Embed Size (px)

Citation preview

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 1/20

SEB Commodities MonthlyWill oil kill the recovery?

5 APRIL 2011

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 2/20

2

Commodities Monthly

Will oil kill the recovery?

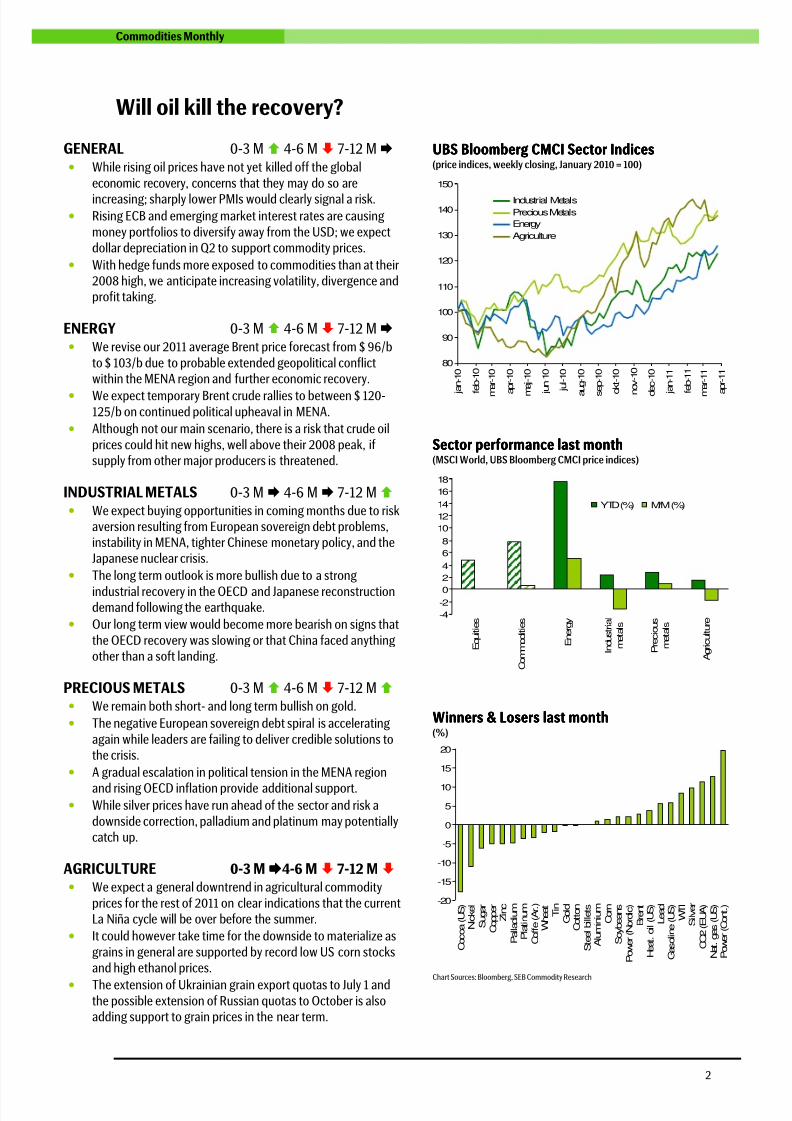

GENERAL 0-3 M 4-6 M 7-12 M • While rising oil prices have not yet killed off the global

economic recovery, concerns that they may do so are

increasing; sharply lower PMIs would clearly signal a risk.• Rising ECB and emerging market interest rates are causing

money portfolios to diversify away from the USD; we expectdollar depreciation in Q2 to support commodity prices.

• With hedge funds more exposed to commodities than at their2008 high, we anticipate increasing volatility, divergence andprofit taking.

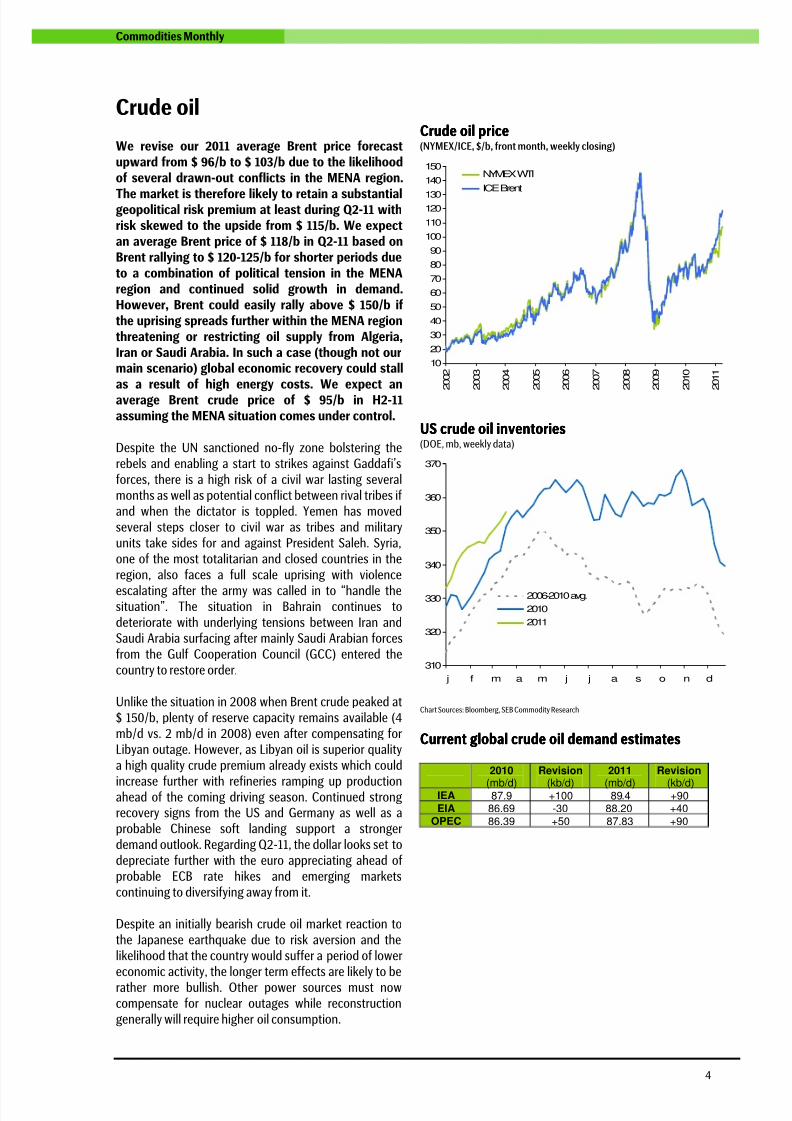

ENERGY 0-3 M 4-6 M 7-12 M • We revise our 2011 average Brent price forecast from $ 96/b

to $ 103/b due to probable extended geopolitical conflictwithin the MENA region and further economic recovery.

• We expect temporary Brent crude rallies to between $ 120-125/b on continued political upheaval in MENA.

• Although not our main scenario, there is a risk that crude oil

prices could hit new highs, well above their 2008 peak, ifsupply from other major producers is threatened.

INDUSTRIAL METALS 0-3 M 4-6 M 7-12 M • We expect buying opportunities in coming months due to risk

aversion resulting from European sovereign debt problems,instability in MENA, tighter Chinese monetary policy, and theJapanese nuclear crisis.

• The long term outlook is more bullish due to a strong

industrial recovery in the OECD and Japanese reconstructiondemand following the earthquake.

• Our long term view would become more bearish on signs that

the OECD recovery was slowing or that China faced anythingother than a soft landing.

PRECIOUS METALS 0-3 M 4-6 M 7-12 M • We remain both short- and long term bullish on gold.

• The negative European sovereign debt spiral is accelerating

again while leaders are failing to deliver credible solutions tothe crisis.

• A gradual escalation in political tension in the MENA region

and rising OECD inflation provide additional support.• While silver prices have run ahead of the sector and risk a

downside correction, palladium and platinum may potentiallycatch up.

AGRICULTURE 0-3 M4-6 M 7-12 M • We expect a general downtrend in agricultural commodity

prices for the rest of 2011 on clear indications that the currentLa Niña cycle will be over before the summer.

• It could however take time for the downside to materialize as

grains in general are supported by record low US corn stocksand high ethanol prices.

• The extension of Ukrainian grain export quotas to July 1 andthe possible extension of Russian quotas to October is alsoadding support to grain prices in the near term.

UBS Bloomberg CMCI Sector IndicesUBS Bloomberg CMCI Sector IndicesUBS Bloomberg CMCI Sector IndicesUBS Bloomberg CMCI Sector Indices(price indices, weekly closing, January 2010 = 100)

80

90

100

110

120

130

140

150

jan-10

feb-10

m

ar-10

a

pr-10

m

aj-10

jun-10

jul-10

aug-10

sep-10

o

kt-10

nov-10

dec-10

jan-11

feb-11

m

ar-11

a

pr-11

Industrial Metals

Precious Metals

Energy

Agriculture

Sector performance last monthSector performance last monthSector performance last monthSector performance last month(MSCI World, UBS Bloomberg CMCI price indices)

-4

-20

2

4

6

8

10

12

14

16

18

Equities

Commodities

Energy

Industrial

metals

Precious

metals

Agriculture

YTD (%) M/M (%)

Winners & Losers last monthWinners & Losers last monthWinners & Losers last monthWinners & Losers last month(%)

-20

-15

-10

-5

0

5

10

15

20

Cocoa (US)

Nickel

Sugar

CopperZinc

Palladium

Platinum

Coffe (Ar.)

Wheat Tin

Gold

Cotton

Steel billets

AluminiumCorn

Soybeans

Power (Nordic)

Brent

Heat. oil (US)

Lead

Gasoline (US)WTI

Silver

CO2 (EUA)

Nat. gas (US)

Power (Cont.)

Chart Sources: Bloomberg, SEB Commodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 3/20

