Embed Size (px)

Citation preview

www.sdblaw.co.za

PROCESS INFORMATION BOOKLET

CONVEYANCING

Seymore Du Toit & Basson is commi�ed to serve the best interests of our clients. Established in 1990, the firm specialises in civil li�ga�on, collec�ons, commercial law, conveyancing and bond registra�ons.

The firm has seen exponen�al growth in the past five years. With offices in Nelspruit, Witbank and Lydenburg, we are four partners and employ one consultant, four associates, five professional assistants, five candidate a�orneys and thirty two secretarial staff. And our correspondents allow us to serve both Mpumalanga and Limpopo Provinces effec�vely and efficiently.

Seymore Du Toit & Basson holds to a strict code of professional ethics. We strive to offer the best legal service to our client cons�tuency. Each member of the firm prides themselves on their dedica�on to deliver the same quality service to all clients, big or small, private or corporate, and the same a�en�on to detail in all legal ma�ers.

Seymore Du Toit & Basson is one of the most experienced property law firms in Mpumalanga with the emphasis on efficiency and reliability.

We offer:

Ÿ Accurate and speedy processing of your transfer or bond registra�on

Ÿ State-of-the-art technology developed to enhance communica�on and service delivery

Ÿ Instant no�fica�on and updates on the progress of your transfer or bond via SMS and email

Ÿ The opportunity to track the progress of your transac�on online

In short, at Seymore Du Toit & Basson we emphasize a�en�on to detail, reliability and the personal touch. Please visit our offices for a cup of coffee to meet us in person. However, we are also willing to come to you, should this prove more convenient.

www.sdblaw.co.za

CONTENTS

Ÿ What is regarded as property? ............................................................

Ÿ Ownership: Residents and non-residents

Ÿ Buying a property ................................................................................

Ÿ Transfer procedure ..............................................................................

Ÿ Costs: Seller .........................................................................................

Ÿ Costs: Purchaser ..................................................................................

Ÿ Signing of documents ..........................................................................

Ÿ The offer to purchase ..........................................................................

Ÿ Purchase price

Ÿ Occupa�on, possession, transfer and occupa�onal interest

Ÿ Voetstoots

Ÿ Electrical and beetle-free cer�ficates

Ÿ Gas and electric fence cer�ficates

Ÿ Fixtures & fi�ngs

Ÿ Fulfilment of suspensive condi�ons

Ÿ FICA .....................................................................................................

Ÿ Capital Gains Tax .................................................................................

Ÿ Non-residents and property ownership ..............................................

Ÿ Withholding tax

Ÿ Are there any restric�ons on non-residents buying property in

SA?

Ÿ How can foreign funds be brought into SA for property

acquisi�on?

Ÿ Can money be borrowed in SA by non-residents to purchase

property?

Ÿ Can a non-resident open a bank account in SA?

Ÿ Can the money be taken out of the country a�er sale of the

property?

Ÿ Is a non-resident liable for payment of any SA income tax?

Ÿ A�er registra�on .................................................................................

Ÿ Levy clearances (applicable to Home Owners’ Associa�ons and Body

Corporates)

Ÿ Latent and patent defects

Ÿ Transfer & Bond costs ..........................................................................

1

2

3

5

6

9

10

12

14

15

18

19

CONVEYANCING PROCESS INFORMATION BOOKLET

WHAT IS REGARDED AS PROPERTY?

OWNERSHIP:

Property includes:

Ÿ Land and fixturesŸ Real rights in land (such as use rights), but excluding rights under

mortgage bonds or leasesŸ Mineral rights or rights to mine for mineralsŸ A share or interest in a “residen�al property company” (i.e., a company

or Close Corpora�on where the only asset or majority asset is a residen�al house)

Ÿ A con�ngent right to residen�al property or share or member's interest in a “residen�al property company” held by a discre�onary trust where the acquisi�on of the right is:Ÿ in consequence of an agreement for considera�on in rela�on to

property held by that trust;Ÿ accompanied by a charge in the debt or security structure of the trust

or accompanied by a charge in the trust's trustees; or Ÿ shares in a share block company.

RESIDENTS NON-RESIDENTSIn South African law property may be owned individually, jointly in undivided shares or by an en�ty such as a company, close corpora�on, trust or similar, registered outside the country.

South Africa is reputed to have one of the best deeds registra�on systems in the world with an excep�onal degree of accuracy and security of tenure. Land registra�on is used to record ownership in one of the regionally located Deeds Registries where such documents are available for public viewing.

Non-residents may own property in South Africa, but illegal aliens are prohibited from owning immovable property.

There are, however, procedures and requirements to be complied with in certain circumstances.

This includes the local registra�on of en��es registered outside of South Africa where they purchase property in South Africa, and the appointment of a South African resident public officer for a local company whose shares are owned by a non-resident. Should a non-resident buy property in the country and intend to reside here for lengthy periods he/she will have to obtain a resident permit in compliance with the provisions of South African law.

1www.sdblaw.co.za

BUYING A PROPERTY

When buying a property it is important that both the buyer and the seller understand the terms of the sales agreement. It is the task of the estate agent to provide the necessary clarifica�on before the par�es sign the agreement.

Such agreement, usually �tled "Offer to Purchase" or "Agreement of Sale", must be legally binding. This requires that it be in wri�ng, contain a prerequisite set of informa�on, and be signed by both buyer and seller. An Offer to Purchase, once accepted, cons�tutes an Agreement of Sale.

An Agreement of Sale that has been signed by both buyer and seller becomes a binding contract.

It is an undertaking from which neither of the par�es may withdraw without facing legal consequences. There are, however, certain instances where withdrawal is possible:

Ÿ If certain condi�ons provided for in the agreement, are not fulfilled;

Ÿ If, in a case where the purchase price is less than R250 000, the buyer is allowed to cancel the transac�on a�er a "cooling" off period in terms of criteria allowed for by provisions in the Aliena�on of Land Act.

