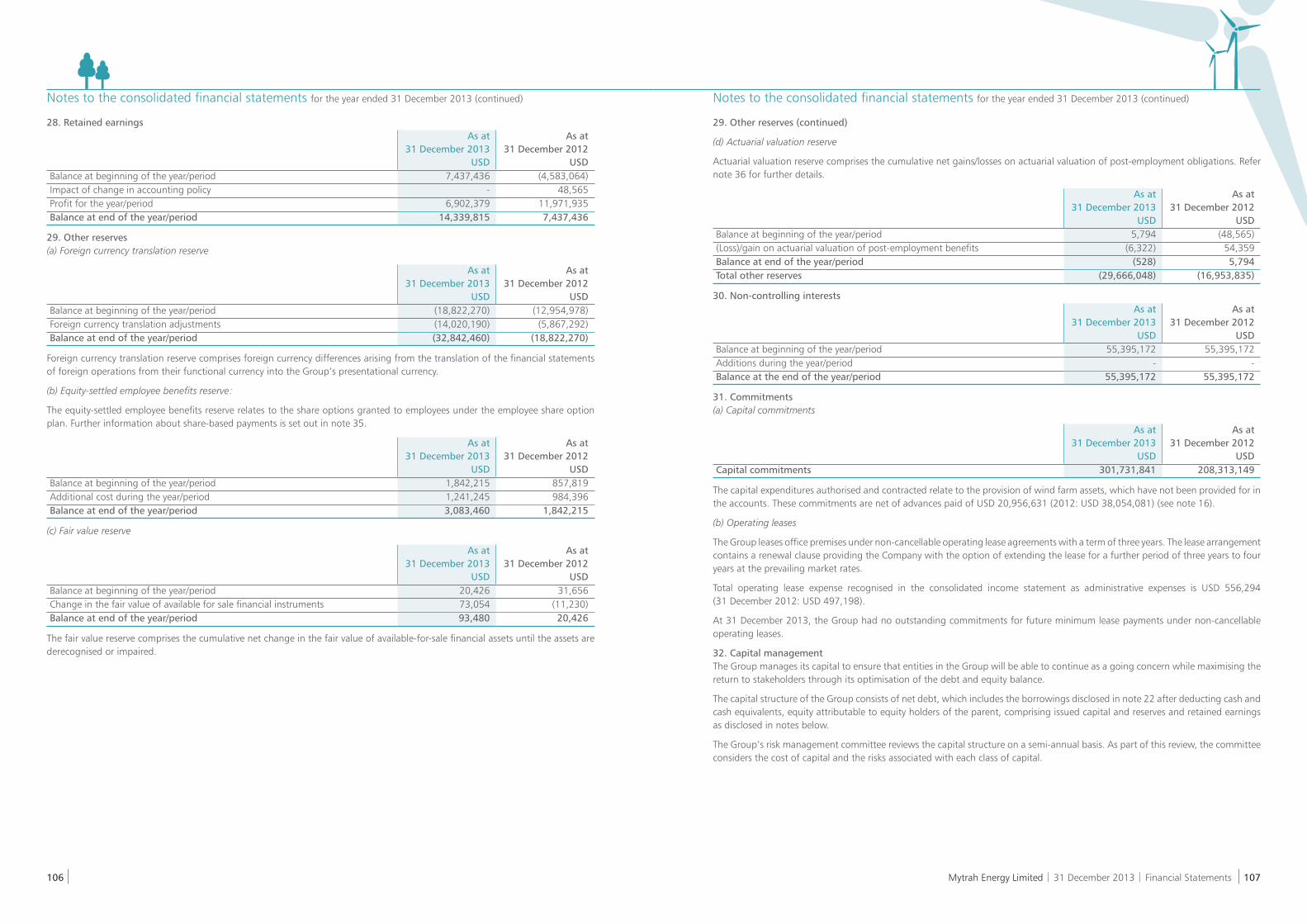

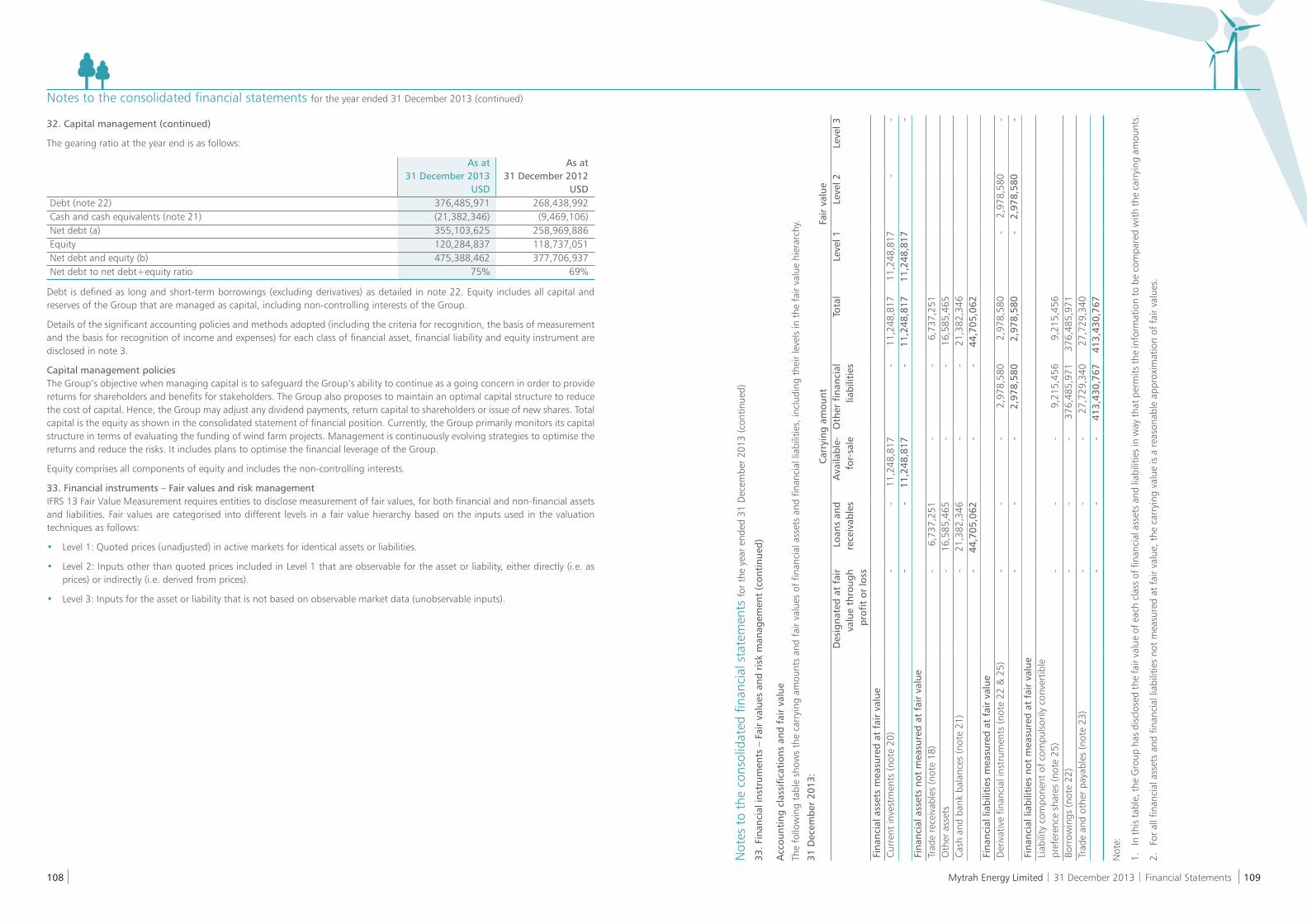

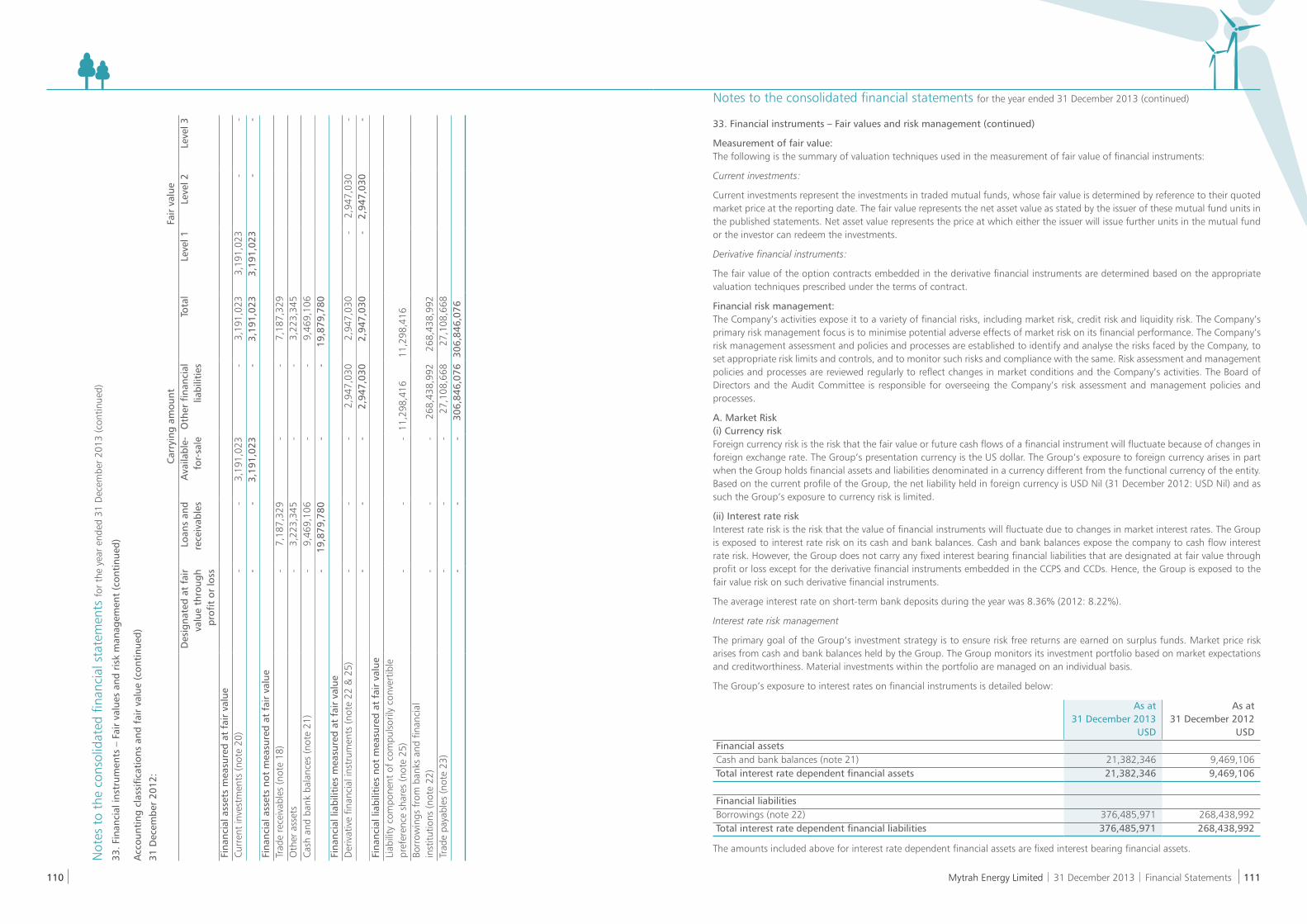

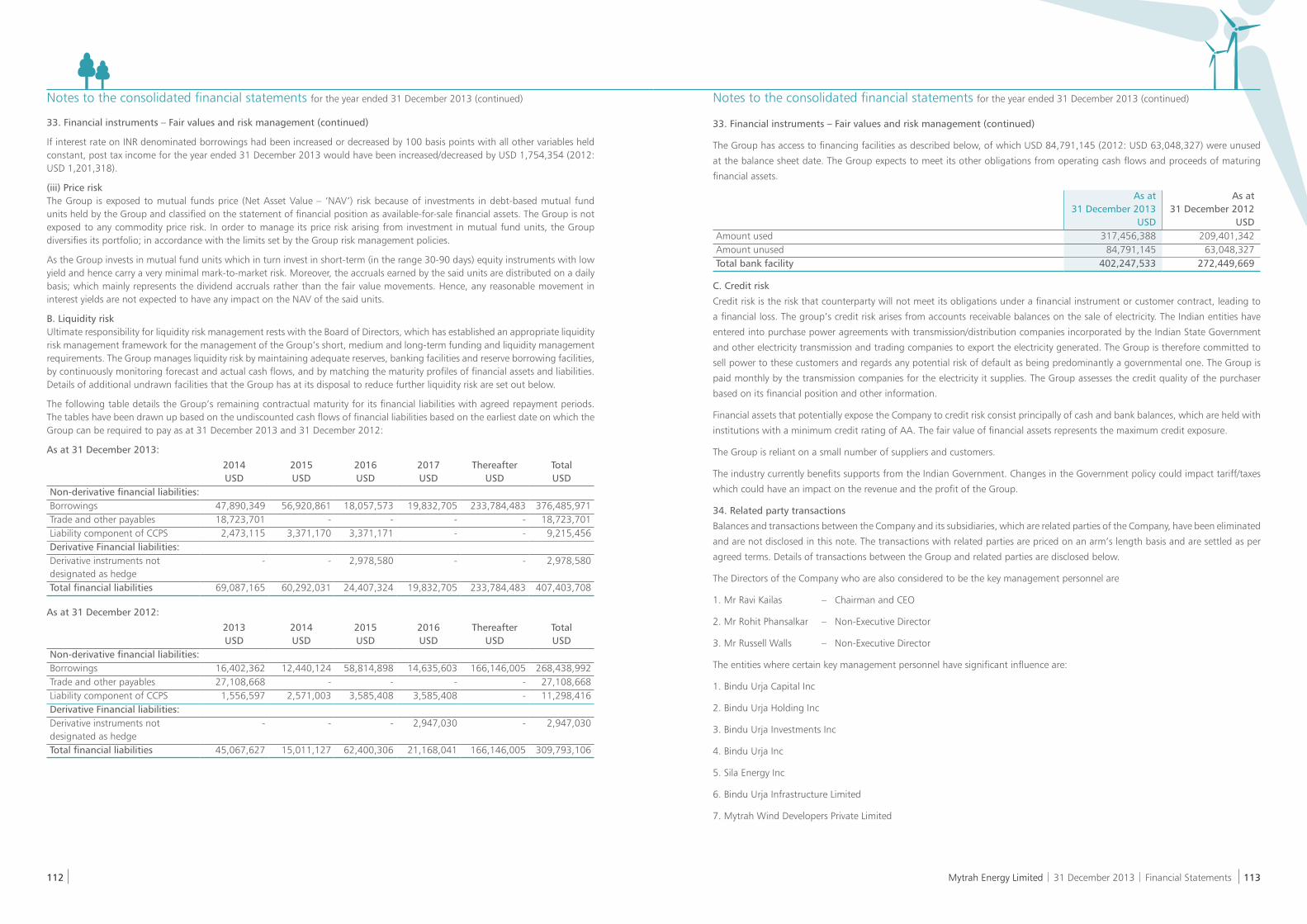

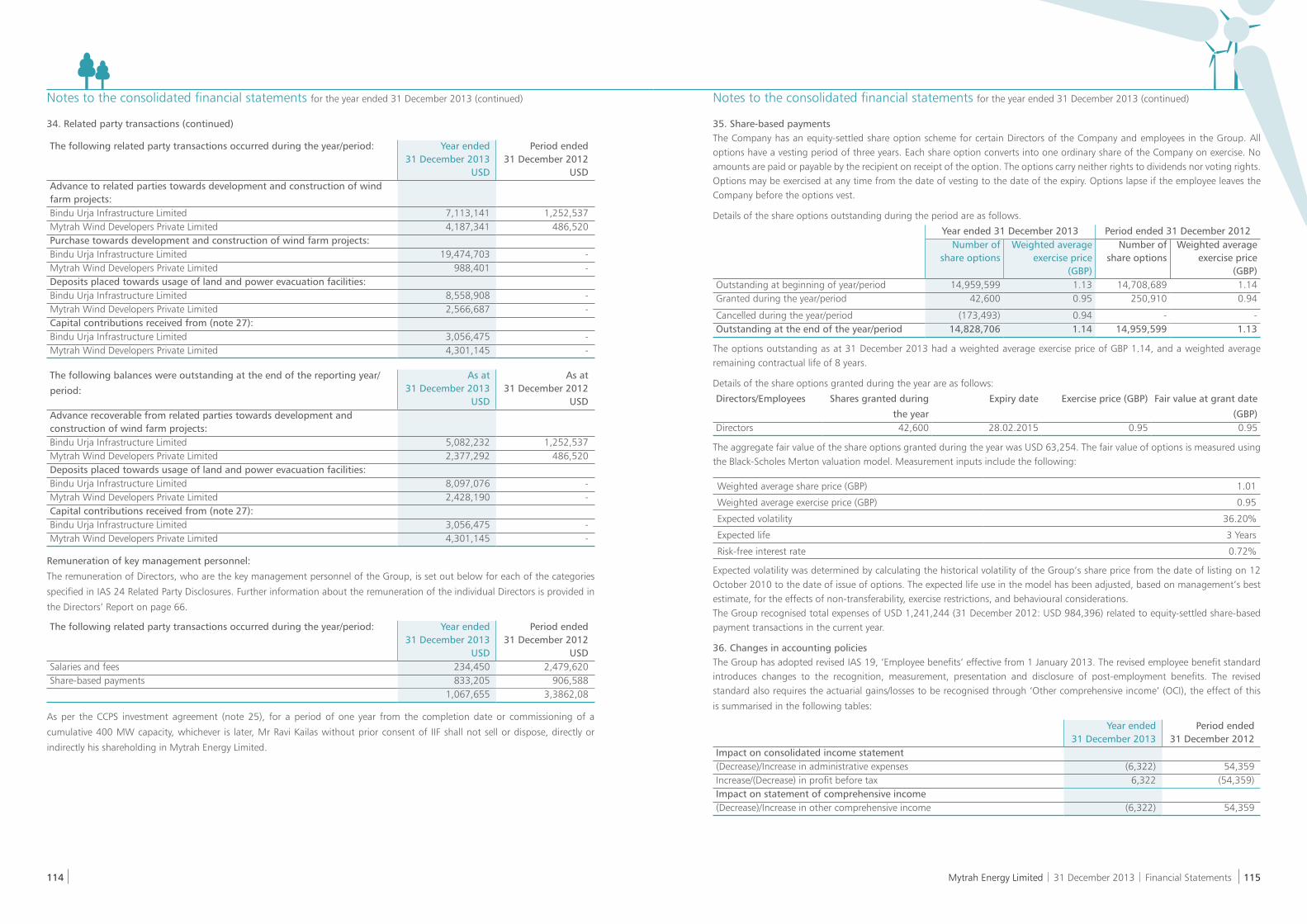

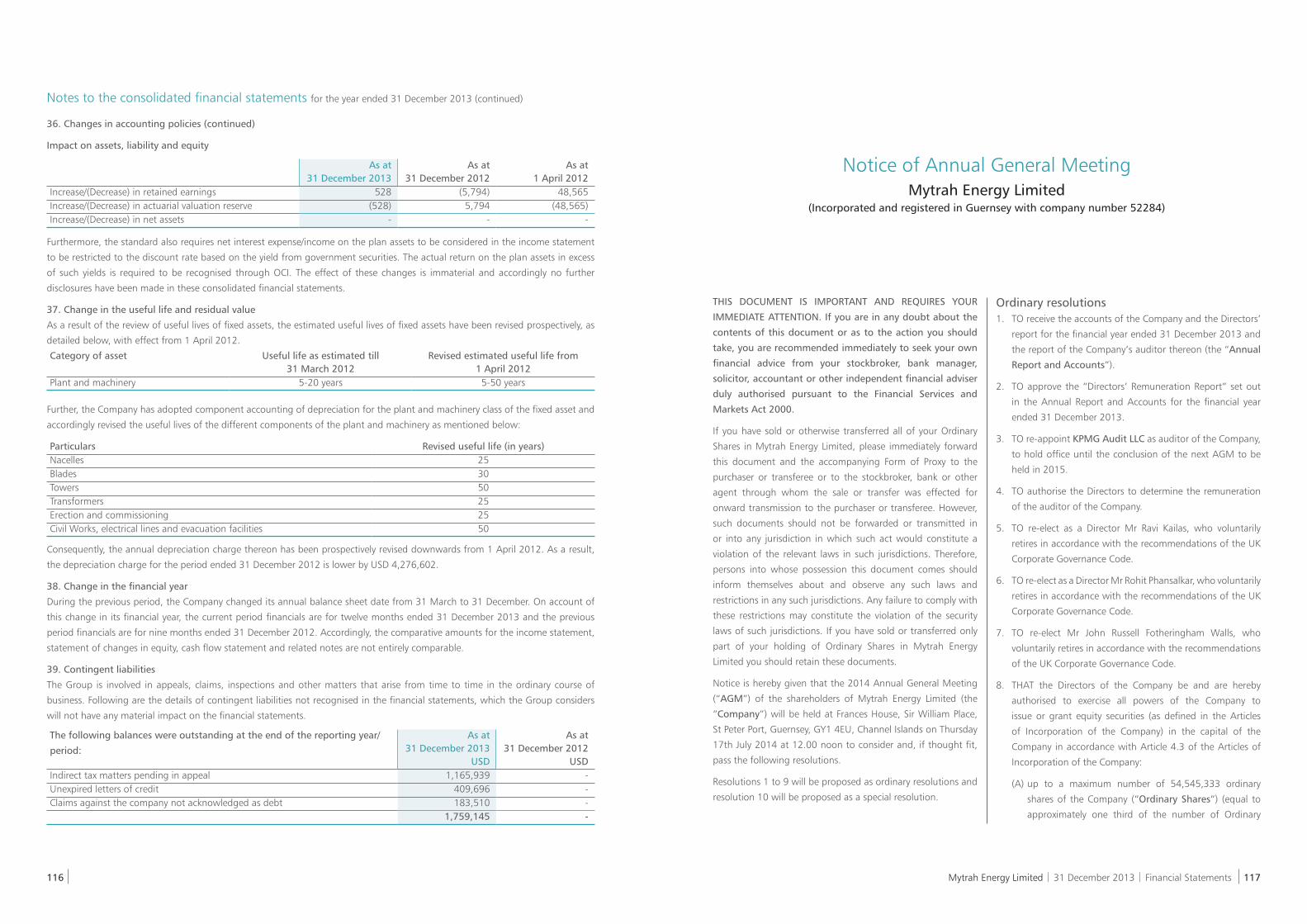

Embed Size (px)

Citation preview

Seizing the potential

Mytrah Energy Limited Annual report 2013

prin

t@pr

agat

i.com

Mytrah_CV_V1.indd 1 11/06/14 12:14 PM

Company Advisers ..................................................01Our Company .......................................................03Our Mission ..........................................................05Our Philosophy .....................................................06Our Core Values ....................................................07Overview ...............................................................08Current Operational Highlights ..............................09Our Performance ...................................................10Chairman and CEO’s Statement .............................12Financial Performance ...........................................21Q&A with CFO ......................................................27Company Structure ...............................................30Our Intellectual Property ........................................43What went right in 2013 .......................................47Human Capital ......................................................49

Greener Earth ........................................................53Sustainability Report ..............................................55Directors’ Biographies ...........................................60Directors’ Report ...................................................66Corporate Governance Report ...............................68Remuneration Report ............................................73Independent Auditor’s Report to the

members of Mytrah Energy Limited .......................77Consolidated Income Statement ............................78Consolidated Statement of Comprehensive Income 79Consolidated Statement of Financial Position .........80Consolidated Statement of Changes in Equity ........81Consolidated Statement of Cash Flows ..................82Notes to the Consolidated Financial Statements .....83

Contents

A PRODuCt

Mytrah_CV_V1.indd 2 11/06/14 12:14 PM

Company Advisers

Nominated and financial adviserInvestec Bank Plc

2 Gresham Street,

London EC2V 7QP

United Kingdom

Tel: +44 (0) 20 7597 4000

Joint brokersInvestec Bank plc

2 Gresham Street,

London EC2V 7QP

United Kingdom

Tel: +44 (0) 20 7597 4000

Mirabaud Securities LLP

33 Grosvenor Place,

London SW1X 7HY

United Kingdom

Tel: +44 (0) 20 7321 2508

LegalKing & Spadling International LLP

125 Old Broad Street,

London EC2N 1AR

United Kingdom

Tessa Laws

21 Arlington Street,

London SW1A 1RN

United Kingdom

RegistrarsComputershare Investor Services

(Guernsey) Limited

P.O. Box 393

Kingsway House,

Havilland Street,

St. Peter Port,

Guernsey,

GY1 3FN

Channel Islands

AuditorKPMG Audit LLC

Heritage Court,

41 Athol Street,

Douglas,

