Embed Size (px)

Citation preview

www. erranet.org

Security of supply in CSEE

Region

Märt Ots

Chairman

ERRA

Budapest, 14.06.2018

2

ERRA

The Energy Regulators Regional Association (ERRA) is a voluntary organization comprising of independent energy regulatory bodies primarily from Europe, Asia, Africa, Middle East, South and North America. Purpose & Objectives •To improve national energy regulation in member countries; •To foster development of stable energy regulators with autonomy and authority; •To improve cooperation among energy regulators; •To facilitate the exchange of information, research, training and experience among members and other regulators around the world. Legal status ERRA is an inter-institutional organisation registered in Hungary based on the Law 2016.LXXXV. The Ministry of Foreign Affairs and Trade of Hungary is the registration and supervision organ of ERRA.

3

ERRA Members

31 Full Members: Albania, Armenia, Azerbaijan, Bhutan, Bosnia & Herzegovina, Bulgaria, Cameroon,

Croatia, Estonia, Georgia, Hungary, Kazakhstan, Kyrgyz Republic, Latvia, Lithuania, Macedonia, Moldova, Mongolia, Nigeria, Oman, Pakistan, Palestine, Poland, Romania, Russia, Saudi Arabia, Serbia, Slovakia, Turkey, Ukraine, United Arab Emirates

10 Associate Members: Energy Regulatory Agency of Azerbaijan, Regulatory Commission for Energy in

Federation of BiH, Regulatory Commission for Energy of Republika Srpska (BiH), Egypt, ERERA (ECOWAS Regional Electricity Regulatory Authority), Ghana, Jordan, Peru, Energy Regulatory Office of UNMIK, NARUC (National Association of Regulatory Utility Commissioners, USA)

4

• Market Monitoring Activities of Energy Regulatory Commissions

• Price Regulation and Tariffs

• Renewable Energy Regulation

• Principles of Electricity Markets

• Introduction to Energy Regulation (ERRA Summer School)

• Seminar for Newly Appointed Commissioners and Chairmen

• Principles of Natural Gas Market Regulation

• Training Course for Regulators from Emerging Economies

• Introduction to Water Utility Regulation

• Educational Workshops: Balancing Markets; Network Codes; Energy Efficiency; CAPEX; Innovation and Regulation

ERRA Training Courses

5

Security of supply in European contexts

EU is net importer of energy.

Power systems are mostly synchronous.

Important subject is security in gas supply.

