Embed Size (px)

Citation preview

CALIFORNIA MORTGAGE FINANCE NEWS 1

CALIFORNIA MORTGAGE BANKERS ASSOCIATION

THE VOICE OF REAL ESTATE FINANCE

FA L L2 0 1 4

in this issue…CHAIRMAN’S CORNER page 1

EXECUTIVE DIRECTOR’S LETTER page 5

LEGISLATIVE REPORT page 7

RESIDENTIAL NEWS page 8

COMMERCIAL NEWS page 9

ROUNDTABLE ARTICLE page 10

LEGAL—RESIDENTIAL page 13

LEGAL—COMMERCIAL page 18

CALENDAR page 21

WELCOME NEW MEMBERS page 23

PHOTO GALLERIES page 43

ROAD TRIP page 50

Contact: California Mortgage

Bankers Association

(916) 446-7100 Phone

(916) 446-7105 Fax

[email protected] Email

555 Capitol Mall, Suite 440

Sacramento, CA 95814

California Mortgage Finance News is published four

times per year: Spring, Summer, Fall and Winter.

California Mortgage Finance News is published by

the California Mortgage Bankers Association.

editor: Dustin Hobbs

publisher/layout: Wolfe Design Marketing

Change! Again!

With the return

of Fall comes the

return of election

season, and this

year’s was quite

the game-changer.

Again. It seems a two-year cycle these

days that each party gets swept in a

‘wave’ only to get rejected two years

later. Unless you’ve been under a rock

for the past few weeks, you know that

the Republicans have captured control

of the U.S. Senate and several additional

state governorships. That’s certainly

the main headline, but there are several

other results that you may not be

as aware of, but could shake up our

industry even more than swapping out

Harry Reid for Mitch McConnell will.

In my backyard, in Richmond,

industry (including the CMBA) has

been diligently fighting a dangerous

eminent domain scheme designed to

help underwater borrowers by seizing

the mortgage notes from investors. If

you’ve heard this before, bear with

me! Just over a year ago, the city

seemed poised to put the plan into

action, giving mortgage investors a

hard deadline to either sell the targeted

loans to the city or face eminent

domain proceedings. That deadline

came and went with no action, in

large part due to the makeup of the

city council. Proponents of the plan

were just short (a single vote at times)

of having enough support to move

CHAIRMAN’S CORNER

Season of Change ReturnsBY CHRISTOPHER M. GEORGE, CMG FINANCIAL, CMBA CHAIRMAN

CONTINUED ON PAGE 4

Use this QR code to download the new

CMBA EVENT APP!

intelligent default solutionswww.goodmandean.com

�REO Asset Management�Valuation Services�Field & Inspection Services�Closing Management/

Title Curative

Masters at Juggling the DetailsTo see how Goodman Dean can helpyou succeed in today’s challengingbusiness environment, call us at 800-930-8999, or [email protected].

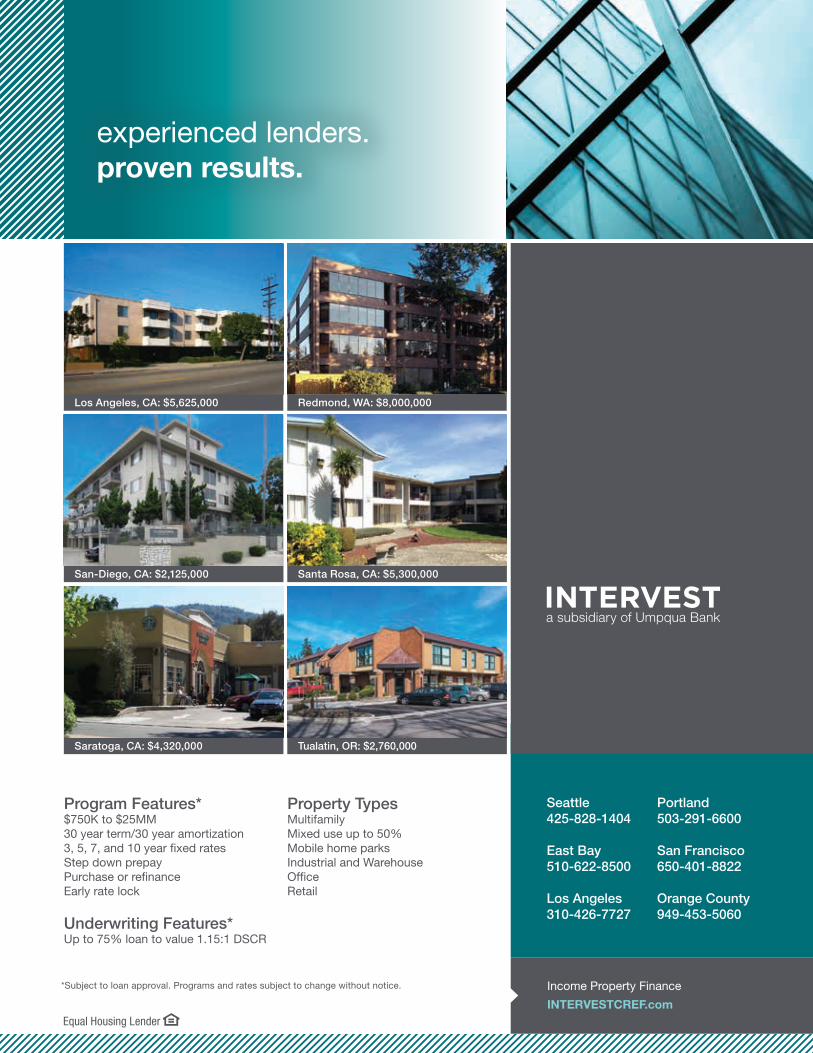

Program Features*$750K to $25MM30 year term/30 year amortization3, 5, 7, and 10 year fixed ratesStep down prepay Purchase or refinanceEarly rate lock

Underwriting Features*Up to 75% loan to value 1.15:1 DSCR

Property TypesMultifamilyMixed use up to 50% Mobile home parks Industrial and WarehouseOfficeRetail

Seattle425-828-1404

East Bay510-622-8500

Los Angeles310-426-7727

Los Angeles, CA: $5,625,000 Redmond, WA: $8,000,000

Income Property Finance

INTERVESTCREF.com

Portland503-291-6600

San Francisco650-401-8822

Orange County949-453-5060

San-Diego, CA: $2,125,000 Santa Rosa, CA: $5,300,000

Saratoga, CA: $4,320,000 Tualatin, OR: $2,760,000

experienced lenders. proven results.

*Subject to loan approval. Programs and rates subject to change without notice.

FALL 20144

CHAIRMAN’S CORNER CONTINUED FROM PAGE 1

Feeling BuriedBy New

ComplianceBy New

ComplianceBy New

Demands?ComplianceDemands?

Compliance

Check out CMBA’s FREE industry resource:

Mortgage, Quality & Compliance

Committee (MQAC)webinars!

Join our FREE webinars(fourth Thursday of each

month at 11 am) and view great presentations

from top experts on:

Dodd-FrankCFPB Exams

LO CompensationCA HomeownerBill of Rights

And more!

CMBA Members - you can access all MQAC

presentations on CMBA’s ‘Members-Only’ page!

Call (916) 446-7100for more details!

forward with eminent domain. As a

result, the plan’s supporters have spent

the past year trying to find partners

in San Francisco and other locales

that would partner with the city and

share costs and (it was hoped) liability,

essentially doing an end-run around

the unfavorable politics on the council.

That may have all changed,

however, on election night. All seven

council members were on the ballot,

either running for a different seat or

up for reelection. Although the council

seats are technically non-partisan, the

race quickly turned into an ideological

contest between a progressive ‘slate’ of

candidates and three existing council

members (Corky Boozè, Nat Bates,

and Jim Rogers) who were viewed as

more business-friendly, and had been

seen as votes against the eminent

domain program. On election night,

all three lost, and the progressive

coalition was swept into power, and

now may hold up to 6 of the 7 seats on

the council. One of the newly-elected

members of the council specifically

mentioned the plan in his post-election

comments, saying “With the new

council, Richmond will continue to

be the trendsetter for local, state and

national policies. Eminent domain is

one of those, and I think it will become

a tool the cities across the country

will use.” After a year of simmering

beneath the radar, I expect the eminent

domain issue to be back on the front

burner in 2015. Stay tuned.

