Embed Size (px)

Citation preview

Citi Online Academy

Examining London’s RQFII Developments

November 21, 2013

Securities and Fund Services

This discussion is provided for informational purposes only. For further information, please contact your Citi Representative.

Table of Contents

1. China RQFII Market Update 3

2. RQFII Scheme: A New Chapter of China Investment 9

3. Funds Passporting in Asia Pacific: Fifteen Markets, Eight Players, Three Schemes, One Objective 22

1. China RQFII Market Update

Kevin Wong

Securities Country Manager, China

Citi Securities and Fund Services

Capital Market Update

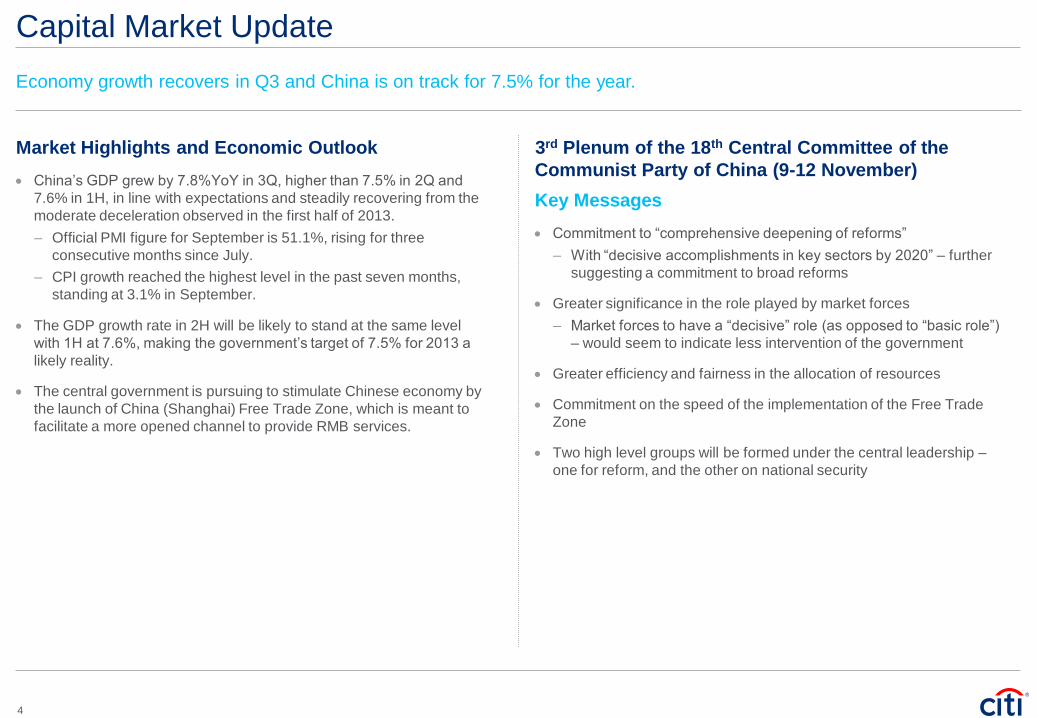

Market Highlights and Economic Outlook

China’s GDP grew by 7.8%YoY in 3Q, higher than 7.5% in 2Q and

7.6% in 1H, in line with expectations and steadily recovering from the

moderate deceleration observed in the first half of 2013.

– Official PMI figure for September is 51.1%, rising for three

consecutive months since July.

– CPI growth reached the highest level in the past seven months,

standing at 3.1% in September.

The GDP growth rate in 2H will be likely to stand at the same level

with 1H at 7.6%, making the government’s target of 7.5% for 2013 a

likely reality.

The central government is pursuing to stimulate Chinese economy by

the launch of China (Shanghai) Free Trade Zone, which is meant to

facilitate a more opened channel to provide RMB services.

Economy growth recovers in Q3 and China is on track for 7.5% for the year.

4

3rd Plenum of the 18th Central Committee of the

Communist Party of China (9-12 November)

Key Messages

Commitment to “comprehensive deepening of reforms”

– With “decisive accomplishments in key sectors by 2020” – further

suggesting a commitment to broad reforms

Greater significance in the role played by market forces

– Market forces to have a “decisive” role (as opposed to “basic role”)