De facto ownership of property can also be obtained by acquiring the shares/members' interest and loan claims in a company/close corpora�on that owns a property.

Contracts of this nature, although legally binding, can be concluded verbally and need not be in wri�ng.

It is recommended, however, that the record of such agreements be kept in wri�ng to avoid the problems that might occur if the material terms of the agreement should come into dispute.

2CONVEYANCING PROCESS INFORMATION BOOKLET

TRANSFER PROCEDURE

The registra�on of a property transac�on is handled by a qualified legal prac��oner (a�orney) called a conveyancer.

The seller customarily appoints the conveyancer responsible for the registra�on of transfer of a property, while the costs incurred are paid by the purchaser - unless the contract s�pulates otherwise.

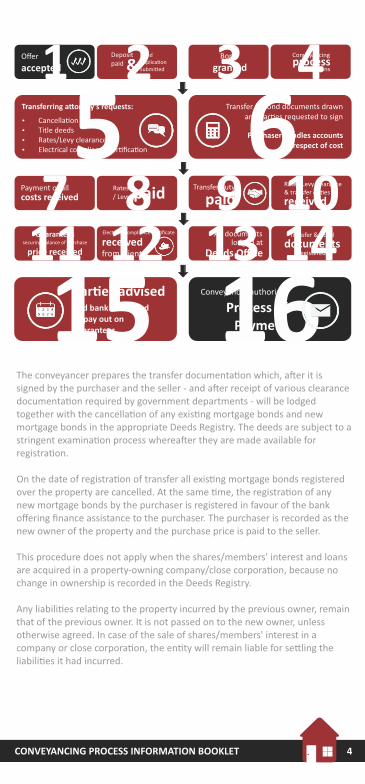

The transfer itself is best described as a process with 10 steps:

1. The a�orney receives instruc�on from the client (Agreement of Sale/Offer to Purchase).

2. The a�orney requests and receives FICA documents from both the seller and purchaser.

3. The a�orneys requests:

3.1 The seller's bond cancella�on figures;

3.2 The municipal clearance figures; and

3.3 The Body Corporate/Home Owners' Associa�on clearance figures, if applicable.

4. The a�orney dra�s the transfer documents.

5. Both the seller and purchaser sign the transfer documents.

6. The a�orney receives transfer costs from the purchaser.

7. The a�orney pays SARS transfer duty/VAT.

8. The a�orney pays the Home Owners' Associa�on (HOA) or Body Corporate and local municipality.

9. The a�orney receives a deposit and/or guarantees from the purchaser.

10. The a�orney receives:

10.1 The SARS transfer duty receipt and clearance; and

10.2 Cer�ficates from HOA/Body Corporate and the local municipality.

3www.sdblaw.co.za

1

711

5

15

6

16

2

812

3

913

4

1014

Transferring a�orney’s requests: Transfer & Bond documents drawnand par�es requested to sign

Conveyancer authorises

Purchaser handles accountsin respect of cost

Offer

accepted

Payment of all

Bond

granted

Transfer duty

All documents

Deposit paid

Rates/ Levy

Guaranteessecuring balance of purchase

price received

Conveyancing

Rates/Levy clearance& transfer du�es

Transfer & Bond

Bondapplica�onsubmi�ed

Electrical compliance cer�ficate

&

paid paid

process

received

documents

begins

registered

Ÿ Cancella�on figuresŸ Title deedsŸ Rates/Levy clearanceŸ Electrical compliance cer�fica�on

costs received

receivedfrom client

lodged at

Deeds Office

Par�es advised

The conveyancer prepares the transfer documenta�on which, a�er it is signed by the purchaser and the seller - and a�er receipt of various clearance documenta�on required by government departments - will be lodged together with the cancella�on of any exis�ng mortgage bonds and new mortgage bonds in the appropriate Deeds Registry. The deeds are subject to a stringent examina�on process wherea�er they are made available for registra�on.

On the date of registra�on of transfer all exis�ng mortgage bonds registered over the property are cancelled. At the same �me, the registra�on of any new mortgage bonds by the purchaser is registered in favour of the bank offering finance assistance to the purchaser. The purchaser is recorded as the new owner of the property and the purchase price is paid to the seller.

This procedure does not apply when the shares/members' interest and loans are acquired in a property-owning company/close corpora�on, because no change in ownership is recorded in the Deeds Registry.

Any liabili�es rela�ng to the property incurred by the previous owner, remain that of the previous owner. It is not passed on to the new owner, unless otherwise agreed. In case of the sale of shares/members' interest in a company or close corpora�on, the en�ty will remain liable for se�ling the liabili�es it had incurred.

and bank instructed to pay out onguarantees

Process ofPayment

4CONVEYANCING PROCESS INFORMATION BOOKLET

COSTS: SELLER

Did you

If an estate agent is used, so-called brokerage has to be paid. This is usually paid by the seller who appointed the estate agent.

In addi�on to brokerage, the following expenses are paid by the seller:

Ÿ An Electrical Compliance Cer�ficate (COC) for any electrical installa�ons on the property

Ÿ An Electrical Fence Compliance Cer�ficate if any electrical fences are installed on the property

Ÿ A Gas Compliance Cer�ficate if any gas operated appliances are on the property

Ÿ The se�lement amount to cancel the seller's current bond account (if applicable). The amount will be confirmed by the bank when the transferring a�orneys request cancella�on figures, once the bank has appointed their a�orneys to cancel the bond

Ÿ Bond Cancella�on Fees (if applicable). These are the fees charged by the bank-appointed a�orneys

Ÿ Any outstanding rates and taxes or levies owed to the municipality and/or Home Owners' Associa�on/Body Corporate, if applicable

You need to give 90 days no�ce on your bond. If not, your bank may hold you liable for penalty interest as prescribed by both the Na�onal Credit Act and Usury Act.

If your bond is cancelled before the 90 days no�ce is up, you will be liable for the early termina�on fee over the remaining no�ce period.

