Embed Size (px)

Citation preview

SESSION ID:

#RSAC

SDS1-F01

Cybersecurity Insurance: New Risks and New Challenges

Mark Weatherford

Chief Cybersecurity StrategistvArmour

@marktw

#RSAC

2

Organizations in the Asia-Pacific region were forecast to spend $230 billion to deal with cybersecurity breaches in 2014 — the highest amount for any region in the world.*

*International Data Corporation (IDC) and the National University of Singapore survey, as reported in Marsh’s “Cybercrime in Asia” 2014 report.

The cybersecurity market in the Asia Pacific region contributes 17.21 percent of the global market and will grow to 21.16 percent by 2019.*

*MicroMarketMonitor

#RSAC

3

Agenda

3

• Insurance challenges in the market today

• 10 reasons to invest in cyber insurance

• Cyber risk assessment tools and services

• 10 key coverage items

• So, why is insurance a catalyst for security?

• Predictions - the future of cybersecurity insurance

#RSAC

4

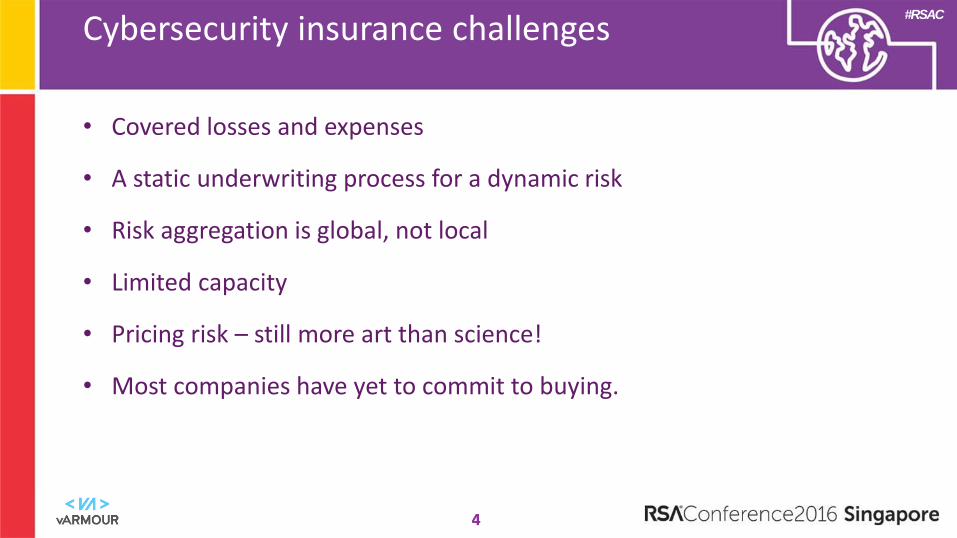

Cybersecurity insurance challenges

4

• Covered losses and expenses

• A static underwriting process for a dynamic risk

• Risk aggregation is global, not local

• Limited capacity

• Pricing risk – still more art than science!

• Most companies have yet to commit to buying.

#RSAC

Covered losses

5

• Two basic categories:

• First-party losses - direct losses to the company that was breached.

• Third-party losses - the costs imposed on related third parties such as partners, vendors, or customers, as a result of the breach.

