Embed Size (px)

Citation preview

See Your RetirementYour guide to transitioning to the next phase in life

Eastman Kodak Employees’ Savings & Investment Plan

It’s time to see your retirement through

Retirement can be a time of freedom, adventure, and personal enjoyment for those who prepare for it. But transitioning away from the work of a lifetime involves some uncertainty and may inspire many questions.

This guide, prepared by Eastman Kodak Company and T. Rowe Price, offers answers that can help create a smooth transition. T. Rowe Price has been helping people invest for and manage their life transitions for more than 70 years, and their unique history of research, investment knowledge, and guidance has helped numerous preretirees approach their retirement with enthusiasm.

< Forward

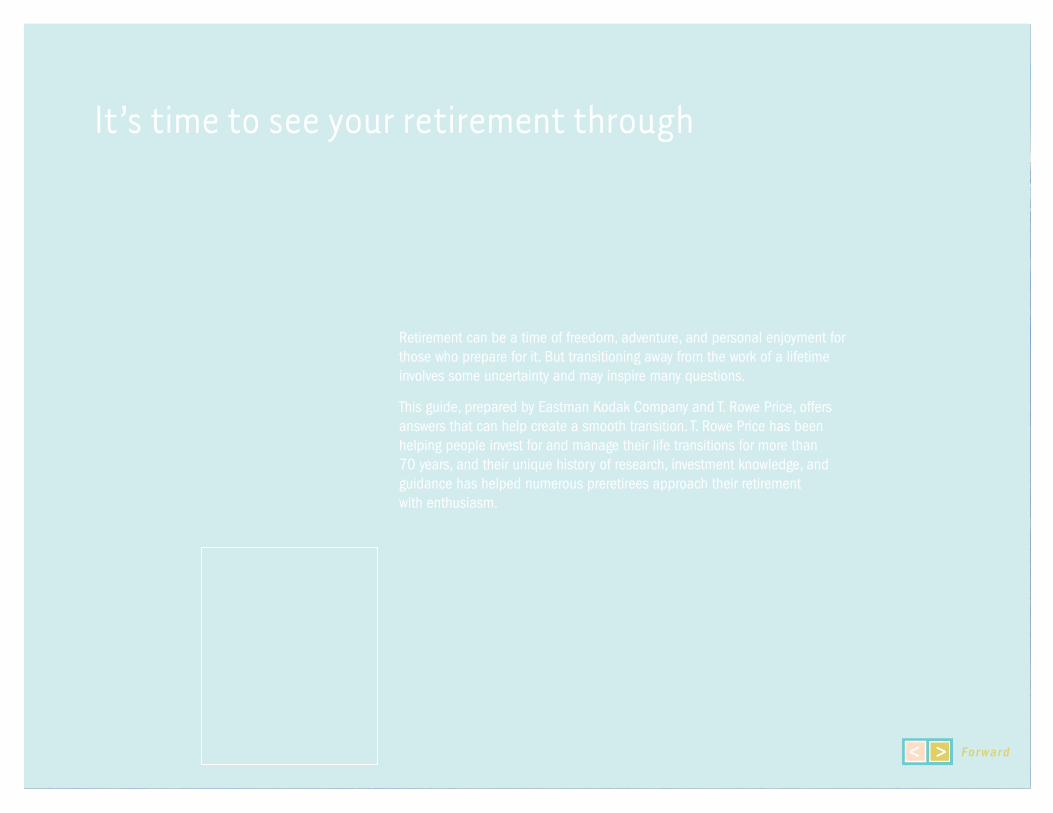

section

1

section

2

section

3

Inside this interactive guide, you will find help to organize your financial information and anticipate your needs in this next phase of your life. There are also valuable, tested strategies that can help you make the most of your retirement.

You can use the buttons at the bottom of each page to help navigate through the brochure, or quickly jump back to the Table of Contents at any time. The spreadsheets are interactive and will provide automatic calculations based on the data you input. In addition, you will find active links to external websites with additional information. You can return to the brochure by simply closing the new web browser window.

If you need more information, you can contact a retirement specialist, who has access to an array of services that can address most retirement issues. Just call 1-800-SIP-4YOU (1-800-747-4968) or visit the SIP website at rps.troweprice.com.

Back

Eastman Kodak Employees’ Savings & Investment Plan l p.1

Picture the Retirement You Wantsection 1

As you begin your planning, it’s important to get a handle on your finances, as well as the factors that could affect your savings once you retire.

Here are some essentials to enjoying your retirement years:1. Have sufficient income to maintain your lifestyle in retirement2. Maintain your purchasing power over the course of a lengthy retirement3. Have a financial cushion for unexpected expenses4. Pass on what you want to your heirs

There is no shortage of other potential retirement goals, but we recommend focusing on strategies that put you in the best position to achieve these four targets. Once these bases are covered, you can approach your other ambitions from a position of financial strength.

At the least, you’ll want to establish a set of priorities going into retirement. But you can add more substance to your visualizations by sketching out a retire-ment budget. Anticipate what your everyday expenses will be in retirement and consider what kind of bigger-ticket items will need to be factored in as well. The next few pages will walk you through the budgeting process. You can also learn more in the next section about how taxes can affect your retirement budget.

Planning Your Retirement Budget: Checklists and Helpful TipsYour everyday expenses in the early years of your retirement may be relatively easy to estimate. But the most effective expense planning anticipates every contingency—including some that may not come about for another 20 years or more, such as a move to be nearer to your children, a major illness, or the need for assisted living. The expense projection checklist starting on the next page will help provide a more specific picture of your financial requirements. If you maintain a budget, you already have most of the information you need. If you don’t, the checklist is a good way to get started.

Tips for Easier OrganizationMake it easier for you and for those who might need to manage your affairs for you if you ever become incapacitated.

Collect paper records in a single location, preferably a fireproof file box or other safe storage system, or use computer or online tools.

In addition to your financial records, you should gather other useful data, such as contact information for your family, as well as any lawyers, accoun-tants, brokers, or financial planners you work with; wills and letters of instruction, powers of attorney, living wills and other health care directives, copies of trust documents, deeds, titles, and insurance policies; recent tax returns, pay stubs, and information on credit card accounts; and birth certificates, death certificates, and marriage licenses.

Be sure to share the location of these important papers with family members or others you trust who would be responsible for your affairs in your absence.

Things ChangeOnce you retire, your income, expenses, and taxes are all still subject to change. Benefits like Social Security currently have cost-of-living increases. Investment assets will fluctuate with the markets. Tax laws and amounts change. So you should review your financial situation once a year to make sure you’re still on track.

Checklist 1 Projecting Your Expenses for One YearYou may want to begin with an inventory of current expenses, both essential and discretionary, as a basis for projecting your in-retirement costs. Or go directly to the “Projected” column if you have a good sense of what you’re spending now, but do take into consideration changes in your spending patterns that may occur in retirement. For example, you won’t be commuting to work each day, and you may need less dry cleaning. On the other hand, you may be spend-ing more on travel and entertainment. Note that income taxes are not included in these projections. You’ll see tax calculation material elsewhere in this guide.

Begin with the expenses on the next page. >

Eastman Kodak Employees’ Savings & Investment Plan l p.2

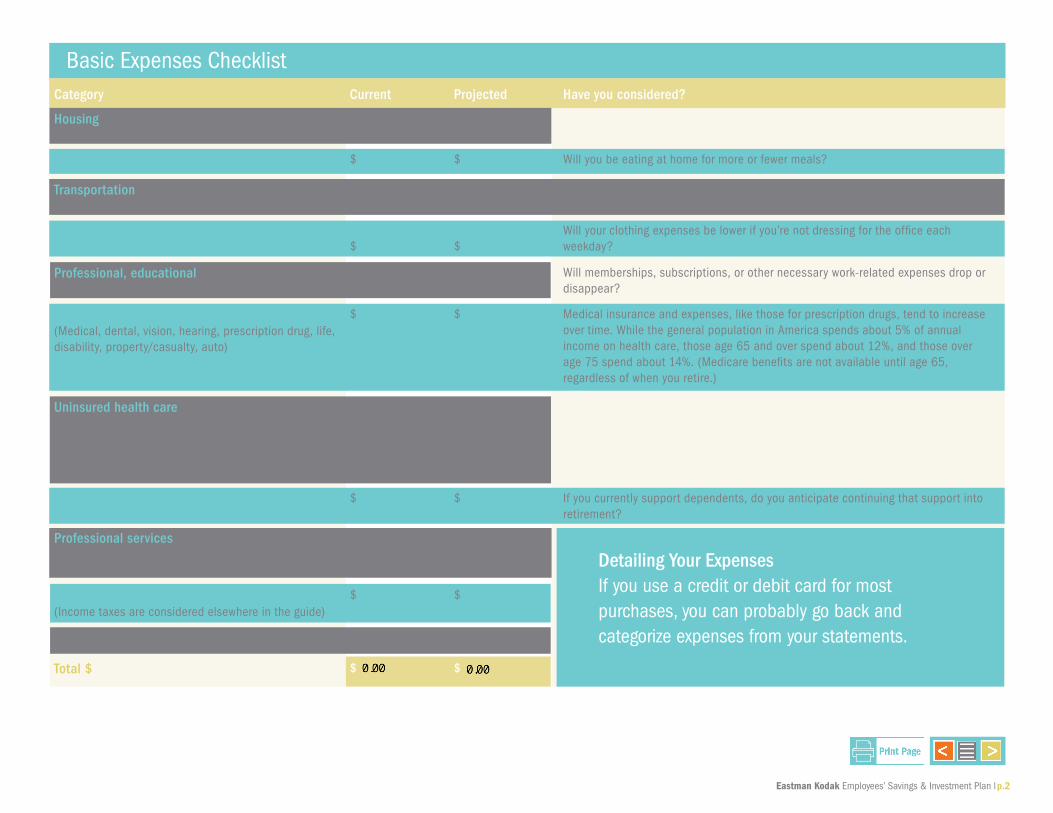

Basic Expenses Checklist

Detailing Your Expenses If you use a credit or debit card for most purchases, you can probably go back and categorize expenses from your statements.