3

Commodities Monthly

General

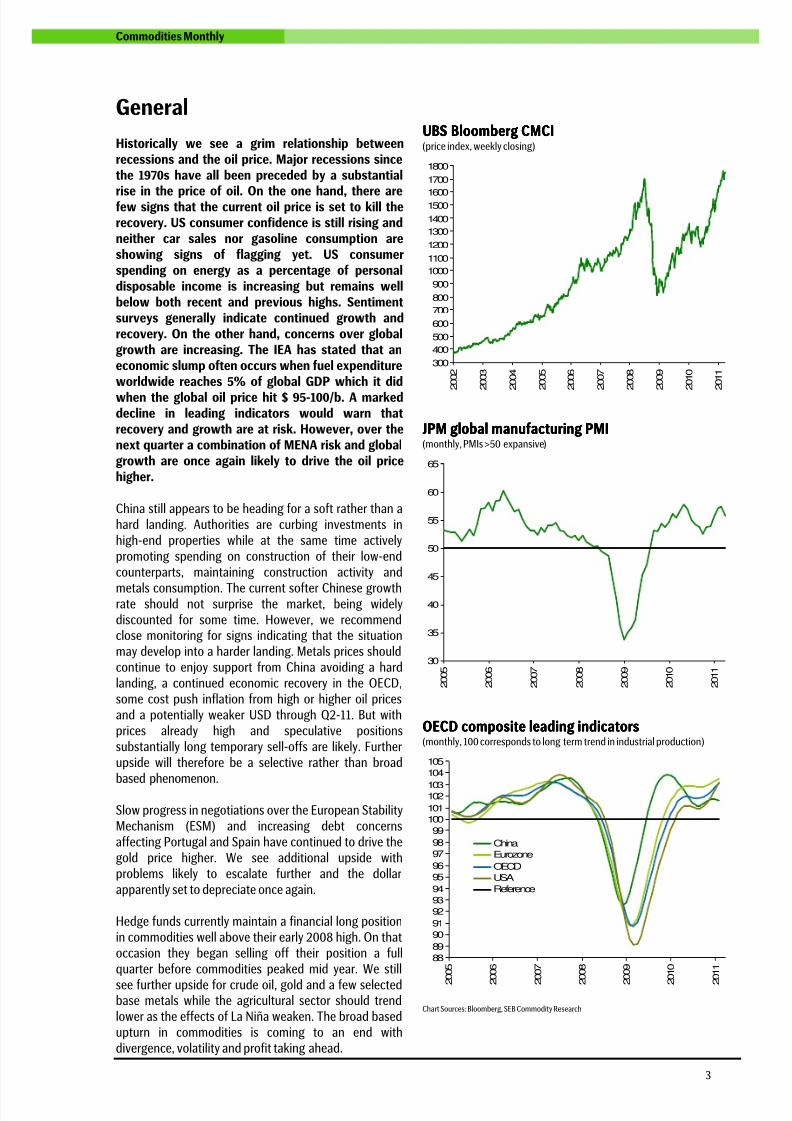

Historically we see a grim relationship betweenrecessions and the oil price. Major recessions sincethe 1970s have all been preceded by a substantial

rise in the price of oil. On the one hand, there arefew signs that the current oil price is set to kill therecovery. US consumer confidence is still rising andneither car sales nor gasoline consumption areshowing signs of flagging yet. US consumerspending on energy as a percentage of personaldisposable income is increasing but remains wellbelow both recent and previous highs. Sentimentsurveys generally indicate continued growth andrecovery. On the other hand, concerns over globalgrowth are increasing. The IEA has stated that aneconomic slump often occurs when fuel expenditureworldwide reaches 5% of global GDP which it did

when the global oil price hit $ 95-100/b. A markeddecline in leading indicators would warn thatrecovery and growth are at risk. However, over thenext quarter a combination of MENA risk and globalgrowth are once again likely to drive the oil pricehigher.

China still appears to be heading for a soft rather than ahard landing. Authorities are curbing investments inhigh-end properties while at the same time activelypromoting spending on construction of their low-endcounterparts, maintaining construction activity and

metals consumption. The current softer Chinese growthrate should not surprise the market, being widelydiscounted for some time. However, we recommendclose monitoring for signs indicating that the situationmay develop into a harder landing. Metals prices shouldcontinue to enjoy support from China avoiding a hardlanding, a continued economic recovery in the OECD,some cost push inflation from high or higher oil pricesand a potentially weaker USD through Q2-11. But withprices already high and speculative positionssubstantially long temporary sell-offs are likely. Furtherupside will therefore be a selective rather than broadbased phenomenon.

Slow progress in negotiations over the European StabilityMechanism (ESM) and increasing debt concernsaffecting Portugal and Spain have continued to drive thegold price higher. We see additional upside withproblems likely to escalate further and the dollarapparently set to depreciate once again.

Hedge funds currently maintain a financial long positionin commodities well above their early 2008 high. On thatoccasion they began selling off their position a fullquarter before commodities peaked mid year. We still

see further upside for crude oil, gold and a few selectedbase metals while the agricultural sector should trendlower as the effects of La Niña weaken. The broad basedupturn in commodities is coming to an end withdivergence, volatility and profit taking ahead.

UBSUBSUBSUBS Bloomberg CMCIBloomberg CMCIBloomberg CMCIBloomberg CMCI(price index, weekly closing)

300

400

500

600

700

800

900

1000

1100

1200

1300

1400

15001600

1700

1800

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

JPM global manufacturing PMIJPM global manufacturing PMIJPM global manufacturing PMIJPM global manufacturing PMI(monthly, PMIs >50 expansive)

30

35

40

45

50

55

60

65

2005

2006

2007

2008

2009

2010

2011

OECD composite leading indicatorsOECD composite leading indicatorsOECD composite leading indicatorsOECD composite leading indicators(monthly, 100 corresponds to long term trend in industrial production)

88

89

90

91

92

9394

95

96

97

98

99

100101

102103

104

105

2005

2006

2007

2008

2009

2010

2011

ChinaEurozone

OECDUSA

Reference

Chart Sources: Bloomberg, SEB Commodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 4/20

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 5/20

5

Commodities Monthly

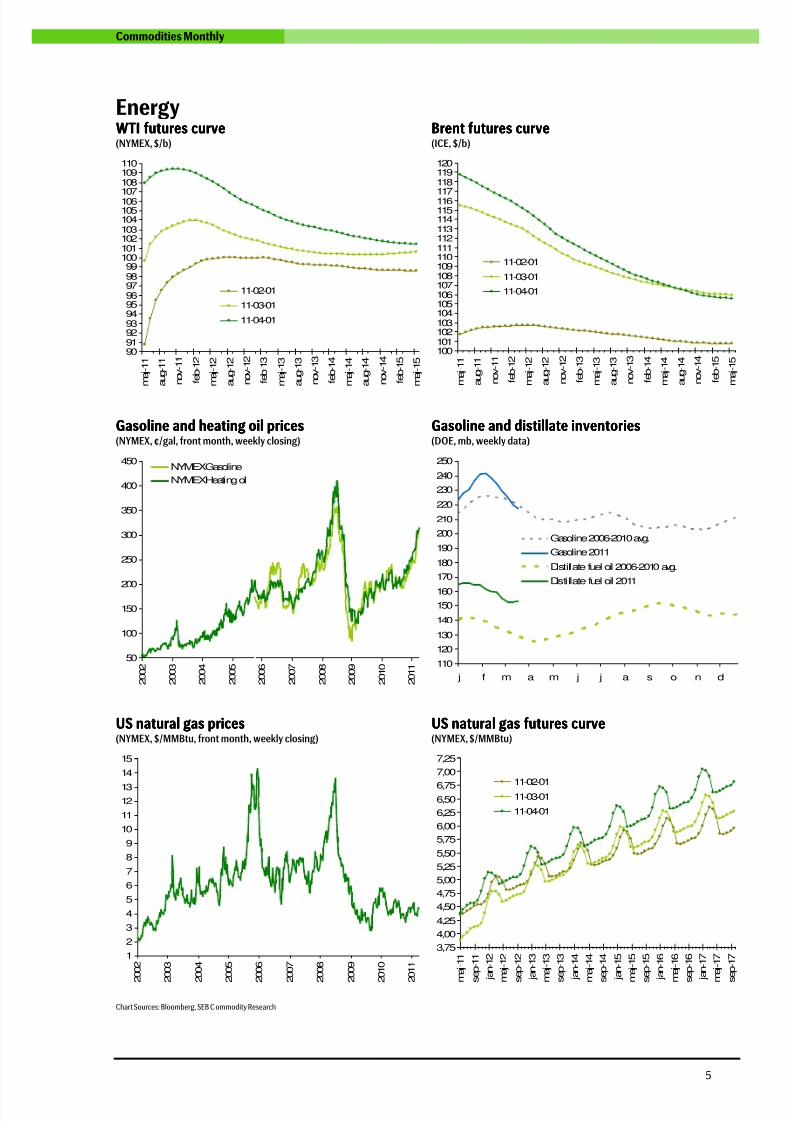

EnergyWTIWTIWTIWTI futures curvefutures curvefutures curvefutures curve(NYMEX, $/b)

BrentBrentBrentBrent futures curvefutures curvefutures curvefutures curve(ICE, $/b)

90919293949596979899

100101102103104105106107

108109110

maj-11

aug-11

nov-11

feb-12

maj-12

aug-12

nov-12

feb-13

maj-13

aug-13

nov-13

feb-14

maj-14

aug-14

nov-14

feb-15

maj-15

11-02-01

11-03-01

11-04-01

100101102103104105106107108109110111112113114115116117

118119120

maj-11

aug-11

nov-11

feb-12

maj-12

aug-12

nov-12

feb-13

maj-13

aug-13

nov-13

feb-14

maj-14

aug-14

nov-14

feb-15

maj-15

11-02-01

11-03-01

11-04-01

Gasoline and heating oil pricesGasoline and heating oil pricesGasoline and heating oil pricesGasoline and heating oil prices(NYMEX, ¢/gal, front month, weekly closing)

Gasoline and distillate inventoriesGasoline and distillate inventoriesGasoline and distillate inventoriesGasoline and distillate inventories(DOE, mb, weekly data)

50

100

150

200

250

300

350

400

450

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

NYMEX Gasoline

NYMEX Heating oil

110

120

130

140

150

160

170

180

190

200

210

220

230

240

250

j f m a m j j a s o n d

Gasoline 2006-2010 avg.

Gasoline 2011

Distillate fuel oil 2006-2010 avg.

Distillate fuel oil 2011

US natural gas pricesUS natural gas pricesUS natural gas pricesUS natural gas prices(NYMEX, $/MMBtu, front month, weekly closing)

US natural gasUS natural gasUS natural gasUS natural gas futures curvefutures curvefutures curvefutures curve(NYMEX, $/MMBtu)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

2

002

2

003

2

004

2

005

2

006

2

007

2

008

2

009

2

010

2

011

3,75

4,00

4,25

4,50

4,75

5,00

5,25

5,50

5,75

6,00

6,25

6,506,75

7,00

7,25

m

aj-11

s

ep-11

jan-12

m

aj-12

s

ep-12

jan-13

m

aj-13

s

ep-13

jan-14

m

aj-14

s

ep-14

jan-15

m

aj-15

s

ep-15

jan-16

m

aj-16

s

ep-16

jan-17

m

aj-17

s

ep-17

11-02-0111-03-01

11-04-01

Chart Sources: Bloomberg, SEB C ommodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 6/20