In Sacramento, we did see

some change, albeit less than at the

national level or in Richmond. Gov.

Jerry Brown was reelected by a wide

margin, and the Democrats continued

to dominate all the statewide

offices. However, the calculation

may have changed a bit in the

Legislature, as Democrats lost their

2/3 ‘supermajority’ advantage in both

the Senate and the Assembly. This

means that on certain bills that require

a 2/3 vote, Republicans will regain

some bargaining power they lost two

years ago. Make sure and read Pat

Zenzola’s column to keep up on what

is happening in Sacramento now and

during the legislative session that will

start up in January.

Change is coming to CMBA

as well, and I am excited to let you

know that in 2015, we will be rolling

out some exciting new programs and

features that will enhance the value of

your membership dollars, and improve

upon the three pillars that CMBA

stands on: advocacy, education, and

connection. I don’t want to give away

too much now, but early next year

I’ll give you all the details and I trust

you’ll be as excited as I am!

Change is by its nature disruptive,

but not necessarily destructive. It

sharpens our focus and refines our

abilities. That’s true of mortgage

companies facing regulatory onslaught,

and trade groups like the California

MBA, working to find new solutions

and new ways to serve our members.

•

CALIFORNIA MORTGAGE FINANCE NEWS 5

2015 will mark the

60th anniversary

of the California

MBA! Six decades

of gradual

development to

evolve into the

association that we are today. Our

organization has weathered wars,

dramatic interest rate fluctuations,

epic bounds forward in technology,

the financial crisis of the early 2000’s

and the onslaught on legislative and

regulatory burdens that have been

placed upon the industry. Over the

years, the term “mortgage banker”

has been viewed as the catalyst for

achieving the American dream, as well

as the cause for global financial crisis.

Through the best of times and the

biggest challenges the California MBA

has remained committed to providing

the strongest representation for the

mortgage industry and serves as the

organization that attracts industry

leaders from across the nation. As we

look back on our 60 years, let’s think

about how we got here.

In early 1955, with strong local

associations in both San Francisco

and Los Angeles, the leaders of the

future California MBA promoted

the idea of forming a statewide

association. The main thrust for

creating this organization came from

Urban K. Wilde, who served as the

California MBA’s first President, and

Willis Bryant, who was the first Vice

President. These individuals gathered

with other mortgage industry leaders

at the Del Monte Lodge (which is now

The Lodge at Pebble Beach) in April

1955 to form the association.

The original goals were simple:

further promote the industry (which

took many forms over the years),

establish an effective legislative

and regulatory advocacy program,

foster strong business relationships

and personal friendships among the

membership, and to attract money out

West! With so much of our legislative

and regulatory focus in recent years

on residential mortgage banking, it is

interesting to note that the founders,

in part, created the California

Mortgage Bankers Association in an

effort to attract East coast investors to

invest in commercial real estate in our

state! Granted they also saw value in

a statewide organization to represent

the real estate finance industry before

the State Legislature but strengthening

our state was a key factor.

Over the years, the California

MBA has been at the forefront of

every legislative and regulatory

proposal that’s come before our

policymakers. We’ve never strayed

from the over-arching message

of protecting access to affordable

credit for qualified borrowers. Our

organization has partnered with other

industry associations to shape the

direction of lending in California, and

we’re not done! Today our member

companies join the thousands of

people who’ve come before them

to work with our lobbying team to

formulate positions on key issues in

our state.

You cannot tell a story about

the California MBA without

mentioning the fact that it was THE

social connection for the industry

before social media! The photos of

conferences and events from the first

few decades show how close these

friendly competitors were and how

important developing and maintaining

those business relationships were

to the industry. We are still a source

of connections and pride ourselves

on offering a variety of methods to

connect with industry leaders and

fellow members.

Education has also been a focal

EXECUTIVE DIRECTOR’S LETTER

Networking. Education. Connection.From the Beginning

BY SUSAN MILAZZO, CMBA EXECUTIVE DIRECTOR

CONTINUED ON PAGE 20

Subscribe to CMBA’s official

YouTube Channel and get the

latest video updates on breaking

news, conference information, and

membership product updates.

Seattle Boston Newark Phoenix Portland Las Vegas New York Twin Cities Orange County San Diego County Los Angeles County

As counselors in a complex legal environment, we search for the best solutions regardless of difficulty. We understand the goals of our clients and strive to exceed their expectations. We provide our clients with cost-effective legal strategies in financial services litigation. With our accomplished and capable team of attorneys, in 11 offices across the country, we are committed to providing our clients with exceptional service and results.

HOUSER WWW.HOUSER-LAW.COM

(877) 686-9145

experienced litigators holding ourselves to the highest standards

CALIFORNIA MORTGAGE FINANCE NEWS 7

The 2014

November general

election resulted

in a strong wave

of victories for

Republicans across

the nation, with a

gain of 7 Senate seats, 13 House seats

and 3 governorships as of this writing.

The Republican wave, however, hit a

wall at the Sierra Nevada. Governor

Jerry Brown won a historic 4th term,

beating the Republican challenger

with roughly 59% of the vote, and

Democrats were successful at sweeping

all of the other California statewide

offices—Lt. Governor, Attorney

General, Secretary of State, Controller,

Treasurer and Insurance Commissioner.

The Governor’s two priorities on the

state ballot also won by wide margins:

Proposition 1, a $7.5-billion water bond

measure, and Proposition 2, which

shores up the state’s rainy day fund.

California Republicans did make

some gains in the State Legislature,

achieving the goal of keeping the

Democrats from obtaining the two-

thirds majority in the Legislature

that they initially achieved in the

2012 elections. Political scandals,

low voter turnout and concern about

one political party having too much

power are likely contributing factors

in the failure of Democrats to regain a

supermajority in the general election.

California experienced a historic low

voter turnout of approximately 30%

on Election Day. It takes weeks after an

election to determine the final turnout

percentage but it is quite possible that

when the count is complete it will be

around 40 %. The lowest previous

turnout percentage of registered voters

in a non-presidential general election, in

2002, was 50.6%. The real importance

of Republicans denying Democrats

supermajorities in the Legislature is that

while the budget can be approved with

a simple majority, it still takes two-

thirds votes to raise taxes. That means

that any new state tax legislation, such

as split-roll changes to Proposition 13

that would raise commercial property

taxes, will most likely need to be put

on the ballot by voters’ signatures

instead of by the Legislature.

Switching gears to the legislative

session, the California Legislature

adjourned early Saturday morning of

the Labor Day weekend, concluding

its 2014 legislative session. September

30 was the last day for the Governor

to sign or veto bills passed by the

Legislature in the final days of session.

Several bills of interest to CMBA’s

members were still being considered

in the last weeks of the legislative

session, and summaries of those

measures are listed below.

AB 1393—Personal Income Taxes:

Mortgage Debt Forgiveness

Chaptered by Secretary of State—

Chapter 152, Statutes of 2014.

AB 1393 extends the exclusion

of the discharge of qualified principal

residence indebtedness for state

income tax purposes to debt that

is discharged on or after January 1,

2013, and before January 1, 2014. The

Personal Income Tax Law provides for

modified conformity to provisions of

federal income tax law relating to the

exclusion of the discharge of qualified

principal residence indebtedness

from an individual’s income if that

debt is discharged after January 1,

2007, and before January 1, 2013.

The federal American Taxpayer Relief

Act of 2012 extended the operation

of those provisions to qualified

principal residence indebtedness that

is discharged before January 1, 2014,

and AB 1393 conforms to the federal

extension. CMBA supported AB 1393,

and it has been signed into law with

an immediate effective date.

AB 1698—Voiding of False or

Forged Real Property Documents

Chaptered by Secretary of State—

Chapter 455, Statutes of 2014.