– would seem to indicate less intervention of the government

Greater efficiency and fairness in the allocation of resources

Commitment on the speed of the implementation of the Free Trade

Zone

Two high level groups will be formed under the central leadership –

one for reform, and the other on national security

Comparative Analysis of Capital Market Access

QFII RQFII

Regulator CSRC, SAFE CSRC, SAFE, PBOC, Hong Kong SFC

Criteria of Applicants Commercial Banks

– In operation for more than 10 years

– Securities AUM no less than USD 5 billion

– Tier 1 Capital no less than USD 300 million

Securities Companies

– In operation for more than 5 years

– Securities AUM no less than USD 5 billion

– Capital no less than USD 500 million

AMC, insurance companies and other institutions

– Business experience of more than 2 years

– Securities AUM no less than USD 500 million

Financial institutions registered and mainly operated

in Hong Kong

Must have asset management license (Type 9 ) from

Hong Kong securities regulators and already have

an asset management business

Investment Scope Stocks, bonds, funds, warrants, IPOs, bond issuance

and index futures

Stocks, bonds, funds, warrants, IPOs, bond issuance

and index futures

FX Required Not required

Markets Accessible Stock Exchange

Interbank Bond Market

CFFEx

Stock Exchange

Interbank Bond Market

CFFEx

5

What’s New in China RQFII

RQFII License and Quota Approval Status

Total RQFIIs since inception: 54

Total approved in 3Q13: 13

Total approved in Oct13: 5

As of end of October 2013, a total of 47 Hong Kong based institutions

with RQFII qualification have been approved with RQFII quota as

below

– Fund management companies: 16

Total approved quota of RMB98.15 billion

– Securities companies: 13

Total approved quota of RMB26.15 billion

– Other FI institutions: 18

Total approved quota of RMB15.3billion

SAFE has indicated a preference to approve smaller size quota per

applicant initially with a streamlined process to grant additional quota.

Total RQFII Quota Approved Since RQFII Launched

6

RQFII ETF by AUM ( as of Nov 15, 2013)

Top 4 RQFIIs by Quota ( as of Nov 15, 2013)

Unit: CNY Billion

Name of ETF AUM (RMB billion)*

CSOP FTSE China A50 ETF 18.708

ChinaAMC CSI 300 Index ETF 8.155

E Fund CSI 100 A-Share Index ETF 1.574

Harvest MSCI China A Index ETF 1.427

Institution Name

RQFII Quota

(RMB in Billions)

CSOP Asset Management Ltd. 22.60

China Asset Management (HK) Ltd. 21.80

E-Fund Management (HK) Ltd. 18.70

Harvest Global Investments Ltd. 11.25

*Source: Hong Kong Exchange and Clearing Limited

RQFII Market Update

RQFII quota of RMB 80 billion granted to London and

RMB 50 billion to Singapore respectively

On 22 October, the Chinese and Singapore governments jointly

announced the expansion of the RQFII scheme to incorporate

Singapore, with an initial quota of RMB 50 billion.

On 15 October 2013, the Chinese and British governments jointly

announced that China is going to grant a RQFII quota of RMB 80

billion to London-based investors at the Fifth China-UK Economic and

Financial Dialogue.

CSRC indicated it is reviewing the application requirements internally.

We are expecting that the London/SG RQFII schemes may be similar

to HK RQFII scheme . CSRC is not expected to make material

changes to the current implementation rules for RQFII scheme when

it is expanded to London/Singapore.

RQFII scheme continues to expand. A quota of RMB 80 billion and RMB 50 billion was granted to London and Singapore

respectively. RQFII qualifications were granted to non-Chinese financial institutions under the HK RQFII scheme.

7

RQFII granted to non-Chinese financial institutions

Since July 2013, CSRC has opened the door to non-Chinese financial

institutions based in Hong Kong for the RQFII qualification.

Previously, only Hong Kong subsidiaries of qualified China mainland

financial institutions registered and mainly operated in Hong Kong

have been granted the RQFII qualification.

Until end of September, below seven eligible financial institutions with

non-Chinese background have been awarded RQFII licenses:

– Income Partners Asset Management (HK) Limited

– HSBC Global Asset Management (Hong Kong) Limited

– The Bank of East Asia, Limited

– SinoPac Asset Management (Asia) Ltd.

– Value Partners Hong Kong Limited

– PineBridge Investments Hong Kong Limited

– Chong Hing Bank Limited

RQFII approved for proprietary trading

After receiving RQFII license approval in August 2013,the Bank of

East Asia ("BEA") publicly indicated that it will use the RQFII

qualification for proprietary trading, thus became the first RQFII

approved to operate proprietary investment.

CSRC further confirmed that it is open to approve RQFIIs for

proprietary trading.

QFII and RQFII Market Update

RQFII products to be launched outside Hong Kong

According to market news, below two RQFII products are soon

to be launched in NYSE Arca, a leading listing and trading

platform for ETFs:

– DB X-trackers Harvest China Fund, utilizing RQFII quota of

Harvest Global Investments, will be launched by Deutsche

Asset & Wealth Mangement.

– KraneShares Bosera MSCI China A Share ETF, utilizing

RQFII quota of Bosera Asset Management (International),

will be launched by KraneShares.

SAFE indicated RQFII is allowed to launch open-ended public

funds with its RQFII quota outside Hong Kong.

– SAFE further confirmed that RQFII needs to clearly outline in

its investment plan the proposed RQFII structure, destination

of product launch, and roles of all relevant parties to the fund.

Citi further clarified with SAFE regarding the restrictions for RQFII to launch products in jurisdictions other than its

registration location and the possibility for open-ended private funds to enjoy daily liquidity treatment after lockup period.