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 7/20

7

Commodities Monthly

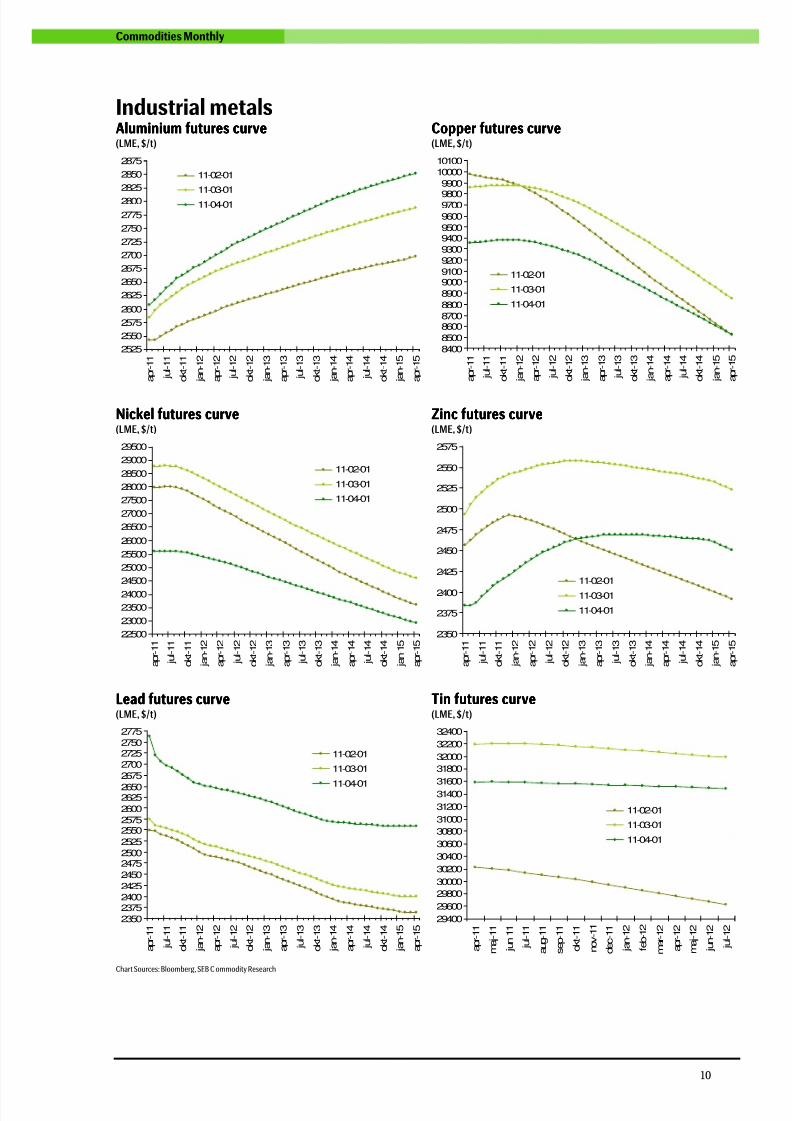

Industrial metals

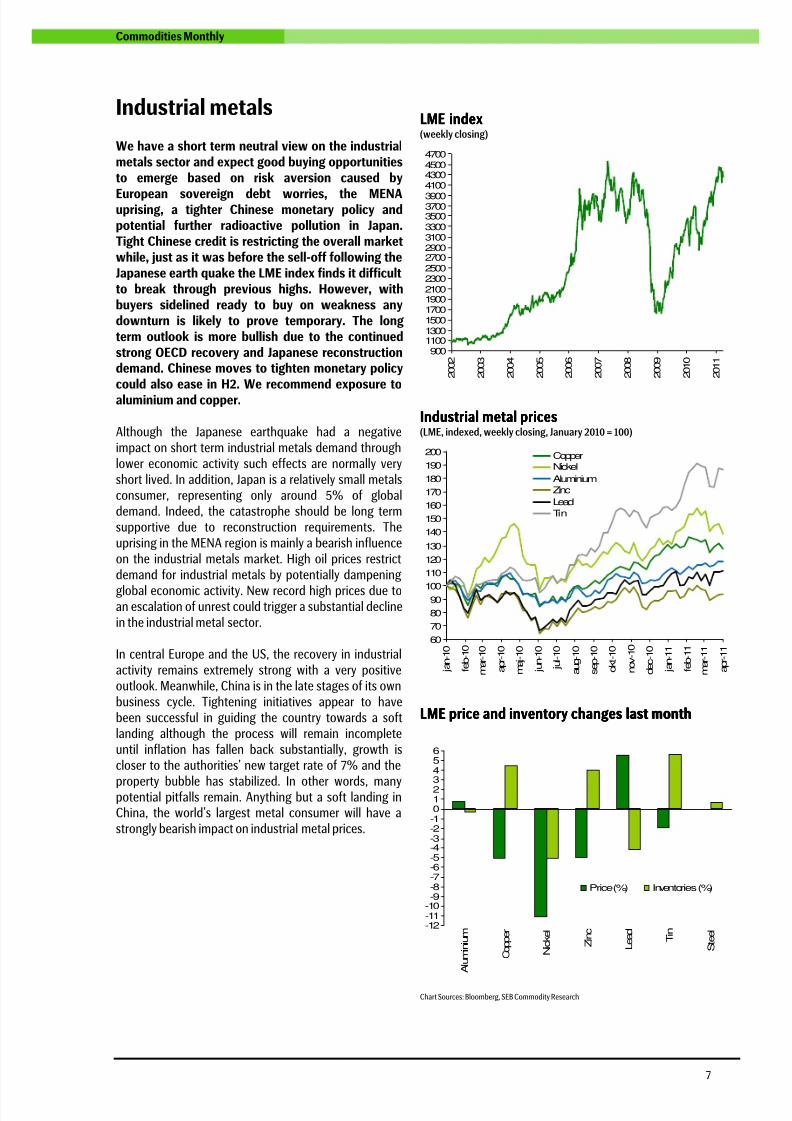

We have a short term neutral view on the industrialmetals sector and expect good buying opportunitiesto emerge based on risk aversion caused by

European sovereign debt worries, the MENAuprising, a tighter Chinese monetary policy andpotential further radioactive pollution in Japan.Tight Chinese credit is restricting the overall marketwhile, just as it was before the sell-off following theJapanese earth quake the LME index finds it difficultto break through previous highs. However, withbuyers sidelined ready to buy on weakness anydownturn is likely to prove temporary. The longterm outlook is more bullish due to the continuedstrong OECD recovery and Japanese reconstructiondemand. Chinese moves to tighten monetary policycould also ease in H2. We recommend exposure toaluminium and copper.

Although the Japanese earthquake had a negativeimpact on short term industrial metals demand throughlower economic activity such effects are normally veryshort lived. In addition, Japan is a relatively small metalsconsumer, representing only around 5% of globaldemand. Indeed, the catastrophe should be long termsupportive due to reconstruction requirements. Theuprising in the MENA region is mainly a bearish influenceon the industrial metals market. High oil prices restrictdemand for industrial metals by potentially dampening

global economic activity. New record high prices due toan escalation of unrest could trigger a substantial declinein the industrial metal sector.

In central Europe and the US, the recovery in industrialactivity remains extremely strong with a very positiveoutlook. Meanwhile, China is in the late stages of its ownbusiness cycle. Tightening initiatives appear to havebeen successful in guiding the country towards a softlanding although the process will remain incompleteuntil inflation has fallen back substantially, growth iscloser to the authorities’ new target rate of 7% and the

property bubble has stabilized. In other words, manypotential pitfalls remain. Anything but a soft landing inChina, the world’s largest metal consumer will have astrongly bearish impact on industrial metal prices.

LMELMELMELME indexindexindexindex(weekly closing)

900110013001500170019002100230025002700290031003300350037003900

4100430045004700

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

IndustrialIndustrialIndustrialIndustrial metal pricemetal pricemetal pricemetal pricessss(LME, indexed, weekly closing, January 2010 = 100)

60

70

80

90100

110

120

130

140

150

160

170

180

190

200

jan-10

feb-10

mar-10

apr-10

maj-10

jun-10

jul-10

aug-10

sep-10

okt-10

nov-10

dec-10

jan-11

feb-11

mar-11

apr-11

CopperNickel

AluminiumZinc

Lead

Tin

LME price and inventory changesLME price and inventory changesLME price and inventory changesLME price and inventory changes last monthlast monthlast monthlast month

-12-11-10-9-8-7-6-5-4-3-2-10123456

Aluminium

Copper

Nickel

Zinc

Lead Ti

n

Steel

Price (%) Inventories (%)

Chart Sources: Bloomberg, SEB Commodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 8/20

8

Commodities Monthly

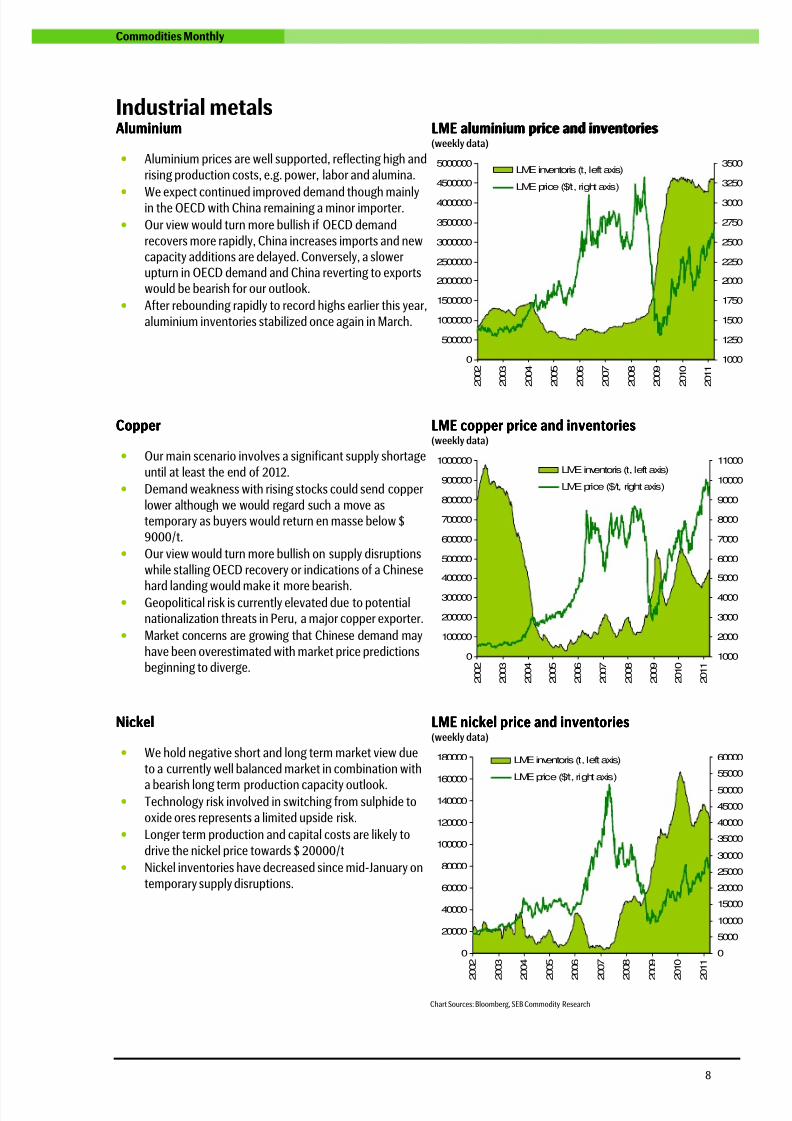

Industrial metalsAluminiumAluminiumAluminiumAluminium LME aluminium price and inventoriesLME aluminium price and inventoriesLME aluminium price and inventoriesLME aluminium price and inventories

(weekly data)

• Aluminium prices are well supported, reflecting high and

rising production costs, e.g. power, labor and alumina.

•

We expect continued improved demand though mainlyin the OECD with China remaining a minor importer.

• Our view would turn more bullish if OECD demand

recovers more rapidly, China increases imports and newcapacity additions are delayed. Conversely, a slowerupturn in OECD demand and China reverting to exportswould be bearish for our outlook.

• After rebounding rapidly to record highs earlier this year,

aluminium inventories stabilized once again in March.

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

5000000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1000

1250

1500

1750

2000

2250

2500

2750

3000

3250

3500LME inventoris (t, left axis)

LME price ($/t, right axis)

CopperCopperCopperCopper LME copper price and inventoriesLME copper price and inventoriesLME copper price and inventoriesLME copper price and inventories(weekly data)

• Our main scenario involves a significant supply shortage

until at least the end of 2012.

• Demand weakness with rising stocks could send copper

lower although we would regard such a move astemporary as buyers would return en masse below $9000/t.

• Our view would turn more bullish on supply disruptions

while stalling OECD recovery or indications of a Chinese

hard landing would make it more bearish.• Geopolitical risk is currently elevated due to potential

nationalization threats in Peru, a major copper exporter.

• Market concerns are growing that Chinese demand may

have been overestimated with market price predictionsbeginning to diverge.

