique et de gestion par des inter& prives. Un groupe d’interet a en effet obtenu un “caracthe public” assez particulier et s’est vu octroyer la respon- sabilite de mettre en place une politique et de contrbler ses societes menibres. Selon cet article, I’autoreglementation par des groupes d’interCt prive a plus de chances de se developper dans des secteurs A haute concentration offrant des services specialises et techniques plutBt que dans le secteur des produits manufactures. Ce point de vue s’appuie sur une etude de cas concernant I’Association canadienne des courtiers en valeurs mobilieres et son rBle dans ce secteur. En utilisant une typologie des reseaux politiques, I’article retrace I’evolution historique de cette industrie depuis un systeme informel et peu develop@ d’autoreglementation, exigeant peu d’attention du gouverne- ment, jusqu’i un systtrne extremement structure, gere conjointement par Ilktat et I’industrie elle-meme.

Until recently, market and financial intermediation were segregated in Canada. Financial intermediaries like the chartered banks received money for deposit that, in turn, was lent t o third parties for personal or business

Research for this article was supported by the Social Sciences and Humanities Research Council of Canada, Research Grant, 410-88-0629. T h e author woiild like to thank the anonymous referees for the comments and A.G. Kniewasser. president, and his staff at the I D A for their co-operation in this research.

CANADIAN PUBLIC ADMINISTRATION / ADMINISTRATION PUBLIQUE DU CANADA VOLUME 32, NO. 4 (WINTEWHIVER), PP. 503-523.

WILLIAM D. COLEMAN

purposes. Market intermediaries, often called investment bankers or investment dealers, accepted monies “for the purchase of the debt or equity of another corporate entity.”’ Investment dealers facilitate direct financing, the immediate transaction of business between borrower and lender. In primary markets, they design financial instruments that are attractive to users of capital and investors, and engineer their sale from users to investors. They participate in secondary markets by facilitating the sale of financial instruments between investors. The essential difference then between financial and market intermediaries is that in the latter, investors emerge with a direct investment in the business, government or other user of capital rather than a loan or a mortgage.* These intermediaries are used primarily by governments and large corporations who seek to issue securities in- cluding stocks, bonds, short-term money market instruments, and a host of new financial innovations.’

This capital markets-based system for industrial financing has faced a series of important changes over the past two decade^.^ The development of international wholesale banking and a movement by governments and large corporations away from debt financing to securities are the most important of these, and they in turn have been facilitated by advances in communica- tions technology. These kinds of changes have had somewhat contradictory consequences for policy. In countries such as Canada, Japan, and the United States where the state used regulations to reserve market intermediation functions for investment dealers, globalization has forced a change in this policy, leading to the breakdown of barriers between investment dealers and other financial institutions. Nonetheless, the intensified competition that forced these changes has also fostered increased risk-taking by financial firms leading, in turn, to a rise in the number of failures. Governments have responded by re-examining their supervisory procedures and the adequacy of their regulatory agencies. In short, deregulation in the marketplace has been accompanied by renewed attempts by governments to design an adequate supervisory system for financial institutions, a system sufficiently adept at detecting solvency problems and fraud that consumers can be adequately protected.

1 Ontario Task Force on Financial Institutions (OTFFI), FinulReport (Toronto: Government of Ontario, 1985), p. 9. 2 Securities Industry Capital Markets Committee (SICMC), “Submission to the Standing Committee on Finance, Trade and Economic Affairs,” August 9, 1985, pp. 2-3. 3 Canada, Department of Finance, The Regulation of Canadian Financial Institutions: Proposals for Dimusion (Ottawa: Supply and Services Canada, 1985), p. 5 1. 4 For an examination of the place of Canadian capital markets in the larger governance system for the financial sector in Canada, see Richard Schultz and Alan Alexandroff, Economic Regulotion ond the Federal System, Royal Commission on the Economic Union and Development Prospects for Canada, Vol. 42 (Toronto: University of Toronto Press, 1985), chapter 4, “Capital Markets, Regulation and Industrial Adjustment.”

504 CANADIAN PUBLIC ADMINISTRATION

CASE STUDY OF INVESTMENT DEALERS ASSOCIATION

One of the most striking facets of this re-regulation process as it has developed in the securities sector is the persistence of private self-regulatory organizations (SROS) at the core of the governance system. As capital markets have become larger, more complex, and more international, the system of self-regulation has evolved from one based on informality, moral suasion, and minimal state supervision, to one that rests on highly formalized legal procedures and an increased state role. Yet in Canada, the United States, and Britain, the state has remained reluctant to supplant completely private S R O S . ~ Consequently, the evolution in systems of self-regulation has witnes- sed the growth of policy networks where associations have moved to complement normal policy advocacy activities with formal participation in the policy process.6 In the course of this development, the policy network devoted to the regulation of securities markets has shifted in form from what Atkinson and Coleman term pressure pluralism, to clientele pluralism, and finally to concertation.’

A pressure pluralist policy network involves an exchange between competing, multiple, narrow, specialized groups and one or more state agencies where the groups act as policy advocates or lobbyists. By contrast, a clientele pluralist network refers to a situation where state officials lack autonomy from societal groups and an independent capacity to develop state policy. Consequently, they become dependent on interest associations to supply information and expertise and to ensure member compliance. In exchange, state actors offer them an opportunity to participate in the policy process. The group then becomes a kind of “private interest government”’ that is delegated authority to implement policy or to regulate its members. Finally, in a concertation network, a single association represents a sector and participates with a corresponding state agency in the formulation and implementation of policy. The state agency has considerable capacity in its own right, being autonomous and able to concentrate power for co- ordinated decision-making. Sectoral interests match the state’s strength by

5 For some analysis of the British and U.S. cases, see the following papers by Michael Moran: “An Outpost of Corporatism: the Franchise State on Wall Street,” Government andOpposition 22, no. 2 (1987): 206-23, and “Deregulating Britain, deregulating America: the case o f the securities industry,” paper presented to the ECPR workshop on Deregulation in Western Europe, University of Amsterdam, 10-15 April 1987. 6 The distinction between policy advocacy and policy partiripation is developed at length in W.D. Coleman, Business and Politics: A Study of Collective Action (Montreal: McGill-Queen’s University Press, 1988). chapter 3. 7 Michael M. Atkinson and William D. Coleman, “Strong States and Weak States: Sectoral Policy Networks in Advanced Capitalist Economies,” Bn’tirhJournal of Political Science 19, no. 1

8 W. Streeck and P.C. Schmitter, “Community, Market, State - and Associations? The Prospective Contribution of Interest Governance to Social Order,” in Streeck and Schrnitter, eds.. Private Interest Government: Bqrond Market and State (London: Sage, 1985). pp. 1-29.