8

Open-ended private RQFII funds not allowed for daily

liquidity after lockup period

Under the current RQFII regulation, open-ended public funds

are allowed to conduct daily injection/ repatriation.

However, it is unlikely to extend the same liquidity treatment to

open-ended funds that are not sold to the public (e.g. private

funds) at the moment as indicated by SAFE.

9By China Asset Management (Hong Kong) Limited 9

RQFII SchemeA New Chapter of China Investment

November 2013

Confidential and not for onward distribution

10By China Asset Management (Hong Kong) Limited 10November 2013

Year of introduction: 2011

Allowing approved offshore financial institutions to use RMB funds sourced overseas to invest in domestic

markets

Effectively the RMB-version of the QFII scheme

Importance:

Opened up an important channel for RMB flowing back to the onshore asset market

Further confirmed Hong Kong's role as the offshore RMB centre

Increased availability and diversity of RMB-denominated products offshore

An important step in the eventual convergence in the onshore/offshore RMB markets

Indicated the government’s determination to internationalize RMB

RQFII Pilot ProgramBackground

*Source: SAFE, as of July 30, 2013

By China Asset Management (Hong Kong) Limited

11November 2013 By China Asset Management (Hong Kong) Limited

Item RQFII QFII

Injection and

repatriation

•Effectively use its RQFII quota within 1 year from the

day of RQFII quota approval

•Injection:

Open ended fund RQFIIs: no specific requirement

Other RQFIIs: fully inject the approved quota within

6 months upon quota approval.

•Repatriation:

Open ended fund RQFIIs can do fund

injection/repatriation on a daily basis, according to the

net difference between its subscription and redemption

each day.

Other RQFIIs can do fund injection/repatriation on a

monthly basis. RQFIIs need to provide audit reports

issued by domestic accounting firm and relevant tax

payment evidence if RQFIIs repatriate investment

gains.

•Injection:

Fully inject the approved quota within 6 months upon

quota approval.

•Repatriation:

For open ended China fund, a QFII is allowed to

repatriate principal or profit in the net amount of its

subscription and redemption funds in the preceding week

on a weekly basis, after lock-up period.

For non open ended China funds, principal and profit

repatriation can be made after the lock-up period. Pre-

approval by the SAFE is required for each repatriation.

Denominated

Currency RMB (No onshore FX conversion required) USD (Onshore FX conversion required)

RQFII vs QFII Structure Differences

Source: CSRC ,SAFE, HSBC and Citi

12November 2013 By China Asset Management (Hong Kong) Limited

Item RQFII QFII

Lock-up Period•Open ended fund: Not applicable

•Non open ended fund: 1 Year

•Open ended fund: 3 months

•Non open ended fund: 1 Year

Investment

restriction – quota

allocation

•No requirement, at RQFII’s discretion

•Not less than 50% investment quota has to invest in

onshore equities (A shares)

•No More than 20% investment quota can be invested in

cash or cash equivalents

Investment Scope•Same for QFII and RQFII

•Including Stocks, bonds, funds, warrants, IPOs, bond issuance and index futures

RQFII vs QFII Structure Differences

Source: CSRC ,SAFE, HSBC and Citi

13November 2013 By China Asset Management (Hong Kong) Limited

Implications of Investment Products

Friendlier liquidity terms to launch public funds

Wider investment scope in China domestic market

Faster process for quota increase

More investment options for offshore RMB

Cost efficiency

Example 1: ChinaAMC Select RMB Bond Fund

14November 2013 By China Asset Management (Hong Kong) Limited

Historical Performance*

Note: All fund statistics are as of September 30, 2013.

*NAV-to-NAV performance with dividends reinvested; The investment returns are denominated in RMB. US/HK dollar-based investors are therefore exposed to fluctuations

in the US/HK dollar /RMB exchange rate. Past performance is not a guide to future performance, future returns are not guaranteed. You should read the Fund’s

Explanatory Memorandum including details of risk factors, before subscribing the units of the Fund.

Portfolio Allocation

Asset AllocationNAV per share RMB 10.34

-1%0%1%2%3%4%5%6%7%8%9%

02/2012 06/2012 10/2012 02/2013 06/2013

ChinaAMC Select RMB Bond Fund 86.47%

9.38%2.12% 2.03%

Credit Products

Fixed Income Funds

Convertible Bonds

Cash

Portfolio holding limits

Fixed income: up to 100% for RQFII portfolio vs 50% limit for QFII

Daily liquidity for the fund

RMB, HKD, and USD share classes

No FX transaction cost at fund level if CNH given

CNH is remitted directly into China, automatically converting CNH to CNY at 1:1

RQFII Bond Fund Advantages

Use offshore RMB to invest

As of August, there were over 700 billion RMB in RMB deposits in Hong Kong

Provides higher yield and ability to subscribe and redeem freely

Trade interbank bond market in China

Directly invest in a large potential universe of onshore Chinese bonds with RMB 26 trillion in outstanding size which

provide investors with exposure to a wide range of issuers (governments, central bank, policy banks, and listed/non-listed

companies etc.)