AB 1698 originally would

have required that after a person is

LEGISLATIVE REPORT

Election Results Boost Republicans in Nation, But State Bucks TrendBY PAT ZENZOLA, KP PUBLIC AFFAIRS, CMBA LEGISLATIVE COUNSEL

CONTINUED ON PAGE 21

FALL 20148

Millennials are an

important target

market in the

mortgage industry

because they

now represent

the largest pool

of potential homebuyers. Defined

between the ages of 14–34, millennials

make up a population of roughly 800

million—larger than that of the baby

boomer generation. Considered the

most educated generation to date, this

demographic requires more information,

research and brand engagement before

making a decision to purchase.

Marketing and communicating

to a younger generation commands

a very different approach to that of

other generations. Traditional forms

of marketing, such as direct mail, print

ads, or even email marketing are not as

effective with this group. Millennials

understand what spam email looks like;

they can vet it out and delete it quicker

than you could imagine. Direct mail is

also ineffective because this group goes

online to search for the information they

need. In turn, text messaging will only

be effective once a relationship has been

built. In order to earn a millennial as a

personal client, mortgage professionals

must understand and familiarize

themselves with the way this generation

engages through various media.

Millennials are really saying “don’t sell

me, engage with me.”

American Pacific Mortgage (APM)

positions itself in the front-line of social

media engagement, taking a millennial-

friendly approach with its interactions.

However, companies should refrain from

selling through social media outlets,

such as Pinterest, LinkedIn, Twitter and

Facebook, but rather use them as a way

to engage and educate this audience.

Because this generation relies heavily

on social endorsements when making

a buying decision, it is vital that your

brand is positively represented online,

both in consumer reviews and paid

media. They have grown up in an era

that has endless choices, creating a

critical need to tread lightly and patiently,

yet with clear intention. It’s very easy

to figure out if you are being sold, and

selling, as a stereotype, holds an array of

negative connotations of pushy behavior

and car salesman mentality.

So how do you communicate and

market to this core group? Positive

affirmations and social endorsements

heavily influence the buying decision of

this audience, so you need to educate

them and earn that trust to get the

commitment to purchase. Boil it down

and get simplistic: this demographic starts

its shopping process online. With the

amount of viable information accessible

to anyone, this generation capitalizes

on an unspoken expectation of limitless

search engines and readily available

information. Engaging at the pre-shopping

level will ensure the consumer receives

RESIDENTIAL NEWS

Marketing to Millennials“Don’t sell me, engage with me”

BY LEIF A. BOYD, EXECUTIVE VICE PRESIDENT OF NATIONAL PRODUCTION, AMERICAN PACIFIC MORTGAGE CORPORATION

positive brand exposure early in their

decision-making process. When engaging,

keep in mind that these individuals are

searching for who they know and who

they can trust, so be familiar and honest

100 percent of the time. They are saying

“engage with me as a consumer, show

me what I need to know, educate me and

help me understand.”

Some consumers may be

unaware of the many advantages of

homeownership; such as: property

selection, customization and investment

opportunities. Although the thrill of

owning a home can seem attractive

to a prospective client, they must

also be educated about the process

and requirements to purchasing their

first home. As a generation who may

have some of the highest debt levels

in history, including student loans

and credit card debt, these potential

homeowners will need guidance to

manage their debt-to-income ratio,

spending habits and ideal credit balances

to maintain. Loan officers experiencing

success with the millennial generation

are the ones providing the most

valuable education. Take a consultative

approach based on this generation’s

communication preferences and create

deep, long-lasting relationships by

developing a personal connection

with each of your customers. Invest in

building these relationships and they

will invest in what you have to offer.

•

CALIFORNIA MORTGAGE FINANCE NEWS 9

COMMERCIAL NEWS

Top Trends to Look for in Commercial Lending in 2015BY ALEXA MIZRAHI, SENIOR LOAN OFFICER, LONE OAK FUND

As 2014 comes

to a close, it’s

important for

mortgage brokers

to recognize and

understand how

the commercial

real estate industry is shifting in order

to best leverage the increasing lending

competition and produce strong

results for their clients.

Niche Lending is on the Rise

Many new hard money lenders

have entered the market in the last

year, giving investors and developers

plenty of alternative financing options.

This increase is forcing lenders to

become more aggressive and creative

in both pricing and leverage.

From the lender’s perspective, it’s no

longer enough to advertise competitive

prices and LTVs. Today’s investors need

to get deals done quickly with experts

who understand their investment needs.

Private lenders have found that defining

a niche is key to setting themselves

apart, which is creating increased

opportunity for mortgage brokers to

find the money their clients need fast.

Lone Oak Fund, for example,

specializes in quick closes, short-term

first trust deeds of commercial and non-

owner occupied residential product.

In addition, many of these niche

CONTINUED ON PAGE 24

• RepresentationthroughoutCalifornia

• Onepointofcontact

• Initiateyourcasebyphone,faxorwebsite:www.kts-law.com

• Noticesservedsamedaywereceivethecase

• Timelyprogressandstatusreports

• Streamlinedprocesstoevictoccupants

• Followupcollectionservicesavailable

Over 35 years of superior legal representation

Residential & Commercial Evictions

Collection & Creditor Representation

Bankruptcy & Secured Creditor Representation

Business & Real Estate Litigation

Educational Programs & Resources

Estate Planning

Fair Housing

Homeowner Association Representation

Real Estate & Business Transactions

Residential & Commercial Evictions

Collection & Creditor Representation

Bankruptcy & Secured Creditor Representation

Business & Real Estate Litigation

Educational Programs & Resources

Estate Planning

Fair Housing

Homeowner Association Representation

Real Estate & Business Transactions

Specializing in Post Foreclosure Evictions

San Diego(800) 338-6039

orange County(800) 564-6611

LoS angeLeS(800) 577-4587

inLanD empire(800) 564-6611

Bay area(800) 525-1690

SaCramento/ CentraL VaLLey(800) 525-1690

www.ktS-Law.Com

Specializing in Post Foreclosure Evictions

FALL 201410

ROUNDTABLE ARTICLE

Social Media and the Mortgage IndustryEDITOR’S NOTE—This is the latest in a series dealing with the issues facing the real estate finance industry. Each issue we touch on

a different topic, asking CMBA’s experts for their thoughts on the issue at hand. In this issue of CMFN, we ask three experts about social

media and its role on the mortgage industry. The topic was addressed further in a recent webinar hosted by CMBA’s Mortgage Quality &

Compliance Committee (MQAC). Jonathan Cannon is an Associate with BuckleySandler, LLP and presented on the topic during the

aforementioned webinar. Lisa Klika is SVP, Compliance & Quality Assurance with Guild Mortgage Company, and Michael Pfeifer is

CMBA’s General Counsel, and Managing Partner at Pfeifer & De La Mora, LLP.

The views and opinions expressed are solely those of the authors.

Q: What are some common

mistakes lenders and their

employees make on social media

that can put the company at risk?

Cannon: One of the most

common mistakes is for companies

and individuals to treat materials

shared on social media differently

than other public-facing materials.

Advertising is advertising, whether

it takes the form of a print ad, an

online banner ad, or a posting to

social media. Because the barriers

to entry are so low for social media

postings, lenders and their employees

may sometimes fail to recognize the

compliance obligations that still apply

to social media materials. But all

advertising has to keep in mind, for

instance, the requirements under TILA

when rates or other trigger terms

are stated, the requirements under

the SAFE Act and state laws related

to licensing disclosures, and the

requirements under the Federal Trade

Commission Act related to topics

such as deceptive advertising and the

use of testimonials.

But specifically, it may be most

common for lenders to fail to put

adequate recourses into their social

media program. Just because it may

be difficult for a lender’s compliance

department to monitor what its

branch employees may be sharing

online does not mean that the lender is

not obligated to monitor this activity.

Having strong social media policies

and procedures, along with sufficient

training and monitoring, are necessary

if a lender and its employees will be

sharing material through social media.

Klika: Social media is one of

the most challenging areas for a

lender to manage from a compliance

perspective. It is a free, accessible,

and instantaneous way for an

individual to have access to a large

population of “friends” (and foes).

In the case of a loan officer, there

is also the frequent misconception

that their posts on social media are

not considered advertisements or

otherwise regulated under state and

federal law. But in fact there are a

whole host of state and federal laws

that can govern social media activity.