(1989): 47-67.

505 ADMINISTRATION PUBLIQUE DU CANADA

WILLIAM D. COLEMAN

drawing on an inclusive, hierarchical associational system capable of engaging in longer-term policy deliberations while maintaining member support.

This article uses an historical case study of the Investment Dealers Association of Canada (IDA) to trace changes in policy networks by which the regulation of the over-the-counter securities markets in Canada has evolved from a very informal, primitive system requiring minimal attention by the government to a system that is highly formalized and jointly managed by complex state and industry organizations.

In making this argument, the article uses a four-stage model for the development of self-regulatory organizations. Drawing from the work of Boddewyn and Farago, the following four steps are distinguished.’

1. Selfdisczpline. Correct business conduct is the responsibility of the individual firm. Each firm is expected to ensure that its partners and employees act in an ethical fashion,

2. Pureself-regulation. Norms are developed, used, and enforced by industry organizations. The state may consult these organizations, whether stock exchanges or associations, from time to time on related policy issues.

3. Negotiated self-regulation. The industry voluntarily negotiates the develop- ment, use, and enforcement of norms with an outside agency, whether government or consumer. Industry organizations are formally incorpor- ated into the processes making relevant policy and become the instru- ments for disciplining firms.

4. Mandated self-regulation. An industry is ordered or designated by the government to develop, use, and enforce norms. Industry organiza- tions become formal, legally recognized, instruments for the implemen- tation of public policy.

Since 1929, regulation of the Canadian securities industry” has evolved from pure self-regulation through negotiated self-regulation introduced in 1937 and finally to a highly formalized mandated system that began to emerge in 1947. At each step, the state’s interest in the industry’s affairs increases; the industry takes this cue and increases its organizational capacity to respond to changes in state organization. Thus, in the course of the development of the self-regulatory system, the IDA has changed its organiza- tional form from that of a common pressure group to that of a “private

9 J.J. Boddewyn, “Advertising Self-regulation: Organization Structures in Belgium, Canada, France and the United Kingdom,” in Streeck and Schmitter, Private Inferest Government, p. 34; Peter Farago, Verbande als Trager oiffentlicher Politik (Griisch: Verlag Kiiegger, 1987), p. 20. 10 In subsequent discussions, we will be using the term “securities industry” to refer to the over-the-counter segment only for which IDAC has assumed responsibility. The corresponding SROS for listed securities are the stock exchanges.

506 CANADIAN PUBLIC ADMINISTRATION

CASE STUDY OF INVESTMENT DEALERS ASSOCIATION

interest government” acting first in a clientele pluralist network and ultimately in a concertation network. As such, the association shares in “the state’s authority to make and enforce binding decisions.”” After tracing this development process in the IDA, the article concludes with an analysis of the conditions that favoured the development of a private interest government sharing in policy implementation and design in this industry, emphasizing the relative isolation of securities trading from the general public, the difficulty in regulating a service as opposed to a good, and the overall philosophy of the state in Canada toward the delivery of financial services.

The Canadian securities industry Securities firms perform five different functions. First, they act as stock- brokers. In this function, they are agents, acting on behalf of buyers or sellers and do not own the securities. They charge a commission for performing a transaction. As brokers, they belong to one or more of four stock exchanges: Toronto (TSE), Montreal (MSE), Vancouver (VSE), or Alberta (ASE). The TSE is by far the dominant exchange in Canada.” Secondly, they provide advisory and investment management services. Thirdly, they act as dealers or principals in buying and then selling securities. These securities normally include Government of Canada, provincial, municipal, and corporate bonds and over-the-counter equities. Fourthly, they maintain an active secondary market for already-issued securities. And finally, they conduct money market operations, buying and selling short-term securities of maturities to a maximum of three years. Historically, separate firms acted as brokers and as dealers. However, in recent years these distinctions have become increasing- ly blurred with firms becoming larger and performing simultaneously all five of these functions.

Determining the actual size of the industry is a difficult task. In 1986 there were ninety-nine firms that were members of at least one of the IDA or the stock exchanges. Securities regulations vary in Canada from province to province and it is possible for a firm to be active in the business without belonging to a stock exchange or the IDA. The number of such firms depends on the specific provincial regulations but is normally quite small. l 3

The industry was long dominated by a restricted number of larger firms. Since the deregulation of 1987, the largest investment houses have all been

I I Streeck and Schmitter, “Community,” p. 20. 12 In 1985 the TSE accounted for 76.5 per cent o f the dollar value of transactions compared to 18.3 for Montreal, 4.7 for Vancouver, and 0.5 for Alberta. In terms of share volumes, the ‘ISE had 47.6 per cent compared to 39.8 for Montreal, 9.3 for Vancouver, and 3.3 for Alberta. Canadian Securities Institute (CSI). The Canadian Securities Course (Toronto: C S I , 1986), p. 238. 13 For example, in Ontario in 1977 there were 15 securities dealers or underwriters out of 1 10 who were not affiliated to the ’rsE or the IDA. J. Peter Williamson, “Canadian Financial Institutions,” in Canada, Department of Consumer and Corporate Affairs, Proposalr for a Securities Market Law for Canada, vol. 3 (Ottawa: Supply and Services Canada, 1979), p. 747.

507 ADMINISTRATION PUBLIQUE DU CANADA

WILLIAM D. COLEMAN

purchased by one of the big, Schedule A, chartered banks. In addition, foreign securities firms, notably from the United States and Japan, applied for and received permission to set up full operations in Canada. Both the new securities affiliates of the banks and the foreign firms have entered the Canadian self-regulatory system by purchasing seats on the stock exchanges and by taking out a membership in the IDA. The deregulation of financial and market intermediaries has been absorbed by a self-regulatory system that has itself become more formalized and subject to state supervision.

