Embed Size (px)

Citation preview

SEE Regional Investment SEE Regional Investment AspectsAspects

Geneva, 19 November 2003Geneva, 19 November 2003

Trajce Cerepnalkovski, Trajce Cerepnalkovski, Assistant General Director & Head of Development & Investment Assistant General Director & Head of Development & Investment DptDpt. & . & SECI Electricity Regional Projects CoordinatorSECI Electricity Regional Projects CoordinatorTlfTlf: +389 2 31 19 611; Fax: +389 2 31 11 160; : +389 2 31 19 611; Fax: +389 2 31 11 160; [email protected]@esmak.com.mk

UNECE Committee on Sustainable Energy

Roundtable: Facilitating Investment in the Transition Economies

Contents:Contents:

•• Introduction & SEE Region DefinitionIntroduction & SEE Region Definition• SEE Power Sector Regional Investment aspects• Obstacles to Investment, Consideration• Internal MKD restructuring progress• Near term investment options in MKD

SEESEE

EUROPEEUROPE

IntroductionIntroduction & SEE Region Definition& SEE Region Definition•• Transition, followed with war Transition, followed with war •• Transition affected the Power Systems, main Transition affected the Power Systems, main

result disconnection from the main UCTE gridresult disconnection from the main UCTE grid•• Power systems ensured secure supply Power systems ensured secure supply •• Big differences (economic, culture, development: Big differences (economic, culture, development:

GDP from 1,000 GDP from 1,000 -- >10,000 $/capita)>10,000 $/capita)•• Clear declaration to joint EUClear declaration to joint EU

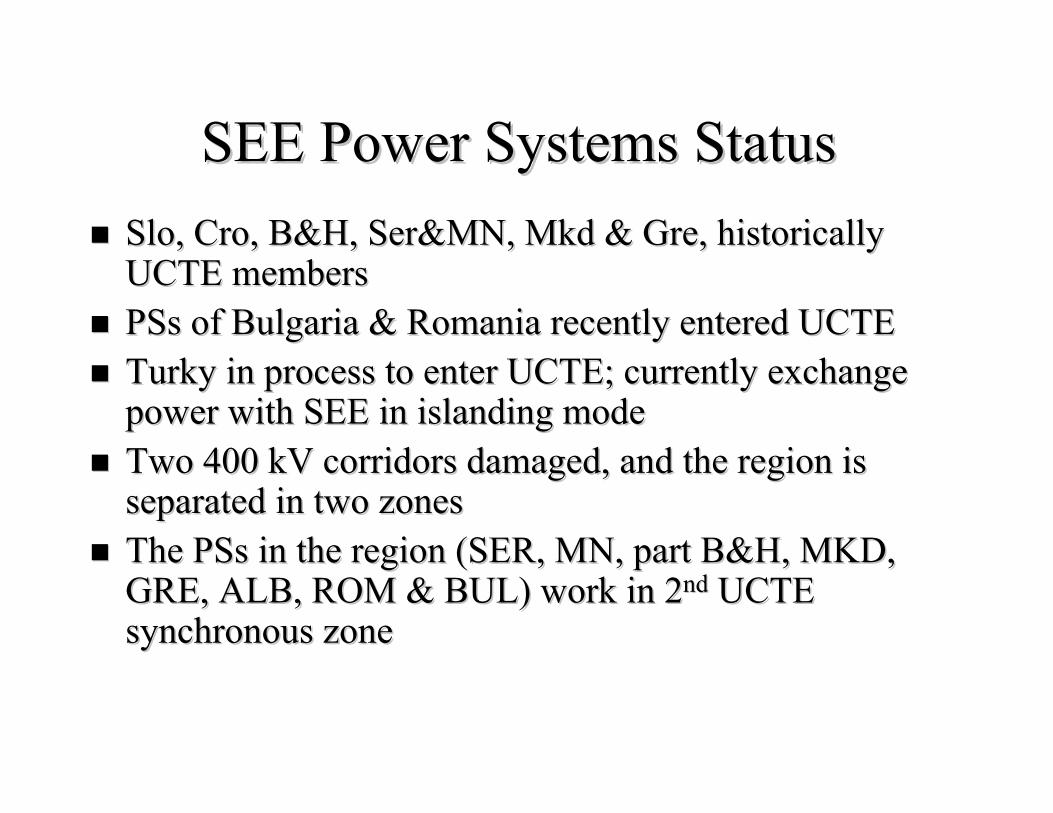

SEE Power Systems StatusSEE Power Systems StatusSloSlo, , CroCro, B&H, Ser&MN, , B&H, Ser&MN, MkdMkd & & GreGre, historically , historically UCTE members UCTE members PSsPSs of Bulgaria & Romania recently entered UCTE of Bulgaria & Romania recently entered UCTE TurkyTurky in process to enter UCTE; currently exchange in process to enter UCTE; currently exchange power with SEE in islanding modepower with SEE in islanding modeTwo 400 kV corridors damaged, and the region is Two 400 kV corridors damaged, and the region is separated in two zonesseparated in two zonesThe The PSsPSs in the region (SER, MN, part B&H, MKD, in the region (SER, MN, part B&H, MKD, GRE, ALB, ROM & BUL) work in 2GRE, ALB, ROM & BUL) work in 2ndnd UCTE UCTE synchronous zonesynchronous zone

