Embed Size (px)

Citation preview

Selected issues on

Capital Gains for Non-residentsChamber of Tax Consultants’ - International Tax Study Circle

CA Rutvik R Sanghvi30th April 2014

Contents

Accrual & Deemed Accrual of Capital Gains in India

Indirect Transfers

Forex Fluctuation Adjustment

Tax Rates for Non-residents

Sec 112 & Forex Fluctuation Adjustment

Taxability under DTAA

Ch. XIIA - Special provisions for NRIs

Taxability of FIIs

TDS u/s. 195

2

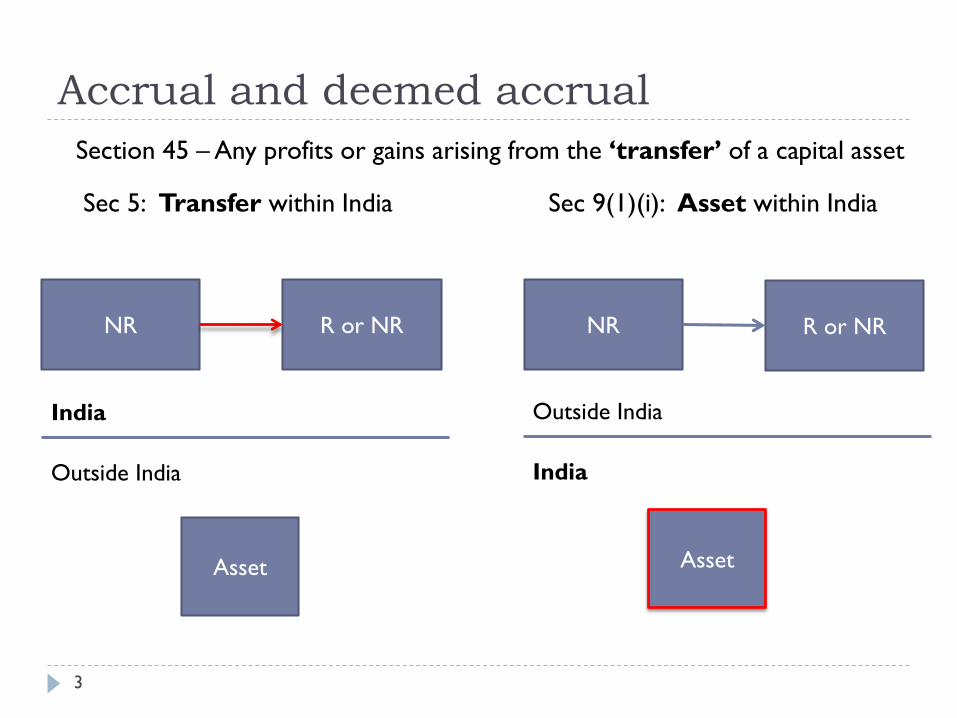

Accrual and deemed accrual

Sec 9(1)(i): Asset within India

NR

Asset

R or NR

Outside India

India

NR

Asset

R or NR

Sec 5: Transfer within India

India

Outside India

Section 45 – Any profits or gains arising from the ‘transfer’ of a capital asset

3

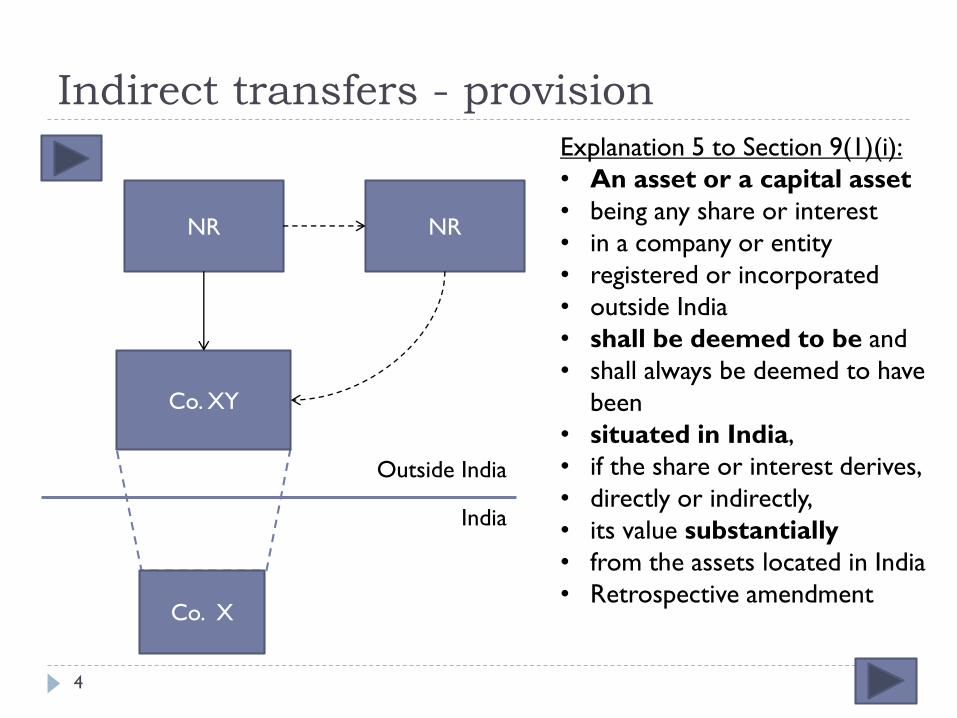

Indirect transfers - provision

NR

Co. XY

India

Outside India

Co. X

Explanation 5 to Section 9(1)(i):

• An asset or a capital asset

• being any share or interest

• in a company or entity

• registered or incorporated

• outside India

• shall be deemed to be and

• shall always be deemed to have

been

• situated in India,

• if the share or interest derives,

• directly or indirectly,

• its value substantially

• from the assets located in India

• Retrospective amendment

NR

4

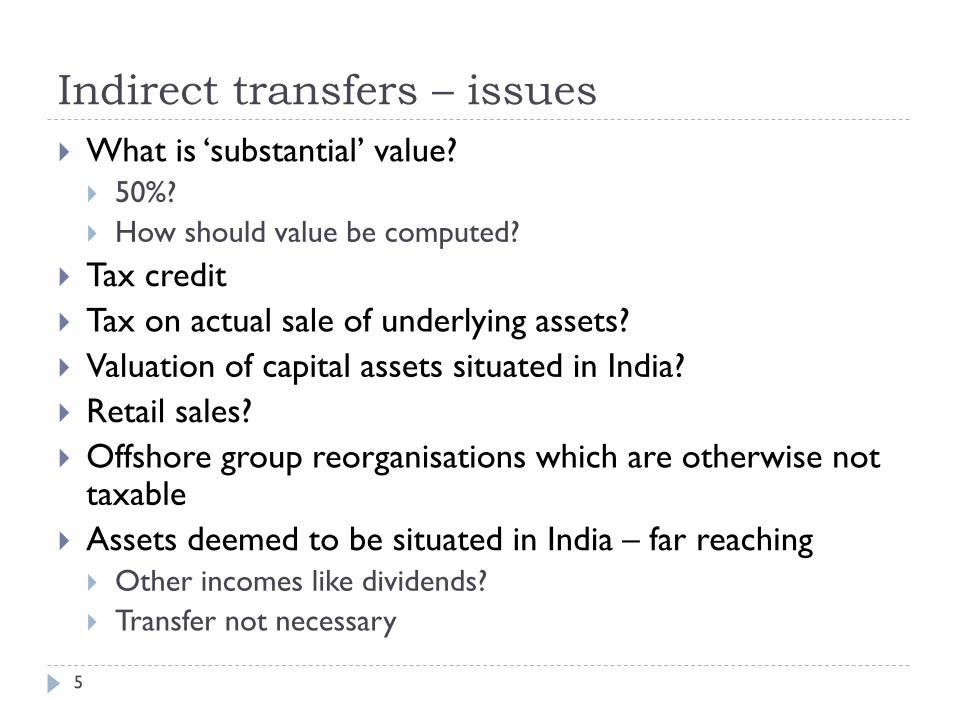

Indirect transfers – issues

What is ‘substantial’ value?

50%?

How should value be computed?

Tax credit

Tax on actual sale of underlying assets?

Valuation of capital assets situated in India?

Retail sales?

Offshore group reorganisations which are otherwise not taxable

Assets deemed to be situated in India – far reaching

Other incomes like dividends?