If your bond is not cancelled within 90 days, the bank will not debit an early termina�on fee except where it takes longer than 12 months to conclude. Then a new request to cancel will be required.

know?

5www.sdblaw.co.za

COSTS: PURCHASER

The purchaser is responsible for the payment of transfer costs and the costs of registering any new mortgage bonds for the property. These are o�en referred to as the “conveyancing fees”. The conveyancing fee is determined by the purchase price of the property and in accordance with a tariff guideline issued by the Law Society.

As men�oned before, either transfer duty or VAT is payable on a transfer of property. VAT takes preference over transfer duty. If the seller is registered for VAT as a vendor and the property forms part of his/her business venture, then VAT is payable. If the seller is not registered for VAT or the property does not form part of his/her taxable supplies, then transfer duty would be payable instead.

buying property in a new development, since the developer will generally be registered for VAT. But, where a VAT vendor sells his/her private residence, the residen�al property will be exempt from VAT and the sale will be subject to transfer duty instead.

Circumstances where VAT is payable (see above) o�en occur when

This is a tax levied by the Receiver of Revenue when a buyer acquires a property. It generally cons�tutes the major por�on of the costs involved and is payable by the buyer within six months of the date of purchase (acceptance of the offer by the previous owner). If not paid within this �me limit, interest will be charged. Transfer duty is levied on the value of any bought or donated property. Transfer duty is a once off payment before the transfer of the property. It is paid to the conveyancing a�orney, who will in turn pay SARS.

At present transfer duty rates are paid on proper�es with purchase agreements concluded on or a�er 23 February 2011.

It applies to all persons (including companies, close corpora�ons and trusts). Keep the following in mind:

Ÿ Proper�es with a purchase price up to R 600 000 have no transfer duty.

Ÿ You don't pay transfer duty on the first R 600 000, only on the por�on that exceeds this amount. The transfer duty is calculated at 3% on the value above R 600 000.

Ÿ From R 1 000 001 to R 1 500 000, transfer duty is calculated at 5% on the value above R 1 000 000 PLUS a flat rate of R 12 000.

Ÿ From R 1 500 001 upwards, transfer duty is calculated at 8% on the value above R1 500 000 PLUS a flat rate of R 37 000.

Transfer costs

VAT

Transfer duty

Transfer duty rates

6CONVEYANCING PROCESS INFORMATION BOOKLET

The fees payable to a conveyancer for registering the transfer of ownership are known as the “transfer fees”. The amount is determined on a sliding scale according to the purchase price of the property. The sliding scale is based on tariffs recommended by the Law Society. The fees may include VAT and are payable to the conveyancing a�orneys as a once-off before registra�on of transfer of the property into the name of the seller.

The transfer a�orneys charge a levy to take care of small expenses such as postage and secure delivery of documents, faxes, telephone calls and the like.

The Deeds Office charges a fee to register the transfer and record the new owner of the home. This is a fixed amount and it is determined by a sliding scale based on the purchase price.

In most instances, the contract will indicate that occupa�onal interest is payable if the buyer occupies the property before the transfer of the property into his name has been formally registered. The interest amount can either be fixed (usually calculated as either the amount of the seller's bond repayment on the property or 1% of the purchase price), or an amount subject to escala�on if the registra�on of transfer has not taken place within a predetermined �meframe.

Occupa�onal interest is payable in advance on a monthly basis as per the offer to purchase, alterna�vely to either the estate agent or the transfer a�orneys (who will pay the seller) or otherwise directly to the seller.

This fee is charged by the bank for the processing of the home loan applica�on. The buyer may expect to pay a base fee of approximately R5 700. This is paid on registra�on of the bond. It may be debited from the home loan account (and added to the outstanding balance), depending on the bank's internal rules.

Conveyancer's Fee for theTransfer

Postage and Small Expenses

Deeds Office Registra�on Fee

Occupa�onal Interest (Occupa�onal Rent)

Home Loan Ini�a�on Fee

7www.sdblaw.co.za

COSTS: PURCHASER (con�nued)

NOTE

This is charged by the bank to administer the home loan account. The buyer can expect to pay between R17 and R57 per month, depending on whether he/she has made use of the bank's in-house homeowners' insurance, in which case the fee will be less. The fee is payable on a monthly basis and will be debited from the home loan account.

If the bond applicant does not already have a life assurance policy as security for the loan, he/she may be required to take out a kind of home loan protec�on insurance which will most likely be a varia�on of any of the following protec�ons: death only; disability only; retrenchment only; death and disability; death and retrenchment; disability and retrenchment; or death, disability and retrenchment.

The bank will insist that the buyer take out homeowner's insurance to cover the risk of damage to the property that may result from natural disasters such as fire or storm.

The amount will vary depending on the value of the property. It is payable on a monthly basis and will most likely be debited from the home loan account. The bank will pass the amount on to the insurance company.

Disclaimer: The transfer duty and conveyancing tariffs detailed above are quoted from the Minister of Finance’s budget speech of February 2011, regarding the transfer duty rates, as well as the prescribed conveyancing tariffs. Other es�mated costs are only a guideline, and may vary in real �me.

Administra�on and ServiceFee

Home Loan Protec�on Insurance

Homeowner's Insurance

Depending on the home loan package, some of the costs men�oned above can be absorbed

into the mortgage bond. Speak to your banker or financial adviser for more informa�on and to verify these costs.

8CONVEYANCING PROCESS INFORMATION BOOKLET

COSTS: PURCHASER (con�nued)

SIGNING OFDOCUMENTS

Documenta�on prepared by the conveyancer for the registra�on of transfer and any mortgage bond to be registered must be signed in ink and blackauthen�cated if signed outside South Africa. The la�er is o�en inconvenient and �me consuming. For this reason it is advisable to leave a general power of a�orney (GPA) in favour of a trusted person in South Africa. However, keep in mind that no person is allowed to sign an affidavit on someone else's behalf, even if a GPA has been granted.