6

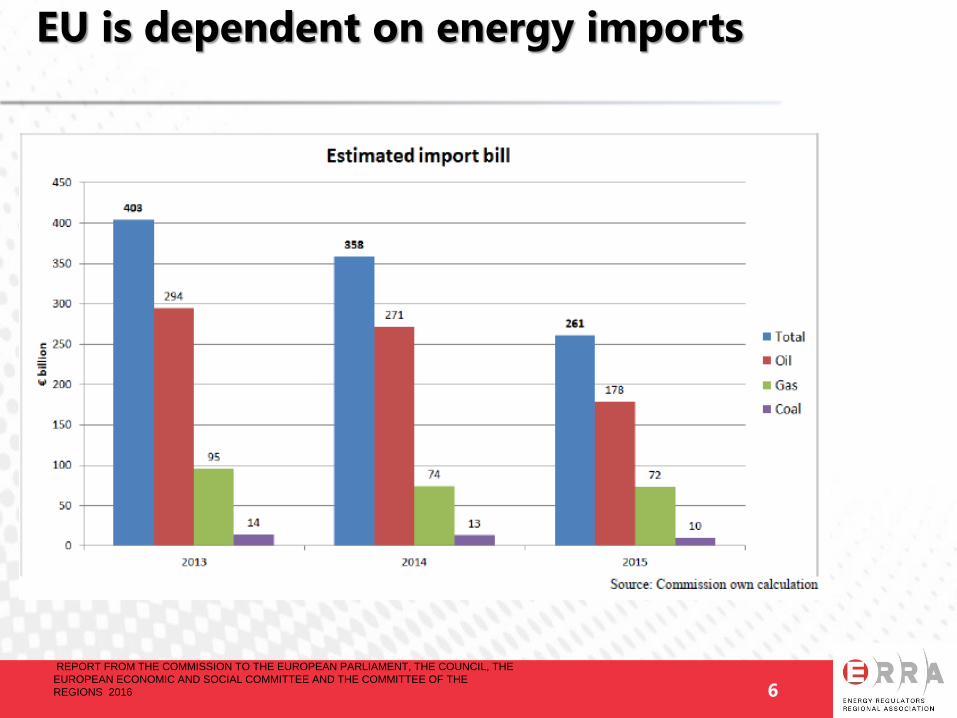

EU is dependent on energy imports

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE

EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE

REGIONS 2016

7

European electricity system is synchronous

8

Target 2030 new directive proposal

50% from EU electricity should be renewable.

Technology is developing – investment costs for solar and wind technologies have been reduced by 80% between 2009 and 2016.

New Technologies for keeping of generation and consumption balance and stronger market integration.

Price for CO2 emissions.

The approach to renewables deployment should be increasingly market-based. Removal of subsidies and transfer to the free market economy. Renewables should compete on free market.

9

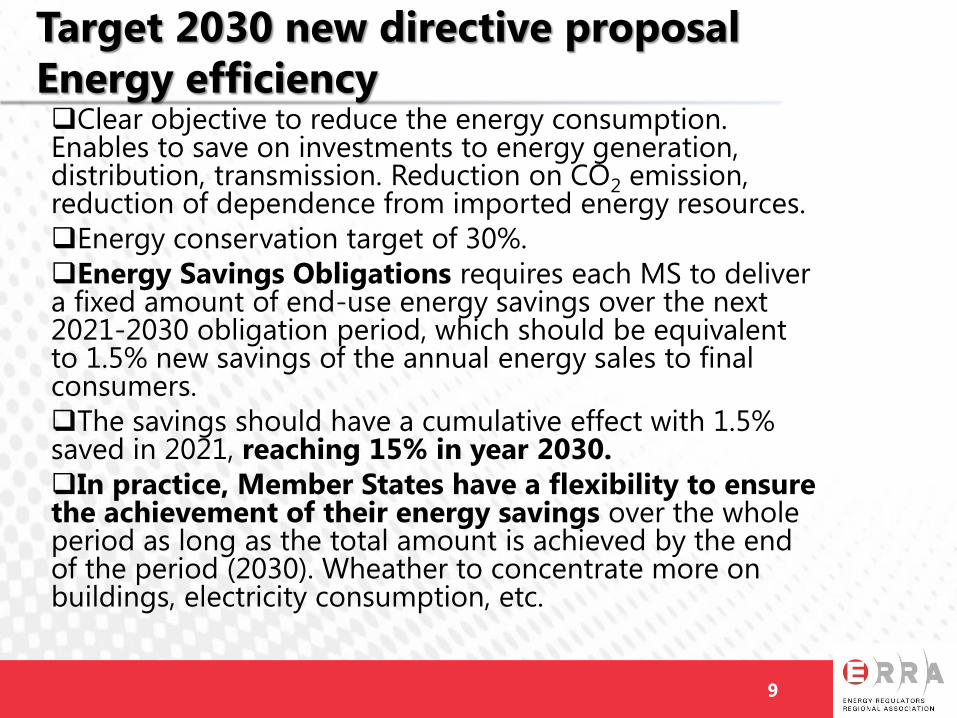

Target 2030 new directive proposal

Energy efficiency Clear objective to reduce the energy consumption. Enables to save on investments to energy generation, distribution, transmission. Reduction on CO2 emission, reduction of dependence from imported energy resources.

Energy conservation target of 30%.

Energy Savings Obligations requires each MS to deliver a fixed amount of end-use energy savings over the next 2021-2030 obligation period, which should be equivalent to 1.5% new savings of the annual energy sales to final consumers.