UCTE

2nd

UCTE Zone

Ukr

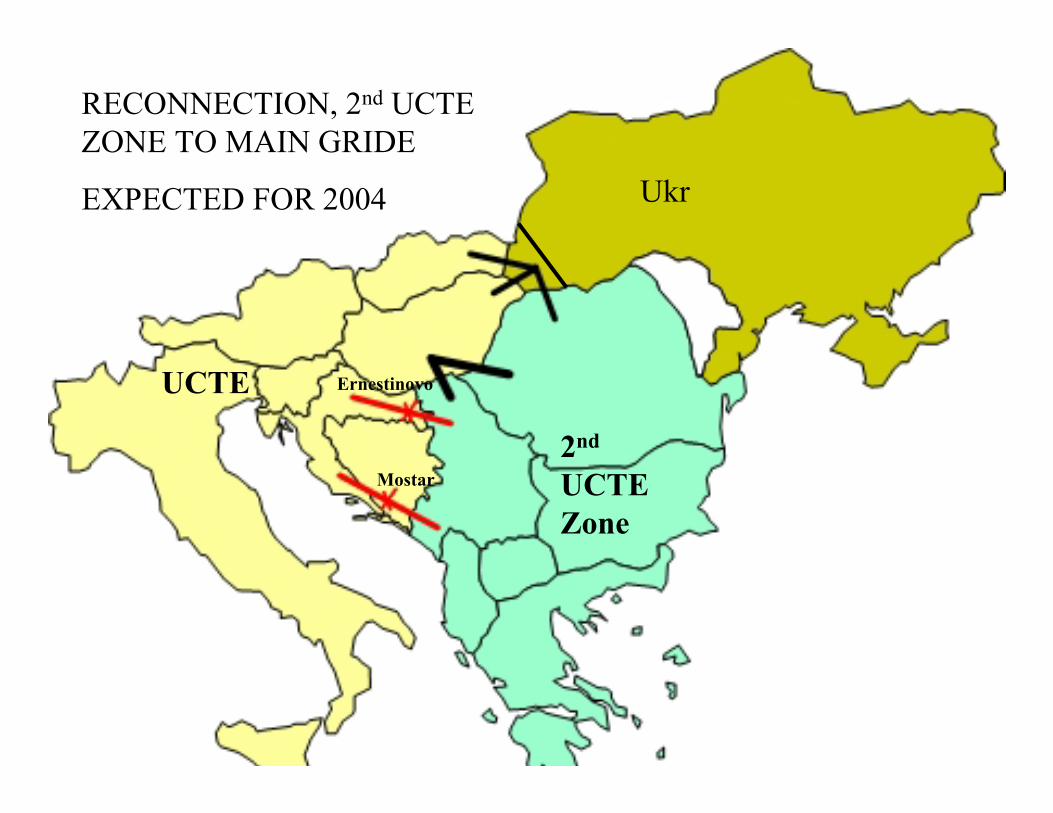

RECONNECTION, 2nd UCTE ZONE TO MAIN GRIDE

EXPECTED FOR 2004

Ernestinovo

Mostar

Reconnection of the 2Reconnection of the 2ndnd Zone to Zone to main UCTE Gridmain UCTE Grid

Long lasting processLong lasting processUCTE, SUDEL, UCTE, SUDEL, IFIsIFIs, others, othersDepends on reconstruction of two 400 kV Depends on reconstruction of two 400 kV Corridors (S/S Corridors (S/S ErnestinovoErnestinovo & S/S & S/S MostarMostar))UCTE Executive teamUCTE Executive teamReconnection expected for 2004!?Reconnection expected for 2004!?

Regional investment approachRegional investment approach

• SEE REM development as driving factor for regional investment approach and regional investment prioritizing

• Solutions to national energy issues based on isolated national markets are neither capable nor desirable as a means to satisfy regional supply and demand imbalances