Isle of Man, IM99 1HN

Tel: +44 (0) 1624 681 000

Financial PRSt Brides Media & Finance Ltd

3 St. Michael’s Alley,

London

EC3V 9DS

Tel: +44 (0) 20 7236 1177

Mytrah_Col_01_68_V3.indd 1 12/06/14 9:55 AM

Our CompanyMytrah Energy Limited (MEL) is based in

Guernsey and is listed on the Alternate

Investment Market (AIM) Segment of

the London Stock Exchange.

Its wholly-owned subsidiary, Mytrah

Energy (India) Limited (MEIL), is one of

the largest wind-based Independent

Power Producers in India with an

operating portfolio of 507.85 MW of

wind energy assets spread over ten

projects across six states in India. All

projects are secured through long-term

Power Purchase Agreements, ensuring

sustainable generation of revenues and

profits for the next 25 years.

Over 500 MW commissioned & operational!

02 03 Mytrah Energy Limited | 31 December 2013 | Financial Statements

Our MissionMytrah will lead the world in seizing renewables opportunities.

Mytrah Energy Limited | 31 December 2013 | Financial Statements 04 05

Our Core ValuesMytrah believes that the Company’s values drive its valuation. Integrity, Creativity,

Excellence, Respect for Individuals and Social Responsibility are the five core values

that engineer Mytrah’s DNA.

IntegrityAll our actions are governed by the

principles of ethics, honesty and

transparency.

CreativityWe foster a spirit of innovation and

entrepreneurship.

ExcellenceWe deliver the best-in-class results, as

we excel in everything we do.

Respect for individualsWe treat others the way we expect to

be treated – with respect.

Social responsibilityWe will be the catalysts of positive

change in the society.

Our PhilosophyBeing an inspiring solution, we are visionary, change catalysts, perceptive to the

needs of others, open, innovative and giving.

VisionaryMytrah was founded on the vision of

wind energy’s huge potential to be the

cheapest, most easily accessible way to

supply power to India.

Change catalystsAt Mytrah, we believe that every

person has the ability to create positive

change in the world. Accordingly, we’re

committed to using renewable energy

to achieve a clean-green world.

Perceptive to the needs of othersSensing India’s growing demand-supply

power gap, Mytrah saw wind energy as

a means to address this gap.

OpenMytrah’s culture encourages diversity

and inclusion while practicing

transparent and ethical corporate

governance.

InnovativeMytrah was a pioneer of the wind

Independent Power Producer (IPP)

model in India.

GivingAt Mytrah, we believe that private

wealth should be used for public good.

06 07 Mytrah Energy Limited | 31 December 2013 | Financial Statements

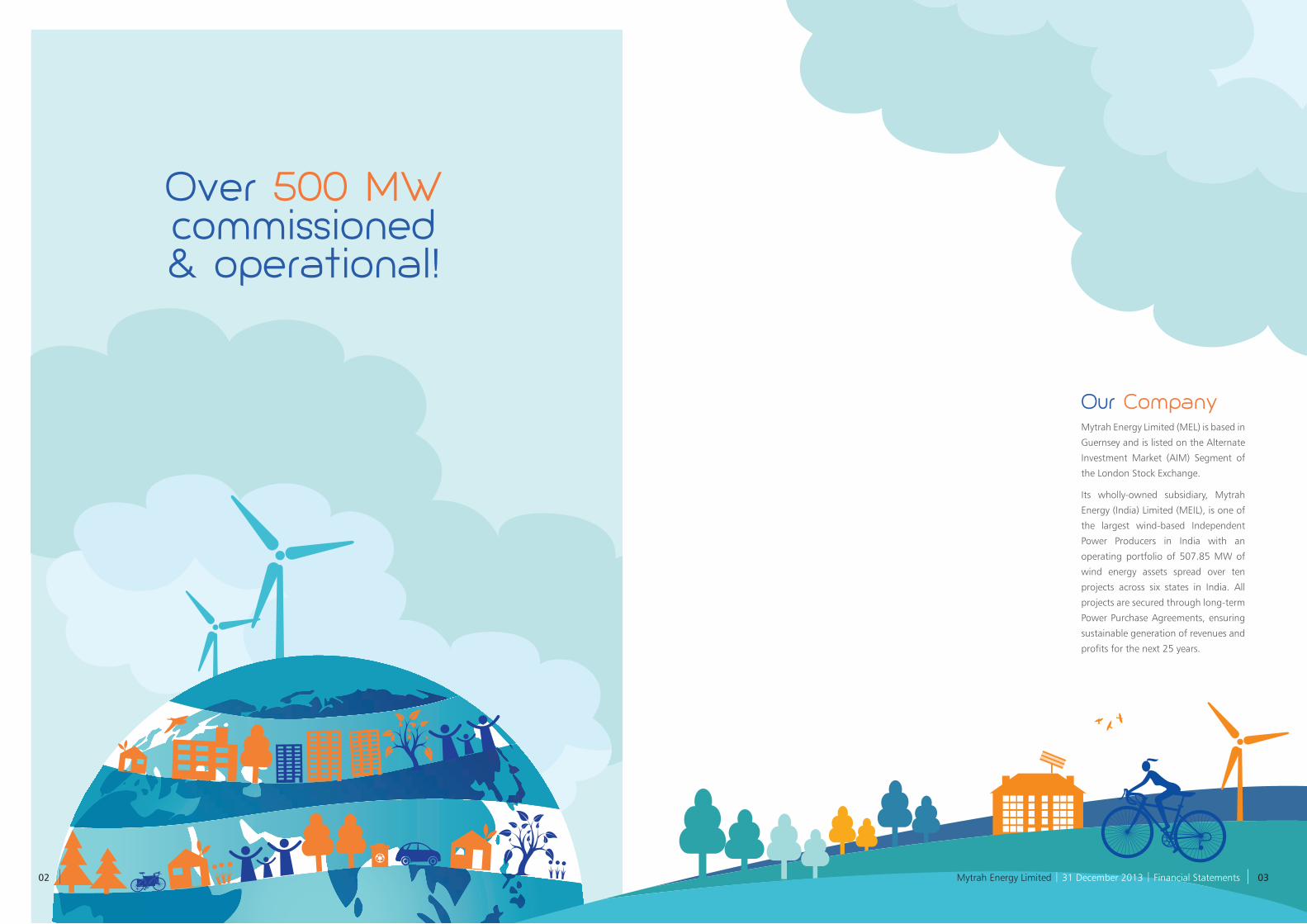

Burgula 37.4 MW operational

Savalsang 70.55 MW (out of 100.3 MW)

operational

Vagarai 90 MW (out of 100.5 MW)

operational

A total operating portfolio of

507.85 MW

Strong receivable

position with no

significant payment

delays

Current Operational Highlights

Performance of

operational projects

slightly ahead of

expectations

Generation Based

Incentive (‘GBI’)