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000LME inventoris (t, left axis)

LME price ($/t, right axis)

NickelNickelNickelNickel LME nickel price and inventoriesLME nickel price and inventoriesLME nickel price and inventoriesLME nickel price and inventories(weekly data)

• We hold negative short and long term market view due

to a currently well balanced market in combination with

a bearish long term production capacity outlook.• Technology risk involved in switching from sulphide to

oxide ores represents a limited upside risk.

• Longer term production and capital costs are likely to

drive the nickel price towards $ 20000/t

• Nickel inventories have decreased since mid-January on

temporary supply disruptions.

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

55000

60000LME inventoris (t, left axis)

LME price ($/t, right axis)

Chart Sources: Bloomberg, SEB Commodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 9/20

9

Commodities Monthly

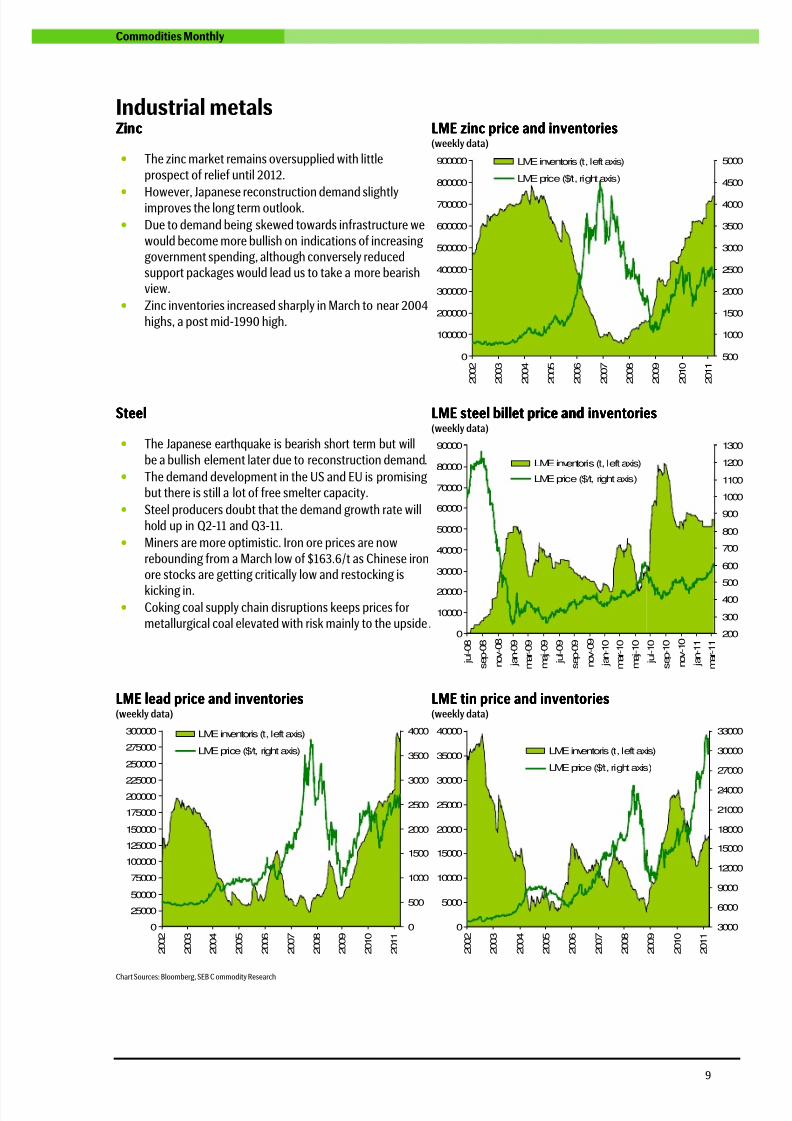

Industrial metalsZinZinZinZincccc LME zinc price and inventoriesLME zinc price and inventoriesLME zinc price and inventoriesLME zinc price and inventories

(weekly data)

• The zinc market remains oversupplied with little

prospect of relief until 2012.

•

However, Japanese reconstruction demand slightlyimproves the long term outlook.

• Due to demand being skewed towards infrastructure we

would become more bullish on indications of increasinggovernment spending, although conversely reducedsupport packages would lead us to take a more bearishview.

• Zinc inventories increased sharply in March to near 2004

highs, a post mid-1990 high.

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

500

1000

1500

2000

2500

3000

3500

4000

4500

5000LME inventoris (t, left axis)

LME price ($/t, right axis)

SteelSteelSteelSteel LME steel billet price and inventoriesLME steel billet price and inventoriesLME steel billet price and inventoriesLME steel billet price and inventories

(weekly data)

• The Japanese earthquake is bearish short term but will

be a bullish element later due to reconstruction demand.

• The demand development in the US and EU is promisingbut there is still a lot of free smelter capacity.

• Steel producers doubt that the demand growth rate will

hold up in Q2-11 and Q3-11.

• Miners are more optimistic. Iron ore prices are now

rebounding from a March low of $163.6/t as Chinese ironore stocks are getting critically low and restocking is

kicking in.• Coking coal supply chain disruptions keeps prices for

metallurgical coal elevated with risk mainly to the upside. 0

10000

20000

30000

40000

50000

60000

70000

80000

90000

jul-08

sep-08

nov-08

jan-09

mar-09

maj-09

jul-09

sep-09

nov-09

jan-10

mar-10

maj-10

jul-10

sep-10

nov-10

jan-11

mar-11

200

300

400

500

600

700

800

900

1000

1100

1200

1300

LME inventoris (t, left axis)

LME price ($/t, right axis)

LME lead price and inventoriesLME lead price and inventoriesLME lead price and inventoriesLME lead price and inventories(weekly data)

LME tin price and inventoriesLME tin price and inventoriesLME tin price and inventoriesLME tin price and inventories(weekly data)

0

25000

50000

75000

100000

125000

150000

175000

200000

225000

250000

275000

300000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0

500

1000

1500

2000

2500

3000

3500

4000LME inventoris (t, left axis)

LME price ($/t, right axis)

0

5000

10000

15000

20000

25000

30000

35000

40000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

3000

6000

9000

12000

15000

18000

21000

24000

27000

30000

33000

LME inventoris (t, left axis)

LME price ($/t, right axis)

Chart Sources: Bloomberg, SEB C ommodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 10/20

10

Commodities Monthly

Industrial metalsAluminiumAluminiumAluminiumAluminium futures curvefutures curvefutures curvefutures curve(LME, $/t)

Copper futures cCopper futures cCopper futures cCopper futures curveurveurveurve(LME, $/t)

2525

2550

2575

2600

2625

2650

2675

2700

2725

2750

2775

2800

2825

2850

2875

apr-11

jul-11

okt-11

jan-12

apr-12

jul-12

okt-12

jan-13

apr-13

jul-13

okt-13

jan-14

apr-14

jul-14

okt-14

jan-15

apr-15

11-02-01

11-03-01

11-04-01

84008500

860087008800

8900

900091009200930094009500

9600

97009800

9900

1000010100

apr-11

jul-11

okt-11

jan-12

apr-12

jul-12

okt-12

jan-13

apr-13

jul-13

okt-13

jan-14

apr-14

jul-14

okt-14

jan-15

apr-15

11-02-01

11-03-01

11-04-01

Nickel futures curveNickel futures curveNickel futures curveNickel futures curve(LME, $/t)

Zinc futures curveZinc futures curveZinc futures curveZinc futures curve(LME, $/t)

22500

23000

23500

24000

24500

25000

25500

26000

26500

27000

27500

28000

28500

29000

29500

apr-11

jul-11

okt-11

jan-12

apr-12

jul-12

okt-12

jan-13

apr-13

jul-13

okt-13

jan-14

apr-14

jul-14

okt-14

jan-15

apr-15

11-02-01

11-03-01

11-04-01

2350

2375

2400

2425

2450

2475

2500

2525

2550

2575

apr-11

jul-11

okt-11

jan-12

apr-12

jul-12

okt-12

jan-13

apr-13

jul-13

okt-13

jan-14

apr-14

jul-14

okt-14

jan-15

apr-15

11-02-01

11-03-01

11-04-01

Lead futures curveLead futures curveLead futures curveLead futures curve(LME, $/t)

Tin futures curveTin futures curveTin futures curveTin futures curve(LME, $/t)

2350237524002425

2450

247525002525

255025752600

26252650

26752700272527502775

apr-11

jul-11

okt-11

jan-12

apr-12

jul-12

okt-12

jan-13

apr-13

jul-13

okt-13

jan-14

apr-14

jul-14

okt-14

jan-15

apr-15

11-02-01

11-03-01

11-04-01

29400

29600

29800

30000

30200

30400

30600

30800

31000

31200

3140031600

31800

32000

32200

32400

apr-11

maj-11

jun-11

jul-11

aug-11

sep-11

okt-11

nov-11

dec-11

jan-12

feb-12

mar-12

apr-12

maj-12

jun-12

jul-12

11-02-01

11-03-01

11-04-01

Chart Sources: Bloomberg, SEB C ommodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 11/20

11

Commodities Monthly

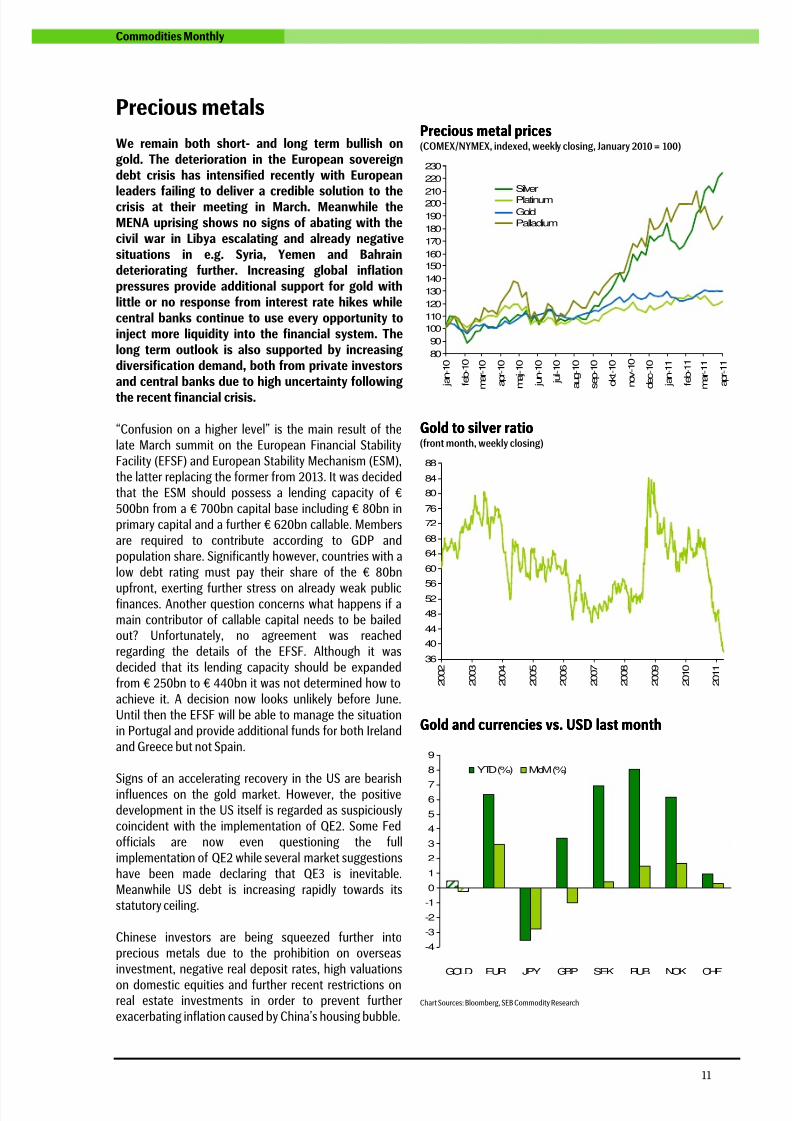

Precious metals

We remain both short- and long term bullish ongold. The deterioration in the European sovereigndebt crisis has intensified recently with European

leaders failing to deliver a credible solution to thecrisis at their meeting in March. Meanwhile theMENA uprising shows no signs of abating with thecivil war in Libya escalating and already negativesituations in e.g. Syria, Yemen and Bahraindeteriorating further. Increasing global inflationpressures provide additional support for gold withlittle or no response from interest rate hikes whilecentral banks continue to use every opportunity toinject more liquidity into the financial system. Thelong term outlook is also supported by increasingdiversification demand, both from private investorsand central banks due to high uncertainty following

the recent financial crisis.