• Balance between national & regional approach

Demand and supply outlook 2003-2012

• An average growth rate of about 2.3% is expected by regional utilities

• The region aims to add a net new capacity of about 4500 MW through 2012

• Rehabilitation of about 4000 MW of existing capacity would be required

• Without investments in generation the region may loose up to 6500 MW

Regional Interconnection

Aspects

Based on SECI Transmission Planning Project

Maritza 3

Hamidabat

BabaeskiPhillipi

Blagoevgrad

Thessaloniki

Florina

Kardia

Bitola

Dubrovo

Stip

Skopje 5

Nis

Kozloduj

TintareniPortiledeFi

erDjerdap

Arad

Oradea

Rosiori

Sandorfalva

Pecs

Heviz

Zerjavinec

Tumbri

Divaca

Meline

Ernestinovo

Ugljevik

Sombor Subotica

S.Mitrovica

Konjsko Mostar

TrebinjeRibarevine

Podgorica

Tirana

Elbasan

Kosovo BC. Mogila

Sofia West

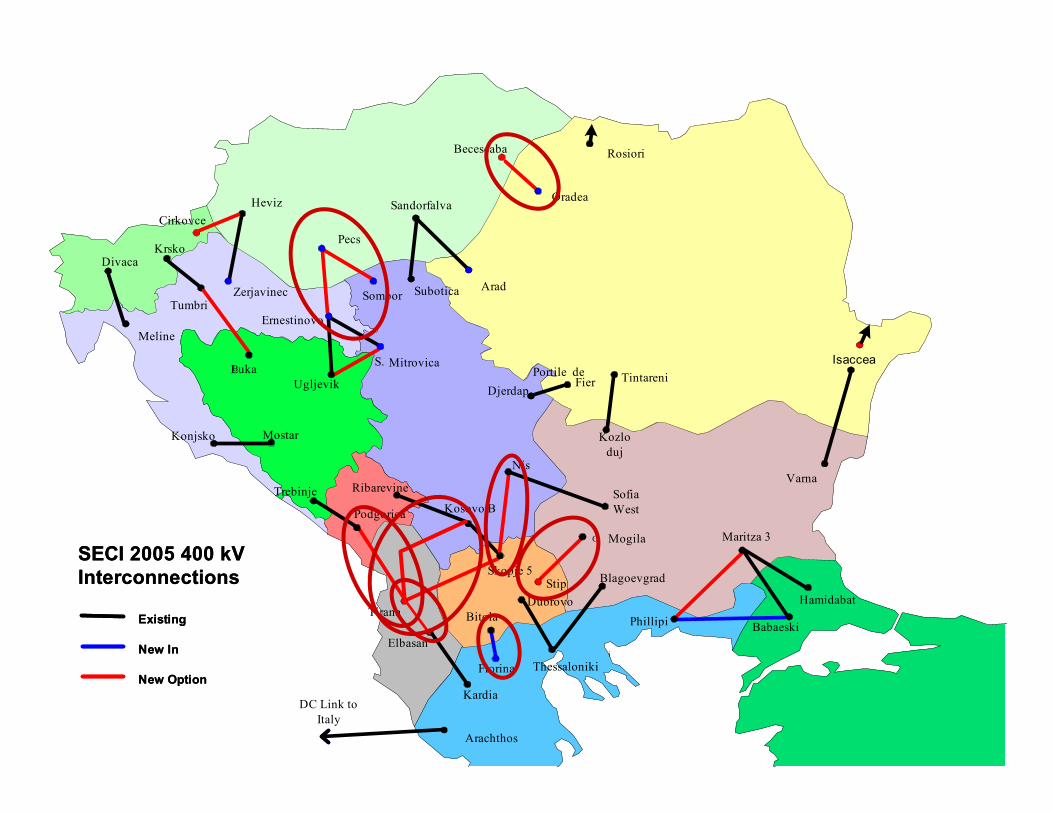

SECI 2005 400 kVInterconnections

Existing

New In

New Option

Krsko

Isaccea

Cirkovce

Becescaba

Varna

B. Luka

Arachthos

Maritza 3

Hamidabat

BabaeskiPhillipi

Blagoevgrad

ThessalonikiFlorina

Kardia

BitolaDubrovo

StipSkopje 5

Nis

Kozloduj

TintareniPortile deFier

Djerdap

Arad

Oradea

Rosiori

Sandorfalva

Pecs

Heviz

ZerjavinecTumbri

Divaca

MelineErnestinovo

Ugljevik

Sombor Subotica

S. Mitrovica

Konjsko Mostar

Trebinje Ribarevine

Podgorica

Tirana

Elbasan

Kosovo B

C. Mogila

SofiaWest

SECI 2005 400 kVInterconnections

Existing

New In

New Option

Krsko

Isaccea

Cirkovce

Becescaba

Varna

B.Luka

Arachthos

DC Link toItaly

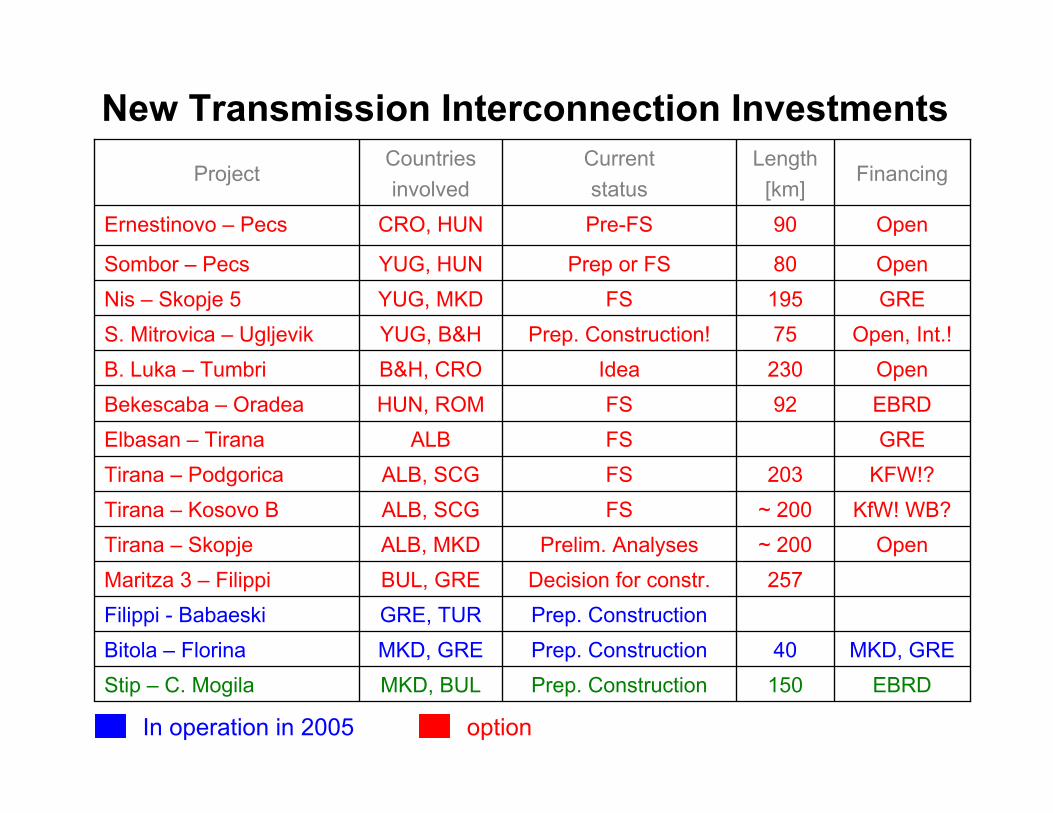

257Decision for constr.BUL, GREMaritza 3 – FilippiPrep. ConstructionGRE, TURFilippi - Babaeski

EBRD150Prep. ConstructionMKD, BULStip – C. MogilaMKD, GRE40Prep. ConstructionMKD, GREBitola – Florina

Open~ 200Prelim. AnalysesALB, MKDTirana – SkopjeKfW! WB?~ 200FSALB, SCGTirana – Kosovo B

KFW!?203FSALB, SCGTirana – PodgoricaGREFSALBElbasan – Tirana

EBRD92FSHUN, ROMBekescaba – OradeaOpen230IdeaB&H, CROB. Luka – Tumbri

Open, Int.!75Prep. Construction!YUG, B&HS. Mitrovica – UgljevikGRE195FSYUG, MKDNis – Skopje 5Open80Prep or FSYUG, HUNSombor – Pecs