Transfer not necessary

5

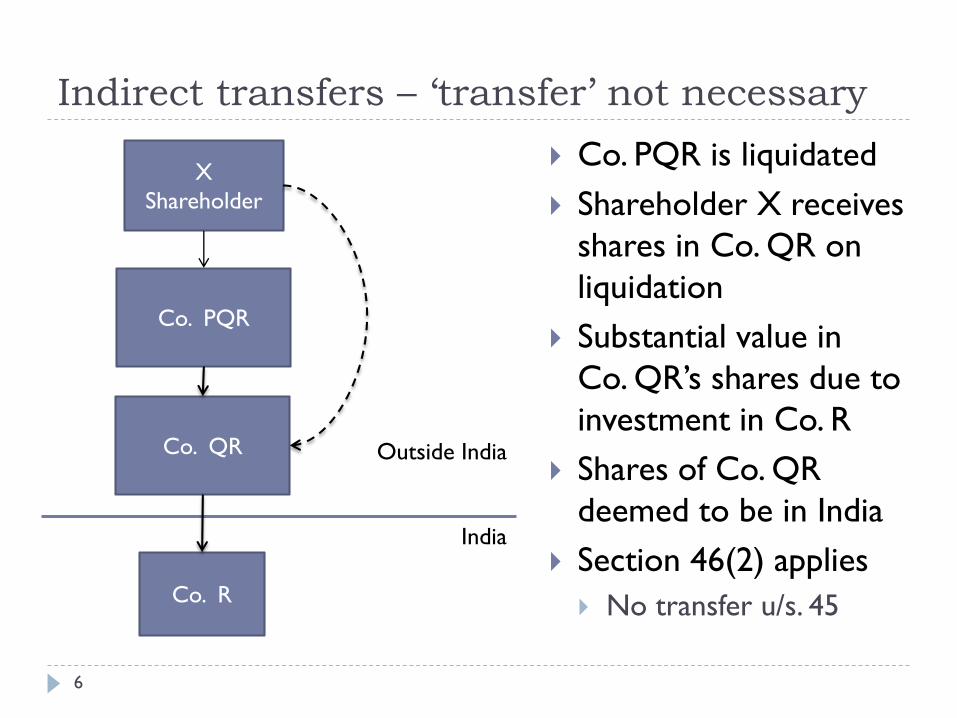

Indirect transfers – ‘transfer’ not necessary

Co. PQR is liquidated

Shareholder X receives

shares in Co. QR on

liquidation

Substantial value in

Co. QR’s shares due to

investment in Co. R

Shares of Co. QR

deemed to be in India

Section 46(2) applies

No transfer u/s. 45

X

Shareholder

Co. QR

India

Outside India

Co. R

Co. PQR

6

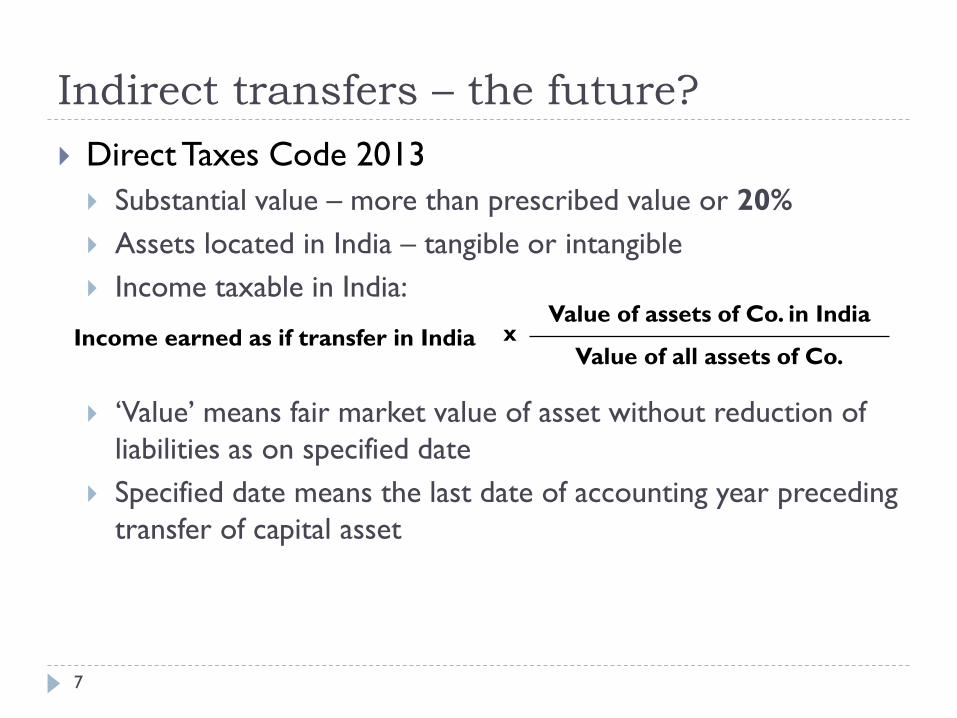

Indirect transfers – the future?

Direct Taxes Code 2013

Substantial value – more than prescribed value or 20%

Assets located in India – tangible or intangible

Income taxable in India:

‘Value’ means fair market value of asset without reduction of

liabilities as on specified date

Specified date means the last date of accounting year preceding

transfer of capital asset

Income earned as if transfer in India x Value of assets of Co. in India

Value of all assets of Co.

7

Indirect transfers – DTAA relief

Section 9(1)(i) not a non-obstante clause

Section 90(2) applies wherever DTAA beneficial

Sanofi Pasteur Holding SA

Groupe Industrial Marcel Dassault, In re

Vodafone South Ltd.

Implications?

8

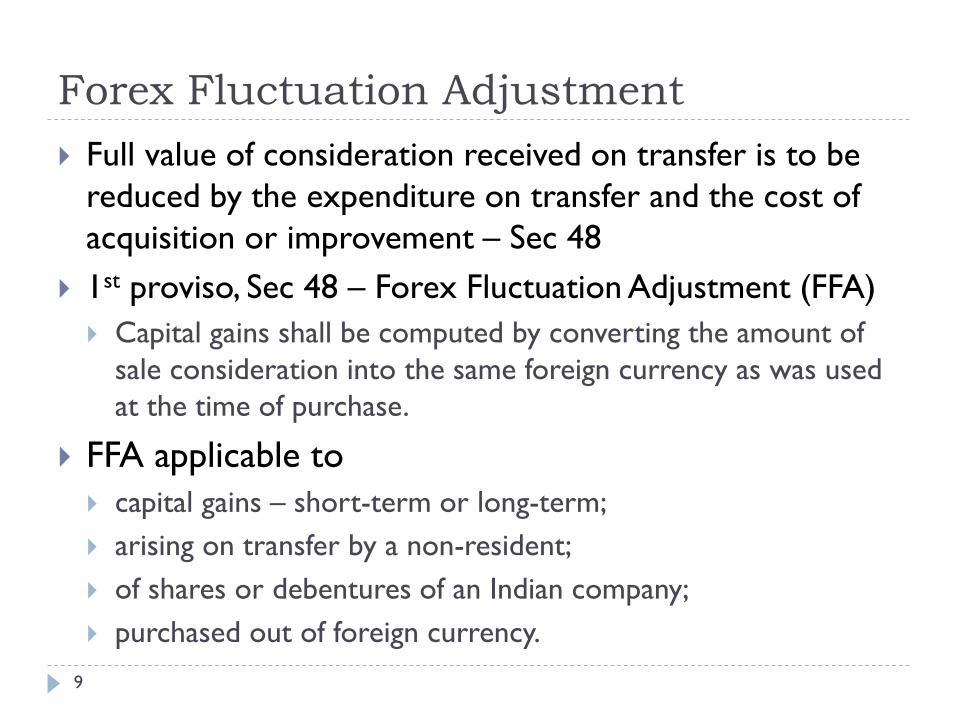

Forex Fluctuation Adjustment

Full value of consideration received on transfer is to be

reduced by the expenditure on transfer and the cost of

acquisition or improvement – Sec 48

1st proviso, Sec 48 – Forex Fluctuation Adjustment (FFA)

Capital gains shall be computed by converting the amount of

sale consideration into the same foreign currency as was used

at the time of purchase.

FFA applicable to

capital gains – short-term or long-term;

arising on transfer by a non-resident;

of shares or debentures of an Indian company;

purchased out of foreign currency.

9

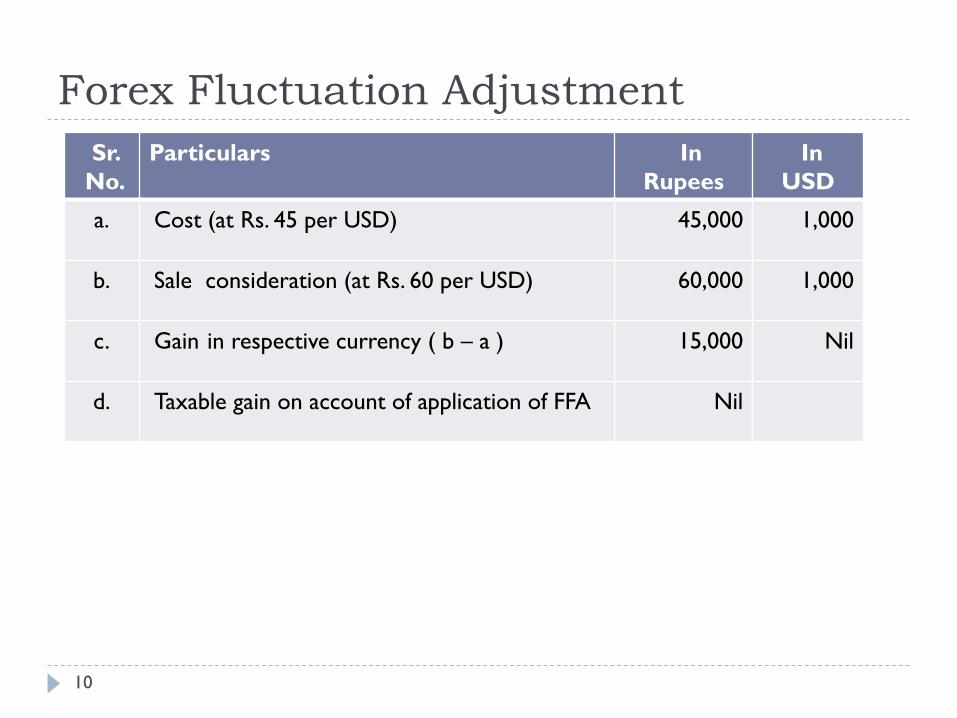

Forex Fluctuation Adjustment

Sr.