Category Current Projected Have you considered?

Housing (Mortgage, utilities, telephone, cable, maintenance)

$

$

Food $ $ Will you be eating at home for more or fewer meals?

Transportation (Fuel, loan payments, maintenance, etc.)

$

$

Will you be traveling more or less in retirement?

Clothing, personal care $

$

Will your clothing expenses be lower if you’re not dressing for the office each weekday?

Professional, educational $ $ Will memberships, subscriptions, or other necessary work-related expenses drop or disappear?

Insurance (Medical, dental, vision, hearing, prescription drug, life, disability, property/casualty, auto)

$ $ Medical insurance and expenses, like those for prescription drugs, tend to increase over time. While the general population in America spends about 5% of annual income on health care, those age 65 and over spend about 12%, and those over age 75 spend about 14%. (Medicare benefits are not available until age 65, regardless of when you retire.)

Uninsured health care (Out-of-pocket expenditures for office visits not covered by medical insurance, the portion of prescription costs not covered, vision and/or dental if not included in your medical plan)

$ $

Dependent care/support $ $ If you currently support dependents, do you anticipate continuing that support into retirement?

Professional services (Lawn care, housecleaning, maintenance, accounting, tax preparation, attorney fees, etc.)

$ $

Property taxes (Income taxes are considered elsewhere in the guide)

$ $

Other $ $

Total $ $ $

Eastman Kodak Employees’ Savings & Investment Plan l p.3

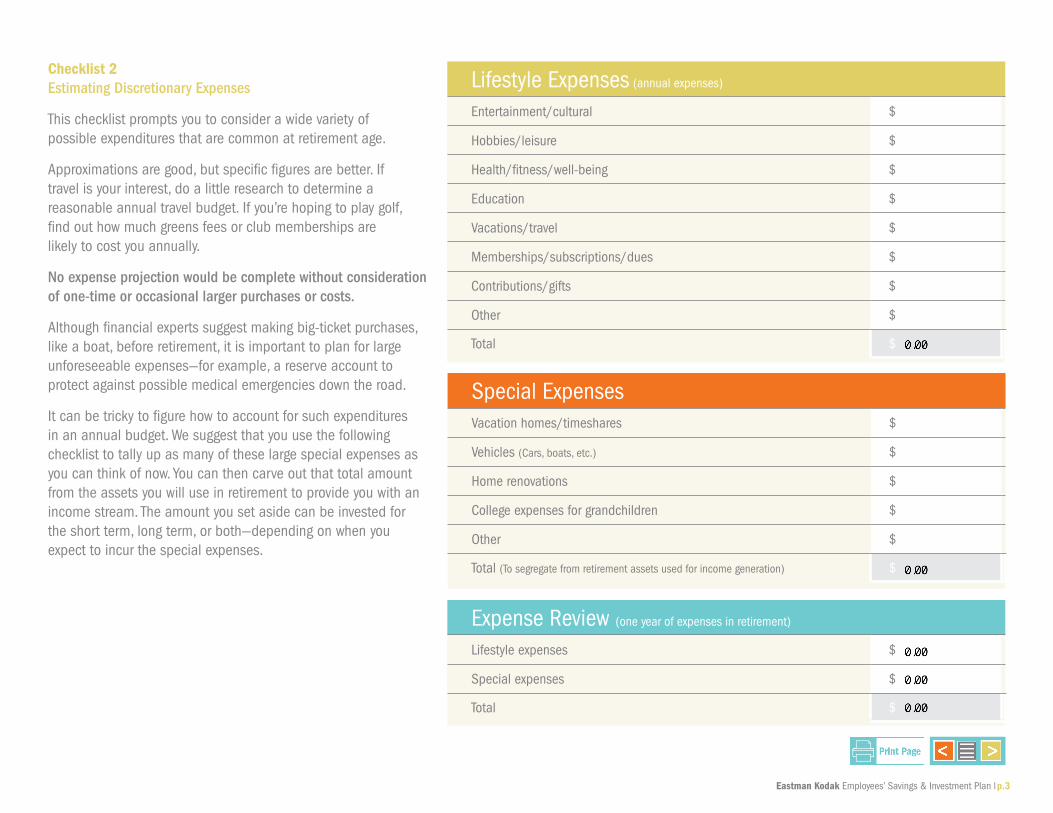

Checklist 2 Estimating Discretionary Expenses

This checklist prompts you to consider a wide variety of possible expenditures that are common at retirement age.

Approximations are good, but specific figures are better. If travel is your interest, do a little research to determine a reasonable annual travel budget. If you’re hoping to play golf, find out how much greens fees or club memberships are likely to cost you annually.

No expense projection would be complete without consideration of one-time or occasional larger purchases or costs.

Although financial experts suggest making big-ticket purchases, like a boat, before retirement, it is important to plan for large unforeseeable expenses—for example, a reserve account to protect against possible medical emergencies down the road.

It can be tricky to figure how to account for such expenditures in an annual budget. We suggest that you use the following checklist to tally up as many of these large special expenses as you can think of now. You can then carve out that total amount from the assets you will use in retirement to provide you with an income stream. The amount you set aside can be invested for the short term, long term, or both—depending on when you expect to incur the special expenses.

Lifestyle Expenses (annual expenses)

Entertainment/cultural $

Hobbies/leisure $

Health/fitness/well-being $

Education $

Vacations/travel $

Memberships/subscriptions/dues $

Contributions/gifts $

Other $

Total $

Expense Review (one year of expenses in retirement)

Lifestyle expenses $

Special expenses $

Total $

Special ExpensesVacation homes/timeshares $

Vehicles (Cars, boats, etc.) $

Home renovations $

College expenses for grandchildren $

Other $

Total (To segregate from retirement assets used for income generation) $

Eastman Kodak Employees’ Savings & Investment Plan l p.4

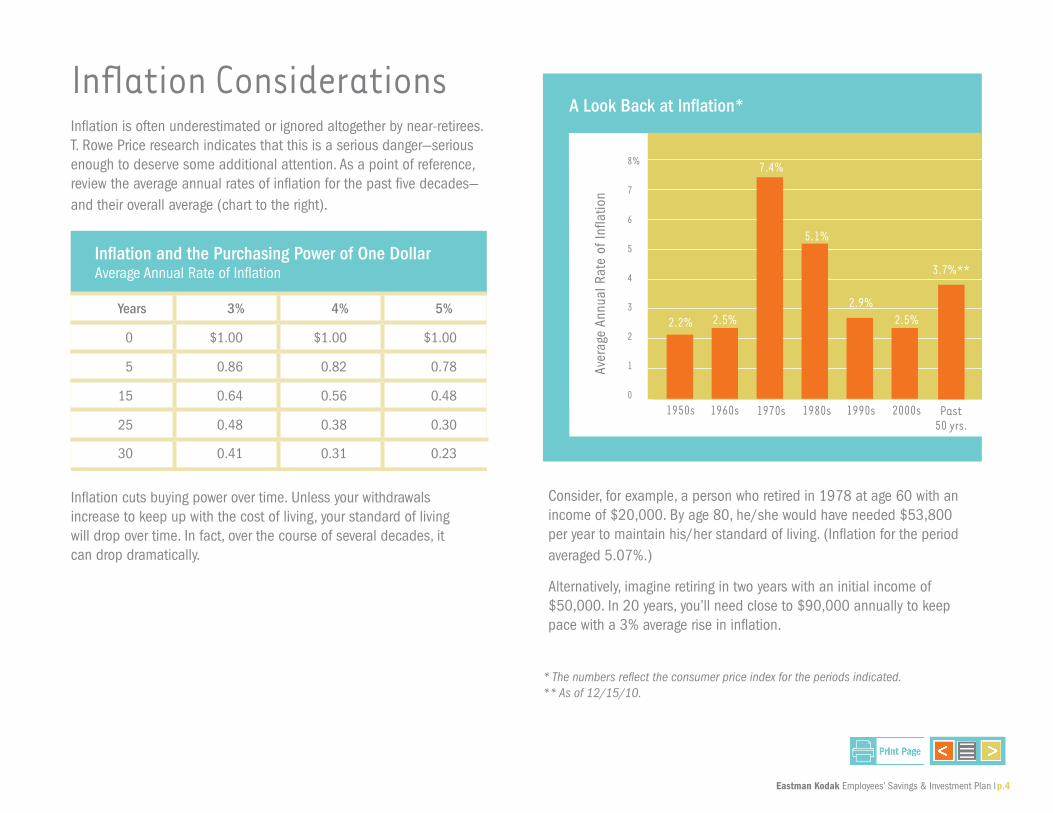

Inflation ConsiderationsInflation is often underestimated or ignored altogether by near-retirees. T. Rowe Price research indicates that this is a serious danger—serious enough to deserve some additional attention. As a point of reference, review the average annual rates of inflation for the past five decades—and their overall average (chart to the right).