Open90Pre-FSCRO, HUNErnestinovo – Pecs

FinancingLength

[km]Currentstatus

Countriesinvolved

Project

New Transmission Interconnection Investments

In operation in 2005 option

SEESEE

EUROPEEUROPE

Regional Teleinformation

Aspects

Based on SECI TeleinformationProject

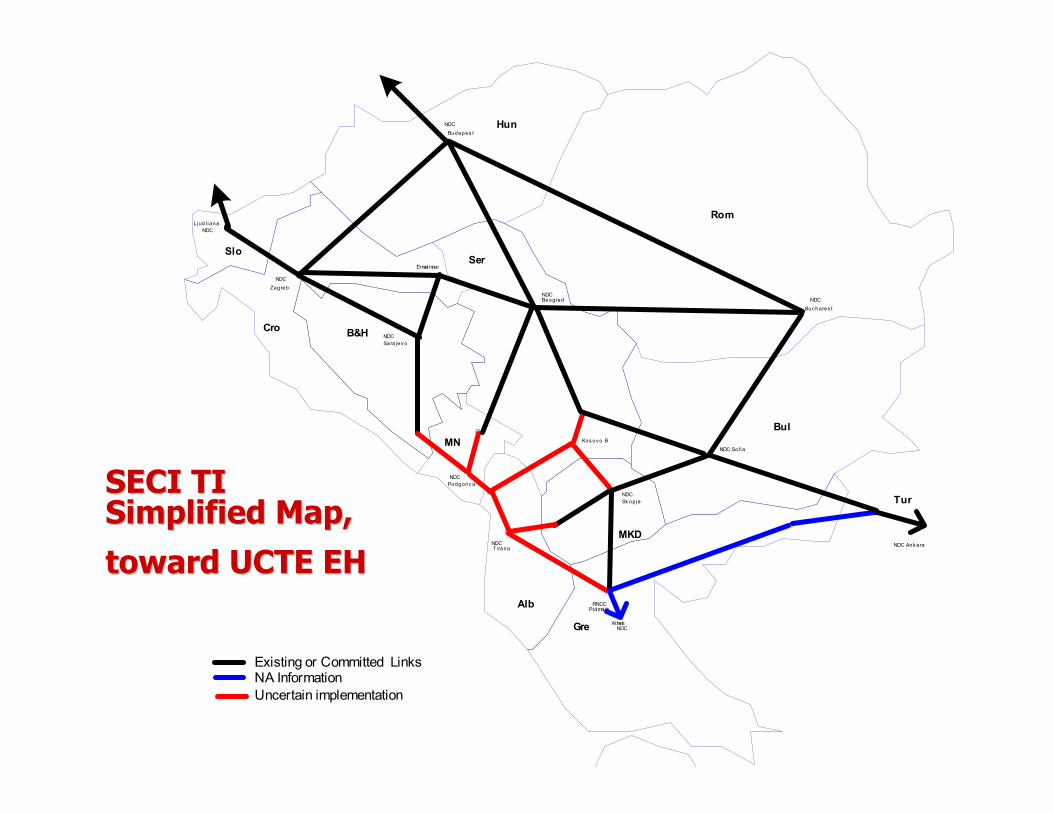

SECI TI SECI TI Simplified Map, Simplified Map,

toward UCTE EHtoward UCTE EH

NA InformationExisting or Committed Links

NDC Sofia

NDCTirana

Kos ov o B

NDCPodgoric a

RNCCPtolmaida

NDCAthens

NDCBudapes t

Ljub l ianaNDC

Ernestinovo

NDCZagreb

NDCSara jev o

NDCBeograd

NDC Ank ara

NDCSk opje

NDCBuc hares t

Gre

Tur

Bul

Rom

Hun

Slo

Cro B&H

Alb

MKD

Ser

MN

Uncertain implementation

3

7

1

9

120

121

23

KESH NDCTirana

Elbasan 220

Prizren

4

5

Kardia

Fierze

Kosovo BTrebinje

NDC EPCG

Podgorica

Nis

139