No.

Particulars In

Rupees

In

USD

a. Cost (at Rs. 45 per USD) 45,000 1,000

b. Sale consideration (at Rs. 60 per USD) 60,000 1,000

c. Gain in respective currency ( b – a ) 15,000 Nil

d. Taxable gain on account of application of FFA Nil

10

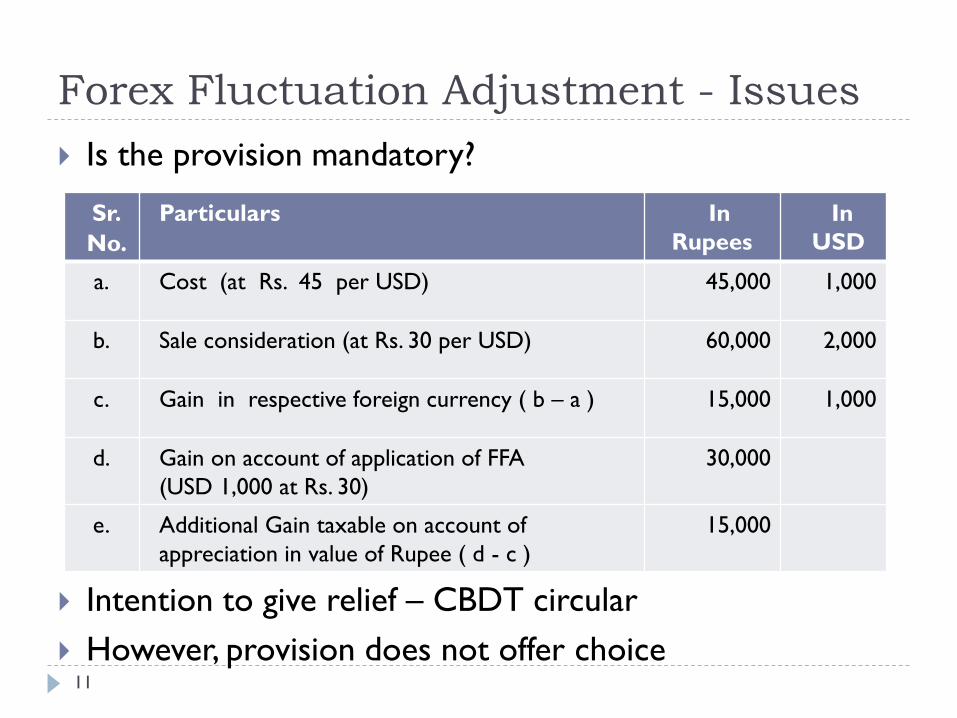

Forex Fluctuation Adjustment - Issues

Is the provision mandatory?

Intention to give relief – CBDT circular

However, provision does not offer choice

Sr.

No.

Particulars In

Rupees

In

USD

a. Cost (at Rs. 45 per USD) 45,000 1,000

b. Sale consideration (at Rs. 30 per USD) 60,000 2,000

c. Gain in respective foreign currency ( b – a ) 15,000 1,000

d. Gain on account of application of FFA

(USD 1,000 at Rs. 30)

30,000

e. Additional Gain taxable on account of

appreciation in value of Rupee ( d - c )

15,000

11

Forex Fluctuation Adjustment - Issues

Provision applicable to Shares or debentures received as

gifts or by way of inheritance

NRO Deposits covered?

Foreign exchange utilised

However non-repatriable investments

No relief for fluctuation from date of remittance till date

of purchase

Reinvestments

Forex rate of which date to be considered?

Gains earned in rupees to be adjusted?

FFA and ‘Indexation benefit’ provisions mutually exclusive

12

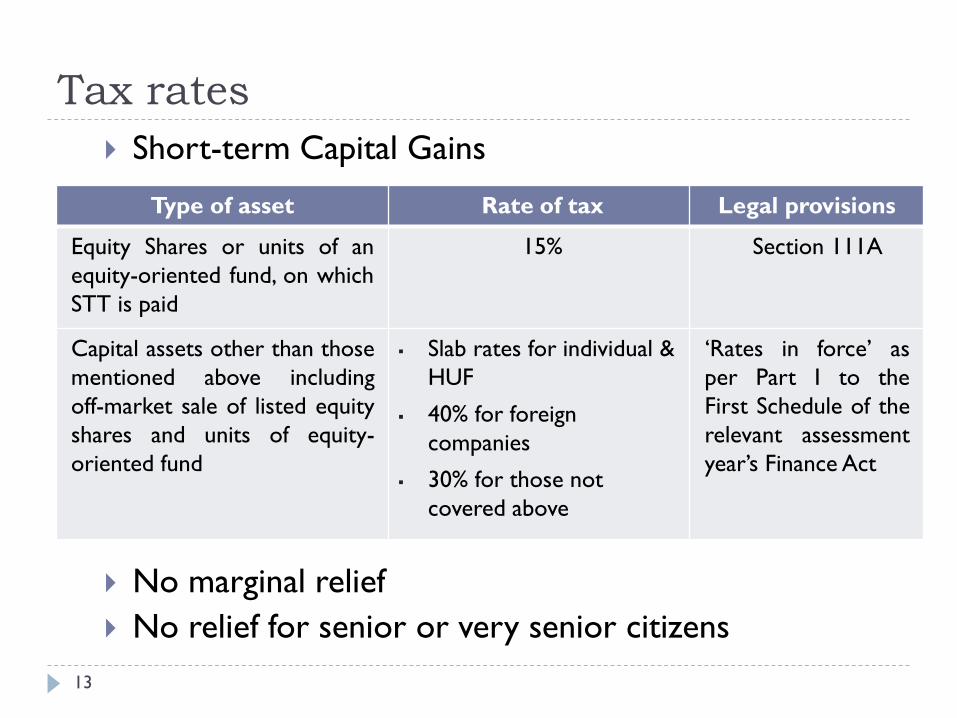

Tax rates

Type of asset Rate of tax Legal provisions

Equity Shares or units of an

equity-oriented fund, on which

STT is paid

15% Section 111A

Capital assets other than those

mentioned above including

off-market sale of listed equity

shares and units of equity-

oriented fund

Slab rates for individual &

HUF

40% for foreign

companies

30% for those not

covered above

‘Rates in force’ as

per Part I to the

First Schedule of the

relevant assessment

year’s Finance Act

Short-term Capital Gains

No marginal relief

No relief for senior or very senior citizens

13

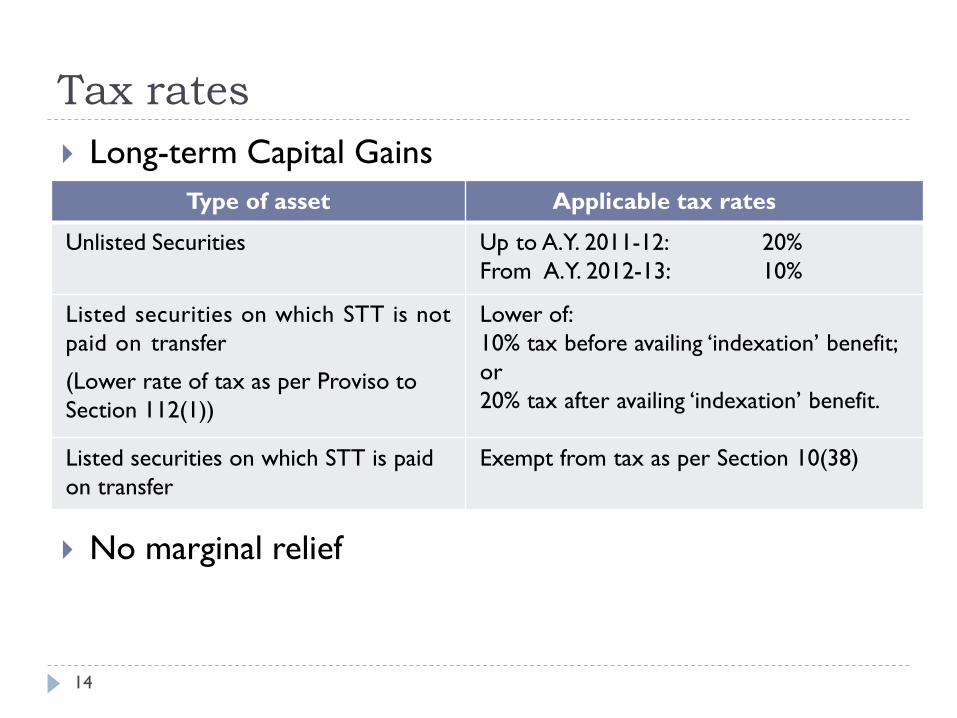

Tax rates

Type of asset Applicable tax rates

Unlisted Securities Up to A.Y. 2011-12: 20%

From A.Y. 2012-13: 10%

Listed securities on which STT is not

paid on transfer

(Lower rate of tax as per Proviso to

Section 112(1))

Lower of:

10% tax before availing ‘indexation’ benefit;

or

20% tax after availing ‘indexation’ benefit.