90% of bonds trade in the interbank bond market, not on the exchanges

Daily liquidity and semi-annual distribution (subject to the discretion of the Manager)

15November 2013 By China Asset Management (Hong Kong) Limited

0

1

2

3

4

5

3M 6M 9M 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y 15Y

(%) Onshore China Government BondOffshore China Government BondCNH Deposit Rates

Onshore vs. Offshore RMB Bond Yields*Benchmark Yield Curves in Major Economies*

0

1

2

3

4

5

6

1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y

China (onshore) Germany U.S. Japan

Example 2: ChinaAMC CSI 300 Index ETF (83188.HK / 3188.HK)

16November 2013 By China Asset Management (Hong Kong) Limited

Source: Bloomberg, from January 01 2013 to October 31 2013

1 Perfomance of ChinaAMC CSI 300 Index ETF is calculated on NAV-to-NAV basis without dividend reinvested and denominated in RMB. US/HK dollar-based investors

are therefore exposed to fluctuations in the US/HK dollar /RMB exchange rate.

2 Source: Bloomberg; Performance of CSI 300 Index is calculated based on price return and denominated in RMB.

Uses allocated RQFII quota to directly invest into underlying basket

Daily liquidity for the fund for daily creation/redemptions

Same day execution of underlying basket

Trades in both RMB and HKD on secondary market. Primary market dealt in RMB

No FX transaction cost at fund level

CNH is remitted directly into China, automatically converting CNH to CNY at 1:1

Stock Code YTD TE Annualized TE

83188 0.11% 1.81%

82822 0.13% 2.12%

83100 0.16% 2.58%

83118 0.12% 1.83%

2827 0.33% 5.20%

2823 0.20% 3.16%

RQFII ETF Advantages

Use offshore RMB to invest

Index fund denominated in RMB but traded in dual currencies

Physical ETF through RQFII

Cost Effective – does not involve any derivatives or collateral cost

No Synthetic Replication – no counterparty risk on derivative issuers, no collateral requirement

Daily Creation/Redemption

17November 2013 By China Asset Management (Hong Kong) Limited

A-shares: RQFII ETF vs Synthetic ETF vs QFII Physical ETF

RQFII ETF’s advantages over synthetic ETFs and QFII ETFs:

Vs Synthetic ETF: Physical A-share underlying allows the ETF to have lower cost, no counterparty risk, and better performance

tracking.

Vs QFII Physical ETFs: RQFII scheme allows for daily repatriation and movement of capital allows for daily

creation/redemption. QFII ETFs have capital movement limits that delays creation/redemption of the ETF.

18August 2013 By China Asset Management (Hong Kong) Limited

RQFII Physical A-Share ETF Synthetic A-Share ETFs QFII Physical A-shares

ETFs

Underlying Instruments China A-Share Stocks

Derivative Instruments which

have China A-share exposure China A-share Stocks

QFII/RQFII Quota Provider ETF Manager Various Third Parties ETF Manager

Derivatives Counterparty

Risk No Yes No

Collateral Requirement No Yes No

Derivatives Costs No Yes No

Trading Currency RMB/HKD Various Various

Capital

repatriation/movement Daily N/A Weekly

RQFII Physical vs Synthetic vs QFII Physical

This material is strictly confidential and is for the intended Professional Investors only. The recipient of this material should not distribute it to any other person.

19November 2013 By China Asset Management (Hong Kong) Limited

Other Considerations

Tax provision

Derivatives instruments

Other fixed income instruments

Choice of service providers

Local capabilities

Risk Factors specific to RQFII A-share ETFs

Investment risk

Risks relating to the RQFII regime

RMB trading and settlement of Units risk

Dual Counter Risk

Risks relating to PRC

PRC tax risk

RMB currency risk

Government intervention and restrictions risk

New manager and reliance on the Investment Adviser risk

Tracking error risk

Reliance on market maker risk

Note: The above does not include all risks factors involved in investing in the ETF. Investors should read the ETF’s Prospectus and

Product Key Fact Statement in detail, including the risk factors, before investing in the ETF.

20By China Asset Management (Hong Kong) LimitedAugust 2013

This material is strictly confidential and is for the intended Professional Investors only. The recipient of this material should not distribute it to any other person.

Contact Information

China Asset Management (Hong Kong) Limited

Contact: Mr. Freddie CHEN

Title: Managing Director

Email: [email protected]

Tel: (852) 3406 8613

Fax: (852) 3406 8500

General Email: [email protected]

Hotline: (852) 3406 8686

Address: 37/F, Bank of China Tower, 1 Garden Road, Hong Kong

21By China Asset Management (Hong Kong) LimitedAugust 2013

Contact: Mr. Curtis TAI

Title: Manager

Email: [email protected]

Tel: (852) 3406 8611

Fax: (852) 3406 8500

This material is strictly confidential and is for the intended Professional Investors only. The recipient of this material should not distribute it to any other person.

