Embed Size (px)

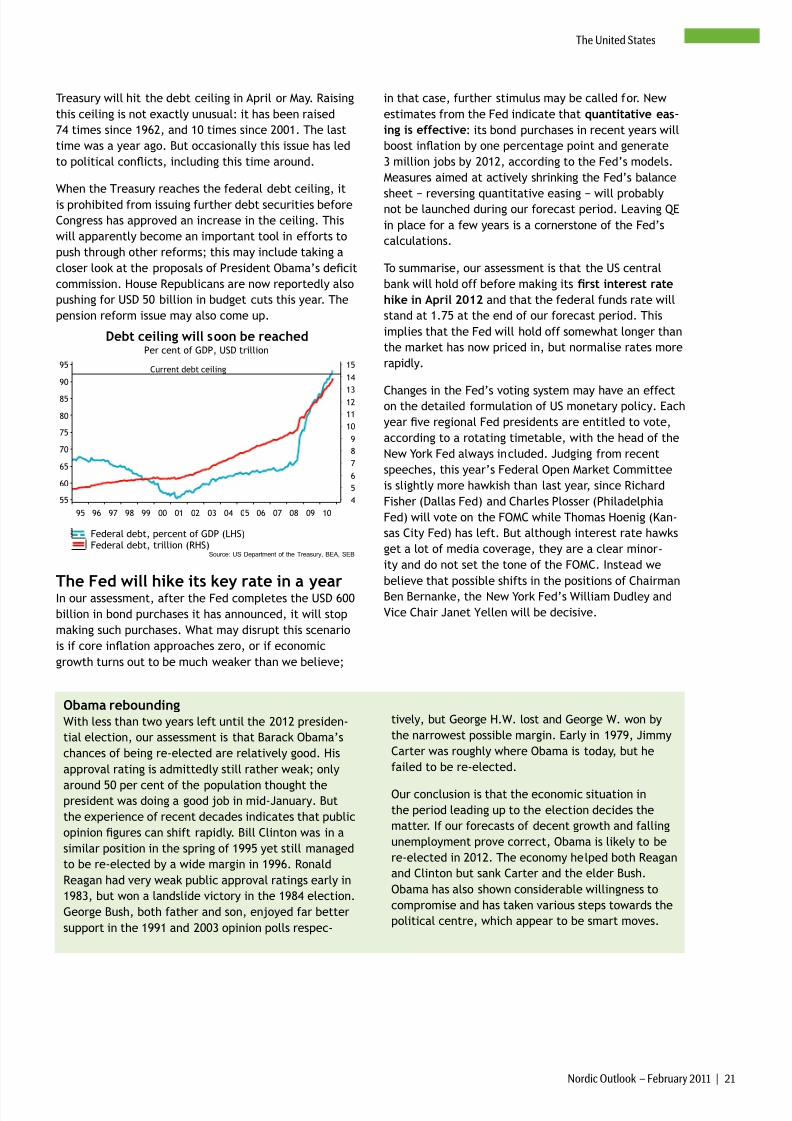

Citation preview

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 1/55

Recovery becoming moreself-sustaining

Faster Nordic key rate hikes

Nordic OutlookEconomic Research – February 2011

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 2/55

Contents

Nordic Outlook – February 2011 | 3

International overview 5

Theme: A model for long-term equilibriumexhange rates (SEBEER) 15

The United States 16

Japan 22

Asia 23

The euro zone 26

The United Kingdom 32

Eastern Europe 33

The Baltics 34

Sweden 36

Denmark 45

Norway 46

Finland 50

Economic data 51

Boxes

Risk and opportunities in North Africa 6

“United Debt of Europe” 8

Continued high commodity prices 10

Falling private sector savings boosts GDP 17

Home price drop jeopardises recovery 18

Little risk of 1970s-style stagation 20

Obama rebounding 21

China’s twelfth ve-year plan, 2011-2015 25

ECB questioning core ination as an indicator 31

The Riksbank and macro supervisory rules 41

Fiscal policy has an expansionary bias 47

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 3/55

4 | Nordic Outlook – February 2011

Economic Research

This report was published on February 8, 2011.

Cut-off date for calculations and foreasts was February 3, 2011.

Robert Bergqvist Håkan FrisénChief Economist Head of Economic Research+ 46 8 506 230 16 + 46 8 763 80 67

Daniel Bergvall Mattias BruérEconomist Economist+46 8 763 85 94 + 46 8 763 85 06

Ann Enshagen Lavebrink Mikael Johansson

Editorial Assistant Economist+ 46 8 763 80 77 + 46 8 763 80 93

Andreas Johnson Tomas LindströmEconomist Economist+46 8 763 80 32 + 46 8 763 80 28

Gunilla Nyström Ingela HemmingGlobal Head of Personal Finance Research Global Head of Small Business Research+ 46 8 763 65 81 + 46 8 763 82 97

Susanne Eliasson Johanna WahlstenPersonal Finance Analyst Small Business Analyst+ 46 8 763 65 88 + 46 8 763 80 72

SEB Economic Research, K-A3, SE-106 40 Stockholm

Contributions to this report have been made by Thomas Köbel, SEB Frankfurt/M and Olle Holmgren,

Trading Strategy. Stein Bruun and Erica Blomgren, SEB Oslo are responsible for the Norwegian analysis.

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 4/55

International overview

Nordic Outlook – February 2011 | 5

The recovery is becoming more self-sustaining Stronger momentum as the US accelerates

Ination will fall − increasing focus onresource utilisation

ECB hike in September, Fed only in 2012

The Riksbank will speed up its rate hikes

Long-term yields sideways next 6 months

Nordic currencies will keep appreciating

In recent months, the global economic outlook has

improved. US growth expectations have risen. Fiscal

policy will be more expansionary in 2011, now that

Congress has resolved important taxation issues. In

addition, the American recovery is entering a more

self-sustaining phase, despite lingering problems in

the labour and housing markets. Emerging economies,

especially in Asia, are continuing their strong expan-

sion although tighter economic policies will now lead

to a slight deceleration. In Europe, economic signals

are more mixed. In Germany and the Nordic countries,

2011 growth will be stronger than we had previously

expected. The United Kingdom is now beginning to feel

the impact of tight scal policy. In southern Europe and

Ireland, growth will be hampered by continued nancial

turmoil and necessary budget consolidation measures.

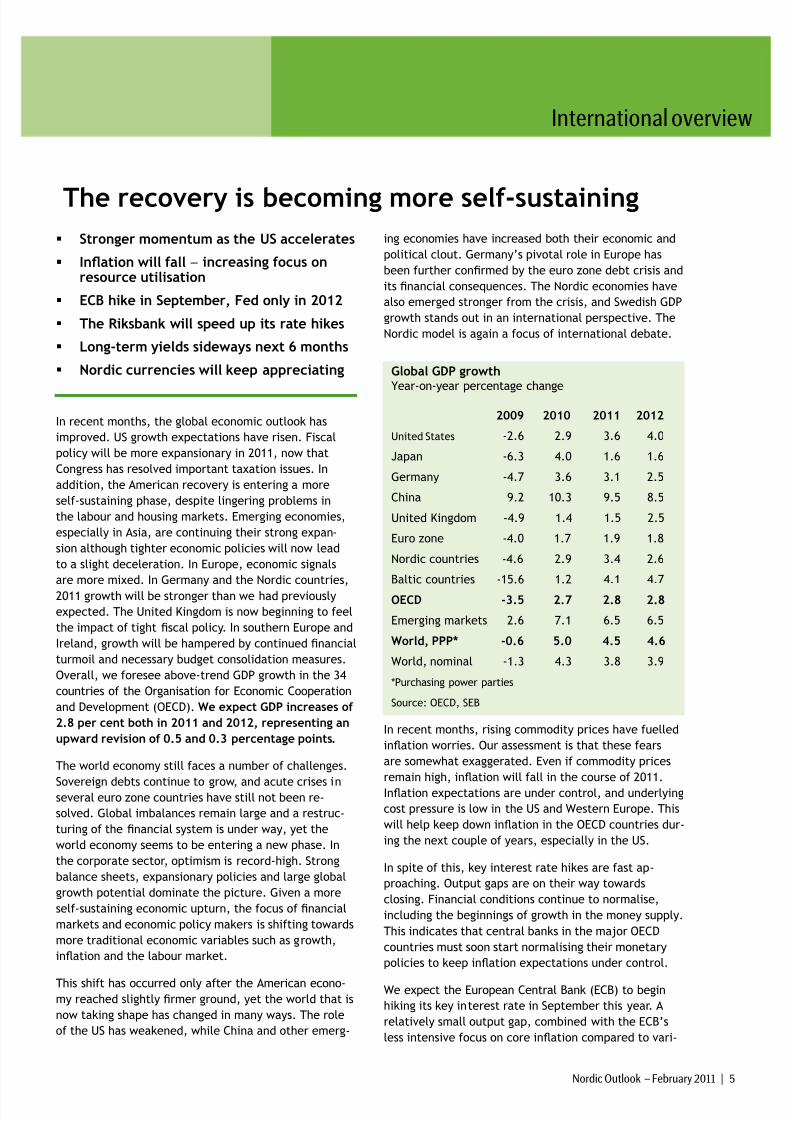

Overall, we foresee above-trend GDP growth in the 34

countries of the Organisation for Economic Cooperation

and Development (OECD). We expect GDP increases of

2.8 per cent both in 2011 and 2012, representing an

upward revision of 0.5 and 0.3 percentage points.

The world economy still faces a number of challenges.

Sovereign debts continue to grow, and acute crises inseveral euro zone countries have still not been re-

solved. Global imbalances remain large and a restruc-

turing of the nancial system is under way, yet the

world economy seems to be entering a new phase. In

the corporate sector, optimism is record-high. Strong

balance sheets, expansionary policies and large global

growth potential dominate the picture. Given a more

self-sustaining economic upturn, the focus of nancial

markets and economic policy makers is shifting towards

more traditional economic variables such as growth,

ination and the labour market.

This shift has occurred only after the American econo-my reached slightly rmer ground, yet the world that is

now taking shape has changed in many ways. The role

of the US has weakened, while China and other emerg-

ing economies have increased both their economic and

political clout. Germany’s pivotal role in Europe has

been further conrmed by the euro zone debt crisis and

its nancial consequences. The Nordic economies have

also emerged stronger from the crisis, and Swedish GDP

growth stands out in an international perspective. The

Nordic model is again a focus of international debate.

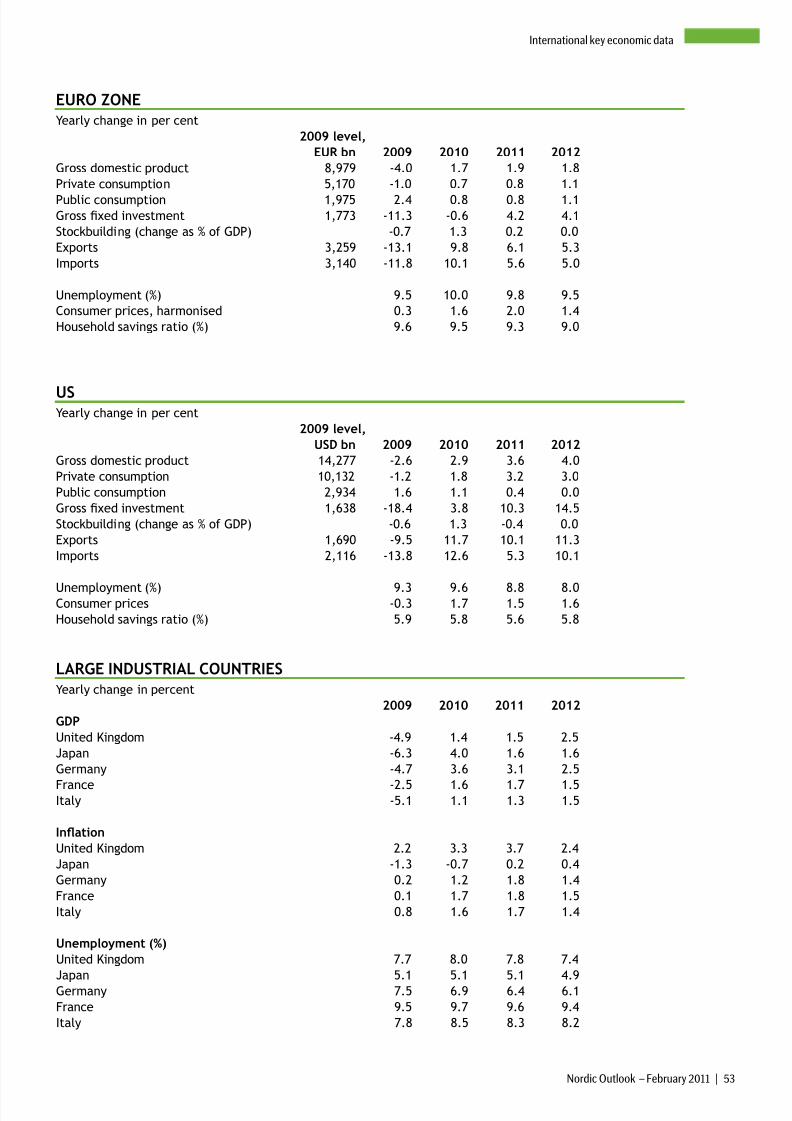

Global GDP growth Year-on-year percentage change

2009 2010 2011 2012

United States -2.6 2.9 3.6 4.0

Japan -6.3 4.0 1.6 1.6

Germany -4.7 3.6 3.1 2.5

China 9.2 10.3 9.5 8.5

United Kingdom -4.9 1.4 1.5 2.5

Euro zone -4.0 1.7 1.9 1.8

Nordic countries -4.6 2.9 3.4 2.6

Baltic countries -15.6 1.2 4.1 4.7

OECD -3.5 2.7 2.8 2.8

Emerging markets 2.6 7.1 6.5 6.5

World, PPP* -0.6 5.0 4.5 4.6

World, nominal -1.3 4.3 3.8 3.9

*Purchasing power parties

Source: OECD, SEB

In recent months, rising commodity prices have fuelled

ination worries. Our assessment is that these fears

are somewhat exaggerated. Even if commodity prices

remain high, ination will fall in the course of 2011.