Inflation and the Purchasing Power of One DollarAverage Annual Rate of Inflation

Years 3% 4% 5%

0 $1.00 $1.00 $1.00

5 0.86 0.82 0.78

15 0.64 0.56 0.48

25 0.48 0.38 0.30

30 0.41 0.31 0.23

Inflation cuts buying power over time. Unless your withdrawals increase to keep up with the cost of living, your standard of living will drop over time. In fact, over the course of several decades, it can drop dramatically.

Consider, for example, a person who retired in 1978 at age 60 with an income of $20,000. By age 80, he/she would have needed $53,800 per year to maintain his/her standard of living. (Inflation for the period averaged 5.07%.)

Alternatively, imagine retiring in two years with an initial income of $50,000. In 20 years, you’ll need close to $90,000 annually to keep pace with a 3% average rise in inflation.

* The numbers reflect the consumer price index for the periods indicated. ** As of 12/15/10.

A Look Back at Inflation*

Aver

age

Annu

al R

ate

of In

flatio

n

8%

7

6

5

4

3

2

1

0

2.2%

1950s

2.5%

1960s

7.4%

1970s

5.1%

1980s

2.9%

1990s

2.5%

2000s

3.7%**

Past 50 yrs.

Eastman Kodak Employees’ Savings & Investment Plan l p.5

Assess your exposure to inflationSocial Security benefits currently include an annual cost-of-living adjustment, which blunts concern about inflation. But what about your other sources of income in retirement?

If you have a pension from a previous employer, check with the plan administrator to see if your payments will rise with inflation.

If you own a deferred annuity, before you begin payments, determine whether you can elect an option that enables your payments to automati-cally increase each year. Although your initial payments will be lower, you will know that your payments will increase each year, thereby helping to offset the effects of inflation.

The amount you invest in short-term bonds, CDs, money market securities, and similar investments is not expected to fluctuate significantly. However, your principal will have little growth potential. Therefore, these types of investments are most suitable for money you expect to spend within the next two to three years—not for a retirement that may last for decades.

The more your sources of income are “fixed,” the greater your exposure to inflation risk. In most cases, keeping pace with inflation in retirement means managing investments for a prudent degree of asset growth.

Keys to Determining Your TaxesTaxes in retirement can vary dramatically, depending on both the amount of income you have and the source of that income. Many retirees find that their taxes drop sharply because their earned income declines. Others may be surprised at how large a bite Uncle Sam takes.

Before retiring, you should at least review the kinds of taxes you’ll probably have to pay during retirement. In addition to quarterly estimated taxes on your income, you’ll need to understand the tax treatment of retirement account withdrawals or distributions, early withdrawal penalties, and gift and estate taxes. By familiarizing yourself with them now, you can possibly avoid some tax surprises later on.

A tax professional can assist you with estimating your liabilities in the first few years of retirement. Tax-estimating software programs may also be helpful and informative.

Tax-Wise Withdrawal StrategiesA tax advisor can also help you navigate tax laws that apply to withdrawals from your retirement accounts. However, there are several rules of thumb you can use as a starting point. It is generally more advantageous to withdraw assets from taxable accounts, such as bank accounts and money market mutual funds, before tapping into those that are tax-deferred, such as 401(k) accounts and IRAs. However, note that there are generally minimum distribution amounts you must take from your tax-deferred retirement account assets once you attain age 70½ (some exceptions apply if you are still employed).

These are called required minimum distributions (RMDs), and they are discussed further in the next section. If you are married, the older spouse should begin taking withdrawals first if he/she has savings of his/her own.

Tap your Roth IRA assets last, since any growth in Roth IRAs is not subject to taxation (assuming several rules are met). Roth IRAs are also not subject to RMDs while the IRA owner is still alive. As your estate planning attorney will inform you, they can be excellent tools for leaving a legacy to your youngest heirs because they may provide decades of tax-deferred growth, as well as tax-free distributions to your heirs.

Now’s the Time for Tax Help Even if you’ve never hired a tax professional before, now is a great time to do so. Anticipating how much you are likely to pay in income taxes each year will be extremely valuable in preparing financially for retirement.

Eastman Kodak Employees’ Savings & Investment Plan l p.6

Many types of tax-advantaged retirement plans, such as the Eastman Kodak Employees’ Savings & Investment Plan (SIP), are subject to required minimum distributions (RMDs), which require you to take a minimum amount out of each account for the year you reach age 70½ and for each year thereafter (although some exceptions apply if you are still employed). Assets you withdraw generally qualify as income and are subject to income tax. RMDs apply to the following types of accounts:

Eastman Kodak Employees’ Savings & Investment Plan and certain other employer retirement plans IRAs (Traditional, Rollover, SEP, SIMPLE, and SAR-SEP) 403(b) plans

You usually must take your first RMD by April 1 of the year after you turn 70½.

For each year after the year in which you turn 70½, you must take an RMD by December 31.

Your RMD is based on your current age and your year-end account bal-ance for the prior year. Since both of these factors change each year, your RMD must be recalculated each year. If you have multiple retire-ment accounts, you must calculate the appropriate RMD for each one. It is important to know that RMDs are not optional—even if you don’t need the money. Any year that you don’t take your RMD, or take too little, the IRS may assess a penalty equal to 50% of the required amount not distributed by the deadline. RMDs do not apply to Roth IRA owners or to spousal beneficiaries who elect to treat the Roth IRA as their own.

Required Minimum Distributions: What you need to know

Eastman Kodak Employees’ Savings & Investment Plan l p.7

Focus on Your Goalssection 2

How do you know when the right moment has come to retire? This section can provide a framework to help you determine your retirement readiness.

Determining when to retire doesn’t have to be strictly a financial decision. Many people find that they prefer the activity and social interaction of working, and, if that’s the case, there’s no reason to rush into retirement. But often, the answer rests largely on whether you have the financial wherewithal to get by without a regular paycheck.

A good rule of thumb is that you may need to replace approximately 75% of your before-tax income when you retire. This percentage reflects the fact that everyday expenses typically decline in retirement (you are no longer saving for retirement) and assumes that you wish to continue the standard of living you enjoyed before retirement.

That 75% ideally should be composed of the following income sources: • 50% from your investments • 20% from Social Security • 5% from other sources (such as pension income or a part-time job)

These rules of thumb are not set in stone. You may decide that you want to simplify your life in retirement and don’t need to replace as much income. Or you may want the ability to spend more in retirement than you did when you were working, now that you’ll have more time to enjoy it. The choice is up to you, but you should be as realistic as possible about how much income you’ll needand whether your assets can produce it. To determine that, you must gauge how much income you can plan to take from your investments.

Determining How Much to Withdraw From Your Investments Gauging the correct amount to withdraw and spend annually from investments has always been a difficult decision for near-retirees. Withdraw too little annually, and you limit your options in the near term; withdraw too much, and you could face an empty nest egg in your later years.

T. Rowe Price has examined thousands of potential market scenarios to determine which withdrawal strategies generate the greatest probability of not running out of assets before the end of a 30-year retirement, lasting to age 95. The research demonstrated that an appropriate initial withdrawal amount is approximately 4% of your total retirement investments. Thereafter, the strategy assumes you will increase your withdrawal dollar amount by 3% each year to combat inflation.

Example. An initial withdrawal amount of 4% from a $500,000 asset base establishes $20,000 as the first year’s withdrawal (i.e., $500,000 x .04). In the second year of retirement, this initial amount is increased by 3%, or $600, for a total second-year withdrawal of $20,600 (i.e., $20,000 x 1.03). In the third year, the new amount is increased by 3% to $21,218 (i.e., $20,600 x 1.03).

This initial withdrawal amount may seem conservative, but our research shows that it will give your nest egg a better chance of lasting throughout retirement. Additionally, this conservative approach may limit the loss of principal if there is a market downturn early in your retirement, as well as provide a much greater chance that you will not outlive your assets, regardless of market volatility.

Rule of thumb: When planning to withdraw assets from your retirement investments for retirement spending, consider starting with an initial withdrawal amount of up to 4% and increase that dollar amount by 3% annually to account for inflation. See the research: If you would like to learn more about T. Rowe Price’s research into retirement withdrawal amounts, order the T. Rowe Price Retirement Savings Guide at troweprice.com. The guide includes analyses of numerous planning issues of value to near-term retirees.

