Embed Size (px)

Citation preview

Bryanston Resources AG * Bahnhofsplatz * 6300 Zug * Switzerland

Selected future demand trends as stimulation to mining investments MINEX Astana conference

March 2015

Draft – For discussion only

1 Copyright: Bryanston

Draft – For discussion only

China is a key player in global demand for major Kazakhstan commodities

Export of Kazakhstan commodities

15,6

18,9

21,3

44,7

29,0

Aluminium

Iron ore

Thermal coal incl. lignite

Zinc

Ferroalloys 136,9

Refined copper and copper alloys 169,0

Copper ore

Top positions of Kazakhstan commodities export (metals & minerals), Dec 2014, Mio. USD

Structure of the global demand

Source: Custom statistics Kazakhstan, Department of Industry and Science Australia, US Geological survey, Bryanston research

48%

66%

44%

49%

66%

72%

46%

34%

28%

54%

52%

51%

34%

56%

China Rest of the world

2014, estimation

2 Copyright: Bryanston

Draft – For discussion only

Traditional China commodity demand challenged by growth slowdown and industry restructuring

Recent trends in the China economy Internal issues in Chinese heavy industries

7,3

7,3

7,57,47,7

13,3

16,817,7

13,517,6

4,0

7,9

17,3

20,3

12,3

-0,8

3,9

7,3

20

10

25

5

15

0

4Q 2014 1Q 2014 2Q 2014 4Q 2013 3Q 2014

1,6

Real GDP Fixed assets investments

Real estate, dwellings Cement production Profits

Utilization

Pollution

Energy demand

GDP growth rate is stable and relatively high, but investments and construction (with related

industries, i.e. cement) decelerated recently

Growth rate,%, year-to-year

Traditional resource consuming industries, such as steel production, coal generation, etc. are under restructuring

& consolidation now

Source: Australian Government, Department of Industry and Science, International steel Association, Bryanston research

• >40% steel plants are making losses • Average steel companies having up to

70% debt ratio

• Utilization rate in steel industry is ~4% lower than global

• ~180-240 Mt of idled steel capacities

• More than 70% of steel plants’ sewage facilities in North China do not meet the national standard

• Energy consumption gap between advanced and outdated capacity, is up to 300 kg/t equalized standard coal

Steel industry examples

3 Copyright: Bryanston

Draft – For discussion only

As a result, China raw materials consumption will shift to more sophisticated “China 2.0“ commodities

Construction Machinery Automotive Aviation High tech industrial

• Iron ore

• Coal

• Chrome

• Titan

• Tungsten

• Nickel

• Aluminum

• Titan

• Gallium

• Germanium

• REE1

1. REE – Rare Earth Elements Source: Bryanston

• Iron ore

• Aluminum

• Platinum

Driving sector

Com-modities

Stages of China

economy develop-

ment

4 Copyright: Bryanston

Draft – For discussion only

Commodity Food/ packaging

Steel/ Construction

Other processing/ Electricity

High tech industrial

Electronics/ other high

tech

Mercury

PGM

Beryllium

Molybden

Vanadium

Indium

Tungsten

Lead

Tin

Cobalt

Germanium

Gallium

Arsenic

REE

Commodity Food/ packaging

Steel/ Construction

Other processing/ Electricity

High tech industrial

Electronics/ other high

tech

Alumina

Iron ore

Magnesium

Zinc

Coal

Silicon

Manganese

Chrome

Copper

Nickel

Uranium

Titanium

Bismuth

Silver

Source: Bryanston Research

Main application in “1.0 industries”

China 1.0 China 2.0 China 1.0 China 2.0

Deep industry demand analysis can discern “China 1.0” and “China 2.0” commodities

Secondary application in “1.0 industries”

Main application in “2.0 industries”

Secondary application in “2.0 industries”

Special steels production: wear-

resistant, stainless, etc.

Aviation and space industry consumption

Indicative

Significant resource base in Kazakhstan

5 Copyright: Bryanston

Draft – For discussion only

Kazakhstan holds significant resources of chrome, copper, and other commodities with “China 2.0” implications

Commodity Global supply/demand forecast Kazakhstan resources,

Mt ore

Share in world resources, %1

Chrome • Demand is to grow together with

global stainless steel demand, oversupply is to move into balance by 2018

369 10%

Copper • China is the biggest consumer of

copper, surplus on the market now with deficit re-emerging from 2016

38 5%

Manganese • Demand is to grow driven by both

ordinary and special steels production in China, oversupply is to move into balance by 2019

688 5%

Tungsten • Demand is to grow driven by China • Supply scarcity due to China limits

on export (~60% of world reserves) 2 ~0.5%

Titanium • Titan demand is forecasted to grow

faster than supply with China/Pacific markets being the main drivers

24 ~0.2%

Tin • Demand is to grow fuelled by

growth in electronics • Supply is to decrease from 2017

0.07 <0.01%

1) Share of Kazakhstan in pure metal content Source: State mining exploration program of Kazakhstan Republic for 2015-2019, US Geological Survey, Bryanston Research