The evolution of self-regulation The acquisition of self-regulating powers occurs in a series of discrete steps. At each stage the government signals its intention to regulate the sector if the industry does not itself assume the responsibility. In each case the industry, fearing public bureaucratic regulation, responds to the state’s request. In doing so, an interest association is gradually transformed into a private interest government and assumes an increasingly prominent role in the policy process itself.

Self-discipline, 191 6-29 Boddewyn uses the term “self-discipline” to describe situations where responsibility for monitoring business conduct rests with the individual firm and not with associations or other S R O S . ’ ~ Such was the practice for the first sixteen years of associative action in the Canadian securities industry. The industry emerged as a distinct sector in the two decades prior to the First World War.I5 By 191 1 sufficient firms were active to give rise to an interest in establishing some common procedures for the conduct of the industry. Discussions among the various firms in the Toronto area led to the creation of a Bond Dealers section within the Board of Trade of the City of Toronto in 1913.16 Movement toward creating a nation-wide association was sparked by the First World War. The minister of finance offered his first and second war loans in 1915 and 1916 without consulting directly with the bond dealers. When the results came in from the second loan, it was discovered

14 Boddewyn, “Advertising Self-regulation,” p. 34. 15 See Ian W. Drummond, Progreu Without Planning: The Economic Histo? of Ontariofrom Confcdeation to the Second World War (Toronto: University o f Toronto Press, 1987), chapter 18 and E.P. Neufeld, The Financial System of Canada: I t s Growth and Development (Toronto: Macmillan of Canada, 1972). 16 The original constitution of the section gave the following justification for its formation: “Whereas the Bond Dealers, members o f the Board o f Trade o f the City of Toronto, unanimously desire to work harmoniously together and to establish uniformity as far as practicable in the general conduct of their business and whereas it is impossible to arrive at any satisfactory result by casual and informal meetings, united and concerted action being essential thereto, it is therefore resolved . . .” Bond Dealers Section, Board of Trade of the City of Toronto, Minutes, 22 May 19 13.

508 CANADIAN PUBLIC ADMINISTRATION

CASE STUDY OF INVESTMENT DEALERS ASSOCIATION

that more than three-quarters of the applications received had come from the bond dealers. The minister then encouraged the bond dealers to form their own association to assist in future war loans, thereby giving a boost to efforts already being made in the industry along these lines.

The Bond Dealers Association of Canada (BDAC), which grouped firms from each region of the country, was formed in June 1916. Its objectives, which remained unchanged until 1969, were unexceptional for a trade association of the day.

- To promote the general welfare and influence of bond dealers, financial institutions and investors generally interested in Government, municipal, and corporation securities.

- To secure united protective action and to cooperate with municipal and other corporations in regard to legislation and sound financing.

- To afford opportunity for discussion and personal exchange of views on subjects of importance to the financial and commercial interests of the Dominion of Canada.

- To afford mutual protection against loss by crime.

Membership in the association was open to “any individual, firm or corporation making a practice of buying Government, Municipal, or Corporation bonds, or other investment securities and publicly offering them for sale.”’7

The first decade of the association’s life was spent in a context of minimal government supervision of the securities industry. Canadian law had followed British practice by focusing upon the company wishing to issue securities rather than on those buying and selling them. Over the first forty years of Confederation, Canadian law moved toward the principle of full disclosure: companies are free to sell anything provided the truth and the whole truth is told about what is being sold. Legislative development culminated in the Ontario Companies Act of 1907 that went considerably beyond the English law in defining the content of a prospectus.’8

The association was scarcely involved in regulating members’ behaviour. Its staff was minimal with a full-time secretary, J.A. Kingsmill, and a stenographer. Its constitution provided the executive committee with the power to summon any member whose behaviour it deemed to be detrimen- tal to the interests of the association. Such a provision is also unexceptional - most Canadian trade associations had and continue to have a similar clause where the emphasis is on protecting the association and its reputation rather

I7 Bond Dealers Association of Canada (BUAC), Constitution and By-Laws (Toronto: BDAC,

1916). 18 J . Peter Williamson, Securities Regulation in Cunadn (Toronto: University of Toronto Press, 1960). pp. 3 , 9

509 ADMINISTRATION PUBLIQUE DU CANADA

WILLIAM D. COLEMAN

than the public. Ensuring proper business conduct was the responsibility of the individual firm. The association occupied pressure pluralist networks spasmodically formed to deal with issues of concern both to the federal and to provincial governments. The association was normally consulted in the drafting stage of legislation affecting its interests.

Pure self-regulation, 1929-32 The legislative environment for the securities industry begin to change for the larger central Canadian firms in the late 1920s with the move to implement so-called blue sky legislation in Ontario and Quebec. Originating in the American state of Kansas in 191 1, such legislation went beyond the question of disclosure to require the registration of both securities and sales persons. The Kansas act was directed primarily at the issuers of securities and their agents as well as other sellers of securities. The three prairie provinces brought in similar legislation in the five years following the Kansas law but it was not until 1928 that a related law was enacted in Ontario. Earlier attempts in 1923 and 1924 in this province had failed. The Ontario Securities Frauds Prevention Act of 1928 sought to control traders in securities and hence had direct relevance for the Investment Bankers Association of Canada (IBAC) (the new name adopted by the Bond Dealers in 1924). It combined anti-fraud provisions with a requirement that brokers and sales persons be registered. The act was revised slightly in 1930 when it became a model for all the provinces except New Brunswick.19

The association responded to this strengthened state presence by taking the first, small steps toward self-regulation. Fearing “unwise and unsatisfac- tory blue sky legislation,” meaning government attempts to set standards for registration, the association had established a Vigilance Committee in 1923.*’ This committee was charged with rooting out sellers of worthless securities and “educating the public to invest monies in reputable dealers.” Reports of the committee at the succeeding four annual meetings all lament the lack of adequate machinery to carry out its tasks. In 1928 the name of the committee was changed to the Business Conduct Committee, a name still in use in the association today, and a new strategy was tried. The Eastern (Quebec) section of the association joined with the Montreal Stock and Curb Exchange to form a Better Business Bureau. A year later a similar bureau was established in Toronto with its secretary being J.A. Kingsmill, the secretary of the Investment Bankers Association.*’

Once blue sky legislation was introduced, but without setting standards,

19 Ibid., pp. 11-12,20-21. 20 BDAC, Minutes of the Seventh Annual Meeting. June 1923. 21 Also involved were the TSE, the Board of Trade, the Retail Merchant’s Association of the Toronto Board of Trade, the Toronto Real Estate Board, the Canadian Association of Advertising Agencies, and the Association of Canadian Advertisers.