“Confusion on a higher level” is the main result of thelate March summit on the European Financial StabilityFacility (EFSF) and European Stability Mechanism (ESM),the latter replacing the former from 2013. It was decidedthat the ESM should possess a lending capacity of €500bn from a € 700bn capital base including € 80bn inprimary capital and a further € 620bn callable. Membersare required to contribute according to GDP andpopulation share. Significantly however, countries with alow debt rating must pay their share of the € 80bn

upfront, exerting further stress on already weak publicfinances. Another question concerns what happens if amain contributor of callable capital needs to be bailedout? Unfortunately, no agreement was reachedregarding the details of the EFSF. Although it wasdecided that its lending capacity should be expandedfrom € 250bn to € 440bn it was not determined how toachieve it. A decision now looks unlikely before June.Until then the EFSF will be able to manage the situationin Portugal and provide additional funds for both Irelandand Greece but not Spain.

Signs of an accelerating recovery in the US are bearishinfluences on the gold market. However, the positivedevelopment in the US itself is regarded as suspiciouslycoincident with the implementation of QE2. Some Fedofficials are now even questioning the fullimplementation of QE2 while several market suggestionshave been made declaring that QE3 is inevitable.Meanwhile US debt is increasing rapidly towards itsstatutory ceiling.

Chinese investors are being squeezed further intoprecious metals due to the prohibition on overseasinvestment, negative real deposit rates, high valuations

on domestic equities and further recent restrictions onreal estate investments in order to prevent furtherexacerbating inflation caused by China’s housing bubble.

PreciousPreciousPreciousPrecious metal pricesmetal pricesmetal pricesmetal prices(COMEX/NYMEX, indexed, weekly closing, January 2010 = 100)

80

90

100

110

120

130

140

150

160

170

180

190

200210

220

230

jan-10

feb-10

mar-10

apr-10

maj-10

jun-10

jul-10

aug-10

sep-10

okt-10

nov-10

dec-10

jan-11

feb-11

mar-11

apr-11

Silver

Platinum

GoldPalladium

Gold to silver ratioGold to silver ratioGold to silver ratioGold to silver ratio(front month, weekly closing)

36

40

44

48

52

56

60

64

68

72

76

80

84

88

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Gold and currencies vs. USD last monthGold and currencies vs. USD last monthGold and currencies vs. USD last monthGold and currencies vs. USD last month

-4

-3

-2

-1

0

1

2

3

4

5

67

8

9

GOLD EUR JPY GBP SEK RUB NOK CHF

YTD (%) MoM (%)

Chart Sources: Bloomberg, SEB Commodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 12/20

12

Commodities Monthly

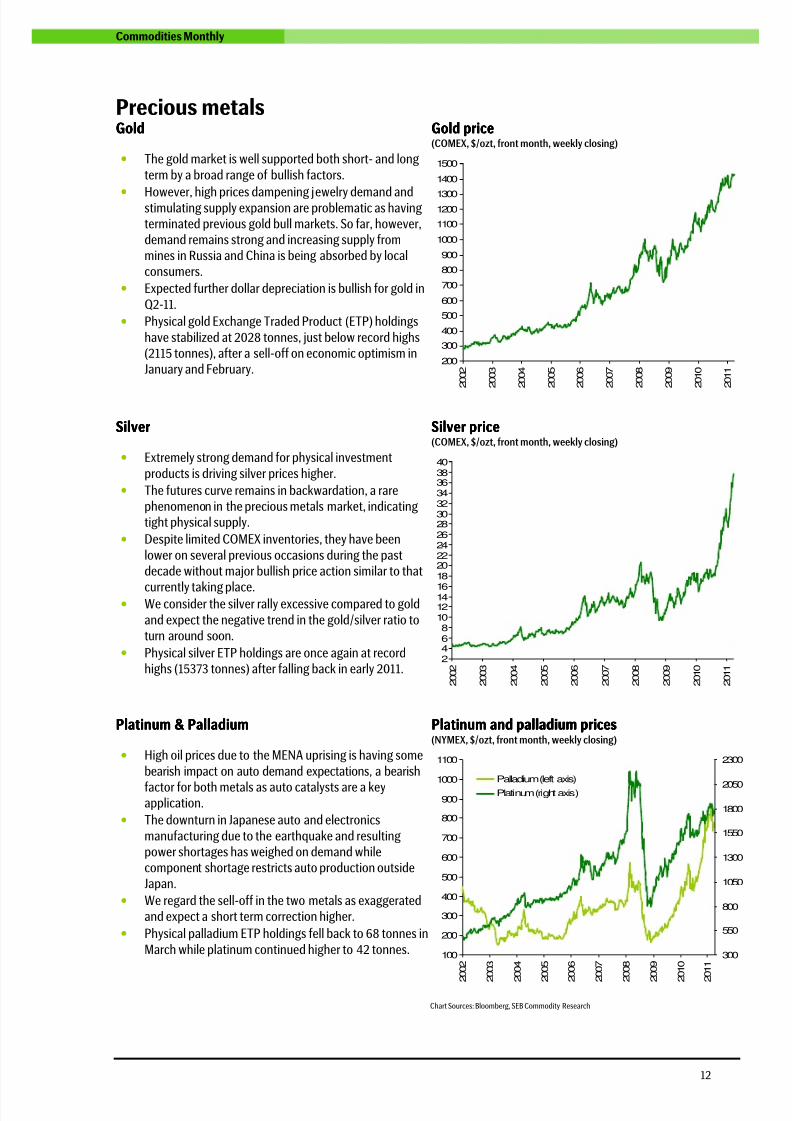

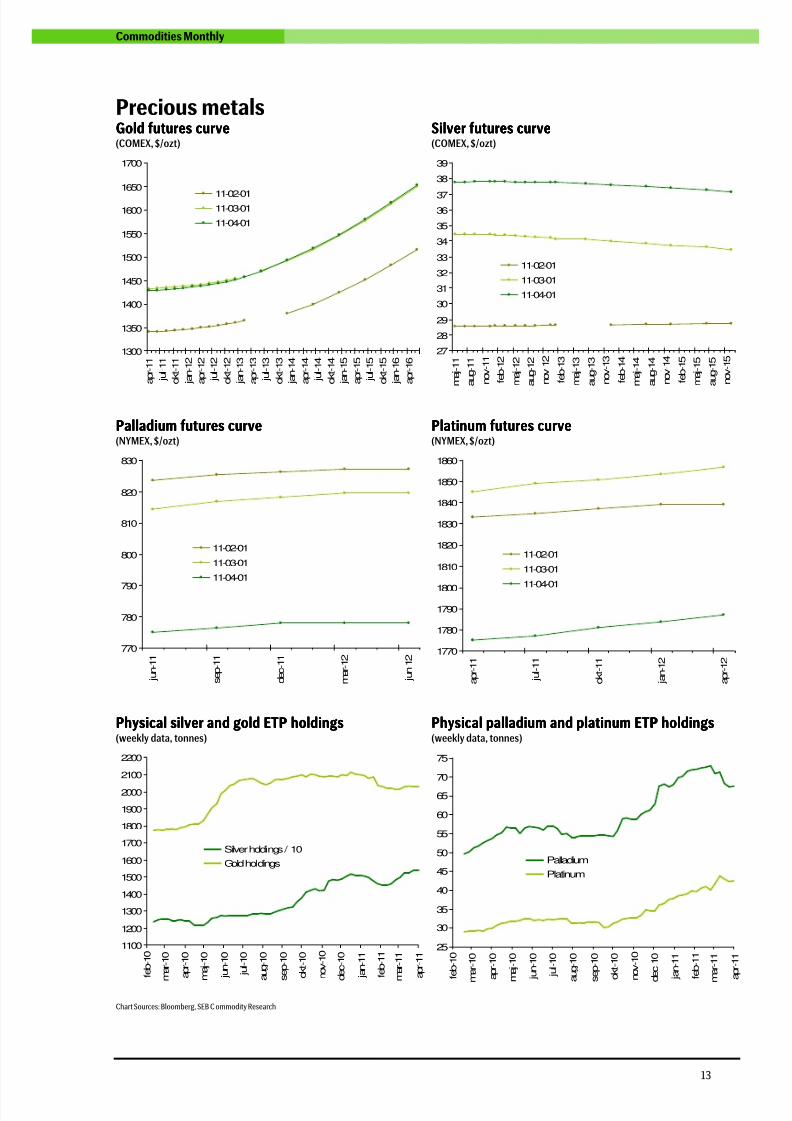

Precious metalsGoldGoldGoldGold Gold priceGold priceGold priceGold price

(COMEX, $/ozt, front month, weekly closing)

• The gold market is well supported both short- and long

term by a broad range of bullish factors.

•

However, high prices dampening jewelry demand andstimulating supply expansion are problematic as havingterminated previous gold bull markets. So far, however,demand remains strong and increasing supply frommines in Russia and China is being absorbed by localconsumers.

• Expected further dollar depreciation is bullish for gold in

Q2-11.

• Physical gold Exchange Traded Product (ETP) holdings

have stabilized at 2028 tonnes, just below record highs(2115 tonnes), after a sell-off on economic optimism inJanuary and February.

200

300

400

500

600

700

800

900

1000

1100

12001300

1400

1500

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

SilverSilverSilverSilver Silver priceSilver priceSilver priceSilver price(COMEX, $/ozt, front month, weekly closing)

• Extremely strong demand for physical investment

products is driving silver prices higher.

• The futures curve remains in backwardation, a rarephenomenon in the precious metals market, indicatingtight physical supply.

• Despite limited COMEX inventories, they have been

lower on several previous occasions during the pastdecade without major bullish price action similar to that

currently taking place.• We consider the silver rally excessive compared to gold

and expect the negative trend in the gold/silver ratio toturn around soon.

• Physical silver ETP holdings are once again at recordhighs (15373 tonnes) after falling back in early 2011.

2468

10121416

182022242628303234363840

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Platinum & PalladiumPlatinum & PalladiumPlatinum & PalladiumPlatinum & Palladium Platinum and palladium priPlatinum and palladium priPlatinum and palladium priPlatinum and palladium pricescescesces(NYMEX, $/ozt, front month, weekly closing)

• High oil prices due to the MENA uprising is having some

bearish impact on auto demand expectations, a bearish

factor for both metals as auto catalysts are a keyapplication.

• The downturn in Japanese auto and electronics

manufacturing due to the earthquake and resultingpower shortages has weighed on demand whilecomponent shortage restricts auto production outsideJapan.