Listed securities on which STT is paid

on transfer

Exempt from tax as per Section 10(38)

Long-term Capital Gains

No marginal relief

14

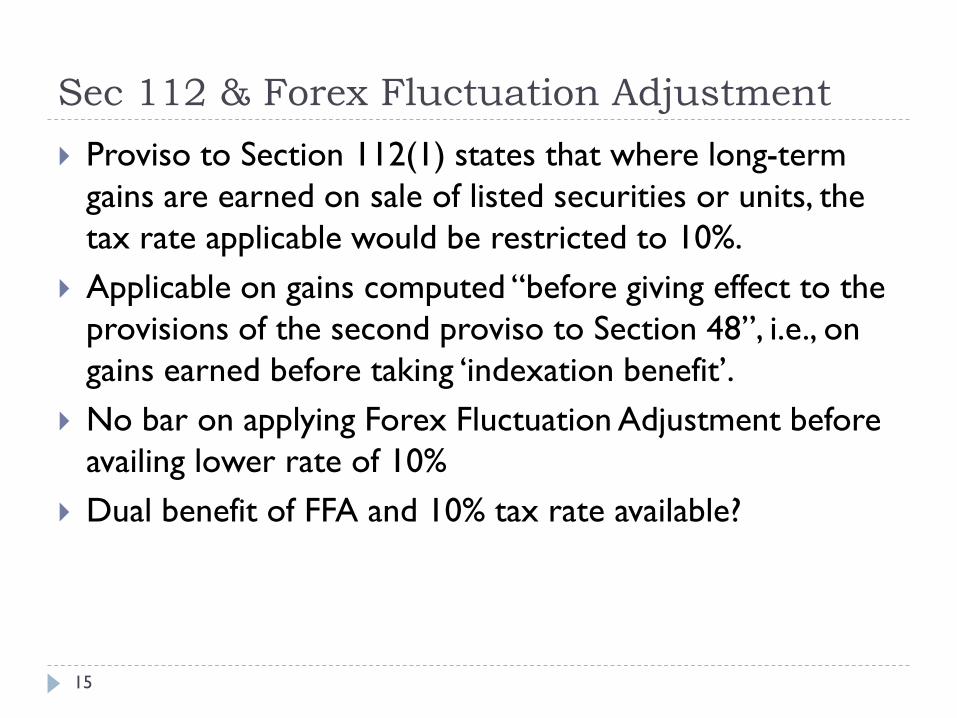

Sec 112 & Forex Fluctuation Adjustment

Proviso to Section 112(1) states that where long-term

gains are earned on sale of listed securities or units, the

tax rate applicable would be restricted to 10%.

Applicable on gains computed “before giving effect to the

provisions of the second proviso to Section 48”, i.e., on

gains earned before taking ‘indexation benefit’.

No bar on applying Forex Fluctuation Adjustment before

availing lower rate of 10%

Dual benefit of FFA and 10% tax rate available?

15

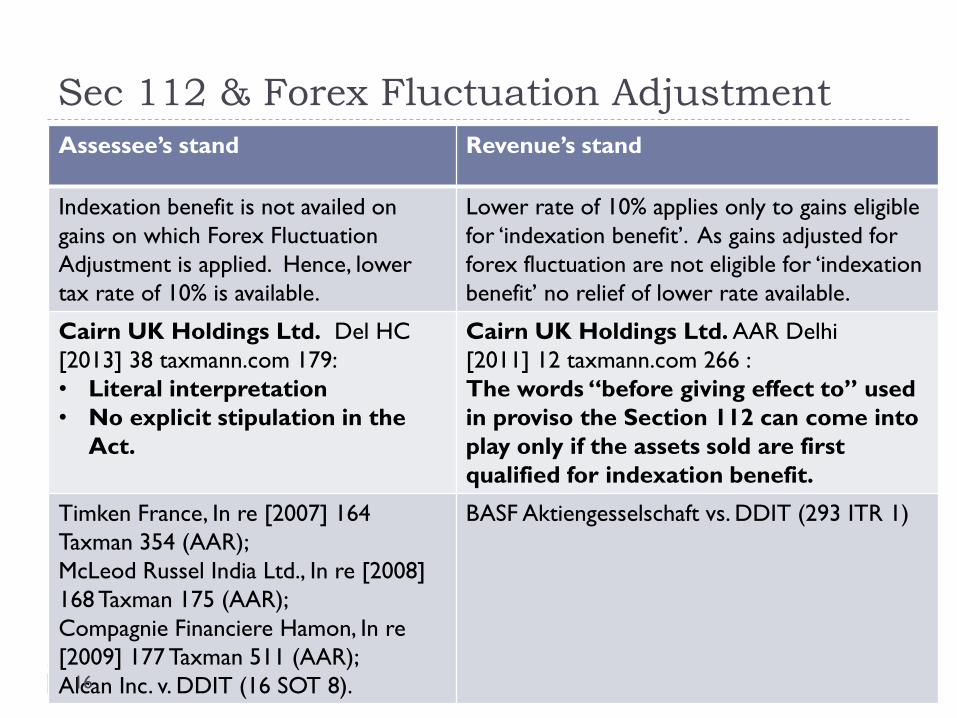

Sec 112 & Forex Fluctuation Adjustment

Assessee’s stand Revenue’s stand

Indexation benefit is not availed on

gains on which Forex Fluctuation

Adjustment is applied. Hence, lower

tax rate of 10% is available.

Lower rate of 10% applies only to gains eligible

for ‘indexation benefit’. As gains adjusted for

forex fluctuation are not eligible for ‘indexation

benefit’ no relief of lower rate available.

Cairn UK Holdings Ltd. Del HC

[2013] 38 taxmann.com 179:

• Literal interpretation

• No explicit stipulation in the

Act.

Cairn UK Holdings Ltd. AAR Delhi

[2011] 12 taxmann.com 266 :

The words “before giving effect to” used

in proviso the Section 112 can come into

play only if the assets sold are first

qualified for indexation benefit.

Timken France, In re [2007] 164

Taxman 354 (AAR);

McLeod Russel India Ltd., In re [2008]

168 Taxman 175 (AAR);

Compagnie Financiere Hamon, In re

[2009] 177 Taxman 511 (AAR);

Alcan Inc. v. DDIT (16 SOT 8).

BASF Aktiengesselschaft vs. DDIT (293 ITR 1)

16

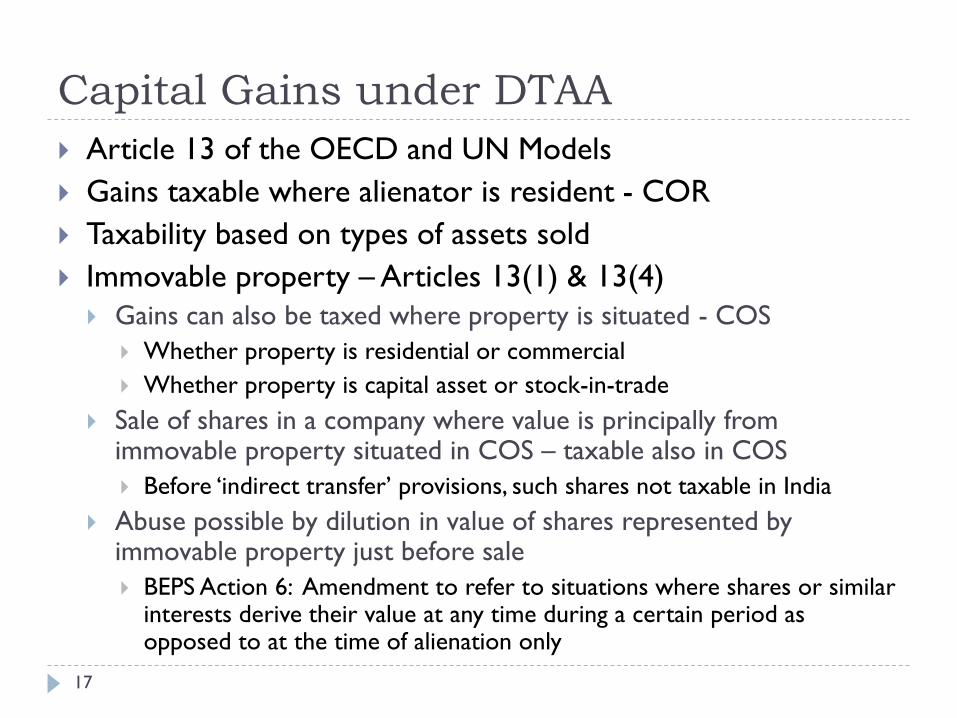

Capital Gains under DTAA

Article 13 of the OECD and UN Models

Gains taxable where alienator is resident - COR

Taxability based on types of assets sold

Immovable property – Articles 13(1) & 13(4)

Gains can also be taxed where property is situated - COS

Whether property is residential or commercial

Whether property is capital asset or stock-in-trade

Sale of shares in a company where value is principally from immovable property situated in COS – taxable also in COS

Before ‘indirect transfer’ provisions, such shares not taxable in India

Abuse possible by dilution in value of shares represented by immovable property just before sale

BEPS Action 6: Amendment to refer to situations where shares or similar interests derive their value at any time during a certain period as opposed to at the time of alienation only