Scheme reinstated with

improved terms

In the process of

securing in-principal

sanction of approximately

USD 200 m of senior

debt for upcoming projects

of 227 MW

Average age of trade

receivables

50 days

EBITDA of USD

46.51m,

an increase of 72%

An EBITDA margin of

approximately 95%

OverviewProfit before tax

(‘PBT’) of USD

10.70 m,

an increase of 107%

65% increase in revenue

and 107% increase in

PBT despite depreciation

in the average Indian

Rupee/USD exchange

rate by 7.47% from USD

54.37 m in FY2012 to

58.44 m

in FY2013

Revenue of USD

50.92 m,

an increase of 65%

Currently

507.85MW

of fully operational

capacity and 40.25 MW

under final stages of

construction

In Indian Rupee terms

revenue increased by

77.0%.Adjusted for one-off and

non-recurring income,

EBITDA by 85.03%, and

PBT by 122%

Strong liquidity as on 31 December 2013, comprising

of USD 32.62 m cash equivalents and liquid

investments and USD 85.34 m of undrawn loan

facilities totalling to USD 117.96 m

Group revenues, costs and debt are denominated in Indian Rupees and are therefore

matched. The dollar strengthening has no cash and

economic impact on the Company as all its contracts

are in Indian rupees

08 09 Mytrah Energy Limited | 31 December 2013 | Financial Statements

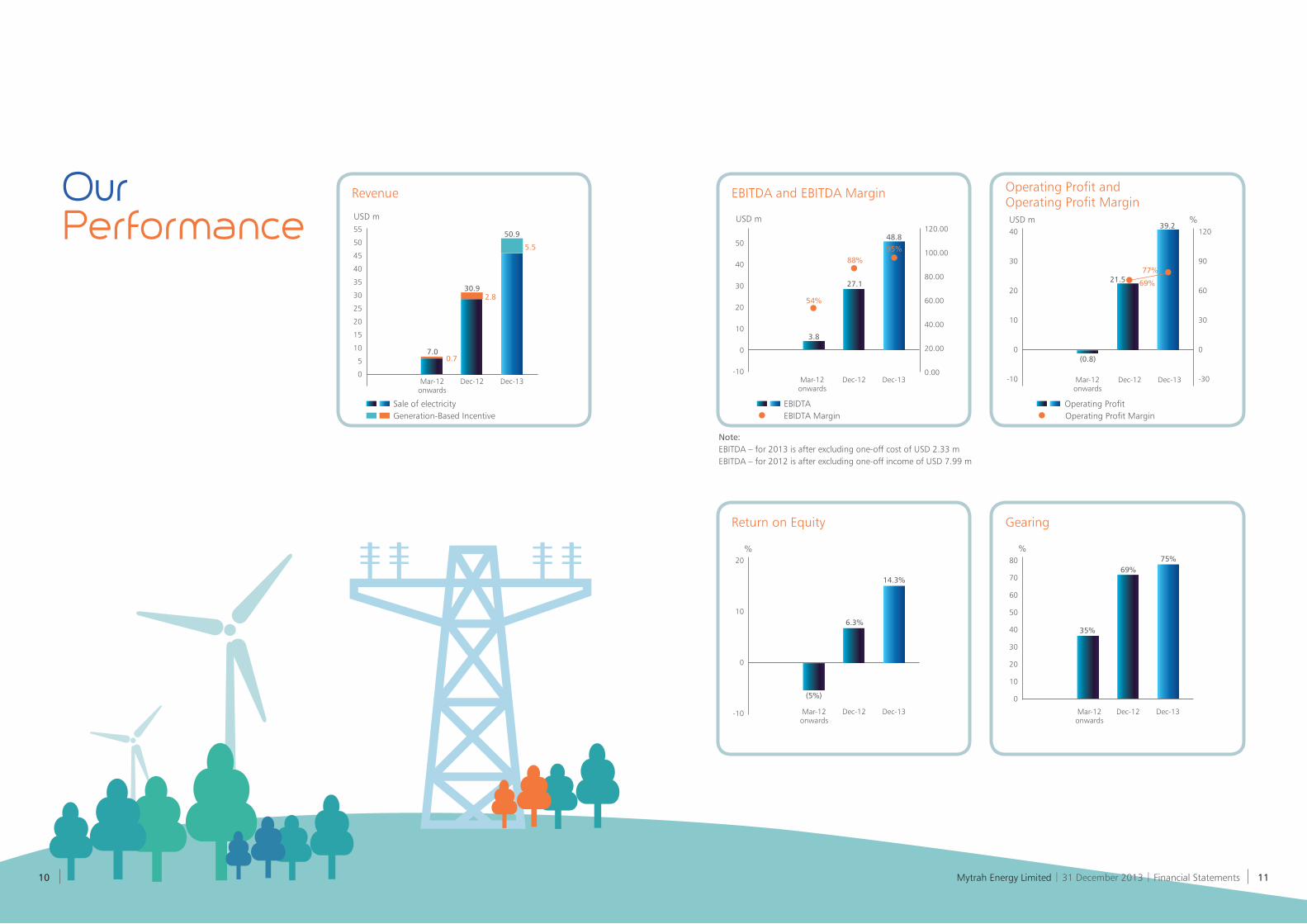

Our Performance

Revenue

55

50

45

40

35

30

25

20

15

10

5

0Mar-12onwards

Dec-12 Dec-13

USD m

2.8

5.5

0.7

Sale of electricityGeneration-Based Incentive

EBITDA and EBITDA Margin

50

40

30

20

10

0

-10

120.00

100.00

80.00

60.00

40.00

20.00

0.00

3.8

27.1

48.8

88%

54%

95%

USD m

EBIDTAEBIDTA Margin

Mar-12onwards

Dec-12 Dec-13

Return on Equity

20

10

0

-10

(5%)

6.3%

14.3%

%

Mar-12onwards

Dec-12 Dec-13

Gearing

80

70

60

50

40

30

20

10

0

35%

69%75%

Mar-12onwards

Dec-12 Dec-13

Operating Profit and Operating Profit Margin

40

30

20

10

0

-10

120

90

60

30

0

-30

Operating Profit

(0.8)

Operating Profit Margin

21.5

39.2

69%

77%

USD m %

Mar-12onwards

Dec-12 Dec-13

7.0

30.9

50.9

Note:EBITDA – for 2013 is after excluding one-off cost of USD 2.33 mEBITDA – for 2012 is after excluding one-off income of USD 7.99 m

%

Mytrah Energy Limited | 31 December 2013 | Financial Statements 10 11

Chairman and CEO’s StatementRavi Kailas Chairman and Chief Executive Officer

There is a significant shortage of power supply in India. We have seen no change in this position during the period and we believe that this will remain the case for many years to come.

507.85 MW commissioned

Machine & grid availability in excess of 97%

150 wind masts installed

200-300 MW of new orders placed

Strong growth in Revenue, EBITDA & PAT

Over the last 12 months, Mytrah has

consolidated its position as a profitable,

cash generative, Independent Power

Producer (”IPP”) with an expanding

portfolio of operating wind farm

projects across India.

Our operational portfolio, which post

year-end has risen from 309.9 MW to

507.85 MW, has performed slightly

ahead of our expectations with an

average Plant Load Factor (“PLF”) of

25.5% at the portfolio level. Within

the portfolio, the stabilised sites are

performing well ahead of our initial

expectations, in some cases exceeding

P50 estimates, with machine and

grid availability in excess of 97%. The

machine availability at the Jamanwada

(Gujarat) and Kaladongar (Rajasthan)

sites was approximately 90% for the

2013 wind season. These sites have

now been stabilised and we expect

their performance also to be ahead

of our expectations during 2014. This

productivity will have a further positive

impact on the overall revenue and

financial performance of the portfolio.

As I mentioned in our interim results, I

would like to reiterate that the Group’s

consistent strategy of holding project

and turbine costs generally constant

over a long period allows us to capture

the positive momentum provided by

rising tariffs. In addition, the fall in

the rupee during 2013, although now

seemingly stabilised, will undoubtedly

put further upward pressure on the

electricity price as the cost of production

from thermal sources increases due to

higher import costs.

We are able to maintain one of the

lowest costs of production in the

industry due to Mytrah’s significant

land assets and our various turbine

supply agreements, a substantial

and non-replicable advantage in the

market. Due to this, we expect to see

increasing margins across our portfolio

as electricity prices rise across India.

We now have 150 wind masts across

India, collecting significant valuable

proprietary wind data on a daily basis.

This allows our internal wind resource

team to evaluate and model this data

alongside independent studies. The

collection and analysis of this data

allows the Company to maximise the

value of our land assets and efficiently

allocate our resources. We believe that

the scale of our development activities

and our ability to obtain licences

and concessions across our land

assets located in wind-rich States are

important drivers for future growth,

long-term sustainability and the

creation of shareholder value.

We believe that Mytrah’s continued

access to financing in India, our access

to permitting enables us to take greater

control over our roll-out schedule, our

diversified range of strong partnerships

with wind turbine manufacturers, our

ability to build assets at a competitive

cost whilst managing development risk,

and the quality of our management

and teams will enable the Group to

continue to grow rapidly and generate

significant value for our shareholders.

Mytrah Energy Limited | 31 December 2013 | Financial Statements 12 13

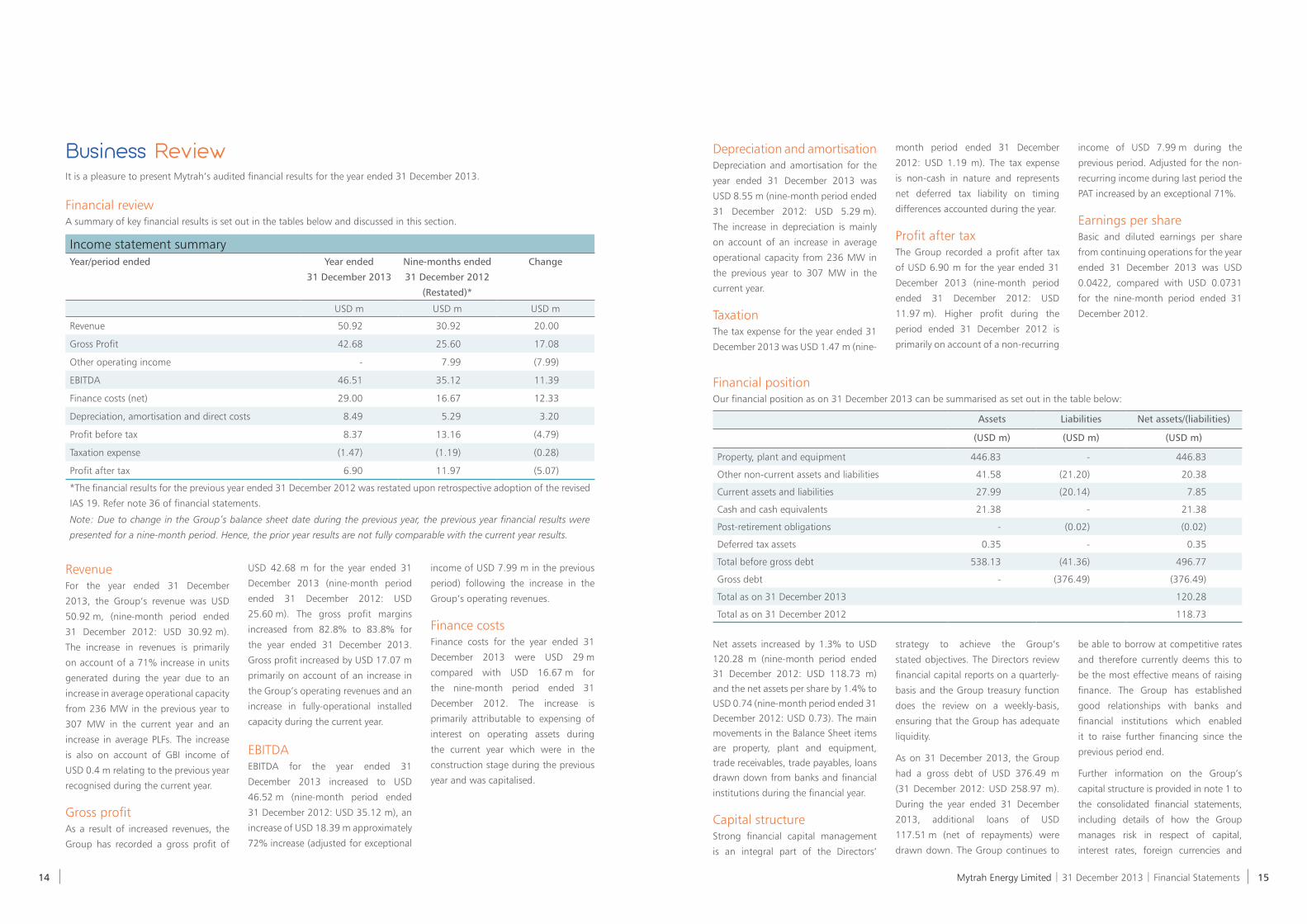

Depreciation and amortisationDepreciation and amortisation for the

year ended 31 December 2013 was

USD 8.55 m (nine-month period ended

31 December 2012: USD 5.29 m).

The increase in depreciation is mainly

on account of an increase in average

operational capacity from 236 MW in

the previous year to 307 MW in the

current year.

TaxationThe tax expense for the year ended 31

December 2013 was USD 1.47 m (nine-

month period ended 31 December

2012: USD 1.19 m). The tax expense

is non-cash in nature and represents

net deferred tax liability on timing

differences accounted during the year.

Profit after taxThe Group recorded a profit after tax

of USD 6.90 m for the year ended 31

December 2013 (nine-month period

ended 31 December 2012: USD

11.97 m). Higher profit during the

period ended 31 December 2012 is

primarily on account of a non-recurring

income of USD 7.99 m during the

previous period. Adjusted for the non-

recurring income during last period the

PAT increased by an exceptional 71%.

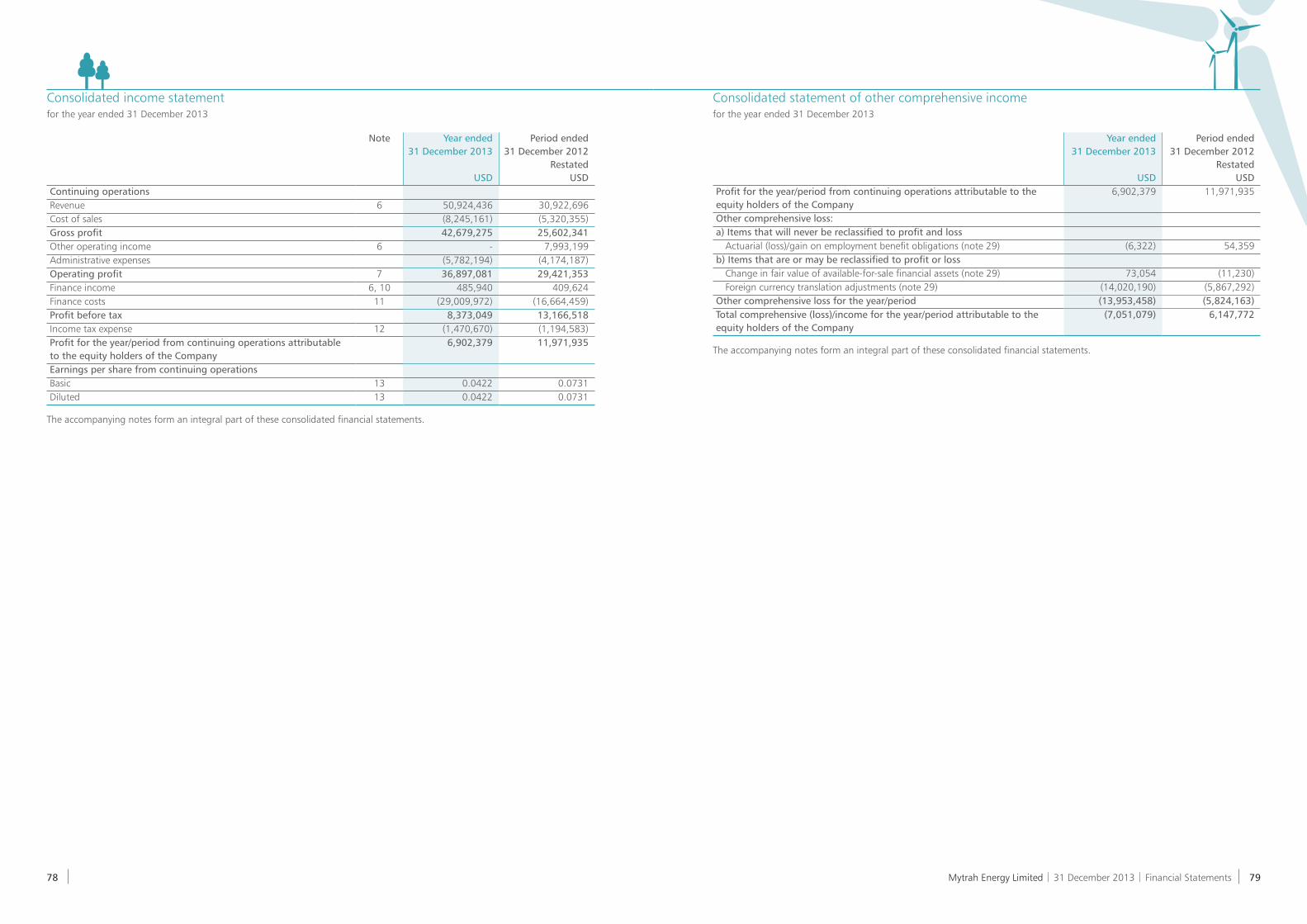

Earnings per shareBasic and diluted earnings per share

from continuing operations for the year

ended 31 December 2013 was USD

0.0422, compared with USD 0.0731

for the nine-month period ended 31

December 2012.

Financial positionOur financial position as on 31 December 2013 can be summarised as set out in the table below:

Assets Liabilities Net assets/(liabilities)

(USD m) (USD m) (USD m)

Property, plant and equipment 446.83 - 446.83

Other non-current assets and liabilities 41.58 (21.20) 20.38

Current assets and liabilities 27.99 (20.14) 7.85

Cash and cash equivalents 21.38 - 21.38

Post-retirement obligations - (0.02) (0.02)

Deferred tax assets 0.35 - 0.35

Total before gross debt 538.13 (41.36) 496.77

Gross debt - (376.49) (376.49)

Total as on 31 December 2013 120.28

Total as on 31 December 2012 118.73

Business ReviewIt is a pleasure to present Mytrah’s audited financial results for the year ended 31 December 2013.