510 CANADIAN PUBLIC ADMINISTRATION

CASE STUDY OF INVESTMENT DEALERS ASSOCIATION

the association stepped into the breach, signalling the start of a brief period of pure self-regulation. In 1929 it introduced the first of four elements that constitute the modern system of self-regulation - stringent membership requirements. Membership in the association was made contingent upon firms having at least two years experience in the industry and the recommendations of two existing members in good standing. These conditions were tightened further in 1932 when it was required that member firms be those whose “primary function” is the buying and selling of bonds. In 1931 and 1932 the association reported the rejection of several applications for membership because the applicants had insufficient ex- perience in the industry.

Secondly, it modified its disciplinary clause. Disciplinary responsibility was devolved upon the district (provincial) executive committees that were empowered to summon any member “whose conduct, or the character or conduct of whose business, or any of whose business or financial arrange- ments, associations, or affiliations, direct or indirect, may be disapproved by the Executive Committee.”*’ Hence the emphasis of the clause shifted from behaviour deleterious to the association to inappropriate business conduct whatever the impact on the association. Relations with the state continued to be close but spasmodic, depending on whether legislation was pending.

In short, this was a period of limited but pure self-regulation in the sense that the initiatives were taken by the association and these were implemented on its own without any delegation of state authority. They represented an attempt to pre-empt more intrusive state regulation and contained the organizational seeds for a future policy participation role. State officials were beginning to trade off policy responsibility for association self- governance. For example, under the terms of the new Ontario act, dealers were required to submit annually an audited financial statement. The chairman of the Central (Ontario) District of the IBAC sought and obtained an exemption from this provision for association members. He commented: “While the Department thus recognizes the standing of the members of the association, it was felt that this places an increased responsibility on the association to see that proper standards are maintained.””

Negotiated self-regulation, 1 933-47 The negotiation of this exemption marked the beginning of a transition from pure self-regulation to negotiated self-regulation: the association henceforth was forced to negotiate the terms of industry governance with the Ontario government. Pressure pluralism begins to give way to clientele pluralism. Following passage of the 1930 version of the Security Frauds

22 Investment Bankers Association of Canada (IBAC), Constitution andBy-laws (Toronto: IBAC, 1932), section 10. 23 IBAC, Minutes of thp Central Districl Executive Committee, 14 October 1931.

5 1 1 ADMINISTRATION PUBLIQUE DU CANADA

WILLIAM D. COLEMAN

Prevention Act, a government board was set up to regulate the securities industry. This board assumed its present name, the Ontario Securities Commission (osc), in 1933.24 The first Securities Commissioner of Ontario, George Drew (later premier of the province), approached the executive committee of the Central District in 1932 with two suggestions. He wondered whether the association should institute some sort of examination for members and sales persons to ensure they had adequate expertise. He also suggested that members would be in a much stronger position with the public if they instituted some sort of voluntary audit system.

This initiative resulted in a series of meetings between Drew and the association over the next two years. Drew was strongly of the opinion that if the association were to assume some disciplinary control over its members, the investment banking industry would be much more efficiently governed than if he were to promulgate any number of statutory regulations. His position reflected the philosophy of governments to the present day: industry self-regulation is the preferred mode of industry governance, but state regulation will be used if industry fails to assume this responsibility.

This initiative by Drew gave rise to considerable debate within the association. In his address to the 1934 annual meeting, the president of the association, W.C. Pitfield, suggested that the association had three options.25 It could remain primarily a voluntary association with no special responsib- ilities for regulating member behaviour. Secondly, the association could develop a voluntary code of ethics along the lines being used by the Investment Bankers Association of America.26 Or finally, it could seek authority to regulate members’ business conduct. The debate came to a head at the 1937 annual meeting when the association’s executive proposed a constitutional amendment that would have the association begin to monitor members’ internal financial affairs. Clearly, the stronger firms in the association had come to favour such an approach. They viewed increasing U.S. government regulation under the auspices of the newly created Securities and Exchange Commission with some alarm and were persuaded that if they did not take action, the Ontario government would. The chairman of the Central District noted: “it has been intimated to the Association that certain changes in organization and methods might be desirable. For this reason, a good deal of consideration was given during the

24 There is some ambiguity about when the osc was actually formed. J.F. Baillie states it was formed “in about 1933” but notes that legislation for thecommission probably emerged in 193 I . Legislation in 1931 and 1932 make reference to a “board” and the name Ontario Securities Commission does not appear until 1933 amendments to the Securities Frauds Prevention Act. J.F. Baillie, “The Protection of the Investor in Ontario: Part 1,” CANADIAN PUBLIC ADMINISTRA- TION 8, no. 2 (Summer 1965): 216. 25 IBAC, Minutes of the A n n w l General Meeting, 1934. 26 For a discussion of this brief American experiment, see Vincent Carosso, Investment Banking in Americu: A Histoty (Cambridge, Mass.: Harvard University Press, 1970). pp. 387-90.

5 12 CANADIAN PUBLIC ADMINISTRATION

CASE STUDY OF INVESTMENT DEALERS ASSOCIATION

past year to proposals for amending the By-Laws of the Association. These proposals are designed to make unnecessary any excessive Government regulation of the business of its members.” A speaker from the floor at the meeting added that the association could not criticize possible government intervention without putting some order in its own house. “We question their ability or capacity to tell us how our business should be run. Up to date, we have gone to the provincial authorities and they say . . . who are you? Have you any evidence you control your members in any way at all? We have been unable to answer that effectively at all.”*’ The motions to amend the constitution were carried.