The Truth in Lending Act, Gramm

Leach Bliley, and UDAAP are just a

few. Even when this is understood,

attempting to apply complex, layered,

and archaic regulatory requirements

to a 140 character “tweet” will make

any millennial roll their eyes and any

compliance officer suffer a migraine.

Social media policy and oversight

also have personnel implications.

Compliance and Human Resources

must work together to evaluate how

consumer financial protection and

employment law intersect.

Pfeifer: I define “social media” as

including the following: microblogging

websites like Facebook, Twitter,

Google Plus and My Space; Customer

review websites and bulletin

boards like Yelp, Google Local, and

Citysearch; photo and video sites

like YouTube and Flickr; professional

networking sites like LinkedIn; and

even virtual “worlds” like “Second

Life” and social games like “Farmville.”

The most common mistake lenders

and employees make is thinking

CONTINUED ON PAGE 25

MORTGAGE WAREHOUSELINES OF CREDIT.

BankoftheSierra.com

Member FDIC

We are pleased to offer Mortgage Warehouse l ines competitive with the “Big

Banks”, combined with the friendliness and flexibi l ity of a Community Bank.

Give us a call !

Ryan ToncheffVP, Mortgage Warehouse(559) 782-4900 [email protected]

1410-0840_AD_California Mortgage Bankers.indd 1 11/3/2014 10:56:27 AM

WORKING TOGETHER TO HAVE A PROFOUND AND POSITIVE IMPACT ON THE LIVES OF ALL WE SERVE.

Owned by Hilltop Holdings (NYSE: HTH), PrimeLending is a national lender that is backed by strong support and long-term staying power. At the same time, loan officers are able to close loans more quickly due to our localized processing and underwriting.

PrimeLending has the best of both worlds – and we want you to be a part our team. If you’re ready to lay down your roots with a company you can trust, PrimeLending can provide you with the tools you need to grow your career with us. Come join us!

Core Convictions

• Honesty and Integrity• People Centric Culture • Agile • Service Beyond Expectations • One Team, One Purpose

PrimeLending offers:

AgilityClose loans more quickly with localized processing and underwriting.

StabilityCount on us for long-term strength and staying power.

TechnologyCapitalize on cutting-edge technology tools for CRM, processing and more.

CultureCultivate relationships through our compelling, people-centric culture.

MarketingCreate more business with professionally designed marketing tools.

Not intended for consumer distribution. Not subject to Reg Z 1026.24. PrimeLending, a PlainsCapital Company (NMLS: 13649). PrimeLending, a PlainsCapital Company, is an equal opportunity employer and ensures that all applicants will receive consideration for employment without regard to race, color, religion, gender, national origin, age, disability, genetic, pregnancy or any other status as protected by federal, state or local law. Equal Housing Lender. © 2013 PrimeLending.

4153421694 [email protected] www.primelending.com/ 4685 MacArthur Court #480 Newport Beach, CA 92660 NMLS: 365837

Daniel Rawitch Senior Vice President, Regional Manager

Legal

CALIFORNIA MORTGAGE FINANCE NEWS 13

What Flagstar Bank Can Teach Mortgage Servicers and Others About the CFPBBY JOSHUA dEL CASTILLO, PARTNER, & KENYON D. HARBISON, ASSOCIATE, ALLEN MATKINS

Residential

On September 29, 2014, the Consumer

Financial Protection Bureau (CFPB)

entered into a highly significant Consent

Order with Michigan-based loan

servicer, Flagstar Bank, F.S.B. (Flagstar).

Flagstar originates residential loans,

but its primary business is servicing

residential loans owned by others.

The CFPB’s enforcement effort and the

recent Consent Order related to this

business. Specifically, the CFPB alleged

that Flagstar had failed to comply with

a number of regulations regarding the

processing of borrower requests for loan

modifications. A total of $37.5 million

was assessed as a result of Flagstar’s

alleged misconduct. The most interesting

aspect of this case was arguably not

the $37.5 million damages and penalty

(though that grabbed initial headlines),

but was instead the prohibition against

Flagstar buying the right to service more

defaulted loans until Flagstar could prove

future compliance. The case provides an

important, and harsh, lesson to mortgage

servicers, and to other businesses.

The CFPB applied a number of

different rules and regulations to

Flagstar’s actions. These included 12

U.S.C. Sections 5536(a)(1)(B) & 5531(c)

(1) of the Consumer Financial Protection

Act of 2010 (CFPA), which authorize the

CFPB to punish “unfair, deceptive, or

abusive” practices. The CFPB also relied

upon the loss mitigation provisions

of the 2013 Real Estate Settlement

Procedures Act Mortgage Servicing Final

Rule (MSFR).

Pursuant to the terms of the

Consent Order, Flagstar neither

admitted nor denied any fact alleged

by the CFPB. Nothing in this article

is intended to suggest Flagstar was

guilty of any violation of applicable

regulations, or contradict anything

stated in the Consent Order. Instead,

the article highlights the consequences

of what were—as found by the CFPB—

particularly egregious violations.

As claimed by the CFPB, during

the period from 2011–2014, Flagstar

serviced loans for over 40,000

delinquent borrowers, for whom it

was responsible for administering

loss mitigation (loan modification)

applications. After the financial crisis,

even after a dramatic increase in the

volume of such applications, Flagstar

allegedly had no written policies,

and no quality assurance function.

The CFPB found that, at one point

in 2011, Flagstar had 13,000 active

loss mitigation applications, but only

25 full-time employees in its loss

mitigation department, not including a

third-party vendor in India reviewing

some applications. The average call

wait time for calls to Flagstar was 25

minutes, and almost 50% of callers

abandoned their calls. The CFPB

found that the understaffing continued

even after a 2011 restructuring, and

Flagstar routinely took more than

90 days to reach a loan modification

decision, three times the 30-day period

identified in applicable guidelines. Of

15,000 borrowers who applied for loss

mitigation, Flagstar closed more than

8,000 applications because of missing,

incomplete or expired documents.

Flagstar sometimes closed applications

due to expired documents, even where

its own delay had caused the documents

to expire, though more typically it

would require borrowers to submit

updated documents.

For a nine-month period in 2012

and 2013, Flagstar allegedly withheld

information borrowers needed to

complete their applications at all:

because of a vendor-related glitch,

Flagstar failed to send or delayed

sending its “missing document” letters to

borrowers, which were the only way a

borrower would know that documents

were missing from an application. Some

CONTINUED ON PAGE 29

WORKING TOGETHER TO HAVE A PROFOUND AND POSITIVE IMPACT ON THE LIVES OF ALL WE SERVE.

Owned by Hilltop Holdings (NYSE: HTH), PrimeLending is a national lender that is backed by strong support and long-term staying power. At the same time, loan officers are able to close loans more quickly due to our localized processing and underwriting.

PrimeLending has the best of both worlds – and we want you to be a part our team. If you’re ready to lay down your roots with a company you can trust, PrimeLending can provide you with the tools you need to grow your career with us. Come join us!

Core Convictions

• Honesty and Integrity• People Centric Culture • Agile • Service Beyond Expectations • One Team, One Purpose

PrimeLending offers:

AgilityClose loans more quickly with localized processing and underwriting.

StabilityCount on us for long-term strength and staying power.

TechnologyCapitalize on cutting-edge technology tools for CRM, processing and more.

CultureCultivate relationships through our compelling, people-centric culture.

MarketingCreate more business with professionally designed marketing tools.

Not intended for consumer distribution. Not subject to Reg Z 1026.24. PrimeLending, a PlainsCapital Company (NMLS: 13649). PrimeLending, a PlainsCapital Company, is an equal opportunity employer and ensures that all applicants will receive consideration for employment without regard to race, color, religion, gender, national origin, age, disability, genetic, pregnancy or any other status as protected by federal, state or local law. Equal Housing Lender. © 2013 PrimeLending.