Financial reviewA summary of key financial results is set out in the tables below and discussed in this section.

Income statement summaryYear/period ended Year ended

31 December 2013

Nine-months ended

31 December 2012

(Restated)*

Change

USD m USD m USD m

Revenue 50.92 30.92 20.00

Gross Profit 42.68 25.60 17.08

Other operating income - 7.99 (7.99)

EBITDA 46.51 35.12 11.39

Finance costs (net) 29.00 16.67 12.33

Depreciation, amortisation and direct costs 8.49 5.29 3.20

Profit before tax 8.37 13.16 (4.79)

Taxation expense (1.47) (1.19) (0.28)

Profit after tax 6.90 11.97 (5.07)

*The financial results for the previous year ended 31 December 2012 was restated upon retrospective adoption of the revised

IAS 19. Refer note 36 of financial statements.

Note: Due to change in the Group’s balance sheet date during the previous year, the previous year financial results were

presented for a nine-month period. Hence, the prior year results are not fully comparable with the current year results.

RevenueFor the year ended 31 December

2013, the Group’s revenue was USD

50.92 m, (nine-month period ended

31 December 2012: USD 30.92 m).

The increase in revenues is primarily

on account of a 71% increase in units

generated during the year due to an

increase in average operational capacity

from 236 MW in the previous year to

307 MW in the current year and an

increase in average PLFs. The increase

is also on account of GBI income of

USD 0.4 m relating to the previous year

recognised during the current year.

Gross profitAs a result of increased revenues, the

Group has recorded a gross profit of

USD 42.68 m for the year ended 31

December 2013 (nine-month period

ended 31 December 2012: USD

25.60 m). The gross profit margins

increased from 82.8% to 83.8% for

the year ended 31 December 2013.

Gross profit increased by USD 17.07 m

primarily on account of an increase in

the Group’s operating revenues and an

increase in fully-operational installed

capacity during the current year.

EBITDAEBITDA for the year ended 31

December 2013 increased to USD

46.52 m (nine-month period ended

31 December 2012: USD 35.12 m), an

increase of USD 18.39 m approximately

72% increase (adjusted for exceptional

income of USD 7.99 m in the previous

period) following the increase in the

Group’s operating revenues.

Finance costsFinance costs for the year ended 31

December 2013 were USD 29 m

compared with USD 16.67 m for

the nine-month period ended 31

December 2012. The increase is

primarily attributable to expensing of

interest on operating assets during

the current year which were in the

construction stage during the previous

year and was capitalised.

Net assets increased by 1.3% to USD

120.28 m (nine-month period ended

31 December 2012: USD 118.73 m)

and the net assets per share by 1.4% to

USD 0.74 (nine-month period ended 31

December 2012: USD 0.73). The main

movements in the Balance Sheet items

are property, plant and equipment,

trade receivables, trade payables, loans

drawn down from banks and financial

institutions during the financial year.

Capital structureStrong financial capital management

is an integral part of the Directors’

strategy to achieve the Group’s

stated objectives. The Directors review

financial capital reports on a quarterly-

basis and the Group treasury function

does the review on a weekly-basis,

ensuring that the Group has adequate

liquidity.

As on 31 December 2013, the Group

had a gross debt of USD 376.49 m

(31 December 2012: USD 258.97 m).

During the year ended 31 December

2013, additional loans of USD

117.51 m (net of repayments) were

drawn down. The Group continues to

be able to borrow at competitive rates

and therefore currently deems this to

be the most effective means of raising

finance. The Group has established

good relationships with banks and

financial institutions which enabled

it to raise further financing since the

previous period end.

Further information on the Group’s

capital structure is provided in note 1 to

the consolidated financial statements,

including details of how the Group

manages risk in respect of capital,

interest rates, foreign currencies and

Mytrah Energy Limited | 31 December 2013 | Financial Statements 14 15

commissioning of a wind farm. The

majority of our current projects and

those under construction and at final

stages of delivery, are under contracts

with Suzlon, and more recently,

ReGen Power and Gamesa which have

provisions that enable Mytrah to make

claims for liquidated damages in the

event there is a delay in commissioning

a project. In addition, our projects are

closely managed on a daily basis with

issues quickly escalated to senior levels

within the organisation.

Information technology/processing

As the business expands and processes

become increasingly automated, our

IT requirements are growing and are

now critical to our operations. We

have an experienced IT team in place,

ensuring systems are well-maintained

and our growing IT requirements are

fulfilled. We operate in SAP enterprise

resource management software

which is facilitating the expansion

of the business and enhancing the

quality of information available to our

management and executive teams.

Environmental compliance

Non-compliance with environmental

legislation would expose the Group

to various potential penalties and

would run counter to our core

values. To mitigate this risk, the

Group undertakes an Environmental

and Social Due Diligence Report for

each project. The majority of our

environmental compliance activities

are currently undertaken by Suzlon and

Regen Power. However, Mytrah has the

necessary expertise and procedures to

ensure compliance with environmental

legislation in respect to the

commissioning of projects under our

self-development strategy. Compliance

with environmental legislation is at the

heart of our self-build development

strategy.

Managing change

The Group continues to be in a

rapid growth phase and the Indian

renewable energy sector is also one

of rapid change with new measures

being introduced on a national and

state-level. To mitigate this risk, the

Group uses independent consultants

and outsourced contractors where

appropriate, to ensure the Group’s

activities can be scaled up or down

as required on a timely-basis and help

ensure the business remains flexible in

response to changes in the industry,

political and economic environment.

Availability and cost of financing

The Group is reliant, at this early

stage of its development, on the

timely availability of senior debt and

mezzanine financing in order to finance

its ambitious asset roll-out schedule.

To mitigate this risk, the financing

team has established relationships

across a diverse range of finance

providers in India, including the State

Bank of India, which is a testament

to the attractiveness of the Group’s

business model and the strength of our

management team. Projects can also be

financed from internal cash generation

in the event that new debt financing

becomes unavailable to the Group.

The largest operational cost of the

Group is the cost of debt. The Group’s

projects are financed by project-

based debt. The Management has

structured the projects in such a way

that debt is only drawn down once key

development milestones are reached

and the majority of debt is only drawn

down once capacity is installed and it

starts generating revenue. The cost

of debt is factored into each project

at the evaluation stage to ensure it

meets or exceeds our minimum IRR

requirements. As mentioned in the half-

year Financial Report, the Board is also

evaluating the possibility of a Business

Trust Listing that would substantially or

The largest operational cost of the Group is the cost of debt. The Group’s projects are financed by project-based debt. Management has structured the projects in such a way that debt is only drawn down once key development milestones are reached and the majority of debt is only drawn down once capacity is installed and it starts generating revenue.

Mytrah companies are rated investment gradeSPV SITE STATE CAPACITY (MW) Rating

MEIL Mahidad Gujarat 25.20* ICRA ‘BBB-’

MEIL Mokal Rajasthan 42.00

BVUPL Chakla Maharashtra 39.00

CARE ‘BBB’BVUPL Kaladongar Rajasthan 75.60

BVUPL Jamanwada Gujarat 52.50

BVUPL Sinnar Maharashtra 12.60

MVPPL Vajrakarur Andhra Pradesh 63.00 **India Ratings ‘A-’MVKPL Burgula Andhra Pradesh 37.40

**India Ratings ‘BBB-’MVKPL Savalsang Karnataka 70.55

MVMPL Vagarai Tamil Nadu 90.00 **India Ratings ‘BBB-’* ICRA, an Associate of Moody’s Investors Service** India Ratings, a Fitch Group Company

liquidity. A debt maturity profile is also

included.

Cash flow

The cash generated from operations

during the year was USD 29.37 m (2012:

USD 32.43 m). Investing activities for the

year ended 31 December 2013 resulted

in a cash outflow of USD 132.00 m

(2012: USD 138.57 m). Net financing

cash inflows were USD 110.50 m

(2012: USD 104.81 m). The increase

in financing cash inflows was mainly

due to draw down of loan facilities

USD 157.87 m (2012: USD 162.81 m)

and capital contributions from issue of

Redeemable Preference Shares (“RPS”) of

USD 7.35 m (2012: USD nil) during the

current year. As on 31 December 2013,

the Group had cash and bank balances

of USD 21.38 m (2012: USD 9.47 m).

Liquidity and investments

As on 31 December 2013, the Group

had liquid assets of USD 32.52 m and

undrawn/committed credit facilities of

USD 84.79 m, which will be used to

repay the short-term (bridge) loans. The

Group’s net debt position has changed

over the course of the year and is mainly

on account of draw down of loan

facilities during the year.

Principal risks and uncertaintiesThe Group is faced with a variety of risks

pertaining to the management of the

business and the execution of its strategy.

These risks are managed on a day-to-day

basis by the Management Committee

and formally reviewed by the Audit

Committee and the Board to monitor

that appropriate and proportionate

mitigation in the form of processes and

controls are in place. A summary of the

key business risks are detailed below.

Business interruption/critical service

failure

The Group’s current wind farms are

dependent on stable patterns of wind,

operations and maintenance undertaken

by Suzlon Energy Limited (“Suzlon”), grid

connectivity and other critical resources.

In the event that a critical resource was

not available then, this could affect the

operation of a wind farm and have a

knock-on effect on our revenue.

To mitigate this risk, Mytrah uses

independent consultants to conduct

wind feasibility studies when evaluating

projects and also use independent

consultants to evaluate wind turbine

generators supplied to our wind farms.

We also ensure that periodic preventative

maintenance is undertaken. The Group

is building an asset management team

to ensure, and where possible, enhance

standards of asset management

undertaken both internally for our self-

build projects and for those projects built

and maintained by our turnkey partners.

We are commissioning 100.5 MW of

capacity from ReGen Power and 137.7

MW with Gamesa, diversifying our

development and asset management

risks.

Delay in commissioning projects

Construction projects are, by their

very nature, complicated and subject

to numerous factors that could

cause a delay in the completion and

Mytrah Energy Limited | 31 December 2013 | Financial Statements 16 17

During the year, Mytrah continued to

draw debt against it facilities for the

238.2 MW asset roll-out scheduled

for Q1 2014. This debt financing was

secured across a diverse range of Indian

senior debt providers. In addition

during the year, we announced the

injection of USD 17.5 m in non-dilutive

mezzanine financing from our sponsor

group companies. This reaffirms the

sponsor Groups’ commitment to the

interests of all shareholders of the

Company and of minority shareholders

in particular.

Market environmentAs we highlight in each of our reports

to shareholders, there is a significant

shortage of power supply in India. We

have seen no change in this position

during the period and we believe that

this will remain the case for many

years to come. Wind energy currently

accounts for 20 GW of India’s total

capacity of 200 GW representing 10%

of installed capacity but less than 5%

of generating capacity. We expect wind

energy to increase significantly over the

next five years but due to the increase

in total capacity expected across India,

wind energy’s share of the generating

capacity is expected to actually reduce.

This puts India in an enviable position

regarding renewable power generation

and we anticipate that Mytrah will

continue to be a leading player within

the Indian market.

The fundamental market continues

to move advantageously for Mytrah.

During 2013, Andhra Pradesh increased

the tariff for wind power projects to

H 4.70 per kWh, Gujarat to H4.15 per

kWh, Rajasthan’s Jaisalmer and Barmer

districts to H 5.52 per kWh and H 5.80

per kWh respectively and Maharashtra

to H 5.81 per kWh.

Rising tariffs have been a constant

theme within the sector since our entry

in 2010. The average realisation price

(including GBI) across our portfolio in

2011 was H 4.75 per kWh. Following the

completion of our current development

of 238.2 MW taking our total portfolio

to 548.1 MW, this price is expected to

rise to H 5.23 per kWh and we anticipate

a continued increase to H 5.35 – 5.40

per kWh during 2014.

During 2013, the Ministry of New and

Renewable Energy of the Government

of India formally announced the

detailed scheme for the re-introduction

of GBI in India on 4 September 2013.

wholly pay down the Group’s debt.

Strategy review and future growth During the financial year we have

moved towards completion on our

first three projects with both Gamesa

and Regen turbines in the states of

Karnataka, Andhra Pradesh and Tamil

Nadu totalling 238.2 MW.

Following the period end, a total

of 197.95 MW including 37.4 MW at

Burgula in Andhra Pradesh, 70.55 MW

at Savalsang 1 in Karnataka and 90

MW at Vagarai in Tamil Nadu have

been added taking our operating

portfolio to 507.85 MW. With the

balance 40.25 MW due for completion

before the start of the 2014 wind

season, Mytrah will have 548.1 MW

spread across six states and 10 projects

providing a portfolio effect from a risk

perspective.

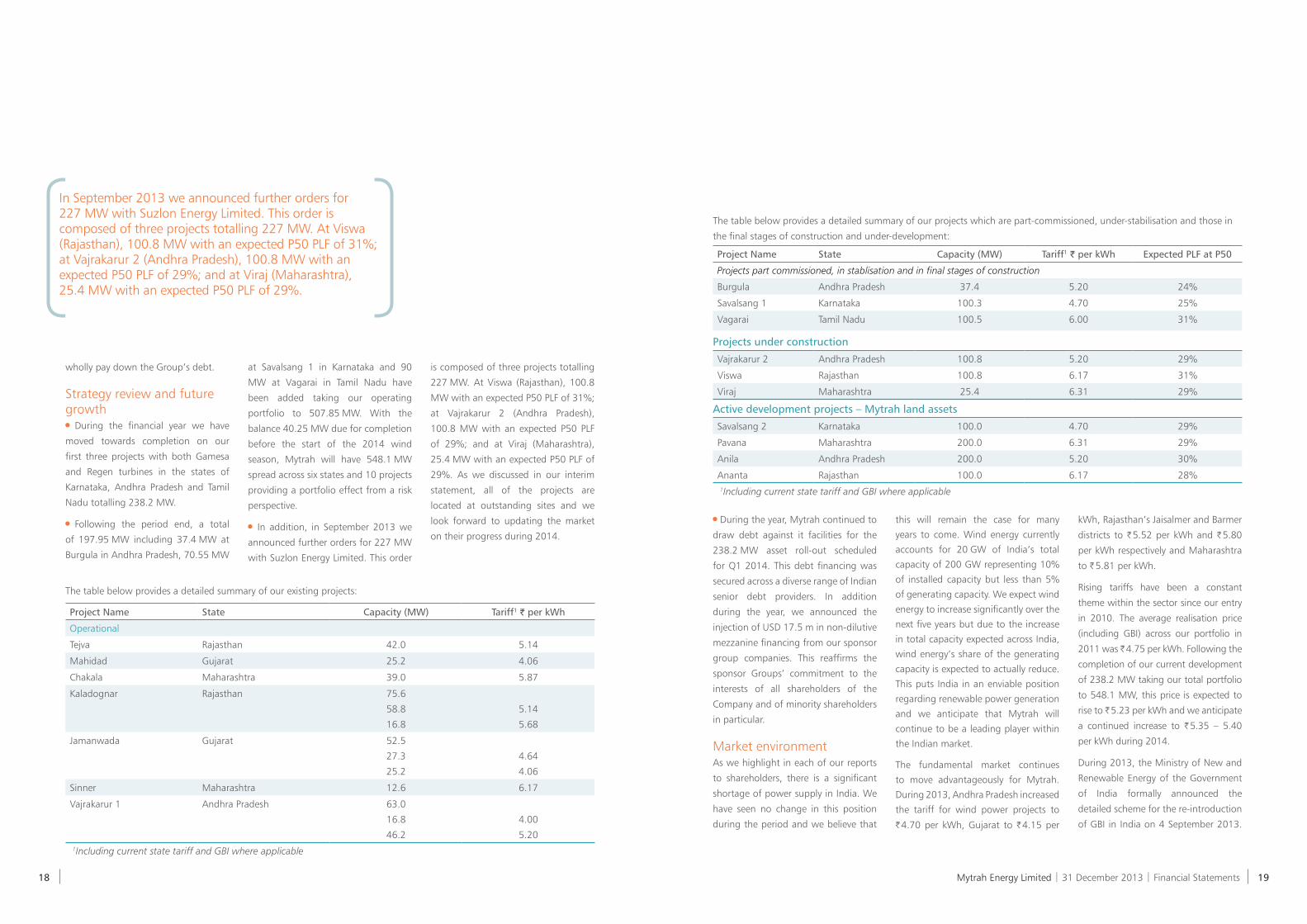

In addition, in September 2013 we

announced further orders for 227 MW

with Suzlon Energy Limited. This order

is composed of three projects totalling

227 MW. At Viswa (Rajasthan), 100.8

MW with an expected P50 PLF of 31%;

at Vajrakarur 2 (Andhra Pradesh),

100.8 MW with an expected P50 PLF

of 29%; and at Viraj (Maharashtra),

25.4 MW with an expected P50 PLF of

29%. As we discussed in our interim

statement, all of the projects are

located at outstanding sites and we

look forward to updating the market

on their progress during 2014.