Eastman Kodak Employees’ Savings & Investment Plan l p.8

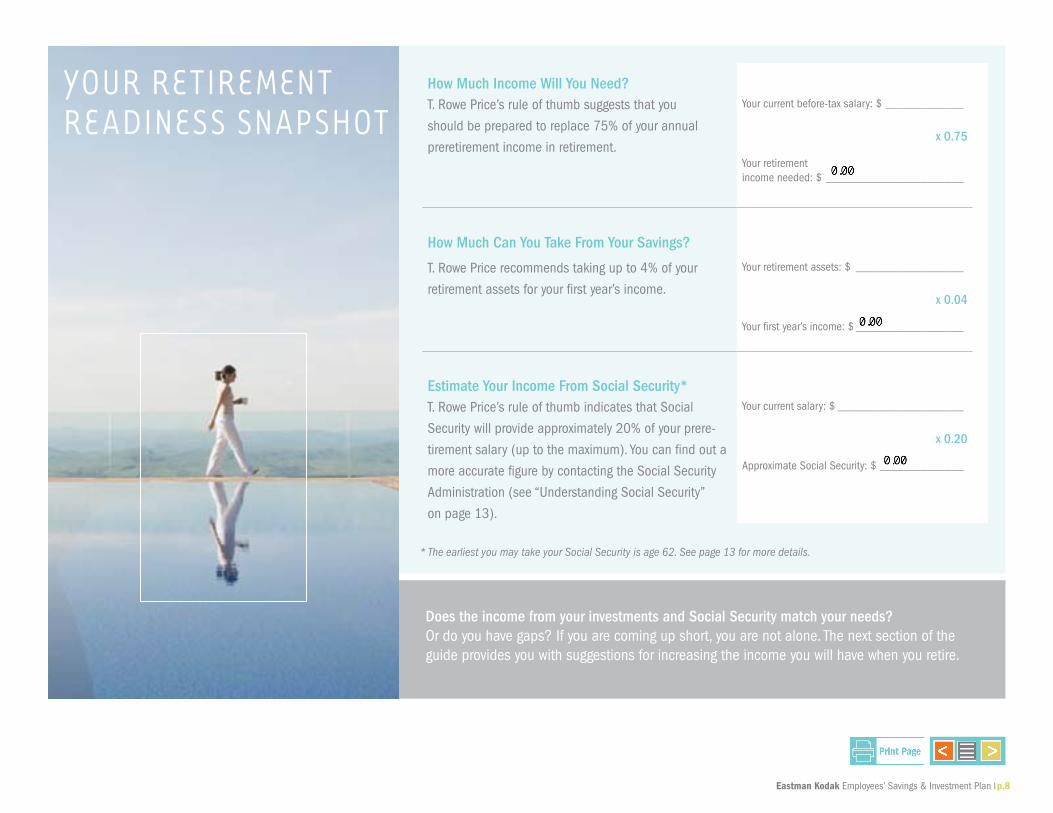

YouR RetIReMent ReADIneSS SnAPShot

Does the income from your investments and Social Security match your needs? Or do you have gaps? If you are coming up short, you are not alone. The next section of the guide provides you with suggestions for increasing the income you will have when you retire.

How Much Income Will You Need?T. Rowe Price’s rule of thumb suggests that you

should be prepared to replace 75% of your annual

preretirement income in retirement.

Your current before-tax salary: $ _____________

x 0.75

Your retirement income needed: $ _______________________

How Much Can You Take From Your Savings?

T. Rowe Price recommends taking up to 4% of your

retirement assets for your first year’s income.

Your retirement assets: $ __________________

x 0.04

Your first year’s income: $ __________________

Estimate Your Income From Social Security*T. Rowe Price’s rule of thumb indicates that Social

Security will provide approximately 20% of your prere-

tirement salary (up to the maximum). You can find out a

more accurate figure by contacting the Social Security

Administration (see “Understanding Social Security”

on page 13).

Your current salary: $ _____________________

x 0.20

Approximate Social Security: $ ______________

* The earliest you may take your Social Security is age 62. See page 13 for more details.

Eastman Kodak Employees’ Savings & Investment Plan l p.9

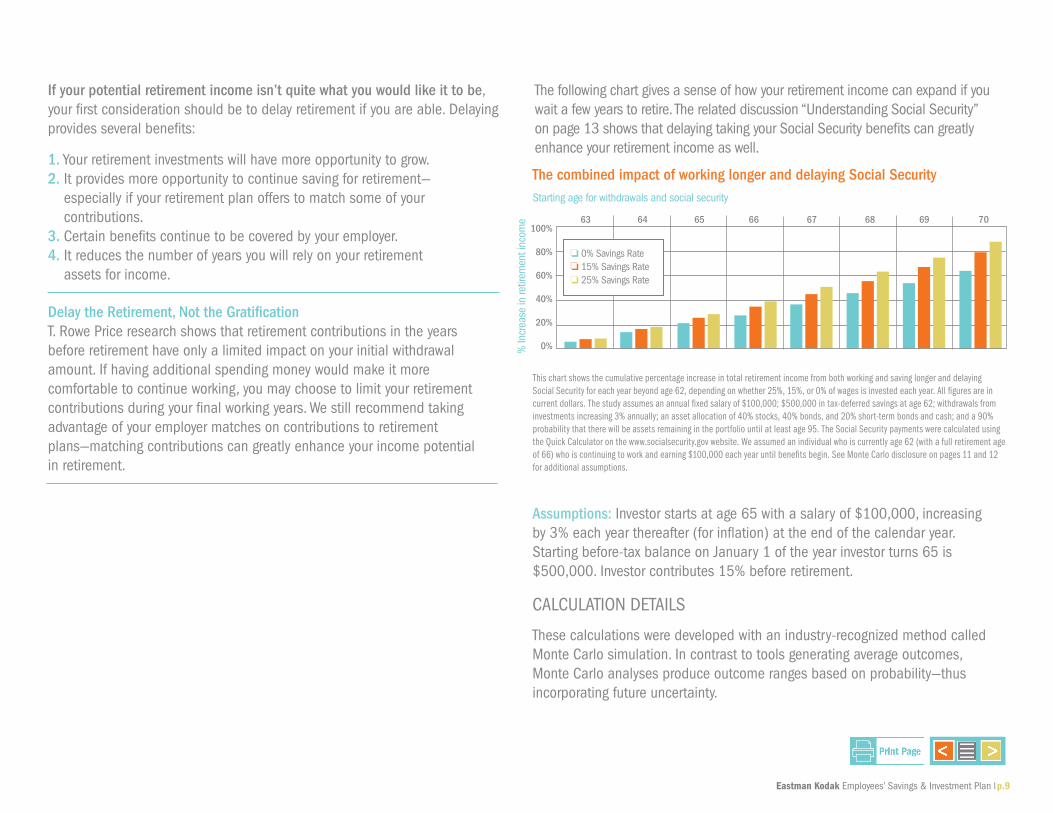

If your potential retirement income isn’t quite what you would like it to be, your first consideration should be to delay retirement if you are able. Delaying provides several benefits:

1. Your retirement investments will have more opportunity to grow. 2. It provides more opportunity to continue saving for retirement— especially if your retirement plan offers to match some of your contributions. 3. Certain benefits continue to be covered by your employer. 4. It reduces the number of years you will rely on your retirement assets for income.

The following chart gives a sense of how your retirement income can expand if you wait a few years to retire. The related discussion “Understanding Social Security” on page 13 shows that delaying taking your Social Security benefits can greatly enhance your retirement income as well.

Delay the Retirement, Not the GratificationT. Rowe Price research shows that retirement contributions in the years before retirement have only a limited impact on your initial withdrawal amount. If having additional spending money would make it more comfortable to continue working, you may choose to limit your retirement contributions during your final working years. We still recommend taking advantage of your employer matches on contributions to retirement plans—matching contributions can greatly enhance your income potential in retirement.

Assumptions: Investor starts at age 65 with a salary of $100,000, increasing by 3% each year thereafter (for inflation) at the end of the calendar year. Starting before-tax balance on January 1 of the year investor turns 65 is $500,000. Investor contributes 15% before retirement.

CALCULATION DETAILS These calculations were developed with an industry-recognized method called Monte Carlo simulation. In contrast to tools generating average outcomes, Monte Carlo analyses produce outcome ranges based on probability—thus incorporating future uncertainty.

The combined impact of working longer and delaying Social Security

63 64 65 66 67 68 69 70

Starting age for withdrawals and social security

o 0% Savings Rate o 15% Savings Rate o 25% Savings Rate

100%

80%

60%

40%

20%

0%% In

crea

se in

retir

emen

t inc

ome

This chart shows the cumulative percentage increase in total retirement income from both working and saving longer and delaying Social Security for each year beyond age 62, depending on whether 25%, 15%, or 0% of wages is invested each year. All figures are in current dollars. The study assumes an annual fixed salary of $100,000; $500,000 in tax-deferred savings at age 62; withdrawals from investments increasing 3% annually; an asset allocation of 40% stocks, 40% bonds, and 20% short-term bonds and cash; and a 90% probability that there will be assets remaining in the portfolio until at least age 95. The Social Security payments were calculated using the Quick Calculator on the www.socialsecurity.gov website. We assumed an individual who is currently age 62 (with a full retirement age of 66) who is continuing to work and earning $100,000 each year until benefits begin. See Monte Carlo disclosure on pages 11 and 12 for additional assumptions.

Eastman Kodak Employees’ Savings & Investment Plan l p.10

Material Assumptions include:

• Results of the analysis are driven primarily by the assumed long-term, compound rates of return of each asset class in the scenarios. Return assumptions take into consideration the impact of reinvested dividends and capital gains.

• The return assumption—plus assumptions about asset class volatility and correlations with other classes—are used to generate random monthly returns for each class over specified time periods.

• These monthly returns are then used to generate a wide range of investment market scenarios, representing a spectrum of possible performance for the modeled asset classes. Success rates are based on these scenarios.

• All initial withdrawal amounts—and all future contributions by active employees—are assumed to be pretax.

• No penalties are deducted for early withdrawals if taken while investor is under age 59½.

• The model assumes required minimum distributions (RMD) begin in the year the participant attains age 70½, even if the participant is actually still employed and exempt from taking RMDs until the year following retirement. Required amounts that exceed the planned withdrawals are reinvested in a taxable side account.

Material Limitations include:

• Extreme market movements may occur more often than in the model.