If the buyer got married abroad (i.e. according to the laws of a foreign country) and a mortgage bond has been applied for, or on the re-sale of the property, the spouse of the buyer must also sign the mortgage bond documenta�on or transfer documents.

The short answer is, yes. However, there are certain formali�es that must be complied with. Documents can either be signed before a Notary Public (in certain countries) or alterna�vely at the South African Embassy in that country. The process is unfortunately o�en costly and �me consuming.

As men�oned, if a seller or buyer is in South Africa at the �me of the transac�on but returning overseas shortly therea�er, it is advisable to sign a special or general power of a�orney (GPA) in favour of a local and trusted friend or family member who will then be able to act on his or her behalf. Remember, however, that affidavits cannot be signed by an authorised representa�ve on your behalf.

CAN TRANSFER AND/OR BOND DOCUMENTS BE SIGNED OVERSEAS AND IF SO, HOW?

9www.sdblaw.co.za

THE OFFER TO PURCHASE

The Offer to Purchase/Agreement of Sale will typically consist of the following:

A deposit is not mandatory but serves as a gesture of good faith on the part of the buyer and an indica�on of financial ability.

The deposit is invested by the estate agent or conveyancer in an interest-bearing trust account for the buyer. Both a�orneys and estate agents are protected by Fidelity Funds which guard against the� or negligence on the side of the agent or a�orney.

In the agreement there will be a request for a guarantee for the balance of the purchase price. Usually, a guarantee has to be issued by a local financial ins�tu�on. This means that, in the case of foreign buyers, the funds will have to be remi�ed to South Africa so that a local bank can issue such a guarantee.

Alterna�vely, arrangements must be made between a foreign and local bank for a so-called back-to-back guarantee. It is, however, also possible under certain circumstances to nego�ate this by means of a Standby Le�er of Credit from an overseas ins�tu�on.

“Occupa�on” is the physical occupa�on of the property whereas “possession” is the date on which the buyer assumes responsibility for the property. It is customary for the risk of ownership to pass on the date of possession, rather than occupa�on (if not the same). “Transfer” refers to the actual date of registra�on of ownership in the Deeds Registry in favour of the buyer.

“Occupa�onal interest” happens when the date of occupa�on and the date of transfer differs. It is the rent paid by the party occupying the property belonging to another. It is usually referred to as an amount (in Rand) or as a percentage of the outstanding balance of the purchase price.

Purchase price Occupa�on, possession, transfer and occupa�onalinterest

Did you know?

Both a�orneys and estate agents are

protected by Fidelity Funds which guard against the� or negligence on the side of the agent or a�orney.

10CONVEYANCING PROCESS INFORMATION BOOKLET

This is a standard inclusion in all deeds of sale. It means that the property is bought “as is”, that is, ”in the exact condi�on in which the property is found.” The Consumer Protec�on Act applies to sale agreements where the seller is a developer or similarly in the business of selling land. In such instances, the seller is obligated to provide the buyer with property that is free from defects, as defined in the Act.

The owner of the property has to provide a valid electrical compliance cer�ficate. It cer�fies that the electrical installa�on at the property meets statutory safety requirements.

Beetle-free cer�ficates only apply to proper�es in the Western Cape and KwaZulu-Natal and it is not included in the sale of sec�onal �tle units. The cer�ficate confirms that the property is free of beetle (defined) infesta�on. Note however that while it is a standard inclusion in the Agreement of Sale, it is not a legal requirement.

The cost of any repairs that might be necessary for the cer�ficates to be issued, is for the account of the seller, although the par�es can contractually agree otherwise.

If there is a gas appliance on the property a Gas Cer�ficate of Compliance is required. It confirms that the installa�on complies with statutory safety requirements. Such a cer�ficate is also a requirement where there is an electric fence installa�on on the property.

A property is sold together with all fixtures and fi�ngs of a permanent nature. Generally, fixtures and fi�ngs include anything which is a�ached to the property. To avoid any unpleasantness or uncertainty, the buyer is advised to ensure that all items intended to be included in the purchase price are specified in wri�ng in the Agreement of Sale.

Voetstoots

Electrical and beetle-free cer�ficates

Gas and electric fencecer�ficates

Fixtures and fi�ngs

11www.sdblaw.co.za

THE OFFER TO PURCHASE (con�nued)

FICA

Fulfilment of suspensive condi�ons

The most comprehensive legisla�on to counter money laundering is the South African Financial Intelligence Centre Act (FICA). FICA puts control obliga�ons in place to counter money laundering for banks and commercial ins�tu�ons, as well as professionals such as estate agents, brokers, a�orneys and insurance companies.

Customer iden�fica�on is a crucial element of any effec�ve money laundering control system and therefore a central feature of FICA.

12

THE OFFER TO PURCHASE (con�nued)

CONVEYANCING PROCESS INFORMATION BOOKLET

The Sale Agreement can contain prerequisites or so-called suspensive condi�ons. These are condi�ons which must be fulfilled before the transfer process can begin. The most common suspensive condi�on is the gran�ng of a bond to the buyer.

A bond is a loan to the buyer by a bank to enable him/her to pay the purchase price of the property, with the purchased property as security. If the buyer fails to make the bond repayments the bank is en�tled to sell the property to recover the money it has lent.

Another common suspensive condi�on is that the agreement is subject to the sale of the buyer’s property. This happens where the buyer is selling his/her property and needs the funds from the sale of that property to pay for the new property.

The seller, in this case, must realise that the transfer of the buyer's

property will have to precede or happen simultaneously with the transfer of the seller's property.

The conveyancers of the current sale will correspond closely with, and even get an undertaking from the conveyancers of the original property to transfer the proceeds of that sale on registra�on and thus expedite the process.

Agreements for the acquisi�on of shares/member's interest and loan accounts in property-owning companies/close corpora�ons contain many of the clauses discussed above. Such agreements are, however, substan�ally different from property sale agreements and include numerous warran�es and indemni�es that the seller gives to the buyer, as the la�er is acquiring the property-owning en�ty together with its financial history.