3. Funds Passporting in Asia Pacific

Fifteen Markets, Eight Players, Three Schemes, One Objective

Stewart Aldcroft

CEO, CitiTrust Limited, Asia Pacific

Senior Advisor, Investor Services, Asia Pacific

Citi Securities and Fund Services

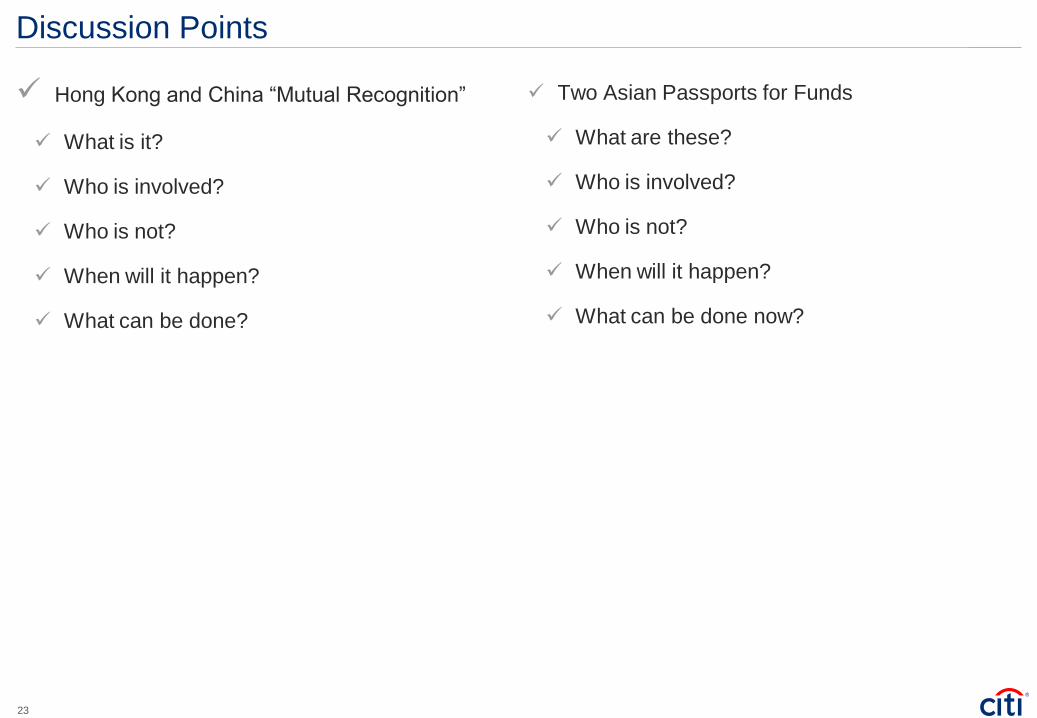

Discussion Points

Hong Kong and China “Mutual Recognition”

What is it?

Who is involved?

Who is not?

When will it happen?

What can be done?

Two Asian Passports for Funds

What are these?

Who is involved?

Who is not?

When will it happen?

What can be done now?

23

Hong Kong/China Mutual Funds “Recognition”

What’s been said?

Alexa Lam (HK SFC) speech in Hong Kong 23 January

2013

“Blessing” of the CSRC

Two stage process. Stage One completed, Stage two is

“implementation”

Added to HK/China CEPA (Closer Economic

Partnership Agreement) in August 2013

Likely scenarios

Hong Kong funds in China

China funds in Hong Kong

Products

SFC only, initially

CSRC only from China

Investment restrictions

Use of derivatives

Appropriate skill set in place

Possible limitations

“Pilot scheme”?

Based on time and size issues?

Distribution

What are Chinese investors interested in?

Access to the big 4 banks is difficult

Will other fund distributors be allowed to develop

Will foreign banks be given the go ahead to distribute

funds in China

24

Hong Kong/China Mutual Funds “Recognition”

What we do know What we don’t know What needs to be known

Bilateral agreement between China and Hong

Kong, no changes to existing “Rules”

Will it be a “pilot” scheme with only a few initial

participants?

Timing, will there be “advanced notice” of

commencement?

Does not involve Taiwan, Singapore or

anywhere else

Will there be restrictions based on AUM, age

and size of fund, age of FMC, etc.?

Any secondary approval process in Hong Kong

and/or China?

Hong Kong domiciled, HK SFC Authorised

funds for HK

Are ETFs included and how? Who will be allowed to distribute?

China CSRC approved funds for China What restrictions on use of derivatives will be

placed?

How to gain support from key market

distributors?

No Hong Kong MPF, UCITS, Cayman or other

funds

How will Mainland funds be allowed into HK?

Will the SFC impose restrictions?

What fund types, markets, products will be

attractive to Mainland investors?

CSRC and SFC are in two stage discussions:

Stage 1: Mapping – Completed in July 2013

Stage 2: Implementation – On-going

Will hedge funds and alternative investment

funds be allowed?

Will RMB Share classes be allowed for these

and all other HK SFC Funds?