145

142

Tivat

143

144

Cetinje

Budva

153

Elbasan 400

Qafathan

6

140Mojkovac

H. Novi

Struga

Ribarevine

Vau Dejes

2

8

141

160

Pod. 2

Pod. 1161

Albania

Serbia

Montenegro

Skopje 5

SECI New BuildCountry Borders

Existing SDH Equipment

New SDH EquipmentInterface

Existing Comm Link

Optional Links

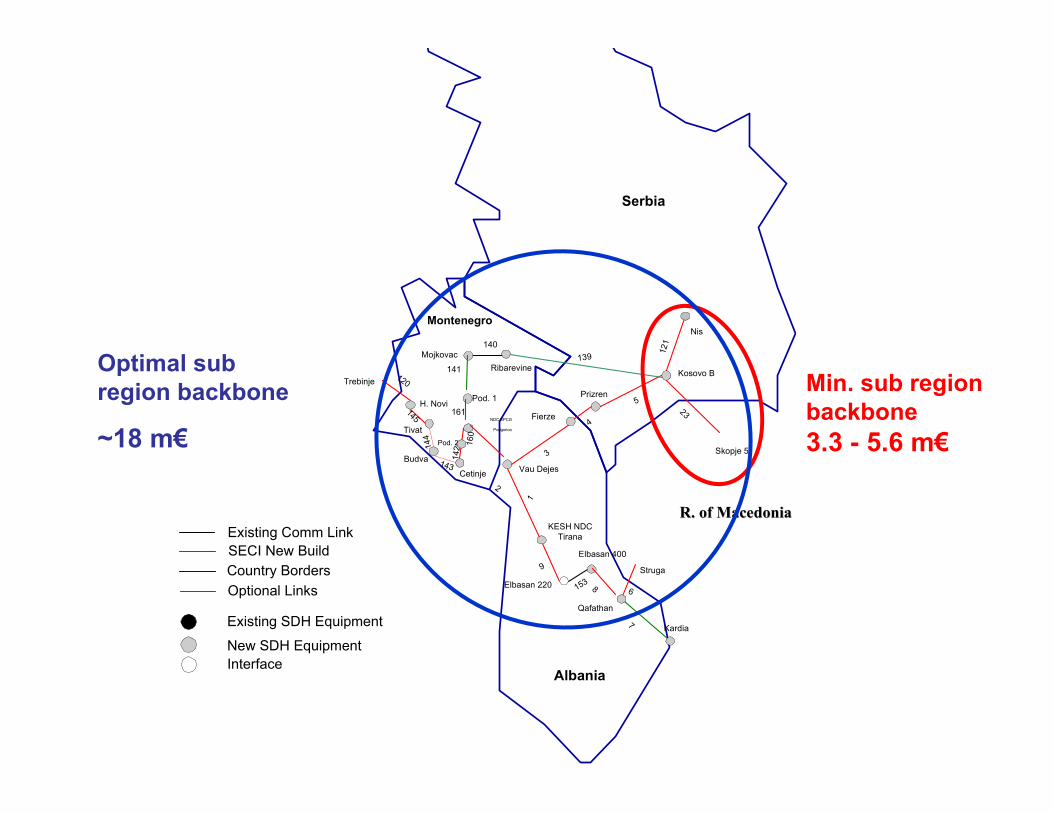

R. of MacedoniaR. of Macedonia

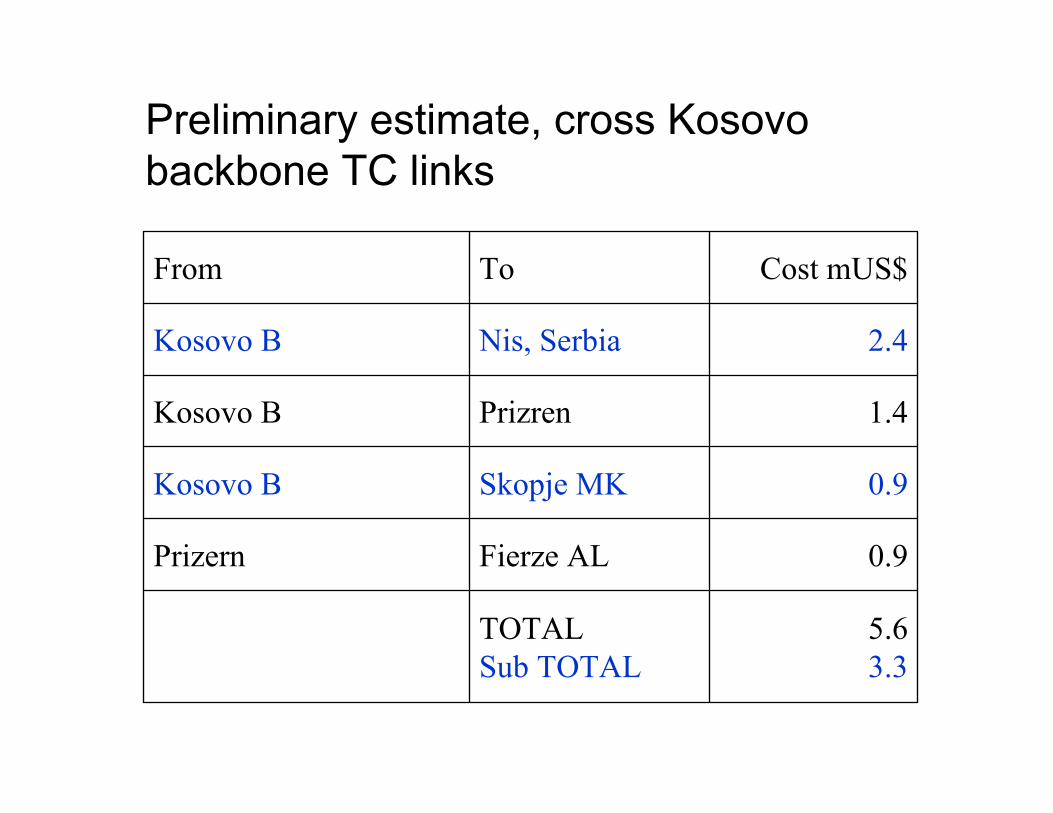

Min. sub regionbackbone3.3 - 5.6 m€

Optimal sub region backbone

~18 m€

5.63.3

TOTALSub TOTAL

0.9Fierze ALPrizern

0.9Skopje MKKosovo B

1.4PrizrenKosovo B

2.4Nis, SerbiaKosovo B

Cost mUS$ToFrom

Preliminary estimate, cross Kosovo backbone TC links

Investment Aspects Consideration

• Investment in G in SEE– Investment in G, considered as commercial!– IFIs generally avoids direct involvements– Market challenges private Investments!?