The savings should have a cumulative effect with 1.5% saved in 2021, reaching 15% in year 2030.

In practice, Member States have a flexibility to ensure the achievement of their energy savings over the whole period as long as the total amount is achieved by the end of the period (2030). Wheather to concentrate more on buildings, electricity consumption, etc.

10

EU Gas supply

ENTSOG TYNDP 2017

11

EU gas demand

ENTSOG TYNDP 2017

12

Security of gas supply

Two case studies

Central and South East Europe

Finland and Baltics

13

Central and South East European Gas

Market

Central and South-East European countries are characterized

by limited gas source diversity

CESEC initiative of 2015

– Enhances regional cooperation to achieving gas policy

objectives of EU member states and ENC contracting parties

– Later expanded to include measures on electricity market,

energy efficiency and renewables

Energy Community Gas Action 2020

– Legal and regulatory measures required to enhance

infrastructure investments to improve connectivity

– Reform measures required to attain the CESEC 2.0 action plan

objectives

14

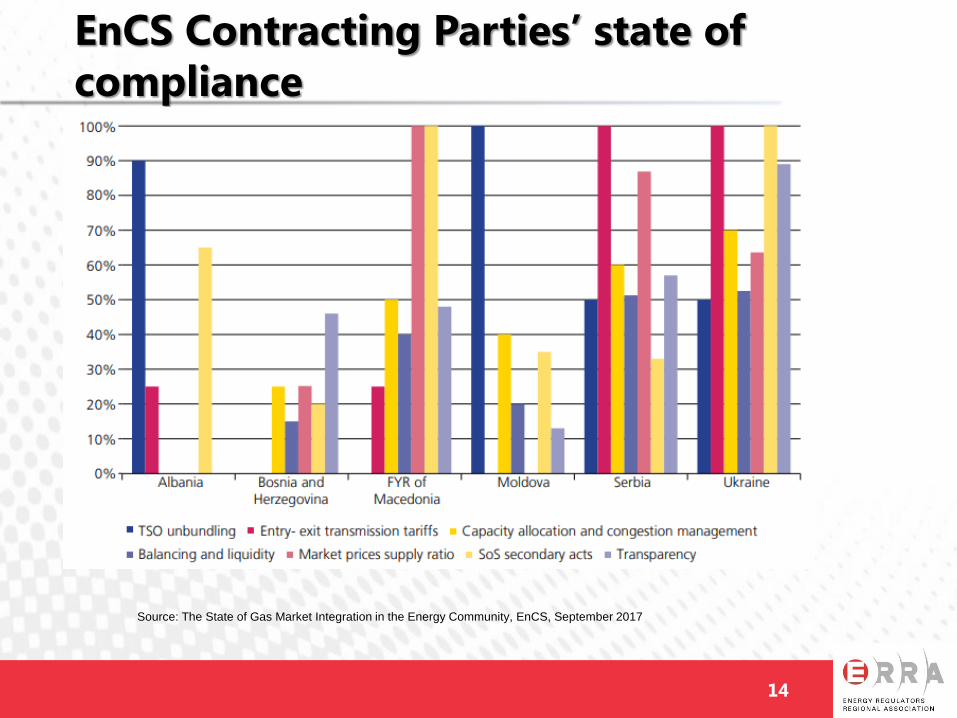

EnCS Contracting Parties’ state of

compliance

Source: The State of Gas Market Integration in the Energy Community, EnCS, September 2017