#RSAC

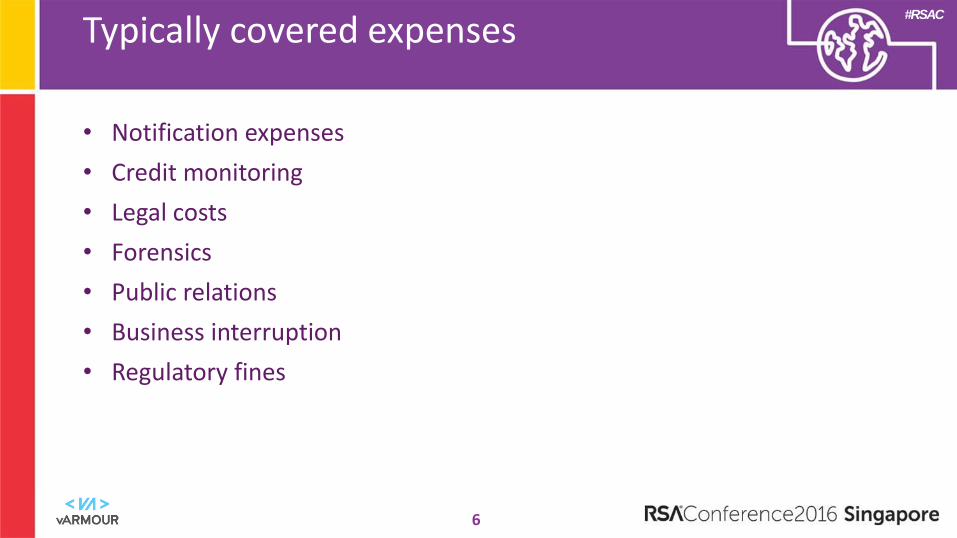

Typically covered expenses

6

• Notification expenses

• Credit monitoring

• Legal costs

• Forensics

• Public relations

• Business interruption

• Regulatory fines

#RSAC

7

Insurance is a traditionally static business

7

• Historically, insurance assessments have been based on a snapshot in time

through the completion of a written questionnaire, a telephone interview,

or a presentation.

• This static approach doesn’t work in the cybersecurity market, where the

threat and vulnerability landscape changes daily.

• Insurers today are investing in, and partnering with, the security industry

to develop and use risk tools and intelligence to predict and monitor the

environment in real time.

#RSAC

8

Aggregation of risk

8

• Aggregation refers to the consequences of concentrated and cascading

cyber risks where key aggregation attributes such as internet failure,

compromised service providers, or a number of companies in the same (or

different) sectors using the same IT system where something happens to

that system and affects all of the companies in that industry.

• As cloud computing becomes more ubiquitous, one successful attack or

the failure of a cloud host could cause losses to hundreds of thousands of

parties who hold their data within the cloud.

#RSAC

9

Limited capacity

9

• Capacity refers to the supply of insurance available to meet market demand and depends on the financial ability to accept risk. For an individual insurer, capacity is the maximum amount of risk it can underwrite based on its financial condition.

• The cybersecurity insurance market only dates back to 1998 so very little actuarial actuarial data exists, which means capacity is still growing. As the cyber insurance market capacity grows, more meaningful limits will develop as loss data accumulates and risk modeling matures.

• Asia accounts for about 28% of the global (total) insurance market today but premiums are expected to double by 2020.*

*Ms. Jacqueline Loh, Deputy Managing Director, Monetary Authority of Singapore

#RSAC

10

How do insurers price risk?

10

• A lack of sufficient metrics with respect to frequency and severity of loss, specifically with Personally Identifiable Information (PII) and Protected Health Information (PHI) assets, and physical destruction as a result of cyber events makes pricing risk a challenge.

• Fundamentally, insurers look for a strong security culture within the company as a first step in risk triage. Additional factors such as industry, revenue size, geography, and actual assets at risk contribute to how risk is priced.

The evolving nature of cyber-threats (DDoS, APT, Ransomware) and the IT environment (virtualization, the Internet of Things, and the Cloud),

compounds the problem of developing accurate actuarial data.

#RSAC

1212

1. Changing threat landscape

2. Governance and an enterprise-wide risk management strategy

3. Increasing regulatory risk

4. Financial incentive

5. Vicarious risk to vendors, business associates

6. Insider threat

7. Compliance does not equal security

8. Monetizing the cost of cybersecurity

9. M&A activity

10. Operational technology

10 reasons to invest in cyber insurance

#RSAC

13

10 reasons to invest in cyber insurance

13

1. Dynamic threat landscape and growing number of adversaries

Private sector companies are out-matched in their ability to combat cyber-attacks from nation states, global criminals and malicious insiders.

In no other arena are private companies expected to do battle with:

#RSAC

14

10 reasons to invest in cyber insurance

14

2. Governance and an enterprise-wide risk management strategy

Cybersecurity has become a significant concern for international Boards of Directors and they are increasingly looking at cybersecurity insurance as afinancial instrument for transferring risk.

Cybersecurity involves the entire enterprise, including stakeholder domains outside the IT department. Driving a culture of collaboration between stakeholders is challenging, but the underwriting process can be the catalyst for better security throughout the organization.

#RSAC

15

10 reasons to invest in cyber insurance

15

3. Increasing regulatory risk

Board of Director liability is resulting in new focus on cybersecurity governance on the international stage. In the United States, the Security & Exchange Commission guidance highlights that regulators see cybersecurity insurance as part of a strong enterprise risk management strategy.

Between 2010 and 2015, the number of jurisdictions with comprehensive “European-style” data protection regulatory regimes more than doubled from five to eleven, with new regimes coming into force in India, Malaysia, the Philippines, Singapore, South Korea and Taiwan.*

* http://www.conventuslaw.com/report/2016-data-protection-and-cyber-security-regulation/

#RSAC

16

10 reasons to invest in cyber insurance

16

4. Incentives

Government officials are beginning to give greater legitimacy to the role of cybersecurity insurance.