FICA (con�nued)

In this context, the transferring a�orney is required to request par�cular documents from both the seller and the buyer in order to comply with FICA.

Where applicable, the documents required are:

Completed informa�on

sheet

Completed informa�on

sheet

Completed informa�on

sheet

Completed informa�on

sheet

Commission invoice with

banking details

Commission invoice with

banking details

Commission invoice with

banking details

Commission invoice with

banking details

Mortgage bond account number

of seller

Mortgage bond account number

of seller

Mortgage bond account number

of seller

Mortgage bond account number

of seller

Par�culars of

bond originator

Par�culars of

bond originator

Par�culars of

bond originator

Par�culars of

bond originator

Copy of �tle deed

if available

Copy of �tle deed

if available

Copy of �tle deed

if available

Copy of �tle deed

if available

Iden�ty document

Iden�ty documents of trustees

Iden�ty documents of directors &

representa�ves

Iden�ty documents of members

Income tax

number

Income TAX and/or

VAT number of trust

Income TAX and/or VAT number of company

Income TAX and/or

VAT number of CC

Proof of

address

Proof of address of trust and

trustees

Proof of address of company

and directors

Proof of address of CC and members

Marriage cer�ficate

Le�ers of authority

COR39 (contents of

register of directors)

Ck1 / CK 2

Antenup�al contract TRUST DEED COR 14.1. (No�ce of incorpora�on)

COR 14.3. (Registra�on cer�ficate)

13www.sdblaw.co.za

Individual Trust Company Close Corpora�on

CAPITAL GAINSTAX

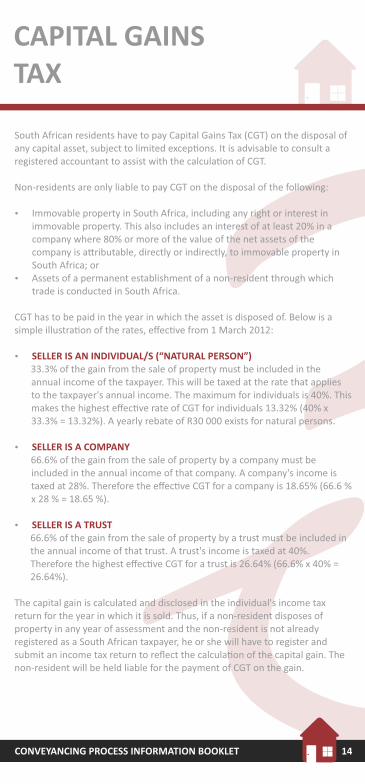

South African residents have to pay Capital Gains Tax (CGT) on the disposal of any capital asset, subject to limited excep�ons. It is advisable to consult a registered accountant to assist with the calcula�on of CGT.

Non-residents are only liable to pay CGT on the disposal of the following:

Ÿ Immovable property in South Africa, including any right or interest in immovable property. This also includes an interest of at least 20% in a company where 80% or more of the value of the net assets of the company is a�ributable, directly or indirectly, to immovable property in South Africa; or

Ÿ Assets of a permanent establishment of a non-resident through which trade is conducted in South Africa.

CGT has to be paid in the year in which the asset is disposed of. Below is a simple illustra�on of the rates, effec�ve from 1 March 2012:

Ÿ SELLER IS AN INDIVIDUAL/S (“NATURAL PERSON”)33.3% of the gain from the sale of property must be included in the annual income of the taxpayer. This will be taxed at the rate that applies to the taxpayer's annual income. The maximum for individuals is 40%. This makes the highest effec�ve rate of CGT for individuals 13.32% (40% x 33.3% = 13.32%). A yearly rebate of R30 000 exists for natural persons.

Ÿ SELLER IS A COMPANY66.6% of the gain from the sale of property by a company must be included in the annual income of that company. A company's income is taxed at 28%. Therefore the effec�ve CGT for a company is 18.65% (66.6 % x 28 % = 18.65 %).

Ÿ SELLER IS A TRUST66.6% of the gain from the sale of property by a trust must be included in the annual income of that trust. A trust's income is taxed at 40%. Therefore the highest effec�ve CGT for a trust is 26.64% (66.6% x 40% = 26.64%).

The capital gain is calculated and disclosed in the individual's income tax return for the year in which it is sold. Thus, if a non-resident disposes of property in any year of assessment and the non-resident is not already registered as a South African taxpayer, he or she will have to register and submit an income tax return to reflect the calcula�on of the capital gain. The non-resident will be held liable for the payment of CGT on the gain.

14CONVEYANCING PROCESS INFORMATION BOOKLET

NON-RESIDENTS ANDPROPERTY OWNERSHIP

Withholding tax

South African law requires that a percentage of the sale proceeds from non-resident sellers be withheld. In terms of this requirement, where a non-resident sells a property for more than R2 million, provisional CGT must be paid to SARS as follows:

Ÿ 5% by an individual (“natural”) non-resident sellerŸ 7.5% by a foreign company andŸ 10% by a foreign trust

? ?

15www.sdblaw.co.za

There no restric�ons except that illegal aliens are prohibited from owning property in South Africa. Non-residents are subject to the same laws and regula�ons as South Africans.

For the most part property is registered in the name of the buyer as an individual. However, should the non-resident prefer to buy in the name of an en�ty (e.g. a company or trust), the en�ty must be locally registered and meet the requirements (such as provided for in the Companies Act), applicable to registra�on of the par�cular type of en�ty. For example, funds brought into the country through a transac�on of this nature will represent a loan to the local en�ty and will require exchange control approval.

It is, of course, possible for a non-resident to purchase South African property over the internet without being present in the country. However, should the buyer intend to live in the property for any length of �me, he or she will be subject to the requirements of the Immigra�on Act, which would mean either being in possession of a permanent residency permit or obtaining a permit to temporarily remain in the country.

