Embed Size (px)

Citation preview

Self-employment in Telework

Presented by: Andrea Dimond

Washington Assistive Technology Foundation

Where we’re going PART I: Who is the Telework entrepreneur

PART II: Reaching the Telework entrepreneur

PART III: Funding the Telework entrepreneur

PART I: Who is the Telework entrepreneur Thousands of people with disabilities have been successful

as small business owners.

The 1990 national census revealed that people with disabilities have a higher rate of self-employment and small business experience (12.2 percent) than people without disabilities (7.8 percent).

The Disabled Businessman’s Association estimates that 40 percent of home-based businesses are operated by people with disabilities

The Federal Reserve Board’s report, “National Survey of Small Business Finances (1995),” found that small businesses were home-based 53 percent of the time

First National Study of People with Disabilities Who are Self-Employed

Conducted by Research & Training Center on Disability in Rural Communities

Research Goals 1. Gather information on the self-employment experiences

of people with disabilities.2. Use this information to improve services for current and future entrepreneurs with disabilities and the agencies supporting them.

Research Process: They sent a 51-question survey to 1,059 individuals. 203 surveys were undeliverable and 390 completed surveys were returned. Of these returned surveys, 330 were usable (45 percent response rate).

What professional back grounds do entrepreneurs with disabilities have? Variety of educational

backgrounds (see chart)

More than half (67%) of entrepreneurs were between the ages of 40 and 59

H.S /GED -18%Voc.School -11%SomeCollege -30%Bachelor's Degree18%Post-Grad- 20%

Why choose entrepreneurship?4 out of 10 respondents chose theentrepreneurial route because:

They "needed to create their own job."

They wanted flexible hours and working conditions "to accommodate a disability."

Other reasons to choose self-employment #1 Reason: Wanted to “work for myself”

Wanted to make more money

Identified need for product or service

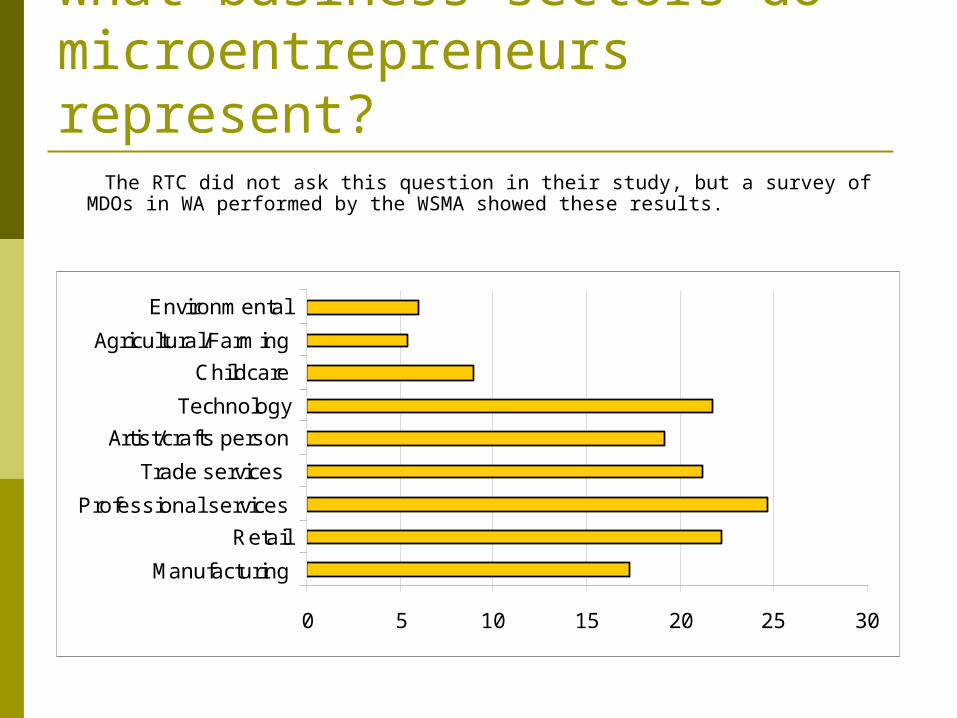

What business sectors do microentrepreneurs represent? The RTC did not ask this question in their study, but a survey of

MDOs in WA performed by the WSMA showed these results.