• Market crises can cause asset classes to perform similarly, lowering the accuracy of simulated portfolio volatility and returns. Correlation assumptions are less reliable for short periods.

• The model assumes no month-to-month correlations among asset class returns. It does not reflect the average periods of “bull” and “bear” markets, which can be longer than those modeled.

• Inflation is assumed to be constant, so variations are not reflected in our calculations.

• The analysis does not use all asset classes. Other asset classes may be similar or superior to those used.

Assumptions Used for Investment Analysis

The analysis includes all investments in a participant’s plan account, but categorizes them simply as stocks, bonds, and short-term investments. Short-term investments include cash, as well as short-term investment-grade bonds. An effectively diversified portfolio theoretically involves all investable asset classes, including stocks, bonds, real estate, foreign investments, commodities, precious metals, currencies, and others. Since it is unlikely that investors will have all of these asset class choices available in their plan, we selected the asset classes we believed to be most appropriate for long-term investors.

For active participants, the estimated plan account balance at retirement is based on the current balance and assumes that annual savings con-tinue at the same annual amount (adjusted by 3% annually to account for inflation) until retirement. The initial withdrawal amount is the percentage of the initial pretax value of the investments withdrawn in the first year, in today’s dollars. In subsequent years, the amount withdrawn is increased by 3% annually for inflation.

Eastman Kodak Employees’ Savings & Investment Plan l p.11

Results are based on simulating 1,000 possible market scenarios and various combined asset-allocation and withdrawal or contribution strategies. We show possible outcomes that, based on our simulations, can be achieved with 80% success. “Success” is defined as the investor having a non-zero balance remaining at the end of the withdrawal period identified by the tool. This means that we estimate that the investor faces an 80% likelihood that there will be some money left in their account at the end of the designated withdrawal period. Con-versely, there is an estimated 20% likelihood of running out of assets prior to the end of the designated withdrawal period. This means that in those 20% of cases, not all of the intended withdrawals can be made. There can be no assurance that the simulated results will be achieved or sustained.

Results of the analysis are driven primarily by the assumed long-term, compound rates of return of each asset class in the scenarios. Our corresponding assumptions, all presented in excess of 3% inflation, are as follows: for stocks, 4.90%; for bonds, 2.23%; and for short-term bonds, 1.38%. Investment expenses in the form of an expense ratio are subtracted from the return assumption as follows: for stocks, 0.70%; for bonds, 0.60%; and for short-term bonds, 0.55%. These expenses represent what we believe to be a reasonable approximation of the fees charged for investing in these asset classes through a professionally managed mutual fund or other pooled investment product.

Eastman Kodak Employees’ Savings & Investment Plan l p.12

Additional ways to stretch your dollarsIf you don’t want to wait to retire, there are other options that can make your retirement income go a little further.

Work in retirement. Employment, perhaps in a different field or part time, can supplement your income for a number of years after your “official” retirement. It may also provide needed benefits, such as medical insurance if you are under age 65.

Make beneficial choices with your home. There are several ways you can do this:

1. Downsize: Many retirees increase their investable assets by selling their home, buying something less expensive, and investing the difference. But even if a smaller house costs the same to purchase, you may still be able to save significantly in the future on annual upkeep and maintenance costs.

2. Move: Consider moving to a location where the cost of living will be significantly less. Reducing major costs such as property taxes can have a very positive impact on your budget.

3. Rent out a room (or a few): Taking in a tenant can provide income, companionship, and assistance with everyday chores. Check local laws for any restrictions.

Examine your spending. For a month or two, keep track of every expenditure—cash included. Use the information to help you make changes in your spending habits that could help you live on less income.

Reduce debt and limit credit card usage. High interest rates on credit cards can dramatically increase your expenses and eat a huge hole in your retirement budget. Plan to pay off your credit cards as quickly as possible, and try to avoid charging more to the card than you can pay off in a given month.

Consider an Alternative Option If you find that you may exhaust your traditional sources of income at some point in retirement, you may want to consider a reverse mortgage. A reverse mortgage may help you remain in your own home while enabling you to turn some of the equity in your home into cash. In these situations, the lender makes payments to you, rather than the other way around. One-time, annual, monthly, and line-of-credit advances are common distribution options. The money is not considered taxable income and generally does not affect your Medicare or Social Security benefits. However, you should not be planning to leave your house to heirs because it will be sold to repay the loan.

The loan must be paid back in full, plus interest and fees, in a number of different circumstances, including:

WHEN the borrower(s) no longer continues to occupy the property as a principal residence; WHEN the borrower(s) does not keep the taxes and insurance current or does not maintain the property; or WHEN the property is sold, transferred, or passed to heirs.

Because the conditions and fees that come with these loans can be complicated to understand, it is very important that before you enter into this type of loan agreement, you confer with a third-party advisor and discuss your choices with close members of your family, if appropriate. For more information, contact the National Center for Home Equity Conversion, the Federal Trade Commission (FTC), AARP, or the National Reverse Mortgage Lenders Association (NRMLA).

If you determine that you are not quite ready for retirement, the preparation you’ve done thus far—organizing your records and considering your income—can help make the retirement transition simpler when you do choose to undertake it. But even if you are ready, there remain two important issues you must work out before taking the retirement plunge: Social Security and health care.

Eastman Kodak Employees’ Savings & Investment Plan l p.13

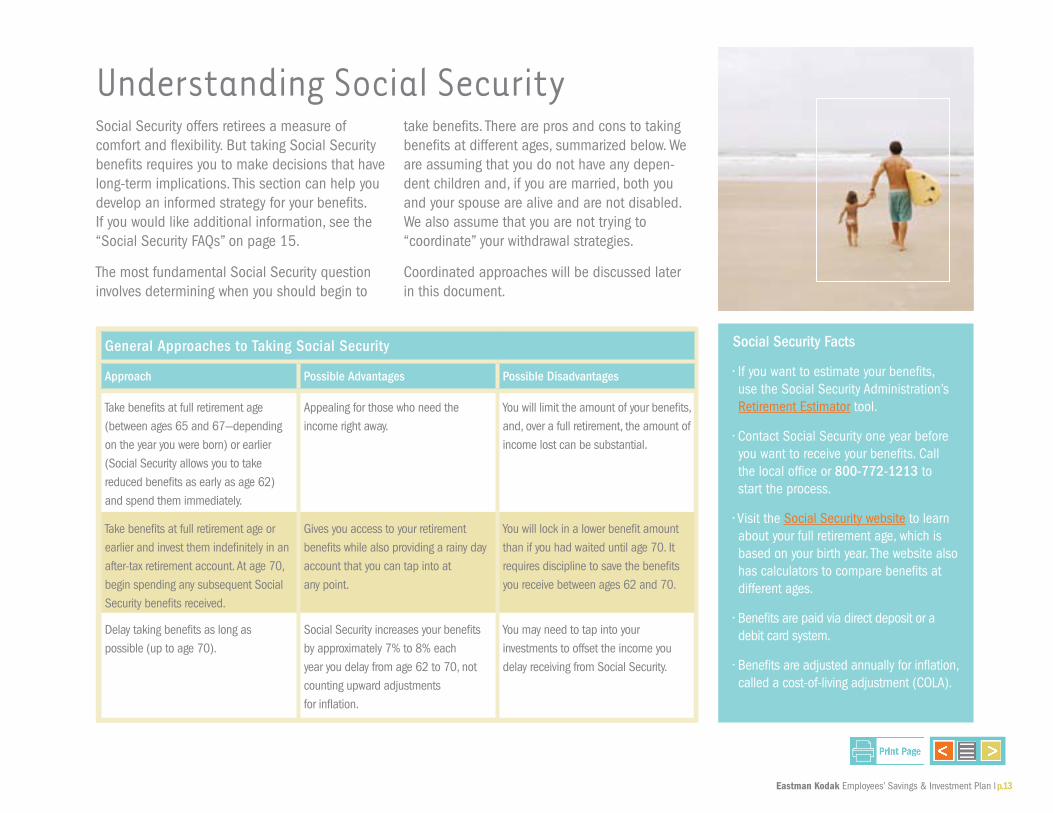

understanding Social SecuritySocial Security offers retirees a measure of comfort and flexibility. But taking Social Security benefits requires you to make decisions that have long-term implications. This section can help you develop an informed strategy for your benefits. If you would like additional information, see the “Social Security FAQs” on page 15.

The most fundamental Social Security question involves determining when you should begin to

take benefits. There are pros and cons to taking benefits at different ages, summarized below. We are assuming that you do not have any depen-dent children and, if you are married, both you and your spouse are alive and are not disabled. We also assume that you are not trying to “coordinate” your withdrawal strategies.

Coordinated approaches will be discussed later in this document.

Social Security Facts

• If you want to estimate your benefits, use the Social Security Administration’s Retirement Estimator tool.

• Contact Social Security one year before you want to receive your benefits. Call the local office or 800-772-1213 to start the process.

• Visit the Social Security website to learn about your full retirement age, which is based on your birth year. The website also has calculators to compare benefits at different ages.

• Benefits are paid via direct deposit or a debit card system.

• Benefits are adjusted annually for inflation, called a cost-of-living adjustment (COLA).

General Approaches to Taking Social Security

Approach Possible Advantages Possible Disadvantages

Take benefits at full retirement age (between ages 65 and 67—depending on the year you were born) or earlier (Social Security allows you to take reduced benefits as early as age 62) and spend them immediately.