15

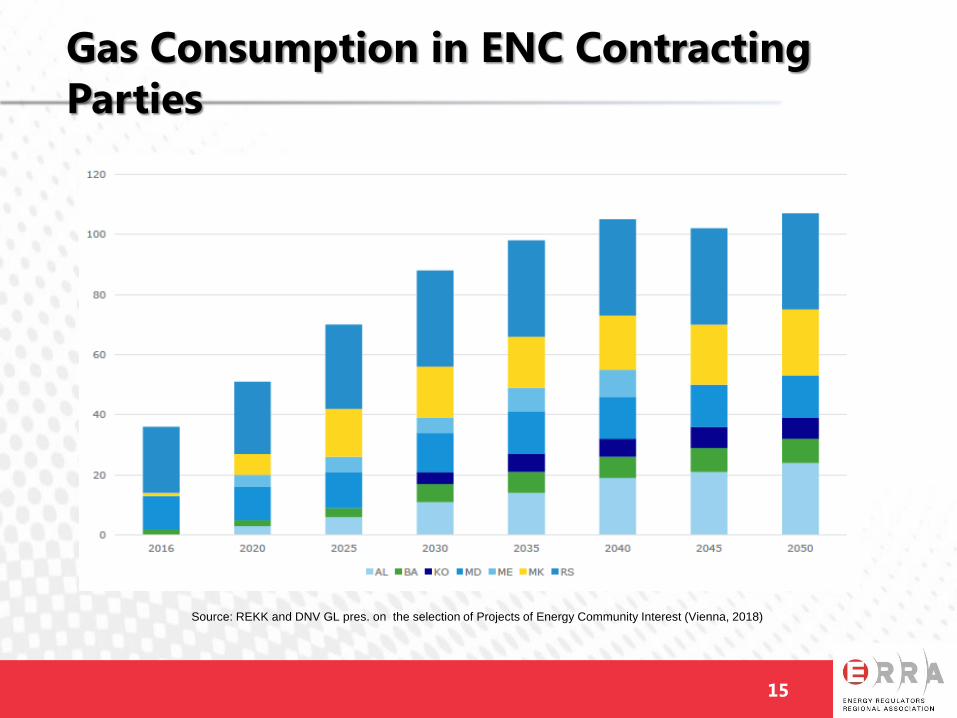

Gas Consumption in ENC Contracting

Parties

Source: REKK and DNV GL pres. on the selection of Projects of Energy Community Interest (Vienna, 2018)

16

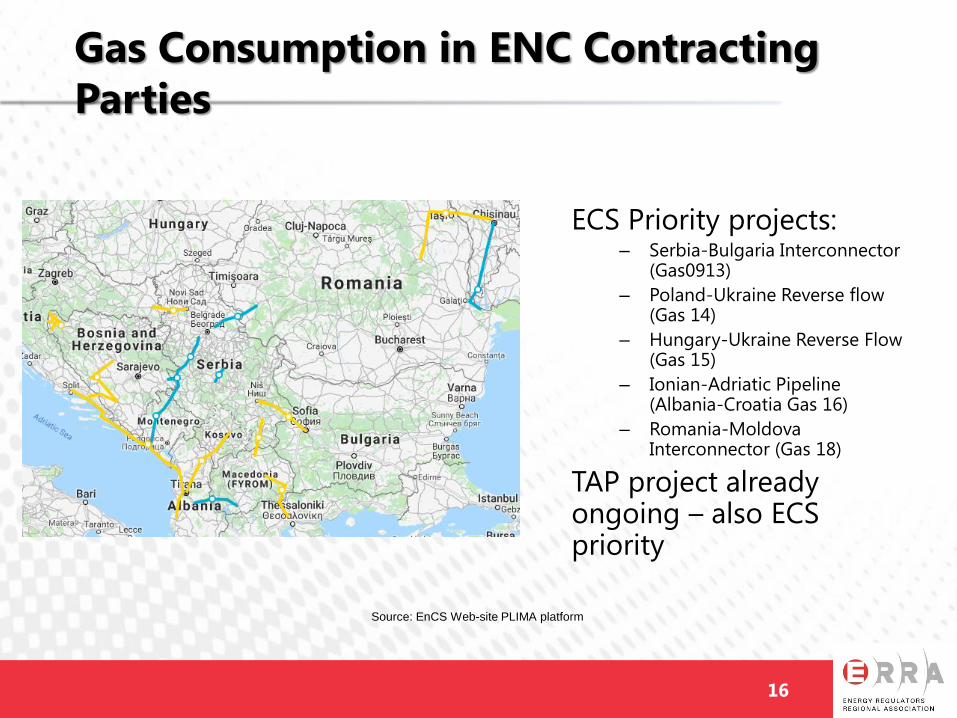

Gas Consumption in ENC Contracting

Parties

Source: EnCS Web-site PLIMA platform

ECS Priority projects: – Serbia-Bulgaria Interconnector

(Gas0913)