The table below provides a detailed summary of our existing projects:

Project Name State Capacity (MW) Tariff1 J per kWh

Operational

Tejva Rajasthan 42.0 5.14

Mahidad Gujarat 25.2 4.06

Chakala Maharashtra 39.0 5.87

Kaladognar Rajasthan 75.6

58.8

16.8

5.14

5.68

Jamanwada Gujarat 52.5

27.3

25.2

4.64

4.06

Sinner Maharashtra 12.6 6.17

Vajrakarur 1 Andhra Pradesh 63.0

16.8

46.2

4.00

5.20

1Including current state tariff and GBI where applicable

In September 2013 we announced further orders for 227 MW with Suzlon Energy Limited. This order is composed of three projects totalling 227 MW. At Viswa (Rajasthan), 100.8 MW with an expected P50 PLF of 31%; at Vajrakarur 2 (Andhra Pradesh), 100.8 MW with an expected P50 PLF of 29%; and at Viraj (Maharashtra), 25.4 MW with an expected P50 PLF of 29%.

Vajrakarur 2 Andhra Pradesh 100.8 5.20 29%

Viswa Rajasthan 100.8 6.17 31%

Viraj Maharashtra 25.4 6.31 29%

Projects under construction

Savalsang 2 Karnataka 100.0 4.70 29%

Pavana Maharashtra 200.0 6.31 29%

Anila Andhra Pradesh 200.0 5.20 30%

Ananta Rajasthan 100.0 6.17 28%

1Including current state tariff and GBI where applicable

Active development projects – Mytrah land assets

Project Name State Capacity (MW) Tariff1 J per kWh Expected PLF at P50

Projects part commissioned, in stablisation and in final stages of construction

Burgula Andhra Pradesh 37.4 5.20 24%

Savalsang 1 Karnataka 100.3 4.70 25%

Vagarai Tamil Nadu 100.5 6.00 31%

The table below provides a detailed summary of our projects which are part-commissioned, under-stabilisation and those in

the final stages of construction and under-development:

Mytrah Energy Limited | 31 December 2013 | Financial Statements 18 19

The re-instated GBI scheme provides

an incentive to qualifying wind assets

commissioned on or after 1 April 2012,

at 50 paisa (H0.50) per kWh produced,

up to an increased cap of H10 m (USD

0.16 m) per MW installed under the

new GBI scheme compared to H6.2 m

(USD 0.11 m) per MW installed under

the old GBI scheme.

Following the announcement of the re-

introduction of the GBI scheme, all our

existing projects, totalling 548.1 MW,

qualify for the GBI scheme, with 186

MW qualifying under the old scheme

and 362.1 MW qualifying under the

new scheme.

ComplianceHR tracks the changes in labour laws

in the locations where we have a

presence. We also ensure that there

is continued emphasis on developing

guidelines and approaches for HR

governance and compliance in this

phase of rapid growth.

Corporate and social responsibility (“CSR”)All CSR activities throughout the lifecycle

of our turnkey projects are undertaken

by our turnkey suppliers, namely Suzlon

and more recently, ReGen Power and

Gamesa Wind Turbines. These activities

are monitored internally.

As we initiate our self-development

projects, Mytrah is responsible for

CSR activities before and after the

construction phase (during which, the

manufacturer is responsible for CSR

activities).

We have engaged independent third

party expertise in this field to assist

in the development of our own

comprehensive social, environmental,

health and safety management

system alongside establishing detailed

standards, policies and procedures

and internal accountabilities and

governance. These standards, policies

and procedures are designed to ensure

Mytrah complies with the following

standards (which are consistent with

local regulatory requirements and

guidelines, both generic and sector

specific, issued by the World Bank

Group):

ISO 14001 (Environmental Manage-

ment Systems)

ISO 18001 (Occupational Health &

Safety)

ISO 9001 (Quality Management

Systems)

Compliance with our internal

standards, policies and procedures

will be monitored by a management

steering committee and also subject to

quarterly review by internal audit and

at least annually by an independent

third party.

SummaryDuring 2013, Mytrah consolidated its

position as a leading IPP. We expect to

further consolidate this position during

2014 with an operational portfolio of

over half a GW completed three years

since our inception. We believe that we

will create significant shareholder value

during the next two years as we reach

an operating portfolio of over 1GW of

wind assets in India.

Finally, I would like to take this

opportunity to welcome our new

shareholders and once again thank

all our shareholders, management,

advisors and associates for their

support as we executed our strategy

over the period.

Ravi Kailas

Chairman and CEO

17 March 2014

Financial Performance

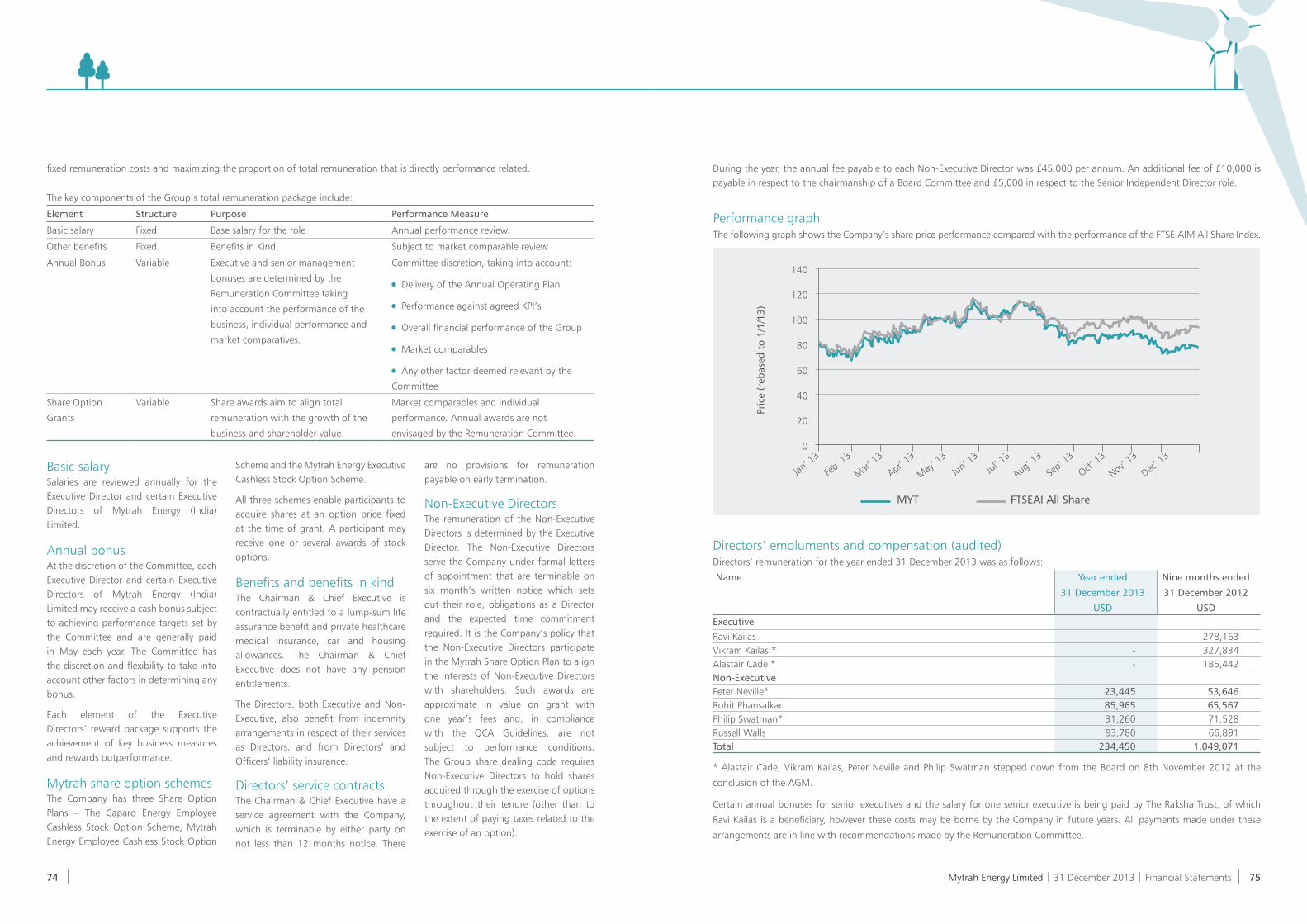

20 21 Mytrah Energy Limited | 31 December 2013 | Financial Statements

Revenue increased by 65% to USD 50.92 mIn 2013, the Group registered a

record performance with an increase

in revenue of USD 50.92 m. This was

due to the increase in units generated

by 70% and increase in average

operational capacity from 236 MW in

the previous year to 307 MW in the

current year.

EBIDTA of USD 46.51 m EBIDTA moved up by 80% to USD

48.84 m (adjusted for one-off non-

recurring cost of USD 2.33 m),

representing 95% EBIDTA margin.

Increase in EBIDTA was primarily

on account of increase in Group’s

operating revenues and increase in

average operational capacity.

Increase in operating profit by 18% to USD 39.22 mDespite an adverse currency movement

in the average Indian Rupee/USD

exchange rate by 7.47%, the Group

has registered an increase in operating

profit by 18% to USD 39.22 accounting

to 77% operating margin. An increase

in EBIDTA and operating profit margin

represents Group’s ability to transform

its strong operational capacity into

quality bottomline metrics.

Liquidity and investmentsLiquid assets of USD 31.52 m and

undrawn committed credit facilities

of USD 84.79 m provides a strong

liquidity position to the Group.

Robust growth with liquidity stock

Financial Highlights (USD m)

2013 2012 Change

Income statement

Revenues 50.92 30.92 +64%

EBIDTA 48.84 27.13 +80%

Operating margin 39.22 21.48 +83%

Balance sheet

Property, plant and equipment 446.83 358.17 +25%

Other assets 91.3 63.1 +45%

Equity 120.28 118.73 +1%

Debt 376.49 258.97 +45%

Other liabilities 41.36 43.57 (5%)

Income statementRobust topline performance

2013 has been a year of

transformational growth for the

Group, as it has continued to deliver

strong operating performance results.

The Group’s revenue has increased

by 65% to USD 50.92 m primarily

on account of an increase in average

operational capacity from 307 MW to

507.85 MW and an increase in average

PLFs of wind farm assets. The Group

has recognised a GBI income of USD

0.4 m based on the notification issued

by the regulatory authority on the GBI

scheme.

Other operating income in the previous

year, amounting to USD 7.99 m,

comprised liquidated damages claimed

on certain project suppliers in relation

to delays in the execution, cancellation

and downsizing for certain project.

There were no such claims during the

current year.

Adjusted EBIDTA increased by 80% to

USD 48.84 due to leading operational

metrics and strong control over costs,

leading to 95% EBIDTA margin.

Depreciation and amortisation

increased by USD 3.20 m primarily

on account of increased average

operational capacity from 236 MW in

the previous year to 307 MW in the

current year.

Finance cost for the year ended 31

December 2013 was higher by USD

3.26 m to 8.55 m primarily on account

of interest expensed off on operating

assets during the current year which

were capitalised in the previous year as

the assets were in construction stage.

The tax expense of the Group is

non-cash in nature and represents

net deferred tax liability on timing

differences accounted during the year.

Profit after tax adjusted for non-

recurring events on other operating

income and expenses during 2013

and 2012 resulted in an increase in

net profit by USD 2.92 m, a growth

of 73%.

Year/period ended Year ended 31

December 2013

Nine-months ended 31

December 2012 (Restated)*

Change

USD m USD m USD m

Revenue 50.92 30.92 +65%

Gross profit 42.68 25.60 +67%

Other operating income – 7.99 +100%

EBITDA 46.51 35.12 +32%

Finance costs (net) 29.00 16.67 +74%

Depreciation, amortisation and direct costs 8.49 5.29 +60%

Profit before tax 8.37 13.16 (36%)

Taxation expense (1.47) (1.19) +24%

Profit after tax 6.90 11.97 (42%)

Adjusted EBIDTA increased by 80% to USD 48.84 due to leading operational metrics and strong control over costs, leading to 95% EBIDTA margin.

Consistent and Sustainable Financial Growth

Mytrah Energy Limited | 31 December 2013 | Financial Statements 22 23

With total liabilities of USD 417.85 m, the debt-to-equity ratio stood at 75% against 69% in 2012. Liabilities primarily comprise loans borrowed to build up new operational projects. During the current year, the Group has drawn additional loans of USD 117.51 m (net of repayments).

Robust Balance Sheet

Total assets increases by 28%The Group continues to build its

available operational capacity. During

the year, the Group has moved towards

completion of three projects in the

states of Karnataka, Andhra Pradesh

and Tamil Nadu totalling 238.2 MW.

This resulted in an increase in property,

plant and equipment by 25% to

USD 446 m.

Major increase in other assets are from

investment liquid mutual fund units,

cash and bank balances and advances

to vendors.

The Group has received capital

contributions of USD 7.3 m from

the issue of redeemable preference

shares during the current year. Strong

financial capital management is an

integral part of the Management’s

strategy to achieve the Group’s stated

objectives. Management reviews the

treasury function on a regular basis to

ensure availability of adequate liquidity.

With total liabilities of USD 417.85 m,

the debt-to-equity ratio stood at

75% against 69% in 2012. Liabilities

primarily comprise loans borrowed to

build new operational projects. During

the current year, the Group has drawn

additional loans of USD 117.51 m

(net of repayments). The Group has

established good relationships with

banks and financial institutions which

enabled it to raise further financing

since the previous period end.

Balance sheet 2013 2012 Change

Property, plant and equipment 446.83 358.17 +25%

Other assets 91.3 63.1 +45%

Total assets 538.13 421.27 +28%

Equity 120.28 118.73 +1%

Financial debt 376.49 258.97 +45%

Other liabilities 41.36 43.57 (5%)

Total liabilities and equity 538.13 421.27 +28%

Relationship with 20 banksOver the last 3 years, Mytrah has developed relationships with 20 banks and financial institutions. These relationships have

enabled us to raise approximately USD 500 m to fund the development of our business.

PTC

Indian Renewable Energy Development Agency Ltd.(A Govt. of India Enterprise)

Mytrah Energy Limited | 31 December 2013 | Financial Statements 24 25

QA& with CFO

26 27 Mytrah Energy Limited | 31 December 2013 | Financial Statements

Q. How did the year pan out for you financially?A. Despite the world economy being

slow as per IMF, Mytrah has had a

successful 2013 with revenue rocketing

up by 65% from USD 30.92 m as

compared to USD 50. 92 m in 2012.

The EBITDA margin has been at an all-

time high of 95% since inception.

Q. What were the significant highlights of 2013? A. One of most significant highlights

of 2013 has been reinstating GBI with

improved terms.

The fundamental market continues

to move advantageously for Mytrah.

During 2013, Andhra Pradesh increased

the tariff for wind power projects to

H 4.70 per kWh, Gujarat to H4.15 per

kWh, Rajasthan’s Jaisalmer and Barmer

districts to H 5.46 per kWh and H 5.73

per kWh, respectively, and Maharashtra

to H 5.81 per kWh.

We have also commissioned 200 MW

of self-development projects in Burgula,

Savalsang and Vagarai.

Q. What is the capex invested during the year? A. The capital expenditure incurred

during the year is approximately USD

118 m. We have invested in land and

power evacuation facilities as well as in

the development and construction of

wind farms.

Q. What is the capex plan for the next 3 years? How do you expect to source funds? A. We are in the process of evaluating

various capex opportunities as well as

conducting several feasibility studies.

As of now, we have a strong relationship

with over 20 banks. Moreover, we plan

to maximise the efficiency of our cash

flows, such that we minimise our debt

component.

Q. What was the extent of funding you received in 2013 and what were the originating sources of the same? A. We raised approximately USD

157.8 m from banks and financial

institutions. We also received mezzanine

financing of USD 7.3 m from our Group

companies, reaffirming the sponsor

group companies’ commitment to our

shareholders.

Q. Please throw some light on your cash flows. A. Operations resulted in net cash inflow

of USD 29.4 m, which is indicative of

efficient cash flow management.

Q. What is the debt on your books? What is your leverage? Are you net debt positive?A. The gearing ratio is 75% which

indicates a strong Balance Sheet.

Q. What were some of the KPIs in finance that you were measurably proud of?A. Our ROE for the year is 14.2% and

expected to increase rapidly following

the commissioning of the new assets in

Savalsang, Vagarai and Burgula.