4153421694 [email protected] www.primelending.com/ 4685 MacArthur Court #480 Newport Beach, CA 92660 NMLS: 365837

Daniel Rawitch Senior Vice President, Regional Manager

Legal

FALL 201414

Residential

First District Court of Appeal Resurrects

“Negligent Loan Servicing” TheoryBY LUKE SOSNICKI, SENIOR COUNSEL, & STEPHANIE T. YU, ASSOCIATE, DYKEMA GOSSETT, PLLC

On August 7, 2014, California’s First

District Court of Appeal opined in

Alvarez v. BAC Home Loans Servicing,

L.P that a residential mortgage servicer

may owe a borrower a duty of care

when reviewing the borrower’s

loan-modification application.1 While

the First District in Alvarez arguably

followed its own precedent, the

decision nonetheless represents a

departure from the general rule in

California that a lender owes no duty

of care to a borrower if the lender

does not exceed its “conventional role

as a lender of money.”2

Over the last few years, borrower

lawsuits relating to servicers’ reviews

of loan-modification applications

have become increasingly common.

“Negligent loan servicing” is a claim

that often appears in such suits.

One of the better defenses to these

common-law negligence claims has

been that servicers owe borrowers

no duty of care to support the claims.

The servicer would argue its actions

in reviewing a loan-modification

application were within a servicer’s

“conventional role,” the court would

conclude the servicer owed no duty

to the borrower, and the court would

thereafter likely dismiss the claim.

In February 2013, the First District

breathed some new life into the

“negligent loan servicing” theory in

Jolley v. Chase Home Finance, LLC.3

There, the Court held that a bank’s

efforts to work with the borrower

to modify a construction loan could

have created a duty of care that, if

breached, would support a negligence

claim. The Court noted both federal

and state statutes demonstrating “a

rising trend to require lenders to deal

reasonably with borrowers in default

to try to effectuate a workable loan

modification,” and, while not relying

on any of these statutes directly,

found they nonetheless “affect[ed]

the assessment” of whether the loan

servicer owed the borrower a duty.

Ultimately the Court found there was

a triable issue with respect to whether

the servicer owed a duty of care.

Jolley’s holding, however, was

then quickly reined by both federal

and other California appellate courts.

In Lueras v. BAC Home Loans Servicing,

LP,4 for example, which was decided

eight months after Jolley, the Fourth

District Court of Appeal declined

to impose a duty of care, finding

that “a loan modification is the

renegotiation of loan terms, which

falls squarely within the scope of a

lending institution’s conventional role

as a lender of money.” Lueras was

followed by numerous federal courts

in dismissing common-law negligence

claims against loan servicers.5

In Alvarez, the First District has

regained some of its lost ground.

The Court acknowledged Lueras,

but elected to follow a 2010 federal

decision instead6 that applied a six-

factor test to determine whether

a duty should be imposed for

“negligent” modification reviews. The

Court further cited to a 2009 article on

“Understanding the Financial Crisis” to

conclude that “servicers may actually

have positive incentives to misinform

and under-inform borrowers…to

save money on customer service”

and “increase the chances they will

be able to collect late fees and other

penalties.” Based in part on these

assumptions, the Court held that

borrowers’ “lack of bargaining power

coupled with conflicts of interest that

exist in the modern loan servicing

industry provide a moral imperative

that those with the controlling hand

be required to exercise reasonable

care in their dealings with borrowers

seeking a modification.”

The Alvarez decision, which is

fairly recent, has not yet been cited

in any published California appellate

decisions, and has only been cited

in a handful of federal opinions. Of

these federal opinions, some have

found ways to distinguish it,7 but the

CONTINUED ON PAGE 31

Legal

CALIFORNIA MORTGAGE FINANCE NEWS 15

Residential

Foreclosing a Junior Deed of TrustHow Will the Court Treat the Senior Deed of Trust When the Same Creditor Held Both the Senior and the Junior?

BY MATTHEW E. PODMENIK, MANAGING PARTNER, McCARTHY HOLTHUS, LLP

It is nearly

impossible to

assess the effect

that foreclosure of

a creditor’s junior

deed of trust will

have on the same

creditor’s senior deed of trust without

involving an analysis of some or all of

the following legal terms: merger of

title; merger of rights; the full credit

bid rule; anti-deficiency; the security

first rule; and maybe even dragnet

clauses. Until the Supreme Court hears

a case on this exact issue, we are left

to guess which doctrine will be used

by the lower courts.

Recently, the Second Appellate

District issued a ruling answering the

question posed in this article’s title by

applying the full credit bid rule and

prohibiting the creditor from collecting

on either the senior or junior deeds of

trust. See Najah v. Scottsdale Ins. Co.,

230 Cal.App.4th 125 (Cal. App. 2nd

Dist. 2014).

In Najah, property was owned

by Orange Crest Realty Corporation

subject to two deeds of trust; the

beneficiary of the senior was the

Lantzman Trust, and Najah was

the beneficiary of the junior deed

of trust in the original amount of

$2,550,000.00. When the Trust

instituted a non-judicial foreclosure on

the first deed of trust, Najah purchased

their note for $1,749,000 and received

an assignment of all interests in the

CONTINUED ON PAGE 32

With more than 150 lawyers in Washington, DC, Los Angeles, New York, Chicago, and London, BuckleySandler provides best-in-class legal counsel to meet the challenges of its financial services industry and other corporate and individual clients across the full range of government enforcement actions, complex and class action litigation, and transactional, regulatory, and public policy issues. The Firm represents many of the nation’s leading financial services institutions.

Washington, DC Los Angeles New York Chicago Londonwww.buckleysandler.com | www.infobytesblog.com

“The best at what they do in the country.”– Chambers USA

Legal

FALL 201416

Residential

Nevada HOA Decision Catches Eye of IndustryBY JONATHAN D. JAFFE, PARTNER, K&L GATES, LLP

A Nevada Supreme

Court opinion,

issued in September

2014, has brought

renewed focus on

the perils of making

loans on properties

subject to “super priority” homeowner

association (“HOA”) assessment liens.1

To give some perspective, this

case involved an HOA‘s foreclosure

of its $6,000 lien, which wiped out

an $880,000 first deed of trust held by

a bank (the “Bank”). While this case

involved Nevada law, it has potentially

much wider application, as there are

a number of states with HOA super

priority lien statutes.2

Background

SFR Investments Pool 1, LLC. v. U.S.

Bank, N.A. (“SFR v. U.S. Bank”) involved

a lien for unpaid HOA dues on an

individual homeowner’s property in

Nevada. The applicable Nevada statute3

provided that the lien was “prior to all

other liens and encumbrances” on the

homeowner’s property. The court was

asked to decide whether the HOA lien

was a true priority lien, such that a

foreclosure of the lien would extinguish

a first deed of trust on the property. The

court held that the HOA’s nonjudicial

foreclose extinguished the Bank’s first

deed of trust.

The dispute involved a residence

in a common-interest community.4 The

property was subject to Covenants,

Conditions, and Restrictions (“CC&Rs”)

that were recorded in 2000. In 2007, the

property was encumbered by a bank’s

(the “Bank”) first deed of trust. By 2010,

the former homeowners had defaulted

on both their HOA dues and their loan

obligations to the Bank. The HOA and the

Bank each initiated nonjudicial foreclosure

proceedings against the property.

The HOA’s trustee’s sale was held

on September 5, 2012 (before the Bank’s

sale, which was scheduled for December

19, 2012). SFR Investments Pool 1, LLC

(“SFR”) purchased the property at the

HOA’s trustee’s sale. Shortly before the

Bank’s scheduled foreclosure sale SFR

filed an action to quiet title and enjoin

that sale, alleging that the Bank had

nothing to foreclose on since the HOA

Trustee’s Deed extinguished the Bank’s

deed of trust.

Not only did the court side with the

HOA, but it held that the Nevada statute

did not permit a provision in the HOA’s

CCR’s that contractually subordinated

the HOA’s super priority lien to the

Bank’s first deed of trust.

How Did We Get Here?