The changes strengthened further the requirements for membership. They also empowered the association to select and pay a firm to be the association auditors. At the close of each financial year, members would be required to submit a financial statement “containing the information heretofore required to be furnished to the Securities Departments or Commissions in the District” and any other information demanded by the district executive committee to the association auditors.** If the information was unsatisfactory, the District Executive Committee could investigate further and suspend or expel the given member. These latter changes signalled the introduction of the second component of the present self- regulatory system - monitoring and disciplining members’ business conduct.

The adoption of these constitutional changes had an immediate impact on the members of the association. In his report to the 1938 annual meeting, the chairman of the Central District reported a number of problems were revealed by the audits. Members were found to be carrying marginal ac- counts with inadequate capital. One member had capital of $342 and another a deficit of $647. Some firms were compelled to rearrange their capital struc- tures and to bring in additional capital, others were directed to terminate certain unsatisfactory practices. Fourteen members were asked to resign.” In his address to the annual meeting of 1939, the president, D.K. Baldwin, noted that government officials and politicians were pleased with the actions taken by the association. “While the voluntary adoption of self-regulation under this By-Law has added to the operating costs of our members and has probably proved irksome to some, there is no doubt that its application has greatly added to the protection of the Public and the prestige of our members. There are many evidences [sic] that the various Securities Commissioners thoroughly understand, and view with favour, our actions in this respect.””

27 IDA, Minuies of the Annual General Meeting, 1937, pp. 34-35, 53. 28 IDA, Constituiion and Ey-Laws, 1937 (Toronto: IDA, 1937), article 8a. 29 IDA, Annual Meeting, 1938, p. 33. 30 Ibid., 1939, p. 9.

513 ADMINISTRATION PUBLIQUE DU CANADA

WILLIAM D. COLEMAN

In short, the association had negotiated an informal arrangement with government authorities enabling it, rather than the state, to regulate mem- bers’ behaviour. In these circumstances, the government saw no reason to involve itself further in monitoring the internal affairs of the association’s members. We have thus by this time a primitive clientele pluralist network. The osc was not a strong agency, having only one full-time administrative officer who also acted as chairperson of the commission. The association began to act as a private interest government regulating member behaviour on behalf of the state.

Mandated self-regulation, 1945-69 Such informal understandings did not last even a decade in the over-the- counter sector. By the mid 1940s government officials were forced to take a further look at securities legislation. A report of a royal commission inquiring into the mining industry indicted severely the existing securities laws; the province had gained an international reputation as a haven for fraudulent stock promoter^.^' In 1945 the government passed a new law, the Ontario Securities Act. Amended further in 1947, this act established the framework that continues to guide securities legislation today. The new legislation refined and expanded the disclosure requirements for the issue of securities. In addition, the law sought to lessen government control over firms in the industry by transferring more responsibility over business conduct to the industry itself. The act identified several categories of firms in the industry and defined “investment dealers” to be members of the Investment Dealers Association of Canada (the association had assumed its present name in 1934).3‘ Practically speaking, this meant that the IDAC had been given an explicit mandate by the state to regulate the business conduct of its members, superseding the informal understanding of heretofore. The association accepted this mandate in order to ward off direct government regulation. Speaking to the annual meeting of the IDA in 1946, the new chairman of the osc, C.P. McTague, drew a stark picture: “Bay Street should organize for the purpose of participating in the government of the Securities Business, or otherwise it would have to reconcile itself to absolute control by a bureaucracy which would inevitably grow more powerful and autocratic as

31 Peter Dey and Stanley Makuch, “Government Supervision of Self-Regulatory Organiza- tions in the Canadian Securities Industry,” in Consumer and Corporate Affairs, Proposals 3: 1419. 32 Broker-dealer was a category created explicitly by the government for firms that were members of neither the TSE nor the IDAC. In fact, these tended to be smaller firms heavily involved in mining stock speculation and the chief source of the problems that had emerged in the 1940s.

5 14 CANADIAN PUBLIC ADMINISTRATION

CASE STUDY OF INVESTMENT DEALERS ASSOCIATION

the time went by.”“’ Over the following two decades the association and the government were to work out the implications of this mandate and to put in place the third and fourth elements of the modern self-regulatory system - educational requirements, and a national contingency fund.

The association responded to the new environment first by strengthening further its existing self-regulatory structures. The minimum capital re- quired for membership was increased to $25,000 in 1952. By 1962 the association required that all new firms should have one-half of their mem- bers/directors continuously employed in the industry for five years prior to entry and that they have the support of five existing members of the associa- tion. The investigation of complaints and the administration of discipline in the association became more formalized. Members could be reprimanded, fined, suspended or expelled for any one of several reasons: any business conduct or practice unbecoming a member of the association; any failure to comply with or carry out provisions of any by-laws, regulations or rule of the association; “failure to comply with or carry out the provisions of any ap- plicable Federal or Provincial Statute relating to the sale of securities or of any rule of regulation made pursuant thereto” (note that the association is responsible for enforcing government statutes); and when the association is of the opinion that the business or financial arrangements of such member are objectionable. These rules were more than simply lines on paper. For example, in the two-year period between September 1969 and September 197 1, three firms were expelled because of serious infractions.34 Expulsion makes it very difficult for a firm to carry on in the industry.

In addition to these revisions to existing procedures, the association introduced two new elements to the self-regulatory system. In 1948, responding to a long-standing concern of some members of the group, it appointed its first director of education. The new director proceeded immediately to prepare materials for the “Elementary Course in Investment Banking” that was offered to 315 students. Following the success of this course, a more advanced course was prepared. Both courses quickly became industry standards and all employees of securities firms, whether members of the IDA or not, were encouraged to complete them. This success culminated in the late 1960s in negotiations between the IDA and the stock exchanges to set up a separate unit to administer and upgrade the courses as required. In 1970 the Canadian Securities Institute was born, with the IDA appointing half of its directors and the stock exchanges the other half. I n 1969 the association amended its membership requirements to demand that

33 IDA, Minutes of the Annual General Meeting, 1946, p. 34. 34 Information drawn from the minutes of the Western and Eastern Business Conduct Committees of the association for the period stated.