• We regard the sell-off in the two metals as exaggeratedand expect a short term correction higher.

• Physical palladium ETP holdings fell back to 68 tonnes in

March while platinum continued higher to 42 tonnes. 100

200

300

400

500

600

700

800

900

1000

1100

2

002

2

003

2

004

2

005

2

006

2

007

2

008

2

009

2

010

2

011

300

550

800

1050

1300

1550

1800

2050

2300

Palladium (left axis)

Platinum (right axis)

Chart Sources: Bloomberg, SEB Commodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 13/20

13

Commodities Monthly

Precious metalsGoldGoldGoldGold futures curvefutures curvefutures curvefutures curve(COMEX, $/ozt)

SilverSilverSilverSilver futures curvefutures curvefutures curvefutures curve(COMEX, $/ozt)

1300

1350

1400

1450

1500

1550

1600

1650

1700

apr-11

jul-11

okt-11

jan-12

apr-12

jul-12

okt-12

jan-13

apr-13

jul-13

okt-13

jan-14

apr-14

jul-14

okt-14

jan-15

apr-15

jul-15

okt-15

jan-16

apr-16

11-02-0111-03-01

11-04-01

27

28

29

30

31

32

33

34

35

3637

38

39

maj-11

aug-11

nov-11

feb-12

maj-12

aug-12

nov-12

feb-13

maj-13

aug-13

nov-13

feb-14

maj-14

aug-14

nov-14

feb-15

maj-15

aug-15

nov-15

11-02-01

11-03-01

11-04-01

Palladium futures curvePalladium futures curvePalladium futures curvePalladium futures curve(NYMEX, $/ozt)

Platinum futures curvePlatinum futures curvePlatinum futures curvePlatinum futures curve(NYMEX, $/ozt)

770

780

790

800

810

820

830

jun-11

sep-11

dec-11

mar-12

jun-12

11-02-01

11-03-01

11-04-01

1770

1780

1790

1800

1810

1820

1830

1840

1850

1860

apr-11

jul-11

okt-11

jan-12

apr-12

11-02-01

11-03-01

11-04-01

Physical sPhysical sPhysical sPhysical silver and goldilver and goldilver and goldilver and gold ETETETETPPPP holdingsholdingsholdingsholdings(weekly data, tonnes)

Physical pPhysical pPhysical pPhysical palladium and platinumalladium and platinumalladium and platinumalladium and platinum ETETETETPPPP holdingsholdingsholdingsholdings(weekly data, tonnes)

1100

1200

1300

1400

1500

1600

1700

1800

1900

2000

2100

2200

feb-10

mar-10

apr-10

maj-10

jun-10

jul-10

aug-10

sep-10

okt-10

nov-10

dec-10

jan-11

feb-11

mar-11

apr-11

Silver holdings / 10

Gold holdings

25

30

35

40

45

50

55

60

65

70

75

feb-10

m

ar-10

apr-10

maj-10

jun-10

jul-10

aug-10

sep-10

okt-10

nov-10

dec-10

jan-11

feb-11

m

ar-11

apr-11

Palladium

Platinum

Chart Sources: Bloomberg, SEB C ommodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 14/20

14

Commodities Monthly

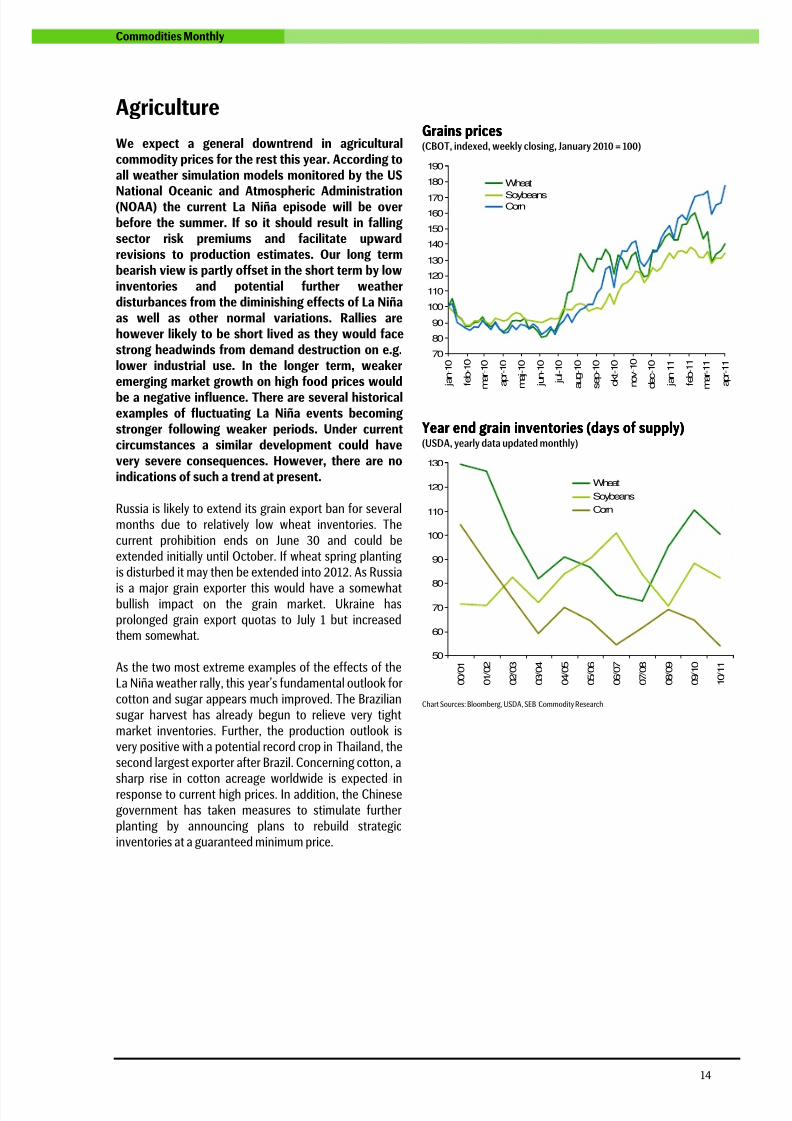

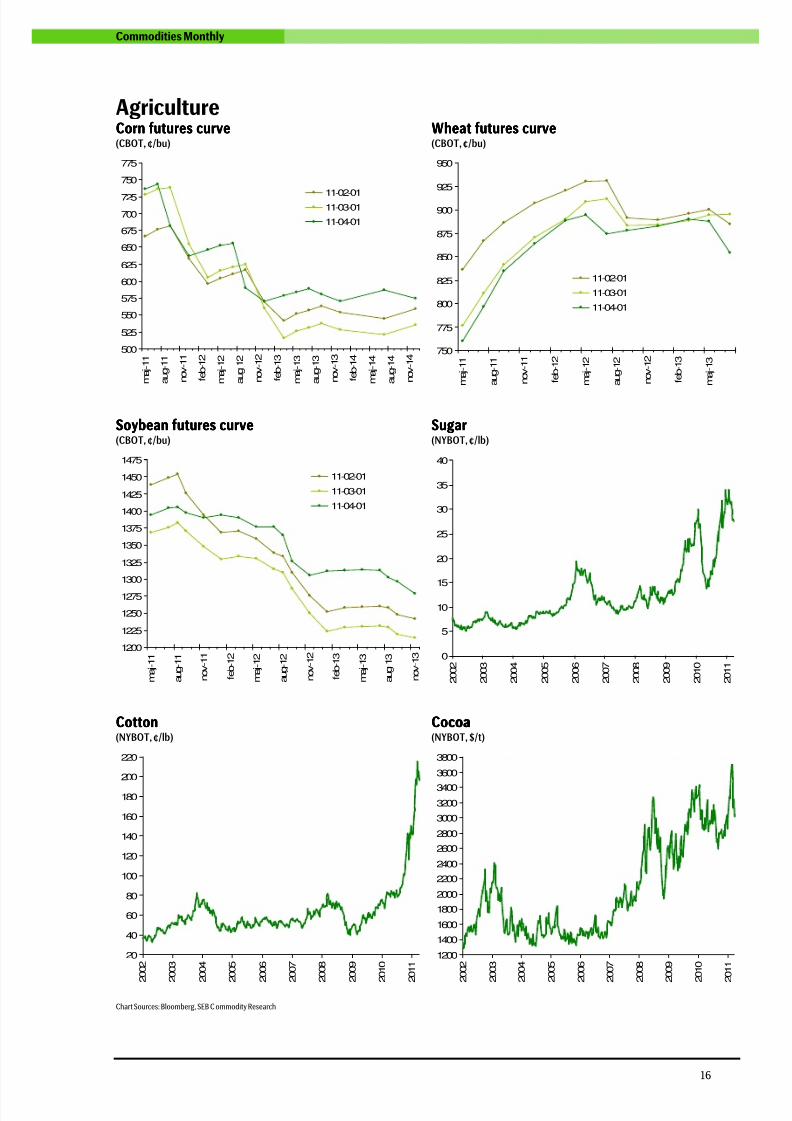

Agriculture

We expect a general downtrend in agriculturalcommodity prices for the rest this year. According toall weather simulation models monitored by the US

National Oceanic and Atmospheric Administration(NOAA) the current La Niña episode will be overbefore the summer. If so it should result in fallingsector risk premiums and facilitate upwardrevisions to production estimates. Our long termbearish view is partly offset in the short term by lowinventories and potential further weatherdisturbances from the diminishing effects of La Niñaas well as other normal variations. Rallies arehowever likely to be short lived as they would facestrong headwinds from demand destruction on e.g.lower industrial use. In the longer term, weakeremerging market growth on high food prices would

be a negative influence. There are several historicalexamples of fluctuating La Niña events becomingstronger following weaker periods. Under currentcircumstances a similar development could havevery severe consequences. However, there are noindications of such a trend at present.

Russia is likely to extend its grain export ban for severalmonths due to relatively low wheat inventories. Thecurrent prohibition ends on June 30 and could beextended initially until October. If wheat spring plantingis disturbed it may then be extended into 2012. As Russia

is a major grain exporter this would have a somewhatbullish impact on the grain market. Ukraine hasprolonged grain export quotas to July 1 but increasedthem somewhat.

As the two most extreme examples of the effects of theLa Niña weather rally, this year’s fundamental outlook forcotton and sugar appears much improved. The Braziliansugar harvest has already begun to relieve very tightmarket inventories. Further, the production outlook isvery positive with a potential record crop in Thailand, thesecond largest exporter after Brazil. Concerning cotton, asharp rise in cotton acreage worldwide is expected inresponse to current high prices. In addition, the Chinesegovernment has taken measures to stimulate furtherplanting by announcing plans to rebuild strategicinventories at a guaranteed minimum price.