Appealing for those who need the income right away.

You will limit the amount of your benefits, and, over a full retirement, the amount of income lost can be substantial.

Take benefits at full retirement age or earlier and invest them indefinitely in an after-tax retirement account. At age 70, begin spending any subsequent Social Security benefits received.

Gives you access to your retirement benefits while also providing a rainy day account that you can tap into at any point.

You will lock in a lower benefit amount than if you had waited until age 70. It requires discipline to save the benefits you receive between ages 62 and 70.

Delay taking benefits as long as possible (up to age 70).

Social Security increases your benefits by approximately 7% to 8% each year you delay from age 62 to 70, not counting upward adjustments for inflation.

You may need to tap into your investments to offset the income you delay receiving from Social Security.

Eastman Kodak Employees’ Savings & Investment Plan l p.14

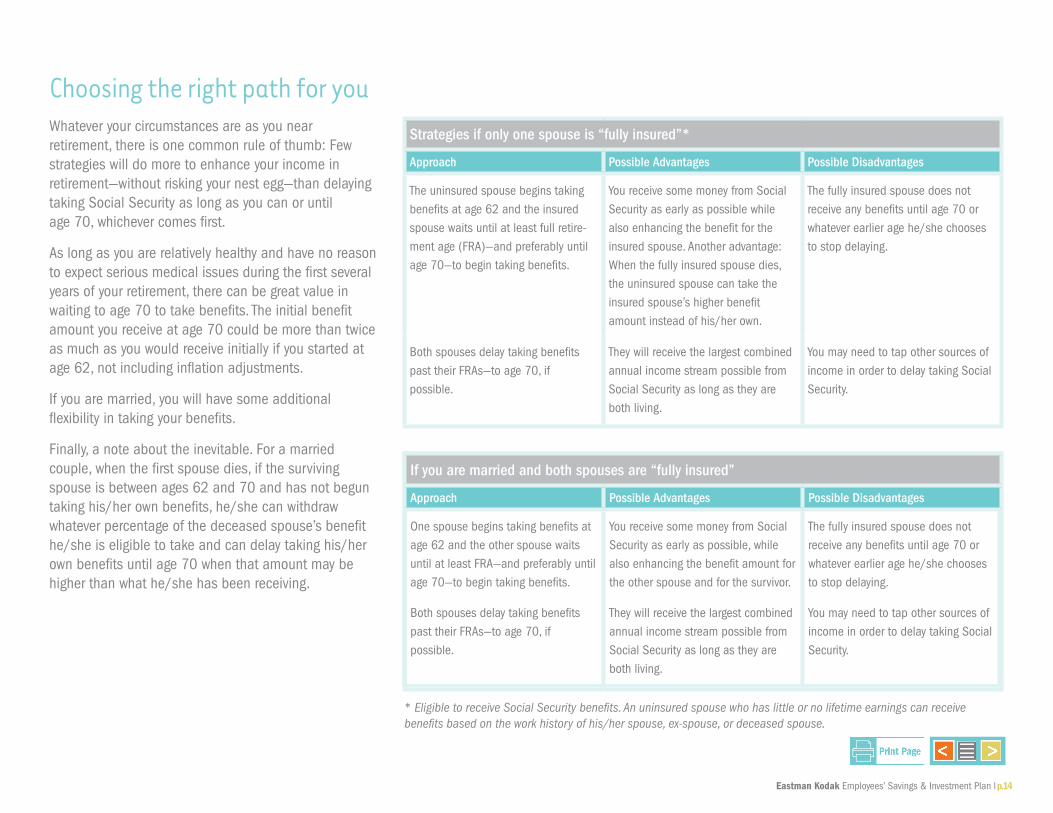

Choosing the right path for youWhatever your circumstances are as you near retirement, there is one common rule of thumb: Few strategies will do more to enhance your income in retirement—without risking your nest egg—than delaying taking Social Security as long as you can or until age 70, whichever comes first.

As long as you are relatively healthy and have no reason to expect serious medical issues during the first several years of your retirement, there can be great value in waiting to age 70 to take benefits. The initial benefit amount you receive at age 70 could be more than twice as much as you would receive initially if you started at age 62, not including inflation adjustments.

If you are married, you will have some additional flexibility in taking your benefits.

Finally, a note about the inevitable. For a married couple, when the first spouse dies, if the surviving spouse is between ages 62 and 70 and has not begun taking his/her own benefits, he/she can withdraw whatever percentage of the deceased spouse’s benefit he/she is eligible to take and can delay taking his/her own benefits until age 70 when that amount may be higher than what he/she has been receiving.

If you are married and both spouses are “fully insured”

Approach Possible Advantages Possible Disadvantages

One spouse begins taking benefits at age 62 and the other spouse waits until at least FRA—and preferably until age 70—to begin taking benefits.

Both spouses delay taking benefits past their FRAs—to age 70, if possible.

You receive some money from Social Security as early as possible, while also enhancing the benefit amount for the other spouse and for the survivor.

They will receive the largest combined annual income stream possible from Social Security as long as they are both living.

The fully insured spouse does not receive any benefits until age 70 or whatever earlier age he/she chooses to stop delaying.

You may need to tap other sources of income in order to delay taking Social Security.

Strategies if only one spouse is “fully insured”*

Approach Possible Advantages Possible Disadvantages

The uninsured spouse begins taking benefits at age 62 and the insured spouse waits until at least full retire-ment age (FRA)—and preferably until age 70—to begin taking benefits.

You receive some money from Social Security as early as possible while also enhancing the benefit for the insured spouse. Another advantage: When the fully insured spouse dies, the uninsured spouse can take the insured spouse’s higher benefit amount instead of his/her own.

The fully insured spouse does not receive any benefits until age 70 or whatever earlier age he/she chooses to stop delaying.

Both spouses delay taking benefits past their FRAs—to age 70, if possible.

They will receive the largest combined annual income stream possible from Social Security as long as they are both living.

You may need to tap other sources of income in order to delay taking Social Security.

* Eligible to receive Social Security benefits. An uninsured spouse who has little or no lifetime earnings can receive benefits based on the work history of his/her spouse, ex-spouse, or deceased spouse.

Eastman Kodak Employees’ Savings & Investment Plan l p.15

Social Security FAQs (For both married and single retirees)

How Can I Get the Most Out of My Social Security Benefits? Wait until as close as you can to age 70 before taking benefits. Each year you delay taking benefits after 65, your starting benefit amount increases by 7% to 8%, up to age 70—and that doesn’t include additional upward adjustments for inflation. However, you should not delay taking benefits beyond age 70, since your payments will not increase after that except for inflation.

In addition, the SSA determines your benefit as the average of your highest 35 years of income. The longer you continue to work, the more years of income (often higher income) will be incorporated into the calculation.

Social Security is a fundamental aspect of retirement for the vast majority of retirees. But the rules that govern benefits can be complex, and there’s often a lack of awareness and even misunderstanding among near-retirees about their benefit options and opportunities.

This short FAQ section can help you brush up on Social Security Administration (SSA) rules or act as a reference as you consider your personal retirement choices.

Q How do I become eligible to receive Social Security benefits?

A You are eligible to receive Social Security benefits if you are “fully insured.” This means that you have earned 40 credits—or have worked about 10 years. Generally speaking, you earn one credit for each quarter of each year you work.

Q When do I become eligible to take benefits?

A You become eligible for some Social Security benefits in the first full month you are age 62. However, the SSA considers age 62 to be an early retirement. Your “full retire-ment age,” or FRA, comes later, based on your year of birth. Generally, your FRA is on or between ages 65 and 67. You will receive the largest benefit amount by delaying initiation until age 70.

Q How does the SSA determine the amount of my benefit?

A The amount you receive from the SSA is based on your highest 35 years of income. If you work for less than 35 years, the amount included in the calculation for years you don’t work will be $0.

Q Do benefits change over time?

A Each year you receive Social Security benefits, the SSA increases your benefit for inflation, if applicable. This feature of Social Security is valuable because it will help you maintain your purchasing power throughout retirement.

Q What if I want to retire before I reach my FRA?

A If you elect to start receiving benefits between ages 62 and your FRA, you will receive a permanently reduced monthly income. Although your benefits will be adjusted annually for inflation, you will never receive as much annual income as you would have if you had delayed taking benefits until your FRA or later.

Q What happens if I delay taking benefits past my FRA?

A The SSA will automatically increase your annual benefit each year you delay taking

benefits up to age 70. The increase can be substantial—approximately 7% to 8% per year, before inflation.

Q How can I find out what my insured status is or what my benefits might be?

A The SSA is no longer sending annual statements. Instead, you can go online to estimate your benefits using the Retirement Estimator tool (www.ssa.gov). It allows you to run scenarios to see the amounts you would receive at any age, between 62 and 70. These figures are estimates in today’s dollars; by the time you actually begin taking your benefits, they are likely to be higher because the SSA adjusts all benefits annually based on the prior year’s inflation rate.

Eastman Kodak Employees’ Savings & Investment Plan l p.16

Q Does it make sense to earn income while also receiving SSA benefits?

A Taking benefits while still earning regular income makes sense in some situations more than others. You should be aware of limits and tax triggers:

If you start taking benefits before you attain your FRA and you earn wages, you will be subject to a relatively severe earn-ings limit (often referred to as “Reduced Retirement Benefits for Workers”). If you were under your FRA throughout 2011, for example, you were permitted to earn $14,160 in wages without having your Social Security benefits reduced. For every dollar you earned over $14,160, the SSA withheld $2 from your benefit. (In the year of your FRA but in the months before you attain it, the withholding is instead $1 for every $3 earned above a wage limit of $37,680.) However, you do not lose those benefits permanently. When you attain your FRA, the SSA recalculates your benefit amount and compensates you for the amounts you “lost” while you were working.