Vikram KailasChief Financial Officer

Q&A

Mytrah Energy Limited | 31 December 2013 | Financial Statements 28 29

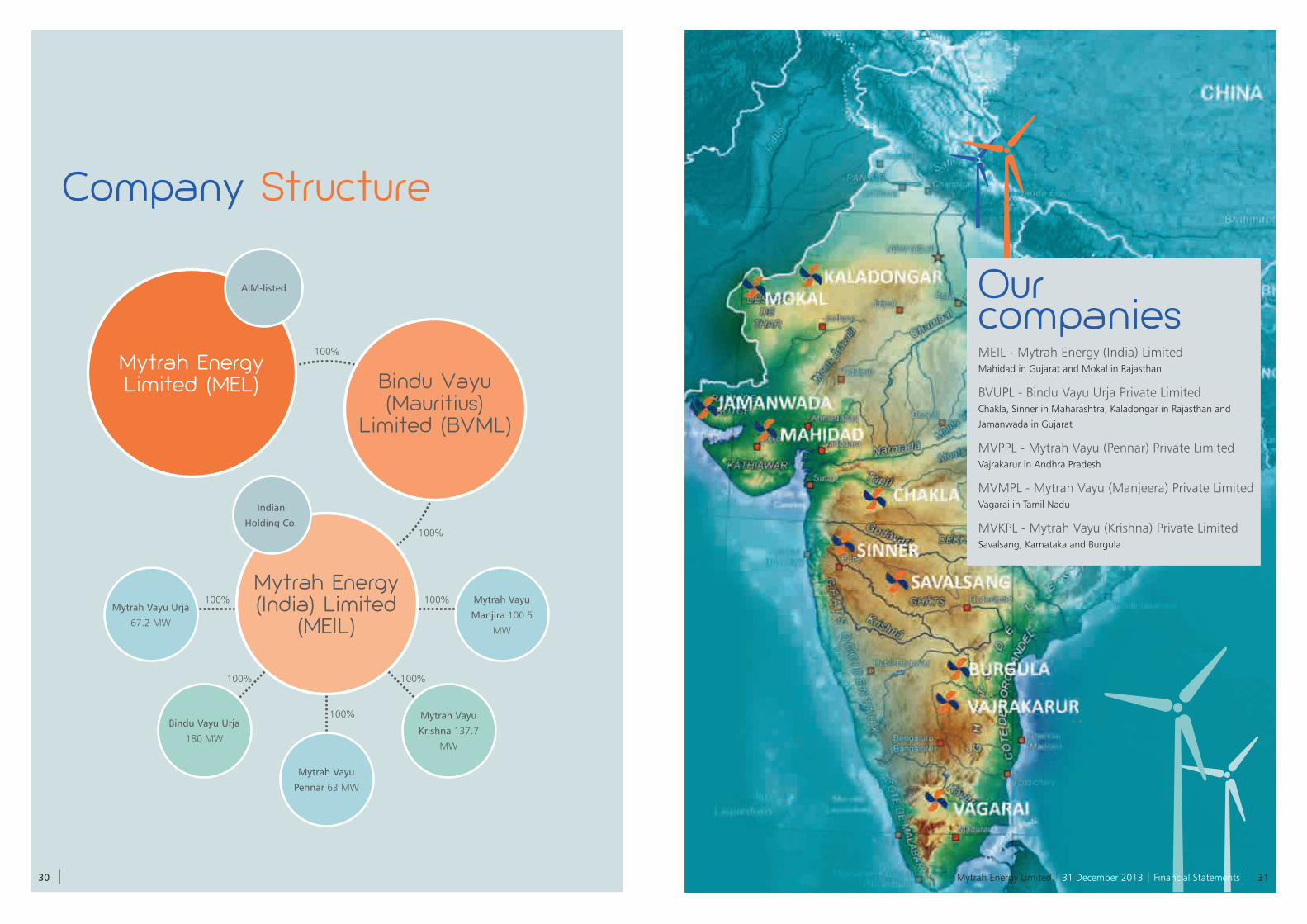

Company Structure

Mytrah Energy Limited (MEL) Bindu Vayu

(Mauritius) Limited (BVML)

Mytrah Energy (India) Limited

(MEIL)

Mytrah Vayu

Pennar 63 MW

Bindu Vayu Urja

180 MW

Mytrah Vayu

Krishna 137.7

MW

Mytrah Vayu Urja

67.2 MW

Mytrah Vayu

Manjira 100.5

MW

AIM-listed

Indian

Holding Co.

100%

100%

100% 100%

100%100%

100%

Our companiesMEIL - Mytrah Energy (India) LimitedMahidad in Gujarat and Mokal in Rajasthan

BVUPL - Bindu Vayu Urja Private LimitedChakla, Sinner in Maharashtra, Kaladongar in Rajasthan and

Jamanwada in Gujarat

MVPPL - Mytrah Vayu (Pennar) Private LimitedVajrakarur in Andhra Pradesh

MVMPL - Mytrah Vayu (Manjeera) Private LimitedVagarai in Tamil Nadu

MVKPL - Mytrah Vayu (Krishna) Private LimitedSavalsang, Karnataka and Burgula

30 31 Mytrah Energy Limited | 31 December 2013 | Financial Statements

JAMANWADA

MAHIDAD

MEIL- Mytrah Energy (India) LimitedMahidad in Gujarat and Mokal in Rajasthan are part-financed with a term

loan of H 2470 m.

ICRA, an Associate of Moody’s Investors Service has rated MEIL BBB-Mokal Wind Power Project

Project location: Jaisalmer zone,

Rajasthan

Capacity: 42 MW

WTG model: S88 – 2.1 MW

There were issues in the initial

phase of operations after installing

the WTGs due to high ambient

temperature and grid related

problems. The issue was solved by

doing retrofit work like arranging

cooling fans with high capacity and

constant monitoring and correcting

the issues affecting the grid.

After rectifying these issues, the

wind farm is performing up to

estimated AEP (Annual Estimated

Production), which was expected

while the project was conceived.

These steps resulted in attaining

a grid availability of 99.42% and

WTG availability of 97.82%.

The best performing WTG

generated a PLF of 21.94%.

Some key factors have been

identified, for further improvement

of performance of the site on

which the asset management team

is working.

Mahidad Wind Power Project

Project location: Rajkot zone,

Gujarat

Capacity: 25.2 MW

WTG model: S88 – 2.1 MW

Preventive measures have been

implemented such as applying

insulation coat to the transmission

lines to protect from moisture/

humidity and arranging bird guards

at the cut points and poles to stop

birds from hitting against the

turbines.

These activities resulted in

performance in line with estimated

AEP (Annual Estimated Production)

considered while the project was

conceived. These steps resulted in

attaining a high grid availability

of 99.59% and WTG availability of

97.24%.

The best performing WTG

generated a PLF of 31.70%.

32 33 Mytrah Energy Limited | 31 December 2013 | Financial Statements

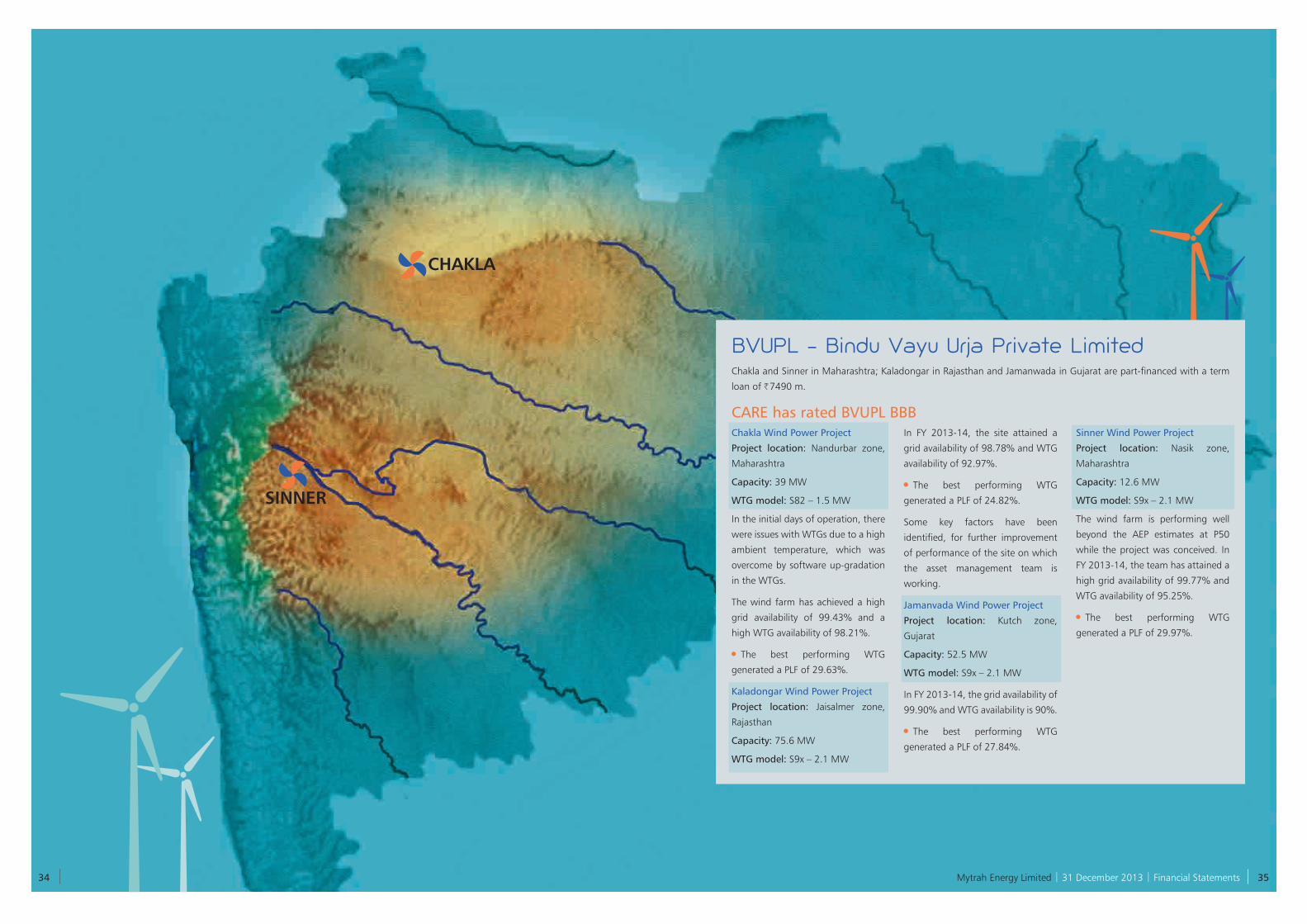

CHAKLA

SINNER

BVUPL - Bindu Vayu Urja Private LimitedChakla and Sinner in Maharashtra; Kaladongar in Rajasthan and Jamanwada in Gujarat are part-financed with a term

loan of H 7490 m.

CARE has rated BVUPL BBB Chakla Wind Power Project

Project location: Nandurbar zone,

Maharashtra

Capacity: 39 MW

WTG model: S82 – 1.5 MW

In the initial days of operation, there

were issues with WTGs due to a high

ambient temperature, which was

overcome by software up-gradation

in the WTGs.

The wind farm has achieved a high

grid availability of 99.43% and a

high WTG availability of 98.21%.

The best performing WTG

generated a PLF of 29.63%.

Kaladongar Wind Power Project

Project location: Jaisalmer zone,

Rajasthan

Capacity: 75.6 MW

WTG model: S9x – 2.1 MW

In FY 2013-14, the site attained a

grid availability of 98.78% and WTG

availability of 92.97%.

The best performing WTG

generated a PLF of 24.82%.

Some key factors have been

identified, for further improvement

of performance of the site on which

the asset management team is

working.

Jamanvada Wind Power Project

Project location: Kutch zone,

Gujarat

Capacity: 52.5 MW

WTG model: S9x – 2.1 MW

In FY 2013-14, the grid availability of

99.90% and WTG availability is 90%.

The best performing WTG

generated a PLF of 27.84%.

Sinner Wind Power Project

Project location: Nasik zone,

Maharashtra

Capacity: 12.6 MW

WTG model: S9x – 2.1 MW

The wind farm is performing well

beyond the AEP estimates at P50

while the project was conceived. In

FY 2013-14, the team has attained a

high grid availability of 99.77% and

WTG availability of 95.25%.

The best performing WTG

generated a PLF of 29.97%.

34 35 Mytrah Energy Limited | 31 December 2013 | Financial Statements

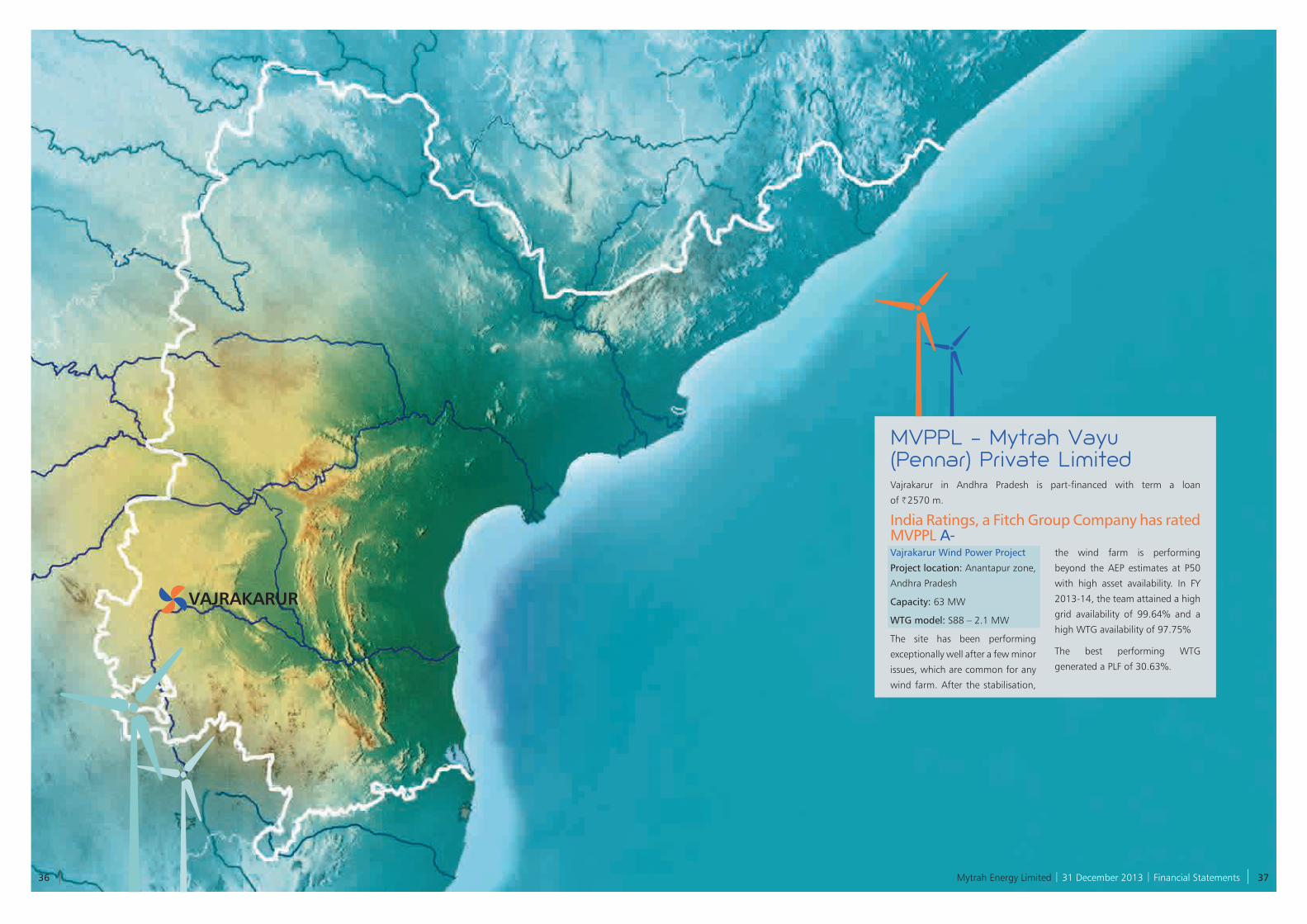

VAJRAKARUR

MVPPL - Mytrah Vayu (Pennar) Private LimitedVajrakarur in Andhra Pradesh is part-financed with term a loan

of H 2570 m.

India Ratings, a Fitch Group Company has rated MVPPL A-Vajrakarur Wind Power Project

Project location: Anantapur zone,

Andhra Pradesh

Capacity: 63 MW

WTG model: S88 – 2.1 MW

The site has been performing

exceptionally well after a few minor

issues, which are common for any

wind farm. After the stabilisation,

the wind farm is performing

beyond the AEP estimates at P50

with high asset availability. In FY

2013-14, the team attained a high

grid availability of 99.64% and a

high WTG availability of 97.75%

The best performing WTG

generated a PLF of 30.63%.