• Obstacles & Risks- Political background- Economic development- Social implications

Political Background• War conflict reconciliation• Important influence of international

community• Even two territories with UN missions

(UNMIK)• Other (even names of the counties!)

Economic & Social Background

• Different level of economic development within the Region (GDP varies between 1000 Euro/capita – 10000 Euro/capita)

• Level of political risk for investors• Ad hoc support measures• Increasing social gaps (unemployment) • Implication of the reform to the social

status of the citizens (energy price, receivables collection)

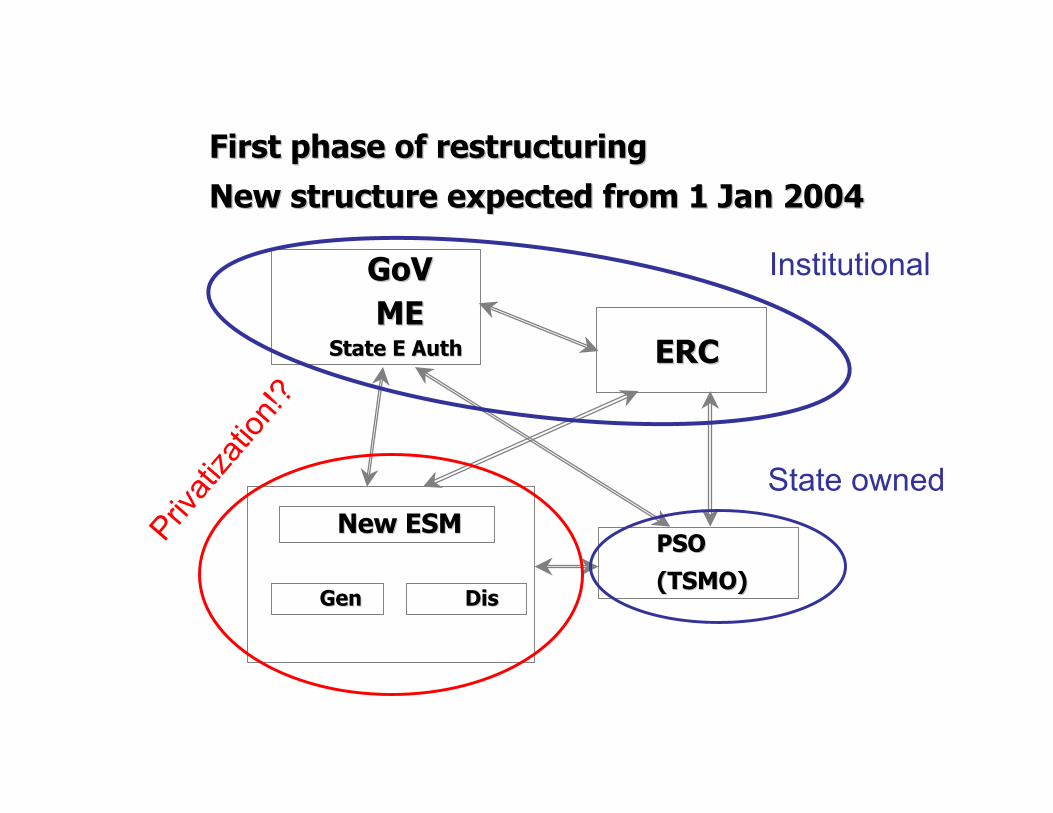

Macedonian Power Sector Restructuring

& Privatization of ESM

GoVGoVMEME

State E Auth State E Auth ERCERC

New ESMNew ESM

GenGen DisDis

PSO PSO

(TSMO)(TSMO)