Foreign funds for the acquisi�on of property can be paid from abroad into any nominated bank account in South Africa. Usually this account is the trust account of the estate agent or transferring a�orneys, and the funds will be invested for the benefit of the NON-RESIDENT.

Since such trust accounts are regulated by the professional bodies that oversee the opera�ons of a�orneys and estate agents, the money is secure and guaranteed. In the case of money being deposited into an a�orney's trust account, the client will be required to sign an instruc�on form direc�ng the a�orney to invest the money and reques�ng interest to accrue to the client. In the absence of such an instruc�on, interest earned will accrue to the Law Society.

When a non-resident transfers funds from a foreign source into a South African bank account, a record known as a “Deal Receipt” is issued by the bank. This is an important document that must be retained for the purpose of possible repatria�on of the funds.

Are there any restric�ons on non-residents buying property in SA?

How can foreign funds bebrought into SA for propertyacquisi�on?

?

?

The South African Reserve Bank considers all foreigners without a domicile in South Africa to be non-residents. This does not include foreigners with South African work permits who are considered to be residents for the dura�on of their work permit.

Non-residents are restricted to borrowing an amount equal to the amount brought in from a foreign bank. A buyer who brings an amount of money into the country that is sufficient to cover the costs and transfer duty of the transac�on and 50% of the purchase price, is en�tled to borrow an amount that is more than 50% of the purchase price. In order to qualify for a South African mortgage bond, the non-resident will need to provide proof of earnings and comply with the provisions of the Financial Intelligence Centre Act (FICA). In terms of these provisions iden�fica�on of the non-resident is required to prevent money laundering. Such iden�fica�on involves the produc�on of documents such as a passport and proof of residen�al address.

A non-resident who has to make repayments on a mortgage bond, needs to open a non-resident bank account. This can only be done if the applicant is present in the country. In addi�on to an applica�on form detailing name, passport number and address, copies of the relevant pages of the applicant's passport, and proof of source of income such as a salary slip or pension statement, need to be submi�ed. All copies have to be cer�fied as copies of the originals. Once the bank account has been opened, foreign funds have to be deposited immediately.

In certain circumstances, for example rental income received from property belonging to the non-resident, local currency may be deposited into the account. The bank, however, has to be provided with a cer�fied copy of the rental agreement. This type of deposit, as well as any other South African deposit into the non-resident account, will require the approval of the Reserve Bank, since non-residents are not en�tled to generate income in South Africa other than interest/rental generated from the foreign funded capital asset. If property is sold in South Africa the money can also be deposited into the non-resident account, provided the necessary documenta�on is submi�ed to the bank before the deposit is made.

Can money be borrowed in SA by non-residents topurchase property?

Can a non-resident open a bank account in SA?

NON-RESIDENTS ANDPROPERTY OWNERSHIP (con�nued)

16CONVEYANCING PROCESS INFORMATION BOOKLET

NON-RESIDENTS ANDPROPERTY OWNERSHIP (con�nued)

17www.sdblaw.co.za

?

?

Understandably, this is an important concern for non-residents considering inves�ng in South Africa. The answer to the ques�on is yes: Money from a foreign source, together with any profit, propor�onate to the non-resident's shareholding in the property, may be repatriated in terms of exchange control regula�ons. However, if the non-resident owns property together with a South African resident, only his/her por�on may be repatriated. This is limited to the amount which can be proven to have emanated from a foreign source, plus the profit on that por�on.

A non-resident owner must retain all deal receipts, a copy of the agreement of sale, and the conveyancer's final statement of all costs, for the dura�on of his/her ownership. These documents have to be presented to the Reserve Bank when the property is sold and the proceeds are to be repatriated abroad. This will facilitate the repatria�on of the funds, provided the bankers are sa�sfied that the profit is reasonable and market related.

If the purchase of the property was par�ally financed by funds borrowed in South Africa, that por�on of the purchase price cannot be repatriated unless the bond has been se�led in full. It is important to note that all instalments towards the bond repayment must have come from a foreign source or from rental/interest income generated from a capital asset purchased partly or wholly with foreign funds.

A foreigner who takes up permanent residence in South Africa will be required to sign a Declara�on and Undertaking with his/her bank, sta�ng whether he/she is in possession of any foreign funds and

undertaking, if this is the case, that such funds will not be placed at the disposal of a third party normally resident in South Africa. The foreigner will then be considered a resident for exchange control purposes and will only be able to repatriate funds within the five years following immigra�on. Therea�er he/she will be considered to be a South African ci�zen and subject to the same regula�ons and limita�ons.

Unlike South Africans who are taxed on their worldwide income, non-residents are liable for income tax only on income derived from a South African source. If, for example, their property is rented, the rental income will be subject to South African income tax. As has already been noted, a non-resident also has to pay capital gains tax when selling a South African property.

It is important to note, finally, that if a non-resident who has not permanently immigrated to South Africa spends more than a certain length of �me within the country, he/she will be considered a resident for income tax purposes. The length of �me is determined by a “physical presence test”, which calculates the days spent in the country over a three year period.

No tax is levied on foreign pensions.

Is a non-resident liable for payment of any SAincome tax?

Can the money be taken out of the country a�er sale ofthe property?

?

?

Please note: We have compiled this informa�on in good faith, but we accept no liability for any errors, or for any use that is made of this

informa�on, or for any problems or damage that may arise as a result of using or ac�ng upon this informa�on.

18CONVEYANCING PROCESS INFORMATION BOOKLET

?ID; le�er from a�orneys confirming that the transac�on is a�ended to; copy of the Deed of Sale.

Ÿ A�er registra�on, it is the responsibility of both the seller and buyer to visit their local municipality to respec�vely close and open accounts in their names.

Ÿ Should occupa�on be given and taken before date of registra�on, the same process is to be followed.

Ÿ This is the same process as for the Rates Clearance Cer�ficate – the figures are only issued by the Home Owners’ Associa�on or the Body Corporate in case of a sec�onal scheme and levies are calculated three months in advance.