Super priority lien laws have been

in place for decades. Most of these laws

are based on uniform laws, such as the

Uniform Condominium Act originally

published by the National Conference

of Commissioners on Uniform State

Laws in 1977 to bring uniformity to the

state condominium statutes. The UCA

was followed by the Uniform Planned

Community Act in 1980, and then the

Uniform Common Interest Ownership

Act promulgated in 1982 (and amended

in 1995). The scope of super priority

liens varies depending on which version

of these uniform laws a state adopted,

and whether the state adopted non-

uniform versions of the uniform law.5

So why is this only now becoming

a significant issue? The answer is tied, at

least in part, to the mortgage crisis. For

years HOAs could count on receiving

payment from the purchaser at a

lender’s foreclosure sale in a relatively

short time frame. So even though an

HOA could have taken advantage of

its super priority, it was willing to

wait. But when state legislators and

regulatory agencies started imposing

significant changes in the loss mitigation

and foreclosure processes, HOAs

found lenders sometimes taking 2,

3 or more years to foreclose. Rather

than waiting for lenders to foreclose,

HOAs initiated their own foreclosures.

Investors and speculators were able to

pick up properties at these sales for a

small fraction of their value, and quickly

recouped their investments by renting

the properties to tenants.6

What Can a Lender or Servicer Do to

Avoid This?

Can lenders and servicers take

CONTINUED ON PAGE 33

Legal

CALIFORNIA MORTGAGE FINANCE NEWS 17

New CA Statute Aims to ClarifyBorrower Intentions & Ensure Lien Releases in HELOC Payoffs

BY STUART B. WOLFE, PARTNER, WOLFE & WYMAN LLP

A new California

statue taking effect

in 2015 resolves a

practical deficiency

in California’s

current statutory

mortgage loan

payoff protocol as it applies to home

equity lines of credit (HELOCs)

and other consumer lines of credit

secured by a borrower’s residence—

namely, discerning intended

paydowns from payoffs.

California’s Existing Statutory

Payoff Scheme

Presently, California has a straight-

forward and sensible protocol for

borrowers and certain others to obtain

payoff demand statements from

existing lenders and secure a timely

lien release following a responsive

tender. (Civ. C. § 2943) For traditional

mortgages, the protocol increases

transactional efficiencies and reduces

disputes in refinance and sale escrows.

Generally, it provides a formal

process for borrowers, property

buyers, new lenders, and certain other

interested stakeholders, and their

respective agents, to request a payoff

demand statement from a borrower’s

secured creditors and requires the

creditors to respond to such requests

with a payoff demand statement

within 21 days. (Civ. C. § 2943) If the

creditor receives full payment during

the effective period of the payoff

demand statement, it has 21 days to

instruct the trustee of the deed of trust

securing the obligation to release the

lien. (Civ. C. § 2941(b)(1)) Thereafter,

the trustee has 30 days to honor the

instruction by executing and recording

a full reconveyance of deed of trust.

(Civ. C. § 2941(b)(1)(A))

Section 2943’s Deficiency: HELOC

Cancellations

As comprehensive and successful

as the existing statutory payoff

scheme is, it does not provide

assistance with certain practical

realities created by secured revolving

credit facilities, including HELOCs.

HELOC loan agreements provide

borrowers with the ability to draw

down and repay all or a portion of

a credit limit at-will. In order for a

borrower to terminate the credit

facility, HELOCs typically require the

borrower to provide the creditor with

(1) an express written cancellation

notice and (2) a tender of the

current balance. Such a cancellation

notice allows a HELOC creditor to

differentiate between a borrower’s

intent to payoff the credit facility from

merely paying down the balance. This

is significant because the former serves

to terminate the HELOC while the

later keeps it open and available for

future draws by the borrower.

One typical example of where

problems develop under the current

statutory scheme is where a HELOC

creditor receives a request for a payoff

demand statement and a full-balance

tender consistent with a responsive

payoff demand statement, but does

not receive a written cancellation

notice. Without the contractually

required cancellation notice, creditors

often assume the tender is merely

a pay-down, not a payoff and

cancellation. (Such an assumption

is consistent with the reality that

sometimes borrowers request payoff

demand statements as an exploratory

exercise and/or pending refinance or

sale escrows are sometimes aborted

or otherwise fail.) Thereafter, the

refinance or sale escrow successfully

closes, but either before or after the

closing, the borrower makes new

draws on the HELOC. Naturally, such

a set of events almost always results

in a priority dispute between the new

lender and/or owner, on the one hand,

and the pre-existing HELOC creditor,

on the other hand. It also creates

potential exposure for the escrow

agent and new title insurer.

Legislative Solution: AB 1770

Assembly Bill 1770 aims to resolve

this issue and creates Civil Code

section 2943.1.

The bill provides a statutory

mechanism to (1) suspend further

CONTINUED ON PAGE 35

Residential

Legal

FALL 201418

The Full Credit BidAvoiding (Expensive) Unintended Consequences

BY SCOTT D. ROGERS, PARTNER, & THEODORE K. KLAASSEN, SENIOR COUNSEL, RUTAN & TUCKER

Foreclosing real estate lenders are

often surprised to learn that their “full

credit bid” at a trustee’s foreclosure

sale has had expensive unintended

consequences. In the recent California

case of Najah v. Scottsdale Insurance

Company, 230 Cal.App.4th 125 (2014),

a full credit bid prevented the lender

from recovering insurance proceeds for

pre-foreclosure damage to the security

property. To avoid this and other

unintended consequences, lenders

are well-advised to understand the

legal import of a full credit bid and to

develop a comprehensive bid strategy

in advance of the trustee’s sale.

Under California law, a foreclosing

lender is permitted to credit bid at the

foreclosure sale any amount due to the

lender with respect to the defaulted

loan. This avoids the inconvenience of

a foreclosing lender having to pay cash

at the foreclosure sale only to have the

money delivered back to the lender.

The amount credit bid is treated the

same as if the lender had bid and

paid cash. A “full credit bid” occurs

when a lender credit bids the sum of

all amounts owed to the lender at the

time of sale, typically including all

unpaid principal, accrued interest, late

charges, advances, foreclosure costs,

legal fees and other sums due. As the

amount credit bid is treated the same

as cash, when a foreclosing lender

obtains title as the result of a full credit

bid, the indebtedness to the lender is

generally deemed to have been paid in

full—the “full credit bid rule.”

In the Najah case, Najah and

Akhavain (together, Najah) sold a

commercial property to Orange Crest

Realty Corporation (Orange Crest)

taking back a second deed of trust

to secure $2,550,000 of the purchase

price. After Orange Crest defaulted

under both deeds of trust, Najah

purchased the senior debt and deed

of trust, presumably to avoid having

their second deed of trust wiped out

if the first lienholder foreclosed. Najah

then instituted foreclosure proceedings

under the second deed of trust and

reacquired title to the property by

making a full credit bid of the amounts

owed under the second deed of trust

($2,878,000) at the trustee’s sale.

After getting the property back

through the trustee’s sale, Najah

brought suit against Scottsdale

Insurance Company (Scottsdale) to

collect under a commercial general

liability insurance policy issued to

Orange Crest covering the property

and naming both the senior lender and

Najah as insured mortgage holders.

Prior to the foreclosure sale, the

property had been vandalized and

many of its fixtures removed by the

principal owner of Orange Crest. The

estimated cost to repair the property

exceeded $500,000, which Najah

hoped to recover from Scottsdale.

When Scottsdale would not pay

Najah’s claim, Najah sued, and the

trial court ruled in favor of Scottsdale

and denied Najah any recovery. Najah

appealed, and the appellate court

affirmed the trial court’s judgment in

favor of Scottsdale. The appellate court

held that Najah’s full credit bid at the

foreclosure sale under the second deed

of trust precluded Najah from making a

claim on the proceeds of the Scottsdale

insurance policy. The appellate court

found that the amount payable to

Najah under the insurance policy was

limited to the amount necessary to

satisfy the debt and that because the

debt was fully satisfied through the full

credit bid, Najah had no further claim

on any insurance proceeds.