First phase of restructuringFirst phase of restructuring

New structure expected from 1 Jan 2004New structure expected from 1 Jan 2004Priv

atiza

tion!?

State owned

Institutional

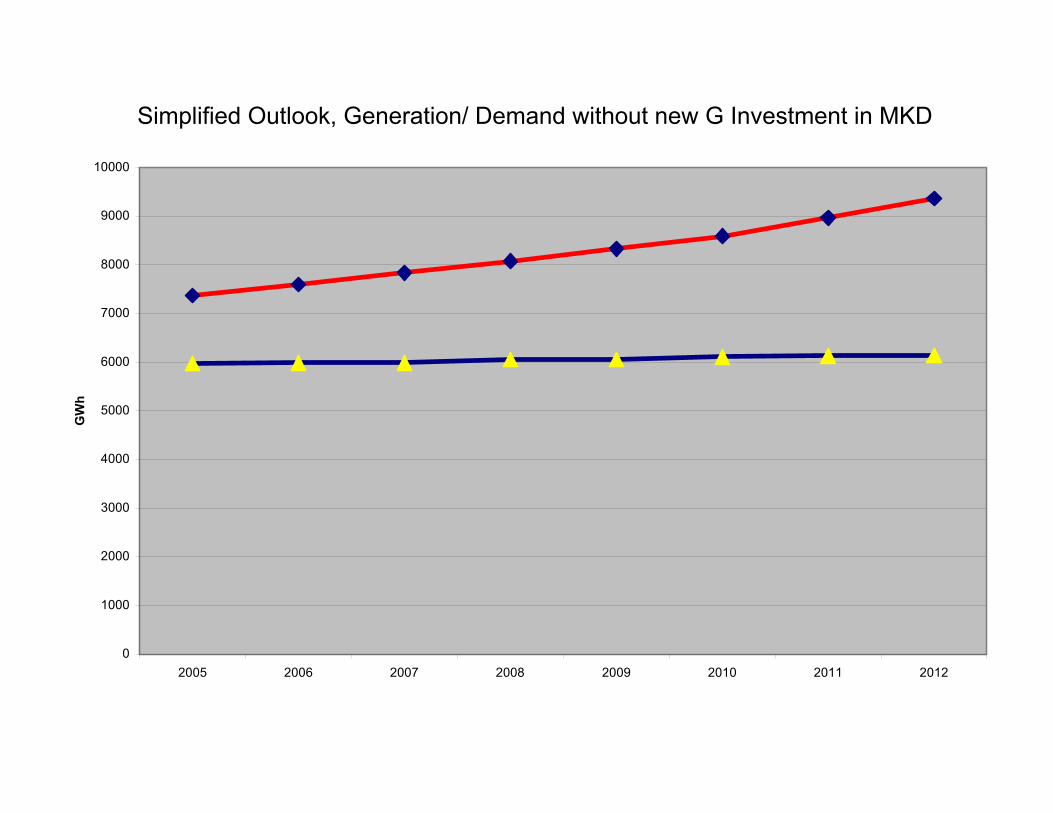

Near term investment needs in Power Sector in

Macedonia

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2005 2006 2007 2008 2009 2010 2011 2012