HK SFC Funds Authorisation Code allows a

wide variety of fund types

Can Fund of Fund products, managed in HK,

invested in UCITS be allowed? (Chap. 8)

When will OEICs (i.e. mutual funds) be allowed

in Hong Kong?

“Technical study” groups meeting in Beijing and

Hong Kong, regularly

Will this lead to a “Greater China Funds

Passport”?

Will the SFC allow new fund applications “on

spec” in parallel with these new recognition

developments?

Purpose is to facilitate cross-border fund

distribution between Hong Kong and China

As China does not have Trust Laws, and only

unit trusts can currently be domiciled in HK, how

will this work?

Will Chinese FMC in HK get priority on

processing of products?

Of the 1,850+ HK SFC authorised funds, less

than 300 currently qualify.

Will this replace QDII? Is it necessary to set up offices in both Hong

Kong and China?

“Mutual Recognition” added to CEPA 10 in

August 2013

How will tax on both the funds and the investor

be applied in China?

Will there be a need for operations management

in both Hong Kong and China?

25

Hong Kong/China Mutual Funds “Recognition”

What can be done now?

Create Hong Kong domicile funds

Use local Trustees, e.g. Cititrust Limited

Build a track record

Ensure organisation can meet the new criteria

Benefits of Hong Kong local funds

Use in MPF

Speed to Market

Lower costs

Not impacted by UCITS V & VI

Relatively simple products

Can enable regional specialities to be developed

RMB shares classes

Next steps

What to set up

How to set up

Where to set up

26

Asian Passports for Funds – Two Schemes

APEC Finance Ministers “Asia Region Funds Passport”

Announced 22 September 2013

Involves Australia, South Korea, Singapore and New Zealand

Expected implementation in 2016

Based on an ASIC initiative from 2008

ASEAN Capital Markets Forum “ASEAN CIS Framework for Cross-Border Offering of Funds”

Announced 2 October 2013

Involves Singapore, Malaysia, Thailand

Expected implementation in 2014

Based on a Singapore MAS initiative from 2012

27

Asian Passports for Funds – Scheme 1

APEC Funds Passport scheme (September 2013)

Involves Australia, South Korea, Singapore and New Zealand

What is known so far:

Limited details available to date, no “Terms & Conditions” issued

More focused on export of funds from Australia and Korea than on import

Fundamental problems on fund importation in Australia and Korea

However:

Named: “Asia Region Funds Passport”

First stage – Joint Public Consultation in 2014 (on Rules and Arrangements)

Next – Each market allowed to decide whether to participate (or not)

Launch – Scheduled for 2016

September 2013, APEC announces ARFP

January to June 2014, public consultations in

countries

July to December 2014, technical and procedural

rules to be developed

February 2015, Arrangement Document

to be signed by participating countries

February to December 2015, pilot group

countries to implement domestic regulations

January 2016, commencement of

ARFP Passport

28

Asian Passports for Funds – Scheme 2

ASEAN Capital Markets Forum (October 2013)

Countries involved – Singapore, Malaysia, Thailand

Have issued “Standards of Qualifying CIS) (Collective Investment Schemes)

CIS Operators (Fund managers) to have:

Minimum 5 year history

Minimum US$500m in AUM

Funds to have limitations on FDI

Target implementation in 1H2014

Standards Required of Qualifying CIS

Minimum AUM to Qualify US$500m

Minimum Track Record 5 years

Fund Management delegation limit 20% NAV

Investment in transferable securities, money market

instruments, deposits, units in other CIS, and financial

derivatives

Allowed

Securities lending, repurchase transactions, direct

lending of monies

Not Allowed

29

Three Funds Passports – but which one(s) will work?

Hong Kong and China “mutual recognition”

Is Regulator-to-Regulator with Government support

Fund industry highly motivated by the opportunity

Could start in late-2013 or early-2014

APEC Finance Ministers “Asia Region Funds Passport”

Is Finance Minister led

Long delay to implementation

Designed to export funds, not import

Involves large mutual fund markets (Australia, Korea)

Is Singapore really involved?

ASEAN-led “ASEAN CIS Framework for Cross-border Offering of Funds”

Is Regulator-led, with clearly defined terms published

Scheduled to start in 1H2014

More likely to benefit local fund managers than global

Domestic mutual fund markets are relatively small by comparison

Also worth noting:

Singapore has a foot in two camps

No participation (yet) by Japan, Taiwan, Indonesia, The Philippines, Vietnam, India, Sri Lanka

How will global fund managers react?

30

Will Asian Funds Passport Schemes impact product development?

In Hong Kong – Yes

Introduction of RMB denominated products

Global fund managers creating local funds

Possibly simpler investment themes

Less use of derivatives

Will likely reduce influence on and of UCITS

In China - ?