Ÿ Should there be a surplus in the account a�er registra�on, the client will be refunded directly by the Home Owners’ Associa�on or Body Corporate.

Ÿ The cost of issuing the clearance cer�ficate is for the account of the buyer.

Ÿ The seller is advised to compile a list of all defects. Problems such as a leaking roof, faulty plumbing, etc. should be pointed out by the seller to the estate agent and/or poten�al buyer before registra�on.

Ÿ The law recognizes two types of defects. “Patent defects” are obvious ones such as broken windows. “Latent defects”, such as dry rot, are not so obvious.

Ÿ The “voetstoots” clause is o�en included in an Agreement of Sale to protect the seller against defects of which the seller has no knowledge. However, if the seller knows of a defect and does not disclose it to the purchaser, the “voetstoots” clause will not protect the seller against liability.

AFTER REGISTRATION? CLOSING OF RATES & TAXES, WATER AND ELECTRICITY ACCOUNTS

LEVY CLEARANCES (applicable to Home Owners’ Associa�ons and Body Corporates)

LATENT AND PATENT DEFECTS

VERY IMPORTANT: Take along the following documents:

Q&A

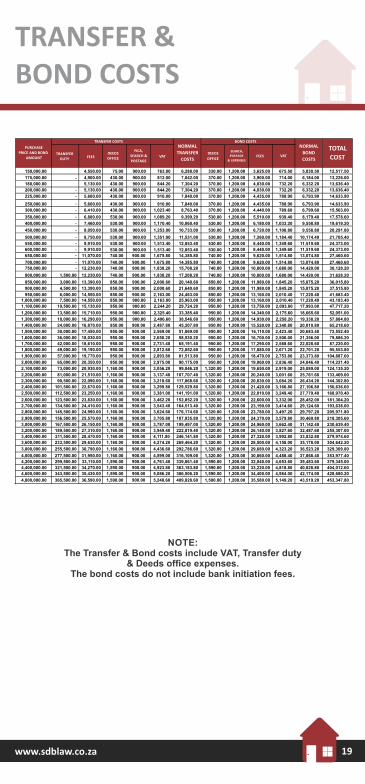

TRANSFER &BOND COSTS

NOTE: The Transfer & Bond costs include VAT, Transfer duty

& Deeds office expenses.The bond costs do not include bank initiation fees.

19www.sdblaw.co.za

-

-

-

650,000.00 11,070.00 740.00 900.00 1,675.80 14,385.80 740.00 1,200.00 9,620.00 1,514.80 13,074.80

700,000.00 11,070.00 740.00 900.00 1,675.80 14,385.80 740.00 1,200.00

750,000.00 12,230.00 740.00 900.00 1,838.20 15,708.20 740.00 1,200.00

800,000.00 1,500.00 12,230.00 740.00 900.00 1,838.20 17,208.20 740.00 1,200.00

850,000.00 3,000.00 13,390.00 850.00 900.00 2,000.60 20,140.60 850.00 1,200.00

900,000.00 4,500.00 13,390.00 850.00 900.00 2,000.60 21,640.60 850.00 1,200.00

950,000.00 6,000.00 14,550.00 850.00 900.00 2,163.00 24,463.00 850.00 1,200.00

1,000,000.00 7,500.00 14,550.00 850.00 900.00 2,163.00 25,963.00 850.00 1,200.00

1,100,000.00 10,500.00 15,130.00 950.00 900.00 2,244.20 29,724.20 950.00 1,200.00

1,200,000.00 13,500.00 15,710.00 950.00 900.00 2,325.40 33,385.40 950.00 1,200.00

1,300,000.00 18,000.00 16,290.00 950.00 900.00 2,406.60 38,546.60 950.00 1,200.00

1,400,000.00 24,000.00 16,870.00 950.00 900.00 2,487.80 45,207.80 950.00 1,200.00

1,500,000.00 30,000.00 17,450.00 950.00 900.00 2,569.00 51,869.00 950.00 1,200.00

1,600,000.00 36,000.00 18,030.00 950.00 900.00 2,650.20 58,530.20 950.00 1,200.00

1,700,000.00 42,000.00 18,610.00 950.00 900.00 2,731.40 65,191.40 950.00 1,200.00

1,800,000.00 49,000.00 19,190.00 950.00 900.00 2,812.60 72,852.60 950.00 1,200.00

1,900,000.00 57,000.00 19,770.00 950.00 900.00 2,893.80 81,513.80 950.00 1,200.00

2,000,000.00 65,000.00 20,350.00 950.00 900.00 2,975.00 90,175.00 950.00 1,200.00

2,100,000.00 73,000.00 20,930.00 1,160.00 900.00 3,056.20 99,046.20 1,320.00 1,200.00

2,200,000.00 81,000.00 21,510.00 1,160.00 900.00 3,137.40 107,707.40 1,320.00 1,200.00

2,300,000.00 90,500.00 22,090.00 1,160.00 900.00 3,218.60 117,868.60 1,320.00 1,200.00

2,400,000.00 101,500.00 22,670.00 1,160.00 900.00 3,299.80 129,529.80 1,320.00 1,200.00

2,500,000.00 112,500.00 23,250.00 1,160.00 900.00 3,381.00 141,191.00 1,320.00 1,200.00

2,600,000.00 123,500.00 23,830.00 1,160.00 900.00 3,462.20 152,852.20 1,320.00 1,200.00

2,700,000.00 134,500.00 24,410.00 1,160.00 900.00 3,543.40 164,513.40 1,320.00 1,200.00

2,800,000.00 145,500.00 24,990.00 1,160.00 900.00 3,624.60 176,174.60 1,320.00 1,200.00

2,900,000.00 156,500.00 25,570.00 1,160.00 900.00 3,705.80 187,835.80 1,320.00 1,200.00

3,000,000.00 167,500.00 26,150.00 1,160.00 900.00 3,787.00 199,497.00 1,320.00 1,200.00