– Poland-Ukraine Reverse flow (Gas 14)

– Hungary-Ukraine Reverse Flow (Gas 15)

– Ionian-Adriatic Pipeline (Albania-Croatia Gas 16)

– Romania-Moldova Interconnector (Gas 18)

TAP project already ongoing – also ECS priority

17

Gas supply in Finland and Baltics

Historically gas supply from Russia only – until 2014.

Isolated region Finland + Baltics.

Large underground storage in Latvia.

Gas used for DH, power generation, industry.

Gas based local heating is not very common. DH is the most popular heating source.

Despite the gas supply, the distribution system is not existing in every city. Large territories with low population density.

18

Gas supply in Finland and Baltics (2)

Historically vertically integrated companies:

transmission, distribution, wholesale, end

customers supply.

Gazprom involvement.

Step by step implementation of EU 3-rd

liberalisation package.

19

Gas supply developments

Political decision „gas release programme“ in the beginning of 2010-s. Initiated by Lithuania and Estonia, followed by Latvia and Finland.

Preconditions for functioning liberalised gas market.

Ownership unbundling of TSO.

Diversification of gas supply.

Competition in supply to end-customers (no price regulation).

Big changes in 2014. Building of Klaipeda LNG terminal – independent supply from Russia.

New interconnections and terminals

Baltic Connector Estonia-Finland. EU co-financing decided.

GIPL Gas Interconnector Poland Lithuania. EU co-financing decided.

Regional LNG terminal

20

Gas supply

Regional gas market in the future: Finland +

Baltics

Gas supply from different sources:

Russian gas

LNG Lithuania, Poland, (Estonia).

Other sources (Poland)

21

Regional connections Baltics - Finland

22

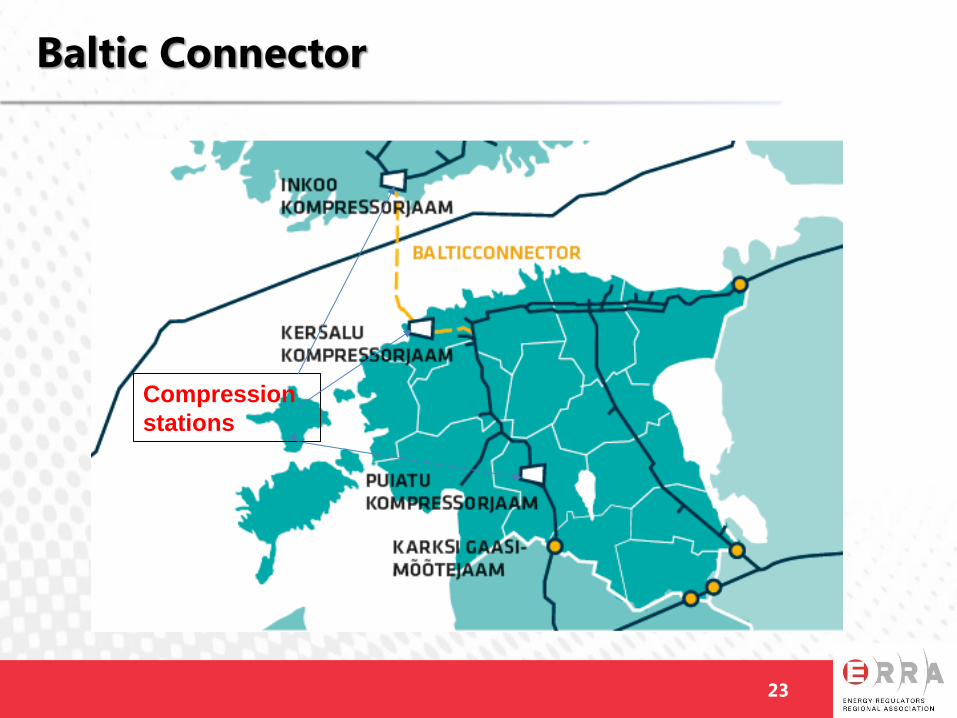

Baltic Connector

Undersea pipe connection Estonia-Finland +

pipeline connections.