36 37 Mytrah Energy Limited | 31 December 2013 | Financial Statements

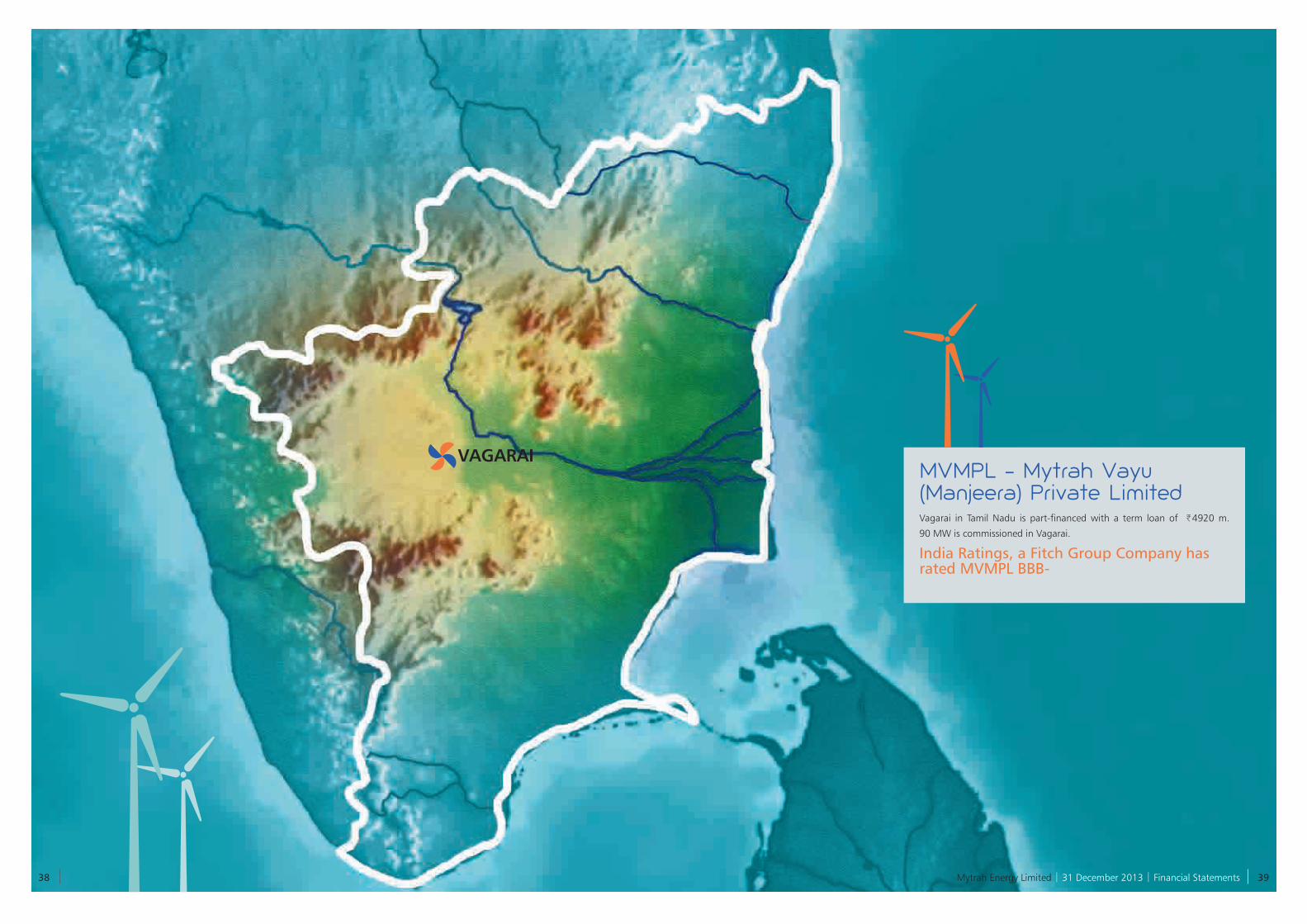

MVMPL - Mytrah Vayu (Manjeera) Private LimitedVagarai in Tamil Nadu is part-financed with a term loan of H 4920 m.

90 MW is commissioned in Vagarai.

India Ratings, a Fitch Group Company has rated MVMPL BBB-

VAGARAI

38 39 Mytrah Energy Limited | 31 December 2013 | Financial Statements

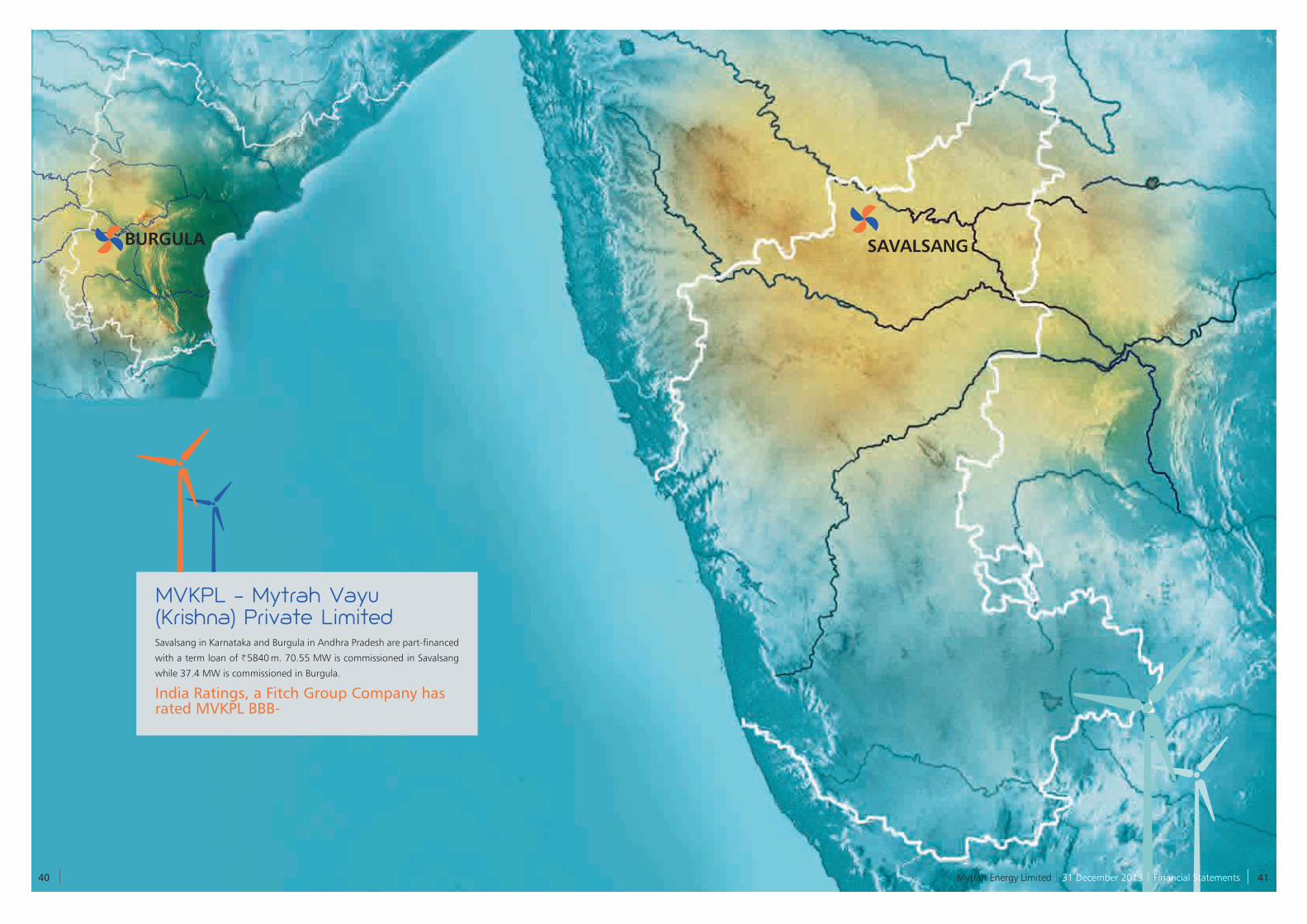

MVKPL - Mytrah Vayu (Krishna) Private LimitedSavalsang in Karnataka and Burgula in Andhra Pradesh are part-financed

with a term loan of H 5840 m. 70.55 MW is commissioned in Savalsang

while 37.4 MW is commissioned in Burgula.

India Ratings, a Fitch Group Company has rated MVKPL BBB-

SAVALSANGBURGULA

40 41 Mytrah Energy Limited | 31 December 2013 | Financial Statements

Our Intellectual Property

42 43 Mytrah Energy Limited | 31 December 2013 | Financial Statements

Day-to-day monitoring and data securityAll the wind masts are connected

through modem and the data banks

which are integrated into a centralized

server on a daily basis. As a new

initiative, some of the sites are installed

with scientific loggers. The performance

monitoring assessment masts are

installed with scientific loggers for real

time monitoring of data. Multiple levels

of data security have been maintained

to ensure high level security. A highly

skilled engineering team is monitoring

the data on a daily basis. Any fault

or anomalies identified in the data

will be conveyed to the site engineers

to resolve issues at the earliest. This

day-to-day monitoring leads to a

high level of data availability of

around 99%.

Immediate futureMytrah is targeting 200 monitoring

stations and the installation of wind

masts of 200 meter height, by end

of financial year 2015 and expect to

roll these out across all the states we

operate in.

Tamil Nadu

Tamil Nadu is one of the leading states

for wind power in India. Even though

a significant number of potential sites

are occupied in Tamil Nadu, Mytrah has

covered all the low mountain passes in

the Western Ghats. The monitoring

covers the southernmost to the

westernmost part of Tamil Nadu. The

Southernmost wind mast is installed 5

km from the Bay of Bengal. To evaluate

the accurate assessment of near passes,

Mytrah has expanded the monitoring

campaigns in such a way that pass

effect will be captured in term of wind

speed and direction. Our first wind

monitoring station was commissioned

in Tamil Nadu in May 2011. Currently

a total of 22 wind masts are installed

in Tamil Nadu, all of which have now

been operating for over 12 months.

Karnataka

Mytrah has installed 30 wind

monitoring stations and screened

potential sites for development.

Monitoring stations are installed in all

types of landscapes from plain terrain

to complex terrain.

Andhra Pradesh

Andhra Pradesh is another one of the

leading state for wind energy. Mytrah

has identified a number of potential

sites in Andhra Pradesh and currently

has 30 wind masts are operating in the

state.

Maharashtra

Mytrah has 42 wind masts installed in

Maharashtra, our largest concentration

in one state. These cover most of the

hilly and elevated areas in the state.

Gujarat

A total of 11 wind masts are installed in

Gujarat, covering both the coastal and

central areas of the state.

Rajasthan

16 wind masts have been installed

in Rajasthan and the northern most

wind mast is just 25 km from the

international border.

Mytrah has one of the largest wind

data bank in India. It is the only

independent power producer that has

more than 150 wind masts across the

country. Mytrah has a geographic mix

of its wind masts from the southern

tip to just 25 kilometers away from the

international border in the north.

Mytrah has more than 150 wind

monitoring stations which range from

80 meter to 120 meter with minimum

four levels of monitoring heights.

Major monitoring levels are 50 meter,

65 meter, 80 meter, 90 meter, 100

meter and 120 meter.

The wind masts cover most of the

terrain in India such as sea shores,

forests, sand dunes, hills, plain lands

and most of the wide low mountain

passes in the Western Ghats.

As a result of extensive research,

Mytrah has plans to install a wind mast

of 200 meter, which will be the tallest

wind mast in Asia Pacific.

Performance Monitoring Assessment

(PMA) wind masts are installed in all the

operational sites of Mytrah to evaluate

and optimize the performance of the

operational wind turbine generators.

These wind masts are installed higher

than the hub height of the operational

turbines to measure the shear across

the rotors.

Our wind masts and extensive research will enable development of 5000 MW executable projects over long-term

Our Intellectual Property

Mytrah Energy Limited | 31 December 2013 | Financial Statements 44 45

What Went Right in 2013?

Implementation of Asset Management Solution (AMS)With an aim to achieve better

operational control by analysing the

performance of all the operational

assets, the Company is rolling out its

Asset Portfolio Management Solution

covering all existing and upcoming

sites. This automated report generation

system is scheduled to go live during

the first quarter of FY 2014-15.

Forecasting of generationThe RRF guidelines have been

suspended by CERC owing to

issues related to its implementation

throughout the country. However,

Mytrah is carrying out forecasting of its

generation across all our operational

projects in order to be ready for the

implementation of new guidelines

from CERC. The Company plans to

develop its forecasting accuracy and

reliability so that it can be integrated

to the condition based and predictive

maintenance of assets.

Condition Monitoring System: The

asset management team is closely

working with vendors and consultants

to install the CMS solution into

operational WTGs. CMS is an on-line

monitoring system of the condition

of major equipment in a WTG. This

system is expected to be the first of its

kind implemented in India.

Implementation of ISO Certification:

Mytrah Energy (India) Limited is

working aggressively to upscale the

renewable energy portfolio to 3,000

MW over the next five years. The

Company considers it essential for

the success of the Group to develop

standard operating procedures. These

will enable the Company not only

to facilitate the challenging needs

of its diverse project portfolio in

widespread geographic locations but

also ensure quality, safety and process

standardisation which will increase the

sustainability and profitability of the

operational assets.

“To standardise the procedures to be followed for operating the projects in accordance with international standards, QSHE certification program has been initiated.

QSHE certification includes the “Quality Management System (QMS): ISO 9001”, “Environment Management System (EMS): ISO 14001” and “Occupational Health and Safety Assessment Series (OHSAS): OHSAS 18000”) helps us to overcome the challenges internally by way of huge capacity additions, diversified project portfolio in terms of self-developed, acquired and turnkey projects”.

Our Asset Management

46 47 Mytrah Energy Limited | 31 December 2013 | Financial Statements

Operational performance Strong development pipeline in Andhra Pradesh, Maharashtra, Madhya

Pradesh, Karnataka, Rajasthan and Gujarat

Successfully commissioned 200 MW self-development projects

Portfolio generation at par with P_75 level

Overall machine availability at 97% and grid availability at 99%

Strong receivables cycle

Human Capital

400 MW projects in

construction pipeline

Other systems and processes ERP second phase

process maturity fund

management module went

live by September 2013

150 wind masts installed

are recording data

continuously

Environment and market Reintroduction of the generation-based Incentive (GBI) – a boost to the industry

Maharashtra (MERC) directed Discoms to meet RPO targets for both solar and non-solar from FY 11 to FY 14 giving

relief to the ailing REC market

Tariff increased in Rajasthan, Karnataka, Maharashtra and Madhya Pradesh

What went right in 2013?

48 49 Mytrah Energy Limited | 31 December 2013 | Financial Statements

steps to engage leaders/managers

more fully in work-related matters

involving their employees. We are now

coaching leaders/managers on how to

discuss performance and development

planning. We are already starting to

see the results of these efforts through

this communication and engagement

model. We launched both formal and

informal forums of communication to

enable this engagement.

Learning and developmentWe have a robust process of employee

and managerial development. In the

space we are, we needed to approach

learning and development differently.

This began from hiring diverse and

talented employees, and tapping into

their unique insights and creativity.

Our online induction program quickly

integrates our new employees into the

system. The culture we have built in the

organisation ensures that we provide

an equal footing for everyone in the

conversation and there is an exchange

of information amongst work groups.

The organisation provides formal

and informal ways of learning. Our

emphasis, through this, has been to

ensure learning both at the individual

level and the organisational level.

There is a formal process of measuring

effectiveness of learning imparted.

This has enabled employees to solve

technical challenges and acquire

additional responsibility in their role.

The purpose is to create opportunity

for everyone.

During the year, the learning programs

equipped our employees not only to

manage but stay ahead of change.

Health, safety and well-being As part of our Health Series initiative,

the Company continued its investments

in various initiatives starting from

comprehensive health insurance for its

employees to regular health check-ups.

We have implemented a Safety Health

and Environment Policy (SHE) to ensure

safety of our employees at project sites.

Code of conductAs per the strong internal governance

practice followed by Mytrah, a code of

conduct for all its employees, within the

core value system of the Company, has

been laid down. The policy is available

on the Company’s ESS (Employee Self

Service) portal and every employee of

the Company has to affirm within the

same at the time of joining. Further, a

regular awareness/induction program

is being scheduled to impart these

initiatives.