5 15 ADMINISTRATION PUBLIQUE DU CANADA

WILLIAM D. COLEMAN

partners in new member firms have completed the course before being admitted, thus formally incorporating the course into the self-regulatory system. All of the provincial securities administrators, save in Quebec, have written the course into their own regulations, requiring it as a prerequisite for registration as a broker or dealer.35

The second new addition to the self-regulation system, - a national contingency fund - also emerged in this period. In 1955, following the failure of a member firm, some members of the Toronto Stock Exchange agreed to cover the public’s loss in the amount of $125,000 dollars. In 1956 the Exchange moved to establish a special contingency reserve for similar cases and paid out of the fund for significant public losses incurred in 1961. The arrangement under the TSE was not totally satisfactory, however, because many members belonged to more than one exchange as well as to the IDA. Logically speaking, it was felt that not only clients of the TSE should be protected. Negotiations then began with the IDA and the other exchanges to establish a national fund that would protect all customers in the securities industry. Agreement was reached among these organizations leading to the creation of the national contingency fund in 1969. The IDA’S contribution to the fund was raised through a special levy on the members; it is now a part of the association’s constitution that all new members must make a contribution to the fund as a condition of joining.

The creation of the fund and the assumption of open-ended, ongoing contingent member liability implied by it have reinforced the self-regulatory efforts of the IDA and the stock exchanges. As Dey and Makuch note, “There is considerable incentive for each SRO (self-regulatory organization) to take a tough position on the maintenance of adequate net free capital because the greater portion of the cost of the failure of a member firm within the audit jurisdiction of the SRO is assumed by members of that S R O . ” ~ ~ By 1970, then, the four elements of present-day self-regulation were in place: stringent membership requirements, monitoring of business conduct, educational prerequisites, and a national contingency fund.

From clientele pluralism to concertation, 1969-86

The filling out of the self-regulatory system between 1947 and 1969 had initiated the structural transformation from conventional trade association 35 Formally speaking, the Quebec Securities Commission allows other courses as well as the csc when qualifying for registration. In practice, the csc is the standard course used in most cases. 36 Dey and Makuch, “Government Supervision,” p. 1413. The incentive works in the following fashion. The rules of the fund provide that the first $500,000 of a loss caused by the insolvency of a member firm be borne by the sponsoring self-regulatory organization primarily responsible for supervising that firm. The remaining loss is apportioned among all of the SROS.

D.W. Grant, “Aide-Memoire: Self-Regulatory Overview” (Toronto: IDA, 1986).

516 CANADIAN PUBLIC ADMINISTRATION

CASE STUDY OF INVESTMENT DEALERS ASSOCIATION

to a private interest government, reinforcing the strong position of the IDA in its clientele pluralist network with the osc and other provincial securities commissions. Events in Ontario during the 1960s, however, were to lead to political pressure to alter this arrangement. The weak government role was to be changed and again the association responded by strengthening its own governance powers. By the mid 1980s a concertation policy network linking a revitalized IDA and a reinforced state apparatus had emerged to manage securities regulation. In this respect the self-regulatory system conformed to the conditions for success laid down by William 0. Douglas, an early chairman of the Securities Exchange Commission in the United States before his appointment to the Supreme Court: “Government would keep the shotgun, so to speak, behind the door, loaded, well-oiled, cleaned, ready for use but with the hope that it would never be used.”37

The crisis began in 1964 when Texas Gulf Sulphur Company announced that it had made a major copper-zinc-silver discovery in the Timmins area of Ontario. The wild selling and trading that followed on the Toronto Stock Exchange proved to be beyond the control of the exchange and the osc. In the wake of the Texas Gulf discovery, another company, Windfall Oils and Mines, had purchased related lands in the Timmins area fostering tremen- dous speculation in its stock. After a dramatic rise, the company announced that no minerals were found on its land and the stock collapsed, leading to serious losses by many stockholders. The resulting public outcry led to the creation of four separate inquiries, inquiries that complemented the already-existing investigation of securities regulation by J.R. Kimber set up in October 1963.38 All the reports that followed indicated that the Ontario Securities Commission had failed to supervise adequately the Toronto Stock Exchange.

Baillie reports that the osc had only a minimal staff and little expertise at this time.3y Its legal status as a branch of the Department of the Attorney General prevented it from paying salaries that could attract expert staff with industry experience. Investigators employed by the commission tended to be retired police officers who possessed little knowledge of the intricacies of securities operations. Amendments to the Ontario Securities Act in 1967 and 1968 increased the supervisory powers of the osc over the TSE, enabled it to hire more’expert staff, and gave members of the exchange the right to appeal decisions of the exchange to the osc. The changes, however, left

37 Joel Seligman, The Transformution of Wall Street: A History of the Securities and Exchange Commission and Modern Corporate Finance (Boston: Houghton Mifflin, 1982), p. 185. 38 These included inquiries by a Select Committee on Mining of the Ontario Legislature, an osc investigation of the Timmins area, an osc investigation of the Windfall collapse, and a royal commission on the Windfall events headed by Mr. Justice Arthur Kelly. See Baillie, “Protection of the Investor.” p. 208. 39 Baillie, “Protection of the Investor,” pp. 216-19.

5 17 ADMINISTRATION PUBLIQUE DU CANADA

WILLIAM D. COLEMAN

some ambiguities about the cotnmission’s status as an independent agency and its ability to make policy. The commission began to use “policy statements” and not specific regulations to achieve its objectives. These statements helped structure and limit the broad discretion possessed by the osc. What is crucial for this study is that the osc was sufficiently strengthen- ed by these legislative changes and policy approaches that by the late 1970s Gray Taylor could argue effectively against the idea that the osc was the “captive” of the securities industry.’”

The increased scrutiny of the self-regulatory system that resulted from these changes could not be ignored by the IDA. It sensed once again the possibility of direct state regulation and reacted over the next ten years by redesigning and formalizing its self-regulatory apparatus. These changes did not come easily. After considerable internal debate and a study by a management consulting firm, the IDA decided to combine the functions of trade association and self-regulatory organization, two roles that had long since been differentiated in the US ~ y s t e m . ~ ’ The organizational changes that followed strengthened the control of the association over its members while leaving it as a powerful partner in a concertation policy network.