Compression stations on both side of Finnish Gulf.

Compression station at Karksi (Estonian –Latvian

border). For Finland – Latvia reverse flow. Enables the

using of Latvian underground storage for Finland.

23

Baltic Connector

Compression

stations

24

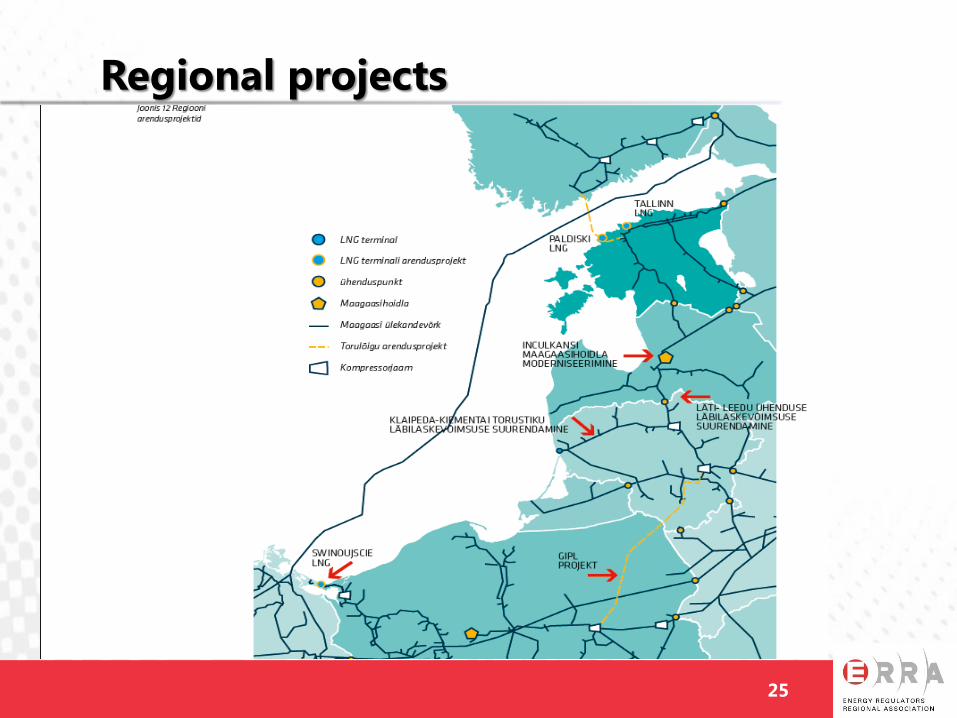

Other regional projects

GIPL (Poland – Lithuania).

Renovation of Latvian Gas storage.

Strengthening of Klaipeda connection,

project completed.