Ination expectations are under control, and underlying

cost pressure is low in the US and Western Europe. This

will help keep down ination in the OECD countries dur-

ing the next couple of years, especially in the US.

In spite of this, key interest rate hikes are fast ap-

proaching. Output gaps are on their way towards

closing. Financial conditions continue to normalise,

including the beginnings of growth in the money supply.

This indicates that central banks in the major OECD

countries must soon start normalising their monetary

policies to keep ination expectations under control.

We expect the European Central Bank (ECB) to begin

hiking its key interest rate in September this year. A

relatively small output gap, combined with the ECB’s

less intensive focus on core ination compared to vari-

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 5/55

6 | Nordic Outlook – February 2011

International overview

ous other central banks, will contribute to earlier rate

hikes. To some extent, the expansion of the European

nancial stability mechanism (ESFS/ESM) is also taking

pressure off the ECB, enabling the bank to focus to a

greater extent on its main task: ensuring price stabil-

ity. High ination gures will also help to persuade the

Bank of England (BoE) to begin key rate hikes beforethe end of 2011. Because of high unemployment and

a continued decline in core ination, the US Federal

Reserve (Fed) will hold off until April 2012 before begin-

ning its rate hikes.

The Nordic central banks will continue raising their key

interest rates. Partly due to rapidly climbing resource

utilisation, Sweden’s Riksbank will adopt a more aggres-

sive stance during 2011. We expect it to hike the repo

rate to 2.75 per cent by year-end. Norges Bank, too,

will nd it easier to raise its deposit rate in response to

Norwegian domestic conditions once the ECB and BoE

also begin hiking their key rates.

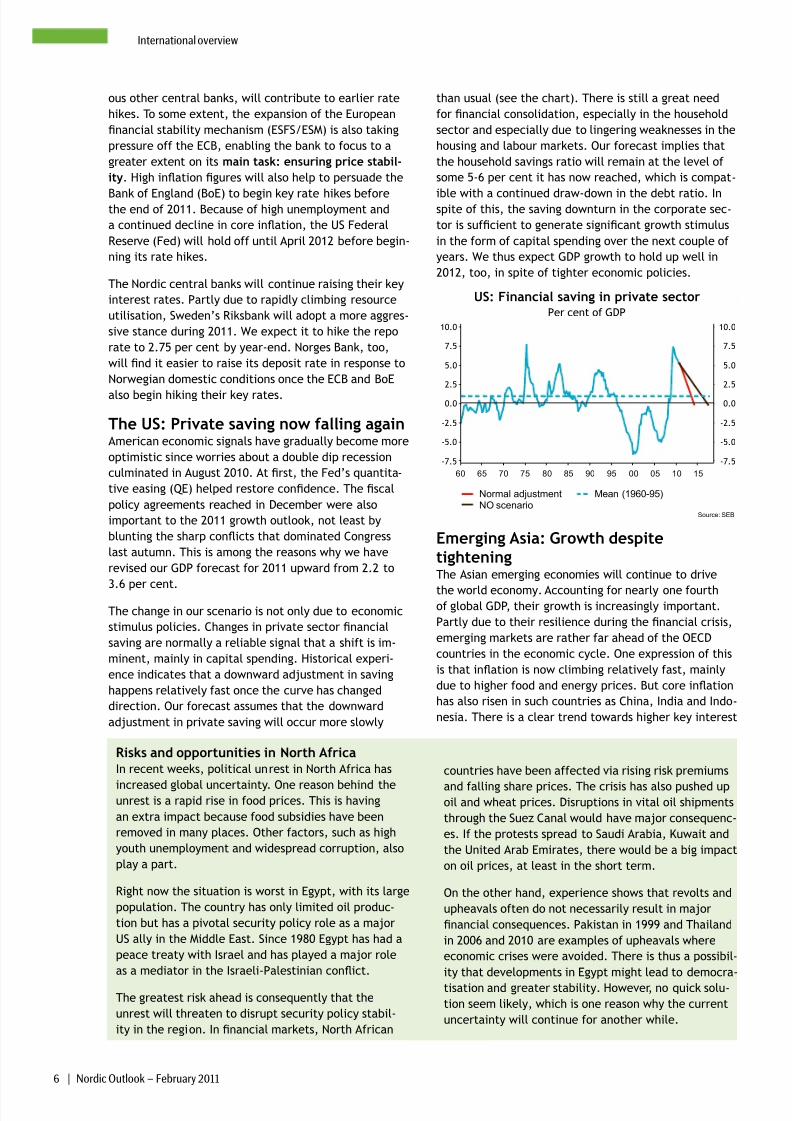

The US: Private saving now falling againAmerican economic signals have gradually become more

optimistic since worries about a double dip recession

culminated in August 2010. At rst, the Fed’s quantita-

tive easing (QE) helped restore condence. The scal

policy agreements reached in December were also

important to the 2011 growth outlook, not least by

blunting the sharp conicts that dominated Congress

last autumn. This is among the reasons why we have

revised our GDP forecast for 2011 upward from 2.2 to

3.6 per cent.

The change in our scenario is not only due to economic

stimulus policies. Changes in private sector nancial

saving are normally a reliable signal that a shift is im-

minent, mainly in capital spending. Historical experi-

ence indicates that a downward adjustment in saving

happens relatively fast once the curve has changed

direction. Our forecast assumes that the downward

adjustment in private saving will occur more slowly

than usual (see the chart). There is still a great need

for nancial consolidation, especially in the household

sector and especially due to lingering weaknesses in the

housing and labour markets. Our forecast implies that

the household savings ratio will remain at the level of

some 5-6 per cent it has now reached, which is compat-

ible with a continued draw-down in the debt ratio. Inspite of this, the saving downturn in the corporate sec-

tor is sufcient to generate signicant growth stimulus

in the form of capital spending over the next couple of

years. We thus expect GDP growth to hold up well in

2012, too, in spite of tighter economic policies.

Per cent of GDP

US: Financial saving in private sector

Normal adjustmentNO scenario

Mean (1960-95)

Source: SEB

60 65 70 75 80 85 90 95 00 05 10 15

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

Emerging Asia: Growth despitetighteningThe Asian emerging economies will continue to drive

the world economy. Accounting for nearly one fourthof global GDP, their growth is increasingly important.

Partly due to their resilience during the nancial crisis,

emerging markets are rather far ahead of the OECD

countries in the economic cycle. One expression of this

is that ination is now climbing relatively fast, mainly

due to higher food and energy prices. But core ination

has also risen in such countries as China, India and Indo-

nesia. There is a clear trend towards higher key interest

Risks and opportunities in North AfricaIn recent weeks, political unrest in North Africa has

increased global uncertainty. One reason behind theunrest is a rapid rise in food prices. This is having

an extra impact because food subsidies have been

removed in many places. Other factors, such as high

youth unemployment and widespread corruption, also

play a part.

Right now the situation is worst in Egypt, with its large

population. The country has only limited oil produc-

tion but has a pivotal security policy role as a major

US ally in the Middle East. Since 1980 Egypt has had a

peace treaty with Israel and has played a major role

as a mediator in the Israeli-Palestinian conict.

The greatest risk ahead is consequently that the

unrest will threaten to disrupt security policy stabil-

ity in the region. In nancial markets, North African

countries have been affected via rising risk premiums

and falling share prices. The crisis has also pushed upoil and wheat prices. Disruptions in vital oil shipments

through the Suez Canal would have major consequenc-

es. If the protests spread to Saudi Arabia, Kuwait and

the United Arab Emirates, there would be a big impact

on oil prices, at least in the short term.

On the other hand, experience shows that revolts and

upheavals often do not necessarily result in major

nancial consequences. Pakistan in 1999 and Thailand

in 2006 and 2010 are examples of upheavals where

economic crises were avoided. There is thus a possibil-

ity that developments in Egypt might lead to democra-

tisation and greater stability. However, no quick solu-tion seem likely, which is one reason why the current

uncertainty will continue for another while.

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 6/55

Nordic Outlook – February 2011 | 7

International overview

rates. In India, for example, the real key rate is well

into negative territory, while economic growth is nearly

9 per cent a year. Many Asian central banks seem more

and more uncomfortable with excessively accommoda-

tive monetary policies. We can thus expect continued

key interest rate hikes during 2011.

Real key rates in selected countriesPer cent

K ey rate Ination Real SEBkey rate forecast

GDP 2011 India 6.5 8.4 -1.9 8.5

Indonesia 6.5 7.0 -0.5 6.3

China 5.8 4.6 1.2 9.5

Euro zone 1.0 2.2 -1.2 1.9

Japan 0.1 0.0 0.1 1.6

United States 0.25 1.5 -1.2 3.6

Source: National statistical ofces, OECD, SEB

Because of their higher trend growth and earlier posi-

tion in the economic cycle, the differences between

nominal emerging market interest rates and those in

the OECD countries will increase this year. This may ex-

acerbate the problems connected to speculative capital

inows, including bubble tendencies in asset markets.

But to a greater extent than before, many countries

seem to accept currency appreciation as an element

of ination-ghting. One reason is that greater risks of

rising food prices might lead to social unrest.

We still foresee an Asian soft landing as the most likely

scenario. Tighter economic policies will decelerate

growth to more sustainable levels, which in the long

term are around 6 per cent. Ination will peak during

the rst half of 2011 and then decline.

Western Europe: Out of stepThe euro zone continues to be characterised by a two-

speed economy. The recovery in Germany is progress-

ing at a rapid pace. Optimism is at record-high levels,

according to the IFO sentiment index. Unemployment

has fallen to its lowest level since 1992. We expect

German GDP to climb by 3.1 per cent in 2011, a bit

less than last year’s 3.6 per cent. Meanwhile powerful

austerity programmes in southern Europe will hamper

growth in the euro zone as a whole. This year, GDP will

fall in Greece and Portugal and will be close to zero in

Spain and Ireland. In France and Italy, growth will end

up around 1½ per cent, both this year and next. Due to

structural decits in both countries, however they also

have a major need for scal austerity measures. Overall

euro zone growth will end up at 1.9 per cent this

year and 1.8 per cent in 2012, somewhat higher than

we believed in November.

During 2011, the British economy will be hampered by

scal tightening and by high ination that will under-

mine purchasing power. The weak British pound and

strong international demand will nevertheless prop up

economic growth. GDP will increase by 1.5 per cent

this year and 2.5 per cent in 2012.