17

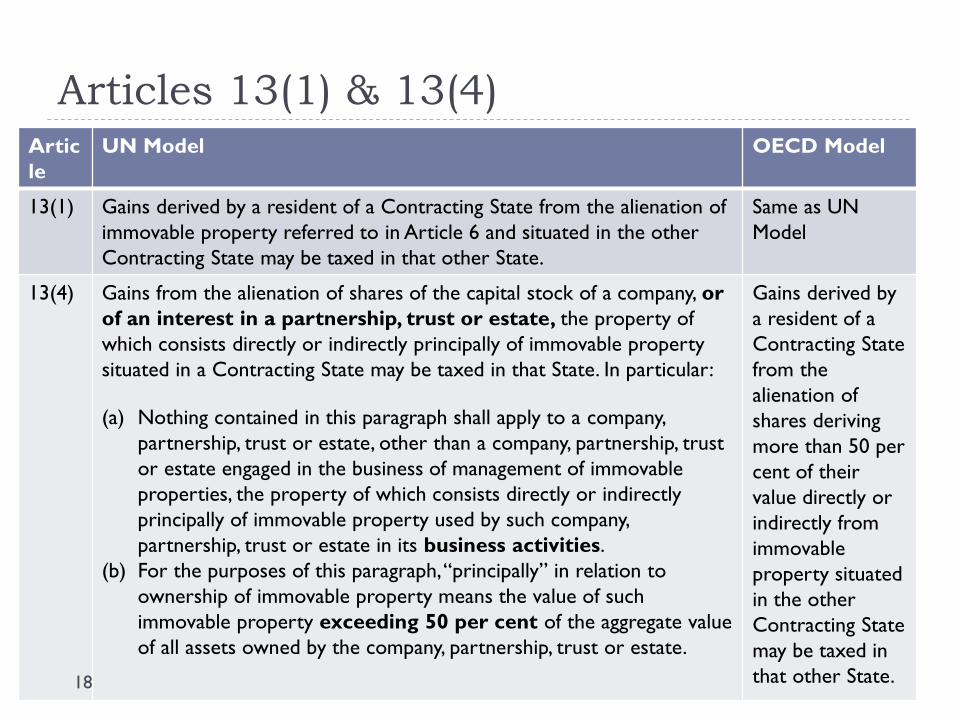

Articles 13(1) & 13(4)Artic

le

UN Model OECD Model

13(1) Gains derived by a resident of a Contracting State from the alienation of

immovable property referred to in Article 6 and situated in the other

Contracting State may be taxed in that other State.

Same as UN

Model

13(4) Gains from the alienation of shares of the capital stock of a company, or

of an interest in a partnership, trust or estate, the property of

which consists directly or indirectly principally of immovable property

situated in a Contracting State may be taxed in that State. In particular:

(a) Nothing contained in this paragraph shall apply to a company,

partnership, trust or estate, other than a company, partnership, trust

or estate engaged in the business of management of immovable

properties, the property of which consists directly or indirectly

principally of immovable property used by such company,

partnership, trust or estate in its business activities.

(b) For the purposes of this paragraph, “principally” in relation to

ownership of immovable property means the value of such

immovable property exceeding 50 per cent of the aggregate value

of all assets owned by the company, partnership, trust or estate.

Gains derived by

a resident of a

Contracting State

from the

alienation of

shares deriving

more than 50 per

cent of their

value directly or

indirectly from

immovable

property situated

in the other

Contracting State

may be taxed in

that other State.18

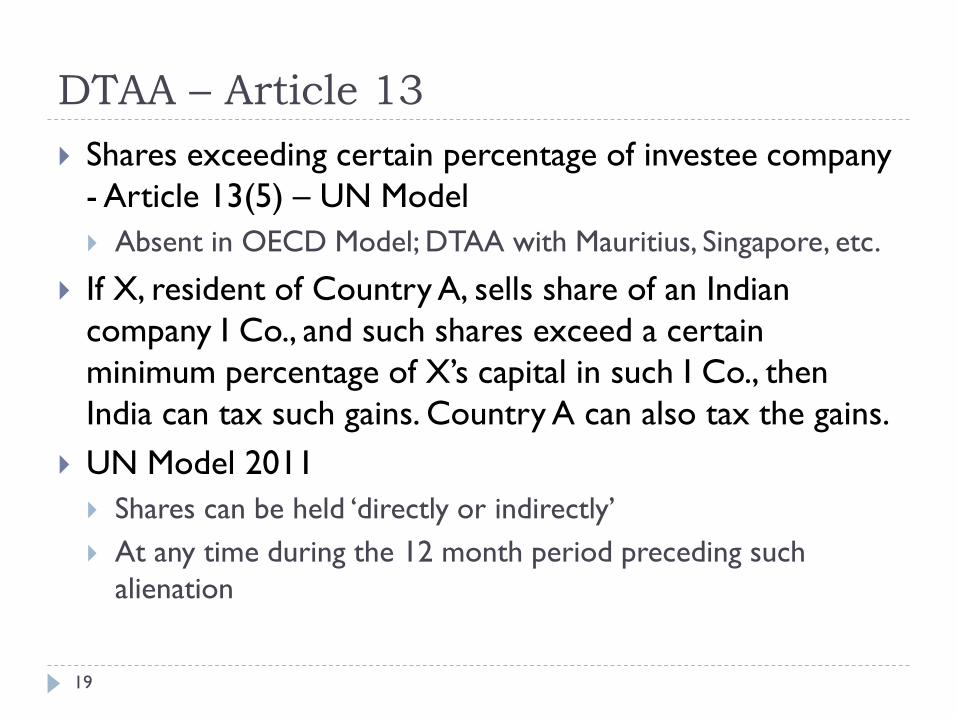

DTAA – Article 13

Shares exceeding certain percentage of investee company

- Article 13(5) – UN Model

Absent in OECD Model; DTAA with Mauritius, Singapore, etc.

If X, resident of Country A, sells share of an Indian

company I Co., and such shares exceed a certain

minimum percentage of X’s capital in such I Co., then

India can tax such gains. Country A can also tax the gains.

UN Model 2011

Shares can be held ‘directly or indirectly’

At any time during the 12 month period preceding such

alienation

19

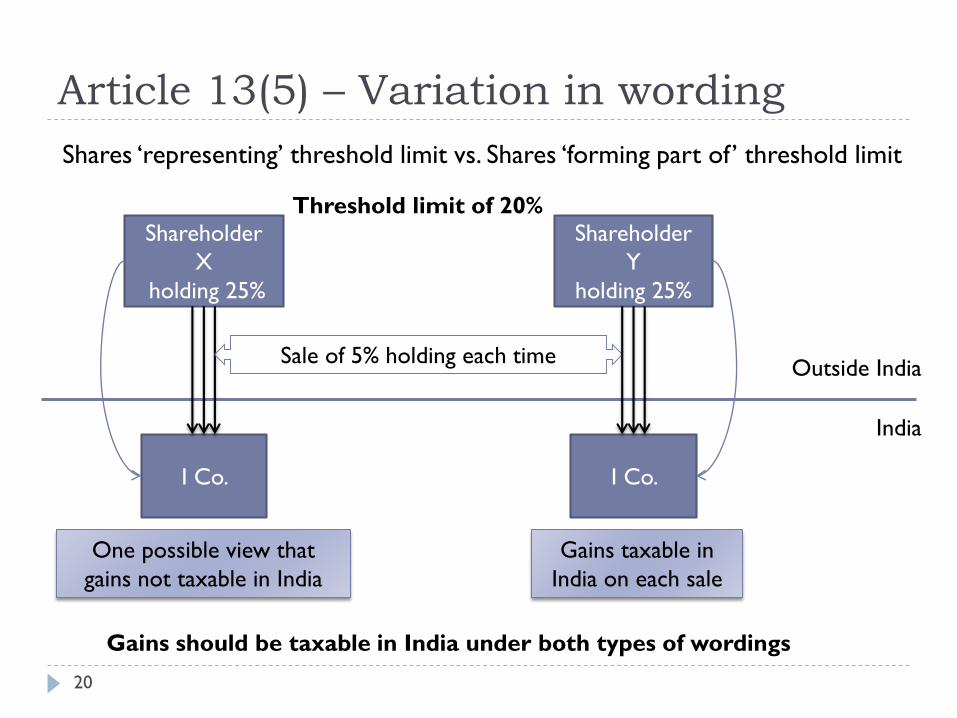

Article 13(5) – Variation in wording

Shareholder

X

holding 25%

India

Outside India

I Co.

Shares ‘representing’ threshold limit vs. Shares ‘forming part of’ threshold limit

Shareholder

Y

holding 25%

I Co.

Sale of 5% holding each time

Threshold limit of 20%

One possible view that

gains not taxable in India

Gains taxable in

India on each sale

20

Gains should be taxable in India under both types of wordings

DTAA – Article 13 – Other provisions

Movable property owned by PE or FB - Article 13(2) Taxable in India if PE or FB in India

Short-term gain u/s. 50 as per ‘block of assets’

Ships & Aircraft - Article 13(3) NR earns Capital Gains from sale of:

ships or aircraft operated in international traffic;

boats engaged in inland waterways transport; or

movable property pertaining to such operation.

Gains can be taxed only in Contracting State in which the place of effective management of the enterprise is situated.