0 5 10 15 20 25 30

Manufacturing

Retail

Professional services

Trade services

Artist/crafts person

Technology

Childcare

Agricultural/Farming

Environmental

Annual gross income of businesses owned by people with disabilities

<$5,000 34%

$5,001 - $10,00010%$10,001-$20,00010%$20,001-$30,000 8%

$30,00,-$100,00010%$100,001-$500,00014%>$500,000 6%

PART II: Reaching the Telework entrepreneur WATF’s experience with Telework Loans

Partnerships & outreach to the small business community

Workshops

Tabling Events

WATF’s Experience with Telework Loaned $38,700 in 9 loans 6 self-employment:

-Wildlife Photographer (Vehicle)-Landscaper (Tractor)-Mobility Specialist (Vehicle)-Embroidery Digitizer (Computer & software)-Notary (Notary equip.)-Online clothing retail (Computer & camera equipment)

3 employment: Primarily computer equipment & accessories

Our Experience in WA Establish Washington State Microenterprise

Association

Referral Source

Opened doors

Lesson Learned: This relationship was not enough to get the results we wanted. We need to better leverage our Telework funds.

Microenterprise Development Organizations (MDOs) Microloan programs are typically non-profit

entities and partnerships that assist individuals in starting microenterprises. MDOs provide hands on technical assistance.

MDOs offer a variety of training and funding products depending on their focus. Many are limited geographically by funding.

MDOs want to reach out to people with disabilities but may not know how

Microenterprise: a business with start up costs of $35,000 or less and employing 5 or fewer people.

Small Business Development Centers (SBDC) These centers provide free business

counseling to entrepreneurs for both start-up and existing businesses.

Many SBDC clients fall into the category of microenterprise, and an increasing number are home-based.

SBDCs do not offer funding but offer referrals to funding sources and help business owners prepare loan applications

Other potential partnersSmall Business AdministrationOffice of Minority and Women Owned BusinessesSCOREOthers?All of these entities can provide: Marketing opportunities

-Publications-Workshops-Newsletter

Networking opportunities-Source of other funding to combine Telework loan with

Client resource-Clients can use SBA business library-Service Corp of Retired Executives (SCORE)

Workshops Small Business Assistive Technology Financial Literacy

Lessons Learned: 1. Workshops are an opportunity for partnership with MDOs, Housing authorities, VR, Independent Living Centers, etc.2. There is a high demand for self-employment workshops 3. It’s a long trip from workshop participant to borrower: include benefits planners, VR, microenterprise, and other small business resources to get a borrower ready for a loan

Tabling & presenting Small Business Fairs

Employment fairs

Lesson Learned: Give a presentation—don’t just table

PART III: Funding the Telework entrepreneur Startup Funding Needs

Tiered Funding Strategy

Putting together a full funding package

Startup Funding Needs Supplies

Inventory (for a product business)

Licensing & Insurance

Equipment

Lesson Learned: 1. It takes more than equipment to start a business2. No one knows what Telework is, but they do know that they need business equipment

Tiered Funding Strategy Evaluate a need vs. a want

Challenge business owners to think of business in stages

Plan on providing multiple small loans to start up businesses

Lesson Learned: Borrowers learn a lot in the first year of business and will spend money more wisely once they have some experience under their belt

Business Loan Requirements Business Plan with 12 months of financial

projections All local & state licenses and insurance

requirements necessary to be legal Borrowers who require funding greater than

$10,000 must have personal health insurance and key person insurance if they are a business owner

Business Checking Account

Lesson Learned: You won’t necessarily get the insurance reimbursement check just because you’re an additional named insured

Putting together a full funding package Business Funding Resources

Partner with other funding sources (MDOs, VR, PASS)

Help clients leverage funds

Lesson Learned: Providing multiple loans from various agencies to one client can be difficult when collateral comes into play.

Thank YouAndrea DimondWashington Assistive Technology Foundation100 South King Street, Ste. 280Seattle, WA [email protected]

Study referenced:First National Study of People with Disabilities Who are Self-EmployedRural Disability and Rehabilitation Research Progress Report #8February 2001This Research Progress Report was prepared by Nancy Arnold, Tom Seekins, and Diana Spas © RTC: Rural, 2001. This publication is available in Braille, large print, and ASCII DOS text formats.