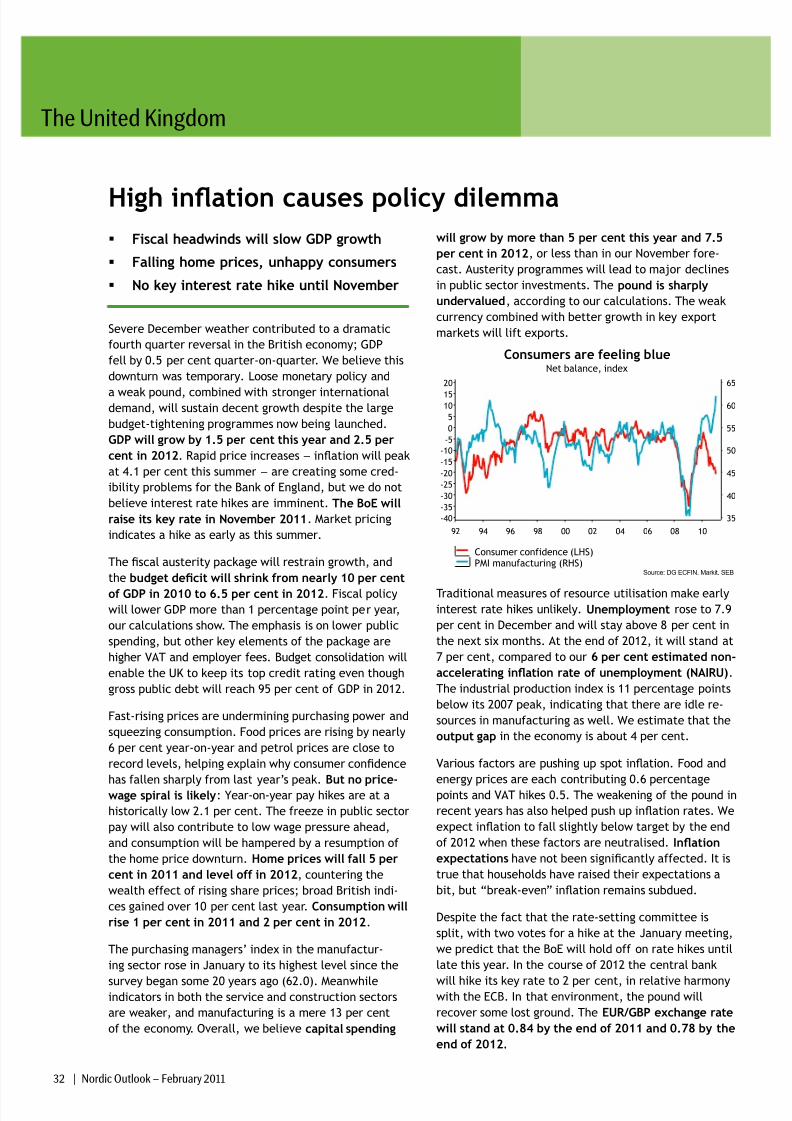

Consumer confidence, net balance

Diverging levels of optimism

United Kingdom GermanySource: DG ECFIN

90 92 94 96 98 00 02 04 06 08 10

-40

-35

-30

-25

-20

-15

-10

-5

0

510

15

-40

-35

-30

-25

-20

-15

-10

-5

0

510

15

Swedish growth in a class by itself The Nordic countries are continuing their strong growth.

These countries are beneting from export sectors that

are well positioned to meet rising global demand for

investment and intermediate goods. In additional, such

fundamental factors as public nances and current ac-

count balances are in very good shape.

GDP growth, Nordic and Baltic countries Year-on-year percentage change

2009 2010 2011 2012

Sweden -5.3 5.7 4.7 2.6

Norway -1.4 0.1 2.7 2.5

Denmark -4.7 2.3 2.6 2.3

Finland -8.1 2.7 3.5 3.0

Nordics -4.6 2.9 3.4 2.6

Estonia -13.9 2.7 4.5 4.0

Latvia -18.0 -0.3 4.0 5.0

Lithuania -14.7 1.0 4.0 4.5

Baltics -15.6 1.2 4.1 4.7

Source: OECD, SEB

The Swedish economy is now expanding very fast. We

have revised our GDP growth forecast upward to 4.5

per cent in 2011, after an increase of no less than 5.7

per cent in 2010. Other Nordic countries will show more

modest growth gures. Danish growth will be 2.6 per

cent in 2011 and 2.2 per cent in 2012, despite a degree

of scal tightening. In Finland, too, exports are the

main driving force. GDP growth will accelerate a bit,

reaching 3.5 per cent in 2011 and 3.0 per cent in 2012,

among other things due to improved competitiveness.

In Norway, supply-side restrictions are already starting

to hamper expansion; GDP growth will thus be only 2.7

per cent in 2011 and 2.5 per cent in 2012.

Rising resource utilisation in both Sweden and Norway

has led to early key rate hikes and sharply appreciating

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 7/55

8 | Nordic Outlook – February 2011

International overview

“United Debt of Europe”Monetary cooperation in Europe is moving into a new

phase. The temporary European Financial Stability

Facility (EFSF), which will be replaced in 2013 by

the permanent European Stability Mechanism (ESM),

serves as a supranational lender of last resort. It willplay a key role in dealing with the short- and medium-

term liquidity and renancing needs of problem coun-

tries. Also of central importance is that the EFSF/ESM

is re-establishing a clear delineation between euro

zone sovereign debt policy and monetary policy.

At their summit in late March, the European Union

heads of state and government are expected to decide

what powers the EFSF/ESM will have. We foresee the

following decisions:

1) The lending amount guaranteed by the euro zone

countries will more than double from today’s EUR 440 billion to EUR 1 trillion. That will reduce the EU’s

dependence on the advice of the International Mon-

etary Fund (IMF), but even so the IMF is still expected

to play an important role for economic policy advice.

2) The EFSF/ESM will be allowed to buy government

bonds in the secondary market. This will take over the

role the ECB has been forced to assume to stabilise

the situation. The EFSF/ESM is also expected to buy

up the approximately EUR 80 billion in government

securities now in the ECB’s balance sheet.

3) The EFSF/ESM will become a tool for long-termdebt consolidation in crisis-hit countries with solven-

cy problems; EFSF/ESM loans can be used to enable

crisis countries to repurchase outstanding bonds that

are trading today at prices sharply below face value.

EU scal policy coordination will also intensify this

year as a result of the “European semester”, a recur-

ring process in which the scal positions and policies

of EU countries will be reviewed before their national

budget process is completed. In June, the EU summit

is also expected to approve tougher standards and

sanctions for the now-toothless Stability and Growth

Pact.

This signies that euro zone government debt and

scal policies will be taking a major step towards

greater coordination. The new system represents

something of a break with the principle that previous-

ly dominated the work of the EU: that each country

should be able to pursue government debt policies

that do not adversely impact other countries (in termsof interest rate effects/credibility). However, this

seems to be the price that must be paid to ensure

the survival of the euro. It is also consistent with the

fundamental concept that the euro zone should serve

as one step in the evolution of a political union.

Increased oversight and demands on scal policy − and

clearer distinctions between different policy areas −

will have an impact on monetary policy. Government

debt problems will be referred to national govern-

ments. Since the ECB will no longer be buying govern-

ment bonds, this will increase the pressure to pursue

responsible scal policies.

The ECB can thus increasingly focus on its main

task, ensuring price stability, which will strengthen

its credibility. Our assessment is that on the margin,

this opens the door to an earlier ECB interest rate

hike. Looking ahead, conrming the ECB’s independ-

ence may also diminish the risk of rising ination ex-

pectations and long-term yields. Such a development

would be especially benecial to such debt-burdened

countries as Greece, Ireland, Portugal and Spain.

But even if the EFSF/ESM gains an enlarged mandate

and stronger nancial muscle, the underlying problemsare fundamentally national. An economy’s competi-

tiveness and scal credibility must be regained by

means of a sustainable structural policy and stable

policy frameworks. Before this is ensured, the risks of

nancial volatility will persist.

During the spring, we expect that both Greece and

Ireland will be offered “soft” debt renegotiations

in the form of lower interest rates on borrowing and

extended loan maturities. Meanwhile these countries

can implement a write-down of debts by repurchasing

some of their outstanding debt. We also believe that

Portugal and Spain will show an interest in borrow-

ing money from EFSF/ESM. These countries must be

taken care of in resolute fashion, to avoid a resur-

gence of mistrust.

currencies. This will slow export growth over the next

couple of years, although our calculations indicate that

their currencies are still undervalued against the euro.

On the other hand, competitiveness in Finland and Den-

mark will benet from the appreciation of the SEK and

NOK from their previously extremely low levels.

Gradual recovery in the BalticsThe three Baltic countries rebounded weakly last year

after their depression-like downturn in 2008-2009. In

2011 and 2012 we expect GDP growth of 4-5 per cent,

which is still above consensus. We have revised our

forecast for Estonia upward by half a percentage point

to 4.5 per cent both in 2011 as well as 2012. This

implies that Estonia will have the fastest growth in the

Baltics during both years. With its relatively high ex-

ports as a percentage of GDP, the Estonian economy is

best positioned to benet from good external demand,

especially from Sweden and Finland.

Growth will continue to be driven by strong, com-

petitive exports. Domestic demand will recover

slowly. Households and businesses are still feeling the

after-effects of internal devaluation and tough public

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 8/55

Nordic Outlook – February 2011 | 9

International overview

budget consolidation; in Latvia, budget austerity meas-

ures will continue. Unemployment will fall slowly, and

at the end of 2012 it will remain far higher than before

the crisis. Ination is being pushed up by international

energy and food price increases. Underlying price pres-

sures remain low but will climb gradually.

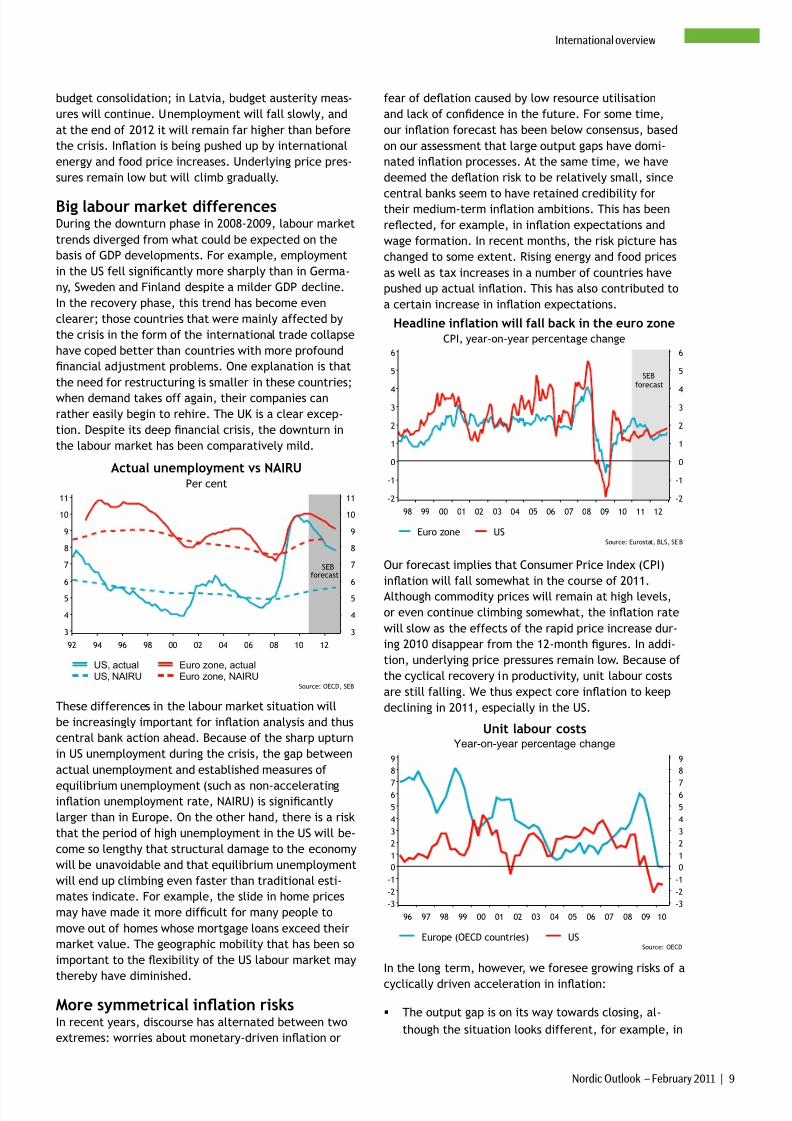

Big labour market differencesDuring the downturn phase in 2008-2009, labour market

trends diverged from what could be expected on the

basis of GDP developments. For example, employment

in the US fell signicantly more sharply than in Germa-

ny, Sweden and Finland despite a milder GDP decline.