Grains pricesGrains pricesGrains pricesGrains prices(CBOT, indexed, weekly closing, January 2010 = 100)

70

80

90

100

110

120

130

140

150

160

170

180

190

jan-10

feb-10

mar-10

apr-10

maj-10

jun-10

jul-10

aug-10

sep-10

okt-10

nov-10

dec-10

jan-11

feb-11

mar-11

apr-11

Wheat

SoybeansCorn

YYYYear endear endear endear end graingraingraingrain inventoriesinventoriesinventoriesinventories (days of supply)(days of supply)(days of supply)(days of supply)(USDA, yearly data updated monthly)

50

60

70

80

90

100

110

120

130

00/01

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

10/11

Wheat

Soybeans

Corn

Chart Sources: Bloomberg, USDA, SEB Commodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 15/20

15

Commodities Monthly

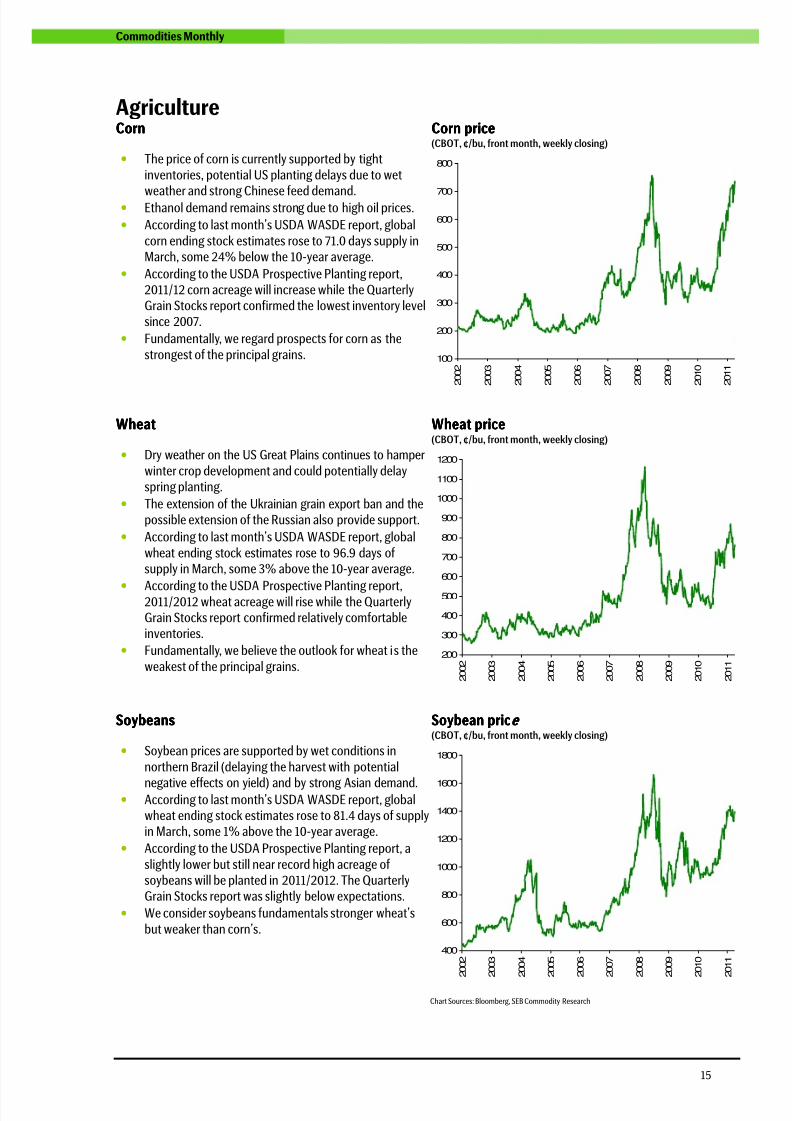

AgricultureCornCornCornCorn Corn priceCorn priceCorn priceCorn price

(CBOT, ¢/bu, front month, weekly closing)

• The price of corn is currently supported by tight

inventories, potential US planting delays due to wet

weather and strong Chinese feed demand.• Ethanol demand remains strong due to high oil prices.

• According to last month’s USDA WASDE report, global

corn ending stock estimates rose to 71.0 days supply inMarch, some 24% below the 10-year average.

• According to the USDA Prospective Planting report,2011/12 corn acreage will increase while the QuarterlyGrain Stocks report confirmed the lowest inventory levelsince 2007.

• Fundamentally, we regard prospects for corn as the

strongest of the principal grains. 100

200

300

400

500

600

700

800

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

WheatWheatWheatWheat Wheat priceWheat priceWheat priceWheat price(CBOT, ¢/bu, front month, weekly closing)

• Dry weather on the US Great Plains continues to hamper

winter crop development and could potentially delayspring planting.

• The extension of the Ukrainian grain export ban and thepossible extension of the Russian also provide support.

• According to last month’s USDA WASDE report, global

wheat ending stock estimates rose to 96.9 days ofsupply in March, some 3% above the 10-year average.

•

According to the USDA Prospective Planting report,2011/2012 wheat acreage will rise while the QuarterlyGrain Stocks report confirmed relatively comfortableinventories.

• Fundamentally, we believe the outlook for wheat is the

weakest of the principal grains.200

300

400

500

600

700

800

900

1000

1100

1200

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

SoybeansSoybeansSoybeansSoybeans Soybean pricSoybean pricSoybean pricSoybean price ee e

(CBOT, ¢/bu, front month, weekly closing)

• Soybean prices are supported by wet conditions in

northern Brazil (delaying the harvest with potential

negative effects on yield) and by strong Asian demand.• According to last month’s USDA WASDE report, global

wheat ending stock estimates rose to 81.4 days of supplyin March, some 1% above the 10-year average.

• According to the USDA Prospective Planting report, a

slightly lower but still near record high acreage ofsoybeans will be planted in 2011/2012. The QuarterlyGrain Stocks report was slightly below expectations.

• We consider soybeans fundamentals stronger wheat’s

but weaker than corn’s.

400

600

800

1000

1200

1400

1600

1800

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Chart Sources: Bloomberg, SEB Commodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 16/20

16

Commodities Monthly

AgricultureCornCornCornCorn futures curvefutures curvefutures curvefutures curve(CBOT, ¢/bu)

WheatWheatWheatWheat futures curvefutures curvefutures curvefutures curve(CBOT, ¢/bu)

500

525

550

575

600

625

650

675

700

725

750

775

maj-11

aug-11

nov-11

feb-12

maj-12

aug-12

nov-12

feb-13

maj-13

aug-13

nov-13

feb-14

maj-14

aug-14

nov-14

11-02-0111-03-01

11-04-01

750

775

800

825

850

875

900

925

950

maj-11

aug-11

nov-11

feb-12

maj-12

aug-12

nov-12

feb-13

maj-13

11-02-01

11-03-01

11-04-01

Soybean futures curveSoybean futures curveSoybean futures curveSoybean futures curve(CBOT, ¢/bu)

SugarSugarSugarSugar(NYBOT, ¢/lb)

1200

1225

1250

1275

1300

1325

1350

1375

1400

1425

1450

1475

maj-11

aug-11

nov-11

feb-12

maj-12

aug-12

nov-12

feb-13

maj-13

aug-13

nov-13

11-02-01

11-03-01

11-04-01

0

5

10

15

20

25

30

35

40

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

CottonCottonCottonCotton(NYBOT, ¢/lb)

CocoaCocoaCocoaCocoa(NYBOT, $/t)

20

40

60

80

100

120

140

160

180

200

220

2

002

2

003

2

004

2

005

2

006

2

007

2

008

2

009

2

010

2

011

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

3200

3400

3600

3800

2

002

2

003

2

004

2

005

2

006

2

007

2

008

2

009

2

010

2

011

Chart Sources: Bloomberg, SEB C ommodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 17/20

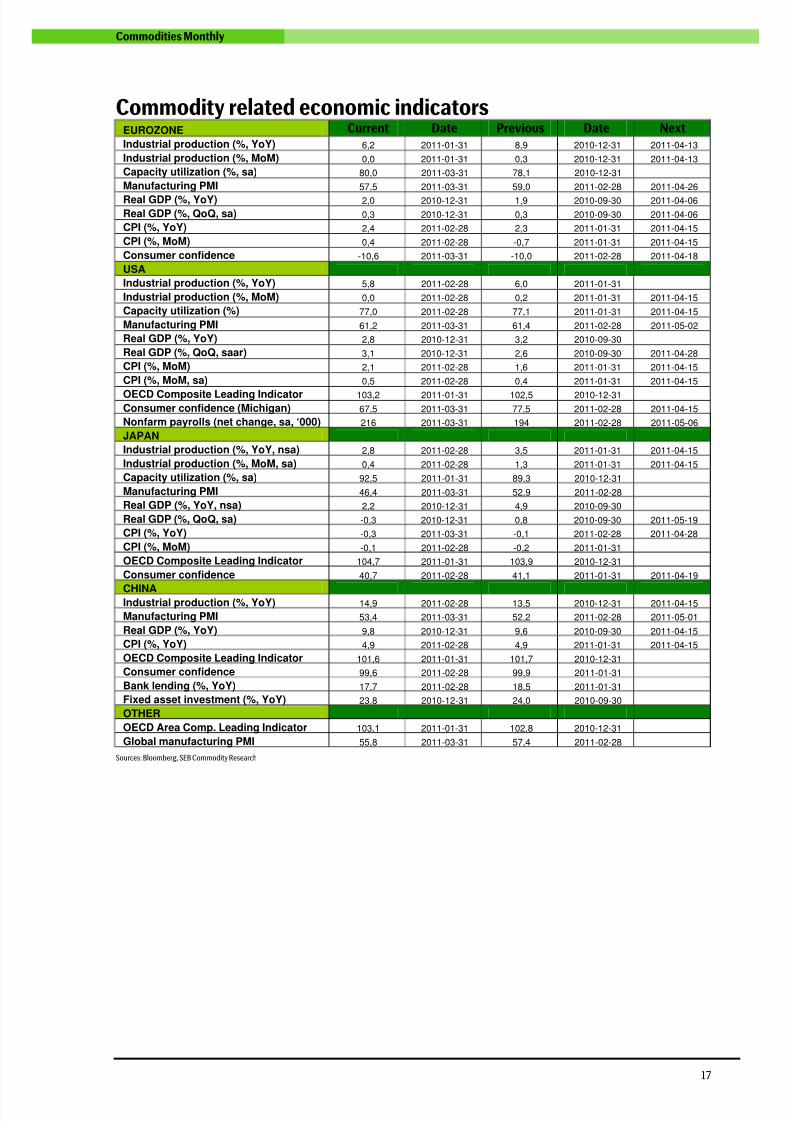

17

Commodities Monthly

Commodity related economic indicatorsEUROZONE Current Date Previous Date NextIndustrial production (%, YoY) 6,2 2011-01-31 8,9 2010-12-31 2011-04-13