25

Regional projects

26

Gas supply in Baltic region

Estonia Latvia Lithuania Finland

27

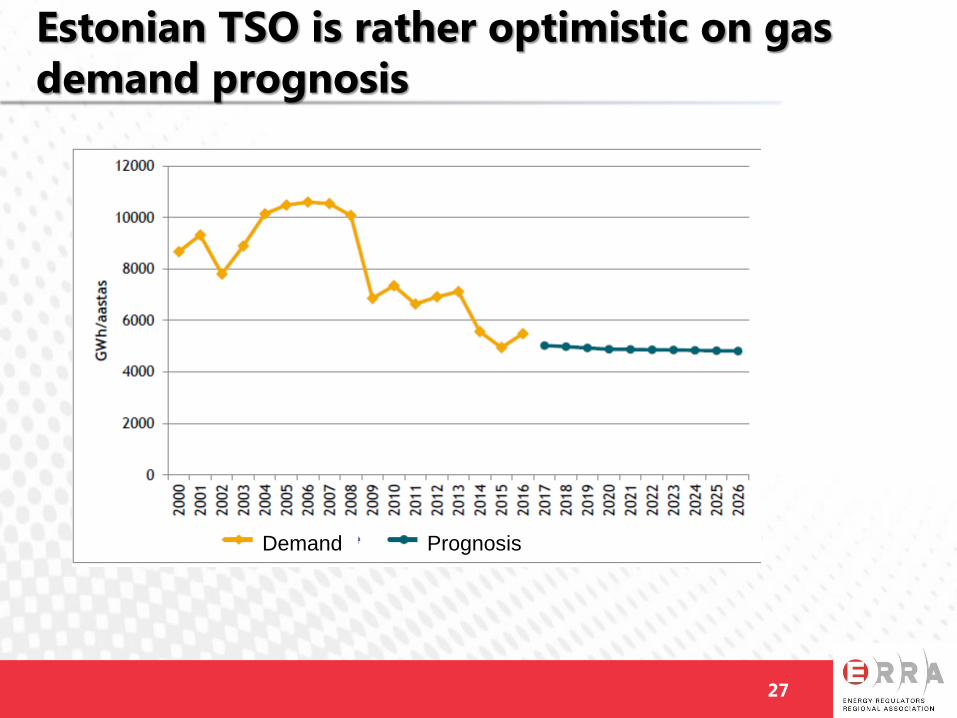

Estonian TSO is rather optimistic on gas

demand prognosis

Demand Prognosis

28

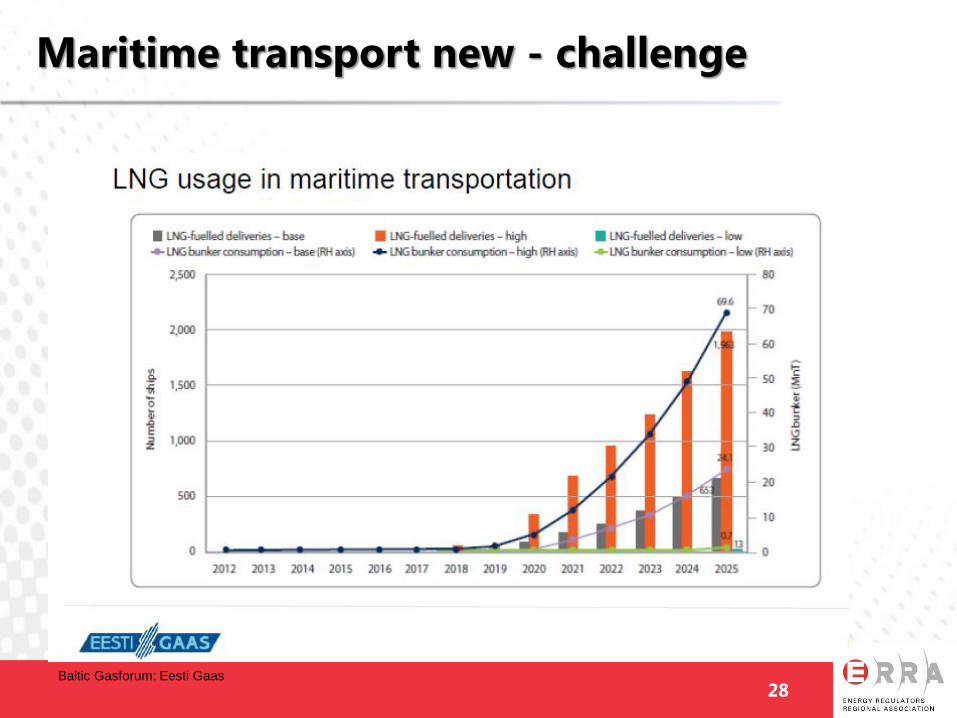

Maritime transport new - challenge

Baltic Gasforum: Eesti Gaas