In the recovery phase, this trend has become even

clearer; those countries that were mainly affected by

the crisis in the form of the international trade collapse

have coped better than countries with more profound

nancial adjustment problems. One explanation is that

the need for restructuring is smaller in these countries;

when demand takes off again, their companies can

rather easily begin to rehire. The UK is a clear excep-

tion. Despite its deep nancial crisis, the downturn in

the labour market has been comparatively mild.

Per cent

Actual unemployment vs NAIRU

US, actualUS, NAIRU

Euro zone, actualEuro zone, NAIRU

Source: OECD, SEB

92 94 96 98 00 02 04 06 08 10 12

3

4

5

6

7

8

9

10

11

3

4

5

6

7

8

9

10

11

forecastSEB

These differences in the labour market situation will

be increasingly important for ination analysis and thus

central bank action ahead. Because of the sharp upturn

in US unemployment during the crisis, the gap between

actual unemployment and established measures of

equilibrium unemployment (such as non-acceleratingination unemployment rate, NAIRU) is signicantly

larger than in Europe. On the other hand, there is a risk

that the period of high unemployment in the US will be-

come so lengthy that structural damage to the economy

will be unavoidable and that equilibrium unemployment

will end up climbing even faster than traditional esti-

mates indicate. For example, the slide in home prices

may have made it more difcult for many people to

move out of homes whose mortgage loans exceed their

market value. The geographic mobility that has been so

important to the exibility of the US labour market may

thereby have diminished.

More symmetrical ination risksIn recent years, discourse has alternated between two

extremes: worries about monetary-driven ination or

fear of deation caused by low resource utilisation

and lack of condence in the future. For some time,

our ination forecast has been below consensus, based

on our assessment that large output gaps have domi-

nated ination processes. At the same time, we have

deemed the deation risk to be relatively small, since

central banks seem to have retained credibility fortheir medium-term ination ambitions. This has been

reected, for example, in ination expectations and

wage formation. In recent months, the risk picture has

changed to some extent. Rising energy and food prices

as well as tax increases in a number of countries have

pushed up actual ination. This has also contributed to

a certain increase in ination expectations.

CPI, year-on-year percentage change

Headline inflation will fall back in the euro zone

Euro zone USSource: Eurostat, BLS, SEB

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

-2

-1

0

1

2

34

5

6

-2

-1

0

1

2

34

5

6

forecastSEB

Our forecast implies that Consumer Price Index (CPI)

ination will fall somewhat in the course of 2011.

Although commodity prices will remain at high levels,

or even continue climbing somewhat, the ination rate

will slow as the effects of the rapid price increase dur-

ing 2010 disappear from the 12-month gures. In addi-

tion, underlying price pressures remain low. Because of

the cyclical recovery in productivity, unit labour costs

are still falling. We thus expect core ination to keep

declining in 2011, especially in the US.

Year-on-year percentage change

Unit labour costs

Europe (OECD countries) USSource: OECD

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

-3

-2

-1

0

1

2

3

4

5

67

8

9

-3

-2

-1

0

1

2

3

4

5

67

8

9

In the long term, however, we foresee growing risks of a

cyclically driven acceleration in ination:

The output gap is on its way towards closing, al-

though the situation looks different, for example, in

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 9/55

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 10/55

Nordic Outlook – February 2011 | 11

International overview

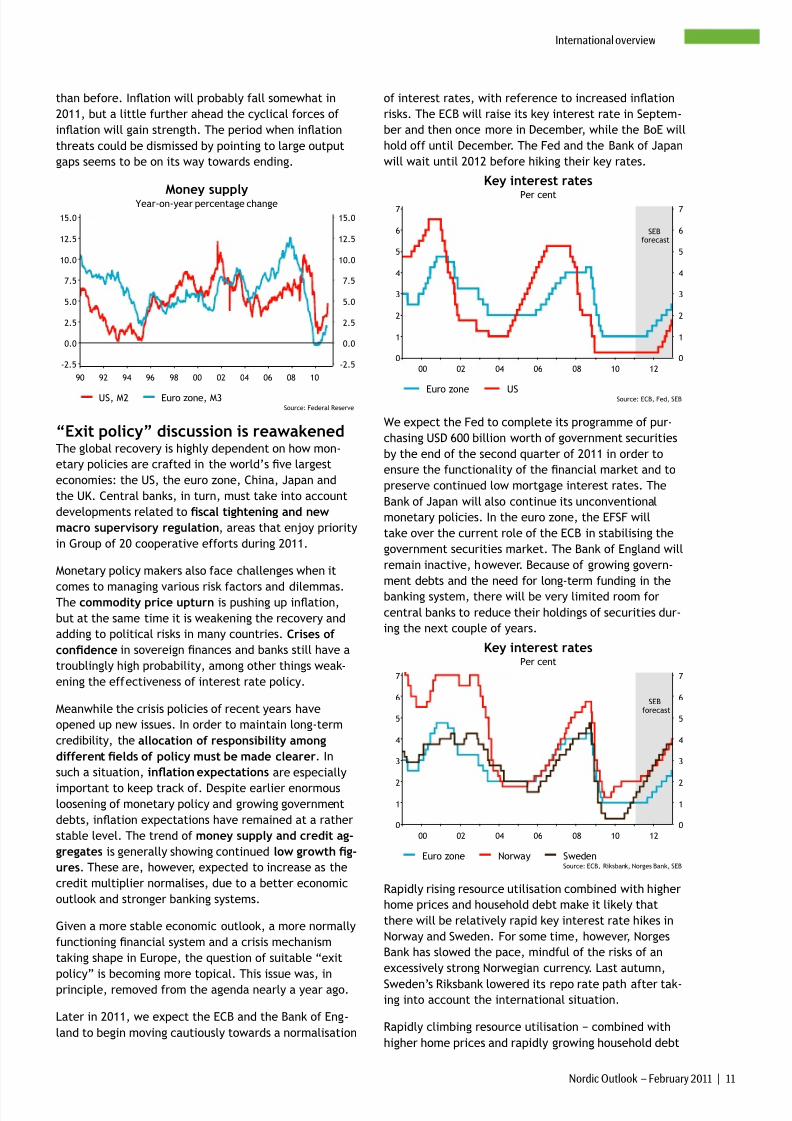

than before. Ination will probably fall somewhat in

2011, but a little further ahead the cyclical forces of

ination will gain strength. The period when ination

threats could be dismissed by pointing to large output

gaps seems to be on its way towards ending.

Year-on-year percentage changeMoney supply

US, M2 Euro zone, M3Source: Federal Reserve

90 92 94 96 98 00 02 04 06 08 10

-2.5

0.0

2.5

5.0

7.5

10.0

12.5

15.0

-2.5

0.0

2.5

5.0

7.5

10.0

12.5

15.0

“Exit policy” discussion is reawakenedThe global recovery is highly dependent on how mon-

etary policies are crafted in the world’s ve largest

economies: the US, the euro zone, China, Japan and

the UK. Central banks, in turn, must take into account

developments related to scal tightening and new

macro supervisory regulation, areas that enjoy priority

in Group of 20 cooperative efforts during 2011.

Monetary policy makers also face challenges when it

comes to managing various risk factors and dilemmas.The commodity price upturn is pushing up ination,

but at the same time it is weakening the recovery and

adding to political risks in many countries. Crises of

condence in sovereign nances and banks still have a

troublingly high probability, among other things weak-

ening the effectiveness of interest rate policy.

Meanwhile the crisis policies of recent years have

opened up new issues. In order to maintain long-term

credibility, the allocation of responsibility among

different elds of policy must be made clearer. In

such a situation, ination expectations are especially

important to keep track of. Despite earlier enormousloosening of monetary policy and growing government

debts, ination expectations have remained at a rather

stable level. The trend of money supply and credit ag-

gregates is generally showing continued low growth g-

ures. These are, however, expected to increase as the

credit multiplier normalises, due to a better economic

outlook and stronger banking systems.

Given a more stable economic outlook, a more normally

functioning nancial system and a crisis mechanism

taking shape in Europe, the question of suitable “exit

policy” is becoming more topical. This issue was, in

principle, removed from the agenda nearly a year ago.

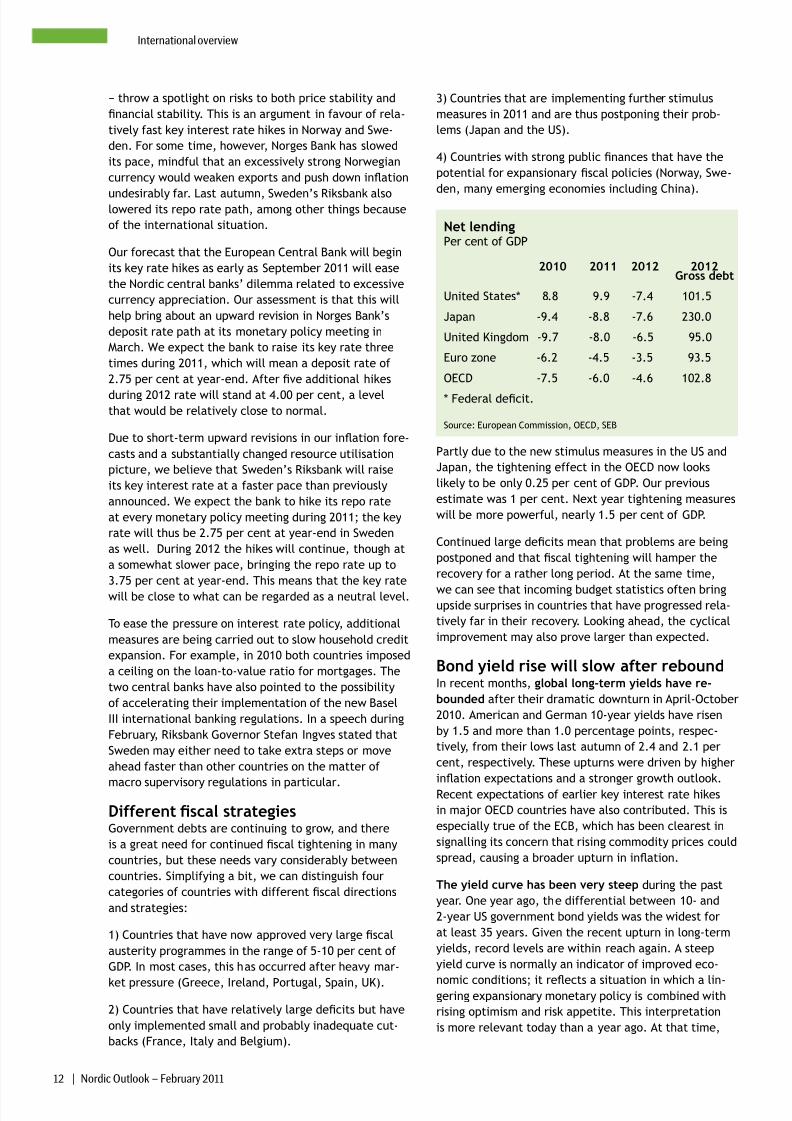

Later in 2011, we expect the ECB and the Bank of Eng-

land to begin moving cautiously towards a normalisation

of interest rates, with reference to increased ination

risks. The ECB will raise its key interest rate in Septem-

ber and then once more in December, while the BoE will

hold off until December. The Fed and the Bank of Japan

will wait until 2012 before hiking their key rates.

Per cent

Key interest rates

Euro zone US Source: ECB, Fed, SEB

00 02 04 06 08 10 120

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7

forecastSEB

We expect the Fed to complete its programme of pur-

chasing USD 600 billion worth of government securities

by the end of the second quarter of 2011 in order to

ensure the functionality of the nancial market and to

preserve continued low mortgage interest rates. The

Bank of Japan will also continue its unconventional

monetary policies. In the euro zone, the EFSF will

take over the current role of the ECB in stabilising the

government securities market. The Bank of England will

remain inactive, however. Because of growing govern-

ment debts and the need for long-term funding in the

banking system, there will be very limited room for

central banks to reduce their holdings of securities dur-

ing the next couple of years.

Per cent

Key interest rates

Euro zone Norway SwedenSource: ECB, Riksbank, Norges Bank, SEB

00 02 04 06 08 10 120

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7

forecastSEB

Rapidly rising resource utilisation combined with higher

home prices and household debt make it likely that

there will be relatively rapid key interest rate hikes in

Norway and Sweden. For some time, however, Norges

Bank has slowed the pace, mindful of the risks of an

excessively strong Norwegian currency. Last autumn,

Sweden’s Riksbank lowered its repo rate path after tak-ing into account the international situation.