Once you attain your FRA, you will receive your full Social Security benefits regardless of how much you earn. Once you cross certain thresholds of “provisional income,” however, a portion of your benefits becomes subject to taxation.

At least 15% of your benefits will not be included in federal taxable income. Many states also do not tax or give a tax preference to Social Security income.

Q If I do not have enough work history to be fully insured but my spouse does, what benefits can I claim?

A The answer will vary depending on your circumstances:

If you are both living and remain married, you are eligible for 50% of your spouse’s Social Security benefit at your FRA.

If your spouse dies before taking Social Security benefits, you will be eligible to collect 100% of the benefit your spouse would have received at his/her FRA, adjusted for inflation, assuming you begin taking payments at your own FRA and not before.

If your spouse dies after taking benefits, you are eligible at your FRA to collect 100% of whatever your spouse’s benefit was at the time of death, adjusted for inflation.

Note that while you are allowed to take a spouse’s benefits ahead of your own FRA, you will be subject to reduction limits.

Q How does Social Security treat circum-stances of divorce and remarriage?

A Social Security provides you with potential rights to your former spouse’s benefits if you divorced after 10 or more years of marriage and are not currently married. Again, pro-fessional advice can be a valuable aid in determining what you might be entitled to and whether it is worthwhile to pursue.

Q My spouse and I are both fully insured for Social Security. How should we approach taking benefits?

A As long as you are both alive and remain married, you may receive Social Security benefits based solely on your own earnings or based on a formula that considers the combination of your and your spouse’s earn-ings—whichever is greater. Timing will also be a consideration.

If you are married and age 62 or older, you will need to decide at what ages you and your spouse should begin taking your respective Social Security benefits. And once one of you dies, the surviving spouse will need to decide at what age to take benefits based on his/her own earnings record, as well as when to begin taking benefits based on the deceased spouse’s earnings record. You may need the advice of a financial planner to compare options and make appropriate choices.

Eastman Kodak Employees’ Savings & Investment Plan l p.17

Health care costs may loom larger than any other single expense in your retire-ment; indeed, many retirees are shocked at how high their health care costs can become. Finding affordable medical insurance is a critical part of your retirement planning, particularly if you want to retire before age 65, the eligibil-ity age for Medicare. Individual or Consolidated Omnibus Budget Reconciliation Act (COBRA) health care insurance can be costly and no retirement planning is complete without a full accounting of your potential health care costs. It’s not easy to guess what your medical needs may be 20 years into the future or how their costs may change. However, you can prepare for three major categories of health care expenses:

1. Everyday expenses 2. Long-term care 3. Medicare and Medigap insurance premium costs

Everyday ExpensesYou’re likely to face outlays for medical insurance copays and deductibles, some prescription drugs, dental care, hearing aids and eyeglasses, depending on the nature of the overall medical insurance coverage you elect to purchase. And you should anticipate that your everyday health care expenses will rise over time.

It’s worth remembering that health and wellness are about more than doctors and hospitals. Well-being also comes from exercise, relaxation, and good habits, such as eating right and exercising throughout retirement.

As you plan for health expenses, consider the cost of activities that would promote good health—a pool or gym membership, for example. You may also think about the cost of home renovations that would make it easier to live with a potential future disability.

Long-Term CareMost health insurance and Medicare plans do not cover the costs of receiving long-term care that would provide assistance with everyday living expenses. For that type of coverage, a long-term care insurance policy must be purchased separately. Long-term care policies generally aren’t cheap, but they can provide considerable peace of mind. If you wish to purchase long-term care insurance, it’s usually better to do so sooner than later. The younger you are, the smaller your annual premiums will be—and the less likely you are to have preexisting medical conditions that could preclude your eligibility.

You can also choose a benefit amount/benefit period corresponding with a premium that fits your budget. Even if the insurance does not cover all of your expenses, it could reduce the overall financial burden your family would otherwise incur.

In some instances, what benefits you don’t receive during the benefit period can be extended until you finally deplete your coverage. Of course, the larger the benefit—and the longer the benefit period—the higher your premiums will be.

Make sure to review a variety of long-term care policies for types and lengths of coverage before you make your purchase. Since the coverage you purchase today is not likely to be worth as much 10 to 20 years from now, consider infla-tion protection, which may come in the form of a rider on your policy. Have an agent explain the different ways you may be able to purchase this benefit—and the pros and cons of each approach.

Plan for Medical Costs and Long-term Care

Medicare and Social Security The premiums for Parts A (if any), B, and D are set each year by the Centers for Medicare & Medicaid Services (CMS). These premiums are automatically deducted from any Social Security benefits you are receiving. Going forward, those individuals with an annual income over certain amounts will be charged more for their premiums.For a detailed look at Medicare basics and benefits, review Medicare & You. This publication is updated each year. For your convenience, you can receive updates automatically via e-mail.

Eastman Kodak Employees’ Savings & Investment Plan l p.18

A Primer on MedicareYou can’t plan for retirement without determining what kind of health insurance you want, and you can’t get health insurance in retirement without wading into the complicated waters of Medicare. Selecting policies and coverages can be a time-consuming and very personal decision. But the process can be easier if you have a grasp of Medicare fundamentals before you begin talking with Medicare representatives and Medigap health insurance providers.

Medicare consists of four parts:1. Part A is primarily a hospitalization benefit. It is generally premium-free—if you

paid Medicare taxes while working. However, for 2011, if you only had a history of between 30 and 39 quarters of Medicare-covered employment, you would pay $248 per month in retirement for Part A coverage; if you had a history of less than 30 quarters, you would pay $450 per month. The benefits cover the cost of hospitalization (except for any deductibles) but not any fees for doctors or procedures.

2. Part B covers doctors’ fees, outpatient services, and some limited home health care. The amount of the premium you pay for coverage depends on your marital status and income that year.

3. Part C, sometimes called Medicare Advantage, is another way to get your Medicare benefits. It combines Part A, Part B, and sometimes Part D (prescrip-tion drug) coverage. Services are typically provided through an HMO or PPO arrangement, and you are required to pay a premium.*

Note: Some retirees choose to forgo Part C in favor of a private fee-for-service or Medigap plan. These plans are generally more expensive but often provide more flexibility to choose your own service providers. It’s important to remem-ber that if you join a Medicare Advantage Plan, you don’t need (and cannot be sold) a Medigap policy. Be sure to study your choices carefully before making a selection.

4. Part D, the prescription drug plan, is available to those already enrolled in Parts A and B to cover some or all of the costs of prescription drugs. Depending once again on your marital status and income in retirement, you may be expected to pay a monthly premium for these benefits.

When you make your Medicare choices, it is vital to read the fine print: By enrolling in Medicare Part A (which is generally free), you are automatically

enrolled in Part B (which will charge you premiums) unless you proactively decline the coverage. Many types of Part C or private Medigap insurance already include prescription

drug coverage. If that’s the case, you may not need Part D. Ask your Part C insurance provider whether your plan is “creditable.”** If your

plan is creditable, be sure to obtain this information in writing. In this case, you may actually have better coverage than Part D, and purchasing Part D coverage might affect what you receive under Part C. If you select a private plan, be sure you are clear on where private coverage

ends and Medicare coverage begins.

Medicare Disability BenefitsYou will be automatically enrolled in Medicare after you receive Social Security disability benefits for two years. This starts 24 months from the month you were entitled to receive Social Security disability benefits. For more information, contact the Social Security Administration at 1-800-772-1213.

* Medicare & You 2011, Centers for Medicare & Medicaid Services, CMS Publication No. 10050, February 2011. **Creditable coverage is a plan that is as good as, or better than, Medicare Part D. Your employer can provide details on its drug benefits. 2008 Medicare Rights Center.

Eastman Kodak Employees’ Savings & Investment Plan l p.19

Timing is critical in making Medicare decisions: Medicare eligibility generally begins on the first day of the month you turn

age 65. Although the FRA for Social Security for today’s “boomers” is 66—and will rise

in the coming years to age 67 for younger beneficiaries—65 is expected to remain the age for Medicare eligibility. If you are taking Social Security prior to age 65, you should automatically

receive a Medicare health insurance card in the mail three months before your 65th birthday. If you are not planning to collect Social Security prior to age 65, you should

sign up for Medicare approximately three months before your 65th birthday (some exceptions apply, as outlined below). Just because you are eligible for Medicare doesn’t mean you need to enroll and

pay the premiums for Parts B, C, or D right away. If you or your spouse are still employed and already receiving adequate coverage from a current medical plan, you can save money by not enrolling until you retire. Once you retire (or if you are already retired at age 65), you will have a six-

month open period to enroll in a Medigap plan, starting with the first month you are age 65 or older and enrolled in Part B. It is advisable to enroll during the open enrollment period: You cannot be denied coverage or be charged more for coverage due to any current or preexisting health conditions. We recommend that you begin learning about Medicare at age 64 or earlier,

rather than waiting until age 65. In addition, over the next few years, it’s smart to learn about the major provisions of recent health care reform, which may affect your decisions. Finally, it is critical to pay attention to application deadlines and the rules associated with applying for benefits. If you enroll late or drop out and enroll again later, you may end up paying higher premiums for the same benefits.