Local fund managers in China have not yet been allowed to invest globally, except via QDII

Elsewhere

Too early to tell

31

Appendix: Introduction to ChinaAMC

November 2013 32By China Asset Management (Hong Kong) Limited

33By China Asset Management (Hong Kong) Limited 33By China Asset Management (Hong Kong) LimitedNovember 2013

ChinaAMC: A Leading Asset Management Firm in China

China Asset Management Co., Ltd. (“ChinaAMC”)

Established in 1998

The largest mutual fund manager in China*

• Total assets under management and advisory by ChinaAMC

Group was RMB 344.77 billion (USD 56.17 billion) as of June 28,

2013 **

*Source: Wind, as of June 28, 2013, in terms of mutual funds AUM of RMB 230.72billion

**Source: ChinaAMC and CAMHK

China Asset Management (Hong Kong) Limited

(“CAMHK”)

Established in September 2008 as a wholly-owned subsidiary

of ChinaAMC

Aims to strategically develop the offshore business and

investment capabilities.

Represents ChinaAMC’s strategic move to expand its overseas

activities by:

• Serving as an integral part of ChinaAMC’s overseas

investment and research team

• Providing international clients with investment products and

services

Currently offers the following strategies to overseas investors:

• China A-shares

• Offshore Chinese equities

• China equity absolute return

• China fixed income

• Index product (ETF)

^Source: Wind

Top Five Fund Management Companies in China^

by Mutual Funds AUM as of June 30, 2013

Ranking Fund Companies

Fund AUM

Market Share(RMB

billion)

1 ChinaAMC 230.72 9.29%

2 Harvest 148.87 6.00%

3 E-Fund 129.10 5.20%

4 Southern 125.67 5.06%

5 Bosera 110.21 4.44%

34

1998: One of the first 3 fund management companies established

in China

1999: Launched one of China’s first enhanced index funds

2001: The first and only fund manager approved by the National Council for Social Security Fund to

manage pension funds in a pilot program

2002: Selected to manage the National Social Security Fund portfolios as one of the

first 6 qualified fund management companies

2004: Launched China’s first ETF: the China 50 ETF

2002: Launched China’s first pure bond fund

2005: Licensed to manage corporate annuities among the first

batch of fund management companies

2005: Designated by EMEAP (comprised of eleven central banks and monetary

authorities in the East Asia and Pacific region) as the sole manager for ABF China Bond

Index Fund

2007: Launched one of China’s first QDII funds

2008: Licensed to manage separate account

2009: Launched offshore funds by CAMHK

2010: Launched UCITS funds by CAMHK

2011: Launched China’s first bond index mutual fund

By China Asset Management (Hong Kong) Limited

2012: Launched one of the first RQFII bond funds and

the first RQFII ETF by CAMHK

November 2013

ChinaAMC GroupThe Industry Pioneer in China

2013: Launched the first batch of sector index

ETFs in China

35

Best Fund Management Company

Shanghai Securities News, Morningstar

2006, 2007, 2008,

2009, 2010, 2011

Fund House of the Year -

China

AsianInvestor

2004, 2007, 2008,

2009, 2010, 2013

China Best Branded ETF

Asia Asset Management

2010

No.1 of China’s

Top 20 Money Managers

Institutional Investor

2008, 2009, 2010, 2011, 2012

By China Asset Management (Hong Kong) Limited

Fund House of the Year -

China Offshore

AsianInvestor

2012

Golden Bull Fund Management Company

China Securities Journal

2006, 2007, 2008,

2009, 2010, 2011

November 2013

ChinaAMC GroupAwards & Recognition

Most Innovative ETF-Asia Pacific

(ChinaAMC CSI 300 Index ETF)

The 9th Annual ETF Global Award (2013)

This presentation is intended for information and internal training purposes only. Please do not distribute to any end investors.

By China Asset Management (Hong Kong) Limited 36August 2013

Important Information:

•ChinaAMC CSI 300 Index ETF (the “Fund”) is a passively managed exchange traded fund (“ETF”) and is traded on the Stock Exchange of Hong Kong (“SEHK”) like stocks. The

investment objective is to provide investment result that, before fees and expenses, closely corresponds to the performance of the CSI 300 Index (the “Index”). The Fund invests in

the PRC’s domestic securities market through the Manager’s status as a RMB Qualified Foreign Institutional Investor (“RQFII”) and the RQFII quota obtained by the Manager on

behalf of the Fund.

•The Fund is subject to concentration risk as a result of tracking the performance of a single geographical region (the PRC).

•The RQFII policy and rules are new and there may be uncertainty to its implementation and such policy and rules are subject to change, such changes may also have potential

retrospective effect.

•Repatriations by RQFIIs in respect of fund such as the Fund conducted in RMB are permitted daily and are not subject to any lock-up periods or prior approval. There is no

assurance, however, that PRC rules and regulations will not change or that repatriation restrictions will not be imposed in the future. Any new restrictions on repatriation of the

invested capital and net profits may impact on the Fund’s ability to meet redemption requests.

•Investing in emerging markets, such as the PRC, involves a greater risk such as greater political, tax, economic, foreign exchange, liquidity and regulatory risks.