In 1969 it redefined its objectives for the first time since its inception in 1916 and incorporated an explicit reference to its self-regulatory role. At the same time, the association reorganized itself internally so it could better fulfill the public dimensions of this self-regulatory role. It created a separate public information division and hired several experts to act as policy advisers. Most importantly, the IDA changed its structure in 1972 to make the association’s president a permanent staff position. The first (and to date only) occupant of this position has developed this position to the point where he has become a widely recognized spokesperson for the securities industry in Canada. In 1976 the IDA modernized its executive structure by setting up for the first time a board of directors composed of senior executives of member firms. This board gives direction to the president and provides him with important backup support when he ventures into the public domain. In 1982 the IDA recognized its mixed advocacy/regulatory role by adding four members to its board, designated “public directors,” who were expected to provide opinions from those outside the industry.

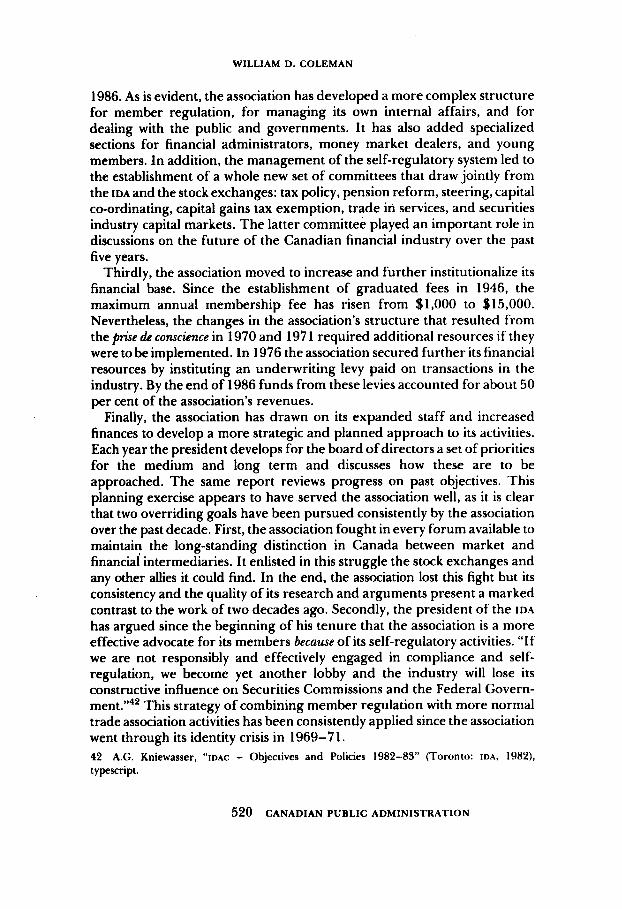

Secondly, the various changes in the association’s scope of activity have resulted in a more differentiated internal organization. Figure 1 compares the internal arrangements of the association in 1969 to those existing in late

40 These questions are reviewed at length in Gray E. Taylor, “Comments on the Mandate and Operation of the Ontario Securities Commission,” Uniuersify ofToronto Faculty of Law Review

41 The self-regulatory organization for the over-the-counter sector in the United States is the National Association of Securities Dealers. Trade association and lobbying responsibilities are assumed by another group, the Securities industry Association.

36 (1978): 1-43.

518 CANADIAN PUBLIC ADMINISTRATION

CASE STUDY OF INVESTMENT DEALERS ASSOCIATION

Figure 1. Organization of Permanent Stafl, ILIAC

1969

National Executive Committee

I Managing Director

I I Regional Chief directors examiner

1986 Board of directors

I

I

I

Executive Committee

President

- Executive vice-president

- Vice- President, Ottawa

- Association secretary

- Director compliance

- Director capital markets

I I Assistant to Secretary managing director

Regional offices Finance and administration Personnel Planning and management District council liasion Investigations department Atlantic regional director

Federal government liasion c Senior policy adviser

Secretary to Board Ontario regional director Membership By-laws Regulations

Compliance department 1 Registration department

- Capital markets and economic analysis

- Director public information

- Executive assistant to the president

519 ADMINISTRATION PUBLIQUE DU CANADA

WILLIAM D. COLEMAN

1986. As is evident, the association has developed a more complex structure for member regulation, for managing its own internal affairs, and for dealing with the public and governments. It has also added specialized sections for financial administrators, money market dealers, and young members. In addition, the management of the self-regulatory system led to the establishment of a whole new set of committees that draw jointly from the IDA and the stock exchanges: tax policy, pension reform, steering, capital co-ordinating, capital gains tax exemption, trade in services, and securities industry capital markets. The latter committee played an important role in discussions on the future of the Canadian financial industry over the past five years.

Thirdly, the association moved to increase and further institutionalize its financial base. Since the establishment of graduated fees in 1946, the maximum annual membership fee has risen from $1,000 to $15,000. Nevertheless, the changes in the association’s structure that resulted from the pnse & conscience in 1970 and 197 1 required additional resources if they were to be implemented. In 1976 the association secured further its financial resources by instituting an underwriting levy paid on transactions in the industry. By the end of 1986 funds from these levies accounted for about 50 per cent of the association’s revenues.

Finally, the association has drawn on its expanded staff and increased finances to develop a more strategic and planned approach to its activities. Each year the president develops for the board of directors a set of priorities for the medium and long term and discusses how these are to be approached. The same report reviews progress on past objectives. This planning exercise appears to have served the association well, as it is clear that two overriding goals have been pursued consistently by the association over the past decade. First, the association fought in every forum available to maintain the long-standing distinction in Canada between market and financial intermediaries. It enlisted in this struggle the stock exchanges and any other allies it could find. In the end, the association lost this fight but its consistency and the quality of its research and arguments present a marked contrast to the work of two decades ago. Secondly, the president of the IDA has argued since the beginning of his tenure that the association is a more effective advocate for its members becawe of its self-regulatory activities. “If we are not responsibly and effectively engaged in compliance and self- regulation, we become yet another lobby and the industry will lose its constructive influence on Securities Commissions and the Federal Govern- men^"^* This strategy of combining member regulation with more normal trade association activities has been consistently applied since the association went through its identity crisis in 1969-7 1. 42 A.G. Kniewasser, “IDAC - Objectives and Policies 1982-83” (Toronto: IDA, 1982), typescript.