However, immovable property pertaining to above covered in Art. 13(1)

Other property - Article 13(6)

Taxable in COR, India does not get right to tax

Used for double non-taxation under Mauritius, Singapore DTAAs

21

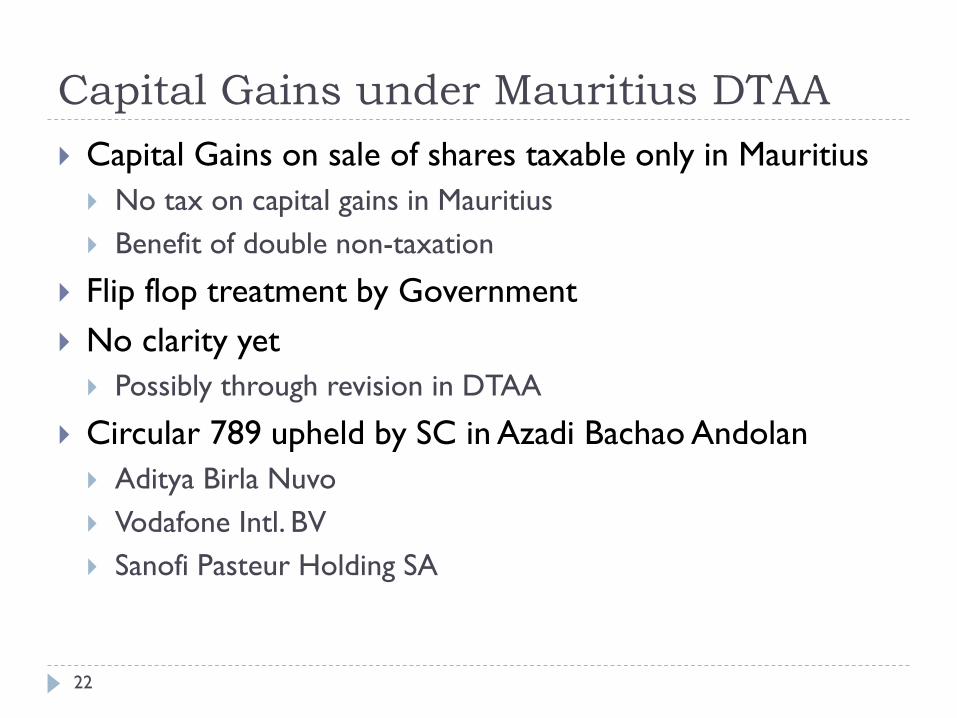

Capital Gains under Mauritius DTAA

Capital Gains on sale of shares taxable only in Mauritius

No tax on capital gains in Mauritius

Benefit of double non-taxation

Flip flop treatment by Government

No clarity yet

Possibly through revision in DTAA

Circular 789 upheld by SC in Azadi Bachao Andolan

Aditya Birla Nuvo

Vodafone Intl. BV

Sanofi Pasteur Holding SA

22

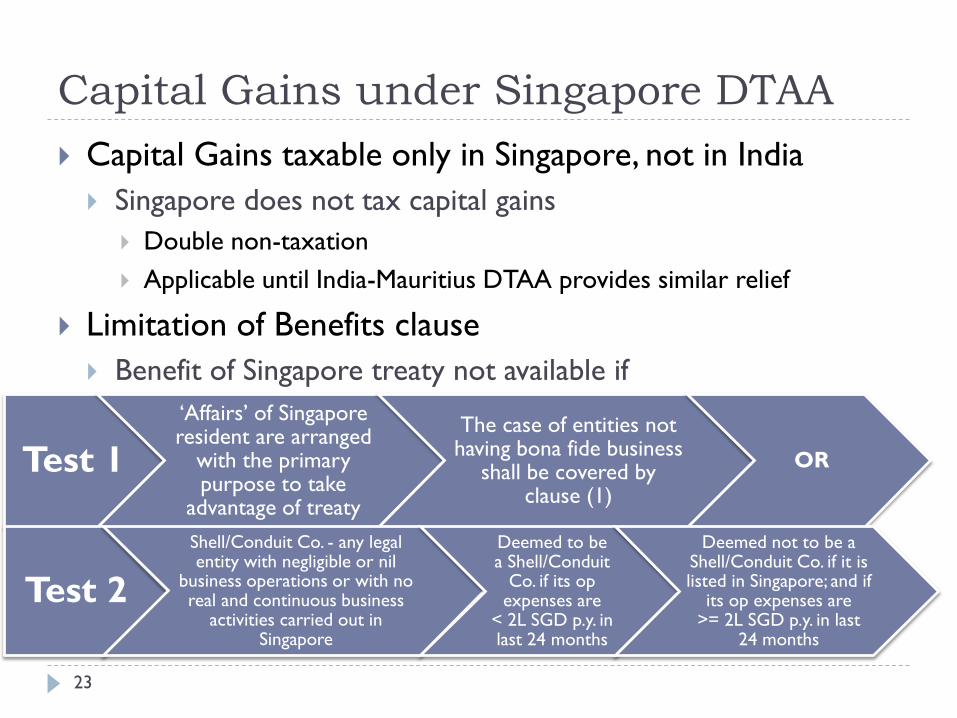

Capital Gains under Singapore DTAA

Capital Gains taxable only in Singapore, not in India

Singapore does not tax capital gains

Double non-taxation

Applicable until India-Mauritius DTAA provides similar relief

Limitation of Benefits clause

Benefit of Singapore treaty not available if

Test 1

‘Affairs’ of Singapore resident are arranged

with the primary purpose to take

advantage of treaty

The case of entities not having bona fide business

shall be covered by clause (1)

OR

Test 2

Shell/Conduit Co. - any legal entity with negligible or nil

business operations or with no real and continuous business

activities carried out in Singapore

Deemed to be a Shell/Conduit

Co. if its op expenses are

< 2L SGD p.y. in last 24 months

Deemed not to be a Shell/Conduit Co. if it is listed in Singapore; and if

its op expenses are >= 2L SGD p.y. in last

24 months

23

Capital Gains under Cyprus DTAA

24

Similar benefits on capital gains as India-Mauritius DTAA.

No tax payable in India on sale of shares in an Indian company.

CBDT has notified Cyprus as “Notified Jurisdictional Area” u/s. 94A from 1/11/2013

All parties to transactions with a person in Cyprus shall be treated as AEs and TP provisions will apply. Additional documentation to be maintained.

Any payment on which tax is deductible at source and made to a person located in Cyprus, will be liable for deduction of tax at source as per the rates under the Act or 30%, whichever is higher.

Impact on capital gains?

Sec 94A does not deny treaty benefits

Deduction at higher rate only on ‘sum chargeable to tax’

As no tax on capital gains, 30% rate not applicable

However, transaction will be scrutinised thoroughly

Capital Gains under Other DTAAs

25

UK & USA DTAAs

Taxable in both countries as per domestic law

Netherlands DTAA

Gains from shares taxable only in Netherlands

If Dutch company holds at least 10% of Indian Co. gains taxable

in India

Only if sale happens to Indian Resident

If sale happens to NR, then gain taxable only in Netherlands

Gain taxable only in Netherlands if realised in course of

corporate organisation, reorganisation, amalgamation, division,

etc. and buyer or seller owns at least 10% of the other co.’s

capital

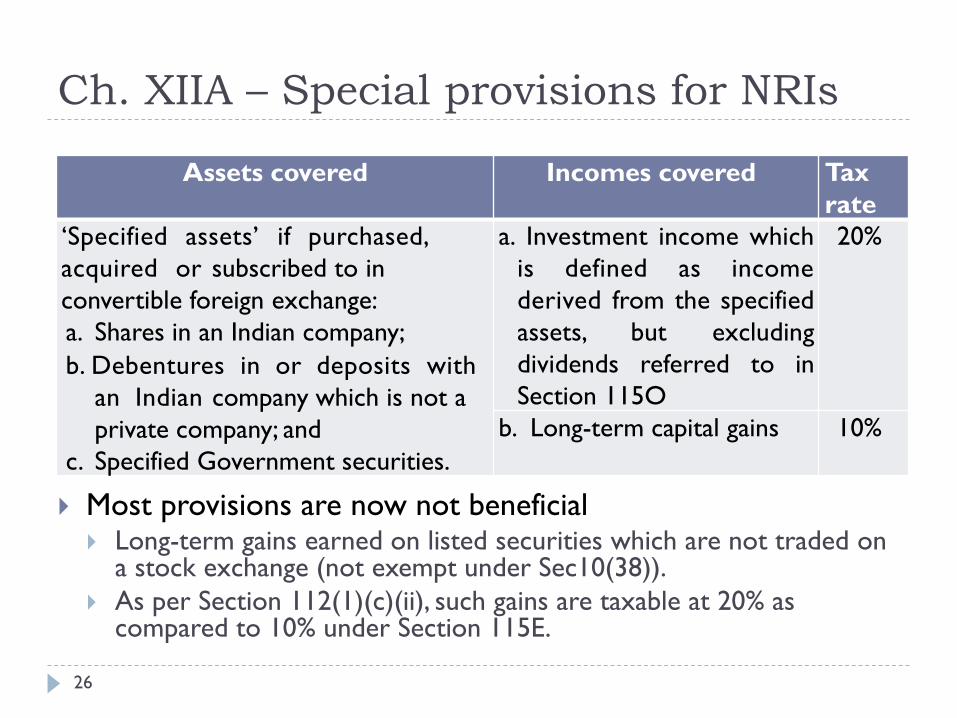

Ch. XIIA – Special provisions for NRIs

Assets covered Incomes covered Tax

rate

‘Specified assets’ if purchased,

acquired or subscribed to in

convertible foreign exchange:

a. Shares in an Indian company;

b. Debentures in or deposits with

an Indian company which is not a

private company; and

c. Specified Government securities.

a. Investment income which

is defined as income

derived from the specified

assets, but excluding

dividends referred to in

Section 115O

20%

b. Long-term capital gains 10%

Most provisions are now not beneficial Long-term gains earned on listed securities which are not traded on

a stock exchange (not exempt under Sec10(38)).

As per Section 112(1)(c)(ii), such gains are taxable at 20% as compared to 10% under Section 115E.