There is growing support for market-based incentives such as insurance, that reward strong cybersecurity programs with discounted premiums and broader coverage.

The lack of robust actuarial data to model risk, and a changing underwriting process that validates the dynamic threat environment is a growing priority for the insurance industry.

#RSAC

17

10 reasons to invest in cyber insurance

17

5. Interdependencies and third party risk

Adversaries are increasingly focused on third parties such as Managed Service Providers, off-premise maintenance, and even cloud services that have access to sensitive information and other critical assets of the target enterprise.

Liability for PII or PHI typically still rests with the enterprise data owner, even though a breach may have occurred at, or been the fault of, the third party.

#RSAC

18

10 reasons to invest in cyber insurance

18

6. Insider threat

Attacks from inside the organization continue to be difficult to prevent. Cybersecurity insurance typically provides coverage when the employee is the perpetrator, just like when the attack is from the outside.

When asked who posed the biggest internal threat to corporate data, 55% of the

respondents to the 2015 Vormetric Insider Threat Report identified Privileged

Users, followed by contractors, service providers, and business partners.

#RSAC

19

10 reasons to invest in cyber insurance

19

7. Security Compliance

Treating security as a compliance issue distracts from real security and ultimately results in a false sense of security. Many companies have been in compliance with their required standards and still fell victim to a data breach or a security incident.

#RSAC

20

10 reasons to invest in cyber insurance

20

8. Monetizing the cost of cybersecurity

One of the biggest security leadership challenges continues to be the ability to quantify cybersecurity risk to the executive team in terms of dollars and cents – Return On Investment (ROI). The premium charged by an insurance company can help solve this problem, especially when implementation of security controls and policies reduces overall risk.

#RSAC

21

10 reasons to invest in cyber insurance

21

9. Merger and Acquisition (M&A) activity

The difficulty in evaluating the cybersecurity posture in any acquisition target leaves the acquirer vulnerable. A comprehensive due diligence risk assessment can go a long way in identifying threats and vulnerabilities that can satisfy the demands of cybersecurity insurance.

#RSAC

22

10 reasons to invest in cyber insurance

22

10. Operational technology

Industry sectors dependent on operational technology and industrial control systems are particularly vulnerable due to the often very distributed nature of the OT/ICS environment. Built primarily for 24/7/365 availability and to operate in remote and isolated environments, these systems and devices have historically been air-gapped but are increasingly being connected to the corporate information technology network and the Internet.

#RSAC

23

Cyber risk assessment tools and services

23

• A number of product and service companies have joined the market for automating the risk assessment process for cybersecurity insurance

• Underwriters are using (and developing) risk assessment products and services to require a higher level of risk maturity for potential customers

• Cybersecurity insurance customers are using risk assessment products and services to validate their maturity for underwriters and to drive down the cost of premiums

#RSAC

Considerations when negotiating a policy

25

• Exclusions: Make sure that nothing essential is excluded from the policy.

• Lack of awareness of limits and sub-limits: Pay attention to the sub-limits. A high policy limit is worthless if sub-limits restrict you from collecting on damages.

• Buying coverage you don’t need: Calculate and document your risks and your risk tolerance to justify your decisions, which may face future scrutiny in the event of third-party inspection.

• Expecting other types of insurance to cover losses: Either buy standalone cyber insurance or review existing policies to determine overall coverage.

FireEye White Paper - Cyber Insurance: A Growing Imperative

#RSAC

26

“Exclusion”

26

An exclusion clause, i.e., “the fine print,” is a clause in an insurance contract that eliminates coverage for specified events.

It’s important that you understand what the restrictions are in the policy, including exclusion clauses, before you execute the contract.

EXAMPLE: The Company shall not be liable for Loss on account of any Claim based upon, arising from, or in consequence of any fact, circumstance, situation, transaction, event, act or omission of which any Insured had knowledge prior to the inception date of the first Liability

Insurance Policy issued and continuously renewed by the Company to the Parent Organization.

#RSAC

27

10 key coverage items

27

1. Full prior acts coverage

2. Restrict knowledge and notice of a circumstance to the executive team

3. Security warranty

4. Operational technology

5. Outside counsel

6. IT Forensics

7. Law enforcement

8. War and Terrorism

9. Intentional Act

10. Continuity of Coverage

#RSAC

28

Ten key coverage items

28

1. Full Prior Acts coverage

Insurers typically try to limit coverage to acts from the first day that the policy begins, known as the retroactive date. However, in the context of the challenges in detecting an attack, buyers should seek to remove this exclusion and avoid the risk of a claim denial.