Rapidly climbing resource utilisation − combined with

higher home prices and rapidly growing household debt

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 11/55

12 | Nordic Outlook – February 2011

International overview

− throw a spotlight on risks to both price stability and

nancial stability. This is an argument in favour of rela-

tively fast key interest rate hikes in Norway and Swe-

den. For some time, however, Norges Bank has slowed

its pace, mindful that an excessively strong Norwegian

currency would weaken exports and push down ination

undesirably far. Last autumn, Sweden’s Riksbank alsolowered its repo rate path, among other things because

of the international situation.

Our forecast that the European Central Bank will begin

its key rate hikes as early as September 2011 will ease

the Nordic central banks’ dilemma related to excessive

currency appreciation. Our assessment is that this will

help bring about an upward revision in Norges Bank’s

deposit rate path at its monetary policy meeting in

March. We expect the bank to raise its key rate three

times during 2011, which will mean a deposit rate of

2.75 per cent at year-end. After ve additional hikes

during 2012 rate will stand at 4.00 per cent, a levelthat would be relatively close to normal.

Due to short-term upward revisions in our ination fore-

casts and a substantially changed resource utilisation

picture, we believe that Sweden’s Riksbank will raise

its key interest rate at a faster pace than previously

announced. We expect the bank to hike its repo rate

at every monetary policy meeting during 2011; the key

rate will thus be 2.75 per cent at year-end in Sweden

as well. During 2012 the hikes will continue, though at

a somewhat slower pace, bringing the repo rate up to

3.75 per cent at year-end. This means that the key rate

will be close to what can be regarded as a neutral level.

To ease the pressure on interest rate policy, additional

measures are being carried out to slow household credit

expansion. For example, in 2010 both countries imposed

a ceiling on the loan-to-value ratio for mortgages. The

two central banks have also pointed to the possibility

of accelerating their implementation of the new Basel

III international banking regulations. In a speech during

February, Riksbank Governor Stefan Ingves stated that

Sweden may either need to take extra steps or move

ahead faster than other countries on the matter of

macro supervisory regulations in particular.

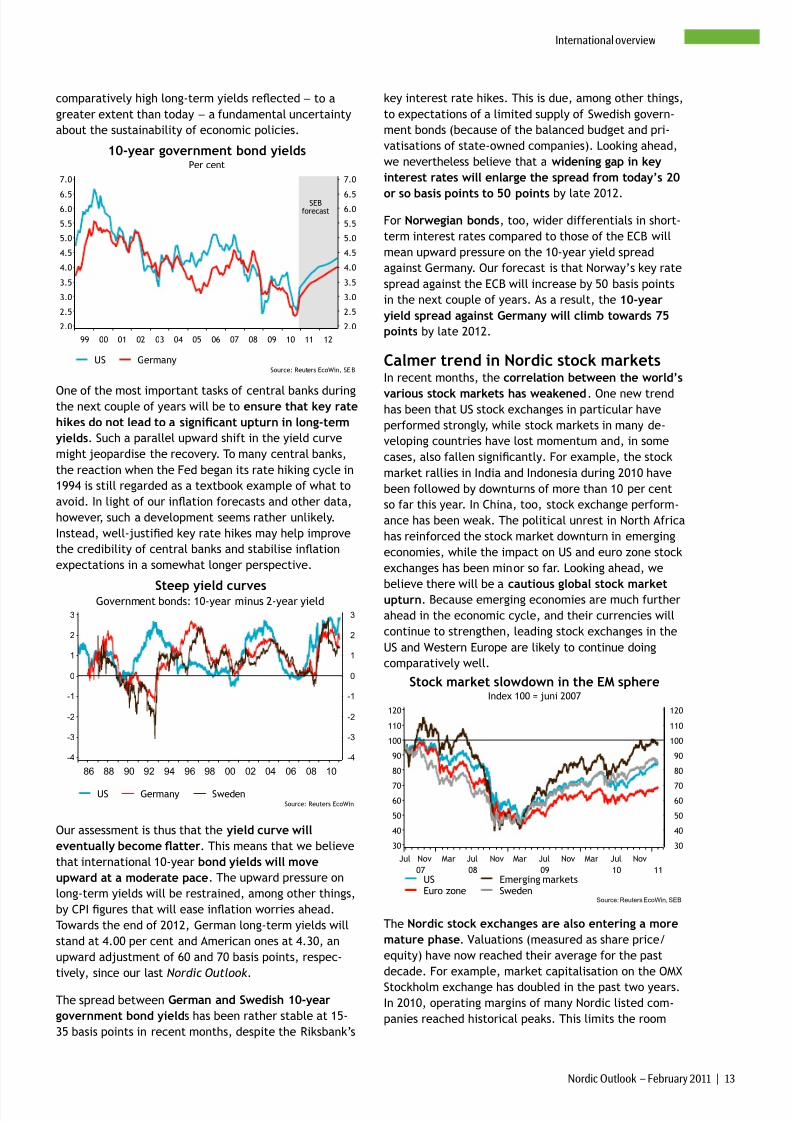

Different scal strategiesGovernment debts are continuing to grow, and there

is a great need for continued scal tightening in many

countries, but these needs vary considerably between

countries. Simplifying a bit, we can distinguish four

categories of countries with different scal directions

and strategies:

1) Countries that have now approved very large scal

austerity programmes in the range of 5-10 per cent of

GDP. In most cases, this has occurred after heavy mar-

ket pressure (Greece, Ireland, Portugal, Spain, UK).

2) Countries that have relatively large decits but have

only implemented small and probably inadequate cut-

backs (France, Italy and Belgium).

3) Countries that are implementing further stimulus

measures in 2011 and are thus postponing their prob-

lems (Japan and the US).

4) Countries with strong public nances that have the

potential for expansionary scal policies (Norway, Swe-

den, many emerging economies including China).

Net lendingPer cent of GDP

2010 2011 2012 2012Gross debt

United States* 8.8 9.9 -7.4 101.5

Japan -9.4 -8.8 -7.6 230.0

United Kingdom -9.7 -8.0 -6.5 95.0

Euro zone -6.2 -4.5 -3.5 93.5

OECD -7.5 -6.0 -4.6 102.8

* Federal decit.

Source: European Commission, OECD, SEB

Partly due to the new stimulus measures in the US and

Japan, the tightening effect in the OECD now looks

likely to be only 0.25 per cent of GDP. Our previous

estimate was 1 per cent. Next year tightening measures

will be more powerful, nearly 1.5 per cent of GDP.

Continued large decits mean that problems are being

postponed and that scal tightening will hamper the

recovery for a rather long period. At the same time,

we can see that incoming budget statistics often bringupside surprises in countries that have progressed rela-

tively far in their recovery. Looking ahead, the cyclical

improvement may also prove larger than expected.

Bond yield rise will slow after reboundIn recent months, global long-term yields have re-

bounded after their dramatic downturn in April-October

2010. American and German 10-year yields have risen

by 1.5 and more than 1.0 percentage points, respec-

tively, from their lows last autumn of 2.4 and 2.1 per

cent, respectively. These upturns were driven by higher

ination expectations and a stronger growth outlook.

Recent expectations of earlier key interest rate hikes

in major OECD countries have also contributed. This is

especially true of the ECB, which has been clearest in

signalling its concern that rising commodity prices could

spread, causing a broader upturn in ination.

The yield curve has been very steep during the past

year. One year ago, the differential between 10- and

2-year US government bond yields was the widest for

at least 35 years. Given the recent upturn in long-term

yields, record levels are within reach again. A steep

yield curve is normally an indicator of improved eco-

nomic conditions; it reects a situation in which a lin-gering expansionary monetary policy is combined with

rising optimism and risk appetite. This interpretation

is more relevant today than a year ago. At that time,

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 12/55

Nordic Outlook – February 2011 | 13

International overview

comparatively high long-term yields reected − to a

greater extent than today − a fundamental uncertainty

about the sustainability of economic policies.

Per cent

10-year government bond yields

US GermanySource: Reuters EcoWin, SEB

99 00 01 02 03 04 05 06 07 08 09 10 11 12

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.06.5

7.0

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.06.5

7.0

SEBforecast

One of the most important tasks of central banks duringthe next couple of years will be to ensure that key rate

hikes do not lead to a signicant upturn in long-term

yields. Such a parallel upward shift in the yield curve

might jeopardise the recovery. To many central banks,

the reaction when the Fed began its rate hiking cycle in

1994 is still regarded as a textbook example of what to

avoid. In light of our ination forecasts and other data,

however, such a development seems rather unlikely.

Instead, well-justied key rate hikes may help improve

the credibility of central banks and stabilise ination

expectations in a somewhat longer perspective.

Government bonds: 10-year minus 2-year yieldSteep yield curves

US Germany SwedenSource: Reuters EcoWin

86 88 90 92 94 96 98 00 02 04 06 08 10

-4

-3

-2

-1

0

1

2

3

-4

-3

-2

-1

0

1

2

3

Our assessment is thus that the yield curve will

eventually become atter. This means that we believe

that international 10-year bond yields will move

upward at a moderate pace. The upward pressure on

long-term yields will be restrained, among other things,

by CPI gures that will ease ination worries ahead.

Towards the end of 2012, German long-term yields will

stand at 4.00 per cent and American ones at 4.30, an

upward adjustment of 60 and 70 basis points, respec-

tively, since our last Nordic Outlook.

The spread between German and Swedish 10-year

government bond yields has been rather stable at 15-

35 basis points in recent months, despite the Riksbank’s

key interest rate hikes. This is due, among other things,

to expectations of a limited supply of Swedish govern-

ment bonds (because of the balanced budget and pri-

vatisations of state-owned companies). Looking ahead,

we nevertheless believe that a widening gap in key

interest rates will enlarge the spread from today’s 20

or so basis points to 50 points by late 2012.

For Norwegian bonds, too, wider differentials in short-

term interest rates compared to those of the ECB will

mean upward pressure on the 10-year yield spread

against Germany. Our forecast is that Norway’s key rate

spread against the ECB will increase by 50 basis points

in the next couple of years. As a result, the 10-year

yield spread against Germany will climb towards 75

points by late 2012.

Calmer trend in Nordic stock marketsIn recent months, the correlation between the world’s

various stock markets has weakened. One new trendhas been that US stock exchanges in particular have

performed strongly, while stock markets in many de-

veloping countries have lost momentum and, in some

cases, also fallen signicantly. For example, the stock

market rallies in India and Indonesia during 2010 have

been followed by downturns of more than 10 per cent

so far this year. In China, too, stock exchange perform-

ance has been weak. The political unrest in North Africa

has reinforced the stock market downturn in emerging

economies, while the impact on US and euro zone stock

exchanges has been minor so far. Looking ahead, we

believe there will be a cautious global stock marketupturn. Because emerging economies are much further

ahead in the economic cycle, and their currencies will

continue to strengthen, leading stock exchanges in the

US and Western Europe are likely to continue doing

comparatively well.

Index 100 = juni 2007

Stock market slowdown in the EM sphere

USEuro zone

Emerging marketsSweden

Source: Reuters EcoWin, SEB

Jul

07

Nov

08

Mar Jul Nov

09

Mar Jul Nov

10

Mar Jul Nov

11

30

40

50

6070

80

90

100

110

120

30

40

50

6070

80

90

100

110

120

The Nordic stock exchanges are also entering a more

mature phase. Valuations (measured as share price/

equity) have now reached their average for the past

decade. For example, market capitalisation on the OMX

Stockholm exchange has doubled in the past two years.

In 2010, operating margins of many Nordic listed com-

panies reached historical peaks. This limits the room

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 13/55

14 | Nordic Outlook – February 2011

International overview

for new positive surprises. For Swedish companies, and

to some extent also Norwegian ones, the strength of

the currency is also starting to become a greater chal-

lenge. This will make it harder for the OMX Stockholm

to continue outperforming exchanges in other countries

during the next couple of years.

Several factors nevertheless point towards a fairly

strong Nordic stock market trend this year. Because

of low debt, corporate transactions will increase after

several years of modest merger and acquisition volume.

Dividends will also be raised. The relationship between

interest rates and the yields on equities will also allow

room for rising share prices. We estimate that total

yield on Nordic stock exchanges will be 3.6 per cent,

which is higher than today’s yields on 10-year govern-

ment bonds in all Nordic countries but Iceland.