Ti Cr

Mn Mn Cu Cu

W

W W

Cu

Ti

W Tungsten

Ti Titanium

Mn Manganese

Cu Copper

Chrome

“China 2.0” on Kazakhstan map

Cr

Tin

Indicative

Cu

Cu Cu

Sn

Sn

Cr

Cr

6 Copyright: Bryanston

Draft – For discussion only

Kazakhstan conducted several initiatives on investment climate recently, as next iteration to previous program

State program for development of Kazakhstan Republic for 2015-2019 Recent initiatives on investment climate

Tax initiatives: • 100% of corporate profit tax exemption for all categories of investment projects for 10 years

• No land tax for investment project sites • Zero rate of property tax for up to 8 years term

Institutional initiatives: • Establishment of one stop shop for foreign investors (Kaznex)

• Development of Special Economic Zones and industrial clusters (Saryarka zone for metallurgy)

• Moratorium for changes in tax, ecology, land and other legislation for investment contracts signed

Initiatives for foreign employees: • Non-visa regime for investors from developed countries • No regulation for foreign labor while investment project is undergo

Priority sectors (80% of investments will be directed to):

Main goals: • Stimulation of economy sustainable development

• Modernization of industry enterprises

• Increase of competitiveness

Expected total financing: ~ 6 600 bln. KZT (80% is non-state investments)

Construction materials

Metallurgy

Food industry

Machinery

Chemistry

Oil processing

Source: Baiterek National Holding, Bryanston Research

7 Copyright: Bryanston

Draft – For discussion only

Bryanston is active in principal investments, advisory and consulting in natural resources

Source: Bryanston

Bryanston Capital

Bryanston Advisory

Bryanston Consulting

Ø Principal investments in raw materials

Ø Principal investments in mining tech-nology / services

Ø Active portfolio management

Ø Fund management

Ø Opportunity origination and due diligence

Ø Financial Advisory / fund raising

Ø Value-in use and commercial excellence

Ø Strategy and operations

Ø Transformation & turnaround

Ferrous Coal Minerals Agriculture Non –

ferrous

BRYANSTON HOLDING

Oil & Gas

8 Copyright: Bryanston

Draft – For discussion only

We have a global presence and can draw on international experience and best practice benchmarks

Bryanston is the fastest growing firm in its space – app. 100 employees are serving clients globally

Opening 2015 Recent projects

Existing offices

Western Africa

North America

South America

Southern Africa

ANZ

South East Asia

Europe

Asia

London

Zug

Tel Aviv

Lagos

Johannesburg

Shanghai

Moscow

Rio de Janeiro

New Delhi

Perth

Munich

Singapore

Toronto

Harare

9 Copyright: Bryanston

Draft – For discussion only

… Coking Coal Steel

We regularly conduct bottom-up market balance, trade flow as well as price & cost analyses for key commodities

Ø Seaborne price forecast in 5 years

Ø Regional price forecast in 5 years given the transport cost

Ø Supply-demand impact on price

Ø Key cost components in operations

Ø Cash cost curves analytics

Ø Comparison with cash cost curves for new projects

Ø Global supply-demand ba-lance development in 5 years

Ø Key global & regional trends in the selected countries

Ø New projects in supply and demand

Ø Overview of key exporting and importing countries

Ø Analysis of exported and imported volumes

Ø Supply-demand balance impact on trade flows

Trade flows Price forecast

Bryanston global commodity competence

center

Cost analysis

Thermal Coal

Supply-demand + + +

36Copyright: Bryanston

China supply & demand balance: China imports will further increase driven by demand from the regions

Thermal coal demand and change of shares

2018e2017e2016e2015e2014e2013e

Local demandLocal supply

Thermal coal supply and demand balance

Supply & demand difference

- x - x - x - x - x

x

- x

In Mt

Source: SXcoal; WorldBank; Bryanston Research; JP Morgan report 2012

Demand potential for Russian TC import exists in coastal provinces and northeast China

In Mt

2013 2018e2015e 2017e2014e 2016e

ChemicalCementPower

MetallurgicalCivil useTransportation

Industrial BoilerOthers

.

40Copyright: Bryanston

Country profile: Germany Total coal-fired PPs capacity reach X GW

Sources: Bundesnetzagentur; Bryanston Research, Bryanston global thermal coal production and consumption data base

Capacities are split between lignite and steam coal almost equally, each accounting for X GW

PPs are usually situated near local coal deposits to leverage the local supply

# Plant Capacity [GW]1 Niederaußem2 KW Jänschwalde3 Boxberg4 Neurath5 Scholven6 GKM 7 Schwarze Pumpe8 Frimmersdorf9 KW Voerde10 Staudinger11 BoA 312 BoA 213 Heilbronn14 Schkopau15 Lippendorf-116 Lippendorf-217 Heyden18 KW Herne

Other on steam coalOther on lignite

Major coal-fired power plants in Germany

5

2

311

8

6

7

12

1

10

9

18

Ruhr deposit

13

14 15

16

17

4

Steam coal PP

Lignite PP

Hard

Brown

GW

34Copyright: Bryanston

Increase in capacity, driven by Turkey, will lead to increase of import of thermal coal in Europe

New

2012

Phase-out

- X %

2018

Retirements outweigh new capacities in EU, but is balanced by Turkey race for power Coal demand supply balance in 2012–18

Thermal coal-fired PPs capacity changes (2012-2018) [GW]

• Turkey has x GW pipeline for new coal-fired PPs that may be challenged by regulation if country adopts EU environmental regulations

• Poland will undergo replacement program building more efficient PPs, while largely phasing-out old ones

• Germany will import more steam coal, since most new PPs are efficient steam-coal ones

• Industrial Emissions Directive is likely to trigger retirements of some coal-fired power plants, especially in the leading coal-consuming countries

Thermal coal demand-supply forecast in OECD EU [Mt.]