According to the appellate court,

the purpose of requiring the trustee’s

sale to be a public auction is to resolve

the question of value of the foreclosed

property through competitive bidding

at a public sale. This gives any

member of the public an opportunity

to participate in setting the value for

the property. This public value setting

provides some degree of market

protection (and transparency) for those

CONTINUED ON PAGE 36

Commercial

Legal

CALIFORNIA MORTGAGE FINANCE NEWS 19

New Markets Tax Credits

Financing OpportunitiesBY BRIAN L. HOLMAN, PARTNER, & ROBERT M. ZELLER, PARTNER, MUSICK PEELER & GARRETT LLP

Mortgage Bankers looking for a

new source of financing for projects

located in low and moderate

income communities may want to

inquire whether financing may be

available through participation in

the federal New Markets Tax Credit

(NMTC) program. Projects that

may qualify for such loans include

educational facilities, commercial

offices and retail centers, mixed use

(commercial/residential) properties,

community centers, entertainment /

cultural facilities, and health-related

facilities. This article describes the

NMTC program and how an NMTC

transaction may assist in funding the

acquisition and development of a real

estate project in a low or moderate

income community.

What is the New Markets Tax Credit?

The New Markets Tax Credit

program is intended to spur

investment of private capital into

a range of privately-managed

investment vehicles that make loans

and equity investments in businesses

operating in low- or moderate-income

areas. By making an equity investment

in a subsidiary of an eligible

“community development entity”

(“CDE”) which has been awarded an

allocation of New Market Tax Credits

Commercial

CONTINUED ON PAGE 37

Grow With Us!California Bureau of Real Estate #01174642, NMLS #79445

11234 El Camino Real San Diego, CA 92130 (800)865-6266 www.rwmloans.com [email protected]

ABILITY TO BROKER DIFFICULT LOANS

SEEKING STRATEGIC PARTNERS & MLO’S

ROBUST RETAIL MORTGAGE BANKING PLATFORM

Of Continued Excellence

Celebrating

DEDICATED GOVERNMENT LOAN CENTER

1994-2014

UPHOLDING INTEGRITY, EXPERIENCE & EXPERTISE

FALL 201420

EXECUTIVE DIRECTOR CONTINUES FROM PAGE 5

Look to Kinecta – Standing strong for over 70 years.

NMLS (Nationwide Mortgage Licensing System) ID: 407870. Information is intended for Mortgage Professionals only and not intended for consumer use as defined by Section 1026.2 of Regulation Z, which implements the Truth-In-Lending Act. The guidelines are subject to change without notice and are subject to Kinecta Federal Credit Union underwriting guidelines and all applicable federal and state rules and regulations. Kinecta Federal Credit Union is an FHA Approved Lending Institution, and is not acting on behalf of or at the direction of HUD/FHA or the federal government. Availability of some loan products may vary in some states/counties and loan limits may apply. Certain loans available to $3.5MM on exception. 14568-05/14

Kinecta Federal Credit Union – a 70-year tradition providing a range of loan products and a dedication to service.

800.854.4600 l www.LoanKinection.com l coast to coast

The mortgage industry has been weathering stormy waters in recent times. Many lenders have significantly reduced their product offerings… some have even abandoned ship. You need a partner that you can count on to stay the course.

Kinecta has been standing strong since 1940 and is one of the nation’s largest credit unions. Our solid financial foundation allows us to provide a full array of mortgages to our broker partners. Ranging from conventional, government, jumbo, and even niche product offerings, Kinecta gives you options that will help you find the right mortgage solution for clients.

• 1st and 2nd Combo Loans up to 89.9% CLTV

• MI-insured Jumbo ARM – 90% LTV & up to $250,000 over FHFA limits

• Loans up to $2 million

• Wholesale & Correspondent (Non-Delegated)

• Minimal agency overlays

point for the association, whether

it is in the form of a conference,

webinar, or article. One of the major

elements of our mission continues

to be the dissemination of critical

industry information being provided

by leading experts and nationally

recognized professionals.

As we bring 2014 to a close, I

invite you to stay tuned for what’s

in store for the California MBA in

2015 and beyond! You will see some

exciting changes and additions that

will take us into our next decade of

service to the industry. If the mortgage

industry has been one in which you’ve

built your career then I invite you to

join your colleagues as well as those

who’ve blazed the trail for you along

the way, and be an active part of this

association. Support the organization

that supports you and your business!

•

FOLLOW CMBA ON

TWITTER!Make sure and follow CMBA

(@CAMortgBankers) on Twitter

to get the latest updates on

legislative, regulatory issues,

and conference and event info!

CALIFORNIA MORTGAGE FINANCE NEWS 21

convicted of knowingly recording or

filing a false or forged real property

instrument in any public office within

the state, the criminal court must

issue a written order that the false or

forged instrument be adjudged void

ab initio. The measure is designed to

help a homeowner or business who

has been victimized by false or forged

deeds by providing an alternative to

requiring the victim to go to civil court

for a ‘quiet title action’ at their own

expense. CMBA had concerns with

the original version of the bill because

it did not protect the rights of a good

faith transferee or obligee relative to

their interest in the real property and

their ability to enforce any obligation

incurred or secured by the underlying

property. CMBA worked with the

author of AB 1698 and the law

enforcement sponsors of the measure

to craft amendments resolving CMBA’s

concerns. The amendments provide

multiple notices to interested parties in

the real property regarding the actions

being taken by the criminal court and

provide the opportunity for those

parties to argue their position in court.

AB 2416—Employee Wage Liens on

Employer Property

On the Floor of the Senate.

AB 2416 would have allowed

an employee to place a lien for any

wages, other compensation, and related

penalties and damages owed to the

employee on the employer’s real and

LEGISLATIVE REPORT CONTINUES FROM PAGE 7

CONTINUED ON PAGE 23

December 8, 2014California MBA Legal Issues ConferenceWestin South Coast Plaza, Costa Mesa, CARegister Now at www.CMBA.com!

Breakfast Sponsor

Mobile App Sponsor

Breakfast Sponsor WiFi Sponsor

Gold Sponsor

Silver SponsorThe Compliance Group, Inc.; Dorsey & Whitney, LLP; Geraci Law Firm; Pfeifer & De La Mora, LLP; The StoneHill Group; Weiner Brodsky Kider PC

Media SponsorMortgage Compliance Magazine

December 11, 2014CMBA Networking Series Presents: CMBA HQ After HoursOffices of California MBA, Sacramento, CARegister Now at www.CMBA.com!

January 22, 2015CMBA Networking Series Presents: Pleasant Hill After HoursOffices of Property Sciences, Pleasant Hill, CARegister Now at www.CMBA.com!

DOWNLOAD THE CMBA EVENTS MOBILE APP!

For iOS and Android Devices:Search app stores for CMBA Events.

For All Other Web-Enabled Devices:Point your mobile browser to m.core-apps.com/cmba_events.

OR scan the below code!

CALENDAR

2014-2015 CalendarMark your calendars now!

FALL 201422

Your correspondent lending partner should understand your market, your business

challenges and how important it is to have an easy, effi cient process that you can rely on.

At Plaza Home Mortgage, we know what you’re up against and we offer a comprehensive

support system designed to make it easier for you to be successful.

Our dedicated team of industry veterans works diligently to not only deliver superior

customer service, but also to serve as trusted consultants throughout the entire loan sales

process. Our hands-on approach means that you have immediate access to one-on-one,

personal guidance, comprehensive training and a robust library of resources to ensure that

each loan is properly underwritten, funded, and meets all regulatory compliance.

Catering to the Business Needs of Correspondent Partners

With a range of competitive products and strategic advice, Plaza offers correspondent

partners support for their business, opportunities to grow their own platforms and the

option of doing business their way. Plaza’s full Correspondent program options include:

• Best effort

• Single loan mandatory

• Bulk mandatory

• Bulk bid tapes delivery also available

• Delegated underwriting

$1 million minimum net worth required. Mini-correspondent program also available.

Correspondent lending is just easier when…

You partner with a company that under-stands what’s at stake.

Wholesale Lending. Mini-Correspondent.

Correspondent. Reverse Mortgage.

www.plazahomemortgage.com

Plaza Home Mortgage, Inc. is an Equal Housing Opportunity Lender. This is not a commitment to lend. Information is intended for mortgage professionals only and not intended for public use or distribution. Terms and conditions of programs are subject to change at any time. Refer to Plaza’s underwriting and program guidelines for loan specifi c details and all eligibility requirements. © 2014 Plaza Home Mortgage, Inc. All rights reserved. Company NMLS #2113. 6/2014.