Continued Nordic currency appreciation

Differences in macroeconomic fundamentals, includ-ing economic growth and government nances, will

remain key driving forces in the foreign exchange mar-

ket. Short-term interest rate spreads will also grow in

importance, as the volatility of the FX market subsides.

An increasingly vigorous world economy will continue to

push up the currencies of emerging market countries. In

many cases, rising commodity prices will help improve

terms-of-trade, making more room for continued ap-

preciation. This also applies to such OECD currencies as

the AUD, CAD and NOK.

Cyclically sensitive currencies will thus appreciate,

though earlier weakening trends have been reversed in

many cases. Central banks in many emerging economies

have intervened forcefully to slow the appreciation of

their currencies. However, we believe that many coun-

tries will, to a greater extent, accept future strength-

ening of their currencies as a means of keeping ination

down. This is one way of taking the edge off rising food

prices and the related risks of social unrest.

China’s currency policy remains cautious. Since late

June 2010, when appreciation against the US dollar was

resumed, the yuan has gained about 3.5 per cent. Real

effective appreciation totalled about 5 per cent during2010. We believe that the pace of appreciation against

the USD will increase somewhat during 2011 in order

to counter ination and contribute to more balanced

economic growth. Our assessment is that the USD/CNY

exchange rate will be 6.30 at the end of 2011.

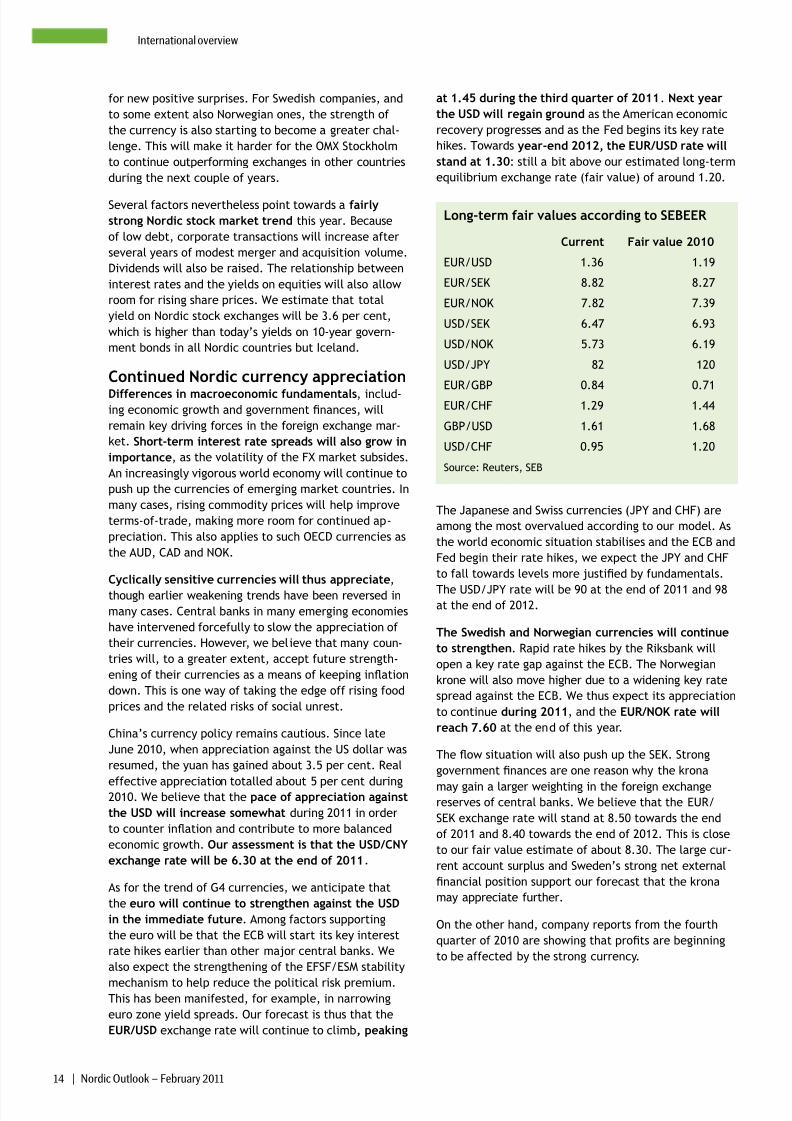

As for the trend of G4 currencies, we anticipate that

the euro will continue to strengthen against the USD

in the immediate future. Among factors supporting

the euro will be that the ECB will start its key interest

rate hikes earlier than other major central banks. We

also expect the strengthening of the EFSF/ESM stability

mechanism to help reduce the political risk premium.This has been manifested, for example, in narrowing

euro zone yield spreads. Our forecast is thus that the

EUR/USD exchange rate will continue to climb, peaking

at 1.45 during the third quarter of 2011. Next year

the USD will regain ground as the American economic

recovery progresses and as the Fed begins its key rate

hikes. Towards year-end 2012, the EUR/USD rate will

stand at 1.30: still a bit above our estimated long-term

equilibrium exchange rate (fair value) of around 1.20.

Long-term fair values according to SEBEER

Current Fair value 2010

EUR/USD 1.36 1.19

EUR/SEK 8.82 8.27

EUR/NOK 7.82 7.39

USD/SEK 6.47 6.93

USD/NOK 5.73 6.19

USD/JPY 82 120

EUR/GBP 0.84 0.71

EUR/CHF 1.29 1.44

GBP/USD 1.61 1.68

USD/CHF 0.95 1.20

Source: Reuters, SEB

The Japanese and Swiss currencies (JPY and CHF) are

among the most overvalued according to our model. As

the world economic situation stabilises and the ECB and

Fed begin their rate hikes, we expect the JPY and CHF

to fall towards levels more justied by fundamentals.

The USD/JPY rate will be 90 at the end of 2011 and 98at the end of 2012.

The Swedish and Norwegian currencies will continue

to strengthen. Rapid rate hikes by the Riksbank will

open a key rate gap against the ECB. The Norwegian

krone will also move higher due to a widening key rate

spread against the ECB. We thus expect its appreciation

to continue during 2011, and the EUR/NOK rate will

reach 7.60 at the end of this year.

The ow situation will also push up the SEK. Strong

government nances are one reason why the krona

may gain a larger weighting in the foreign exchangereserves of central banks. We believe that the EUR/

SEK exchange rate will stand at 8.50 towards the end

of 2011 and 8.40 towards the end of 2012. This is close

to our fair value estimate of about 8.30. The large cur-

rent account surplus and Sweden’s strong net external

nancial position support our forecast that the krona

may appreciate further.

On the other hand, company reports from the fourth

quarter of 2010 are showing that prots are beginning

to be affected by the strong currency.

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 14/55

Theme

Nordic Outlook – February 2011 | 15

SEBEER: A model for long-term equilibriumexchange rates

EUR/USD equilibrium at 1.20

JPY and CHF the most overvalued

NOK and SEK undervalued against theeuro

The economic literature includes many approaches to

calculating equilibrium exchange rates (fair values).Purchasing Power Parity (PPP) emphasises the associa-

tion between relative price levels in different countries

and exchange rate. Other methods focus on internal

and external balance conditions − with the situation

related to resource utilisation and ination rate, on the

one hand, and current account balance and net exter-

nal nancial position, on the other, providing the basis

for estimating equilibrium exchange rates.

In addition to these more fundamental, theoretical

approaches, there are more empirical methods based

on actual historical exchange rate trends. SEB Research

recently estimated such equilibrium rates (BehaviouralEquilibrium Exchange Rate, BEER). The variables that

proved to have the largest impact on fair values in the

model that we have named SEBEER are the following:

Relative prices: Long-term fair value is affected by

relative price levels between countries, in keeping with

the above-mentioned PPP theory. A low domestic price

level relative to other countries indicates that the cur-

rency is undervalued.

Terms-of-trade: Differences in world market price

trends between a country’s exports and imports inu-

ence fair value. A favourable trend with faster-rising

export prices strengthens a country’s fair value.

Relative productivity: Differences in productivity

growth inuence fair value. A country with higher pro-

ductivity growth than its peers can maintain a gradually

appreciating currency without seeing its competitive-

ness undermined.

Current account: In the long term, the current account

balance affects the exchange rate. A surplus leads to

greater demand for the currency, thereby strengthening

its exchange rate.

Interest-rate differentials: Differences in interest rates

generate capital ows, which inuence the exchange

rate. A country with higher interest rates receives an

inow of capital that helps strengthen its exchange rate

in the short and medium term.

The usual way of estimating fair values is to use tradi-

tional time series analysis on individual currencies. One

way of carrying the analysis further is to estimate fair

values for a panel of exchange rates simultaneously.

The number of observations − and the precision of

the estimates−

is larger, without having to extend theestimate period as far back in time. The panel approach

also makes it possible to estimate several fair values

simultaneously, so the approach is internally consistent.

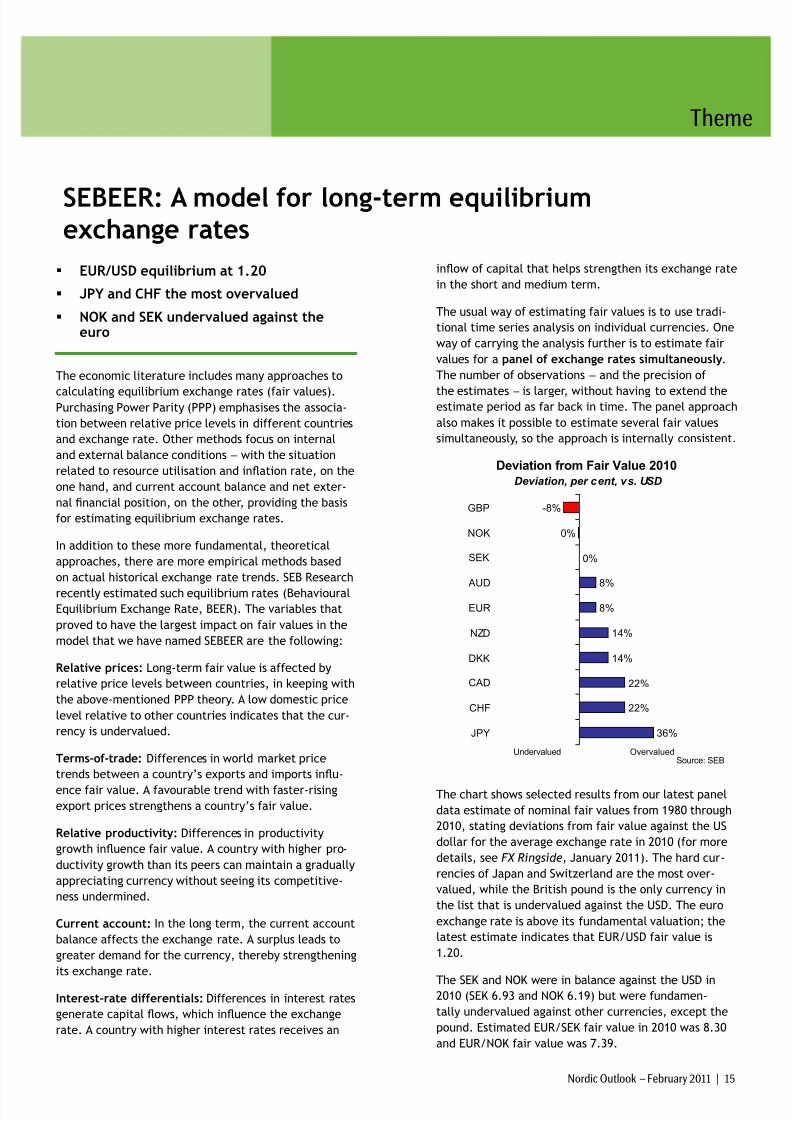

Deviation from Fair Value 2010

Deviation, per cent, vs. USD

36%

22%

22%

14%

14%

8%

8%

0%

0%

-8%

JPY

CHF

CAD

DKK

NZD

EUR

AUD

SEK

NOK

GBP

OvervaluedUndervaluedSource: SEB

The chart shows selected results from our latest panel

data estimate of nominal fair values from 1980 through

2010, stating deviations from fair value against the US

dollar for the average exchange rate in 2010 (for more

details, see FX Ringside, January 2011). The hard cur-

rencies of Japan and Switzerland are the most over-

valued, while the British pound is the only currency in

the list that is undervalued against the USD. The euro

exchange rate is above its fundamental valuation; the

latest estimate indicates that EUR/USD fair value is

1.20.