#RSAC

29

Ten key coverage items

29

2. Restrict knowledge and notice of a circumstance to the executive team

An insurer should not be allowed to attribute liability to the whole enterprise because enterprise-wide detection has proven to be a challenge for most organizations.

#RSAC

30

Ten key coverage items

30

3. Security warranty

Remove any language that tries to warrant that security is maintained to the same level as represented in the underwriting submission. The dynamic nature of the risk leaves this too open to insurer interpretation in the event of a loss.

#RSAC

31

Ten key coverage items

31

4. Operational technology

The majority of insurance policies provide coverage only to the corporate IT network. If relevant, ensure that language is broadened to also address operational technology such as SCADA and industrial control systems.

#RSAC

32

Ten key coverage items

32

5. Outside counsel

Choice of counsel must be agreed upon at the outset. In the event of a security breach, a dedicated legal expert must take the response lead, including attorney client privilege. Negotiating with an insurer during a security incident is a very bad idea.

#RSAC

33

Ten key coverage items

33

6. IT Forensics

Similarly to choice of counsel, the preferred forensics firm should be agreed upon up front and the decision should not be left to the underwriter. Incident response and forensics can be very expensive and and a significant part of the overall incident cost.

#RSAC

34

Ten key coverage items

34

7. Law enforcement

Law enforcement is typically involved in major security breaches and oftentimes the first time a company knows they’ve been a victim is when the law enforcement knocks on the door. A claim should not be excluded by an insurer for “failure to disclose as soon as practicable” if law enforcement had advised nondisclosure during the investigation.

#RSAC

35

Ten key coverage items

35

8. War and Terrorism

Many insurance policies exclude coverage for acts of war such as invasion, insurrection, revolution, military coup and terrorism. With the emergence and growth of nation state adversaries and international terrorism, this clause should be eliminated from any insurance contract.

#RSAC

36

Ten key coverage items

36

9. Intentional Act

Coverage that addresses the employee or insider as perpetrator acting in isolation of the executive team.

#RSAC

37

Ten key coverage items

37

10. Continuity of Coverage

When renewing the insurance policy with the same insurer, you should always avoid signing a warranty regarding a circumstance or claim.

#RSAC

38

So, why is insurance a catalyst for security?

38

• Shareholders expectations are rising

• CEO’s are paying attention

• Boards don’t understand security and are nervous

• Regulators are enforcing compliance

• Government wants to legislate

• Underwriters are incentivizing better security behavior

• The cloud is providing new technical solutions

#RSAC

39

The future of cybersecurity insurance

39

• Continuous monitoring and risk scoring will be the new norm. This is the process of maintaining real time awareness of security threats and vulnerabilities that support organizational risk management decisions.

• Premiums and rates will vary monthly, weekly, daily, and hourly based on dynamic threat and vulnerability environment

• Underwriters will establish new relationships with security product vendors to incentivize spending

#RSAC

Brokers are your new best friend

40

The role of a broker:

1. Helps document the current organizational security posture - strengths and weaknesses.

2. Helps with the application and the underwriter interview process to present the best possible case.

3. Helps choose an underwriter and negotiates the best policy.

FireEye White Paper - Cyber Insurance: A Growing Imperative

#RSAC

41

To understand what is covered in any cybersecurity policy, remember the most

important three rules of insurance:

1. READ THE POLICY!

2. READ THE POLICY!

3. READ THE POLICY!

#RSAC

42

Apply what we’ve discussed today

42

• Next week you should ask about and review your corporate cybersecurity insurance policy (if you have one)

• In the next three months you should:

• Review your most recent enterprise risk assessment

• Discuss your corporate cyber risk appetite with CEO and CRO

• Meet with your insurance broker to discuss your cybersecurity insurance policy

• In the next six months you should begin budgeting and scheduling an enterprise risk assessment and considering potential tools or services to automate and provide visibility into your risk environment.

#RSAC

Thank YouMark Weatherfordmark@varmour+1.916.200.8801

![STIX Patterning: Viva la revolución! · ersion\\Run\\CryptoLocker_0388'] ... $hex_string and filesize > 31284} #RSAC ... Con't. #RSAC. HTTP Network Traffic with User Agent](https://img.pdfslide.us/doc/110x75/5b1d14747f8b9a0b2c8bad8d/stix-patterning-viva-la-revolucion-ersionruncryptolocker0388-hexstring.jpg)