GW

h

Simplified Outlook, Generation/ Demand without new G Investment in MKD

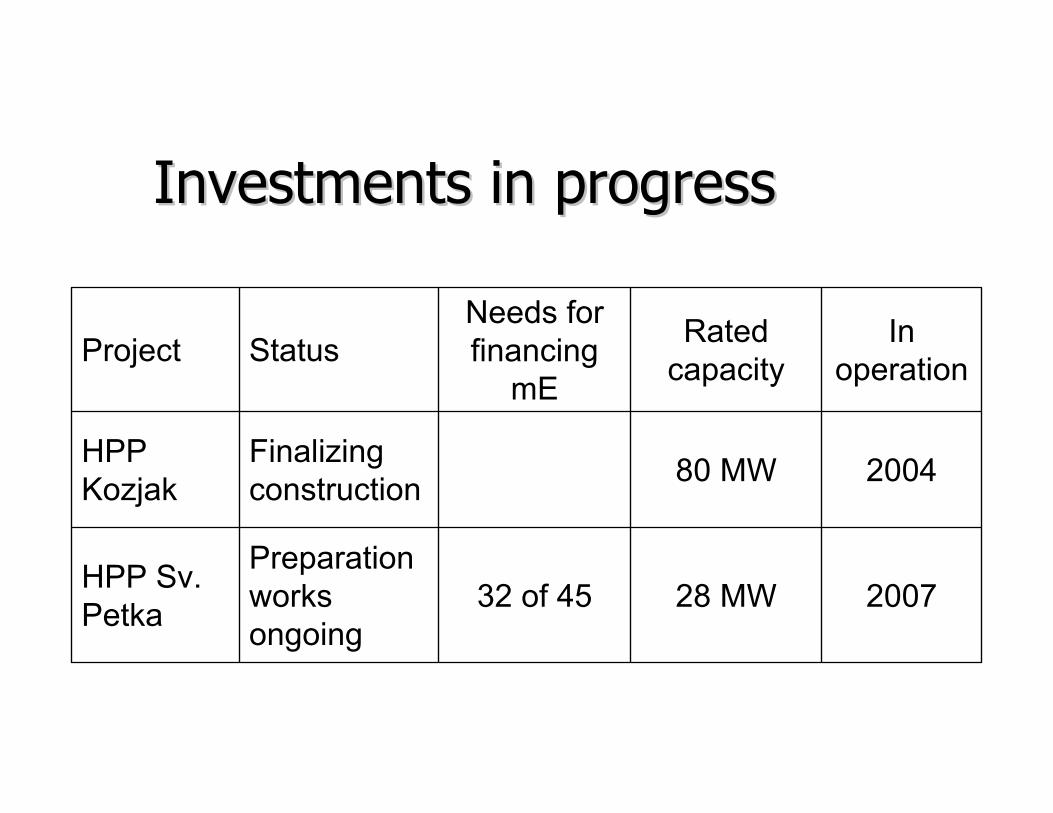

200728 MW32 of 45 Preparation works ongoing

HPP Sv. Petka

200480 MWFinalizing construction

HPP Kozjak

In operation

Rated capacity

Needs for financing

mEStatusProject

Investments in progressInvestments in progress

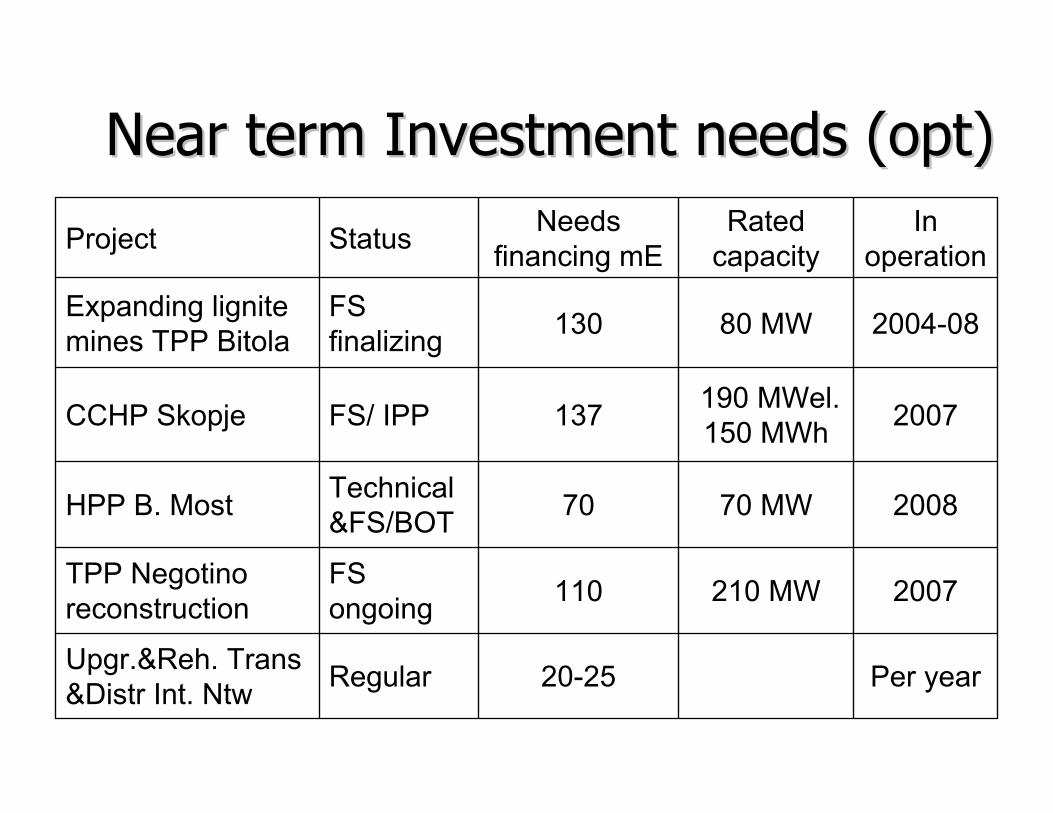

Per year20-25Regular Upgr.&Reh. Trans &Distr Int. Ntw

2007210 MW110FS ongoing

TPP Negotinoreconstruction

200870 MW70Technical &FS/BOTHPP B. Most

2007190 MWel. 150 MWh137FS/ IPP CCHP Skopje

2004-0880 MW130FS finalizing

Expanding lignite mines TPP Bitola

In operation

Rated capacity

Needs financing mEStatusProject

Near term Investment needs (opt)Near term Investment needs (opt)

SECI

&

ESM

END