520 CANADIAN PUBLIC ADMINISTRATION

CASE STUDY OF INVESTMENT DEALERS ASSOCIATION

Conclusion: conditions for private interest government

This case study of the IDA suggests several conditions that appear to en- courage self-regulation through a private interest government. First, self- regulation will be favoured when a sector is dominated by a small number of larger firms. In investment banking, the long-standing regulatory distinc- tion between market and financial intermediaries in Canada encouraged the growth of a distinctive set of investment dealer firms. Banks, trust companies, and insurance companies were prohibited from offering extensive invest- ment services because of a fear of self-dealing: governments wished to avoid having the same institution underwriting the issues of a client to which it was also granting loans. The market intermediaries that emerged as a con- sequence of this policy had matured as an industry by the end of the Second World War. The industry was dominated by less than a dozen large in- tegrated houses that engaged in all aspects of the business. These were joined by a number of distributing houses that did not normally originate large industrial issues, and by specialty houses that concentrated on a par- ticular phase of the investment bu~iness.~’

Investment banking was also a difficult sector to enter, not because of any collusive practices, but because of the very nature of the business. As has been noted, virtually all bond trading in Canada takes place in the over-the-counter market and not through the stock exchanges. Those wishing to invest money depended on investment dealers to provide them with advice on new issues. Gradually, a relationship of trust builds up between a dealer and an investor, making the latter reluctant to change firms. On the side of issuers, again the corporation involved would rely heavily on the dealer for advice in designing the securities and establishing their amount, characteristics, and price. Consequently, “a close advisory relationship will grow up between dealer and company somewhat similar to the professional relationship between a lawyer and his client, and the dealer may on occasion be represented on the corporation’s board of director^."^^ These kinds of relationships made it rather difficult for a firm to enter the industry and achieve success quickly.

Secondly, self-regulation becomes more likely when firms must co- operate on a regular basis in doing business. Normally, when a corporation decided to embark on a bond issue, it consulted with its dealer. Once the arrangements were finalized, the dealer in turn would put together a “banking group,” composed of itself and a number of other dealers who shared in the risks and profits of the underwriting, and a “selling group” that participated in the marketing of the issue. In virtually all instances, members

43 44 CSI, Course, p. 138.

D.H. Fullerton, The BondMarket in Canada (Toronto: Carswell, 1962), p. 84.

52 1 ADMINISTRATION PUBLIQUE DU CANADA

WILLIAM D. COLEMAN

of the banking and selling groups were IDA members only. In the domestic floating of government issues, the practice has been for the Government of Canada and for provincial governments to work through groups of dealers, all of which are members of the IDA. Such a collective approach to securities dealing created a strong collective interest in ensuring that all members were trustworthy, ethical, and solvent.

Thirdly, self-regulation becomes more attractive when regulation is directed at highly specialized and technical aspects of business conduct rather than specific end-products. Practically speaking, regulation of a financial service is not so simple as comparing the ingredients of a product to those listed on its label. Rather, regulation focuses on the capital base of firms - something which changes daily - and on business conduct. Most of the business in the industry takes place over the telephone and in private meetings, and is simply not susceptible to direct government regulation. Moreover, the expertise required for monitoring conduct and capital adequacy is difficult for bureaucratic agencies to develop and retain; the industry itself can provide the expertise more easily. Self-regulation thus creates better opportunities for establishing and enforcing standards than does direct, bureaucratic regulation.

The history of self-regulation in the Canadian industry also reveals a decided reluctance on the part of political leaders and their public servants to get too involved. The capital base of firms, their internal financial management, and the day-to-day conduct of business - all are parts of a business enterprise that traditionally are sacrosanct from government intervention. Hence governments have encouraged the industry to monitor these operations themselves, occasionally with the big stick of direct regulation, but content to oversee from some distance once the industry has shown a willingness to regulate itself. In the bond trading and underwriting side of the industry with which the IDA has been most directly concerned, there has been little history of political fallout from such a modus operundi. The sellers of bonds tend to be large, highly secure, institutions. Conse- quently, buyers are less likely to become the victims of a fraud and a source of political pressure than are the buyers of more speculative and risky mining stocks, for example.

To conclude, the path from pure self-regulation to a formalized man- dated self-regulatory system is more likely to be taken in sectors where firms are mature and relatively concentrated, with high barriers to entry. In addi- tion, industry practices that encourage some collective action in the market- place, and suppliers and customers that are large and institutional rather than small with more votes, add to the probability. The difficulties inherent in keeping track of human relationships makes self-regulation more attractive in sectors providing services than those producing goods. Governments may also have a greater philosophical reluctance to intervene in service sectors

522 CANADIAN PUBLIC ADMINISTRATION

CASE STUDY OF INVESTMENT DEALERS ASSOCIATION

because they wish to avoid having to monitor either the detailed internal operations of firms or trust-based customer-client relationships.

Finally, this article has argued that assumption of a private interest governmendpolicy participation role by an interest association takes place within a policy network involving state actors. The structure of this network may vary over time. In the Canadian securities industry, networks began by following a typical pressure pluralist mode and then gradually changed into clientele pluralism and finally concertation. The study of such networks to date has not taken sufficient account of the dynamics of change from one type of network to another and the conditions favouring such change^."^ Such historical analysis would appear to be necessary not only for the further elaboration of theory on the policy process, but also for an evaluation of the relationship between the type of policy network and the nature of policy outcomes. This article suggests that the change from clientele pluralism to concertation helped lessen the dominance of the securities industry itself over policy outcomes; a stronger state increased the probability of a consideration of a “public” interest. Yet the relatively closed character of a concertation network may still frustrate policy innovation in other cir- cumstances. The deregulation of 1987 allowing banks entry into the securi- ties sector had to be imposed on the network from the outside following a political battle. Concertation networks may be more stable than clientele pluralism, but also more resistant to societal change.

45 For an attempt along these lines, see Brigitte Young, “Does the American Dairy Industry Fit a Meso-Corporatism Model?” Political Studies (forthcoming).

523 ADMINISTRATION PUBLIQUE DU CANADA