26

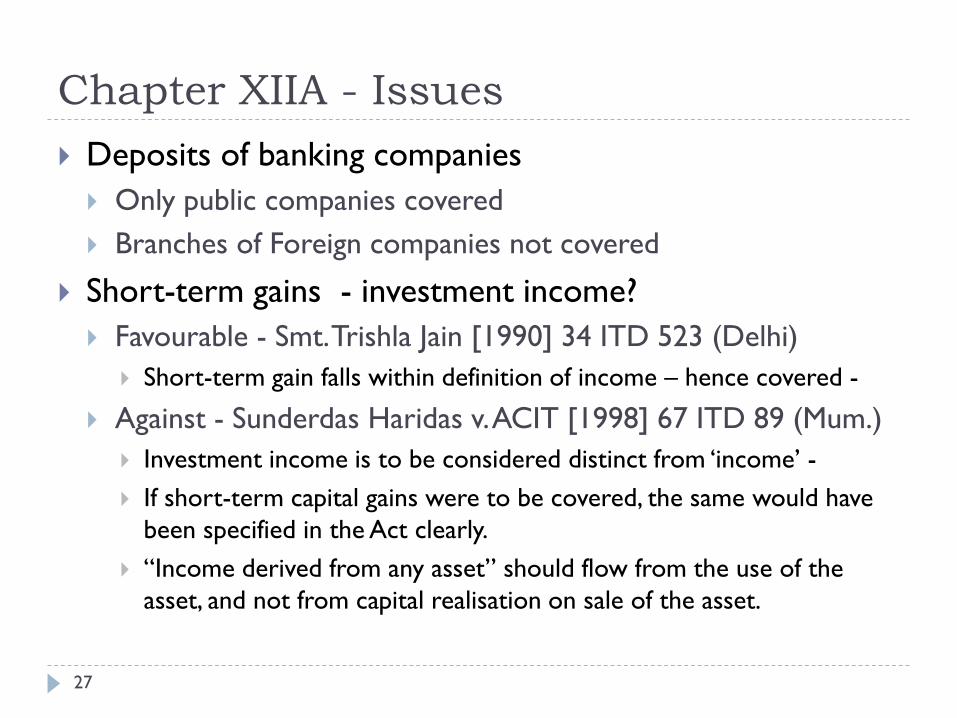

Chapter XIIA - Issues

Deposits of banking companies

Only public companies covered

Branches of Foreign companies not covered

Short-term gains - investment income?

Favourable - Smt. Trishla Jain [1990] 34 ITD 523 (Delhi)

Short-term gain falls within definition of income – hence covered -

Against - Sunderdas Haridas v. ACIT [1998] 67 ITD 89 (Mum.)

Investment income is to be considered distinct from ‘income’ -

If short-term capital gains were to be covered, the same would have

been specified in the Act clearly.

“Income derived from any asset” should flow from the use of the

asset, and not from capital realisation on sale of the asset.

27

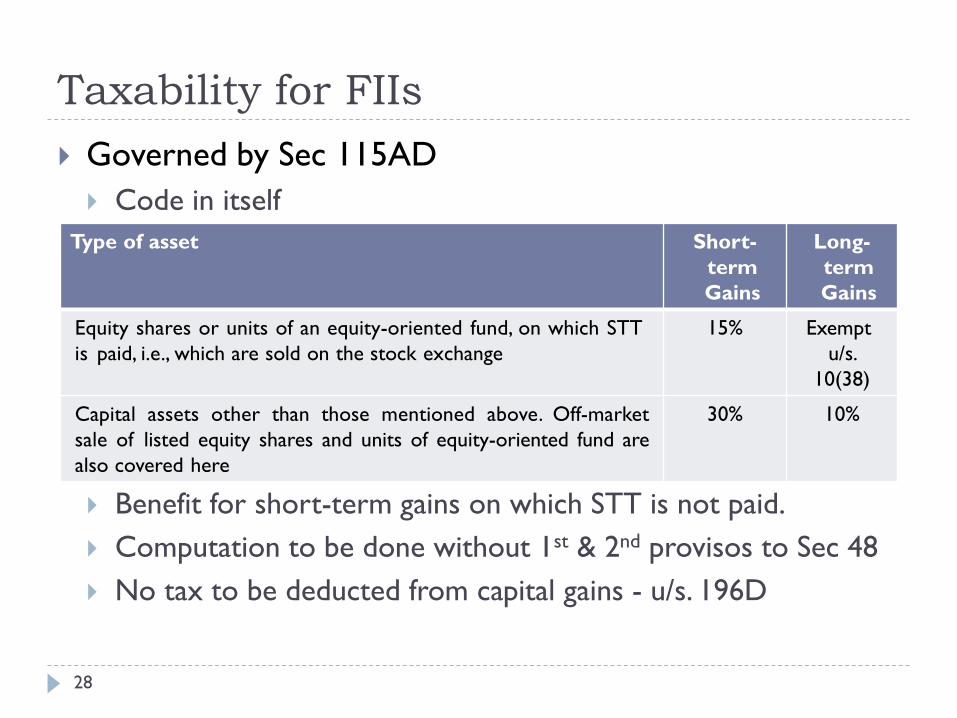

Taxability for FIIs

Type of asset Short-

term

Gains

Long-

term

Gains

Equity shares or units of an equity-oriented fund, on which STT

is paid, i.e., which are sold on the stock exchange

15% Exempt

u/s.

10(38)

Capital assets other than those mentioned above. Off-market

sale of listed equity shares and units of equity-oriented fund are

also covered here

30% 10%

Governed by Sec 115AD

Code in itself

Benefit for short-term gains on which STT is not paid.

Computation to be done without 1st & 2nd provisos to Sec 48

No tax to be deducted from capital gains - u/s. 196D

28

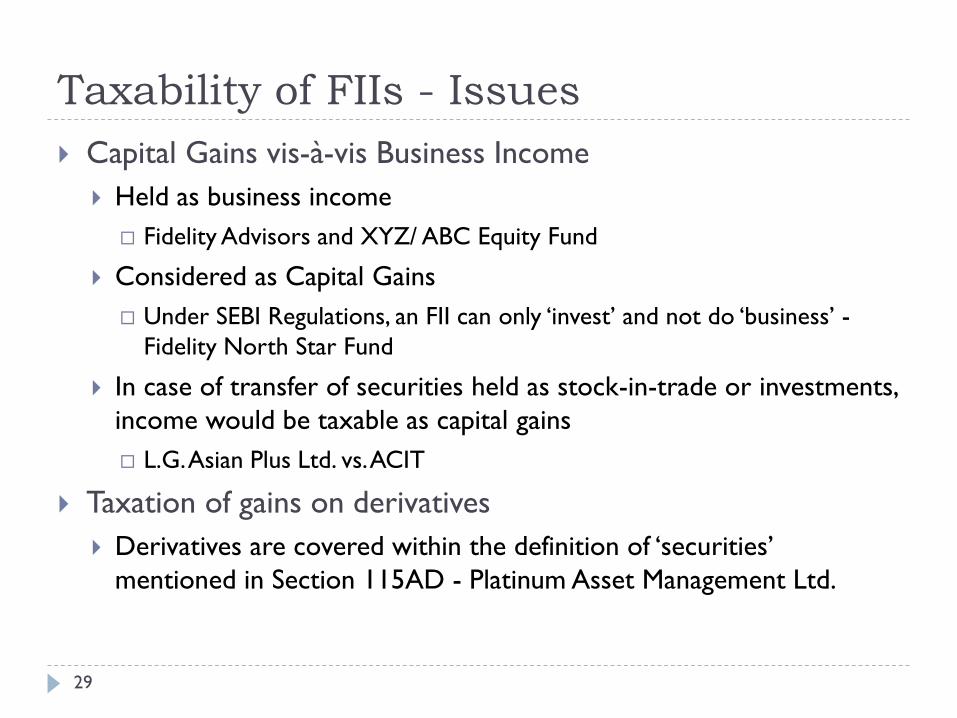

Taxability of FIIs - Issues

Capital Gains vis-à-vis Business Income

Held as business income

Fidelity Advisors and XYZ/ ABC Equity Fund

Considered as Capital Gains

Under SEBI Regulations, an FII can only ‘invest’ and not do ‘business’ -

Fidelity North Star Fund

In case of transfer of securities held as stock-in-trade or investments,

income would be taxable as capital gains

L.G. Asian Plus Ltd. vs. ACIT

Taxation of gains on derivatives

Derivatives are covered within the definition of ‘securities’

mentioned in Section 115AD - Platinum Asset Management Ltd.