During the year under review, there

were no such transactions, which were

entered by the Company or any of its

employees that fraudulent, illegal or

violative of Mytrah’s code of conduct,

ethics and its core value system, except

certain minor incidents, which had

no impact on the Company’s overall

financial position. However, these have

been appropriately dealt with in terms

of the Company’s code of conduct and

ethics.

Sexual harassment policyThe Company also recognises that

sexual harassment violates the

fundamental right of gender equality,

right to life and liberty and right to work

with human dignity. To implement the

Company’s zero-tolerance to sexual

harassment, a strong policy has been

developed within a provision for

suitable penal actions against sexual

At Mytrah, our core values drive our

valuation. We aspire to be considered

as an employer of choice, and thereby

have fostered high working standards

and positive employee relations. Our

work culture is inclusive, where we

respect and value individual differences.

In 2013, we began to place a

greater focus on developing the

skills and knowledge of our human

resources. We laid an emphasis on

sharpening the saw through a range

of technical learning programs and

skill enhancement assignments. Our

belief stemmed from the premise that

if we can engage employees fully then

we will achieve our goals, and they, as

individuals, can achieve theirs.

We identified three major HR initiatives

that were focused on engaging

employees. They were recognition

and awards programs, the employee

engagement survey and fostering

communication.

Recognition and awards programs One of the key drivers of engagement

is recognition. Employees appreciate

when their contributions are recognised

and valued. Recognition also reinforces

positive employee behavior that reflect

organisational values and are critical

to achieving goals. The Company

promoted a culture of employee

recognition where contributions

and successes are acknowledged

and celebrated. We introduced and

awarded the Chairman’s Award for

‘Outstanding Performance’ for our

employees. We also launched the

‘Myway’ Awards which recognised

employees who exhibited the core

values of the organisation.

Touch (Employee Engagement Survey)To increase employee engagement,

we need to know to what extent

employees are currently engaged,

and where there are opportunities to

improve their work life. Conducting a

survey early in the year allowed us to

gather information to help us make

work place improvements and tell

employees what we want to hear from

them. This helped in creating a higher

sense of morale and a stronger sense of

loyalty and commitment.

The team led the design and

administration of the survey along with

an external firm that possesses survey

expertise. Employees and the leadership

team actively participated in the survey

and were involved in identifying actions

to be taken in response to the results.

The overall engagement score moved

from 85% last year (12-13) to 89% this

year (13-14). The top 5 dimensions that

scored high this year were Leadership

(93%), Autonomy and empowerment

(92%), Mission and Purpose (92%),

Decision Making (92%) and Role Clarity

(91%). Findings indicate that we are a

great place to work, with high levels of

engagement overall. However, there is

room for improvement and we have

identified actions to be taken in the

areas identified for improvement.

Fostering communication The relationship between employees

and their leaders/managers is critical

to attract, engage and retain talent.

Employees who feel a connection to

their leaders/managers and have good

communication with them perform at

a higher level and are more engaged in

their work. Our HR team started taking

Human Capital

Mytrah Energy Limited | 31 December 2013 | Financial Statements 50 51

misbehaviour across any level. We

have also taken initiatives to spread

awareness amongst the employees

about the sexual harassment policy and

the Company’s zero-tolerance to any

such incidents. A high level committee

with appropriate representations, who

possess subject matter knowledge

to look after these issues, has been

formed.

No single case was registered under the

policy during the year under review.

Whistle blower policyTo maintain the highest level of

governance and to provide a gateway

to employees to voice concern in a

responsive manner about financial

impropriety, abuse, malpractices or any

other wrongdoing within the Company.

The Whistle Blower Policy has been

formulated. The detailed policy is made

available on the Company’s portal for

all the employees. One senior-most

management personnel has been

designated as Ombudsman to deal

with such issues.

During the year under review, there

were no such cases, which have

been brought to the notice of the

Ombudsman.

Anti-fraud policyThe Company has established

a reasonable process to detect,

investigate and resolve potentially

significant frauds. Such a process,

also includes proper framework that

facilitate to detect potentially significant

frauds/wrongdoings identified within

the organisation. A detailed Fraud Risk

Management Policy is being drafted to

make the Company furthermore robust

and strong against any possible fraud

risk scenario.

During the year under review, there has

been no significant instances of fraud

which have been noticed/reported.

There has been no occurrence of any

fraud which involves the management

or senior employees who have a

significant role in the internal control

structure.

Ombudsman processMytrah has also laid down the

‘Ombudsman’ process to deal with the

concerns raised through Whistle Blower

Policy and other matters pertaining to

the Code of Conduct and Ethics and

Fraud. Pursuant to such a process,

one of the senior-most personnel has

been appointed as the Ombudsman

by the Compliance Committee. It is

the responsibility of the Ombudsman

to initiate proper investigation on the

concern raised by any employee over

the malpractices, abuse, financial

impropriety or any other wrongdoing.

The process lays down a systematic

and time-bound approach to resolve

the concerns. Based on the findings

of the Ombudsman, the Compliance

Committee will initiate appropriate

action. The process assures that all

the concerns are treated with full

confidentiality and the employee

raising the concern is safeguarded.

Greener Earth

52 53 Mytrah Energy Limited | 31 December 2013 | Financial Statements

It is our business to leave a greener

earth for generations to come. By

choosing to generate power from wind

energy, we have made a conscious

decision in avoiding carbon emissions,

which is not the case when power is

produced from conventional sources.

By producing power from wind, we

are also making a conscious decision

in conserving water, which is used for

creating steam that turns the turbine

in thermal to generate electricity and

is also used to cool the turbines in the

thermal plant.

At Mytrah, we have avoided carbon

footprint of around 5,51,000 tons of

carbon emissions in FY 2013-14.

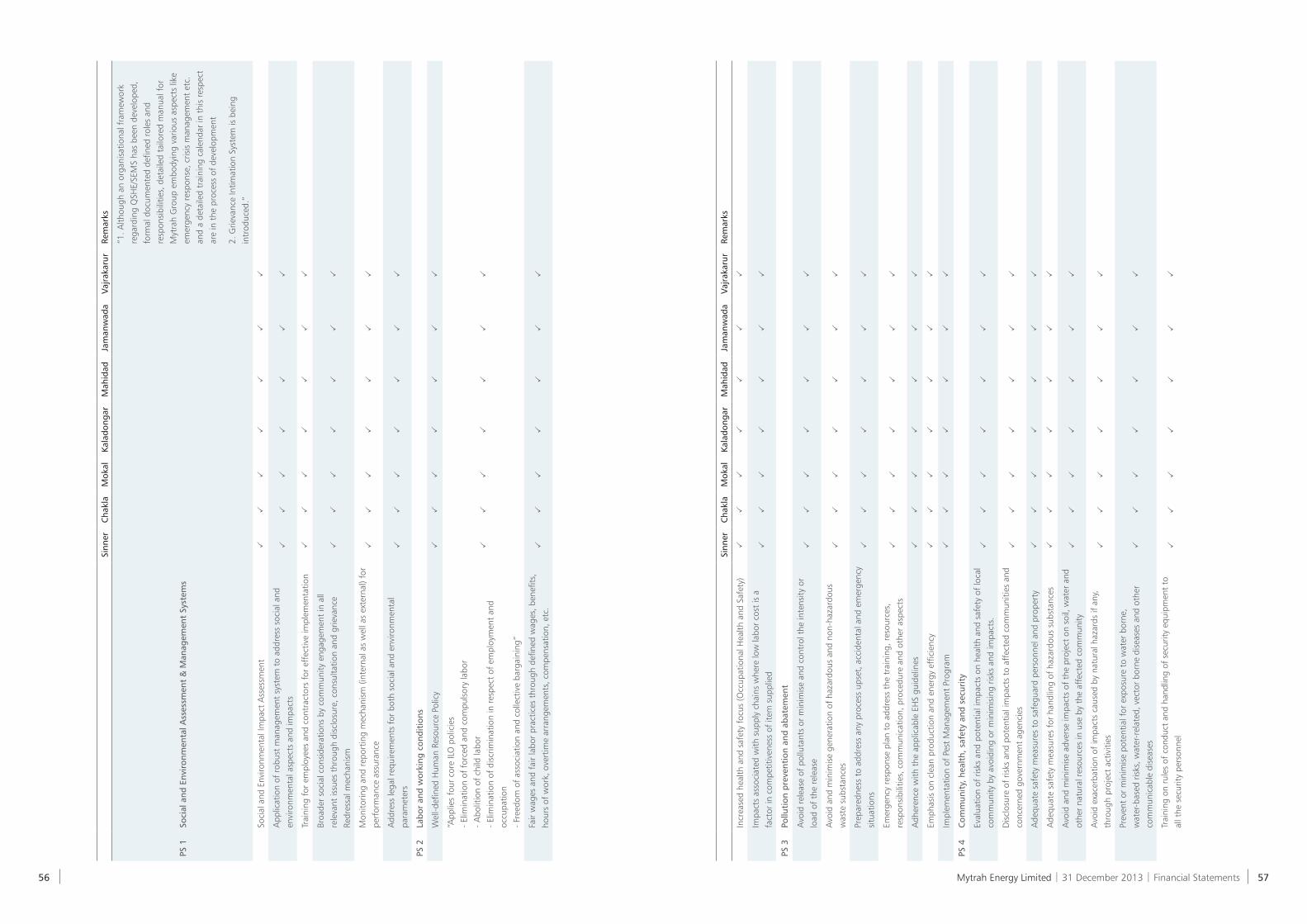

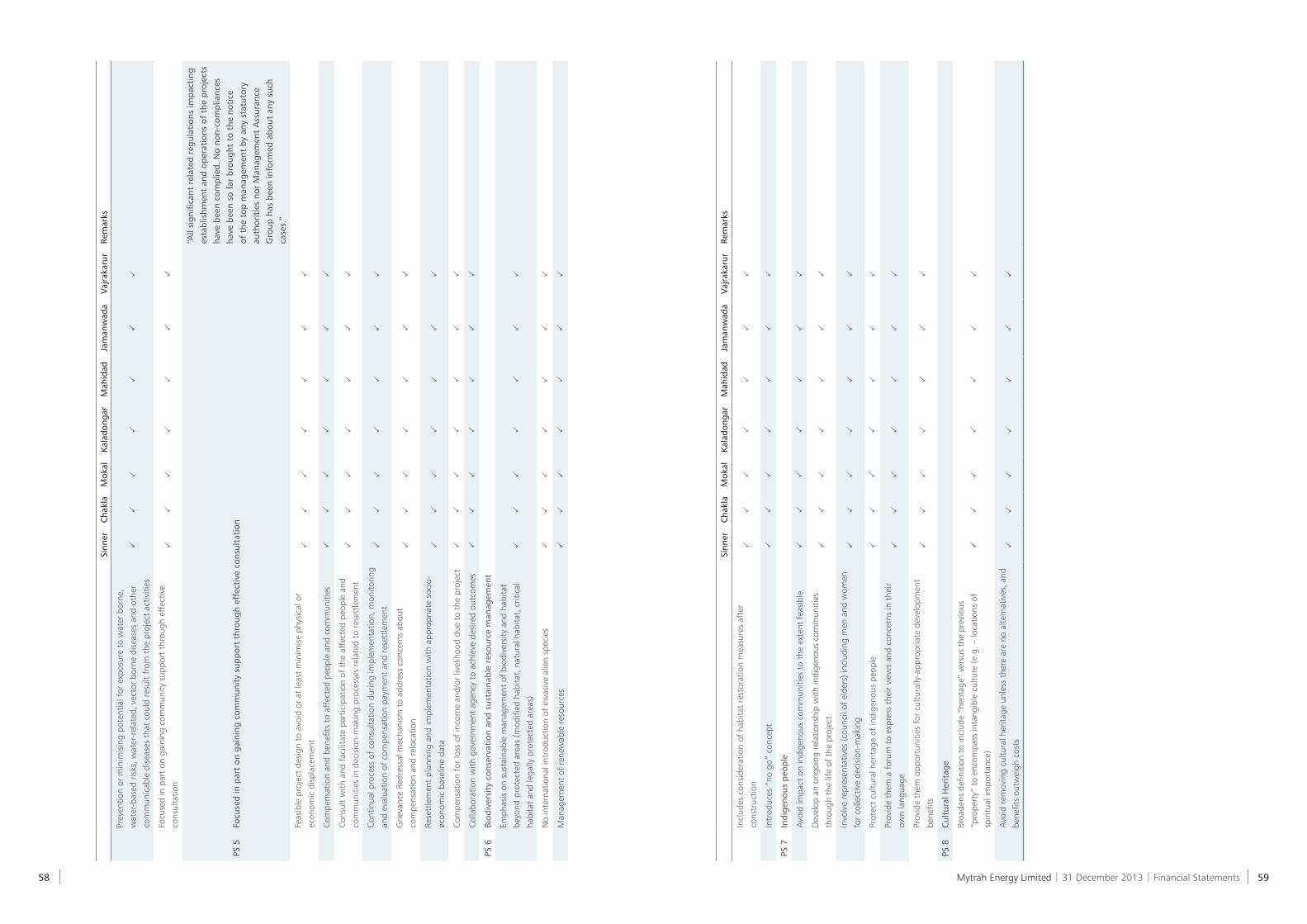

SustainabilityIn line with our core values and

philosophy – Inspiring solution – we

ensure that we are responsible in

utilising nature’s resources. At Mytrah,

we believe that the only way we can

do business is to do it in a sustainable

manner. We firmly believe that we are

catalysts of change and have taken it

upon ourselves in building a powerful

nation.

We have engaged independent third

party expertise in this field to assist in the

development of our own comprehensive

social, environmental, health and

safety management system alongside

establishing detailed standards,

policies and procedures and internal

accountabilities and governance. These

standards, policies and procedures are

designed to ensure that we comply

with the following standards (which

are consistent with local regulatory

requirements and guidelines, both

generic and sector specific, issued by the

World Bank Group)

Performance standard 1: Assessment

and management of environmental

and social risks and impacts

Performance standard 2: Labor and

working conditions

Performance standard 3: Resource

efficiency and pollution prevention

Performance standard 4: Community

health, safety, and security

Performance standard 5: Land

acquisition and involuntary resettlement

Performance standard 6: Biodiversity

conservation and sustainable

management of living natural resources

Performance standard 7: Indigenous

peoples

Performance standard 8: Cultural

heritage

The study was conducted across eight

wind farms comprising – Sinner, Chakla

in Maharashtra; Mokal and Kaladongar

in Rajasthan; Mahidad and Jamanwada

in Gujarat and Vajrakarur in Andhra

Pradesh.

Sustainability Report

Greener Earth

54 55 Mytrah Energy Limited | 31 December 2013 | Financial Statements

Sinn

erC

hakl

aM

okal

Kala

dong

arM

ahid

adJa

man

wad

aVa

jrak

arur

Rem

arks

Incr

ease

d he

alth

and

saf

ety

focu

s (O

ccup

atio

nal H

ealth

and

Saf

ety)

PP

PP

PP

P

Impa

cts

asso

ciat

ed w

ith s

uppl

y ch

ains

whe

re lo

w la

bor

cost

is a

fact

or in

com

petit

iven

ess

of it

em s

uppl

ied

PP

PP

PP

P

PS 3

Pollu

tion

pre

vent

ion

and

abat

emen

t

Avo

id r

elea

se o

f po

lluta

nts

or m

inim

ise

and

cont

rol t

he in

tens

ity o

r

load

of

the

rele

ase

PP

PP

PP

P

Avo

id a

nd m

inim

ise

gene

ratio

n of

haz

ardo

us a

nd n

on-h

azar

dous

was

te s

ubst

ance

sP

PP

PP

PP

Prep

ared

ness

to

addr

ess

any

proc

ess

upse

t, a

ccid

enta

l and

em

erge

ncy

situ

atio

nsP

PP

PP

PP

Emer

genc

y re

spon

se p

lan

to a

ddre

ss t

he t

rain

ing,

res

ourc

es,

resp

onsi

bilit

ies,

com

mun

icat

ion,

pro

cedu

re a

nd o

ther

asp

ects

PP

PP

PP

P

Adh

eren

ce w

ith t

he a

pplic

able

EH

S gu

idel

ines

PP

PP

PP

P

Emph

asis

on

clea

n pr

oduc

tion

and

ener

gy e

ffic

ienc

yP

PP

PP

PP

Impl

emen

tatio

n of

Pes

t M

anag

emen

t Pr

ogra

mP

PP

PP

PP

PS 4

Com

mun

ity,

hea

lth,

saf

ety

and

secu

rity

Eval

uatio

n of

ris

ks a

nd p

oten

tial i

mpa

cts

on h

ealth

and

saf

ety

of lo

cal

com

mun

ity b

y av

oidi

ng o

r m

inim

isin

g ris

ks a

nd im

pact

s.P

PP

PP

PP

Dis

clos