3,200,000.00 189,500.00 27,310.00 1,160.00 900.00 3,949.40 222,819.40 1,320.00 1,200.00

3,400,000.00 211,500.00 28,470.00 1,160.00 900.00 4,111.80 246,141.80 1,320.00 1,200.00

3,600,000.00 233,500.00 29,630.00 1,160.00 900.00 4,274.20 269,464.20 1,320.00 1,200.00

3,800,000.00 255,500.00 30,790.00 1,160.00 900.00 4,436.60 292,786.60 1,320.00 1,200.00

4,000,000.00 277,500.00 31,950.00 1,160.00 900.00 4,599.00 316,109.00 1,320.00 1,200.00

4,200,000.00 299,500.00 33,110.00 1,590.00 900.00 4,761.40 339,861.40 1,590.00 1,200.00

4,400,000.00 321,500.00 34,270.00 1,590.00 900.00 4,923.80 363,183.80 1,590.00 1,200.00

4,600,000.00 343,500.00 35,430.00 1,590.00 900.00 5,086.20 386,506.20 1,590.00 1,200.00

4,800,000.00 365,500.00 36,590.00 1,590.00 900.00 5,248.60 409,828.60 1,590.00 1,200.00

9,620.00 1,514.80 13,074.80

10,800.00 1,680.00 14,420.00

10,800.00 1,680.00 14,420.00

11,980.00 1,845.20 15,875.20

11,980.00 1,845.20 15,875.20

13,160.00 2,010.40 17,220.40

13,160.00 2,010.40 17,220.40

13,750.00 2,093.00 17,993.00

14,340.00 2,175.60 18,665.60

14,930.00 2,258.20 19,338.20

15,520.00 2,340.80 20,010.80

16,110.00 2,423.40 20,683.40

16,700.00 2,506.00 21,356.00

17,290.00 2,588.60 22,028.60

17,880.00 2,671.20 22,701.20

18,470.00 2,753.80 23,373.80

19,060.00 2,836.40 24,046.40

19,650.00 2,919.00 25,089.00

20,240.00 3,001.60 25,761.60

20,830.00 3,084.20 26,434.20

21,420.00 3,166.80 27,106.80

22,010.00 3,249.40 27,779.40

22,600.00 3,332.00 28,452.00

23,190.00 3,414.60 29,124.60

23,780.00 3,497.20 29,797.20

24,370.00 3,579.80 30,469.80

24,960.00 3,662.40 31,142.40

26,140.00 3,827.60 32,487.60

27,320.00 3,992.80 33,832.80

28,500.00

4,158.00

35,178.00

29,680.00

4,323.20

36,523.20

30,860.00

4,488.40 37,868.40

32,040.00

4,653.60 39,483.60

33,220.00

4,818.80 40,828.80

34,400.00 4,984.00 42,174.00

35,580.00 5,149.20 43,519.20

27,460.60

27,460.60

30,128.20

31,628.20

36,015.80

37,515.80

41,683.40

43,183.40

47,717.20

52,051.00

57,884.80

65,218.60

72,552.40

79,886.20

87,220.00

95,553.80

104,887.60

114,221.40

124,135.20

133,469.00

144,302.80

156,636.60

168,970.40

181,304.20

193,638.00

205,971.80

218,305.60

230,639.40

255,307.00

279,974.60

304,642.20

329,309.80

353,977.40

379,345.00

404,012.60

428,680.20

453,347.80

-

-

-

-

-

-

-

-

-

TRANSFER

DUTYFEES

DEEDS

OFFICE

FICA,

SEARCH &

POSTAGEVAT

DEEDS

OFFICE

PURCHASE

PRICE AND BOND

AMOUNT

TRANSFER COSTSNORMAL

TRANSFER

COSTS

NORMAL

BOND

COSTS

TOTAL

COST FEES VAT

BOND COSTS

-

-

& EXPENSES

POSTAGE

SEARCH,

150,000.00 4,550.00 75.00 900.00 763.00 6,288.00 330.00 1,200.00

175,000.00 4,900.00 430.00 900.00 812.00 7,042.00 370.00 1,200.00

180,000.00 5,130.00 430.00 900.00 844.20 7,304.20 370.00 1,200.00

200,000.00 5,130.00 430.00 900.00 844.20 7,304.20 370.00 1,200.00

225,000.00 5,600.00 430.00 900.00 910.00 7,840.00 370.00 1,200.00

250,000.00 5,600.00 430.00 900.00 910.00 7,840.00 370.00 1,200.00

300,000.00 6,410.00 430.00 900.00 1,023.40 8,763.40 370.00 1,200.00

350,000.00 6,880.00 530.00 900.00 1,089.20 9,399.20 530.00 1,200.00

400,000.00 7,460.00 530.00 900.00 1,170.40 10,060.40 530.00 1,200.00

450,000.00 8,050.00 530.00 900.00 1,253.00 10,733.00 530.00 1,200.00

500,000.00 8,750.00 530.00 900.00 1,351.00 11,531.00 530.00 1,200.00

550,000.00 9,910.00 530.00 900.00 1,513.40 12,853.40 530.00 1,200.00

600,000.00 9,910.00 530.00 900.00 1,513.40 12,853.40 530.00 1,200.00

3,625.00 675.50 5,830.50 12,517.50

3,900.00 714.00 6,184.00 13,226.00

4,030.00 732.20 6,332.20 13,636.40

4,030.00 732.20 6,332.20 13,636.40

4,435.00 788.90 6,793.90 14,633.90

4,435.00 788.90 6,793.90 14,633.90

4,440.00 789.60 6,799.60 15,563.00

5,510.00 939.40 8,179.40 17,578.60

6,180.00 1,033.20 9,558.80 19,619.20

6,720.00 1,108.80 9,558.80 20,291.80

7,260.00 1,184.40 10,174.40 21,705.40

8,440.00 1,349.60 11,519.60 24,373.00

8,440.00 1,349.60 11,519.60 24,373.00