The SEK and NOK were in balance against the USD in2010 (SEK 6.93 and NOK 6.19) but were fundamen-

tally undervalued against other currencies, except the

pound. Estimated EUR/SEK fair value in 2010 was 8.30

and EUR/NOK fair value was 7.39.

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 15/55

The United States

16 | Nordic Outlook – February 2011

The US economy gears up above trend

The labour market is improving

Corporate prots will continue upward

The housing market is stumbling

The Fed will hike its key rate in April 2012

The US economic outlook has improved. A combination

of the Federal Reserve’s ultra-loose monetary policy

and a new scal stimulus has bolstered optimism. GDPgrowth in the fourth quarter of 2010 was signicantly

stronger than we expected in the last Nordic Outlook,

and there are many indications of continued good

growth gures early in 2011. Private sector nancial

saving has now started falling, which is usually an

important signal that a recovery is becoming self-

sustaining. Measured as annual averages, we foresee

GDP growth of 3.6 per cent this year and 4.0 per cent

in 2012, which is above consensus and a sharp upward

revision for 2011. Housing market reversals and poor

state government nances will nevertheless keep the

recovery a few percentage points weaker than histori-cal averages during the corresponding cyclical phase.

Employment will increase by an average of about

180,000 per month this year, despite public sector

cutbacks. Unemployment will fall but will remain at

a high 7.8 per cent at the end of our forecast period.

Large output and labour market gaps will lead to low

core ination; our ination forecasts are below consen-

sus. We thus anticipate that the Fed will hike its key

interest rate in April 2012, later than market pricing

indicates.

Index, year-on-year percentage changeComposite ISM and GDP growth

ISM Composite index (LHS) Real GDP (RHS)Source: ISM, SEB

02 03 04 05 06 07 08 09 10 11 12

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

35,0

37,5

40,0

42,5

45,0

47,5

50,0

52,5

55,0

57,5

60,0

62,5

SEBforecast

Continued strong company prot growthCapacity utilisation has risen at a brisk pace since it

bottomed out a year and a half ago, but remains at low

levels. Capital spending by businesses is now increas-

ing 10 per cent year-on-year but is still at a histori-

cally very low level as a percentage of GDP. Meanwhile

current market values relative to the replacement

costs are giving companies good incentives for invest-

ments. (Tobin’s Q has continued to climb). Add strong

corporate balance sheets and great optimism, bothin manufacturing and service sectors. Our composite

ISM purchasing managers’ index is compatible with

5 per cent GDP growth. The manufacturing ISM index

currently is close to 25-year highs. In a shorter perspec-

tive, however, weaker order bookings for capital goods

in recent months are evidence against an acceleration

in capital spending activity.

Good protability is also helping to stimulate capital

spending activity. Corporate after-tax prots are at 5.6

per cent of GDP, slightly above the historical average

but far below previous peaks. A combination of ris-

ing labour costs and higher taxes will eventually push

down prots. But 2011 will probably be another year of

double-digit prot growth. The gap between ination

and labour costs has historically been a good indicator

of which way prots are headed. This indicator points

towards an increase in prots 2-3 times higher than

GDP growth in current prices during 2011. Prots as a

percentage of GDP will continue upward.

Difference, year-on-year percentage change

Strong profit growth in 2011 as well

Headline inflation less unit labor cost inflation (LHS)Net profits after tax (RHS)

Source: BLS, BEA, SEB

90 92 94 96 98 00 02 04 06 08 10

P e r c e n t

-40-30

-20

-10

0

10

2030

40

5060

70

80

-4-3

-2

-1

0

1

23

4

56

7

8

Our overall forecast is that corporate capital spending

will grow by 13 per cent in 2011 and 15 per cent in2012. Its contribution to GDP growth will average 1.6

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 16/55

Nordic Outlook – February 2011 | 17

The United States

percentage points during our forecast period, compared

to 2.1 per cent for private consumption.

Exports will climb in rst half of 2011The weakening of the US dollar will lift exports dur-

ing the next six months, while import gures will be

kept down because an inventory build-up has alreadyoccurred. We foresee increases in exports averaging

11 per cent in 2011-12. Foreign trade will contribute

positively to GDP growth during the rst half of 2011,

followed by a shift to a negative contribution in the

second half and in 2012. The 2010 US current account

balance, which stood at -3.2 per cent of GDP in 2010, is

expected to approach -4 per cent of GDP by the end of

2012.

Consumers getting bolderA strong Christmas shopping season helped lift consump-

tion by 4.4 per cent annualised in the fourth quarter of

2010, the strongest gure since 2006. Several factors

indicate that this positive trend will persist. Extend-

ing the Bush-era tax cuts for another two years as well

as cutting the employees’ federal payroll tax in 2011

will increase room for consumption. Meanwhile the

consumer condence surveys look a bit brighter; for

example the Conference Board indicator posted a heavy

gain in January. We foresee a gradual return to normal

condence levels as the labour market and incomes

strengthen.

Looking further ahead, a stronger labour market will

also help bolster household income. Given the large

role of private consumption in GDP (71 per cent), this

is one key explanation for our brighter economic view.

Household savings adjustment has also come a long way.

According to our calculations, household savings levels

are close to the equilibrium justied by such factors as

wealth position. We are thus expecting only a marginal

additional upturn in household savings ratios during

the next couple of years. Such savings behaviour is also

compatible with a continued decline in household debt

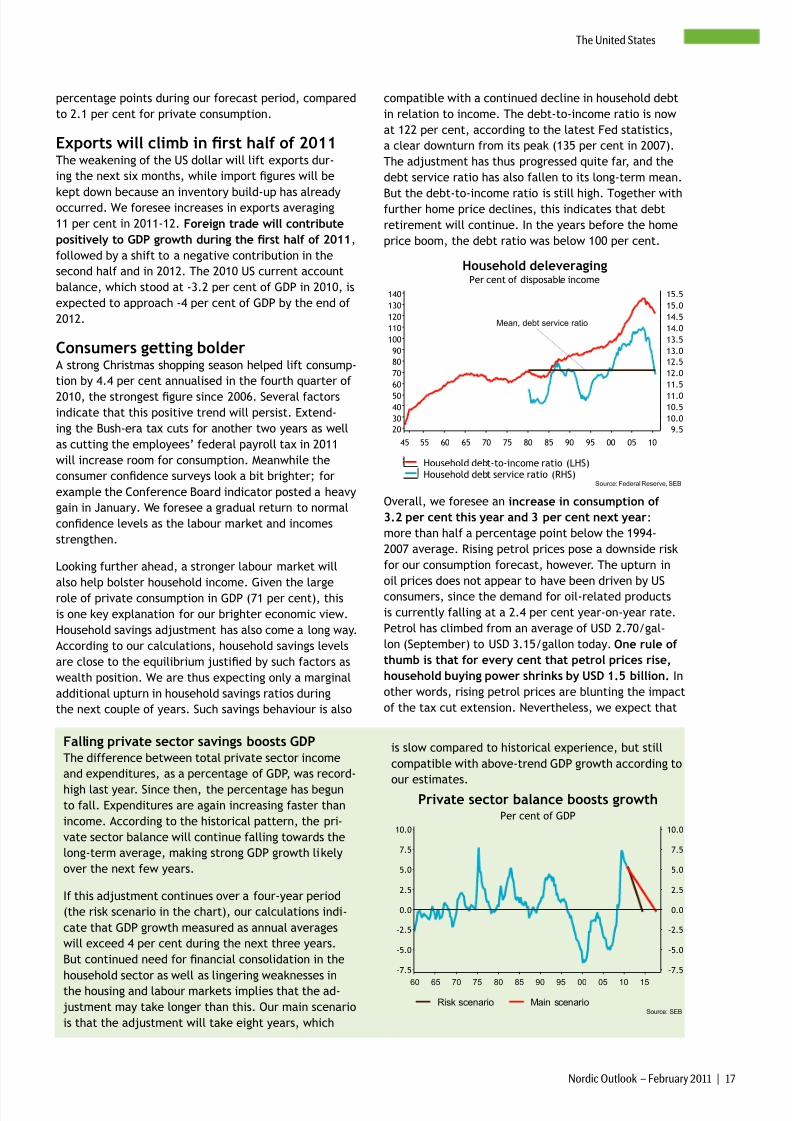

in relation to income. The debt-to-income ratio is now

at 122 per cent, according to the latest Fed statistics,

a clear downturn from its peak (135 per cent in 2007).

The adjustment has thus progressed quite far, and the

debt service ratio has also fallen to its long-term mean.

But the debt-to-income ratio is still high. Together withfurther home price declines, this indicates that debt

retirement will continue. In the years before the home

price boom, the debt ratio was below 100 per cent.

Per cent of disposable income

Household deleveraging

Household debt-to-income ratio (LHS)Household debt service ratio (RHS)

Source: Federal Reserve, SEB

45 55 60 65 70 75 80 85 90 95 00 05 10

9.5

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.5

2030

4050

60

70

8090

100

110

120

130

140

Mean, debt service ratio

Overall, we foresee an increase in consumption of

3.2 per cent this year and 3 per cent next year:

more than half a percentage point below the 1994-

2007 average. Rising petrol prices pose a downside risk

for our consumption forecast, however. The upturn in

oil prices does not appear to have been driven by US

consumers, since the demand for oil-related products

is currently falling at a 2.4 per cent year-on-year rate.

Petrol has climbed from an average of USD 2.70/gal-

lon (September) to USD 3.15/gallon today. One rule of

thumb is that for every cent that petrol prices rise,

household buying power shrinks by USD 1.5 billion. In

other words, rising petrol prices are blunting the impact

of the tax cut extension. Nevertheless, we expect that

Falling private sector savings boosts GDP

The difference between total private sector income

and expenditures, as a percentage of GDP, was record-

high last year. Since then, the percentage has begun

to fall. Expenditures are again increasing faster than

income. According to the historical pattern, the pri-

vate sector balance will continue falling towards the

long-term average, making strong GDP growth likely

over the next few years.

If this adjustment continues over a four-year period

(the risk scenario in the chart), our calculations indi-

cate that GDP growth measured as annual averages

will exceed 4 per cent during the next three years.

But continued need for nancial consolidation in the

household sector as well as lingering weaknesses in

the housing and labour markets implies that the ad-

justment may take longer than this. Our main scenario

is that the adjustment will take eight years, which

is slow compared to historical experience, but still

compatible with above-trend GDP growth according to

our estimates.

Per cent of GDP

Private sector balance boosts growth

Risk scenario Main scenarioSource: SEB

60 65 70 75 80 85 90 95 00 05 10 15

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 17/55

18 | Nordic Outlook – February 2011

The United States

real disposable income will rise at an annualised rate

of 5-6 per cent in the rst quarter, compared to slightly

below 2 per cent in the fourth quarter. Some of the

boost will be saved, thus reversing the recent drop in

the savings ratio. Even so, we expect impressive con-

sumption growth in the current quarter as well.

The housing market is stumblingHousing investments as a share of GDP are at a deeply

depressed 2.2 per cent. There is thus little risk of a fur-

ther decline, but no upswing will occur until the market

catches up with the oversupply of homes. Housing

investments will grow by 2 per cent in 2011, accel-

erating to a 14 per cent rate in 2012, which will still

provide a relatively small contribution to GDP growth

(0.4 percentage points in 2012).

Per cent of GDP

Huge investment swings

Residential (LHS) Nonresidential (RHS)Source: Reuters EcoWin, SEB

50 55 60 65 70 75 80 85 90 95 00 05 10

8

9

10

11

12

13

14

15

2

3

4

5

6

7

8

9

According to the Case-Shiller index, home prices have

fallen for ve months in a row, and our assessment is

that home prices will fall by an additional 5 per cent

this year. Higher mortgage interest rates will contrib-

ute to the downturn, but their effect should not be

exaggerated: a 60 basis point increase in 30-year mort-

gage rates from their bottom level will lower prices by

about 1 per cent in a one-year time frame, according to

our estimates.

The steeper yield curve is positive for bank earnings,

which would mean a gradual easing of credit condi-

tions and increased new lending. But bad commercial

property loans will pull down the banking system, es-

pecially the regional banks. These problems have been

relegated to the future, since banks have postponed

loan maturity dates and thus avoided taking losses on

their balance sheets. Commercial property loans worth

USD 1.5 trillion will reportedly fall due in the next four

years. About half of this volume is related to loans

exceeding current property value.

The labour market is gaining strengthAccording to the Fed’s latest Beige Book, stronger

employment growth is occurring in most parts of the

United States, although the improvement is rather slow.