National Correspondent Full Page Ad.indd 1 7/30/2014 9:30:08 AM

CALIFORNIA MORTGAGE FINANCE NEWS 23

NEW MEMBERS

Welcome New MembersWelcome to the CMBA family!

CHERRYWOOD COMMERCIAL, LLCVictor DominguezDiamond Bar, CACommercial/Multi-Family Mortgage Banker

DEEPHAVEN MORTGAGE, LLCBrett J. HivelyCharlotte, NCResidential Mortgage Banker

THE PRIESTON GROUPLynette NelsonNovato, CAIndustry Professional Advisor

LEGISLATIVE REPORT CONTINUES FROM PAGE 21

personal property, including property

upon which the employee bestowed

labor. The amount of the lien includes

alleged unpaid wages or compensation,

penalties and damages available under

the Labor Code, interest at the same

rate as for prejudgment interest in this

state, and the costs of filing and service

of the lien. The lien attaches to all real

property owned by the employer at

the time of the filing of the notice of

lien, or that is subsequently acquired

by the employer, that is located in any

county in which the notice of lien is

recorded. The lien was originally a

super-lien, which was one of CMBA’s

main concerns with the bill, but the

super-lien provision was removed. The

lien, however, would still have applied

to unsecured loans and non-purchase

mortgage loans made on or after

January 1, 2016. In addition to removing

the super-lien provision, the author

exempted an employer’s principal

residence from coverage by the bill and

included a mechanism to enable an

employer to remove the wage lien in

certain circumstances. CMBA opposed

AB 2416, and it died in the Senate.

AB 1770—Termination of Equity

Lines of Credit

Chaptered by Secretary of State—

Chapter 206, Statutes of 2014.

AB 1770 creates a statutory

method for suspending and closing

a home equity line of credit by way

of a codified notice signed by the

borrower(s) and transmitted by an

entitled person (i.e. title company)

to the beneficiary (lender). CMBA

participated in extensive negotiations

with title industry representatives,

policy makers and legislative staff

to address CMBA concerns with

the original proposal and to reach

a compromise on the final version

of the bill that was signed into law.

This legislation is intended to reduce

litigation between lenders and title

companies that has been occurring

when lines of credit are not terminated

when real property changes

ownership. The bill also includes a

July 1, 2015 delayed effective date, a

July 1, 2019 sunset date for the statute,

and a statement that the beneficiary

may conclusively rely on the

borrower’s instruction to suspend and

close the equity line of credit provided

by the entitled person.

AB 2372—Property Taxation:

Change in Ownership

In the Senate Appropriations

Committee.

AB 2372 would have required

that when more than 90% or more

of the direct or indirect ownership

interests in a legal entity are

cumulatively transferred in one

or more transactions, the assessor

should reassess the property owned

by the legal entity as a change in

ownership, regardless of whether a

single individual acquires more than

50% of the ownership interest. The

bill specifically excluded from its

reassessment requirements publicly

traded entity stock sales. It also

specified that multiple transfers

of the same ownership interest be

counted only once in determining

whether cumulatively 90 percent

or more of the ownership interests

have transferred. AB 2372 applied to

ownership interest sales made on or

after January 1, 2015. CMBA and most

business groups did not oppose the

final version of the bill, and some, like

the California Chamber of Commerce

supported the bill as amended and

narrowed. Provisions initially of

concern to CMBA were amended

out of the final version of the bill.

Interestingly some of the consumer

tax groups that initially supported the

measure removed support or opposed

the final bill version because they did

not believe the tax provisions went

far enough on the split-roll issue. This

CONTINUED ON PAGE 24

FALL 201424

LEGISLATIVE REPORT CONTINUES FROM PAGE 23

controversy led to the bill dying in the

Senate Appropriations Committee.

AB 1513—Possession by

Declaration of Residential Property

Chaptered by Secretary of State—

Chapter 666, Statutes of 2014.

AB 1513 establishes a three

year pilot program until January 1,

2018 to facilitate removal of persons

unlawfully occupying residential

property that, pursuant to the

program, has been registered with and

verified by local law enforcement to

be vacant. The bill was sponsored by

the California Association of Realtors

and seeks to provide property owners

with an additional tool to enforce

criminal trespass laws in cities where

the so-called practice of “squatting”

by unauthorized occupants in

residential property poses a problem

to the community at large. The pilot

program applies to residential property

of one to four units, with the Cities of

Palmdale, Lancaster, and Ukiah named

as the initial cities to participate in the

program. The bill does not mandate

registration of a vacant property.

Originally the bill would have created

a felony crime for refusal to leave a

property that could have negatively

impacted servicers maintaining a

property presumed to be vacant, but

that language was removed after the

CMBA voiced concerns.

•

lenders are now working together to

provide more competitive terms. For

example, many senior lenders that

specialize in a certain product or loan

type are now partnering with junior

lenders to provide higher leverage to

get deals done.

By working with a lender or

combination of lenders with a specific

niche, mortgage brokers are better

positioned to receive quality service

and certainty of execution.

However, brokers should also be

cautious. Many new, inexperienced

lenders have entered the marketplace

in search of yield. The returns from

hard money lending are higher than the

returns these new lenders could achieve

by investing in properties. The fact is,

with sub 5 percent cap rates in many

primary markets, it is more profitable to

lend capital than it is to invest it. Many

of these new lenders have never lent

money before, and don’t have the same

experience and expertise as seasoned

companies. For this reason, it’s extremely

important for brokers and borrowers to

be diligent when seeking a new lender.

With so many new lenders

offering low rates and high leverage in

a specific niche, it’s vital that mortgage

professionals conduct careful due

diligence to find established lenders

who have a strong track record

in providing speed, service, and

assurance that their loan will close.

Creative Office Space is Hot,

Residential Investment is Cooling Off

In the current market, value-add

and development opportunities are

still in favor, while smaller residential

flips are becoming less common.

Specifically, creative office space is

increasingly becoming the hot product

type, especially as millennials become

more dominant in the workforce. As

a result of this increased demand,

commercial lenders are finding new

opportunities to expand their client

base and increase deal flow.

Alternatively, there is less

opportunity in residential investment

than in previous years. There is

significant activity in the high-end

home market, but many investors

are beginning to feel that the profit

margins may be narrowing. Mortgage

professionals should prepare themselves

now for a time when residential flips

will become less desirable for investors.

New Markets Emerging and

Development Activity Increasing

While foreign investors continue

to flock to primary markets such as Los

Angeles and San Francisco where they

are rapidly acquiring high-end homes

and multifamily product, many other

investors are looking for new options.

There is limited inventory of

quality product in primary markets

and cap rates have been compressed

to historic lows. Many investors are

migrating to secondary and tertiary

markets in search of yield.

In addition, construction and

development is stronger than ever. This

trend will continue as developers and

investors continue to have access to an

abundance of capital. Overall, developers

are extremely bullish right now. This

fact will make it very interesting to see

how the market reacts to all of the new

product being delivered in 2015.

•

COMMERCIAL NEWS CONTINUES FROM PAGE 9

CALIFORNIA MORTGAGE FINANCE NEWS 25

The CFPB Says...

With the AllRegs® Compliance Management System, you’ll be able to:

n Audit and ensure correct policies are in placen Deliver training on policiesn Archive and track historical policy practicesn Assess, test and train staff on policiesn Provide one system of record for all reports

What are youwaiting for?

Call (800) 848-4904

or visit us atwww.allregs.com.

© AllRegs 2014

You NeedA Compliance

Management System!

that, because they are in the “cloud,”

and accessible electronically through

privately controlled means (e.g.

private smart phones, tablets, home

computers), or otherwise outside

the immediate physical premises

and obvious control of the lender,

social media somehow exist in a

“Kings X” universe exempt from the

legal and regulatory restrictions and

accountability otherwise applicable

to a lender’s business activities. In

mortgage banking, these mistakes

most often show up in the form

of personal advertising on private

websites—which may not be

vetted by lenders and is often in

violation of applicable regulations—

or in embarrassing photographs,

videos, comments, “rants,” or other

communications mistakenly thought

to be “private,” but which reflect badly