•There are risks and uncertainties associated with the current PRC tax laws, regulations and practice in respect of capital gains realised by RQFIIs on its investments in the PRC

(which may have retrospective effect). The Manager will at present make a provision of 10% for the account of the Fund in respect of any potential tax liability on capital gains. In

case of any shortfall between the provision and actual tax liabilities, which will be debited from the Fund’s assets, the Fund’s asset value will be adversely affected.

•The Fund is denominated in RMB. RMB is currently not freely convertible and is subject to exchange controls and restrictions. There is no guarantee that the value of RMB against

the investors’ base currencies (for example HKD) will not depreciate.

•In the event of any default of either a PRC broker or the PRC Custodian (directly or through its delegate) in the execution or settlement of any transaction or in the transfer of any

funds or securities in the PRC, the Fund may encounter delays in recovering its assets which may in turn impact the NAV.

•The Fund is not “actively managed” and therefore, when there is a decline in the Index, the Fund will also decrease in value. The Manager will not adopt any temporary defensive

position against any market downturn. Investors may lose part or all of their investment.

•Due to fees and expenses of the Fund, liquidity of the market and different investment strategies adopted by the Manager, the Fund’s return may deviate from that of the Index.

•The units of the Fund are traded on the SEHK. The prices on the SEHK are based on secondary market trading factors and thus the Fund’s market prices on the SEHK may deviate

from the net asset value.

•You should not make any investment decision solely based on the information on this material alone. Please read the relevant offering documents for details including the risk

factors before making any investment decisions. If necessary, seek independent professional advice.

CSI Disclaimer

The CSI 300 Index (“Index”) is compiled and calculated by China Securities Index Co., Ltd. (“CSI”). All copyright in the Index values and constituent list vest in CSI.CSI will apply all

necessary means to ensure the accuracy of the Index. However, CSI does not guarantee its instantaneity, completeness or accuracy, nor shall it be liable (whether in negligence or

otherwise) to any person for any error in the Index or under any obligation to advise any person of any error therein.

This material is strictly confidential and is for the intended Professional Investors only. The recipient of this material should not distribute it to any other person.

By China Asset Management (Hong Kong) LimitedAugust 2013

Disclaimer

Investment involves risk. Past performance is not indicative of future performance, future return is not guaranteed. The price of the Fund’s units may go up as well as down and a

loss of your original capital may occur. This material is for informational purposes only and does not constitute an offer or solicitation of any transaction in any securities, nor does it

constitute any investment advice. It expresses no view as to the suitability of any investments described herein to the individual circumstances of any recipient. You should read the

Fund’s Prospectus upon its official publication for details of the Fund including the risk factors. If necessary, you should seek independent professional advice. You should not

invest in the Fund unless the intermediary who sells the Fund to you has advised you that the Fund is suitable for you and has provided explanation of such advice.

This material has been prepared and issued by China Asset Management (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission.

Disclaimer

37

This material is strictly confidential and is for the intended Professional Investors only. The recipient of this material should not distribute it to any other person.

Citi believes that sustainability is good business practice. We work closely with our clients, peer financial institutions, NGOs and other partners to finance solutions to climate change, develop industry standards, reduce our own environmental

footprint, and engage with stakeholders to advance shared learning and solutions. Highlights of Citi’s unique role in promoting sustainability include: (a) releasing in 2007 a Climate Change Position Statement, the first US financial institution to do

so; (b) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of renewable energy, clean technology, and other carbon-emission reduction activities; (c) committing to an

absolute reduction in GHG emissions of all Citi owned and leased properties around the world by 10% by 2011; (d) purchasing more than 234,000 MWh of carbon neutral power for our operations over the last three years; (e) establishing in

2008 the Carbon Principles; a framework for banks and their U.S. power clients to evaluate and address carbon risks in the financing of electric power projects; (f) producing equity research related to climate issues that helps to inform investors

on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on the issue of climate change to help advance understanding and solutions.

Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

efficiency, renewable energy and mitigation

© 2013 Citibank, N.A. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied upon, by

you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of any transaction contemplated hereby ("Transaction"). Accordingly, you should seek advice

based on your particular circumstances from an independent tax advisor.

In any instance where distribution of this communication is subject to the rules of the US Commodity Futures Trading Commission (“CFTC”), this communication constitutes an invitation to consider entering into a derivatives

transaction under U.S. CFTC Regulations §§ 1.71 and 23.605, where applicable, but is not a binding offer to buy/sell any financial instrument.

Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a financing, underwrite or

purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable law or regulation, you agree to keep confidential the

information contained herein and the existence of and proposed terms for any Transaction.

Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and accounting

characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us for) legal, tax or accounting advice, (b)

there may be legal, tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior management in your organization as to

such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials, you and we hereby agree that from the commencement of discussions with

respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction.

We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number. We may also

request corporate formation documents, or other forms of identification, to verify information provided.

Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time without notice and are

not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or

may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof and are subject to change without any notice. We and/or our

affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at any time.

Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a favorable or

negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific recommendations or views contained in

research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies and procedures designed to limit communications between its investment banking and

research personnel to specifically prescribed circumstances.