New unemployment benet claims have also fallen

noticeably since August, which is usually a good indica-

tor that a clear increase in employment is imminent.

A cyclical slowdown in the productivity upturn is also

helping increase the need for new hiring. We expect

productivity to rise by 1.3 per cent this year and 2 per

cent in 2012, compared to 3.5 per cent in both 2009

and 2010.

Our overall assessment is that employment will in-

crease by an average of 180,000 a month this year

and by 200,000 next year, or double the 2010 level.

Home price drop jeopardises recovery

The downward trend in home prices reversed during

the second half of 2009, which can be explained by

several factors: the Fed’s mortgage bond purchases

helped push mortgage rates to record lows, while

mortgage modication plans and temporary morato-

riums on home foreclosures reduced supply. But the

market was still too weak to sustain itself, as illustrat-

ed by the renewed price declines following the expira-tion of temporary tax credits for home purchases.

The supply of available homes is still large: 3.6 mil-

lion, or 65 per cent above the historical average.

Meanwhile the “shadow supply” is signicantly larger

than the 8 month inventory that ofcial gures indi-

cate. According to Fed estimates, the actual inventory

of available homes is around 24 months. In addition,

every fth household with a mortgage owes more

money than its home is worth, and nearly half of bank

assets are tied to the housing market. Sharper home

price declines than we are expecting in our main sce-

nario are thus the biggest risk to US economic recov-ery. Although home prices in real terms have fallen by

one third from their 2006 peak, there is quite a way

left down to the historical average.

Index 1890 = 100

Real home prices well above the mean

Source: Robert Shiller, SEB

90 00 10 20 30 40 50 60 70 80 90 00 10

50

75

100

125

150

175

200

225

50

75

100

125

150

175

200

225

-1 std dev

-23%

+1 std dev

+85% -33%

What may prevent such sharp home price declines is

that a stronger labour market will help prop up the

housing market. In addition, new support measures

will probably be launched if conditions get much

worse.

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 18/55

Nordic Outlook – February 2011 | 19

The United States

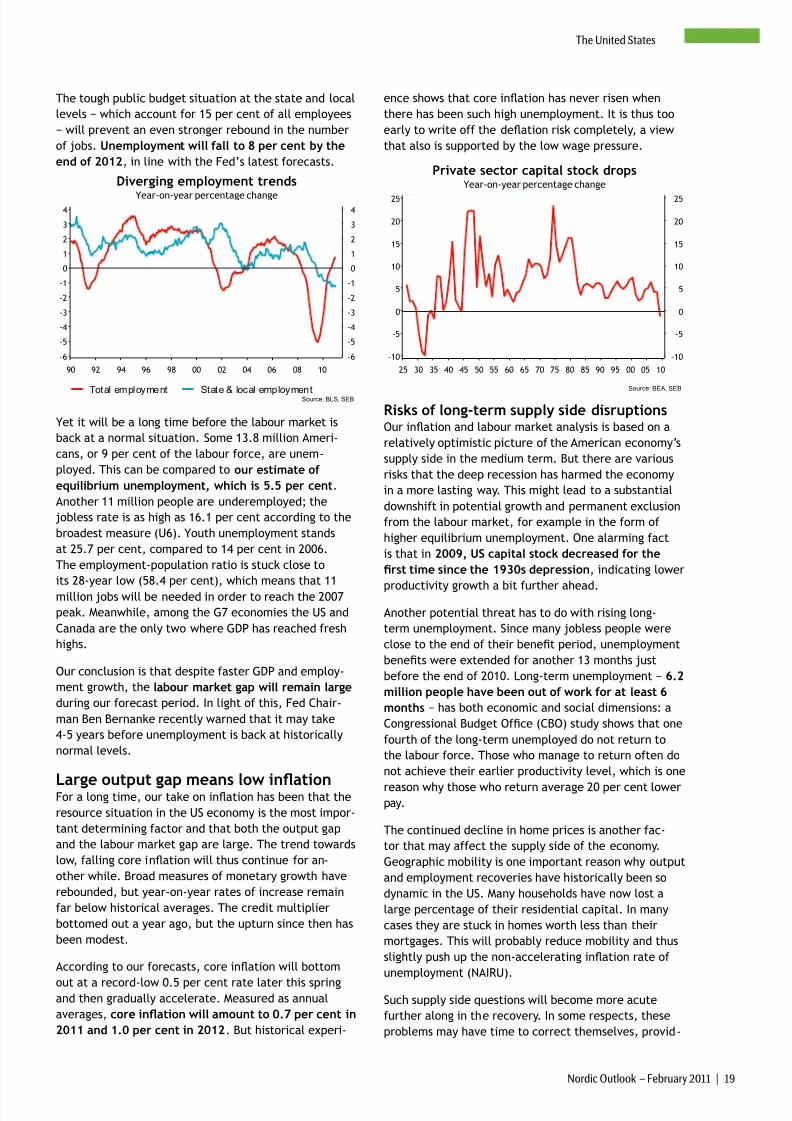

The tough public budget situation at the state and local

levels − which account for 15 per cent of all employees

− will prevent an even stronger rebound in the number

of jobs. Unemployment will fall to 8 per cent by the

end of 2012, in line with the Fed’s latest forecasts.

Year-on-year percentage change

Diverging employment trends

Total employment State & local employmentSource: BLS, SEB

90 92 94 96 98 00 02 04 06 08 10

-6

-5

-4

-3

-2

-1

0

1

2

3

4

-6

-5

-4

-3

-2

-1

0

1

2

3

4

Yet it will be a long time before the labour market is

back at a normal situation. Some 13.8 million Ameri-

cans, or 9 per cent of the labour force, are unem-

ployed. This can be compared to our estimate of

equilibrium unemployment, which is 5.5 per cent.

Another 11 million people are underemployed; the

jobless rate is as high as 16.1 per cent according to the

broadest measure (U6). Youth unemployment stands

at 25.7 per cent, compared to 14 per cent in 2006.

The employment-population ratio is stuck close to

its 28-year low (58.4 per cent), which means that 11

million jobs will be needed in order to reach the 2007

peak. Meanwhile, among the G7 economies the US and

Canada are the only two where GDP has reached fresh

highs.

Our conclusion is that despite faster GDP and employ-

ment growth, the labour market gap will remain large

during our forecast period. In light of this, Fed Chair-

man Ben Bernanke recently warned that it may take

4-5 years before unemployment is back at historically

normal levels.

Large output gap means low inationFor a long time, our take on ination has been that the

resource situation in the US economy is the most impor-

tant determining factor and that both the output gap

and the labour market gap are large. The trend towards

low, falling core ination will thus continue for an-

other while. Broad measures of monetary growth have

rebounded, but year-on-year rates of increase remain

far below historical averages. The credit multiplier

bottomed out a year ago, but the upturn since then has

been modest.

According to our forecasts, core ination will bottom

out at a record-low 0.5 per cent rate later this springand then gradually accelerate. Measured as annual

averages, core ination will amount to 0.7 per cent in

2011 and 1.0 per cent in 2012. But historical experi-

ence shows that core ination has never risen when

there has been such high unemployment. It is thus too

early to write off the deation risk completely, a view

that also is supported by the low wage pressure.

Year-on-year percentage change

Private sector capital stock drops

Source: BEA, SEB

25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 00 05 10

-10

-5

0

5

10

15

20

25

-10

-5

0

5

10

15

20

25

Risks of long-term supply side disruptionsOur ination and labour market analysis is based on a

relatively optimistic picture of the American economy’s

supply side in the medium term. But there are various

risks that the deep recession has harmed the economy

in a more lasting way. This might lead to a substantial

downshift in potential growth and permanent exclusion

from the labour market, for example in the form of

higher equilibrium unemployment. One alarming fact

is that in 2009, US capital stock decreased for the

rst time since the 1930s depression, indicating lower

productivity growth a bit further ahead.

Another potential threat has to do with rising long-

term unemployment. Since many jobless people were

close to the end of their benet period, unemployment

benets were extended for another 13 months just

before the end of 2010. Long-term unemployment − 6.2

million people have been out of work for at least 6

months − has both economic and social dimensions: a

Congressional Budget Ofce (CBO) study shows that one

fourth of the long-term unemployed do not return to

the labour force. Those who manage to return often do

not achieve their earlier productivity level, which is one

reason why those who return average 20 per cent lowerpay.

The continued decline in home prices is another fac-

tor that may affect the supply side of the economy.

Geographic mobility is one important reason why output

and employment recoveries have historically been so

dynamic in the US. Many households have now lost a

large percentage of their residential capital. In many

cases they are stuck in homes worth less than their

mortgages. This will probably reduce mobility and thus

slightly push up the non-accelerating ination rate of

unemployment (NAIRU).

Such supply side questions will become more acute

further along in the recovery. In some respects, these

problems may have time to correct themselves, provid-

8/7/2019 SEB report: Giddy euphoria about the Swedish economy

http://slidepdf.com/reader/full/seb-report-giddy-euphoria-about-the-swedish-economy 19/55

20 | Nordic Outlook – February 2011

The United States

ed that the US economy enters a more positive recovery

dynamic. Otherwise fresh economic policy thinking may

be required to avoid long-term damage.

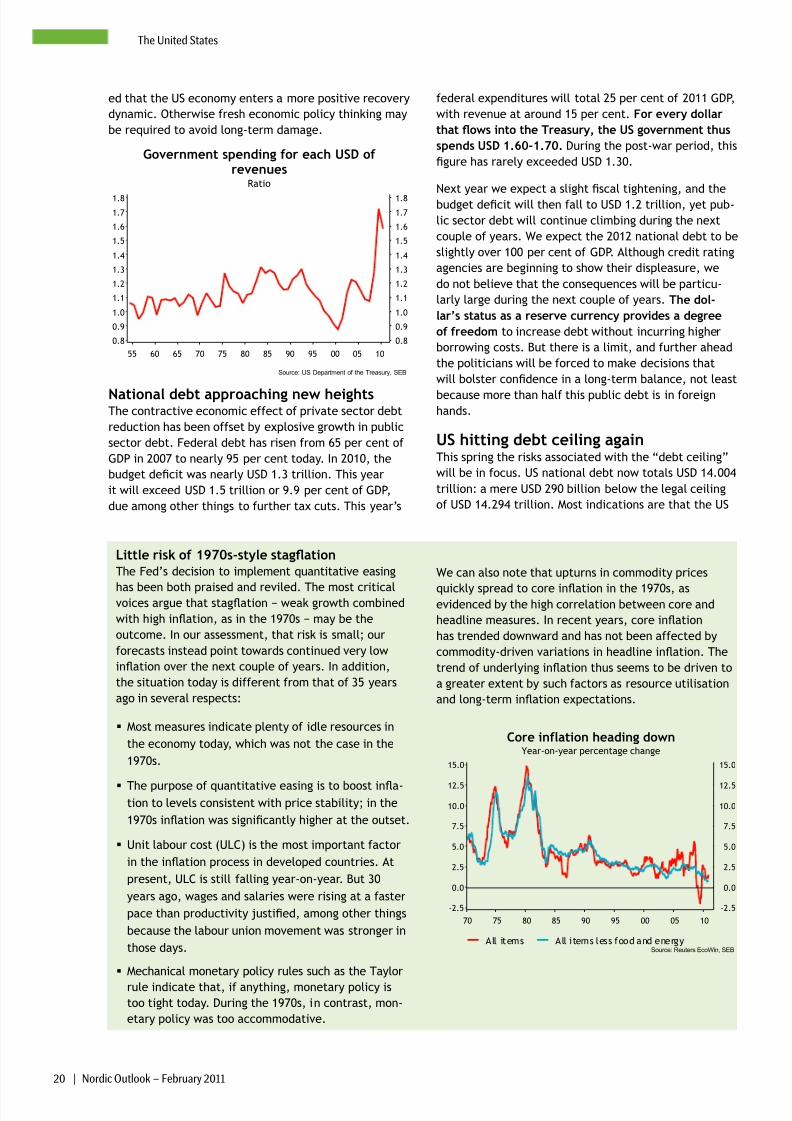

Ratio

Government spending for each USD of revenues

Source: US Department of the Treasury, SEB

55 60 65 70 75 80 85 90 95 00 05 10

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

National debt approaching new heightsThe contractive economic effect of private sector debt

reduction has been offset by explosive growth in public

sector debt. Federal debt has risen from 65 per cent of

GDP in 2007 to nearly 95 per cent today. In 2010, the