29

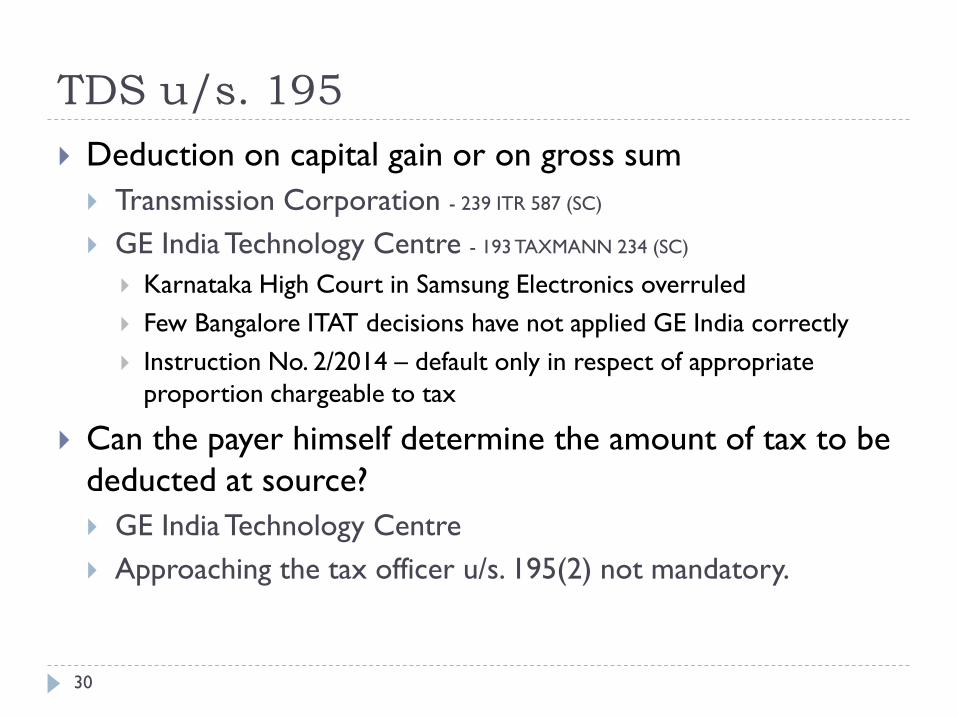

TDS u/s. 195

Deduction on capital gain or on gross sum

Transmission Corporation - 239 ITR 587 (SC)

GE India Technology Centre - 193 TAXMANN 234 (SC)

Karnataka High Court in Samsung Electronics overruled

Few Bangalore ITAT decisions have not applied GE India correctly

Instruction No. 2/2014 – default only in respect of appropriate

proportion chargeable to tax

Can the payer himself determine the amount of tax to be

deducted at source?

GE India Technology Centre

Approaching the tax officer u/s. 195(2) not mandatory.

30

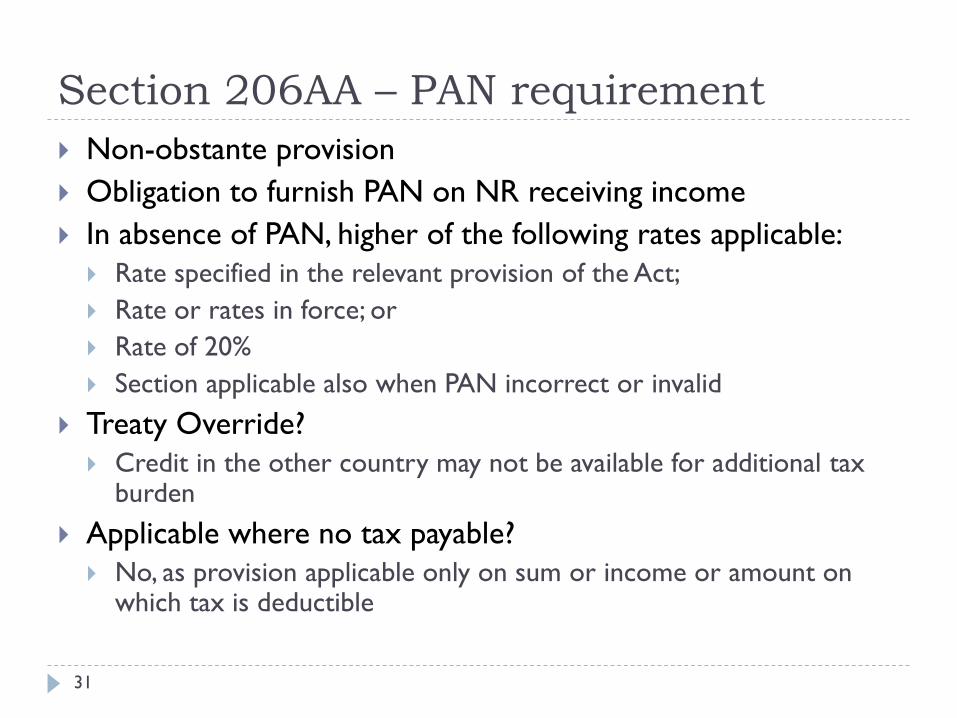

Section 206AA – PAN requirement

31

Non-obstante provision

Obligation to furnish PAN on NR receiving income

In absence of PAN, higher of the following rates applicable:

Rate specified in the relevant provision of the Act;

Rate or rates in force; or

Rate of 20%

Section applicable also when PAN incorrect or invalid

Treaty Override?

Credit in the other country may not be available for additional tax burden

Applicable where no tax payable?

No, as provision applicable only on sum or income or amount on which tax is deductible

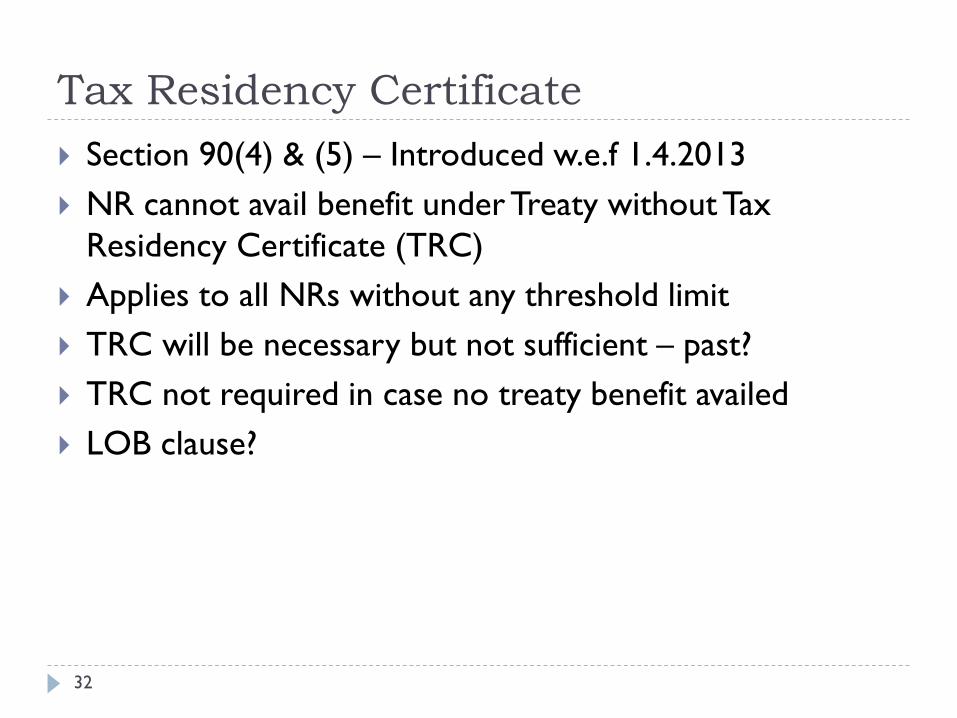

Tax Residency Certificate

32

Section 90(4) & (5) – Introduced w.e.f 1.4.2013

NR cannot avail benefit under Treaty without Tax

Residency Certificate (TRC)

Applies to all NRs without any threshold limit

TRC will be necessary but not sufficient – past?

TRC not required in case no treaty benefit availed

LOB clause?

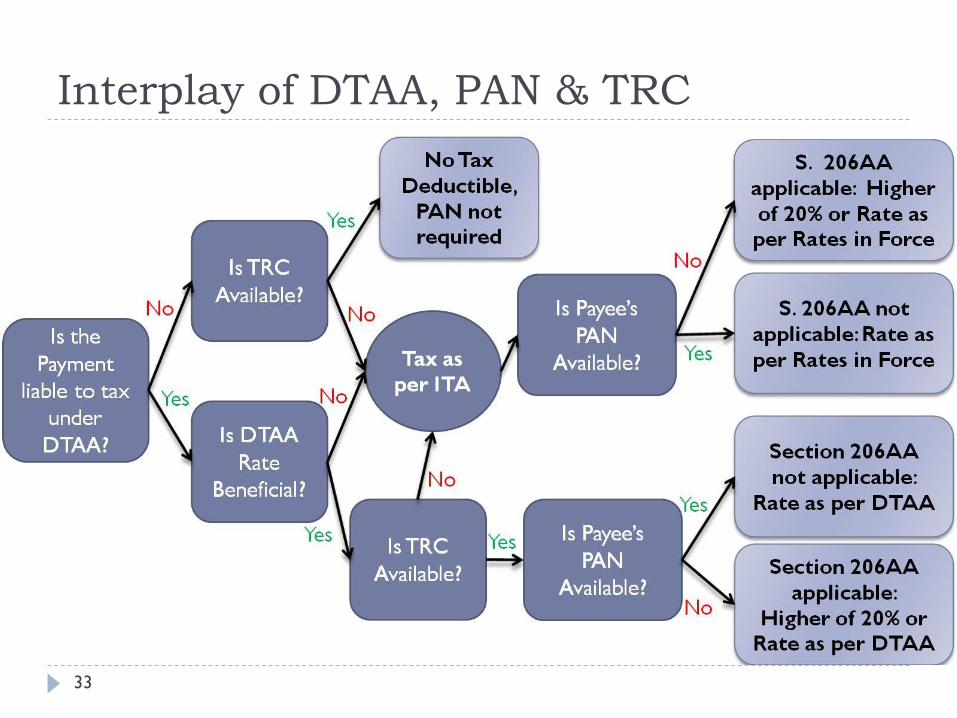

Interplay of DTAA, PAN & TRC

33

Thank you!

34

CA Rutvik Sanghvi

www.rashminsanghvi.com