Source: IEA; Annual reports of European utilities companies; Bryanston global thermal coal production and consumption data base and research

2012 2018

34Copyright: Bryanston

China Import: China became a net importer in 2009 and will approach pure import status in the future

OthersColombiaCanada

MongoliaUSA

RussiaS. Africa

IndonesiaAustralia

1009

38

+ x %

131211

51

Imports of thermal coal in China by source [Mt]

Source: SXCoal, National bureau of statistics, Bryanston Research

Note: Lignite is not included in the thermal coal imports

Major importing provinces in China (>1Mt in 2012)

OthersTaiwanS.KoreaJapan

- x %

1312111009

Exports of thermal coal in China by destination [Mt]

TC Import routes TC Export routes

10 Copyright: Bryanston

Draft – For discussion only

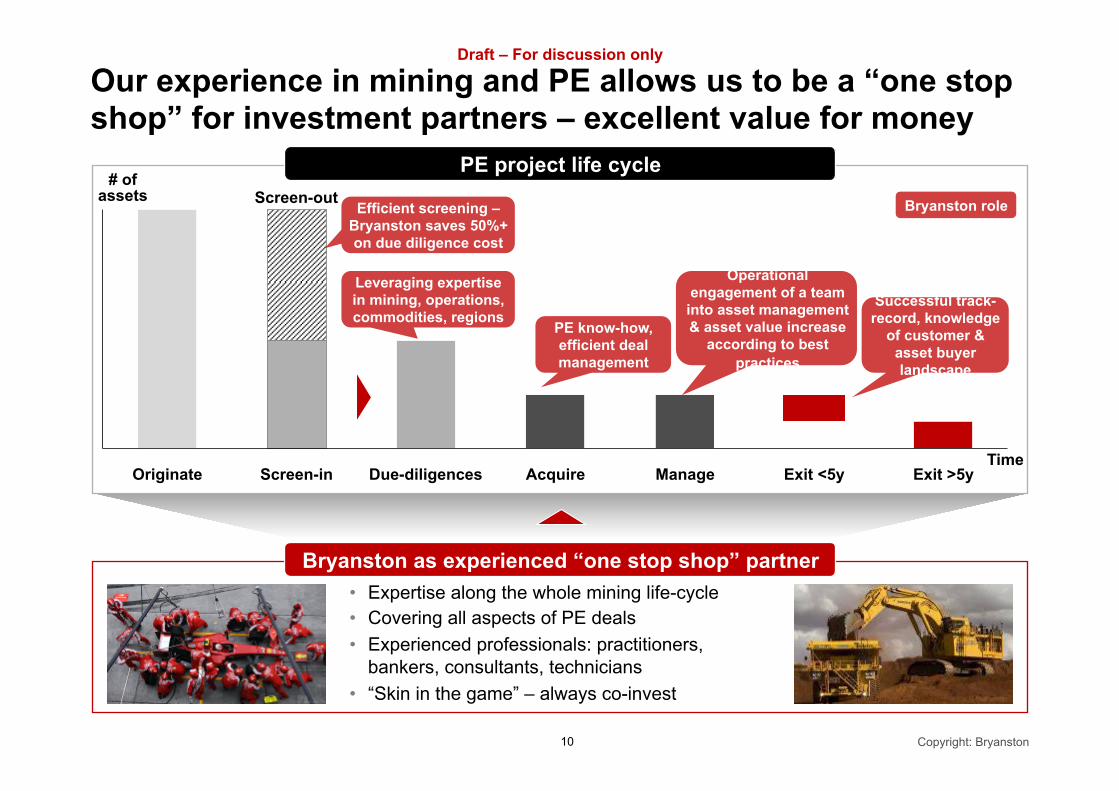

Our experience in mining and PE allows us to be a “one stop shop” for investment partners – excellent value for money

• Expertise along the whole mining life-cycle • Covering all aspects of PE deals • Experienced professionals: practitioners,

bankers, consultants, technicians • “Skin in the game” – always co-invest

PE project life cycle

Exit >5y Manage Exit <5y Acquire Due-diligences Screen-in

Screen-out

Originate

# of assets

Bryanston as experienced “one stop shop” partner

Time

Leveraging expertise in mining, operations, commodities, regions

PE know-how, efficient deal management

Efficient screening – Bryanston saves 50%+ on due diligence cost

Successful track-record, knowledge

of customer & asset buyer landscape

Operational engagement of a team

into asset management & asset value increase

according to best practices

Bryanston role