The Costs of MedicareMedicare provides retirees with coverage and some peace of mind, but it’s not free. Unlike the COLAs for Social Security benefits, which are based each year on changes in the CPI, annual Medicare premium adjustments are based on increases in the actual costs of care, which have been increasing at an annual rate higher than the CPI. For those starting coverage in 2011, annual Medicare premiums for Part B alone can range from about $1,300 annually to more than $7,000—and that doesn’t include deductibles and copayments. Medicare’s Part D prescription drug insurance premiums are in addition to that, and there is a “donut hole” in drug coverage where you may choose private coverage (although, with recent legislation, the hole will gradually close over time, with specific provisions for new beneficiaries through 2020). You may also choose Part C to coordinate the other components, for an additional premium, or purchase Medigap insurance for health needs not covered by Medicare.

Eastman Kodak Employees’ Savings & Investment Plan l p.20

section 3 Make Your Vision a Reality

* The T. Rowe Price Retirement Date Trusts (the “Trusts”) are not mutual funds. They are common trust funds established by T. Rowe Price Trust Company under Mary-land banking law, and their units are exempt from registration under the Securities Act of 1933. Units of the Trusts are not deposits or obligations of, or guaranteed by, the U.S. government or its agencies or T. Rowe Price Trust Company and are subject to investment risks, including possible loss of principal.

The preparation is complete, and the major ques-tions have been answered. Your next step is to make some choices about your retirement portfolio.

First, you’ll need to consider what you currently own. If your retirement assets include a pension plan from a previous employer in addition to your retirement savings through your Eastman Kodak Employees’ Savings & Investment Plan (SIP) and other employer-sponsored plans, there are some steps you should consider right away.

Pension Plans. If you have a pension, you’ll need to make your payout elections. If you are married, you will have to choose “joint

and survivor” options unless both you and your spouse decline them. This type of payout guar-antees payments to you for your lifetime and a percentage to your spouse should he/she survive you. However, your payments are reduced to pay for your spouses payments when you die. You may also have the option of a lump-sum

payment, where you receive the entire amount at once. You assume the responsibility for investing the proceeds and making sure that you don’t run out of income from your investments.

Individual Stock. If you have large individual stock holdings, you should consider reducing your stock positions and moving the assets into a more diversified investment vehicle (such as a mutual fund). T. Rowe Price research has indicated that individual stock holdings can as much as double the day-to-day volatility in your portfolio. And the greater

the regular volatility, the less you can safely withdraw from your accounts for retirement income. Generally, you should consider reducing your individual stock holdings to 5% to 10% of your overall portfolio.

Feel the Flexibility. Because people have different experience and com-fort levels, SIP offers you three tiers to investing.

SIMPLE/TIER 1: The T. Rowe Price Retirement Date Trusts* If you’re not very comfortable with the idea of choosing specific investment options or determin-ing your own asset allocation or don’t care to spend a lot of time in making your investment choices, the simple Tier 1 approach could be right for you. Designed using 12 preselected Retirement Date Trusts, Tier 1 is for people who like having a diversi-fied retirement portfolio in one step.

How the Retirement Trusts work. The Retirement Date Trusts invest in up to five underlying trusts that include stocks, bond, and short-term investments. That means you get a portfolio that is profession-ally diversified among hundreds or even thousands of investments in large and small companies, both foreign and domestic. This gives you the benefit of the potential return from many areas of the market and exposure to each area’s unique risks.

Please note: The principal value of the Retirement Funds is not guaranteed at any time, including at or after the target date, which is the approximate date when investors turn age 65. The funds invest in a

broad range of underlying mutual funds that include stocks, bonds, and short-term investments and are subject to the risks of different areas of the market. The funds emphasize potential capital appreciation during the early phases of retirement asset accu-mulation, balance the need for appreciation with the need for income as retirement approaches, and focus more on income and principal stability during retirement. The funds maintain a substantial alloca-tion to equities both prior to and after the target date, which can result in greater volatility.

Diversification cannot assure a profit or protect against loss in a declining market. Call 1-800- SIP-4YOU (1-800-747-4968) to request a trust fact sheet, which includes investment objectives, risks, fees, expenses, and other information that you should read and consider carefully before investing.

TIERS 2 and 3: It’s your choice. If you prefer to have more control over your investment mix, these tiers might be right for you. They allow you to pick and choose from the SIP lineup of funds and from the universe of funds available through the TradeLink service. With these tiers, you can put together a portfolio that satisfies your own investment strategy and modify it over time.

Learn more about your investment style and SIP’s options online. You can learn about your risk tolerance with an online self-assessment and use free planning tools to help you select investments. It’s easy: Visit rps.troweprice.com and click on Tools.

Eastman Kodak Employees’ Savings & Investment Plan l p.21

Focus on Investing: three rules all retirees should considerT. Rowe Price planning professionals have focused attention on this critical stage in portfolio planning and have uncovered the following rules. Regardless of how large or small your portfolio is or what your investments are composed of, we believe these rules are vital to ensuring the long-term health of your retirement finances.

1. Lower inflation risk through effective allocation. Including an allocation to stocks or stock mutual funds in a retirement portfolio feels risky to some investors due to the inherent price volatility of the stock market. T. Rowe Price research has shown, however, that including stock funds in your retirement portfolio does not materially reduce your odds of success (that is, your odds of not running out of assets over your retirement time frame). As we’ve discussed, avoiding stocks can be even more problematic since keeping up with inflation will almost certainly require you to dip into principal over time.

You can use the principles of diversification to manage investment risk in your retirement portfolio. In a well-diversified portfolio, investments in some markets

should rise while others fall, muting overall volatility and keeping portfolio growth on track. Diversification cannot assure a profit or protect against loss in a declining market, but it is a good way to help control volatility in your portfolio.

2. Review your investment mix and your withdrawals periodically. Plan to rebalance your portfolio at least annually to maintain the overall asset allocation you have chosen.

3. Abide by the rules regarding taking required withdrawal amounts from certain retirement accounts. Once you turn 70½, you are required to withdraw minimum amounts each year from most types of retirement accounts (excluding Roth IRAs). These requirements, called required minimum distributions (RMDs), could have an impact on your retirement income plan by forcing you to with-draw more than you planned. You are always allowed to withdraw more than the RMD amounts from your accounts each year if you need to in order to meet expenses. See the related discussion, “Required Minimum Distributions: What You Need to Know,” on page 6.

* The number zero shows an investor at age 65. Use this as a reference to find your age (10 to the left of zero shows you at age 55, 10 to the right of zero shows you at age 75).

Investing by Time Horizon This chart makes it easy to discover an age-appropriate investment mix for retirement. Find your time horizon (shown in years across the top of the chart), and an age-appropriate portfolio will be directly below.

Years BEFORE You Retire Years AFTER You Retire

100% 20% 10% 20% 30%

80% 30% 40% 50%

60% 40% 20%

25 20 15 10 5 0* 5 10 15 20 25

Eastman Kodak Employees’ Savings & Investment Plan l p.22

Simplify Your Retirement Income DecisionsIntroducing T. Rowe Price Retirement Income ManagerSM Build your own retirement income plan with this new service.

With T. Rowe Price Retirement Income Manager, you can develop a personal retirement income strategy. You can start by viewing T. Rowe Price’s suggested monthly withdrawal strategy based on your age, contribution amount, and account balance. Then build your own retirement income plan—and compare the two.

Personalized*Displays current account information and balances.

ConvenientSuggests an initial gross monthly payment

FlexibleAllows you to customize key factors:• Payment amount• Age to begin withdrawals• Estimated payment length• Asset allocation

To try out this tool today, visit the website for SIP at rps.troweprice.com and click on the Tools icon at the top of the tools bar.

This interactive tool will help you estimate the retirement income you may expect to receive each month based on your current retirement balances, savings rates, age, and Social Security estimates. It will also help you address the following considerations:

Can you increase your retirement income? • Consider a more aggressive investment strategy, especially if you are not within 5 years of retirement. • Increase your contributions. • Delay your retirement a few years.

Other Resources In addition to resources provided throughout this guide—as well as the services available through SIP and T. Rowe Price—you may want to check out the following information:

AARPaarp.org1-888-687-2277

American Council of Life Insuranceacli.com1-202-624-2000

American Institute of Certified Public Accountantsaicpa.org1-888-777-7077

National Association of Personal Financial Advisors (NAPFA)napfa.org 1-800-366-2732

*When you are applying particular asset allocations to your individual situation, you should consider your other assets, income, and investments (e.g., equity in your home, IRA investments, savings accounts, and interests in any other employer plans) in addition to your assets in this plan.

105292_bro_csm_0611107537

12/11

T. Rowe Price Retirement Plan Services, Inc., its affiliates, and its associates do not provide legal or tax advice. Any tax-related discussion contained in this communication, including any attachments, is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax penalties or (ii) promoting, marketing, or recommending to any other party any transaction or matter addressed herein. Please consult your independent legal counsel and/or professional tax advisor regarding any legal or tax issues raised in this communication.

All information provided in this guide is subject to the terms of the applicable plan document, which will govern if there are any differences. The information is not intended to provide specific advice with respect to any individual’s situation and should not be construed as a recommendation to make any particular investment or take any other action. It is important to remember that you are responsible for your SIP invest-ments. Kodak reserves the right to amend or terminate any of its plans at any time.