Industrial production (%, MoM) 0,0 2011-01-31 0,3 2010-12-31 2011-04-13

Capacity utilization (%, sa) 80,0 2011-03-31 78,1 2010-12-31

Manufacturing PMI 57,5 2011-03-31 59,0 2011-02-28 2011-04-26

Real GDP (%, YoY) 2,0 2010-12-31 1,9 2010-09-30 2011-04-06

Real GDP (%, QoQ, sa) 0,3 2010-12-31 0,3 2010-09-30 2011-04-06

CPI (%, YoY) 2,4 2011-02-28 2,3 2011-01-31 2011-04-15

CPI (%, MoM) 0,4 2011-02-28 -0,7 2011-01-31 2011-04-15

Consumer confidence -10,6 2011-03-31 -10,0 2011-02-28 2011-04-18

USA

Industrial production (%, YoY) 5,8 2011-02-28 6,0 2011-01-31

Industrial production (%, MoM) 0,0 2011-02-28 0,2 2011-01-31 2011-04-15

Capacity utilization (%) 77,0 2011-02-28 77,1 2011-01-31 2011-04-15

Manufacturing PMI 61,2 2011-03-31 61,4 2011-02-28 2011-05-02

Real GDP (%, YoY) 2,8 2010-12-31 3,2 2010-09-30

Real GDP (%, QoQ, saar) 3,1 2010-12-31 2,6 2010-09-30 2011-04-28

CPI (%, MoM) 2,1 2011-02-28 1,6 2011-01-31 2011-04-15

CPI (%, MoM, sa) 0,5 2011-02-28 0,4 2011-01-31 2011-04-15

OECD Composite Leading Indicator 103,2 2011-01-31 102,5 2010-12-31

Consumer confidence (Michigan) 67,5 2011-03-31 77,5 2011-02-28 2011-04-15

Nonfarm payrolls (net change, sa, ‘000) 216 2011-03-31 194 2011-02-28 2011-05-06

JAPAN

Industrial production (%, YoY, nsa) 2,8 2011-02-28 3,5 2011-01-31 2011-04-15

Industrial production (%, MoM, sa) 0,4 2011-02-28 1,3 2011-01-31 2011-04-15

Capacity utilization (%, sa) 92,5 2011-01-31 89,3 2010-12-31

Manufacturing PMI 46,4 2011-03-31 52,9 2011-02-28

Real GDP (%, YoY, nsa) 2,2 2010-12-31 4,9 2010-09-30

Real GDP (%, QoQ, sa) -0,3 2010-12-31 0,8 2010-09-30 2011-05-19

CPI (%, YoY) -0,3 2011-03-31 -0,1 2011-02-28 2011-04-28

CPI (%, MoM) -0,1 2011-02-28 -0,2 2011-01-31

OECD Composite Leading Indicator 104,7 2011-01-31 103,9 2010-12-31

Consumer confidence 40,7 2011-02-28 41,1 2011-01-31 2011-04-19

CHINAIndustrial production (%, YoY) 14,9 2011-02-28 13,5 2010-12-31 2011-04-15

Manufacturing PMI 53,4 2011-03-31 52,2 2011-02-28 2011-05-01

Real GDP (%, YoY) 9,8 2010-12-31 9,6 2010-09-30 2011-04-15

CPI (%, YoY) 4,9 2011-02-28 4,9 2011-01-31 2011-04-15

OECD Composite Leading Indicator 101,6 2011-01-31 101,7 2010-12-31

Consumer confidence 99,6 2011-02-28 99,9 2011-01-31

Bank lending (%, YoY) 17,7 2011-02-28 18,5 2011-01-31

Fixed asset investment (%, YoY) 23,8 2010-12-31 24,0 2010-09-30

OTHER

OECD Area Comp. Leading Indicator 103,1 2011-01-31 102,8 2010-12-31

Global manufacturing PMI 55,8 2011-03-31 57,4 2011-02-28

Sources: Bloomberg, SEB Commodity Research

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 18/20

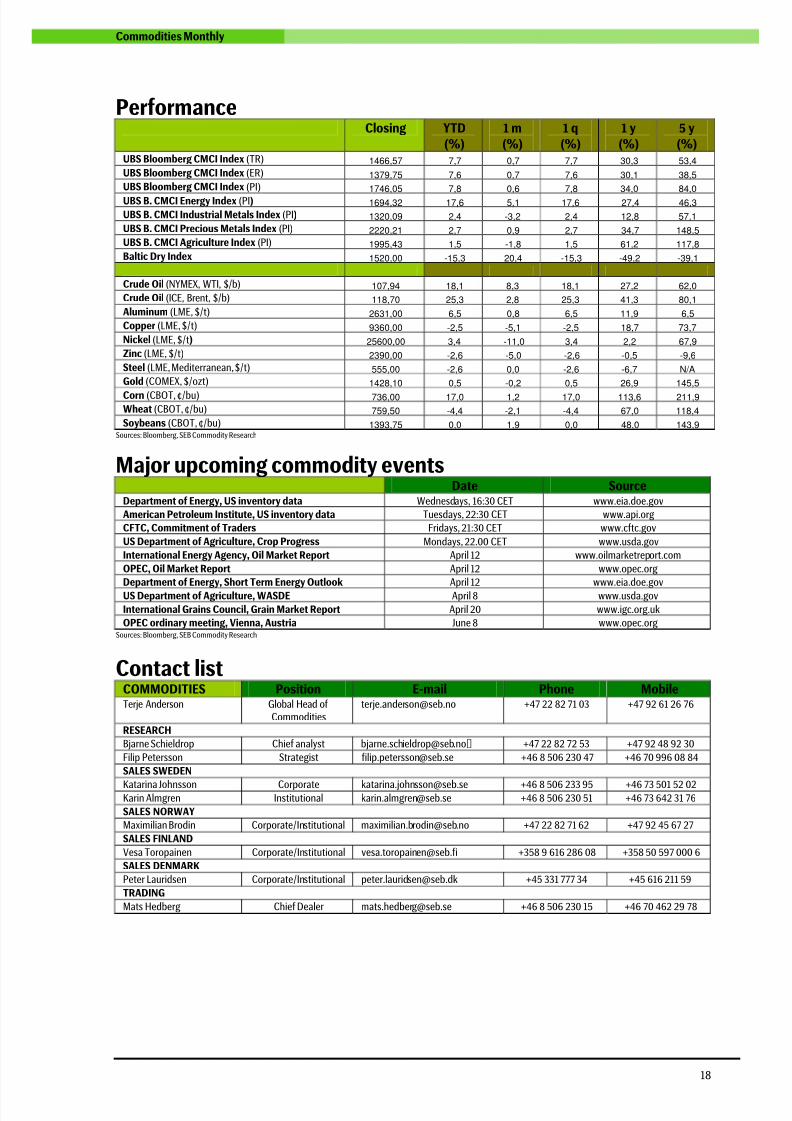

18

Commodities Monthly

PerformanceClosing YTD

(%)1 m(%)

1 q(%)

1 y(%)

5 y(%)

UBS Bloomberg CMCI Index (TR) 1466,57 7,7 0,7 7,7 30,3 53,4

UBS Bloomberg CMCI Index (ER) 1379,75 7,6 0,7 7,6 30,1 38,5

UBS Bloomberg CMCI Index (PI) 1746,05 7,8 0,6 7,8 34,0 84,0

UBS B. CMCI Energy Index (PI) 1694,32 17,6 5,1 17,6 27,4 46,3

UBS B. CMCI Industrial Metals Index (PI) 1320,09 2,4 -3,2 2,4 12,8 57,1

UBS B. CMCI Precious Metals Index (PI) 2220,21 2,7 0,9 2,7 34,7 148,5

UBS B. CMCI Agriculture Index (PI) 1995,43 1,5 -1,8 1,5 61,2 117,8

Baltic Dry Index 1520,00 -15,3 20,4 -15,3 -49,2 -39,1

Crude Oil (NYMEX, WTI, $/b) 107,94 18,1 8,3 18,1 27,2 62,0

Crude Oil (ICE, Brent, $/b) 118,70 25,3 2,8 25,3 41,3 80,1

Aluminum (LME, $/t) 2631,00 6,5 0,8 6,5 11,9 6,5

Copper (LME, $/t) 9360,00 -2,5 -5,1 -2,5 18,7 73,7

Nickel (LME, $/t) 25600,00 3,4 -11,0 3,4 2,2 67,9

Zinc (LME, $/t) 2390,00 -2,6 -5,0 -2,6 -0,5 -9,6

Steel (LME, Mediterranean, $/t) 555,00 -2,6 0,0 -2,6 -6,7 N/A

Gold (COMEX, $/ozt) 1428,10 0,5 -0,2 0,5 26,9 145,5

Corn (CBOT, ¢/bu) 736,00 17,0 1,2 17,0 113,6 211,9

Wheat (CBOT, ¢/bu) 759,50 -4,4 -2,1 -4,4 67,0 118,4

Soybeans (CBOT, ¢/bu) 1393,75 0,0 1,9 0,0 48,0 143,9Sources: Bloomberg, SEB Commodity Research

Major upcoming commodity eventsDate Source

Department of Energy, US inventory data Wednesdays, 16:30 CET www.eia.doe.gov

American Petroleum Institute, US inventory data Tuesdays, 22:30 CET www.api.org

CFTC, Commitment of Traders Fridays, 21:30 CET www.cftc.gov

US Department of Agriculture, Crop Progress Mondays, 22.00 CET www.usda.gov

International Energy Agency, Oil Market Report April 12 www.oilmarketreport.com

OPEC, Oil Market Report April 12 www.opec.org

Department of Energy, Short Term Energy Outlook April 12 www.eia.doe.gov

US Department of Agriculture, WASDE April 8 www.usda.gov

International Grains Council, Grain Market Report April 20 www.igc.org.uk

OPEC ordinary meeting, Vienna, Austria June 8 www.opec.orgSources: Bloomberg, SEB Commodity Research

Contact listCOMMODITIES Position E-mail Phone MobileTerje Anderson Global Head of

[email protected] +47 22 82 71 03 +47 92 61 26 76

RESEARCH

Bjarne Schieldrop Chief analyst [email protected] +47 22 82 72 53 +47 92 48 92 30

Filip Petersson Strategist [email protected] +46 8 506 230 47 +46 70 996 08 84

SALES SWEDEN

Katarina Johnsson Corporate [email protected] +46 8 506 233 95 +46 73 501 52 02Karin Almgren Institutional [email protected] +46 8 506 230 51 +46 73 642 31 76

SALES NORWAY

Maximilian Brodin Corporate/Institutional [email protected] +47 22 82 71 62 +47 92 45 67 27

SALES FINLAND

Vesa Toropainen Corporate/Institutional [email protected] +358 9 616 286 08 +358 50 597 000 6

SALES DENMARK

Peter Lauridsen Corporate/Institutional [email protected] +45 331 777 34 +45 616 211 59

TRADING

Mats Hedberg Chief Dealer [email protected] +46 8 506 230 15 +46 70 462 29 78

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 19/20

19

Commodities Monthly

DISCLAIMER & CONFIDENTIALITY NOTICE

The information in this document has been compiled by SEB Merchant Banking, a division within Skandinaviska EnskildaBanken AB (publ) (“SEB”).

Opinions contained in this report represent the bank’s present opinion only and are subject to change without notice. All

information contained in this report has been compiled in good faith from sources believed to be reliable. However, norepresentation or warranty, expressed or implied, is made with respect to the completeness or accuracy of its contents andthe information is not to be relied upon as authoritative. Anyone considering taking actions based upon the content of thisdocument is urged to base his or her investment decisions upon such investigations as he or she deems necessary. Thisdocument is being provided as information only, and no specific actions are being solicited as a result of it; to the extentpermitted by law, no liability whatsoever is accepted for any direct or consequential loss arising from use of this documentor its contents.

SEB is a public company incorporated in Stockholm, Sweden, with limited liability. It is a participant at major Nordic andother European Regulated Markets and Multilateral Trading Facilities (as well as some non-European equivalent markets)for trading in financial instruments, such as markets operated by NASDAQ OMX, NYSE Euronext, London Stock Exchange,Deutsche Börse, Swiss Exchanges, Turquoise and Chi-X. SEB is authorized and regulated by Finansinspektionen in Sweden;

it is authorized and subject to limited regulation by the Financial Services Authority for the conduct of designatedinvestment business in the UK, and is subject to the provisions of relevant regulators in all other jurisdictions where SEBconducts operations.

SEB Merchant Banking. All rights reserved.

SEB Commodity Research

Bjarne Schieldrop, Chief Commodity [email protected]

+47 9248 9230

Filip Petersson, Commodity [email protected]

+46 8 506 230 47

8/7/2019 SEB’s Commodities Monthly: Will oil kill the recovery?

http://slidepdf.com/reader/full/sebs-commodities-monthly-will-oil-kill-the-recovery 20/20

www.seb.se/mb